29

IHS Petrochemical Outlook Presentation to Indian Petrochem 2014 Tony Potter Vice President Asia Pacific IHS Chemical October 30, 2014

IHS Petrochemical

Outlook

Presentation to Indian Petrochem 2014

Tony Potter

Vice President Asia Pacific

IHS Chemical

October 30, 2014

Best-in-Class Brands

Brought together to form the most comprehensive

source for chemical market research and

expertise in the world – IHS Chemical.

© 2014 IHS

IHS CHEMICAL

IHS Chemical

Agenda: Petrochemical Outlook

• Key Drivers In Base

Chemicals

• Energy at the Extremes

Impacts Cracker Build

• Coproducts: Producers

Adapt to Meet Supply Gap

• Costs and Profitability

Energy &

Feedstocks …make up 60-70% of the costs of chemical

production. Investments seek a

competitive advantage in energy and feedstock costs.

Demand Growth Proximity to

demand growth essential without

distinct cost or technology

advantage. Trade access is also key.

Technology Technology to

enable competitive production costs,

economies of scale, high performance products. First to

market is important.

Chemical Investments Seek A

Sustainable Advantage

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Percentage

5

Asia’s Large Increase in Manufacturing Supports

Base Chemical and Polymer Demand Growth

0

20

40

60

80

100

PE PP PVC Polyester Butadiene Bz PX

China Rest of Asia

Share of World Demand Growth 2008-2018, Percent

China, 1,221

Indonesia, 150

S. Korea, 184

Singapore, 73

Thailand, 120

Malaysia, 65

Japan, 1,047

Taiwan, 149

-2%

-1%

0%

1%

2%

3%

-2% 0% 2% 4% 6% 8% 10% 12%

Bubble Size: Total Consumption for Durable, Non-Durable and Semi-Durable Goods in 2018, Billion of

Population Growth Rate for 2013-2018 (15 to 65 years)

Middle/ Upper Class Growth Rate for 2013-2018 (Household Income >

USD5,000)

Middle Class Growth and Urbanisation

Agenda: Petrochemical Outlook

• Key Drivers In Base

Chemicals

• Energy at the Extremes

Impacts Cracker Build

• Coproducts: Producers

Adapt to Meet Supply Gap

• Costs and Profitability

Feedstock Price Differentials vs. Crude Oil Create opportunities in coal, gas, ethane

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Brent - Nat Gas Brent - Coal Brent-ethane

Price Difference, $MMBtu

Chemical Projects Leveraging Local

Natural Resources Gas/Coal/Oil

Requires

Infrastructure

and policy

definition

Needs

infrastructure

and

government

support Focus is

primarily

LNG

LPG/MTO

investigations early

but promising

Active Projects Reserve potential

Numerous shale

and LPG based

projects.

Potential for MTO

Continued

gas, liquid &

LPG based

investing

Numerous

CTO / MTO

projects

underway

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

-2 0 2 4 6 8 10 12 14

Americas

Europe

MDE/Afr

China

Rest of Asia

Naphtha & Heavier LPG Ethane Coal/ Methanol Others

Incremental Ethylene Capacity 2014-19, Million Metric Tons

A Time of Coal and Ethane

10

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Cracker Feed Stocks Are Getting Lighter, But

the World Still Needs Naphtha

35%

9% 5%

46%

3% 1% 1%

2014: 137.3 MT

39%

7% 4%

40%

3% 1% 3% 3%

2019: 167.1 MT

Ethane Propane Butane Naphtha Gas Oil Methanol to Olefins Coal to Olefins Others

32%

8%

5%

50%

4% 1%

2009: 110.7 MT

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

North America: The Natural Gas Shift

0%

20%

40%

60%

80%

100%

120%

0

2

4

6

8

10

12

14

16

18

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Crude (WTI) Natural Gas Gas as % of Crude

