53

1 Taxation and Compliances in Restructuring CA Vishal Hakani / CA Shabala Shinde 4 May, 2019 1

1

Ta

xa

tio

n a

nd

Co

mp

lia

nce

s in

Re

stru

ctu

rin

g

CA

Vis

ha

l Ha

ka

ni /

CA

Sh

ab

ala

Sh

ind

e4

Ma

y, 2

019

1

2

So

me

Re

cen

t T

ran

sact

ion

s

No

tab

le m

erg

er

tra

nsa

ctio

ns

Ra

dia

nt

Lif

e C

are

Pvt

. L

td

wit

h M

ax

He

alt

hca

re L

td.

Me

rge

r o

f In

du

s T

ow

ers

L

imit

ed

wit

h B

ha

rti I

nfr

ate

l L

imit

ed

Me

rge

r o

f Vo

da

fon

e

Se

rvic

e L

imit

ed

, Vo

da

fon

e

Ind

ia L

imit

ed

an

d Id

ea

C

ellu

lar

Lim

ite

d

Me

rge

r o

f G

laxo

Sm

ith

Klin

e

Co

nsu

me

r H

ea

lth

care

L

imit

ed

wit

h H

ind

ust

an

U

nile

ver

Lim

ite

d

No

tab

le a

cqu

isit

ion

s /

div

est

ure

s

Wa

lma

rt I

nc.

acq

uir

es

ma

jori

ty s

take

in F

lipk

art

O

nlin

e S

erv

ice

s P

vt. L

td

De

me

rge

r o

f b

ran

de

d

ap

pa

rel b

usi

ne

ss o

f A

rvin

d

Lim

ite

d in

to A

rvin

d

Fa

shio

ns

an

d e

ng

ine

eri

ng

d

ivis

ion

into

Arv

ind

A

nve

sha

n

Co

mp

osi

te s

che

me

of

arr

an

ge

me

nt

invo

lvin

g,

inte

r a

lia,

de

me

rge

r o

f T

rave

l Co

rpo

rati

on

(In

dia

) L

imit

ed

into

SO

TC

Tra

vel

Ma

na

ge

me

nt

Pri

vate

L

imit

ed

Tata

Ste

el a

cqu

ire

s co

ntr

olli

ng

sta

ke in

B

hu

sha

n S

tee

l

3

Wh

y M

&A

Wh

y

M&

A

Eco

no

mie

s o

f S

cale

Re

du

ce a

dm

in c

ost

s, R

eg

ula

tory

eff

icie

nci

es,

ta

x lo

sse

s e

tc.

Inn

ov

ati

on

La

un

chin

g n

ew

se

gm

en

ts,

pro

du

cts.

Glo

ba

l / In

tern

al R

est

ruct

uri

ng

Pa

rt o

f G

lob

al r

est

ruct

uri

ng

or

exi

t n

on

-co

re

bu

sin

ess

Gro

wth

dri

ve

n s

tra

teg

ies

Ino

rga

nic

gro

wth

, co

mp

eti

tive

po

siti

on

4

Mo

de

s o

f M

&A

in In

dia

5

Mn

A

Re

stru

ctu

rin

gA

cqu

isit

ion

Me

rge

rD

em

erg

er

Me

rge

r/

De

me

rge

r

Inte

rna

l

rest

ruct

uri

ng

Ca

pit

al

red

uct

ion

Bu

y-b

ack

of

sha

res

Sh

are

pu

rch

ase

Bu

sin

ess

pu

rch

ase

Slu

mp

sa

leIt

em

ize

d s

ale

Ty

pic

al m

od

es

of

Bu

sin

ess

Re

org

an

iza

tio

n in

Ind

ia

Co

nso

lida

tio

n o

f

bu

sin

ess

es

/

en

titi

es

Fo

cus

on

co

re

bu

sin

ess

/ h

ive

off

of

no

n c

ore

bu

sin

ess

/

mo

ne

tise

Fin

an

cia

l

rest

ruct

uri

ng

/

en

ha

nci

ng

sta

ke/

cash

re

pa

tria

tio

n

En

ha

nci

ng

sta

ke/

cash

re

pa

tria

tio

n

Fo

cus

on

ino

rga

nic

gro

wth

/ st

rate

gic

or

no

n-

stra

teg

ic

inve

stm

en

ts

Fo

cus

on

co

re

bu

sin

ess

/ se

ll o

ff

or

hiv

e o

ff n

on

-co

re b

usi

ne

ss

6

�M

erg

ers

7

Me

rge

r –

Ty

pic

al W

ay

s

A C

o.

B C

o.

Me

rge

r

Sh

are

ho

lde

rsS

ha

reh

old

ers

Sh

are

s is

sue

d a

s co

nsi

de

rati

on

Su

bsi

dia

ry C

o

Ho

ld C

o

100

%

Me

rge

r

No

sh

are

s w

ill b

e is

sue

d

as

con

sid

era

tio

n

Sh

are

ho

lde

rs

Ho

ld C

o

Su

bsi

dia

ry C

o

Me

rge

rS

ha

res

issu

ed

as

con

sid

era

tio

n

Mer

ger

of

A C

o w

ith

B C

o

Mer

ger

of

WO

S w

ith

ho

ldin

g c

om

pa

ny

Me

rge

r o

f h

old

ing

co

mp

an

y w

ith

su

bsi

dia

ry c

om

pa

ny

BC

oC

Co

Sh

are

ho

lde

rsS

ha

reh

old

ers

Sh

are

s is

sue

d a

s co

nsi

de

rati

on

to

sh

ds

of

A a

nd

B

A C

o

Sh

are

ho

lde

rs

Mer

ger

of

A C

o a

nd

B C

o w

ith

C C

o

Illu

stra

tiv

e s

cen

ari

os

on

ly

Me

rge

r o

f A

an

d B

8

Me

rge

r –

Ke

y T

ax

Imp

lica

tio

ns

Tra

nsf

ero

r C

om

pa

ny

•C

ap

ita

l Ga

ins

Tax

-E

xem

pt

•G

ST

-E

xem

pt

Tra

nsf

ere

e C

om

pa

ny

•A

ctu

al c

ost

of

the

ass

ets

a

cqu

ire

d –

sam

e a

s tr

an

sfe

ror

com

pa

ny

•W

DV

of

the

ass

ets

acq

uir

ed

–W

DV

of

ass

ets

in t

he

bo

ok

s o

f tr

an

sfe

ror

•Ta

x h

olid

ay

–a

vaila

ble

exc

ep

t 8

0IA

•D

ep

reci

ati

on

–a

vaila

ble

p

rop

ort

ion

ate

ly b

asi

s p

eri

od

of

ho

ldin

g d

uri

ng

th

e y

ea

r

•N

o t

ax

imp

lica

tio

ns

un

de

r 5

6(2

)(x)

•C

arr

y f

orw

ard

of

loss

es

–a

vaila

ble

su

bje

ct t

o c

on

dit

ion

s

•M

AT

cre

dit

–T

ran

sfe

rab

le*

•G

ST

cre

dit

–T

ran

sfe

rab

le

Sh

are

ho

lde

rs o

f

Tra

nsf

ero

r C

om

pa

ny

•C

ap

ita

l ga

ins

–e

xem

pt

•C

OA

of

ne

w s

ha

res

–sa

me

as

CO

A o

f p

revi

ou

sly

he

ld s

ha

res,

e

xce

pt

112

A s

itu

ati

on

pe

rio

d

of

ho

ldin

g o

f n

ew

sh

are

s –

ava

ilab

le f

rom

da

te o

f a

cqu

isit

ion

of

pre

vio

us

sha

res

•C

ost

of

infl

ati

on

ind

ex

on

su

bse

qu

en

t sa

le –

to b

e t

he

y

ea

r o

f a

cqu

isit

ion

of

pre

vio

us

sha

res

•N

o t

ax

imp

lica

tio

ns

un

de

r 5

6(2

)(x)

*B

asi

s ju

dic

ial p

rece

den

ts

9

Imp

act

of

Ex

pln

2A

of

sec.

