MODELS FOR LINKING FARMERS TO MARKETS IN INDIA: IMPLICATIONS FOR SMALLHOLDERS Pratap S Birthal National Institute of Agricultural Economics and Policy Research, New Delhi Pallavi Rajkhowa & PK Joshi IFPRI IFPRI-IIDS- FNCCI Workshop on Best Practices in Contract Farming: Challenges and Opportunities in Nepal February 10-11, 2015, Kathmandu Nepal

Transcript

MODELS FOR LINKING FARMERS TO

MARKETS IN INDIA: IMPLICATIONS FOR

SMALLHOLDERS

Pratap S Birthal

National Institute of Agricultural Economics and Policy Research, New Delhi

Pallavi Rajkhowa & PK Joshi

IFPRI

IFPRI-IIDS- FNCCI Workshop on Best Practices in Contract Farming:

Challenges and Opportunities in Nepal

February 10-11, 2015, Kathmandu Nepal

WHY DIFFERENT MODELS? Farmers and farm heterogeneity

Farm size

Resource endowments and capabilities

Activity choices

Attitude toward production and price risk

Differential access to markets, financial and non-financial services

The less-endowed farmers require a different treatment

From agribusiness perspective

Dominance of smallholders, Disbursed production

Diseconomies of scale in aggregation of outputs and provision of technology, inputs and services

Organization of production is essential to overcome problems or costs associated with diseconomies of small-scale, poor access to services, finances, technology, inputs; inconsistent volume and quality, lack of traceability and risk management

Business models Model Drivers Rationale

Producer-driven Small scale producers, as

groups such associations

or cooperatives

Large scale farmers

Access to new markets

Obtain higher market prices

Stabilize and secure market

positions

Buyer-driven Processors

Exporters

Traders

Retailers

Assure supply

Increase supply volumes

Serve niche markets

consumer preferences

Facilitator-driven Non-governmental

organizations

National and local

governments

Make markets work for the poor

Regional and local development

Integrated Lead firms

Supermarkets

Multinationals

New. higher value markets

Low prices for good quality

Market monopolies

Business Models in India

Direct marketing models: (Apani mandi; Raythu bazar; farmers’ mall)

• Low transaction costs of contracting (negotiation, enforcement and monitoring), Large volume, Quality compliance, Economies of scale in provision of inputs, services and markets

Tend to contract with large producers

Mixed evidence

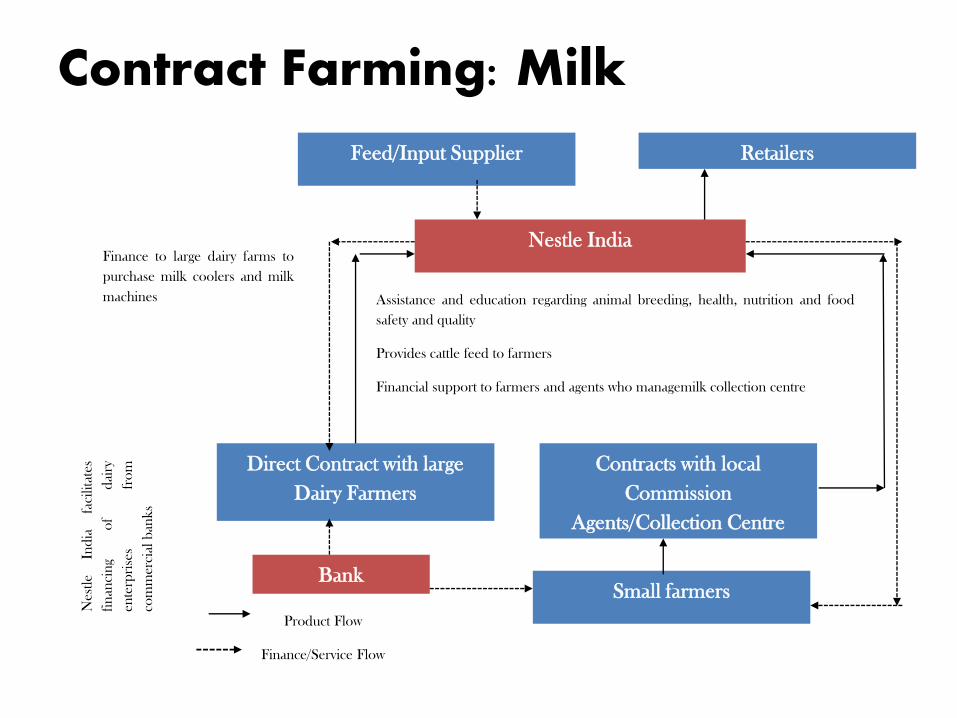

• Vegetables SAFAL (≤ 2ha) = 37%; Gherkin in Karnataka =51% ; All crops in Punjab (≤ 2ha)=15%

