MIL-15.1/13.12-07112017-142804/DF CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited Impacts of new accounting standards for Credit Loss Allowances (IFRS 9) Mumbai, January 23 rd , 2018 | Insights from the industry survey

Transcript

MIL-15.1/13.12-07112017-142804/DF

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Impacts of new accounting

standards for Credit Loss

Allowances (IFRS 9)

Mumbai, January 23rd, 2018 | Insights from the industry survey

2IACPM – McKinsey & Company

▪ What we did

▪ What we learned

Agenda

3IACPM – McKinsey & Company

Why did we decide to do a survey on new accounting standards for credit

loss allowances?

1 Report on Results from the EBA Impact Assessment of IFRS9 European Banking Authority, November 2016, p. 33, eba.europa.eu

GLOBALNew accounting standards with worldwide

coverage

MATERIAL

INCOMING

POTENTIALLY

DISRUPTIVE

EBA estimates1 20% increase in provisions at

first-time adoption and highly pro-cyclical with

significant future reserve volatility

First application in 2018 for IFRS 9

Beyond accounting, introducing also business

and strategic implications

4IACPM – McKinsey & Company

The survey aims to achieve 3 main objectives through the analysis

of 6 areas

Get an industry view on strategic

and business implications of the

accounting changes, and

understand key priorities for banks

on this topic

Create a common view on critical

elements to discuss with

stakeholders, e.g., regulators

OBJECTIVES

Project status and governance

Key design choices

SURVEY'S SECTIONS

Impact on portfolio strategies

Implications on commercial

policies

Modification of credit risk

management practices

Regulatory response

Gather and share insights on

different approaches that banks

are using for the implementation of

IFRS91

2

3

The final survey contains a maximum of 38 questions, depending on applicable standards and facultative topics

5IACPM – McKinsey & Company

51 financial institutions across all regions completed the survey

LEADING INSTITUTIONS HELPED IDENTIFY TRENDS

South

America

(2 banks)

Africa (3 banks)

Europe (15 banks)

North America (25 banks)

Asia (4 Banks)

Australia/

Oceania

(2 banks)

▪ The survey’s

focus was to

understand

market

participants’

