18

IDC FutureScape: Latin America IT Industry 2016 Predictions Jay Gumbiner Research Vice President, Latin America December 10, 2015

IDC FutureScape: Latin America IT Industry 2016 Predictions

Jay Gumbiner

Research Vice President, Latin America

December 10, 2015

IDC Predictions: How the Process Works

Global brainstorm of over 1,000

IDC analysts

How we choose our prediction themes…

• Opportunity-oriented

• Impact many market segments

• Involve structural changes, require strategic choices

• Unique opportunities to establish market leadership

2

Latin America Predictions Team

Alejandro Floreán

Jay Gumbiner

Marcelo Leiva

Jerónimo Piña

Enrique Phun

Waldemar Schuster

Juan Pablo Seminara

Paola Soriano

Ricardo Villate

Daniel Zegarra

Leandro Agion

Diego Anesini

David Ayvar

Luciano Crippa

Carlo Dávila

3

IDC FutureScape: Latin America IT Industry 2016 Predictions

Figure

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 4

Note: The size of the bubble indicates complexity/cost to address. Source: IDC, 2015

1

2

3

4

5

6

7

8

9

10

By the End of 2017, one in three CEOs of the Top 3,000

Companies in Latin America will have Digital

Transformation at the center of their corporate strategy

3rd Platform Workload First will be the initial IT

infrastructure decision point in the DX era and involve more

than 40% of IT infrastructure investments by 2018

By 2018, at least 40% of enterprise IT spending will be

cloud based, reaching more than half of all IT Infrastructure,

software, services, and technology spending by 2020

By 2016, 45% of Latin American Companies will align IT

and LOB efforts towards a definitive Mobile Strategy

Disruptive computing form factors will change how workers

create, access and interact with data for their companies

with over 14 million ‘hybrid’ devices shipped in Latin

America in 2016

In 2016, 30% of Latin American consumer goods and retail

businesses will invest in 3rd Platform IT to exploit the

ecommerce explosion happening beneath the economic

slowdown surface

By the end of 2016, nearly half of Latin American

companies will be implementing a Next Generation Security

strategy by investing in specialized security consulting,

services and technologies

During 2016, more than two-thirds of IT project initiatives

will require demonstration of cost savings, forcing ‘open

sourced’ 3rd Platform into the spotlight

As IoT crosses the chasm, ten use cases in manufacturing,

transportation, consumer, government, and utilities will

become mainstream in LA and represent 80% of IoT

spending in 2016

By 2018, one third of companies pursuing DX will add

cognitive and VR/XR design capabilities to their app design

strategies

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

10

3

8

1

7

6

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9

eCommerce

IoT use cases

Cognitive, AR/VR design capability

“Digital Transformation (DX) Scales Up”

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 5

Source : IDC

IT/BU

Impact

Guidance

DX initiatives will rest on 3rd

Platform Pillars, mobility and

Cloud first

New mission critical

applications will be developed

mostly in a Cloud environment.

Most DX oriented strategies

will require the creation of an

executive DX position

IT suppliers should accelerate

the shift of the offerings from

the 2nd Platform to the 3rd

Platform, mapping them to DX

initiatives.

CIOs/CTOs must transform

their role from technology

expert and project execution to

a DX enabler.

