IEE MANAGEMENT & DESIGN DIVISION: CHAIRMAN'S ADDRESS Managing a business in the public sector D.G. Jefferies, CEng, FIEE, CBIM Indexing terms: Management, Engineering administration, Electric power distribution Abstract: The paper describes some of the chal- lenges — opportunities, problems and changes — faced by the management of a public sector elec- tricity Board. Managers in electricity supply operate in a complex organisation and within a framework of financial controls, constraints and social obligations imposed by Government and other statutory bodies. The paper considers how a distribution Board fits into the overall industry and looks at initiatives, in terms of management and technical innovation, taken by managers to improve business performance. Aspects covered include tariffs, energy management, manpower management, finance and various factors affecting system efficiency. The industry's marketing philos- ophy of promoting cost effective uses of electricity is highlighted as are the particular responsibilities of having 21 million customers. Attention is drawn to the important role that corporate plan- ning and targeting play in the overall management of a Board and the paper concludes with some general observations on how the industry's man- agement has performed. 1 Introduction In the electricity supply industry the need to maintain a safe and secure supply of electricity is a prime consider- ation. This results in an Industry which is careful, reliable and quietly efficient but is seen by the media as unex- citing, particularly the distribution side. This lack of drama is sometimes thought to reflect an unprogressive and complacent management living a quiet life in a cosy monopoly. That is far from the truth. The purpose of this paper is to explain the task of management in the industry drawing particularly on my experiences of man- aging a distribution Board. I will describe the environment in which a distribution Board's manage- ment has to work, the challenges which have to be faced and some of the measures which have been, and are being, taken to improve business performance. With pri- vatisation approaching, it is perhaps timely to report on the stewardship of the industry's management. I shall start by setting the general scene and then focus in on the management of an Area Board. Paper 5599A (M3, M4), delivered before the IEE Management & Design Division on the 20th October 1987 Mr. Jefferies is Deputy Chairman of the Electricity Council, 30 Mill- bank, London SW1P 4RD, United Kingdom 2 Background Public electricity supply in Great Britain was born out of the Electricity Act of 1947. This nationalised some 650 different local undertakings, some with only a few thou- sand customers; one in fact had only 410 customers; rather different from today's 2 million plus in some Area Boards. When I joined the Industry in 1949 we were selling 36 000 GWh to 11 million customers, now we sell 220000 GWh to 21 million customers. Back in 1949, the Industry supplied 10200 MW at time of maximum demand but it was not enough to avoid widespread power cuts — we were chronically short of capacity. In January 1987 we met a maximum demand of 47925 MW. 50000 r 40000 30000 20000 10000 20 15 1948 52 56 60 64 68 72 76 year ending March 80 84 Fig. 1 Growth in number of customers and system maximum demand number of customers system maximum demand In 1949 large areas of the country had no electricity, but if you were one of the lucky ones your idea of the latest all-electric kitchen would probably have been simply a two ring cooker, a kettle and an electric iron. Only one in 20 owned a refrigerator or washing machine, there were no food processors, no spin driers, and cer- tainly no microwave ovens. Only some 50000 homes possessed a television set. It is little surprise that elec- tricity consumption per head of population has increased six-fold since nationalisation. IEE PROCEEDINGS, Vol. 135, Pt. A, No. I, JANUARY 1988 13

Indexing terms: Management, Engineering administration, Electric power distribution

Abstract: The paper describes some of the chal-lenges — opportunities, problems and changes —faced by the management of a public sector elec-tricity Board. Managers in electricity supplyoperate in a complex organisation and within aframework of financial controls, constraints andsocial obligations imposed by Government andother statutory bodies. The paper considers how adistribution Board fits into the overall industryand looks at initiatives, in terms of managementand technical innovation, taken by managers toimprove business performance. Aspects coveredinclude tariffs, energy management, manpowermanagement, finance and various factors affectingsystem efficiency. The industry's marketing philos-ophy of promoting cost effective uses of electricityis highlighted as are the particular responsibilitiesof having 21 million customers. Attention isdrawn to the important role that corporate plan-ning and targeting play in the overall managementof a Board and the paper concludes with somegeneral observations on how the industry's man-agement has performed.

1 Introduction

In the electricity supply industry the need to maintain asafe and secure supply of electricity is a prime consider-ation. This results in an Industry which is careful, reliableand quietly efficient but is seen by the media as unex-citing, particularly the distribution side. This lack ofdrama is sometimes thought to reflect an unprogressiveand complacent management living a quiet life in a cosymonopoly. That is far from the truth. The purpose of thispaper is to explain the task of management in theindustry drawing particularly on my experiences of man-aging a distribution Board. I will describe theenvironment in which a distribution Board's manage-ment has to work, the challenges which have to be facedand some of the measures which have been, and arebeing, taken to improve business performance. With pri-vatisation approaching, it is perhaps timely to report onthe stewardship of the industry's management. I shallstart by setting the general scene and then focus in on themanagement of an Area Board.

Paper 5599A (M3, M4), delivered before the IEE Management &Design Division on the 20th October 1987Mr. Jefferies is Deputy Chairman of the Electricity Council, 30 Mill-bank, London SW1P 4RD, United Kingdom

