F ive Central American countries (Costa Rica, El Salvador, Guatemala, Honduras, and Nicaragua) and the United States signed the Central American Free Trade Agreement (CAFTA) in May 2004. The Dominican Republic (DR) joined the negotiations at the beginning of 2004 and signed the agreement (CAFTA-DR) in August 2004. The agreement will go into effect after the respective legislative bodies have ratified it. 1 CAFTA-DR negotiations were seen as a boost in regional cooperation because Central America negoti- ated as a region and most of the issues were addressed within a single framework. Schedules for market ac- cess, however, were negotiated bilaterally between the United States and the individual Central American countries. In many respects, the agreement is modeled on other bilateral free trade agreements the United States has recently signed, such as those with Chile and Singapore. 2 Though the Central American coun- tries already have strong trade and investment rela- tions with the United States and enjoy preferential ac- cess in the context of the Caribbean Basin Initiative (CBI), CAFTA-DR is substantially more comprehen- sive and changes the form of trade relations from the unilateral preferential arrangement defined under the CBI to a permanent bilateral agreement. 3 For the Cen- tral American countries, the main expected benefits of the agreement are enhanced access to their largest ex- port market, increased foreign direct investment, and institutional strengthening across a range of trade- and investment-related areas. CAFTA-DR’s main objective is to eliminate all tariffs and substantially reduce nontariff barriers between the United States and the Central Ameri- can countries. 4 CAFTA-DR also includes a provi- sion to foster trade flows between the Central American countries. During the past 10 years, the Central American countries have already signifi- cantly decreased tariffs for intraregional trade, and the common external tariff (CET) of the Central American Common Market is generally low and covers about 95 percent of imports to the region (Table 2.1). 5 In addition, these countries have taken various steps to reduce the dispersion of tariffs. Im- mediately after CAFTA-DR enters into force, tar- iffs on all nonagricultural and nontextile exports from Central America to the United States, and tar- iffs on about 80 percent of nonagricultural and non- textile exports from the United States to Central America, will be reduced. Tariffs on other goods will be phased out incrementally over a 5- to 20-year period. Though a significant proportion of exports from the Central American countries have already had tariff-free access to the U.S. mar- ket under the CBI, CAFTA-DR would further re- duce various restrictions and eliminate compliance costs necessary to qualify for preferential access (Griswold and Ikenson, 2004). In the case of agriculture and textiles, CAFTA-DR provides some enhanced market access, but its II Macroeconomic Implications of CAFTA-DR M. Ayhan Kose, Alessandro Rebucci, and Alfred Schipke 7 1 As of June 2005, the congresses of El Salvador, Guatemala, and Honduras have ratified the agreement. In 1998 the Domini- can Republic had already signed a free trade agreement with Cen- tral American countries that went into effect with El Salvador, Guatemala, and Honduras in 2001 and with Costa Rica in 2002. 2 In addition to Israel (1985), NAFTA (1994), and Jordan (2001), the United States has free trade agreements in effect with Chile and Singapore (both 2003) and Australia (2005). The United States has also signed free trade agreements with Bahrain and Morocco and has begun negotiations with several other coun- tries, including Colombia, Ecuador, Oman, Panama, Peru, Thai- land, United Arab Emirates, and the five nations of the Southern African Customs Union. 3 The CBI currently provides 24 beneficiary countries with duty-free access to the U.S. market for most goods. It was first launched in 1983 through the Caribbean Basin Economic Recov- ery Act (CBERA) and expanded in 2000 through the U.S.–Caribbean Basin Trade Partnership Act (CBTPA). 4 It was estimated that nearly 80 percent of Central American products enter the United States duty free, partly because of unilat- eral preference programs, including the CBI and Generalized Sys- tem of Preferences (GSP) (see USTR, 2005a). Hornbeck (2004) provides a detailed discussion about the provisions of CAFTA-DR. Salazar-Xirinachs and Granados (2004) discuss economic and po- litical objectives of the Central American countries in CAFTA. The full text of the agreement is available on the web page of the United States Trade Representative: http://www.ustr.gov/Trade_ Agreements/Bilateral/CAFTA/CAFTA-DR_Final_Texts/ Section_Index.html. 5 Section III provides a detailed discussion of tax and tariff poli- cies of the Central American countries.

Transcript

F ive Central American countries (Costa Rica, ElSalvador, Guatemala, Honduras, and Nicaragua)

and the United States signed the Central AmericanFree Trade Agreement (CAFTA) in May 2004. TheDominican Republic (DR) joined the negotiations atthe beginning of 2004 and signed the agreement(CAFTA-DR) in August 2004. The agreement will gointo effect after the respective legislative bodies haveratified it.1

CAFTA-DR negotiations were seen as a boost inregional cooperation because Central America negoti-ated as a region and most of the issues were addressedwithin a single framework. Schedules for market ac-cess, however, were negotiated bilaterally between theUnited States and the individual Central Americancountries. In many respects, the agreement is modeledon other bilateral free trade agreements the UnitedStates has recently signed, such as those with Chileand Singapore.2 Though the Central American coun-tries already have strong trade and investment rela-tions with the United States and enjoy preferential ac-cess in the context of the Caribbean Basin Initiative(CBI), CAFTA-DR is substantially more comprehen-sive and changes the form of trade relations from theunilateral preferential arrangement defined under theCBI to a permanent bilateral agreement.3 For the Cen-tral American countries, the main expected benefits ofthe agreement are enhanced access to their largest ex-

port market, increased foreign direct investment, andinstitutional strengthening across a range of trade- andinvestment-related areas.

CAFTA-DR’s main objective is to eliminate alltariffs and substantially reduce nontariff barriersbetween the United States and the Central Ameri-can countries.4 CAFTA-DR also includes a provi-sion to foster trade flows between the CentralAmerican countries. During the past 10 years, theCentral American countries have already signifi-cantly decreased tariffs for intraregional trade, andthe common external tariff (CET) of the CentralAmerican Common Market is generally low andcovers about 95 percent of imports to the region(Table 2.1).5 In addition, these countries have takenvarious steps to reduce the dispersion of tariffs. Im-mediately after CAFTA-DR enters into force, tar-iffs on all nonagricultural and nontextile exportsfrom Central America to the United States, and tar-iffs on about 80 percent of nonagricultural and non-textile exports from the United States to CentralAmerica, will be reduced. Tariffs on other goodswill be phased out incrementally over a 5- to 20-year period. Though a significant proportion of exports from the Central American countrieshave already had tariff-free access to the U.S. mar-ket under the CBI, CAFTA-DR would further re-duce various restrictions and eliminate compliancecosts necessary to qualify for preferential access(Griswold and Ikenson, 2004).

In the case of agriculture and textiles, CAFTA-DRprovides some enhanced market access, but its

II Macroeconomic Implications of CAFTA-DR

M. Ayhan Kose, Alessandro Rebucci, and Alfred Schipke

7

1As of June 2005, the congresses of El Salvador, Guatemala,and Honduras have ratified the agreement. In 1998 the Domini-can Republic had already signed a free trade agreement with Cen-tral American countries that went into effect with El Salvador,Guatemala, and Honduras in 2001 and with Costa Rica in 2002.

2In addition to Israel (1985), NAFTA (1994), and Jordan(2001), the United States has free trade agreements in effect withChile and Singapore (both 2003) and Australia (2005). TheUnited States has also signed free trade agreements with Bahrainand Morocco and has begun negotiations with several other coun-tries, including Colombia, Ecuador, Oman, Panama, Peru, Thai-land, United Arab Emirates, and the five nations of the SouthernAfrican Customs Union.

3The CBI currently provides 24 beneficiary countries withduty-free access to the U.S. market for most goods. It was firstlaunched in 1983 through the Caribbean Basin Economic Recov-ery Act (CBERA) and expanded in 2000 through theU.S.–Caribbean Basin Trade Partnership Act (CBTPA).

4It was estimated that nearly 80 percent of Central Americanproducts enter the United States duty free, partly because of unilat-eral preference programs, including the CBI and Generalized Sys-tem of Preferences (GSP) (see USTR, 2005a). Hornbeck (2004)provides a detailed discussion about the provisions of CAFTA-DR.Salazar-Xirinachs and Granados (2004) discuss economic and po-litical objectives of the Central American countries in CAFTA. The full text of the agreement is available on the web page of theUnited States Trade Representative: http://www.ustr.gov/Trade_Agreements/Bilateral/CAFTA/CAFTA-DR_Final_Texts/Section_Index.html.

5Section III provides a detailed discussion of tax and tariff poli-cies of the Central American countries.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

extent is more limited than initially expected. Theagreement envisages transition periods of up to 20years for several agricultural goods, and it maintainsimport tariffs on sensitive items such as sugar andcorn while increasing related import quotas. A widerange of agricultural products, including beef, butter,cheese, milk, and peanuts, continues to be protectedby rather prohibitive tariff rate quotas. Although sev-eral of the Central American countries are majorproducers of sugar, CAFTA-DR does not open theU.S. markets to sugar imports from these countries.The agreement slightly increases their quotas onsugar imports, but the quota tariff on sugar remainsvery high, which is likely to prevent any sizable in-crease in sugar exports from the region.6

For textiles—compared with the current situation,in which Central America enjoys preferences underthe CBI—the main changes will be the permanentnature of those preferences, and some easing of therules of origin. CAFTA-DR also provides more com-prehensive coverage of certain fabrics from Canadaand Mexico and provisions for declaring certain fab-rics in short supply, which would allow sourcingfrom third countries. However, rules-of-origin provi-sions require that exports of textile and apparel prod-ucts of the Central American countries be producedusing local components to qualify for duty-free ac-cess to the U.S. market.7

CAFTA-DR includes various provisions aboutflows of investment and financial services, govern-ment purchases, and protection of intellectual prop-erty rights. CAFTA-DR provides for strict obser-vance of rules on intellectual property rights,investment, government procurement, and competi-tion policies. In addition, it provides for broad ac-cess to several other markets, including services.Labor provisions are slightly tighter than under pre-vious agreements because they offer a platform forexamining the quality of legislation rather thanmerely ensuring its implementation.8 Dispute reso-lution provisions of CAFTA-DR are modeled onNAFTA, promoting cooperative settlement of dis-putes but also providing dispute resolution by panelson both the governmental and the investor-state lev-els. The agreement would create a permanent com-mittee on trade capacity building to help the CentralAmerican countries in trade negotiations.9

Although CAFTA-DR’s provisions ease restric-tions on investment flows, they do not contain bal-ance of payments safeguards for transfers related toa wide range of financial and direct investments. Inparticular, the agreement (like the Singapore andChile free trade agreements) contains a general pro-hibition on the use of capital controls for transac-tions covered by the agreement and restricts the useof capital controls in extremis by omitting a balance

8

Table 2.1.Tariffs in Central America, 1980–99(In percent)

Average Tariffs Tariff Dispersion______________________________ ______________________________1980s 1990s 1999 1980s 1990s 1999

6For the details of sugar provisions in CAFTA-DR and theirimplications for trade flows between the member countries, seeJurenas (2003) and USTR (2005b). Elliott (2005) discusses howthe U.S. agricultural policies, including those protecting the sugarindustry, affect free trade agreements like CAFTA-DR.

7Griswold and Ikenson (2004) argue that these rules-of-originrequirements are restrictive, since the size of the textile industryis very small in the region, implying that the Central Americancountries have to rely on U.S. textile components to gain duty-free access for their exports.

8Elliott (2004) provides a detailed account of the labor marketprovisions of CAFTA-DR and the potential implications for laborstandards in the region. USTR (2005c) argues that the labor pro-visions are comparable to those in other agreements the UnitedStates signed, including with Jordan and Morocco.

9The United States and the other members of CAFTA-DR alsosigned supplemental agreements, including an EnvironmentalCooperation Agreement, to implement environmental provisionsof CAFTA-DR and to coordinate the efforts to strengthen envi-ronmental cooperation in the region.

Implications for Trade and Investment Flows

of payments safeguard exception. Although these re-strictions could help protect U.S. investors from po-tential costs associated with capital controls that oth-erwise could be imposed by Central Americancountries during periods of financial crises, theymay be premature given the still underdeveloped do-mestic financial systems in the region. In particular,they could limit policy options during financialcrises when controls may be useful if implementedon a short-term basis in conjunction with other ap-propriate adjustment and reform measures.10

CAFTA-DR will likely have significant macroeco-nomic implications for Central America. The remain-der of this section examines some of the key macro-economic issues associated with the agreement. Itnext focuses on the impact of CAFTA-DR on tradeflows and foreign direct investment (FDI). The sec-tion then addresses the question of whether the agree-ment is likely to give the region a boost in economicgrowth. Finally, it discusses how increased opennessof trade and greater economic integration with theUnited States will affect countries’ business cycles.

