FOCUS: Journal of International Business

Vol. 5(1), Jan-Jun 2018, pp. 81-95

DOI: 10.17492/focus.v5i01.13139

www.journalpressindia.com/fjib

© 2018 Journal Press India

Impact of Foreign Institutional Investors on the Volatility of Indian Stock

Market using GARCH Model

Prateek Kumar Bansal* and Om Prakash Agrawal**

ABSTRACT

Foreign institutional investors have played an important role in the development of

Indian stock market. In this paper, we study the relationship between the FII capital

flows and the volatility of Indian stock market. To conduct the study, daily Index and

trading data of SENSEX, NIFTY and FIIs was collected for fifteen years from April 1,

2001 to March 31, 2017. After testing for data stationarity using Augmented Dickey

Fuller test (ADF) unit root test, different statistical tools were applied such as S.D.,

mean, variance, skewness, correlation and GARCH model for testing the impact of FIIs

flows on stock market volatility. The study concludes that there is strong relationship

between the FIIs and the stock market return. Further, positive correlation exists

between the variables and volatility transmission is there from FIIs to both the indices.

Keywords: FIIs; Indian Stock Market; NIFTY; SENSEX; GARCH.

1.0 Introduction

For the big challenge to create investment opportunities for the investor. There are a

lot of factors which economy it’s a affect the investors’ decision which includes economic

condition, returns, market future, political situations, Growth etc. Investors outside India can

invest in two ways - Foreign Direct Investment (FDI) where investment is made directly to

a firm and other is Foreign Institutional Investors (FIIs) where they can invest to the equity

and debt market of the destination economy in the listed or unlisted securities of the

companies. FDI is considered as a developmental tool and they help in achievement of

robust growth of an economy. It helps in capital formation, enhancing efficiency of the

economy and development of infrastructure.

_____________________

*Corresponding author: Assistant Professor, Institute of Business Management, GLA University,

Mathura, Uttar Pradesh, India. (Email: [email protected])

**Assistant Professor, Institute of Business Management, GLA University, Mathura, Uttar

Pradesh, India. (Email: [email protected])

82 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

On the other hand, FIIs are the foreign investors who plays a dynamic role in

development of economy and shape the stock market and effect the stock prices of

companies in the country. Foreign institutional investment provides various ways of

financing by sharing different risk and return of stock market (Han at el., 2000;

Singhania and Saini, 2016).

India receives more than 19.788 million US $ from the investment done by the

FIIs during the April to December 2017. Further, if we compare current year then, it

shows the highest year FIIs volume of investment to previous trend. The reasons can be

enumerated as changing government policies which back the expectations of FIIs and

falling interest rates, improving earnings outlook, low barriers for FIIs investment and

introduction of reform in indirect taxation (GST) etc.

FII can invest in the debt as well as equity market which stood in the year 2017

as 7.46 billion US $ and as cumulative value stood $183.69 billion. India records high in

terms of investment in the private equity investment which worth’s 24.4 billion US $ and

the private equity investment shows the growth rate of 9% in the logistic industry which

leads to the investment of $501.71 million during 2016-17.

FIIs investment improves the market efficiency as it leads to decline in the cost

of capital but FIIs capital flow in stock market affect the indexes which create volatility

in stock market. The reason of volatility is that FIIs tap the primary market because they

deploy large amount at a fixed price in one go which is not possible in secondary market

easily and FIIs capital flow affect primary market stock usually relatively at low price as

compared to secondary market. The FIIs affects investment pattern of domestic investors

also. Hence, it becomes imperative to study the association between select indices and

FII flows. Further, volatility transmission can also be assessed between FIIs flows and

SENSEX and NIFTY.

Volatility is explained as the degree of changes in price between the share prices

of a security for a period. Sometime volatility is required in the stock market so that the

interest of investors is there and they invest in the way of market ups and down, this

desirable action changes value across economic activities which facilitate for the

allocation of resources but on the other hand when this volatility is high then investors

feel lack of confidence which can be negative for the economic growth. Volatility

describes the stability and instability of any variable. It can also be used as a common

statistical measure of depression of regularity in any random variable such as market-to-

market values, earnings, losses due to default, market value etc. Many a times it is

questioned that the Foreign Investors create volatility in stock market and they affect the

inflow and outflow in stock market. so this study is related to study the FIIs impact on

the Volatility of India’s two largest stock exchanges.

