Page 1

1

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

growth team m e m b e r s h i p™

Co-Sponsor

Improving Productivity and Customer Focus

americas

®

2012 sales leadership priorities survey results

TWEET ABOUT THE SURVEYS

#2012priorities

Page 2

2

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

CONTENTS

INTRO

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Survey Purpose and Respondents . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

What is the Growth Team Membership™ . . . . . . . . . . . . . . . . . . . . . . . . 5

Sales Leadership Overarching Challenges . . . . . . . . . . . . . . . . . . . . . . . . 6

Key Sales Leadership Challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7SECTION

1

Respondent Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25SECTION

4

Sales Leadership Resource Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11SECTION

2

Special Interest Topic: Tools and Social Media . . . . . . . . . . . . . . . . . . . . . . 17SECTION

3

Page 3

3

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Introduction

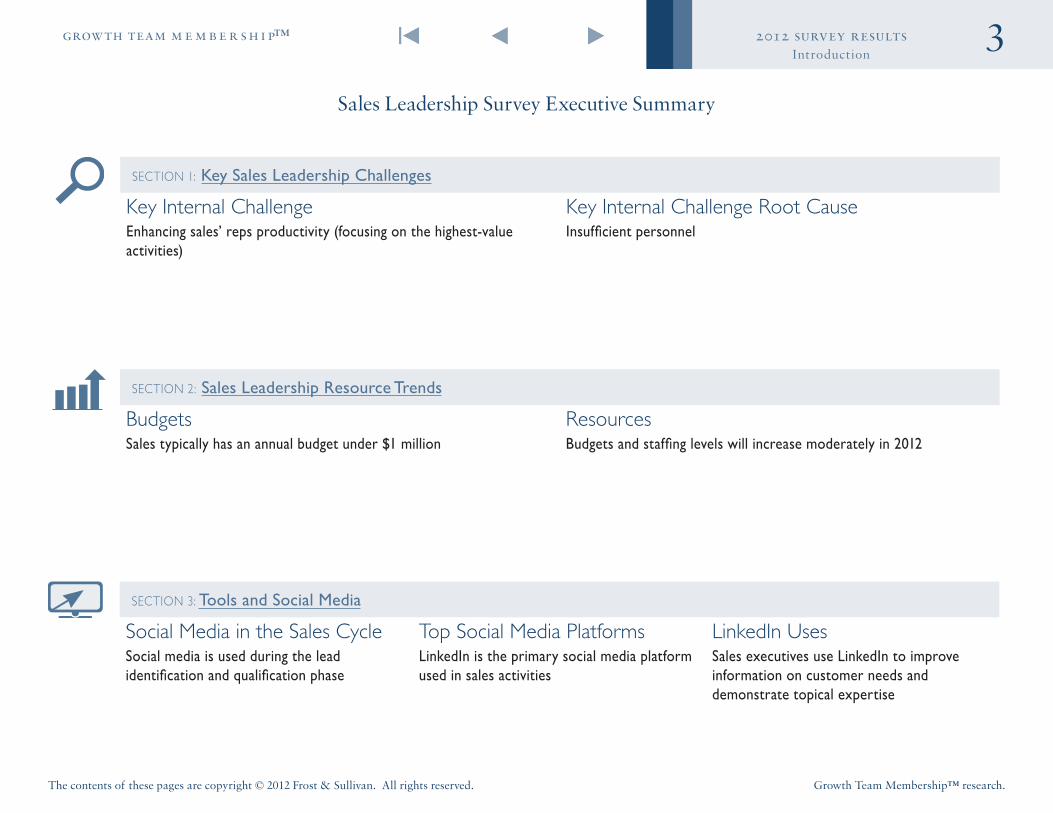

Sales Leadership Survey Executive Summary

SECTION 1: Key Sales Leadership Challenges

Key Internal Challenge Key Internal Challenge Root CauseEnhancing sales’ reps productivity (focusing on the highest-value activities)

Insufficient personnel

SECTION 2: Sales Leadership Resource Trends

Budgets ResourcesSales typically has an annual budget under $1 million Budgets and staffing levels will increase moderately in 2012

SECTION 3: Tools and Social Media

Social Media in the Sales Cycle Top Social Media Platforms LinkedIn UsesSocial media is used during the lead identification and qualification phase

LinkedIn is the primary social media platform used in sales activities

Sales executives use LinkedIn to improve information on customer needs and demonstrate topical expertise

Page 4

4

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Introduction

Survey Purpose and Respondents

Co-SponsorSurvey PopulationMethodologyResearch Objective

To understand the most pressing external and internal challenges shaping sales executives’ 2012 planning

Web-based survey platform Manager level and above sales executives from companies in North and South America

