29

CFA Institute Research Challenge Hosted in CFA Spain Society (Madrid) IE Business School Team

| Date post: | 28-Jul-2015 |

| Category: |

Documents |

| Upload: | daniel-d-mirolli |

| View: | 76 times |

| Download: | 1 times |

CFA Institute Research ChallengeHosted in

CFA Spain Society (Madrid)IE Business School Team

Highlights

Forecast Summary, €M 2011 2012 2013E 2014E 2015E 2016E 2017E

Total Net Revenues 825.5 827.5 862.1 831.8 841.9 841.8 835.9

EBITDA 139.1 139.3 166.8 134.1 138.3 142.5 141.1

Net profit 41.2 43.0 52.1 43.3 40.8 43.2 41.6

Earnings per Share (€) 0.16 0.17 0.19 0.16 0.15 0.16 0.15

Dividend/Share (€) 0.1 0.07 0.08 0.06 0.06 0.06 0.06

We initiate our coverage of ENCE with a sell recommendation and a price target of EUR 2.26,

which represents a 12.3% downside potential from the current stock price. The Company’s business

model has suffered from recent regulations and we see an unfavorable market environment.

Pulp division: ENCE’s market share in pulp sales is diversified among European countries and the

Company has a good strategic positioning with respect to suppliers and customers. It has been

decreasing its exposure to the Spanish market, but Spain and Italy’s economies still represent a high

portion of sales of approximately 35%. As a result of South American pulp producers building up

capacities, we expect downward pressure on global pulp prices in the second half of 2014.

Energy division: The Royal Decree Act 9/2013 has heavily impacted the counter-cyclical energy

business, which has a stabilizing effect on Company revenues compared to the volatile pulp sales.

After the regulatory change, however, we project the NPV of cash flows to equity of this segment to

be equal to zero.

Financials: A reduced but stable operating cash flow generation of around EUR 50M is predicted

to continue going forward, attributed to a relatively stagnant pulp sector and the diminished but

stable effect of the renewables business. This sustainable ability of generating cash combined with

fewer predicted capital expenditures of around EUR 81M p.a. going forward result in relatively

high cash balances. Consequently, net financial debt is expected to halve in the years from 2014 to

2017, throughout being in line with the Company's target of maximum 2.5x Net Debt / EBITDA.

Market Snapshot

Market Capitalization (EM) 710

Shares Outstanding (M) 275

Main Shareholders

Alcor Holding 26.5%

Juan Luis Arregui 23.2%

Free Float 33.4%

52w Price Range (EUR) 1.90 - 3.13

Avg. monthly Volume (M shares) 1.308

Beta (to IBEX Mid Cap) 1.18

Relative Performance (to IBEX Mid Cap)

1 Month -13%

3 Months -27%

12 Months -37%

3 Years -21%

Key Ratios 2013

Debt / Equity 0.47

Net Debt / Equity 0.12

Net Debt / EBITDA 0.53

ROE 6.9%

ROA 3.7%

EV/EBITDA 4.96

P/E 13.03

P/CF 5.51

P/B 0.86

Valuation

Target (€) 2.26

DCF (€) 2.05

Multiples (€) 2.48

Downside -12%

WACC 6.7%

Cost of Equity 9.5%

Cost of Debt 4.7%

Target Leverage D/(D+E) 45%

Downside -12.3%

ENCE Energia y Celulosa S.A. Ticker: ENC:SM (Bloomberg)

Current price:

Target price:

Downside:

Recommendation:

€2.58

€2.26

-12.30%

SELL

IE Business School Research Team

Sector: Materials and Energy

Industry: Forest & Paper products and Renewable energy

Exchange: Madrid Stock Exchange

Akshay Dalmia, Fabian Dienemann,

Daniel Mirolli, Yehor Serdiuk, Viktor

Stoichkov

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 2

Business Description

ENCE Energia y Celulosa SA, formerly Grupo Empresarial ENCE SA (ENCE), is Europe’s leading

producer of eucalyptus pulp, the second largest in terms of sales. The Company operates across

three divisions: pulp production, renewable energy (utilizing forest biomass), and forestry supply

management. Three industrial sites, located in Huelva, Navia, and Pontevedra, serve as production

and power generation mills.

Business Units Pulp

Eucalyptus pulp production (abbreviated as BHKP) comprises 71% of ENCE’s total sales (Q3

2013). ENCE’s three plants supply a production capacity of 1.34 million tons of pulp per year.

Energy

Power production generates 28% of total sales (for the same period), utilizing seven production

plants spread across the aforementioned industrial sites with an additional (biomass) plant slated for

Merida (construction began in 2012). Three of the existing seven plants are cogeneration facilities

integrated into pulp plants. Three generation plants produce energy from wood and pulp by-

products and there is one stand-alone project which is still under construction.

Forestry

A mere 1% of total sales, forestry supply management is quickly being transferred to a third-party

supplier model. December 17, 2013 saw the sale of all ENCE’s forestry assets in Portugal for $15.4

million.

Geographic Units

While the Company operates throughout Europe, with 56% of annual sales in European countries

other than Spain and 5% in the Asian Pacific region, all sales of Renewable Energy production

occur within Spain’s borders. Consequently, sales in Spain grew by 86% from 2011-2012 filing

dates while Asia Pacific saw a drop in sales of 24.9% in the same period. The Company has 92% of

annual sales in Europe with the remaining 8% in China (see Figure 1.2 – 1.3).

Company Strategy

Currently the Company is enroute to adopt a 3rd party forestry supply management strategy in order

to improve efficiency and cost reduction. Compared to 12% in 2007, approximately 30% of wood

supply in 2012 came from landowners (a trend that continued in 2013). Consequently, forestry

share in the Company revenue has been decreasing steadily from 11% in 2007 to only 1% in

September 2013. Therefore, we consider this division to be immaterial for our analysis.

On the contrary, Energy’s share of revenue has been increasing from 10% in 2007 to 28% in 2013.

The amount sold has evolved from 1,161 GWh in 2012 to 1,420 GWh in 2013. However, due to the

recent regulatory changes (RDL 9/2013) the expected ROI from biomass projects in Spain is

unattractive and the Company will likely halt further investment. At the moment we expect the

NPV of cash flows to equity from the Energy division to be zero. The sudden change in strategy

will again increase the relative importance of the pulp division and decrease the balancing effect of

the energy division’s counter-cyclical revenue stream.

Due to the cyclicality of the pulp business, the Company has been using derivative instruments to

hedge against the risk of fluctuating cellulose pulp prices on a 12-month basis. Further cost

reduction measures are also being applied through the Company’s employee reduction program.

The projected savings amount to EUR 5.5M in 2014 and EUR 6.3M in 2015 respectively.

Shareholder Structure Stable ownership but low liquidity

With a market capitalization of approximately EUR 710M, ENCE has around 275M shares

outstanding with one-third in free float and two-thirds as internal ownership (Figure 1.5). Of the

total equity available, institutional money managers currently hold 15.5% while 18.23% is spread

amongst other investors. The high level of private and institutional ownership for a small cap could

pose a risk for potential investors and result in liquidity issues in future atypical market phases.

The Company is largely owned by private individuals, e.g. Juan Luis Arregui (23.24% ownership),

who has acted as the president of the Company since 2006. His stake is therefore strategic and long-

term, which can be a stabilizer for the share price.

Alberto Alcocer and Alberto Cortina, publicly known for their ownership in ACS (major Spanish

Figure 1.1 | Change in Sales Q2 2012 to Q2 2013

Source: Company Annual Report

Figure 1.2 | Country % of Sales

Source: Company Annual Report

Figure 1.3 | Geographic % of Annual Sales

Source: Company Annual Report

Figure 1.4 | BHKP End Use

Source: Company Annual report

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 3

construction company), form the largest shareholding party with a 26.52% stake through Alcor

Holding. Contrary to the stabilizing effect of Mr. Arregui’s stake, Alcor’s ownership might pose a

risk to the share price, citing dubious business activities in the past. This year they have been fined

EUR 10.8M plus EUR 14M in interest payable to the minority shareholders of Urbanor after being

found guilty of racketeering. As a consequence there are rumors of disinvesting activities in their

portfolio holdings.

In first half of 2013 the Company decreased its treasury shares that resulted from an issue premium.

Firstly, a stock dividend was distributed (1:25). Secondly, treasury stock representing 5% of total

equity was sold to private investors to further stabilize the shareholder structure. Also worth

mentioning, Liberbank (Spain based) recently liquidated its holdings that were later acquired by

Amber Capital (a British asset manager).