•Kenya’s :exporters of fresh fruits and vegetables source their requirement through contracts with small producers

•Malawi: exporters of paparika depend on small farmers

•Madagascar: exporters of french beans from small-scale producers

•Zimbabwe: exporters of flowers and vegetables from large farmers

•Other studies from China, Thailand, Mexico showed a preference for large farmers

International experience

There are not enough large farmers

• Diversified base is essential to reduce supply risk

• Political acceptance or community good will

Small farmers have comparative advantage in labor; lower implicit wage rate; low cost of production;

They are better motivated to respond to product quality, and better farm management

Small farmers are dependent on firms for inputs, services and technology, hence better compliance with terms and conditions

Why contract with small farmers?

Key lessons • Building efficient and inclusive value chains for agricultural commodities

is a big challenge, but is not insurmountable if firms follow innovative and targeted approaches.

• Collective action is essential to overcome scale limitation of smallholders’ participation in value chains, and to reduce transaction costs and risks

• Collective action may not happen in its own, and may require intermediation from the government or its subsidiaries, the non-governmental organizations or the lead firms driving the value chains.

• Mutual trust and incentives are essential for cementing the relationship between buyers and sellers

• For common commodities the prices must be linked with prevailing market prices to avoid side-selling, and breach of contract

• Financing value chain is largely internal to value chain, and limited to production credit in the form of inputs. Long-term and external financing is limited and mainly to large farmers (dairy, orchard, etc.)

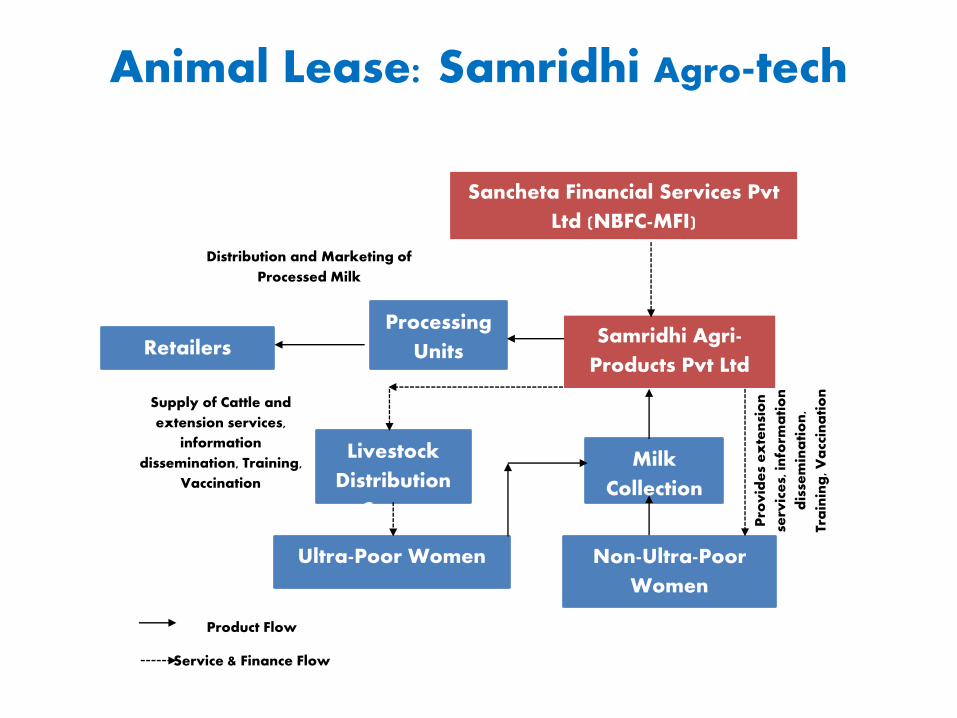

• Microfinance institutions with an agribusiness orientation can act as catalyst in development of efficient and inclusive value chains.

• Risk sharing is important for commodities as contract broilers, (Kesla coop) but are rare for other commodities. While institutional insurance is limited.

Policy Implications Level playing field for private sector participation (regulations, taxes, etc. incentives)

Facilitate growers’ association

Check monopsony and monopoly Reduce transaction costs

Involve smallholders

Provide credit and insurance

Evolve policies for contract farming

Incentives to agro-processing industry

Market fee, taxes on processed foods

Strengthen public infrastructure (road, electricity, communication, etc.)