2(2

2)

Pa

rtic

ula

rsIN

R

Acc

um

ula

ted

Pro

fit

of

A C

o4

50

Acc

um

ula

ted

Pro

fit

of

B C

o50

To

tal

500

Acc

um

ula

ted

pro

fit

for

cap

ita

l re

du

ctio

n

A C

o.

B C

o.

Me

rge

r –

1 A

pri

l 20

19S

ha

reh

old

ers

Ca

pit

al r

ed

uct

ion

–

15

Ju

ly 2

01

8

Wh

at

if t

he

me

rge

r h

ad

ha

pp

en

ed

in 2

016

? C

an

acc

um

ula

ted

pro

fits

of

A C

o.

be

con

sid

ere

d a

t th

e t

ime

of

cap

ita

l re

du

ctio

n ?

•In

ca

se o

f a

n a

ma

lga

ma

ted

co

mp

an

y, t

he

acc

um

ula

ted

pro

fits

, wh

eth

er

cap

ita

lize

d

or

no

t, o

r lo

ss, a

s th

e c

ase

ma

y b

e, s

ha

ll b

e in

cre

ase

d b

y t

he

acc

um

ula

ted

pro

fits

, w

he

the

r ca

pit

alis

ed

or

no

t, o

f th

e a

ma

lga

ma

tin

g c

om

pa

ny

on

th

e d

ate

of

am

alg

am

ati

on

Exp

ln 2

A

of

sec.

e

2(2

2)

10

Cri

tica

l ta

x a

spe

cts

-M

erg

er

Wh

eth

er

me

rge

r fa

lls w

ith

in t

he

de

fin

itio

n a

s p

er

sec.

2(1

B)

Dis

cha

rge

of

con

sid

era

tio

n b

y w

ay

of

mix

of

eq

uit

y a

nd

de

be

ntu

re o

r ca

sh

Me

rge

r o

f h

old

ing

co

mp

an

y w

ith

wh

olly

ow

ne

d s

ub

sid

iary

co

mp

an

y?

Go

od

will

cre

ate

d u

po

n a

ma

lga

ma

tio

n a

nd

its

tax

tre

atm

en

t

Tra

nsf

er

of

MA

T c

red

it u

po

n a

ma

lga

ma

tio

n

Ava

ilab

ility

of

bu

sin

ess

loss

es

an

d u

na

bso

rbe

d d

ep

reci

ati

on

Wh

eth

er

56

(2)(

viib

) a

pp

lies

in c

ase

of

issu

e o

f sh

are

s p

urs

ua

nt

to m

erg

er?

11

Me

rge

r –

S.7

2A

-C

arr

y f

orw

ard

of

Bu

sin

ess

Lo

sse

s a

nd

U

na

bso

rbe

d d

ep

reci

ati

on

Acc

um

ula

ted

bu

sin

ess

loss

a

nd

un

ab

sorb

ed

d

ep

reci

ati

on

of

the

a

ma

lga

ma

tin

g c

om

pa

ny

sha

ll b

e d

eem

edto

be

b

usi

ne

ss lo

sse

s o

r u

na

bso

rbe

d d

ep

reci

ati

on

of

the

am

alg

am

ate

d c

om

pa

ny

for

the

pre

vio

us

yea

rin

w

hic

h t

he

am

alg

am

atio

n is

ef

fect

ed

Sh

ou

ld b

e in

th

e ‘b

usi

ne

ss’

in w

hic

h s

uch

ca

rry

fo

rwa

rd o

f lo

sse

s a

nd

UA

D

are

incu

rre

d•

a c

om

pa

ny

ow

nin

g a

n

“in

du

stri

al u

nd

erta

kin

g”

or

a s

hip

or

a h

ote

l wit

h

an

oth

er

com

pa

ny;

•a

ba

nk

ing

co

mp

an

y w

ith

a

sp

eci

fie

d b

an

k;

•o

ne

or

mo

re p

ub

lic s

ect

or

com

pa

ny

or

com

pa

nie

s e

ng

ag

ed

in t

he

bu

sin

ess

o

f o

pe

rati

on

of

air

cra

ft

wit

h o

ne

or

mo

re p

ub

lic

sect

or

com

pa

ny

or

com

pa

nie

s e

ng

ag

ed

in

sim

ilar

bu

sin

ess

an

y u

nd

ert

ak

ing

en

ga

ge

d in

:•

the

ma

nu

fact

ure

or

pro

cess

ing

of

go

od

s; o

r•

the

ma

nu

fact

ure

of

com

pu

ter

soft

wa

re; o

r•

the

bu

sin

ess

of

ge

ne

rati

on

or

dis

trib

uti

on

of

ele

ctri

city

or

an

y o

the

r fo

rm o

f p

ow

er;

or

•th

e b

usi

ne

ss o

f p

rovi

din

g

tele

com

mu

nic

ati

on

se

rvic

es,

in

clu

din

g r

ad

io p

ag

ing

, d

om

est

ic s

ate

llite

se

rvic

e,

ne

two

rk o

f tr

un

kin

g,

bro

ad

ba

nd

ne

two

rk a

nd

in

tern

et

serv

ice

s; o

r•

min

ing

; or

•th

e c

on

stru

ctio

n o

f sh

ips,

a

ircr

aft

s o

r ra

il sy

ste

ms

Wh

at

is “

Ind

ust

ria

l

Un

de

rta

kin

g”

‘Bu

sin

ess

’ of

Se

c. 7

2A

Fre

sh le

ase

of

life

fo

r c/

f B

usi

ne

ss L

oss

es

on

am

alg

am

ati

on

?

