26

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin Chapter Two

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | alec-terrell |

| View: | 67 times |

| Download: | 2 times |

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter Two

2-2

Explain how to implement a competitive strategy by using Strengths-Weaknesses-Opportunities-Threats (SWOT) Analysis

Explain how to implement a competitive strategy by focusing on the execution of goals

Explain how to implement a competitive strategy using value-chain analysis

Learning Objectives

2-3

Learning Objectives (continued)

Explain how to implement a competitive strategy using the Balanced Scorecard (BSC)

Explain how to expand a conventional Balanced Scorecard (BSC) by integrating sustainability

2-4

There are two main competitive strategies:cost leadershipdifferentiation

Once a firm chooses which strategy to follow, there are various means of implementation:SWOT AnalysisFocus on executionValue-chain analysisBalanced scorecard (BSC)

Implementing a Strategy

2-5

SWOT AnalysisIdentification of critical success factors

(CSFs) tied to strategy—for example:Product innovation QualitySkill development

Identification of quantitative measures for the specified CSFs—for example:Number of design changes or new patentsNumber of defects or number of returnsNumber of training hours or amount of skill

performance improvement

2-6

SWOT Analysis (continued)

The SWOT analysis has four areas:

S – strengths/internalW – weaknesses/internalO – opportunities/externalT – threats/external

Look at product lines, management, R&D, manufacturing, marketing, and strategy

Look at barriers to entry, intensity of rivalry among competitors, substitute goods, and customer/supplier bargaining power

2-7

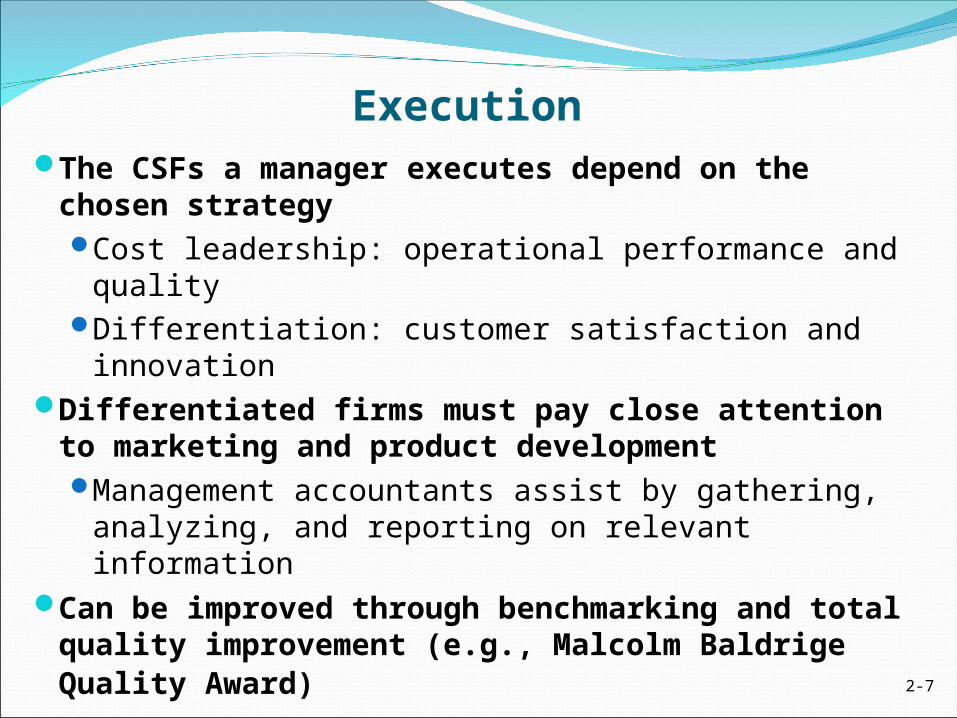

The CSFs a manager executes depend on the chosen strategyCost leadership: operational performance and

qualityDifferentiation: customer satisfaction and

innovation Differentiated firms must pay close attention

to marketing and product developmentManagement accountants assist by gathering,

analyzing, and reporting on relevant informationCan be improved through benchmarking and

total quality improvement (e.g., Malcolm Baldrige Quality Award)

