71

2017 Full-year results 26 February 2018

2017 Full-year results 26 February 2018

Image TBU – WQ light show?

Agenda

01 2017 highlights, market backdrop and strategy David Atkins – Chief Executive

02 Financial results Timon Drakesmith – CFO; Managing Director, Premium Outlets

03 Operational and portfolio review Timon Drakesmith – CFO; Managing Director, Premium Outlets Mark Bourgeois – Managing Director, UK and Ireland Jean-Philippe Mouton – Managing Director, France

04 Transaction update and conclusion David Atkins – Chief Executive

2

Strong financial returns driven by record occupier demand

3

Another year of strong growth

EPS +6.5%

DPS +6.3%

NAVPS +5.0%

Preferred position with shoppers and retailers

Record volume of new leasing, +34%

Highest occupancy for 17 years

Strong footfall outperformance

Positive operational results

LFL NRI: France +2.6%; Ireland +7.4% (1)

Consistently strong Premium outlets sales +9%

Consistent capital recycling

Sold £400m; diversity of buyers

Further £76m investment in Premium outlets announced today

Significant acquisition aligned to strategy

Advancing intu acquisition

(1) Proforma figure assuming properties owned throughout 2016 and 2017

Riverside at The Oracle, Reading

2017 highlights

Brent Cross extension

Cabot Circus

Images TBC

Victoria, Leeds

Dundrum, Dublin

Bicester Village

L’Occitane, Victoria Leeds Les 3 Fontaines, Cergy

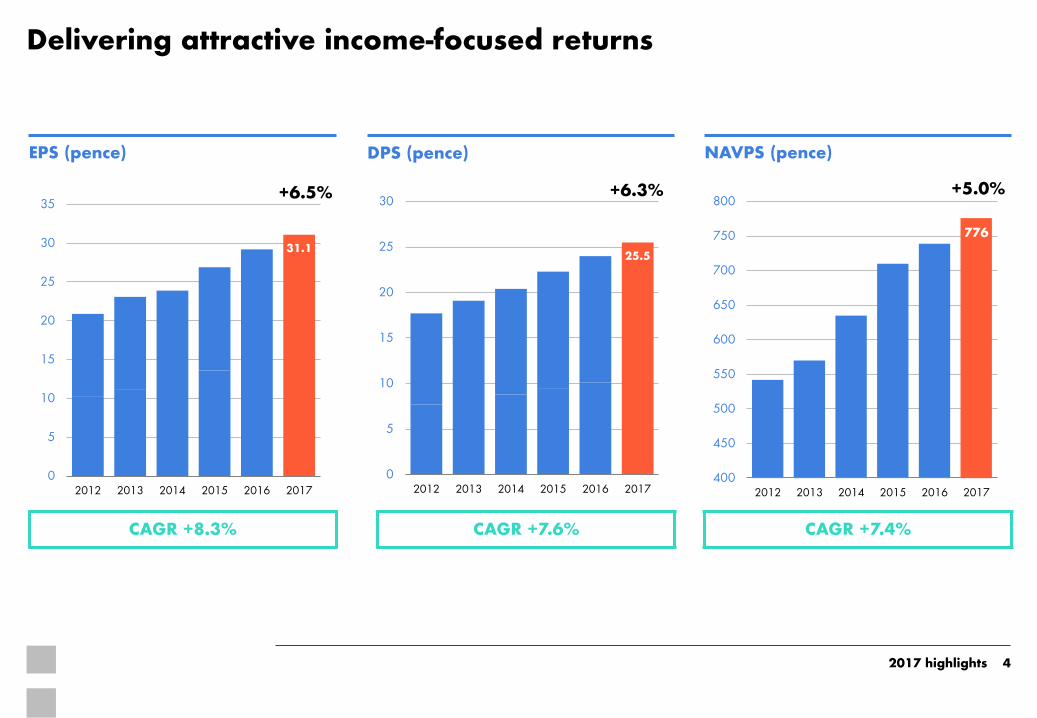

Delivering attractive income-focused returns

4

NAVPS (pence)

776

400

450

500

550

600

650

700

750

800

2012 2013 2014 2015 2016 2017

CAGR +7.4%

EPS (pence) DPS (pence)

31.1

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016 2017

CAGR +8.3%

25.5

0

5

10

15

20

25

30

2012 2013 2014 2015 2016 2017

CAGR +7.6%

2017 highlights

+6.5% +6.3% +5.0%

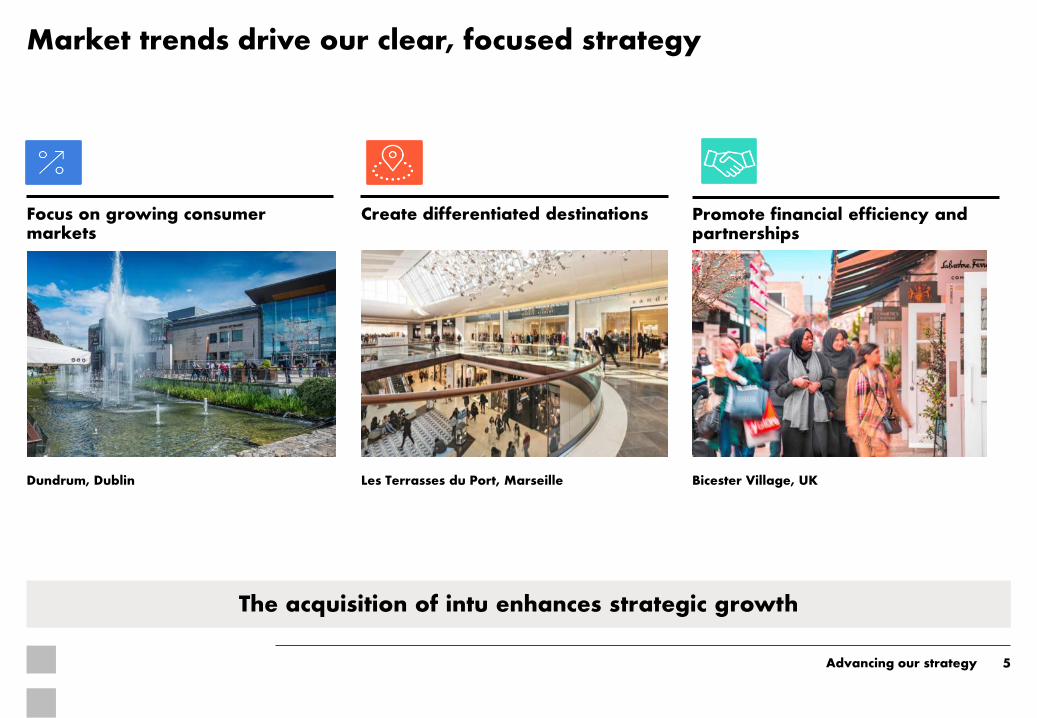

Market trends drive our clear, focused strategy

5

Focus on growing consumer markets

Create differentiated destinations Promote financial efficiency and partnerships

Les Terrasses du Port, Marseille Bicester Village, UK Dundrum, Dublin

The acquisition of intu enhances strategic growth

Advancing our strategy

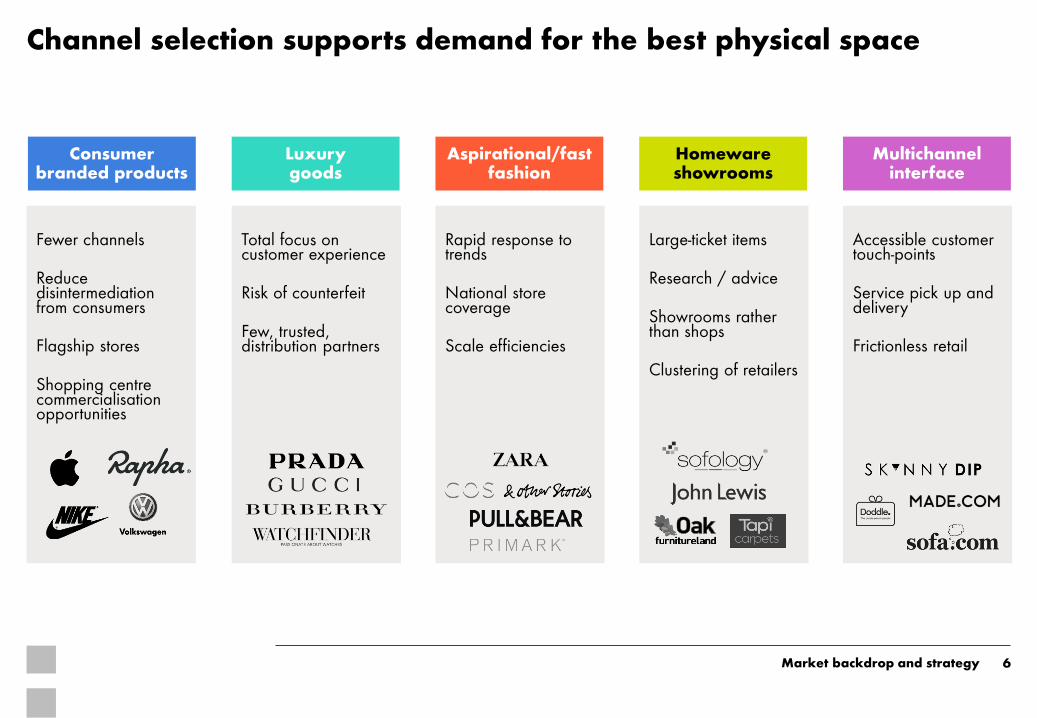

Large-ticket items

Research / advice

Showrooms rather than shops

Clustering of retailers

Rapid response to trends

National store coverage

Scale efficiencies

Channel selection supports demand for the best physical space

6

Consumer branded products

Multichannel interface

Aspirational/fast fashion

Homeware showrooms

Luxury goods

Fewer channels

Reduce disintermediation from consumers

Flagship stores

Shopping centre commercialisation opportunities

Total focus on customer experience

Risk of counterfeit

Few, trusted, distribution partners

Accessible customer touch-points

Service pick up and delivery

Frictionless retail

Market backdrop and strategy

UK catchment spend market-share split (%) (1)

High-quality retail destinations are increasingly valuable in a multichannel landscape

7 (1) Source: MasterCard spend data (collected and analysed by Javelin Group)

0%

10%

20%

30%

40%

50%

60%

70%

Hammerson UK shoppingcentres

Rest of catchment retail Online spend

2015 2017

+2% +6%

-2%

Shoppers are shifting towards large retail destinations and online

Market backdrop and strategy

Other retail locations

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1 2 3 4 5 6 7 8 9 10

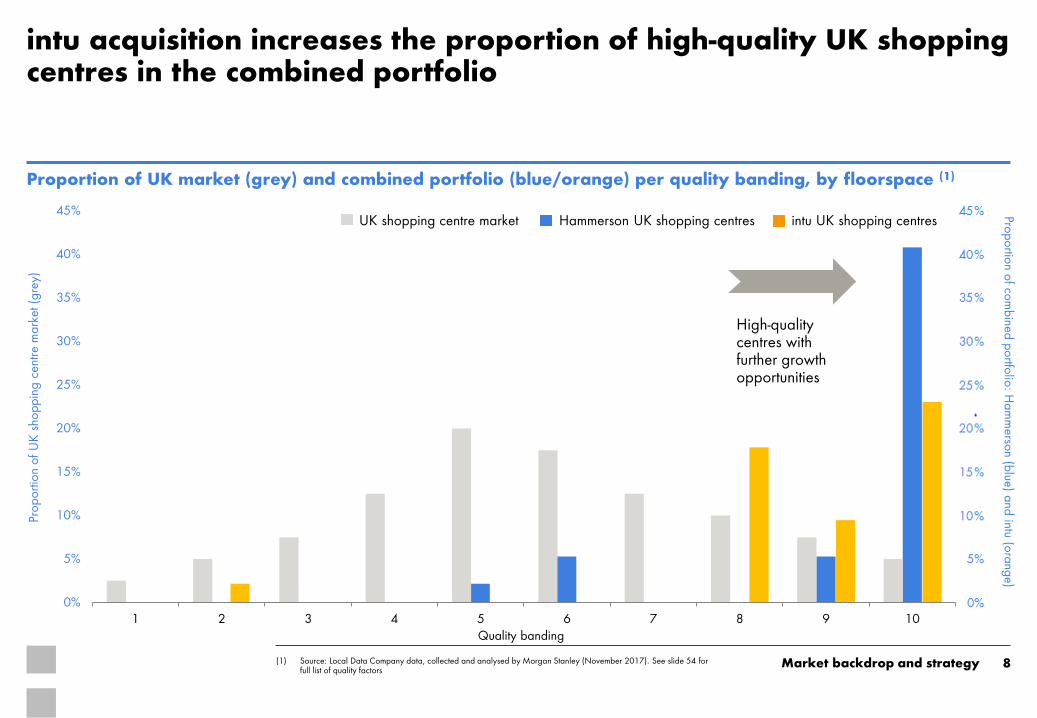

intu acquisition increases the proportion of high-quality UK shopping centres in the combined portfolio

8

Proportion of UK market (grey) and combined portfolio (blue/orange) per quality banding, by floorspace (1)

(1) Source: Local Data Company data, collected and analysed by Morgan Stanley (November 2017). See slide 54 for full list of quality factors

High-quality centres with further growth opportunities

Market backdrop and strategy

Proportio

n of co

mbined

portfo

lio: H

am

merso

n (blue) a

nd intu (o

rang

e)

Footnote to direct to

appendix for full list of properties

Proportio

n of U

K s

hoppin

g c

entre

mark

et (

gre

y)

UK shopping centre market Hammerson UK shopping centres intu UK shopping centres

Quality banding

Successful track-record of capital recycling through varied conditions to a breadth of buyers

9

Hammerson annual disposal proceeds (£m)

2011-2017 total £2.5bn; average £360m disposals p.a.