12

S.7

2A

-C

om

pli

an

ce C

on

dit

ion

s:

12

Amalgamating companyh

as

be

en

en

ga

ge

d in

th

e b

usi

ne

ss, i

n

wh

ich

th

e a

ccu

mu

late

d lo

ss o

ccu

rre

d

or

de

pre

cia

tio

n r

em

ain

s u

na

bso

rbe

d,

for

3 o

r m

ore

yea

rs;

ha

s h

eld

co

nti

nu

ou

sly

as

on

th

e d

ate

of

am

alg

am

ati

on

atl

ea

st 3

/4th

of

the

b

oo

k v

alu

e o

f fi

xed

ass

ets

he

ld b

y it

tw

o y

ea

rs p

rio

r to

th

e d

ate

of

am

alg

am

ati

on

Amalgamated Company

-h

old

s co

nti

nu

ou

sly

fo

r a

min

. 5

yea

rsfr

om

th

e d

ate

of

am

alg

am

ati

on

atl

ea

st

3/4

tho

f th

e B

V o

f fi

xed

ass

ets

of

the

a

ma

lga

ma

tin

g c

om

pa

ny

acq

uir

ed

;

-co

nti

nu

es

the

bu

sin

ess

of

the

a

ma

lga

ma

tin

g c

om

pa

ny

fo

r a

min

imu

m

pe

rio

d o

f 5

ye

ars

fro

m t

he

da

te o

f a

ma

lga

ma

tio

n;

-w

hic

h o

wn

s a

n in

du

stri

al

un

de

rta

kin

g o

f th

e a

ma

lga

ma

tin

g c

om

pa

ny

by

wa

y o

f a

ma

lga

ma

tio

n,

sha

ll a

chie

ve t

he

leve

l of

pro

du

ctio

n o

f a

tle

ast

50

% o

f th

e in

sta

lled

ca

pa

city

of

the

un

de

rta

kin

g b

efo

re t

he

e

nd

of

4 y

ea

rs f

rom

th

e d

ate

of

am

alg

am

ati

on

an

d c

on

tin

ue

to

ma

inta

in

the

sa

id m

inim

um

le

vel o

f p

rod

uct

ion

til

l th

e e

nd

of

5 y

ea

rs f

rom

th

e d

ate

of

am

alg

am

ati

on

;

-to

fu

rnis

h t

o A

O -

Fo

rm N

o.

62

du

ly

veri

fie

d b

y a

n C

A f

rom

th

e y

ea

r o

f a

chie

vin

g f

ifty

pe

rce

nt

leve

l of

pro

du

ctio

n

up

to c

om

ple

tio

n o

f 5

ye

ars

fro

m t

he

da

te

of

am

alg

am

ati

on

In c

ase

of

vio

lati

on

of

an

y c

on

dit

ion

s, t

he

se

t o

ff o

f B

L/U

AD

ava

iled

by

am

alg

am

ate

d

com

pa

ny

sh

all

be

de

em

ed

to

be

inco

me

of

am

alg

am

ate

d c

om

pa

ny

fo

r th

e y

ea

r in

wh

ich

such

co

nd

itio

ns

are

no

t co

mp

lied

wit

h.

13

S.

79

-C

ha

ng

e in

su

bst

an

tia

l sh

are

ho

ldin

g

If, w

ith

in t

he

sa

me

ye

ar,

sh

are

ho

ldin

g c

ha

ng

es

by

mo

re t

ha

n 4

9%

an

d s

ub

seq

ue

ntl

y,

ori

gin

al s

ha

reh

old

ing

is r

est

ore

d. C

an

pro

visi

on

s o

f se

c. 7

9 t

rig

ge

r ?

Ca

rry

fo

rwa

rd a

nd

se

t o

ff o

f lo

sse

s (i

ncu

rred

in a

ny

yea

r p

rio

r to

th

e ye

ar

of

cha

ng

e in

sha

reh

old

ing

)a

ga

inst

fu

ture

inco

me

(p

ost

ch

an

ge

in s

ha

reh

old

ing

) sh

all

no

t b

e

ava

ilab

le,

if,

•th

ere

is c

ha

ng

e in

sh

are

ho

ldin

g o

f a

co

mp

an

y (

no

t b

ein

g a

co

mp

an

y i

n w

hic

h

pu

bli

c a

re s

ub

sta

nti

all

y i

nte

rest

ed

);

•S

ha

reh

old

ers

be

ne

fici

ally

ho

ldin

g n

ot

less

th

an

fif

ty-o

ne

pe

rce

nt

of

the

vo

tin

g

po

we

r o

n t

he

last

da

y o

f th

e y

ea

r(s)

in w

hic

h lo

ss w

as

incu

rre

da

re n

ot

the

sa

me

sha

reh

old

ers

be

ne

fici

ally

ho

ldin

g s

ha

res

carr

yin

g n

ot

less

th

an

fif

ty-o

ne

pe

rce

nt

of

the

vo

tin

g p

ow

er

on

th

e l

ast

da

y o

f th

e y

ea

r o

f se

t o

ff

Tri

gg

er

for

S.7

9

14

S.

79

-D

ich

oto

my

in t

ho

ug

hts

Le

ga

l O

wn

ers

hip

Be

ne

fici

al

ow

ne

rsh

ip

•S

.79

sta

tes

tha

t sh

are

s ca

rry

ing

no

t le

ss t

ha

n 5

1% o

f

the

vo

tin

g p

ow

er

we

re b

en

efi

cia

lly h

eld

by

pe

rso

ns

wh

o b

en

efi

cia

lly

he

ldsh

are

s o

f th

e c

om

pa

ny

carr

yin

g n

ot

less

th

an

51%

of

voti

ng

po

we

r o

n t

he

last

da

y o

f th

e y

ea

r in

wh

ich

loss

incu

rre

d

•A

su

bsi

dia

ry i

s e

ffe

ctiv

ely

co

ntr

olle

d b

y it

s p

are

nt

com

pa

ny

; th

e p

are

nt

com

pa

ny

co

ntr

ols

th

e v

oti

ng

po

we

r o

f th

e c

om

pa

ny

•se

c. 7

9 is

no

t tr

igg

ere

d if

th

e b

en

efi

cia

l

sha

reh

old

ers

re

ma

in t

he

sa

me

, e

ven

if t

he

re is

cha

ng

e in

th

e im

me

dia

te s

ha

reh

old

ers

•C

ase

La

ws:

i.A

mco

Po

we

r S

yst

em

s (I

TA

T B

an

ga

lore

; u

ph

eld

by

Ka

rna

tak

a H

C)

ii.S

ele

ct H

olid

ay

s R

eso

rts

(IT

AT

De

lhi)

iii.

Wa

dh

wa

& A

sso

. R

ea

lto

rs P

vt L

td.

(IT

AT

Mu

mb

ai)

•A

co

mp

an

y is

a d

isti

nct

leg

al e

nti

ty, a

nd

ha

s

an

exi

ste

nce

se

pa

rate

fro

m t

ha

t o

f it

s

sha

reh

old

ers

–a

sse

ts o

f th

e c

om

pa

ny

are

no

t a

sse

ts o

f th

e s

ha

reh

old

ers

•A

pe

rso

n c

an

be

a b

en

efi

cia

l o

wn

er

wh

en

sha

res

are

he

ld b

y s

om

eo

ne

els

e o

n h

is

be

ha

lf

•C

ha

ng

e in

re

gis

tere

d s

ha

reh

old

er

trig

ge

rs

sec.

79

•C

ase

La

ws:

i.Y

um

Re

sta

ura

nts

(D

elh

i HC

)

ii.A

cer

Co

mp

ute

r In

tern

ati

on

al L

imit

ed

(A

AR

)

iii.T

ain

wa

la T

rad

ing

an

d In

vest

me

nts

(IT

AT

Mu

mb

ai)

iv.J

ust

Lif

est

yle

(IT

AT

Mu

mb

ai)

15

S.