Corporate Governance and CSR Strategic importance for ENCE

ENCE's Corporate Governance (CG) policies and Corporate Social Responsibility (CSR) are

designed to help achieve its general objectives and to protect its shareholders. The board of

directors has established an executive, audit as well as appointments and remuneration committee.

The Management Committee, the Company's main decision-making body, is responsible for the

management of ENCE and is comprised of the directors of business and management. Although the

Company is not strictly following international guidelines such as the International Corporate

Governance Network, which can be attributed to its small size, we believe that their corporate

governance is sufficiently strong.

Total Quality Management was adopted in 2011 to develop a model of excellence in management

based on quality, efficiency, human capital and continuous improvement. The Company integrates

economic, social and environmental sustainability criteria into their activities and shows

commitment to all stakeholders, acting in accordance with the Ten Principles of the UN Global

Compact (which promote corporate social responsibility). The fundamental rules are established in

an internal code of conduct and since 2004 the Firm also publishes a yearly sustainability report

based on the Global Reporting Initiative.

Pulp

Industry Analysis Setting up the dominoes

Wood pulp comes from softwood trees such as spruce, pine, fir, larch and hemlock and hardwood

trees such as aspen, birch, and eucalyptus (the focus of ENCE’s production). China has been

leading in global pulp consumption growth since 2009.

Cool-down in China and bearish on commodities

China is a major market for pulp. We forecast China’s economy to slow and its demand for pulp to

decline on the premise of a declining macroeconomic outlook. China’s GDP saw only a 7.7%

growth in 2013 (while consensus estimates were 8%). China’s economic growth is a leading

indicator of global commodity markets (Figure 2.1), with a correlation of 84% in the period 2009-

2012. As China’s economic growth continues to slow, the commodity outlook is expected to be

bearish.

Pressure on Pulp Prices

We also find that (Figure 2.2) the Commodities Index is correlated (60%) with the price of pulp,

especially during bearish markets. While history shows growth well above the index average in bull

markets, following our expectation of China’s slowing growth, we are bearish on the price of

commodities and therefore the price of pulp. Furthermore, there is a strong correlation of 90.3%

between ENCE’s sales (delayed 6 months) and global pulp prices (Figure 2.3). It should be noted

that sales have been relatively stable since 2011 due to hedging strategies employed by ENCE (with

derivatives hedged on a twelve month basis).

Increasing Pulp Production in a Consolidating Industry

There is an increasing production trend (Figure 2.4) and decreasing trend in the number of pulp

mills for that same production (Figure 2.5). This indicates an increase in operating capacities for

pulp producers and a potential increasing maintenance CAPEX for the industry as a whole.

Global Pulp Supply Expected to Outstrip Demand

It is expected that in 2014 supply will outstrip demand by 0.6 million tons and between 2013-2016

Figure 1.5 | Share Ownership

Source: FactSet

“Although the Company is not strictly

following international guidelines…we

believe that their corporate governance is

sufficiently strong”

Figure 2.1 | China’s Real GDP vs Commodities Index

Source: FactSet

Figure 2.2 | CRB Index vs FOEX PIX BHKP Prices

Source: FactSet

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 4

the supply will be (on average) in excess by 0.3 million tons (Figure 2.6). This shift in the supply

curve is mainly due to increased capacities of South American pulp producers who are going to

supply this excess quantity to the market in 2014. This further reinforces our bearish outlook on the

pulp market.

Pressure from Higher Production Costs

Wood and chemicals prices are the main cost drivers in pulp production. The Company expects

input prices to increase in the near future that will negatively affect industry margins.

Substitute Products

There is a growing threat from recycled paper as “world recovered paper demand has grown by

45% in the last 10 years” (RISI, global forestry industry data provider). As recycling and pressing

processes continue to improve, substitute products will pose a greater threat on the pulp industry.

High Pulp Inventories and Lower Consumption

It can be observed that over a 1-year period, levels of consumption and pulp prices have been on a

downtrend while inventory levels have been increasing (YoY basis). In the past year, the average

(YoY) change in prices and consumption has been -2.17% and -3.96%, respectively. Inventories

have increased 4.23% over the same period (Figure 2.7). Furthermore, the pulp inventory levels for

end consumers have been declining while the producers are stocking up excess production. This

reaffirms the downward pressure on pulp prices.

Competitive Position

ENCE enjoys several advantages over its European competitors in the pulp industry. Being based in

Spain and Portugal affords the Company the ability to produce pulp through eucalyptus wood, a

process resulting in a shorter rotation cycle per ton of pulp produced than other hardwoods. Spain is

one of the only countries in Europe whose climate can sustain eucalyptus pulp production (the

others being Portugal and parts of Italy).

ENCE already operates in a saturated market, as the 2nd largest supplier of pulp in Europe and its

location on the Iberian peninsula will continue to serve as a platform for substantial port-shipping

capabilities and a logistic advantage due to the proximity of production facilities to major ports.

These factors provide ENCE with strong competitive advantage within the European market. On a

global scale ENCE has 5% of the global BHKP market share. However, ENCE has higher cash

costs in comparison with pulp producers in LATAM as well as fewer opportunities for land

accretion. Moreover, ENCE is not well positioned for competing for the Chinese market, which is

the one with the highest global growth in pulp demand.

Renewable energy

Industry Analysis Promising industry subject to regulatory changes

The European Commission and many other private and public organizations believe that biomass

for energy production can play an important role in meeting Europe’s targets for renewable energy

generation. However, its potential is being realized at a slow pace, as the current growth rate is only

1/3 of EU projections. In Spain, biomass comprises the largest share of renewable electricity

production. Although 75% of all renewable electricity comes from biomass, there is still capacity

for growth. According to the European Climate Foundation, there is a large cost improvement

potential in biomass-generated power through economies of scale (15-40% compared to today).

Furthermore, biomass is the most reliable source of alternative energy for grid stability.

Political issues

The European market is currently governed by the EU Climate and Energy Package, which stipulate

that by the year 2020, 20% of all the energy produced within member countries should come from

renewables. Currently, 16.4% (Figure 3.1) of all energy generated in Spain comes from renewables,

9.5% of which is attributable to renewable-electrical and 6.5% to renewable-thermal, providing

limited room for growth.

Regulated prices

The new Royal Decree Law 9/2013 (RDL 09/13) governs all prices of renewable energy in Spain.

The political aim is to sustainably prevent future deficits in the electricity system. The previously

adopted tariff system was replaced with a system offering an internal rate of return based on the

average yield on Spanish 10-year government bonds plus a differential (currently 300bp). At the

Figure 2.3 | ENCE Sales vs BHKP Prices

Source: FactSet

Figure 2.4 | Production Trend

Source: PPPC

Figure 2.5 | Consolidating Industry Trend

Source: Company Annual Report and PPPC

Figure 2.6 | Evolution of Global Supply & Demand

Source: RISI (all figures in million tons)

Figure 2.7 | Inventory Trends (Consumption and

Prices)

Source: PPPC

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 5

moment this adds to approximately 6.5%. The return received is calculated from the rate of return

obtained on renewable projects based on the “standard” sales income, operating costs and initial

investment. The law also removes the payments for efficiency and reactive bonuses. Effectively, the

law change has an extremely negative impact on biomass firms, that up to date is not easy to

quantify, however we expect prices to be around 15% below the old remuneration system.

Cost-efficiency

Approximately 60% of biomass electricity comes from cogeneration in production facilities or from

using by-products from manufacturing, allowing for very low costs. Moreover, integrated energy

facilities lead to higher cost-competitiveness, as energy can be both consumed internally while the

excess can be sold.

Competitive Position

ENCE owns seven energy generation facilities at four different locations across Spain with one still

under construction. These plants add up to c.300 MW of total installed capacity. This makes the

Company the nation's largest producer of renewables from biomass, which translates to a market

share of more than 50%. We believe that this dominant position is a strength and leads to economies

of scale. However, due to the recent regulatory changes, market-leadership cannot be seen as a

competitive advantage and the Company does not plan further growth investments into their energy

business in the coming years.

The Company benefits from synergies between their pulp and energy divisions as the energy comes

from co-generation (integration in pulp plants) or from wood and pulp by-products. Furthermore,

self-produced energy is used for their own pulp plants, reducing the costs of production. Currently,

around 230 MW comes from co-generation or by-products and only 70 MW of capacity is

contributed from standalone projects.

