Page 1

Improving Socio Economic Lives of Deserving Masses of Society

20

10

Imp

act

Ass

essm

ent

of

Mic

rofi

nan

ce

Impact

Assessment of

Microfinance:

A Case Study

of Akhuwat

Ather Azim Khan

Syed Hussain Haider

Muzaffar Asad

Research and Development

Centre Faculty of Commerce

University of Central Punjab

Page 2

a

Message from Chairman Board of Governors

Akhuwat, an interest free microfinance NGO is an inspiring experience, which has not only

infused great interest among various financial circles of local community but has also gained

tremendous admiration from the global academic institutions and microfinance organizations.

Philosophy of Akhuwat is the true reflection of Islamic teachings of Qarz-e-Hasna (helping

someone in need with interest free loan) which is preferred by all means over charity. Akhuwat

has commendably targeted the class of society, which is haunted with all kinds of misfortunes

like massive pockets of poverty, unemployed youth, illiteracy, widespread corruption, gender

inequality, skyrocketing prices of commodities, lack of access to basic amenities and socio

economic stratification.

It is critical for MFIs, particularly those working with very poor and vulnerable clients, to be

sensitive to the impact of their work particularly to the potential negative impacts that their

services may produce. An MFI should know that it is having a positive impact or, at the very

least, that it is not having a negative impact on some people. All MFIs have knowledge about

how their work affects their clients, but this knowledge is often not formalized.

I would like to facilitate the faculty and volunteer students of Faculty of Commerce, University

of Central Punjab for executing this unique exercise and for conducting this comprehensive

Impact Assessment study of Akhuwat. University of Central Punjab cherishes its social

relationship with Akhuwat and looks for mutually reinforcing its commitment to the betterment

of Pakistan through corporate social responsibility.

Mian Amer Mahmood

Page 3

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT b

Message of Executive Director Akhuwat

Akhuwat is dedicated to improve the lives of the poor; those who are financially abused,

abandoned and disregarded by society. As a registered NGO, Akhuwat provides the poor with

interest free loans so that they may acquire a livelihood and the skills and support they need to

reach their full potential. In this regard, to highlight the achievements of Akhuwat and to check

the impact of Akhuwat on the lives of its beneficiaries, University of Central Punjab conducted

an impact assessment survey. University of Central Punjab undertook the initiative to conduct a

comprehensive impact assessment of microfinance taking the case of Akhuwat. An impact

assessment team was constituted by the university, which was assigned this challenging task.

Based upon primary data and survey of the Akhuwat beneficiaries an impact assessment report

was developed, which showed the performance of Akhuwat. All the contents of the study and

survey have been incorporated in this report.

Page 4

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT c

Message from Dean Faculty of Commerce

An impact assessment of microfinance is a research study that measures how the services of

microfinance institutions impact the lives of their clients in areas such as employment, income,

nutrition, education, health, and gender equity. It is a primary tool used to determine the

effectiveness of microfinance as a development intervention.

Significantly, MFIs can also use impact assessment as a management tool to improve operational

efficiency, product design, and social effectiveness. Assessments vary depending on the type of

microfinance institution, its mission and the objectives. It seeks to accomplish the type of

information required and cost considerations.

May God bless Dr. Amjad Saqib, a man with a diamond heart and influencing commitment, the

Executive Director of Akhuwat, who is running this institution with an extraordinary missionary

spirit. All those associated with this organization have been working with great zeal and

enthusiasm and they deserve the thanks and blessings of our society. I would also like to

commend and appreciate the contribution and efforts of Prof. Ather Azeem Khan, Prof. Syed

Hussain Haider, and Prof. Muzaffar Asad in the entire Impact Assessment of Akhuwat. It is

important to mention the input of Muhammad Bilal Akhtar, Muhammad Usman Javaid, Nabeel

Waseem, Abubakar Cheema, Muhammad Usman Shafique, Muhammad Shah, Atif Ali, Rohail

Iftikhar, Nazir Hussain, Hassan Aftab, Fakhar Islam, Benish Awais, Rizwan Hameed, Adeel

Athar, Abdul Rahim, Hassan Zafar, and Adeel Waheed. The support of the members of Faculty

of Commerce is also appreciated. The continued guidance and encouragement of Mian Amer

Mahmood (Chairman Board of Governors, UCP) and Prof. Sohail Afzal (Executive Director

Punjab Group of Colleges) has been the spirit behind the work executed by the Faculty of

Commerce.

Page 5

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT d

Table of Contents

Sr. No. Particular Page No.

1 Message from Chairman Board of Governors, UCP a

2 Message from Executive Director Akhuwat b

3 Message from the Dean of Commerce, UCP c

4 Table of Contents d

5 Executive Summary 1

6 Introduction 2

7 Microfinance 3

8 Difference between Microfinance and Micro Credit 4

9 Different Micro Finance Models of the World 5

10 Bangladesh Micro Finance Model (Grameen Bank) 5

11 Methodology of Grameen Bank 5

12 Credit Delivering System 6

13 Kenya Micro Finance Model (One Acre Fund) 8

14 Methodology 9

15 Program Model 10

16 Indian Micro Finance Model (Swayam Krishi Sangam) 11

17 Methodology of Swayam Krishi Sangam 11

18 Kinds of Loans & their Methodology 14

19 Akhuwat Model 16

20 Methodology of Akhuwat 17

21 Loan Products 21

22 Impact Assessment 23

23 Unit of Impact Assessment 23

24 Objectives of Impact Assessment 24

25 Research Methodology 24

26 Selection of Respondent 25

27 Survey and Questionnaire 25

28 Data Analysis 26

29 Wilcoxon Test 70

30 Conclusion 72

Page 6

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 1

Executive Summary

In the current era microfinance institutions and micro financing is becoming a very important

tool of development strategies for poverty alleviation. Despite of the importance of microfinance

institutions and microfinance programs its importance and impact are partial and contested. This

research study has tried to find out the impact of Akhuwat a microfinance institution over the life

of its beneficiaries. This research presents the findings of a regional level impact assessment of

Akhuwat in Punjab. The study aims to assess on a regional scale the outreach and development

impact of Akhuwat activities in the life of its beneficiaries. In this study the borrowers of

Akhuwat from different cities of Punjab have been taken and were interviewed regarding their

social and economic life before the intervention of microfinance and after the intervention of

microfinance from Akhuwat. The results have shown that the beneficiaries of Akhuwat have

benefitted a lot from the financing that they have got from Akhuwat. The lives of beneficiaries

changes and they got a social as well as economic empowerment. The campaign of before and

after taking loans from Akhuwat was conducted in the following areas.

Girls attending school, head of family income, total family income, eating meat, eating fruit,

servants, falling sick, medical treatment, visit of relatives, behavior of relatives, relatives and

friends lends you money, lent money to your friends and relatives, family and friends invitation

on functions, family and friends involves you in solving issues and problems, involvement of,

women in your family decisions, members of any community in any society, daily travel,

personal vehicle, own house, physical condition of house, entertainment.

Page 7

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 2

1. Introduction

Microfinance programs and institutions have become increasingly important components

of strategies to reduce poverty or to promote micro and small enterprises. However, knowledge

about the achievements of such initiatives remains only partial and contested. The assessment of

microfinance programs remains an important field for researchers, policymakers, and

development practitioners. This research study reviews the methodological options for assessing

the impact of such programs. It views impact assessment as being ‘as much an art as a science’.

Econometricians and statisticians are particularly concerned with this field.

Microfinance is considered as an important tool for alleviating poverty. The potential for

reaching and assisting low-income households in meeting their basic financial needs, for

protecting against risks, and for developing social and economic empowerment on a sustainable

basis have precipitated donor funding into microfinance in the late 90’s causing the sector to

expand rapidly. Akhuwat is providing financial services to the poor. Akhuwat operates under a

corporate mission of poverty reduction. Akhuwat has allocated increasing amounts of funding to

microfinance on this basis. Microfinance programs have burgeoned in many developing

countries as part of their efforts to reduce poverty. The portion of poor clients served by

microfinance institutions has been rapidly growing at a rate of 25 to 30 percent annually over the

last five years.

Despite its rapid expansion, the effectiveness of microfinance in achieving its potential

has always been put into question. The scarce reliable data on the impact of direct access to

financial services on income, expenditure or wealth of poor households hinder attempts at

deriving a clear conclusion on the matter. One reason is that the effect of accessing financial

services can have multiple and cross-cutting effects on poverty; these effects are hard to isolate

Page 8

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 3

and determine direct causal relationships. The impact of anti-poverty measures is often not

immediately apparent, sometimes necessitating an intergenerational study of the impact on

households. That’s why this survey has been conducted again after two years and as a result

significant improvement has been seen.

