22

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | sidney-willy |

| View: | 217 times |

| Download: | 4 times |

In Governmental accounting, the budget is RECORDED in the booksas an integral part of the accounting system.

This allows budgeted amounts to be compared to actualamounts during the year and at year end.

PURPOSE: To record the total ESTIMATED REVENUES expectedto be received during the year.

The government is provided an estimate of what total revenueswill be from various sources (taxes, grants, fines, fees, etc.). Assumeit is $20,000,000.

ENTRY:

ESTIMATED REVENUES……$20,000,000FUND BALANCE (UNRESERVED)….. $20,000,000

IN ADDITION

Must also be updated for EACH TYPE of estimated revenue. This is a supplementary record which records the unique types of estimatedrevenues (taxes, license/permits, intergovernmental, etc.). Illustration 4-3 (page 130)

Each of these entries are DEBITS

Type of estimated revenue

DR CR DR (CR)Est Rev Revenue (actual) Balance

$20,000,000 total (1) $20,000,000

FINALLY

Also impact the budget entries because as they are recorded they are done soas follows:

1. Suppose cash of $12,000,000 is receivedin taxes.

Cash…$12,000,000Revenues…$12,000,000

But in the SUBSIDIARY LEDGER THE FOLLOWINGENTRY IS ALSO POSTED:

DR CR DR (CR)Est Rev Revenue (actual) Balance

$20,000,000 est(from before)

$12,000,000 actual (2) $8,000,000 est to be collected

SUM OF BALANCES OF

REVENUES SUBSIDIARY

LEDGER…$8,000,000

ESTIMATED REVENUES

-

REVENUES------------------------------------REVENUES TO BE COLLECTED

$20,000,000

$12,000,000

$8,000,000

GENERAL FUNDLEDGER

Assets Liabilities

Fund BalanceEst Revenue

$20M 20M

SUBSIDIARY LEDGERS

Tax Est Rev Other Est Rev

5M(madeupbreakdown)

15M

Cash

12M

Revenues

12M

12M

3M

5M + 3M = 8M

$20M - 12M = 8M

PURPOSE: To record the total ESTIMATED EXPENDITURES expectedto be incurred during the year.

The government is provided an estimate of what total expenditureswill be for all possible reasons. These are like the legally voted upon (enacted)estimated and authorized expenditures. Suppose for a year they are $19,000,000.

ENTRY:

FUND BALANCE (UNRESERVED)….$19,000,000APPROPRIATIONS………………..$19,000,000

IN ADDITION

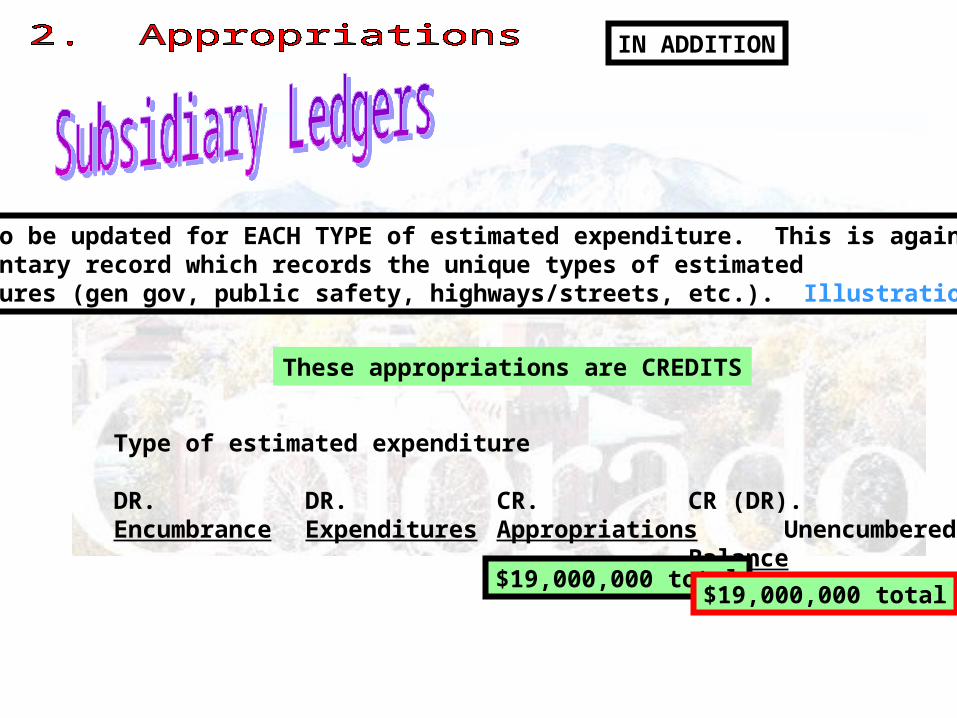

Must also be updated for EACH TYPE of estimated expenditure. This is again a supplementary record which records the unique types of estimatedexpenditures (gen gov, public safety, highways/streets, etc.). Illustration 4-4 (pg 131)