As the first Spanish producer of renewable energy from biomass, we believe that one competitive

advantage is ENCE's industry expertise. The firm’s experience combined with investments in R&D,

provides a higher productivity compared to competitors. This was shown by the higher than

expected efficiency of the Huelva plant that started its operations in 2012 (with more operating

hours and less self-consumption of energy). The previously estimated EBITDA for the 50 MW

plant in 2013 of EUR 17.5 M was improved to EUR 20.7 M.

Nevertheless, ENCE’s capital expenditures in the last two years were largely due to their energy

asset requirements (c. 80% of total CAPEX). We assume the investment approach to be above the

“standard” investment on which the target return of RDL 09/2013 will be applied and therefore

estimate an IRR of around 3% on their projects compared to the 6.5% on a “standard” investment.

Investment Summary

Bearish Outlook - Sell Recommendation

We initiate coverage of ENCE S.A. with a target price of €2.26 given a downside potential of

12.3% from the current market price €2.58. We therefore issue a SELL recommendation since the

downside potential exceeds our requirement of 10%. Our bearish outlook is founded on the

unfavourable market environment and disruption of the Company’s business model resulting from

recent regulatory changes.

Valuation Methods

The valuation target we obtained was by way of a Discounted Cash Flow analysis with a fair value

of EUR 2.05 and peer group multiples analysis with a target price of EUR 2.48. Both methods were

weighted equally and both indicate an overvaluation. Our selection criteria for equity multiples took

into account divergent capital structures and eliminated outliers.

Financial Position

Financial Health

ENCE's balance sheet in terms of solvency, liquidity, profitability and turnover ratios and margins

are superior compared to the industry. The financial health combined with the efficiency of the past

years provides a positive outlook for the Company. Furthermore, ENCE is sustainably financed

until 2020, which indicates that no major capital injections will be required in the next years. This

results in a BB rating by S&P thereby assigning ENCE the highest possible rating within the non-

investment grade category with a stable outlook. However, this corporate rating of S&P was

updated in last July and therefore does not incorporate the implications of the new energy

regulations.

Figure 3.1 | Distribution of energy production in

Spain, 2012

Source: Ministry of Industry, Energy and Tourism

Figure 3.2 | Porter’s Five Forces Analysis

ENCE Average 3.25 Source: Appendix 10.

“This results in a BB rating by S&P…with

a stable outlook.”

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 6

Cash Flow Generation

The operating cash flow (CFO) has seen a positive development in the past years, rising from EUR

88M in 2009 to EUR 112M in 2012. Mainly due to the adverse effect of the energy reforms, going

forward our financial model predicts a sharp drop in CFO to levels around EUR 50M in 2014 and a

stable development in the following years.

EBITDA development

The EBITDA was negative in 2009 and went up to EUR 178M in 2010. For FY 2013 we forecast

an EBITDA of EUR 167M and again a sharp decline due to lower energy revenues in 2014 to an

expected value of EUR 134M, recovering slightly in the following years.

Market Prospects Stable global demand and increasing supply

We expect prices of pulp to go down by around 1% annually in the next five years due to a stable

European market combined with our negative outlook on China and shifts in the supply curve

resulting from new capacities in South America (both of which serve as a catalysts in the downward

pulp price trend). We do not see significant growth potential for total revenues in the pulp

producing industry.

Unprofitable Energy Business

By comparing Spain's current share of renewables in total energy consumption to the goals set by

the European Union to be reached in 2020 one could get a bullish view on the market. Due to high

subsidies resulting in a tariff deficit, companies have been overinvesting into the sector in the past

few years. Recently, the government changed the regulation, which has substantial negative impact

for the industry and results in a decrease in renewable energy prices of around 15% compared to the

previous remuneration system according to our estimate.

Risks

Investors should be aware of a stock-overhang risk based on the relatively high percentage of

portfolio holdings of the main investors in the Company and liquidity issues due to the low amount

of free-float shares. Additionally, they should be aware of the adverse influences of Latin American

producers who are building up capacities thus increasing the world supply of pulp and creating

downward pressure in pulp prices. An unexpectedly high slowdown of Chinese growth is another

factor that might negatively affect the Company, as China is one of the main absorbers of pulp

supplied to the market. We identify the main risks in our Potential Risks section.

Valuation

To determine our valuation of ENCE, we used a combination of two approaches with equal

weights: The Discounted Cash Flow (DCF) and Multiples Pricing Approach. Our technical analysis

coincides with aforementioned valuation methods and suggests several bearish indicators including

negative momentum and candlestick patterns as well as a potential downside to the next major

support line.

DCF Analysis

Our DCF values ENCE at EUR 2.05/share. Our two-stage model consists of forecasts to 2017, after

which we apply a terminal value to our calculations. The revenue figures are broken down into the

two divisions: pulp and energy.

Terminal Value

We assume a terminal growth rate of 1.5% in Free Cash Flow to Firm, which coincides with our

long-term inflation rate expectations.

Sales

The Royal Decree is expected to have a one time negative impact on the price of energy to the tune

of -15%. The new price is expected to be EUR 97.10/MWh. Also, we expect pulp prices to be in a

downtrend and use a price reduction of around 1% (YoY) going forward. The impact on sales is

however mitigated partly by the increase in production capacity from pulp (1% YoY) given that

ENCE operates at 95% capacity and no major CAPEX is planned going forward apart from energy

due to a one time 158,000 MWh increase in 2015 due to the new plant in Merida and 2% increase

YoY due to efficiency gains.

“We expect prices of pulp to go down by

around 1% annually in the next years…”

“Due to high subsidies… companies have

been overinvesting into the sector…”

Figure 5.1 | Total Net Turnover, in € millions

Source: Appendix Financial Model

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 7

COGS

We are expecting a 0.5% increase in cost of inputs YoY due to slightly higher timber and chemical

prices in the market.

WACC

Our cost of capital calculations are obtained using a weighted average of cost of debt and equity

using a long-term target structure of 55% equity and 45% debt. For our cost of equity, we used the

CAPM with the 10-year German Bunds rate of 1.68% as a risk-free rate (Figure 6.2) benchmark and

market return of 8.26% using a 10-year period for the return on the IBEX Medium Cap Index. The

cost of debt is based on the high yield bond issued by the Company and the option-adjusted spread

over the risk-free benchmark to produce a value of 4.72%. The tax rate applied in our model is 30%

based on the historical average of the past two fiscal years.

Dividends

The Company has firmly established its stance on dividend policy given that it is in its mature and

arguably decline phase of growth. We expect the firm to maintain a 40-50% payout ratio going

forward given the limited growth opportunities for the corporation.

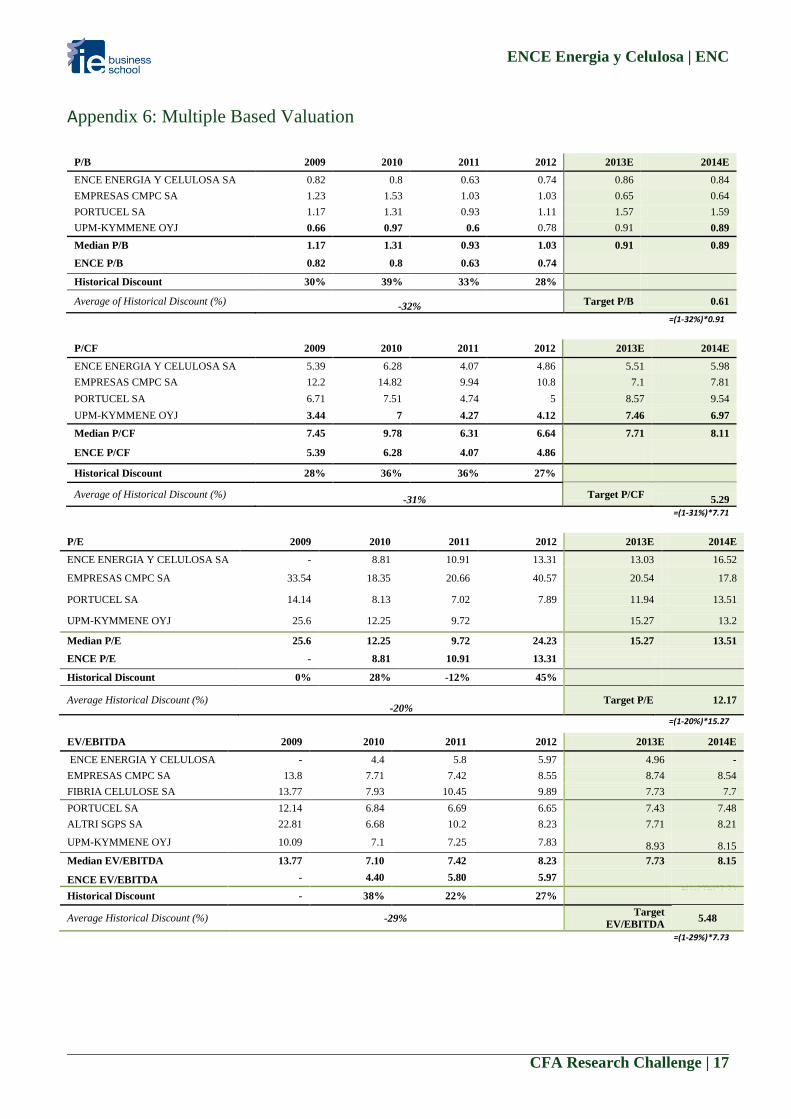

Multiples analysis

Philosophy

We calculated a target price by relative valuation to companies that we considered to be appropriate

