Page 1

1|V

• The40-year-oldglobalwarehouseclubsectorisestimatedtogenerateapproximately$191billioninrevenuesin2017.

• Theclubs’businessmodelseekstolimitgrossprofitssoastoofferlowpricestomemberswhilegeneratingprofitsforshareholdersthroughreasonablemembershipfees.

• ThemajorityoftheclubsarelocatedintheUS,whichaccountedfornearlythree-quartersofsectorrevenuesin2016.Themarketisdominatedbythreecompanies:BJ’sWholesaleClub,CostcoWholesaleandSam’sClub(adivisionofWalmart).

• TheUSwarehouseclubsectorgrewata7.2%CAGRfrom2001through2016.ItsgrowthrateoutpacedthatofthetotalUSretailindustryby3.3percentagepointsovertheperiod.Theinternationalmarketgrewatanevenbrisker10.8%CAGR.

• Yetthesector’sgrowthrateslowedoverthesameperiod,actuallyhittingzeroin2015.AndresearchersareforecastingthattheUSsegmentwillgrowata2.4%CAGR,morethan1.5pointslowerthanoverallretail,from2016through2020.

• Thespoilerbehindthesector’sdeceleratinggrowthratehaslikelybeene-commerce,whichtheclubshavebeenslowtoembrace.Warehouseclubscurrentlygenerate4%orlessoftheirrevenuesfrome-commerce.

• Asisthecasewithmanyotherretailers,warehouseclubsneedtodevelopastrategytocompetewithe-commerceplayers,aswellasleveragetheiruniquestrengthstoadapttootherdemographicandtechnologicalchanges.

InPartOneofthisDeepDive,weprovideanoverviewofthewarehouse-clubsector.

May 29, 2017

Page 2

2

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

AboutThisDeepDive...........................................................................................................................3ExecutiveSummary..............................................................................................................................4WarehouseClubCompaniesataGlance...............................................................................................6SectorOverview...................................................................................................................................7HistoricallyStrongGrowthandOutperformance..................................................................................7SectorInflectionPointin2015............................................................................................................10WarehouseClubCharacteristics.........................................................................................................11Conclusion………………………………………………………………………………………………………………………………………...26

Table of Contents

Page 3

3|V

AboutThisDeepDiveFungGlobalRetail&TechnologyispublishingitsDeepDive:WarehouseClubStores—TimetoTaketheTreasureHuntOnlineinthreeinstallments.

TheExecutiveSummaryoutlinesthespectacularriseofthesectoroverits40-yearhistory.Fromhumblebeginnings,warehouseclubshavegrownintobelovedshoppingdestinationsfortheirmembers,whoenjoylowpricesaswellasthechancetobesurprisedanddelightedastheygoonatreasurehuntthroughthestores.Yettheindustryisatacrossroads,characterizedbyslowinggrowth,demographicchanges,andthechallengespresentedbytheconvenienceandappealofe-commerce.

Part One Overview: Sector Overview PartOneofthereportdiscussesthehistoricalstronggrowthandperformanceofthewarehouseclubsector,itsheavyconcentrationintheUSandthetopthreecompaniesinthespace.Theanalysisrevealsthatthesectorhitaninflectionpointin2015andhasexperiencedaslowinggrowthtrendinrecentyearsthatmarketresearchersexpecttocontinuethrough2020.

Thewarehouseclubsectorfeaturesauniquebusinessmodel,wheremembershipfeesaretheprimarycontributortoprofitsandlargevolumesoffsetultraslimmargins.Whilethemajorityofwarehouseclubmembersareindividualconsumers,smallbusinessesarealsoanimportantcomponentofmembership.Warehouseclubs’growthhasexceededthatofdepartmentstoresandgrocerystores.E-commerce,however,accountsforasmallerpercentageofsalesinthesectorthanitdoesforotherretailsectorsandtheUSretailindustryoverall.ThesectorisledbyCostco,thelargestclubbyrevenue.PartOneconcludeswithananalysisofwarehouseclubsbyregion.

Part Two Overview: Warehouse Club Advantages and Challenges PartTwoofthereportexaminestheadvantagesandchallengeswarehouseclubsface.Theclubsbenefitfromeconomiesofscaleandtheirbroadproductmixes,whichattractshoppers.Theyprovidesignificantvaluepricingtotheircustomers,atreasurehuntshoppingexperiencethatoffersunexpectedsurprisesandbargains,andafocusonorganicproducts.RetailerssuchasCostcoarelocatedintheprosperoustopthirdoftheWeinswigRetailHourglass,amodelthatillustrateshowcompaniesoperatinginthemidmarketgetsqueezed.

Challengesthewarehouseclubsfaceincludeshiftingshopperpreferencesduetogenerationalanddemographicchanges,thesteadyencroachmentofe-commerce,andAmazon’sentryintomultipleareasofcommerce.