The scarcity of data or the difficulty of undertaking comparative studies on the impact of

microfinance in alleviating poverty should not be an excuse to neglect the impact evaluation of

specific microfinance programs. Assessing the social impact of microfinance is vital in

determining whether established microfinance programs achieve the desired outcome. Thus, for

the different stakeholders in the microfinance industry, impact assessment has become a

necessity. Donors want to be assured that their resources are being used for the intended

objective and emphasize the importance of impact assessment to evaluate the social return on

their investment. For microfinance institutions social impact assessments enable them to draw

out strategic management information to better orient them for improved financial performance.

Concrete and available information about the impact of microfinance and specific services

provided by Akhuwat on household income and risk management enables clients to make

informed decisions about range of credits they need.

1.1 Microfinance

Microfinance is often defined as financial services for poor and low-income clients. In

practice, the term is often used more narrowly to refer to loans and other services from providers

that identify themselves as Microfinance Institutions (MFIs). These institutions commonly tend

to use new methods developed over the last 30 years to deliver micro loans to unsalaried

borrowers, taking little or no collateral. These methods include group lending and liability, pre-

Page 9

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 4

loan savings requirements, gradually increasing loan sizes and an implicit guarantee of ready

access to future loans if present loans are repaid fully and promptly.

More broadly, microfinance refers to a movement that envisions a world in which low-

income households have permanent access to a range of high quality financial services to finance

their income-producing activities, build assets, stabilize consumption and protect against risks.

These services are not limited to credit but include savings, insurance and money transfers.

1.2 Difference between Microfinance and Micro Credit

The term microcredit is used for such loans that are given to unsalaried masses of the

society with little or no collateral. Currently, the credit provided to salaried workers based on

automated credit scoring is not termed a microcredit. Microfinance typically refers to

microcredit, savings, insurance, money transfer and other financial products targeted at poor and

low income level group.

Page 10

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 5

2. Different Microfinance Models of the World

There are different models of Microfinance used in the world. Each model has its own

strength and mainly tailored for a particular society and economy. Some of the models have the

strength to be used in the whole world; in different circumstances and conditions. Here a

comparison of some popular Microfinance program is provided here.

2.1 Bangladesh Microfinance Model (Grameen Bank)

Grameen Bank has reversed conventional banking practice by removing the need for

collateral and a banking system based on mutual trust, accountability, participation and

creativity. Grameen Bank provides credit to the poorest of the poor in rural Bangladesh, without

any collateral. At Grameen Bank, credit is a cost effective weapon to fight poverty and it serves

as a catalyst in the overall development of socio-economic conditions of the poor who have been

kept outside the banking orbit on the ground that they are poor and hence are not bankable. Prof

Muhammad Yunus, the founder of "Grameen Bank" reasoned that if financial resources can be

made available to the poor people on appropriate and reasonable terms and conditions then

“these millions of poor people with their millions of small pursuits can add up to create the

biggest development wonders in the society as of June, 2011, it has 8.37 million borrowers, 97%

of whom were women. With 2,565 branches, Grameen Bank provides services in 81,379

villages, covering more than 97% of the total villages in Bangladesh. Its positive impact on poor

and formerly poor borrowers has been documented in many independent studies carried out by

external agencies including the World Bank, the International Food Research Policy Institute

(IFPRI) and the Bangladesh Institute of Development Studies (BIDS).

2.2 Methodology

Grameen bank sets up a branch with a branch manager and a number of center managers

Page 11

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 6

to cover an area of about 15 to 22 villages. The manager and the workers start by visiting

villages to familiarize themselves with the local milieu in which they will be operating and

identify the prospective clientele, as well as to explain the purpose, the functions, and the mode

of operation of the bank to the local population. Groups of five prospective borrowers are

formed; in the first stage, only two of them are eligible for, and receive, a loan. The group is

observed for a month to see if the members are conforming to the rules of the bank. Only if the

first two borrowers begin to repay the principal plus interest over a period of six weeks, the other

members of the group become eligible for a loan. Because of these restrictions, there is

substantial group pressure to keep individual records clear. Thus, the collective responsibility of

the group serves as the collateral of the loan.

Loans are small, but sufficient to finance the micro-enterprises undertaken by borrowers:

rice-husking, machine repairing, purchase of rickshaws, buying of milk cows, goats, cloth,

pottery etc. The repayment rate of loans is currently – 95% - due to group pressure and self-

interest, as well as due to high motivation level of borrowers. Although mobilization of savings

is also being pursued alongside the lending activities of the Grameen Bank, most of the latter's

loan-able funds are increasingly obtained on commercial terms from the central bank, other

financial institutions, the money market and from bilateral & multilateral aid organizations.

2.3 Credit Delivery System

Grameen Bank credit delivery means giving loans to the very poor in their villages by

means of the essential elements of the Grameen credit delivery system. Grameen Bank credit

delivery system has the following features:

2.3.1 Main Focus

The organization has a unique system through which they screen out those people who do

Page 12

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 7

not lie in the category of poorest of the poor and thus, true poor clients are targeted. Another

importance is given in delivering the loan to the poor women of the country. The whole system is

basically developed to enhance the socio economic development of the poorest of the poor

women of the society.

2.3.2 Group Lending

The organization basically lends in groups this characteristic helps in group participation

and group participatory interaction. The system of Grameen bank is to make a foundation of five

members and federating them into centers stress from the start is to strengthen the organizational

customer, so that they can learn the skills of planning and implementation of development

decision. The centers are functionally linked to the Grameen bank, whose field workers have to

attend the center each week.

2.3.3 Special Loan

These include very small loans given without any guarantee. Loans are repayable in

weekly installments spread over a year. Eligibility for a subsequent loan depends upon

repayment of first loan, individual, self chosen, quick income generating activities which employ

the skills that borrowers already posses, close supervision of credit by the group as well as the

bank staff, stress on credit discipline and collective borrower responsibility or peer pressure and

special safeguards through compulsory and voluntary savings to minimize the risks that the poor

confront.

2.3.4 Customer’s Basic Needs

This is shown in the sixteen decisions adopted by Grameen borrowers. It helps

to increase the social and political consciousness. Grameen bank has recently organized a

group to focus more and more women from the poorest households. The urge for survival of

Page 13

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 8

such women has much greater impact on the development of the family to facilitate their

monitoring of the social and physical infrastructure projects. These social and physical

infrastructure projects include housing, sanitation, drinking water, education, family planning,

etc.

2.3.5 Delivering of Resources to Clients

The system has evolved gradually through a structured learning process that includes

testing, errors, and constantly adjustment is required for an operational system. The special

training is provided for the development of highly motivated employees in the decision-making

and operational authority. Operational authority has been gradually decentralized and

administrative functions are delegated to the zonal level.

2.3.6 Expansion of Loan to Meet Needs of the Poor

Since the overall lending program gathers momentum and borrowers access to credit

discipline, other loan programs have been introduced to meet growing social and economic

development needs of the clients. Besides housing, such programs include credit for building

sanitary toilets, credit for installation of tube-wells that supply drinking water and irrigation for

kitchen gardens, credit for seasonal cultivation to buy agricultural inputs, loan for leasing

equipment / machinery. Grameen bank also finances projects undertaken by the entire family of

a seasoned borrower.

2.4 Kenya Microfinance Mode (One Acre Fund)

One Acre Fund is a nonprofit organization started in January 2006 with the goal of

completely rethinking how to solve the chronic hunger problem in Africa. Food aid is at best just

a temporary solution, and instead has to put together a permanent solution. Proven investment

package for farmers and their families, help them to double farm income because of provision

Page 14

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 9

seeds and fertilizer, weekly farm education, and market access. This investment package is the

core of the program. Since founding of the organization has expanded to serve 54,000 families in

10 districts in Kenya and Rawanda.

One Acre Fund is an organization that aims to help poor East African farmers who

emerge from persistent poverty and hunger by increasing their farm-based incomes. They do this

by introducing more profitable crops and farming techniques to farmers and by providing

farming inputs in exchange for a share of future revenues. Unlike most interventions designed to

improve farming incomes in poor settings, One Acre Fund facilitates activities and transactions

at each level of the farming value chain, from organizing farmer groups to negotiating with

export markets.

2.5 Methodology

One Acre Fund utilizes a market bundle to help subsistence farmers in Sub-Saharan

Africa grow themselves out of poverty. The market bundle is made up of five components.

First, One Acre Fund identifies existing local farmer groups with an interest in

working together to increase their farming incomes.

Second, One Acre Fund provides the farmer groups with agricultural education to

improve their farming techniques and knowledge of how to grow more valuable

crops.