£1.2bn over last 3 years, 2% below book value

Split of Hammerson’s disposals by category of acquirer (2015-2017)

European institutions

Private equity

Global capital

UK institutions

Local Authorities

Other

33%

24%

17%

13%

8% 5%

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016 2017

£1.2bn

Market backdrop and strategy

Check disposals total

10 (1) Pro-forma GAV as at 31 December 2017 (2) Darker blue indicates top 10 largest combined group ownerships in UK shopping centres by value (3) Illustrative portfolio mix post disposals and reinvestment into Premium outlets, Ireland, Spain and Developments, assumes organic

growth of 2% p.a. on largest 10 UK shopping centres and growth of 5% p.a. on Premium outlets, Ireland and Spain

2018 combined portfolio split (GAV, £bn) (1,2)

2021+ illustrative portfolio split (£bn) (2,3)

72% higher-growth segments

64% higher-growth segments

intu acquisition allows for agile capital recycling into higher-growth segments

European shopping centres and retail parks (2)

Ireland

Spain

Developments

Premium outlets

£2bn disposals

Market backdrop and strategy

02 Financial results

Timon Drakesmith – CFO; Managing Director, Premium Outlets

- Review of 2017 performance

- Analysis of cost:income ratios

- New debt facility

- 2018 disposal plans

- Drivers of future EPS growth

Image TBC

Headline results

12 (1) Does not include premium outlets. NRI including premium outlets is £468.0m (2) Valuation for total portfolio including premium outlets (3) Change reflects capital return, not absolute increase of 5.9%

Income statement 31 December 2017 31 December 2016 Change

Net rental income (£m) (1) 370.4 346.5 +6.9%

Adjusted profit (£m) 246.3 230.7 +6.8%

Adjusted EPS (p) 31.1 29.2 +6.5%

Total dividend (p) 25.5 24.0 +6.3%

Balance sheet

Portfolio value (£m) (2) 10,560 9,971 +2.2%(3)

EPRA NAVPS (p) 776 739 +5.0%

LTV (%) 36 36 n/a

Financial results

LfL NRI growth

13 (1) Figures on a proportionally consolidated basis (2) Proforma figure assuming properties owned throughout 2016 and 2017 (3) LFL NRI growth includes the impact of extensions due to multiple tenant relocations from the existing scheme into new phases. Hammerson

management estimate that the extensions have contributed approximately 1-2% to LfL NRI growth

2017 NRI growth by sector (1)

LFL NRI growth (%)

UK shopping centres

+1.8

UK retail parks

−2.5

France +2.6

EPRA LfL NRI

+1.0

Ireland (2)

+7.4

LfL NRI incl. Ireland +1.7

Premium outlets (3)

+15.3

Total LfL NRI incl. Ireland and Premium outlets

+4.4

Financial results

UK shopping centres LFL NRI

2017 2016

Net rents, commercialisation and other

2.3% 2.0%

Car parks (business rates) −0.5% 0.4%

Total 1.8% 2.4%

Note - Slide appears as

build

UK retail parks LFL NRI

2017 2016

Net rents, commercialisation and other

2.4% −2.1%

Surrender premiums −4.9% 4.5%

Total −2.5% +2.4%

With VM to check

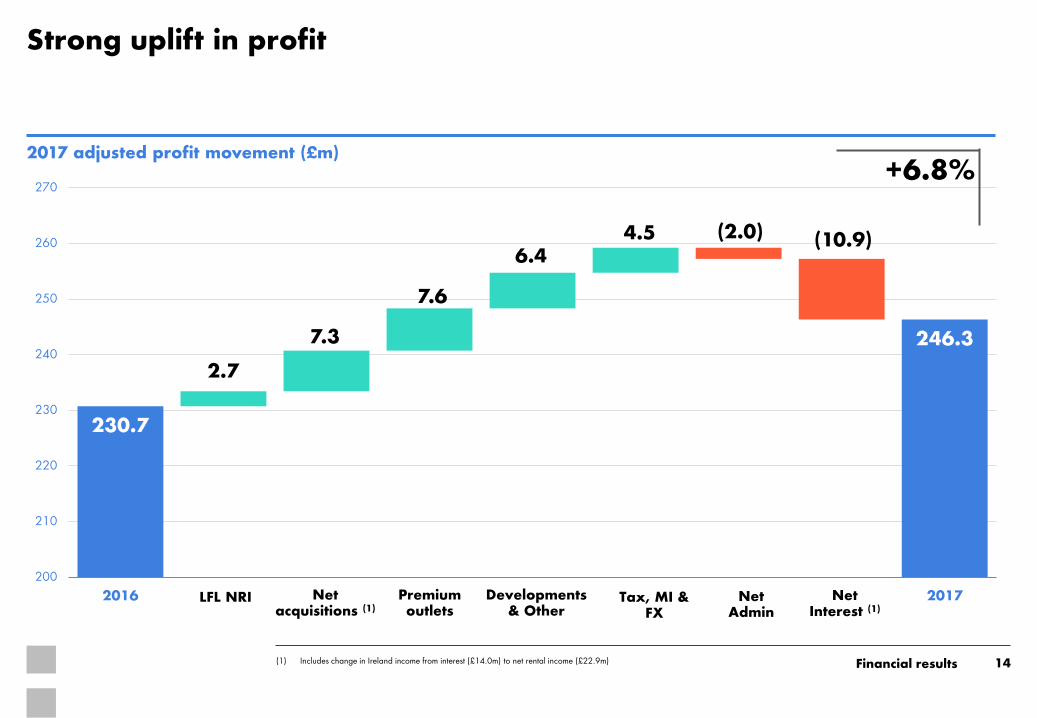

Strong uplift in profit

14

230.7

246.3

2.7

7.3

7.6

6.4 4.5 (2.0) (10.9)

200

210

220

230

240

250

260

270

2016 2017

2017 adjusted profit movement (£m)

Developments & Other

Premium outlets

Net acquisitions (1)

Tax, MI & FX

Net Admin

+6.8%

Financial results

LFL NRI Net Interest (1)

(1) Includes change in Ireland income from interest (£14.0m) to net rental income (£22.9m)

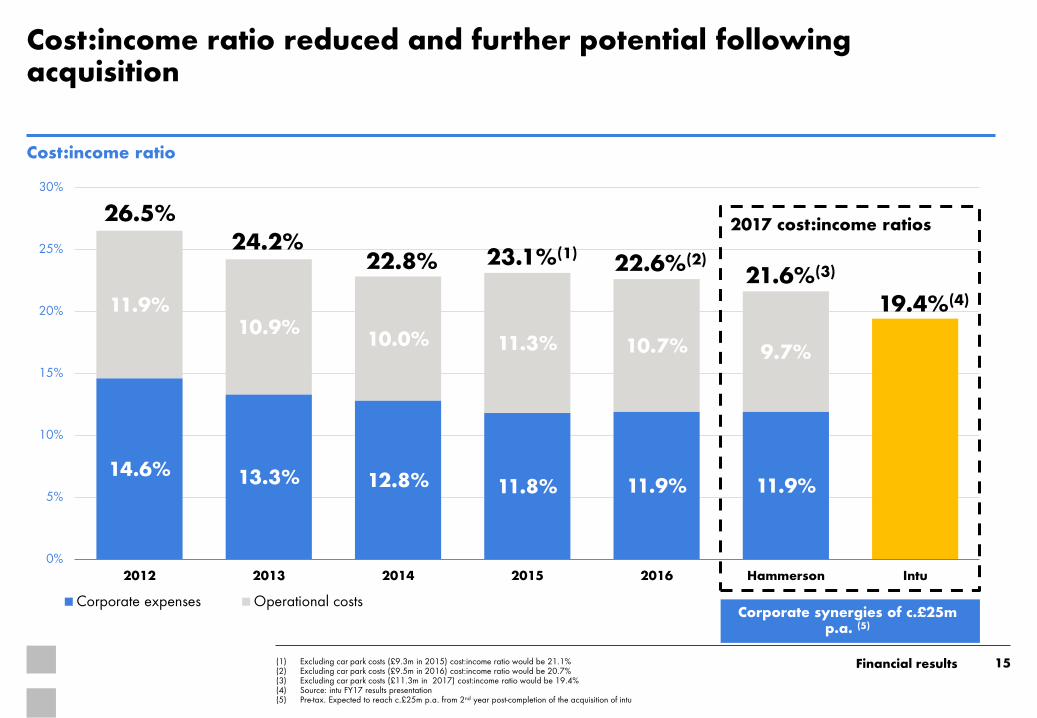

14.6% 13.3% 12.8% 11.8% 11.9% 11.9%

11.9% 10.9%

10.0% 11.3% 10.7% 9.7%

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014 2015 2016 Hammerson Intu

Corporate expenses Operational costs

Cost:income ratio reduced and further potential following acquisition

15

Cost:income ratio

26.5% 24.2%

22.8% 23.1%(1)

(1) Excluding car park costs (£9.3m in 2015) cost:income ratio would be 21.1% (2) Excluding car park costs (£9.5m in 2016) cost:income ratio would be 20.7% (3) Excluding car park costs (£11.3m in 2017) cost:income ratio would be 19.4% (4) Source: intu FY17 results presentation (5) Pre-tax. Expected to reach c.£25m p.a. from 2nd year post-completion of the acquisition of intu

22.6%(2) 21.6%(3)

Financial results

19.4%(4)

2017 cost:income ratios

Corporate synergies of c.£25m p.a. (5)

Income growth driving valuation

16 (1) At constant exchange rates. Developments included per geographical segment (2) Figures on a proportionally consolidated basis. Principally assets held for development and non-core (3) Other capital movements reflects the impact of changes in purchasers’ costs, development surpluses and capital expenditure (4) Excluding stamp duty, proforma capital return 3.9%

Financial results

2017 capital return (1)

Drivers of underlying valuation change Value at 31 December

2017 (2)

(%) Yield shift (%) Income (%) Other (%)(4) (£m)

UK shopping centres +0.7 +0.2 +1.1 −0.6 3,528

UK retail parks −2.9 −2.8 −0.1 0.0 1,270

UK other (3) +3.8 +1.2 +1.3 +1.3 422

France +0.3 +0.0 +0.1 +0.2 2,011

Ireland (5) −0.3 +0.4 +3.5 −4.2 1,095

Premium outlets +11.5 +1.2 +10.1 +0.2 2,234

Total +2.2 +0.1 +2.5 −0.4 10,560

Financing ratios underpin our balance sheet strength

17

Financing policy 31 December 2017 31 December 2016

Net debt - £3,501m £3,413m

Gearing <85% 58% 59%

Loan to value <40% 36% 36%

Cash and undrawn facilities - £958m £592m

Weighted average cost of debt - 2.9% 3.1%

Interest cover >2.0x 3.4x 3.5x

Net debt/EBITDA <10x 9.3x 9.5x

Fixed rate debt >50% 78% 70%

GBP/EUR FX balance sheet hedging 70% - 90% 78% 79%

Financial results

35.1

22.5

0

5

10

15

20

25

30

35

40

Intu facilities NewHammerson

RCF

intu debt refinancing opportunities

18 (1) Terms agreed with core Hammerson relationship banks for a new £1.5bn 3 year credit facility, subject to documentation. (2) Assumed fully drawn, based on initial margin of 100bps plus 3month LIBOR of 0.65% (3) Assumed fully drawn, based on in-place coupons and margins of intu credit facilities

Selected intu near-term debt maturities

Facility Maturity

Convertible bonds, 2.5% coupon £160m 2018

SGS bank loan £352m 2021

RCF £600m 2021

Convertible bonds, 2.875% coupon £375m 2022

Total £1,487m

Illustrative annualised interest cost (3) £38.5m

Illustrative annualised interest cost difference (£m)

Financial results

£12.6m

Facility Maturity

New Hammerson RCF (1) £1,500m 2021

Illustrative annualised interest cost (2) £23.4m

Opportunity for significant

refinancing benefit

Capital recycling and funding flexibility

19

Deleverage through disposals ahead of phased development and reinvestment (£m)

0

500

1000

1500

2000

2500

2015-2017 Short to medium term Capex 2018-2020

Financial results

£2.0bn Hammerson and

intu total disposals

£500m Hammerson target disposals in 2018

(1) Includes intu committed capex and Spain (Source: intu FY17 results ). Further detail on slide 62

+£2.0bn Combined group disposals in short-

medium term

£660m Hammerson and

intu annual run-rate of disposals

£1.3bn Combined group

medium term capex (1)

