ICTSD Series on Trade-Supported Strategies for Sustainable Development By Munir Ahmad Executive Director, International Textiles and Clothing Bureau Impact of Origin Rules for Textiles and Clothing on Developing Countries ICTSD Programme on Competitiveness and Sustainable Development December 2007 Issue Paper No. 3

Transcript

ICTSD Series on Trade-Supported Strategies for Sustainable Development

By Munir Ahmad Executive Director, International Textiles and Clothing Bureau

Impact of Origin Rules for Textiles and Clothing on Developing Countries

www.ictsd.org

ICTSD Programme on Competitiveness and Sustainable DevelopmentDecember 2007

Issue Paper No. 3

Impact of Origin Rules for Textiles and Clothing on Developing Countries

December 2007 l ICTSD Programme on Competitiveness and Sustainable Development

ICTSD

By Munir Ahmad Executive Director, International Textiles and Clothing Bureau

Issue Paper No. 3

ii Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

Published by

International Centre for Trade and Sustainable Development (ICTSD)International Envrionment House 27 Chemin de Balexert; 1219 Geneva, SwitzerlandTel: +41 22 917 8492 Fax: +41 22 917 8093E-mail: [email protected] Internet: www.ictsd.org

This paper was prepared by Mr. Munir Ahmad, Executive Director, International Textiles and Clothing Bureau (ITCB) at the request of the International Centre for Trade and Sustainable Development (ICTSD). Mr. Ahmad received invaluable assistance from his ITCB colleagues, Ms. Dinora Diaz and Mr. Guan Weigang. The views expressed in the paper do not necessarily represent that of the ITCB or that of its members.

ICTSD is grateful for support for this project, provided by the Dutch Ministry of Foreign Affairs (DGIS) and the UK Department for International Development (DFID).

For more information about ICTSD’s Programme on Competitiveness and Sustainable Development, visit our website at www.ictsd.org

ICTSD welcomes feedback and comments on this document. These can be forwarded to Gloria Carrion at [email protected]

Citation: Ahmad, Munir (2007). Impact of Origin Rules for Textiles and Clothing on Developing Countries, ICTSD Programme on Competitiveness and Sustainable Development, International Centre for Trade and Sustainable Development, Geneva, Switzerland.

Copyright ICTSD, 2007. Readers are encouraged to quote and reproduce this material for educational, non-profit purposes, provided the source is acknowledged.

This work is licensed under the Creative Commons Attribution-Noncommercial-No-Derivative Works 3.0 License. To view a copy of this license, visit http://creativecommons.org/licenses/by-nc-nd/3.0/ or send a letter to Creative Commons, 171 Second Street, Suite 300, San Francisco, California, 94105, USA.

The views expressed in this publication are those of the author(s) and do not necessarily reflect the views of ICTSD or the funding institutions.

ISSN 1995-6932

iiiICTSD Programme on Competitiveness and Sustainable Development

TABLE OF CONTENTS

LIST OF BOXES AND TABLES iv

LIST OF CHARTS v

ABBREVIATIONS/ACRONYMS vi

INTRODUCTION 1

I. THE MAKING OF TEXTILE-RELATED ORIGIN RULES 2

A. NON-PREFERENTIAL ORIGIN RULES 2

B. PREFERENTIAL ORIGIN RULES 5

II. PREFERENTIAL TRADE ARANGEMENTS WITH TEXTILE- SPECIFIC ORIGIN RULES 8

A. PREFERENTIAL TARIFF ARRANGEMENTS 8

B. TYPICAL TEXTILE-SPECIFIC ORIGIN RULES IN PREFERENTIAL ARRANGEMENTS 9

III. THE NEXUS BETWEEN ORIGIN RULES AND TRADE UNDER PREFERENTIAL ARRANGEMENTS 15

A. TEXTILE TRADE HAS BEEN SUBjECT TO PERSISTENT POLICY CHANGES 15

B. RECENT DEVELOPMENTS IN TEXTILE TRADE 16

C. TRADE FLOWS UNDER PREFERENTIAL ARRANGEMENTS 19

D. SOURCING OF RAW MATERIALS BY PREFERENCE- RECEIVING COUNTRIES 20

IV. ORIGIN RULES AND DISTORTIONS IN TEXTILE TRADE 30

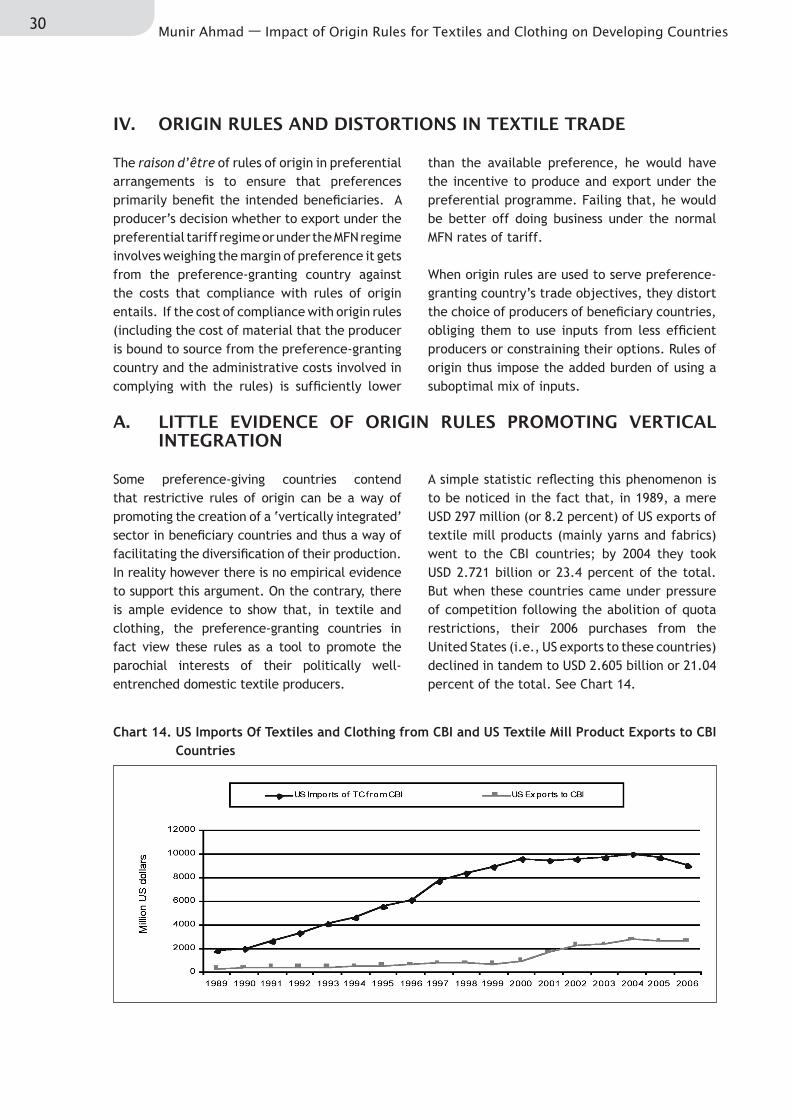

A. LITTLE EVIDENCE OF ORIGIN RULES PROMOTING VERTICAL INTEGRATION 30

B. ORIGIN RULES AND SUB-OPTIMAL UTILIzATION OF PREFERENCES 31

C. IMPEDIMENT TO DEVELOPMENT OF SOUTH-SOUTH TRADE 33

D. IMPACT ON NAMA NEGOTIATIONS 39

E. THE NEED TO FIX THE RULES OF ORIGIN CONUNDRUM 39

V. CONCLUDING REMARKS 41

ENDNOTES 43

REFERENCES 46

APPENDIX 47

iv Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

LIST OF BOXESBox 1. US Textiles and Clothing* Imports from Cbi, Agoa and Andean Countries (US Versus Non-US

Content) 12

Box 2. US/EU-25/Canada Textiles and Clothing Imports from Selected Preferential Partners 19

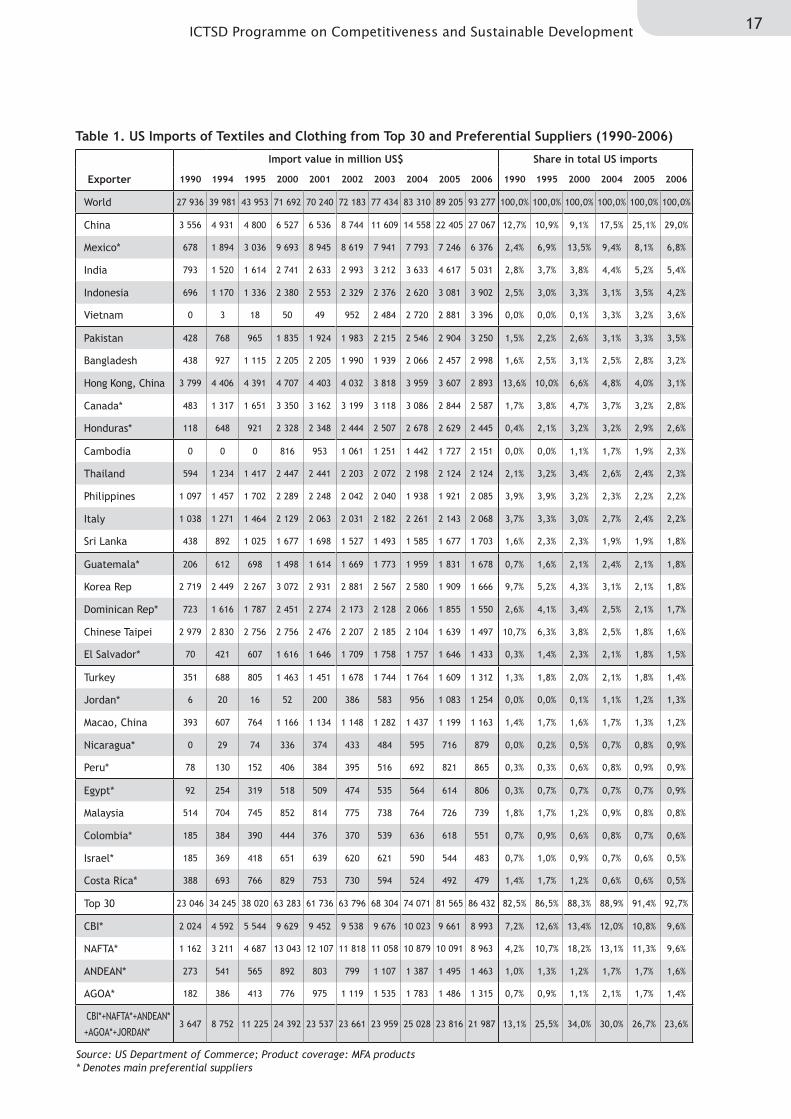

LIST OF TABLESTable 1. US Imports of Textiles and Clothing from Top 30 and Preferential Suppliers (1990–2006) 17