comparables and have similar business drivers. Instead of valuing ENCE as the sum of its two

businesses (Pulp and Energy) we forecast the importance of its energy business to decrease over

time and expect the NPV of this division’s cash flows to equity to be zero. We also believe that

comparing relative stock prices of energy companies across borders is irrelevant given the diversity

of regulatory forces in different regions. Therefore, we are focused on finding competitors in the

pulp industry.

Comparable Entities

ENCE's business mix and European presence is unique and makes it hard to find perfect

comparables. For the European market we found UPM (a Finnish pulp manufacturer that is also

engaged in renewables) and Portucel (a Portuguese pulp and paper company) to be appropriate

peers. Furthermore, we are using the South American pulp producers Fibria, Altri and CMPC as

comparables, citing the global pulp industry’s tendency to correlate across similar business cycles.

Multiples Selection

We believe that EV/EBITDA gives the best approximation for value since we are able to compare

companies with different depreciation and amortization schedules independently of their capital

structure. We therefore assign 50% weight to this EV-based multiplier. The other 50% will be

distributed evenly between P/B, P/CF and P/E. Since theses equity based multipliers can only be

used for companies with a similar capital structure like ENCE, we decided to exclude Fibria and

Altri, which both have significantly higher leverage ratios (Figure 6.3).

We investigate the years 2009 to 2012 to find an average difference at which ENCE is trading

relative to its peers. Based on this analysis, in the past ENCE traded at a discount of 32% using P/B,

31% using P/CF, 20% using P/E and 29% according to EV/EBITDA. We furthermore assume this

discount to stay stable in the future. Consequently, we come up with a target multiple for ENCE

using the historical discounts and compare this value to the consensus estimate for ENCE to finally

get a target share price.

After calculating equity value from enterprise value we come up with a fair price of EUR

2.71/Share from EV/EBITDA. The three equity-based multipliers suggest a downside development

of 13% on average, which with a share price of EUR 2.585 at the time of analysis results in a target

price of EUR 2.24. Applying the aforementioned weights for enterprise and equity based multipliers

we receive a target price of EUR 2.48 for ENCE's share.

Financial Statement Analysis

DuPont

Since the return on equity measures the rate of return that is attributable to stockholders and is

therefore an important ratio the development of ROE will be analyzed over the past three years

starting in FQ3 2010 to identify the drivers. We will make use of the three-stage DuPont model,

which breaks down the ROE into profit margin (net income/sales), asset turnover (sales/assets) and

financial leverage (assets/equity). It can easily be identified that the ROE developed positively from

Figure 6.2 | WACC Calculation

Ratio Value

Levered Beta 1.179

Tax rate 30%

Rf 1.68%

ERP 8.3%

D/D+E 45%

E/D+E 55%

Ke 9.48%

Kd 4.72%

WACC 6.68%

Source: WACC Appendix

Figure 6.3 | D/E Criteria for Equity Multiples

Source: Appendix Multiples Analysis

Figure 7.1 | DuPont Analysis

Source: Company Annual Report

Ratio 09/13 09/12 09/11 09/10

Profit Margin 5.9% 4.0% 5.8% 5.0%

Asset Turnover 0.64 0.59 0.61 0.55

Fin. Leverage 1.84 1.86 1.81 1.90

ROE 0.07 0.04 0.07 0.05

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 8

5.22% to 6.95% (+33%). However, the highest return was realized in the first quarter of 2011 with

around 10%. The positive development was supported by an increase in profitability and operating

efficiency. The profit margin was the biggest contributor to the increase in ROE over the last three

years since it developed from 5% to 5.9% (+18%) whereas the asset turnover ratio increased 16%.

The increase in profit margin and asset turnover was partly offset by the decrease of the financial

leverage of 3%. However, the deleveraging process benefits shareholders in a way that financial

risk is decreased.

In summary, the DuPont analysis gives a favorable picture of the Company that has been able to

increase its ROE with a lower share of debt in its capital structure by becoming more profitable

through increased efficiency. This can be interpreted as fundamental backup for the positive share

price development in the investigated period.

Financial Metrics and Ratios Revenues

Due to the aforementioned slowdown in China’s projected growth, combined with the current

regulation changes in the Renewable Energy Industry in Spain, we project that annual revenues will

decrease at a CAGR of -0.62% over the next five years.

Expenses

COGS have increased 25.7% over the last five years, following the transition from internally

produced timber to payment for inventories of 3rd party suppliers. We project COGS to increase by

4.8% over the next five years, having a negative impact on the gross margin (Figure 7.3).

Depreciation

We project continued growth for this fixed-asset intensive Company, particularly when the biomass

plant in Merida becomes operational, with stable depreciation expenses of EUR 81.4M through

2017.

EBITDA Margin

We predict that the EBITDA margin will only decrease (from 2013E to 2017E) by a CAGR of -

2.72% over the next five years (Figure 7.3). It is important to note that while Gross Margin will fall

sharply during that time, improved efficiencies are expected to maintain the EBITDA margin.

Net Debt/ EBITDA

Currently Net Debt to EBITDA is 53%, which is a very conservative value when compared to the

Company’s target of maximum 2.5x. We project net debt to decrease, following less CAPEX in the

coming years, as we do not see much growth potential in the energy and pulp markets. Therefore we

expect Net Debt to EBITDA to remain at a low level.

Operating Cash Flow

Net operating cash flow has remained positive throughout the last five years, rising from 87.9

million in 2009 to 111.6 million in 2012. Going forward, we project the operating cash flow to be

stable at levels around EUR 50 million (Figure 7.4).

Interest Coverage Ratio

Decreasing by over 25% from 2011 to 2012 the Company finished out the fiscal year (2012) with an

Interest Coverage Ratio of 5.23. We expect this ratio to remain stable in the coming years.

Inventory Levels

ENCE’s active transition to 3rd party suppliers of timber and other raw materials provides the firm

with greater flexibility in its manufacturing processes, resulting in a current Inventory Turnover

ratio of 7.85 (Figure 7.5) and projected inventory levels between EUR 80.1M and EUR 84.4M for

the next five years.

Net Working Capital

We project net working capital of EUR 15.527 million for year-end 2014 decreasing to EUR 12.065

million and EUR 10.98 million for 2015 and 2016, respectively.

Debt Profile

As the Company is fully financed through 2020 we project no new debt issuances for the next five

years (Figure 7.6), which was made possible by the successful issuance of the high yield corporate

bond in 2013 at a face value of EUR 250 million.

Figure 7.2 | 3 Year Change of Ratios

Source: Company Annual Report

Figure 7.3 | Margins (%)

Source: Company Annual Report

Figure 7.4 | Cash Flow from Operations, in € millions

Source: Appendix Valuation Model

Figure 7.5 | Selected ratios

Ratio ENCE Industry

Average

Quick Ratio

1.44

0.68

LT Debt to Equity

55.41

89.20

Total Debt to Equity

84.44

143.89

Operating Margin 9.84% 3.39%

Asset Turnover

0.43

0.62

ROA 0.53% 1.85%

Inventory Turnover 7.85 5.12

Source: Company Annual Report. Industry defined by Reuters.