Disposals Capex

c.£440m

Average run-rate capex

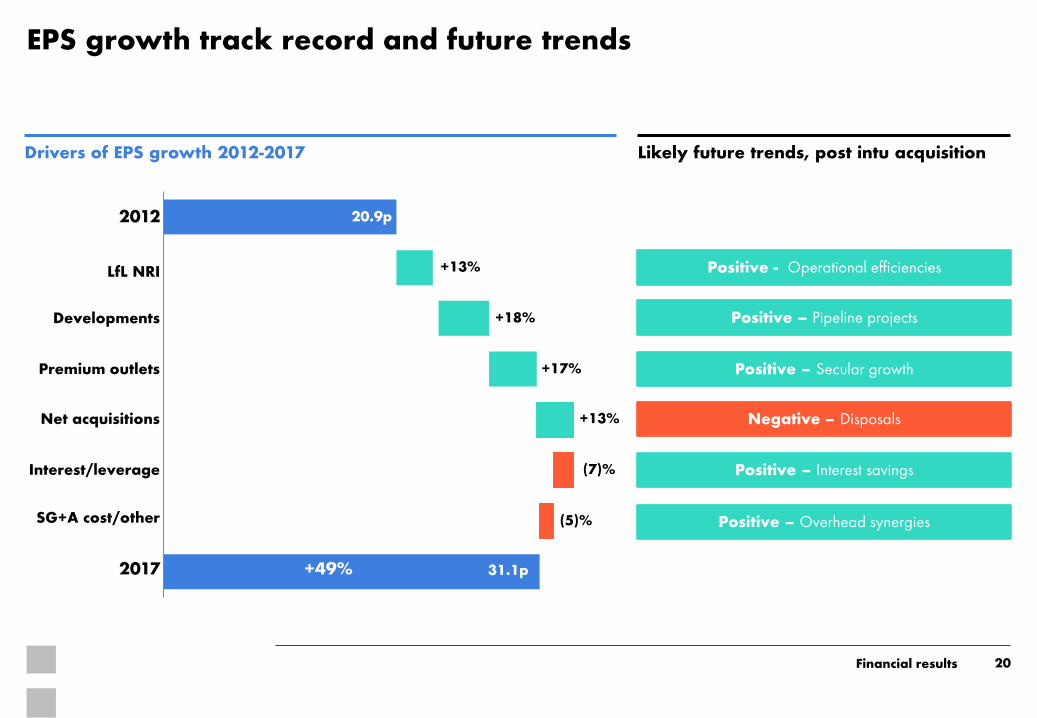

EPS growth track record and future trends

20

Drivers of EPS growth 2012-2017

LfL NRI

2012

+49%

+13%

+18%

+17%

+13%

(7)%

(5)%

20.9p

31.1p

Developments

Premium outlets

Net acquisitions

Interest/leverage

SG+A cost/other

2017

Likely future trends, post intu acquisition

Positive - Operational efficiencies

Positive – Pipeline projects

Positive – Secular growth

Negative – Disposals

Positive – Interest savings

Positive – Overhead synergies

Financial results

03 Portfolio review

Timon Drakesmith - CFO

- Premium Outlets

Mark Bourgeois - MD UK & Ireland

- UK and Ireland operational review

Jean-Philippe Mouton – MD France

- France

Bicester Village, UK

Change image

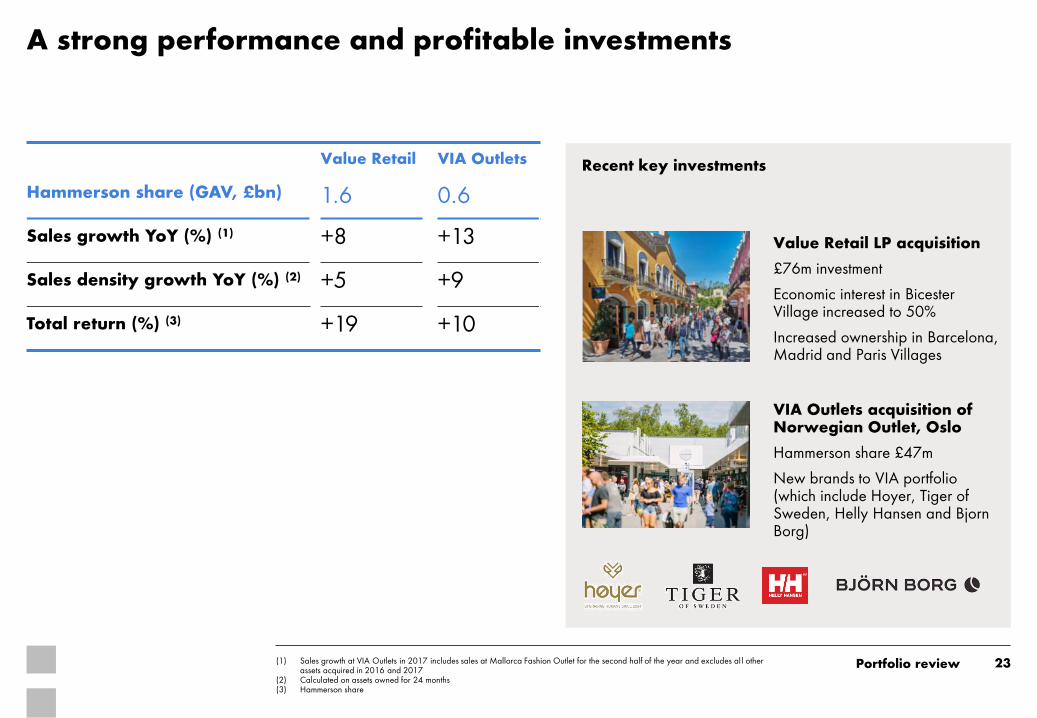

Portfolio review:

Premium outlets

A strong performance and profitable investments

23 (1) Sales growth at VIA Outlets in 2017 includes sales at Mallorca Fashion Outlet for the second half of the year and excludes all other assets acquired in 2016 and 2017

(2) Calculated on assets owned for 24 months (3) Hammerson share

Value Retail VIA Outlets

Hammerson share (GAV, £bn) 1.6 0.6

Sales growth YoY (%) (1) +8 +13

Sales density growth YoY (%) (2) +5 +9

Total return (%) (3) +19 +10

La Vallée Village, Paris

Recent key investments

Value Retail LP acquisition

£76m investment

Economic interest in Bicester Village increased to 50%

Increased ownership in Barcelona, Madrid and Paris Villages

VIA Outlets acquisition of Norwegian Outlet, Oslo

Hammerson share £47m

New brands to VIA portfolio (which include Hoyer, Tiger of Sweden, Helly Hansen and Bjorn Borg)

Portfolio review

Global tourism continues as a growth driver

24 (1) Source: Global Blue, (Value Retail Villages) (2) Other includes countries which are not in the top 15

Breadth of international visitors

Growth in sales to smaller source markets

Partnerships with hotels and tour operators

Promotions targeted to specific traveller groups

2017 European tax refunded sales by nationality (1)

48%

14%

10%

5%

3% 1%

19%

YoY growth (%) (1)

Greater China +16

South and East Asia +17

Gulf/Middle East -2

Russia +28

India +38

USA +22

Other (2) +10

Total +14

update

Portfolio review

Premium outlets offer attractive yields and higher growth

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Dec

2017 N

OI

yie

ld (

%)

2017 ERV growth (%)

25 (1) Data as at 31 December 2017 Source: Cushman and Wakefield

Frankfurt

Paris Madrid

Barcelona Porto

Bicester

Amsterdam

Trophy Central London retail

Premium outlets

Spanish super-regional shopping

centres

Zürich Super-regional

UK shopping centres

Jumbo French shopping centres

Local UK shopping

centres

UK Logistics

NOI yield and ERV growth of selected premium outlets (1)

Local UK shopping centres

UK large shopping centres

France large shopping centres

Spain large shopping centres

Trophy central London retail (2)

UK logistics

Portfolio review:

UK and Ireland operational review

The Oracle, Reading

Impressive volume of new leasing across the group

27 (1) Portfolio leasing on a proportionally consolidated basis, excludes developments and premium outlets

Hammerson new leasing volume 2017 (£m) (1)

0

5

10

15

20

25

30

35

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cumulative 2016 Cumulative 2017

[add additional logos for leases signed in H2

2017]

Discuss best logos to include (RP and UK)

[ ]

Portfolio review

+6.7%

+34%

UK shopping centres

Bullring, Birmingham

UK brands in administration 2008-12: MFI Barratt Shoes Woolworths Comet BHS La Senza

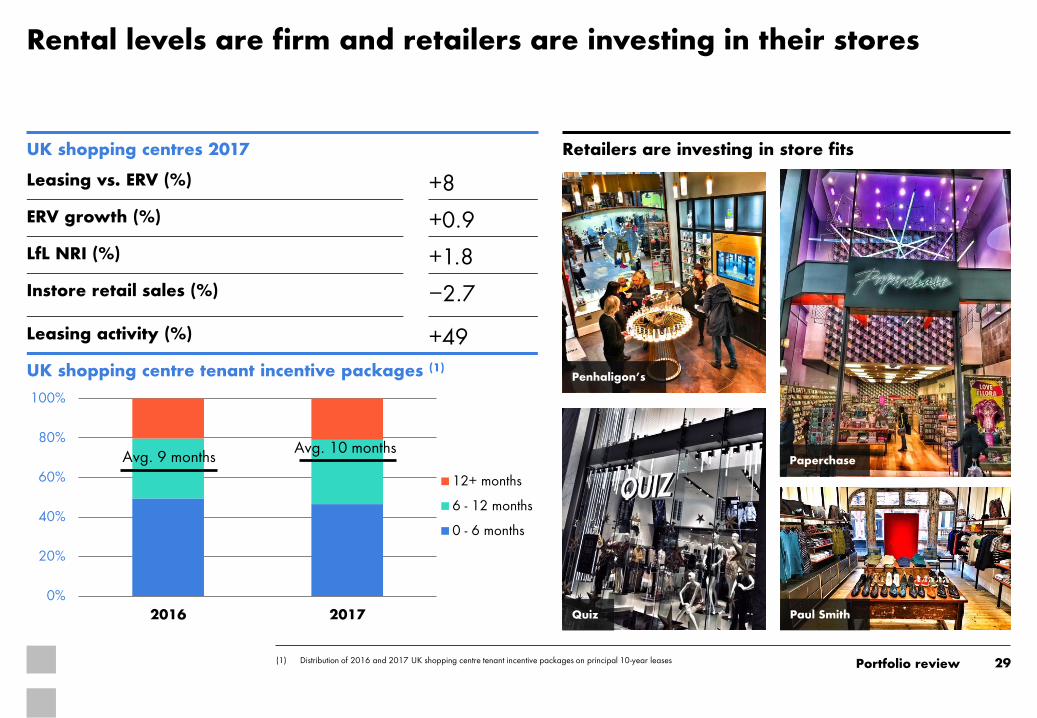

Rental levels are firm and retailers are investing in their stores

Zweibrucken, Germany

[ ]% of Hammerson portfolio at time of

going into administration

New UK brands since 2012: Rituals LuLu Lemon

Retailers are investing in store fits UK shopping centres 2017

Leasing vs. ERV (%) +8

ERV growth (%) +0.9

LfL NRI (%) +1.8

Instore retail sales (%) −2.7

Leasing activity (%) +49

UK shopping centre tenant incentive packages (1)

Avg. [ ] months

Avg. 10 months

Avg. 10 months

0

4

8

12

16

2015 2016 2017

Average Spread

(1) Distribution of 2016 and 2017 UK shopping centre tenant incentive packages on principal 10-year leases

29 Portfolio review

Paperchase

Quiz Paul Smith

Penhaligon’s

Images TBC

0%

20%

40%

60%

80%

100%

2016 2017

12+ months

6 - 12 months

0 - 6 months

Avg. 9 months Avg. 10 months

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

Cha

nge

in s

hare

of le

asi

ng,

by

ERV

(2015 -1

7)

Hammerson instore sales growth, 2017 (%)

Consumer brands

Ath-leisure

Gifts

Convenient services

Leisure

Personal luxuries

Aspirational homeware

Fast fashion

Aspirational fashion

Menswear

Household Casual dining

Footwear Cosmetics

Jewellers

High street fashion

Lingerie

Confectionary Cafe Toys Hairdresser

Stationer Accessories Books

Takeaway food

Travel agent Health foods Dept

store

Our insights into consumer trends drive our leasing strategy

30 (1) Includes leases signed across all Hammerson UK shopping centres 2015 – 2017, measuring change in proportion of new leasing signed; Hammerson same-centre instore sales YoY

Hammerson UK shopping centre leasing growth and instore sales growth(1)

Portfolio review

Add circles as builds?

