Page 1

i

IMPLICATIONS OF CORPORATE SOCIAL RESPONSIBILITY ON FINANCIAL AND

NON-FINANCIAL PERFORMANCE OF BANKING SECTOR OF PAKISTAN:

MODERATING ROLE OF STAKEHOLDER PRESSURE AND MEDIATING ROLE OF

INNOVATION AND CORPORATE REPUTATION

BY

MUZAMMAL ILYAS SINDHU

ENROLMENT: 01-280152-007

A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY

IN MANAGEMENT SCIENCES

To

DEPARTMENT OF MANAGEMENT STUDIES

BAHRIA UNIVERSITY, ISLAMABAD, PAKISTAN

2020

Page 2

ii

SUBMISSION FORM OF THESIS FOR HIGHER RESEARCH DEGREE

BAHRIA UNIVERSITTY, ISLAMABAD

Candidate Name: Muzammal Ilyas Sindhu

Thesis Titled:

“Implications of Corporate Social Responsibility on Financial and Non-Financial Performance

of Banking Sector of Pakistan: Moderating Role of Stakeholder Pressure and Mediating Role of

Innovation and Corporate Reputation”

Candidate Signature: ____________________

Certificate of Principal Supervisor

I Dr Muhammad Arif being the principal Supervisor for the above scholar, certifies that thesis is

in a form suitable for examination and that the candidate has pursued his course in accordance

with the Rules of the University.

Signature: _______________________ Date: ______________________

Recommendation for Examination

I recommend that the thesis be examined.

Principal Supervisor: _______ Dr Muhammad Arif __________ Date: _____________________

Co-Supervisor:_________________ Date: _____________________

Not Recommended for Examination

I recommend that the thesis be examined.

Principal Supervisor: ____________________________________ Date: ___________________

Co-Supervisor:______________________ Date: __________________

Statement by the Head Faculty/Department

I support the submission of the thesis of the above named student for examination under the

University Rules for higher degrees.

Signature: ______________________________________________ Date: _________________

Page 3

iii

BAHRIA UNIVERSITY, ISLAMABAD

APPROVAL SHEET

SUBMISSION OF HIGHER RESEARCH DEGREE THESIS

Candidate’s Name: Muzammal Ilyas Sindhu

Discipline: Management Sciences

Faculty/ Department: Management Studies

I hereby certify that the above candidate’s work, including the thesis, has completed to my

satisfaction and that the thesis is in a format and of an editorial standard recognized by the

faculty/ department as appropriate for examination.

Signature(s) Principal Supervisor: Dr Muhammad Arif

Dated: -----------------------------------

The undersigned certify that:

The candidate presented at a pre-completion seminar, and overview and synthesis of

major findings of the thesis, and that the research is of a standard and extent appropriate for

submission as a thesis.

I have checked the candidate’s thesis and its scope, format; editorial standards are

recognized by the faculty/department as appropriate.

Signature(s) Dean/Head of Faculty/ Department:

Dated: ------------------

Page 4

iv

COPYRIGHT

Copyright © [2019] by Muzammal Ilyas Sindhu

All Rights Reserved

The thesis and its content including the proposed title “Implications of Corporate Social

Responsibility on Financial and Non-Financial Performance of Banking Sector of Pakistan:

Moderating role of Stakeholder pressure and mediating role of innovation and corporate

reputation” are the copyright of in the undersigned PhD scholar’s name as author.

Sign(s) PhD scholar: Muzammal Ilyas Sindhu

Page 5

v

AUTHOR’S DECLARATION

I, Muzammal Ilyas Sindhu, PhD Scholar in the Department of Management Studies, Bahria

University, Islamabad, certify that the research work presented in this thesis is to the best of my

knowledge my own. All sources used and any help received in the preparation of this dissertation

have been acknowledged. I hereby declare that I have not submitted this material, either in

whole or in part, for any other degree at this or other institution. At any time if my statement is

found to be incorrect even after my graduation, the University has the right to withdraw/cancel

my PhD Degree.

Signature: ___________________

Name: Muzammal Ilyas Sindhu

Page 6

vi

Dedication

I dedicate this thesis to “Allah Almighty” my eternal rock and source of refuge,

Who gave me the passion to work hard and struggle to comply with my destiny

and to “Hazrat Muhammad (PBUH)” the one who enlightened my heart with the

rules to follow.

This thesis is also dedicated to

My beloved parents, siblings, my wife and daughters (Manahil Bahu, Mahnoor

Muzammal, Malaika Muzammal) as their love, care and support for my studies

without which I could not be able to reach at this level.

(May Allah Bless Me, My Family and Well Wishers)

Page 7

vii

ACKNOWLEDGEMENTS

All praises to “Allah Almighty” Who enabled me to complete this task successfully and my

utmost respect to His last Prophet Muhammad (PBUH).

I would like to express the deepest appreciation of my respected supervisor Prof Dr Muhammad

Arif for his patience, motivation, enthusiasm, immense knowledge and continuous support in

completion of my PhD thesis. His guidance helped me all the time in research and writing of

thesis. I could not have imagined having a better advisor and mentor for my PhD thesis.

Besides my supervisor, I would like to thank the rest of my Final defense committee: respected

Dr. Muhammad Khalid Sohail, Dr. Muhammad Razzaq Athar and Dr. Shehzad Anjum, for their

encouragement, insightful comments, and hard questions. I want to gratefully acknowledge my

respected teachers Prof. Dr Hafiz Mushtaq Ahmed, Prof. Dr. Muhammad Ismail Ramay, Prof. Dr

Nadia Tahir, Prof. Dr. Faisal Aftab, Dr Muhammad Hanif, Dr. Riaz Ahmed, Dr Abdul Sattar, Dr

Taqaddas Bashir Chaudhry, and Dr Abdul Qazi Subhan; all of them revolutionized my life in a

very real sense by planting the seeds of research and logic, what I learnt in their classes and from

their professionalism has not only add up to my knowledge but, I feel to be a better person. I am

grateful to Dr. Anwar Fazal Chishti for enlightening me the first glance of research.

I thank my beloved friends Dr Hafiz Muhammad Waqar, Muhammad Irfan Khadim, Saif ul

Rehman, Syeda Urooj Babar, Aqil Waqar Khan, Kamran Iqbal, Faisal Mehmood, Syed Usman

Lutfi, Sarina Shrizai, and Tanveer Taj who guide me in initiation of this research thesis. I also

thanks to my fellows Ehtasham Ul Haq and Muhammad Iftikhar Ali for the stimulating

discussions, for the sleepless nights we were working together before deadlines, and for all the

fun we have had in the couple of months. Also I thank my well-wisher’s Sana Ullah Khan,

Akhter, Shakeel Abbas, Ali Hassan, Abid Hussain, and Muhammad Ifraheem. In particular, last

but not the least; I would like to thank my parents for giving birth to me at the first place and to

my wife, siblings for always being encouraging and supporting me spiritually.

Muzammal Ilyas Sindhu

Page 8

viii

PLAGIARISM UNDERTAKING

I, solemnly declare that research work presented in the thesis titled

“Implications of Corporate Social Responsibility on Financial and Non-Financial

Performance of Banking Sector of Pakistan: Moderating role of Stakeholder

pressure and mediating role of innovation and corporate reputation” is solely my

research work with no significant contribution from any other person. Small

contribution / help wherever taken has been duly acknowledged and that complete

thesis has been written by me.

I understand the zero tolerance policy of the HEC and Bahria University towards

plagiarism. Therefore I as an Author of the above titled thesis declare that no portion

of my thesis has been plagiarized and any material used as reference is properly

referred / cited.

I undertake that if I am found guilty of any formal plagiarism in the above titled

thesis even after award of PhD degree, the university reserves the right to withdraw /

revoke my PhD degree and that HEC and the University has the right to publish my

name on the HEC / University website on which names of scholars are placed who

submitted plagiarized thesis.

Scholar / Author’s Sign: ____________

Name of the Scholar: Muzammal Ilyas Sindhu

Page 9

ix

ABSTRACT

In the banking sector, besides the short-term internal business interests of financial companies,

social, environmental and human rights objectives are gaining a dominant and interesting role. In

this perspective, engagement in socially responsible activities can serve as a strategic tool for a

firm’s to avail competitive edge. This evident that corporate social responsibility plays important

role in determining bank performance and it convinced to examine the relationship between CSR

and performance in the banking industry of Pakistan. Furthermore, this study examined the

moderating impact of stakeholder pressure and mediating influence of innovation and corporate

reputation in between the relationship of CSR and performance. There were total 405 responses

analyzed for examining aforementioned relationships. Structural equation modeling was applied

and the direct relationship indicated that there is a significant and positive relationship between

corporate social responsibility and financial performance. These findings were supported by

multiple studies, as they already tested the significant and positive relationship between these

two factors. The direct relationship indicated that there is a significant and positive relationship

between corporate social responsibility and non-financial performance. Corporate social

responsibility directly influenced financial and non-financial performance. In other direct

relationships, corporate social responsibility also influenced innovation and corporate reputation.

The innovation influenced corporate reputation, financial and non-financial performance.

Corporate reputation showed no significant influence on financial and non-financial

performance. In research analysis, simple mediations indicated that innovation played significant

mediation role in relationship between CSR, financial and non-financial performance. Moreover,

corporate reputation also mediated among CSR, financial and non-financial performance. In case

of sequential mediation, innovation and corporate reputation have strongly played role as

mediating variable among CSR, financial and non-financial performance. Last but not least,

stakeholder pressure moderated and established relation of CSR, financial and non-financial

performance. This study contributes to existing knowledge, and beneficial to policy makers,

corporate managers, and executives in establishing corporate strategies. As proposed that if the

banking industry improves their socially responsible activities, it tends toward establishing trust

among stakeholders and enhances their performance.