79

-E

xcl

usi

on

s

Ch

an

ge

in s

ha

reh

old

ing

o

f In

dia

n S

ub

Co

. as

a

resu

lt o

f m

erg

er/

de

me

rge

r o

f it

s ‘f

ore

ign

ho

ldin

g

com

pa

ny

’

•C

on

dit

ion

-5

1%

sh

are

ho

lde

rs o

f th

e

am

alg

am

ati

ng

/de

me

rge

d f

ore

ign

co

mp

an

y co

nti

nu

e

to b

e t

he

sh

are

ho

lde

rs o

f th

e

am

alg

am

ate

d o

r th

e r

esu

ltin

g f

ore

ign

co

mp

an

y

Ch

an

ge

in

sha

reh

old

ing

in c

ase

o

f e

ligib

le “

sta

rt-u

p”

com

pa

nie

s

•A

ll th

e s

ha

reh

old

ers

(i

n t

he

yea

r o

f in

curr

ing

th

e lo

ss)

ou

gh

t to

co

nti

nu

e

to h

old

sh

are

s a

s o

f th

e la

st d

ay

of

the

p

revi

ou

s ye

ar

in

wh

ich

th

e s

eto

ff is

to

be

cla

ime

d

•A

bo

ve e

xce

pti

on

a

pp

lica

ble

on

ly f

or

loss

es

incu

rre

d in

fi

rst

7 ye

ars

fro

m

inco

rpo

rati

on

Ch

an

ge

pu

rsu

an

t to

re

solu

tio

n u

nd

er

‘IB

C

201

6’

•re

solu

tio

n p

lan

a

pp

rove

d u

nd

er

the

In

solv

en

cy a

nd

B

an

kru

ptc

y C

od

e,

20

16

Oth

ers

•T

ran

sfe

r o

f sh

are

s b

y w

ay

of

gif

t to

an

y re

lati

ve f

rom

th

e

sha

reh

old

er

•D

ea

th o

f sh

are

ho

lde

r

Wh

eth

er

sec.

79

ap

plie

s to

all

loss

es

incl

ud

ing

un

ab

sorb

ed

de

pre

cia

tio

n ?

Wh

eth

er

sec.

72

A o

verr

ide

s se

c. 7

9 ?

16

�D

em

erg

ers

17

De

me

rge

r –

Ty

pic

al W

ay

s

Dem

erg

er o

f a

un

it f

rom

A C

o t

o B

Co

an

d

sha

res

issu

ed b

y B

Co

Dem

erg

er o

f a

un

it f

rom

A C

o t

o B

Co

an

d s

ha

res

issu

ed

by

Ho

ld C

o o

f B

Co

Th

e a

bo

ve

are

bro

ad

illu

stra

tiv

e s

cen

ari

os

Ca

nce

llati

on

of

de

me

rge

d C

o’s

sh

are

ho

ldin

g in

B C

o

No

n –

mir

ror

sha

reh

old

ing

de

me

rge

rM

irro

r sh

are

ho

ldin

g d

em

erg

er

–th

is is

ty

pic

all

y c

arr

ied

ou

t b

y t

he

list

ed

co

mp

an

y a

nd

pu

rsu

an

t to

de

me

rge

r th

e r

esu

ltin

g c

om

pa

ny

wil

l als

o g

et

list

ed

A C

o.

B C

o.

De

me

rge

r o

f U

nit

II

Sh

are

ho

lde

rsS

ha

reh

old

ers

Sh

are

s is

sue

d a

s co

nsi

de

rati

on

Un

it I

Un

it I

I

A C

o.

B C

o.

De

me

rge

r o

f U

nit

II

Sh

are

ho

lde

rsS

ha

reh

old

ers

Sh

are

s is

sue

d a

s co

nsi

de

rati

on

Un

it I

Un

it I

I

18

De

me

rge

r –

Ke

y c

on

dit

ion

s

Ta

x n

eu

tra

lity

co

nd

itio

ns

•T

ran

sfe

r o

f a

ll p

rop

ert

ies

& li

ab

iliti

es

rela

tab

leto

th

e u

nd

ert

ak

ing

be

ing

tra

nsf

err

ed

b

y t

he

de

me

rge

d c

om

pa

ny

to

th

e r

esu

ltin

g c

om

pa

ny

at

bo

ok

va

lue

;

•D

isch

arg

e o

f co

nsi

de

rati

on

by

th

e r

esu

ltin

g c

om

pa

ny

by

wa

y o

f is

sue

of

sha

res

on

p

rop

ort

ion

ate

ba

sis

(exc

ep

t w

he

re r

esu

ltin

g c

om

pa

ny

itse

lf is

a s

ha

reh

old

er

of

the

d

em

erg

ed

co

mp

an

y);

•Is

sue

of

sha

res

to t

he

sh

are

ho

lde

rs h

old

ing

no

t le

ss t

ha

n 3

/4th

sha

res

(in

va

lue

) in

th

e

de

me

rge

d c

om

pa

ny

(oth

er

tha

n t

he

sh

are

s a

lre

ad

y h

eld

by

th

e r

esu

ltin

g c

om

pa

ny

of

its

no

min

ee

s o

f it

s su

bsi

dia

ry);

•T

ran

sfe

r o

f u

nd

ert

ak

ing

to

be

on

a ‘g

oin

g c

on

cern

ba

sis’

“De

me

rge

r” m

ea

ns

the

tra

nsf

er

of

on

e o

r m

ore

un

de

rta

kin

gs

by

th

e

de

me

rge

d c

om

pa

ny

to

an

y r

esu

ltin

g c

om

pa

ny

19

“Un

de

rta

kin

g”

me

an

s

Un

de

rta

kin

g”

sha

ll in

clu

de

an

y

pa

rt o

f a

n u

nd

ert

ak

ing

, o

r a

u

nit

or

div

isio

n o

f a

n

un

de

rta

kin

g o

r a

bu

sin

ess

a

ctiv

ity

ta

ken

as

a w

ho

le,

bu

t d

oe

s n

ot

incl

ud

e in

div

idu

al

ass

ets

or

lia

bil

itie

s o

r a

ny

co

mb

ina

tio

n t

he

reo

f o

r n

ot

con

stit

uti

ng

a b

usi

ne

ss

act

ivit

y

“Lia

bil

itie

s” m

ea

ns

the

lia

bili

tie

s d

ire

ctly

re

lata

ble

to

th

e u

nd

ert

ak

ing

;

spe

cifi

c lo

an

s o

r b

orr

ow

ing

s (i

ncl

ud

ing

de

be

ntu

res)

of

the

u

nd

ert

ak

ing

am

ou

nts

of

ge

ne

ral o

r m

ult

ipu

rpo

se b

orr

ow

ing

s o

n

pro

po

rtio

na

te b

asi

s

Va

lue

of

Pro

pe

rty

Re

valu

ati

on

am

ou

nt

to b

e

ign

ore

d

Str

ictl

y m

ea

ns

‘Bo

ok

Va

lue

’

De

me

rge

r –

Ke

y c

on

dit

ion

s

20

“De

me

rge

d C

om

pa

ny”

me

an

s th

e c

om

pa

ny

wh

ose

un

de

rta

kin

g is

tra

nsf

err

ed

to

a r

esu

ltin

g

com

pa

ny

pu

rsu

an

t to

de

me

rge

r

De

me

rge

d

Co

mp

an

y[s

ec.