Implications for Trade and Investment Flows

Though similar preferential trade agreements arerelatively recent—therefore providing little empiri-cal evidence—Mexico’s experience under the NorthAmerican Free Trade Agreement (NAFTA) providessome insights on how CAFTA-DR could affect Cen-tral America. Signed by the United States, Canada,and Mexico a decade ago, NAFTA was the firstmajor trade agreement to include a developing coun-try and highly developed economies.11 CAFTA-DRand NAFTA share a number of common characteris-tics, as both agreements envisage comprehensive tar-iff reductions, cover a broad spectrum of sectors, andinclude provisions for dispute settlement.

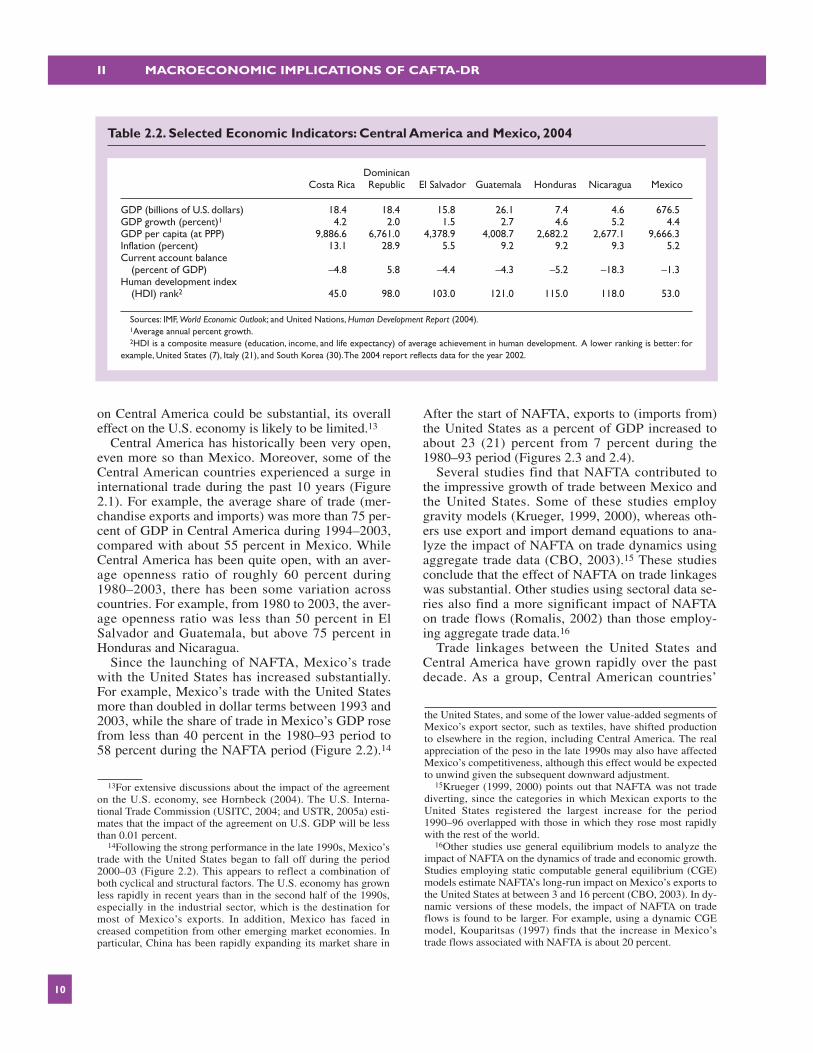

There are, of course, some caveats in analyzingthe potential impact of CAFTA-DR in light of Mex-ico’s NAFTA experience. For example, isolating theeffects of NAFTA on Mexico is complicated giventhe other significant external and policy shocks thathave occurred over the past decade. Also, Mexicodiffers from the Central American countries in that itshares a common border with the United States andhas a larger and more diverse economy and higherper capita GDP than all Central American countriesexcept Costa Rica (Table 2.2). Moreover, there havebeen some differences in the evolution of U.S. traderelations with Mexico and with the Central Ameri-can countries. For example, the Central Americancountries have developed strong trade relations withthe United States through their preferential access tothe U.S. market under the CBI since 1983.12 Beforethe advent of NAFTA, roughly 50 percent of Mex-ico’s exports to the United States were duty free,whereas 80 percent of exports from Central Americahad duty-free access to the U.S. market in 2003.

Nevertheless, Mexico’s experience under NAFTAprovides some guidance in analyzing the potentialimplications of CAFTA-DR because of the commoncharacteristics noted above. The following subsec-tions analyze the evolution of trade, finance, andmacroeconomic data of the CAFTA-DR membersand Mexico covering the period 1980–2003. This pe-riod can be partitioned into three segments: 1980–93represents the pre-NAFTA period; 1994–2003 is theNAFTA period; and 1996–2003 is the period follow-ing Mexico’s peso crisis. This demarcation is usefulbecause it helps isolate the impact of Mexico’s pesocrisis when analyzing Mexico’s experience withNAFTA before and after its implementation.

Dynamics of Trade Flows

The United States is already the most importanttrading partner for Central America. In contrast, andcounting the European Union as a single market,CAFTA-DR was only the United States’ thirteenth-largest export market in 2003. However, within LatinAmerica, Central America is the United States’ sec-ond largest trading partner behind Mexico, as mea-sured by the dollar value of U.S. trade in 2003. Imports from the Central American countries consti-tuted less than 1.4 percent of total U.S. imports in2003. Therefore, although the impact of CAFTA-DR

9

10There has been intensive debate about the relative costs andbenefits of capital controls. Birdsall (2003) examines the implica-tions of limiting the use of capital controls in the context of theU.S.-Chile FTA. Birdsall concludes that this could be viewed as abad precedent for future preferential trade agreements since there isscope for limited market intervention even in financially developedmarkets during periods of crises. Forbes (2004) argues that thecosts of blocking capital market integration are much greater thangenerally realized, because such controls could make it very diffi-cult for small firms to obtain financing for productive investment.Rogoff (2002) provides a summary of various views about the costsand benefits of capital controls. In the case of CAFTA-DR, furtherresearch is necessary to understand the implications of the provi-sions on transfers and capital controls, including an assessment ofadequacy of prudential exemptions in the financial services chapterof the agreement (see Section VI).

11Kose, Meredith, and Towe (2005) provide a review ofNAFTA’s impact on the Mexican economy.

12One could also argue that the macroeconomic implications ofCAFTA-DR should be less extensive than those of NAFTA, sinceCentral American countries have already reacted to NAFTA andundertaken some economic and institutional reforms to be able tocompete with Mexico in the U.S. market during the past 10years.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

on Central America could be substantial, its overalleffect on the U.S. economy is likely to be limited.13

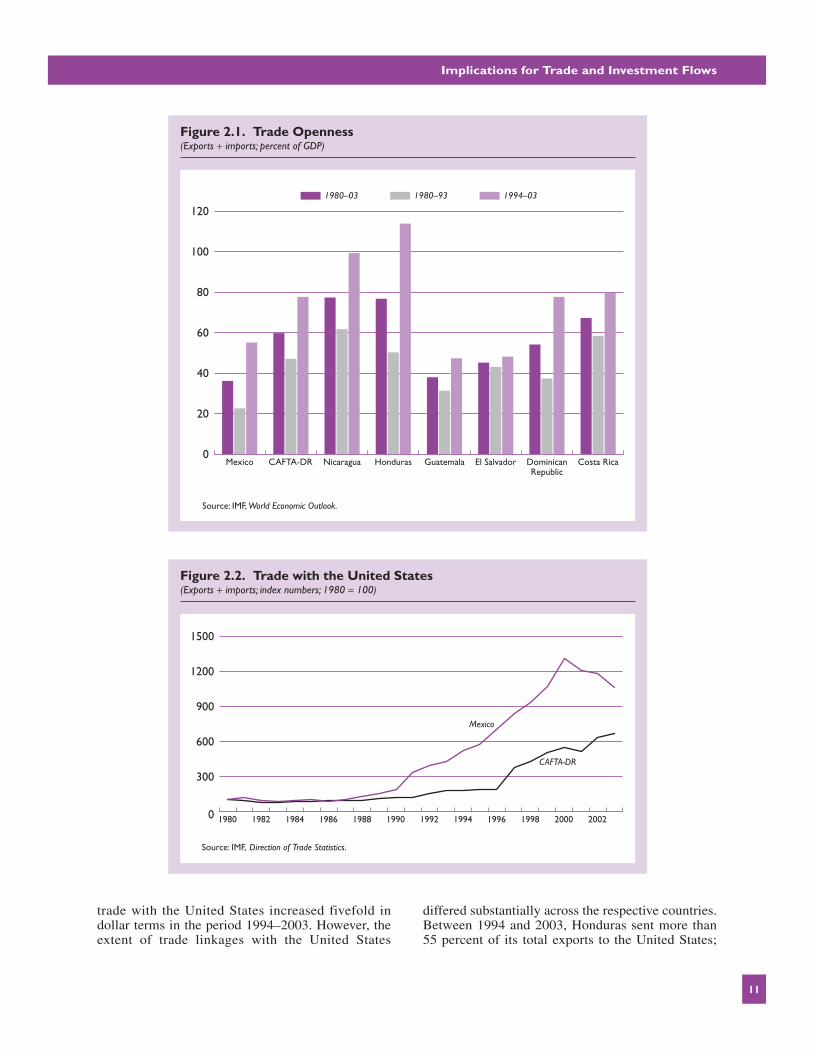

Central America has historically been very open,even more so than Mexico. Moreover, some of theCentral American countries experienced a surge ininternational trade during the past 10 years (Figure2.1). For example, the average share of trade (mer-chandise exports and imports) was more than 75 per-cent of GDP in Central America during 1994–2003,compared with about 55 percent in Mexico. WhileCentral America has been quite open, with an aver-age openness ratio of roughly 60 percent during1980–2003, there has been some variation acrosscountries. For example, from 1980 to 2003, the aver-age openness ratio was less than 50 percent in ElSalvador and Guatemala, but above 75 percent inHonduras and Nicaragua.

Since the launching of NAFTA, Mexico’s tradewith the United States has increased substantially.For example, Mexico’s trade with the United Statesmore than doubled in dollar terms between 1993 and2003, while the share of trade in Mexico’s GDP rosefrom less than 40 percent in the 1980–93 period to58 percent during the NAFTA period (Figure 2.2).14

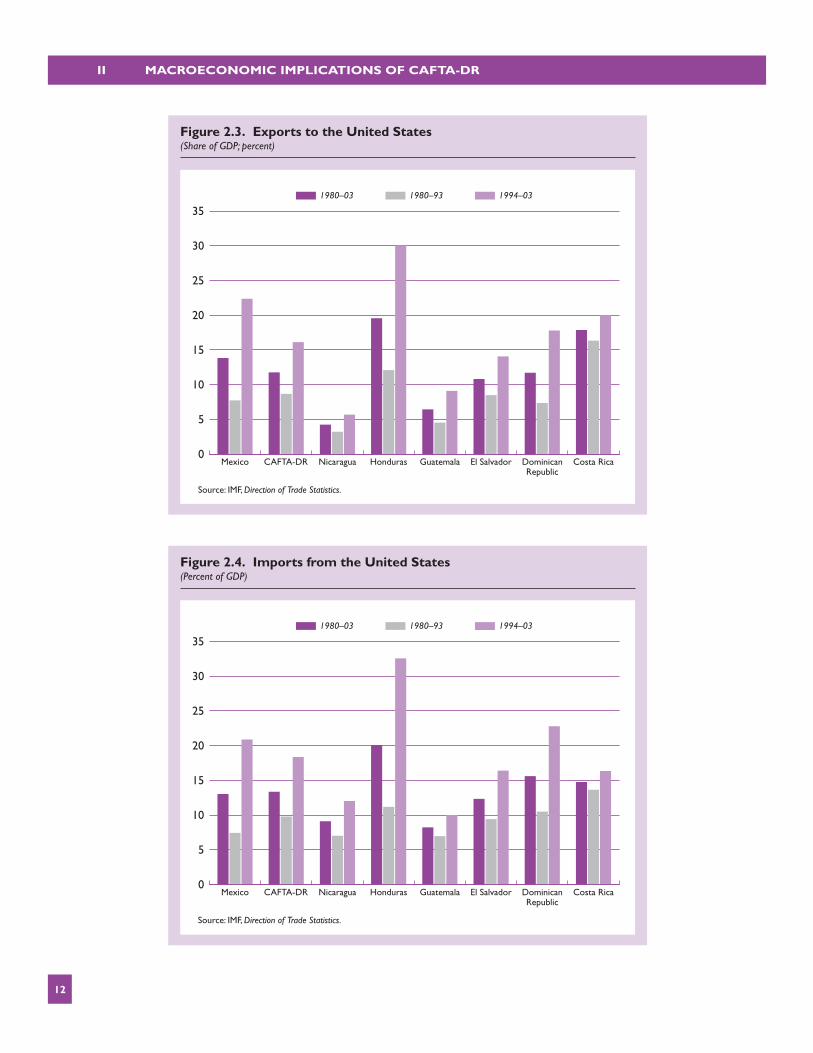

After the start of NAFTA, exports to (imports from)the United States as a percent of GDP increased toabout 23 (21) percent from 7 percent during the1980–93 period (Figures 2.3 and 2.4).