Execution

2-8

Value-Chain AnalysisAn analysis for better understanding the

details of the organization’s competitive strategyCSFs must be implemented in each and every

phase of operations

Helps a firm better understand its competitive advantage by analyzing what processes add value (processes that do not add value can be deleted or outsourced)

Will include upstream (prior to manufacturing or operations) and downstream activities

2-9

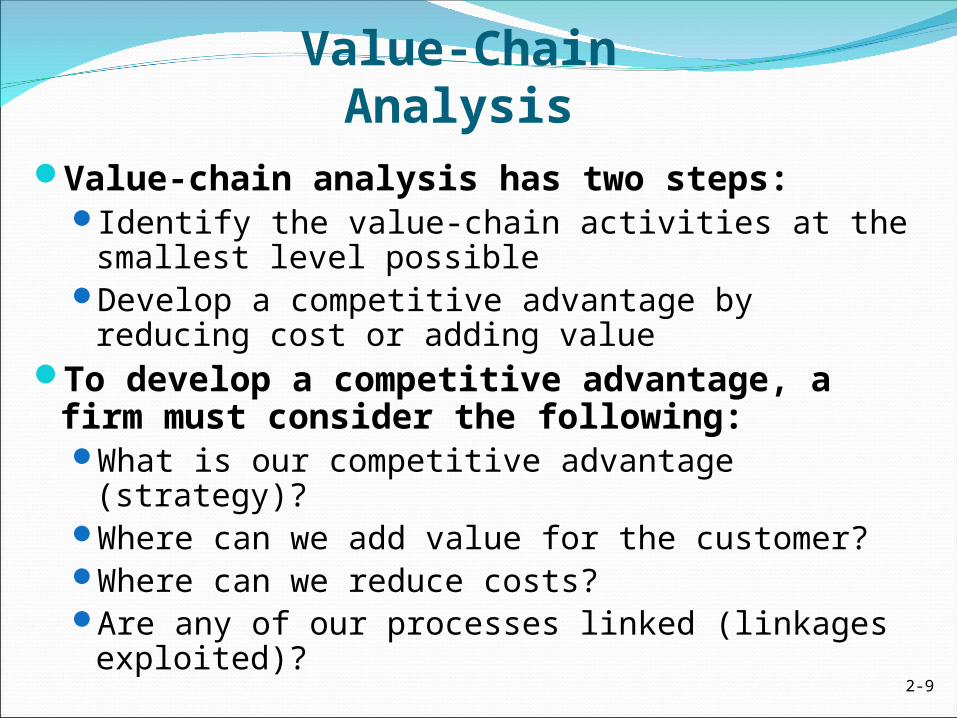

Value-Chain AnalysisValue-chain analysis has two steps:

Identify the value-chain activities at the smallest level possible

Develop a competitive advantage by reducing cost or adding value

To develop a competitive advantage, a firm must consider the following:What is our competitive advantage (strategy)?Where can we add value for the customer?Where can we reduce costs?Are any of our processes linked (linkages

exploited)?

2-10

Example: Value-Chain Analysis in Computer Manufacturing

Computer Intelligence Company (CIC) manufactures computers for small businesses

The company has an excellent reputation for service and reliability as well as a growing customer list: competes on differentiation

Is there any way to add value for the customer while reducing costs?

2-11

Example: Value-Chain Analysis in Computer Manufacturing (continued)

