www.imrg.org IMRG Capgemini e-Retail Sales Index January 2016 (reporting December 2015 results) What is the IMRG Capgemini e-Retail Sales Index? The IMRG Capgemini e-Retail Sales Index is the primary performance indicator of the UK online shopping industry, tracking 'hard' sales data from reputable e-retailers since April 2000. The participating merchants represent a significant proportion of the UK internet shopping market.

Transcript

www.imrg.org

IMRG Capgemini

e-Retail Sales Index January 2016 (reporting December 2015 results)

What is the IMRG Capgemini e-Retail Sales Index? The IMRG Capgemini e-Retail Sales Index is the primary performance indicator of the UK online

shopping industry, tracking 'hard' sales data from reputable e-retailers since April 2000. The

participating merchants represent a significant proportion of the UK internet shopping market.

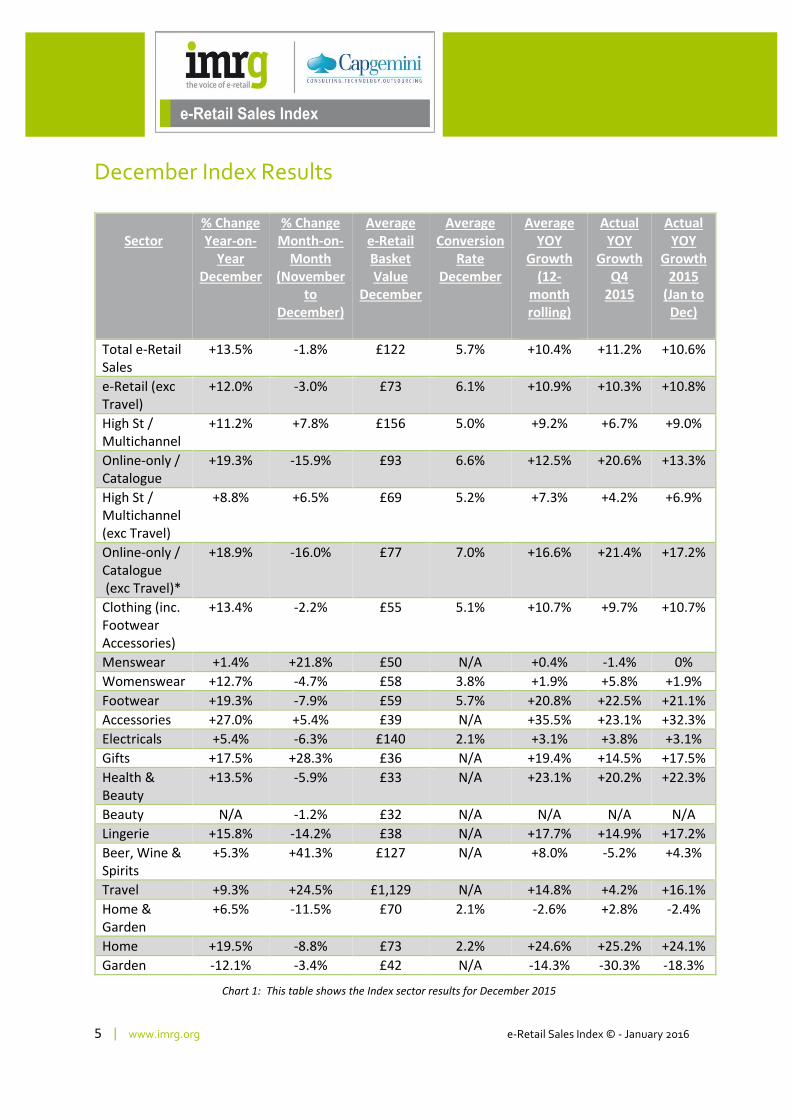

UK e-retail sales grew 13.5% year-on-year in December and fell 1.8% from the previous month

As we observed in 2014, the Index peaked in November due to the effect of sales during Black Friday week (w/c 22nd November)

The monthly decline between November and December 2015 (-1.8%) was less steep than the previous year, when the Index fell 4.1% between November and December 2014

Online sales over the Christmas period (November and December) grew in line with IMRG and Capgemini’s forecast, up 12% year-on-year

Index recorded a week-on-week surge of 62% in e-retail sales in the week of Black Friday – this compares with 44% during the same week in 2014

17% of total online sales during the Christmas period (1st November to 26th December) were during Black Friday week

Strongest performing sectors in December were footwear, accessories, gifts, lingerie and home with year-on-year growth exceeding the overall market performance

Britons spent an estimated £13.1 billion shopping online during December, resulting in total estimated e-retail spend in 2015 reaching £114.9 bn