Several studies find that NAFTA contributed tothe impressive growth of trade between Mexico andthe United States. Some of these studies employgravity models (Krueger, 1999, 2000), whereas oth-ers use export and import demand equations to ana-lyze the impact of NAFTA on trade dynamics usingaggregate trade data (CBO, 2003).15 These studiesconclude that the effect of NAFTA on trade linkageswas substantial. Other studies using sectoral data se-ries also find a more significant impact of NAFTAon trade flows (Romalis, 2002) than those employ-ing aggregate trade data.16

Trade linkages between the United States andCentral America have grown rapidly over the pastdecade. As a group, Central American countries’

10

Table 2.2. Selected Economic Indicators: Central America and Mexico, 2004

DominicanCosta Rica Republic El Salvador Guatemala Honduras Nicaragua Mexico

Sources: IMF, World Economic Outlook; and United Nations, Human Development Report (2004).1Average annual percent growth.2HDI is a composite measure (education, income, and life expectancy) of average achievement in human development. A lower ranking is better: for

example, United States (7), Italy (21), and South Korea (30).The 2004 report reflects data for the year 2002.

13For extensive discussions about the impact of the agreementon the U.S. economy, see Hornbeck (2004). The U.S. Interna-tional Trade Commission (USITC, 2004; and USTR, 2005a) esti-mates that the impact of the agreement on U.S. GDP will be lessthan 0.01 percent.

14Following the strong performance in the late 1990s, Mexico’strade with the United States began to fall off during the period2000–03 (Figure 2.2). This appears to reflect a combination ofboth cyclical and structural factors. The U.S. economy has grownless rapidly in recent years than in the second half of the 1990s,especially in the industrial sector, which is the destination formost of Mexico’s exports. In addition, Mexico has faced increased competition from other emerging market economies. Inparticular, China has been rapidly expanding its market share in

the United States, and some of the lower value-added segments ofMexico’s export sector, such as textiles, have shifted productionto elsewhere in the region, including Central America. The realappreciation of the peso in the late 1990s may also have affectedMexico’s competitiveness, although this effect would be expectedto unwind given the subsequent downward adjustment.

15Krueger (1999, 2000) points out that NAFTA was not tradediverting, since the categories in which Mexican exports to theUnited States registered the largest increase for the period1990–96 overlapped with those in which they rose most rapidlywith the rest of the world.

16Other studies use general equilibrium models to analyze theimpact of NAFTA on the dynamics of trade and economic growth.Studies employing static computable general equilibrium (CGE)models estimate NAFTA’s long-run impact on Mexico’s exports tothe United States at between 3 and 16 percent (CBO, 2003). In dy-namic versions of these models, the impact of NAFTA on tradeflows is found to be larger. For example, using a dynamic CGEmodel, Kouparitsas (1997) finds that the increase in Mexico’strade flows associated with NAFTA is about 20 percent.

Implications for Trade and Investment Flows

trade with the United States increased fivefold indollar terms in the period 1994–2003. However, theextent of trade linkages with the United States

differed substantially across the respective countries.Between 1994 and 2003, Honduras sent more than55 percent of its total exports to the United States;

11

0

20

40

60

80

100

120

Costa RicaDominicanRepublic

El SalvadorGuatemalaHondurasNicaraguaCAFTA-DRMexico

1980–03 1980–93 1994–03

Source: IMF, World Economic Outlook.

Figure 2.1. Trade Openness(Exports + imports; percent of GDP)

Figure 2.2. Trade with the United States(Exports + imports; index numbers; 1980 = 100)

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

12

0

10

5

15

20

25

30

35

Costa RicaDominicanRepublic

El SalvadorGuatemalaHondurasNicaraguaCAFTA-DRMexico

1980–03 1980–93 1994–03

Source: IMF, Direction of Trade Statistics.

Figure 2.3. Exports to the United States(Share of GDP; percent)

0

10

5

15

20

25

30

35

Costa RicaDominicanRepublic

El SalvadorGuatemalaHondurasNicaraguaCAFTA-DRMexico

1980–03 1980–93 1994–03

Source: IMF, Direction of Trade Statistics.

Figure 2.4. Imports from the United States(Percent of GDP)

Implications for Trade and Investment Flows

the corresponding figure for Costa Rica was 27 per-cent. The Dominican Republic commanded thelargest share of the region’s exports to the UnitedStates, accounting for more than 25 percent of thedollar value of exports in 2003; Nicaragua’s sharewas the smallest, at less than 5 percent. The region’simports from the United States also increased sub-stantially over the same period and, on average, ac-counted for more than 20 percent of GDP of theCentral American countries during 1994–2003.

CAFTA-DR’s Potential Impact on Trade Flows

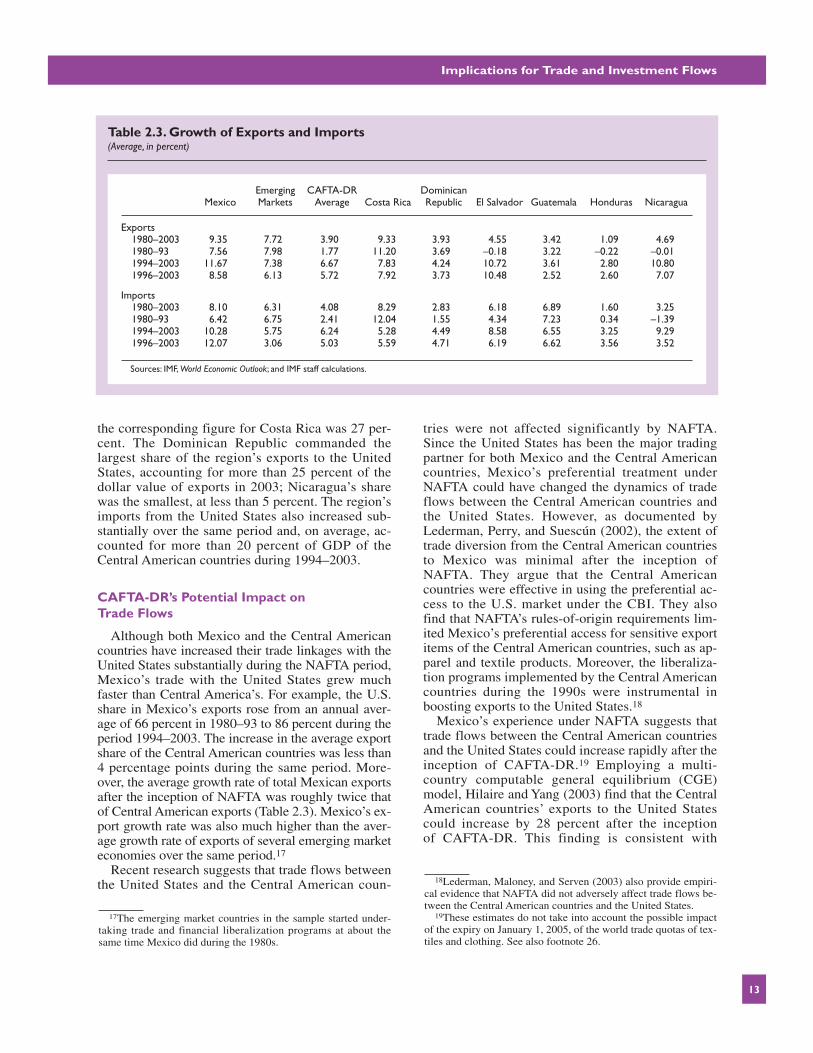

Although both Mexico and the Central Americancountries have increased their trade linkages with theUnited States substantially during the NAFTA period,Mexico’s trade with the United States grew muchfaster than Central America’s. For example, the U.S.share in Mexico’s exports rose from an annual aver-age of 66 percent in 1980–93 to 86 percent during theperiod 1994–2003. The increase in the average exportshare of the Central American countries was less than4 percentage points during the same period. More-over, the average growth rate of total Mexican exportsafter the inception of NAFTA was roughly twice thatof Central American exports (Table 2.3). Mexico’s ex-port growth rate was also much higher than the aver-age growth rate of exports of several emerging marketeconomies over the same period.17

Recent research suggests that trade flows betweenthe United States and the Central American coun-

tries were not affected significantly by NAFTA.Since the United States has been the major tradingpartner for both Mexico and the Central Americancountries, Mexico’s preferential treatment underNAFTA could have changed the dynamics of tradeflows between the Central American countries andthe United States. However, as documented by Lederman, Perry, and Suescún (2002), the extent oftrade diversion from the Central American countriesto Mexico was minimal after the inception ofNAFTA. They argue that the Central Americancountries were effective in using the preferential ac-cess to the U.S. market under the CBI. They alsofind that NAFTA’s rules-of-origin requirements lim-ited Mexico’s preferential access for sensitive exportitems of the Central American countries, such as ap-parel and textile products. Moreover, the liberaliza-tion programs implemented by the Central Americancountries during the 1990s were instrumental inboosting exports to the United States.18

Mexico’s experience under NAFTA suggests thattrade flows between the Central American countriesand the United States could increase rapidly after theinception of CAFTA-DR.19 Employing a multi-country computable general equilibrium (CGE)model, Hilaire and Yang (2003) find that the CentralAmerican countries’ exports to the United Statescould increase by 28 percent after the inception of CAFTA-DR. This finding is consistent with

13

17The emerging market countries in the sample started under-taking trade and financial liberalization programs at about thesame time Mexico did during the 1980s.

18Lederman, Maloney, and Serven (2003) also provide empiri-cal evidence that NAFTA did not adversely affect trade flows be-tween the Central American countries and the United States.

19These estimates do not take into account the possible impactof the expiry on January 1, 2005, of the world trade quotas of tex-tiles and clothing. See also footnote 26.

Table 2.3. Growth of Exports and Imports(Average, in percent)

Emerging CAFTA-DR DominicanMexico Markets Average Costa Rica Republic El Salvador Guatemala Honduras Nicaragua

Sources: IMF, World Economic Outlook; and IMF staff calculations.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

Mexico’s experience under NAFTA, since Mexico’sexports to the United States also rose by more than50 percent in dollar terms in less than two years afterthe inception of NAFTA. They also find that themain sources of the increase in CAFTA-DR’s ex-ports to the United States are textiles, clothing, andprocessed crops.20

CAFTA-DR also could lead to an increase intrade flows through its impact on productivity andspecialization patterns. Because the agreement in-cludes various provisions about the flows of invest-ment, financial services, and intellectual property,these gains could be substantial. Kehoe (2003) ar-gues that static CGE models severely underesti-mated the impact of NAFTA on the volume of re-gional trade, because these models were unable toaccount for much of the increase in sectoral tradeflows. Yet another potential problem associatedwith these models is that they do not capture the ef-fects of productivity changes associated with tradeagreements and they do not allow endogenouschanges in specialization patterns. Thus, staticCGE models, such as those used in Hilaire andYang (2003), might show that the largest increasein trade would take place in those sectors that al-ready have intensive trade linkages, though in fact

the opposite could be true, as in the case ofNAFTA.21 Overall, these findings imply thatCAFTA-DR’s positive effect on trade flows be-tween the Central American countries and theUnited States could be larger than suggested by thestatic CGE models.