1. By the End of 2017, one in three CEOs of the Top 3,000

Companies in Latin America will have Digital Transformation

at the center of their corporate strategy

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 6

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

$4.5 BIT spending driven by digital transformation initiatives

in 2016

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

2. 3rd Platform Workload First will be the initial IT infrastructure

decision point in the DX era and involve more than 40% of IT

infrastructure investments by 2018

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 7

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

SDx related investment will

continue to grow 50% in 2016

Multi-cloud orchestration will

need to address network

transport, storage, and security

IT staff should reduce cost of

legacy without massive

migration as IT operation

budgets will reduce 10 to 15%

Beyond cloud and/or 3rd

platform strategy, organizations

must become "App first" ones

IT organizations should

evaluate software-defined and

open source elements in

infrastructure implementation

Skills development will remain

a great challenge

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

5 102

3

8

1

7

6

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

3. By 2018, at least 40% of enterprise IT spending will be

cloud based, reaching more than half of all IT Infrastructure,

software, services, and technology spending by 2020

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 8

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT Impact

Guidance

Faster business transformation

becomes the expected

business outcome of cloud

Hybrid ecosystems will persist

and will be the rule

Industry cloud platforms will

transform many Latin American

enterprises into cloud services

providers

CIOs must integrate a "cloud

first" vision into their IT top

initiatives for 2016

Many companies

will incorporate IT

workload dashboards to their

operational balanced

scorecards

$3.6 BInvestment in public cloud services and in hosted

private clouds in 2016

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

10

3

8

1

7

6

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

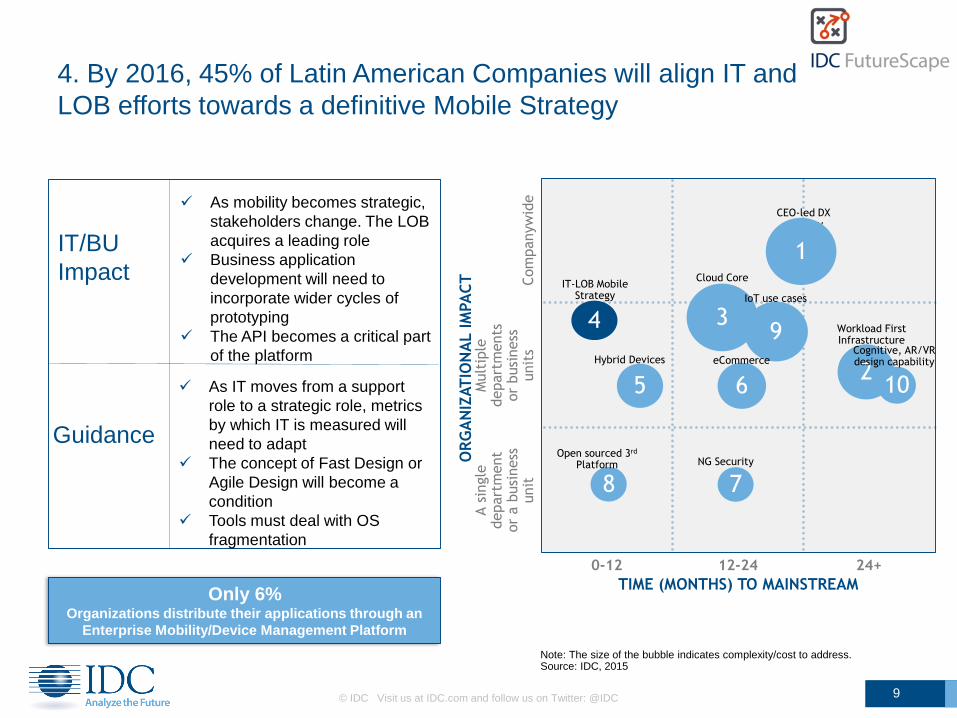

4. By 2016, 45% of Latin American Companies will align IT and

LOB efforts towards a definitive Mobile Strategy

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 9

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

As mobility becomes strategic,

stakeholders change. The LOB

acquires a leading role

Business application

development will need to

incorporate wider cycles of

prototyping

The API becomes a critical part

of the platform

As IT moves from a support

role to a strategic role, metrics

by which IT is measured will

need to adapt

The concept of Fast Design or

Agile Design will become a

condition

Tools must deal with OS

fragmentation

Only 6%Organizations distribute their applications through an

Enterprise Mobility/Device Management Platform

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

10

3

8

1

7

6

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

5. Disruptive computing form factors will change how workers create,

access and interact with data for their companies with over 14 million

‘hybrid’ devices shipped in Latin America in 2016

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 10

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

Employees will have smaller

and lighter computing devices

with them at all times

Business applications built to

take advantage of these

devices will have a profound

impact on how internal/external

processes are completed

Business managers must

analyze internal and external

processes to determine better

screen size and functionality

Use country specific ROI

Ensure applications running in

new form factors makes proper

use of the functionality

14 million

Hybrid devices shipped in Latin America in 2016

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

6. In 2016, 30% of Latin American consumer goods and retail

businesses will invest in 3rd Platform IT to exploit the ecommerce

explosion happening beneath the economic slowdown surface

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 11

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

Online commerce platforms will

shift from a ‘nice to have’ to a

‘must have’

Companies will invest in

adaptable, scalable and secure

online payment systems

Pursue a seamless omni-

channel experience

Optimize physical and online

supply chain and establish

policies for returned goods

Optimize the user experience

regardless of the device being

used to access the data

$68 BillionOnline spending in top six countries in the region in

2016

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

7. By the end of 2016, nearly half of Latin American companies will be

implementing a Next Generation Security strategy by investing in

specialized security consulting, services and technologies

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 12

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

Implementing an NGS strategy

demands specialized security

services

In 2016 2 out of 3 companies

will face challenges for

underutilizing security

Cloud and Mobility exacerbate

the need to address risk of

data in motion

Companies need to develop an

Incident Response strategy,

which could mean setting up

an IR team or outsource it

Consider a network

segmentation strategy

LOB’s cloud initiatives need to

adhere to corporate security

strategy

53%Growth in 2016 in spending on security solutions

offered from a cloud platform

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

8. During 2016, more than two-thirds of IT project initiatives will

require demonstration of cost savings, forcing ‘open sourced’

3rd Platform into the spotlight

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 13

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

LOB managers will request

consideration of open source

elements in half of the Cloud

investments in 2016.