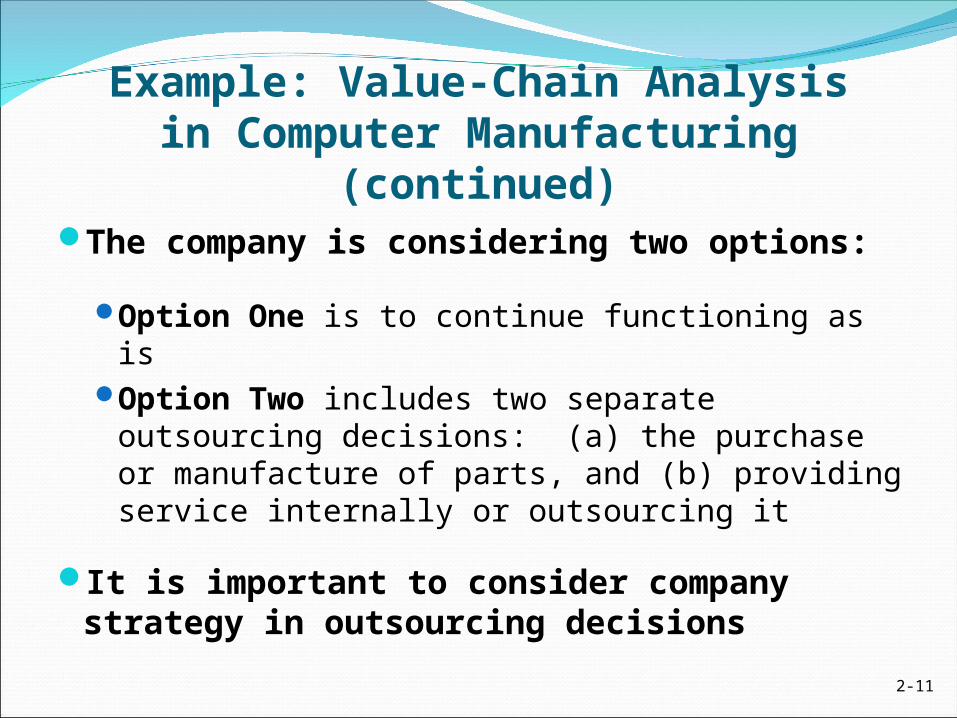

The company is considering two options:

Option One is to continue functioning as isOption Two includes two separate

outsourcing decisions: (a) the purchase or manufacture of parts, and (b) providing service internally or outsourcing it

It is important to consider company strategy in outsourcing decisions

Value-Chain Analysis in Computer Manufacturing (continued)