Apparel is a dynamic category; we are tilting our mix towards the winning brands

31 (1) ‘Apparel’ includes clothing, footwear and lingerie

UK shopping centre leasing (£m) (1)

Steady volume of fashion leasing; less as a proportion of total

Apparel is lower as a proportion of total leasing

Total fashion leasing 2015: 55% 2017:43%

New brands are replacing old: Evolving consumer preferences inform our leasing strategy

Portfolio review

39%

33%

0%

20%

40%

60%

80%

100%

2015 2017

Apparel Non-apparel

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

High-street and fast-fashion Athleisure Aspirational fashion

2015 2017Example tenants

UK shopping centre apparel leasing (£m)

Ath-leisure High street fashion

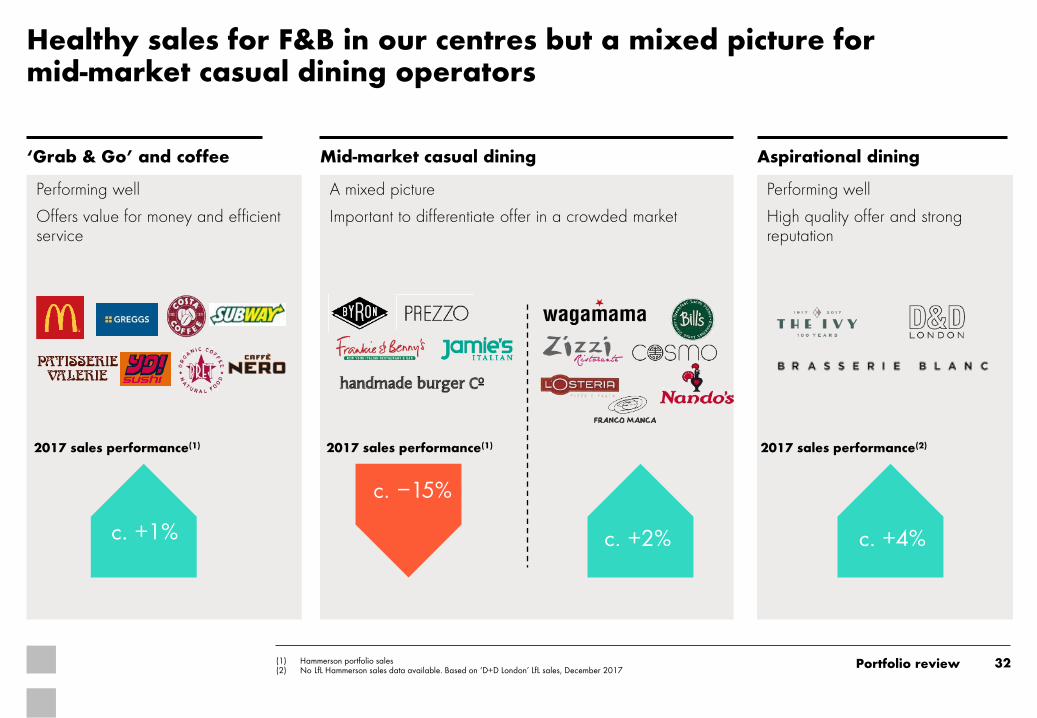

Performing well

High quality offer and strong reputation

Performing well

Offers value for money and efficient service

A mixed picture

Important to differentiate offer in a crowded market

Healthy sales for F&B in our centres but a mixed picture for mid-market casual dining operators

32 (1) Hammerson portfolio sales (2) No LfL Hammerson sales data available. Based on ‘D+D London’ LfL sales, December 2017

‘Grab & Go’ and coffee Mid-market casual dining Aspirational dining

c. +1% c. +2%

c. −15%

2017 sales performance(1)

c. +4%

2017 sales performance(1) 2017 sales performance(2)

Portfolio review

Retailer rotation provides positive opportunities

33

Market data TBC (Source: Deloitte)

UK retail market administrations (no. of stores) and Hammerson impact on income (%)

(1) Source: Centre for Retail Research

Portfolio review

0%

2%

4%

6%

8%

10%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012 2013 2014 2015 2016 2017%

of H

am

merso

n incom

e

UK

mark

et a

dm

inis

tratio

ns, no

of st

ore

s Brent Cross

Jaeger All Saints / Ernest Jones / JD Sport

Highcross

House of Fraser Zara / JD Sport

Handmade Burger

All 6 units re-let or reassigned

Hammerson UK shopping centre portfolio administrations <1% of income

Selected retail administrations 2011-13:

Less than 1% negative impact on income from tenants in administration, even at the peak in 2012

2017 milestones

Resolution to grant outline planning consent secured October 2017

Scheme approved by GLA

Next steps

Secure remaining land interests 2018

Pre-letting, detailed design and construction tendering

Progressing with key development projects

34

Croydon

(1) Hammerson share

Brent Cross

175,000m2 Total retail space

Cost to complete (1)

£475-550m

Portfolio review

200,000m2 Croydon Partnership retail

Cost to complete (1)

£650-700m

2017 milestones

Detailed reserved matters planning application approved October 2017

Confirmation of CPO received December 2017

Agreements reached with two anchors – John Lewis and Marks & Spencer

Preferred retail contractor selected

Next steps

Infrastructure contractor appointment Spring 2018 and pre-letting

Retail parks

Elliott’s Field, Phase 2, Rugby

UK brands in administration 2008-12: MFI Barratt Shoes Woolworths Comet BHS La Senza

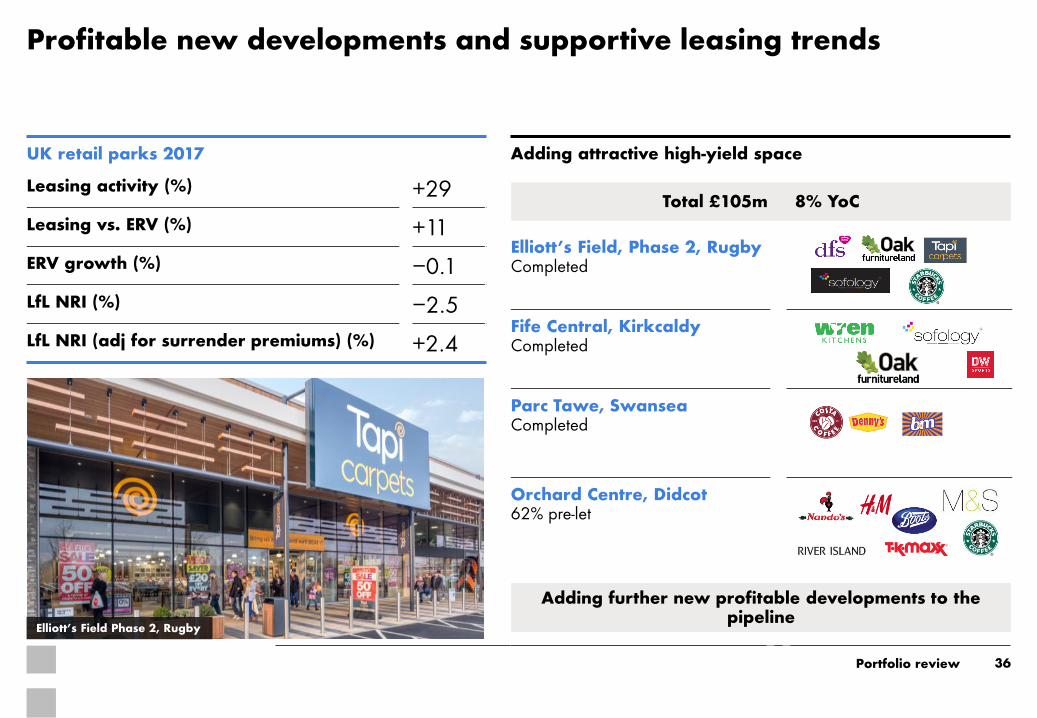

Profitable new developments and supportive leasing trends

Zweibrucken, Germany

[ ]% of Hammerson portfolio at time of

going into administration

New UK brands since 2012: Rituals LuLu Lemon

UK retail parks 2017

Leasing activity (%) +29

Leasing vs. ERV (%) +11

ERV growth (%) −0.1

LfL NRI (%) −2.5

LfL NRI (adj for surrender premiums) (%) +2.4

Elliott’s Field Phase 2, Rugby

36

With retail parks team to

populate

Portfolio review

Elliott’s Field, Phase 2, Rugby Completed

Fife Central, Kirkcaldy Completed

Parc Tawe, Swansea Completed

Orchard Centre, Didcot 62% pre-let

Adding further new profitable developments to the pipeline

Adding attractive high-yield space

Total £105m 8% YoC

Ireland

POCO store launch, Dundrum, Dublin

20

40

60

80

100

120

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

Jan-

17

Jan-

18

Consumer Sentiment Monthly Index

Hammerson Ireland portfolio 2017

Leasing vs. ERV (%) +10

ERV growth (%) +2.7

LfL NRI (%) +7.4

Confident consumer backdrop supports continued strong ERV growth

38

Uplift in Dundrum ERV since ownership (2)

Portfolio review

€65m

c.€90m

€9m

Acquisition ERVJuly 2016

Uplift at Dec2017

Expected growth2018-2021

Forecast 2021ERV

+13%

On track with targeted 4-5% ERV CAGR

Consumer confidence at record high (1)

(1) Source: KBC/ESRI (2) Dundrum ERV 100%

Delivering value-add asset management initiatives

39 (1) Cushman and Wakefield

On track with Ireland strategy

1. Short term: rent reviews, leasing and commercialisation

Best-practice customer experience initiatives

New brands introduced

2. Medium term: value-add asset management

Signed Fallon & Byrne food hall

Progressing with plans to redevelop Pavilions food court

Ongoing

3. Long-term: development

Masterplan at Dundrum phase 2. Target planning application 2019

Supportive Court of Appeal ruling at Dublin Central

Planning phase

Fallon & Byrne Food Hall 10,000 sq. ft. speciality food hall

Reconfiguration of Pembroke Square

2. Value-add asset management initiatives

Pavilions food court

Portfolio review

Three new restaurant units

Improving casual dining offer to drive dwell time

Les Terrasses du Port, Marseille

Portfolio review:

France

Image TBU

Growing consumer confidence translating into sales and footfall outperformance

(1) Source: INSEE (2) By volume (3) CNCC benchmark -1.0%

Consumer confidence index (1)

Portfolio review

Retail leasing index (ILC) (%) Hammerson in-store retail sales +0.1%

Benchmark: -1.0% (1)

Hammerson footfall +1.6%

Benchmark: -1.8% (2)

41

3.3

1.4

0.0 (0.2) 0.1 1.0

1.5

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2012 2013 2014 2015 2016 2017 Q1 2018

Hammerson France portfolio 2017

Leasing activity (%) (2) +9

Leasing vs. ERV (%) +5

ERV growth (%) +0.9

LfL NRI (%) +2.6

Instore retail sales (%) (3) +0.1

70

80

90

100

110

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Les Terrasses du Port, Marseille

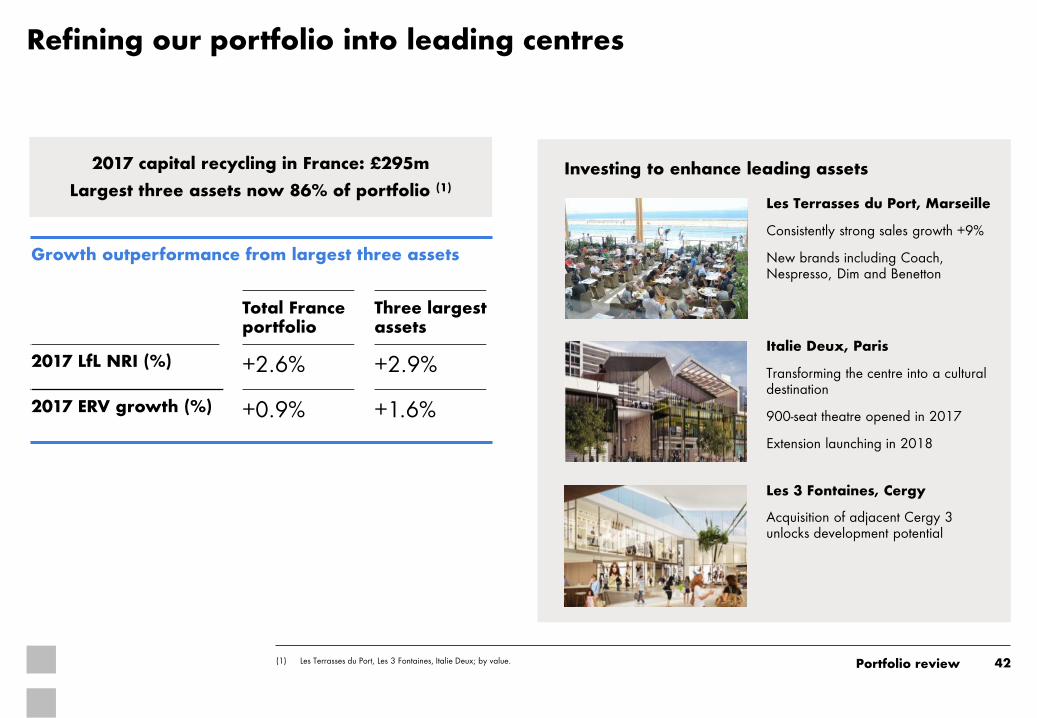

Refining our portfolio into leading centres

42 (1) Les Terrasses du Port, Les 3 Fontaines, Italie Deux; by value.