30% of CIOs have recognized

open source and born-in-the-

cloud vendors as best qualified

to support on-demand projects

Cost vs. ease of

implementation and

governance will define

decisions in 2016

Companies driving IT initiatives

related to open source will

select those vendors with

better local support and SLAs

30%+

Growth in spending on open source solutions

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

9. As IoT crosses the chasm, ten use cases in manufacturing,

transportation, consumer, government, and utilities will become

mainstream in LA and represent 80% of IoT spending in 2016

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 14

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

Network is an essential asset

to ensure quality in data

transport

Analytics tools of fundamental

importance

During 2016, Latin America will

also see the birth of hundreds

of companies developing IoT

solutions

Interoperability, adaptability,

scalability, and security are

essential

Industry forums,

standardization and

orchestration will greatly

accelerate the development of

an ecosystem

59%Organizations in Latin America actively exploring IoT

initiatives for 2016

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

10. By 2018, one third of companies pursuing DX will add

cognitive and VR/XR design capabilities to their app design

strategies

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 15

Note: The size of the bubble indicates complexity/cost to address.Source: IDC, 2015

IT/BU

Impact

Guidance

Curated content, content

aggregation, integration and

collaboration are required

These technologies promise a

revolutionary change in the

experience

The marketplace will be quickly

exposed to applications

originating around the globe

Early adopters: educate on

platform maturity

Vendors and application

developers: consider the

implications of multiple existing

platforms

All: integration to legacy must

not slow down innovation

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

3

8

1

7

6 10

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9eCommerce

IoT use cases

Cognitive, AR/VR design capability

IDC FutureScape: Latin America IT Industry 2016 Predictions

Figure

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 16

Note: The size of the bubble indicates complexity/cost to address. Source: IDC, 2015

1

2

3

4

5

6

7

8

9

10

By the End of 2017, one in three CEOs of the Top 3,000

Companies in Latin America will have Digital

Transformation at the center of their corporate strategy

3rd Platform Workload First will be the initial IT

infrastructure decision point in the DX era and involve more

than 40% of IT infrastructure investments by 2018

By 2018, at least 40% of enterprise IT spending will be

cloud based, reaching more than half of all IT Infrastructure,

software, services, and technology spending by 2020

By 2016, 45% of Latin American Companies will align IT

and LOB efforts towards a definitive Mobile Strategy

Disruptive computing form factors will change how workers

create, access and interact with data for their companies

with over 14 million ‘hybrid’ devices shipped in Latin

America in 2016

In 2016, 30% of Latin American consumer goods and retail

businesses will invest in 3rd Platform IT to exploit the

ecommerce explosion happening beneath the economic

slowdown surface

By the end of 2016, nearly half of Latin American

companies will be implementing a Next Generation Security

strategy by investing in specialized security consulting,

services and technologies

During 2016, more than two-thirds of IT project initiatives

will require demonstration of cost savings, forcing ‘open

sourced’ 3rd Platform into the spotlight

As IoT crosses the chasm, ten use cases in manufacturing,

transportation, consumer, government, and utilities will

become mainstream in LA and represent 80% of IoT

spending in 2016

By 2018, one third of companies pursuing DX will add

cognitive and VR/XR design capabilities to their app design

strategies

TIME (MONTHS) TO MAINSTREAM

OR

GA

NIZ

AT

ION

AL I

MPA

CT

A s

ingle

depart

ment

or

a b

usi

ness

unit

Mult

iple

depart

ments

or

busi

ness

unit

sCom

panyw

ide

0-12 12-24 24+

CEO-led DX strategy

Cloud Core

52

10

3

8

1

7

6

Workload First Infrastructure

IT-LOB Mobile Strategy

4

Hybrid Devices

NG SecurityOpen sourced 3rd

Platform

9

eCommerce

IoT use cases

Cognitive, AR/VR design capability

Joining us for Q&A:

Ricardo Villate, Group VP

Alejandro Floreán, Consulting

Diego Anesini, Enterprise Solutions

Juan Pablo Seminara, Enterprise HW

Paola Soriano, Devices

Carlo Dávila, Security Solutions

Daniel Zegarra, Emerging Markets

Leandro Agion, Telecom Services

Jerónimo Piña, Software

Luciano Crippa, Devices

Marcelo Leiva, Software

17

18