®

260survey

respondents

Page 5

5

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Introduction

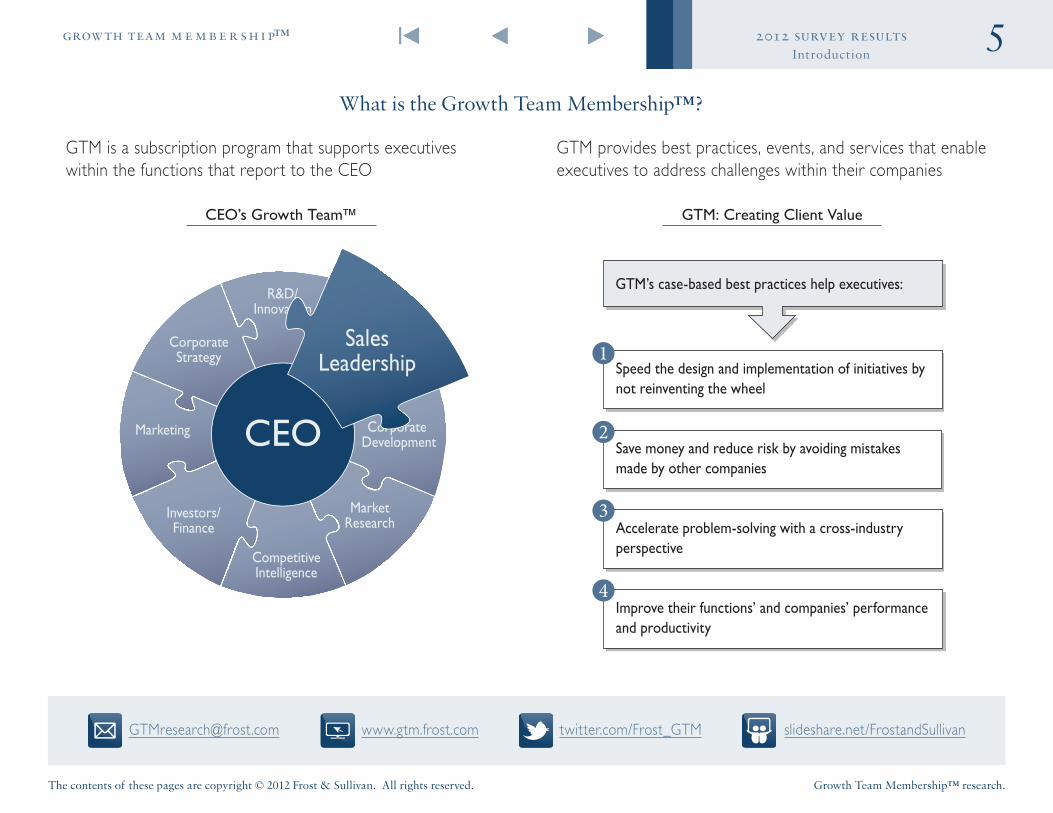

What is the Growth Team Membership™?

GTM is a subscription program that supports executives within the functions that report to the CEO

GTM provides best practices, events, and services that enable executives to address challenges within their companies

CorporateStrategy

Corporate Development

Marketing

CompetitiveIntelligence

MarketResearch

SalesLeadership

R&D/Innovation

Investors/Finance

CEO

SalesLeadership

CEO’s Growth Team™ GTM: Creating Client Value

GTM’s case-based best practices help executives:

Speed the design and implementation of initiatives by not reinventing the wheel

Save money and reduce risk by avoiding mistakes made by other companies

Accelerate problem-solving with a cross-industry perspective

Improve their functions’ and companies’ performance and productivity

[email protected] www.gtm.frost.com slideshare.net/FrostandSullivantwitter.com/Frost_GTM

Page 6

6

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Introduction

Sales Leadership Overarching Challenges Sample Solutions from GTM

What’s Keeping Sales Executives Up at Night in 2012?

Contact us at GTMResearch@frost .com .

Customer Focus

Sales executives must increase their familiarity with their clients so they can respond to the changes in their customers’ decision-making behavior and needs .

Learn how Tandberg made customer segmentation the foundation of its customer-centric business model .

Lead Generation Strategies

Sales executives are struggling with identifying and qualifying high-potential leads and need a strategy for improving the overall demand generation process .

Learn how Kronos developed a demand management strategy to provide Sales with high-quality, actionable leads.

Distribution Channel PartnersCompanies tend to rely heavily on distribution channels for sales. However, due to changes in customer purchasing behavior, Sales must ensure that distribution channels are still meeting its needs .

Learn how our Distribution Channel Optimization toolkit helps you evaluate your distribution channels’ ability to reach customers and differentiate your value proposition from the competition .