CAFTA-DR’s Potential Impact on theComposition of Trade

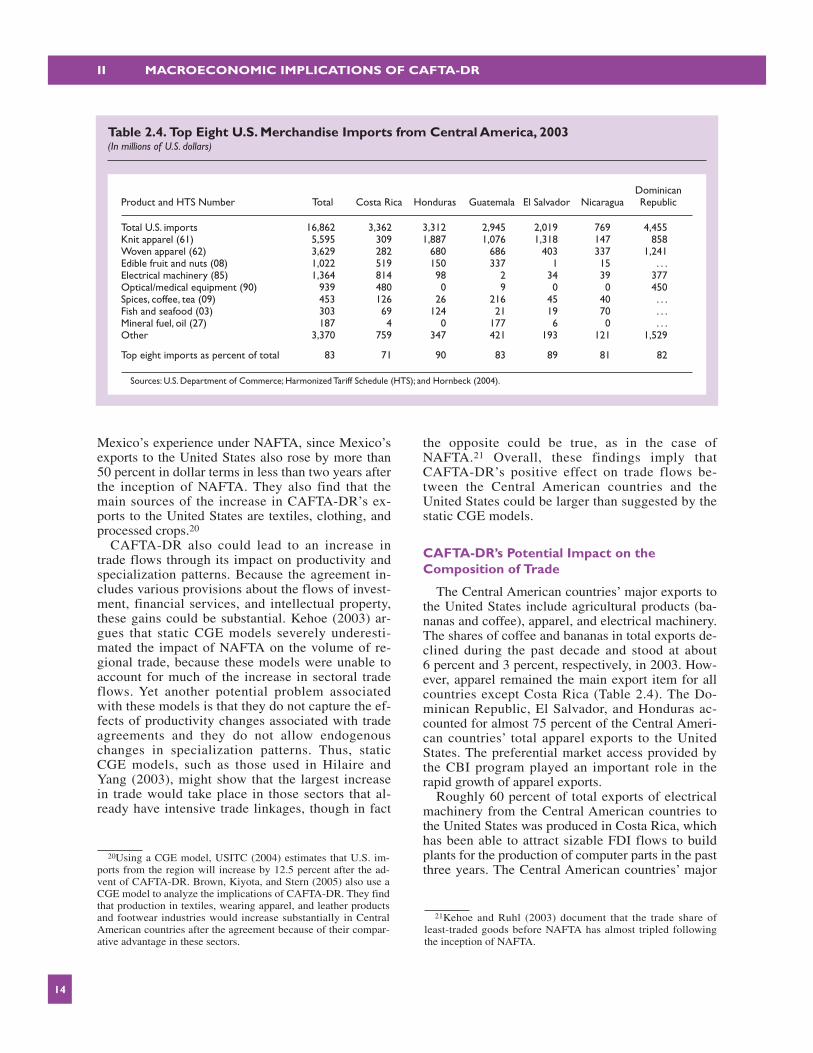

The Central American countries’ major exports tothe United States include agricultural products (ba-nanas and coffee), apparel, and electrical machinery.The shares of coffee and bananas in total exports de-clined during the past decade and stood at about 6 percent and 3 percent, respectively, in 2003. How-ever, apparel remained the main export item for allcountries except Costa Rica (Table 2.4). The Do-minican Republic, El Salvador, and Honduras ac-counted for almost 75 percent of the Central Ameri-can countries’ total apparel exports to the UnitedStates. The preferential market access provided bythe CBI program played an important role in therapid growth of apparel exports.

Roughly 60 percent of total exports of electricalmachinery from the Central American countries tothe United States was produced in Costa Rica, whichhas been able to attract sizable FDI flows to buildplants for the production of computer parts in the pastthree years. The Central American countries’ major

14

20Using a CGE model, USITC (2004) estimates that U.S. im-ports from the region will increase by 12.5 percent after the ad-vent of CAFTA-DR. Brown, Kiyota, and Stern (2005) also use aCGE model to analyze the implications of CAFTA-DR. They findthat production in textiles, wearing apparel, and leather productsand footwear industries would increase substantially in CentralAmerican countries after the agreement because of their compar-ative advantage in these sectors.

Table 2.4. Top Eight U.S. Merchandise Imports from Central America, 2003(In millions of U.S. dollars)

DominicanProduct and HTS Number Total Costa Rica Honduras Guatemala El Salvador Nicaragua Republic

Top eight imports as percent of total 83 71 90 83 89 81 82

Sources: U.S. Department of Commerce; Harmonized Tariff Schedule (HTS); and Hornbeck (2004).

21Kehoe and Ruhl (2003) document that the trade share ofleast-traded goods before NAFTA has almost tripled followingthe inception of NAFTA.

Implications for Trade and Investment Flows

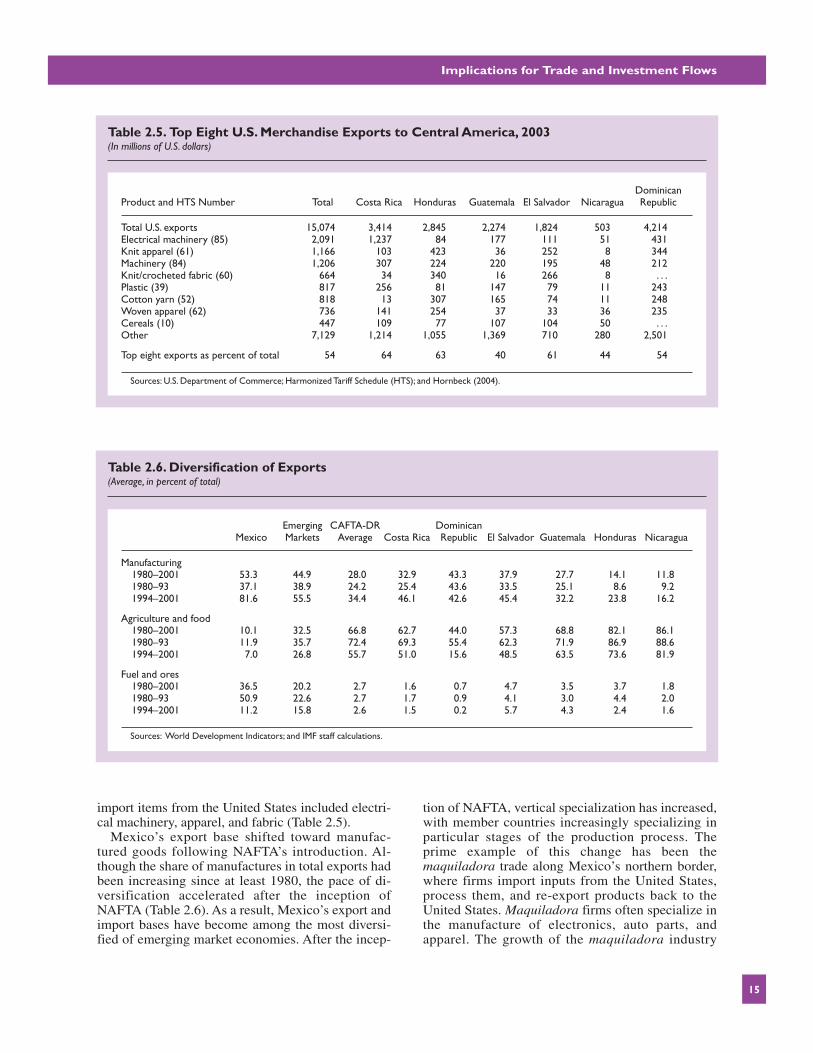

import items from the United States included electri-cal machinery, apparel, and fabric (Table 2.5).

Mexico’s export base shifted toward manufac-tured goods following NAFTA’s introduction. Al-though the share of manufactures in total exports hadbeen increasing since at least 1980, the pace of di-versification accelerated after the inception ofNAFTA (Table 2.6). As a result, Mexico’s export andimport bases have become among the most diversi-fied of emerging market economies. After the incep-

tion of NAFTA, vertical specialization has increased,with member countries increasingly specializing inparticular stages of the production process. Theprime example of this change has been themaquiladora trade along Mexico’s northern border,where firms import inputs from the United States,process them, and re-export products back to theUnited States. Maquiladora firms often specialize inthe manufacture of electronics, auto parts, and apparel. The growth of the maquiladora industry

15

Table 2.5. Top Eight U.S. Merchandise Exports to Central America, 2003(In millions of U.S. dollars)

DominicanProduct and HTS Number Total Costa Rica Honduras Guatemala El Salvador Nicaragua Republic

Sources: World Development Indicators; and IMF staff calculations.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

accelerated during the 1990s, as the average annualgrowth rate of real value added produced by themaquiladora sector was about 10 percent in the pe-riod 1990–2002, over three times the average growthrate of real GDP during the same period (Hanson,2002). Intra-industry trade between Mexico and theUnited States also rose significantly as the share ofintra-industry trade in Mexico’s manufacturing sec-tor rose from 62.5 percent in the period 1988–91 to73.4 percent in 1996–2000 (OECD, 2002). More-over, NAFTA boosted intrafirm trade and resulted ina substantial increase in the variety of productstraded between Mexico and the United States (Hill-berry and McDaniel, 2002).

During the period 1994–2001, the Central Ameri-can countries substantially diversified their tradebases. For example, the share of manufacturing ex-ports rose from less than 25 percent in 1980–93 to ap-proximately 34 percent over the period 1994–2001.Costa Rica, El Salvador, Honduras, and Nicaraguasignificantly increased their manufacturing exports.However, agricultural and food products still ac-counted for almost 60 percent of total exports duringthe period 1994–2001. Moreover, the extent of diver-sification was much lower in the Central Americancountries than in Mexico. During the period1994–2001, the average share of manufactured ex-ports of the Central American economies was lessthan half that of Mexico.

Mexico’s experience under NAFTA suggests thatCAFTA-DR could further accelerate diversificationof Central America’s trade base. There was a majorchange in the nature of goods exported from Mex-ico to the United States as these two countries de-veloped stronger trade linkages during the past twodecades. As discussed above, NAFTA was instru-

mental in the rapid growth of intra-industry andvertical trade between Mexico and the UnitedStates in the past 10 years. Compared with Mexico,the extent of the Central American countries’ intra-industry trade with the United States—exceptCosta Rica’s—has been much smaller. However,the Central American countries have recentlybegun expanding the scope of both vertical andintra-industry trade. For example, most of their im-ports of electrical machinery and apparel from theUnited States have been used as intermediate inputsin the production of other goods that have been re-exported back to the United States.22

Foreign Direct Investment Flows

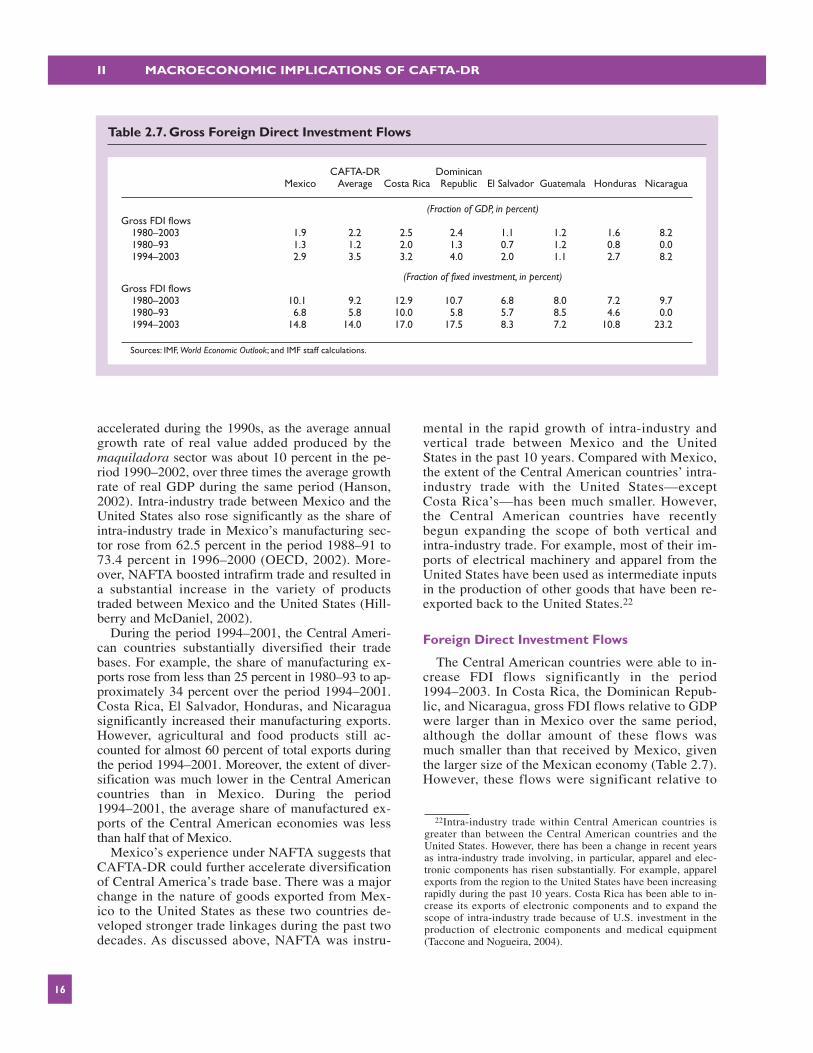

The Central American countries were able to in-crease FDI flows significantly in the period1994–2003. In Costa Rica, the Dominican Repub-lic, and Nicaragua, gross FDI flows relative to GDPwere larger than in Mexico over the same period,although the dollar amount of these flows wasmuch smaller than that received by Mexico, giventhe larger size of the Mexican economy (Table 2.7).However, these flows were significant relative to

16

Table 2.7. Gross Foreign Direct Investment Flows

CAFTA-DR DominicanMexico Average Costa Rica Republic El Salvador Guatemala Honduras Nicaragua

Sources: IMF, World Economic Outlook; and IMF staff calculations.