Value Activity Option One – Current Option Two – Potential

Acquiring raw materials

CIC is not involved at this step

CIC is not involved at this step

Manufacturing computer chips and other parts

CIC is not involved at this step; cost is $200

CIC is not involved at this step; cost is $200

Manufacturing components, some of which CIC can make

CIC purchases $300 of parts for each unit

CIC manufactures these parts for $190 per unit plus $55,000 monthly

Assembling CIC’s costs are $250 CIC’s costs are $250

Marketing, distributing, and servicing

CIC’s costs are $175,000 per month

CIC contracts out these services for $130 per month

2-12

Results of Value-Chain Analysis

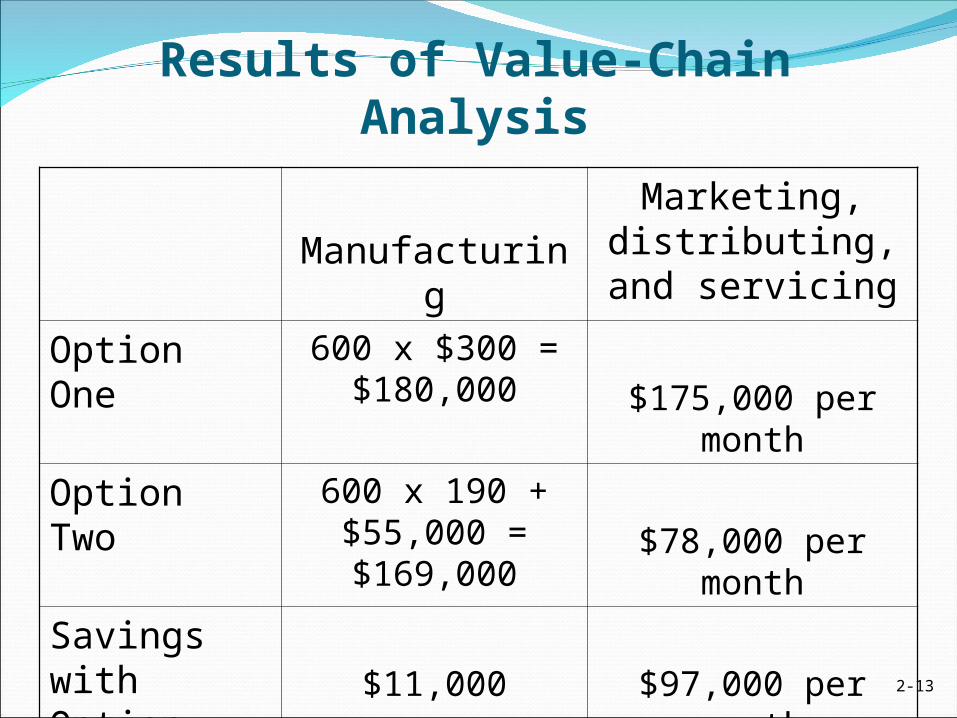

Manufacturing

Marketing, distributing, and

servicing

Option One 600 x $300 = $180,000 $175,000 per month

Option Two 600 x 190 + $55,000 = $169,000

$78,000 per month

Savings with Option Two $11,000 $97,000 per month

2-13

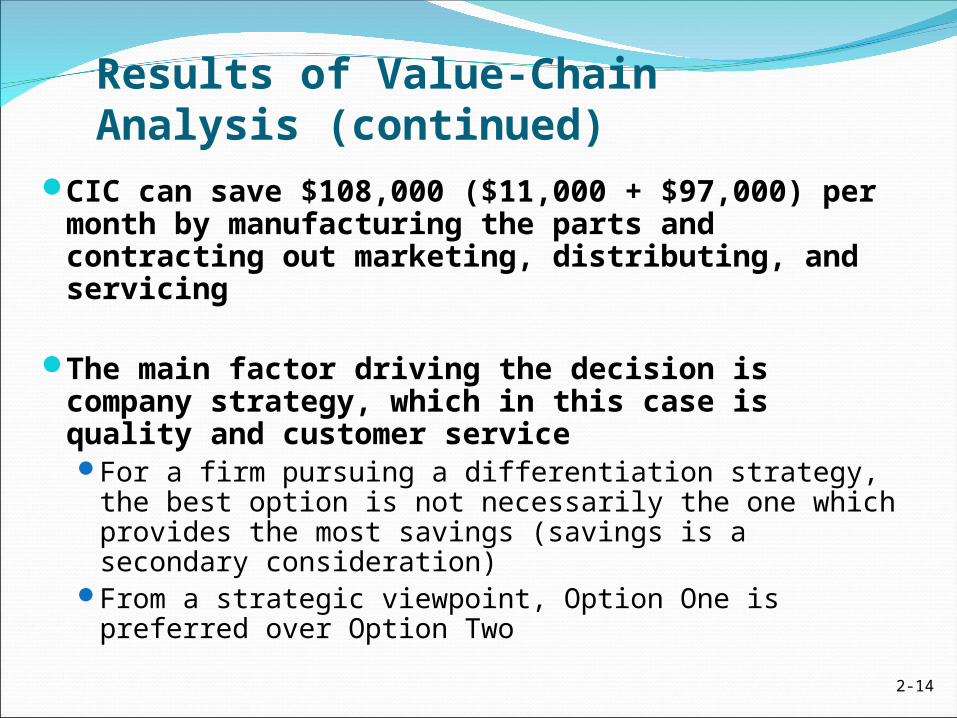

Results of Value-Chain Analysis (continued)CIC can save $108,000 ($11,000 + $97,000)

per month by manufacturing the parts and contracting out marketing, distributing, and servicing

The main factor driving the decision is company strategy, which in this case is quality and customer serviceFor a firm pursuing a differentiation strategy, the best

option is not necessarily the one which provides the most savings (savings is a secondary consideration)