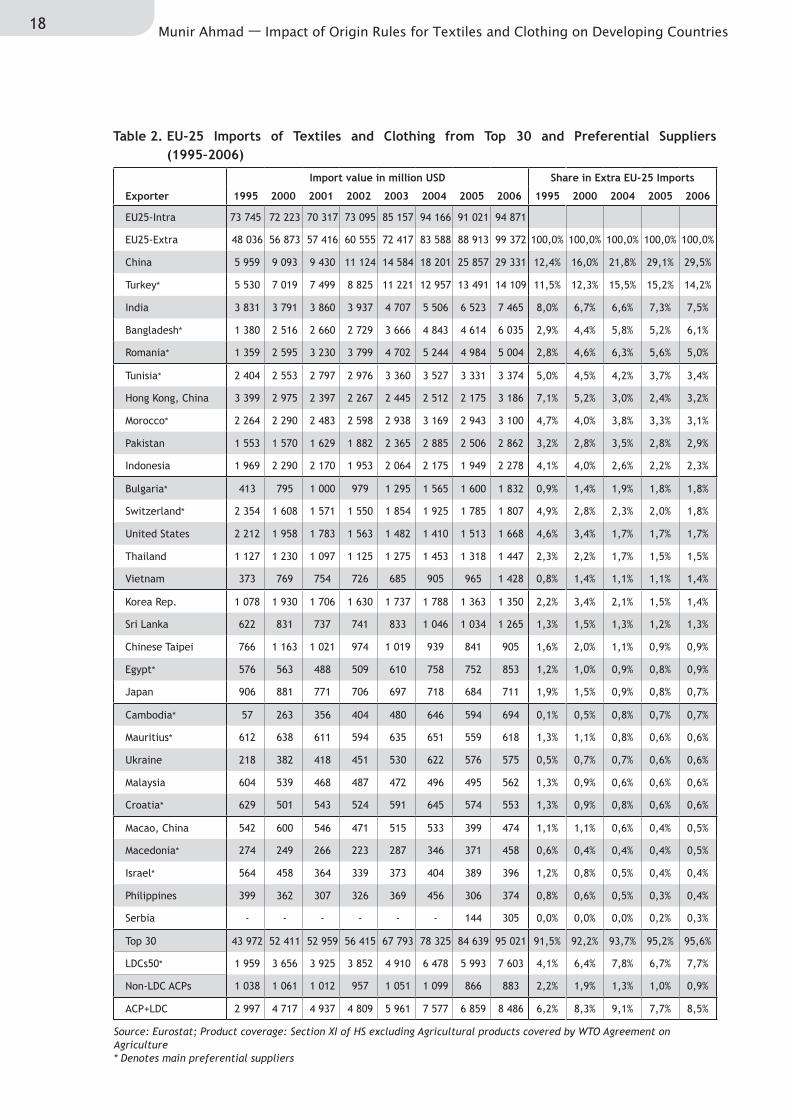

Table 2. EU-25 Imports of Textiles and Clothing from Top 30 and Preferential Suppliers (1995–2006) 18

Table 3. United States Textile and Clothing Exports – Composition and Main Destinations 22

Table 4. EU-25 Textiles and Clothing Exports – Composition and Main Destinations 23

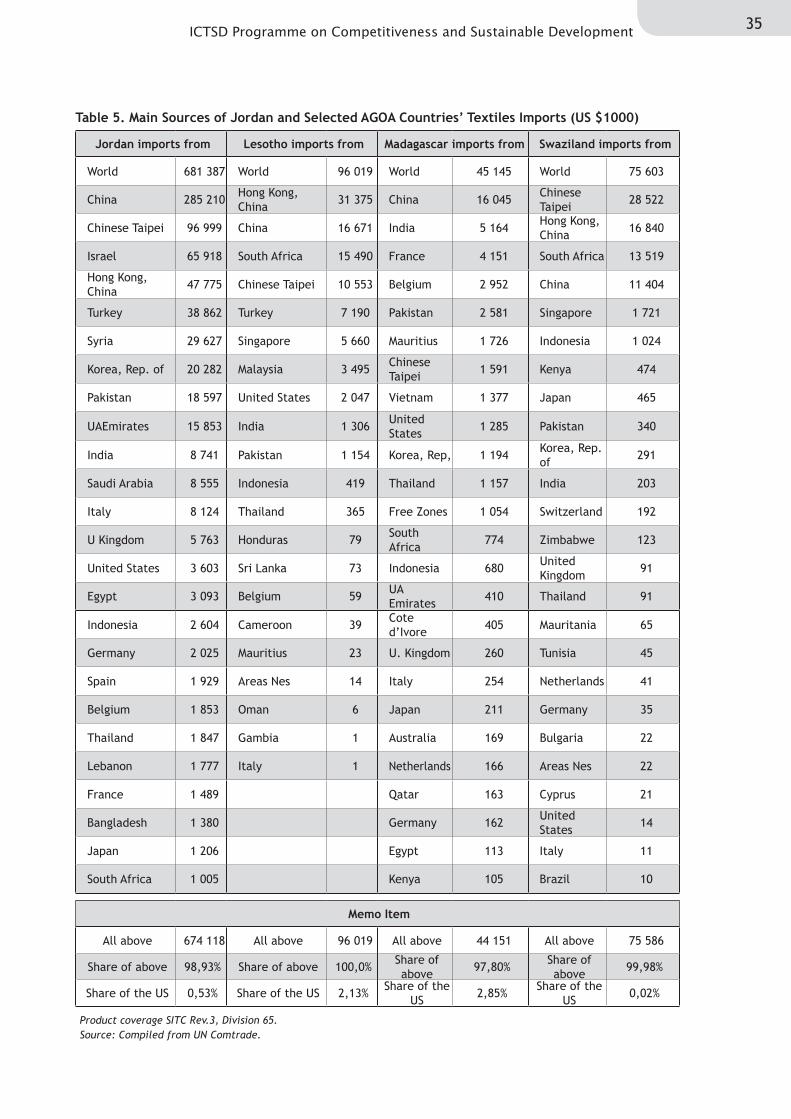

Table 5. Main Sources of Jordan and Selected AGOA Countries’ Textiles Imports (US $1000) 35

Table 6. Main Sources of EU Preferential Partners’ Textiles Imports, 2005 (US $1000) 36

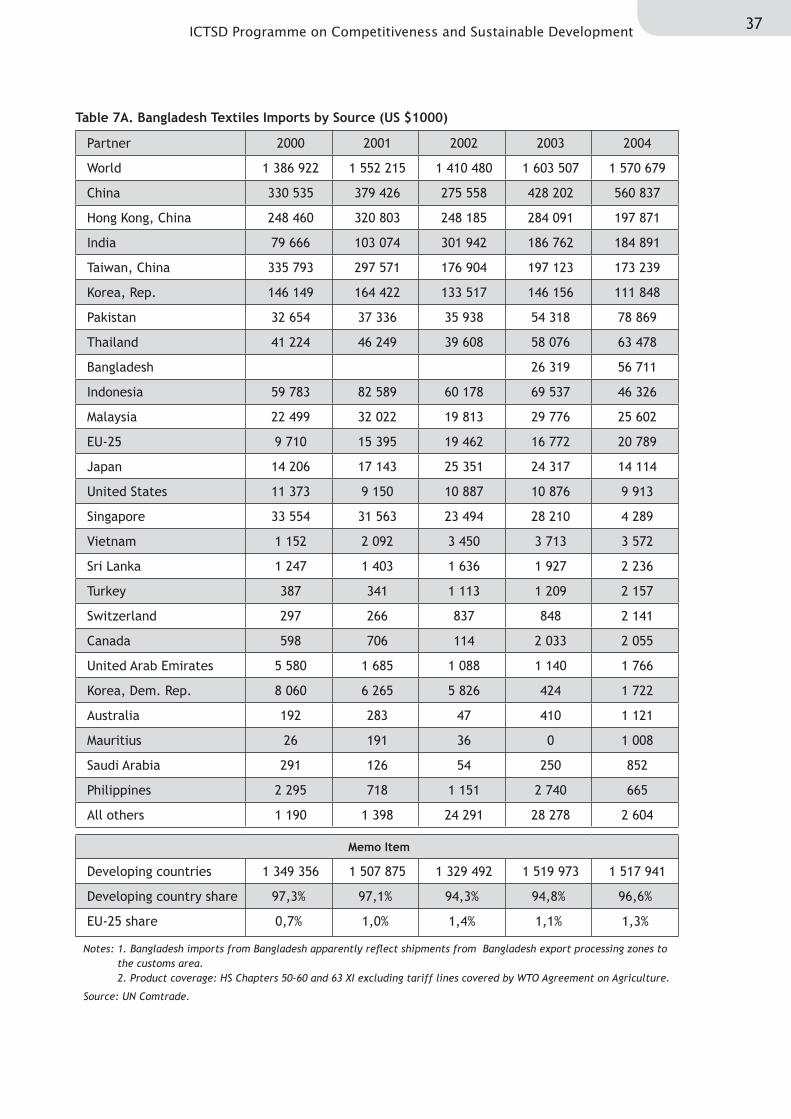

Table 7A. Bangladesh Textiles Imports by Source (US $1000) 37

Table 7B. Cambodia Textiles Imports by Source (US $1000) 38

Appendix Table: Countries covered by non-reciprocal preference schemes 47

vICTSD Programme on Competitiveness and Sustainable Development

LIST OF CHARTSChart 1. US Exports of Textile Mill Products to Mexico and CBI Countries 6

Chart 2. Canada Clothing Imports from Least-Developed Countries 14

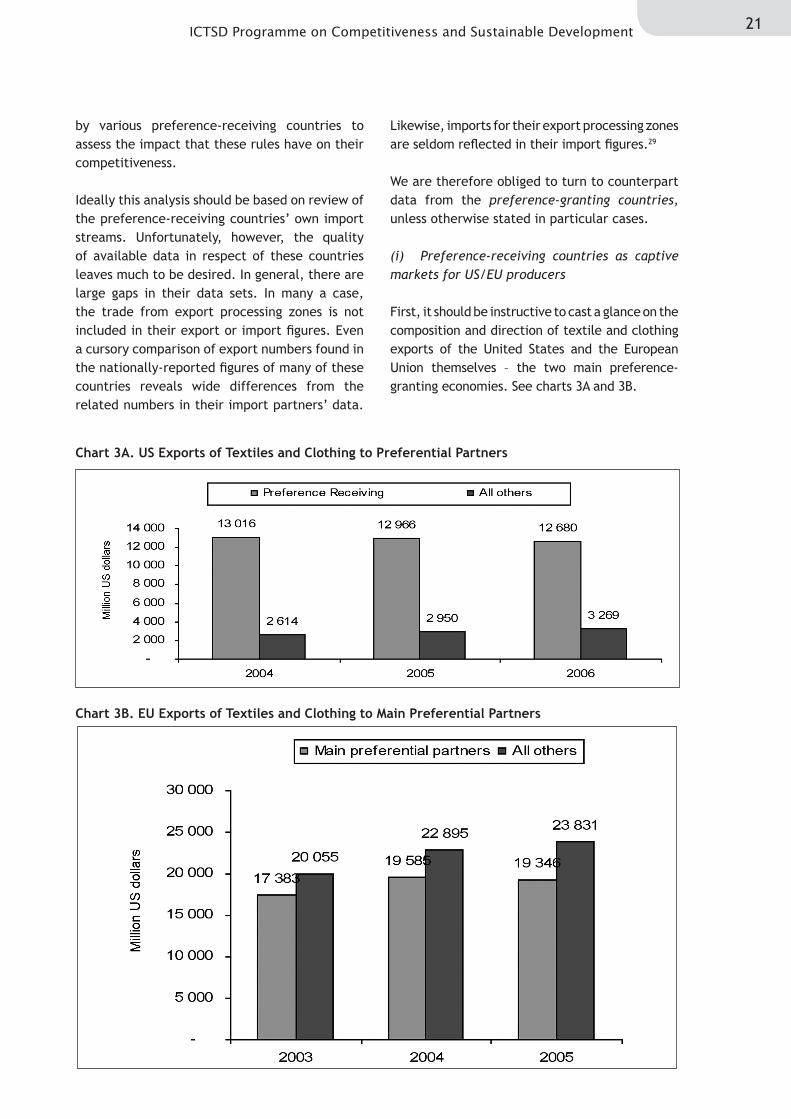

Chart 3A. US Exports of Textiles and Clothing to Preferential Partners 21

Chart 3B. EU Exports of Textiles and Clothing to Main Preferential Partners 21

Chart 4. US Imports from Mexico Versus US Exports to Mexico 25

Chart 5. US Imports from CBI Versus US Exports to CBI Countries 25

Chart 7. US Imports from Andean Versus US Exports to Andean Countries 26

Chart 8. EU-25 Imports from Romania Versus EU-25 Exports to Romania 27

Chart 9. EU-25 Imports from Tunisia Versus EU-25 Exports to Tunisia 27

Chart 10. EU-25 Imports from Morocco Versus EU-Exports to Morocco 28

Chart 11. EU-25 Imports from Bulgaria Versus EU-25 Exports to Bulgaria 28

Chart 12. EU-25 Imports from Bangladesh Versus EU-25 Exports to Bangladesh 29

Chart 13. EU-25 Imports from Cambodia Versus EU-25 Exports to Cambodia 29

Chart 14. US Imports Of Textiles and Clothing from CBI and US Textile Mill Product Exports to CBI Countries 30