2 Background

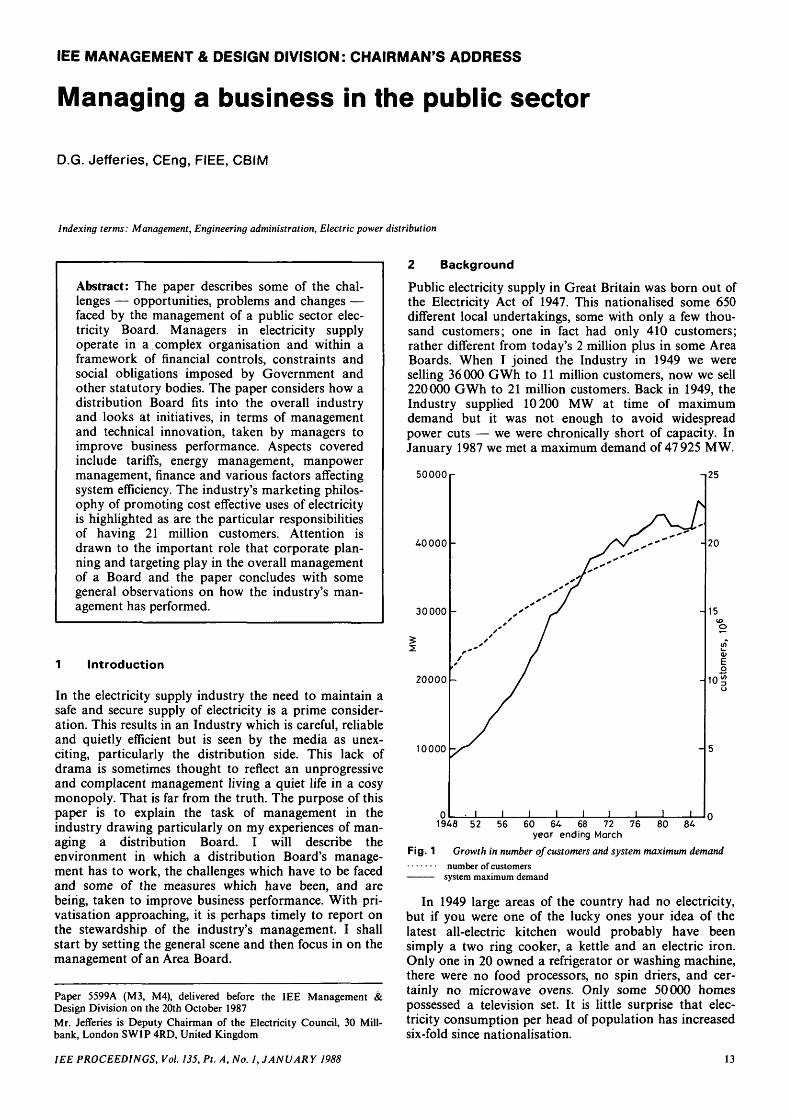

Public electricity supply in Great Britain was born out ofthe Electricity Act of 1947. This nationalised some 650different local undertakings, some with only a few thou-sand customers; one in fact had only 410 customers;rather different from today's 2 million plus in some AreaBoards. When I joined the Industry in 1949 we wereselling 36 000 GWh to 11 million customers, now we sell220000 GWh to 21 million customers. Back in 1949, theIndustry supplied 10200 MW at time of maximumdemand but it was not enough to avoid widespreadpower cuts — we were chronically short of capacity. InJanuary 1987 we met a maximum demand of 47925 MW.

50000r

40000

30000

20000

10000

20

15

1948 52 56 60 64 68 72 76year ending March

80 84

Fig. 1 Growth in number of customers and system maximum demand

number of customerssystem maximum demand

In 1949 large areas of the country had no electricity,but if you were one of the lucky ones your idea of thelatest all-electric kitchen would probably have beensimply a two ring cooker, a kettle and an electric iron.Only one in 20 owned a refrigerator or washing machine,there were no food processors, no spin driers, and cer-tainly no microwave ovens. Only some 50000 homespossessed a television set. It is little surprise that elec-tricity consumption per head of population has increasedsix-fold since nationalisation.

IEE PROCEEDINGS, Vol. 135, Pt. A, No. I, JANUARY 1988 13

2.1 Present structureThe present structure of the industry is the result of theElectricity Act of 1957. This introduced the Central Elec-tricity Generating Board (CEGB) and the ElectricityCouncil and left the Industry in England and Walesorganised on what is essentially a federal basis with gen-eration and transmission separated from distribution.The Electricity Council is where the various parts of theindustry come together to resolve their common prob-lems, under independent guidance, and to gain the benefitof shared experience. It consists of a Chairman, a DeputyChairman and three other members, all directlyappointed by the Secretary of State for Energy. Theremaining members are the chairman and two othermembers of the CEGB and the chairmen of the 12 AreaBoards. The Council's functions are to advise the Secre-tary of State on questions affecting the electricity supplyindustry and to promote the development by Boards ofan efficient, co-ordinated and economical system ofsupply [1]. It does not control the CEGB or the AreaBoards. Like the CEGB, the Area Boards are directlyresponsible to the Secretary of State and, through him, toParliament.

Central ElectricityGenerating Board

Fig. 2 Outline structure of the industry

The organisation of the Industry is unique and confu-sing. Its structure has been much criticised both fromwithin and without and attempts have been made tochange it. A report by Lord Plowden in 1976 [2] con-cluded that divided responsibilities made it hard forBoards to co-operate and that where decisions wererequired for the industry as a whole the process ofachievement was slow and cumbersome. The basic organ-isation has in fact remained unchanged for the last 30years and has been made to work effectively by the effortsof management in all parts of the industry. It is currentlya matter of no little interest what organisational structurethe industry might have in the private sector.

2.2 Frame work of financial objectivesIn common with most businesses, managers in theindustry attempt to improve their financial performancethrough an effective combination of cost control, market-ing strategy, cash management and capital investment.The difference for this industry is that the owners(Government) set down a very comprehensive andexplicit range of financial targets and constraints inadvance, these comprise:

(a) a financial target(b) a rate of return on new capital projects(c) an external financing limit(d) a performance aim

(e) an annual Government review of capital expendi-ture.

The financial target was described in a 1978 White Paperas the primary expression of financial performance. It isbased on the ratio of operating profit to average netassets employed. The current target requires the industryto achieve an average return of 2.75 per cent on a CCA(current cost accounting) basis over the period 1985/86 to1987/88. The CCA system allows for price changes spe-cific to the industry when reporting assets employed andprofits earned. In particular, depreciation and assetvalues are calculated either on the basis of the replace-ment cost of tangible fixed assets by reference to theirmodern equivalent or by indexation. The results achievedusing this method are very different to those achievedusing HCA (historical cost accounting), the methodmostly used by other organisations. The industry's targetof 2.75% is estimated to be equivalent to about 15% onan HCA basis. The specification of a target to twodecimal places may seem trivial, but in an industry of thissize 0.05 per cent is equal to £15 million per annum. Toachieve this target requires the closest possible attentionto financial control and to the prospects for turnover.

The 1978 White Paper also introduced the requiredrate of return (RRR) approach to investment appraisal.Under these rules the industry is required to achieve a5% real rate of return on the aggregate of new capitalinvestment, including non-revenue-earning projects. Thelevel of the return is set to reflect the opportunity cost ofcapital to the nation and is meant to ensure there is no'crowding out' of private sector investment. Externalfinancing limits (EFLs) control the level of external bor-rowing or financing. The system has been in operationsince 1976/77 and for several years the industry has beena net repayer; i.e. cash has been paid back to the Govern-ment rather than borrowed. In 1986/87, £1,325 millionwas repaid, equivalent to more than lp on the standardrate of income tax or one-third of the UK's public sectorborrowing requirement.