Keywords:

Corporate Social Responsibility; Financial Performance; Non-Financial Performance;

Innovation; Corporate Reputation; Stakeholder Pressure; Structural Equation Modeling

Page 10

x

TABLE OF CONTENTS

Title Page i

Submission Form ii

Approval Sheet iii

Copy Right iv

Author’s Declaration v

Dedication vi

Acknowledgements vii

Plagiarism undertaking viii

Abstract ix

Table of Contents x

List of Tables xiv

List of Abbreviations xvi

HEC Publication Requirement xvii

CHAPTER 1

INTRODUCTION

1.1 Background of the Study 01

1.2 Contextual Analysis 07

1.3 Rationale of the Study 11

1.4 Problem Statement 13

1.5 Research Questions 15

1.6 Research Objectives 15

1.7 Significance of the study 16

CHAPTER 2

LITERATURE REVIEW

2.1 Introduction 17

2.2 Literature Search Strategy 17

2.3 Corporate Social Responsibility 17

2.4 Dimensions of CSR 24

2.5 Stakeholder Pressure 28

2.6 Corporate Reputation 32

2.7 Innovation 33

2.8 Corporate social responsibility and Financial Performance 35

2.9 Corporate social responsibility, Stakeholder Pressure and Performance 39

2.10 Corporate social responsibility, Corporate Reputation and Performance 42

2.11 Corporate social responsibility, Innovation and Performance 47

2.12 Theoretical Background 52

2.13 Conceptual Framework 54

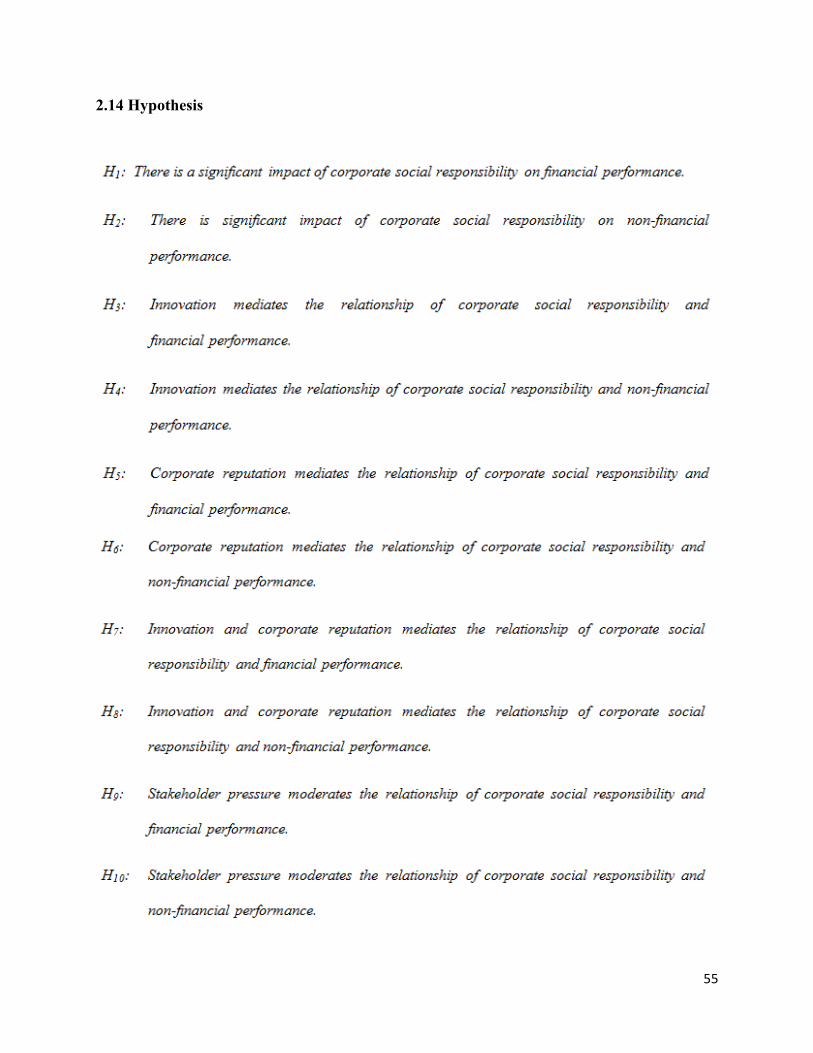

2.15 Hypothesis 55

Page 11

xi

CHAPTER 3

THE DATA AND RESEARCH METHODOLOGY

3.1 Introduction 56

3.2 Target Population 57

3.3 Sampling Design 57

3.4 Data Collection 58

3.5 Measurement Scale 58

3.6 Data Analysis Techniques 59

3.6.1 Normality Tests 60

3.6.2 Descriptive Statistics 60

3.6.3 Correlation 61

3.6.4 Structural Equation Modeling 61

3.7 Pilot Testing 63

3.8 Ethical Consideration 64

CHAPTER 4

EMPIRICAL STUDY

4.1 Introduction 65

4.2 Assessment of Measurement Models 65

4.2.1 Measurement Models of Corporate Social Responsibility 65

4.2.1.1 Descriptive Statistics 65

4.2.1.2 Assessment of Overall Fitness 67

4.2.1.3 Assessment of Inter Item Correlation and Reliability 73

4.2.2 Measurement Models of Corporate Reputation 74

4.2.2.1 Descriptive Statistics 74

4.2.2.2 Assessment of Overall Fitness 75

4.2.2.3 Assessment of Inter Item Correlation and Reliability 79

4.2.3 Measurement Models of Innovation 81

4.2.3.1 Descriptive Statistics 81

4.2.3.2 Assessment of Overall Fitness 82

4.2.3.3 Assessment of Inter Item Correlation and Reliability 86

4.2.4 Measurement Models of Financial Performance 87

4.2.4.1 Descriptive Statistics 87

4.2.4.2 Assessment of Overall Fitness 88

4.2.4.3 Assessment of Inter Item Correlation and Reliability 91

4.2.5 Measurement Models of Non-Financial Performance 93

4.2.5.1 Descriptive Statistics 93

4.2.5.2 Assessment of Overall Fitness 94

Page 12

xii

4.2.5.3 Assessment of Inter Item Correlation and Reliability 98

4.2.6 Measurement Models of Stakeholder Pressure 100

4.2.6.1 Descriptive Statistics 100