Investing to enhance leading assets

Les 3 Fontaines, Cergy

Acquisition of adjacent Cergy 3 unlocks development potential

Italie Deux, Paris

Transforming the centre into a cultural destination

900-seat theatre opened in 2017

Extension launching in 2018

Les Terrasses du Port, Marseille

Consistently strong sales growth +9%

New brands including Coach, Nespresso, Dim and Benetton

Portfolio review

Growth outperformance from largest three assets

Total France portfolio

Three largest assets

2017 LfL NRI (%) +2.6% +2.9%

2017 ERV growth (%) +0.9% +1.6%

2017 capital recycling in France: £295m

Largest three assets now 86% of portfolio (1)

Size Size

Italie Deux, Paris Les 3 Fontaines, Cergy

Progressing with key development projects

Co-ownership agreement, building permit and retail consent obtained

Acquired adjacent centre, Cergy 3

Main contractor selected

Good pre-letting to fashion brands and F&B (Pret A Manger, Vapiano)

Project commenced

43

Italie Deux, Paris

Les Trois Fontaines, Cergy

Portfolio review

33,000m2 Total development cost

£225m

6,400m2 Total development cost

£38m

Project to enhance tenant mix and F&B offer at central Paris scheme

Obtained planning consent and agreement with co-owners

Pre-lets include Pret A Manger and M&S Simply Food

Start on site Spring 2018 Target rent

£16m Target rent

£2m

44

04 Transaction update and conclusion

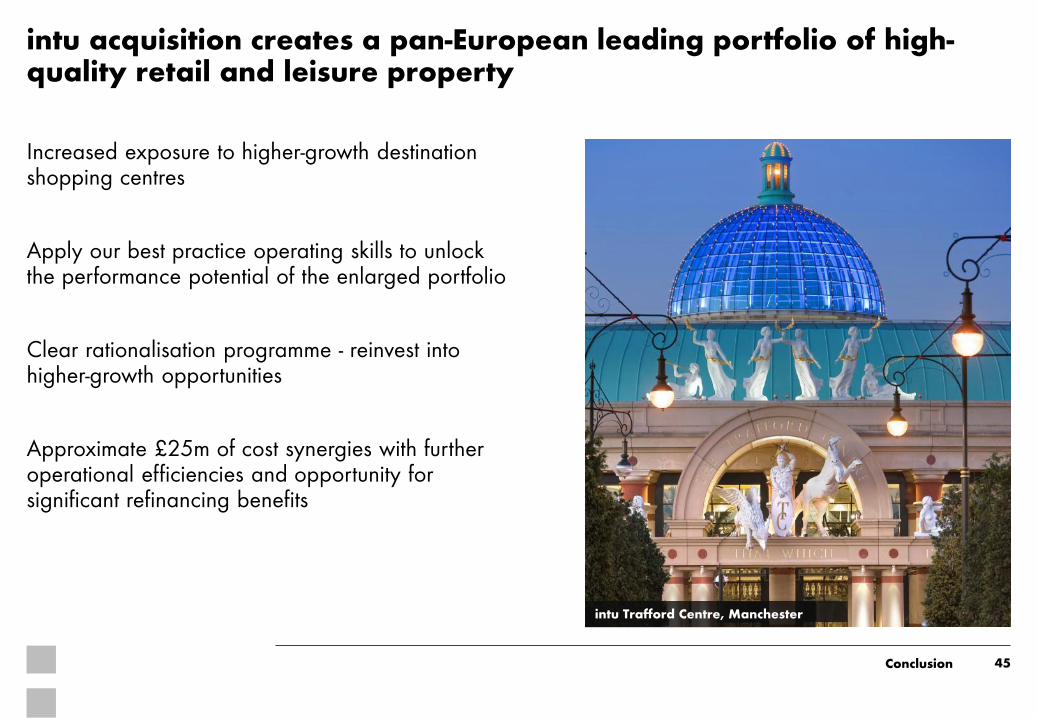

intu acquisition creates a pan-European leading portfolio of high-quality retail and leisure property

45 Conclusion

intu Trafford Centre, Manchester

Increased exposure to higher-growth destination shopping centres

Apply our best practice operating skills to unlock the performance potential of the enlarged portfolio

Clear rationalisation programme - reinvest into higher-growth opportunities

Approximate £25m of cost synergies with further operational efficiencies and opportunity for significant refinancing benefits

Advancing the intu acquisition

46

Shareholder documentation and approval process

Q1 2018 Q2 2018 Q3 2018

Integration

Competition

Shareholder meetings

Year-end company accounts

Combined accounts + shareholder docs

Asset strategy planning

Integration strategy planning

Pre-close integration preparation

Preparatory merger work and planning

Pre-notification engagement with CMA

Q4 2018 Material progress toward the acquisition • Shareholder approval process

• [Met with X% of combined shareholder register]

• Pro-forma combined accounts in preparation • Shareholder documentation to be published

[date] • EGM and shareholder vote scheduled [date]

• Operational • Asset strategy planning started • Commencement of brand review

• Competition • Market reviews and catchment surveys

ongoing • Engaged with the CMA to commence

clearance process • Reviewing learnings from recent Grand

Central transaction (1)

Next steps… • Shareholder documentation published • EGM and vote • CMA commence Phase 1 review process

[See Appendix for timetable of dates]

Publish shareholder documents EGM

CMA Review

Conclusion

Our strategy continues to deliver success

47

Strong financial performance; positioned for structural change in retail

High demand for our premium retail destinations

Strengthening quality and future opportunities through intu acquisition

Victoria, Leeds

Conclusion

48

Questions

Westquay, Southampton

Disclaimer

This presentation contains certain statements that are neither financial results nor other

historical information. These statements are forward-looking in nature and are subject to

risks and uncertainties. Actual future results may differ materially from those expressed or

implied by these statements.

Many of these risks and uncertainties relate to factors that are beyond Hammerson’s

ability to control or estimate precisely, such as future market conditions, currency

fluctuations, the behaviour of other market participants, the actions of governmental

regulators and other risk factors such as the Company’s ability to continue to obtain

financing to meet its liquidity needs, changes in the political, social or regulatory

framework in which the Company operates or in economic or technological trends or

conditions, including inflation and consumer confidence, on a global, national or

regional basis.

Readers are cautioned not to place undue reliance on these forward-looking statements,

which speak only as of the date of this document. Hammerson does not undertake any

obligation to publicly release any revision to these forward-looking statements to reflect

events or circumstances after the date of these materials. Information contained in this

presentation relating to the company or its share price, or the yield on its shares, should

not be relied upon as a guide to future performance.

49

Appendices

Image TBU

2.3m sq m retail space

14 Countries

UK shopping centres - £3.5bn

France - £1.9bn

Ireland - £1.0bn

UK retail parks - £1.2bn

Premium outlets - £2.2bn

Development & UK other - £0.8bn

£10.6 billion leading pan-European retail platform (1)

51

33%

18% 9%

12%

21%

7%

57 European shopping destinations

Top 3 Market position in all chosen sectors

43% non-UK assets

440m visitors

4,900 Tenants

11 - UK shopping centres

8 - France shopping centres

3 - Ireland shopping centres

15 - UK retail parks

20 - Premium outlets

(1) As at 31 December 2017

TBU

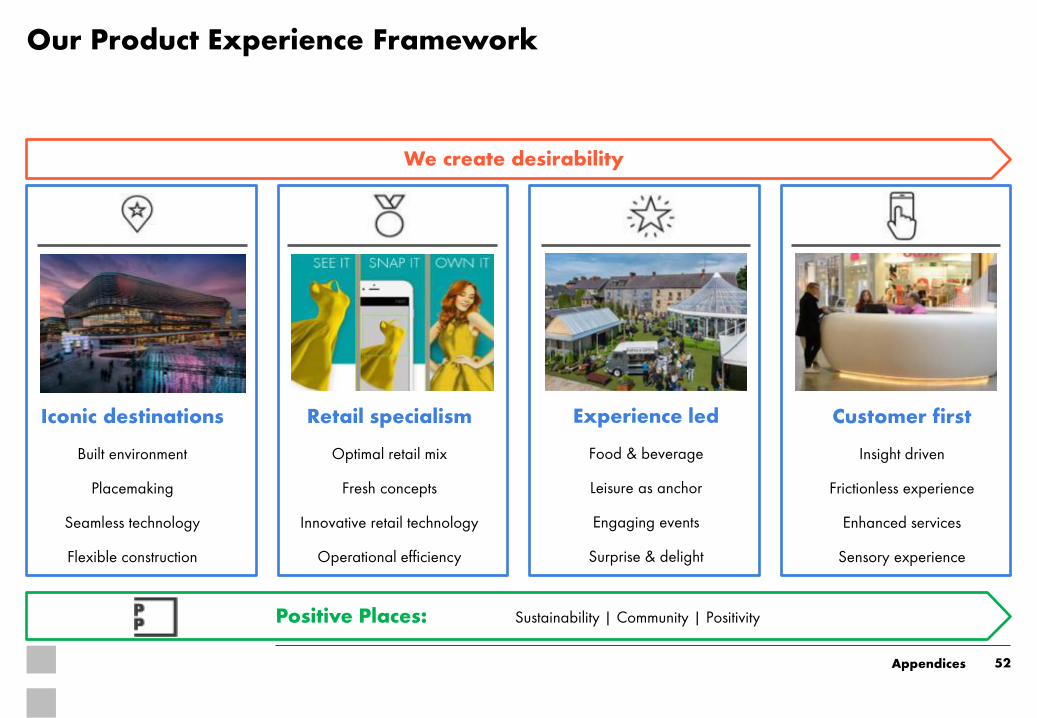

Our Product Experience Framework

52

We create desirability

Iconic destinations

Built environment

Placemaking

Seamless technology

Flexible construction

Customer first

Insight driven

Frictionless experience

Enhanced services

Sensory experience

Experience led

Food & beverage

Leisure as anchor

Engaging events

Surprise & delight

Retail specialism

Optimal retail mix

Fresh concepts

Innovative retail technology

Operational efficiency

Positive Places: Sustainability | Community | Positivity

Appendices

Examples of our Framework in action

53 (1) UK shopping centre portfolio

Victoria Gate awarded Best Shopping Centre at the MIPIM

& MAPIC Awards

New leisure extension & events space at Westquay South attracted over 3.4m visitors

across 2017

Delivered 20 new brands in 2017 across the portfolio(!), including the first VW brand

experience

Launch of Style Seeker AI visual search tool with 90k product impressions since November

2017

Christmas light switch on at Cabot drove a 10.6% increase in daily sales & reached 95k

Facebook users

Award winning Garden of Pure Imagination at Dundrum drove

an 8% uplift in footfall

Nearly 450k downloads of the Plus app with over 3.3m app

opens since launch

Over 130k click & collect parcels handled across our UK

& French centres in 2017

Iconic destinations Retail specialism Experience led Customer first

Appendices

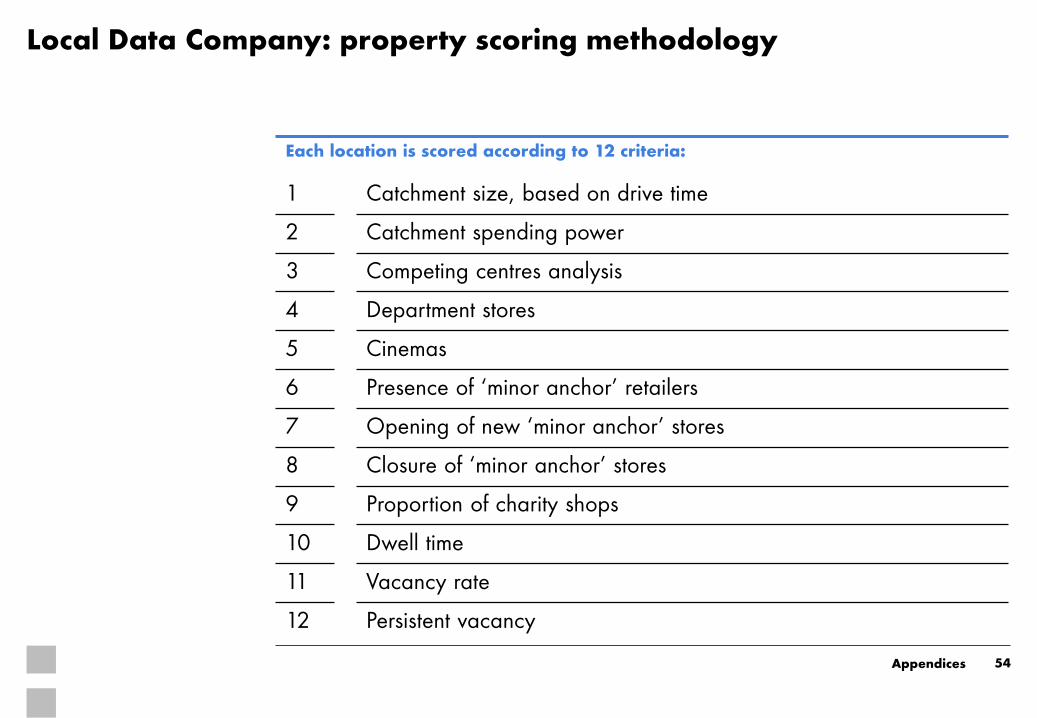

Local Data Company: property scoring methodology

Each location is scored according to 12 criteria:

1 Catchment size, based on drive time

2 Catchment spending power

3 Competing centres analysis

4 Department stores

5 Cinemas

6 Presence of ‘minor anchor’ retailers

7 Opening of new ‘minor anchor’ stores

8 Closure of ‘minor anchor’ stores

9 Proportion of charity shops

10 Dwell time

11 Vacancy rate

12 Persistent vacancy

54 Appendices

Value Retail Villages VIA Outlets centres

Bicester Village, Oxford

GLA: 28,000m2

Boutiques: 157

Batavia Stad Amsterdam Fashion Outlet

GLA: 31,900m2 Units: 119

La Roca Village, Barcelona GLA: 23,500m2 Boutiques: 136

Fashion Arena Prague Outlet GLA: 24,000m2 Units: 99

Las Rozas Village, Madrid GLA: 16,500m2 Boutiques: 102

Freeport Lisbon Fashion Outlet GLA: 35,700m2 Units: 142

La Vallée Village, Paris GLA: 21,900m2 Boutiques: 107

Hede Fashion Outlet, Gothenburg GLA: 16,300m2 Units: 53

Maasmechelen Village, Brussels GLA: 19,800m2 Boutiques: 104

Landquart Fashion Outlet, Zürich GLA: 20,900m2 Units: 75

Fidenza Village, Milan GLA: 20,900m2 Boutiques: 117

Mallorca Fashion Outlet GLA: 33,200m2 Units: 75

Wertheim Village, Frankfurt GLA: 21,200m2 Boutiques: 117

Seville Fashion Outlet GLA: 16,400m2 Units: 62

Ingolstadt Village, Munich GLA: 21,100m2 Boutiques: 112

Wroclaw Fashion Outlet, Poland GLA: 13,700m2 Units: 89

Kildare Village, Dublin GLA: 16,700m2 Boutiques: 91

Zweibrücken Fashion Outlet, Germany GLA: 29,300m2 Units: 112

Vila do Conde Porto Fashion Outlet GLA: 27,800m2 Units: 123

Norwegian Outlet, Oslo GLA: 13,300m2 Units: 77

55

Premium outlets portfolio

Appendices

Hammerson’s total investment in Value Retail (1)