views of the

business and

commercial

impacts of the

new

accounting

standards

McKinsey & Company

▪ What we did

▪ What we learned

Agenda

7IACPM – McKinsey & Company

Three key takeaways from the survey Focus of next pages

… and there is concern that the new, highly pro-

cyclical reserving model, could have profound

consequences for earnings and capital in a

downturn

While banks have focused on the high

complexity of IFRS 9 implementation… 1

… substantially less time has been focused on

impact, with significant uncertainty on strategic

and business implications…

2

3

8IACPM – McKinsey & Company

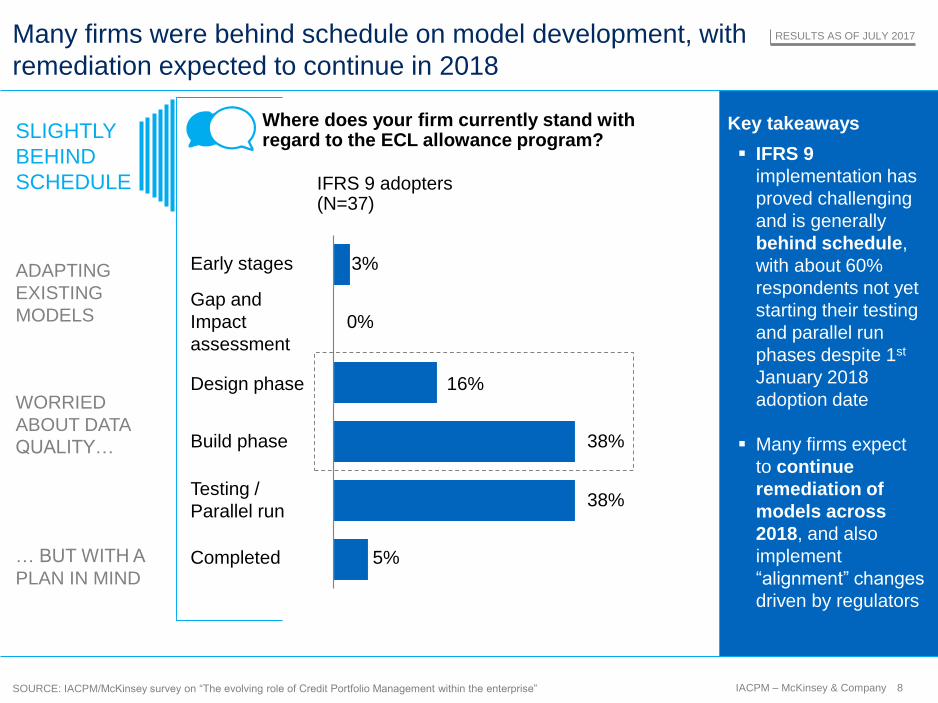

Many firms were behind schedule on model development, with

remediation expected to continue in 2018

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

Completed

38%

5%

0%

Early stages

Gap and

Impact

assessment

38%

16%

3%

Design phase

Build phase

Testing /

Parallel run

IFRS 9 adopters (N=37)

Key takeaways

▪ IFRS 9

implementation has

proved challenging

and is generally

behind schedule,

with about 60%

respondents not yet

starting their testing

and parallel run

phases despite 1st

January 2018

adoption date

▪ Many firms expect

to continue

remediation of

models across

2018, and also

implement

“alignment” changes

driven by regulators

SLIGHTLY

BEHIND

SCHEDULE

ADAPTING

EXISTING

MODELS

WORRIED

ABOUT DATA

QUALITY…

… BUT WITH A

PLAN IN MIND

RESULTS AS OF JULY 2017

Where does your firm currently stand with regard to the ECL allowance program?

9IACPM – McKinsey & Company

Key takeaways

The majority of firms are building on existing models for

IFRS 9, but data quality is frequently the biggest challenge

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

Is your firm planning to leverage / use existing model infrastructure for ECL models to drive synergies?

▪ The majority of the

banks are leveraging

on existing models

and infrastructure

(e.g., Stress Testing,

Basel II)

▪ Only ~10% of the

IFRS 9 adopters plan

to redevelop new

models and

segmentation

▪ More than 60% of the

banks anticipate

limitations in internal

data to cause

implementation

challenges, however

they have already

identified potential

remediation

strategies

RESULTS AS OF JULY 2017

SLIGHTLY

BEHIND

SCHEDULE

ADAPTING

EXISTING

MODELS

WORRIED

ABOUT DATA

QUALITY…

… BUT WITH A

PLAN IN MIND

14%

11% 65% 24%

62%

11%

8%

87%

86%

30%

3%

0%

Topic still under investigation / Not applicableYesNo

IFRS 9 adopters (N=37)

Segmentation

C&IB Lending

Project Finance

Retail Lending

10IACPM – McKinsey & Company

Three key takeaways from the survey Focus of next pages

… and there is concern that the new, highly pro-

cyclical reserving model, could have profound

consequences for earnings and capital in a

downturn

While banks have focused on the high

complexity of IFRS 9 implementation… 1

… substantially less time has been focused on

impact, with significant uncertainty on strategic

and business implications…

2

3

11IACPM – McKinsey & Company

Uncertain effects will be unequally distributed, with the

potential for significant impacts on pricing, average terms

and willingness to lend for the most affected asset classes

ortDisprop ional effects

12IACPM – McKinsey & Company

Key takeaways on impact on portfolio strategies

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

LIMITED

BUSINESS

ENGAGEMENT

LENDING MIX

About 40% of the banks expect to change

the treatment of high risk clients as a

consequence of IFRS 9 adoption, but the

majority of the responders are still

investigating possible future mitigation

interventions

HIGH RISK

CLIENTS

FOOD FOR

THOUGHT

▪ Responses reveal a

lack of clear

consensus on how

the new standards

will affect price /

term / willingness

to lend

▪ The first adoption

may cause no

significant

commercial

impact, requiring a

downturn before

the consequences of

the new models are

fully understood

About 40% of the banks expect to change

their lending mix as a consequence of IFRS 9

adoption, with reductions in appetite for

disproportionately affected asset classes:

volatile sectors, higher risk assets and long

maturity deals

The lack of focus on business and strategic

impact is exacerbated by the fact that most

banks are running their IFRS 9 adoption

programs from their risk and finance

departments, without the active involvement of

business unit leaders.