-200.00%

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

Dec '10 Dec '11 Dec '12

Total Debt / Total Assets Net Debt Growth

Total Liabilities Growth ROE

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 9

Dividends

With an official dividend policy of 40%-50% payout ratio, the firm ended the 2012 fiscal year with

a Dividend Yield of 3.29%. We expect the future five-year dividend growth rate to decrease (in

absolute terms) due to a lower projected level of net income.

CAPEX/Revenue

Due to the highly intensive capital requirements of ENCE’s industry, CAPEX/Revenue was taken

to find the proportion of revenue relative to long-term capital requirements. We project CAPEX to

remain stable over the next five years but at lower levels compared to the previous years. As

mentioned before, we project revenues to decrease by -0.62% per annum for the next five years.

Therefore, from 2014 onwards, we project this ratio to remain stable at around 10%.

Financial Health

Despite the grim outlook of the industry, ENCE is currently operated with very healthy balance

sheets. Comparable quick ratios, long-term debt to equity, debt to equity, operating margin, and

ROA all provide a positive outlook for ENCE’s future, relative to the competition.

Investment Risks

In this section we identify the main risks that could negatively affect our target price. The risks are

divided into four main categories: Macroeconomic, Industry, Operational and Shareholder Risks.

Macroeconomic Risks GDP Growth Rate

ENCE has exposure to the cyclical pulp market and the paper sector, which is sensitive to economic

growth expectations. China is a major market for pulp and main driver of demand. Besides stable

markets in Asia, ENCE is dependent on a strong European demand where they generate around

90% of revenues. The forces of supply and demand determine the prices in the pulp market and

ENCE’s revenues are highly correlated to price movements. Consequently, adverse shifts in the

macroeconomic environment will have negative impact on prices, revenue generation and hence

ENCE’s stock value.

Currency/Exchange Rate Risk

Pulp prices are globally denominated in US dollars and influenced by supply and demand dynamics

and foreign exchange rates against the dollar. An appreciation of the US dollar with respect to the

Euro makes European producers more competitive since their exports become relatively cheaper

and they therefore have higher sales. Moreover, revenues in dollar are worth more in euro. In case

of depreciation of the dollar/euro exchange rate the opposite is observed.

Interest Rate Risk

The Company has been using debt to finance its energy plants in Huelva and Merida. If expansion

and investment is financed by debt, interest rate increase can have an impact on the debt and interest

coverage ratios of ENCE. However, the Company makes usage of derivatives to partly hedge this

risk (on a 12-month basis). Furthermore, the Company is sustainably financed until 2020 (Figure

10.1), so we assume no further major debt injections in the next years.

Cost Inflation

ENCE is a company that mainly transforms wood into pulp and is therefore dependent on price

increases of this commodity. Because the firm is reducing their ownership in forests they are

becoming increasingly exposed to price changes affecting their suppliers in Spain. Moreover a

domestic inflationary environment, that raises the cost of wages and energy consumed, would

damage the Company’s gross margin since prices are denominated in USD and given by the market.

Country risk

ENCE is exposed to weaker European economies as approximately 35% of pulp revenues are

attributed to Spain and Italy and all its renewable energy sales go to the domestic grid (though this

might change, citing aforementioned legislation). The Company is heavily exposed to the Southern

European economies and therefore suffers more than others from decreasing demand in times of

crisis. The firm has realized this issue and tries to increase the revenue shares of countries like

Germany. However, it can be criticized that ENCE does not plan to diversify its revenue streams by

heavily entering emerging economies, namely China.

Industry Risks

Figure 7.6 | Debt Maturity Profile, in € millions

Source: Company Annual Report

“…adverse shifts in the macroeconomic

environment will have negative impact

on…ENCE’s stock value”

“…a domestic inflationary

environment…would damage the

Company’s gross margin…”

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 10

New manufacturing capacities in South America

South American competitors have been building capacity, which will affect cellulose prices if the

excess capacity is not absorbed by growth in demand, which is a likely scenario.

Competitive LATAM if Oil Falls

A decrease in the price of oil could drive LATAM exporters to be more cost competitive on the

global stage through reduced transportation costs, resulting in either increased margins for LATAM

producers of pulp or decreased market share for European-based producers.

Renewable energy sector regulations

Political reforms and new legislations regarding remuneration on renewable energy projects can

have an adverse impact on cash flow generation from ENCE’s plants and diminish the buffering

effect of those plants during pulp cycle troughs.

Substitute recycle paper

There are two phenomena that have a negative effect on ENCE's business. Firstly, it can be seen

that during times of high pulp prices customers switch to recycled paper to minimize costs.

Secondly, there is a sustainability movement in the developed world towards the usage of recycled

paper instead of newly produced pulp-based paper. If these trends continue, they will certainly have

an impact on ENCE.

Competition from Other Renewables

As mentioned earlier, biomass has the biggest share in electricity production from renewables in

Spain. If research or technological developments make other sources of renewables, relative to

biomass, more cost effective, ENCE will have a competitive disadvantage being highly engaged in

this sector and not diversified through additional energy generation from wind or solar.

Operational risks Strikes

ENCE has been able to improve its cost structure during the last years, which is partly due to

employment reduction plans. As this is positive on the one side, however, the Company should be

careful with further savings on cost of their employees. The overall staff sentiment is important

since it could be very harmful for the business even if only some key divisions lay down work and

thereby stop the whole production process. Given the currently high unemployment rate in Spain,

we do not see a high risk of employee unrest.

Production Process

Due to the high fixed costs resulting from running big plants, it is important to always make use of

full capacities and reduce non-operating hours to a small extent. Every hour of interruption in the

production process means a loss of money and therefore implies a risk for ENCE's shareholders.

Furthermore, ENCE will do well by investing enough into their factories (CAPEX) to keep

efficiencies at high levels.

Shareholder Risks Stock Overhang

As mentioned above, there is a high percentage of insider and institutional ownership of ENCE’s

stock (e.g. Alcor Holding 26.52%), which results in a potential risk of stock overhang for common

stock shareholders. In general, the big owners seem to be long-term investors. However, in the case

of a sale of a big stake to the market, the prices of ENCE's shares will be under huge pressure in the

short-term.

Liquidity risk

Linked to the shareholder structure of below 20% free float in combination with the relatively small

market cap there exists a significant liquidity risk. We believe that the resulting low turnover of

traded shares will push prices further down in turbulent market phases and sell-offs. We interpret

this as one of the reasons why ENCE is traded at a discount to its peers (see multiples valuation).

Dividend Policy

In the past years shareholders have been remunerated well through cash and stock dividends. In

terms of dividend yield over the last three years ENCE delivered 3.57% whereas the average in the

IBEX Mid Cap lies around 2.63%. If the Company decides to finance its investments through

retained earnings, historic payout ratios will be decreasing. However, we believe that the

management will sustainably deliver higher dividend yields than the national average.

“…during times of high pulp prices

customers switch to recycled paper to

minimize costs…”

“…a high percentage of insider and

institutional ownership…[is] a potential

risk of stock overhang for common stock

shareholders”

