15

IFRS 4 Phase II Insurance contracts Key Issues for Western Europe and Implementation Considerations Christine Holmes, Partner, The Netherlands

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | verity-peters |

| View: | 215 times |

| Download: | 2 times |

IFRS 4 Phase II Insurance contracts Key Issues for Western Europe andImplementation Considerations

Christine Holmes, Partner, The Netherlands

Key Issues for Western Europe

Presentation titlePage 3 Page 3© 2010 EYGM Limited.

Key accounting impacts of the Exposure DraftMeasurement model

The accounting changes set out in the recently published Exposure Draft will fundamentally change the presentation and measurement of insurance contracts and are a significant departure from Phase I and current local GAAPs

PremiumResidual

margin

Short duration contracts

Unallocated premium reserve

for pre-claims liability

Present value of fulfilment cash flows

Expected future cash

flows

DiscountingRisk

adjustmentInsurance

contract liabilities

Deferred income

Measurement

The new rules introduce a single measurement model that focuses on:

► a current assessment of the amount, timing and uncertainty of future cash flows

► a ‘building block’ approach to measuring insurance liabilities

The ‘building block’ approach generates information about the changes in the insurance liability and its performance during the period

Presentation titlePage 4 Page 4© 2010 EYGM Limited.

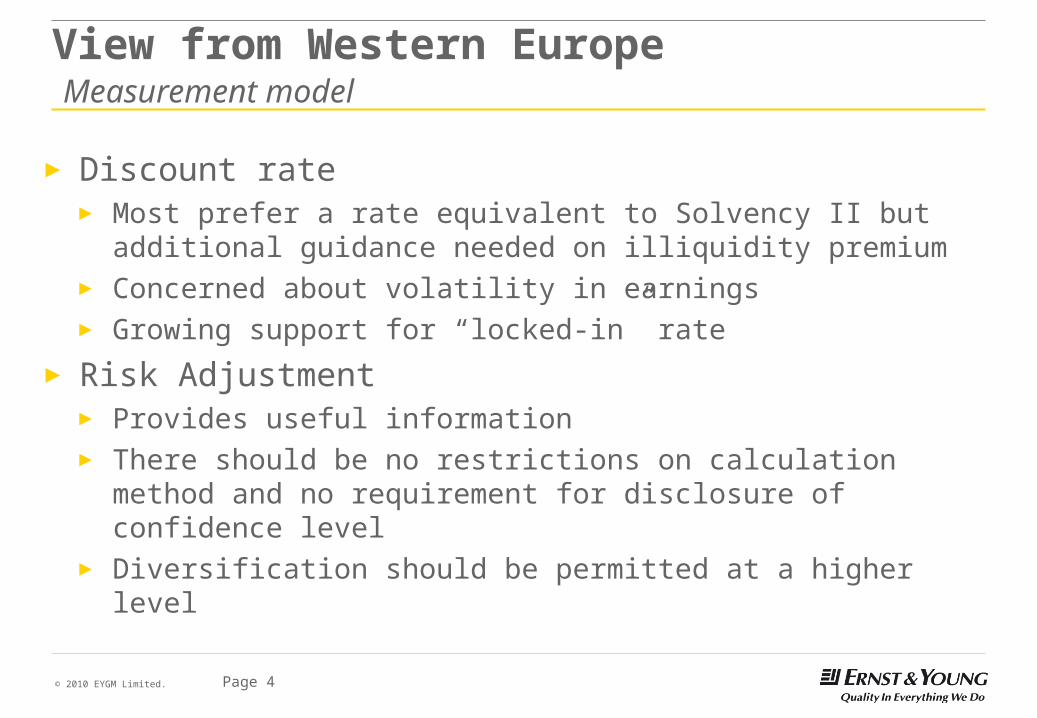

View from Western Europe Measurement model

► Discount rate► Most prefer a rate equivalent to Solvency II but additional

guidance needed on illiquidity premium► Concerned about volatility in earnings► Growing support for “locked-in” rate

► Risk Adjustment► Provides useful information► There should be no restrictions on calculation method and no

requirement for disclosure of confidence level ► Diversification should be permitted at a higher level

Presentation titlePage 5 Page 5© 2010 EYGM Limited.

View from Western Europe Measurement model (continued)

► Residual margin► Should not be locked-in► Should be used as a “absorber”

► Modified approach for Short-Duration contracts► Generally support an alternative approach► Needs further simplification► Should not be mandatory

Presentation titlePage 6 Page 6© 2010 EYGM Limited.