Gas as % of Crude Dollars per MMBtu

Forecast

-6

-4

-2

0

2

4

6

8

10

12

14

Benzene Chlroine Methanol Propylene Ethylene

00 to 10 10 to 20

Million Metric Tons

Chlorine

United States Basic Chemicals Growth 2000/2010 versus 2010/2020

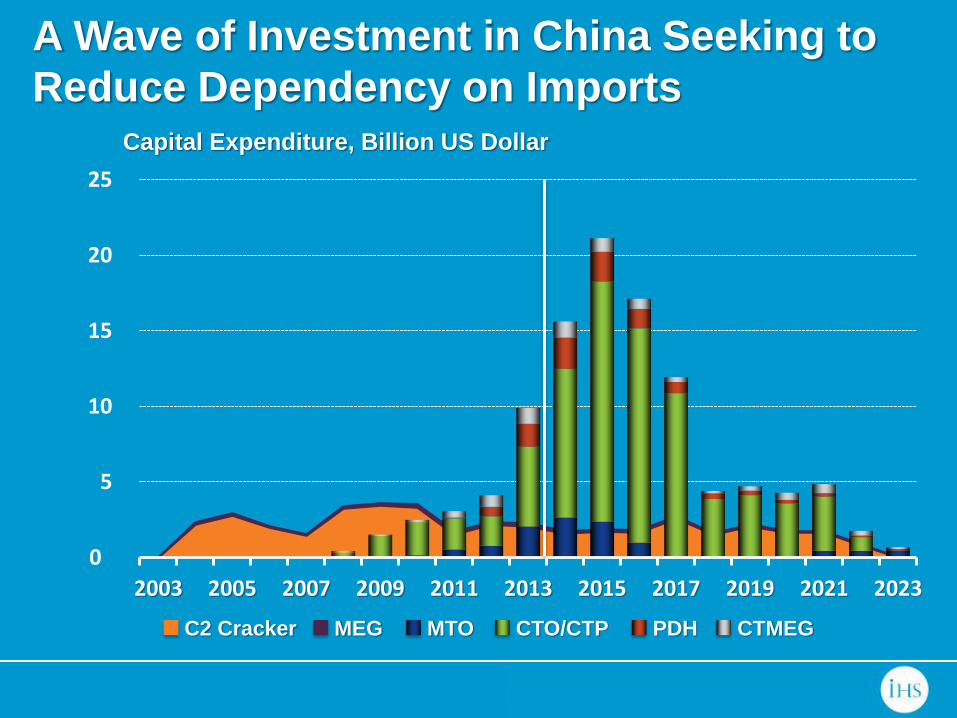

A Wave of Investment in China Seeking to

Reduce Dependency on Imports Capital Expenditure, Billion US Dollar

0

5

10

15

20

25

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

CTMEG CTO/CTP MTO PDH C2 Cracker MEG

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Coal-to-Olefin/ Methanol-to-Olefin Projects (2010 to 2018)

Baotou Shenhua

600 KTA CTO

Inner Mongolia, 2010

Shenhua Ningmei

500 KTA CTP

Ningxia, 2010

Zhongyuan PC

200 KTA CTO

Henan, 2011

Datang International

500 KTA CTP

Inner Mongolia, 2012

Wison (Nanjing)

300 KTA MTO

Nanjing, 2013

Fund Energy

(Ningbo)

600 KTA MTO

Zhejiang, 2013

15

CTO/CTP: 20

MTO/ MTP: 9

CTO/CTP: 4

MTO/ MTP: 2

Completed Projects

Upcoming Projects

China Is Reducing Ethylene Derivative Import

Dependency (But Still Needs Imports)

16

20

30

40

50

60

70

80

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019Net Equivalent Import (Export) Domestic Derivative Equivalent Demand

Self-sufficiency

Million Metric Tons Equivalent Ethylene Percent, %

16

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

08 09 10 11 12 13 14 15 16 17 18Ethylene Vinyls Styrenics Polyethylene

Glycol Others Net Trade

Net Exports

Net Imports

Million Metric Tons, Equivalent Ethylene

India Import Requirement Grows Despite New

Capacity Build

Agenda: Petrochemical Outlook

• Key Drivers In Base

Chemicals

• Energy at the Extremes

Impacts Cracker Build

• Coproducts: Producers

Adapt to Meet Supply Gap

• Costs and Profitability

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Cracker Production of Propylene and

Butadiene Falls Relative to Ethylene

70%

80%

90%

100%

110%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23

P/E B/E

2000 = 100%

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Propylene Producers Adapt, Some More

Aggressively

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

00 02 04 06 08 10 12 14 16 18 20 22

US Propylene Supply

Stm. Crackers FCC Splitters DehydroMetathesis Olefin Cracking Methanol to OlefinsMethanol to Propylene Coal to Olefins Coal to PropyleneHS FCC Others On-Purpose

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

00 02 04 06 08 10 12 14 16 18 20 22

China Propylene Supply

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

-2 0 2 4 6 8 10 12 14 16 18 20

Americas

Europe

MDE/Afr

China

Rest of Asia

Steam Cracker FCC Coal/ Methanol PDH Others

Incremental Propylene Capacity 2013-18, Million Metric Tons

Coal and Propane Drive Propylene

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Upcoming PDH Projects in Northeast Asia

(to 2018)

Bohai Chemical 600 KTA C3

Tianjin

22

1 (China)

2 (South Korea)

12 (China)

2 (South Korea)

Completed Projects

Upcoming Projects

Hyosung 165 KTA C3

Ulsan

Tae Kwang 250 KTA C3

Ulsan

Agenda: Petrochemical Outlook

• Key Drivers In Base

Chemicals

• Energy at the Extremes

Impacts Cracker Build

• Coproducts: Producers

Adapt to Meet Supply Gap

• Costs and Profitability

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Global Ethylene Balance Is Tightening

75

80

85

90

95

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Demand Total Capacity Operating Rates

Million Metric Tons Operating Rates, %

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

But Substantial Over-Build of Propylene Capacity

-4

0

4

8

12

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 23

North America Middle EastChina West EuropeOthers Annual Demand Increase

Million Metric Tons, Propylene

© 2014 IHS, Inc. No portion of this presentation may be reproduced,

reused, or otherwise distributed in any form without prior written consent.

Ethylene Cash Cost Snapshot Regional Comparison: 2013 vs 2023

0

225

450

675

900

1125

1350

1575

WesternCanada

U.S.Ethane

U.S.WeightedAverage

China CTO WestEuropeNaphtha

NortheastAsia

Naphtha

SoutheastAsia

Naphtha

China MTO

U.S. Dollars Per Metric Ton

2013 2023

-$100

-$50

$0

$50

$100

$150

$200

$250

$300

-$100

-$50

$0

$50

$100

$150

$200

$250

$300

85 88 91 94 97 00 03 06 09 12 15 18

$ per ton $ per Ton

Basic Chemicals & Plastics EBIT Comparison

Global Average West Europe Asia North America

Global Profit on the Upswing; Down-Cycle Will

Be Muted for Advantaged Regions

Conclusions

• The petrochemical world has

split between advantaged cost

feedstock “haves” and “have

nots”

• But….the world still needs

investment in naphtha

crackers

• Shale (and Coal) create supply

imbalances in other value

chains

• Profits are on the upswing; but

large regional variations

IHS Petrochemical Outlook

THANK YOU

Tony Potter

Vice President, Asia Pacific

IHS Chemical