RESULTS AS OF JULY 2017

13IACPM – McKinsey & Company

METHODOLOGY

FOR PRICING

Key takeaways on implications on commercial policies

50% of the banks think that IFRS 9 could affect

the pricing methodology, both through

utilization of better models and taking account

of lifecycle credit costs

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

More than 40% of the banks expect unequal

effects on profit margins across firms as a

consequence of IFRS 9 adoption, mainly due

to differences in assumptions, geography,

portfolio, data availability and modelling

approaches

DIFFERENTIATED

PROFIT

MARGINS

The changes in appetite and profitability are

likely to determine capital re-allocation and

increasing competitiveness in “IFRS 9 friendly”

asset classes

APPETITE AND

PROFITABILITY

FOOD FOR

THOUGHT

▪ The change in

appetite and costs

are likely to result in

capital re-allocation

▪ Banks could adopt

pricing schemes

that could help to

distribute part of the

IFRS 9 cost to

customers

▪ Banks could develop

“IFRS 9 friendly”

products especially

for high risk clients

▪ RM’s will play a more

active portfolio

management role

RESULTS AS OF JULY 2017

14IACPM – McKinsey & Company

Key takeaways on modification of credit risk practices

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

About 40% of the banks think that IFRS 9 will

trigger the necessity to review credit

management processes and organization

CREDIT

MANAGEMENT

PROCESS

CREDIT RISK

APPETITE

EARLY WARNING

SYSTEMS

About 40% of the banks expect credit risk

appetite to change as a result of the new

IFRS 9 standards

There are two camps of responders: those who

say credit economics are not changing, and

those who say that impact on EAR and Capital

will be significant and affect appetite.

Almost 50% of the IFRS 9 adopters anticipate

changes in their early warning systems by

establishing new measures (e.g., introduction

of forward-looking risk indicators, enhancing

watch list)

RESULTS AS OF JULY 2017

FOOD FOR

THOUGHT

▪ Banks could

reinforce

underwriting

criteria and active

credit portfolio

management by:

– Enhancing

early-warning

system

– Developing a

rating advisory

service

– Reinforcing

dedicated

approach for

proactive credit

management

15IACPM – McKinsey & Company

Key takeaways on regulatory response

About 43% of the banks adopting IFRS 9

anticipate increased capital requirement

whilst about ~70% plan to embed ECL into

stress testing

Impact on increased stress testing peak-to-

through still poorly understood.

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

STRESS

TESTING

NON-LEVEL

PLAYING FIELD

GUIDANCE ON

SCENARIO

ASSUMPTIONS

▪ Stress capital impacts likely to be substantial as a result of accelerated recognition of forward credit losses without offsetting PPNR

▪ In order to better face next regulatory stress test, banks could develop methodological approach to better simulate staging under stressed test scenario

About 65% of the banks expect that

differences between CECL and IFRS 9 will

drive significant differences in provisions

levels and volatility, creating a non-level

playing field for certain products, with a

general advantage for IFRS 9 adopters

Almost one third of the banks anticipate

guidance on scenario assumptions to drive

consistency and comparability of results,

while half of the banks are not expecting any

formal or informal guidance

RESULTS AS OF JULY 2017

FOOD FOR TOUGHTS

16IACPM – McKinsey & Company

Three key takeaways from the survey Focus of next pages

… and there is concern that the new, highly pro-

cyclical reserving model, could have profound

consequences for earnings and capital in a

downturn

While banks have focused on the high

complexity of IFRS 9 implementation and

modelling…

1

… substantially less time has been focused on

impact, with significant uncertainty on strategic

and business implications…

2

3

17IACPM – McKinsey & Company

Closing reflections: the consequences of pro-cyclicalityImplementing pro-cyclical models during benign credit periods can have unintended consequences

17IACPM – McKinsey & Company

THANK YOU!

In a typical 2-3 year downturn, impairments are charged over the

period as losses are incurred. These losses are partially mitigated by

PPNR over the same period.

In the new world, there is intended to be accelerated recognition of

all future expected credit losses on entering a downturn.