Third, One Acre Fund distributes planting materials and fertilizers to the farmer

groups. Generally, these are farming inputs that these farmers would not use

because the up-front investment costs are too high.

Fourth, One Acre Fund facilitates the collection and sale of its farmers, crops. A

portion of the revenue is retained by One Acre Fund to cover the cost of the

Page 15

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 10

capital investments and farmer education; the remainder is distributed to farmers

based on their individual contributions to the harvest.

Finally, One Acre Fund offers its farmers crop insurance to mitigate the risks of

drought and disease.

2.6 Program Model

Markets are used to eradicate hunger permanently. One Acre Fund is concentrated on

one-acre subsistence farmers in Sub-Saharan Africa – one of the largest groups of forgotten poor

in the world. One Acre Fund provides a complete, functioning market system. Thus, making it

possible for even the poorest and most rural farmer to generate more income, and permanently

solve their hunger problem.

2.6.1 Empower Local Group

The first component of the "market bundle" is to empower local groups of farmers. One

Acre Fund finds existing self-help groups (mostly made of women farmers). This group brings

farmers together and makes it possible for them to economically interact with markets.

2.6.2 Farm Education

The second piece of the "market bundle" is farm education, provided by the field officer.

One Acre Fund takes the latest practices from top academic agronomists and translates that into

simple easy-to-understand lessons.

2.6.3 Capital

The third piece of the "market bundle" is capital, environmentally-sensitive planting

materials and fertilizer. Planting materials of the organization have shown a significant

improvement in production. Commercial seed is professionally graded, stored, and selected.

Fertilizer provided by the organization is badly-needed nutrient to soil that has been stripped bare

Page 16

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 11

over decades of poor management.

2.6.4 Connection with Harvest Markets

The fourth component of the "market bundle" is connection with harvest markets. The

organization acts as a bulk-selling agent. Thus, allowing its members to access much higher

prices of the market. This cash creates a savings-and-investment cycle that leads to self-driven,

permanent growth out of hunger.

2.6.5 Crop Insurance

The final component of the "market bundle" is crop insurance. It is estimated that only

0.3% of poor of Africa are insured in any way. One Acre Fund has pioneered a crop insurance

product that pays farmers in the event of a significant drought or disease.

2.7 Indian Micro-Finance Model (Swayam Krishi Sangam)

Swayam Krishi Sangam Microfinance was founded in 1997 by Dr. Vikram Akula. As of

January 31, Swayam Krishi Sangam reached 500,000 clients throughout India. As of March

2006, Swayam Krishi Sangam had a gross loan portfolio of USD 20,596,150 total assets of

26,814,820, a return on assets of 2.80% and a debt to equity ratio of 636.06%. Micro-Credit

Ratings International Limited (M-Cril), a rating agency of microfinance, gave Swayam Krishi

Sangam, a rating of alpha.

2.8 Methodology

Swayam Krishi Sangam Microfinance follows the Joint Liability Group Model. The

methodology involves lending to individual women, utilizing five member groups where groups

serve as the ultimate guarantor for each member. Their approach is to provide financial services

at the doorstep of members in villages and urban colonies. This provides convenience to the poor

and helps them in savings in terms of cost and time associated with travelling to mainstream

Page 17

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 12

banks and enables Swayam Krishi Sangam staff to promptly and fully collect repayments. Their

loans are designed for convenience with small weekly repayments corresponding to cash flows.

Small first loans inculcate credit discipline and collective responsibility. Interest and loan

repayments are simplified for easy comprehension. From village selection to loan disbursal,

Swayam Krishi Sangam follows a clear process in its operations. Details of operational

methodology of the organization are captured below:

2.8.1Village Selection

Before starting operations, the staff of Swayam Krishi Sangam conducts village surveys

to evaluate local conditions of the village. Local conditions include population, poverty level,

road accessibility, political stability and means of livelihood.

2.8.2 Projection Meeting

After a village is selected the organization holds a projection meeting. Swayam Krishi

Sangam staff introduces the community to its mission, methodology and services.

2.8.3 Mini-projection Meeting

The organization holds a mini-projection meeting which is basically a follow-up with

interested women, and direct appeal to those who may not have attended earlier because of

religious, class, caste or gender barriers.

2.8.4 Group Formation

Women form self-selected five-member groups are grouped to serve as guarantors for

each other. Experience has shown that a five-member group is small enough to effectively

enforce group peer pressure and, if necessary, large enough to cover repayments in case a

member needs assistance.

Page 18

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 13

2.8.5 Compulsory Group Training (CGT)

Compulsory group training is a four-day process consisting of hour-long sessions

designed to educate clients on Swayam Krishi Sangam processes and procedures. This training

also builds a culture of credit discipline. Using innovative visual and participatory teaching

methods, Swayam Krishi Sangam staff introduces clients to the financial products and delivery

methods. Compulsory group training also teaches clients about the importance of collective

responsibility. They teaches how to elect group leaders, how to affix signatures, and a pledge that

serves as a verbal contract between Swayam Krishi Sangam and its members. During this

training period, Swayam Krishi Sangam staff collects quantitative data on each client to ensure

that qualification requirements are met. It also helps to record base-line information for future

analysis. On the fourth day, clients take a “Group Recognition Test” conducted by a different

staff member than the one who trained them. If they pass, they are officially accepted as Swayam

Krishi Sangam members.

2.8.6 Center Meetings

As additional groups are formed within a single village, a Centre (Sangam) emerges.

During centre formation, groups are combined to form a centre of 3 to 10 groups or 15 to 50

members. Weekly Centre meetings serve as a time to conduct financial transactions. Meetings

are held early in the morning, so as to not interfere with clients’ daily activities. A leader and

deputy leader are selected to facilitate meetings and ensure compliance with Swayam Krishi

Sangam procedures. In addition to financial transactions, members use the weekly meetings to

discuss new loan applications and community issues. Centre meetings are conducted with rigid

discipline in order to sustain the environment of credit discipline created during Compulsory

group training.

Page 19

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 14

2.9 Kinds of loans & their Methodology

2.9.1 Proprietary Products

2.9.1.1 Income Generation Loans (IGL)

The organization gives loans ranging from (Rupees1) Rs. 4,000 to Rs. 10,000 for the first

loan. Then the subsequent loan amount is determined by past credit history and increased each in

set increments up-to a maximum of Rs. 26,000. Term of the loan is 50 weeks with principal and

interest payments due on a weekly basis. 12.5% flat interest rate / 24.55% annual effective

interest rate. The organization provides self-employed women financial assistance to support

their business enterprises, such as raising livestock, running local retail shops called kiranastores,

providing tailoring and other assorted trades and services.

2.9.1.2 Midterm loan (MTL)

The organization provides midterm loans. The amount of these loans ranges from Rs.

2,000 to Rs. 14,000 in each annual cycle. These loans are available any time after the completion

of 20 weeks & before 40 weeks of an income generation loans cycle.

2.9.1.3 Mobile Loans

The organization also provides financing for mobile phones and telephone services. The

range of such loans amounts from Rs. 1,500 to Rs. 3,000 at 26.14% annual effective interest rate

and loan processing fee of 1%. The term of the loan is 25 weeks.

2.9.1.4 Sangam Store Loans

The organization gives working capital loans. These loans ranging from Rs. 1,000 to Rs.

12,500 are interest free loans. The term of the loan is 14 days.

1 Here Rupees are Indian Rupees

Page 20

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 15

2.9.1.5 Housing Loans

The organization gives housing loans. These loans range from Rs. 50,000 to Rs. 150,000.

Then members have to complete at least three Income generation loans cycles to qualify or one

ILP has to be completed. Term of loan is three to five years with principal and interest payments

due on a monthly basis. 11.9% flat interest rate or 21 % annual effective interest rate is being

charged by the organization. In addition, loan processing fee of 2% collected upfront. The

organization provides financial access to women for construction of new houses or improvement

& extension of existing houses.

2.9.1.6 Funeral Assistance

The organization also gives a funeral assistance of Rs.1000. This assistance is given only

to those members who have paid insurance premium. This assistance is provided to family of the

member if the organization receives information within 14 days of death. This amount is

adjusted in the final payout of the principal amount.

2.9.1.7 Gold Loan

The organization also gives gold loans. These loans range from Rs. 2,000 to Rs. 100,000.

Nature of loan can be Bullet and tenure can be opted up-to 12 months. Annual effective interest

rate ranges from 12 to 30%, depending on the percentage of disbursement opted to net weight of

gold jewelry. Membership fee of 0.5% on the first loan disbursed to non members. The

organization provides personal or business loans to the members and non -members secured by

gold jewelry to meet their short term liquidity requirements.