Part Three Preview: 10 Topics for Retail, Company Profiles and International Overview PartThreediscusses10topicsaffectingthewarehouseclubsectorandretailingeneral:thechanginggroceryshopper,e-commerce,mobilecommerce,roboticsinretail,privatelabels,thesourcingrevolution,ancillaryproductsandservices,USmarketsaturation,internationalexpansion,andthebriefindependenceofJet.com.

PartThreeconcludeswithprofilesofthetopthreeUSwarehouseclubsandananalysisoftheattractivenessofselectedglobalmarkets.

TheFungGlobalRetail&TechnologyteamhopesthatyouwillfindthisDeepDiveinterestingandinformative!

Page 4

4

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

1

1

Warehouseclubstoreshavehadagreatruninthe40yearssince1976,whenSolPricefoundedthefirstPriceClub,whichultimatelybecametoday’sCostco.Theclubswereinitiallyopenonlytobusinesscustomers,butlaterallowedemployeesofnonprofitandgovernmentorganizationstojoin,andeventuallyopenedtothepublic.Theclubshadauniquebusinessmodel—limitingprofitabilitysoastopassthesavingsontocustomersandmakingthebulkoftheirprofitsfrommembershipfees.Customerslovetheclubs’lowprices,theabilitytobuyinenormousquantitiesandthedelightoffindingunexpectedbargainsintreasurehuntsthroughoutthestores.Therearenotmanystoresinwhichcustomerscanpurchasea20lb.packageofsteaks,aflat-panelTVandadiamondengagementringallinonetrip.

Thewarehouseclubshavesuccessfullyleveragedpostwardemographics,generallysituatingthemselvesinsuburbanareaswithhighmedianincomesandmanysmallbusinessestoserve,offeringconsumersinthoseareastheconveniencetheyneed.Whileshoppersinsuchareastendtobeaffluent,everybodylovesabargain,somanywell-offconsumersshopthewarehouseclubsalongwiththeirmoreprice-consciousneighbors.

Executive Summary

Page 5

5|V

22

Theclubs’popularityhasshownupintheirfinancials.From2001through2016,USwarehouseclubrevenuesgrewataCAGRof6.2%,outpacingthe3.0%annualgrowthrateoftheoverallretailindustrybymorethanthreepercentagepoints.Thesector’sgrowthoutsidetheUSwasevenmorebriskoverthesameperiod,averaging10.8%.Profitabilitydidnotsuffer,either.Despitetheclubs’vowtolimitgrossmarginsinordertoofferattractiveprices,thetopthreeUSwarehouseclubsgenerallyhaveseenoperatingmarginsofaround2%–4%.

Despitethisprosperity,growthhasslowedoverthepast15years,andglobalgrowthgroundtonearzeroin2015,makingitaninflectionpoint.Now,theUSsegmentisforecasttogrowannuallyatabout2.4%,lessthanhalfapointhigherthanthetotalretailindustry.Theslowdowncanbeattributedtochangesindemographicsandthewayspeopleshopand,ofcourse,tothesteadygrowthandencroachmentofe-commerce.In2016,e-commerceaccountedfor8.1%ofUSretailandgrewby15.1%yearoveryear.

Whatshouldthewarehouseclubsdotorecapturetheirpreviousappealtoconsumersandreignitethegrowthratesofyearspast?Clearly,e-commerceispartoftheanswer.Amongthemajorwarehouseclubs,e-commerce’sshareofsalesislikelyhighestatCostco,wherethechannelaccountsfor4%ofrevenues.Oneshort-livedbutinterestingplayerinthee-commercefieldwasJet.com,whichWalmartacquiredin2016.Jetattemptedtocombinethelowpricesofwarehouseclubswiththeconvenienceandeaseofe-commerceandm-commerce.Thecompanyalsoimplementedsomeinnovativewaystoreduceshippingcosts.

Thewarehouseclubsneedtoleveragetheiruniquestrengths,whichincludeprovidinghigh-qualitygoodsatlowpricesandprovidingcustomerswithatreasurehuntexperience,aswellasofferingstrongprivate-labelbrands.Costco’sKirklandSignatureprivatelabelaccountsforaboutone-quarterofthecompany’ssales,makingita$30billionbrand.KirklandSignatureproductsareavailableonAmazon.comandJet.com,andthelabelisarguablyamajorinternationalbrandinitsownright.

WarehouseclubsalsoneedtoadapttothechangingdemographicpatternsofAmericansuburbanlife.Membersofyoungergenerationsareincreasinglylivingincitiesratherthaninsuburbs.Inurbanareas,livingspaceandstorageareatapremium,andmanyurbandwellersdonotownavehiclethattheycandrivetoawarehouseclubandfillwithlarge,bulkypurchases.Tomeettheseconsumers’needs,warehouseclubsshouldexploreofferingmoreoftheirgoodsinsmallerquantitiesonlineandalsoexploredeliverymethodsthate-commercecompaniesareusing,suchasclick-and-collectandexpeditedshipping.