22Intra-industry trade within Central American countries isgreater than between the Central American countries and theUnited States. However, there has been a change in recent yearsas intra-industry trade involving, in particular, apparel and elec-tronic components has risen substantially. For example, apparelexports from the region to the United States have been increasingrapidly during the past 10 years. Costa Rica has been able to in-crease its exports of electronic components and to expand thescope of intra-industry trade because of U.S. investment in theproduction of electronic components and medical equipment(Taccone and Nogueira, 2004).

Implications for Economic Growth and Welfare

total domestic investment, representing about 14percent of domestic investment on average. TheUnited States is the largest source of FDI flows toeach Central American economy. About one-thirdof FDI flows from the United States went to CostaRica between 1999 and 2002 (Table 2.8), and aboutone-fourth went to the Dominican Republic.

FDI flows between Mexico and its partnersstrengthened after NAFTA. The agreement con-tained various provisions that improved the relativestanding of investors from the partner countries inMexico and expanded the sectors in which theycould operate. These changes helped boost FDIflows to Mexico from US$12 billion during1991–93 to roughly US$54 billion in the period2000–02. The share of FDI flows in domestic grossfixed capital formation (investment) also increasedfrom 6 percent in 1993 to 11 percent in 2002,mainly as a result of inflows from Mexico’sNAFTA partners.

CAFTA-DR is likely to boost FDI flows to theCentral American countries, as NAFTA did in thecase of Mexico. Recent research suggests thatNAFTA membership significantly affected the vol-ume of FDI flows to Mexico. For example, Cuevas,Messmacher, and Werner (2002a) and Waldkirch(2003) show that NAFTA led to a significant in-crease in FDI flows to Mexico. The latter study ar-gues that NAFTA’s impact on FDI flows to Mexicowas the result of increased vertical specialization aswell as the agreement’s effect on Mexico’s commit-ment to liberalization and reform programs. AsNAFTA did, CAFTA-DR could serve as a commit-ment device and encourage FDI flows while induc-ing a change in the nature of trade flows in favor ofvertical trade. CAFTA-DR could also help attract

foreign multinational corporations to the CentralAmerican countries, as Mexico’s NAFTA experi-ence proved (see Blomström and Kokko, 1997).23

CAFTA-DR could, however, encourage subopti-mal policymaking in efforts to encourage FDI in-flows. The individual Central American countriescould be inclined to offer tax incentives to attractFDI flows and by doing so induce a “race to the bot-tom.” To limit this risk, policy coordination might bewarranted (see Section III on taxation and the fiscalimplications of CAFTA-DR).

Implications for Economic Growth and Welfare

How would CAFTA-DR affect the long-rungrowth prospects of Central America? The theoreti-cal impact of regional trade agreements on economicgrowth and welfare is somewhat ambiguous, since itdepends on various factors, including changes intrade volume and terms of trade after the advent ofsuch agreements.24 However, various theoreticalmodels emphasize the importance of trade openness

17

Table 2.8. Foreign Direct Investment Inflows from the United States(In millions of U.S. dollars)

Source: U.S. Department of Commerce, Bureau of Economic Analysis.Note: Data reflect stock of FDI historical-cost basis (Hornbeck, 2004).

23Cuevas, Messmacher, and Werner (2002a) employ panel re-gressions and find that Mexico’s participation in NAFTA led toroughly a 70 percent increase in FDI flows. Waldkirch (2003)concludes that NAFTA induced a 40 percent increase in the vol-ume of FDI flows. Blomström and Kokko (1997) conclude thatforeign multinationals increased their investment in Mexico in re-sponse to NAFTA as well as to the relaxation of various barrierson FDI flows since the mid-1980s.

24Baldwin and Venables (1995) provide a survey of theoreticalstudies on the growth and welfare implications of regional tradeagreements.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

in promoting economic growth. Some of these mod-els focus on static gains, including the gains derivedfrom increased specialization. Others considerknowledge spillovers associated with internationaltrade as an engine of growth (Grossman and Help-man, 1991).

Several empirical studies suggest that trade open-ness has a direct and positive effect on economicgrowth (Sachs and Warner, 1995; Frankel andRomer, 1999; and Dollar and Kraay, 2004). Someother studies focus on the positive effect of increasedtrade linkages on productivity (USITC, 2004) and on

18

Mexico, Volatility

0

2

4

6

8

10

12

14

Impo

rts

Expo

rts

Inves

tmen

t

Consu

mptionGDP

Impo

rts

Expo

rts

Inves

tmen

t

Consu

mptionGDP

Impo

rts

Expo

rts

Inves

tmen

t

Consu

mptionGDP

Impo

rts

Expo

rts

Inves

tmen

t

Consu

mptionGDP

0

2

4

6

8

10

12

14Mexico, Growth Rate Central America, Growth Rate

0

5

10

15

20

25

0

10

5

15

20

25Central America, Volatility

1980–93 1994–03 1996–03

Source: IMF staff calculations.

Figure 2.5. Growth Rate and Volatility of Macroeconomic Aggregates inMexico and Central America(Average; in percent)

Implications for Economic Growth and Welfare

investment growth (Levine and Renelt, 1992; and Baldwin and Seghezza, 1996). Rodrik and Rodriguez (2000), however, present a critical reviewof some of these empirical studies.25

There are various direct and indirect channelsthrough which increased financial flows can enhancegrowth in developing countries. While direct chan-nels include augmentation of domestic savings, re-duction in the cost of capital through better globalallocation of risk, development of the domestic financial sector (Levine, 1996), and transfer of tech-nological know-how, indirect channels are associ-ated with promotion of specialization and induce-ment for better economic policies (Gourinchas andJeanne, 2004).

However, recent empirical research has been un-able to establish a clear link between financial inte-gration and economic growth. Prasad and others(2003) review several empirical studies and con-clude that the majority of the studies find financialintegration has no effect or a mixed effect on eco-nomic growth. For example, Edison and others(2002) employ a regression model that controls forthe possible reverse causality—that is, the possibil-ity that any observed association between financialintegration and growth could result from the mecha-nism that faster-growing economies are also morelikely to liberalize their capital accounts. They con-clude that there is no robust, significant effect of fi-nancial integration on economic growth. However,some other studies (Borenzstein, De Gregorio, andLee, 1998) find that FDI flows (rather than othercapital movements) tend to be positively associatedwith investment and output growth.

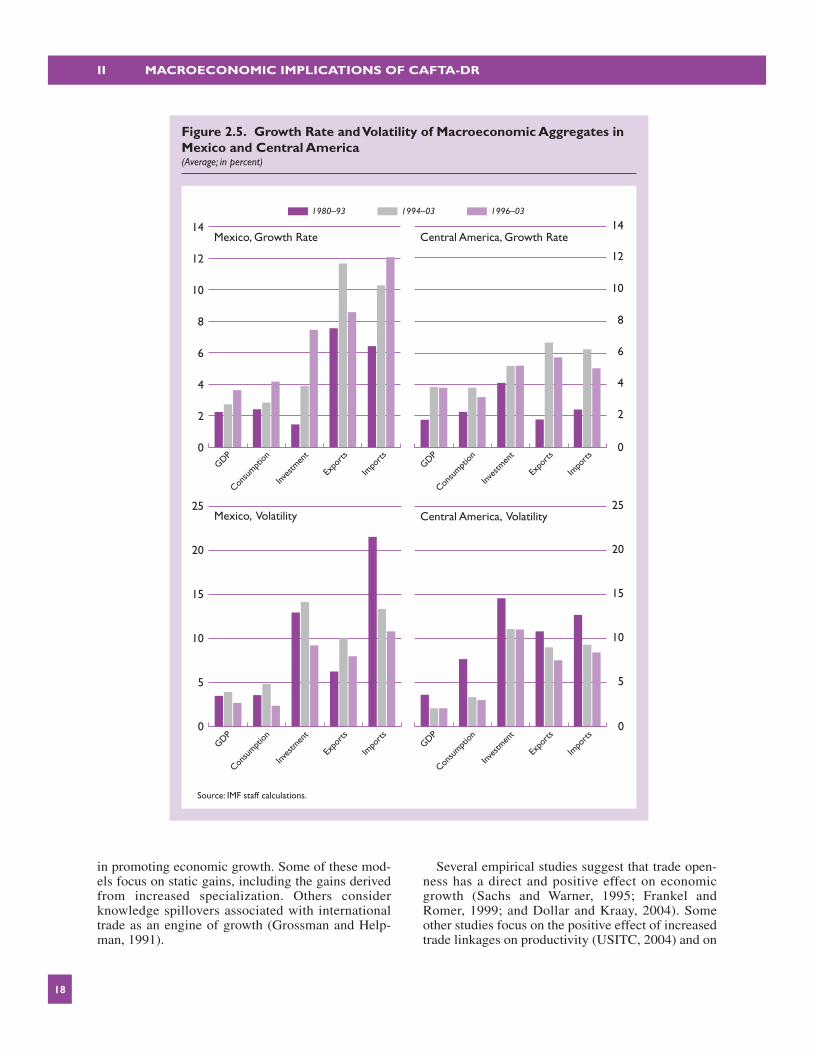

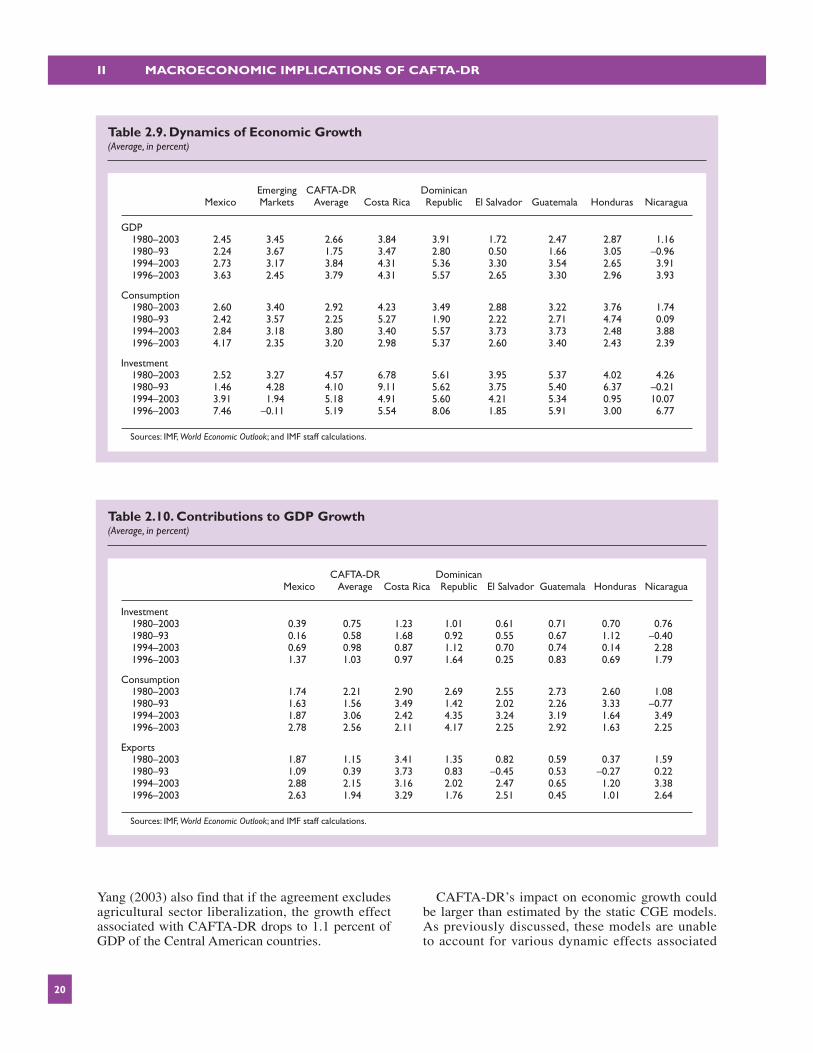

Mexico’s growth performance improved after theinception of NAFTA. Compared with several otheremerging market countries, the Mexican economyperformed well since NAFTA’s implementation and, in particular, after the 1995 crisis (Figure 2.5).Moreover, the average growth rate of investment wasparticularly impressive, as it rose almost eightfoldduring the period 1996–2003 (Table 2.9).