Squeeze

impairments

into fewer

periods

Steep

reserve

builds

Less time

for offsetting

PPNR

High

earnings

volatility

Sharp

impact on

capital

Model overshooting likely to worsen this effect

18IACPM – McKinsey & Company

Appendix

19IACPM – McKinsey & Company

New accounting standards constitute a paradigm shift in requirements

FROM EVENT DRIVEN … … TO MODEL DRIVEN

IAS 39 accounting standard is based on

"incurred loss" criteria where the impairment is

mainly recognized only after a trigger loss event

has occurred

IFRS 9 is based on “expected loss” criteria

requiring forward-looking approaches incorporate

future economic scenarios

An event driven approach implies:

▪ Delays in the recognition of a credit loss event until there is objective evidence of an impairment

▪ Lack of consideration of future credit loss events even when they are expected

A model driven approach implies:

▪ Basel II – like expected loss approaches with consideration of PD, LGD and EAD

▪ Data quality and availability to feed models with

▪ Significant increase in pro-cyclicality, with losses accelerated to today as expectations worsen

▪ Potential disconnect of income and expense, as future losses are provided before income is earned

20IACPM – McKinsey & Company

Key takeaways on strategic and business implications

IMPACT ON

PORTFOLIO

STRATEGIES

IMPACT ON

COMMERCIAL

STRATEGIES

REGULATORY

GUIDANCE

MODIFICATION

IN CREDIT RISK

MANAGEMENT

PRACTICE

The majority of banks expect to change their lending mix,

▪ Banks could aim to steer their commercial focus to sectors that are more resilient

through the economic cycle

▪ Banks could consider developing asset-light business models for higher risk

products and/or sectors

The change in appetite and costs are likely to result in capital re-allocation

▪ Banks could adopt pricing schemes that could help to distribute part of the IFRS 9

cost to debtors

▪ Banks could develop “IFRS 9 friendly” products especially for high risk clients

▪ Relationship managers will have to play a more active role on portfolio

management

By a ratio of 2.5 to 1, CECL adopters are expecting the new standards to drive

increased capital requirements through the stress testing (CCAR) process

Banks could reinforce underwriting criteria and active credit portfolio

management by:

▪ Enhancing early-warning system

▪ Developing a rating advisory service

▪ Reinforcing dedicated approach for proactive credit management

21IACPM – McKinsey & Company

Summary of main insights and possible

areas of intervention QUALITATIVE ANALYSIS

1 Impact on lending mix, lending mix evolution analysis

2 Effects on pricing, effects on profit margins

3 Credit management review, changes in credit management

IMPACT ON PORTFOLIO

STRATEGIES1

IMPLICATIONS ON

COMMERCIAL STRATEGIES2

MODIFICATION OF CREDIT

RISK MANAGEMENT3

Complexity Complexity Complexity

Rea

din

es

s

Rea

din

es

s

Rea

din

es

s

High priorityHigh priority High priority

IFRS 9

▪ Adjust portfolio strategies to prevent increase in P&Lvolatility (e.g., steer commercial focus, accelerate active portfolio management)

▪ Review pricing methodologies and approaches to preserve profitability (e.g., pricing grids)

▪ Review of current product catalogue (e.g., extension options, break-up covenants)

▪ Develop dedicated products for high risk clients (e.g., adjust maturity, repayment schedule)

▪ Reform credit management practices to prevent the deterioration of the exposure (e.g., upgrade early warning management)

▪ Introduce rating advisory services

▪ Rethink deal organization to reflect changes in risk appetite

RESULTS AS OF JULY 2017

22IACPM – McKinsey & Company

~40% of the banks anticipate changes in lending mix,

whether by lowering maturities or reducing risks

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

LENDING MIX – IMPACT ON PORTFOLIO STRATEGIES

Reduction of unsecured

portfolio asset classes

14%

3%

3%

Reduction of large loans

during the last months

Changes expected; but topic

is still under investigation24%

11%

Reduction in lending to

high-risk clients14%

Reduction of long-maturity

portfolio asset classes

Reduction in lending to

more volatile sectors

46%Impact on lending mix 38% 16%

Can’t say, topic

under investigation

No change

Changes expected

IFRS 9 adopters2

(N=37)

1 Multiple choice question, respondents could chose more than one applicable options

2 IFRS 9 ready participants (i.e., in the testing or completed phase) show results consistent with the others IFRS 9 responders, despite a reduction in “still under investigation” weight

How do you expect your firm’s lending mix to evolve as a result of these potential increases in provisioning levels?1

RESULTS AS OF JULY 2017

Key takeaways

▪ IFRS 9 adopters expect reduction in more volatilesectors and high-risk clients are key changes in the lending mix