2.9.2 Distributor products

2.9.2.1 Life insurance

Page 21

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 16

The organization charges weekly payment of Rs. 20 for the term of five years. Upon

death, the organization disburses to the beneficiary the full sum assured of Rs. 5,000 plus the

account value, which is equal to the aggregate of the premiums paid plus interest accrued, if any,

less any charges for the administration of the policy. In the event the death is deemed an

accidental death, the beneficiary receives Rs. 10,000 plus the account value. Upon maturity in

five years where no death has occurred, the organization disburses to the policyholder the

account value.

2.10 Akhuwat Model

Akhuwat was established in 2001 with the objective of providing interest free micro

credit to the poor so as to enhance their standard of living. The organization started with a first

loan of Rs. 10,000, which was given to a widow. This brave lady did not believe in charity hence

she asked for Qarz-e-Hasna. She purchased two sewing machines and started a small boutique in

her house. She worked so hard that in six months she returned the loan. During this period she

also ran her house and married one of her daughters. That was the beginning of what later

became a movement.

Akhuwat is dedicated to improving the lives of the poor; those who are financially

abused, abandoned and disregarded by society. As a registered non-governmental organization,

Akhuwat provides the poor with interest-free loans so that they may acquire a livelihood and the

skills and support they need to reach their full potential. To this end, Akhuwat raises its funds

from Civil Society. It does not depend on international funding; instead it uses the spirit of

volunteerism and the tradition of giving, a cardinal principle of all religions.

Akhuwat derives inspiration from the Muslim spirit of Muakhaat or brotherhood. The

earliest example of Muakhaat was first displayed by the citizens of Madina at the dawn of Islam,

Page 22

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 17

when they shared their wealth with the immigrants or Muhajirin of Mecca. Akhuwat’s

philosophy is based on the principle of Qarze-e-Hasna, helping someone in need with interest-

free loans, which is favored over charity. From a first loan of Rs. 10,000, Akhuwat’s total

disbursement has now increased to more than Rs. 1.1 billion in just over nine years. Akhuwat’s

greatest success is that it has been instrumental in helping 99,844 families move from being

dependent on others to being self-sufficient. The success stories of these people bring hope to

those still in need of help.

Akhuwat started its operations in Lahore and to date has fifteen branches in this city. It

has also expanded to Rawalpindi and Faisalabad in collaboration with the Chambers of

Commerce and Industry and philanthropists of these two cities. Besides these big cities it has

opened branches in other cities like Bahawalpur, Multan, Gujrat, Dera Ghazi Khan, Khanewal,

Rajanpur, Nowshera, Peshawar and Karachi. Akhuwat has also expanded its programme in small

cities and towns like Mansehra, Sahiwal, Miani, Kot Momin (Sargodha), Chiniot, Dijkot,

Samundari, Lodhran, Jehanian, Duniyapur, Nain Sukh, Chunian, Changa Manga (Kasur), Choti

Zaireen (Dera Ghazi Khan), Chak Madressah (Bahawalnagar), Sheikhupura, Toulamba, Jampur,

Kot Mithan and Khairpur(Sindh). Few more branches are under process in Mardan and

Farooqabad. Akhuwat’s model is also a part of curriculum at University of Southern New

Hampshire USA, Lahore University of Management Sciences (LUMS) and university of central

Punjab (UCP). All this has been made possible because of the tireless efforts made by our

dedicated staff. Akhuwat sincerely appreciates and is grateful to hundreds of individuals and

families who have donated money, time and skills to this cause.

2.11 Methodology

Akhuwat provides the economically poor with interest free loans so that they may acquire

Page 23

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 18

a self-sustaining livelihood. It also provides the skills and support they need to actualize their full

potential and abilities. Since its inception Akhuwat has solely relied upon the philanthropists in

extending its services to the community. However, in order to fulfill the increased credit needs of

its ever-increasing clientele it is now willing to work with the international donors as well.

The spirit of volunteerism that Akhuwat’s management and its team member’s exhibit are

indicative of the success Akhuwat achieved within a short span of time.

2.11.1 Family Loans

Family loan is the most common type of loan that Akhuwat offers to its clients for setting

up or expanding a business. Income from this business is jointly shared by the whole family. The

loans given by Akhuwat are co-signed by male and female head of the family. Akhuwat believes

in strengthening family unit as some studies show that separate loans to male and female in a

family may result in tensions in the family and hence may cause disintegration of this important

institution.

2.11.2 Linkages with Mosque and Church

An important and novel idea associated with individual loans is the use of the local

mosque/church infrastructure as the center for loan disbursement and as an avenue for

community participation.

2.11.3 Combination of Individual and Group Lending Program

Diversification of loan portfolio by offering different loan products has helped to increase

the outreach of the organization.

2.11.4 Credit plus approach

Akhuwat has employed a credit plus approach by introducing the idea of social guidance

for its credit beneficiaries. The purpose of this approach is to help borrowers flourish their small

Page 24

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 19

enterprises so that they can lead socially healthier lives than before.

2.11.5 Program Introduction

Individual loans are marketed through awareness campaign in poor localities, market

places and through previous borrowers. An introduction to the program is also given in nearby

mosque or church when people have congregated there for prayers. This has not only

tremendously saved the operational costs but has also opened the doors of the religious places for

socio-economic development. It also attaches a moral responsibility to return the loan on time.

2.11.6 Individual Selection

The loan process starts with the submission of applications by persons interested in

getting financial assistance. The Unit Manager (Loan Officer) then evaluates that whether the

applicant deserves the loan or not i.e. lives below the poverty line, has a reliable social capital, is

not involved in any illegal business and possesses entrepreneurial abilities.

2.11.7 Preparation of Business Plans

Through the preparation of business plans the business idea of the intended loanee is

evaluated to see if it is viable and whether it can generate income beyond the household expenses

of the individual so that the loan could be repaid easily. The applicant's family is also

interviewed to make sure that they know about the loan and support the business idea.

2.11.8 Credit Appraisal

After initial appraisal by the Unit Manager, the application is forwarded to Branch

Manager who appraises the technical section of the appraisal process. Then the case is referred to

Loan Approval Committee. The committee comprising of Unit, Branch and Area Mangers

reviews the credit cases. If the committee approves the case loan disbursement is done. The

whole process takes almost three weeks.

Page 25

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 20

2.11.9 Guarantors of Loans

Every borrower also provides two individual guarantors who vouch for his/her

credentials and accept the responsibility of monitoring the borrower and give assurance to

persuade the borrower for timely payment of loan. One of the two guarantors may be from the

same family.

2.11.10 Credit Disbursement/Capacity Building

Disbursement takes place 2-3 times a month and 100-150 loans are disbursed at one event

usually held at branch office/mosque or church. Every borrower has to be accompanied by one of

the guarantors. Other people present at the time of disbursement include community members,

Akhuwat staff, from the branch and Head office. Social Guidance events are also held

simultaneously in which the capacity of loanees is built to carry on their work more efficiently

and effectively. Akhuwat is also apprised of social agenda that includes:

Emphasis on girls education

Serving the community at large

Protection and improvement of environment

Importance of plantation

Observance of traffic rules and local laws

2.11.11 Recovery/Follow up

Once a loan is disbursed, the Unit Manager monitors the client with regular visits to his

residence and place of work. The loan repayment has to be submitted at the branch by the 7th of

each month. If a payment is not in by the 10th, the Unit Manager visits the client to remind and if

repayment is still not done then the guarantors are contacted and asked to make the payment.

Page 26

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 21

2.12 Loan Products

2.12.1 Family Enterprise Loan

These loans are given for establishing a new business or expanding an existing one.

Family Enterprise loan is the most common type of loan offered by Akhuwat. It comprises 91%

of Akhuwat's loan portfolio. The Family Enterprise loan varies in the bracket of Rs.10, 000 to

Rs. 30,000, however, most common amount for the first loan is Rs.15, 000. The individual has to

come up with a viable business plan to become eligible for the loan. The Enterprise loan is also

known as the family Enterprise loan because during the period of appraisal and lending the entire

family is involved in the process with the view to make it a family venture instead of individual

effort.

2.12.2 Liberation Loan

It is used for repayment of loans taken from money lender on exorbitantly high interest

rates. This type of loan is given to those who have borrowed money from moneylenders at very

high interest rates. Akhuwat pays the principle amount in one go for the client and then the client

has to pay back the amount in interest free installments to Akhuwat. Range of this loan is up-to

Rs. 40,000.

2.12.3 Education Loan

It is utilized for paying dues (fees) or purchase of books and material of poor students. It

provides education expenses in easy way. Range of education loan is up-to Rs. 25, 000.