Holding companies 25% equity

Bicester Village

36

50

La Roca Village

26

39

Las Rozas Village

23

35

La Vallée Village

14

26

Maasmechelen Village

14

27

Fidenza Village

23

35

Wertheim Village

33

45

Ingolstadt Village

2

14

Kildare Village

28

41

56 (1) Pro-forma for February 2018 acquisition of LP economic interests (2) Total Village ownership calculated as economic entitlement of directly held and indirectly held interests

Village ownership via LPs (%)

Total Village ownership (%) (2)

Hammerson €2m shareholder loan

Appendices

2017 operational statistics

57 (1) Retail sales on same-centre basis, includes all shopping centres. 2017 UK benchmark -3.0% (Source: Visa Face to Face index); 2017 France benchmark -1.0% (Source: CNCC)

(2) 2017 UK benchmark -2.8% (Source: Tyco Shoppertrak); 2017 France benchmark -1.8% (Source: CNCC) (3) Excludes anchor stores. France data includes VAT (rent:sales and OCR) (4) Excludes anchor stores. France data includes VAT; Jeu de Paume, Beauvais, excluded

Appendices

Occupancy (%) UK shopping centres

UK retail parks

France Ireland Group

31 December 2017 98.1 99.4 97.9 99.7 98.3

30 June 2017 97.2 99.0 96.6 99.9 97.3

31 December 2016 97.8 98.6 96.5 99.5 97.5

UK shopping centres

France

Sales (1) –2.7% 0.1%

Footfall (2) 0.4% 1.6%

Rent:sales (3) 13.3% 11.0%

OCR (3) 21.7% 13.8%

Sales densities(4)

UK £/ft2

France £/ft2

2017 240 – 490 395 – 620

2016 250 – 515 350 – 715

2015 250 – 520 355 – 725 Check number

TBU Add benchmark

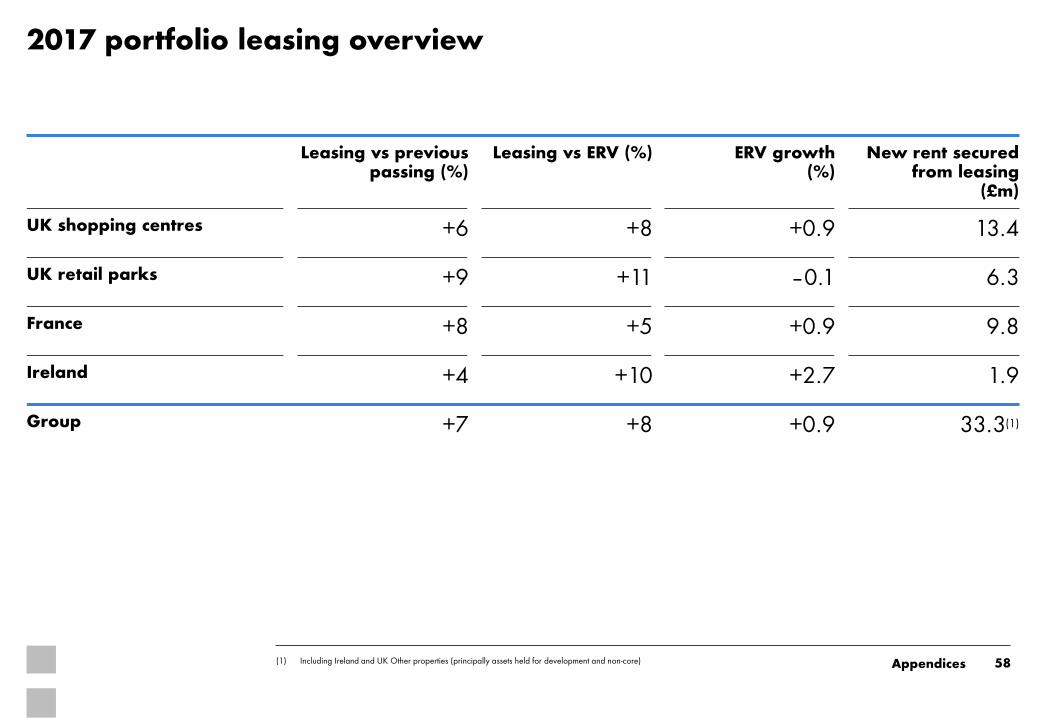

2017 portfolio leasing overview

58 (1) Including Ireland and UK Other properties (principally assets held for development and non-core)

Leasing vs previous passing (%)

Leasing vs ERV (%) ERV growth (%)

New rent secured from leasing

(£m)

UK shopping centres +6 +8 +0.9 13.4

UK retail parks +9 +11 –0.1 6.3

France +8 +5 +0.9 9.8

Ireland +4 +10 +2.7 1.9

Group +7 +8 +0.9 33.3(1)

Appendices

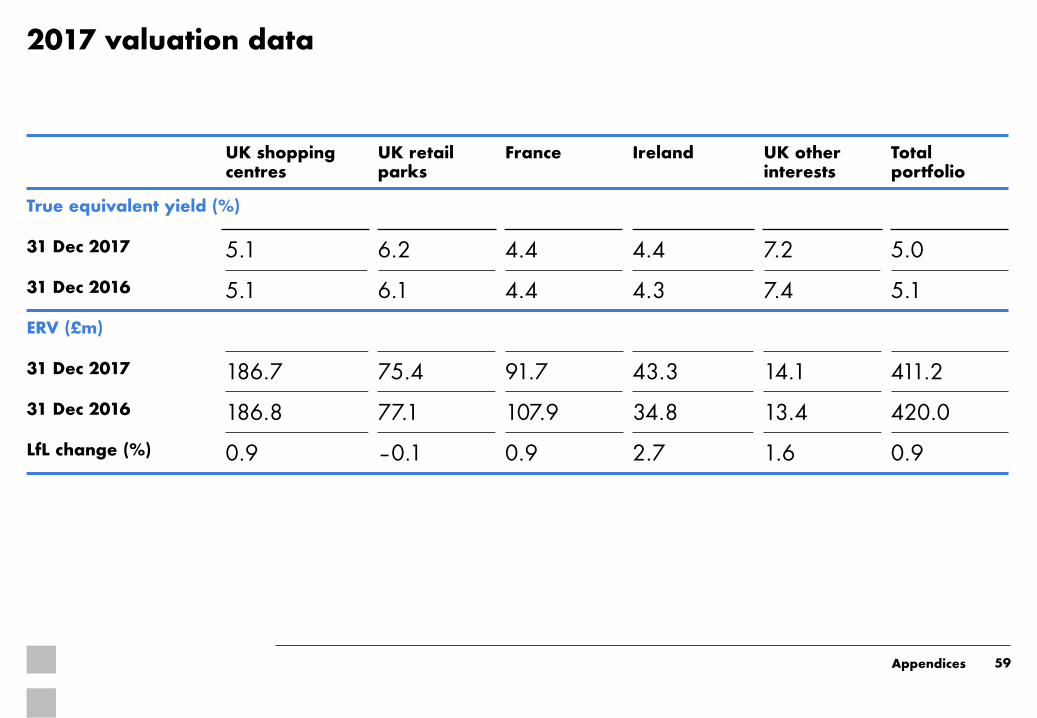

2017 valuation data

59

UK shopping centres

UK retail parks

France Ireland UK other interests

Total portfolio

True equivalent yield (%)

31 Dec 2017 5.1 6.2 4.4 4.4 7.2 5.0

31 Dec 2016 5.1 6.1 4.4 4.3 7.4 5.1

ERV (£m)

31 Dec 2017 186.7 75.4 91.7 43.3 14.1 411.2

31 Dec 2016 186.8 77.1 107.9 34.8 13.4 420.0

LfL change (%) 0.9 –0.1 0.9 2.7 1.6 0.9

Appendices

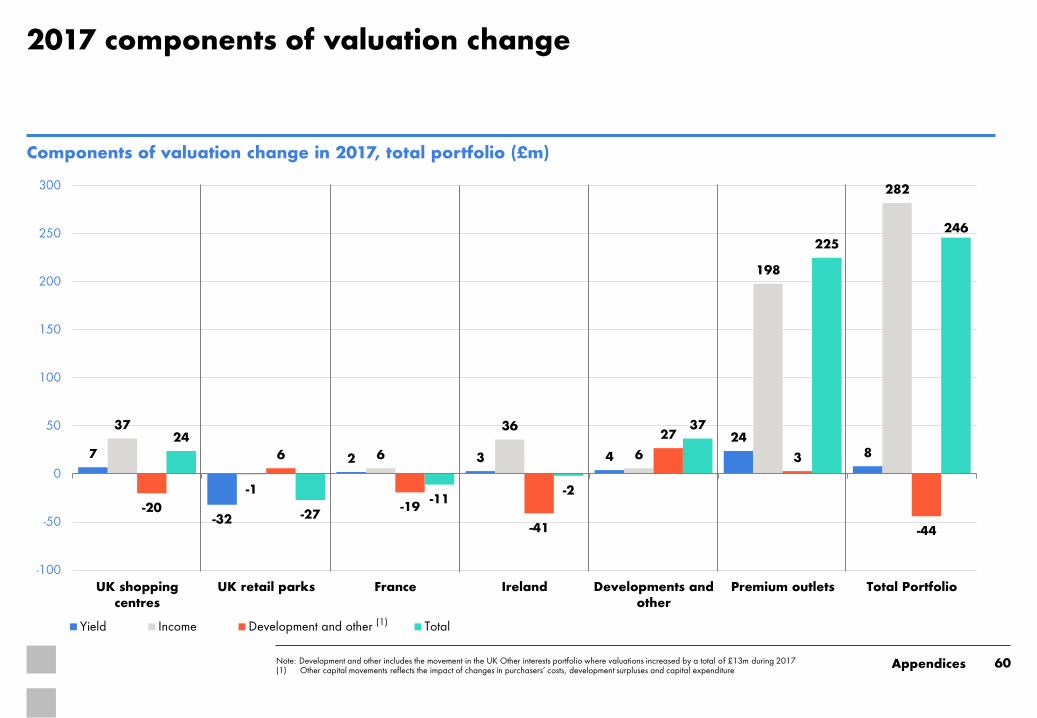

2017 components of valuation change

60 Note: Development and other includes the movement in the UK Other interests portfolio where valuations increased by a total of £13m during 2017 (1) Other capital movements reflects the impact of changes in purchasers’ costs, development surpluses and capital expenditure

Components of valuation change in 2017, total portfolio (£m)

7

-32

2 3 4

24 8

37

-1

6

36

6

198

282

-20

6

-19

-41

27

3

-44

24

-27 -11

-2

37

225 246

-100

-50

0

50

100

150

200

250

300

UK shoppingcentres

UK retail parks France Ireland Developments andother

Premium outlets Total Portfolio

Yield Income Development and other Total

Appendices

(1)

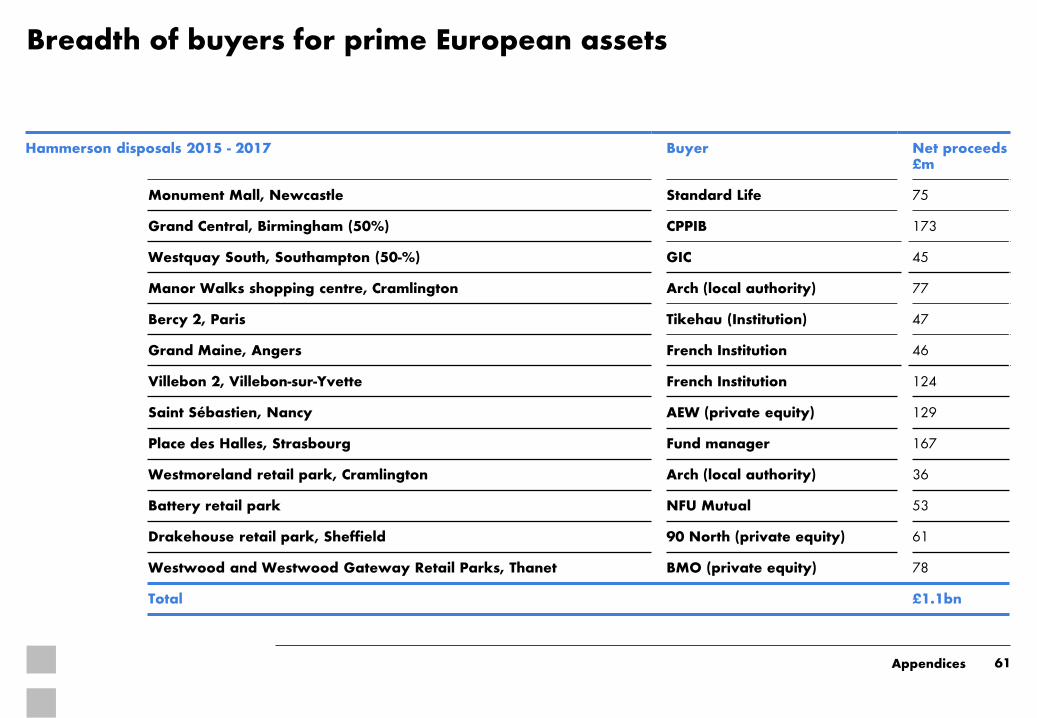

Breadth of buyers for prime European assets

61

Hammerson disposals 2015 - 2017 Buyer Net proceeds £m

Monument Mall, Newcastle Standard Life 75

Grand Central, Birmingham (50%) CPPIB 173

Westquay South, Southampton (50-%) GIC 45

Manor Walks shopping centre, Cramlington Arch (local authority) 77

Bercy 2, Paris Tikehau (Institution) 47

Grand Maine, Angers French Institution 46

Villebon 2, Villebon-sur-Yvette French Institution 124

Saint Sébastien, Nancy AEW (private equity) 129

Place des Halles, Strasbourg Fund manager 167

Westmoreland retail park, Cramlington Arch (local authority) 36

Battery retail park NFU Mutual 53

Drakehouse retail park, Sheffield 90 North (private equity) 61

Westwood and Westwood Gateway Retail Parks, Thanet BMO (private equity) 78

Total £1.1bn

Appendices

Arch – Local Authority (Cramlington, £87m)