4.2.6.2 Assessment of Overall Fitness 101

4.2.6.3 Assessment of Inter Item Correlation and Reliability 104

4.3 Assessment of Structural Model 106

4.3.1. Normality 106

4.3.1.1. Descriptive Statistics of Overall Selected Variables 106

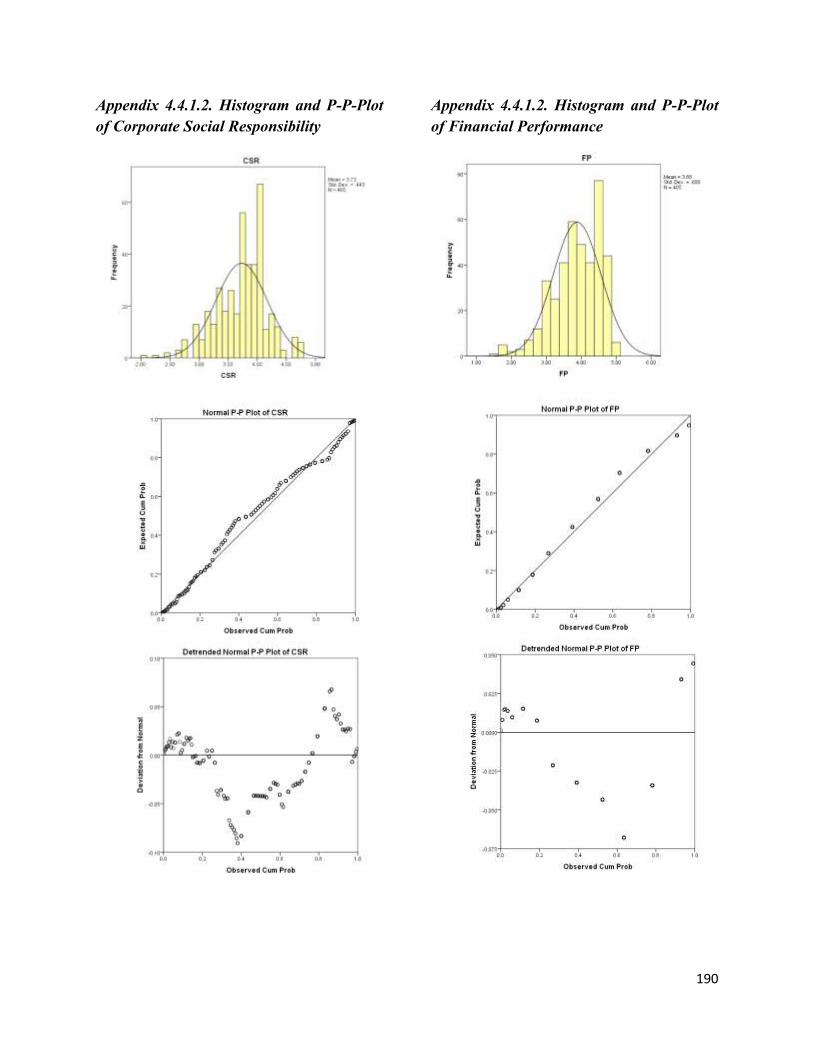

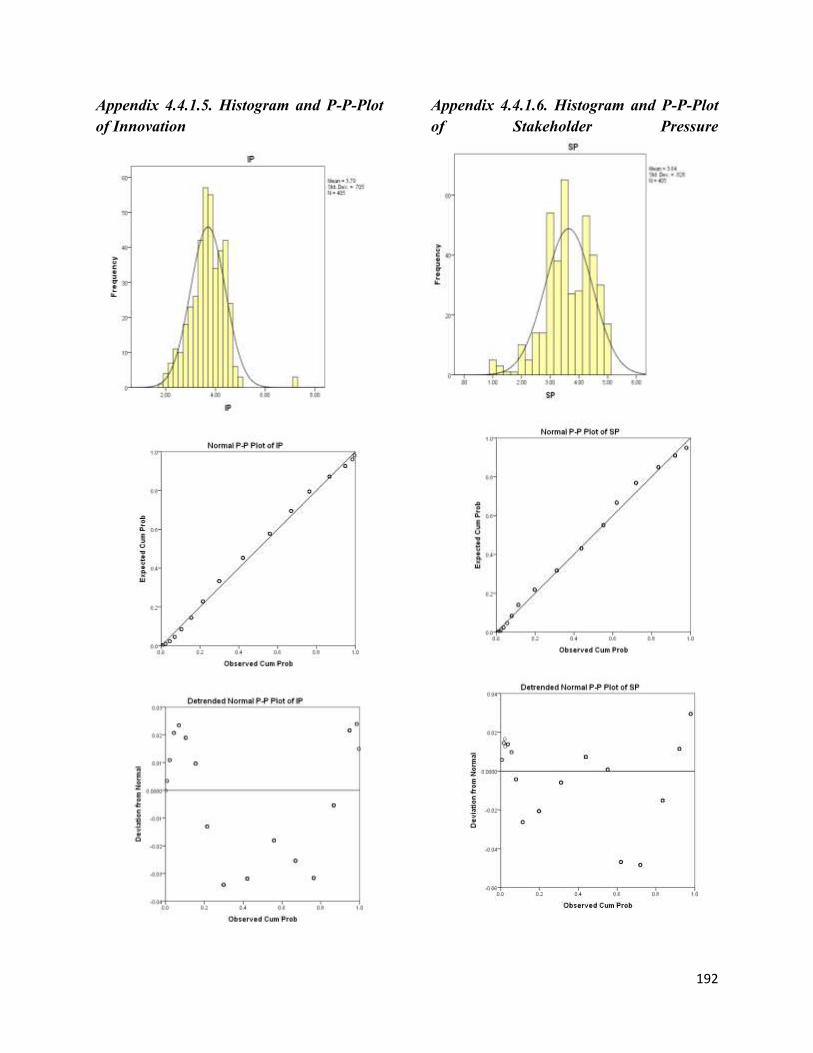

4.3.1.2. Histogram and P-P Plot 107

4.3.2. Linearity 108

4.3.3. Multicollinearity 108

4.3.4. Demographics 110

4.3.5. Reliability and Validity Analysis 111

4.3.6. Goodness and Fitness 112

4.3.7. Correlation Matrix 114

4.4 Hypothesis Testing 115

4.4.1 Direct Relationship 115

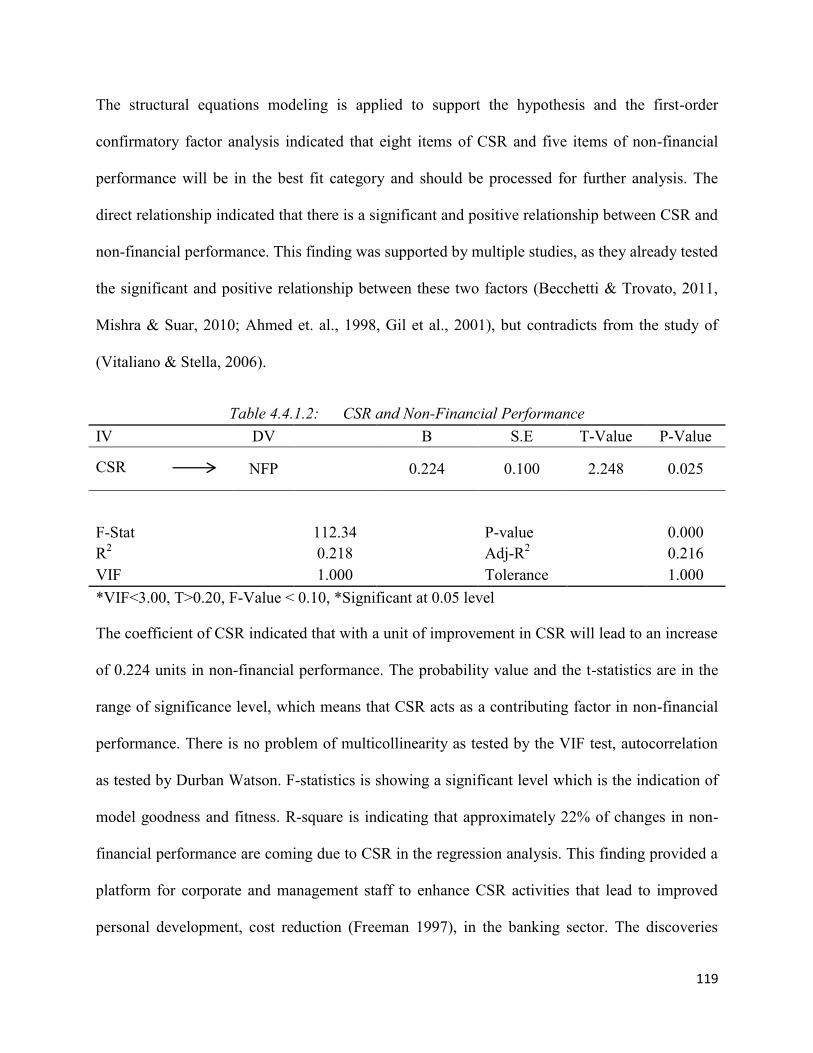

4.4.1.1 Corporate Social Responsibility and Financial Performance 115

4.4.1.2 Corporate Social Responsibility and Non-Financial Performance 118

4.4.1.3 Remaining Direct Relationships 120

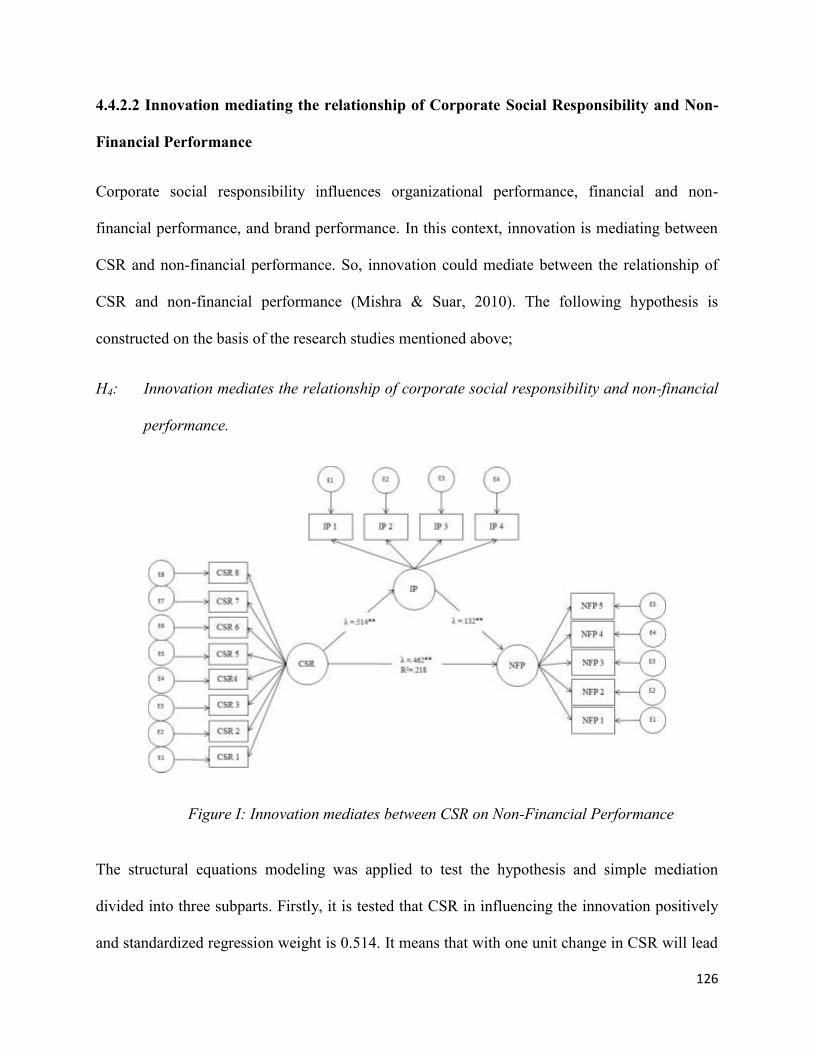

4.4.2 Simple Mediation 122

4.4.2.1 Innovation mediating the relationship of Corporate Social Responsibility

and Financial Performance 122

4.4.2.2 Innovation mediating the relationship of Corporate Social Responsibility

and Non-Financial Performance 126

4.4.2.3 Corporate Reputation mediating the relationship of Corporate Social

Responsibility and Financial Performance 129

4.4.2.4 Corporate Reputation mediating the relationship of Corporate Social

Responsibility and Non-Financial Performance 132

4.4.3 Sequential Mediation 135

4.4.4 Moderation 140

4.4.4.1 Moderation I 140

4.4.4.2 Moderation II 142

CHAPTER 5

DISCUSSION AND CONCLUSION REMARKS

5.1 Introduction 144

5.2 Discussion 144

5.3 Conclusion 148

5.4 Contribution to knowledge 150

5.5 Implications 151

Page 13

xiii

5.6 Limitations 152

5.7 Delimitations 153

5.8 Recommendations and Future direction 154

References 156

Appendixes 190

Questionnaire 195

Sample selection 199

Page 14

xiv

LIST OF TABLES

Table 2.1: Evolving definitions of CSR 20

Table 4.2.1.1 Descriptive Statistics of CSR 66

Table 4.2.1.2: Fit levels of Original CSR Measurement Model 68

Table 4.2.1.3: Comparative Fitness levels of CSR Measurement Model 72

Table 4.2.1.4: Inter Item Correlation of CSR Measurement Model 73

Table 4.2.2.1 Descriptive Statistics of Corporate Reputation 74

Table 4.2.2.2: Fit levels of Original CR Measurement Model 76

Table 4.2.2.3: Comparative Fitness levels of CR Measurement Model 78

Table 4.2.2.4: Inter-item Correlation of CR Measurement Model 79

Table 4.2.3.1 Descriptive Statistics of Innovation 81

Table 4.2.3.2: Fit levels of Original IP Measurement Model 83

Table 4.2.3.3: Comparative Fitness levels of IP Measurement Model 85

Table 4.2.3.4: Inter-Item Correlation of IP Measurement Model 86

Table 4.2.4.1 Descriptive Statistics of Financial Performance 87

Table 4.2.4.2: Fit levels of Original FP Measurement Model 89

Table 4.2.4.3: Comparative Fitness levels of FP Measurement Model 91

Table 4.2.4.4: Inter-item Correlation of Financial Performance Measurement Model 92

