I IMPLEMENTING AN AUTOMATED CASHIERING SYSTEM IN THE MUNICIPAL COURTS IN LOS ANGELES COUNTY: A CASE STUDY ____ Presented to: THE INSTITUTE FOR COURT MANAGEMENT OF THE NATIONAL CENTER FOR STATE COURTS to satisfy requirements of the COURT EXECUTIVE DEVELOPMENT PROGRAM Robert J. Steiner Court Administrator Plalibu Municipal Court June 1985 ,

Transcript

I

IMPLEMENTING AN AUTOMATED CASHIERING SYSTEM IN THE MUNICIPAL COURTS IN

LOS ANGELES COUNTY: A CASE STUDY

____

Presented to:

THE INSTITUTE FOR COURT MANAGEMENT OF THE NATIONAL CENTER FOR STATE COURTS

to satisfy requirements of t h e

COURT EXECUTIVE DEVELOPMENT PROGRAM

Robert J. Steiner Court Administrator

Plalibu Municipal Court

June 1985

,

I

- 1 -

"Traffic ,Ticket 'Fix' In Clerk's Office Probed by County" -_- Los Angeles Daily Journal - 7-16-82

"2 L.B. court clerks charged with accepting bribes to fix tickets" --- Independent-Press Telegram - 9-27-03

"Probe of Court Computer System Ordered in Bribe Case" -..- Los Angeles Times - 10-12-83

"The Auditor-Controller and Director of Data Processing (are ordered) t o '

review the system controls over the automated traffic citation controls system, make any needed changes, and report back t o the Board in 30 days"

--- 'Board Order' from Los Angeles County Board of Supervisors

"Modular construction insuring that your MICROS Cash Management System will fit your needs today and it will grow w i t h your business tomorrow, You can even link MICROS to a central computer."

-&I Sales brochure from cash register manufacturer

THE PROBLEM:

Could an automated cashiering system help the Municipal

Courts in Los Angeles County solve cash handling problems

that had caused negative publicity? What are the security

concerns of such a system? Are there any potential for

savings from such a system? What difficulties might be

involved in planning and implementing such a system? What

can be learned from the implementation? This project is

an attempt t o provide the answers t o these questions and

to provide some suggestions f o r future projects of this

- 2 -

type. The project is in actuality a case study of the

implementation of an automated cashiering system for the

municipal' courts in Los Angeles County. The methodology

of the case study involved:

o Introduction and background to the project and

o

o A case tracking study of 100 cases where fines

o Analysis of problems encountered with

the courts in Los Angeles County. Documentation of the current system of handling records and payments.

were paid, to document the need for the system..

implementing other major automated systems in

- -

' the courts in the county. Post-Implementation audit of the Expanded Traffic Records System. Interview with principal manager involved in implementing the Municipal Court ,

Information System. o Review and recreation of the steps taken in the

implementation of an automated cashiering system in the county.

o Findings and conclusions.

THE SCOPE:

In'order to better understand the issues and complexity of

implementing any major system in Los Angeles County it is

first necessary to have some background on the California

court system; Los Angeles County; the various Municipal

Court District in Los Angeles County and how they relate

to one another. It is a l s o important to understand the

complexity of the revenue distribution requirements and

h o w they are currently handled.

MUNICIPAL COURTS IN CALIFORNIA:

The Municipal Courts in California are courts of limited

jurisdiction. Briefly they have exclusive jurisdiction

- 3 -

over all misdemeanor violations (maximum of one year in

county j a i l and/or $1,000.00 f i n e ) and al'l traffic

infractions (maximum $100.00 fine), except for juvenile

violations, that occur within the geographic boundaries of

the district. They also conduct Preliminary Hearings' for

felony matters to determine i f probable cause exists f o r a

person to stand trial in the Superior Court (the general

jurisdiction court in California). Municipal Courts also

exercise jurisdiction over civil lawsuits in which the

amount in controversy does not exceed $15,000.00.~and Small

Claims Court which involve cases of $1,500.00 o y , l e s s .

SEE FIGURE I.

The Constitution of the State of California requires that

the S t a t e Legislature prescribe for the Municipal Courts,

and they have done so in prescribing jurisdiction; the

number of judges and staff; and the salaries and benefits

of the judges and staff. The legislature has a l so

prescribed that the local counties shall pay f o r the

expenses of the courts within each county . The Municipal

Courts are therefore a step-child of the State and often a

thorn in the side of the local Board of Supervisor's which

a c t as a combined legislative and executive branch to

administer county government.

The Courts of California are administered by the Judicial

Council (chaired by t h e Chief J u s t i c e of t h e S t a t e Supreme

I I '

COURTS OF APPEAL

5 D i s t r i c t s

- 4 -

P THIRD

DISTRICT sacrmento 7 Justices

*

, ,-

1 ,

FIFTH FOURTH DISTRICT DISTRICT

SUI Diego rresllo san Fkrnardino a J U S ~ ~ C ~ S

14 Justices J

FIGURE I

C A L I F O R N I A C O U R T S T R U C T U R E

I FIRST

DISTRICT san prancisco 16 Justices

SECOND D I S T R I C T L13s Angeles 28 Justices

1 Chief Justice 6 kmcia te Juti.ces

SUPERIOR COURTS

8 in the state ( m e for ead wunty) w i t h over 654 ydgc

JLmsnlcT10N Civil-

Criminal- mer s15,ooo

Felonies

Go to D i s t r i c t Caurt of ~QEZLI a m i c a b l e to the district

Appeals-

TRIAL COURTS G=l MUNICIPAL COURTS

85 in the state w i t h over 510 judges

~ S D I C T I C B O C i v i l -

smdll Claims-

criminal-

Over $15,000 or lw

$1,500 or less

Preliminary Hearings Mkdemanors and Infractions

-Sumnor cuurt ma-

JUSTICE COURTS

09 in the state

JURZSDICTION

S15,oOO or less

S l , 5 0 0 or less

Preliminary Hearings M i S d € C E S l O r S

Jrd Infraction

SuDerior Court

C i v i l -

SmU Claims-

criminal-

AppedLs-

' .- - 5 -

Court) and its staff known as the Administrative Office of

I-

-

the Courts (the A.O.C.). The Administrative Director of

the Courts organizes and directs the A.O.C.. The

authority of the Judicial Council and the A.O.C. over the

Municipal Courts is largely in area of rule making. 'They

also provide some technical and statistical assistance t o

the courts if they are asked. Neither the Judicial

Council or the A.O.C. take any active part in the

administration of any of the trial courts in the state.

Judges of the Municipal Courts are elected by the ,voters

of the district for six-year texms, any vacancies in a

judicial office awe filled by the Governor to fulfill the

unexpired terms. They must have been admitted to the

California Bar for at least five years before election o r

appointment to office. Many districts a l s o employ Court

Commissioners to perform many subordinate judicial duties.

These Commissioners must have the same qualifications the

law requires o f a judge and can perform most of the

functions of a judge. Commissioners are appointed by and

serve at t h e pleasure of the the judge or judges of the

district .