Inthisdeep-divereport,weofferanoverviewofthewarehouseclubsector,analyzethekeyfactorsthatareinfluencingthesectorandprofilethemajorplayers,aswellasprovidesuggestionsonwhatwarehouseclubscandotorecapturethestronggrowththeysawinpreviousperiods.

Page 6

6

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

Warehouse Club Companies at a Glance

Figure1.SelectedMetricsfortheBigThreeUSWarehouseClubs,2016

Category BJ’s1 Costco2 Sam’sClub3Financial NetRevenues(USDBil.) $15.0 $119.6 $57.4YoY%Change 4.0% 2.5% 0.9%

E-Commerce’sShareofRevenues(LastFY) N/A 4.0% 2.8%*MembershipFeeIncome(USDMil.) $270 $2,683 $1,348

GrossMargin 16.5% 13.8% 16.0%

OperatingProfit(USDMil.) $294 $4,211 $1,671OperatingMargin 2.0% 3.5% 2.9%

Membership NumberofMembers(Mil.) 11.1 87.6 60.3PercentBusiness 25% 55% 20%

PercentConsumer 75% 45% 80%Avg.AnnualHouseholdIncome(USD) $59,600 $74,000 $45,000+

MembershipFee—Basic/Premium(USD) $50/$100 $55/$1104 $45/$100Avg. Annual Membership Fee Revenue perMember(USD)5

$25 $32 $23

Stores NumberofClubs—USandPuertoRico 219 506 659NumberofClubs—International — 219 2016

NumberofClubs—Total 219 725 860TotalStoreArea(Mil.Sq.Ft.) 24 104 88

AverageStoreSize(Thous.Sq.Ft.) 107 144 132

Products NumberofSKUs 7,000 4,000 6,000

NumberofPrivate-LabelSKUs 500 550 500

NumberofPrivate-LabelBrands 8 3 11

Other Avg.SalesperClub(USDMil.) $70 $168 $87

Avg.SalesperSq.Ft. $637 $1,168 $659Avg.SalesperEmployee(USDThous.) $571 $554 $497

Avg.SalesperMember(USD) $1,362 $1,405 $970*ForparentcompanyWalmartSource:Companyreports/eMarketer/USCensusBureau/FungGlobalRetail&Technology

1BJ’swasacquiredbyseveralprivateequityfirmsonSeptember30,2011.Thecompany’slastpublicfilingwasforthefiscalyearendedJanuary2011;allsubsequentfiguresareestimates.2FiguresforCostcointhisreportarecalendarized(Costco’sfiscalyearendsAugust31),unlessotherwisenoted.3FiguresforSam’sClubconsiderthefiscalyearashavingendedinDecemberoftheprioryear.4Costcoannouncedthat,effectiveJune1,2017,themembershipfeeforallUSandCanadaGoldStar(individual),BusinessandBusinessadd-onmemberswillriseto$60,andthatmembershipfeesforExecutivemembersintheUSandCanadawillriseto$120.5Averagefeerevenueisbelowthemembershipfeeduetofreememberships(e.g.,Costcoprovidesafreehouseholdcardwithallpaidmemberships).6Sam’sClub’sinternationalstoresarereportedunderWalmart’sInternationalsegment.

Page 7

7|V

HistoricallyStrongGrowthandOutperformanceTotalrevenuesforglobalwarehouseclubsareestimatedtohitarecord$191billionin2017,accordingtoEuromonitorInternational.ThesectorpostedanexceptionalCAGRof7.2%intheUSoverthe15-yearperiodfrom2001through2016,andEuromonitorpredictsthattheglobalsectorwillgrowata4.1%ratefrom2016through2020.

Figure2.GlobalWarehouseClubSectorRevenues(USDBil.)