Because electricity is a virtual necessity in many areasof modern life, there exists a potential for the industry toovercome any operating inefficiency simply by raisingprices. It is for this reason that the industry has a per-formance aim which puts pressure directly on costs. Theindustry is currently targeted to reduce its controllablecosts (i.e. those costs under direct management control)per unit sold by 6.1 per cent in real terms between1983/84 and 1987/88. The aim is for the Industry in total,but each Area Board, the CEGB and Council itself has acontributory target appropriate to what is judged achiev-able in the circumstances of each organisation. Finally,the Electricity Act 1957 requires that programmes ofcapital expenditure are approved by the Secretary ofState for Energy.

With the exception of capital expenditure approval,the main financial controls stem from the 1978 WhitePaper. They are not statutory duties in the same sense.Indeed under the 1957 Act the industry's statutory finan-cial duty is simply to see that revenue is not less thanexpenditure taking one year with another. There havebeen times when, in the industry's view, these varioustargets have been inconsistent. Particular problems havearisen with EFLs.

Boards are also subject to a wide range of specialstatutory duties under various Acts of Parliament and tospecial regulations relating to the supply of electricity. Inthe interests of brevity I shall not describe them, but they

14 IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988

add up to a myriad of special rules, regulations andrestrictions within which management has to operate andachieve its range of financial targets. While the industrydoes not therefore, at present, have shareholders and thestockmarket to satisfy, it does, in Government, have verydemanding masters.

2.3 External monitoringThe industry is subject to an exceptional degree of exter-nal monitoring. By law each Board reports directly to theSecretary of State for Energy and to the ElectricityCouncil. In addition, the Monopolies and Mergers Com-mission (MMC) is empowered to undertake examinationof specific aspects of the Industry's operations. Both theDirector of Fair Trading and the Secretary of State forTrade and Industry can ask the MMC to undertake sucha review. In recent years the MMC has examined someor all of the activities of seven Area Boards. A moregeneral form of review is provided by the House ofCommons system of Select Committees. The Select Com-mittee on Energy is empowered to make extensive inquir-ies into the industry. The results of MMC and SelectCommittee inquiries are published.

Customer interests are represented at local level by the12 area Electricity Consultative Councils. These have 20to 30 members each, some of whom represent localauthorities, the remainder represent other interest groupssuch as agriculture, commerce, industry, labour and cus-tomers in general. The councils monitor the industry'sstandards of service and, where necessary, put pressureon the industry to improve performance. They alsoexamine customer complaints. At national level, cus-tomer interests are represented by the Electricity Con-sumers Council.

2.4 Corporate planningElectricity supply is a business of contrasts. There is theneed to meet demand on a minute-by-minute basis on theone hand and the very long term planning horizonsrequired for many areas of electricity supply on the other.This, coupled with the complex environment in which theindustry's managers have to operate, means that apremium is placed on good business planning and plan-ning has therefore always occupied a very importantplace in the industry. Formalised corporate planningcommenced in the early 1970s following proposals madeby Sir Henry Benson, and the industry in England andWales has been producing industry-wide corporate planssince 1974. In recent years these plans have beenpublished outside the industry.

The industry sees corporate planning as a processwhich enables its management to develop a corporatestrategy for the business in a changing environment. Itinvolves agreeing objectives, implementing plans andmonitoring progress. The industry's prime objective,which emanates from the Acts of Parliament, is tocheapen the cost of electricity supply subject to:

(a) meeting the Government's financial targets(b) maintaining the quality of supply and service(c) having regard to the welfare of customers and

employees and to the care of the environment.

Industry-wide plans are generally produced for one andseven years ahead, but in some circumstances it is neces-sary to look much further than this, e.g. to the year 2000and even beyond. Plans once formulated are not howevertablets of stone. They are regularly updated with thelatest information available. Circumstances change and

IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988

plans have to change with them if the industry is to havethe strategy necessary to achieve its objectives.

2.5 Tariff settingBecause the Industry is a virtual monopoly it could, inprinciple, achieve almost any level of profit requiredsimply by using its monopoly power to raise prices. Toavoid this situation, the industry has adopted a pricingpolicy which uses 'market' principles to set prices [3].This means trying to estimate the prices that would occurif there were perfect competition in the supply of elec-tricity. The concept of market pricing is a major elementin the discussions with Government that lead to thefixing of the financial target. Essentially, the objective isto reflect in prices the additional cost of supplying a cus-tomer on a continuing basis — the industry's long runmarginal costs.

There is a different cost for supplying each of theindustry's 21 million customers but obviously it wouldnot be practicable to have 21 million different tariffs. Theindustry therefore groups together customers with similarusage characteristics so that the range of tariffs is limitedto a sensible number. Care is taken when doing this toensure that no 'undue preference' is shown between cus-tomers — a statutory requirement. The characteristics ofcustomer usage are ascertained by some 3000 datarecorders installed in samples of customers premises.These monitor electricity use every half hour and fromthis data typical daily load curves are derived. Thisallows an assessment to be made of the contribution dif-ferent customers make to the demand on the system andthe consumption of each customer group within particu-lar periods of the day, month and year.

40 000

30 000

o 20 000

10000

/ • • / .•\N

• w

0400 0800 1200 1600hour of the day

2000 2400

Fig. 3 Contributions of main customer classes to national systemdemand on a typical winter's day

total domestic— • — industrial — — commercial and other

This information together with the detailed break-down of system costs between energy-related, demand-related and customer-related allows the Industry tocalculte the long-run marginal costs that should be allo-cated to each customer group. Finally, these costs areturned into tariffs. This requires a balance to be struck

15

between having a simple tariff which is cheap to meter,and a more complex tariff with more precise cost reflec-tion but which is more costly to meter. Price setting inthis way is very demanding and is a management taskvirtually unique to the electricity supply industry. Itrequires a comprehensive and complex analysis and theinterpretation of many factors. Its results affect everyhome and business in the country.

3 Area Boards

The Area Boards are essentially distribution Boards.They buy electricity from the CEGB and distribute it totheir customers. The amount of own generation is verysmall. The Boards cover quite different geographic areasranging from as little as 257 square miles to as much as7763 square miles. The number of customers varies fromunder a million to nearly three million. In total, theBoards have fixed assets worth over £9,000 million atcurrent cost values and undertake capital investmentworth about £500 million a year. They employ some82 000 staff.