2.12.4 Marriage Loan

Page 27

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 22

Marriage loan is given for dowry of bride (daughter) or marriage ceremony

arrangements. This loan helps in meeting the marriage expenses of a girl of a poor family. Range

of this loan is up-to Rs. 25, 000. Boys are not entitled for such loans.

2.12.5 Emergency Loan

This type of loan is given to meet emergency situations such as school admission fee,

treatment, purchase of medicine, etc. These loans are given to prevent the poor from major

fallbacks. The amount loaned to the poorest of the poor is generally Rs. 5, 000 and this has to be

repaid within one year.

2.12.6 Silver Loan

This is given to increase the size of the existing business. This medium size loan of Rs.

50, 000 is given to those who have successfully completed three or more cycles of borrowing

from Akhuwat and are interested to further expand their business.

2.12.7 Housing Loan

For renovation of house, construction of room, roof, or walls, etc. Range of this loan

varies between Rs. 25, 000 to 70, 000 and has to be repaid within two years time limit. Akhuwat

started this product in collaboration with Al-Noor Umar Welfare Trust, another nonprofit

organization founded by Mr. Khalil Mian, former Chairman of Pakistan Credit Rating Agency

(PACRA).

Page 28

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 23

3. Impact Assessment

An almost infinite array of variables can be identified to assess impacts on different units.

Conventionally, economic indicators have dominated microfinance impact assessment with

assessors particularly keen to measure changes in income. Other popular variables have been

levels and patterns of expenditure, consumption, and assets. A strong case can be made that

assets are a particularly useful indicator of impact because their level does not fluctuate as

greatly as other economic indicators and is not simply based on an annual estimate.

The social indicators that became popular in the early 1980s like educational status,

access to health services, nutritional levels, anthropometric measures and contraceptive use, have

recently been checked in addition to some newly identified indicators in an attempt to assess

whether microfinance can promote empowerment. This has led to the measurement of individual

control over resources, involvement in household and community decision-making, levels of

participation in community activities and social networks and electoral participation. The bulk of

this work has been focused on changes in gender relations, but there are sometimes partially-

formulated assessments of class relations within it.

While not fully comprehensive, the detailed sets of domains and markers, produced in

their paper provide an excellent checklist for impact assessors that should be considered while

designing the impact assessment instrument. In addition, impact assessors should always seek to

keep the number of variables they measure to a manageable number and not be tempted to go for

a comprehensive approach that will impact adversely on data quality and study relevance.

3.1 Unit of Assessment

Unit of assessment in this study is only the borrower. Occasionally studies have

attempted to assess impact at an individual level, but this is relatively rare and has to take a

Page 29

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 24

quantitative focus. More recently some studies have attempted to assess impacts at a number of

levels. The Beneficiary Economic Portfolio Model has been used because institutional impact

was incorporated in the community level analysis. It does have the profound disadvantage of

making assessment demanding in terms of costs, skilled personnel and time. If used with limited

resources it risks sacrificing depth for breadth of coverage of possible impacts.

3.2 Objectives of Impact Assessment

Now a days impact assessment studies are becoming more and more important and

popular with donor agencies and as a result, this activity is becoming necessity of recipient

agencies. This term in general is a substitute for evaluation of the performance of the institution.

These are two major objectives of this impact assessment to prove the impact of microfinance

provided by Akhuwat in the life of its beneficiaries and in the social and economic improvement

of the borrowers. There are many factors that are associated with the two goals. Behind the shift

from evaluation to impact there are number of factors. These factors are not explored in this

research study as the primary goal is to find the impact of micro financing in the life of its

beneficiaries. Explicitly, impact assessment is promoted by both the sponsors and implementers

of programs. They can learn what is being achieved, and thus can, improve the effectiveness and

efficiency of their activities. Implicitly, impact assessment is a method by which sponsors seek to

get more information about program effectiveness than is available from the routine

accountability systems of implementing organizations. Impact assessment has also a great

significance to aid agencies in terms of meeting the ever increasing accountability demands from

their governments and for contesting the contradiction of the anti-aid lobby.

3.3 Methodology

In microfinance impact assessment the borrowers who have received the loans for three

Page 30

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 25

or four times were selected as respondent the people were interviewed about the different

variables, that were chosen as mean of assessment in their life, before the intervention of

Akhuwat in their lives and after the intervention of Akhuwat in their lives.

3.4 Selection of Respondents

Mature borrowers who have been clients of the Akhuwat for more than three years and

continued using the financial services were chosen as respondent on random basis regardless of

the financial position or geographic location.

3.5 Survey and Questionnaire

The survey consisted of following parts:

The first part consisted of the demographics of the respondent

The second part consisted of current position of the respondent

The third art consisted of financial position of the respondent

The fourth part consisted of societal conditions of the respondent

The fifth part consisted of health conditions of the respondent

The sixth part consisted of economic position and economic strength of the respondent

Page 31

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 26

Data Analysis

Years of association with Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid 2 15 5.0 5.1 5.1

3 81 27.2 27.3 32.3

4 45 15.1 15.2 47.5

5 84 28.2 28.3 75.8

6 57 19.1 19.2 94.9

7 5 1.7 1.7 96.6

8 10 3.4 3.4 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The above table mentions the frequency distribution of time period that the borrowers have spent

with Akhuwat the table shows that 3.4% people have been associated with Akhuwat for last eight

years and five percent people are associated with Akhuwat since last two years. The remaining

table shows the same frequencies showing that 27.2% people are associated from last 3 years,

15.1% people are associated with Akhuwat for last 4 years. The above table is briefly explained

in the form of Bar chart which is more easy for he reader to understand the chart is drawn below:

Page 32

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 27

Marital status

Frequency Percent Valid Percent

Cumulative

Percent

Valid

1 No 29 8.7 8.8 8.8

3 Yes 269 91.3 91.2 100.0

Total 298 100.0 100.0

Total 298 100.0

The above table shows the frequency distribution of marital status of the borrowers associated

with Akhuwat. The table shows that 8.7% borrowers are unmarried while 90.3% borrowers are

married and 1% did not respond to this question. The above table is briefly explained in the form

of Bar Chart, which is easier for the reader to understand the chart is drawn below.

Page 33

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 28

Girls attending school before Akhuwat

Frequency Percent Valid Percent Cumulative Percent

Valid

1 Not sending

School 222 74.7 74.7 74.7

3 Govt. School 74 24.9 24.9 99.7

5 Private

School 1 .3 .3 100.0

Total 297 100.0 100.0

The above table shows the frequency distribution of the girls who were not attending school

before association with Akhuwat. The table shows that 74.7% were not attending school and

24.9% were attending government school and 1% were attending private school. Most of its

borrowers before association with Akhuwat were unable to send their girls to good school.

Page 34

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 29

Girls attending school after Akhuwat

Frequency Percent Valid Percent Cumulative

Percent

Valid

1 Not Sending

School 103 34.7 34.7 34.7

3 Govt. School 137 46.1 46.1 80.8

5 Private

School 57 19.2 19.2 100.0

Total 297 100.0 100.0

The above table shows that after associating with Akhuwat the girls starts attending school and

the percentage of girls who were not attending schools went down to 34.7%. 46.1% girls started

attending government school and 19.2% girls started attending private school. So Akhuwat has

improved the living standard of the borrowers.

Page 35

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 30

Head of family income before Akhuwat

Frequency Percent

Valid

Percent

Cumulative

Percent

500-3,000 48 16.1 16.1 16.1

3,500-7,000 117 39.26 39.26 55.36

7,500-13,000 79 26.51 26.51 81.87

15,000-30,000 54 18.12 18.12 100

Total 298 100 100

The table shows that the income of the borrowers was low before they were not associated with

Akhuwat. The maximum income of the borrowers was 30,000 which is also comparatively low.

90% borrowers’ income was less than 17,000 and also the diagram shows that majority of the

people were earning Rs. 3,000 to 8,000 before associating with Akuwat. Some of them were not

earning even a single penny or were earning 1,000 and very few were earning above 15,000.