From a strategic viewpoint, Option One is preferred over Option Two

2-14

2-15

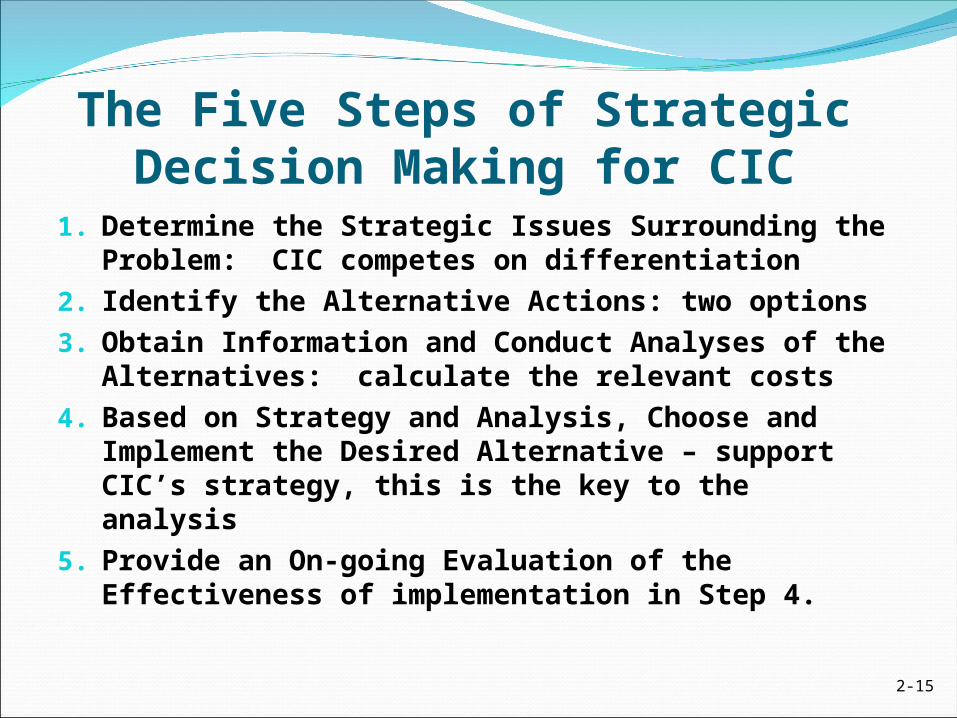

The Five Steps of Strategic Decision Making for CIC

1. Determine the Strategic Issues Surrounding the Problem: CIC competes on differentiation

2. Identify the Alternative Actions: two options3. Obtain Information and Conduct Analyses of

the Alternatives: calculate the relevant costs4. Based on Strategy and Analysis, Choose and

Implement the Desired Alternative – support CIC’s strategy, this is the key to the analysis

5. Provide an On-going Evaluation of the Effectiveness of implementation in Step 4.

2-16

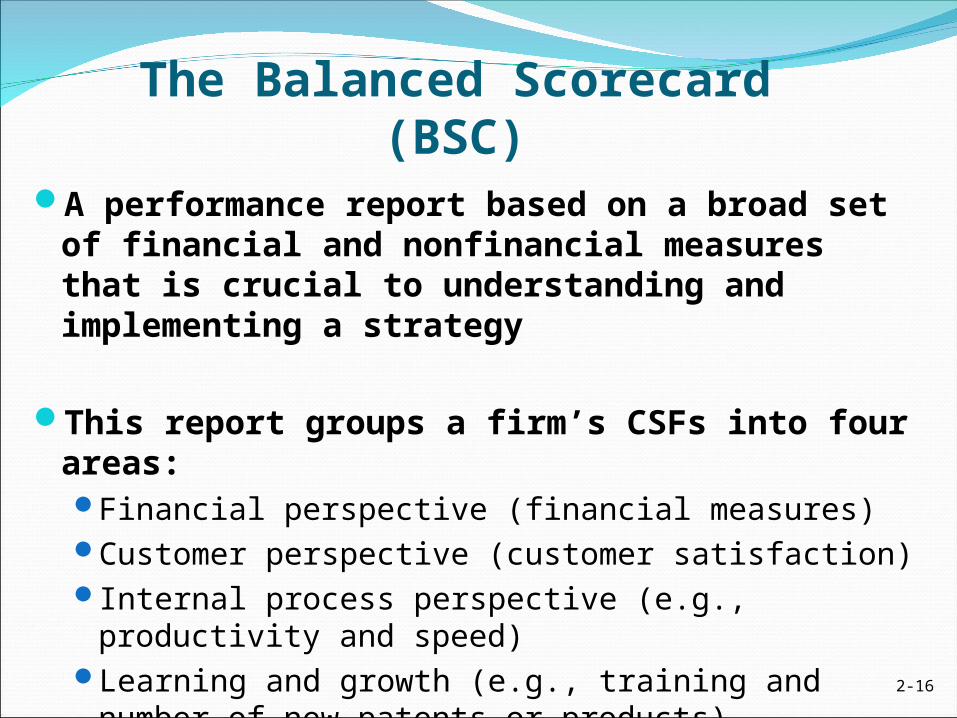

The Balanced Scorecard (BSC)A performance report based on a broad set

of financial and nonfinancial measures that is crucial to understanding and implementing a strategy