Page 7

7

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

INTRO

SECTION

1

SECTION

2

SECTION

4

SECTION

3

SECTION

1 Key Sales Leadership Challenges

Page 8

8

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 1

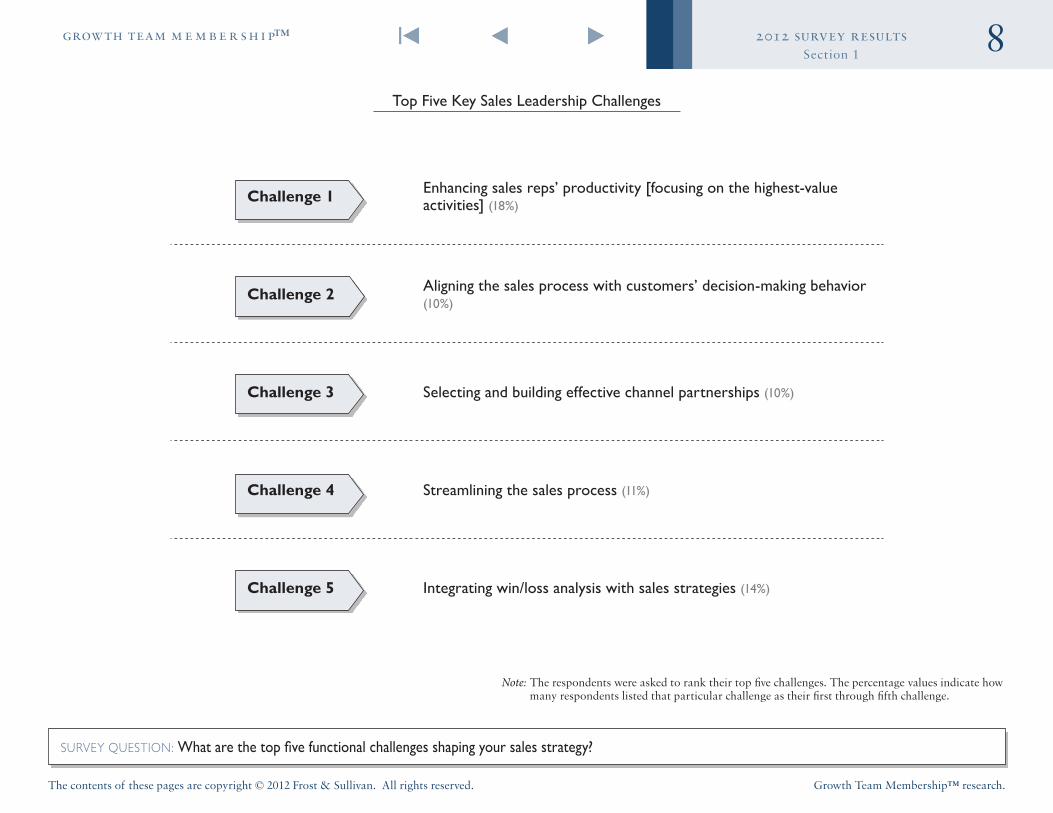

Challenge 1 Enhancing sales reps’ productivity [focusing on the highest-value activities] (18%)

Challenge 2 Aligning the sales process with customers’ decision-making behavior (10%)

Challenge 3 Selecting and building effective channel partnerships (10%)

Challenge 4 Streamlining the sales process (11%)

Challenge 5 Integrating win/loss analysis with sales strategies (14%)

Top Five Key Sales Leadership Challenges

SURVEY QUESTION: What are the top five functional challenges shaping your sales strategy?

Note: The respondents were asked to rank their top five challenges. The percentage values indicate how many respondents listed that particular challenge as their first through fifth challenge.

Page 9

9

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 1

Respondents in B-to-B companies are focused on productivity, while those in B-to-C companies are concerned with customer needs and behavior

Top Five Sales Leadership Challenges (By Business Model)

B-to-B B-to-C

Challenge 1 Enhancing sales reps’ productivity [focusing on the highest-value activities] (20%)

Implementing lead generation strategies (22%)

Challenge 2 Aligning the sales process with customers’ decision-making behavior (10%)

Responding to pricing pressures from competitors, the market, and customers (17%)

Challenge 3 Responding to pricing pressures from competitors, the market, and customers (10%)

Aligning the sales process with customers’ decision-making behavior (15%)

Challenge 4 Streamlining the sales process (11%)Identifying and responding to clients’ changing needs (20%)

Challenge 5 Integrating win/loss analysis with sales strategies (12%)

Integrating win/loss analysis with sales strategies (20%)

Note: The respondents were asked to rank their top five challenges. The percentage values indicate how many respondents listed that particular challenge as their first through fifth challenge.