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 83

Government is taking numerous initiatives to increase the Foreign Investment.

The Securities and Exchange Board of India (SEBI) has increased the limit up to 25%

for the strategic investors so that they can make boost up in the REITs and INvlTs. The

Govt. of India has made major reforms in the economy like demonetization and

implementation of GST. As SEBI regulates all the securities markets, hence it creates

rules and regulation for the purpose of making securities markets a safe avenue for

investors to invest

SEBI has made changes in their regulation as SEBI (FII) regulation 1995 to

SEBI(FPI) regulation 2014 in June 2014. Which merge all FIIs, QFIIs and Sub-accounts

of FIIs are FPIs. It’s effect was that the number of registered investors increased in the

Indian stock markets.

More than 1300 new FPIs are get registered during the year as compared to the

previous year this is because of the continuous interest of the foreign investors in the

Indian equity and debt market (Figure 1). In the previous year total registered FPIs are

7807 and in this year it is 9136. SEBI to control and manage approved depositories to

make the procedure easy and they work as an intermediary between the FIIs and SEBI

they care called DDPs after getting the certificate form the SEBI.

Figure 1: Country-Wise AUC (Crore) and Number of Registered FPIs

Source: SEBI Annual Report 2016-17

3024

1007

677 608 518

493

392

304

1758

857945

238682

72,299 511293

136022

71,043

73,082

274472

470930 AUC

No.of FIIs

USA

Luxembourg

Canada

Mauritius

UnitedKingdomIreland

Japan

84 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

According to the SEBI annual report 2016-17, 18 DDPs are approved and total

FPIs registered shown in fig 1 was from the USA (3024); Luxembourg (1,007), Canada

(677) and Mauritius (608) (Figure 2.25). In terms of AUC as well, FPIs from the USA

had the maximum AUC (8,57,945 crore), followed by Mauritius (5,11,293 crore),

Singapore (2,74,472 crore) and Luxembourg (2,38,642 crore).

The opportunities to get more investment in the future by the foreign investors is

expected because of the growth in the economic condition and the strong support from

the side of Government. Most of the investors seek the developing countries to invest

their funds because there is more chance of growth in Indian market as it shows the best

investment destination based on the various variables like long – term economic growth

potential demographic growth and increase productivity.

2.0 Review of Literature

Mukherjee et al. (2002) empirically tests the relationship of FIIs flows to the

Indian equity market. Author taken daily traded time series data from 1999 to 2002 and

also tries to explore the interrelationship by using Granger causality test. Author

concluded that the flow of FIIs is total based upon the near past return of the stock and

there is no other way. Prasanna (2008) examined the relationship of BSE listed

companies’ share price and the FIIs. Author concluded that the FIIs are willing to invest

their fund only in those share which are owned by the general public in large number.

Author also tried to establish the relationship among the investment and capital structure,

financial performance and stock performance.

Chandra (2012) examined the cause and effect relationship between the trading

behaviour of FIIs and the Stock market return. The main purpose of this paper was to

explain the direction of relationship between them and vice versa. Using Granger-

causality approach author find that FIIs and India stock market return have bi-directional

relationship and also suggested that the stock market return causes the change in the

behaviour of FIIs trading. Dharani et.al. (2015) examined the volatility pattern of Shariah

complaint stocks in India. At first author calculated the return for each Shariah complaint

stock and secondly data tested for stationery by using ADF test and then autocorrelation

by using Q test. This study revealed that the return series showing stationary at level and

the existence of autocorrelation for all selected Shariah compliant stocks.

Garg and Mitra (2015) stated that the foreign ownership of host country’s stocks

increase due to liberalization of financial markets in emerging economies. Huge amount

of investment through FIIs may have a prominent impact on host country’s stock market.

In this study the author wants to investigate the investment pattern of FIIs investment

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 85

and their relation with the return of Indian stock market. Author concluded that FIIs

investment pattern can create the short term volatility and also suggested that FIIs are

having intense to buying rather than focusing on sale side.