Table 4.2.5.1 Descriptive Statistics of Non-financial performance 93

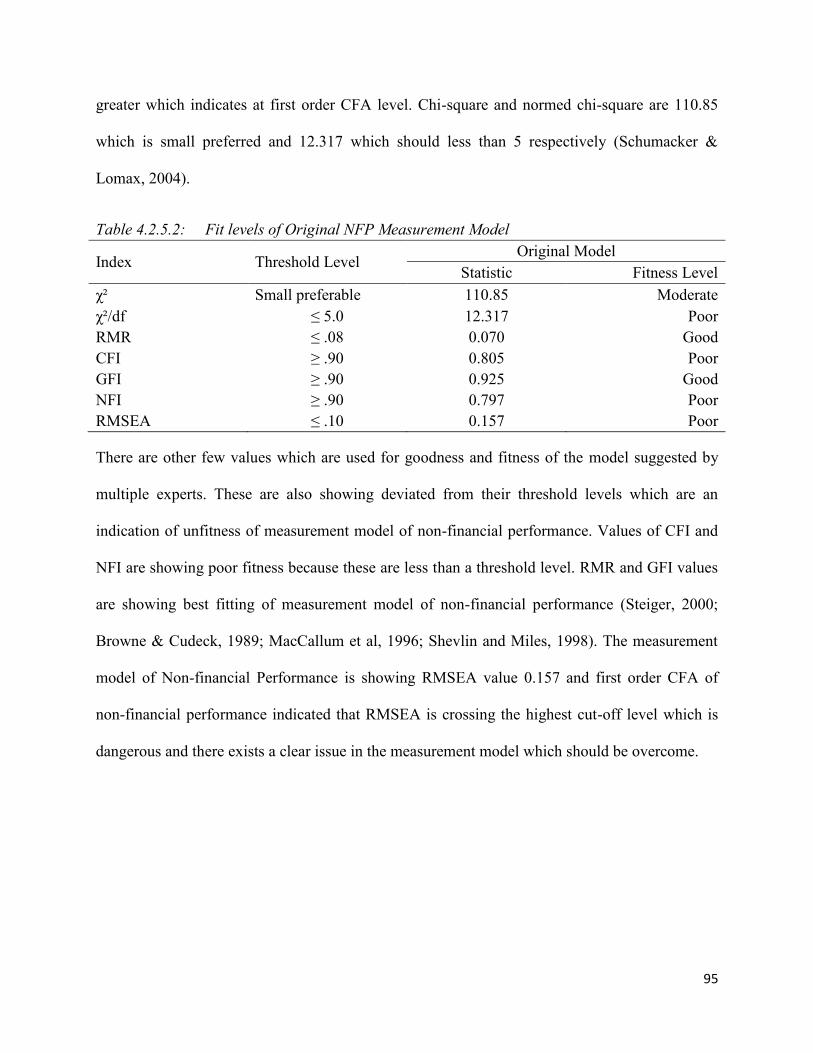

Table 4.2.5.2: Fit levels of Original NFP Measurement Model 95

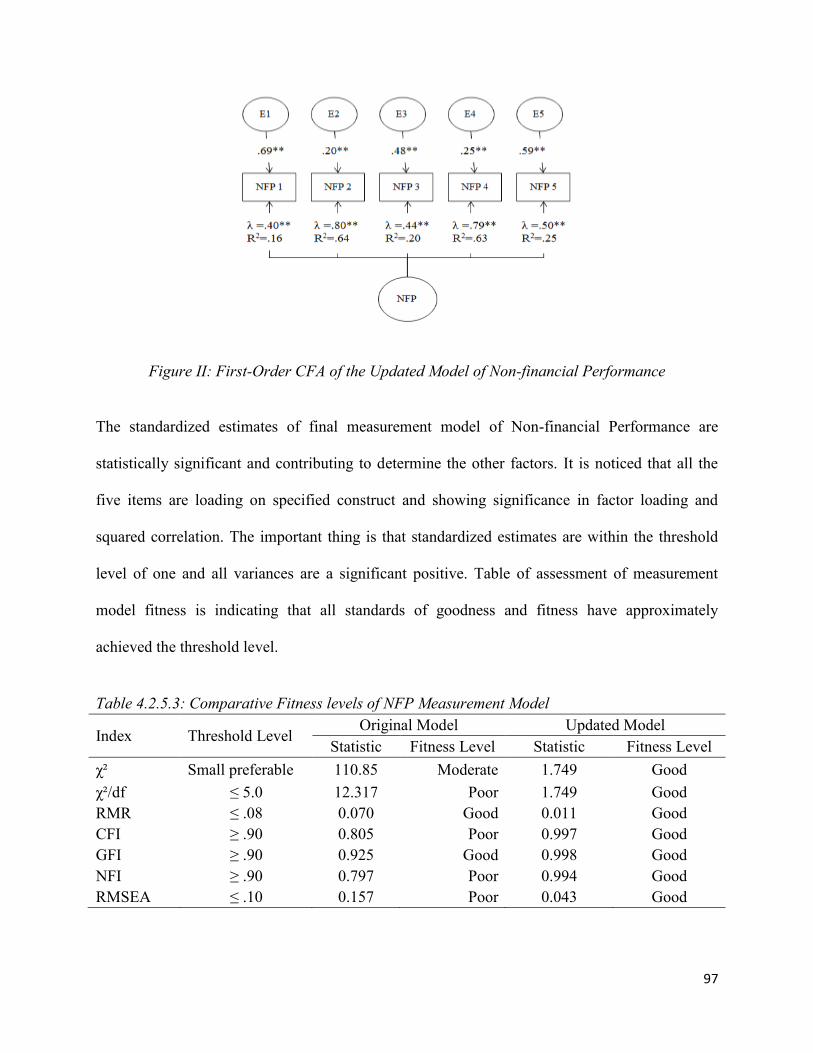

Table 4.2.5.3: Comparative Fitness levels of NFP Measurement Model 97

Table 4.2.5.4: Inter-item Correlation of NFP Measurement Model 98

Table 4.2.6.1 Descriptive Statistics of Stakeholder Pressure 100

Table 4.2.6.2: Fit levels of Original SP Measurement Model 102

Table 4.2.6.3: Comparative Fitness levels of SP Measurement Model 104

Table 4.2.6.4: Inter-item Correlation of SP Measurement Model 105

Table 4.3.1.1 Descriptive Statistics Overall 107

Table 4.3.3.1: Tolerance Level for Multicollinearity 109

Table 4.3.3.2: VIF Level for Multicollinearity 109

Table 4.3.4.1: Demographics 110

Table 4.3.5.1 Reliability and Validity Analysis 111

Table 4.3.6.1: Good and Fitness levels of Final Structural Model 112

Table 4.3.7: Correlation Matrix 114

Table 4.4.1.1: CSR and Financial Performance 117

Table 4.4.1.2: CSR and Non-Financial Performance 119

Table 4.4.1.3: Direct Relationships 120

Table 4.4.1.1: Mediation I 124

Table 4.4.2.2: Mediation II 127

Table 4.4.2.3: Mediation III 130

Table 4.4.2.4: Mediation IV 133

Page 15

xv

Table 4.4.3.1: Mediation V 136

Table 4.4.3.2: Mediation VI 139

Table 4.4.4.1: Moderation I 140

Table 4.4.4.2: Moderation II 142

Appendixes 190

Page 16

xvi

LIST OF ABBREVIATIONS

Sr No. Detailed Word Abbreviation

1 Analysis of Moment Structures AMOS

2 China Pakistan economic corridor CPEC

3 Chi-square χ²

4 Comparative fit index CFI

5 Confirmatory factor analysis CFA

6 Corporate reputation CR

7 Corporate social responsibility CSR

8 Exploratory factor analysis EFA

9 Financial performance FP

10 Goodness of fit index GFI

11 Gross domestic product GDP

12 Human resource Management HRM

13 Innovation IP

14 Karachi stock exchange KSE

15 Kurtosis Kurt

16 Non-governmental organization NGO

17 Non-financial performance NFP

18 Normed chi-square χ²/df

19 Normed fit index NFI

20 Return on Asset ROA

21 Root Mean Square Error of Approximation RMSEA

22 Root mean square residual RMR

23 Skewness Skew

24 Stakeholder pressure SP

25 Standard error SE

26 State Bank of Pakistan SBP

27 Statistical Package for the Social Sciences SPSS

28 Structural equation modeling SEM

29 United States of America US/USA

30 Variance inflation factor VIF

Page 17

xvii

HEC REQUIREMENT OF PUBLICATION

Paper Title:

1. Sindhu, M. I., & Arif, M. (2017). The inter linkage of corporate reputation between

corporate social responsibility and financial performance. Pakistan Journal of Commerce

and Social Sciences, 11(3), 898-910.

2. Sindhu, M. I., & Arif, M. (2017). Corporate social responsibility and loyalty: Intervening

influence of customer satisfaction and trust. Cogent Business & Management, 4(1), 1-10.

Authors Name:

Muzammal Ilyas Sindhu

Dr Muhammad Arif

Journal Name:

1. Pakistan Journal of Commerce and Social Sciences (Y Category)

2. Cogent Business & Management (ISI Indexed – ESCI)

Page 18

1

CHAPTER 1

INTRODUCTION

1.1 Background of the Study

Classical theories of finance are based on the notion that the main objective of any organization

is to maximize the shareholder‟s wealth. In the context of capitalistic economy, the sole

organizational concern should be to enhance their operating performance. Financial firms are

particularly more concerned about their performance because they have to contribute toward the

financial well-being of a society. So, organization does not concern only with financial goals but

they have to respond the non-financial interests of stakeholders. However, last few years

enlightened the stakeholder‟s activism and long term sustainability context. So, the main thrust

of my study is to examine the impact of corporate social responsibility on financial performance

(Robin, Salim & Bloch, 2018; Abusharbeh, 2017; Evans et al., 2014).

Financial performance considered a key indicator of financial firms specially banks. It indicates

whether the firms work efficiently, fulfill its goals, enhanced returns and maximized

shareholder‟s wealth. It leads toward the development of human resource, business prosperity,

and more profit distribution among shareholders. The strong financial position of the business is

an important aspect for everyone like workers, stakeholders, financial institutions and

government organizations and it indicate the effectiveness and efficiency of a business entity

(Robin, Salim & Bloch, 2018; Abusharbeh, 2017; Evans et al., 2014; Mohanty, 2006; Duncan &

Elliott., 2004; Reddy, 2004; Lin & Piesse, 2004; Beck & Levine, 2004; Waddock & Graves,

1997; Griffin & Mahon, 1997).

Page 19

2

In the modern era, the financial performance of banks is measured through asset evaluation,

efficient risk management, offering the innovative financial product. Moreover, issuance of

secured loan, return on asset, return on investment, earning per share, dividend yield, sales, and

profitability, orientation on wealth maximization, return on capital employed, wealth creation for

shareholders, and market value of shares are also considered important yardstick for the

valuation of banks (Bektas & Kaymak, 2009; Makni, Francoeur, & Bellavance, 2009; Gilbert &

Wheelock, 2007; Mishra & Suar, 2010; Agle et al., 1999; Fowler & Schmidt, 1988;

Govindarajan, 1984). Although financial performance remains vital, however non-financial

performance is also significant that affect the stakeholder‟s perceptions about an entity. Financial

performance remains exceptional, however due to rising competitive pressure; organizations are

focusing on non-economic aspects of business which remain material in long run. Non-financial

performance reflects the going concerns and long term sustainability of a business. Although it

seems subjective, however, its long term effects are objective and definite. It is operationalized

by using the measures of a number of employees, customer satisfaction, good customer dealing,

workplace relations; new product development, cost reduction programs, research and

development, personal development, ensuring employee health and safety (Govindarajan, 1984;

Hoque, 2004; Seiford & Zhu, 1999).