Source:EuromonitorInternational/FungGlobalRetail&Technology

$0

$50

$100

$150

$200

$250

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E18E19E20E

Sector Overview

Page 8

8

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

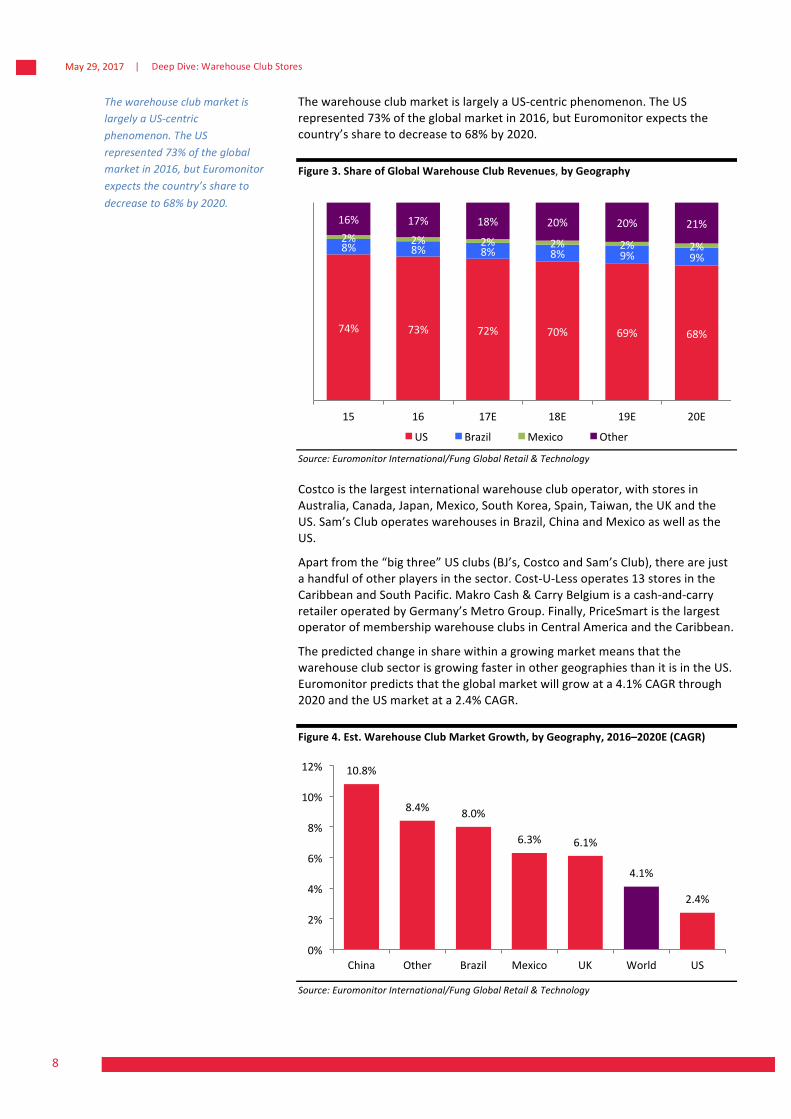

ThewarehouseclubmarketislargelyaUS-centricphenomenon.TheUSrepresented73%oftheglobalmarketin2016,butEuromonitorexpectsthecountry’ssharetodecreaseto68%by2020.

Figure3.ShareofGlobalWarehouseClubRevenues,byGeography

Source:EuromonitorInternational/FungGlobalRetail&Technology

Costcoisthelargestinternationalwarehousecluboperator,withstoresinAustralia,Canada,Japan,Mexico,SouthKorea,Spain,Taiwan,theUKandtheUS.Sam’sCluboperateswarehousesinBrazil,ChinaandMexicoaswellastheUS.

Apartfromthe“bigthree”USclubs(BJ’s,CostcoandSam’sClub),therearejustahandfulofotherplayersinthesector.Cost-U-Lessoperates13storesintheCaribbeanandSouthPacific.MakroCash&CarryBelgiumisacash-and-carryretaileroperatedbyGermany’sMetroGroup.Finally,PriceSmartisthelargestoperatorofmembershipwarehouseclubsinCentralAmericaandtheCaribbean.

ThepredictedchangeinsharewithinagrowingmarketmeansthatthewarehouseclubsectorisgrowingfasterinothergeographiesthanitisintheUS.Euromonitorpredictsthattheglobalmarketwillgrowata4.1%CAGRthrough2020andtheUSmarketata2.4%CAGR.

Figure4.Est.WarehouseClubMarketGrowth,byGeography,2016–2020E(CAGR)

Source:EuromonitorInternational/FungGlobalRetail&Technology

74% 73% 72% 70% 69% 68%

8% 8% 8% 8% 9% 9%

2% 2% 2% 2% 2% 2%

16% 17% 18% 20% 20% 21%

15 16 17E 18E 19E 20E

US Brazil Mexico Other

10.8%

8.4% 8.0%

6.3% 6.1%

4.1%

2.4%

0%

2%

4%

6%

8%

10%

12%

China Other Brazil Mexico UK World US

ThewarehouseclubmarketislargelyaUS-centricphenomenon.TheUSrepresented73%oftheglobalmarketin2016,butEuromonitorexpectsthecountry’ssharetodecreaseto68%by2020.

Page 9

9|V

IntheUS,thesectorisdominatedbyCostco,whichrepresentsabout65%ofthemarketandgeneratesmorethantwicetherevenueofitsnearestcompetitor,Sam’sClub.