Page 10

10

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 1

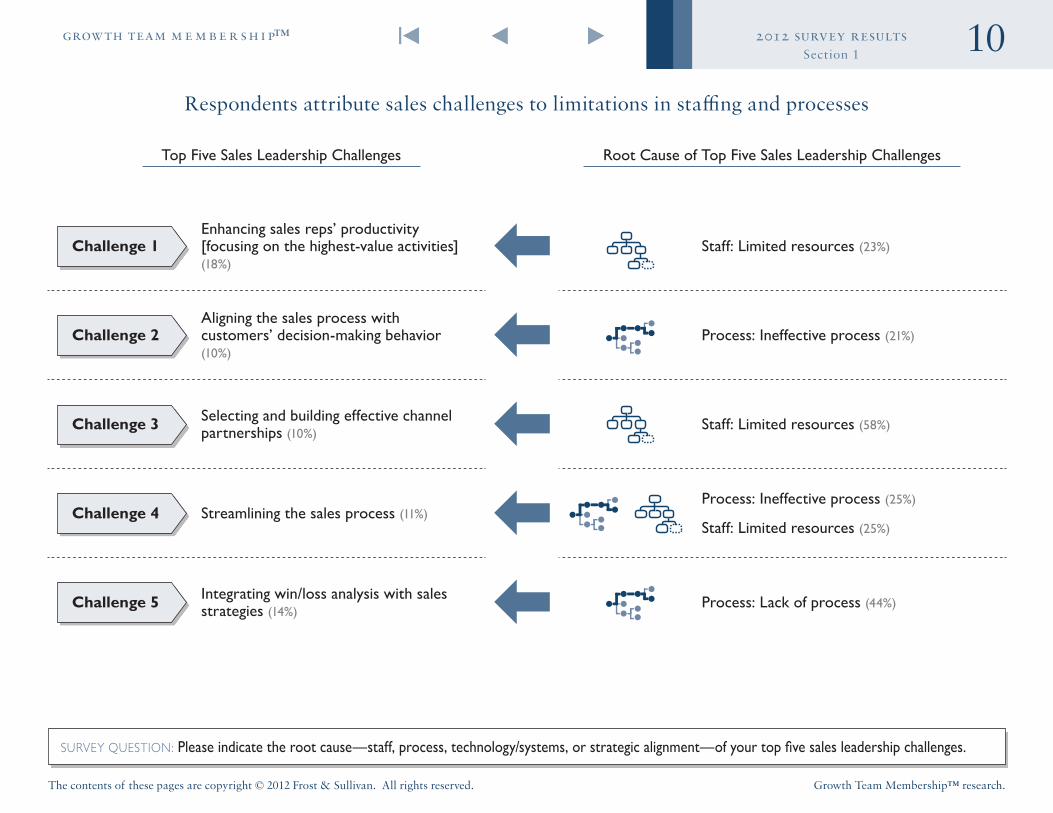

Respondents attribute sales challenges to limitations in staffing and processes

SURVEY QUESTION: Please indicate the root cause—staff, process, technology/systems, or strategic alignment—of your top five sales leadership challenges.

Root Cause of Top Five Sales Leadership ChallengesTop Five Sales Leadership Challenges

Challenge 1Enhancing sales reps’ productivity [focusing on the highest-value activities] (18%)

Staff: Limited resources (23%)

Challenge 2Aligning the sales process with customers’ decision-making behavior (10%)

Process: Ineffective process (21%)

Challenge 3 Selecting and building effective channel partnerships (10%)

Staff: Limited resources (58%)

Challenge 4 Streamlining the sales process (11%)Process: Ineffective process (25%)

Staff: Limited resources (25%)

Challenge 5 Integrating win/loss analysis with sales strategies (14%)

Process: Lack of process (44%)

Page 11

11

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

INTRO

SECTION

1

SECTION

2

SECTION

4

SECTION

3

SECTION

2 Sales Leadership Resource Trends

Page 12

12

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 2

F

F

F

F

F

F

0%

10%

20%

30%30%

28%

23%

21%

9%

12%

8%7%

10%11%

20%21%

29%

23%

10%

7%

11%

20%

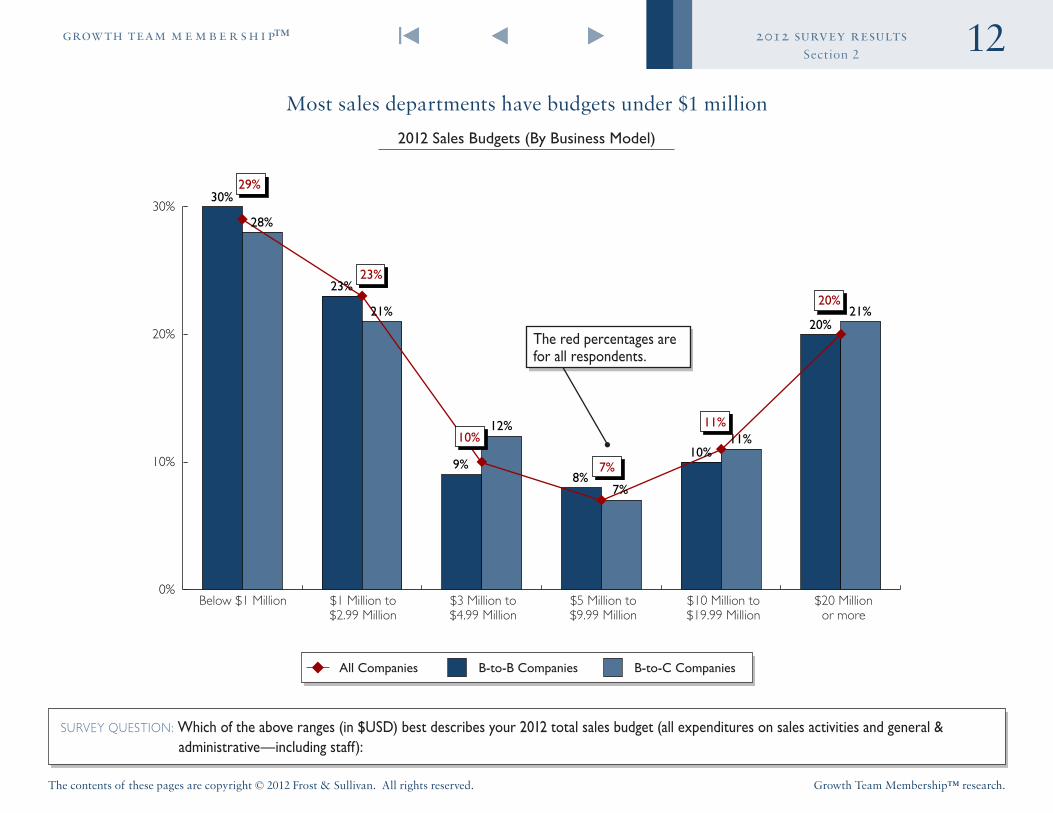

Most sales departments have budgets under $1 million

2012 Sales Budgets (By Business Model)

SURVEY QUESTION: Which of the above ranges (in $USD) best describes your 2012 total sales budget (all expenditures on sales activities and general & administrative—including staff):

The red percentages are for all respondents .