Chart 15. EU GSP Utilization Rates by Bangladesh 31

Chart 16. EU-25 and US Clothing Imports from African Least-Developed Countries 33

Chart 17. US Exports of Textiles and Clothing to Preferential Partners 33

Appendix Chart 1. US Imports from Dominican Republic Versus US Exports to Dominican Republic 49

Appendix Chart 2. US Imports from El Salvador Versus US Exports to El Salvador 49

Appendix Chart 3. US Imports from Honduras Versus US Exports to Honduras 50

Appendix Chart 4. US Imports from Jordan Versus US Exports to Jordan 50

vi Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

ABBREVIATIONS/ACRONYMS

ACP African, Caribbean and Pacific Island group of countries

AGOA Africa Growth and Opportunity Act (of the United States)

ASEAN Association of Southeast Asian Nations

ATC Agreement on Textiles and Clothing

ATPA Andean Trade Preference Act (of the United States)

ATPDEA Andean Trade Promotion and Drug Eradication Act (of the United States)

CBERA Caribbean Basin Economic Recovery Act (trade vehicle under CBI of the United States)

CBI Caribbean Basin Initiative (US programme to assist countries of the Caribbean and Central

America)

CBTPA Caribbean Basin Trade Promotion Act (of the United States in modification of CBERA)

CTG Council for Trade in Goods of the WTO

EBA Everything-But-Arms (initiative of the EU granting quota-free, duty-free treatment to

least-developed countries)

EU European Union

FTA Free Trade Agreement

GALs Guaranteed Access Levels (system establish by the United States providing additional MFA

quotas for CBI countries)

GATT General Agreement on Tariffs and Trade (forerunner of the WTO)

GSP Generalized System of Trade Preferences

HS Harmonized Commodity Description and Coding System (classification system devised by

World Customs Organization)

ICTSD International Centre for Trade and Sustainable Development

ITCB International Textiles and Clothing Bureau

LDCs Least-developed countries

MFA Multi-Fibre Arrangement

MFN Most-Favoured-Nation treatment

NAFTA North American Free Trade Agreement (between Canada, Mexico and the United States

of America)

NAMA Non-Agricultural Market Access (negotiations under Doha Round)

OPT Outward processing trade

QIZ Qualifying Industrial Zones (US programme of duty-free treatment for imports from

Jordan and Egypt)

SAARC South Asian Association for Regional Cooperation

SITC Standard International Trade Classification (classification system devised by the UN)

TPLs Tariff Preference Levels (under US free trade agreements)

TRQ Tariff Rate Quota

US United States of America

WTO World Trade Organization

1ICTSD Programme on Competitiveness and Sustainable Development

INTRODUCTION

Rules of origin are an essential for the conduct of international trade. They are needed to determine the nationality of traded products, which, in turn, is used for a whole variety of commercial policy purposes: to collect trade statistics; to apply import tariffs; to impose countervailing or anti-dumping duties on unfairly traded products; to apply safeguard measures for temporary protection to domestic industries in times of need; to administer requirements with respect to marking of products to help consumers to distinguish between them depending on their source. Origin rules are also required for administering preferential trade agreements to ensure that only the intended countries benefit from those preferences.

Textile and clothing are no exception to these essentials. Over time, however, origin rules in this sector have so evolved as to serve as conditions on access to markets or to provide protection to domestic textile industries. And, in the context of preferential arrangements, these rules have increasingly been designed to provide advantage to textile producers in preference-granting countries. While, on the one hand, this situation limits the possibility for preference-receiving countries to derive full benefit from preference schemes, on the other it has led to the creation of new distortions to trade in the sector. Origin rules are also a major factor behind concerns about the sustainability of many developing countries’ exports following the expiry of quota restrictions.

This paper is intended as an input to policy-makers and other stakeholders. It aims to provide an analysis of the working of various origin schemes in as simple and user-friendly a manner as possible.

To this end, the first section gives a brief background to the making and evolution of present-day origin rules relating to textiles and clothing in some major economies, both in the context of normal most-favoured-nation (MFN) trade and preferential trading arrangements which now account for a large portion of trade in the sector. Section II identifies the main preferential trade arrangements in which textile-related origin rules play a significant role. It also brings out the aspects of these rules that condition the utilization of preferential access by preference-receiving countries to the use of inputs from preference-giving countries. Section III gives a short account of recent developments in textile trade in general and its evolution under preferential trade arrangements in particular. It then maps the binding influence of origin rules on the sourcing of raw materials by various groups of preference-receiving countries. It shows the nexus between origin rules and trade and how preferential origin rules constrain many countries’ trade prospects, contrasting their situation with those countries that are not bound by these rules and have been better able to cope with competition due to the flexibility of their sourcing options. Section IV highlights how restrictive origin rules constitute a source of continuing distortions in textile and clothing trade. Section V offers some concluding reflections.

2 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

(i) The context of quota restrictions

Trade in textiles and clothing has long been controversial. For over four decades, markets in developed countries were shielded from imports by a series of international arrangements that authorized developed countries to impose limits on the quantities that could be exported to their markets from particular exporting countries. Beginning with the “Short Term” Arrangement Regarding International Trade in Cotton Textiles in 1961, it evolved into the Arrangement Regarding International Trade in Textiles, usually called the Multi-Fibre Arrangement or MFA, in 1974 until it was replaced by the Uruguay Round Agreement on Textiles and Clothing (ATC) from January 1995.1 The ATC itself expired at the end of 2004 and, with it, came the end of the system of quota restrictions.

Neither these arrangements nor GATT rules set out any specific criteria to determine the origin of imported products. Not surprisingly, exporters and importers would attempt to maximize trade in whatever ways the regime would permit. One way was to ship unfinished or semi-finished products to countries that were not covered by restraints or could not fully use their available quotas. The transformation of unfinished products in the second country would confer origin on the second country and would thus free the final product from quota limits imposed on the first country. Much of this development had to be a natural evolution of production methods in a globalizing world. Notwithstanding, however, it inflamed the textile industries in importing countries which sought the protection of quotas and brought persistent calls for plugging the loopholes.

(ii) The United States

In general, the rule-of-thumb standard for origin determination had long been ‘substantial transformation’, i.e., to deem a product as originating in a place where it had undergone substantial transformation in its making. The

United States law however did not provide for any specific definition of the ‘substantial transformation’ standard. Following court rulings, it was interpreted as a process that created a new and different article of commerce “having a distinctive name, character or use.”

In response to complaints that textiles and clothing were being imported by getting around the applicable quotas, in May 1984 2 President Reagan directed the Secretary of the Treasury to issue new country of origin regulations for textiles and apparel. Pursuant to this, interim regulations were published in August 1984 and final regulations in March 1985.3 They provided that a textile or apparel product will be considered to have undergone a substantial transformation if it had been transformed by means of “substantial manufacturing or processing operations” into a new and different article of commerce.

The concept of substantial manufacturing or processing operations thus came to be added to the interpretation of ‘substantial transformation’. Following these regulations, until the conclusion of the Uruguay Round, US Customs conferred origin to an apparel article on the basis of where its components were cut to shape or, in the case of apparel of knitted fabric, where the knit panels were sewn together. However, as even this standard afforded possibilities of quota utilization by parcelling out the assembly of components to a different location, on the eve of implementation of the Uruguay Round results the US textile industry extracted a concession from the US Administration and succeeded in getting the origin rules relating to textile and clothing products to be significantly changed and formally codified in law. This was accomplished by Section 334 of the US Uruguay Round Agreements Act. The actual implementation of these changes came into effect in July 1996.4

The modifications effected through this law substantially departed from the previous US practice, particularly insofar as the

I. THE MAKING OF TEXTILE-RELATED ORIGIN RULES

A. NON-pREFERENTIAL ORIGIN RULES

3ICTSD Programme on Competitiveness and Sustainable Development

determination of origin of finished fabrics, made-up articles, apparel assembled in different locations, and apparel made from knit-to-shape panels was concerned. It was now provided that such manufacturing operations as dyeing/printing of fabric, a multitude of operations in the making of made-up articles from fabric, cutting to shape of apparel, and sewing together of knit-to-shape panels would no more be deemed to confer origin.

Thus, for example, even if greige fabric imported from developing countries was further processed by dyeing, printing and other finishing operations in, say, a European country and then exported from that European country to the United States, its origin remained the developing country where the greige fabric was originally made. Likewise, flat goods (bed linen, kitchen linen, table line, toilet linen, curtains, bedspreads and other furnishing articles, sacks and bags, tarpaulins, tents, sails, and similar other articles) imported into the United States, say, from a European country (where fabrics imported from quota-restrained developing countries were dyed, printed and subjected to other operations) also came to be treated as originating in the developing country where the fabric was originally made, not the European country where the fabric had been subjected to further processing and making into various flat goods.

This gave rise to disruption of established patterns of trade and to loud protests from a wide cross-section of stakeholders. Under pressure, especially from the European Union, the US relented and enacted an amendment to its Uruguay Round Agreements Act 5 which resulted in further modifications, essentially accommodating the EU concerns. Under these amendments:

(a) For processed fabrics: The origin reverted to the pre-July 1996 rule so that fabrics are now conferred origin of the country where they are both dyed and printed and, in addition, undergo two or more of the following finishing operations: bleaching, shrinking, fulling, napping, decating, permanent stiffening, weighting, permanent embossing or moireing.

However this same rule does not apply to fabrics made of wool. In other words, for fabrics of wool, origin remains where the basic fabric is formed.

(b) For made-up articles: For 16 specified categories of made-up articles, the July 1996 change established the origin as the country where the constituent greige fabric was formed by weaving or knitting, regardless of any further processing such as dyeing and printing of fabric, and subsequent conversion of fabric to made-up articles.

The 2000 changes with respect to some (not all) of these 16 articles resulted in the following:

(i) For non-cotton and non-wool made-up articles (i.e., only those of silk, man-made fibres or other vegetable fibres), the rule now recognizes dyeing and printing as origin conferring. Therefore the origin is the country where the constituent fabric is dyed and printed and undergoes two or more finishing operations.

However, if these same products are made of cotton or wool fabric, the origin continues to be deemed to be the country where the constituent cotton or wool fabric is formed.

(ii) For all made-up articles, contrary to pre-ATC rules, the new rule continues to disregard such processing operations as designing, cutting, hemming, sewing that are necessary to be undertaken on the fabric to convert it to made-up articles.

(c) For apparel products: No modification was effected in 2000. Consequently, origin continues to be determined on the basis of rules as modified and implemented with effect from July 1996, i.e., designing and cutting to shape of apparel is no more deemed to be origin conferring; nor are the sewing together of knit-to-shape panels and a variety of finishing operations that are commonly undertaken for the final product.