Figure5.BigThreeWarehouseClubs:EstimatedRevenue(LeftAxis,USDBil.)andMarketShare(RightAxis,%),2016

FiguresareinUSdollars,convertedbasedonyear-over-yearexchangerates.Source:EuromonitorInternational/FungGlobalRetail&Technology

Inaddition,thesectorhasremainednicelyprofitable,withthebigthreeUSplayerspostingsolidandgrowingprofitsinrecentyears.

Figure6.BigThreeWarehouseClubs:AnnualOperatingIncome(USDBil.)

Source:Companyreports/Bloomberg/NationalRetailFederation(NRF)/KantarWorldpanel/FungGlobalRetail&Technology

$4.9$5.2

$5.5 $5.7$6.2

$0

$1

$2

$3

$4

$5

$6

$7

12 13 14 15 16

Costco SamʼsClub BJʼs

$119.6

$57.4

$15.0

62%

30%

8%

0%

10%

20%

30%

40%

50%

60%

70%

$0

$20

$40

$60

$80

$100

$120

$140

Costco SamʼsClub BJʼs

IntheUS,thesectorisdominatedbyCostco,whichrepresentsabout65%ofthemarketandgeneratesmorethantwicetherevenueofitsnearestcompetitor,Sam’sClub.

Page 10

10

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

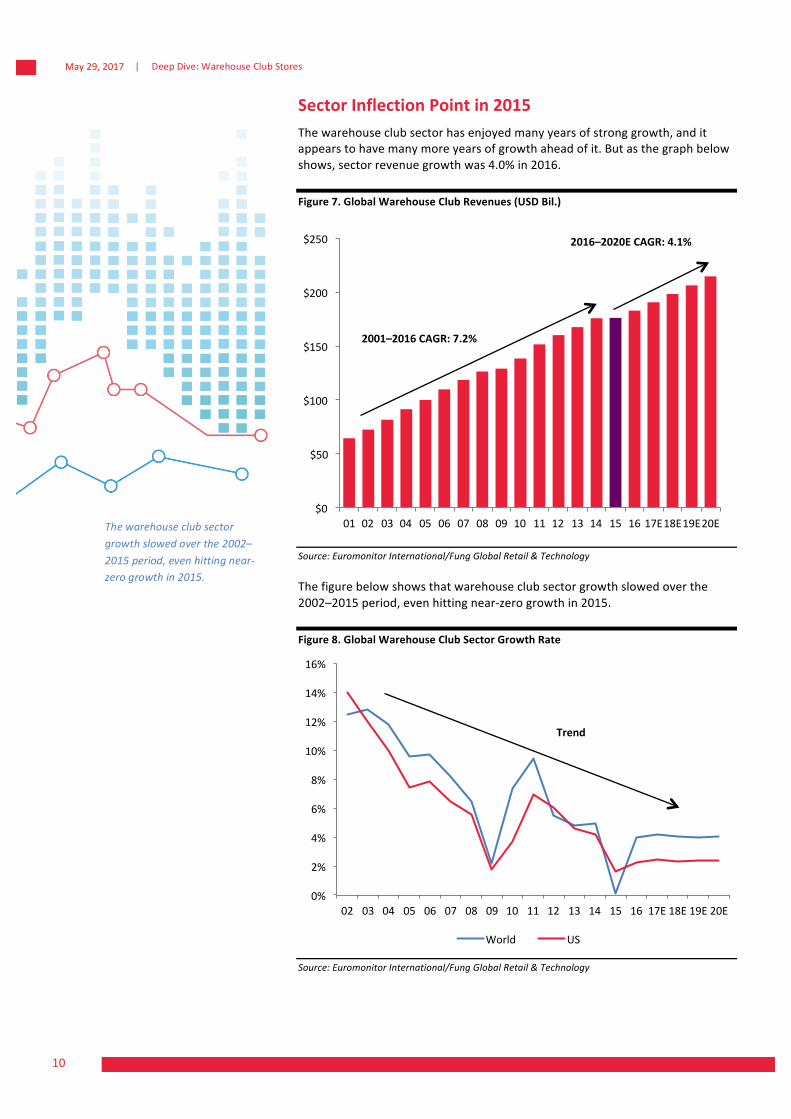

SectorInflectionPointin2015Thewarehouseclubsectorhasenjoyedmanyyearsofstronggrowth,anditappearstohavemanymoreyearsofgrowthaheadofit.Butasthegraphbelowshows,sectorrevenuegrowthwas4.0%in2016.

Figure7.GlobalWarehouseClubRevenues(USDBil.)

Source:EuromonitorInternational/FungGlobalRetail&Technology

Thefigurebelowshowsthatwarehouseclubsectorgrowthslowedoverthe2002–2015period,evenhittingnear-zerogrowthin2015.

Figure8.GlobalWarehouseClubSectorGrowthRate

Source:EuromonitorInternational/FungGlobalRetail&Technology

$0

$50

$100

$150

$200

$250

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 1617E18E19E20E

2001–2016CAGR:7.2%

2016–2020ECAGR:4.1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E18E19E20E

World US

Trend

Thewarehouseclubsectorgrowthslowedoverthe2002–2015period,evenhittingnear-zerogrowthin2015.