Below $1 Million $1 Million to $2.99 Million

$3 Million to $4.99 Million

$5 Million to $9.99 Million

$10 Million to $19.99 Million

$20 Million or more

All Companies B-to-B Companies B-to-C Companies

Page 13

13

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 2

B-to-B companies attribute a greater percentage of their revenue to distribution channels or partners

Percent of Revenue Attributed to Distribution Channels and Partners (By Business Model)

SURVEY QUESTION: What percentage of your 2011 company sales were attributed to distribution channels or partnerships and alliances?

All Companies B-to-B Companies B-to-C Companies0%

10%

20%

18%

20%

18%

Page 14

14

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 2

Respondents anticipate a moderate increase in sales staffing for 2012

Sales Staffing Changes (By Business Model)

SURVEY QUESTION: In comparison to 2011, your 2012 sales staffing will…

7%

1%

41% 43%Stay the Same

Decrease Moderately Decrease Substantially Increase Substantially

Increase Substantially

Increase Moderately

All Companies

B-to-C Companies

B-to-B Companies

5%

3%

45%33%

Stay the Same

Decrease Moderately Decrease Substantially

Decrease SubstantiallyIncrease Substantially

Increase Moderately

8%

14%

6%

1%

40% 46%

7%

Stay the Same

Decrease Moderately

Increase Moderately

Page 15

15

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 2

Most sales executives foresee moderate budget increases in 2012

Sales Budget Changes (By Business Model)

SURVEY QUESTION: In comparison to 2011, your 2012 sales budget will…

7%

2%

16%

2%

28%

45%

Stay the Same

Decrease Moderately Decrease Substantially

Increase Substantially Increase Substantially

Increase Moderately

All Companies

B-to-C Companies

B-to-B Companies

2%

36%

39%

Stay the Same

Decrease Moderately

Increase Substantially

Increase Moderately

18%

23%

24%

48%

10%

Stay the Same

Decrease Moderately Decrease Substantially

Increase Moderately

Page 16

16

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 2

B-to-C companies are more likely to rate their sales functions as “Above Average”

Sales Effectiveness (By Business Model)

SURVEY QUESTION: How would you rate the performance or effectiveness of your function compared to others within your industry?

All Companies B-to-B Companies

B-to-C Companies

8% 9%

5%

52% 45%

65%

34% 39%

25%

6% 7%

5%

Above Average

Above Average

Above Average

Exceptional Exceptional

Exceptional

Below Average Below Average

Below Average

Average Average

Average

Page 17

17

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

INTRO

SECTION

1

SECTION

2

SECTION

4

SECTION

3SECTION

3 Special Interest Topic: Tools and Social Media

Page 18

18

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

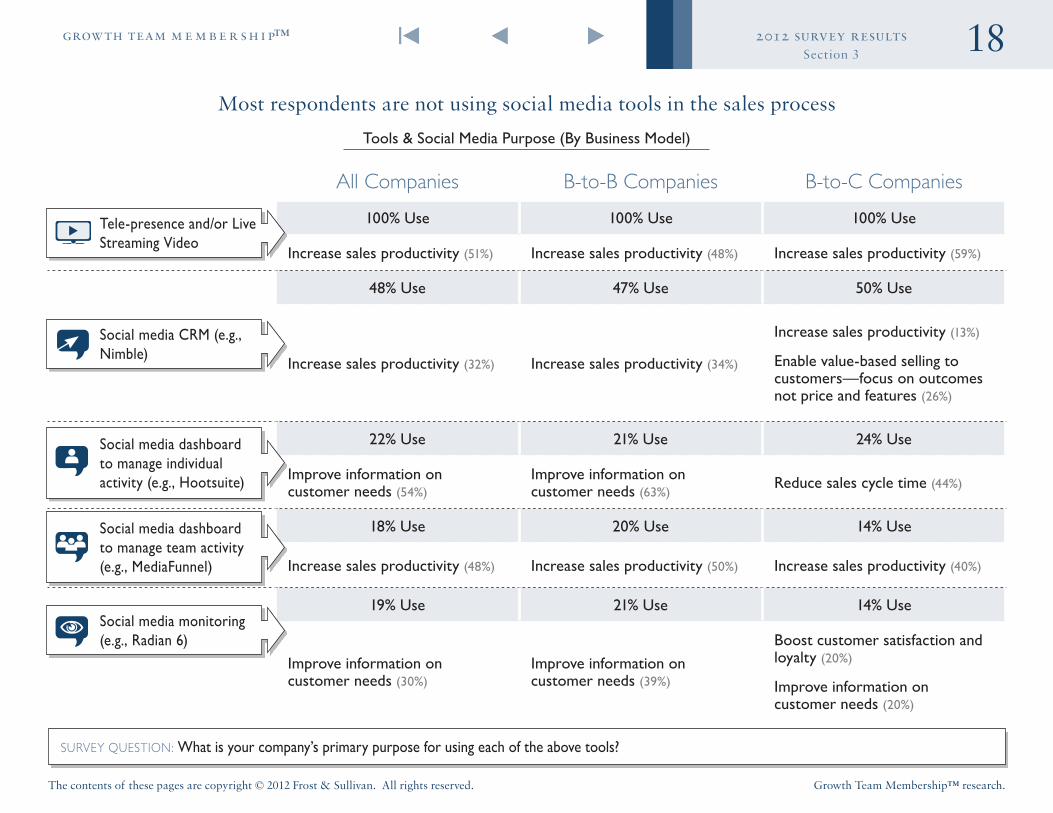

Section 3

SURVEY QUESTION: What is your company’s primary purpose for using each of the above tools?