Kumari and Mahakud (2015) examined the relationship between stock market

volatility and macroeconomic volatility in Indian stock market. In this study author

examined the problem with two phase estimation techniques. Conditional volatility is

take out by using univariate autoregressive conditional heteroscedasticity models and for

further analysis author used multivariate VAR technique with the impulse response.

Author find linkage between stock market volatility and macroeconomic volatility.

Dhingra et.al. (2016) investigated the interactions of FIIs with market volatility and

market return in the context of India by using daily basis data and used static and

dynamic models both. According to them foreign investors have positive feedback

traders at the time of investment and negative feedback traders at the time of withdrawal.

Poshakwale and Mandal (2016) studied the sources of stock return in both

economic and non-economic terms in the emerging Indian stock market as well as in the

established stock market of US, Germany, U K, France, Canada and Japan. Authors

concluded that the probability value s higher in economic expansion system as compared

to the economic contraction system. It is also revealed that inflation, uncertainty,

international interest rates and dividend yields are the main components of asymmetric

return in co-movements. Singhania and Saini (2016) states that FIIs ownership does not

provide only adequate capital but also marketing skills, managerial skills, business

connections and training to the host country. FIIs provide alternative ways of financing

by sharing the risk in the domestic stock market, and they reduce the risk exposure of

listed firms. Additionally, FIIs inflow help to improve the quality of information in

domestic markets with good corporate governance.

Vyas and Shah (2016) studied the quarterly appraisal between the FIIs and their

impact on the SENSEX movement. Author used regression analysis to find the

significance effect of FIIs on the SENSEX movement and also used t-test to find the

significant relationship between them and taken 5 years’ data of SENSEX and FIIs. They

concluded that FIIs not having any significant impact on the share price movement and

there is no significant relationship exist between them and also suggested to take the

weekly data for the further study.

3.0 Objectives

To understand the dynamics of relation between foreign institutional investors and

Indian stock market.

86 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

To examine the trend of Indian major stock exchange and FIIs.

4.0 Research Methodology

The main aim of this paper is to determine whether there is some relationship

exists between the stock market indices return and Foreign Institutional investors in this

paper the volatility of Indian stock market is also determine. To complete the objective

secondary data from April 1st 2001 to March 31

st 2017 has been used. Daily trading data

of FIIs, Daily closing data of National stock exchange index (NSE) and Bombay stock

exchange index (SENSEX) data has been collected from www.sebi.gov.in,

www.nseindia.com, www.bseindia.com and the depository of SEBI websites

https://www.fpi.nsdl.co.inandhttps://www.cdslindia.com. FIIs net investment data used

of equity and debt market.

Eviews 9.0 software used to apply the tools to find out the results. To find out

the volatility tools S.D. (Standard Deviation), correlation and GARCH Model are used.

At First correlation between the FIIs and Indian Stock Exchange will be considering and

after that data converted in to stationarity because the data is time series, to convert data

into stationarity Augmented Dickey Fuller test is used. and Finally, Foreign Institutional

Investors Volatility is checked using GARCH model according to Kim and Singhal

(1993);Agarwal (1997); Radelet and Sachs, (1998); buckley et. al., (2002); Batra (2003);

Singh (2004); Kulwantraj, (2004); pal (2005); Bhattacharya and Mukherjee (2005);

Biswas (2005); Mohan (2006); Upadhyay (2006); Karmakar (2006); Banerjee and Sarkar

(2006);Behera (2010); Gupta (2011);Sultana and Pardhasadhi (2012).

4.1 Hypothesis

H0: There is no significant impact of FIIs on the Volatility of Indian Stock

Market.

H1: There is significant impact of FIIs on the Volatility of Indian Stock Market.

4.2 Stationary test

Stationarity of data means when a data is constant over a time period in

reference to mean and its deviation. As, the time series tools can be applied only if the

select time series is stationary. It means the mean and variance are not varying with time.

In this study, Foreign Institutional Investors Daily Net Purchase and sale in Equity as

well as in debts Market is considered.

In statistics, the Dickey-Fuller test check the hypothesis that data is stationarity

or not and unit root is present in an autoregressive model.

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 87

In present study to check the relationship the Augmented Dickey Fuller (ADF)

test is used.