Each Municipal Court has a Clerk of Court who in most

cases also acts as the Court Administrator. The Clerk or

Court Administrator is appointed by the judge or judges of

the district. The duties of the Clerk/Court Administrator

-6-

,-

axe varied, they include: Financial administration of the

training and discipline of all non-judicial personnel

employed by the court. Administration of requirements

concerning the ,court records, information systems and

statistical compilations and controls. Management and

acquisition of court facilities and equipment. Assisting

the presiding judge with the court's calendar management.

And maintaining liaison with public and private 'agencies .

. 4 ,

.. and persons concerned with the court.

MUNICIPAL COURTS IN LOS ANGELES COUNTY:

The County of Los Angeles is a county of 7,781,109 people

and covers an area of 4,083.21 square miles. There are 84

incorporated cities in the county and some vast areas of

unincorporated land. Out of these cities 83 are served by

the municipal court districts in Los Angeles County.

There are twenty-four municipal court districts in the

coun ty , holding court sessions in thirty-six different

buildings throughout the county. See Figure 11. Each

district is an independent and autonomous district, with

i t s o m judges and staffs. The courts range in size from

small courts in the outlying areas w i t h one or two judges

to a large urban court (the Los Angeles Municipal Court

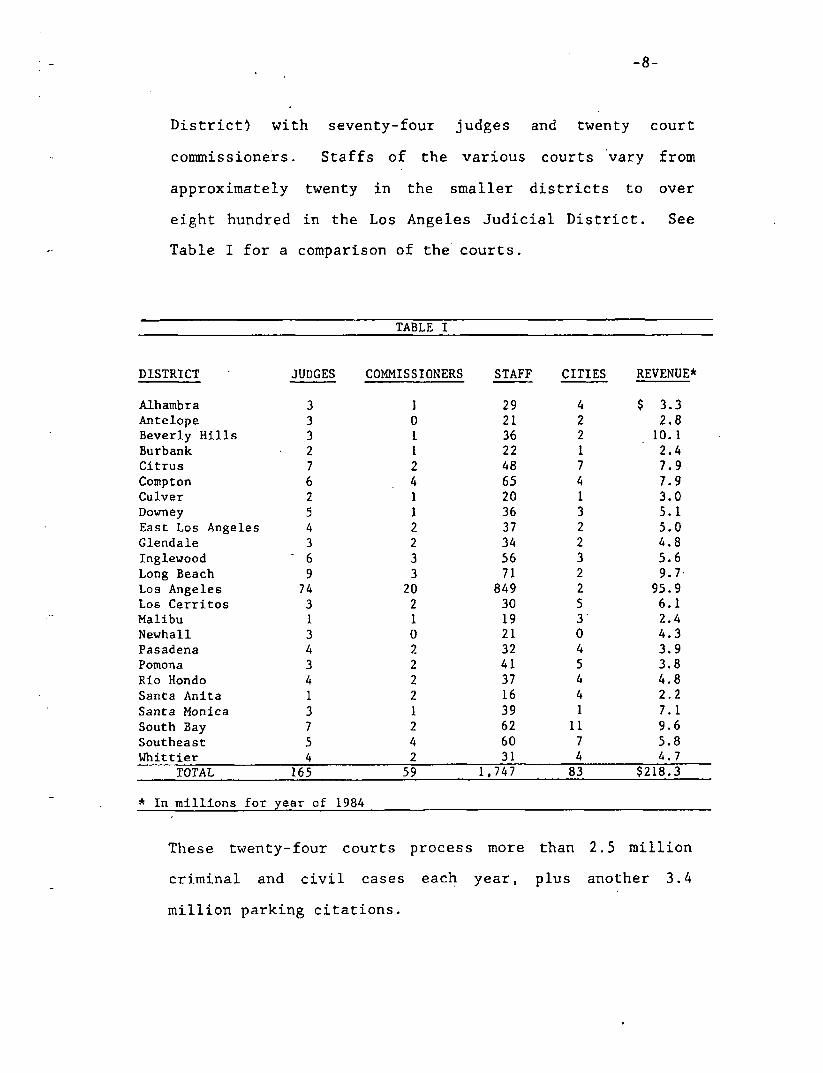

-8-

D i s t r i c t . ) w i th seventy-four judges and twenty court

commissioners. Staffs of the var ious courts 'vary from

approximately twenty in the smaller districts to over

eight hundred in the Los Angeles Judicial District. See

Table I f o r a comparison of the' courts.

TABLE I

DISTRICT .

Alhambra Antelope Beverly H i l l s Burbank Citrus Comp t on Culver Downey East Los Angeles Glendale Inglewood Long Beach Lo3 Angeles Lo6 Cerritos Malibu Newhall Pasadena Pomona R i o Hondo Santa Anita Santa Monica South Bay South east

These twenty-four courts process more than 2.5 million

criminal and civil cases each year, plus another 3 . 4

million parking citations.

- 9 -

The combined annual budgets of the municipal courts in the

county is $86,250,632. The courts .collect revenue for

city, county and state government that was approximately

$218,300,000 in the year of 1984. Collection o f this

amount of revenue is an ever increasing problem. Revenue

is distributed to more than 270 different funds and

receipting for and accounting for this revenue i s a time

consuming, l a b o r intensive effort. Since the passage 'of

Proposition 13 (a property tax limitation initiative) by

the voters of California in 1978, local and state

officials have realized that the courts provide a ,source

for additional revenue that does not require voter

approval. In the ensuing years the legislature has added

various "assessments", "surcharges" and other types of

"user fees". -

Each and every fine o r forfeiture collected by the courts

must be allocated to some fund. Which fund the money goes

to is determined by a number of factors such as type of

violation (e.&. Vehicle Code, Penal Code, local

ordinance) ; location of violation (which city or

unincorporated area); and arresting agency (local Police,

State Highway Patrol, County Sheriff, - etc.). Depending on

the type of violation additional charges may be added to

the base fine to be deposited into other funds. These

a d d i t i o n a l charges, usually referred to as penalty

assessments or surcharges are specifically earmarked f o r

I . . ... I

I

- 7 -

I

,- -10-

s p e c i a l 'programs. See Table IT for an example of a

p o s s i b l e revenue distribution. . . -

TABLE I1 Sample of revenue d i s t r i b u t i o n f o r minimum f i n e

f o r a d r i v i n g under t h e i n f l u e n c e charge.

Sample A: Arrest made i n t h e C i t y of P o l i c e Department.

BASIC FINE TO: R e s t i t u t i o n Fund

Lab Se rv ices Fund Alcohol Program Fund

County General Fund ' C i t y T r a f f i c S a f e t y Fund

ASSESSMENTS TO :

TOTAL

Sample B:

BAS IC TO :

Long Beach by the l o c a l

$390.00 $ 20.00

50.00 50.00

232.20 37.80

$2 74.00 Night Court 1.00 Courthouse C o n s t r u c t i o n Fund 39.00 Cr imina l J u s t i c e C o n s t r u c t i o n Fund 39.00 To S t a t e of C a l i f o r n i a 195.00 DUE $664.00

Arrest made i n t h e C i t y of Long Beach by t h e C a l i f o r n i a Highway P a t r o l . FINE $390.00 R e s t i t u t i o n Fund $ 20.00 Lab Se rv ices Fund 50.00 Alcohol Program Fund 50.00 C i t y T r a f f i c S a f e t y Fund 135.00 Countv Road Fund 135.00

ASSESSMENTS $274.00 TO :

TOTAL

Sample C:

BAS I C TO :

Night Court 1.00 Courthouse C o n s t r u c t i o n Fund 39.00 Criminal Jus t i ce C o n s t r u c t i o n Fund 39.00 To S t a t e of C a l i f o r n i a 195.00 DUE $664.00

Arrest made in an un incorpora t ed a r e a by the County S h e r i f f . FINE $390.00 R e s t i t u t i o n Fund $ 20.00 Lab S e r v i c e s Fund 50.00 Alcohol Program Fund 50.00 County Road Fund 270.00

AS s ES SMENT S- $274.00 TO: Night Court 1.00

Courthouse C o n s t r u c t i o n Fund 39.00 Cr imina l J u s t i c e Cons t ruc t ion Fund 39.00 To S t a t e of C a l i f o r n i a 195.00

TOTAL DUE $664.00

- 11 -

The amount of money that must be distributed to each city

differs from city to city, In Sample A the City of Long

Beach is'entitled to 86% and the County the remaining 1 4 % .