Financial performance is an integral part of the financial sector's planning and development. A

number of researchers examined positive relation between financial performance and economic

development, and a negative association between financial distress and economic development

(Muyambiri & Odhiambo, 2018; Musamali et al., 2014; Skare & Golja, 2014; Ekmekcioglu,

2012; Caprio & Levine, 1994). As global financial environment change rapidly, therefore

governments, regulators, managers, and investors are more concerned about banks performance

Page 20

3

as well as their working practices (Khan et al., 2017). Particularly, financial performance in the

context of banking remains more pragmatic and exceptional because the spillover effect of banks

financial instability leads toward other sectors of society. Therefore generally all entities,

however particularly banks remain more sensitive and proactive towards meeting their financial

goals.

The sound financial and non-financial performance positively affects the behavior of stakeholder

and increases the chances of customer retention. Past studies proclaimed various potential

determinants of financial and non-financial performance. Studies have been conducted in

different context and remain consistent in this opinion that financial and non-financial

performance is being determined by micro and macro-economic factors. Various

macro/microeconomic factors influence financial performance of banks. The gross domestic

product, inflation, operating cost efficiency, bank size, risk, and liquidity positively influence the

bank‟s financial performance while there is the negative impact of capital adequacy and

exchange rates on the bank performance (Elyor, 2009; Uzhegova, 2010; Kamau, 2009;

Heffernan & Fu, 2010). Financial innovation contributes to economic development (Schumpeter,

2013). Innovative companies have a competitive edge in this rapidly changing market

environment than its competitors having the low pace of innovation. Therefore, innovation is

also pivotal to signify the organizational performance (Abdulai Mahmoud & Hinson, 2012;

Gonzalez-Ramos et al., 2014). The companies which remain famous for innovation are

considered good companies (Padgett & Moura-Leite, 2012). According to past studies, the good

company means with a good reputation, so innovation remains a potential determinant to reflect

in entities' reputation in today's dynamic market environment (Anser et al., 2018; Padgett &

Moura-Leite, 2012; Padgett & Galan, 2010; Wagner, 2010).

Page 21

4

Studies expounded in past literature, advocate that company reputation is a potential determinant

of financial performance (Deephouse, Li & Newburry, 2009; Gardberg, 2006). Most of the

stakeholder believes that high returns are induced from companies having good reputation. The

firm reputation is a rare and inimitable resource of an entity which further result into competitive

advantage and improved organizational performance (Rindova et al., 2005; Roberts & Dowling,

2002; Barney, 1991). However, there is limited empirical evidence which devotes their efforts to

determine how corporate reputation affects organizational performance. Besides affecting

organizational performance, corporate reputation is also robust to affect stakeholder's perception

(Gatzert, 2015; Maden et al., 2012). It is the image of the organization in the mind of stakeholder

to decide to interact with an entity. Most of the economic contracts are earned on the basis of

corporate reputation.

Therefore, the extending this notion, it will be thought-provoking to investigate that how and to

what extent corporate reputation derive financial performance (Gatzert, 2015; Maden et al.,

2012; Alniacik, Alniacik & Erdogmus, 2012). Moreover, it is also important to study that how

corporate reputation is built over time by the organizations and what are the factors which

composite a favorable reputation in the mind of stakeholder. Last couple of years have witnessed

the surge of social and environmental activism and it is demanded by stakeholder that

organizations should meet the goal of long term sustainability and environmental preservation.

Though literature revealed various antecedents of corporate reputation, however corporate social

responsibility (CSR) is integral determinant (Choongo, 2017; Crifo et al., 2016; Lee & Jung,

2016; Gatsi et al., 2016; Famiyeh et al., 2016; Elouidani & Zoubir, 2015).

Corporations are legal entities, whose major responsibilities to earn a profit, maximize

shareholder wealth, and also contribute to society by enhancing value-added activities. These

Page 22

5

entities establish a corporate agenda with clearly indicating their social role which reveal them as

good citizens. Carroll (1999, 1979) suggested that CSR is operationalized into four categories,

which includes economic, legal, ethical, and philanthropic. Among all economic part of CSR

plays a vital role in organization's performance and helps the stakeholder to analyze important

economic factor, make strategic planning, manage operations of banks, earn profits and

maximize shareholder wealth (Young & Thyil, 2009; Decker & Sale, 2009; Manne & Wallich

1972; Crowther & Aras, 2008). CSR is strictly voluntary action which provides the basis of

legitimacy to operate in the society and fulfill the expectation of various stockholders. It leads to

reduce the information risk and check whether the organization is on right track and fulfill its

obligations. Consequently, it is argued that all these favorable results can have an effect on the

financial performance of a corporation, such as return on sale and return on investment (Peloza

& Shang 2011; McWilliams, Siegel & Teoh, 1999).

Economic responsibility is full filled by focusing on financial innovation. In competitive

environment, financial institutions needs to modify existing structures, generate new

opportunities through effective risk management, developing and introducing new products, that

helps to generate income, earn profit and wealth maximization (Lentner, Szegedi & Tatay, 2015;

Decker & Sale, 2009; Garriga & Mele, 2004; Carroll, 1991). Legal responsibilities are

considered the second cornerstone of CSR which described the country's legal system and it is

more important for financial institutions.

The regulators define rules which purpose is to reduce the risk, ensure security, and enhanced

customer confidence in the financial system. The supervisory agencies and trade associations

prepared rules for implementation and compliance. The basic purpose of these rules is to ensure

social responsibility in corporate activities to safeguard customer‟s stake, reduce frauds and

Page 23

6

ensure the safety of customer's assets (Lentner, Szegedi & Tatay, 2015; Decker & Sale, 2009;

Carroll, 1991). But it was found that the legal system of developed countries is more appropriate

in comparison of developing counties (Sood & Arora, 2006; Chapple & Moon, 2005; Arora &

Puranink, 2004).

Ethical responsibility comprised fair, impartial and smart working environment. Ethical norms

are interpreted with individual integrity and fulfillment of stakeholder‟s expectations. It

represents the fundamental ethical principles of moralities, which is in line with confidence and

is linked to the financial sector (Decker & Sale, 2009; Carroll, 2004). Business ethics based on

principles of integrity, fair conduct, respect, and transparency in the financial sector, are in

accordance with the host country's environment. So, there is need to consider, ethical values and

expectations which communicating in the context of stakeholder perspective (Lentner, Szegedi &

Tatay, 2015; Decker & Sale, 2009; Carroll, 1994).

Philanthropic responsibility is an important element of CSR. In philanthropy, the organizations

voluntarily try to improve the social life of the people through building parks, clean water

projects, making shelter homes, and helping poor persons etc. (Crane & Matten, 2007). Today's

philanthropy helps the banking sector in enhancing good reputation and global corporate

citizenship (Lentner, Szegedi & Tatay, 2015; Decker & Sale, 2009; Carroll, 1994; Carroll, 1991).

In recent years, modern researchers examined that the level of social expectations from the

banking industry was changed. CSR activities are considered integral for the survival of the

banking industry so that they can meet the expectations of stakeholder other than wealth

maximization. This context of corporate social responsibility and financial performance is

supported by multiple theories which include stakeholder theory, social identity theory,

Page 24

7

legitimacy theory, and consumer inference making theory (Pirsch, Gupta & Grau, 2007; Porter &

Kramer, 2002).

Classical theories of finance support the concept of shareholder's theory, which proposed that

main organizational objectives are to maximize the shareholder wealth (Friedman, 1970).

Besides this main objective, societal and other stakeholder's interests should not be compromised

(Crane et al., 2008). Stakeholder theory explained that an organization should consider

stakeholder perspective while making a corporate decision (Barnett & Salomon, 2012). These

stakeholders influence the organizational performance directly and indirectly, so dissatisfaction

of any stakeholder can adversely affect the business performance (Delmas & Toffel, 2008;

Henriques & Sadorsky, 1999; Clarkson, 1995).

Stakeholder theory supports to stakeholders or individuals who influence or influenced by the

corporate strategies or practices. Management is considered to respond the stakeholder concerns

because the main function of managers is to meet the stakeholder's expectations effectively.

Emshoff and Freeman (1978) proposed that organizational objectives should be aligned with

stakeholder‟s expectations. Considering stakeholders expectations while making corporate

decision reflect conventional reputation in the mind of stakeholders. This stakeholder context

explained the notion that consideration of stakeholders interests can lead toward influencing the

organizational performance.

1.2 Contextual Analysis:

Financial sector comprises banks, leasing companies, insurance, investment companies, asset

management companies, Mudarbah, and mutual funds etc. But among all these institutions, the

banking sector of Pakistan comprises 95% of the total financial market and therefore it is

Page 25

8

considered an integral part of the economy (SBP, 2016). It plays an important role in the

prosperity of the economy, while a weak banking sector leads toward financial crisis and it is

dangerous for sustainability of the economy (Herwartz & Walle, 2014; Hsueh, Hu & Tu, 2013).

Therefore, its performance significantly impacts the economy of Pakistan indirectly and

investors stakes directly. But it was found that banking sector of Pakistan is not as performing as

performed by the banking sector of developed countries due to the requirement of the strict

legitimate system (Yamak & Suer, 2005).

In the context of developing counties especially, Pakistan is ranked as the sixth most populated

country in the world and forty-third largest countries in terms of its GDP. In recent years the

banking industry of Pakistan has flourished at a significant level. According to the State Bank of

Pakistan (SBP), the banking industry of Pakistan comprises more than thirty-four scheduled

banks, including four foreign banks and consists of around 12,993 branches with thousands of

ATM‟s (SBP, 2017).

The rapid growth of the banking industry of Pakistan plays a significant role in driving the

growth of the economy (SBP, 2017). The increasing number of national and international banks

reflects tough competition in the banking industry. It is more customers centric with the intention

to earn more profit and maximize shareholder wealth. Banks use modern marketing techniques to

generate customer intention, instead of only improving their performance. In the era of

technological advances and the competitive market, the banking sector has expanded its borders,

such as Islamic, mobile banking and Internet banking, etc. The findings and analysis of historical

investigations, there are different methods of marketing for survival, improvements and

enhanced performance in a tough competition of services industry (Poolthong & Mandhachitara,

Page 26

9

2009). There are different sort of and challenges which the banking industry is facing in

developing economies specifically in Pakistan.

There is a need to improve the corporate governance structure of the banking sector because all

the business strategies are established be corporate managers. Weak governance system leads

toward the numerous frauds, embezzlement cases, excessive leveraging, and risky investments

etc. Banking sector associated with the interest of depositors and investors. They want to make

sure, either their money is invested in less risky, secured, and beneficial projects. Shareholders,

lenders, borrowers, managers, employees, and regulators are other stakeholders of banks. As

compared to other industries, there is comparatively number of stakeholders associated with the

banking industry. It leads toward more complicated information asymmetry. So, there is a need

to improve and establish strict compliance and regulation systems (Yamak & Suer, 2005).