As pointed out in Section I, the average growthrate of the Central American countries increased no-tably during the period 1994–2003. In particular, theaverage growth rate of GDP more than doubled overthis period, with all countries, except Honduras,recording significant increases in their growth rates(Figure 2.5). The average growth rate of investmentalso rose in the Central American countries, but itfell short of the increase in Mexico. Although El Sal-vador and Nicaragua were able to achieve muchhigher rates of investment growth, Costa Rica andHonduras witnessed a significant decline over the1994–2003 period.

Mexico’s experience under NAFTA suggests thatCAFTA-DR could change the dynamics of economicgrowth in the Central American countries. The effectsof exports and investment on growth in Mexico havechanged after NAFTA’s implementation, as their con-tributions to GDP growth have more than doubledfollowing the introduction of the agreement (Table2.10). For example, while the contribution of invest-ment (exports) was about 0.4 (1.1) percentage pointsbefore NAFTA, it went up to 1.4 (2.6) percentagepoints during the period 1996–2003. A similarchange in the roles of investment and exports tookplace in Central America over the period 1994–2003,although their contribution to growth is still lower inthe Central American countries than in Mexico.

CAFTA-DR could generate various growth bene-fits to the Central American countries, as NAFTAdid in the case of Mexico. Hilaire and Yang (2003)use a CGE model to examine the growth benefits ofCAFTA-DR and conclude that GDP of the CentralAmerican countries could increase by as much as 1.5percent as a result of the agreement.26 This finding isin the range of the estimates produced by variousstudies using similar models to analyze the impact ofNAFTA on the Mexican economy.27 Hilaire and

19

25Berg and Krueger (2003), Baldwin (2003), and Winters(2004) provide extensive surveys of the literature on trade andgrowth. Winters (p. F4) concludes that “while there are seriousmethodological challenges and disagreements about the strengthof the evidence, the most plausible conclusion is that liberaliza-tion generally induces a temporary (but possibly long-lived) in-crease in growth.” Harrison and Tang (2004) argue that “whiletrade integration can strengthen an effective growth strategy, itcannot ensure its effectiveness. Other elements are needed, suchas sound macroeconomic management, building trade-related in-frastructure, and trade-related institutions, economy-wide invest-ments in human capital and infrastructure, or building strong in-stitutions.” Brown, Kiyota, and Stern (2005) use a different CGEmodel and estimate that the GNP of Central American countriescould increase by 4.4 percent after the inception of CAFTA-DR.

26Hilaire and Yang use the Global Trade Analysis Project(GTAP) model for their simulations, which assume that the agree-ment is signed by the United States and five Central Americancountries, including Costa Rica, El Salvador, Guatemala, Hon-duras, and Nicaragua. Their findings indicate that the welfare ef-fect of CAFTA-DR on the United States is also positive, althoughit is much smaller than the positive effect on the Central Americancountries. The agreement also increases global welfare as thegains from expanded sales of textiles, clothing, and processedcrops offset potential losses associated with trade diversion. Hilaire and Yang also conduct some alternative simulations involv-ing the global removal of quotas in textiles and clothing alongsidethe CAFTA-DR agreement. These alternatives reduce the growth ofthe Central American countries’ exports to the United States, butCAFTA-DR still leads to a 1.1 percent increase in regional GDP.

27Baldwin and Venables (1995) provide a summary of the stud-ies using CGE models to evaluate the impact of NAFTA. Somerecent empirical studies also establish a positive association be-tween NAFTA membership and Mexico’s growth performance(Arora and Vamvakidis, 2005; CBO, 2003).

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

Yang (2003) also find that if the agreement excludesagricultural sector liberalization, the growth effectassociated with CAFTA-DR drops to 1.1 percent ofGDP of the Central American countries.

CAFTA-DR’s impact on economic growth couldbe larger than estimated by the static CGE models.As previously discussed, these models are unable to account for various dynamic effects associated

20

Table 2.9. Dynamics of Economic Growth(Average, in percent)

Emerging CAFTA-DR DominicanMexico Markets Average Costa Rica Republic El Salvador Guatemala Honduras Nicaragua

Sources: IMF, World Economic Outlook; and IMF staff calculations.

Implications for Economic Growth and Welfare

with accumulation of capital, changes in specializa-tion patterns, and stronger productivity spillovers.Though the growth impact associated with NAFTAis estimated to be about 2 percent in static models, itis more than 3 percent in dynamic models.28

CAFTA-DR has extensive provisions involving ser-vices and investment flows. However, the staticmodels, including the one employed by Hilaire andYang (2003), do not incorporate the effects of suchprovisions, which could lead to potentially largechanges in the flows of services and investment.29

Moreover, Mexico’s experience under NAFTAsuggests that CAFTA-DR could have a positive ef-fect on productivity growth and institutional qualityin Central America. Recent research shows thatNAFTA contributed to total factor productivity inMexico and accelerated economic convergence inthe region. For example, Lopez-Cordova (2002),using plant-level data, finds that NAFTA raised totalfactor productivity by roughly 10 percent in Mexicoover the sample period, partly in response to foreigncapital inflows. Easterly, Fiess, and Lederman(2003) document that the speed of convergence ofproductivity among NAFTA partners acceleratedafter the implementation of NAFTA. Lopez-Cordova(2001) argues that the passage of NAFTA inducedsome institutional changes, among them a revamp-ing of institutions in charge of competition policy,intellectual property protection, and standards.

Increased trade and financial integration associ-ated with CAFTA-DR could reduce the adverse ef-fects of macroeconomic instability (volatility) oneconomic growth. As documented by a growing lit-erature, there is a negative relationship betweenvolatility and growth (Ramey and Ramey, 1995).This implies that policies and exogenous shocks thataffect volatility can also influence growth. Thus,even if volatility is considered intrinsically a second-order issue, its relationship with growth suggeststhat volatility could indirectly have first-order wel-fare implications. Highly volatile macroeconomicfluctuations have been a major impediment to sus-tained growth in Central America. Kose, Prasad, andTerrones (2005a, 2005b) document that increasedtrade and financial integration appear to diminish thenegative impact of volatility on growth. Specifically,in regressions of growth on volatility and other con-

trol variables, they find that the estimated coeffi-cients on interactions between volatility and trade in-tegration are significantly positive. In other words,countries that are more open to trade appear to face aless severe tradeoff between growth and volatility.They also find a similar, although slightly less sig-nificant, result for the interaction of financial inte-gration with volatility.30

The need to move forward with CAFTA-DR be-comes more urgent given the rising competitionfrom Asia, especially from China. Simulations basedon the GTAP model suggest that the first round im-pact on exports and GDP could be sizable.31 Whilethe negative impact could be more moderate—giventhe proximity to the United States and deepeningsupply chain linkages—pressures are likely to rise.The recent decision by the United States to imposecurbs on some categories of Chinese textile exportsto the United States will give Central America somerelief in the short term, allowing the region to imple-ment CAFTA-DR.

The degree to which CAFTA-DR will lead tostrong growth and improve the long-run growth po-tential of the region will depend critically on sup-porting policies. As Mexico’s NAFTA experienceshows, the Central American countries must under-take various structural reforms to sustain the poten-tial benefits associated with CAFTA-DR. AlthoughNAFTA has had a significant and favorable impacton exports and foreign direct investment flows, Mex-ico’s growth performance could have been evenstronger if structural reforms had been pursued moreaggressively. The major lesson from Mexico’s expe-rience is that a trade agreement like CAFTA-DRshould be used to accelerate, rather than postpone,needed structural reform.

In particular, the Central American countries needto employ policies to improve the quality of institu-tions, regulatory bodies, the rule of law, propertyrights, the flexibility of labor markets, and humancapital infrastructure. Gruben (2005) argues thatwhile the Central American countries have been ableto liberalize their trade regimes during the past 10years, they have lagged in undertaking the necessary

21

28Kouparitsas (1997) considers a dynamic general equilibriummodel that captures the impact of NAFTA on investment flows inthe region. He finds that the agreement increases Mexico’ssteady-state level of GDP by 3.3 percent, consumption by 2.5 per-cent, and investment by more than 5 percent.

29More importantly, CAFTA-DR could affect economic growththrough its impact on the country risk premium of the CentralAmerican economies. This was the case in Mexico after the in-ception of NAFTA as documented by Manchester and McKibbin(1995).

30Kose, Prasad, and Terrones (2005a) document that during the1990s, emerging markets had a similar level of output volatility,on average, to other developing economies but experienced muchhigher growth. Their findings indicate that the higher level oftrade openness of emerging markets accounts for about half of theobserved difference of about 2 percentage points in averagegrowth rates between emerging markets and other developingeconomies. In other words, despite experiencing a similar level ofvolatility, emerging markets were able to post higher growth ratesbecause of the greater degree of trade openness.

31The first-round static impact on GDP could range between0.7 percent in the case of Guatemala and 4.7 percent in the case ofHonduras.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

structural reforms to improve various domestic poli-cies, including those pertaining to financial systems,labor markets, protection of property rights, trans-parency, regulatory frameworks, and importance ofthe informal sector.32 CAFTA-DR has the potential toproduce much larger benefits for the countries in theregion if the agreement is used effectively as an an-chor to implement the necessary policy reforms (seeSalazar-Xirinachs and Granados, 2004).

There are some concerns about the potential ef-fects of CAFTA-DR on fiscal balances in the region.An immediate concern for the Central Americaneconomies is the potential impact of CAFTA-DR ontheir fiscal balances. Since a significant percentageof the Central American economies’ imports issourced from the United States, CAFTA-DR mightlead to a fall in customs revenue and deterioration ofthe countries’ fiscal positions. These issues are dis-cussed in detail in Section III. Another concern is as-sociated with the potential impact of the agreementon poverty, which is discussed in the following.

Could CAFTA-DR Help ReducePoverty in the Region?

Free trade agreements, like CAFTA-DR, couldhave distributional implications involving various in-come groups. In particular, some argue that free tradeagreements could have an adverse impact on the poor-est segments of the population since these agreementscould compress their employment opportunities andwages (see Aisbett, 2005). Moreover, they claim thatthese agreements could decrease government spend-ing on the poor because of their potentially negativeeffects on fiscal revenues. The following summarizesthe main issues about the potential impact of CAFTA-DR on poverty in the region in light of recent empiri-cal and theoretical studies.

Liberalization and Poverty: What Do We Know?

In theory, there are several channels throughwhich increased trade and financial flows could helpreduce poverty. As discussed earlier in the section,some of these channels are related to growth-enhancing effects of increased trade and financial

flows. For example, augmentation of domestic sav-ings, reduction in the cost of capital, increase in pro-ductivity through transfer of technological know-how, and stimulation of domestic financial sectordevelopment could all provide direct growth bene-fits, which in turn help reduce poverty (see Agénor,2002; Easterly, 2005, and Goldberg and Pavcnik,2005). Trade liberalization could also translate into areduction in the prices of goods consumed by poorhouseholds. Moreover, increased trade and financialflows could help reduce macroeconomic volatility,which also could have beneficial effects for the poor(Aizenman and Pinto, 2005).

This is supported through some recent empiricalstudies.33 For example, research by Dollar andKraay (2002, 2003) suggests that increased tradeflows are associated with higher economic growth.34

Kraay (2004) provides strong evidence for the im-portance of economic growth in poverty reduction ashis analysis shows that most of the variation inchanges in poverty during the 1980s and 1990s is ex-plained by growth in average income in developingcountries.35 Agénor (2002) finds that there is a non-

22

32Gruben (2005) compares the extent of trade openness with anindex of market orientation that measures the degree of marketopenness in eight nontrade domestic policy categories: fiscal pol-icy and fiscal balance, government intervention in the economy,monetary policy (with its inflationary implications), banking pol-icy, flexibility of wages and prices, protection of property rights,transparency and simplicity of regulation, and importance of theinformal sector versus the formal taxpaying sector.