Null Hypothesis is that Data is stationarity

Alternative Hypothesis is data is not stationarity

To check the hypothesis, the following equation is used

∇𝑦𝑡 = 𝛿𝑦𝑡−1 + 𝑢𝑡

In the above equation, the null hypothesis of unit root, 𝛿 = 0 is taken and the

alternative hypothesis of 𝛿 < 0 is tested. So, the null hypothesis of non-stationarity

would be rejected, if, 𝛿 is negative and significantly different from zero.

4.3 Model used

To check the volatility, the most appropriate tools by Modern economics is the

least square model. In this it is determine that how much one variable will change the

response of other variable.

Least square model assumes that the expected value of the all error tem and

when it is squared at the same given point. This process is called homoscedasticity and

this assumption focused on ARCH and GARCH Model. These Models are used as basic

model to use the volatility in data.

5. 0 Empirical Results and Findings

5.1 Trend analysis

Figure 2 depicts the trend analysis and it shows that the flow of FIIs is increasing

from time to time and in the last decades it shows more fluctuations. It means that FIIs

have interest in Indian Stock Market. Various factors do influence FIIs investment

behaviour like political situation, inflation, market condition and investment

opportunities, Stock returns etc. FIIs shows positive interest in Indian economy because

of investment opportunities is available in Indian Market. BSE SENSEX and NSE

NIFTY are the Indian Stock Market Index which is well recognizable in Indian as well

as in international market. The trend of daily net trade of FIIs and daily closing of both

the indexes is presented and all variables are moving together and show increasing trend

from April 1st 2001 to March 31

st 2017.

5.2 Descriptive analysis

Table 1 depicts the central tendency and dispersion properties of the data series.

It comprises of mean, maximum, minimum values, median, standard deviation. It also

tells about presence of asymmetry and peak in the data series through skewness and

88 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

kurtosis respectively. From the table it is evident that both indices bear same amount of

risk i.e. 1.65% and 1.67% but risk in SENSEX is relatively more.

Figure 2: Present the Flow of NIFTY, SENSEX and NET FIIs

-20,000

-10,000

0

10,000

20,000

30,000

40,000

01 02 03 04 05 07 08 09 10 11 12 13 14 15 16

Net FIIs Nifty Sensex

Source: Computed data

Table 1: Descriptive Analysis of NIFTY, SENSEX and NET FIIs

NET_FIIS NIFTY_RETURN SENSEX_RETURN

Mean 295.4889 0.000575 0.000583

Median 104.6000 0.000766 0.000807

Maximum 16377.57 0.409962 0.443217

Minimum -10675.40 -0.130539 -0.118092

Std. Dev. 1336.725 0.016597 0.016743

Skewness 1.853093 3.977256 5.051912

Kurtosis 25.16077 111.0501 142.5194

Jarque-Bera 76040.83 1768052. 2947394.

Probability 0.000000 0.000000 0.000000

Sum 1068193. 2.078151 2.106317

Sum Sq. Dev. 6.46E+09 0.995510 1.013166

Observations 3615 3615 3615

Source: Computed data

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 89

Further the value of skewness is more than 0 and value of kurtosis is more than 3

for all the data series, hence it confers the presence of asymmetry in the data. All the

series are positively skewed. The p value of Jarque-Bera statistic is less than .05 which

means the rejection of null hypothesis that data is normal.

5.3 Volatility analysis

Volatility is a rate in which the security increases or decreases for a given set of

returns. it measures the S.D. (Standard Deviation) over the time period and estimate the

fluctuations. Stock Market Volatility indicates the variances between the Indexes during

a particular time period. Stock market is fluctuating timely because of different

economic activities which is desirable but when it fluctuate more then it creates

uncertainty in market which shakes the confidence of the investor. While the overall

stock market volatility has fluctuated over the time with no discernible trend, some

authors have argued that volatility is higher during the bear markets.

5.4 Correlation analysis

Correlation analysis is a method of statistics in which the degree of relation is

checked between two or more variable. Positive correlation shows that if one variable

change systematically then other variable is also have some systematic change. To find

the relationship between the Net Flows of FIIs, NIFTY and SENSEX Pearson correlation

analysis is used. 16 years Daily Closing Index data is taken and Daily Net traded data is

taken for Net FIIs. Table 2 shows the output of Correlation between all the variable.