23IACPM – McKinsey & Company

Banks who have started analyzing future treatment

of high-risk clients, anticipate still unclear changes

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

HIGH RISK CLIENTS – IMPACT ON PORTFOLIO STRATEGIES

1 Multiple choice question, respondents could chose more than one applicable options

2 IFRS 9 ready participants (i.e., in the testing or completed phase) show results consistent with the others IFRS 9 responders, despite a reduction in “still under investigation” weight

16%

22%

27%

35%

IFRS 9

adopters

(N=37)

Key takeaways

▪ Almost 50% of the banks are still investigating treatment of higher-risk client under new regulation

▪ Early trend indicates scrutinized/ reduced lending and price increase for high-risk clients

RESULTS AS OF JULY 2017

Do you expect different treatment of higher-risk clients in your firm’s lending decisions?1

No

Yes

Can’t say,

topic under

investigation

Largely yes,

but still under

investigation

8%

8%

5%

11%

IFRS 9 adopters2

(N=37)

Scrutinize lending to

performing but high

risk clients/segments

Reduce lending to

higher-risk

clients/segment

Reduce credit limit

headroom for higher-

risk clients/segment

Increase collateral

requirements for

highe-risk clients

Increase pricing for

higher-risk

clients/segment

3%

24IACPM – McKinsey & CompanySOURCE: IACPM/McKinsey survey on “New Accounting Standards for Credit Loss Allowances (IFRS 9/CECL)”

5%

32%30%

32%

Do you perceive there will be differential effects across firms?

DIFFERENTIATED PROFIT MARGINS – IMPLICATIONS ON COMMERCIAL STRATEGIES

Banks expect differentiated effects on profit margins

across firms as a consequence of IFRS 9 adoption

IFRS 9 adopters (N=37)

RESULTS AS OF JULY 2017

Largely yes, but

I still don’t have

any evidence

Yes, I expect

clear winners

and losersTopic still

under

investigation

No significant

impact

expected

Arbitrage opportunities might

arise across jurisdictions,

even though regulatory floors

will reduce differential effects

within a country

There may be a period where

US banks will have advantage

until CECL is adopted

IFRS 9 adopters will have

advantage as they don’t need

to provision for for Stage 1

25IACPM – McKinsey & Company

IFRS 9 adopters anticipate changes in commercial

policies or product design

57

43

Yes No

38%

Topic still under

investigation

14%

Overall volatility of

provisioning costs38%

Treatment of

guarantees

0%

Treatment of high

risk exposures

32%Treatment of longer

term exposures

Do you expect effects

on commercial policies

or product design?

What would be the main aspects of the

new ECL standards that lead to effects

on commercial policy decisions?1

METHODOLOGY FOR PRICING – IMPLICATIONS ON COMMERCIAL STRATEGIES

SOURCE: IACPM/McKinsey survey on “New Accounting Standards for Credit Loss Allowances (IFRS 9/CECL)”

1 Multiple choice question, respondents could chose more than one applicable options

IFRS 9 adopters

(N=37)

Key takeaways

▪ 43% of IFRS9 adopters anticipate changes in commercial policies and product design

▪ For IFRS9 adopters, the key factors that can effect commercial policy decisions are thetreatment of high exposure loans and overall volatility of provisioning costs as the underperforming (stage 2) assets are subject to provision

RESULTS AS OF JULY 2017

IFRS 9 adopters

(N=37)

26IACPM – McKinsey & CompanySOURCE: IACPM/McKinsey survey on “New Accounting Standards for Credit Loss Allowances (IFRS 9/CECL)”

Banks anticipate update in the risk appetite framework as

one of the key changes as a result of new standards

1 Multiple choice question, respondents could chose more than one applicable options

CREDIT RISK APPETITE– MODIFICATION IN CREDIT RISK MANAGEMENT PRACTICE

24%Expect updates in risk appetite

framework; specifics not determined

Introduction of new risk metrics,

triggers and limits14%

Changes in risk guidelines

Changes in existing risk limits

5%

Changes in risk taxonomy

3%

5%

46%Expect changes to credit

risk appetite 32% 22%

No changes

Topic under investigation

Changes expected

IFRS 9 adopters

(N=37)

Do you expect your firm’s credit risk appetite to change as a result of the new standards?1

RESULTS AS OF JULY 2017

Key takeaways

▪ More than 20% of the banks are still investigatingchanges in risk appetite framework