Corporate social responsibility context gaining dominance in modern era in Pakistan (Khan,

2015; Qazi, Ahmed, Kashif, & Qureshi, 2015). Somehow, at corporate level, CSR is mixed with

philanthropic or charitable context. It is found that up to some extent, corporate managers are not

aware off with their social responsibilities (Khan, 2015; Waheed, 2005). Evidence founded that

corporate managers are not so interested to understand the true context of CSR while on the other

hand, there is lack of systematically and formal procedure to train and guide top management

regarding their social responsibilities (Ehsan & Kaleem, 2012). Studies highlighted that extra

working hours, less safety measures, lower level of awareness regarding regulations and non-

compliance of regulations (Kamal et al., 2012; Pasha & liesivuori, 2003).

In the banking sector, besides the short-term internal business interests of financial companies,

social, environmental and human rights objectives are gaining a dominant and interesting role. In

Page 27

10

this perspective, engagement in socially responsible activities can serve as a strategic tool for a

firm‟s to avail competitive edge (McWillians & Siegel, 2000; Porter & Kramer, 2007). Corporate

social responsibility practices in the context of financial benefit remain more robust because

financial institutions play a social role by mobilizing the financial resources in the society. CSR

in the context of the banking sector not only result in competitive advantage but also result in

superior financial performance.

Page 28

11

1.3 Rationale of the Study:

On the basis of extensive literature review, there are certain gaps which have been deduced and

being filed by this study. First of all, historical studies have broadly conducted and literature

posit that studies relevant to CSR and its consequences conducted in the context of developed

economies (Gangi, Mustilli & Varrone, 2018; Lentner, Szegedi & Tatay, 2015; Chiu, 2014;

Decker & Sale, 2009). Therefore due to divergent governance intra-structure, their findings

cannot be generalized in the context of developing economies, particularly for Pakistan. There is

limited empirical evidence in the context of developing economies to determine the quest of CSR

(Ip, 2008). Moreover, CSR practices in developed countries remain divergent than developing

economies (Gao, 2011; Belal, 2001). However past studies in the context of developing

economies provide limited empirical evidence that how and to what extent CSR affects firm

performance (Nyeadi, Ibrahim & Sare, 2018; Choongo, 2017; Crifo et al., 2016; Lee & Jung,

2016; Gatsi et al., 2016).

Historical studies in developing economies have limited scope and based on self-reported

questionnaires. Most of the studies focused on secondary data analysis. Studies only explored the

relationship between CSR and firm performance with a limited number of samples. Non-

financial parameters are necessary that has ignored in current literature (Mishra & Suar, 2010).

Similarly, past studies have not effectively examined the potential significance of non-financial

parameters in context of banking sector. There are few evidences among the relation of CSR and

performance which have demonstrated positive (Malik & Nadeem, 2014), negative (Iqbal et al.,

2013; Aga et al., 2012) and no relation (Kiran et al., 2015), which motivated for current research.

CSR‟ idea is now developing in the Pakistani context, and in addition some analysts carried out

research work in non-financial sector by overlooking the financial sector, especially in the oil

Page 29

12

and gas sector (Kiran et al., 2015), KSE 100 index non-financial sector (Javed et al., 2013),

textile, cement, chemical, tobacco, and pharmaceutical industries (Iqbal et al., 2012; Kakakhel et

al., 2015; Jan & Baloch, 2011), but no evidence found in context of banking sector of Pakistan.

Stakeholder pressure is a recommended as a moderator which never tested earlier (Haleem et al.,

2015). Innovation and corporate reputation could establish the relationship between CSR and

performance. There is no evidence of sequential mediation of innovation and reputation between

CSR and performance. There is the significant role of CSR in determining performance and it

motivated to examine the relationship of CSR and performance in the banking industry of

Pakistan. Moreover, current study leads to validate the theoretical assumptions of stakeholder

theory. Therefore, considering all these potential GAPS, this study aim is to examine CSR-FP,

NFP, and stakeholder pressure as moderating factor, innovation and corporate reputation as

mediating factors in context of Pakistan.

Page 30

13

1.4 Problem Statement:

In developed market economies, financial institutions give more importance to corporate social

responsibility. As they think, their CSR is considered an important factor, like others that helps

them in enhancing profit that resulted in the maximization of shareholder's wealth. They

considered that financial literacy and awareness, financial education, responsible, prudent

lending, risk management, fair and transparent financial services, handling of complaints are

important elements which improve business operations and to get the intention of stakeholders

(Lentner, Szegedi & Tatay, 2015). In essence, a bank‟s stable financial position, increasing

economic performance, ethical and transparent activities, and responsible financial services

ensure its predictable and reliable operations. It is evident of fact that effective implementation

of CSR activities enabled the banking industry to reduce the chances of frauds, embezzlement

cases, excessive leveraging, and risky investments etc.

In banks, besides the short-term internal business interests of entities, social, environmental, and

human rights objectives are gaining a dominant and increasing role (Lentner, Szegedi & Tatay,

2015; Chiu, 2014; Audretsch & Lehmann, 2004). There is an increase in a number of

stakeholders, who think that business decision making must go beyond profit maximization and

it is required to involve in socially responsible activities to solve social issues. Such activities are

far away from their economic interest but included as moral responsibility (Chiu, 2014).

As in developed countries, the banking industry contributing significant role to resolve financial,

economic and social issues. There is significant importance of banking industries in developing

and emerging economies especially in Pakistan. But this industry is facing challenges like

numerous frauds, embezzlement cases, excessive leveraging, and risky investments etc. The

Page 31

14

expectations of the stakeholders include safe products and adequate information. Employees

need a safe and motivating work environment that must be separate from discrimination. In

addition, there is a need for care with the respect and dignity of employees. Furthermore, the

banking sector must be aware of indirect environmental impacts, such as lending activities to

environmentally friendly organizations (Lentner, Szegedi & Tatay, 2015; Hu & Scholtens, 2014;

Chiu, 2014; Branco & Rodrigues, 2008; Scholtens, 2009; Douglas, Doris, & Johnson, 2004.

In developed economies, it is evident that corporate social responsibility contributes to a

significant role in economic development. Moreover, CSR plays an integral role in determining

the financial benefits of financial institutions, because it has a direct link with customer

satisfaction. If clients of any banks are satisfied and feel secure about their investments, they will

lead toward publicity of that banks and repeated association and the long-term relationship will

be established. According to researchers, there are limited evidences on corporate social

responsibility in banking sector of developing counties (Choongo, 2017; Crifo et al., 2016; Lee

& Jung, 2016; Gatsi et al., 2016; Famiyeh et al., 2016; Kilic et al., 2015; Siregar & Bachtiar,

2010; Monteiro & Aibar Guzmán, 2010; Cormier & Gordon, 2001). This evident that corporate

social responsibility plays important role in determining bank performance and it convinced to

examine the relationship between CSR and performance in the banking industry of Pakistan.

Page 32

15

1.5 Research Questions:

1.6 Research Objectives:

Page 33

16

1.7 Significance of the study:

This study examined the influence of corporate social responsibility on the financial and non-

financial performance of the banking sector of Pakistan. Findings of this study are significantly

beneficial to academicians focusing on CSR research studies. It is a contribution to existing

knowledge with the addition to the literature. This study is beneficial to businessmen, managerial

personnel and investors who are concerned with the impact of CSR on firms' financial

performance. It will support to regulators in establishing socially responsible policies keeping in

mind the expectations of stakeholders (Kilic et al., 2015; Lentner, Szegedi & Tatay, 2015; Chiu,

2014; Decker & Sale, 2009).

Most importantly, this study will be beneficial to bankers in developing and introducing financial

products and services keeping in mind the customer‟s interests (Fernando, 2007; Rathnasiri,

2003). The finding and implication of this research will be beneficial to local organizations as

they deal with CSR as a vital segment of the business. Furthermore, it is beneficial to

international organizations as they are making an investment that might crop up as a result of

CPEC etc., to utilize the benefit of developing consumer markets. This study will contribute in

multiple ways to the existing literature and it is a study which is considering both aspects of

financial and non-financial performance in developing countries.

Page 34

17

CHAPTER 2

LITERATURE REVIEW

2.1 Introduction

The objective of this chapter is to review theoretical and practical aspects of CSR literature

covering the objective and philosophy of CSR, empirical studies related to financial verses non-

financial performance of the firms. In addition, historical and current studies on innovation,

corporate reputation, and stakeholder pressure were examined. The main objective of this chapter

is threefold. Firstly, it explained multiple concepts of CSR, financial and non-financial

performance, corporate reputation, innovation, and stakeholder pressure. Secondly, it examined

the relationship between CSR, financial and non-financial performance. Thirdly, it addressed the

CSR performance in the banking sector of Pakistan and the rest of the world. In this section,

literature reviewed and final research gap found which leads toward examining different direct

and indirect relationships.

2.2 Literature Search Strategy

Literature review was based on numerous sources (journals and books), publishers (science

direct, Wiley, Taylor and Francis, sage, emerald, Elsevier), indexing bodies (Thomson Reuter,

Scopus, Proquest, Ulrich), Google scholar and local and foreign dissertations. Recent research

publications were focused for literature review but the theoretical context was covered since the

emergence of theory and basic concepts.

2.3 Corporate Social Responsibility

Many years have passed to investigate CSR and multiple experts, analysts, and researchers are

defining CSR in their own way (McWilliams, Siegel, & Wright, 2006). The evolution in the

Page 35

18

definitions was noticed when thoughts of the multiple researchers are considered. Davis (1973)

described that CSR started with the end of legal obligations. This was a step more than good

citizenship that for society's welfare. CSR was considered to be socially responsible besides legal

responsibility. Gomez (2014) illuminated the social responsibility of the university that other

researchers ignored. Lauesen (2016) explored the question of whether CSR can be used as a

relationship of trust between companies and society, and which part of CSR plays a better role in

organizations.

CSR was the scarification of maximization of profits over being responsible for societal well-

being. It was considered as subjective concept and source of extensive research and arguments

from last few years (Jamali, 2008). European commission defined it as deliberate interaction

between social, environmental activities and interaction with their stakeholders. Friedman (1970)

supported the above arguments and proposed it as a source of agency problem between managers

and stakeholders. It was further examined that CSR is utilized for personal career development

by managers.

Shareholder wealth maximization was the main goal of any business, but social development

activities are gaining momentum in the business. In spite of the fact that, organizations were

observed to be involved in some type of social exercises during the nineteenth century after the

industrial revolution (Maden et al., 2012); however the topic of the impact of CSR on financial

and economic performance have empowered the scholastic and business interests. Socially

responsible organization‟s demand was increasing as they need to meet the multifarious needs of

shareholders as well as stakeholders (Aguinis & Glavas, 2012). CSR was a common part of

corporate entities and organizations are now assigning senior management for discussion on CSR

Page 36

19

issues which coordinate the curriculum of business administration goals relent to social activities

(Montiel & Delgado-Ceballos, 2014).