2(1

9A

AA

)]

“Re

sult

ing

Co

mp

an

y” m

ea

ns

on

e o

r m

ore

co

mp

an

ies

(in

clu

din

g a

wh

olly

ow

ne

d s

ub

sid

iary

the

reo

f) t

o w

hic

h t

he

un

de

rta

kin

g o

f th

e d

em

erg

ed

co

mp

an

y is

tra

nsf

err

ed

in a

de

me

rge

r a

nd

,

the

re

sult

ing

co

mp

an

y in

co

nsi

de

rati

on

of

such

tra

nsf

er

of

un

de

rta

kin

g, i

ssu

e s

ha

res

to t

he

sha

reh

old

ers

of

the

de

me

rge

d c

om

pa

ny

an

d in

clu

de

s a

ny

au

tho

rity

or

bo

dy

or

loca

l au

tho

rity

or

pu

blic

se

cto

r co

mp

an

y o

r a

co

mp

an

y e

sta

blis

he

d, c

on

stit

ute

d o

r fo

rme

d a

s a

re

sult

of

de

me

rge

r [s

ec.

2(4

1A)]

Re

sult

ing

Co

mp

an

y [s

ec.

2(4

1A)]

De

me

rge

r –

Ke

y c

on

dit

ion

s

Wh

eth

er

wh

olly

ow

ne

d s

ub

sid

iary

incl

ud

es

ste

p d

ow

n w

ho

lly o

wn

ed

su

bsi

dia

ry a

lso

?

21

De

me

rge

r –

Ta

x Im

pli

cati

on

s

In t

he

ha

nd

s o

f T

ax

ab

ilit

y/

Tre

atm

en

t

Se

c.C

on

dit

ion

s /

Re

ma

rks

De

me

rge

dC

om

pa

ny

No

ca

pit

al

ga

ins

tax

on

tra

nsf

er

of

ass

ets

47(

vib

)R

esu

ltin

gco

mp

an

y s

ho

uld

be

an

Ind

ian

co

mp

an

y

Sh

are

ho

lde

rs o

f

De

me

rge

d C

om

pa

ny

No

ca

pit

al

ga

ins

tax

on

rece

ipt

of

sha

res

fro

m t

he

resu

ltin

g c

om

pa

ny

47(

vid

)

Co

sto

f A

sse

ts f

or

Re

sult

ing

Co

mp

an

y:

-D

ep

reci

ab

le A

sse

ts

-C

ap

ita

l Ass

et

= W

DV

of

de

pre

cia

ble

ass

et

to b

e t

he

sa

me

as

WD

V in

th

e h

an

ds

of

the

De

me

rge

d C

om

pa

ny

=N

o s

pe

cifi

c p

rovi

sio

n f

or

cost

of

Ca

pit

al A

sse

t

acq

uir

ed

-E

xpln

7A

to

43(

1)

-E

xpln

2B

to

43(

6)(

c)

-4

9(1

)

Re

sult

ing

co

mp

an

ysh

ou

ld b

e

an

Ind

ian

Co

mp

an

y

Co

st o

f a

cqu

isit

ion

of

sha

res

rece

ive

d o

n

de

me

rge

r b

y t

he

sha

reh

old

ers

= C

ost

of

acq

uis

itio

no

f

sha

res

in d

em

erg

ed

com

pa

ny

be

sp

lit o

n t

he

ba

sis

of

ne

t b

oo

k v

alu

e o

f

the

ass

ets

tra

nsf

err

ed

be

ari

ng

to

th

e N

et

Wo

rth

of

the

De

me

rge

d

Co

mp

an

y im

me

dia

tely

be

fore

su

ch d

em

erg

er

49

(2C

)

22

De

me

rge

r –

Ta

x Im

pli

cati

on

s

In t

he

ha

nd

s o

f T

ax

ab

ilit

y/ T

rea

tme

nt

Se

c.C

on

dit

ion

s /

Re

ma

rks

Pe

rio

d o

f h

old

ing

of

sha

res

rece

ive

d o

n d

em

erg

er

by

the

sh

are

ho

lde

rs

Incl

ud

es

pe

rio

d o

f h

old

ing

of

sha

res

he

ld in

th

e

de

me

rge

d c

om

pa

ny

Exp

ln 1

(i)(

g)

to s

ec.

2(4

2A

)

Pe

rio

d o

f h

old

ing

of

cap

ita

l a

sse

ts

Incl

ud

es

pe

rio

d o

f h

old

ing

of

cap

ita

l a

sse

ts h

eld

by

th

e

de

me

rge

d c

om

pa

ny

Exp

ln 1

(i)(

b)

to 2

(42

A)

r.w

.s.

49

(1)

an

d 4

7(vi

b)

23

De

me

rge

r –

Ta

x C

on

sid

era

tio

n

Co

st S

pli

t u

p in

th

e h

an

ds

of

sha

reh

old

ers

‘Co

st o

f a

cqu

isit

ion

of

sha

res

of

resu

ltin

gco

mp

an

y’ [

sec.

49

(2C

)]

=

X

‘Co

st o

f a

cqu

isit

ion

of

the

ori

gin

al

sha

res

by

th

e s

ha

reh

old

ers

in t

he

de

me

rge

d c

om

pa

ny

’ -

[se

c. 4

9(2

D)]

= C

ost

of

acq

uis

itio

n o

f sh

are

s in

de

me

rge

d c

om

pa

ny

–co

st o

f a

cqu

isit

ion

of

sha

res

of

resu

ltin

g c

om

pa

ny

arr

ive

d a

t u

nd

er

sec.

49

(2C

)

‘Ne

t w

ort

h’

is d

efi

ne

d a

s th

e a

gg

reg

ate

of

the

pa

id u

p s

ha

re c

ap

ita

l an

d g

en

era

l re

serv

es

as

ap

pe

ari

ng

in t

he

bo

ok

s

of

acc

ou

nt

of

the

de

me

rge

d c

om

pa

ny

imm

ed

iate

ly b

efo

re t

he

de

me

rge

r .

Ne

t b

oo

k v

alu

e o

f th

e a

sse

ts t

ran

sfe

rre

d i

n t

he

de

me

rge

r

Ne

t w

ort

h o

f th

e d

em

erg

ed

co

mp

an

y b

efo

re t

he

de

me

rge

r

Co

st o

f a

cqu

isit

ion

of

sha

res

in d

em

erg

ed

com

pa

ny

Wh

eth

er

de

fin

itio

n o

f N

etw

ort

h is

to

be

inte

rpre

ted

str

ictl

y t

o in

clu

de

on

ly ‘G

en

era

l

rese

rve

’ ?

Ho

w t

o c

om

pu

te t

he

co

st s

plit

in c

ase

of

de

me

rge

r o

f n

eg

ati

ve n

etw

ort

h u

nd

ert

ak

ing

?