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 11

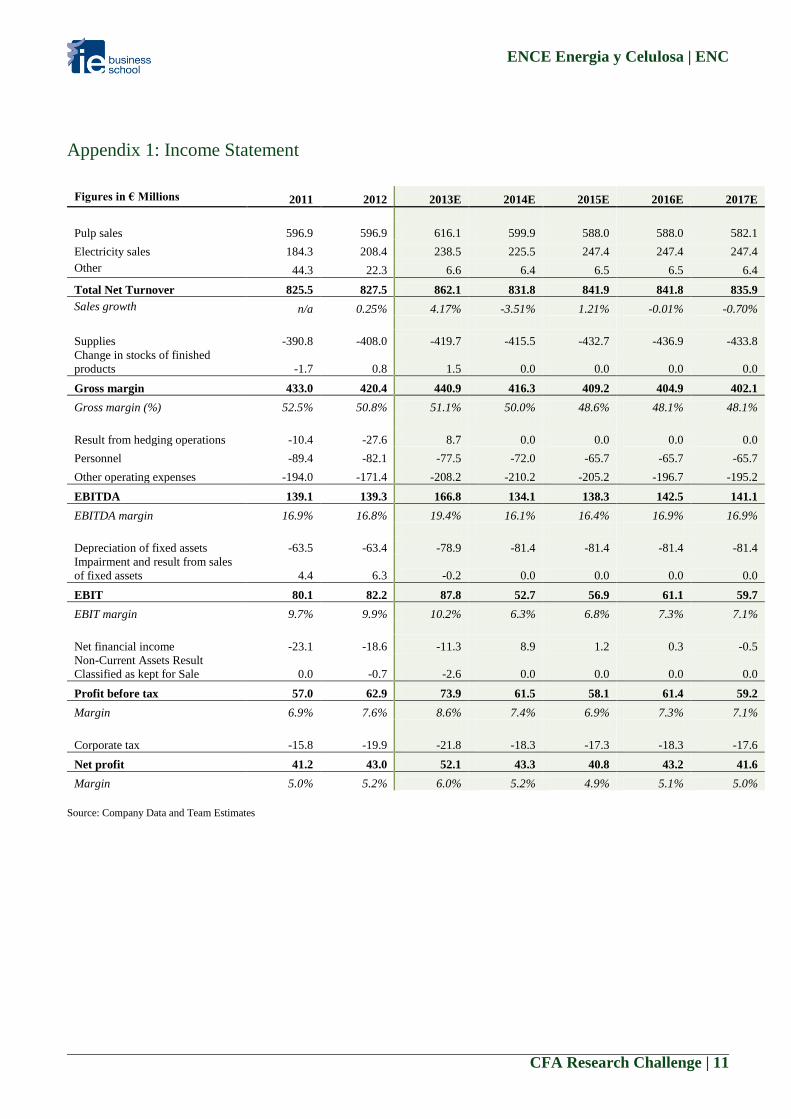

Appendix 1: Income Statement

Figures in € Millions 2011 2012 2013E 2014E 2015E 2016E 2017E

Pulp sales 596.9 596.9 616.1 599.9 588.0 588.0 582.1

Electricity sales 184.3 208.4 238.5 225.5 247.4 247.4 247.4

Other 44.3 22.3 6.6 6.4 6.5 6.5 6.4

Total Net Turnover 825.5 827.5 862.1 831.8 841.9 841.8 835.9

Sales growth n/a 0.25% 4.17% -3.51% 1.21% -0.01% -0.70%

Supplies -390.8 -408.0 -419.7 -415.5 -432.7 -436.9 -433.8

Change in stocks of finished

products -1.7 0.8 1.5 0.0 0.0 0.0 0.0

Gross margin 433.0 420.4 440.9 416.3 409.2 404.9 402.1

Gross margin (%) 52.5% 50.8% 51.1% 50.0% 48.6% 48.1% 48.1%

Result from hedging operations -10.4 -27.6 8.7 0.0 0.0 0.0 0.0

Personnel -89.4 -82.1 -77.5 -72.0 -65.7 -65.7 -65.7

Other operating expenses -194.0 -171.4 -208.2 -210.2 -205.2 -196.7 -195.2

EBITDA 139.1 139.3 166.8 134.1 138.3 142.5 141.1

EBITDA margin 16.9% 16.8% 19.4% 16.1% 16.4% 16.9% 16.9%

Depreciation of fixed assets -63.5 -63.4 -78.9 -81.4 -81.4 -81.4 -81.4

Impairment and result from sales

of fixed assets 4.4 6.3 -0.2 0.0 0.0 0.0 0.0

EBIT 80.1 82.2 87.8 52.7 56.9 61.1 59.7

EBIT margin 9.7% 9.9% 10.2% 6.3% 6.8% 7.3% 7.1%

Net financial income -23.1 -18.6 -11.3 8.9 1.2 0.3 -0.5

Non-Current Assets Result

Classified as kept for Sale 0.0 -0.7 -2.6 0.0 0.0 0.0 0.0

Profit before tax 57.0 62.9 73.9 61.5 58.1 61.4 59.2

Margin 6.9% 7.6% 8.6% 7.4% 6.9% 7.3% 7.1%

Corporate tax -15.8 -19.9 -21.8 -18.3 -17.3 -18.3 -17.6

Net profit 41.2 43.0 52.1 43.3 40.8 43.2 41.6

Margin 5.0% 5.2% 6.0% 5.2% 4.9% 5.1% 5.0%

Source: Company Data and Team Estimates

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 12

Appendix 2: Balance Sheet

Source: Company Data and Team Estimates

Figures in € Millions 2011 2012 2013E 2014E 2015E 2016E 2017E

Tangible fixed assets 952.9 947.2 955.0 955.0 955.0 955.0 955.0

Intangible fixed assets 8.1 21.6 20.1 20.1 20.1 20.1 20.1

Long- term financial assets 4.1 4.1 3.0 3.0 3.0 3.0 3.0

Other non-current assets 42.7 30.6 29.4 29.4 29.4 29.4 29.4

Total fixed assets 1,007.8 1,003.5 1,007.4 1,007.4 1,007.4 1,007.4 1,007.4

Inventories 112.5 87.6 80.1 83.4 84.1 84.9 84.4

Trade debtors and other accounts receivable 135.8 168.2 144.8 144.9 144.1 144.1 143.1

Cash and other short-term financial assets 94.5 47.8 268.9 197.8 226.6 262.0 298.0

Other current assets 1.8 11.6 9.5 9.5 9.5 9.5 9.5

Non-Current Assets Classified as kept for Sale 16.5 59.3 11.2 11.2 11.2 11.2 11.2

Total current assets 361.0 374.6 406.7 446.7 475.6 511.7 546.1

Total assets 1,368.8 1,378.0 1,414.1 1,454.1 1,483.0 1,519.1 1,553.5

Equity 720.2 724.7 753.7 785.3 811.3 838.5 864.9

Long- term financial debt 283.4 318.9 350.5 347.5 344.5 341.5 341.5

Long-term provisions 23.2 13.3 16.0 16.0 16.0 16.0 16.0

Financial instruments for long-term hedging 25.5 16.6 9.0 9.0 9.0 9.0 9.0

Other non-current liabilities 48.5 51.8 45.1 45.1 45.1 45.1 45.1

Total non-current liabilities 380.6 400.6 420.6 417.6 414.6 411.6 411.6

Short-term financial debt 21.0 25.7 6.7 17.7 20.2 30.2 40.2

Trade creditors 165.8 184.7 188.1 188.3 191.8 193.7 191.7

Short-term provisions 7.9 8.5 8.3 8.3 8.3 8.3 8.3

Financial Instruments for short-term hedging 34.6 14.9 4.2 4.2 4.2 4.2 4.2

Other current liabilities 26.4 19.0 32.6 32.6 32.6 32.6 32.6

Non-Current liabilities classified as kept for

Sale 12.3 0.0 0.0 0.0 0.0 0.0 0.0

Total current liabilities 268.1 252.7 239.9 251.1 257.1 269.0 277.0

Total Liabilities + Equity 1,368.8 1,378.0 1,414.1 1,454.1 1,483.0 1,519.1 1,553.5

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 13

Appendix 3: Cash Flow Statement

Source: Team Estimates

Figures in € Millions 2013E 2014E 2015E 2016E 2017E

Net Income 52.1 52.8 43.2 45.5 43.9

Depreciation & amortization 78.9 81.4 81.4 81.4 81.4

Gross Cash Flows 131.0 134.2 124.6 126.9 125.3

Capex -102.3 -81.4 -81.4 -81.4 -81.4

Change in Working Capital 87.3 -3.3 3.5 1.1 -0.4

Operating Current Assets 245.6 248.9 248.9 249.7 248.1

Operating Current Liabilities 233.1 233.1 236.9 238.7 236.8

Total Working Capital 12.4 15.8 12.1 11.0 11.4

Cash Flow From Operating Activities -15.0 -84.5 -78.0 -80.3 -81.8

New Debt Issued 1.4 7.0 7.0 7.0 7.0

Old Debt Retired -6.0 -8.0 -10.0 -10.0 -10.0

Cash Flow From Financial Activities 12.6 8.0 -0.5 7.0 10.0

Dividends -20.844 -21.129 -17.273 -18.188 -17.561

Capital change 0.000 0.000 0.000 0.000 0.000

Cash Flow From Investing Activities -20.8 -21.1 -17.3 -18.2 -17.6

Cash Flow Generated 107.8 36.6 28.9 35.4 36.0

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 14

Appendix 4: Key Financial Ratios

Source: Company Data and Team Estimates

Liquidity Ratios 2011 2012 2013E 2014E 2015E 2016E 2017E

Current Ratio 1.35 1.5 1.70 1.78 1.85 1.90 1.97

Quick Ratio 0.87 0.9 1.32 1.40 1.48 1.55 1.63

Cash Ratio 0.35 0.2 1.12 0.79 0.88 0.97 1.08

Efficiency Ratios

Total Asset Turnover 0.60 0.6 0.61 0.57 0.57 0.55 0.54

Fixed Asset Turnover 0.82 0.8 0.86 0.83 0.84 0.84 0.83

Net Working Capital Turnover 8.88 6.8 5.17 4.25 3.85 3.47 3.11

Days Sales Outstanding 60.05 74.2 61.33 63.56 62.49 62.49 62.49

Days Inventory Outstanding 105.05 78.3 69.64 73.27 70.97 70.97 70.97

Days Payables Outstanding 154.83 165.2 163.55 165.43 161.77 161.80 161.27

Cash Conversion Cycle 10.26 -12.6 (32.58) (28.59) (28.31) (28.34) (27.82)