Organizations were presently incorporating the CSR with their plans of action and working

structures since they outlined a procedure for expanding benefit through self-intrigue (Servaes &

Tamayo, 2013). In the time of globalization, they additionally needed to contend

incomprehensibly (Surroca, Tribo & Zahra, 2013), restoration on the reputational crisis,

mechanical progression (Avram & Avalsilcai, 2014), expanding concerns of environmental

safety and ecological sustainability. There were various ideas of CSR, despite these energetic

social interests by business firms.

CSR has multiple concepts with respect to people, constructs, and researchers are not agreed on a

common definition (Saeidi et al., 2015). The absence of a union, definitional agreement, and

hypothetical development was not allowed to develop a common definition. A universal

understanding of the definition, development and wide acceptance of the concept was essentially

inevitable. CSR considered as a common ideology in existing literature which explained the

method of wealth creation for stockholders relatively stakeholders (Peloza & Shang, 2011).

According to the off-shoot concept, CSR defined as an arrangement of setting particular

corporate activities and approaches that coordinate the stakeholder's expectations and economic,

social, and environmental performance (Aguinis & Glavas, 2012). As per existing gap on CSR

definition and historical researches, it was acknowledged for research on CSR as deliberate

business firm activity coordinated toward enhancing the economic, social, ethical and legal

business activities which influence the organizational performance (Okoye, 2009).

Page 37

20

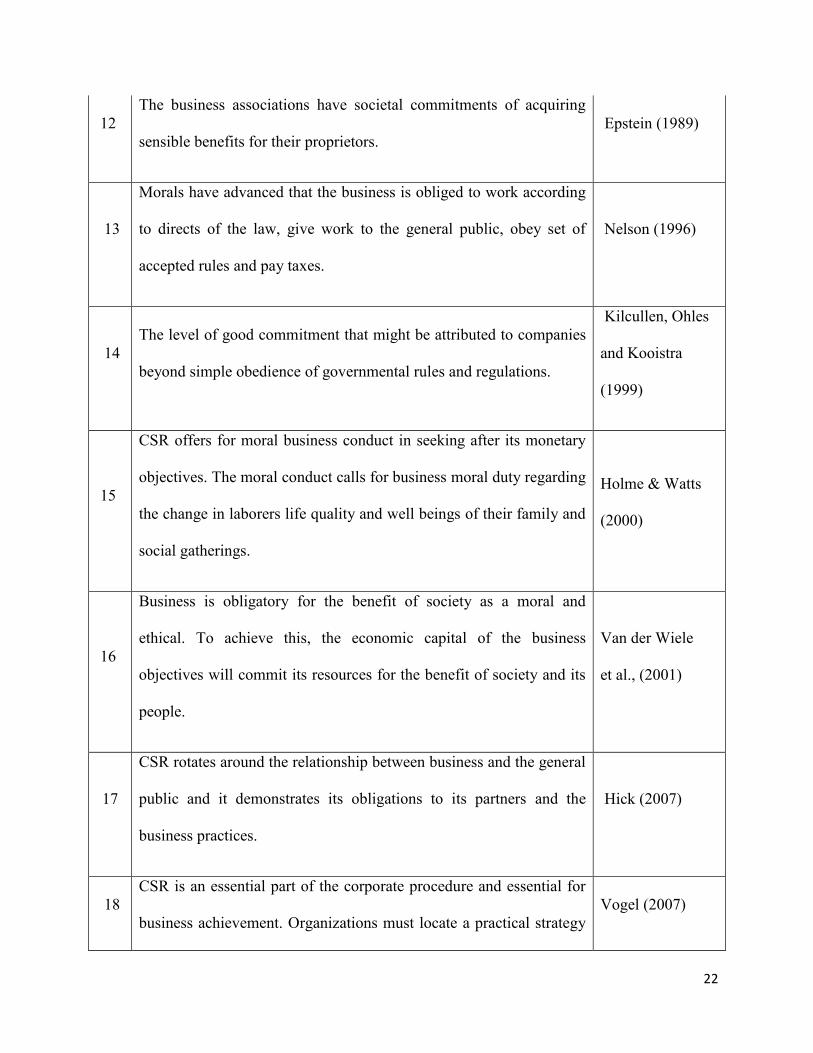

Table 2.1.1.1: Evolving definitions of CSR

Sr.

No

Definitions of CSR Reference

1

The monetary motivation behind the presence of any business

organization is an intensification of benefit. This objective is

accomplished through the acknowledgment of social measurement

that is consumer loyalty. Accordingly, social security and social

wellbeing of any modern culture are one of the necessary factors

organization's duties other than its financial matters targets.

Drucker (1942)

2

The goal of any organization ultimately is survival that is the result of

amicability between the framework and the general population

places. Any conflict between these three players' intuitive

destinations is located in the central business position. In this way,

human labor dignity, status, and workers' training and development

are considered the asset of the company's.

Drucker (1946)

3

The main question of the society, we want a big business but we do

not know what you expect out of it? This means how organizations

are going to ensure their organizational goal of maximization of

profits to serve the aspirations and demands of society as well? To

ensure an equal balance between profit maximization and high

employment as social contributions, government administration

should clearly mention the controlling policies over it.

Drucker (1946)

Page 38

21

4

Businesses are bound to follow policies and decisions which are

necessary for the social values of any society.

Bowen and

Howard (1953)

5

Business will not be limited to corporate interests‟ implementation of

firm policies only, but should also cater for social and legal aspects as

well.

Davis (1960)

6

CSR could not be limited only to economic and legal responsibilities

but societal obligations must be incorporated.

McGuire (1963)

7

CSR is a response to a firm‟s technical and economic issues beyond

legal requirements.

Davis (1973)

8

This "fit" between the business communities' expectations and

business ethics.

Zenisek (1979)

9

Social responsibility is set to operate within complex business

organizations society's economic, legal, ethical and philanthropic

expectations.

Carroll (1979)

10

The distributing a portion of corporate organization is to need

people's needs with master capacities, continue reacting to the

business focus, make quality items in any event possible cost by

compelling and practical use of benefits.

Vogel and

Bradshaw (1981)

11

Philanthropy, responsibility, and policy are three main corporate

levels of any large organization.

Vogel and

Bradshaw (1981)

Page 39

22

12

The business associations have societal commitments of acquiring

sensible benefits for their proprietors.

Epstein (1989)

13

Morals have advanced that the business is obliged to work according

to directs of the law, give work to the general public, obey set of

accepted rules and pay taxes.

Nelson (1996)

14

The level of good commitment that might be attributed to companies

beyond simple obedience of governmental rules and regulations.

Kilcullen, Ohles

and Kooistra

(1999)

15

CSR offers for moral business conduct in seeking after its monetary

objectives. The moral conduct calls for business moral duty regarding

the change in laborers life quality and well beings of their family and

social gatherings.

Holme & Watts

(2000)

16

Business is obligatory for the benefit of society as a moral and

ethical. To achieve this, the economic capital of the business

objectives will commit its resources for the benefit of society and its

people.

Van der Wiele

et al., (2001)

17

CSR rotates around the relationship between business and the general

public and it demonstrates its obligations to its partners and the

business practices.

Hick (2007)

18

CSR is an essential part of the corporate procedure and essential for

business achievement. Organizations must locate a practical strategy

Vogel (2007)

Page 40

23

between what is social, ethically and economically profitable.

19

Kotler holds the view that a firm, other than fulfilling prompt needs

and wants of an objective market, should likewise convey an

incentive to the client that keeps up or boosts buyers and social

prosperity for a long period of time.

Kotler and

Armstrong (2008)

20

CSR is a deliberate business firm activity coordinated toward

enhancing the economic, social, ethical and legal business activities

which influence the organizational performance.

Okoye (2009)

21

CSR identifies with non-benefit exercises of partnerships executed

for the welfare of groups beyond their monetary advantages.

Carroll and

Shabana (2010)

22

CSR is a common ideology which explains the method of wealth

creation for stockholders relatively stakeholders.

Peloza and Shang

(2011)

23

CSR could be defined as an arrangement of setting particular

corporate activities and approaches that coordinate the stakeholder‟s

expectations and economic, social and environmental performance.

Aguinis and

Glavas (2012)

24

CSR is normally related as a way to deal with coordinate social and

environmental aspects into corporate exercises.

Baumgartner

(2014)

Page 41

24

2.4 Dimensions of CSR

Numerous measurements of the CSR were considered as satisfactory for research considerations.

The early conceptualization of CSR was the generous point of view whereby business firms

make altruistic gifts or commitments to the general public (Caroll, 1991). The associations that

make such corporate commitments including banks do open up such demonstrations of liberality

in their distributed information to attract open regard for them in order to accumulate support and

authenticity.

Carroll (1991) proposed that all the dimensions are integrated and could not anyone be

considered as mutually exclusive. CSR framework incorporated the all concepts and definitions

of CSR, corporate citizenship and stakeholder theory during this time period (Carroll, 1979, 1999

& 2004). He divided these responsibilities into four subparts like economic, legal, ethical and

philanthropic. Having a structure and order to the social and moral responsibilities of business

partners around the world was a fundamental best practice. The Pyramid of worldwide CSR was

considered as an attractive method to deal with graphically depicted the four sorts of social

commitment that the organization has concerns about overall stakeholders. The pyramid

delineates the four sections of overall CSR, beginning with the basic building square of financial

performance. Meanwhile, business depended upon to agree to the law since the law is each

nation's codification of adequate and unsatisfactory activities and practices (Carroll, 2004).

Moral and ethical aspects were commercially dependent on business. At its core level, it is

dedicated to reducing stakeholder's loss by opting correct choices. Lastly, policies of acceptable

social and philanthropic activities should be adopted for corporate citizenship. Today, the

Page 42

25

organizations are relying on to collect money and to "give back" to support financial and human

labor resources, so that personal satisfaction can be improved and supported (Carroll, 1999).

Picture-I, Carroll’s (1991), CSR-Pyramid

Economic activities referred to the factors of production to meet consumer market' demand

(Garriga & Mele, 2004). The firm's financial commitments, regardless of whether or not the

world around it is considered as a foundation for business. The overall organizations were

dependent on each other and they offer them an advantage in making ventures. The key sound

organization offers rules on how and where it can be refined in a general environment. At this

level, the agreement is definitely necessary, but the activities related to the money of the

commercial companies are difficult to achieve. What may change according to the nation or

place in the world is the issue of what constitutes a satisfactory rate of return or rate of

development (Carroll, 1999). Associations working in critical situations may consider this issue

remarkably opposed to those working in developed countries. Subsequently, this part of the

structure depends on the neighborhood and regional goals found in financial markets, but they

are still fundamental for survival and advancement (Carroll, 2004).