4 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

(iii) The European Union

In the case of the European Union, the concept of substantial transformation, insofar as textile and clothing products falling under Section XI of the Harmonized Commodity Description and Coding System (HS) are concerned, has been reflected in detailed rules specifying the criteria for each main group of products. This method of determining origin is sometimes also referred to as the ‘list system’.

In general, under this method, origin is conferred to an imported product if it was so transformed by working or processing in the exporting country as to fall under a different tariff heading.6 The relevant EU Regulation provides a listing of the working or processing operations that must be carried out on non-originating materials.

With respect to textiles and clothing, the practical reflection of the above principle is contained in a specific annex to an EU Regulation,7 item by item. Thus, for example, printed or dyed woven fabric, classifiable under chapters 50 to 56 of the HS, qualifies to receive origin status if it was manufactured from yarn, or was printed or dyed from unbleached or pre-bleached fabric and had undergone two preparatory or finishing operations in the exporting country. Thus, printing or dying of fabric by itself is also accepted as origin conferring, provided, however, that it is accompanied by two preparatory or finishing operations. Non-printed or non-dyed fabric is considered as originating in the exporting country only if it was manufactured there from yarn.

Finished or complete apparel of woven fabrics classified under HS Chapter 62 receives origin if it received ‘complete making up’ in the exporting country. Complete making up is, in turn, defined as “all operations following the cutting of the fabric.” However, shawls, scarves, mufflers and veils which are also classified under the same Chapter 62 receive origin only if they were manufactured from yarn. But if these articles are embroidered, they receive origin either if they were manufactured from yarn or were manufactured from unembroidered fabric, provided that the value of the fabric does not

exceed 40 percent of the ex-works price of the final product.

In fact, the annex listing the origin criteria for textile and clothing products is spread over more than five pages. By contrast, the annex pertaining to all other products (including agricultural products) consists of less than four pages. Such has been the attention devoted to origin rules for textiles and clothing!

(iv) Some other jurisdictions

While several other countries including Japan, Norway and Switzerland follow the change-in-tariff-heading method, in some other jurisdictions the origin rules are based on prescribed minimum proportions of value addition. For example, Canadian rules confer origin if at least 50 percent of the cost of imported good was incurred in the exporting country and was finished there in the form in which it is imported into Canada.

(v) Harmonization of non-preferential origin rules

It was in recognition of such diversity of origin criteria (admittedly not just in textiles but other sectors as well) that the WTO Membership reached an interim agreement during the Uruguay Round to harmonize non-preferential origin rules on the basis of the principle that they “should provide for the origin of a particular good to be either the country where the good had been wholly obtained or, when more than one country is concerned in the production of the good, the country where the last substantial transformation had been carried out” (the Agreement on Rules of Origin). The practical reflection of this otherwise simple principle, however, continues to defy resolution and has remained a source of contention in WTO negotiations for over ten years (although, admittedly, not just on textiles but a number of other sectors as well). The work aimed at harmonizing non-preferential origin rules has therefore yet to be finalized.

Although non-preferential origin rules remain important, in particular concerning possible application of any new safeguard actions under

5ICTSD Programme on Competitiveness and Sustainable Development

normal GATT rules and disciplines, countervailing or anti-dumping duties, or marking of the origin of imported products, they do not enjoy the level of significance that they used to have under the MFA or the ATC. Now that quota restrictions have gone, it matters little, for example, if bed linen exported from, say, Indonesia to the United States had only been assembled in Indonesia from fabric imported from Chinese Taipei and gets classified in the United States as originating in Chinese Taipei. Even so, it is to be recognized

that varying origin criteria remain responsible for creating unnecessary confusion in data on textile and clothing trade because, as it happens, some export shipments made to particular countries actually end up being shown in import figures from elsewhere and for something else. Consequently, it is not uncommon to find large differences between export figures of certain countries and the counterpart import data of their partner importing economies.

B. pREFERENTIAL ORIGIN RULES

(i) The quota system loomed large

Like non-preferential origin rules, the evolution of the making of present-day preferential origin rules for textiles and clothing can also be traced to the strong influence of quota restrictions in the sector as brought out in the following sub-sections.

(a) Outward processing trade (OPT)

Outward processing had long been an established feature of trade, especially in Europe. In textile and clothing, given the labour-intensive nature of sewing and other operations required in the making of clothing products, it essentially involved the shipping of fabric and cut or unfinished parts of apparel from high-wage importing countries to neighbouring low-wage developing economies for making up into garments and re-importing the finished garments. The practice initially developed in some EC member states, especially Germany and France, on the one hand, and former Yugoslavia, on the other. With passage of time, it received added significance and was extended to countries of the Mediterranean, especially, Tunisia and Morocco.

To take advantage of the opportunities offered by outward processing trade a provision was included in the Multi-Fibre Arrangement of 1974, even though it effectively involved a further departure from the general GATT rule of non-discrimination. It provided that “Consideration shall be given to special and

differential treatment to re-imports into a participating [importing] country of textile products which that country has exported to another participating country for processing and subsequent re-importation in the light of the special nature of such trade …” 8

On the back of this provision, the EC provided additional quota entitlements for outward processing trade. Although, with the passage of time, the possibility of OPT quotas was offered on a more generalized basis, as a matter of sheer economic logic it was of the greatest significance to some of the EC member states themselves inasmuch as it enabled their yarn and fabric makers to find convenient outlets for their products and also to economize on the cost of labour. It also provided the much-needed export prospects for some exporting countries with surplus pools of available labour. Besides Yugoslavia, the more successful examples were Morocco and Tunisia. As subsequent developments (discussed in the following section) were to show, the system proved to be a boon in creating ready availability of markets for developed countries’ textile producers but could not promote the long-term viability of industries in developing exporting countries.

On the other side of the Atlantic, the United States also established (in 1988) a similar “Special Regime” for most apparel and selected made-up textiles from Mexico whereby a significant portion of Mexico’s quotas was set aside for export of articles assembled from fabrics wholly formed and cut in the United States.9

6 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

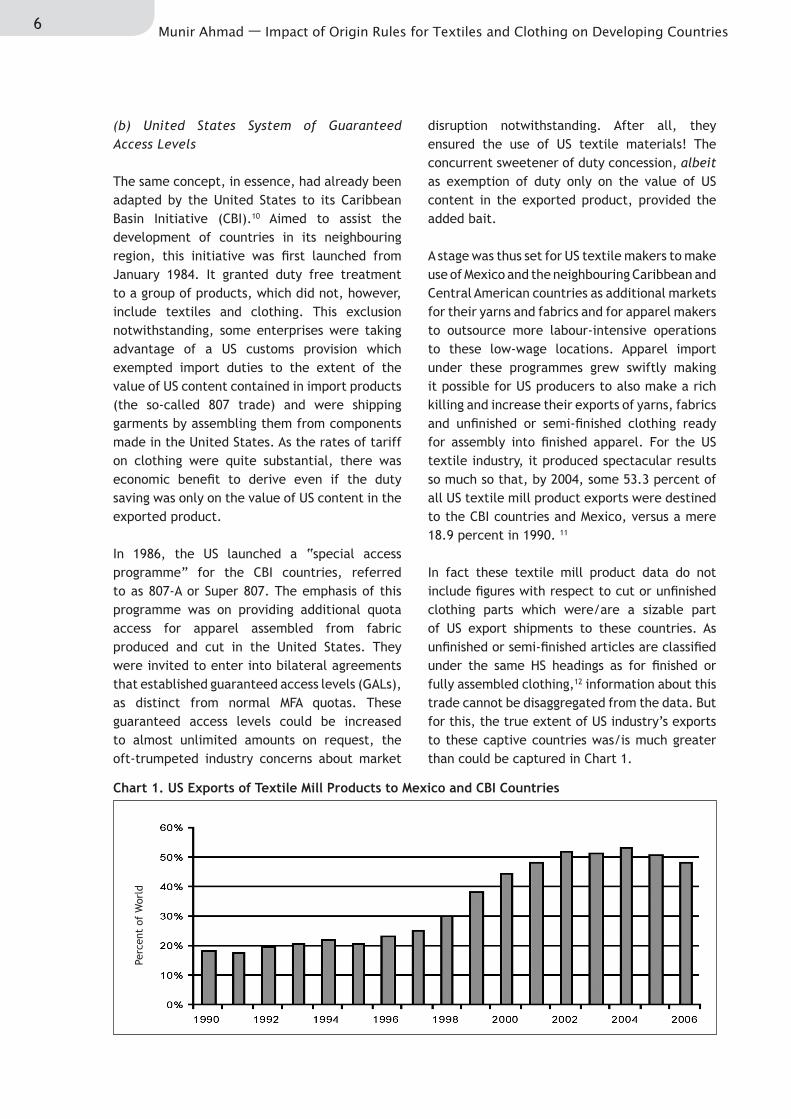

(b) United States System of Guaranteed Access Levels

The same concept, in essence, had already been adapted by the United States to its Caribbean Basin Initiative (CBI).10 Aimed to assist the development of countries in its neighbouring region, this initiative was first launched from January 1984. It granted duty free treatment to a group of products, which did not, however, include textiles and clothing. This exclusion notwithstanding, some enterprises were taking advantage of a US customs provision which exempted import duties to the extent of the value of US content contained in import products (the so-called 807 trade) and were shipping garments by assembling them from components made in the United States. As the rates of tariff on clothing were quite substantial, there was economic benefit to derive even if the duty saving was only on the value of US content in the exported product.

In 1986, the US launched a “special access programme” for the CBI countries, referred to as 807-A or Super 807. The emphasis of this programme was on providing additional quota access for apparel assembled from fabric produced and cut in the United States. They were invited to enter into bilateral agreements that established guaranteed access levels (GALs), as distinct from normal MFA quotas. These guaranteed access levels could be increased to almost unlimited amounts on request, the oft-trumpeted industry concerns about market

disruption notwithstanding. After all, they ensured the use of US textile materials! The concurrent sweetener of duty concession, albeit as exemption of duty only on the value of US content in the exported product, provided the added bait.

A stage was thus set for US textile makers to make use of Mexico and the neighbouring Caribbean and Central American countries as additional markets for their yarns and fabrics and for apparel makers to outsource more labour-intensive operations to these low-wage locations. Apparel import under these programmes grew swiftly making it possible for US producers to also make a rich killing and increase their exports of yarns, fabrics and unfinished or semi-finished clothing ready for assembly into finished apparel. For the US textile industry, it produced spectacular results so much so that, by 2004, some 53.3 percent of all US textile mill product exports were destined to the CBI countries and Mexico, versus a mere 18.9 percent in 1990. 11

In fact these textile mill product data do not include figures with respect to cut or unfinished clothing parts which were/are a sizable part of US export shipments to these countries. As unfinished or semi-finished articles are classified under the same HS headings as for finished or fully assembled clothing,12 information about this trade cannot be disaggregated from the data. But for this, the true extent of US industry’s exports to these captive countries was/is much greater than could be captured in Chart 1.

Chart 1. US Exports of Textile Mill Products to Mexico and CBI Countries

Perc

ent

of W

orld

7ICTSD Programme on Competitiveness and Sustainable Development

And, during 1984–87, the US-made content averaged 64 percent of the value of apparel imports from these countries versus only 20 percent for all other sectors combined.13 This, because of the high average tariff of over 20 percent on apparel compared to only 3.5 percent for all other product categories.

The attraction held out by this mode of trade had subsequently to become the focus of lobbying efforts by domestic industry groups as the core basis for origin rules in most preferential arrangements, irrespective of whether these were in the context of autonomous non-reciprocal schemes or bilateral or regional free trade

agreements. The phenomenon, euphemistically called the “local content requirement”, has thus become the central plank of US preferential origin rules found today.