In order to make the accounting simpler for the clerk

collecting the fine the amounts f o r the Lab Services Fund;

Alcohol Program Fund; and the City and County shares are

collected together in one lump some. The accounting

division makes the proper adjustments at the end of each

month; The amounts collected for the Courthouse

Construction Fund; Criminal Justice Construction Fund and

the amount that goes to the State are handled in the same .

manner. The amount that each city is entitled to is

primarily set out in section 1463 of the State Penal Code.

SEE APPENDIX A . This section applies to the majority of

all revenue distributions including Vehicle Code, Penal

Code, and local ordinances.

There are various other miscellaneous codes and ordinances

that have their own unique distributions. These

exceptions" represent some of the more complicated

distributions and are areas where more mistakes are made

by cashiers. More mistakes occur simply because some of

these distributions occur so rarely that most cashiers may

11

not even be aware of them. Some of the more interesting

of these create special distributions for violations

involving the Prophylactics Law; Outdoor Advertising A c t ;

Rabies Control; Littering; Fish & Game Code; and Off-Road

- 1 2 -

Vehicles', just t o 'name a few. These sections and others

are set o u t in the State Controller's .Manual of 'Accounting

f o r Municipal and Justice Courts. SEE APPENDIX B.

The defendant may a l s o be required to reimburse the County

for additional fees such as: Appointed Counsel; C o s t s of

Incarceration; or Costs of Probation. These additional

fees compound the revenue distribution problem,

When a defendant does nor pay the entire fine in one . '

payment most judges allow the f i n e to be paid in

installments, in amounts the defendant can afford; Each

fund is credited on a priority basis established by the

State Controller. Payments are credited t o each fund

until the amount in that fund is equal to the amount due

that fund, additional payments then go to the next fund in

the priority. See Table 111.

-

I

- 13 .-

I-

. .

. .

TABLE I11 .Priority of revenue distribution, .using information from Table I, Sample A, and assuming a monthly

R e s t i t u t i o n Fund Night Court S t a t e of C a l i f o r n i a C i t y T r a f f i c Sa fe ty Lab S e r v i c e s Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c Sa fe ty Lab S e r v i c e s Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c S a f e t y Lab S e r v i c e s Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c S a f e t y Lab S e r v i c e s Fund

Fund

Fund

Fund

Fund - - Alcohol Program Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c S a f e t y Fund Alcohol Program Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c S a f e t y Fund Alcohol Program Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c S a f e t y Fund Alcohol Program Fund Courthouse Cons t ruc t ion Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c S a f e t y Fund Courthouse Cons t ruc t ion Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c Sa fe ty Fund Courthouse Cons t ruc t ion Fund Cr imina l J u s t i c e Cons t ruc t ion Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c S a f e t y Fund Cr imina l J u s t i c e Cons t ruc t ion Fund S t a t e of C a l i f o r n i a Ci ty T r a f f i c S a f e t y Fund Cr imina l J u s t i c e Cons t ruc t ion Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c S a f e t y Fund Cr imina l J u s t i c e Cons t ruc t ion Fund County Genera l Fund S t a t e of C a l i f o r n i a C i ty T r a f f i c S a f e t y Fund County Genera l Fund S t a t e of C a l i f o r n i a C i t y T r a f f i c Sa fe ty Fund County General Fund

- 15 -

_...

This legislative change is typical of the number of

changes that take place each year. The j o b of educating

employees t o keep abreast of these changes is a continual

cycle. Often the rules change every year and sometimes

even during the middle of the year. Two examples of these

changes have been the changes in the Assessment Fund and

' the Alcohol Program Fund.

The Assessment Fund (originally called Penalty

Assessments) is a state mandated fund that goes to pay for

various things, such as: Driver training in the public .

schools; peace officer and correction officer training;

victim and witness reimbursement; and construction of

courthouses and criminal justice facilities. Penalty

Assessments originated in 1935 and originally provided for

an additional assessment o f $1.00 for each fine of $20.00

or fraction thereof. In 1962 the amount was increased to

$ 2 . 0 0 , it was increased again in 1 9 6 7 to $3.00 then to

$ 4 . 0 0 in 1969 and then to $5.00 in 1974. In 1 9 8 0 the

sections dealing with Penalty Assessments was rewritten

and completely reorganized. As a result effective January

1, 1 9 8 1 the Assessment Fund was created and the amount of

the assessment was $3.00 for each fine of $10.00 or

fraction thereof. On June 28 , 1 9 8 1 as a result of urgency

legislation the amount became $4.00 for each $10.00.

Effective January 1, 1982 two additional increments of

$ 1 . 0 0 were added to fund Courthouse Construction and

- 16 -

,- I

C r i m i n a l Justice Facilities. A s a result the practical

effect meant that the assessment was now $6.00. On

January € , .1984 the essential assessment became $7.00 for

each $10.00 of fine. All of these changes causes problems

for training and supervision of personnel. It is

especially difficult to train people to remember all the

operative dates of the changes when they are handling o l d

cases. Many times fines and assessments are collected on

cases that are years old and the clerks must know what are

the proper amount of assessments to collect.

The second example is that of the Alcohol Program Fund.

This is a $50.00 assessment for all violations of driving

under the influence. The funds go t o finance programs the

county has to aid those with alcohol problems. The

difficulty with this fund has been the changes in the

manner it is collected. The original law effective in

1981 provided that the $50.00 was b a s e d on the CONVICTION

of the charge. This meant that a record of all

convictions is kept then at the end of each month, $50.00

for each of these convictions would be deducted from each

cities share of fines. This occurred in all cases even in

those where the defendant never paid a fine. In 1984 the

method was changed to be only in those cases where a fine

w a s collected. Effective January 1985 the method was

changed back to t h e original method. This has caused much

confusion among cashiers in which cases to collect the

,- - 17 -

I 0 I -

.-

fund and which cases the money i s accounted f o r on a

monthly bas i s .

The above formulas and problems are admittedly complex and

difficult t o understand, but have been included for a

better understanding of the issues involved in . this

project.