The Boards total annual turnover is in the region of£11000 million. This is roughly on a par with Shell andEsso and somewhat more than British Gas. The turnoverof an average Board is comparable to that of companiessuch as Cable and Wireless or Blue Circle industries.Boards also retail electrical appliances and undertakecontracting (mainly wiring) work. The annual turnoveron appliance retailing is currently over £500 million andis generated through 900 shops. The financial results forthe total activity in 1986/87 are given below for AreaBoards in aggregate:

Table 1 : Area boards' consolidated profit and loss accounts,1986/87

Operating profit before MWCAElectricity supplyContractingAppliance marketing

Interest (received), MWCA and tax

Net profit transferred to reserves

£ million

10220184550

10954

9874175511

10560

3469

39394

125

269

3.1 Management of an Area BoardEach Area Board consists of a Chairman and five toseven other members appointed by the Secretary of State.Most of these other members are part-time and aredrawn from outside the industry. The chairman, with hisBoard, is directly responsible to the Secretary of State forhis area. He is also a member of the Electricity Counciland shares in the decisions made for the industry overall.There are tremendous advantages to be gained fromworking with other Boards on common problems, andthere is great potential for cost savings arising fromeconomies of scale due to the application of common sol-utions. Successful developments in any one of the Boardsmay well be applicable in others, and there is a great dealof information exchange and co-operation through a

comprehensive committee structure based on Council.But there has to be room for local initiatives by localmanagers which grasp local opportunities. The chairmanof an Area Board often has to balance local advantageagainst national advantage.

The Boards' organisations are also a balance betweenlocal division, or district, management teams, who maybe responsible for up to half a million customers in theirdivision or district, and functional directors at headquar-ters. Headquarters staff set policy for the engineering,commercial, accounting, secretarial and IT functions andprovide specialist services such as personnel and manage-ment services. They also provide the link to the Elec-tricity Council. Both the divisional, or district, managersand functional directors report to the Deputy Chairmanwhose span of control is typically about ten: a numberreminiscent of the organisation of Roman legions.Getting the right relationship between line and staff func-tions with clear management accountabilities is the keyto a well organised Board.

But what is the organisation trying to achieve? Theindustry's key financial target is return on assets; eachBoard therefore has a financial target consistent with theoverall target. For an Area Board the financial target canbe usefully broken down using a ratio analysis hierarchy:

//

salesnet assets

profitnet assets

profitsales

/ \

income (price)sales

\costssales

Fig. 4 Illustrative ratio analysis hierarchy

To meet the financial target and achieve the objectiveof cheapening the cost of supply, the sales/net-assets rationeeds to be maximised and the necessary profit marginachieved at lowest possible prices; i.e. costs per unit areminimised. Improving asset utilisation and reducing con-trollable costs per unit are therefore central to thebusiness of managing a Board.

3.2 Sales and marketing managementThe industry has developed its marketing capability toencourage the cost effective use of electricity and toimprove asset utilisation. The Boards operate teams ofhighly trained marketing staff, backed up by furtherspecialists at the Electricity Council. Boards have lookedat each of their markets and potential markets, carriedout comprehensive load and market research, looked atprice competitiveness, looked at product availability andtargeted their sales forces accordingly. The industry is nota monopoly supplier of energy, and it needs to market itsproduct successfully like any other commercial organis-ation.

Marketing strategy is geared to identifying marketopportunities for electrical applications and communicat-ing the potential benefits to customers. What are the keyfeatures of the industry's marketing plans? In the domes-tic sector, new space heating sales are focused on off-peakconsumption, particularly through the promotion of theMedallion, Civic Shield and Energy Wise AwardSchemes. These schemes encourage high thermal insula-tion standards in homes. Incidentally, one of the reasonsstorage heaters are now more attractive is the develop-

16 IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988

ment of Feolite, a highly efficient heat storage material, atthe industry's own laboratories at Capenhurst. This hasallowed manufacturers to build storage heaters half thesize of those in the 1960s. Electric heat pumps open upnew opportunities. An interesting development in theLondon Board is the promotion of the water-to-waterheat pump to heat new buildings in the London dock-lands area using the water of the docks as the heatsource. In the commercial sector, the industry has intro-duced awards to encourage energy efficiency, while inindustry, where electricity offers a wide range of tech-niques for drying, curing and baking there is an award —the Power for Efficiency and Productivity Award — formanufacturing companies that have extended their use ofelectricity and improved energy efficiency, productquality or the working environment. Last year's 28regional winners saved over £2 million by switching toelectricity.

The electricity supply industry does not simply leave itto others to develop new electrical products and pro-cesses; its own research centre at Capenhurst has devel-oped new techniques to assist British industry on anumber of fronts, notably metal melting, metal workingand shaping. A particularly interesting area is the heating

of superplastic metals, these metals have unusual proper-ties and when heated can be vacuum moulded. Concorde,the European Airbus and the Tornado aircraft allcontain parts made by techniques developed from workat Capenhurst. Other successful industrial researchincludes the recovery of valuable metals and chemicalsfrom process waste, the development of a high-temperature heat pump with many potential applicationsin process drying, and the development of radiofrequencyand microwave techniques, also for drying.

3.3 Energy managemen tLarge customers often install sophisticated equipment tomonitor electricity usage so that they can reduce demandat times of high cost. For the domestic customer thescope for cost reduction is the range of off-peak tariffs.These tariffs have been very successful in promoting salesat times of low production cost and Boards are currentlyselling almost half a million storage heaters a year. Overthe years, these efforts have helped to produce a signifi-cant increase in system load factor: from 45% in the mid-1950s to almost 60% now. This represents a considerableimprovement in asset utilisation. The change in the shapeof national demand on the system on a typical cold

Fig. 5 Some PEP award winners in 1986PEP award winners West Yorkshire Foundries of Leeds, who manufacture cylin-der blocks and heads, invested in an electric system to hold and distribute moltenaluminium which led to improvements in quality and an increase in ordersCritchley, Sharp and Tetlow, wire manufacturers of Cleckheaton, won their awardfor the benefits they recorded on switching to electricity for the heat treatment of

IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988 17

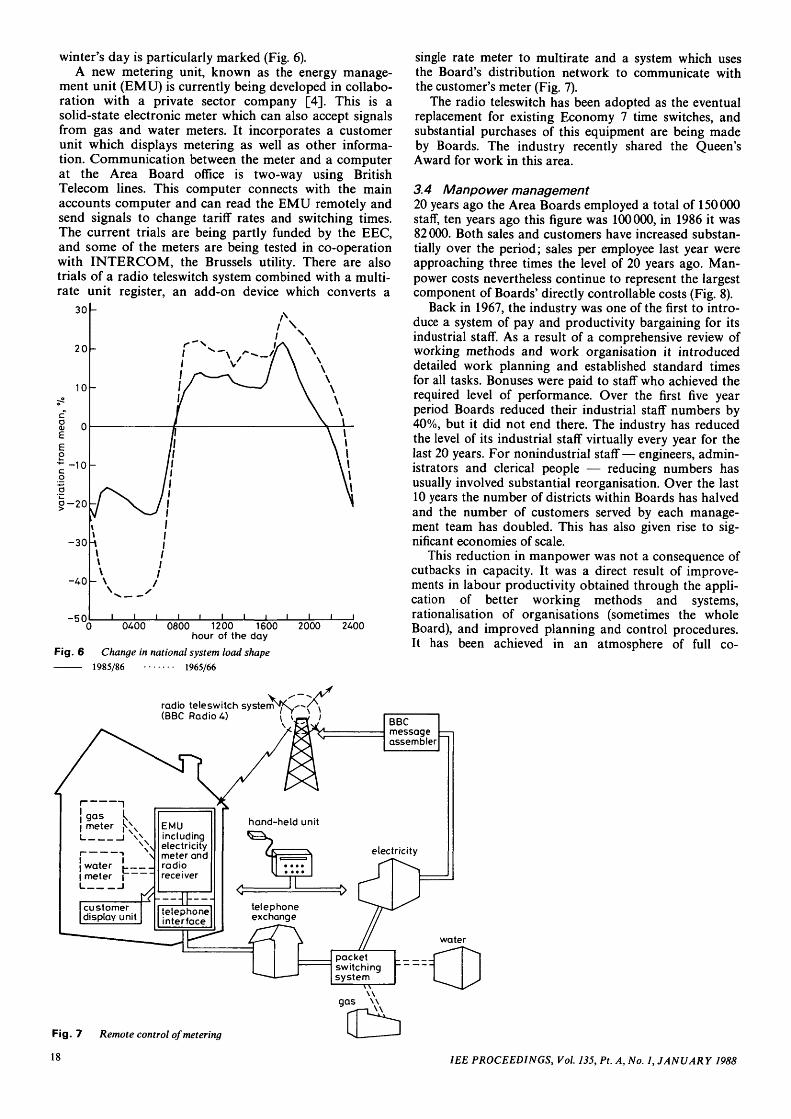

winter's day is particularly marked (Fig. 6).A new metering unit, known as the energy manage-

ment unit (EMU) is currently being developed in collabo-ration with a private sector company [4]. This is asolid-state electronic meter which can also accept signalsfrom gas and water meters. It incorporates a customerunit which displays metering as well as other informa-tion. Communication between the meter and a computerat the Area Board office is two-way using BritishTelecom lines. This computer connects with the mainaccounts computer and can read the EMU remotely andsend signals to change tariff rates and switching times.The current trials are being partly funded by the EEC,and some of the meters are being tested in co-operationwith INTERCOM, the Brussels utility. There are alsotrials of a radio teleswitch system combined with a multi-rate unit register, an add-on device which converts a

30 -

- 5 0

Fig. 6

i 0400 0800 1200 1600hour of the day

Change in national system load shape1985/86 1965/66

2000 2400

single rate meter to multirate and a system which usesthe Board's distribution network to communicate withthe customer's meter (Fig. 7).

The radio teleswitch has been adopted as the eventualreplacement for existing Economy 7 time switches, andsubstantial purchases of this equipment are being madeby Boards. The industry recently shared the Queen'sAward for work in this area.

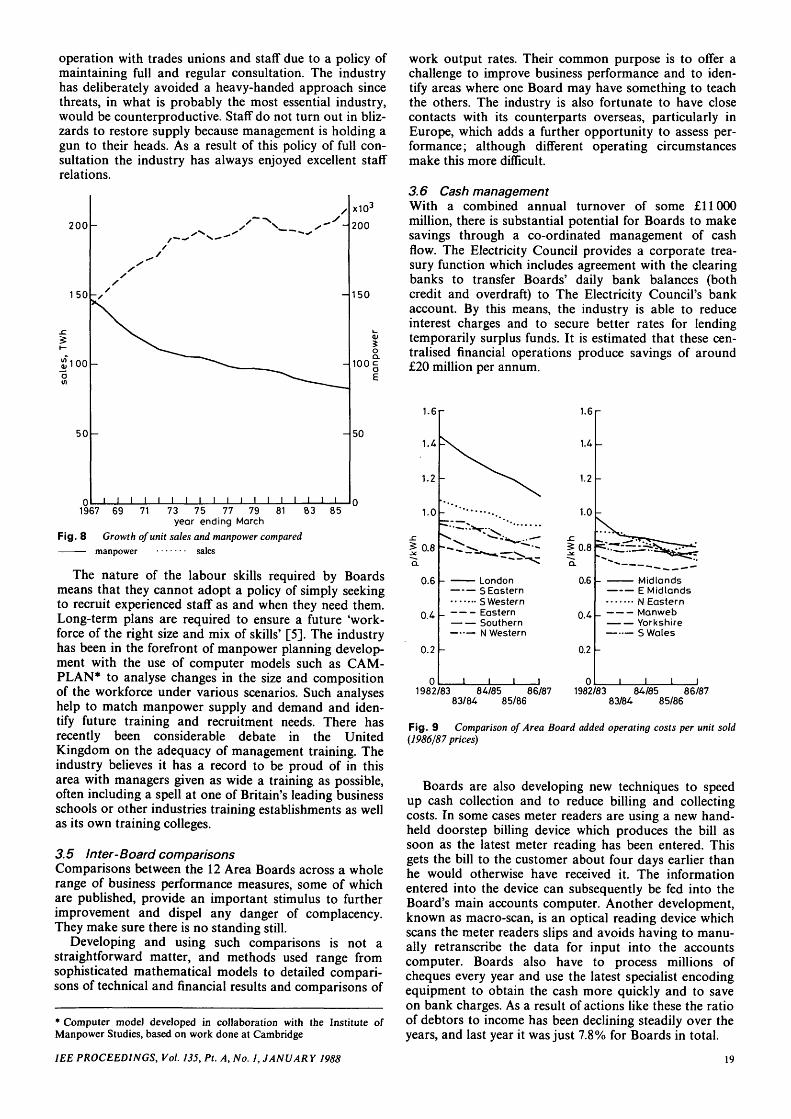

3.4 Manpower management20 years ago the Area Boards employed a total of 150000staff, ten years ago this figure was 100000, in 1986 it was82 000. Both sales and customers have increased substan-tially over the period; sales per employee last year wereapproaching three times the level of 20 years ago. Man-power costs nevertheless continue to represent the largestcomponent of Boards' directly controllable costs (Fig. 8).