Profitability Ratios

Gross Margins (%) 52.5% 0.5 51.1% 50.0% 48.6% 48.1% 48.1%

EBITDA Margins (%) 16.9% 0.2 19.4% 16.1% 16.4% 16.9% 16.9%

Net Profit Margins 5.0% 0.1 6.0% 5.2% 4.9% 5.1% 5.0%

ROA 3.01% 0.0 3.68% 2.97% 2.75% 2.84% 2.68%

ROE 5.72% 0.1 6.91% 5.51% 5.03% 5.15% 4.81%

Solvency Ratios

Leverage Ratio (Debt/Assets) 0.47 0.47 0.47 0.46 0.45 0.45 0.45

Debt to Equity Ratio 0.9 0.9 0.88 0.85 0.81 0.81 0.81

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 15

Appendix 5: DCF Assumptions

1) Volume and Prices of Pulp and Energy

We expect the pulp production to grow at a slow pace from 1272 thousand tons in 2013 to 1297 thousand tons in 2017. Meanwhile, pulp prices experience

a slight decrease. For the electricity sales we expect a stable development, besides the expected increase in the year 2015 for the new stand-alone project in

Merida that will start its operations in late 2014. Our assumption for the energy price from 2014 going forward is stable at c. EUR 97 per MWh.

2) Cost of Goods Sold

For our DCF we assume COGS to increase by around 5% in the years 2013 to 2017. In combination with revenues to experience a slight decrease in the

mentioned period, the gross margin is projected to develop from 51% to 48%.

3) Weighted Average Cost of Capital

Price and Volume 2013E 2014E 2015E 2016E 2017E

Total Revenues 862 832 842 842 848

Pulp sales 616 600 588 588 594

Pulp production (tons) 1271539 1274717 1284254 1297097 1297097

Prices BHKP, $/ton 798 784 762 755 762

Exchange rate 1,30 1,25 1,25 1,25 1,25

Net sale price (€/t) 484 471 458 453 458

Electricity sales 238 225 247 247 247

Electricity production (MWh) 1519879 1624773 1782773 1782773 1782773

Average sale price (€/MWh) 117 97 97 97 97

2013E 2014E 2015E 2016E 2017E

Cost of Goods sold 420 416 433 437 440

Gross Margin 51% 50% 49% 48% 48%

Risk Free Rate

Beta

Equity Risk Premium

Cost of Debt

Marginal Tax Rate

Capital Structure

10-year German government bond yield (1.68%) given the investment is denominated in Euro and default risk of

German government is close to zero

Benchmark for ENCE's share is IBEX Medium Cap Index in which the stock is listed. The Beta of 1.179 applied to

the model is calculated on the distribution of daily stock returns in January 2014 relative to index returns. The

chosen time period was optimized by means of the R^2 coefficient which yields a reasonably high value of 0.642.

The selected benchmark yields an annual equivalent total return of 8.26% over the last ten years (year end 2003

until year end 2013) reduced by the risk-free rate to get the risk premium of 6.58%. Since the benchmark return is

historically calculated it includes the country risk for Spain.

The cost of debt with the value of 4.72% is estimated based on the high yield bond issuance by ENCE in 2013. We

believe this is a good representation for the cost of debt because market rates can be utilized and the maturity

represents the company's financing profile well. The bond pays coupon of 7.25% p.a. However, the true yield is

4.72% based on the option-adjusted spread added to the risk-free benchmark yield.

The assumed marginal tax rate of 30% is based on the historical average of the last two fiscal years.

Based on our financial model we assume a long-term capital structure of 55% equity and 45% debt. This

approximately represents the current financial leverage.

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 16

4) Regression Analysis of Beta

Source: Bloomberg

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 17

Appendix 6: Multiple Based Valuation

P/B 2009 2010 2011 2012 2013E 2014E

ENCE ENERGIA Y CELULOSA SA 0.82 0.8 0.63 0.74 0.86 0.84

EMPRESAS CMPC SA 1.23 1.53 1.03 1.03 0.65 0.64

PORTUCEL SA 1.17 1.31 0.93 1.11 1.57 1.59

UPM-KYMMENE OYJ 0.66 0.97 0.6 0.78 0.91 0.89

Median P/B 1.17 1.31 0.93 1.03 0.91 0.89

ENCE P/B 0.82 0.8 0.63 0.74

Historical Discount 30% 39% 33% 28%

Average of Historical Discount (%) -32%

Target P/B 0.61

=(1-32%)*0.91

P/CF 2009 2010 2011 2012 2013E 2014E

ENCE ENERGIA Y CELULOSA SA 5.39 6.28 4.07 4.86 5.51 5.98

EMPRESAS CMPC SA 12.2 14.82 9.94 10.8 7.1 7.81

PORTUCEL SA 6.71 7.51 4.74 5 8.57 9.54

UPM-KYMMENE OYJ 3.44 7 4.27 4.12 7.46 6.97

Median P/CF 7.45 9.78 6.31 6.64 7.71 8.11

ENCE P/CF 5.39 6.28 4.07 4.86

Historical Discount 28% 36% 36% 27%

Average of Historical Discount (%) -31%

Target P/CF 5.29

=(1-31%)*7.71

P/E 2009 2010 2011 2012 2013E 2014E

ENCE ENERGIA Y CELULOSA SA - 8.81 10.91 13.31 13.03 16.52

EMPRESAS CMPC SA 33.54 18.35 20.66 40.57 20.54 17.8

PORTUCEL SA 14.14 8.13 7.02 7.89 11.94 13.51

UPM-KYMMENE OYJ 25.6 12.25 9.72 15.27 13.2

Median P/E 25.6 12.25 9.72 24.23 15.27 13.51

ENCE P/E - 8.81 10.91 13.31

Historical Discount 0% 28% -12% 45%

Average Historical Discount (%) -20%

Target P/E 12.17

=(1-20%)*15.27

=(1-29%)*7.73

=(1-29%)*7.73

EV/EBITDA 2009 2010 2011 2012 2013E 2014E

ENCE ENERGIA Y CELULOSA - 4.4 5.8 5.97 4.96 -

EMPRESAS CMPC SA 13.8 7.71 7.42 8.55 8.74 8.54

FIBRIA CELULOSE SA 13.77 7.93 10.45 9.89 7.73 7.7

PORTUCEL SA 12.14 6.84 6.69 6.65 7.43 7.48

ALTRI SGPS SA 22.81 6.68 10.2 8.23 7.71 8.21

UPM-KYMMENE OYJ 10.09 7.1 7.25 7.83 8.93 8.15

Median EV/EBITDA 13.77 7.10 7.42 8.23 7.73 8.15

ENCE EV/EBITDA - 4.40 5.80 5.97

Historical Discount - 38% 22% 27%

Average Historical Discount (%) -29% Target

EV/EBITDA 5.48

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 18

Target EV/EBITDA multiple 5.48

2013 EBITDA 167.6

EV 919.2

Net Financial Debt 173.7

Equity Value 745.5

No. Shares 275

Expected Price 2.71

Downside P/B 29% (= 1-0.61/0.86) Current Price Expected Price

Downside P/FCF 4% (= 1-5.29/5.51) 2.585 2.24

Downside P/E 7% (= 1-12.17/13.01)