24

S.7

2A

-C

om

pli

an

ce C

on

dit

ion

s:

24

Losses ‘Directly related’ E

nti

re a

mo

un

to

f‘d

ire

ctly

re

lata

ble

’bu

sin

ess

loss

es

an

d

un

ab

sorb

ed

de

pre

cia

tio

n is

a

llo

we

d t

o b

e c

arr

ied

fo

rwa

rd a

nd

se

t-o

ff in

th

e h

an

ds

of

the

re

sult

ing

co

mp

an

y

Losses ‘Not-directly related’

Th

e a

ccu

mu

late

d b

usi

ne

ss lo

ss a

nd

un

ab

sorb

ed

de

pre

cia

tio

n s

ho

uld

be

‘ap

po

rtio

ne

d’b

etw

ee

n t

he

resu

ltin

g c

om

pa

ny

an

d t

he

de

me

rge

d c

om

pa

ny

in t

he

ra

tio

of

the

ass

ets

tra

nsf

err

ed

to

th

e

resu

ltin

g c

om

pa

ny

an

d a

sse

ts

reta

ine

d b

y t

he

de

me

rge

d

com

pa

ny

an

d b

e a

llow

ed

to

be

carr

ied

fo

rwa

rd a

nd

se

t o

ff in

th

e

ha

nd

s o

f th

e d

em

erg

ed

co

mp

an

y

or

the

re

sult

ing

co

mp

an

y, a

s th

e

case

ma

y b

e

25

De

me

rge

r –

Oth

er

ke

y a

spe

cts

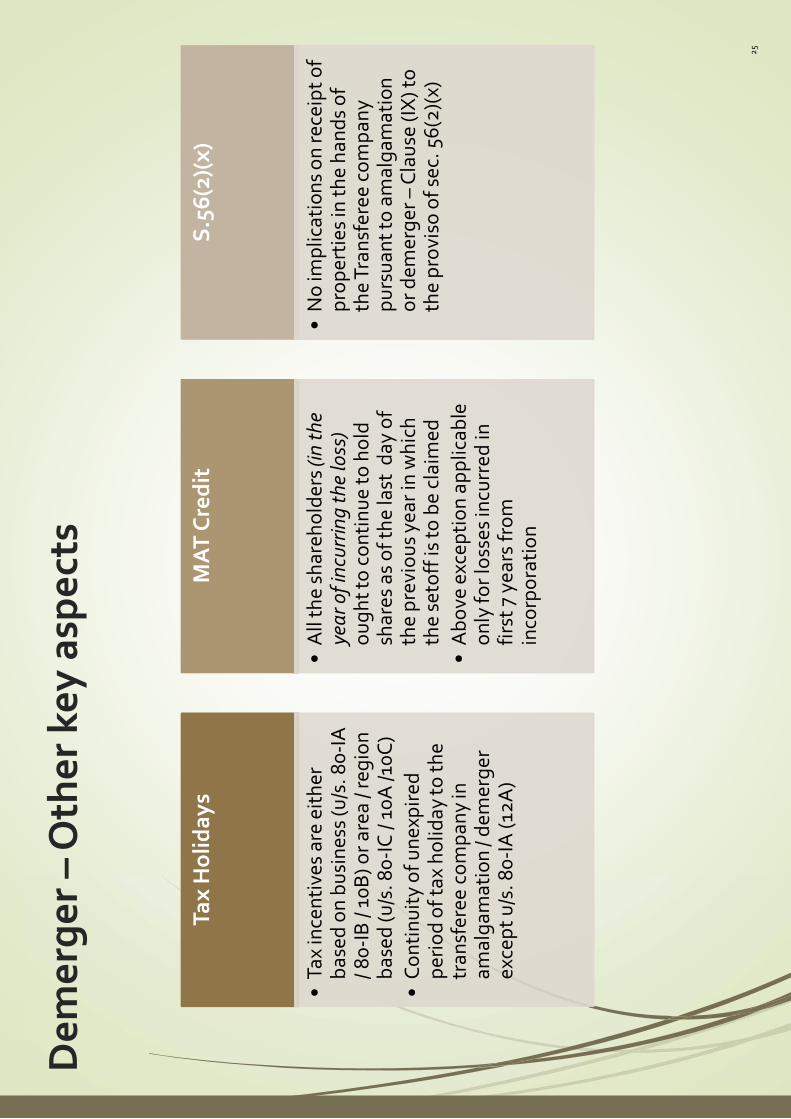

Ta

x H

oli

da

ys

•Ta

x in

cen

tive

s a

re e

ith

er

ba

sed

on

bu

sin

ess

(u/s

. 80

-IA

/ 8

0-I

B /

10B

) o

r a

rea

/ re

gio

n

ba

sed

(u

/s. 8

0-I

C /

10

A /1

0C

)

•C

on

tin

uit

y o

f u

ne

xpir

ed

p

eri

od

of

tax

ho

lida

y to

th

e

tra

nsf

ere

e c

om

pa

ny

in

am

alg

am

ati

on

/ d

em

erg

er

exc

ep

t u

/s. 8

0-I

A (

12A

)

MA

T C

red

it

•A

ll th

e s

ha

reh

old

ers

(in

th

e ye

ar

of

incu

rrin

g t

he

loss

)o

ug

ht

to c

on

tin

ue

to

ho

ld

sha

res

as

of

the

last

da

y o

f th

e p

revi

ou

s ye

ar

in w

hic

h

the

se

toff

is t

o b

e c

laim

ed

•A

bo

ve e

xce

pti

on

ap

plic

ab

le

on

ly f

or

loss

es

incu

rre

d in

fi

rst

7 ye

ars

fro

m

inco

rpo

rati

on

S.5

6(2

)(x

)

•N

o im

plic

ati

on

s o

n r

ece

ipt

of

pro

pe

rtie

s in

th

e h

an

ds

of

the

Tra

nsf

ere

e c

om

pa

ny

pu

rsu

an

t to

am

alg

am

ati

on

o

r d

em

erg

er

–C

lau

se (

IX)

to

the

pro

viso

of

sec.

56

(2)(

x)

26

�S

lum

p S

ale

27

Slu

mp

Sa

le -

Me

an

ing

•th

e t

ran

sfe

r o

f o

ne

or

mo

re

un

der

tak

ing

s

•a

s a

re

sult

of

sale

fo

r a

lum

p s

um

con

sid

era

tio

n

•w

ith

ou

t v

alu

es b

ein

g a

ssig

ned

to

ind

ivid

ua

l ass

ets

an

d li

ab

ilit

ies

in

such

sa

les

•E

xpla

na

tio

n –

De

term

ina

tio

n o

f va

lue

of

an

ass

et/

liab

ility

fo

r p

urp

ose

of

pa

yme

nt

of

sta

mp

du

ty, r

eg

istr

ati

on

fee

s sh

all

no

tb

e r

eg

ard

ed

as

ass

ign

me

nt

of

valu

es

to in

div

idu

al

ass

ets

or

liab

iliti

es

Me

an

ing

of

Slu

mp

Sa

le

[se

c. 2

(42

c)]

“Un

de

rta

kin

g”

sha

ll in

clu

de

an

y p

art

of

an

un

der

tak

ing

, or

a u

nit

or

div

isio

n o

f a

n

un

de

rta

kin

g o

r a

bu

sin

ess

act

ivit

y ta

ken

as

a w

ho

le, b

ut

do

es n

ot

incl

ud

e in

div

idu

al

ass

ets

or

lia

bil

itie

s o

r a

ny

co

mb

ina

tio

n t

her

eof

or

no

t co

nst

itu

tin

g a

bu

sin

ess

act

ivit

y

[Exp

lan

ati

on

1 t

o s

ec.