CURRENT ACCOUNTING METHODS:

The courts currently handle this revenue by basically

manual methods. All of the courts own electronic cash

registers, but in terms of their usage their application

is simply for control purposes and receipt issuance. The

only real memory these machines have is the ability to

accumulate totals. The rest of the accounting functions

are done entirely by manual methods. The cashier

collecting a payment must examine each file and make an

intelligent and informed decision about how the revenue

should be distributed. Some of the things to be

considered are: where was the arrest made; what agency

made the arrest; what ordinance or code was v i o l a t e d ; have

any other payments previously been made and if so how were

they distributed. This situation often leads t o errors,

either due to the ability of the individual cashier; lack

o f attention; inadequate training; or other "people"

related problems. At the end of each day totals are taken

from the cash register and transferred by the accounting

- 18 -

section'to various spreadsheets and ledgers. If errors in

distributions are discovered notice are forwarded to

accounting f o r the proper adjustments to be made. As

adjustments are made to the various funds during the

month, they are credited or debited to these spreadsheets

and ledgers, A t the end of each month the bookkeeper then

totals each of the revenue categories ( p l u s or minus and

adjustments) f o r final distribution to each jurisdiction.

Each of these manual procedures invite a variety of

possible errors.

A sample of misdemeanor cases in the Malibu Municipal

Court resulted in the following findings. Out: of one

hundred cases sampled there were a total of twenty-four

errors involving the initial revenue distribution. SEE

TABLE V. Of these twenty-four errors thirteen in some way

involved the Alcohol Program Fund, either in collecting o r

failing t o collect it for appropriate cases. In two cases

the priority of distribution was incorrect. The other

nine cases involved incorrect distributions t o various

other funds with no particular pattern. The cases were

sampled by taking random groups of docket sheets

representing cases where fines were collected over a

period of months. Within each group of dockets every

fifth case was examined to determine if there were any

errors. The types of cases involved in this sample were

misdemeanor cases, admittedly the most complex. T r a f f i c

. - -

r . - 19 -

..

or parking citations would be less complicated with fewer

errors likely. But i f this pattern of errors was likely

to occur countywide the potential impact on the various

revenue accounts could be very sizeable. With over

$200,000,000 in collections even a five percent error

factor involves over $10,000,000.

TABLE V Errors in revenue distributions a t Malibu Municipal Court

0 . . TOTAL CASES 100

Cases w i t h zero errors 76 Cases w i t h one error per case 23 Cases w i t h two errors per case 1 * . . . * . . .

CURRENT AUTOMATION IN THE COUNTY:

The courts in the county currently have a fully automated

system for processing its traffic records. This system,

the "Expanded Traffic Records System" (ETRS) is an

online" countywide data base which currently. holds more

than 3,000,000 records and has a monthly transaction

volume of 1,100,000. The system provides for full case

tracking and disposition of all records. In addition ETRS

calculates bail for each violation according to a built in

bail schedule, The Los Angeles County Auditor-Controllers

Office recently completed an audit of ETRS. In their

I I

audit they made some forty-three recommendations t o "clean

up'' or improve the system. The major findings were:

o Cont ro l over access to the ETRS security function is not adequate.

. . . .

I '- - 20 -

o User ID and password security can be improved.

o -Computer assisted audit trails for ETRS transactions should be enhanced.

0 Procedures for t h e use of system output reports

0 System edits improperly allow numerous types on

. are not adequate.

invalid transactions t o be accepted.

o System interfaces w i t h Automated Want/Warrant System and the State Department of Motor Vehicles can be improved.

System and program documentation is not in compliance with Data Processing Departnient standards.

0

I n the opinion of the Auditor ETRS was.performing its .

designed objectives but it still had some serious problems

or at least the potential for problems. ETRS was f i r s t

implemented in t he Spring of 1981 and the audit was

completed in 1984 a full three years after its

implementation. SEE APPENDIX D. Many of the

recommendations are planned to b e implemented with the

proposed automated accounting system.

Currently under development is another system, t h e

"Municipal Court Information System" (MCI) which will be

an "online" case tracking and docketing system, f o r all

misdemeanor and felony cases. MCI is currently being

tested in five " p i l o t " courts and should be expanded to

the rest of the county before t h e end of this year.

.. - . . __ . . ..

- 21 -

..

When a payment f o r a ba 1 o r f i n e i s taken on a case i n

ETRS o r t h o s e t h a t w i l l be i n M C I , t h e c l e r k must f i r s t

access t h e ‘p rope r d a t a base t o determine t h e amount due.

The c l e r k then r i n g s t h e proper amounts, d i s t r i b u t e d t o

t h e proper funds i n t h e cash r e g i s t e r . A t some l a t e r t i m e

another c l e r k must access t h e proper d a t a b a s e and update

t o f i l e . Because of t h e volume of cases t h i s updat ing i s

o f t e n done l a t e o r i n c o r r e c t l y o r maybe even no t at a l l .

If any of t h e s e s i t u a t i o n s occur , an a r r e s t warran t may be

i s sued i n e r r o r . These could l e a d t o f a l s e a r r e s t s and

p o s s i b l e l i t i g a t i o n a g a i n s t t h e c o u r t and the county.

SECURITY PROBLEMS:

During t h e past few yea r s many of t h e c o u r t s i n t h e county

have had a problem w i t h t h e f t of funds by employees. The

c u r r e n t manual systems do l i t t l e t o d iscourage t h e f t and

make t h e p o s s i b i l i t y of d e t e c t i o n remote. F o r t u n a t e l y t h e

v a s t m a j o r i t y of c o u r t employees a r e honest and hard

working peop le , b u t t h e r e are always “en t r ep reneur s” who

w i l l f i n d some angle t o make t h e system ‘‘work f o r them”.

Most people a r e only caught because they g o t c a r e l e s s o r

t o o greedy . During t h e p a s t two t o t h r e e yea r s t h e r e have

been documented cases of t h e f t i n seven of t h e twenty-four

municipal c o u r t s : ALhambra, C i t r u s , Compton, Long Beach,

Los Angeles, Pasadena and San ta Monica. The p o s s i b i l i t y of

the same type of t h i n g s going on i n t h e o t h e r c o u r t s i s

very h igh .

- 22 -

LOCAL AUTONOMY :

Since each court is independent, each one has its own

presiding judge and I t s own court administrator. While

all the courts attempt to work together on mutual problems

it is not always possible to obtain 100% cooperation from

a l l twenty-four districts, This is due in some cases to

stubbornness and resistance to change and in other cases

due to real problems that may be unique to one district

and not to the others. Given t h i s problem any countywide

policy or program must

needs of all the various

be flexible enough to meet the

courts in the county, *

. - * I

b

.

' . . .--... - .

-.

c

- 23 ..