From Table 2, it is concluded that there is positive Correlation between Net FIIs and

NIFTY (.141) and SENSEX (.139). There is a significant and positive relationship exists

between the Stock market and FIIs Investment.

Table 2: Correlation Analysis

Variable Correlation Significance Value

Net FIIs 1 0.0000

Sensex .141**

0.0000

Nifty .139**

0.0000

Source: Computed data

5.5 Augmented Dickey Fuller (ADF) test

Stationarity of time series data is required to apply the GARCH and ARCH

Model. Firstly, to apply the test, collected data is required to test for stationary properties

and for this Graph (to examine trend in the data) and Augmented Dicky Fuller Test is

90 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

used. As already stated that following indices -NIFTY and SENSEX are taken for this

purpose. In this null Hypothesis (H0) is that data is stationary and Alternative

Hypothesis (H1) is data is non-stationary and after that data is tested on different levels.

Log returns are calculated for the closing values of SENSEX and NIFTY by the

following formula:

Log returns= ln(P1-P0)

The results of Augmented Dickey Fuller (ADF) test shows that H0 is rejected

because the t-statistic is -56.12776 for NSE NIFTY and -55.99155 BSE Sensex, -

14.94466 for NETFIIS and the probability value is less than 0.05. Hence, NIFTY and

SENSEX is not having any unit root problem which is basic requirement for GARCH

model. Now GARCH (1,1) model is applied to check the volatility of FIIs on stock

market.

Table 3: Stationary Test Results of ADF Test

Augmented Dickey-Fuller test statistic

Variables t-Statistic Prob.*

Test critical values:

1% level 5% level 10% level

FIIs Net -14.9447 0.0000 -3.43198 -2.86214 -2.56714

Nifty Return -56.1278 0.0001 -3.43197 -2.86214 -2.56713

SENSEX Return -55.9916 0.0001 -3.43197 -2.86214 -2.56713

*MacKinnon (1996) one-sided p-values.