Type of estimated expenditure

DR. DR. CR. CR (DR).Encumbrance Expenditures Appropriations Unencumbered

Balance$19,000,000 total

$19,000,000 total

These appropriations are CREDITS

GENERAL FUNDLEDGER

Assets Liabilities

Fund BalanceEst Revenue

$20M 20M

SUBSIDIARY LEDGERS

Tax Est Rev Other Est Rev

5M(madeupbreakdown)

15M

Cash

12M

Revenues

12M

12M

3M

5M + 3M = 8M

$20M - 12M = 8M

Appropriation

19M

19M

Estimated expenditures (many ofthem)

19M

IMPORTANT TO NOTICE

Fund balance is left with $1,000,000 increase and nothing has even happenedyet.

1M

Thus its important to REVERSE BUDGETARYENTRIES if statements needed to be drawnup in the middle of the year.

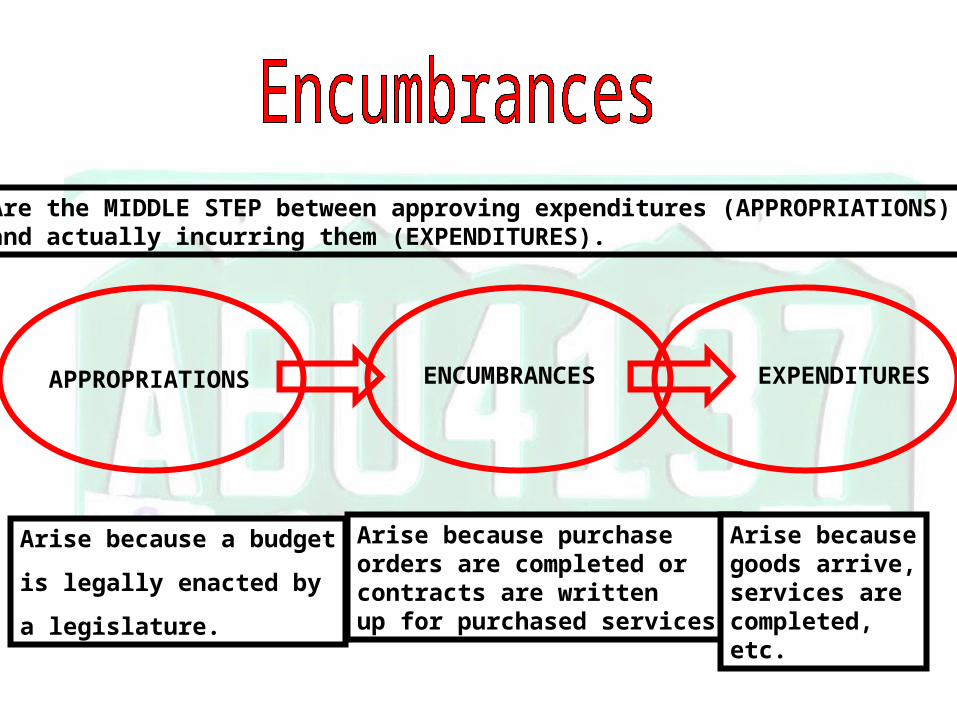

Are the MIDDLE STEP between approving expenditures (APPROPRIATIONS)and actually incurring them (EXPENDITURES).

APPROPRIATIONS ENCUMBRANCES EXPENDITURES

Arise because a budget

is legally enacted by

a legislature.

Arise because purchaseorders are completed orcontracts are writtenup for purchased services.

Arise becausegoods arrive,services are completed,etc.