33Since it is difficult to measure poverty and isolate the impactof trade and financial flows on poverty from various other factors,recent studies do not reach an unambiguous conclusion on thisissue. While Easterly (2005) documents that neither financial nortrade flows have any significant impact on poverty, Harrison(2005, p. 15) notes that “there is certainly no evidence in the ag-gregate data that trade reforms are bad for the poor.” Winters,McCulloch, and McKay (2004, p. 105) also argue that the empiri-cal evidence often suggests that trade liberalization helps reducepoverty in the long run and note that “it lends no support to the po-sition that trade liberalization generally has an adverse impact.”

34Although there has been an intensive debate about the poten-tially adverse impact of increased trade and financial flows asso-ciated with globalization on income inequality, there is no clearempirical evidence that globalization has fostered a sharp rise inworldwide inequality. Several recent studies focus on the impactof globalization on income inequality across countries, but thesestudies have yet to provide a conclusive answer. For example,globalization could accentuate the already substantial inequalityof national incomes and, in particular, lead to stagnation of in-comes and living standards in countries that do not participate inthis process. Consistent with this view, Quah (1997) has docu-mented that there is evidence in cross-country data of a “twinpeaks” phenomenon whereby per capita incomes converge withineach of two groups of countries (advanced countries and globaliz-ers) while average incomes continue to diverge across these twogroups of countries. In other words, advanced countries and glob-alizers converge in terms of per capita incomes and so do non-globalizers, but these two groups diverge from each other in termsof their average incomes. Sala-i-Martin (2002), on the other hand,argues that a more careful analysis, using individuals rather thancountries as the units of analysis, shows that global inequality hasdeclined during the recent wave of globalization.

35Some researchers argue that there are severe data and measure-ment problems involving poverty series and suggest alternativetests to analyze the impact of trade liberalization. For example, Weiand Wu (2002) find that tariff reductions could lead to a significantincrease in life expectancy and reduction in infant mortality.

Could CAFTA-DR Help Reduce Poverty in the Region?

linear relationship between increased trade and fi-nancial flows and poverty. His empirical results indi-cate that while these flows could reduce poverty incountries that have a higher degree of integrationwith the global economy, they could have an adverseimpact on the income levels of the poor in countrieswith a lower degree of integration.36

Mexico’s experience during the 1990s also sug-gests that increased trade and financial flows couldbe beneficial to the poor. For example, while Hanson(2005) documents that poverty increased in Mexicoduring the 1990s, in part owing to the 1995 peso cri-sis, income in states that were more open to tradeand financial flows increased relative to those thatwere less open. Moreover, the increase in povertywas only marginal in states that were more exposedto trade and financial flows while it was much higherin those with limited integration with the globaleconomy. Some other country case studies, includ-ing those on China, India, and Poland, also suggestthat trade liberalization could have poverty alleviat-ing effects (Harrison, 2005).

Some studies emphasize the importance of com-plementary policies to help increase the benefits oftrade and financial integration for the poor. In partic-ular, policies encouraging labor mobility, improvingaccess to credit and technical know-how, and estab-lishing social safety nets seem to increase the bene-fits of increased integration for the poor. Trade liber-alization could lead to contraction in some previouslyprotected industries. Policies that could help workersmove from such sectors to sectors that are expandingcould diminish the adverse effects of trade liberaliza-tion on the poor in the short run while also contribut-ing to poverty reduction in the long run.

Poverty in Central America and CAFTA-DR

Poverty, as pointed out in Section I, is a majorproblem in some Central American countries (exceptCosta Rica). The poverty rate is about 80 percent inHonduras, and about 50 percent in El Salvador,Guatemala, and Nicaragua. Heavy dependence onagriculture appears to accentuate the poverty prob-lem in some Central American countries. For exam-ple, agricultural production accounts for roughly 25percent of GDP in Guatemala and more than 30 per-cent in Nicaragua.

Some argue that CAFTA-DR could have a nega-tive impact on the poor in the region. They note thatby eliminating tariffs on agricultural goods, theagreement opens the small markets of CentralAmerican economies to relatively cheaper agricul-tural exports from the United States (see Oxfam,2004). They suggest that severe dislocation prob-lems could arise since workers in the agriculturalsector, especially poor subsistence farmers, couldlose their jobs. They also point out that this couldfurther exacerbate the poverty problem in the re-gion, with consequences for the dynamics of in-come distribution.

To provide the necessary relief for the vulnerablesegments of the population, the CAFTA-DR agree-ment includes prolonged tariff phase-out and safe-guard schedules to all countries with sensitive agri-cultural products.37 For example, tariffs and quotason various agricultural imports from the UnitedStates, including pork, beef, poultry, rice, and yellowcorn, will be phased out over a 15-year period. Riceand dairy products are subject to longer transitionperiods (18 to 20 years). All agricultural trade wouldeventually become duty free except for sugar im-ported by the United States, fresh potatoes andonions imported by Costa Rica, and white corn im-ported by the other Central American countries.38

Moreover, CAFTA-DR could be beneficial to thepoor in the region by improving growth prospectswhile contributing macroeconomic stability. Sus-tained economic growth appears to be highly corre-lated with poverty reduction, and CAFTA-DR hasthe potential to increase growth in the region. In ad-dition, as discussed later in section, CAFTA-DRcould reduce macroeconomic volatility, which has asignificantly negative and causal impact on poverty(Laursen and Mahajan, 2005).

Complementary policies should be in place tomaximize the benefits of CAFTA-DR for the poor.In particular, policies are needed to strengthen socialsafety nets and help poorer households take advan-tage of the benefits of CAFTA-DR. Since their de-pendence on agriculture varies, the Central Ameri-can countries could utilize specific policies to ease

23

36Agénor (2002) uses a weighted average of trade and financialopenness indicators as a measure of economic integration. Thenonlinearity stems from the fact that trade and financial integra-tion have a sizable impact on the quality of institutions only be-yond a certain level of trade, and financial integration and institu-tions (including an efficient social safety net) play a major role inchanneling the beneficial effects of globalization to the poor andshielding them from its costs.

37Tariffs on more than half of U.S. agricultural exports wouldbe eliminated immediately but the rest are subject to phaseout pe-riods of up to 20 years. For some agricultural products, changesin tariff schedules would be effective only after 7–12 years.

38Mason (2005) documents the effects of lifting tariffs on sen-sitive agricultural products on the poor in Nicaragua, Guatemala,and El Salvador using a net consumer-net producer approach,which helps isolate the first-order effects of such policy changeson welfare. His findings indicate that reduction of barriers couldlead to welfare gains for a significant majority of households inthese countries because of the reduction in prices, while produc-ers of the sensitive agricultural products could experience welfarelosses.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

the transition process of workers in the agriculturalsector to export-oriented manufacturing and servicesindustries. In addition to providing the necessary in-frastructure for labor mobility across sectors,improving access to credit, including microcredit,could also help in this transition.

CAFTA-DR’s Potential Impact onMacroeconomic Volatility and the Co-Movement of Business Cycles

Increased trade and financial flows between theCentral American economies and the United Statesas a result of CAFTA-DR could affect macroeco-nomic volatility and co-movement of business cyclesin the region. Though the Central Americaneconomies have been successful in regaining macro-economic stability over the past decade, they havecontinued to face substantial shocks. Against thisbackground, the following analyzes how the natureof business cycle fluctuations in the region mightchange after the inception of CAFTA-DR.

Macroeconomic Volatility

The theoretical impact of increased trade and fi-nancial flows on output volatility depends on a num-ber of factors, including the nature of financial flows,patterns of specialization, and sources of shocks. Forexample, increased trade openness, if associated withfurther interindustry specialization across countriesand if industry-specific shocks are important in dri-ving business cycles, could lead to an increase in out-put volatility. However, if increased trade is associ-ated with increased intra-industry specializationacross countries, which leads to a larger volume ofintermediate inputs trade, then the volatility of outputcould decline. In addition, economic theory suggeststhat increased access to international financial mar-kets should dampen the volatility of consumptionwhile inducing an increase in investment volatility(Kose, Prasad, and Terrones, 2003a).

Recent empirical studies are unable to establish aclear link between stronger economic linkages andmacroeconomic volatility. Although some of thesestudies find no significant relationship between the in-creased degree of economic interdependence and do-mestic macroeconomic volatility (Buch, Dopke, andPierdzioch, 2005), others find that an increase in thedegree of trade openness leads to higher outputvolatility, especially in developing countries (Easterly,Islam, and Stiglitz, 2001). Kose, Prasad, and Terrones(2003a) find that while trade openness increases thevolatility of output, income, and consumption inemerging market economies, it reduces the relative

volatility of consumption to output, implying that itimproves the consumption risk–sharing possibilities.They also document that increased financial integra-tion is associated with rising relative volatility of con-sumption, but only up to a certain threshold.

Macroeconomic volatility declined in Mexico afterthe inception of NAFTA. This can be seen in the uni-form decline in the variance of several macroeco-nomic aggregates between the pre-NAFTA period(1980–93) and the post-crisis period (1996–2003)(Figure 2.5).39 In particular, output volatility de-creased by 20 percent and investment volatility fellby more than 40 percent in the latter period. Consis-tent with theoretical predictions, increased trade andfinancial linkages also led to a reduction in thevolatility of consumption in Mexico. In addition,consumption became slightly less volatile than out-put during the 1996–2003 period. This, along withthe increased cross-country consumption correlations(documented below), suggests that Mexico becamebetter able to share macroeconomic risk with theUnited States through increased trade and financiallinkages.

The decreased volatility of the Mexican economyduring the past 10 years could be the result of severalfactors, including, in particular, NAFTA and the pol-icy regime changes that Mexico enacted. However,the decrease in volatility could be the result ofNAFTA’s effect on intra-industry and vertical traderather than the result of increased stability of domes-tic macroeconomic policies stemming from the im-plementation of sound monetary and fiscal policiesover the period 1996–2001 (Cuevas, Messmacher,and Werner, 2002a). Both the theory reviewed earlierand the available evidence of the increased impor-tance of regional and external shocks in driving theMexican business cycles (Kose, Meredith, andTowe, 2005) suggest that this might be the case.

Reflecting in part the success of pursuing soundmacroeconomic policies, the volatility of macroeco-nomic variables decreased in the Central Americaeconomies during the past 10 years (Figure 2.5). Inparticular, there was a significant decrease in thevolatility of output fluctuations in El Salvador,Guatemala, and Nicaragua. Both consumption andinvestment volatility declined in Central Americaduring the period 1996–2003. Although volatility ofconsumption in Nicaragua and the Dominican Re-public declined from 18 percent to less than 7 per-cent, it was still high in these two countries relativeto the rest of Central America. In all countries except

24

39Table 2.A1 in Appendix II presents the volatility of macro-economic aggregates in detail. Volatility is measured as the stan-dard deviation of the annual growth rate. Since only a limitednumber of annual date series are available, standard errors associ-ated with volatility statistics are not reported.

Potential Impact on Macroeconomic Volatility and the Co-Movement of Business Cycles

Costa Rica, there was a moderation in the size ofbusiness cycle fluctuations in exports and imports.

Output volatility in Central America was lowerthan that of Mexico during the period 1994–2003.However, consumption and investment in thosecountries exhibited higher volatility than in Mexicoover the same period. In addition, during the period1996–2003, consumption fluctuations were morevolatile than those of output in Central America,whereas the volatility of consumption was slightlybelow that of output in Mexico.

The NAFTA experience suggests that CAFTA-DRcould help reduce output volatility in Central Amer-ica. CAFTA-DR could further reduce volatility byaccelerating the diversification of the export baseand by fostering intra-industry and vertical tradelinkages with the United States. After the inceptionof CAFTA-DR, shocks originating in the UnitedStates could play a more prominent role in CentralAmerica, as documented below. Given the stabilityof the U.S. economy, however, these shocks are ex-pected to be relatively less volatile than shocks spe-cific to Central America, which on balance would re-sult in a more stable macroeconomic environment.Moreover, CAFTA-DR may have a positive effect onthe quality of institutions and country risk premium,which in turn should further reduce volatility.