Hea

d of

fami

ly

inco

me

befo

re

Akh

uwa

t

500-3,000

3,500-7,000

7,500-13,000

15,000-30,000

Page 36

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 31

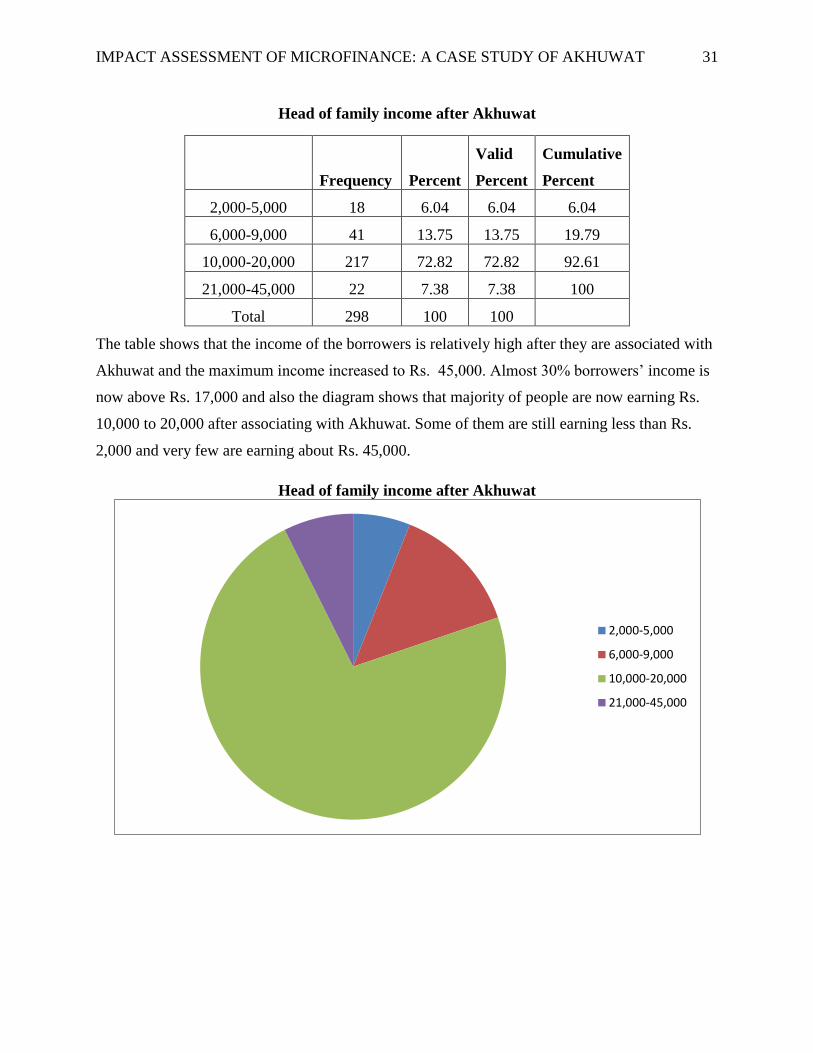

Head of family income after Akhuwat

Frequency Percent

Valid

Percent

Cumulative

Percent

2,000-5,000 18 6.04 6.04 6.04

6,000-9,000 41 13.75 13.75 19.79

10,000-20,000 217 72.82 72.82 92.61

21,000-45,000 22 7.38 7.38 100

Total 298 100 100

The table shows that the income of the borrowers is relatively high after they are associated with

Akhuwat and the maximum income increased to Rs. 45,000. Almost 30% borrowers’ income is

now above Rs. 17,000 and also the diagram shows that majority of people are now earning Rs.

10,000 to 20,000 after associating with Akhuwat. Some of them are still earning less than Rs.

2,000 and very few are earning about Rs. 45,000.

Head of family income after Akhuwat

2,000-5,000

6,000-9,000

10,000-20,000

21,000-45,000

Page 37

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 32

Total family income before Akhuwat

Frequency Percent

Valid

Percent

Cumulative

percent

1,500-5,000 59 19.8 19.8 19.8

6,000-9,000 65 21.8 21.8 41.6

10,000-20,000 130 43.62 43.62 85.22

21,000-31,000 44 14.76 14.76 100

Total 298 100 100

The table shows that the total family incomes were low when the borrowers were not associated

with Akhuwat. The maximum total family income is Rs. 31,000. Which is comparatively low

and almost 80% borrowers income was below than Rs. 16,000. The diagram also shows that the

majority of the families were earning Rs. 7,000 to Rs. 15,000 approximately before associating

with Akhuwat. Some of these were earning below Rs. 1,500 and very few of these were earning

about Rs. 31,000.

Total family income before Akhuwat

1,500-5,000

6,000-9,000

10,000-20,000

21,000-31,000

Page 38

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 33

Total family income after Akhuwat

Frequency Percent

Valid

Percent

Cumulative

Percent

3,000-9,000 14 4.69 4.69 4.69

10,000-15,000 147 49.32 49.32 54.01

16,000-22,000 84 28.18 28.18 82.19

24,000-35,000 53 17.78 17.78 100

Total 298 100 100

This table shows that the borrowers’ total family income increased after associating with

Akhuwat. The maximum income increased to Rs. 40, 000 which is comparatively high. More

than 50% borrowers’ income is more than Rs. 19, 000 and the diagram also shows that the

majority of the families are now earning Rs.10, 000 to Rs. 20,000 after associating with

Akhuwat. Some of these still earning about Rs. 3,000 and very few of these are earning Rs.

40,000.

Total family income after Akhuwat

3,000-9,000

10,000-15,000

16,000-22,000

24,000-35,000

Page 39

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 34

Eating meat before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Once a Month 90 30.2 30.3 30.3

Twice a Month 98 32.9 33.0 63.3

Once a Week 98 32.9 33.0 96.3

Twice a Week 11 3.7 3.7 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The table shows that the meat consumption of the borrowers was low before associating with

Akhuwat the borrowers eat meat only a few times in a month. The 30.2% of the borrowers eat

meat only once a month, 32.9% borrowers eat meat twice a month, 32.9% borrowers eat meat

once a week and only 3.7% eat meat twice a week. Remaining 1% did not eat meat.

Page 40

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 35

Eating meat after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Twice a Month 125 41.9 42.1 42.1

Once a Week 147 49.3 49.5 91.6

Twice a Week 15 5.0 5.1 96.6

Once a Month 10 3.4 3.4 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The above table mentions that the capacity of the borrowers eating meat has increased after they

are associated with Akhuwat. They started eating meat more times before and the table also

shows that 41.9% of the borrowers started eating meat twice a month and the number of

borrowers eating twice a week increased to 5% which is higher than before.

Page 41

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 36

Eating Fruit before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Once a Month 2 .7 .7 .7

Twice a Month 165 55.4 55.6 56.2

Once a Week 118 39.6 39.7 96.0

Twice a Week 7 2.3 2.4 98.3

Almost Daily 5 1.7 1.7 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows the fruit consumption of the borrowers before they were associated with the

Akhuwat and maximum consumption was twice a month. The table also shows that the fruit

eating capacity of the borrowers was low before taking loan from Akhuwat. Almost 56% people

used to eat fruit twice a month. Only 1.7% people were able to eat fruit daily.

Page 42

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 37

Eating Fruit after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Once a Month 1 .3 .3 .3

Twice a Month 151 50.7 50.8 51.2

Once a Week 114 38.3 38.4 89.6

Twice a Week 25 8.4 8.4 98.0

Almost Daily 6 2.0 2.0 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The above table shows that the fruit eating capacity of the borrowers has increased after taking

loan from Akhuwat. Almost 89% people used to eat fruit once a week it means that because of

Akhuwat people shifted from twice a month to once a week. Another important point is that now

almost the ratio of people who were using fruit daily has been doubled from previous.