Back in 1967, the industry was one of the first to intro-duce a system of pay and productivity bargaining for itsindustrial staff. As a result of a comprehensive review ofworking methods and work organisation it introduceddetailed work planning and established standard timesfor all tasks. Bonuses were paid to staff who achieved therequired level of performance. Over the first five yearperiod Boards reduced their industrial staff numbers by40%, but it did not end there. The industry has reducedthe level of its industrial staff virtually every year for thelast 20 years. For nonindustrial staff— engineers, admin-istrators and clerical people — reducing numbers hasusually involved substantial reorganisation. Over the last10 years the number of districts within Boards has halvedand the number of customers served by each manage-ment team has doubled. This has also given rise to sig-nificant economies of scale.

This reduction in manpower was not a consequence ofcutbacks in capacity. It was a direct result of improve-ments in labour productivity obtained through the appli-cation of better working methods and systems,rationalisation of organisations (sometimes the wholeBoard), and improved planning and control procedures.It has been achieved in an atmosphere of full co-

radio teleswitch system(BBC Radios) \

EMUincludingelectricitymeter andradioreceiver

—It—telephoneinterface

Fig. 7 Remote control of metering

18 1EE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988

operation with trades unions and staff due to a policy ofmaintaining full and regular consultation. The industryhas deliberately avoided a heavy-handed approach sincethreats, in what is probably the most essential industry,would be counterproductive. Staff do not turn out in bliz-zards to restore supply because management is holding agun to their heads. As a result of this policy of full con-sultation the industry has always enjoyed excellent staffrelations.

200

150

jpooo

50

x10J

200

150

O

100 |

E

50

Q | I I I I I I I I I I I I I I I I I I | Q

1967 69 71 73 75 77 79 81 63 85year ending March

Fig. 8 Growth of unit sales and manpower compared

manpower sales

The nature of the labour skills required by Boardsmeans that they cannot adopt a policy of simply seekingto recruit experienced staff as and when they need them.Long-term plans are required to ensure a future 'work-force of the right size and mix of skills' [5]. The industryhas been in the forefront of manpower planning develop-ment with the use of computer models such as CAM-PLAN* to analyse changes in the size and compositionof the workforce under various scenarios. Such analyseshelp to match manpower supply and demand and iden-tify future training and recruitment needs. There hasrecently been considerable debate in the UnitedKingdom on the adequacy of management training. Theindustry believes it has a record to be proud of in thisarea with managers given as wide a training as possible,often including a spell at one of Britain's leading businessschools or other industries training establishments as wellas its own training colleges.

3.5 Inter-Board comparisonsComparisons between the 12 Area Boards across a wholerange of business performance measures, some of whichare published, provide an important stimulus to furtherimprovement and dispel any danger of complacency.They make sure there is no standing still.

Developing and using such comparisons is not astraightforward matter, and methods used range fromsophisticated mathematical models to detailed compari-sons of technical and financial results and comparisons of

• Computer model developed in collaboration with the Institute ofManpower Studies, based on work done at Cambridge

work output rates. Their common purpose is to offer achallenge to improve business performance and to iden-tify areas where one Board may have something to teachthe others. The industry is also fortunate to have closecontacts with its counterparts overseas, particularly inEurope, which adds a further opportunity to assess per-formance; although different operating circumstancesmake this more difficult.

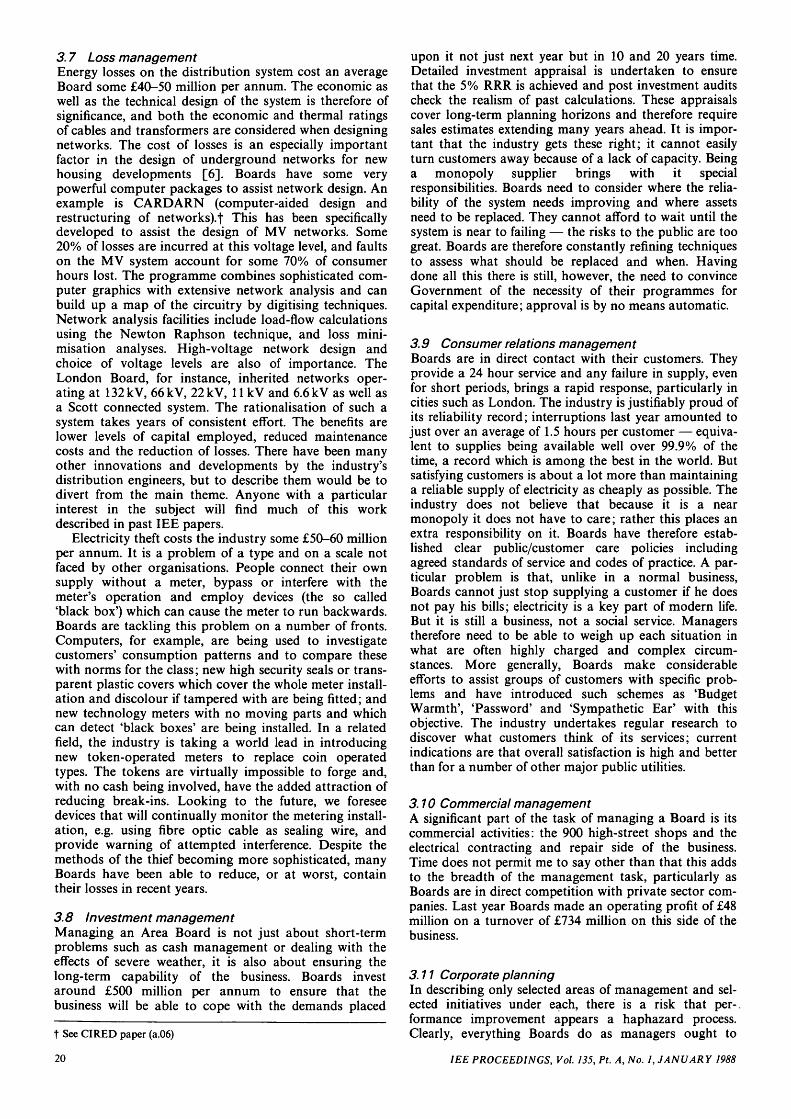

3.6 Cash managementWith a combined annual turnover of some £11000million, there is substantial potential for Boards to makesavings through a co-ordinated management of cashflow. The Electricity Council provides a corporate trea-sury function which includes agreement with the clearingbanks to transfer Boards' daily bank balances (bothcredit and overdraft) to The Electricity Council's bankaccount. By this means, the industry is able to reduceinterest charges and to secure better rates for lendingtemporarily surplus funds. It is estimated that these cen-tralised financial operations produce savings of around£20 million per annum.