This report groups a firm’s CSFs into four areas: Financial perspective (financial measures)Customer perspective (customer satisfaction)Internal process perspective (e.g., productivity

and speed)Learning and growth (e.g., training and number of

new patents or products)

2-17

The Balanced Scorecard (continued)Benefits

Provides a means for implementing strategy

Provides a means to achieve a desired organizational change in strategy

Can be used to determine management’s compensation and rewards

Aligns managers’ efforts with strategyCoordinates efforts within the firm to

achieve CSFs

2-18

The Balanced Scorecard (continued)A properly constructed BSC can be used to

infer a company’s strategy

BSC → Strategy, and Strategy → BSC

The emphasis placed on each performance perspective reflects the strategy of the firm

For a cost leader, the operations perspective might be the most important; for a differentiator, the customer perspective…

2-19

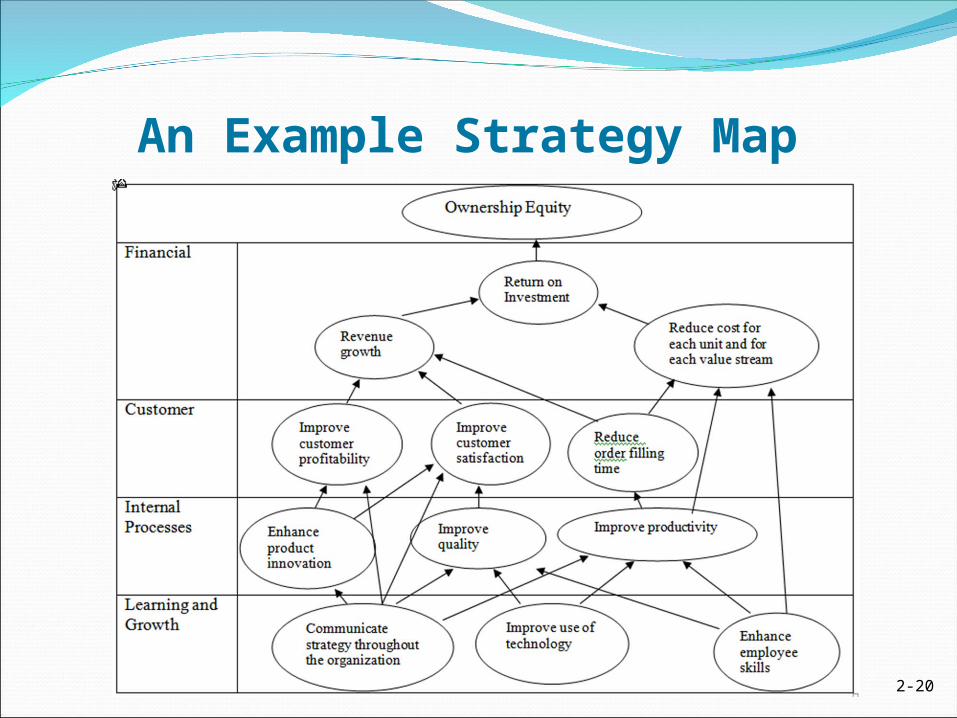

Strategy MapA strategy map is a cause-and-effect diagram of the relationships embodied in a BSC:

Shows how the achievement of CSFs in one

perspective should affect the achievement of goals in another perspective

The financial perspective is the target in the strategy map because financial performance is the ultimate goal for most profit-seeking organizations

Success in the other perspectives leads directly to improved financial performance and shareholder value