During 2015 the UK online retail sector recorded annual growth of 11%, slightly below IMRG and Capgemini’s growth forecast of 12%

IMRG and Capgemini forecast the UK e-retail sector will grow 11% during 2016, with estimated online spend (including travel) expected to reach £126 billion

M-retail sales (including tablets) grew 48.3% year-on-year and 11.5% from the previous month

The latest results from the IMRG Capgemini e-Retail Sales Index reveal online sales grew 12% year-on-

year during the festive period (November and December), in line with our overall growth forecast for

2015. For the second year running, the Index recorded a decline between November and December,

due to the effect of Black Friday sales in the last week of November, however, the 1.8% dip was less

steep than the rate observed in 2014 when the Index fell 4.1% during this period.

It is clear that consumers were holding back during October waiting for Black Friday discounts and

promotions, which resulted in the weakest-ever annual growth recorded during that month, while in

November we observed a record monthly rise of 39.8% - the steepest monthly growth ever recorded in

the 15-year history of the Index. During the fourth quarter of 2015 the UK e-retail sector recorded

annual growth of 11.2%, resulting in total growth for the year of 10.6%. The Q4 performance compares

with 12% annual growth in the same period in 2014.

Tina Spooner, Chief Information Officer at IMRG said: “Rounding off a mixed year for e-retail, where we

saw single-digit growth in several months, the UK online retail industry recorded a solid performance in

December, with sales growth significantly higher than the same month in 2014. With December being

the wettest since records began, it appears the unseasonal weather, together with growth in mobile

commerce helped to boost online sales over the festive period. As we observed in 2014, the effect of

Black Friday resulted in November being the peak month for the online retail industry as consumers

brought forward much of their Christmas spending, no doubt boosted by promotional activity around

Looking at conversion rates for the online-only retailers, we can see the average rate has increased 17%

since 2010 – from 4.7% to 5.5% in 2015. Although, conversion rates are lower for high street /

multichannel retailers, the average for this group has increased 21% during the same period, from 3.4%

to 4.1%. The overall e-retail conversion rate reached 4.8% in 2015, up from 4.1% in 2010, representing a

rise of 17%.

Chart 12: This chart shows the average e-retail conversion rates for high st / multichannel and online-only / catalogue retailers

since 2012

Average Conversion Rates

2010 2011 2012 2013 2014 2015

High St / Multichannel

3.4% 3.3% 3.6% 3.8% 4.0% 4.1%

Online-only / Catalogue

4.7% 4.8% 4.4% 5.2% 5.4% 5.5%

Total e-Retail 4.1% 4.0% 4.0% 4.5% 4.6% 4.8% Chart 13: This table shows the average conversion rates for high st / multichannel and online-only / catalogue retailers since 2010

Additional Index results, including supplementary charts and commentary are available on our website.

Please see links below:

Market Information Commentary and Graphs

Total Market Performance Average Basket values Channel performance (Pure Play v Multi Channel) Average Conversion Rates Market Sectors relative Performance

Sectors Information Commentary and Graphs

Accessories Beers, Wines and Spirits Electricals Footwear Gifts Health and Beauty Home and Garden

IMRG Capgemini e-Retail Sales Index Sector Classification The IMRG Capgemini Index records UK online retail sales of the products and services listed in the Index Sector

Classification, as set out below.

INDEX SECTOR CLASSIFICATION These products and services bought online by UK consumers are

recorded by the IMRG Capgemini Index

EXCLUDED FROM INDEX Online spending by UK consumers of these items

is excluded from the IMRG Capgemini Index

Beer / wine / spirits Books CDs / tapes / records Clothing / footwear / accessories Computer hardware / peripherals / consumables Consumer electronics Digital downloads (e.g. music, software) Flowers Food, beverages and household supplies Furniture Garden / DIY Gifts Health and beauty Home appliances (e.g. washing machines) Household goods (e.g. kitchenware, bedding) Jewellery / watches Software Sporting goods Tickets (e.g. cinema, theatre, events) Toys Travel (e.g. flights, holidays, hotels, car hire) Video games Videos / DVDs

Adult Auctions Cars / motor vehicles Gambling Gaming Houses / real estate Telecom services Utilities (e.g. water, heating, electricity) Financial services, e.g. - CREDIT: mortgages, loans, credit cards, overdrafts - INVESTMENT: savings accounts, funds, stocks & shares, bonds, life assurance, pensions - INSURANCE: car, home, life

About the IMRG Capgemini Index:

The IMRG Capgemini Index tracks 'online sales', which we define as 'transactions completed fully, including payment, via interactive channels' from any location, including in-store. These sales are predominantly internet-based today, but the Index remains ready to record e-retail sales conducted via whatever interactive channels the market may embrace in the future.