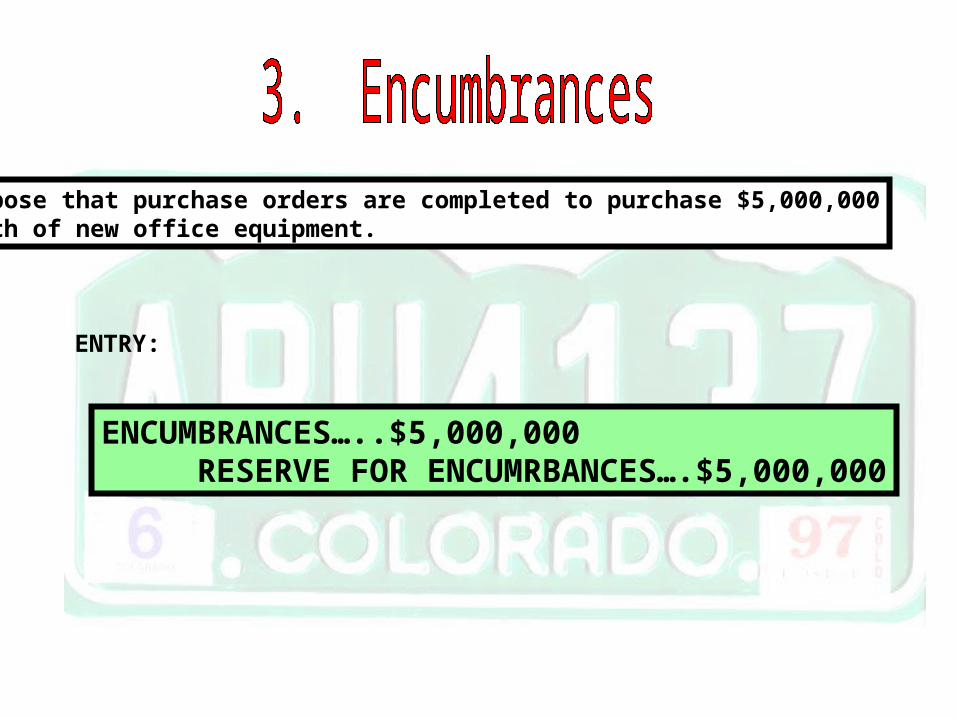

Suppose that purchase orders are completed to purchase $5,000,000worth of new office equipment.

ENTRY:

ENCUMBRANCES…..$5,000,000RESERVE FOR ENCUMRBANCES….$5,000,000

Each encumbrance is then posted to the ENCUMBRANCES COLUMNof the Expenditures Subsidiary Ledger reducing the amountof unencumbered balance of appropriation available for expenditure.

Type of estimated expenditure

DR. DR. CR. CR (DR).Encumbrance Expenditures Appropriations Unencumbered

Balance$19,000,000 from before$5,000,000 $19,000,000

- $5,000,000

$14,000,000

GENERAL FUNDLEDGER

Assets Liabilities

Fund BalanceEst Revenue

$20M 20M

SUBSIDIARY LEDGERS

Tax Est Rev Other Est Rev

5M(madeupbreakdown)

15M

Cash

12M

Revenues

12M

12M

3M

5M + 3M = 8M

$20M - 12M = 8M

Appropriation

19M

19M

Estimated expenditures (many ofthem)

19M

1M

Encumbrance

5M

Reserve for Encum

5M

5M

14M

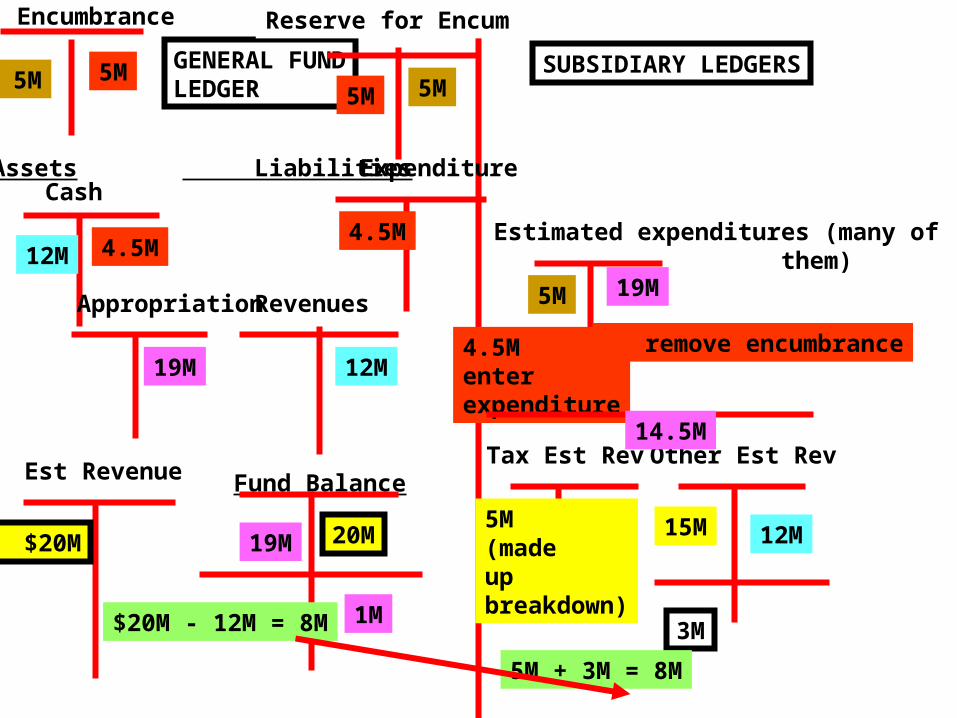

Suppose that the goods ordered previously for $5,000,000 are receivedand that they actually only cost $4,500,000 and that amount is paid incash.