Page 43

26

The legal responsibilities involve the activities executed in the legal system of the country and

more important for multinational companies. Those countries that have well supported financial

systems will definitely apply legitimate systems. The social contract between commercial

companies and host countries varies by country and, in this sense, legal systems and

responsibilities also vary. At this level, we observe critical differences in honest systems and

commitments with those of kindness on the part of the countries and local regions of the world.

For example, we understand that Chinese labor laws are not executed routinely and that outside

financial professionals are observing that China's legal structure resolves some disputes. We also

realized that the absence of a legitimate framework is repressing remote post-war interest in Iraq

(Dolven, 2003). One thing is clear, however: legitimate duty exists and is found similarly in

developed, emerging, developing and similar underdeveloped nations (King, 2003).

Ethical obligations comprise fair, just and accurately working (Gregory & Mayell, 2004). Ethical

responsibilities deal with those undertakings and practices that are general or repudiated by

society, regardless of whether these principles are not organized (Carroll, 2004). In fact, around

the world, business ethics based on the country's ethical instructions, host country; and the

commitment to the quality. The act of good relativism, in which organizations basically conform

to neighborhood standards, creates a circumstance that is regularly unsustainable in light of the

fact that many nations, especially those that are creating, do not have verbal ethical measures that

guarantee the helpless fire. Ethical universalism as a norm that would establish an ethical

standard recognized by all cultures (Carroll, 2004). The ethical universalism was the

recognizable test of ethical points of reference that would have broad global support, for

example, the United States Global Compact or the Global Reporting Initiative.

Page 44

27

In Philanthropic responsibilities, social work included work to ensure the better quality of social

life (Crane & Matten, 2007). These responsibilities reflected the wishes of society around the

world that companies should participate in social exercises that cannot be ordered by law. The

fact is that it is sometimes handled with a moral chain of social practices. Today's philanthropy

is, as a rule, key in nature, with anticipated businesses that would assume a dynamic part in

global corporate citizenship (Carroll, 1991). As a result of law and morality, philanthropic

desires usually change from one to another nation and will find the wishes of host nations.

Finland, for example, it is discovered that Finns do not respect philanthropy excessively in light

of the fact that in their framework, senior positions are considered by companies rather than to

deal with this type of desire to citizenship. Schwartz and Carroll (2003) merged later on, these

dimensions and provided three overlapping CSR categories because the philanthropic dimension

is not the official responsibility of any business (Lantos, 2001). Look picture I & II which

explains the (Schwartz and Carroll (2003) three domain approach.

Picture-II, Schwartz & Carroll, (2003), Three Domain Approach of CSR

The Global Pyramid of CSR and Performance will help organizational governing bodies to

consider the various stakeholders‟ wishes interconnected with their associations. It is important

Page 45

28

to understand that these duties necessarily to be implemented. Past studies supported that

administrators found the significance of their obligations as taking after this succession of needs:

financial, lawful, moral, and charitable (Aupperle, Carroll & Hatfield 1985).

2.5 Stakeholder Pressure

Many researchers included the customers, suppliers, employees, shareholders, the community,

and government in the category of stakeholders (Buysse & Verbeke 2003; Donaldson & Preston

1995; Freeman 1983; Henriques & Sadorsky 1999). Business strategies toward CSR were

improved from simply showing social responsibilities to internal and external organizational

environments which are associated with stakeholders. These are the forces which influence the

organizational performances in multiple ways. There is a direct impact of losing the interest of

these stakeholders on financial performance (Lee, 2008). Customers stop to purchase products,

shareholders prefer to sell its shares, and employees lose confidence in work and environmental

personnel go for sue (Wood, 1991). Organizational success and survival primarily based on

manager's abilities who want to create enough wealth and stakeholder's' satisfaction (Clarkson,

1995). He further depicted that if anyone from stakeholders ready to support the organization

then its performance will automatically improve.

Impact of stakeholder's based CSR on financial and non-performance could be understood with

help of different underpinning theories which validate the views, concepts and thoughts.

According to social identity theory, there is a direct impact of image and reputation of

organization on employee's self-image, loyalty, and sincerity. Organizational employees relevant

policies reflect the company's intention to fulfill their needs, the participation of employees in

Page 46

29

strategies and union relations, decision making, remuneration policy, better work environment,

employees eradication of child labor expose the practices of organizational CSR.

These proactive activities enhanced improvement in financial and non-financial performance. It

referred to as reputational component and responds as a glamorous power for potential workers

(Turban & Greening, 1997). Moral trustworthiness and positive responses from family and

companions adds to worker work fulfillment and lower job turnover (Riordan et al., 1997) on the

grounds that workers with higher confidence and inspiration will work all the more proficiently

and viable (Berman et al., 1999) and participate in improvement of organizational performance

(Koys, 2001). Valmohammadi, (2014) examined that employee-related CSR activities are

strongly correlated with organizational performance. Gbadamosi, (2016) conducted the study in

US-based banks for identifying CSR and financial performance. He proposed that governance,

diversity, and worker connection were emphatically identified with bookkeeping returns.

According to CIM theory, consumers prefer to purchase products of such like organization which

is socially responsible. So, it is a way of improving purchase intention and consumer goodwill

(Gildea, 1994). According to signaling theory, consumers prefer more products where there exist

information and communication asymmetry in between buyer and sellers. Consumers think that

warranty is an indication of higher product quality and reliability, so it is also an indication of

corporate citizenship (Boulding & Kirmani, 1993; Maignan & Ferrell, 2000).

Customers are also considered as part of stakeholder because CSR practices are impossible to

execute with them. Consumer loyalty can be characterized as a general assessment of the

consumer's aggregate purchasing and utilization which includes different products. Fornell et al.

(2006) expressed that consumer loyalty is perceived as a promoting technique and a key driver of

Page 47

30

organization long-run financial performance and market value (Gruca & Rego 2005).

Valmohammadi, (2014) examined that consumer-related CSR activities are significant and

positively participate in organizational performance.

Firms can improve their relationships with local and international investors by embracing

suitable corporate governance measures. After the financial crisis in all over the worlds, there is

given proper importance to secure the interest and rights of shareholders and investors. This

corporate governance embraces on the suitable financial and non-financial transparency with

legal and regulatory requirements, data frameworks, and the proper accessibility of information.

Investors prefer those organizations which actively participating in CSR related activities like

consulting shareholders' opinion in financial decisions, autonomous audits, and insider's trading

strategies. From above evidences, we can propose that appropriation of better corporate

governance's standards can improve organizational performance. Investors prefer those

corporations which are participating in better governance standards (Coombes & Watson, 2000).

Corporate governance positively contributed toward the financial performance of sector (Dahya

& McConnell, 2007; Black & Khanna, 2007).

Post liberalization decades giving much importance on health and safety, environmental

influences, social involvement, payment of living allowances both at home and within

organizations to outsourced suppliers. In the present ages, organizations are ensuring loyalty with

suppliers if they also make ensure in the eradication of child labor, moral acquisition in raw

material, following human right policies. There is inverse relation in CSR benchmarks and

financial performance of organizations if suppliers violate the CSR standards. In recent evidence,

the Indian carpet industry was banned by international purchasers due to child labor because

Page 48

31

international buyers prefer Rugmark certified firms (Mishra & Suar, 2010). So, we can say that

there is a relation in the CSR of suppliers and organization performance.

Organizations are involving in education, health and development programs for eradication of

poverty from the community. These corporations are performing CSR activities through public-

private partnerships, establishing welfare foundations and NGO's, in the empowerment of the

local community. Microsoft is offering quality educations in backward rural areas (Brugmann &

Prahalad, 2007). Hewlett Packard is offering sustainable livelihoods to women self-held groups

of India (Dunn & Yamashita, 2003). These community development programs are influencing

investors and stakeholders in way of investing, purchasing and motivations toward performance

developments. Valmohammadi, (2014) examined that community-related CSR activities are

participating in organizational performance. Gbadamosi, (2016) conducted a study in US-based

banks for identifying CSR and financial performance and he proposed that product and

community factors were negatively related to profits while study of (Yusoff and Adamu, 2016)

proposed a positive relationship with community-related CSR and performance.

From last few years, global environment protection departments are mounting pressure to follow

strict legislation and organizations are adopting proactive strategies for environmental and

societal development. Organizations are modifying the policies with respect to environmentally

friendly products and manufacturing procedures. Greenhouse and processing resources

developed following environment protection standards. Resource saving and recyclable

technology, efficient manufacturing systems, and management information systems are utilized

as key instruments for protection.

Page 49

32

Graafland, (2002) conducted a research study to analyze long-term reputations are affected by

short-term profit-making strategy. He depicted that today's globalization and growing dynamics

are forcing the organization to consider social and environmental factors stakeholders.

Valmohammadi, (2014) proposed that environment-related CSR activities are strongly related to

organizational performance. These environment protectants improve the organization

performance in way of profitability and growth (Russo & Fouts, 1997; Klassen & Mc Laughlin,

1996), reputation and financial performance (Gil et al., 2001). Yusoff and Adamu (2016)

proposed positive relationship among environment-related CSR and performance.

2.6 Corporate Reputation

Margolis and Walsh (2003) comment that many researches concentrated just on testing the

immediate relationship amongst CSR and firm performance, and concluded that only few

evidences found that are in support of direct relationship (Wood, 2010). Hence, keeping in mind

the main goal to acquire solid outcomes, powerful factors which are excluded and disregarded

should be considered and observationally analyzed. Three interconnected factors, consumer

loyalty, reputation, and feasible competitive edge, were incorporated into to acquire reliable

findings. Existing studies explained that consumer loyalty, reputation, and competitive edge are

connected with organizational performance. Studies on the relationship amongst reputation and

organizational performance demonstrated that financial advantages, as well as non-financial

benefits, are results of a decent reputation (Flatt & Kowalczyk, 2011).

Helm (2007) said that a corporation with decent credibility "is considered less dangerous than

corporations with low economic performance and less reputable corporation". From the financial

perspective, (Roberts & Dowling, 2002) has shown that the organizations with the best

Page 50

33

reputation offer good returns when investing in them. (Shamsie, 2003) proposed the direct and

positive effect of the best reputation on organizational performance. Finally, (Cabral, 2012)

ensures that organizational performance is based on its best reputation, and it is assumed that in

order to maintain overall reputation, organizations should focus on developing good

methodologies.

In the 21st century, development context is increasing as new corporate difficulties for

complexity, rapid competition, corporate direct promotion, and social responsibility. It has

threatened companies to worry about corporate reputation. It is expected that the performance of