1.6r 1.6

1.i\ 1.4

1.2 - ^ ^ ^ 1.2

1.0r- " ' " 10

0.8 h - ^ - - " ^ T ^ I 0.8

LondonS EasternS WesternEasternSouthernN Western

MidlandsE MidlandsN EasternManwebYorkshireS Wales

j I

0.6 I London 0.6

0.4SouthernN Western

0.21- 0.2

01982/83 84/85 86/87 1982/83 84/85 86/87

83/84 85/86 83/84 85/86

Fig. 9 Comparison of Area Board added operating costs per unit sold(1986/87 prices)

Boards are also developing new techniques to speedup cash collection and to reduce billing and collectingcosts. In some cases meter readers are using a new hand-held doorstep billing device which produces the bill assoon as the latest meter reading has been entered. Thisgets the bill to the customer about four days earlier thanhe would otherwise have received it. The informationentered into the device can subsequently be fed into theBoard's main accounts computer. Another development,known as macro-scan, is an optical reading device whichscans the meter readers slips and avoids having to manu-ally retranscribe the data for input into the accountscomputer. Boards also have to process millions ofcheques every year and use the latest specialist encodingequipment to obtain the cash more quickly and to saveon bank charges. As a result of actions like these the ratioof debtors to income has been declining steadily over theyears, and last year it was just 7.8% for Boards in total.

1EE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988 19

3.7 Loss managementEnergy losses on the distribution system cost an averageBoard some £40-50 million per annum. The economic aswell as the technical design of the system is therefore ofsignificance, and both the economic and thermal ratingsof cables and transformers are considered when designingnetworks. The cost of losses is an especially importantfactor in the design of underground networks for newhousing developments [6]. Boards have some verypowerful computer packages to assist network design. Anexample is CARDARN (computer-aided design andrestructuring of networks).! This has been specificallydeveloped to assist the design of MV networks. Some20% of losses are incurred at this voltage level, and faultson the MV system account for some 70% of consumerhours lost. The programme combines sophisticated com-puter graphics with extensive network analysis and canbuild up a map of the circuitry by digitising techniques.Network analysis facilities include load-flow calculationsusing the Newton Raphson technique, and loss mini-misation analyses. High-voltage network design andchoice of voltage levels are also of importance. TheLondon Board, for instance, inherited networks oper-ating at 132 kV, 66 kV, 22 kV, 11 kV and 6.6 kV as well asa Scott connected system. The rationalisation of such asystem takes years of consistent effort. The benefits arelower levels of capital employed, reduced maintenancecosts and the reduction of losses. There have been manyother innovations and developments by the industry'sdistribution engineers, but to describe them would be todivert from the main theme. Anyone with a particularinterest in the subject will find much of this workdescribed in past IEE papers.

Electricity theft costs the industry some £50-60 millionper annum. It is a problem of a type and on a scale notfaced by other organisations. People connect their ownsupply without a meter, bypass or interfere with themeter's operation and employ devices (the so called'black box') which can cause the meter to run backwards.Boards are tackling this problem on a number of fronts.Computers, for example, are being used to investigatecustomers' consumption patterns and to compare thesewith norms for the class; new high security seals or trans-parent plastic covers which cover the whole meter install-ation and discolour if tampered with are being fitted; andnew technology meters with no moving parts and whichcan detect 'black boxes' are being installed. In a relatedfield, the industry is taking a world lead in introducingnew token-operated meters to replace coin operatedtypes. The tokens are virtually impossible to forge and,with no cash being involved, have the added attraction ofreducing break-ins. Looking to the future, we foreseedevices that will continually monitor the metering install-ation, e.g. using fibre optic cable as sealing wire, andprovide warning of attempted interference. Despite themethods of the thief becoming more sophisticated, manyBoards have been able to reduce, or at worst, containtheir losses in recent years.

3.8 Investment managementManaging an Area Board is not just about short-termproblems such as cash management or dealing with theeffects of severe weather, it is also about ensuring thelong-term capability of the business. Boards investaround £500 million per annum to ensure that thebusiness will be able to cope with the demands placed

t See CIRED paper (a.06)

20

upon it not just next year but in 10 and 20 years time.Detailed investment appraisal is undertaken to ensurethat the 5% RRR is achieved and post investment auditscheck the realism of past calculations. These appraisalscover long-term planning horizons and therefore requiresales estimates extending many years ahead. It is impor-tant that the industry gets these right; it cannot easilyturn customers away because of a lack of capacity. Beinga monopoly supplier brings with it specialresponsibilities. Boards need to consider where the relia-bility of the system needs improving and where assetsneed to be replaced. They cannot afford to wait until thesystem is near to failing — the risks to the public are toogreat. Boards are therefore constantly refining techniquesto assess what should be replaced and when. Havingdone all this there is still, however, the need to convinceGovernment of the necessity of their programmes forcapital expenditure; approval is by no means automatic.

3.9 Consumer relations managemen tBoards are in direct contact with their customers. Theyprovide a 24 hour service and any failure in supply, evenfor short periods, brings a rapid response, particularly incities such as London. The industry is justifiably proud ofits reliability record; interruptions last year amounted tojust over an average of 1.5 hours per customer — equiva-lent to supplies being available well over 99.9% of thetime, a record which is among the best in the world. Butsatisfying customers is about a lot more than maintaininga reliable supply of electricity as cheaply as possible. Theindustry does not believe that because it is a nearmonopoly it does not have to care; rather this places anextra responsibility on it. Boards have therefore estab-lished clear public/customer care policies includingagreed standards of service and codes of practice. A par-ticular problem is that, unlike in a normal business,Boards cannot just stop supplying a customer if he doesnot pay his bills; electricity is a key part of modern life.But it is still a business, not a social service. Managerstherefore need to be able to weigh up each situation inwhat are often highly charged and complex circum-stances. More generally, Boards make considerableefforts to assist groups of customers with specific prob-lems and have introduced such schemes as 'BudgetWarmth', 'Password' and 'Sympathetic Ear' with thisobjective. The industry undertakes regular research todiscover what customers think of its services; currentindications are that overall satisfaction is high and betterthan for a number of other major public utilities.

3.10 Commercial managementA significant part of the task of managing a Board is itscommercial activities: the 900 high-street shops and theelectrical contracting and repair side of the business.Time does not permit me to say other than that this addsto the breadth of the management task, particularly asBoards are in direct competition with private sector com-panies. Last year Boards made an operating profit of £48million on a turnover of £734 million on this side of thebusiness.