"The IBM '4700 Finance Communication Syetem devices are small and modular providing flexibility to design workstations tailored to s u i t individual operator requirements and applications. Geared to the . continual expansion of the financial marketplace, Data Lfne has chosen to offer a system of IBM products designed to grow right alona with your operation." _-_ Sales brochure from computer sales company

"It appears after investigation, that the IBM, Financial Communication System (4700) can be adapted to service this Court's need for simple and controlled caeh handling. The 4700 can provide compatibility with the current county IBM system." -- 'Policy Paper' from the Loa Angeles

Municipal Court

FINDING THE SOLUTION:

Beginning with the obvious problems indicated above and

the mandates of the Board of Supervisors of Los Angeles

County, Court Administrators in the county began to

intensify their efforts t o improve the accounting systems

for the' municipal court districts in the county. What

most Court Administrators wanted was a cashiering system

that would communicate directly to ETRS and eventually t o

MCI. The system that was envisioned would determine the

amount of money due, determine how it .was to be

distributed, and update the file all within the same

transaction. The system would also provide detailed audit

reports for security as well as reports for the accounting

section to simplify the operation at that end.

c

- 24 -

c

0

A small'group of Court Administrators began a search for a

system to accomplish this task, This "quest" first began

with the vendors of the electronic cash registers who had

stated.that their machines could be used to interface with

the county's data base. It soon became apparent that .

these statements were typical salesman type statements and

the expertise and ability of these companies to live up to

their billing, was not as advertised. Since the county

systems are all run on I.B.M. equipment this seemed to be

the next logical place t o look for some technical

assistance as to what products they might offer that could

begin to solve the problems the courts were having wi.tb.

their cash handling. The I.B.M. salesmen from their

"Government" section were of little help, they knew of no

system that. could handle the types of cash handling

situations the courts faced. Through contacts with other

court districts in the state, it w a s discovered that two

courts in two neighboring counties (Riverside and San

Bernardino) did have an automated cashiering system. But

after thorough investigation it was decided that because

of the operating system that these counties maintained and

the volumes of records in Los Angeles these other systems

were not feasible for Los Angelea County.

- . .

. .

It was finally suggested that the courts investigate a

product that I.B.M. marketed to its banking customers. It

was thought that the I.B.M. 4700 Finance Communication

. . .

- 25 -

System supported by an L.B.M. software package known as

Advanced.Branch Controller System (ABCS) might meet the

requirements of the courts. SEE APPENDIX E. This system

had never been installed in a court environment or any

governmental agency as far as the sales people knew. A

demonstration was held for people from the courts and the

County Department of Data Processing. After the

demonstration it was decided that this system would indeed

meet the needs of the courts and that implementation of

the system should proceed as quickly as possibie. This

then W R S the birth of the Municipal Court Finance System .

(MCFS).

- 26 - I

I

;r\

..

c

"This projec t ' s scope w i l l encompass eventua l ly a l l revenue r e c e i p t *

p o i n t s wi th in the twenty-four Los Angeles County Municipal Court d i s t r i c t s . . , . ( i t ) wi.11 i n t e r f a c e wi th the Expanded Traffic Records System t o accomplish i n i t i a l l y t h e r e c e i p t of moving b a i l f o r f e i t u r e monies.... (It) w i l l eventua l ly expand t o inc lude co l l ec t ion of a l l f i n e s and fees.' ' -- 'Concept Paper' f o r Finance Communications

System - 129-84

"The Finance Communications System w i l l be ab le t o process eqme Bail-By-Mail, t r ansac t ions by February 29, 1984." - 'P ro jec t Control Document' f o r Finance

Canrmunicatlons System - 1-4-84

"Problems w i t h loading t h e IBM 4700 software are in the process of being resolved."

e- Minutes of t h e S teer ing Committee - 1,-30-86

"In July 1984 t he B a i l by Mail w i l l come up I n Loa Angelee Metro. The Cashier funct ion w i l l come up August 1st. The cur ren t plan is t o i n s t a l l prototype equipment i n Long Beach and Glendale on July 2 7 , 1984. They vi11 have t h e Los Angeles Metro t r a f f i c software t o experiment with a t t h a t time.'' -- Minutes of t h e Steer ing Committee - 2-22-84

"I, the re fo re , move t h a t t h e newly formed Ad Hoc Committee (on Municlpal Courts) atudy the need f o r t h e c e n t r a l i z a t i o n and computerization of the Municipal Courts' accounting system and r epor t back t o t h l a Board wi th in 90 days." --- Motion of Superviaor Pete Schabarum of the

Los Angeles County Board of Supervisors

Coukte t o Supervisor Schabarum'e Motion - 7-13-84

IMPLEMENTATION PLAN:

In order to implement the decision to proceed with the

project two committees were formed. The first committee

- 27 -

,...

was the- Municipal Court Finance System Ad-Hoc Steering

Comittee, this committee was initially made up of court

administrators and representatives from the Data

Processing Department (a representative from the County

Auditor-Controllers Office was later added). This

committee was charged with the overall evaluation,

planning and design of the system, The second committee

was the Project Team, this was a committee composed 'of

hands on practitioners who would assist the Data

Processing Department in the detail design of the system.

The initial meeting of the Ad-Hoc Steering Committee was

held on December 9, 1983 with this writer named the

committee chairman. At this time the decision was made to

approach the- problem with various phases. The phases

were :

0 PHASE I - A prototype system at the Los Angeles -a1 Court's Metro Traffic Divieion. This prototype to handle only Bail-By-Mail functions in the court's mail area.

0 PHASE 11 - Expansion of the prototype to the public cashier windows at L.A. Metro Traffic.

0 PHASE I11 - Implementation of full cashiering functions in the Glendale and Long Beach Municipal Courts on a pilot basis:

PHASE IV - Expansion of the full tested system to the other 21 courts.

0

Phase I was limited to Bail-By-Mail functions because

these were seen by all parties as the simplest and least

complicated of all functions. They could also be done in

4

. '.

- 28 -

an area-away from the public counter without the pressure

of meeting and handling the public while attempting to

learn a 'new system. The L.A. Metro Traffic court was

selected because of its volume of cases where almost any

and all possible case situations were likely to happen.

Metro Traffic was also selected because the Lo8 Angeles

Judicial District serves only two cities thus limiting the

number of revenue distributions needed, therefore

requiring less programing problems for the pilot court.

Phase I1 would take place in the same court with people .

already familiar with the system from Phase I, thus

increasing the likelihood for success.

Phase I11 as planned will involve expansion to two

"outlying" courts Glendale and Long Beach, it was f e l t

that expansion to these two varied courts with Court

Administrators that were DEDICATED to the project would

a l so help in the succe88 of the project.

At the first meeting the decision was also made to have

the Data Processing Department (DPD) handle all the

necessary programing responsibilities. Since DPD did not

have anyone technically familiar with the ABCS software a

consultant was hired to modify the software to our needs.

I

- 29 -

I

I .I

. .-.

.-

It was also agreed to hire a consulting firm to perform a

systems analysis for all twenty-four judicial districts,

for identification of Phase 11 requirements.

By the time of the second meeting of the Steering

Committee held on January 10, 1984 a preliminary Project

Control Document. and a Detail Work Plan had already been

prepared. Both documents were approved by the committee

with same minor modifications.

PROBLEMS BEGIN:

Since Phase I involved only Bafl-By-Mail which are the

simplest and least complicated transactions, this phase

w a s perceived as requiring relatively little effort. A

date of February 29, 1984 was established as the target

date to be able to process "at least one piece of

Bail-By-Mail". The major issues of concern at this point

were: 1) making the "link" between ABCS and the County's

operating system IMS and 2) a major concern about the

system being developed before the hardware could be

delivered. Many people were concerned that the system

would be "up and running" before I.B.M. could deliver the

equipment or the County Mechanical Department could

perform the work at each site to install the equipment.

Subsequent committee meetings were held on January 30 and

February 22, 1984. By the February 22 meeting the

r

...

I

..

- 30 -

complexity of the ABCS software was becoming evident. It

was not just a few minor modifications to a simple system.