2(1

9A

A)]

Un

de

rta

kin

g

A C

o.

B C

o.

Slu

mp

Sa

le o

f U

nit

II

Sh

are

ho

lde

rsS

ha

reh

old

ers

Ca

sh c

on

sid

era

tio

n

Un

it I

Un

it I

I

Co

nce

pt

of

‘Go

ing

Co

nce

rn’ –

mo

st c

riti

cal

28

Slu

mp

Sa

le –

Ke

y t

ax

asp

ect

s

Co

mp

uta

tio

n o

f C

ap

ital G

ain

sIN

R

Full V

alu

e o

f Consid

era

tion

XX

Le

ss: T

ax

Ne

t-w

ort

ho

f th

e U

nd

ert

aki

ng

[R

efe

r T

ab

le b

elo

w]

(YY

)

Ta

xa

ble

Ca

pit

al G

ain

ZZ

Ta

x @

20

%*

(exc

lud

ing

su

rch

arg

e @

12%

an

dC

ess

@4

%)

ZZ

Z

*A

ssu

min

g t

he

Bu

sin

ess

is h

eld

fo

r 36

mo

nth

s o

r m

ore

. A

cco

rdin

gly

, th

e re

sult

an

t g

ain

is l

on

g t

erm

.

Els

e @

30%

plu

s su

rch

arg

e &

ces

s

Co

mp

uta

tio

n o

f C

ap

ital G

ain

sIN

R

Tax W

DV o

f D

epre

cia

ble

assets

X

Ad

d: B

oo

k V

alu

e o

f N

on

-de

pre

cia

ble

ass

ets

(exc

lud

ing

R

eva

lua

tio

n)

Y

Le

ss: B

oo

k V

alu

e o

f lia

bili

tie

s (e

xclu

din

g R

eva

lua

tio

n)

(Z)

Ta

x N

et-

wo

rth

YY

Co

mp

uta

tio

na

l Me

cha

nis

m

Wh

at

is T

ax

Ne

t-w

ort

h

No

tes:

•C

apital gain

will be r

egard

ed a

s s

hort

-term

if

the o

wners

hip

of

busin

ess is 3

6 m

onth

s o

r le

ss

•Benefit

of

Indexation is n

ot

available

in c

ase

of

slu

mp s

ale

•If

valu

e o

f liabilitie

s t

ransfe

rred is m

ore

than

the v

alu

e o

f assets

, i.e.

netw

ort

h o

f undert

akin

g is n

egative,

the d

iffe

rence m

ay

be a

dded t

o t

he v

alu

e o

f th

e c

onsid

era

tion f

or

tax p

urp

oses

•The c

urr

ent

year

tax b

usin

ess losses,

UAD

, b/f

capital lo

ss m

ay b

e s

et

off a

gain

st

the c

apital

gain

s a

risin

g o

n s

lum

p s

ale

−Long t

erm

Capital Loss m

ay b

e s

et

off

again

st

Long t

erm

capital G

ain

s

•Tax losses inclu

din

g U

AD

of

the identified

busin

ess w

ill not

be t

ransfe

rred in t

he h

ands

of

buyer. S

imilarly i

ncom

e t

ax b

ala

nces i.e

. Advance t

ax &

TD

S

als

o t

ypic

ally r

em

ain

with

the S

eller

29

Ta

x L

iab

ilit

y

•C

ap

ita

l Ga

ins

tax,

OR

•M

AT

pa

yab

le

•M

AT

pa

yab

le ,

if t

ax

on

bo

ok

pro

fits

* >

ca

pit

al

ga

ins

tax

+ c

orp

ora

te t

ax

−D

iffe

ren

ce b

etw

ee

n M

AT

pa

id a

nd

ca

pit

al

ga

ins

ava

ilab

le a

s M

AT

Cre

dit

fo

r ca

rry

forw

ard

a

nd

se

t o

ff u

p t

o s

ub

seq

ue

nt

15 y

ea

rs

−N

et

po

siti

on

(pro

fit

on

sa

le o

f b

usi

ne

ss a

nd

o

the

r ro

uti

ne

inco

me)

fo

r F

Y o

f cl

osi

ng

ne

ed

s to

be

ass

ess

ed

to

se

e if

lia

bili

ty u

nd

er

MA

T o

r n

orm

al t

ax

is p

aya

ble

−M

AT

cre

dit

, if

an

y, in

th

e b

oo

ks

of

Se

ller

as

on

th

e d

ate

of

tra

nsf

er

of

bu

sin

ess

will

no

t b

e

tra

nsf

err

ed

via

slu

mp

sa

le

•A

dvi

sab

le t

o c

on

firm

th

e a

cco

un

tin

g t

rea

tme

nt

wit

h t

he

Au

dit

ors

on

acc

ou

nt

of

imp

act

un

de

r In

dA

S

Se

con

da

ryri

sk–

pa

stta

xd

ue

s

•If

th

e S

elle

r fa

ils t

o p

ay

its

tax

du

es

-a

cqu

isit

ion

of

Bu

sin

ess

ma

y b

e c

on

sid

ere

d a

s vo

id

•B

uye

r m

ay

insi

st S

elle

r o

bta

inin

g a

Ta

x C

lea

ran

ce

Ce

rtif

ica

te f

rom

TA

Su

cce

ssio

n R

isk

•If

slu

mp

sa

le is

co

nsi

de

red

to

be

su

cce

ssio

n o

f b

usi

ne

ss:

−B

uye

r co

uld

be

he

ld li

ab

le f

or

an

y in

com

e t

ax

liab

iliti

es

of

Se

ller

pe

rta

inin

g t

o F

Y y

ea

r in

w

hic

h t

he

su

cce

ssio

n t

oo

k p

lace

up

to t

he

da

te

of

succ

ess

ion

an

d F

Y p

rece

din

g t

ha

t ye

ar.

Eg

: T

ran

sact

ion

co

mp

lete

d -

1 F

eb

20

18, B

uye

r’s

risk

-Ta

x lia

bili

ty o

f F.

Y. 1

6-1

7 a

nd

1 A

pri

l 17

till

31 J

an

18

.

−A

cco

rdin

gly

, Bu

yer

ma

y in

sist

fo

r in

de

mn

ity

as

a s

afe

gu

ard

.