Most respondents are not using social media tools in the sales process

Tools & Social Media Purpose (By Business Model)

All Companies B-to-B Companies B-to-C Companies

100% Use 100% Use 100% Use

Increase sales productivity (51%) Increase sales productivity (48%) Increase sales productivity (59%)

48% Use 47% Use 50% Use

Increase sales productivity (32%) Increase sales productivity (34%)

Increase sales productivity (13%)

Enable value-based selling to customers—focus on outcomes not price and features (26%)

22% Use 21% Use 24% Use

Improve information on customer needs (54%)

Improve information on customer needs (63%)

Reduce sales cycle time (44%)

18% Use 20% Use 14% Use

Increase sales productivity (48%) Increase sales productivity (50%) Increase sales productivity (40%)

19% Use 21% Use 14% Use

Improve information on customer needs (30%)

Improve information on customer needs (39%)

Boost customer satisfaction and loyalty (20%)

Improve information on customer needs (20%)

Tele-presence and/or Live Streaming Video

Social media CRM (e.g., Nimble)

Social media dashboard to manage individual activity (e.g., Hootsuite)

Social media dashboard to manage team activity (e.g., MediaFunnel)

Social media monitoring (e.g., Radian 6)

Page 19

19

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

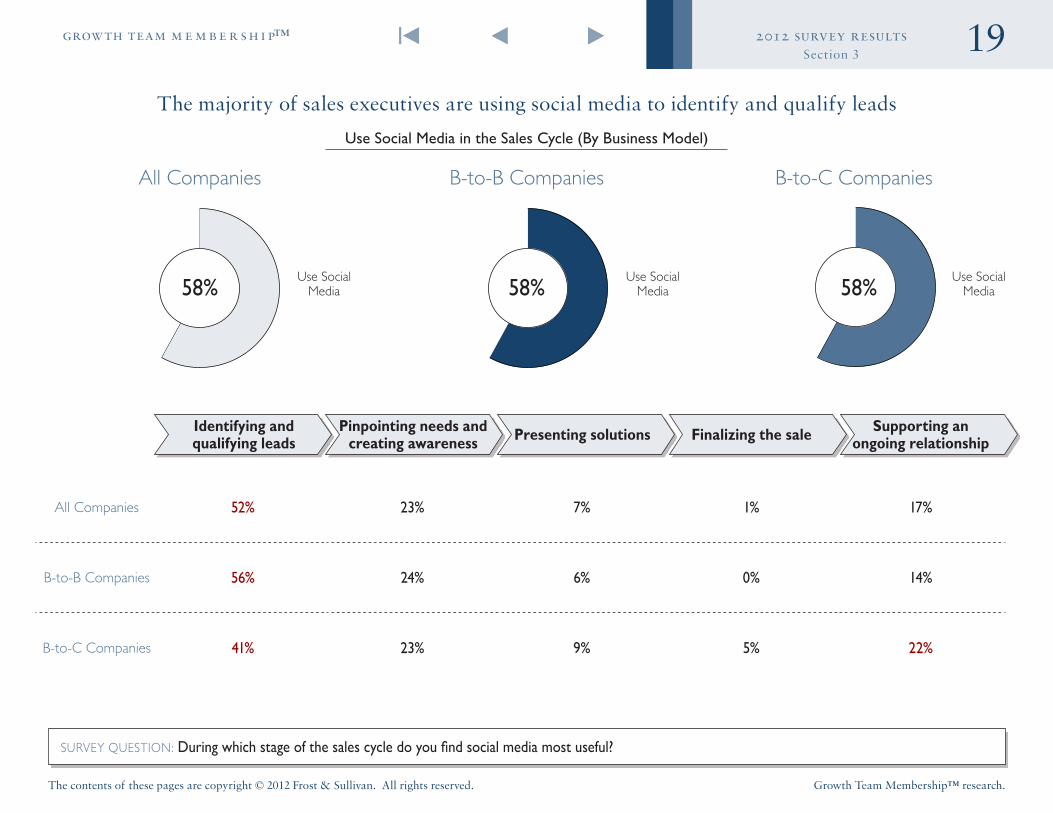

SURVEY QUESTION: During which stage of the sales cycle do you find social media most useful?

The majority of sales executives are using social media to identify and qualify leads

Use Social Media in the Sales Cycle (By Business Model)

All Companies 52% 23% 7% 1% 17%

B-to-B Companies 56% 24% 6% 0% 14%

B-to-C Companies 41% 23% 9% 5% 22%

Identifying and qualifying leads

Pinpointing needs and creating awareness Presenting solutions Finalizing the sale Supporting an

ongoing relationship

All Companies B-to-B Companies B-to-C Companies

Use Social Media

Use Social Media

Use Social Media58%58%58%

Page 20

20

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

All Companies

SURVEY QUESTION: Please list the top three social media platforms (e.g., LinkedIn, Twitter, SlideShare) you use in your sales efforts.