Page 43

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 38

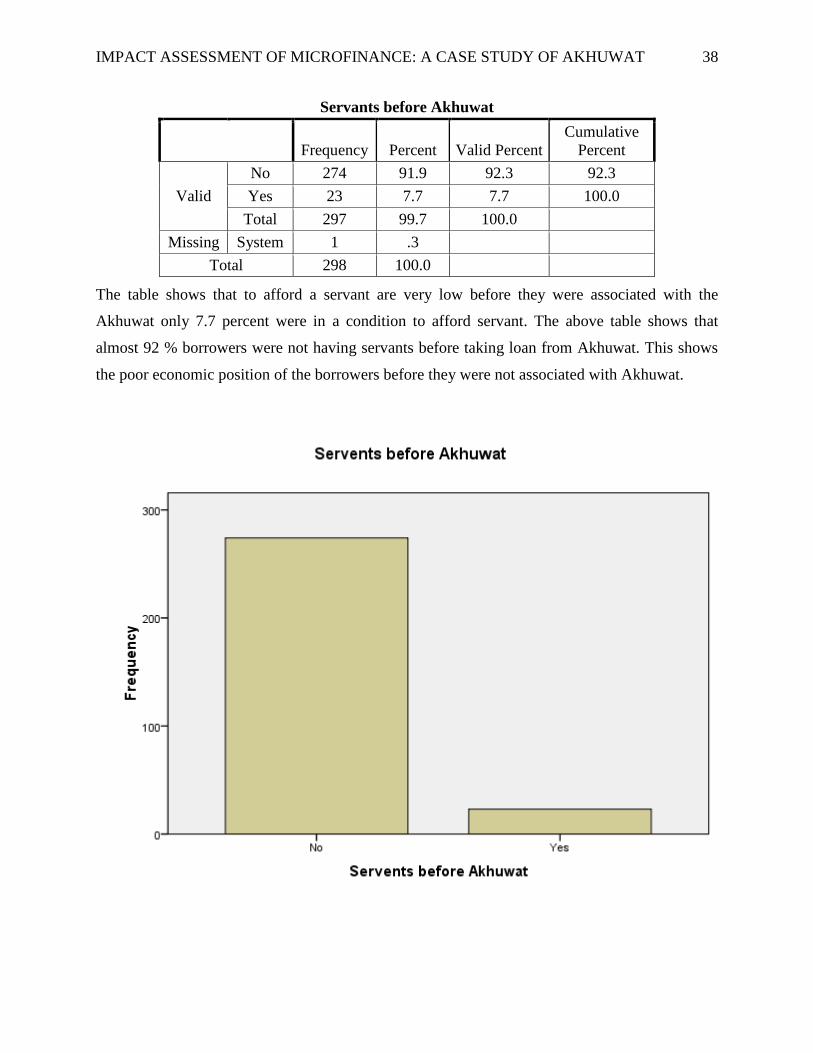

Servants before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 274 91.9 92.3 92.3

Yes 23 7.7 7.7 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The table shows that to afford a servant are very low before they were associated with the

Akhuwat only 7.7 percent were in a condition to afford servant. The above table shows that

almost 92 % borrowers were not having servants before taking loan from Akhuwat. This shows

the poor economic position of the borrowers before they were not associated with Akhuwat.

Page 44

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 39

Servants after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 220 73.8 74.1 74.1

Yes 77 25.8 25.9 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The above table shows that after taking loan from Akhuwat people started to have servants and

now almost 25 percent people are having servants and the percentage of NO has declined from

92 percent to 73.8 percent. This shows that Akhuwat has also increased employment

opportunities for others as well and also making the people in the condition to afford the servant.

Page 45

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 40

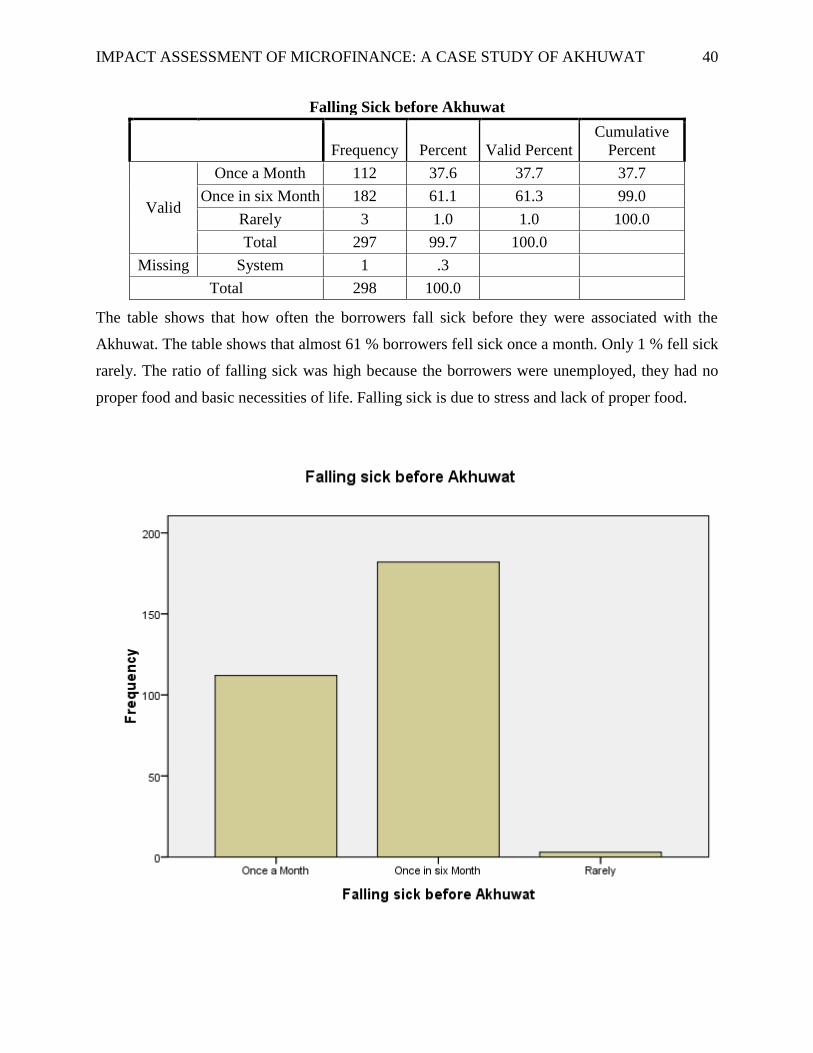

Falling Sick before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Once a Month 112 37.6 37.7 37.7

Once in six Month 182 61.1 61.3 99.0

Rarely 3 1.0 1.0 100.0

Total 297 99.7 100.0

Missing System 1 .3

Total 298 100.0

The table shows that how often the borrowers fall sick before they were associated with the

Akhuwat. The table shows that almost 61 % borrowers fell sick once a month. Only 1 % fell sick

rarely. The ratio of falling sick was high because the borrowers were unemployed, they had no

proper food and basic necessities of life. Falling sick is due to stress and lack of proper food.

Page 46

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 41

Falling Sick after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Once a Month 36 12.1 12.1 12.1

Once in six Month 254 85.2 85.5 97.6

Rarely 7 2.3 2.4 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how often people fell sick after they were associated with the Akhuwat. The

above mentioned table shows that after taking loan from Akhuwat almost only 12 % borrowers

fell sick once a month. The people who got sick rarely have shown an increase which is more

than double as compared to previous. So Akhuwat has reduced the stress of the borrowers thats

why they fell sick rarely.

Page 47

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 42

Medical Treatment before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Dispensary 211 70.8 71.0 71.0

Government Hospital 85 28.5 28.6 99.7

Private Hospital 1 .3 .3 100.0

Total 297 99.7 100.0

Total 298 100.0

The above mentioned table shows the affordability of the medical treatment of the borrowers and

the living standard of borrowers before they were attached with the Akhuwat. The table shows

that only 0.3% people were capable of going to private hospitals and even only 28% people were

capable of going to government hospitals. 70 % borrowers were going to free dispensaries.

Page 48

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 43

Medical Treatment after Akuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Dispensary 145 48.7 48.8 48.8

Government Hospital 151 50.7 50.8 99.7

Private Hospital 1 .3 .3 100.0

Total 297 99.7 100.0

Total 298 100.0

The above mentioned table shows the affordability of the medical treatment of the borrowers and

the living standard of borrowers after they were attached with Akhuwat. The table shows that

only 0.3 % people were capable of going to private hospitals which has not shown any increase

but people were capable of going to government hospitals rather than free dispensaries. The

percentage of people who started going to government hospitals has increased to almost 50 %

which shows an improvement in the living standard of the borrowers. Akhuwat has increased the

living standard of the people.

Page 49

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 44

Visit of Relatives before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Never 277 93.0 93.3 93.3

Once a year 20 6.7 6.7 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how frequently the relatives visit to borrowers before they were not

associated with the Akhuwat and they were not financially strong. The above mentioned table

shows a drastic behavior of our society. The table shows that even relatives did not meet their

poor relatives 93 % people were not visited by their relatives because of their poor economic

conditions. Only 6 % people were visited by their relatives once a year.

Page 50

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 45

Visit of Relatives after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Never 208 69.8 70.0 70.0

Once a year 24 8.1 8.1 78.1

Once in six months 63 21.1 21.2 99.3

Frequently 2 .7 .7 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how frequently the relatives visit to borrowers after they were associated

with the Akhuwat and they were now financially strong. This ratio has decreased to 70 percent

which was previously 93 %. Almost 8 % people were visited by their relative once a year which

has shown an improvement. This is happened just because of Akhuwat and the support of

Akhuwat to the people and by making them financially strong.

Page 51

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 46

Behavior of Relatives before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Dont want to meet 9 3.0 3.0 3.0

Humilating 53 17.8 17.8 20.9

Insulting 8 2.7 2.7 23.6

Show hatred 190 63.8 64.0 87.5

Positive behavior 36 12.1 12.1 99.7

Normal respect 1 .3 .3 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how the relatives behave with borrowers before they were not associated

with Akhuwat. The table shows that even relatives did not respect their poor. 17 % borrowers

were humiliated by their relatives because of their poor economic conditions. 64 % people

showed hatred towards the poor relatives. 12 % people had positive behavior and only 0.3 %

people showed normal behavior.