Se

lle

rs P

ers

pe

ctiv

eB

uy

ers

pe

rsp

ect

ive

Slu

mp

Sa

le –

Ke

y t

ax

asp

ect

s

30

Ta

x D

ep

reci

ati

on

•In

th

e y

ea

r o

f tr

an

sfe

r -

−Seller

can c

laim

depre

cia

tion o

n a

ssets

in

ratio o

f num

ber

of

days t

he a

ssets

were

used

Wit

hh

old

ing

ob

lig

ati

on

s o

n t

ran

sfe

r o

f im

mo

va

ble

p

rop

ert

y

•M

ay

no

t b

e r

eq

uir

ed

–A

rgu

ab

ly, i

n c

ase

of

a s

lum

p

sale

, ‘b

usi

ne

ss’ i

s b

ein

g t

ran

sfe

rre

d a

nd

th

ere

is n

o

sta

nd

alo

ne

tra

nsf

er

of

imm

ova

ble

pro

pe

rty

•T

his

ne

ed

s to

be

te

ste

d w

ith

re

leva

nt

loca

l p

rop

ert

y re

gis

tra

tio

n o

ffic

e

Ta

x D

ep

reci

ati

on

•In

th

e y

ea

r o

f tr

an

sfe

r -

−B

uye

r ca

n c

laim

de

pre

cia

tio

n o

n a

sse

ts in

ra

tio

o

f n

um

be

r o

f d

ays

th

e a

sse

ts w

ere

use

d

−In

su

bse

qu

en

t ye

ars

, ta

x d

ep

reci

ati

on

ma

y b

e

ava

ilab

le o

n s

tep

pe

d u

p v

alu

e (a

s p

er

PP

A)

−B

uye

r co

uld

cla

im d

ep

reci

ati

on

on

ce

rta

in

inta

ng

ible

s re

cord

ed

ba

sis

PP

A s

uch

as

go

od

will

, kn

ow

-ho

w, p

ate

nts

, co

pyr

igh

ts, t

rad

e

ma

rks,

lice

nse

s, f

ran

chis

es

or

an

y o

the

r b

usi

ne

ss o

r co

mm

erc

ial r

igh

ts o

f si

mila

r n

atu

re

Se

lle

rs P

ers

pe

ctiv

eB

uy

ers

pe

rsp

ect

ive

Slu

mp

Sa

le –

Ke

y t

ax

asp

ect

s

31

Slu

mp

Sa

le –

Ke

y t

ax

asp

ect

s

Pa

rtic

ula

rs

Slu

mp

Sa

le v

ia S

che

me

Slu

mp

Sa

lev

ia B

TA

Invo

lvin

g g

ove

rnm

en

t co

ntr

act

so

r lic

en

se

tra

nsf

ers

or

oth

er

reg

ula

tory

ap

pro

vals

•P

refe

rab

le

•L

ess

pre

fera

ble

Pre

-qu

alif

ica

tio

ns

tra

nsf

er

en

visa

ge

d

•P

refe

rab

le•

Le

ss p

refe

rab

le

Tim

ein

volv

em

en

t•

Lo

ng

er

tim

elin

e•

Sh

ort

er

tim

elin

e

Re

gu

lato

ry a

pp

rova

ls•

Ma

nd

ato

ry a

pp

rova

ls o

f va

rio

us

au

tho

riti

es

un

de

r N

CLT

ro

ute

incl

ud

ing

a

n in

tim

ati

on

to

inco

me

ta

x a

uth

ori

tie

s

•L

ess

er

ap

pro

vals

re

qu

ire

d

Sta

mp

du

ty *

Co

uld

be

re

stri

cte

d t

o M

axi

mu

m s

tam

p

du

ty o

f th

at

pa

rtic

ula

r st

ate

; Eg

: M

ah

ara

shtr

a –

INR

25

crs

No

su

ch r

est

rict

ion

Inco

me

Ta

x / G

ST

Sa

me

tre

atm

en

t in

bo

th s

cen

ari

os

Slu

mp

Sa

le v

ia S

che

me

vs

Slu

mp

Sa

le v

ia B

TA

32

�It

em

ise

d S

ale

33

Ite

miz

ed

Sa

le –

Me

an

ing

an

d T

ax

Imp

lica

tio

ns

•N

ot

de

fin

ed

un

de

r IT

Act

•In

volv

es

ind

ivid

ua

l sa

le o

f a

sse

ts

•C

on

sid

era

tio

n is

ide

nti

fia

ble

ag

ain

st e

ach

ass

et

•B

uy

er

dis

cha

rge

s co

nsi

de

rati

on

to

th

e s

elle

r fo

r th

e a

sse

t a

cqu

ire

d

Me

an

ing

Ta

x Im

pli

cati

on

s

Na

ture

of

Ass

et

Na

ture

of

Inco

me

De

pre

cia

ble

Ass

ets

-P

rovi

sio

ns

of

S.5

0a

re a

pp

lica

ble

-

Sh

ort

te

rm c

ap

ita

l ga

ins

(if

the

con

sid

era

tio

n >

WD

V o

f th

e re

leva

nt

blo

ck o

f a

sset

)

No

n –

De

pre

cia

ble

Ass

ets

-S

ho

rt t

erm

ca

pit

al g

ain

s / L

on

g t

erm

ca

pit

al g

ain

s(D

ep

en

din

go

n t

he

pe

rio

d o

f h

old

ing

)

Cu

rre

nt

Ass

ets

Bu

sin

ess

pro

fits

34

Ite

miz

ed

Sa

le v

s S

lum

p S

ale

Pa

rtic

ula

rsIt

em

ize

d S

ale

Slu

mp

Sa

le

De

fin

itio

n u

nd

er

IT A

ctN

ot

spe

cifi

ed

De

fin

ed

spe

cifi

cally

Cri

teri

a o

f ‘U

nd

ert

ak

ing

’N

ot

req

uir

ed

to

be

co

mp

lied

wit

hR

eq

uir

ed

to

be

co

mp

lied

wit

h

Tra

nsf

er

of

‘Lia

bil

itie

s’F

lexi

bili

ty o

f n

ot

acq

uir

ing

th

e

liab

iliti

es

No

Fle

xib

ility

Co

nsi

de

rati

on

No

sp

eci

fic

con

dit

ion

sL

um

psu

mC

on

sid

era

tio

n

Ca

pit

al G

ain

s

com

pu

tati

on

me

cha

nis

mC

ap

ita

l ga

ins

to b

e c

om

pu

ted

fo

r e

ach

ite

m o

f ca

pit

al a

sse

tC

ap

ita

l ga

ins

to b

e c

om

pu

ted

fo

r ‘u

nd

ert

ak

ing

’ as

pe

r sp

eci

fie

d f

orm

ula

in

th

e IT

Act

Na

ture

of

ga

ins

/ lo

ss-

Fo

r d

ep

reci

ab

le a

sse

ts–

sho

rt

term

-F

or

no

n d

ep

reci

ab

le a

sse

ts–

de

pe

nd

s o

n t

he

pe

rio

d o

f h

old

ing

of

ass

ets

-D

ep

en

ds

on

th

e p

eri

od

of

ho

ldin

g o

f

the

un

de

rta

kin

g

-H

old

ing

pe

rio

d o

f in

div

idu

al

ass

ets

no

t

rele

van

t

Ind

exa

tio

n b

en

efi

tA

vaila

ble

(in

ca

se o

f n

on

de

pre

cia

ble

lon

g-t

erm

ass

ets

)

No

t A

vaila

ble

Pro

visi

on

s o

f se

c. 5

0C

Ap

plic

ab

leN

ot

Ap

plic

ab

le

35

�S

ha

re A

cqu

isit

ion

s

36

Sh

are

Acq

uis

itio

n –