Key accounting impacts of the Exposure DraftOther key proposals

Presentation

Disclosures

► Unbundling is obligatory under certain conditions

► The ED provides specific examples of applicability e.g. Unit Linked

► Margin based approach will require new KPIs such as change in risk margin, release of residual margin and differences between actual and expected cash flows

► Roll forward of liabilities - qualitative and quantitative disclosure of amount, frequency and uncertainty of cashflows (with particular attention to reconciliation between opening and closing balances) and assumptions used in measurement

► Contracts in force prior to the date of transition are treated separately

Unbundling

Transition

Presentation titlePage 7 Page 7© 2010 EYGM Limited.

View from Western Europe Other key proposals

► Unbundling► More guidance needed on “closely related” and principles► Strong disagreement from UK, France and Netherlands –

contracts should be valued as a whole

► Presentation► Prefer traditional premiums and claims presentation► Would support margin approach as a disclosure only

Presentation titlePage 8 Page 8© 2010 EYGM Limited.

View from Western Europe Other key proposals (continued)

► Disclosures ► Proposals lead to increase in volume and need a rethink

► Transition► Generally disagree with no residual margin on transition► Alternative approaches are being investigated

Implementation considerations

Presentation titlePage 10 Page 10© 2010 EYGM Limited.

Main impacts for insurersThe overall view

The impact on business processes and systems will be significant, requiring careful consideration and comprehensive implementation programmes. The main impacts can be analyzed against the following areas:

Governance

ProcessesSystems

and Modelling

Data

People and Organisation

The impetus to understand and address Phase II is made all the more urgent as many insurers are currently investing significantly in upgrading systems and processes to implement Solvency II.

BusinessINSURANCE CONTRACT MEASUREMENT ► Governance frameworks and IFRS specific policies to ensure valuation assumptions are

consistently applied and auditable. Increased focus on data reconciliation and control

INSURANCE CONTRACT PRESENTATION AND DISCLOSURES ► Transparent end to end audit trail for primary financial statements and disclosures with robust

controls over financial reporting. Management information and KPIs which make performance transparent

INSURANCE CONTRACT MEASUREMENT ► Adoption of new procedures and assumptions, design of specific

controls and alignment with Solvency II

INSURANCE CONTRACT PRESENTATION AND DISCLOSURES ► The content and structure of data captured from business units to

support Group statutory and regulatory reporting will change significantly and require major changes to group financial consolidation and reporting systems

INSURANCE CONTRACT MEASUREMENT

Models must be updated and upgraded to introduce flexibility e.g.

► Rules for portfolio definition and availability of models for building block approach. Under the ED a portfolios can be defined as an individual contract, cohort or portfolios of similar risks

► Differences in discount rates, cash flows and risk margins with Solvency II

► Differences in cashflows between Phase II and Solvency II► Stochastic models to model policyholder behaviour

dynamically

INSURANCE CONTRACT PRESENTATION AND DISCLOSURES

► Changes to the primary financial statements and disclosures will impact the general ledger and chart of accounts at group and business unit level

INSURANCE CONTRACT MEASUREMENT

Completeness, depth and granularity of data e.g. ► Specific information at inception and information on

contract boundaries► Information to update portfolios and assumptions at

reporting dates► Information on policyholder behaviour to measure

options and guarantees► Cashflows and assumptions by portfolio and by cohort

within portfolio► Data to support analysis and disclosures

INSURANCE CONTRACT PRESENTATION AND DISCLOSURES

► Investment in data warehousing, data quality, control and management to provide increased granularity to support additional KPIs and disclosures

INSURANCE CONTRACT MEASUREMENT ► Focus on training to develop skills in depth. Retain Solvency II project expertise.

INSURANCE CONTRACT PRESENTATION AND DISCLOSURES ► Allocation of activities and assessment of resources.► Education and awareness training to explain the changes and the new KPIs

Presentation titlePage 11 Page 11© 2010 EYGM Limited.

SOURCE SYSTEMS

Main impacts for insurersFocus on systems, applications and modelling

MAIN IMPACTS

Actuarial Systems

DeterministicModels

Stochastic models

Economic Scenario

Generator

Other Valuation

tools

Accounting / Reporting SystemsGeneral Ledger and

Consolidation Reporting Tools

Policy Admin Systems

Life

CommissionsReinsurance

Claims

Other Systems

….