DPD could not even complete the link between ABCS and ETRS

(it would take until September 1984 for the communication

link to be established). The implementation date for

Bail-By-Mail was now set for July 1, 1984 and Phase 11 was

"very tentatively" set for implementation on August 1,

1984.

By the March 21, 1984 Steering Committee meeting the DPD

Project Manager had received a promotion and moved ,on to

other areas and was replaced by another Project Manager.

The new manager suffered a serious illness requiring

hospitalization soon thereafter and missed more than a

month on the project. During this period the Project Team

continued to work very hard on the design of the system

and the plan for implementation.

DOCUMENTING REQUIREMENTS:

The requirements of Metro Traffic for Phase I were closely

identified by the staff of the Los Angeles Municipal

Court, the Project Team and the Steering Committee. These

requirements were reported in a System Design

Specification document. SEE APPENDIX F. The systems

requirements for the next phases were not as easy to

document. Information would have to be gathered and

verified from each court district. Much of this

- 31 -

verification could have been done by the committee or it'6

staff, but to insure the "absolute" reliability of the

information it was decided that each court district must

be-contacted.

The decision to personally Involve each court in the

project was also made on another basis. By personally

involving each court, they would feel some involvement and

commitment t o the project, thereby helping to ensure

success. A questionnaire was developed with the

assistance of a consultant to gather each court's input.

SEE APPENDIX G. The questionnaire was divided into the

following categories:

0 0 0

0 0 0

Description of Cashiering Functions Description of Flow of Cash through the Court Daily Reporting of: - Cashier Balancing - Bookkeeping - Revenue Distribution - Audit Reports - Management Control Reports Internal Control System Computational Requirements Fee Distribution Tables

In addition to the questionnaire, Interviews were

conducted at twelve of the courts. Five of these twelve

(Los Angelee, Long Beach, Glendale, Beverly Hills and

South Bay) were interviewed at each court site on a very

detailed basis . These interviews took at feast one day in

each location to complete, as the entire collection and

accounting function of each location was examined. The

interviews covered all the material in the questionnaire

- 32 -

' -. I

! - I I

.. i

plus specific details of each courts accounting and

revenue distribution were explored. The other seven

courts (Alhambra, Citrus, Compton, East Los Angeles,

Inglewood, Malibu and Newhall) all received on site

interviews that allowed for personal input and suggestions

by the various Court Administrators and staff. These

interviews were less indepth than the first interviews and

lasted approximately two hours each.

returned from twenty-two of the twenty-four courts.

Questionnaires weke

From the questionnaires and interviews a repor$ was *

prepared detailing the cashiering requirements for the

next phases. SEE APPENDIX H. The major systems

requirements identified were:

Input requirements - Security * Limiting access to the system to only * Insuring system protected from unauthorized * Providing for accountability of each

authorized employees

access from external forces

transaction to a specific employee on a specific terminal

ProcessinR requirements - Pertorxntng automatic revenue distributions based on tables for each district that could be- quickly and accurately changed to accommodate changes in legislation etc. Accumulating of revenue distributiozta for Month-to-date or Year-to date reports

-

Output requirements - Providing reports to all the various courts with the ability t o for some courts whic court-to-court.

rovide specific reports R may vary from

.

I

I I F I I

- 33 - I

.-

I

* .-

o * Cashiering system interface requirements Interfacing wlth ETRS and MCI -

This repdrt also included some specific recommendations,

the major recomnendations and conclusions of the report

were :

0 Revenue distribution - Programming ot revenue distribution tables should be done according to comon requirements, but consideration should be given to individual needs of local courts, Responsibility for maintaining and updating tables should be responsibility of DPD and courts responsible for insuring accuracy of tables.

.)

0 Implementation of the IBM 4 7 0 0 - Implementing the system in stages as outlined previously

0 System communication with the host computer - Linking of ABCS to the County's IMS d ata base is vital, with technical support the key Issue. Programmers within DPD should establish some expertise in ABCS to facilitate initial programming and maintenance

0 Data accumulation capability - Storing data for monthly, quarterly or yearly reports should be done on the host computer, then transferred to the 4 7 0 0 syetem when required

System acceptable subject to establishing a reliable communication "link" and the continued availability of technical support

o Acceptability of the IBM 4700 -

DATA PROCESSING SUPPORT:

All during this time period it became apparent that the

major "stumbling block" with the project was the

complexity of the ABCS software. Support for the software

seemed to be almost non-existent. The consultant hired on

.- - 34 -

a "time and material" basis t o do the required

t- modifications for Phase I was doing the progranbing on a

part-time' basis, This consultant also had a full time job

with B company providing ABCS software for financial

,- institutions. During the course of the Phase I

programing his company transferred him to North Carolina

so at this point hi6 "expertise" became almost advisory

only while he worked with DPD programmers over the

telephone. The lack of expertise in the 4 7 0 0 equipment

and the ABCS

the work of this part time consultant.

,-

software at DPD made the project dependant on .' i In order to, begin I C

to solve this problem, in May of 1984 a programer from

DPD was sent to New Jersey to attend an IBM training class

on the 4700. Again in August 1984 the same programmer

along with a fellow programer went to New Jersey to

! - .

,-

attend IBM training on ABCS. Despite this training the

ability of DPD to establish local expertise in ABCS was

not forthcoming. The ability of the DPD programmers to do

any sort of programming has been limited to small

slow-as-you-go" type programs. They have not yet

developed the technical knowledge to do any major

programming jobs , By October 1984 DPD conceded that they

would be unlikely t o develop enough expertise in ABCS to

4 8

do the programming for Phase I1 and suggested that we

continue contracting for 4700 program support.

!

- 35 -

c

c

.-

r

Once the' communication link between ABCS and fMS was

eetabliehed (September 1984) actual testing of the system

began. Two. different deliveries of equipment had been

made, one configuration was set up at the DPD computer

center in Downey. The equipment at DPD was used for

programming and development purposes. The second

configuration of equipment was set up at L.A. Metro

Traffic. Testing by court personnel could now 6e

conducted, during this testing several problems were

encountered. The first and most serious problem was that

of the printers used in the project. The printers are .

required to issue receipts, journal tapes and reports.

There are two basic printers available for the 4700

equipment, one printer is the model 4710, it fs a emall

limited use printer which can print a journal and endorse

up to four lines of print of forty-eight characters each.

The second printer I s the model 4720, this 5s a larger

multiple use printer which can print fu l l size documents

with an unlimited number of lines of print of up t o

ninety-nine characters each. The in i t ia l information

provided from IBM and the consultant indicated that the

4710 printer was not designed to produce reports. Since

the project invisioned getting multiple audit reports for

security and since many cases might require more than the

four print lines available, the decision was made to go

with the 4720 printer. During the Phase I system testing

- 36 -

. .

it was discovered that that the time required for the 4720

printer to produce a receipt was approximately 24 minutes.

This was totally unacceptable to everyone involved because

of a potential time saving system we were now presented

with a system that took more time than the present system.