Arch – Local Authority (Westmoreland, £36m)

BMO – PE (Thanet, £78m)

NFU Mutual – institution (Battery, £53m)

Drakehouse retial park (90 North – PE £59m)

Hammerson and intu capex 2018-2020

62

Hammerson (£m) 2018 2019 2020

Brent Cross extension 67 94 96

Highcross reconfiguration, Leicester 14 2 0

Whitgift, Croydon 30 10 11

Retail parks schemes 48 34 9

Les 3 Fontaines, Cergy 70 61 56

Italie 2, Paris 35 20 5

Total Hammerson 264 221 176

Intu (£m) 2018 2019 2020

intu Trafford Centre 25 47

intu Watford 77 3

intu Lakeside 52 50

intu Spain 23 157 217

Total intu 177 257 217

2018-2020 1,300

Run-rate 440

Appendices

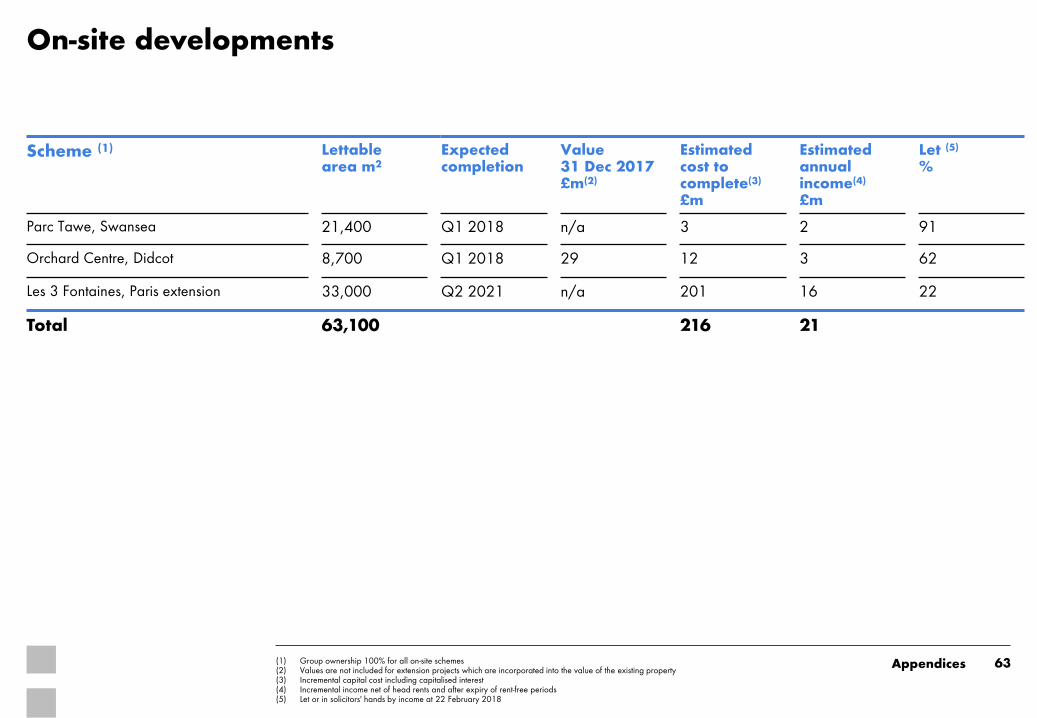

On-site developments

Scheme (1) Lettable area m2

Expected completion

Value 31 Dec 2017 £m(2)

Estimated cost to complete(3)

£m

Estimated annual income(4)

£m

Let (5)

%

Parc Tawe, Swansea 21,400 Q1 2018 n/a 3 2 91

Orchard Centre, Didcot 8,700 Q1 2018 29 12 3 62

Les 3 Fontaines, Paris extension 33,000 Q2 2021 n/a 201 16 22

Total 63,100 216 21

63 (1) Group ownership 100% for all on-site schemes (2) Values are not included for extension projects which are incorporated into the value of the existing property (3) Incremental capital cost including capitalised interest (4) Incremental income net of head rents and after expiry of rent-free periods (5) Let or in solicitors' hands by income at 22 February 2018

Appendices

NB aligned with final press

release

TBC

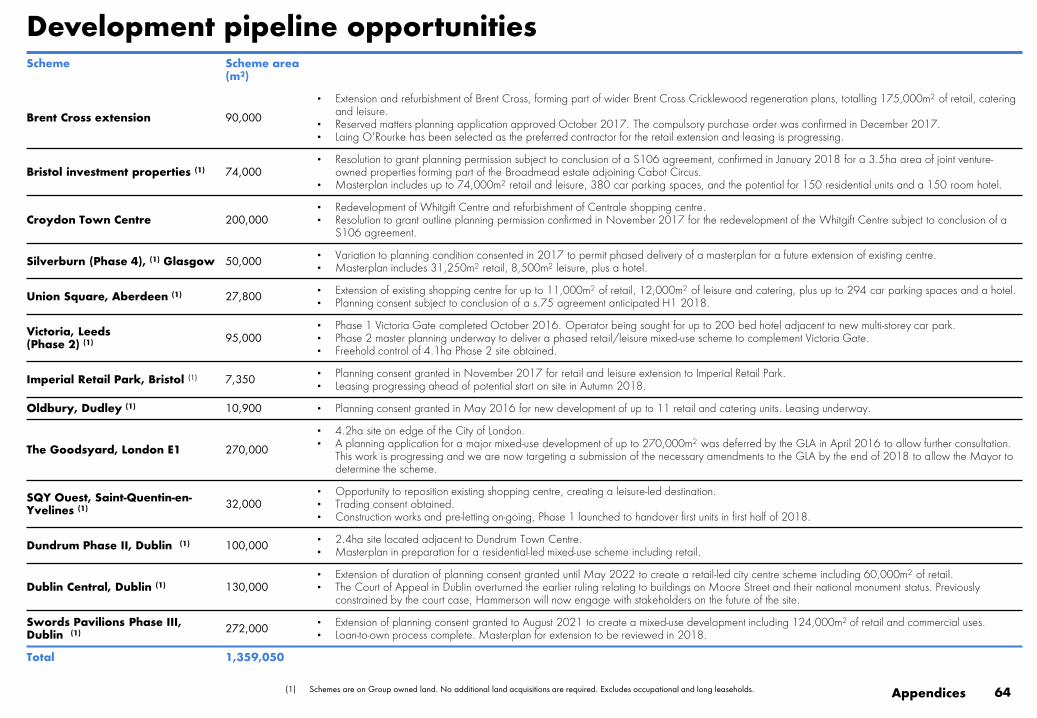

Scheme Scheme area (m2)

Brent Cross extension 90,000

• Extension and refurbishment of Brent Cross, forming part of wider Brent Cross Cricklewood regeneration plans, totalling 175,000m2 of retail, catering and leisure.

• Reserved matters planning application approved October 2017. The compulsory purchase order was confirmed in December 2017. • Laing O'Rourke has been selected as the preferred contractor for the retail extension and leasing is progressing.

Bristol investment properties (1) 74,000 • Resolution to grant planning permission subject to conclusion of a S106 agreement, confirmed in January 2018 for a 3.5ha area of joint venture-

owned properties forming part of the Broadmead estate adjoining Cabot Circus. • Masterplan includes up to 74,000m2 retail and leisure, 380 car parking spaces, and the potential for 150 residential units and a 150 room hotel.

Croydon Town Centre 200,000 • Redevelopment of Whitgift Centre and refurbishment of Centrale shopping centre. • Resolution to grant outline planning permission confirmed in November 2017 for the redevelopment of the Whitgift Centre subject to conclusion of a

S106 agreement.

Silverburn (Phase 4), (1) Glasgow 50,000 • Variation to planning condition consented in 2017 to permit phased delivery of a masterplan for a future extension of existing centre. • Masterplan includes 31,250m2 retail, 8,500m2 leisure, plus a hotel.

Union Square, Aberdeen (1) 27,800 • Extension of existing shopping centre for up to 11,000m2 of retail, 12,000m2 of leisure and catering, plus up to 294 car parking spaces and a hotel. • Planning consent subject to conclusion of a s.75 agreement anticipated H1 2018.

Victoria, Leeds (Phase 2) (1) 95,000

• Phase 1 Victoria Gate completed October 2016. Operator being sought for up to 200 bed hotel adjacent to new multi-storey car park. • Phase 2 master planning underway to deliver a phased retail/leisure mixed-use scheme to complement Victoria Gate. • Freehold control of 4.1ha Phase 2 site obtained.

Imperial Retail Park, Bristol (1) 7,350 • Planning consent granted in November 2017 for retail and leisure extension to Imperial Retail Park. • Leasing progressing ahead of potential start on site in Autumn 2018.

Oldbury, Dudley (1) 10,900 • Planning consent granted in May 2016 for new development of up to 11 retail and catering units. Leasing underway.

The Goodsyard, London E1 270,000

• 4.2ha site on edge of the City of London. • A planning application for a major mixed-use development of up to 270,000m2 was deferred by the GLA in April 2016 to allow further consultation.

This work is progressing and we are now targeting a submission of the necessary amendments to the GLA by the end of 2018 to allow the Mayor to determine the scheme.

SQY Ouest, Saint-Quentin-en-Yvelines (1) 32,000

• Opportunity to reposition existing shopping centre, creating a leisure-led destination. • Trading consent obtained. • Construction works and pre-letting on-going, Phase 1 launched to handover first units in first half of 2018.

Dundrum Phase II, Dublin (1) 100,000 • 2.4ha site located adjacent to Dundrum Town Centre. • Masterplan in preparation for a residential-led mixed-use scheme including retail.

Dublin Central, Dublin (1) 130,000 • Extension of duration of planning consent granted until May 2022 to create a retail-led city centre scheme including 60,000m2 of retail. • The Court of Appeal in Dublin overturned the earlier ruling relating to buildings on Moore Street and their national monument status. Previously

constrained by the court case, Hammerson will now engage with stakeholders on the future of the site.

Swords Pavilions Phase III, Dublin (1) 272,000

• Extension of planning consent granted to August 2021 to create a mixed-use development including 124,000m2 of retail and commercial uses. • Loan-to-own process complete. Masterplan for extension to be reviewed in 2018.

Total 1,359,050

Development pipeline opportunities

(1) Schemes are on Group owned land. No additional land acquisitions are required. Excludes occupational and long leaseholds.

64 Appendices

NB aligned with final press

release

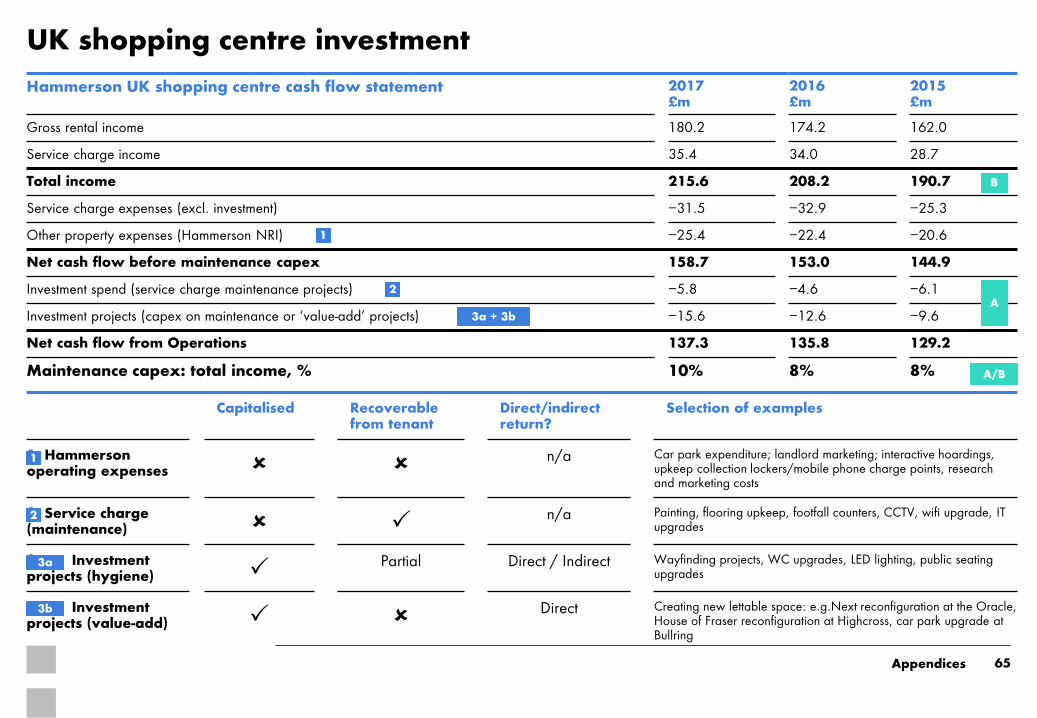

UK shopping centre investment

65

Capitalised Recoverable from tenant

Direct/indirect return?