Source: Computed Data

5.6 GARCH Test

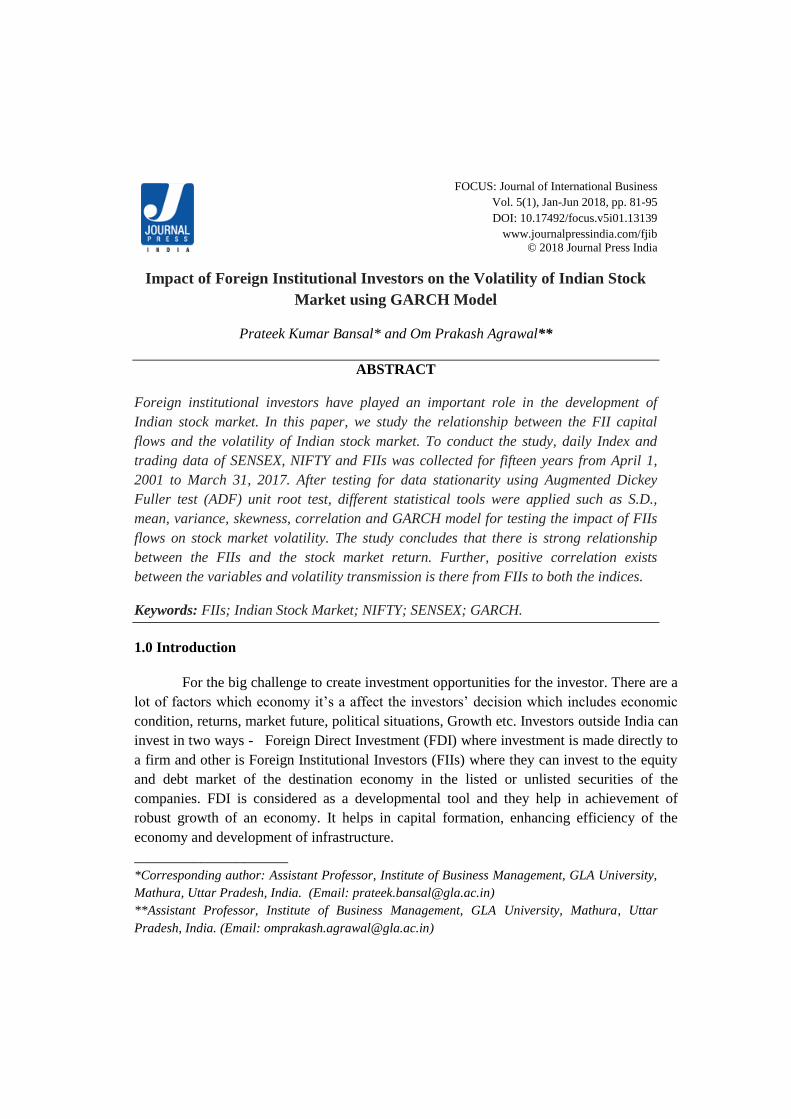

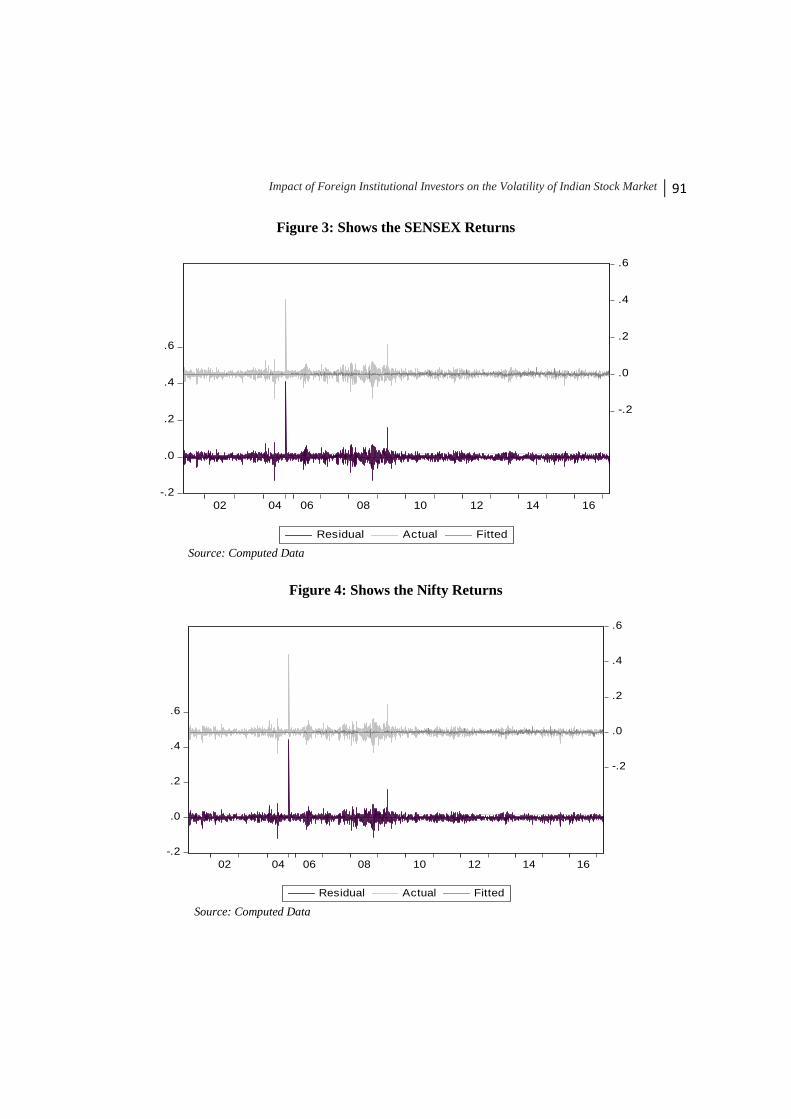

The results of Figure 3 and Figure 4 show the presence of ARCH effect in the

residuals. It means that period of high volatility is followed by high volatility and periods

of low volatility are followed by low volatility. Finally, after converting data into

stationarity GARCH (1,1) Model is used to get the results. Two different equations

prepare, in first equation NET FIIs consider as independent variable and NIFTY is

considering as dependent variable. In Second equation SENSEX is considering as

dependent variable.