3.11 Corporate planningIn describing only selected areas of management and sel-ected initiatives under each, there is a risk that per-,formance improvement appears a haphazard process.Clearly, everything Boards do as managers ought to

IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988

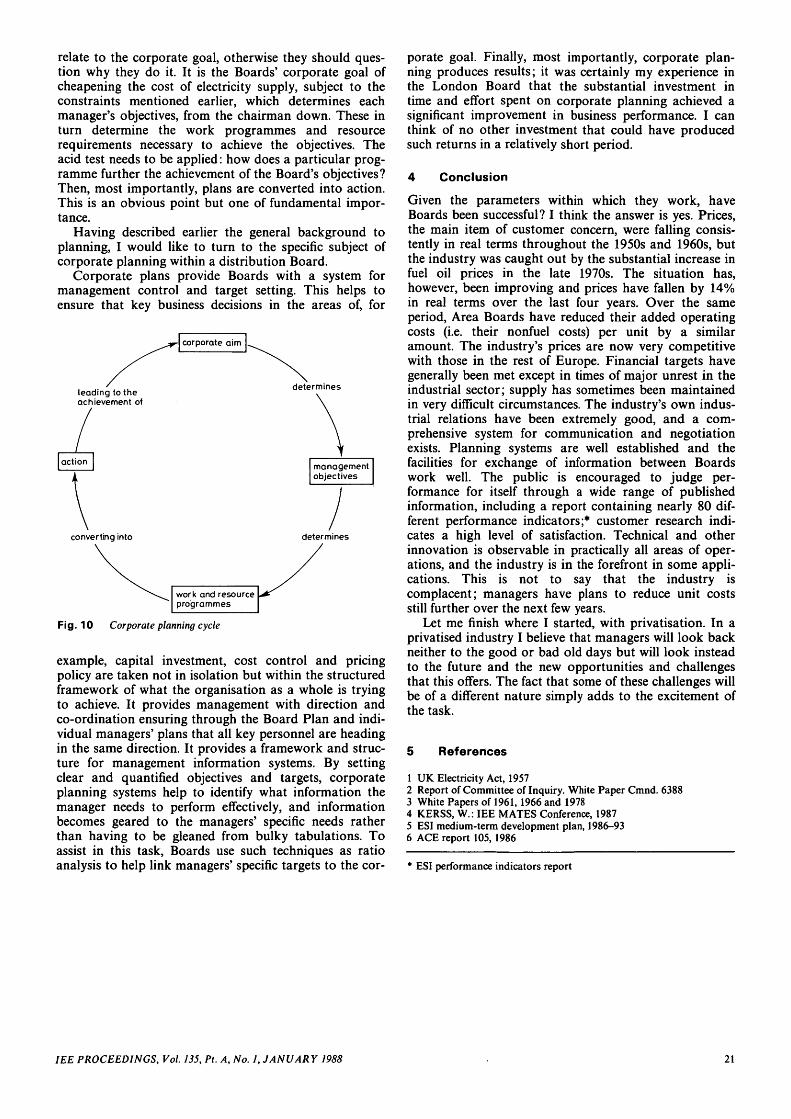

relate to the corporate goal, otherwise they should ques-tion why they do it. It is the Boards' corporate goal ofcheapening the cost of electricity supply, subject to theconstraints mentioned earlier, which determines eachmanager's objectives, from the chairman down. These inturn determine the work programmes and resourcerequirements necessary to achieve the objectives. Theacid test needs to be applied: how does a particular prog-ramme further the achievement of the Board's objectives?Then, most importantly, plans are converted into action.This is an obvious point but one of fundamental impor-tance.

Having described earlier the general background toplanning, I would like to turn to the specific subject ofcorporate planning within a distribution Board.

Corporate plans provide Boards with a system formanagement control and target setting. This helps toensure that key business decisions in the areas of, for

leading to theachievement of

determines

action managementobjectives

converting into determines

work and resourceprogrammes

Fig. 10 Corporate planning cycle

example, capital investment, cost control and pricingpolicy are taken not in isolation but within the structuredframework of what the organisation as a whole is tryingto achieve. It provides management with direction andco-ordination ensuring through the Board Plan and indi-vidual managers' plans that all key personnel are headingin the same direction. It provides a framework and struc-ture for management information systems. By settingclear and quantified objectives and targets, corporateplanning systems help to identify what information themanager needs to perform effectively, and informationbecomes geared to the managers' specific needs ratherthan having to be gleaned from bulky tabulations. Toassist in this task, Boards use such techniques as ratioanalysis to help link managers' specific targets to the cor-

porate goal. Finally, most importantly, corporate plan-ning produces results; it was certainly my experience inthe London Board that the substantial investment intime and effort spent on corporate planning achieved asignificant improvement in business performance. I canthink of no other investment that could have producedsuch returns in a relatively short period.

4 Conclusion

Given the parameters within which they work, haveBoards been successful? I think the answer is yes. Prices,the main item of customer concern, were falling consis-tently in real terms throughout the 1950s and 1960s, butthe industry was caught out by the substantial increase infuel oil prices in the late 1970s. The situation has,however, been improving and prices have fallen by 14%in real terms over the last four years. Over the sameperiod, Area Boards have reduced their added operatingcosts (i.e. their nonfuel costs) per unit by a similaramount. The industry's prices are now very competitivewith those in the rest of Europe. Financial targets havegenerally been met except in times of major unrest in theindustrial sector; supply has sometimes been maintainedin very difficult circumstances. The industry's own indus-trial relations have been extremely good, and a com-prehensive system for communication and negotiationexists. Planning systems are well established and thefacilities for exchange of information between Boardswork well. The public is encouraged to judge per-formance for itself through a wide range of publishedinformation, including a report containing nearly 80 dif-ferent performance indicators;* customer research indi-cates a high level of satisfaction. Technical and otherinnovation is observable in practically all areas of oper-ations, and the industry is in the forefront in some appli-cations. This is not to say that the industry iscomplacent; managers have plans to reduce unit costsstill further over the next few years.

Let me finish where I started, with privatisation. In aprivatised industry I believe that managers will look backneither to the good or bad old days but will look insteadto the future and the new opportunities and challengesthat this offers. The fact that some of these challenges willbe of a different nature simply adds to the excitement ofthe task.

5 References

1 UK Electricity Act, 19572 Report of Committee of Inquiry. White Paper Cmnd. 63883 White Papers of 1961, 1966 and 19784 KERSS, W.: IEE MATES Conference, 19875 ESI medium-term development plan, 1986-936 ACE report 105,1986

* ESI performance indicators report

IEE PROCEEDINGS, Vol. 135, Pt. A, No. 1, JANUARY 1988 21