Investment Management

Systems

Asset Data

External data / third party

data providers

Non Life

Pricing

Data Warehouse

UnderwritingCost allocations

Update group financial consolidation and reporting systems to support changes to the content and structure of data captured from business units

2

Update chart of accounts and identify potential interfaces with systems in order to manage new data

1

Reporting tools and data marts to support analysis and reconciliation of results and preparation of disclosures

3

Solution to support double reporting during the transition period

4

Models capable of projecting cashflows at portfolio level and by cohort within portfolio, including stochastic modelling where required

1

Models able to distinguish appropriate cash flows for use in projections

2

Models able to recalculate liabilities for different cashflows depending on the boundary

5

4Manage changes in assumptions between Solvency II and IFRS 4

3 Determination of residual margin and its amortization

Historical amortization of residual margin per cohort1

Auditability of historical cashflow projections regarding technical, operational and financial assumptions

2

4Structured management of information needed for disclosures

3Ensure governance on rules used to build homogeneous portfolios

Granular data to support modelling of homogeneous portfolios and within portfolio by inception date and duration

1

Cost allocations to provide outputs at portfolio level. Allocation rules updated to exclude non-incremental acquisition costs and overheads from renewal costs

2Avaialbility of market and non-market data at the appropriate level to update assumptions

5

4Claims data for homogeneous risks, particularly in situations where claims handling is outsourced to third parties

3Enrichment of product records for compliance with new principles (e.g. contract boundary, unbundling)

Presentation titlePage 12 Page 12© 2010 EYGM Limited.

Main impacts for insurersBroader business implications

Changes to product features due to changes in profit signaturesProduct design and pricing

Internal and external KPIs / Management Information will need to change to clearly communicate the levers available to manage and control business performance

KPIs and performance measurement

Clear and transparent external communications that help external stakeholders navigate their way through the changes to regulatory and statutory reporting

External stakeholder management

Business planning and forecasting

Investment appraisal

Executive incentive schemes

Business planning and forecasting models will need to be brought into line with the new external reporting basis

Models for evaluating potential investments and acquisitions will need updating to align to the new measurements basis

The earnings based component of executive incentive compensation schemes will also need to be redesigned for the new environment

Allowable acquisition costs and hence residual margin will vary depending on the distribution model and related cost structure

Distribution

Presentation titlePage 13 Page 13© 2010 EYGM Limited.

Managing the projectNext steps

Working back from adoption in 2013/2014 and comparatives and opening balance sheet for 2012 /2013, Insurers need to initiate their programmes now. Next steps should include:

Business effort

Timing

Presentation titlePage 14 Page 14© 2010 EYGM Limited.

Project planning

Identify the potential for alignment between existing Solvency II programmes and IFRS 4 Phase II requirements and exploit the systems and organizational synergies of these parallel projects to save costs

Assess how IFRS 4 Phase II would affect reported numbers along with the impact on systems and operations, including resource levels, required skill-sets and finance function organization

There is a window of opportunity to understand potential synergies with Solvency II and to adapt or leverage existing programmes to manage the change in the most cost effective manner

Identify, as early as possible, the major impacts across the Finance and Business functions, and understand the key challenges

Evaluate whether investing in data management, modeling and reporting systems to automate through a common process the production of local regulatory, Solvency II and IFRS 4 Phase II data and reports is likely to be lower risk and more cost efficient than tactical approaches and workarounds

Assess the resources required including any skills and capability gaps and put in place training and recruitment programs at an early stage

Synergies with other projects

Project implications

Finance and Business functions

Industrialize processes

People

Presentation titlePage 15 Page 15© 2010 EYGM Limited.

IFRS 4 Phase II Gap Analysis and RoadmapOutline project approach

Identify material gaps and the capability which will need to be developed to deliver the requirements of the Exposure Draft

Assess the Exposure Draft requirements vs. current local GAAP to ensure the accounting gaps reflect the organisation, its products and marketsP

urp

os

eS

tep

s

Prioritize conversion activities and set an implementation roadmap including project structure, milestones, deliverables, resources & dependencies on existing programmes

Further analysis and validation of the gaps from an end-to-end process view, to group the underlying issues into logical workstreams and to extend the analysis to include broader business impacts

Accounting Gap Assessment Diagnostic Gap Analysis Roadmap

Synergies with Solvency II / IFRS 9

De

liv

era

ble

s

Accounting, reporting and disclosure impacts

Capability gaps analysed between data, processes, actuarial modeling and systems issues

Validated gap analysis and definition of key activities required to deliver the various changes

Overall implementation plan highlighting synergies with other programmes and resourcing

Accounting

Financial reporting

Actuarial

Business / Governance

Information Technology / Actuarial Models

Project structure and dependencies on other programmes

Project plan and key milestones

Project costs & resources

Ma

in a

rea

s

General Ledger and Consolidation

Tax

Data

Modeling

Processes

Finance systems

End-to-end process owners

People

![HOLMES,GEORGE · Holmes Spear, dec ], and George Holmes, heirs of Oliver Holmes subsequent to his death. I always understood that Oliver Holmes got the lot from Kamehameha 1. Holmes](https://static.documents.pub/doc/80x56/60677df317bc235d9b7d2724/holmesgeorge-holmes-spear-dec-and-george-holmes-heirs-of-oliver-holmes-subsequent.jpg)