ENTRY: Office Equipment Expenditure….$4,500,000Cash……………………………$4,500,000

ALSO NEED TO REVERSE ENCUMRBANCE AT ITS ESTIMATED AMOUNT:

Reserve for encumbrances…… $5,000,000Encumbrances………………$5,000,000

The unencumbered balance is adjusted for any differencebetween the estimated expenditure (encumbrance) and theactual expenditure. In this case $5M - 4.5M = $500,000

Type of estimated expenditure

DR. DR. CR. CR (DR).Encumbrance Expenditures Appropriations Unencumbered

Balance$19,000,000 from before$5,000,000 $4,500,000

($5,000,000)

$19M (a) -5M ------------$14M -4.5M ------------- 9.5M +5M ------------14.5M

GENERAL FUNDLEDGER

Assets Liabilities

Fund BalanceEst Revenue

$20M 20M

SUBSIDIARY LEDGERS

Tax Est Rev Other Est Rev

5M(madeupbreakdown)

15M

Cash

12M

Revenues

12M

12M

3M

5M + 3M = 8M

$20M - 12M = 8M

Appropriation

19M

19M

Estimated expenditures (many ofthem)

19M

1M

Encumbrance

5M

Reserve for Encum

5M

Expenditure

4.5M4.5M

5M5M

5M

5M remove encumbrance4.5Menterexpenditure

14.5M

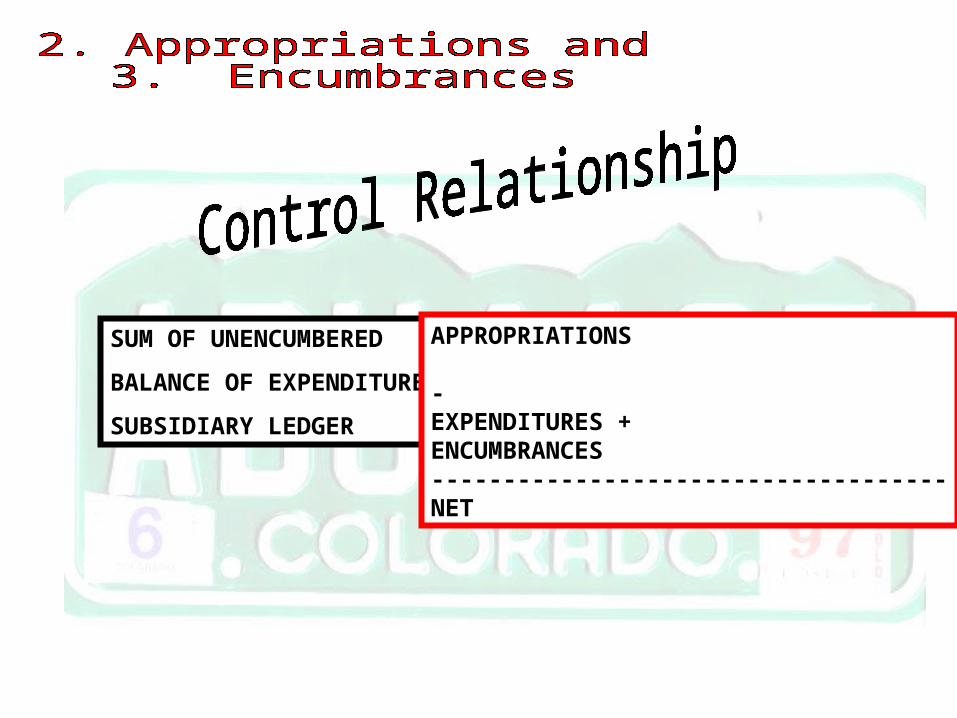

SUM OF UNENCUMBERED

BALANCE OF EXPENDITURES

SUBSIDIARY LEDGER

APPROPRIATIONS

-EXPENDITURES +ENCUMBRANCES------------------------------------NET

SUM OF UNENCUMBERED

BALANCE OF EXPENDITURES

SUBSIDIARY LEDGER

APPROPRIATIONS

-EXPENDITURES +ENCUMBRANCES------------------------------------NET14.5M

19M

4.5M

14.5M