Page 11

11|V

WarehouseClubCharacteristics

BusinessModelWarehouseclubssellpaidmembershipstoconsumersandsmallbusinesscustomersthatprovideaccesstoawideselectionofgoods,ofteninbulk,atdiscountedpricesinlarge-storeformats.Groceryproductsareamajordriveroffoottraffic,butshopperscanpurchaseeverythingfromappareltoappliancestoseasonalgoodstoeyeglassesatwarehouseclubs.Attheheartofthewarehouseclubbusinessmodelaremembershipsandeconomiesofscale.Theclubs’largemembershipbasesenablethemtopurchaseitemsfromsuppliersinlargevolumesatlowcost,which,inturn,helpsthemattractmoremembers.Clubscanpriceproductswithjustenoughmarkuptocovercostsandoperatingexpensesand,insomecases,asliverextratocontributetothebottomline.

Attheirinception,warehouseclubssolditemsgearedtowardsmallbusinessowners,generallythemoreaffluentdemographicinaregion.Asthebusinessmodelevolved,theclubsaddedgreat-qualitymerchandiseatbargainpricesfornonbusinessuse,andthetreasurehuntaspectofshoppingintheclubs,whichdelightsconsumers,gainedtractionandbecameintegraltotheclubs’operations.Today,generalconsumersrepresentagreaterportionoftheclubs’membershipbasethanbusinessownersdo.

Thewarehouseclubsectorhasenjoyedresilientgrowththroughmosteconomiccycles,offeringvaluepricingonbrand-namestaplesanddiscretionary“luxuries”whentheeconomystalls,aswellashigh-enditemsthatappealtoshoppersinarobusteconomy.OnarecenttriptowarehousestoresinConnecticut,ourteamfounditemsavailablefromavarietyofwell-knownbrands,includingBosesoundsystems,AppleiPadsandiPhones,Charismasheets,Dockerskhakis,SpeedoswimsuitsandFitbitactivitytrackers.WhileCostcohadluxuriousdiamondringsforsaleat$16,999,Sam’sClubofferedanaspirationalhandbagcollectionfeaturingCoach,KateSpade,MichaelKorsandToryBurch.Inadditiontowell-pricednationalbrands,warehouseclubsareincreasinglyofferingprivate-labelitemsandancillaryservicesthatrangefromgasstationstopharmacies.

BJ’s,Costco,Sam’sClub—theBigThreeTheUS,whichcomprisesthemajorityoftheglobalwarehouseclubmarket,ishometothreemainwarehouseclubcompanies,knownasthebigthree:BJ’s,CostcoandSam’sClub(adivisionofWalmart).

Figure9.BigThreeWarehouseClubs:Revenues,2016(USDBil.)

Source:Companyreports/FungGlobalRetail&Technology

$119.6

$57.4

$15.0

$0

$20

$40

$60

$80

$100

$120

$140

Costco SamʼsClub BJʼs

Warehouseclubssellpaidmembershipstoconsumersandsmallbusinesscustomersthatprovideaccesstoawideselectionofgoods,ofteninbulk,atdiscountedpricesinlarge-storeformats.

Page 12

12

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

MembershipFeesAretheMainProfitDriverWhilesalespermemberdriverevenueatwarehouseclubs,membershipfeesarewhatexpandprofits.Overtime,membershiprevenueexceedsnetincomeandaccountsforasubstantialportionofpretaxoperatingprofits.Weestimatethattotalmembershipfeescontributed70%ofthebigthree’soperatingincomein2016.

Figure10.BigThreeWarehouseClubs:OperatingIncomeBreakdown,2016(USDMil.)

Source:Companyreports/FungGlobalRetail&Technology

AtCostco,membershipfeesexceedednetincomeeveryfiscalyearfrom2004through2016,andfellwithinarangeof69%–86%ofoperatingincome,averaging75%duringtheperiod.Giventheimportanceofmembershipfees,attractingandretainingmembersisapriorityforthecompany.Infiscal2016,Costco’srenewalratewas90%intheUSandCanadaand88%worldwide.

Costcorunsonleanoperatingmarginstoensuremembersavings,andleadsthesectorinsalespermember.Thecompanygenerated45%highersalespermemberthanSam’sClubdidin2016.Costcoalsomaintainsalargeandgrowingmembershipbasethatdrivesprofits.