Page 52

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 47

Behavior of Relatives after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

Don’t want to meet 8 2.7 2.7 2.7

Humiliating 7 2.3 2.4 5.1

Insulting 3 1.0 1.0 6.1

Show hatred 11 3.7 3.7 9.8

Unbiased 1 .3 .3 10.1

Positive behavior 112 37.6 37.7 47.8

Normal respect 1 .3 .3 48.1

Respectfully 153 51.3 51.5 99.7

Total 297 99.7 100.0

Total 298 100.0

The table shows that how the relatives behave with our borrowers after they are associated with

Akhuwat. The above mentioned table shows the behavior of our society. The table shows that

even relatives did not respect their poor relatives. This ratio decreased to 2.7 %. 2.4% borrowers

were humiliated by their relatives because of their poor economic conditions. 3.7 % people

showed hatred towards the poor relatives. 37 % people had positive behavior and 51% people

started giving respect to their relatives with the improvement in their economic conditions.

Page 53

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 48

Relatives and Friends Lends You Money before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 206 69.1 69.4 69.4

Yes 91 30.5 30.6 100.0

Total 297 99.7 100.0

Total 298 100.0

The above mentioned table shows that before taking loan from Akhuwat when the economic

condition of the borrowers was low almost 70 % friends and relatives were not helping their

relatives. Only 30% borrowers were helped by their relatives and friends. This shows the

behavior of relatives and friends. They were not ready to lend money to thoses poor borrowers.

Page 54

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 49

Relatives and Friends Lends You Money after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 75 25.2 25.3 25.3

Yes 222 74.5 74.7 100.0

Total 297 99.7 100.0

Total 298 100.0

The above mentioned table shows that after taking loan from Akhuwat when the economic

condition of the borrowers became better and now only 25 % friends and relatives were not

helping them. Almost 74% borrowers were helped by their relatives and friends because now

their economic position has improved. This shows that the Akhuwat has helped the borrowers

very much because if had made the people financially strong.

Page 55

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 50

Lent Money to Your Friends and Relatives before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 244 81.9 82.2 82.2

Yes 53 17.8 17.8 100.0

Total 297 99.7 100.0

Total 298 100.0

The table mentioned above shows that as the financial position of the borrowers was very weak

before taking loan from Akhuwat. Thus they were not capable of giving loan to their friends and

relatives. Only 17% people were in a position of giving loan to their relatives. Almost 82 %

people were not in a position to help their friends and relatives.

Page 56

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 51

Lent Money to Your Friends and Relatives after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 201 67.4 67.7 67.7

Yes 96 32.2 32.3 100.0

Total 297 99.7 100.0

Total 298 100.0

The table mentioned above shows that as the financial position of the borrowers improved after

taking loan from Akhuwat. After taking loan from Akhuwat the borrowers became capable of

giving loans to their friends and relatives. The percentage increased to 32 % as compared to 17%

before taking loan.

Page 57

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 52

Family and Friends Invitation on Functions before Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid No 40 13.4 13.5 13.5

Some times 198 66.4 66.7 80.1

Yes 59 19.8 19.9 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how often the relatives invite our borrowers before they were not associated

with Akhuwat because they were not financially strong. The values show that 13 % people were

not invited by their friends and relatives on their functions, 66% people were rarely invited by

their friends and relatives and only 19% people were regularly invited by their friends and

relatives.

Page 58

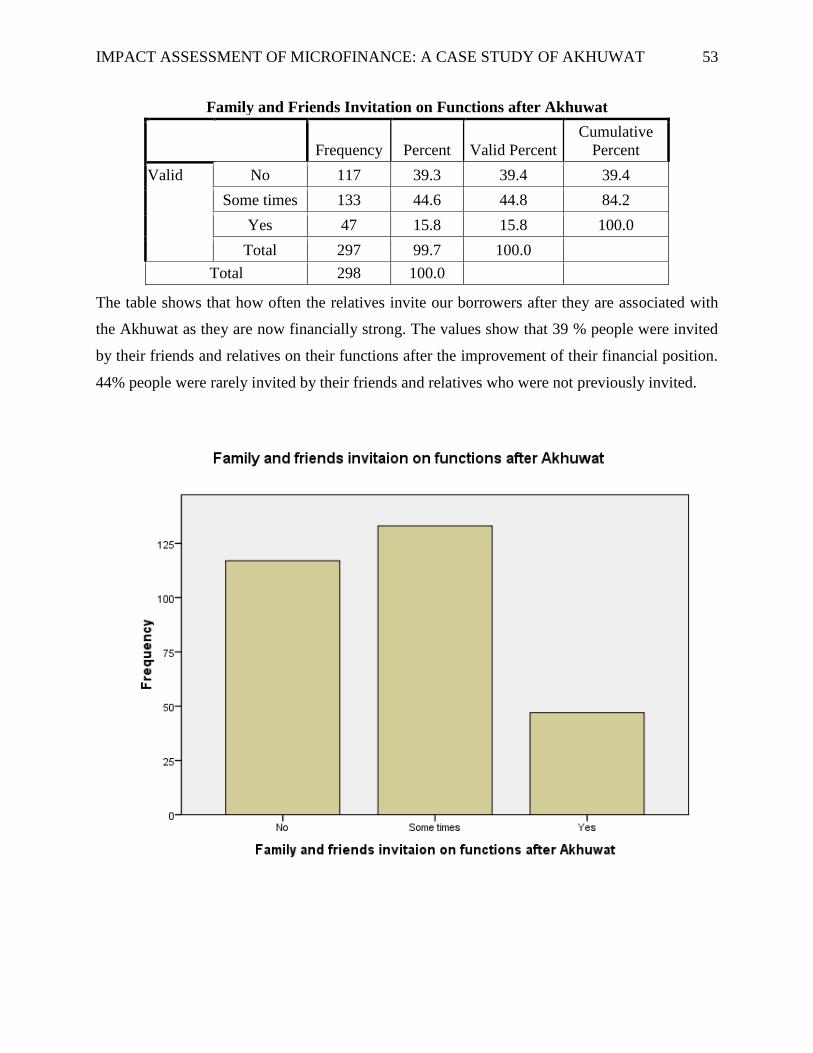

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 53

Family and Friends Invitation on Functions after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid No 117 39.3 39.4 39.4

Some times 133 44.6 44.8 84.2

Yes 47 15.8 15.8 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how often the relatives invite our borrowers after they are associated with

the Akhuwat as they are now financially strong. The values show that 39 % people were invited

by their friends and relatives on their functions after the improvement of their financial position.

44% people were rarely invited by their friends and relatives who were not previously invited.

Page 59

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 54

Family and Friends Involves You in Solving Issues and Problems before

Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 48 16.1 16.2 16.2

Some times 184 61.7 62.0 78.1

Yes 65 21.8 21.9 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that the family and friends did not involve our borrowers in solving the issues

when they were not associated with Akhuwat and they were not financially good. The table

mentioned above shows that people were not involving their friends and family in solving issues

and problems when they were poor. Only 21 % people responded that they were involved by

their friends and families in their problem solving.

Page 60

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 55

Family and Friends Involves You in Solving Issues and Problems after

Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 7 2.3 2.4 2.4

Some times 188 63.1 63.3 65.7

Yes 102 34.2 34.3 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that the family and friends now involve our borrowers in solving their issues

because they are now attached with Akhuwat and are financially good. The table mentioned

above shows that people started involving their friends and family in solving issues and problems

when their economic conditions improved and 34 % people responded that they were involved

by their friends and families in their problem solving.

Page 61

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 56

Involvement of Women in Your Family Decisions before Akuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 27 9.1 9.1 9.1

Some times 170 57.0 57.2 66.3

Yes 100 33.6 33.7 100.0

Total 297 99.7 100.0

Total 298 100.0

The table shows that how many women were given the right to get involved in decision making

from our borrowers who were not associated with the Akhuwat at that time. This table shows the

behavior of the borrowers when they were poor and were in the darkness of poverty. The

behavior of people towards the involvement of their women in decision making was not good

due to frustration and tensions. Only 33 % borrowers used to involve their women in decision

making when they were poor.

Page 62

IMPACT ASSESSMENT OF MICROFINANCE: A CASE STUDY OF AKHUWAT 57

Involvement of Women in your Family Decisions after Akhuwat

Frequency Percent Valid Percent

Cumulative

Percent

Valid

No 9 3.0 3.0 3.0

Some times 175 58.7 58.9 62.0

Yes 113 37.9 38.0 100.0

Total 298 99.7 100.0

Total 298 100.0