As the main purpose of this short paper is not to trace the evolution of the making of origin rules in all its details, in the following Section we turn to the identification of the main preferential trade arrangements in which textile-related origin rules play a significant role. Suffice to say, the origin rules in preferential arrangements have been heavily influenced by the experience of the quota regime.

8 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

II. pREFERENTIAL TRADE ARANGEMENTS WITH TEXTILE-SpECIFIC ORIGIN RULES

A. pREFERENTIAL TARIFF ARRANGEMENTS

Presently, all major developed economies provide tariff preferences on import of textiles and apparel from a variety of developing countries. Some of these programmes are autonomous in nature and do not require reciprocal concessions in return. Others are bilateral or regional free trade agreements. In almost all cases, these programmes or agreements provide for specific origin criteria for textile exports to be able to benefit from duty concession or preference.

The principal programmes under which textile and clothing exports from developing economies are provided tariff preference by developed economies are:

(i) The European Union

Non-reciprocal

Generalized System of Preferences • framework for developing and least-developed countries.14 (A list of least-developed countries is provided in the Appendix.)The partnership agreement with African, • Caribbean and Pacific Island countries (ACP) in the framework of the Cotonou (formerly Lome) Convention. (The list of the ACP group of countries is given in the Appendix.)

Reciprocal

EU–Turkey Customs Union.• European Association agreements with • Bulgaria and Romania (These two have since joined the EU as full members and have had large apparel exports to the other EU member states.)Stabilization and Association Agreements • with Western Balkan countries.Euro-Mediterranean Association Agreements • with Algeria, Morocco, Tunisia, Israel, Palestinian Authority, Egypt, Jordan, Lebanon and Syria.

(ii) The United States

Non-reciprocal

Caribbean Basin Initiative (CBI),• 15 the group of Caribbean countries, of whom Haiti is now the largest exporter. (The list of CBI eligible countries is provided in the Appendix table.)Africa Growth and Opportunity Act • (AGOA), under which Botswana, Kenya, Lesotho, Madagascar, Mauritius, Namibia, South Africa and Swaziland are significant exporters of apparel. (The list of all AGOA countries is also provided in the Appendix table.)Andean Countries (ATPA), of whom Colombia • and Peru are significant apparel exporters.Qualifying Industrial Zones (QIZ) schemes: • for Jordan and Egypt.

Reciprocal

North American Free Trade Agreement • (NAFTA), under which Mexico is a substantial exporter of textile and apparel to the US.US/Central American Free Trade Agreement • (CAFTA-DR): Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras and Nicaragua, all of which have sizeable apparel exports to the US.Other US Free Trade Agreements: with • Australia, Jordan, Israel, Morocco, Bahrain, Chile and Singapore.

(iii) Canada

Generalized System of Preferences (GSP) • (especially duty-free access to least-developed countries in its framework).

9ICTSD Programme on Competitiveness and Sustainable Development

(iv) Japan

Generalized System of Preferences.•

(v) Australia

Duty-free access to least-developed • countries in the framework of Generalized System of Trade Preferences.

B. TYpICAL TEXTILE-SpECIFIC ORIGIN RULES IN pREFERENTIAL ARRANGEMENTS

In the scope of this short paper, it seems unnecessary to provide detailed descriptions of all origin schemes, with all their twists and shades. The following account therefore brings out only the main features with emphasis on those aspects that have a significant impact on developing countries’ trade prospects.

(i) The European Union

EU preferential origin rules are specified in each preferential arrangement or agreement. The basic architecture of these rules is substantially the same irrespective of whether they pertain to non-reciprocal schemes in the framework of the GSP or they relate to reciprocal preferences under free trade area agreements (FTAs). In general, they are based on a scheme of ‘list rules’ which are in turn organized according to the structure of HS classification. The criteria for determining the origin of various products are listed against each product category, setting out the minimum amount of working or processing required on non-originating materials in order for the resulting product to obtain originating status.

Generally, two broad criteria are used to identify origin:

The ‘wholly-obtained or produced’ criterion • applies in cases in which the product is manufactured in the country from inputs that are also wholly obtained within the country; it thereby precludes the use of second-country components.The more complex ‘substantial • transformation’ criterion, which is used in the majority of cases as most products contain varying amounts of imported inputs, defines various levels of requisite working or processing to receive origin status.

Typically the criteria require the final product to undergo particular manufacturing operations expressed as change from a specified tariff heading to a different heading. The change of tariff headings is also defined at various degrees of aggregation.

In general, the EU rules also provide for the possibility of use of materials or components produced in other countries specified in the particular arrangement or with which the EU has free trade arrangements. Known as ‘cumulation’, it allows producers from preference-benefiting countries to import non-originating materials from other beneficiaries without affecting the final product’s originating status and therefore the possibility of benefiting from duty concession.

There are four types of cumulation criteria: bilateral cumulation, diagonal cumulation, regional cumulation and full cumulation.

Bilateral cumulation is the most common form and applies to trade between two partners in a preference scheme. It stipulates that producers in beneficiary country A may use inputs from the preference-giving country B without affecting the final good’s originating status.

Under diagonal cumulation, beneficiary countries included in the same programme can use materials that originate in another beneficiary country – as if the materials were originating in the country where further processing is undertaken. As with bilateral cumulation, only products or materials originating in the parties to these agreements can benefit from diagonal cumulation. Although more than one country can be involved in the manufacture of a product, it will have the origin of the country where the last working or processing operation took place, provided that it was more

10 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

than a prescribed minimal operation. Diagonal cumulation operates between the European Community and the countries of the so-called ‘pan-European cumulation zone’.

Regional cumulation: Regional cumulation is a form of diagonal cumulation, which only exists under the GSP and operates between members of a regional group of beneficiary countries (e.g. ASEAN and the South Asian Association for Regional Cooperation/SAARC).

Finally, under full cumulation, all processing or transformation of a product within a set of beneficiary countries can be counted as qualifying content, regardless of whether the processing is sufficient to confer originating status to the materials themselves. Full cumulation is less common than diagonal but is applied by the EU in its agreements with Algeria, Morocco and Tunisia and in the Cotonou Agreements. It allows for greater flexibility in production processes.

Leaving aside the somewhat technical description of origin criteria outlined above, in a nutshell the EU requires that, to be accorded duty concession under its GSP schemes, the product concerned must have undergone ‘double transformation’, i.e., “at least two manufacturing/processing operations” in the country of export. Thus, for example, for a woven shirt to benefit from duty concession, it should have been assembled in the exporting least-developed country from fabric made in that country. Consequently, most least-developed countries are unable to take full advantage of the facility, lacking as they are in textile manufacturing capacity due to the highly capital-intensive nature of this segment of textile and clothing production. Moreover, a significant portion of clothing is made with fabrics of new fibres with technologies patented in the developed world.

Likewise, although the origin criteria under other preference programmes allow relatively more flexibility in the use of components made outside the Union (but from within the wider cumulation areas), yet, effectively, these criteria necessitate the use of EU materials and components by major clothing exporters such as Bulgaria, Morocco,

Romania, Tunisia etc., given that these countries also possess only limited textile manufacturing capacities.

The practical effect of EU origin criteria for preferential arrangements is thus two-fold. In the case of least-developed countries, the actual utilization of preferential access is much less than optimal. In the case of the countries of the Maghreb (Morocco, Tunisia, etc.) and Central and East European countries, by sheer economic logic, their producers and exporters are obliged to import their raw material (yarns and fabrics, etc.) from the EU member states. These phenomena are brought out at some length in Section III of the paper.

(ii) The United States

(a) Free trade agreements

With the exception of US/Jordan and US/Israel FTAs, the main benchmark for textile and clothing origin rules is the so-called ‘yarn forward’ of NAFTA. In fact, although it is generally described as yarn forward, for many products it is actually ‘fibre forward’. Simply expressed, this rule makes duty-free treatment of textiles and clothing imports conditional on the requirement that the imported product is made within the free trade area from yarn (fibre) onward. In other words, for a shirt to benefit from duty concession it must be manufactured with yarn as well as fabric that is produced or sourced in any of the NAFTA member countries, or effectively a triple transformation process. For fabric, it must have been manufactured with yarn that was also produced in the FTA partner concerned.

Typically, the US free-trade agreements contain two main exceptions from the general yarn forward standard. First, they provide for the so-called Tariff Preference Levels (TPLs) that stipulate import of specified maximum quantities at preferential rates of duty even if the products concerned are made with material that does not otherwise qualify under the prescribed origin criteria. Second, they provide for a process for determination of inputs (yarns and fabrics) that may not be available in commercial quantities

11ICTSD Programme on Competitiveness and Sustainable Development

within the United States and may therefore be sourced from non-FTA partners. However, there is no uniformity as to the existence of these exceptions across all FTAs to which the United States is a party.

(b) Non-reciprocal preferential programmes

The criteria in US non-reciprocal preference arrangements under the Caribbean Basin Initiative (CBI), Africa Growth and Opportunity Act (AGOA) and Andean Trade Promotion Act (ATPA) are in, some respects, even stricter. They stipulate duty benefit for apparel imports from these countries mainly if the component inputs are sourced from the United States itself. This

is the so-called local content requirement. As in the case of free trade agreements, there are a few deviations permitted from this general principle, but subject to strict criteria including limits on the maximum quantities that may benefit from duty concession.

Perhaps the simplest way to understand the origin criteria under non-reciprocal preference schemes of the United States is to see the specific conditions under which duty-free access is available under these programmes (Box 1 below). For convenience sake, and to avoid repetition in later sections of the paper, the volumes of imports benefiting from preferential access under various criteria are also indicated.

12 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

Box 1. US Textiles and Clothing* Imports from Cbi, Agoa and Andean Countries (US Versus Non-US Content)

CBI COUNTRIES (CARIBBEAN BASIN TRADE pARTNERSHIp ACT) 2005Total Imports (Million US$) 9 661.20Subject to US content Apparel assembled from US cut fabric from US yarn 16.00%Knit apparel from US fabric, yarn and thread 15.90%Knit apparel from regional or US fabric from US yarn (TRQ) 13.40%Apparel cut and assembled from US fabric, yarn & thread 12.70%Articles assembled from any fabric cut in the United States 9.80%Brassieres cut and assembled in the US and/or CBI 3.50%T-shirts made of regional fabric from US yarn (TRQ) 2.10%Apparel assembled from US cut fabric & yarn, further processed 1.60%Apparel assembled with US thread and fabric (mixed cutting) 1.30%Total above 76.40%With no US content or under MFN duty Apparel from fabric or yarn determined as not available in US 1.50%Outside the preference programme (i.e., subject to MFN duty) 22.10%Total above 23.60%

AGOA COUNTRIES (AFRICAN GROWTH AND OppORTUNITY ACT) Total Imports (Million US$) 1 481.90Subject to US content Apparel assembled from US cut fabric & yarn, further processed 0.30%With no US content or under MFN duty Apparel made in a lesser-developed AGOA with non-US fabric 83.40%Apparel from regional fabric from US or African yarn 7.40%Apparel from fabric or yarn determined as not available in US 4.40%Cashmere sweaters, knit-to-shape 0.30%Outside the preference programme (i.e., subject to MFN duty) 4.30%Total above 99.70%

ANDEAN COUNTRIES (ANDEAN TRADE pROMOTION AND DRUG ERADICATION ACT)

Total Imports (Million US$) 1 495.30Subject to US content Apparel assembled from US fabric (finishing in US) 10.60%Brassieres cut and assembled in the US and/or an ATPDEA country 0.20%Total above 10.90%With no US content or under MFN duty Apparel assembled from ANDEAN fabric/yarn 74.90%Apparel, chief value of llama, alpaca, etc. (i.e., Andean components) 1.90%Apparel from fabric or yarn determined as not available in US 0.30%Outside the preference programme (i.e., subject to MFN duty) 12.00%

Total above 89.10%* Product coverage: MFA Source: Compiled from US Department of Commerce data.