The GARCH results of NIFTY return sows that the significant level and have

influenced by the information provided to them and results related to the SENSEX is

similar to the NIFTY. It is concluded that the FIIs Investment does have influence on the

Stock market volatility of India.

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 91

Figure 3: Shows the SENSEX Returns

-.2

.0

.2

.4

.6

-.2

.0

.2

.4

.6

02 04 06 08 10 12 14 16

Residual Actual Fitted Source: Computed Data

Figure 4: Shows the Nifty Returns

-.2

.0

.2

.4

.6

-.2

.0

.2

.4

.6

02 04 06 08 10 12 14 16

Residual Actual Fitted Source: Computed Data

92 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

6.0 GARCH Model

Model 1: Independent Variable NET FIIs Flows and Dependent Variable as SENSEX

RETURNS)

The result of Model 1 states that there is significant effect of ARCH and

GARCH on the Sensex returns. It means that current volatility is influenced by past

volatility. Also, the square values of the lag variables are significant. Further the series is

affected by volatility in values of FIIS as p value < 5% for all the series.

Table 4: GARCH Test with the Independent Variable as Net FIIs Flows and

Dependent as SENSX

GARCH = C(3) + C(4)*RESID(-1)^2 + C(5)*GARCH(-1)

Variance Equation

Coefficient Standard error T statistics p value

C 4.38E-05 2.99E-06 14.64123 0.0000**

RESID(-1)^2 0.576172 0.030753 18.73520 0.0000**

GARCH(-1) 0.482396 0.018617 25.91193 0.0000**

NET_FIIS 1.67E-06 1.24E-07 13.47464 0.0000**

Source: Computed Data

Model 2: Independent Variable NET FIIs Flows and Dependent Variable as NIFTY

RETURNS

The result of model 2 is also stating that there is significant effect of ARCH and

GARCH on the Sensex returns. It means that current volatility is influenced by past

volatility. Also, the square values of the lag variables are significant. Further the series is

affected by volatility in values of FIIS as p value < 5% for all the series.

Hence, FII does affect volatility of both the indices in India.

Table 5: GARCH Test with the Independent Variable as Net FIIs Flows and

Dependent as SENSX

Variance Equation

Coefficient Standard error T statistics p value

C 2.18E-05 1.86E-06 11.74275 0.0000**

RESID(-1)^2 0.441857 0.021080 20.96122 0.0000**

GARCH(-1) 0.624229 0.015859 39.36147 0.0000**

NET_FIIS 1.61E-06 1.13E-07 14.20969 0.0000**

Source: Computed Data

Note: **Significant at 5 %

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 93

6.0 Conclusion

This paper has explored that the relationship between the FIIs and the Volatility

in NIFTY and SENSEX. Trend analysis shows the positive flow that as the Indexes

increases the flow FIIs investment is positively flow with the indexes. Correlation

analysis show a positive relation between the FIIs and the Indexes. Finally,

ARCH/GARCH test analysis shows the significant impact on NIFTY and SENSEX,

after analysis all the result concluded that there was inferred that the Indian Stock

Market volatility influenced by the volatility of previous and FIIs investment.

References

Agarwal, R. N. (1997). Foreign portfolio investment in some developing countries: A

case study of determinants and macroeconomic impact. Indian Economic Review,

XXXII(2), 217-229.

Banerjee, A., & Sarkar, S. (2006). Modelling daily volatility of the Indian stock market

using intra-day data. IIM Calcutta Working Paper Series 588.

Batra, A. (2003). The dynamics of foreign portfolio inflows and equity returns in

India. Indian Council for Research on International Economic Relations, Working

Paper 109.

Behera, H. K. (2010). An assessment of foreign investment in Indian capital market.

Retrieved from http: //ssrn.com/abstract=2258352.

Bhattacharya, B., & Mukherjee, J. (2005, December). An analysis of stock market

efficiency in the light of capital inflows and exchange rate movements: The Indian

context. In Annual Conference of Money & Finance. Mumbai: Indira Gandhi Institute of

Development Research.

Biswas, J. (2005). Foreign portfolios investment and stock market behavior in a

liberalized economy: An Indian experience. Asian Economic Review, 47(2), 221-232.