Sales executives use LinkedIn as their primary social media platform

Top Three Social Media Platforms Used During Sales (By Business Model)

B-to-B Companies B-to-C Companies

LinkedIn (72%)

Twitter (41%) Twitter (47%) Facebook (27%)

Facebook (22%)Facebook (18%) Twitter (40%)

LinkedIn (75%) LinkedIn (65%)

Page 21

21

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

SURVEY QUESTION: For what purpose do you use the above LinkedIn activities in your sales efforts?

Respondents use LinkedIn primarily to look up information on customer needs and promote their topical expertise

Use of Specific LinkedIn Activities

Yes YesYes

Yes

Conduct individual searches Join special interest groups Actively participate in special interest groups

Create/moderate special interest group(s)

75% 82% 65% 43%

Primary Purpose:Improve information on customer needs (40%)

Primary Purpose:Improve information on customer needs (37%)

Primary Purpose:Demonstrate topical expertise (43%)

Primary Purpose:Demonstrate topical expertise (35%)

Boost brand recognition (35%)

Page 22

22

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

SURVEY QUESTION: For what purpose do you use the above LinkedIn activities in your sales efforts?

Sales executives are promoting their thought leadership through special interest groups on LinkedIn

Use of Specific LinkedIn Activities (By Business Model)

B-to-C Companies

71%

29%

79%

21%

44%

56%64%

36%

86%

14%

88%

12%

41%

59%

72%

28%

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

B-to-B Companies

Conduct individual searches Join special interest groups Actively participate in

special interest groupsCreate/moderate special

interest group(s)

71%

86%

79%

88%

64%

72%

44%

41%

Primary Purpose:Improve information on customer needs (29%)

Primary Purpose:Improve information on customer needs (50%)

Primary Purpose:Improve information on customer needs (42%)

Primary Purpose:Improve information on customer needs (37%)

Primary Purpose:Demonstrate topical expertise (40%)

Primary Purpose:Demonstrate topical expertise (52%)

Primary Purpose:Demonstrate topical expertise (29%)

Boost brand recognition (29%)

Primary Purpose:Demonstrate topical expertise (31%)

Boost brand recognition (31%)

Page 23

23

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

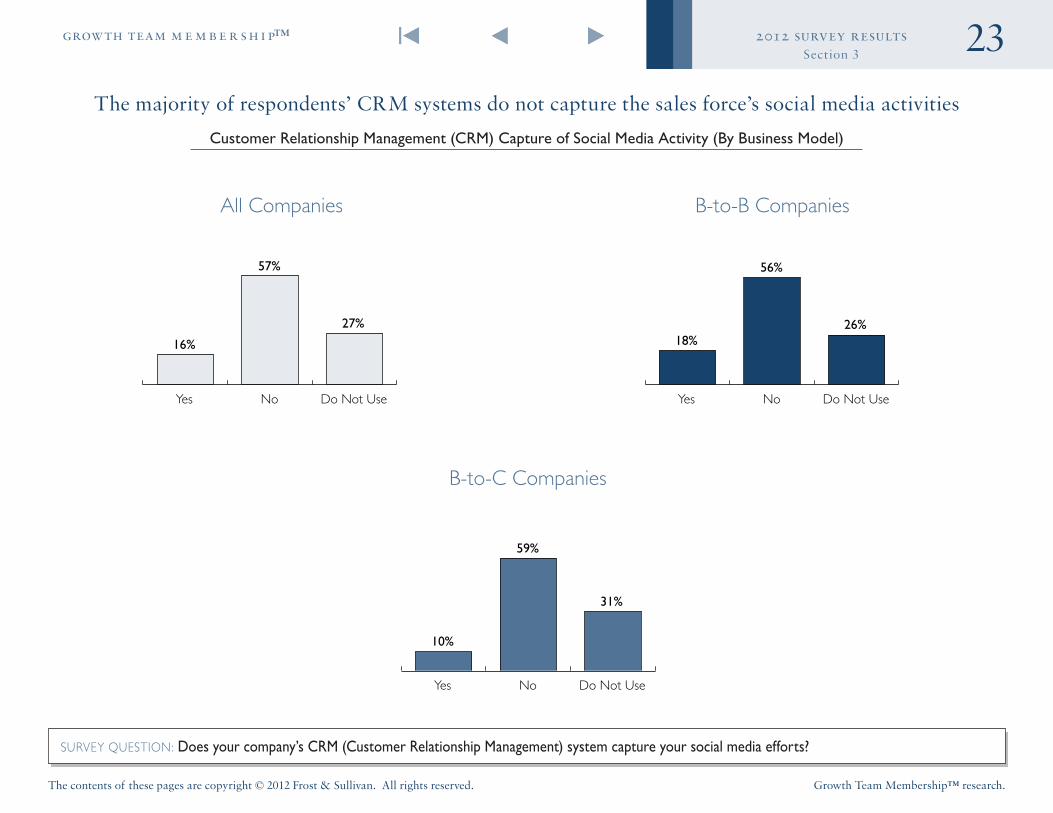

The majority of respondents’ CRM systems do not capture the sales force’s social media activities

Customer Relationship Management (CRM) Capture of Social Media Activity (By Business Model)

SURVEY QUESTION: Does your company’s CRM (Customer Relationship Management) system capture your social media efforts?