Figure11.BigThreeWarehouseClubs:MerchandiseRevenueperMember(LeftAxis)andMembershipFeeRevenueperMember(RightAxis),2016

Source:Companyreports/FungGlobalRetail&Technology

$2,683

$1,345$270

$1,528

$326

$24

$4,211

$1,671

$294

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Costco SamʼsClub BJʼs

MembershipFees OtherOperasngIncome

$1,405

$970

$1,362$32

$23 $25

$0

$5

$10

$15

$20

$25

$30

$35

$40

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

Costco SamʼsClub BJʼs

RevenueperMember AverageMembershipFeeperMember

Whilesalespermemberdriverevenueatwarehouseclubs,membershipfeesarewhatexpandprofits.Overtime,membershiprevenueexceedsnetincomeandaccountsforasubstantialportionofpretaxoperatingprofits.

Page 13

13|V

Infiscalyear2016,Costcohadthehighestmembershipofthebigthreewarehouseclubsandonlyabout11%ofitsmembershadexplicitbusinessaccounts.

Figure12.BigThreeWarehouseClubs:MemberComposition,FY16(Mil.)

BJ’sandSam’sClubfiguresareestimates.Source:Companyreports/FungGlobalRetail&Technology

Inrecentyears,CostcoandWalmart(servinghereasaproxyforSam’sClub)bothsawflattishgrowthinthepercentageoftheirrevenuesderivingfrome-commerce.E-commerceaccountsforalowershareofbothcompanies’salesthanitdoesfortheoverallUSretailindustry:in2016,e-commerceaccountedfor8.1%ofallretailsalesintheUS,andgrewby15.1%yearoveryear.

Figure13.CostcoandWalmart:E-Commerce’sShareofSales

Source:Companyreports/InternetRetailer/FungGlobalRetail&Technology

36.8

10.8

39.1

10.9

86.7

50.7

0

10

20

30

40

50

60

70

80

90

100

BJʼs Costco SamʼsClub

Costco-GoldStar Costco-Business

Costco-HouseholdMembers Members

3.0% 3.0% 3.0%

4.0%

1.7%

2.1%

2.5%2.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

FY13 FY14 FY15 FY16

Costco Walmart

Infiscalyear2016,Costcohadthehighestmembershipofthebigthreewarehouseclubsandonlyabout11%ofitsmembershadexplicitbusinessaccounts.

Page 14

14

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

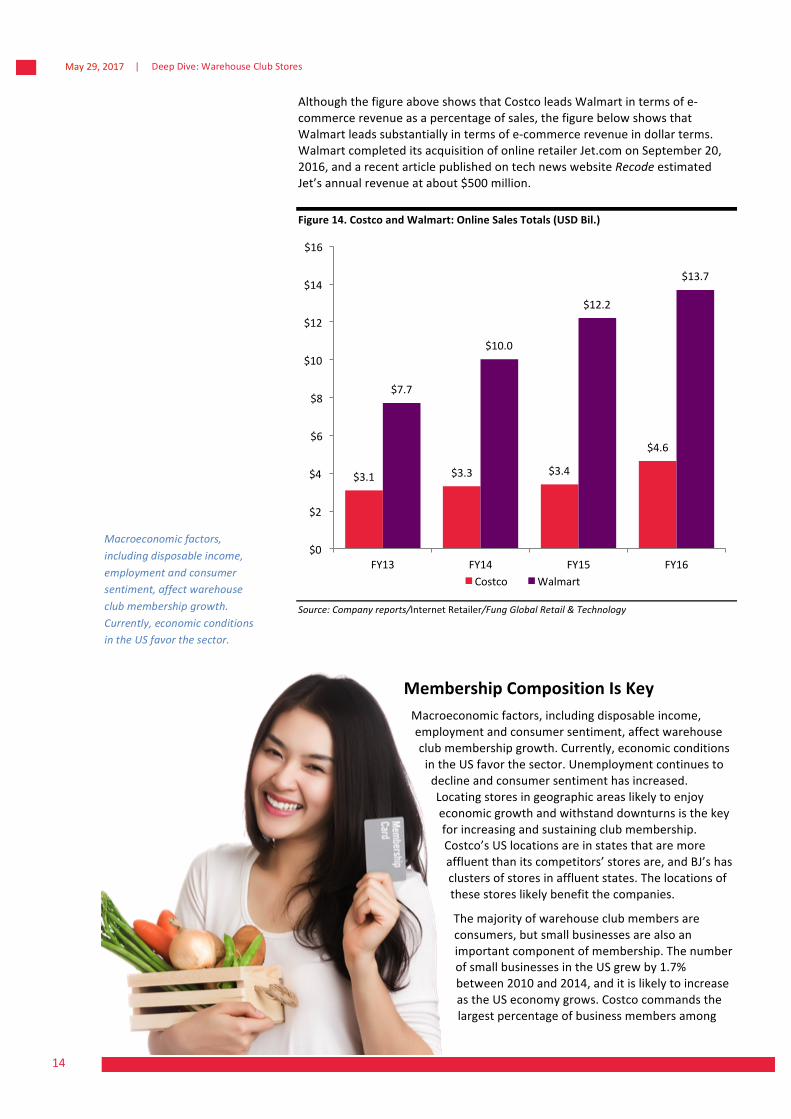

AlthoughthefigureaboveshowsthatCostcoleadsWalmartintermsofe-commercerevenueasapercentageofsales,thefigurebelowshowsthatWalmartleadssubstantiallyintermsofe-commercerevenueindollarterms.WalmartcompleteditsacquisitionofonlineretailerJet.comonSeptember20,2016,andarecentarticlepublishedontechnewswebsiteRecodeestimatedJet’sannualrevenueatabout$500million.