Selection of examples

1. Hammerson operating expenses n/a Car park expenditure; landlord marketing; interactive hoardings,

upkeep collection lockers/mobile phone charge points, research and marketing costs

2. Service charge (maintenance) n/a Painting, flooring upkeep, footfall counters, CCTV, wifi upgrade, IT

upgrades

3.a Investment projects (hygiene) Partial Direct / Indirect Wayfinding projects, WC upgrades, LED lighting, public seating

upgrades

3.B Investment projects (value-add) Direct Creating new lettable space: e.g.Next reconfiguration at the Oracle,

House of Fraser reconfiguration at Highcross, car park upgrade at Bullring

2014 2015 2016Ref £m £m £m

Gross rental income 149.4 162.0 174.2Service charge income 27.0 28.7 34.0Total income 176.4 190.7 208.2Service charge expenses (excl. maintenance capex) (23.5) (25.3) (32.9)

1 Other property expenses (Hammerson NRI) (19.4) (20.6) (22.4)Net cash flow before maintenance capex 133.5 144.9 153.0

2 Maintenance capex - service charge (Service charge P&L) (5.6) (6.1) (4.6)3 Maintenance capex - land and buildings (Hammerson L&B) (9.7) (9.6) (12.6)

Net "cash flow" from Operations 118.2 129.2 135.8Maintenance capex:Total income, % 9% 8% 8%

Hammerson UK shopping centre cash flow statement 2017 £m

2016 £m

2015 £m

Gross rental income 180.2 174.2 162.0

Service charge income 35.4 34.0 28.7

Total income 215.6 208.2 190.7

Service charge expenses (excl. investment) −31.5 −32.9 −25.3

Other property expenses (Hammerson NRI) −25.4 −22.4 −20.6

Net cash flow before maintenance capex 158.7 153.0 144.9

Investment spend (service charge maintenance projects) −5.8 −4.6 −6.1

Investment projects (capex on maintenance or ‘value-add’ projects) −15.6 −12.6 −9.6

Net cash flow from Operations 137.3 135.8 129.2

Maintenance capex: total income, % 10% 8% 8%

1

2

3a + 3b

1

2

A

B

A/B

3a

3b

Appendices

31 Dec 2017

Net debt

Reported (£m) Fully proportionally consolidated (£m)

Group 3,501 3,501

VIA Outlets - 174

Value Retail - 512

Loan 3,501 4,187

Property values

Group 8,326 8,326

VIA Outlets - 600

Value Retail - 1,634

Less minority interest (14) (14)

VIA Outlets net assets 361 -

Value Retail net assets 1,069 -

Value 9,742 10,546

LTV 36% 40%

LTV methodology

66 Appendices

67

0

100

200

300

400

500

600

700

800

900

1000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Revolving credit facilities

Private placement

Sterling bonds

Euro bonds

Secured debt

Debt maturity profile 31 December 2017 (£m) Continuing to take advantage of refinancing opportunities

TBU

Appendices

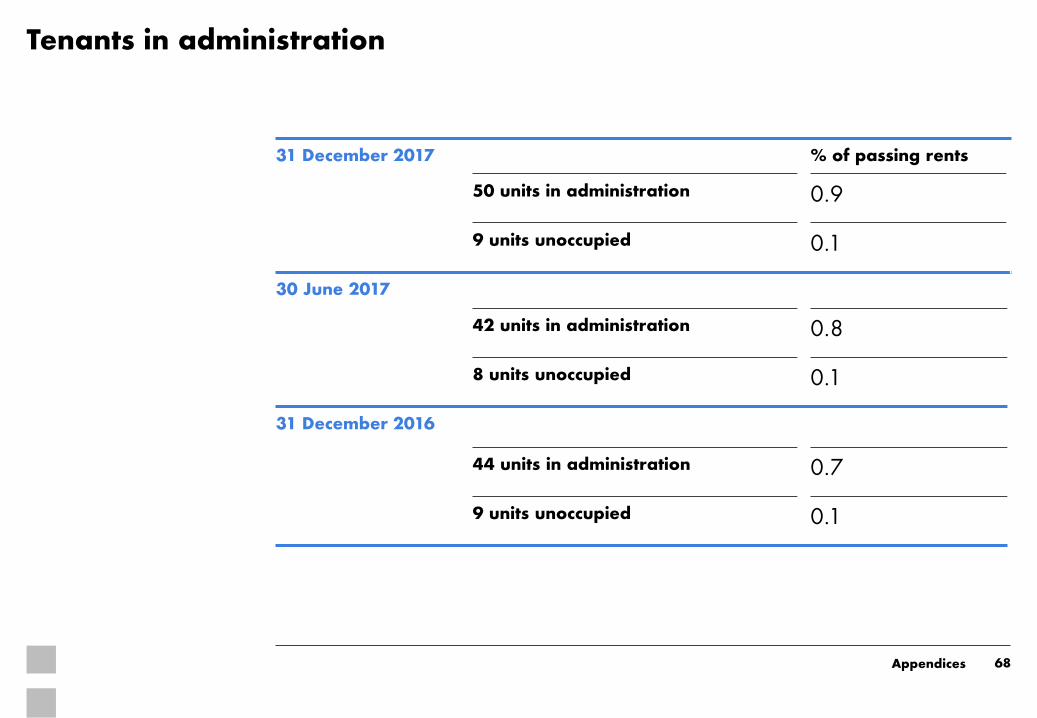

Tenants in administration

68

31 December 2017 % of passing rents

50 units in administration 0.9

9 units unoccupied 0.1

30 June 2017

42 units in administration 0.8

8 units unoccupied 0.1

31 December 2016

44 units in administration 0.7

9 units unoccupied 0.1

Appendices

TBC

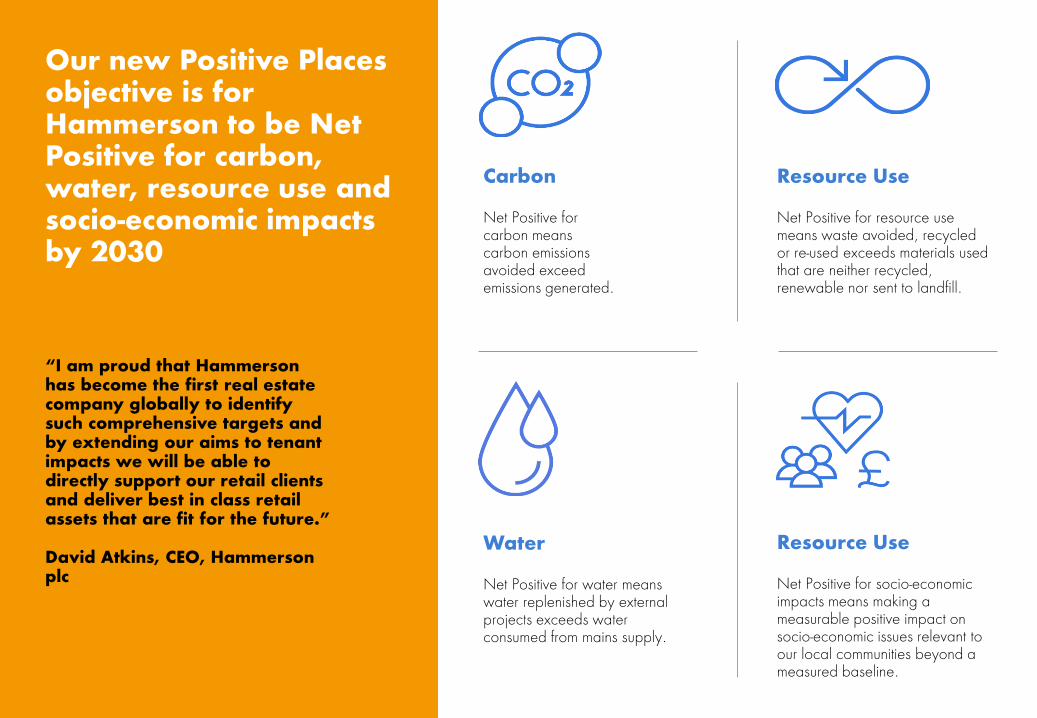

Our new Positive Places objective is for Hammerson to be Net Positive for carbon, water, resource use and socio-economic impacts by 2030

Carbon Net Positive for carbon means carbon emissions avoided exceed emissions generated.

Resource Use Net Positive for resource use means waste avoided, recycled or re-used exceeds materials used that are neither recycled, renewable nor sent to landfill.

Water Net Positive for water means water replenished by external projects exceeds water consumed from mains supply.

Resource Use Net Positive for socio-economic impacts means making a measurable positive impact on socio-economic issues relevant to our local communities beyond a measured baseline.

“I am proud that Hammerson has become the first real estate company globally to identify such comprehensive targets and by extending our aims to tenant impacts we will be able to directly support our retail clients and deliver best in class retail assets that are fit for the future.” David Atkins, CEO, Hammerson plc

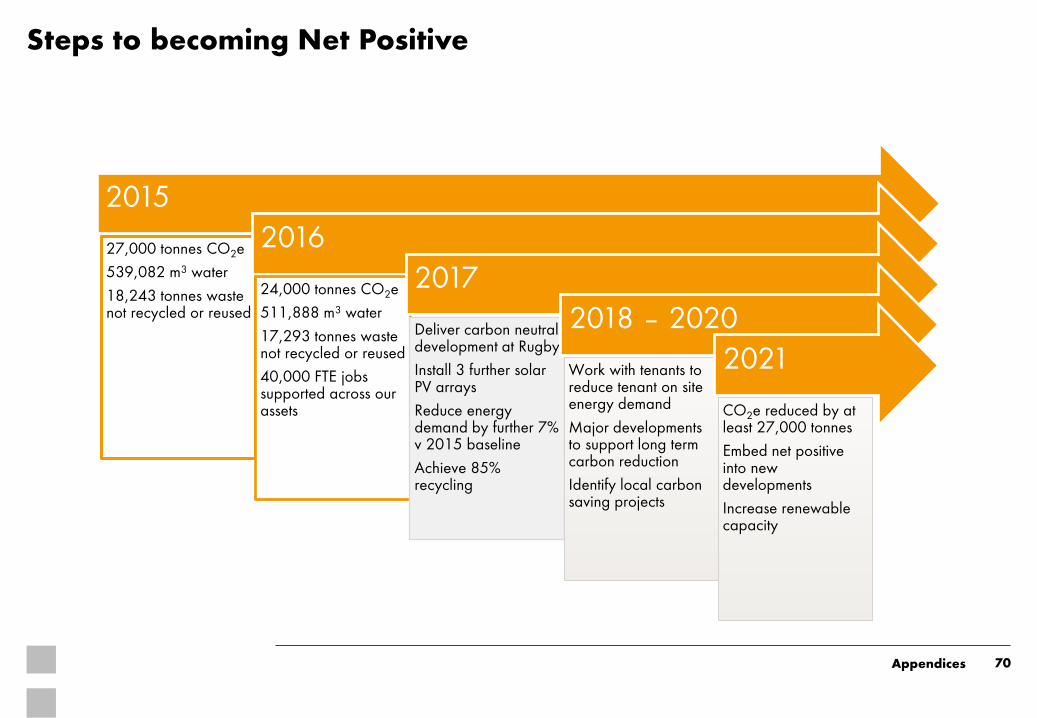

Steps to becoming Net Positive

2015

27,000 tonnes CO2e

539,082 m3 water

18,243 tonnes waste not recycled or reused

2016

24,000 tonnes CO2e

511,888 m3 water

17,293 tonnes waste not recycled or reused

40,000 FTE jobs supported across our assets

2017

Deliver carbon neutral development at Rugby

Install 3 further solar PV arrays

Reduce energy demand by further 7% v 2015 baseline

Achieve 85% recycling

2018 – 2020

Work with tenants to reduce tenant on site energy demand

Major developments to support long term carbon reduction

Identify local carbon saving projects

2021

CO2e reduced by at least 27,000 tonnes

Embed net positive into new developments

Increase renewable capacity

70 Appendices

Our 2017 sustainability highlights

71

Delivered the world’s first BREEAM Outstanding, carbon neutral retail park at Elliott’s Field, Rugby

Developed the second zero energy Costa Coffee EcoPod at Parc Tawe, Swansea

Managed exposure to Mimimum Energy Efficiency Standards (MEES) risk out of the UK portfolio

Installed additional 910 kWp clean electricity capacity

Achieved 3% improvement in the carbon intensity of the business, one of our corporate KPIs

Recycled 73% of waste across our UK, France and Ireland portfolios

Supported over 100 people with skills training and into employment at our shopping centres

Supported over 70 business-start-ups in France and 400+ entrepreneurs in the UK through the Initiative France and Pop-Up Business

Appendices