2-20

An Example Strategy Map

2-21

SustainabilityThe fifth perspective for many organizations

The balancing of short-term and long-term goals in all three dimensions of the company’s performance–economic, social, and environmental:

Environmental reports use environmental performance indicators (EPIs) to measure sustainability

These indicators are in three areas: Operational (measure stresses to the environment/regulatory

compliance issues) Management (try to reduce environmental effects) Environmental condition (measure environmental quality)

2-22

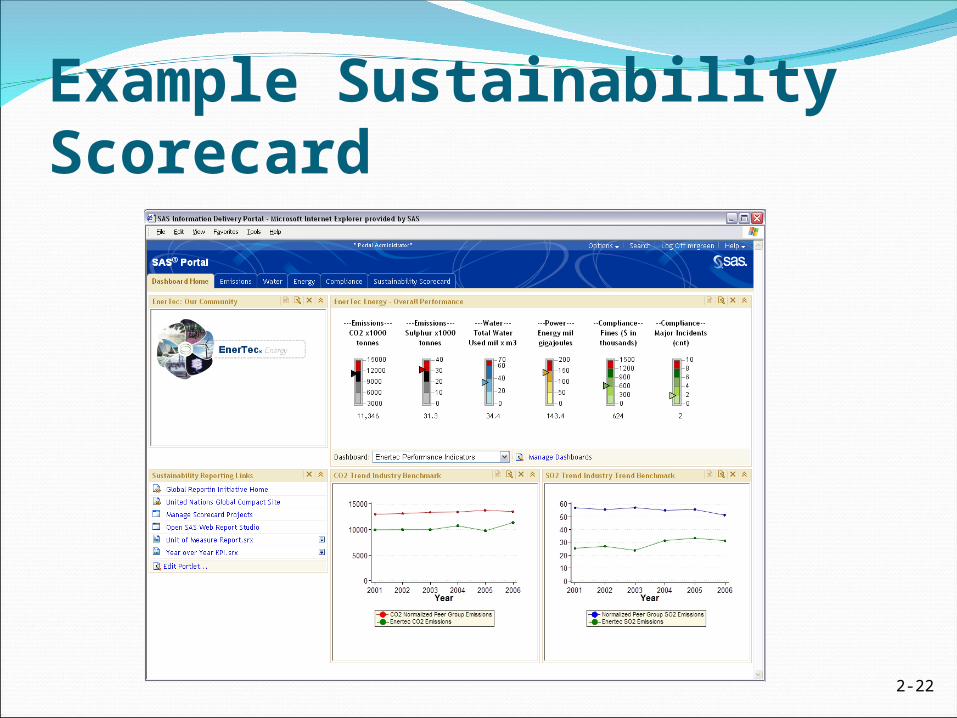

Example Sustainability Scorecard

2-23

The BSC and Not-For-Profit Organizations

Competitive strategy is different:

Must satisfy funding authorities, political leaders, and the general public

The BSC can still be used to monitor CSFs related to internal processes, customer satisfaction, financial measures, and human resources measures

Value-chain analysis can still be used to determine at what points costs can be reduced or value added on the value chain

2-24

The Role of Cost ManagementThree cost-management resources for implementing strategy are discussed in this chapter: SWOT analysis provides a system and structure to

identify CSFs

Value-chain analysis builds on the CSFs by breaking them down into detailed activities

The BSC provides a way to implement the detailed strategy developed through the previous two analyses; it provides the processes for evaluating the organization’s achievement of CSFs

2-25

Strengths-Weaknesses-Opportunities-Threats (SWOT) Analysis provides a system and structure in which to identify a firm’s critical success factors (CSFs)

Execution of goals is important in implementing a strategy

Execution depends on the competitive strategy a firm is pursuing

Management accountants assist management by gathering, analyzing, and reporting on relevant information

Chapter Summary

2-26

Chapter Summary (continued)• Value-chain analysis builds on the CSFs identified in

SWOT analysis by breaking them into detailed activities

• The balanced scorecard (BSC) provides the processes

for evaluating a firm’s achievement of CSFs

• Sustainability builds on the conventional BSC by balancing short-term and long-term goals

• Sustainability focuses on economic, social, and environmental issues