13ICTSD Programme on Competitiveness and Sustainable Development

The design of AGOA and Andean preference programme is also essentially the same as that for the CBI, the main difference being that, under AGOA, there is an exception which allows duty-free treatment to apparel made in designated lesser-developed countries16 regardless of the source of fabric or yarn, subject to prescribed annual quantitative limits. Similar to AGOA, the Andean programme permits duty-free entry of apparel assembled in the beneficiary countries from fabric made in the [Andean] region from US or regional yarn. Luckily, for Colombia and Peru, both have had substantial indigenous yarn and fabric production capacities and are therefore able to make do without using US made yarns.

The relative flexibility of origin rules for these programmes can be gleaned from the percentages of imports accounted for by US content or otherwise. The largest share of imports under the CBI programme (over 76 percent) is with US components because they do not have the possibility of enjoying duty benefit unless they use US textile materials. On the other side, the largest shares under AGOA and Andean programmes are against those exceptions that do not require the use of US inputs. Thus little of imports from AGOA countries are made with US content. For Andean countries, too, 89 percent is outside the US-content requirement. Unfortunately, however, those provisions are time-limited 17 and are also subject to prescribed limits as to the maximum annual quantities that could be entered duty-free.

Qualifying Industrial Zones (QIZs)

In 1996 the United States Congress established the Qualifying Industrial Zones (QIZ) initiative to support the peace process in the Middle East.18 These zones are designated industrial parks in Egypt, Israel or Jordan, from which goods can be exported to the United States duty free. The QIZ initiative does not have any expiration date; nor is it required to be renewed by Congress every few years like the Generalized System of Preferences or other trade legislations such as certain provisions of AGOA.

In the case of Jordanian QIZs, the product must be a substantially transformed good, with at least 35 percent of its value added generated in Israel, a Jordanian QIZ or the West Bank/Gaza. Of that 35 percent, a minimum of 11.7 percent must be added in a Jordanian QIZ, 8 percent in Israel, and the remaining 15.3 percent can come from a Jordanian QIZ, Israel or the West Bank/Gaza.19

It is worth noting that the United States also has a free trade agreement with Jordan. The FTA, however, does not supersede or eliminate the QIZ programme. Indeed, currently, the bulk of Jordanian apparel export is under the QIZ programme because it offers immediate tariff and quota-free access to the US market to goods that are produced in the QIZs and meet the specific rules of origin requirements. Under the US–Jordan FTA, on the other hand, tariffs and quotas for many goods are phasing out over time, and rules of origin require 35 percent Jordanian content. Thus for some high-tariff goods, producing in QIZs continues to offer a better advantage. For instance, many apparel goods face US tariffs of up to 30 percent. Under the FTA, tariffs on these goods are to be reduced over ten years, and Jordanian exports would have to meet the 35 percent Jordanian content level. Under the QIZ initiative, those same goods enjoy immediate elimination of tariffs and quotas and require a lower level of Jordanian value-addition.

In the case of the QIZs in Egypt, industrial products, including textiles and apparel, are authorized duty-free entry into the US if these products comply with rules of origin requirements. The required rules state that 35 percent of the commodity’s value must be manufactured in an Egyptian QIZ, with a minimum of 11.7 percent of Israeli inputs.20 The Israeli content requirement is fulfilled if a factory’s cumulative export in each quarter satisfies the agreed-upon ratio.

Furthermore, unlike under some elements in the CBI and AGOA programmes, duty-free access under the QIZ arrangements is not limited by any quotas on quantities that could benefit from duty-free treatment.

14 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

(iii) Canada

From 1 January 2003, Canada substantially modified its GSP scheme for least developed countries, extending full duty-free access to imports of textile and clothing products.21 It also significantly relaxed the origin rules pertaining to these imports. Under these rules, apparel products exported from least-developed countries were made eligible for duty-free treatment if they were cut, or knit to shape, and sewn from inputs from any of the 48 eligible LDCs.

More significantly, apparel products were also made eligible for duty-free treatment even when they used inputs from other developing countries, the only condition being that at least 25 per cent of value addition on the apparel product must have taken place in the LDC exporting country. Any Canadian input materials used in the manufacture of apparel exported from the LDCs are also deemed to originate in the LDC concerned.

In other words, the LDC exports to Canada are now duty-free provided they fulfill any of the following origin criteria: (i) the exported apparel are made with inputs from any least-developed country or Canada; (ii) the exported apparel contain at least 25 per cent value-added in the least-developed country concerned even when the inputs are sourced from other developing countries.

This relaxation compares very favourably with 40 percent value-added required for most of the other non-textiles and clothing items and 60 percent under the normal GSP for developing countries. Little wonder that this revised dispensation resulted in major improvements in the rates of utilization and, thereby, exports from several least-developed countries to Canada (see Chart 2 and Box 2).

Chart 2. Canada Clothing Imports from Least-Developed Countries

(iv) Japan

The Japanese GSP regime includes duty-free treatment for covered textile and clothing from least-developed countries and duty concession at different rates for other developing countries. There is a complex system of ceilings beyond which duty concessions do not apply.

(v) Australia

Like Canada, Australia also extended duty-free

treatment to imports from least-developed countries, but with effect from 1 July 2003. Rules of origin require local content to be 50 percent of total factory cost and that the last manufacture take place in the LDC. A fairly broad definition of local content is provided to meet the 50 percent target. An LDC can include input from other LDCs, developing countries, Pacific Island countries and Australia in calculating the 50 percent content. Within this, non-LDC developing country content is, however, subject to a maximum of 25 percent of manufacturing cost.22

15ICTSD Programme on Competitiveness and Sustainable Development

III. THE NEXUS BETWEEN ORIGIN RULES AND TRADE UNDER pREFERENTIAL ARRANGEMENTS

For years, then, trade in textiles and clothing has been subject to the influence of policy intervention through three main policy tools: (i) quota restrictions, (ii) tariff preferences, and (iii) origin rules including, especially those that condition the access to preferences to the sourcing of textile inputs from preference-giving countries.

This section is designed to map the development of trade in textiles and clothing, especially in the context of preferential arrangements and the role of origin rules in linking the sourcing of textile inputs by preference-receiving countries from preference-granting countries.

A. TEXTILE TRADE HAS BEEN SUBjECT TO pERSISTENT pOLICY CHANGES

Interpreting textile and clothing trade data is fraught with complications. It does not lend itself to broad-brushed generalizations. For one thing, all preferential schemes were not launched at the same time. For another, over time, changes have been introduced to the extent and quality of preferences under some preferential programmes. Further still, the origin rules pertaining to various preference schemes have been far from uniform.

The US CBI initiative has been on the go since 1984; NAFTA became effective from 1994; AGOA from late 2000; the US programme of Qualifying Industrial Zones (QIZs) in respect of Jordan and Egypt from 2001 and 2005 respectively; and the Andean preferences from 2002. 23

As to the quality of preference, the Caribbean Basin Economic Recovery Act (which covered the trade elements of the umbrella programme, CBI) did not include textiles and clothing for duty-free treatment. Traders could only take advantage of a US Customs provision that provided duty exemption on the value of US inputs incorporated in the imported products. In 1986, the US established the Special Access Programme for CBI countries, the accent of which was on extending additional (virtually unlimited) quota access for textiles and apparel provided the additional quotas were used in conjunction with US inputs. The Trade Act of 2000 accorded complete duty-free treatment to CBI apparel subject of course to prescribed origin rules requiring, in most cases, that the products are made with US yarns and fabrics. The Andean programme was brought at par with that for the CBI beneficiaries only from 2002.

As noted in the previous section, Mexico was also provided special access quotas from 1988 linking this access to the use of “fabrics wholly formed and cut in the United States”.24 The added advantage of duty concession in the form of remission of duty on the value of US content was also available as in the case of the Caribbean countries. From 1994, Mexico got on to a faster track – complete duty free access – pursuant to NAFTA.

The AGOA included a time-bound exception to the general origin rule so that it provided duty-free access for specified quantities of apparel from designated lesser-developed Sub-Saharan African countries regardless of the source of fabric or yarn.25 This so-called ‘third country fabric’ provision has since been extended through September 2012.26

Origin rules under Jordanian and Egyptian QIZ schemes did not tie the duty-free treatment to the use of US materials.

On the EU side, too, Bulgaria and Romania became entitled to duty exemption from different times. Prior to that, both these countries also used to be subject to MFA/ATC quotas. In the case of the countries of the Maghreb, the preferential treatment had been in effect for much longer.

And Canada and Australia extended duty-free access to least-developed countries with vastly liberal origin rules only from 2003.27

In a nutshell, aside from the implementation of various preferential programmes from different

16 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

points in time, significant modifications were made over time to the origin rules relating to particular schemes. And the textile and clothing scene witnessed a fundamental transformation in the competitive landscape with the expiry of

quota restrictions at the end of 2004. All these changes naturally exerted profound influence on the evolution of trade in the sector, as also on the fortunes of many countries.

B. RECENT DEVELOpMENTS IN TEXTILE TRADE

Under strong influence of major developed countries’ trade policy, trade in textiles and clothing has been far from any consistent or level playing field. Even so, the world has never stood still in the sector. With every major change in the policy environment, the sector has a history of responding with agility and pace.

Little wonder therefore that many a forecast made in the run up to the final phase-out of quota restrictions proved wide of the mark. Tables 1 and 2 show the progression of US imports from 1990 and EU imports from 1995.

Noticeably, countries that the pundits had predicted to become casualties of quota abolition, or who feared for their competitiveness in the face of increased competition, have defied predictions and forged ahead very strongly. Top of the list of such countries have been Bangladesh, Cambodia, Egypt, Indonesia and Vietnam.

Taking the US and EU markets together, in the two years since the expiry of quotas, Bangladesh increased its exports by 31 percent or a handsome

USD 2.13 billion; Cambodia by 36 percent or USD 756 million; Indonesia by 29 percent or USD 1.39 billion, Vietnam by 33 percent or USD 1.2 billion and Egypt by 25 percent or USD 337 million.

However, countries that were assumed to continue to do well have been increasingly feeling the pinch of competition. Ironically, most of these are precisely those that enjoy the advantage of preferential access to the main developed country markets. A major factor standing in the way of sustainability of their exports appears to be the inflexibility of their trade structures due, in large measure, to the rigidity of origin rules.

The following analysis of the influence of origin rules is therefore set in light of experience with the working of those rules. It offers, first, a short overview of the development of trade for preference-receiving countries. It then presents an exposition of their general export profiles, followed by an analysis of the sourcing patterns of their raw material requirements under compulsion of the applicable origin rules.

17ICTSD Programme on Competitiveness and Sustainable Development

Table 1. US Imports of Textiles and Clothing from Top 30 and Preferential Suppliers (1990–2006)

Import value in million US$ Share in total US imports

Source: Eurostat; Product coverage: Section XI of HS excluding Agricultural products covered by WTO Agreement on Agriculture * Denotes main preferential suppliers

Table 2. EU-25 Imports of Textiles and Clothing from Top 30 and Preferential Suppliers (1995–2006)

19ICTSD Programme on Competitiveness and Sustainable Development

Source: US Department of Commerce, Eurostat, UN Comtrade. Note: Product coverage for US: MFA; EU and Canada: HS Section XI excluding agricultural products covered by WTO Agreement on Agriculture.

C. TRADE FLOWS UNDER pREFERENTIAL ARRANGEMENTS

The progression of trade from preference-receiving countries is summed up in Box 2 below. For purposes of this analysis preference-receiving countries are taken as those in receipt of both non-reciprocal and reciprocal preferences.