Buckley, P., Clegg, J., Wang, C., & Cross, A. (2002). FDI, regional differences and

economic growth: Penal data evidence from China. Transnational Corporation, 11(1), 1-

28.

94 FOCUS: Journal of International Business, Volume 5, Issue 1, Jan-Jun 2018

Chandra, A. (2012). Cause and effect between FII trading behaviour and stock market

returns: The Indian experience. Journal of Indian Business Research, 4(4), 286-300.

Dharani, M., Narayanamoorthy, V., & Natarajan, P. (2015). An Empirical Study on

Volatility Pattern of the Shariah Compliant Stocks in Indian Capital Market. Journal of

Economic Policy and Research, April – Sept, 2015, 10(2),150-165.

Dhingra, V. S., Gandhi, S., & Bulsara, H. P. (2016). Foreign institutional investments in

India: An empirical analysis of dynamic interactions with stock market return and

volatility. IIMB Management Review, 28(4), 212-224.

Garg, A. K., & Mitra, S. K. (2015). A study of lead-lag relation between FIIs herding

and stock market returns in emerging economies: Evidence from India. Decision, 42(3),

279–292.

Gupta, A. (2011). Does the stock market rise or fall due to FIIs in India. Researchers

World - Journal of Arts, Science & Commerce, 2(2), 99-107.

Han, K. E., & Singal, V. (2000). Stock market openings: Experience of emerging

economies. Journal of Business, 73(1), 25-66.

Karmakar, M. (2006). Stock market volatility in the long run 1965-2005. Economic and

Political Weekly, 41(18), 1796-1802.

Kim, E. H., & Singal, V. (1993). Opening up of stock markets by emerging economies:

Effects on portfolio flows and volatility of stock prices in portfolio investment in

developing countries. World Bank Discussion Paper No.228. Stijn Claessens and

Sudarshan Gooptu (Ed.) Washington: World Bank, 383-403.

Kulwantraj, N. B. (2004). The determinants of foreign institutional investments in India

and the role of risk, inflation and return. Indian Economic Review, 32(2), 217-229.

Kumari, J., & Mahakud, J. (2015). Relationship between conditional volatility of

domestic macroeconomic factors and conditional stock market volatility: some further

evidence from India. Asia-Pacific financial markets, 22(1), 87-111.

Impact of Foreign Institutional Investors on the Volatility of Indian Stock Market 95

Mohan, R. T. T. (2006). Neither dread nor encourage them. Economic and Political

Weekly, 41(2), 95-99. Retrieved from http://www.jstor.org/stable/4417661

Mukherjee, P., Bose, S. & Coondoo, D. (2002). Foreign institutional investment in

Indian equity market: an analysis of daily flows during January 1999-May 2002. ICRA

Bulletin Money and Finance, April-September, pp. 21-52

Pal, P. (2005). Volatility in the stock market in India and foreign institutional investors:

A study of the post-election crash. Economic and Political Weekly, 40(8), 765-772.

Poshakwale, S. S., & Mandal, A. (2016). Sources of time varying return comovements

during different economic regimes: Evidence from the emerging Indian equity

market. Review of Quantitative Finance and Accounting, 48(4), 859-892.

Prasanna, P. K. (2008). Foreign institutional investors: Investment preferences in India.

Journal of Administration & Governance, 3(2), 40-51

Radelet, S., & Sachs, J. (1998). The East Asian financial crisis: diagnosis, remedies,

prospects. The Brookings Paper on Economics Activity, 29(1), 1-90.

Singh, S. K. (2004). Foreign portfolio investment. The Indian Journal of Commerce,

57(4), 120-137.

Singhania, M., & Saini, N. (2016). FII, Stock Exchange Return, and the Leverage Effect:

Evidence from India. The Journal of Wealth Management, 19(1), 103-119

Sultana, S. T., & Pardhasaradhi, S. (2012). Impact of flow of FDI & FII on Indian stock

market. Finance Research, 1(3), 4-10.

Upadhyay, S. (2006). FIIs in the stock market and the question of volatility. Portfolio

Organizer, May, 12(5), 22-30.

Vyas, D. J., & Shah, M. D. (2016). Determinants of foreign institutional investors'

investment and its effect on Sensex movement-a quarterly appraisal. International

Education and Research Journal, 2(4), 111-115.