In the same vein, CAFTA-DR could play a majorrole in reducing consumption and investment volatil-ity in Central America. NAFTA appears to havehelped Mexico achieve relatively more stable con-sumption and investment dynamics through its im-pact on FDI flows. CAFTA-DR could be similarlyinstrumental in increasing the volume of FDI flowsto the region, since it would signal a long-term com-mitment to implementing trade-promoting policiesand thus help reduce the amplitude of investmentfluctuations. In addition, CAFTA-DR could expandthe scope of international risk-sharing opportunities,which in turn could help diminish the variation inconsumption fluctuations.

CAFTA-DR could result in welfare gains in Cen-tral America by helping to expand the set of avail-able financial instruments for international risk-sharing purposes. These instruments would allowdomestic residents and firms to use international fi-nancial markets for consumption smoothing, result-ing in significant welfare benefits. Recent studiesdocument that the benefits from international risksharing tend to be large when a country’s consump-tion growth is volatile, positively correlated with do-mestic output growth, and not highly correlated withworld consumption.

Some of the Central American economies facehighly volatile consumption fluctuations, implyingthat the benefits to CAFTA-DR and consequent re-ductions in consumption volatility could be large.

Although these benefits would, on average, have thesame effect as about a 5 percent permanent increasein the level of per capita consumption, they differsignificantly across the Central American economies(Table 2.11).40 The gains are generally inversely pro-portional to the volatility of consumption. To illus-trate, Nicaragua, the most volatile Central Americaneconomy, stands to gain close to 15 percent, whereasthe gain for the least volatile economy, Guatemala, isless than !/2 percent.41

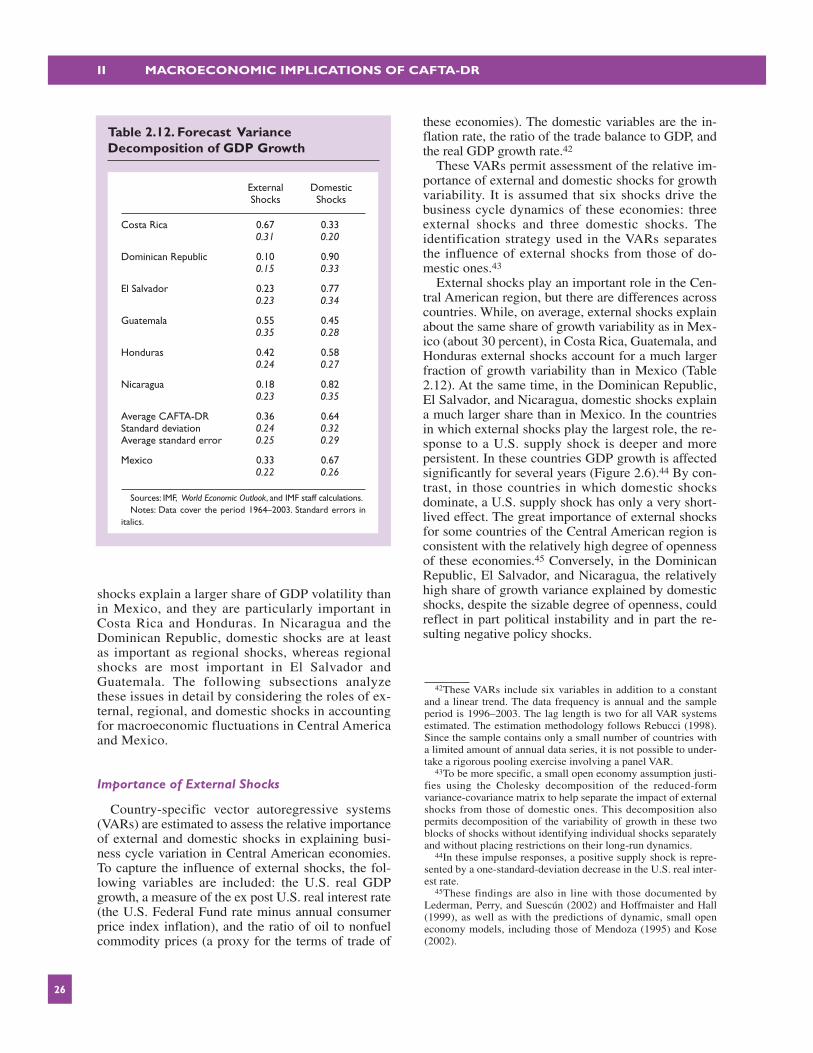

Sources of Business Cycles in Central America

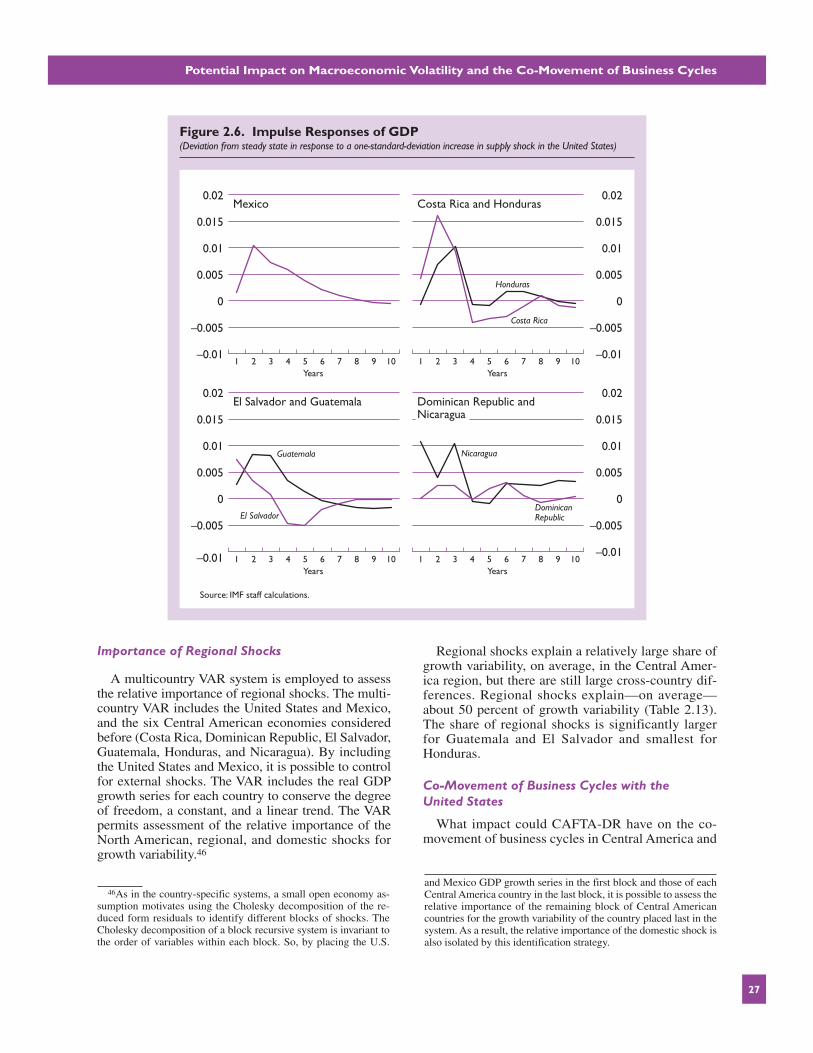

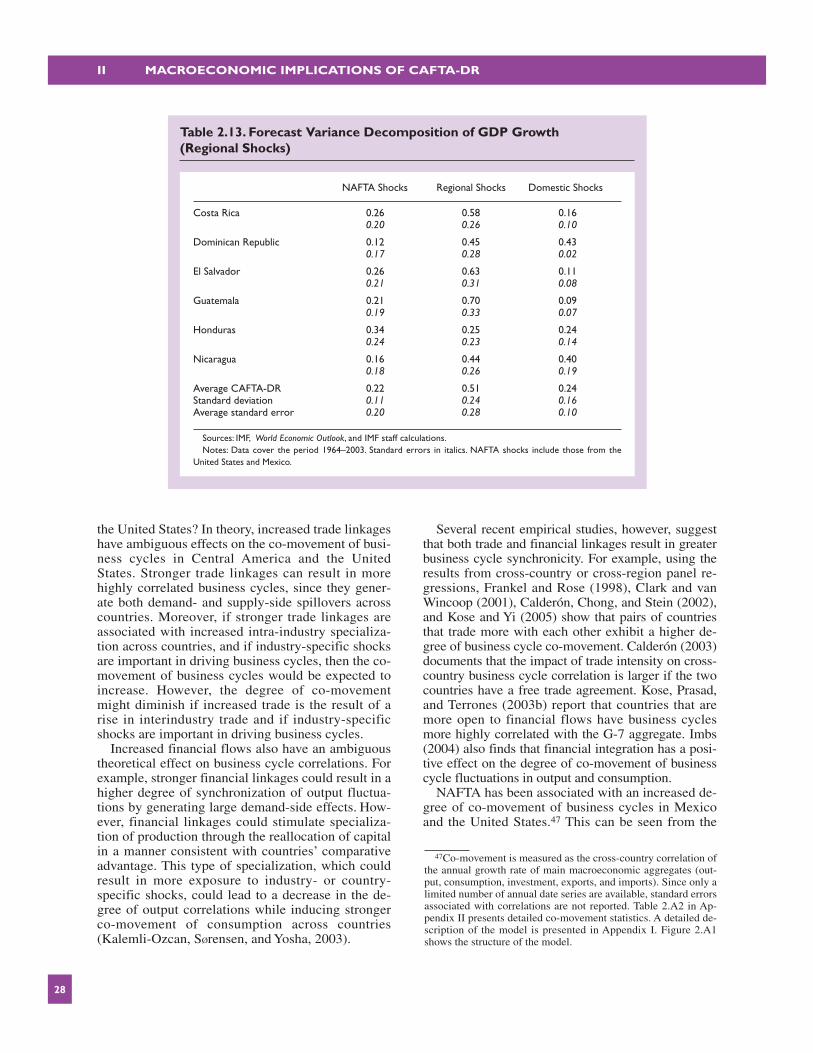

Consistent with the high degree of openness tointernational trade of the countries in the region,both external and regional shocks play importantroles in Central America, even though there aremarked differences in their roles across countries.For example, in at least three countries, external

25

40A simple general equilibrium model is used to assess the ex-tent of potential welfare gains from international risk sharing. Themethodology is similar to the one employed in Van Wincoop(1999). In brief, the model compares two scenarios. The first sce-nario has no additional risk sharing relative to what is already im-plied by observed consumption behavior; in the second, there isperfect risk sharing so that each country consumes a constant frac-tion of total world consumption (see Prasad and others, 2003).

41There has been a substantial increase in the volume of remit-tance inflows to the region from Central Americans in the UnitedStates (see Taccone and Nogueira, 2004, and IMF, 2005). AlthoughEl Salvador and the Dominican Republic on average received thehighest levels of remittances during the period 1990–2003, thegrowth of the remittances was quite significant in other countries,especially Nicaragua and Honduras. These flows could be instru-mental in helping the Central American countries to mitigate theimpact of various shocks and thereby lowering the volatility of con-sumption (Rapoport and Docquier, 2005, and IMF, 2005).

Costa Rica 1.30Dominican Republic 6.38El Salvador 3.74Guatemala 0.39Honduras 1.21Nicaragua 14.95

CAFTA-DR (average) 4.66CAFTA-DR (median) 2.52

Source: IMF staff calculations.

II MACROECONOMIC IMPLICATIONS OF CAFTA-DR

shocks explain a larger share of GDP volatility thanin Mexico, and they are particularly important inCosta Rica and Honduras. In Nicaragua and theDominican Republic, domestic shocks are at leastas important as regional shocks, whereas regionalshocks are most important in El Salvador andGuatemala. The following subsections analyzethese issues in detail by considering the roles of ex-ternal, regional, and domestic shocks in accountingfor macroeconomic fluctuations in Central Americaand Mexico.

Importance of External Shocks

Country-specific vector autoregressive systems(VARs) are estimated to assess the relative importanceof external and domestic shocks in explaining busi-ness cycle variation in Central American economies.To capture the influence of external shocks, the fol-lowing variables are included: the U.S. real GDPgrowth, a measure of the ex post U.S. real interest rate(the U.S. Federal Fund rate minus annual consumerprice index inflation), and the ratio of oil to nonfuelcommodity prices (a proxy for the terms of trade of

these economies). The domestic variables are the in-flation rate, the ratio of the trade balance to GDP, andthe real GDP growth rate.42