Average 0.13

Multiple Weight Expected Price Final Value

P/E, P/B, P/FCF 0.5 2.24 2.48

EV/EBITDA 0.5 2.71

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 19

Appendix 7: Porter’s Five Forces

CompanyAverage= 0.75*Pulp+0.25*Renewables= 3.25

Source: Team estimates

0

1

2

3

4

5Threat of New Entrants

Bargaining Power of Suppliers

Competition in the IndustryThreat of Substitute Products

Bargaining Power of Buyers

Pulp

Renewables

Pulp Renewables

Threat of New Entrants 4 3

Bargaining Power of Suppliers 2 2

Competition in the Industry 5 1

Threat of Substitute Products 4 3

Bargaining Power of Buyers 2 5

3.4 2.8

Scale of Interaction

0 No interaction 1 Insignificant 2 Low

3 Average 4 High 5 Very High

3.25

Company Specific Average

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 20

Appendix 8: Peer Group Selection

Source: Bloomberg and Team Estimates

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 21

Appendix 9: SWOT Analysis

Strenghts

Synergies between pulp and energy business

Market leader

Know-how and high R&D

Strategic location of production facilities

Strong Balance Sheet Financial Ratios

Weaknesses

High operating leverage during cycle troughs

Renewable energy projects less profitable due to new

regulation

Lately increased cash costs

No access to emerging markets

Opportunities

Sale of current forestry assets

Increase local wood supply

Chinese market absorbs demand

Iberian Peninsula only region in Europe capable to

produce eucalyptus cellulose

Threats

Regulation on renewable energy

Latin American producers entering European market

South American producers building up capacities

Subsitute recycle paper

Competition from other renewables

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 22

Appendix 10: Shareholding Structure

Top 10 Institutional Holders Position (Shares) Market Value O/S

Amber Capital (UK) LLP 10,070,000 25,980,600 3.65%

Norges Bank Investment Management 7,576,352 19,546,988 2.75%

Dimensional Fund Advisors LP 5,602,146 14,453,537 2.03%

JPMorgan Asset Management (UK) Ltd. 1,646,400 4,247,712 0.6%

Banco Madrid Gestion de Activos SGIIC SA 1,401,511 3,615,898 0.51%

Guggenheim Funds Investment Advisors LLC 1,249,612 3,223,999 0.45%

Barclays Wealth Managers Espana SGIIC SA 1,229,316 3,171,635 0.45%

Batterymarch Financial Management, Inc. 983,246 2,536,775 0.36%

Mellon Capital Management Corp. 801,987 2,069,126 0.29%

S.W. Mitchell Capital LLP 797,305 2,057,047 0.29%

Board member Function

D. Juan Luis Arregui Ciarsolo Chairman

D. Ignacio de Colmenares y Brunet CEO

D. Pedro Barato Triguero Director

D. José Guillermo Zubía Guinea Director

D. Gustavo Matías Clavero Director

D. José Manuel Serra Peris Director

D. José Carlos del Álamo Jiménez Director

Retos Operativos XXI, S.L.(represented by D. Óscar Arregui Abendivar) Director

D. Pascual Fernández Martínez Director

D. Javier Echenique Landiríbar Director

D. Fernando Abril-Martorell Hernández Director

Dña. Isabel Tocino Biscarolasaga Director

D. José Antonio Escalona de Molina Secretary

D. Guillermo Medina Ors Vice Secretary

Insiders Position (Shares) Market Value O/S

Retos Operativos (Juan Luis Arregui) 64,046,105 165,238,949.86 23.24%

Alcor Holding (Alberto Alcocer y Alberto Cortina) 73,085,314 188,560,109.73 26.52%

Lopez Jimenez Pedro Jose 13,338,345 34,412,931.04 4.84%

DE URRUTIA VAL VICTOR JUAN 12,511,588 32,279,898.12 4.54%

COMENGE SANCH JOSE IGNACIO 12,511,588 32,279,898.12 4.54%

Treasury Stocks 8,047,101 20,761,520.38 2.92%

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 23

Appendix 11: Manufacturing process

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 24

Appendix 12: Risk Matrix

Macroeconomic Industry Operational Shareholder

New Capacities from SA

Decrease in Transportation Costs

Cost Inflation Low Liquidity

FX and IR risk Slowdown of GDP

Strikes Stock Overhang

New Regulation of Renewables

PR

OB

AB

ILIT

Y

Lo

w

Mo

der

ate

H

igh

Insignificant Moderate Severe IMPACT

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 25

Appendix 13: Sensitivity Analysis of DCF Valuation

We estimated sensitivity of the DCF output target price to external factors as well as our assumptions on valuation. The sensitivity tables are depicted

below. Firstly we analyze the sensitivity of the target price to gross margin development in the long-term as well as pulp price changes.

Gross margin

-1.5% -1.0% -0.5% 0% 0.5% 1.0% 1.5%

Pu

lp (

BH

KP

) P

ric

e

-1.5% 1.41 1.50 1.60 1.70 1.80 1.89 1.99

-1.0% 1.52 1.62 1.71 1.81 1.91 2.01 2.11

-0.5% 1.63 1.73 1.83 1.93 2.03 2.13 2.23

0% 1.74 1.84 1.95 2.05 2.15 2.37 2.35

0.5% 1.86 1.96 2.06 2.17 2.27 2.37 2.47

1.0% 1.98 2.08 2.18 2.29 2.39 2.49 2.60

1.5% 2.10 2.20 2.31 2.41 2.52 2.62 2.72

The table below depicts the sensitivity of the target price to valuation estimates, namely to terminal growth rate and WACC of the company.

Terminal growth rate

-1.5% -1.0% -0.5% 0% 0.5% 1.0% 1.5%

WA

CC

-1.5% 2.16 2.43 2.76 3.18 3.74 4.50 5.61

-1.0% 1.90 2.12 2.39 2.71 3.13 3.68 4.43

-0.5% 1.69 1.87 2.08 2.34 2.67 3.08 3.62

0% 1.51 1.66 1.83 2.05 2.30 2.62 3.02

0.5% 1.35 1.48 1.63 1.80 2.01 2.26 2.58

1.0% 1.21 1.32 1.45 1.59 1.77 1.97 2.22

1.5% 1.09 1.19 1.29 1.42 1.56 1.73 1.94

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 26

Appendix 14: Monte Carlo Simulation Analysis

Our DCF valuation model depends on a number of assumptions about external factors as well as internal indicators. We decided to perform Monte Carlo

simulation to examine the sensitivity of our valuation further. The list of input to valuation is depicted below.

Lower limit Upper limit Range

Pulp prices -4% 4% 8%

Cost of Goods Sold 5% -5% -10%

Price of energy -7% 2% 9%

Days Sales Outstanding 5% -5% -10%

Days Payables Outstanding -5% 5% 10%

Days Inventories Outstanding 5% -5% -30%

We assumed a reasonable range for simulation for each variable. The change in energy prices is skewed to the negative due to the negative effect of reform

on prices, even though the effect is difficult to quantify.

The mean price resulting from simulation is €2.24, which is in line with out sell recommendation.

0

0,01

0,02

0,03

0,04

0,05

0,06

0,07

Pro

bab

ilit

y Current price

Mean price €2,24

DCF Target price

BUYHOLDSELL

Summarized Monte Carlo Output

# Scenarios 2000

SDV 69%

Lower range €0.37

Upper range €4.06

Range €3.69

Average €2.24

ENCE Energia y Celulosa | ENC

CFA Research Challenge | 27

Appendix 15: Technical Analysis

Number Technical Analysis Description

1 Support/Resistance Lines The technical indicators generally point towards a downwards potential in price movement. The

long term support line now acts as a resistance line to prices. The upper price range is bound at

€3.20 and the lower price is bounded by two major support lines at €2.30 and €1.90

respectively. The stock is in a downtrend and has the potential to go down by €0.25 from

trading price as of 17/02/2014.

2 Relative Strengh Index The RSI is just under 40 and can go lower before it reaches "oversold" territory.

3 Candlestick Patterns There was a formation of a bearish "evening star" pattern recently which signals negative

sentiment in price charts of ENCE.

4 MACD / MACD Signal The MACD is still below the MACD signal indicating a strong sell signal. This would change

when MACD crosses above MACD Signal

Disclosures:Ownership and material conflicts of interest:The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company.The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might biasthe content or publication of this report.Receipt of compensation:Compensation of the author(s) of this report is not based on investment banking revenue.Position as a officer or director:The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subjectcompany.Market making:The author(s) does not act as a market maker in the subject company’s securities.Disclaimer:The information set forth herein has been obtained or derived from sources generally available to the public and believed by theauthor(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy orcompleteness. The information is not intended to be used as the basis of any investment decisions by any person or entity. Thisinformation does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This reportshould not be considered to be a recommendation by any individual affiliated with CFA Society Spain, CFA Institute or the CFAInstitute Research Challenge with regard to this company’s stock.

CFA Institute Research Challenge