The Steering Committee directed its staff to reevaluate

the printers. The staff made the following findings:

0 4720 Printers - More capable and flexible - Can print reports requirfng a full page width Inserting of documents very difficult -

- Requires-lengthly processing time

- Can produce reports (contrary to previous

- Easy to insert documents - Very fast (reduces time to issue receipts from minutes to seconds) - Uses less counter space - Could handle the majority of cases even with the four lines of print restriction

0 4710 Printers

information) - E86y to Use

With the new information the Steering Committee directed

that for future orders, 4710 printers would be placed at all public counter and all high volume areas. Each court

would also have at l eas t one 4720 printer to handle the

cases that had transactions that required more than four

lines of print and to handle some of the more

sophisticated reports that the 4710 might not be able to

handle.

Toward. the end of the year of 1984 the Steering Committee

became more and more frustrated over the slow progress of

.

- 37 -

I

I

the project due t o what they perceived as a lack of

commitment t o t h e pro jec t by DPD. The DPD projec t manager

assigned t o the -pro jec t was a l s o assigned t o numerous

other p ro jec t s f o r other county agencies. Through a

series of meetings with the Director of Data Processing

the MCFS pro jec t was given a high v i s i b i l i t y and high

p r i o r i t y s t a t u s . The pro jec t manager was re l ieved of a

majority of his other pro jec ts t o devote more time t o

MCFS ,

S i m i l a r d i f f i c u l t i e s have been experienced i n *other

municipal court da ta processing pro jec ts . One prime

example of t h i s is t he MCI p ro jec t , This p ro jec t f i r s t

began i n 1979 and has s t i l l not been f u l l y implemented

today. In an interview w i t h Mr. Dominic Polimeni, the

Court Administrator of the Alhambra Municipal Court and

Chairman of t he MCI Steering Committee, the following

i s sues were brought up i n r e l a t i o n t o the delay i n

implementation of M C I :

o The pro jec t was i n i t i a l l y being developed as a prototype and f a i l e d t o ge t recognition as a ma j o r sys tern soon enough The shortage of DPD programers meant t h a t most of t he programming had to be contracted out t o p r iva t e pa r t i e s . The cumbersome procedures required f o r contracting led t o delays i n h i r ing t h e cont rac t programmers Sa la r i e s ava i lab le f o r contract pro rammers were

months and because of the delay i n the contract process this of ten led t o gaps i n the contracts . In some cases t h e programer had found another job during t h i s gap.

o

o

o

0 Each contract could not be f o r more than s i x not high enough t o a t t r a c t “qual i ty 6 programmers

.

0

- 30 -

Through January 1985 four different contract programmers had worked on the project, each

familiar with the project. l e d to a "reinventing the wheel" situation

-requiring three or four months to become totally *

More than once this

Mr. Polimeni concedes that if he had it to do over again

he would have put more pressure for better support, on DPD

sooner and stronger. He also stated that he would have

reduced the scale of the project, by implementing it $n

smaller incremental phases.

In February 1985 DPD assigned one person with the overall

responsibility to implement the MCFS and MCI projects.

Each of the projects also had its own project manager

assigned to these projects as a full time assignment. The

development of both projects has benefited greatly from

this move and both projects have advanced faster than ever

before.

IMPLEMENTATION FINALLY?:

During this same time period another issue arose that led

t o a delay in the implementation of MCFS Phase 1. An

updated version of the ABCS software was released by IBK

that could take care of some of the minor problem8

discovered in testing. The decision was made to hold off

making changes until the newer software could be

implemented and modified, This new software was received

at the end of A p r i l 1985 and is now in place. All of the

systems are now in place and as of this date testing is

.

- 39 - going an at L.A. Metro Traffic, Actual changeover to

production for Phase I "Bail-By-Mail" is now scheduled f o r

July 1, '1985.

Programming support for development of Phases 11, IIX and

IV will be provided by a contract with IBM. The estimates

for implementation of the next Phases are:

Phase I1 - approximately six months after implementation of Phase I 0

Phase I11 - approximately ten months after implementation of Phase I1

,

Phase IV - approximately two months after implementation of Phase 111

The following is a table for quick reference showing the

major milestones of the project.

TABLE V I

DATE

1 2 4 1-83

12-09-83

01-04-84

1-10-84

01-30-84

02-09-84

EVENT DECISIONS/HIGHLIGHT

Planning Meeting Committees established

Responeibllitieo defined Implementation plan eetebliehed let Steering Committee Meeting

Initial Project Control Document prepared

Steering Committee Meeting Phase I implementation date set for 02-29-84

Steering Committee Meeting

Initial equipment ordered by DPD

DPD Project Hgr promoted 6 reassigned

I

.

02-22-84

03-21-84

03-27-84

April 84

04-1 2-84

04-1 8-84

05-0 7-84

05-08-84

05-17-84

05-21-84

06-13-84

06-20-84

07-09-84

07- 18-84

08-03-84

Steering Committee Meeting

Steering Committee Meeting

Design Review Document prepared

Project Manager hospitalized

Prospective consultants interviewed for Phase If epece.

Steering Committee Meeting

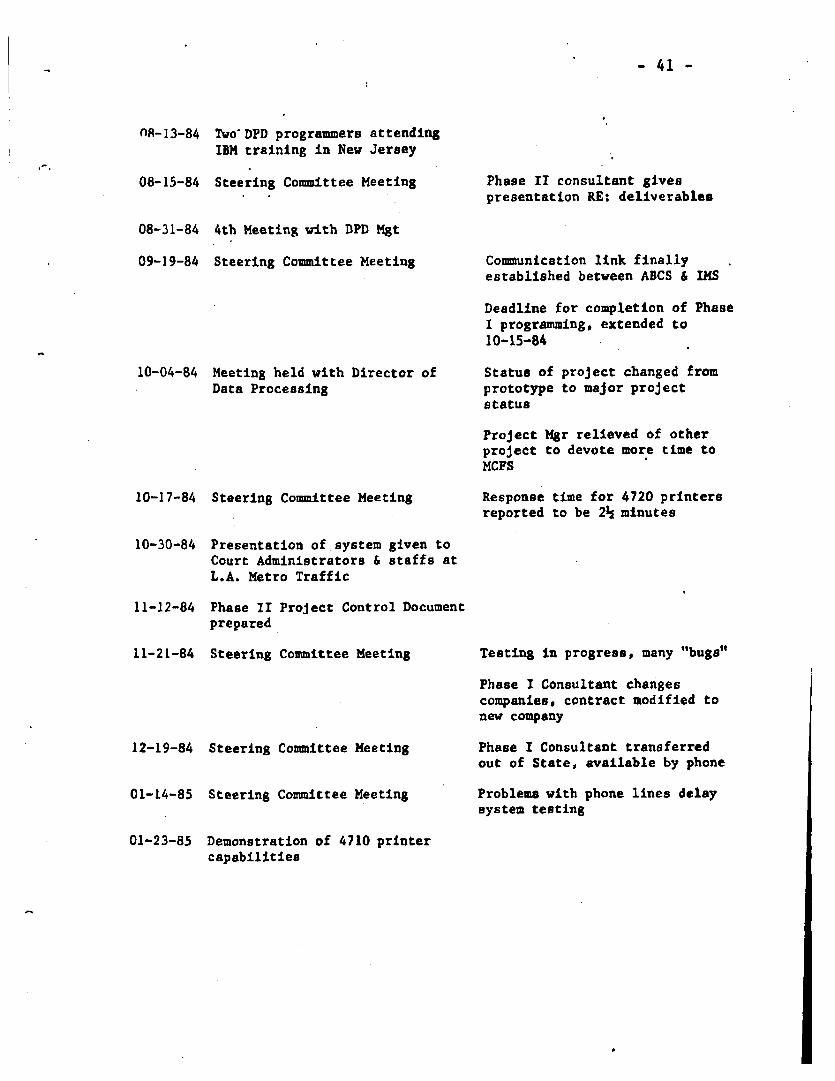

DPD programmer attendlng IBM 4700 training in New Jersey

Steering Committee Meeting

I - 40' - Phase I implementation dace now 07-01-84 6 Phase If 08-01-84

Plan discussed to have Phase 11 systems requirements done by an outside consultant New Project Mgr

Phase I date (07-01-84) still . OK, but may need more time for Phase 11

Papemork delay In equipment orders concerns C o d t t e c

Project Mgr back to work

Outside consultant eelected to do Phasa 11 specs.