Insofar as the US market is concerned, in • 1990, i.e., before NAFTA, the share of NAFTA partners in US imports of MFA textiles and clothing was only 4.2 percent. By 2000, this share had leapt to 18.2 percent. Mexico’s share alone ballooned from 2.4 percent in 1990 to 13.5 percent in 2000.

The CBI countries likewise advanced from 7.2 percent of total US imports in 1990 to 13.4 percent in 2000.

Between 1990 and 2000 the share of AGOA countries had merely inched forward from 0.7 percent to 1.1 percent. With AGOA preferences becoming available towards the end of 2000, it advanced to 2.1 percent by 2004.

Box 2. US/EU-25/Canada Textiles and Clothing Imports from Selected Preferential Partners

20 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

D. SOURCING OF RAW MATERIALS BY pREFERENCE-RECEIVING COUNTRIES

As noted in earlier sections, by virtue of applicable origin rules tariff preferences for most preference-receiving countries are closely linked to the use

of yarn and fabrics from preference-granting countries. In this sub-section we study the actual patterns of sourcing of textile materials

Jordan got on to the fast track by virtue of the duty-free access under US’s QIZ scheme in 2001. It consequently boomed from non-existent exports to capture 1.3 percent of the import market by 2006.

Overall, the combined share of NAFTA, CBI, Andean and AGOA countries and Jordan in US imports of MFA textile and clothing increased from 13.1 percent in 1990 to 34 percent in 2000, before declining to 23.6 percent in 2006.

On the EU market, too, Bulgaria and • Romania became relatively new entrants to the preference league. While Bulgaria increased its share of extra-EU imports from 0.9 percent in 1995 to 1.9 percent in 2004, Romania advanced from 2.8 percent to 6.3 percent in the same period. Under pressure of competition in the wake of expiry of quota restrictions, both these countries’ shares also declined in 2006: to 1.8 percent and 5 percent, respectively.

Morocco and Tunisia have been struggling as much as some established preferential supplier countries to the United States.

Canada granted duty free access with • vastly improved origin rules to least-developed countries from the beginning of 2003. On the back of this concession, LDCs share of Canadian imports increased from 1.9 percent in 2002 to 4.3 percent in 2003, and 5.9 percent in 2004. Of these, Bangladesh alone advanced from 1.3 percent in 2002 to 4.1 percent in 2004.

(i) Preferential suppliers’ export profile:Predominantly apparel and concentration on single markets

Most preference-receiving countries mainly export apparel products, owing largely to their small or, in most cases, non-existent indigenous capacities to produce textile materials (yarns and fabrics). Virtually all US imports from Costa Rica, the Dominican Republic, El Salvador, Guatemala, Haiti, Honduras, Nicaragua28, Jordan and almost all AGOA countries consist of apparel products. Even for Mexico, the share of apparel in its total textile and clothing exports to the US is about 84 percent. Compared to this, the share of clothing in US imports of textiles and clothing from China is 68 percent, India 63 percent, and Pakistan 43 percent.

A similar situation is to be observed on the EU market where 88 percent of Romania’s sector exports are apparel. The comparable percentages of other major preferential suppliers to this market are: Bulgaria 83 percent, Tunisia 91 percent, Bangladesh 95 percent, Morocco 96 percent, and Cambodia 100 percent.

It is also worth noting that exports of a majority of preference-receiving countries are concentrated on either the US or the EU market. Only a few – mainly Asian – countries’ exports are diversified over both these main markets. Thus, for example, in 2006 Mexico shipped USD 6,376 million worth of textile and clothing to the US, but just USD 121 million to EU-25. Similarly, Jordan’s exports to the US amounted to USD 1,254 million, but only USD 12 million to EU-25. On the other side of the Atlantic, Romania exported USD 5,004 million worth to EU-25, just USD 130 million to the US. Likewise, Tunisia’s exports to EU-25 were USD 3,374 million, but to the US only USD 49 million; and Morocco’s USD 3,100 million to the EU, only USD 102 million to the US.

21ICTSD Programme on Competitiveness and Sustainable Development

by various preference-receiving countries to assess the impact that these rules have on their competitiveness.

Ideally this analysis should be based on review of the preference-receiving countries’ own import streams. Unfortunately, however, the quality of available data in respect of these countries leaves much to be desired. In general, there are large gaps in their data sets. In many a case, the trade from export processing zones is not included in their export or import figures. Even a cursory comparison of export numbers found in the nationally-reported figures of many of these countries reveals wide differences from the related numbers in their import partners’ data.

Likewise, imports for their export processing zones are seldom reflected in their import figures.29

We are therefore obliged to turn to counterpart data from the preference-granting countries, unless otherwise stated in particular cases.

(i) Preference-receiving countries as captive markets for US/EU producers

First, it should be instructive to cast a glance on the composition and direction of textile and clothing exports of the United States and the European Union themselves – the two main preference-granting economies. See charts 3A and 3B.

Chart 3A. US Exports of Textiles and Clothing to Preferential Partners

Chart 3B. EU Exports of Textiles and Clothing to Main Preferential Partners

22 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

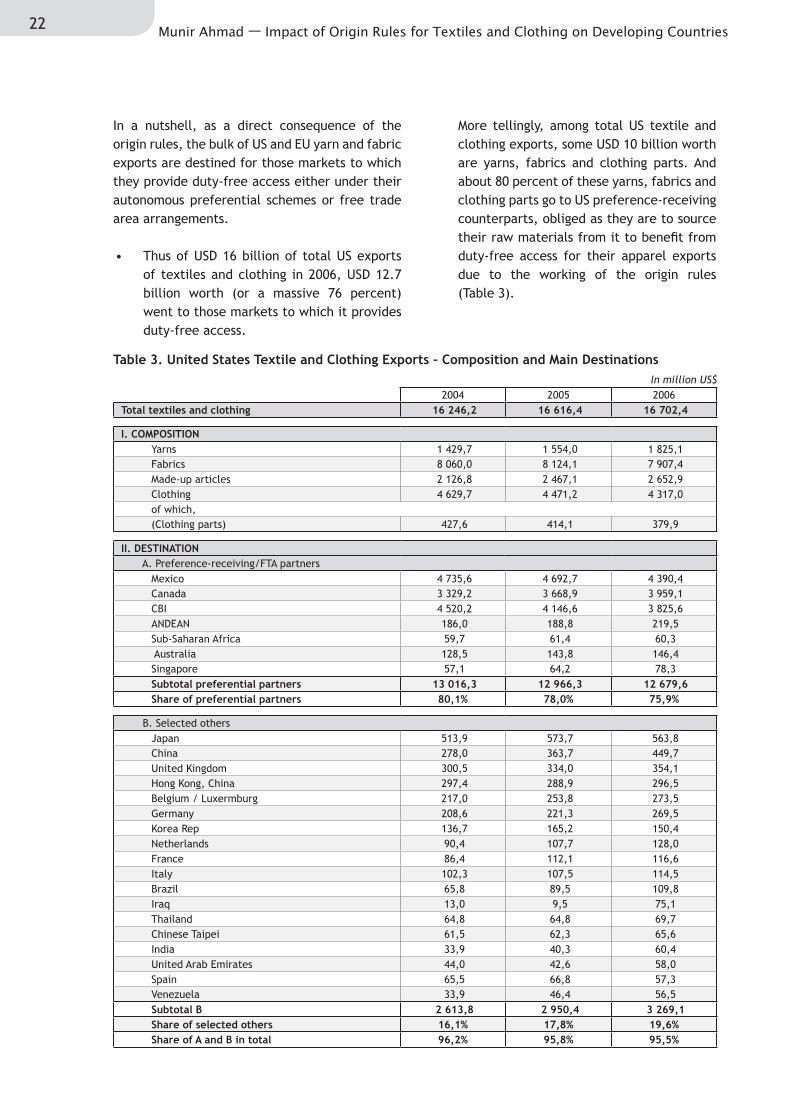

In a nutshell, as a direct consequence of the origin rules, the bulk of US and EU yarn and fabric exports are destined for those markets to which they provide duty-free access either under their autonomous preferential schemes or free trade area arrangements.

Thus of USD 16 billion of total US exports • of textiles and clothing in 2006, USD 12.7 billion worth (or a massive 76 percent) went to those markets to which it provides duty-free access.

More tellingly, among total US textile and clothing exports, some USD 10 billion worth are yarns, fabrics and clothing parts. And about 80 percent of these yarns, fabrics and clothing parts go to US preference-receiving counterparts, obliged as they are to source their raw materials from it to benefit from duty-free access for their apparel exports due to the working of the origin rules (Table 3).

Table 3. United States Textile and Clothing Exports – Composition and Main DestinationsIn million US$

B. others 1 911,9 2 088,3 2 357,5 Share of others 19,3% 20,7% 23,3%

Source: Compiled from US Commerce Department data Note: Clothing parts for this table are only HS lines: 611780, 611790, 6217.

A similar situation is found in the EU, • although the extent of its textile industry’s dependence on captive preference-receiving markets is not as pronounced as it is in the case of the United States. Thus, of the total extra-EU exports of USD 43 billion, well

over 40 percent goes to nine30 of its main preferential markets. More significantly, as in the case of the US, the largest share of its yarns, fabrics and clothing parts (about 55 percent) goes to those same preferential countries (Table 4).

Table 4. EU-25 Textiles and Clothing Exports – Composition and Main Destinations

In million US$

2003 2004 2005

Total textiles and clothing (Extra EU-25) 37 437,5 42 480,2 43 177,1

I. Composition

Yarns 2 484,1 3 260,3 3 090,3

Fabrics 10 782,6 12 108,9 11 477,8

Made-up articles 8 149,6 9 158,2 9 445,9

Clothing 15 740,0 17 585,6 18 454,4

of which,

(Clothing parts) 1 083,4 1 215,0 1 171,5

II. Destination

A. Main preference-receiving/FTA partners

Switzerland 3 919,5 4 358,5 4 453,5

Romania 3 124,3 3 625,2 3 426,8

Tunisia 2 144,8 2 282,6 2 097,8

Turkey 1 671,2 2 192,2 2 023,6

Morocco 1 864,5 1 955,4 1 862,6

Norway 1 183,0 1 276,3 1 315,3

Bulgaria 1 127,4 1 294,0 1 255,0

Croatia 712,5 775,1 758,8

Mexico 521,5 547,9 600,3

Subtotal main preferential partners 16 268,7 18 307,1 17 793,7

Share of main preferential partners 43,5% 43,1% 41,2%

24 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

2003 2004 2005

B. Selected others

United States 5 205,3 5 756,2 5 673,6

Russia 1 839,2 2 425,8 3 037,2

Japan 2 211,8 2 288,3 2 282,1

Hong Kong, China 1 540,1 1 787,5 1 854,4

Ukraine 786,8 992,6 1 098,0

China 549,8 683,8 840,4

Korea Rep. 762,1 721,3 738,3

Canada 614,0 692,1 682,0

United Arab Emirates 382,5 633,8 674,8

Saudi Arabia 534,2 570,6 571,2

Australia 413,9 442,1 455,0

Israel 286,0 339,0 341,3

Chinese Taipei 284,2 324,1 333,1

Macedonia 254,4 302,4 313,0

South Africa 182,2 216,2 241,3

Bosnia and Herzegovina 171,4 197,7 240,5

India 177,0 202,4 233,0

Brazil 147,0 187,4 225,7

Lebanon 219,8 222,7 214,7

Belarus 175,4 188,7 211,2

Singapore 191,2 207,8 203,8

Albania 169,9 201,9 202,3

Serbia - - 201,2

Thailand 162,8 193,7 201,1

Subtotal B 17 260,9 19 778,0 21 069,2

Share in total 46,1% 46,6% 48,8%

Share of A and B in total 89,6% 89,7% 90,0%

III. Destination of yarns, fabrics, clothing parts

Total to world 14 350,1 16 584,2 15 739,6

A. Main preference-receiving/FTA partners

Romania 2 199,5 2 556,5 2 371,0

Morocco 1 558,1 1 598,3 1 467,3

Tunisia 1 471,3 1 569,1 1 420,6

Turkey 974,3 1 314,2 1 096,4

Bulgaria 666,6 776,2 760,4

Switzerland 532,2 613,6 595,9

Croatia 273,5 305,7 272,5

Mexico 182,6 185,2 190,3

Norway 118,0 122,8 119,2

Subtotal main preferential partners 7 976,0 9 041,6 8 293,6

Share of main preferential partners 55,6% 54,5% 52,7%

B. Others 6 374,1 7 542,6 7 445,9

Share of others 44,4% 45,5% 47,3%

Note: Clothing parts for this table are only HS lines: 611780, 611790, 6217. Source: Compiled from Eurostat data.