▪ Early trend indicates introduction of new risk metrics and changes in risk taxonomy as key changes in the current risk appetite framework

27IACPM – McKinsey & Company

~50% of IFRS 9 adopters anticipate changes in early

warning mechanism

SOURCE: IACPM/McKinsey survey on “New Accounting Standards for Credit Loss Allowances (IFRS 9/CECL)”

EARLY WARNING SYSTEMS – MODIFICATION OF CREDIT RISK MANAGEMENT PRACTICES

1 Multiple choice question, respondents could chose more than one applicable options

Enhancement in

early warning mechanisms 43% 8%49%

Changes expected

Can’t say, topic

under investigation

No change

Key takeaways

▪ Banks are likely to strengthen their early warning mechanisms

▪ Expected changes (e.g., introduction of forward-looking indicators, adjustments to thresholds) are mostly focused around monitoring longer maturities or, higher risk assets

IFRS 9 Adopters

(N=37)

Do you expect your firm to enhance early warning mechanisms to detect deterioration of clients' lifetime credit risks?1

8%

32%

Adjustment to classification

criteria for watch lists27%

8%

Adjustment of thresholds

for early warning signals32%

Increased monitoring staff

Largely yes, but still

don’t have evidence

Introduction of forward-

looking risk indicators

RESULTS AS OF JULY 2017

28IACPM – McKinsey & Company

About 43% of the banks adopting IFRS 9 anticipate

increased capital requirement whilst about ~70% plan to

embed ECL into stress testing

SOURCE: IACPM/McKinsey survey on “New Accounting Standards for Credit Loss Allowances (IFRS 9/CECL)”

STRESS TESTING – REGULATORY RESPONSE

Do you expect the new standards will

drive increased capital requirements

through the stress testing process?

RESULTS AS OF JULY 2017

32%24%

38%

5%

Yes, I expect a

significant impact

Topic still under

investigation

Largely yes, but I do not

have specific evidence

No significant

increased capital

requirements expected

IFRS 9 Adopters (N=37)

14%

16%43%

14%

14%

Topic under

investigation

No changes in stress

testing provisions

methodology

expected until after

adoption of the new

standards

Yes, I already model

ECL provisions in my

stress test projections

Yes, but I expect to

be able to delay this

For at least a year

Yes, I expect to need to

model the effects of ECL

provisions in my next

regulatory stress test

27%

38%

8

IFRS 9 Adopters (N=37)

Do you expect your firm will start

embedding ECL into stress testing?

29IACPM – McKinsey & Company

Modelling (3/4): Data quality is the most relevant issue

identified by survey's participants

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

Total respondents #1

IFRS 9 respondents

(N=37)#2

Of which in the “testing”

and “completed” phases

(N=16)#2

Data quality ranking out of 11 possible issues1

1 Possible implementation challenges: 1) data quality, 2) data governance and controls, 3) model development and validation, 4) program resourcing, 5) system development, 6) target state

operating model with clearly defined roles and responsibilities among different stakeholder 7) reserving process reorganization 8) timeline 9) uncertainty in requirements and accounting

related regulatory guidance 10) securing early participation of all key stakeholder

In which design and implementation areas is your firm expecting to face the biggest challenges? ▪ Data quality is the

most relevant issue identified by survey's participants for new standards’ implementations

▪ IFRS 9 adopters have identified data quality as the second relevant issue after system development

▪ However, the two topics are strictly correlated, being data availability and quality a relevant driver for system development

RESULTS AS OF JULY 2017

SLIGHTLY

BEHIND

SCHEDULE

ADAPTING

EXISTING

MODELS

WORRIED

ABOUT DATA

QUALITY…

… BUT WITH A

PLAN IN MIND

For IFRS 9

adopters, the

first issue is

system

development

Key takeaways

30IACPM – McKinsey & Company

Key takeaways

Identified 4 key takeaways on modelling components (4/4)

SOURCE: IACPM/McKinsey survey on “The evolving role of Credit Portfolio Management within the enterprise”

3%

8%

11%

43%

32% 3%65%

Topic under investigationYesNo

IFRS 9 adopters (N=37)

Do you expect limitations in internal data to cause implementation challenges?

▪ More than 60% of the banks anticipate limitations in internal data to cause implementation challenges, however they have already identified potential remediation strategies

▪ IFRS 9 adopters are more focused on implementing remediation actions on data based on in internal sources