Over one hundred e-retailers now regularly contribute data to the IMRG Capgemini Index, including: A. Hume Country Clothing, Amara, Appliance House, Arcadia Group (Burton, Top Man, Top Shop, Dorothy Perkins, Evans, Wallis, Miss Selfridge), Ask Direct, ASOS.com, B&Q, Ben Sherman, Berry Bros & Rudd, Blacks, Boden.co.uk, Boots, Brora, Buyagift.com, Carphone Warehouse, Charles Tyrwhitt, Clarks, Clinkards, Crocus.co.uk, Dabs.com, Damart, Debenhams, Deckers, Dunelm Mill, Effortless Skin, Ethical Superstore, Feelunique.com, Firebox, First Choice, Freemans Grattan Holdings (Freemans, Grattan, Look Again, Kaleidoscope, Curvissa, Swimear365, Witt International UK), Game, Get The Label, Greenfingers.com, House of Fraser, HouseTrip.co.uk, JD Sports, JD Williams, John Lewis Partnership, Ladderstore.com, Lakeland Furniture, Liz Earle, LK Bennett, M and M Direct, Made in Design, Majestic Wine, Marks & Spencer, Millets, Moss Bros, Naked Wines, NaturalCollection.com, New Look, Next, Notonthehighstreet.com, Oasis, PetPlanet.co.uk, PetsPyjamas.com, Prezzybox.com, QVC, River Island, Scales Express, Schuh, Scotlight Direct, Scott, Screwfix.com, Shoe-Shop.com, Shop Direct Home Shopping (Littlewoods, Very, Very Exclusive, Serenata Flowers, Silentnight, Size, Sofa and Home, Sparkling Strawberry, Sunshine.co.uk, Tesco.com, The Body Shop, The Great Gift Company, The Mat Factory, The White Company, TUI UK, Turton Wines, Universal Music, Waitrose, Within Home, Woods of Shropshire & Wynsors World of Shoes.

Participation in the IMRG Capgemini Index is available to reputable e-retailers of all sizes. For further details, or to participate in the survey, please contact:

Tina Spooner Chief Information Officer IMRG Tel : +44 (0)203 696 0987 Email: [email protected]

*Estimate of Market Cash Value: 1 Index point currently = GBP £0.77 million

Please note that IMRG has rebased its Index-linked estimates of the UK e-retail market size downwards by 24.9%, and will no longer use Forrester Research’s IMRG Capgemini E-retail Sales Index Multiplier, which we have previously used to estimate the size of the UK e-retail market. IMRG’s own extensive research now provides the basis for the IMRG Index Multiplier, which has been rebased to: - 1 Index point = GBP 0.77 million.

The IMRG Capgemini Index is a trend line that represents the collective gross sales value of participating merchants. We attribute a cash value to an Index point - i.e. a 'multiplier', with which we estimate the market's cash value, month by month. To accommodate the fact that the overall internet shopping market's growth is greater than that of the Index group, as more merchants trade online, we have rebased the multiplier value from time to time:

- November 2008: 1 point = £0.77 million (IMRG) - May 2006: 1 point = £1.02 million (Forrester Research) - January 2005: 1 point = £0.87 million (Forrester Research) - February 2003: 1 point = £0.82 million (Forrester Research) - April 2000: 1 point = £0.8 million (Forrester Research)

We do not recalculate Index cash value estimates retrospectively, as this would skew the historical data.

About IMRG: IMRG (Interactive Media in Retail Group) is the UK’s industry association for e-retail. Formed in 1990, IMRG is setting and maintaining pragmatic and robust e-retail standards to enable fast-track industry growth, and facilitates its community of members with practical help, information, tools, guidance and networking. Consumers can be confident when dealing with IMRG Members because all interact in an environment where they are encouraged to operate using methods that are Honest, Decent, Legal, Truthful and Fair, and have undertaken to not bring the industry into disrepute. The strength of IMRG is the collective and cooperative power of its members. For more information please visit http://www.imrg.org/ or email [email protected].

About Capgemini: With around 120,000 people in 40 countries, Capgemini is one of the world's foremost providers of consulting, technology and outsourcing services. The Group reported 2011 global revenues of EUR 9.7 billion. Together with its clients, Capgemini creates and delivers business and technology solutions that fit their needs and drive the results they want. A deeply multicultural organization, Capgemini has developed its own way of working, the Collaborative Business ExperienceTM, and draws on Rightshore®, its worldwide delivery model. Learn more about us at www.capgemini.com. Rightshore® is a trademark belonging to Capgemini.