Table 4. continued

25ICTSD Programme on Competitiveness and Sustainable Development

It is important to note that, for purposes of this analysis, clothing parts were defined as only those covered by HS codes/headings 6117.80, 6117.90 and 62.17. As a matter of fact, however, unfinished or semi-finished articles31 of clothing are classified in the same headings as for the finished articles. Therefore taking only the three HS headings (as done here) significantly understates the true extent of US/EU exports of unfinished apparel. As a factual matter, traffic in unfinished apparel represents much larger trade between them and their preference-receiving partners than is captured in the HS codes earmarked for our calculations. Therefore, a better gauge is to look at US and EU total exports of textiles and clothing and compare them to their imports from the partner

preference-receiving countries. Much of the following analysis is on this basis.

(ii) Binding influence of origin rules onpreference-receiving countries’ sourcing of textile materials from preference-granting countries

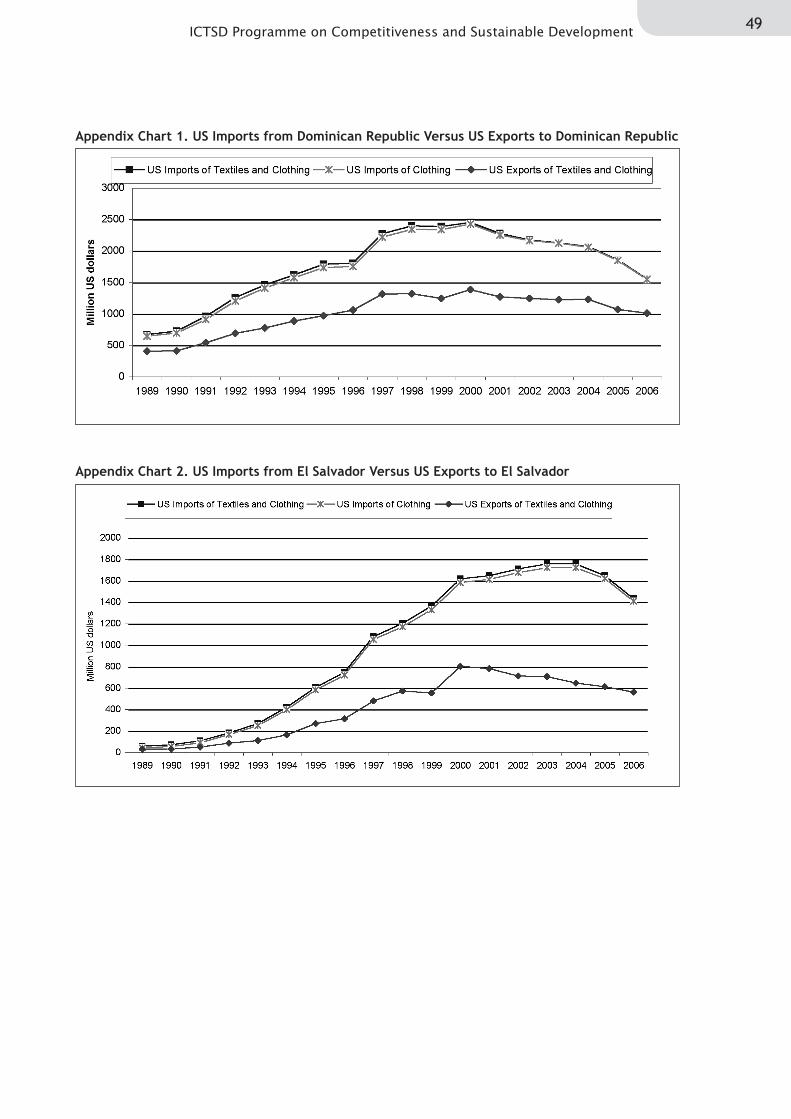

Charts 4–7 are designed to show the flow of trade between the US and Mexico and CBI group of countries on one side and AGOA and the Andean country groups on the other. Separate charts relating to the Dominican Republic, El Salvador, Honduras and Jordan are provided in the Appendix. These are the main preferential exporters to the United States.

Chart 4. US Imports from Mexico Versus US Exports to Mexico

Chart 5. US Imports from CBI Versus US Exports to CBI Countries

26 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

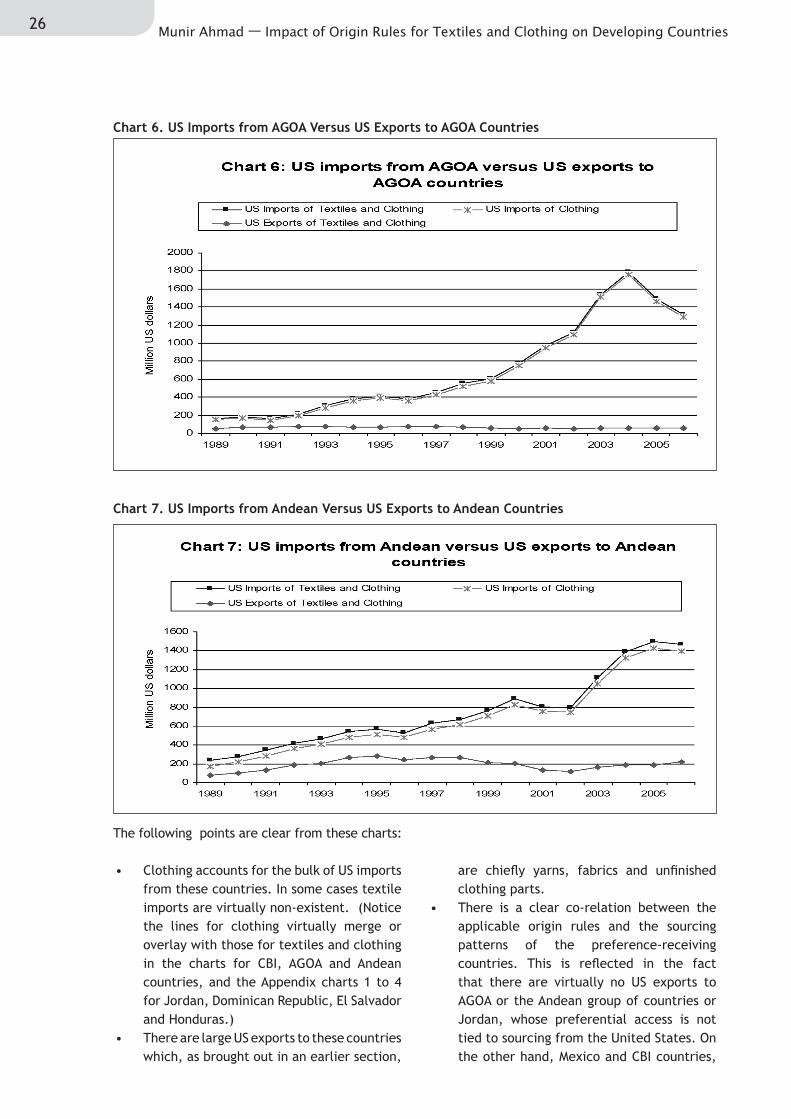

Chart 6. US Imports from AGoA Versus US Exports to AGoA Countries

Chart 7. US Imports from Andean Versus US Exports to Andean Countries

The following points are clear from these charts:

Clothing accounts for the bulk of US imports • from these countries. In some cases textile imports are virtually non-existent. (Notice the lines for clothing virtually merge or overlay with those for textiles and clothing in the charts for CBI, AGOA and Andean countries, and the Appendix charts 1 to 4 for Jordan, Dominican Republic, El Salvador and Honduras.) There are large US exports to these countries • which, as brought out in an earlier section,

are chiefly yarns, fabrics and unfinished clothing parts.There is a clear co-relation between the • applicable origin rules and the sourcing patterns of the preference-receiving countries. This is reflected in the fact that there are virtually no US exports to AGOA or the Andean group of countries or Jordan, whose preferential access is not tied to sourcing from the United States. On the other hand, Mexico and CBI countries,

27ICTSD Programme on Competitiveness and Sustainable Development

Chart 8. EU-25 Imports from romania Versus EU-25 Exports to romania

Chart 9. EU-25 Imports from Tunisia Versus EU-25 Exports to Tunisia

whose privileged access is linked to sourcing from the United States, are large recipients of US exports. While those bound by tight origin rules have • seen their exports either decline or struggle following the expiry of quota restrictions (as Mexico and the CBI), those that are not so obliged appear to be holding their own (notice especially the performance of

Jordan shown in Appendix Chart 4 and of the Andean countries in Chart 7 above!). A similar situation is to be found with respect to the EU’s relationship with Bulgaria, Morocco, Romania and Tunisia, on one hand, and Bangladesh or Cambodia on the other. All these are by far the largest and most representative of the preference-receiving exporters of clothing to the EU. See charts 8–13.

28 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

Chart 10. EU-25 Imports from Morocco Versus EU-Exports to Morocco

Chart 11. EU-25 Imports from Bulgaria Versus EU-25 Exports to Bulgaria

29ICTSD Programme on Competitiveness and Sustainable Development

Chart 12. EU-25 Imports from Bangladesh Versus EU-25 Exports to Bangladesh

Chart 13. EU-25 Imports from Cambodia Versus EU-25 Exports to Cambodia

Here again there is a close nexus between EU imports from Bulgaria, Morocco, Romania and Tunisia and EU exports to these countries. They are obliged to source their raw material requirements from EU countries or, at most, from within the larger cumulation area. And, as for Jordan, Andean and AGOA countries in the United States, there are virtually non-existent EU exports to Bangladesh and Cambodia as these do not have to operate under any such bind.

It follows from the analysis presented in this section that rules of origin have closely tied the sustainability of many preference-receiving countries apparel exports to sourcing of textile materials from preference-granting countries with all the added costs that such sourcing entails – by way of the rigidity of production processes and additional administrative costs.

30 Munir Ahmad — Impact of Origin Rules for Textiles and Clothing on Developing Countries

IV. ORIGIN RULES AND DISTORTIONS IN TEXTILE TRADE

The raison d’être of rules of origin in preferential arrangements is to ensure that preferences primarily benefit the intended beneficiaries. A producer’s decision whether to export under the preferential tariff regime or under the MFN regime involves weighing the margin of preference it gets from the preference-granting country against the costs that compliance with rules of origin entails. If the cost of compliance with origin rules (including the cost of material that the producer is bound to source from the preference-granting country and the administrative costs involved in complying with the rules) is sufficiently lower

than the available preference, he would have the incentive to produce and export under the preferential programme. Failing that, he would be better off doing business under the normal MFN rates of tariff.