Presentation of system given to Court Administrators & DPD staff at IBM seminar, San Joae, CA.

Phaee I System Deeign Specification Document prepared

Specfalmeeting with upper Mgt from DPD and Chair of Steering Committee to get more support

Communication link finally established between ABCS 6

Deadline for completion of Phase I programming, extended to 10-15-84

Statue of project changed from prototype to major project status

Project Mgr relieved of other project to devote more time to MCPS

Responee t h e for 4720 printers reported to be 24 minutes

Teeting In progress, many "bage"

Phase I Consultant changes companies, contract modified to new company

12-19-84 Steering Committee Meeting

01-14-85 Steering Committee Meeting

Phase X Consultant transferred out of State, 8vailable by phone

Problem with phone lines delay eystem testing

01-23-85 Demonstration of 4710 printer c apab il it ies

A

I

02-11-85 Steering Committee Meeting

02-26-85

03-08-85

03-11-84

04-08-85

04-1 9-85

05-01-85

05-20-85

- 42 -

DPD assigns an overall Manager to assure implementation of HCFS 6 MCI projects. DPD staff to meet weekly with Director of DPD to keep him personally apprised of projects progress

Decision made to change orders to 4710 printers

I . B . H . proposal for Phase I1 System Design presented

Agreement with I .B.M. for Phase I programming support

Steering Cornittee Meeting Testing suspended pending receipt of new version of sof ware

I.B.M. Phase If propose1 approved

Steering Committee Meeting

ABCS

Nev Phase I. Project Control P l a n prepared

Steering Committee Meeting New ABCS software installed

Steering Committee Meeting Phase I implementation date 07-01-85

In review the implementation of the project has been

delayed for many reasons, but at this point the project i s

on solid ground with what seems to be a very realistic

implementation schedule. The July 1 , 1985 implementation

date for Bail-By-Mail appears to be holding fast with even

a little optimism of improving the date "slightly". It is possible of course that the dates of the later phases may

"slip" somewhat, but unless something unforeseen happens,

a l l the courts should be online within eighteen months.

I

,

- 43 - D

I

,“nrganization~, which deal with the collective efforts of men, are - dtvoted t o the proceesing of information and the generation of - k.nwledge. Their a b i l i t y to test the envlronment so as to correct - cI’ror and reinforce truth makes them effective. Inability t o learn j s fatal. Yet learning is more d i f f i c u l t because 60 many men must do i t together.” -- from IMPLEMENTATION by Jeffrey Preeeman and

Aaron Wildavsky - 1973 Delay ... is a function of resources, intensity and direction .of in t e rest . I’ -- from IMPLEMENTATION by Jeffrey Preesmsa and

I Aaron Uildavsky - 1973

CONCLUSIONS AND RECOMMENDATIONS:

Over the course of the past year and one half of the MCFS

project there have been many p i t f a l l s and disappointments.

Many of these could and should have been foreseen while

others were unavoidable.

good decisions and some poor ones.

The Steering Committee made some

c

f-’

WHAT WENT WRONG?:

The first and most serious mistake made In this entire

project was one of impatience. Because of the negative

publicity received by the courts, the Data Processing

Department, the Auditor-Controller and the County on

several issues this project sprang out of the air. Some

more i n i t i a l analysis of the problems and issues involved

.

- 4 4 -

may have led to B smoother implementation. Because of this impatience and naivety about the system some rather

unrealistic targets fox implementation were set.

A few of the decisions made about the project were a

result of poor information. Even IBM representatives had little first hand knowledge of the 4700 equipment or the

ABCS software, this led on occasion to the wrong decisiohe

being made. This was most obvious in the initial

selection of the printers.

-4

*

Another major problem with this project was the lack of

good programming support. The ABCS software is complex

and not easily mastered even by experienced programmers . This led US t o rely on some sometimes undependable and

careless programers.

The last major area of problems was in the lack of

sufficient early support from the management of DPD. It was only after months of cajoling and finally screaming

that the project received the status and support it

deserved. .

WHAT WENT RIGHT?;

While the goals and objectives of the project -were aLways

clearly in sight. From the beginning there was little I

- 45 -

, 4.

..

i

disagreement about the goals and objectives, everyone

agreed on what they saw the system doing for them.

The overall plan for implementing the system was good.

The decision to implement the project in phases was a wise

one and helped avoid some of the problems that plagued

MCI. This way the project could be brought along piece by

pieceq, speeding up the process of getting some parts of in

automated system on board and also helping to ease the

training process. If the cashiers could learn the system

one piece at time the initial learning curve would not be

as severe.

The involvement of all the other courts in the process was

a crucial step in the development of the project. Also

the involvement of the people who would be actually using

the system was a very positive step. This helped get a

commitment from all the players in the process. Without

this involvement and cooperation the project would never

succeed.

WHAT ABOUT NEXT TIME? :

Before any major project such as MCFS will work in a place

like Los Angeles County a number of things must - be resolved. The issues that need to be dealt with include:

C .

I

- 46 -

.-

* .-

,-.

0

0

0

0

0

I hope

o A clear understanding of the goals and objectives of the project by everyone involved,

Administrative Office, and some commitment from the Board of Supervisors for continued funding.

-the user, DPD, the budget people in the County

Each "major" project should have its own DPD project manager. managers to too many projects only delays the implementation of all that managers projects.

The policy of spreading these

Ideally DPD would have enough qualified programming staff to develop any system. Lacking this staff the method of contracting fo private programmers must be reevaluated. process now is too long and complicated, often resulting in the loss of good and qualified programmers because of lapses in the process.

The

If the project involves an area that DPD has little or no expertise, they should insist,that the entire process be taken a little slower so that more analysis can be done.

It should be clear to everyone involved that the process of implementing these ty R es of projects, involves "people". important part of the project. And with people in the project, problems will always occur. For this reason all of the participants must expect thin s to go wrong and expect things to take a litt e longer. Based on this they should plan for some delays.

Reviews must be built into the project. ongoing commitment for the project must be maintained after the project is up and running, Ideally as we learned from the ETRS audit that this commitment should involve all the same people as involved in the initial project. These are the people who have a stake in the project, i f they move on to other projects and someone else takes their place 6ome of the dedication to and understanding of the project is lost.

People are t e most

f An

that the next project of this type that L am

involved in, that I will have the persistence and tenacity

to insist on and get the things I know are needed.