Yes No Do Not Use

16%

57%

27%

Yes No Do Not Use

18%

56%

26%

All Companies

Yes No Do Not Use

10%

59%

31%

B-to-B Companies

B-to-C Companies

Page 24

24

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 3

Few respondents are using predictive analytics in their sales processes

Approach to Predictive Analytics (By Business Model)

SURVEY QUESTION: Which of the above best describes your approach to predictive analytics (the analysis of customer behavioral data to identify patterns and provide insights for customer interactions)?

All Companies B-to-B Companies

B-to-C Companies

52%

5%

66%

5%

30%

16%

47%

4%

8%

27%

19%

21%

Combination of Internal and External Efforts

Combination of Internal and External Efforts

Combination of Internal and External Efforts

Do Not Use Do Not Use

Do Not Use

Conduct Internally Conduct Internally

Conduct Internally

Outsource to Vendor Outsource to Vendor

Outsource to Vendor

Page 25

25

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

INTRO

SECTION

1

SECTION

2

SECTION

4

SECTION

3

SECTION

4 Respondent Demographics

Page 26

26

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 4

Respondent Demographics

SURVEY QUESTION: Please indicate the type of enterprise, business model, and revenue that best represents your company.

N = 255

N = 257N = 260

Enterprise Type Business Model

Company Revenue

55%

4%

1% 1%

5%

34%

18%

11%

71%

Public

Private

Hybrid

B-to-B Company

Venture CapitalGovernment/Public Sector

Not for Profit

0%

30%

60%

43%

22%

9%

21%

5%

Below $100 Million

$100 Million to $499.99 Million

$500 Million to $999.99 Million

$1 Billion to $11 Billion

More than $11 Billion

B-to-C Company (Indirect)

B-to-C Company (Direct)

The majority of the respondents come from B-to-B companies .

The majority of the respondents come from privately held companies .

Page 27

27

The contents of these pages are copyright © 2012 Frost & Sullivan. All rights reserved.

2012 survey resultsgrowth team m e m b e r s h i p™

Growth Team Membership™ research.

Section 4

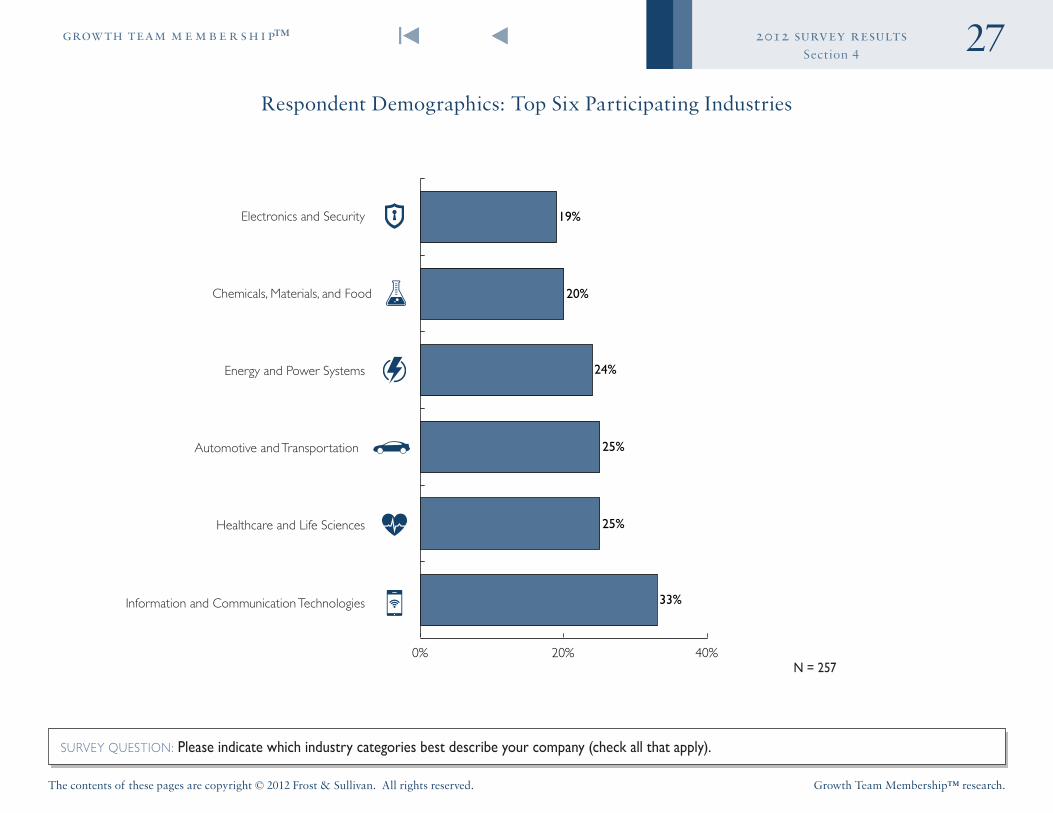

Chemicals, Materials, and Food

Electronics and Security

SURVEY QUESTION: Please indicate which industry categories best describe your company (check all that apply) .

Respondent Demographics: Top Six Participating Industries

N = 2570% 20% 40%

33%

25%

25%

24%

20%

19%

Automotive and Transportation

Energy and Power Systems

Healthcare and Life Sciences

Information and Communication Technologies