Figure14.CostcoandWalmart:OnlineSalesTotals(USDBil.)

Source:Companyreports/InternetRetailer/FungGlobalRetail&Technology

MembershipCompositionIsKeyMacroeconomicfactors,includingdisposableincome,employmentandconsumersentiment,affectwarehouseclubmembershipgrowth.Currently,economicconditionsintheUSfavorthesector.Unemploymentcontinuestodeclineandconsumersentimenthasincreased.Locatingstoresingeographicareaslikelytoenjoyeconomicgrowthandwithstanddownturnsisthekeyforincreasingandsustainingclubmembership.Costco’sUSlocationsareinstatesthataremoreaffluentthanitscompetitors’storesare,andBJ’shasclustersofstoresinaffluentstates.Thelocationsofthesestoreslikelybenefitthecompanies.

Themajorityofwarehouseclubmembersareconsumers,butsmallbusinessesarealsoanimportantcomponentofmembership.ThenumberofsmallbusinessesintheUSgrewby1.7%between2010and2014,anditislikelytoincreaseastheUSeconomygrows.Costcocommandsthelargestpercentageofbusinessmembersamong

$3.1 $3.3 $3.4

$4.6

$7.7

$10.0

$12.2

$13.7

$0

$2

$4

$6

$8

$10

$12

$14

$16

FY13 FY14 FY15 FY16Costco Walmart

Macroeconomicfactors,includingdisposableincome,employmentandconsumersentiment,affectwarehouseclubmembershipgrowth.Currently,economicconditionsintheUSfavorthesector.

Page 15

15|V

thebigthreewarehouseclubs.Inastrongeconomy,thisisanadvantage,butfallingdemandfromsmallbusinesscustomersinaweakeconomycouldslowthechain’sgrowth.

Figure15.US:SmallBusinessData

2010 2012 2014NumberofSmallBusinesses 5,717,302 5,707,941 5,806,382

%Change — (0.2)% 1.7%

EmploymentbySmallBusinesses 54,996,680 56,062,893 57,894,592

%Change — 1.9% 3.3%2014datawerereleasedonSeptember29,2016.Source:USCensusBureau

SectorPerformanceTheUScontinuestodominatethewarehouseclubsector,asitistheonlyinternationalmarketwithasubstantialnumberofmajorclubchains.TheUSisalsotheonlymajoreconomywhosestatisticsofficeroutinelyreportssectordataforwarehouseclubs.Thesesectordataarebundledwithdataonpredominantlynonfoodsupercenters,suchasthoseoperatedbyWalmart.Inthissection,weexaminefiguresforboththewarehouseclubsectorandthewarehouseclubandsupercentersectorscombined.CostcohasledthegainsintheUSsector.Infiveyears,thecompanygainedmorethantwopercentagepointsofshareofthebroader,combinedwarehouseclubandsupercentersector.

Figure16.BigThreeWarehouseClubs:ShareofWarehouseClubandSupercenterSales

Source:Companyreports/USCensusBureau/FungGlobalRetail&Technology

3.1% 3.1% 3.1% 3.2% 3.3% 3.4%

17.2%18.0% 18.2%

18.9% 19.3% 19.7%

13.9% 13.9% 13.6% 13.4% 12.9%13.0%

0%

5%

10%

15%

20%

25%

2011 2012 2013 2014 2015 2016

BJʼs Costco(US) SamʼsClub

TheUScontinuestodominatethewarehouseclubsector,asitistheonlyinternationalmarketwithasubstantialnumberofmajorclubchains.

Page 16

16

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

TheWarehouseClubSectorHasEnjoyedRobustGrowthInthefaceofcompetitionfromdiscountchannels,Internetpureplaysandspecialists,somenonspecializedretailsectorsarefaltering.Warehouseclubs,though,remainstrong,evencomparedwithrivalgroceryanddepartmentstores.

Figure17.US:SectorSalesforWarehouseClubsandSupercenters,DepartmentStores,andGroceryStores(USDBil.)

Source:Companyreports/USCensusBureau/FungGlobalRetail&Technology

BasedonUSCensusBureaudata,grocerywasthefastest-growingsectorofthethreein2016,withsalesincreasingby2.3%,followedbywarehouseclubsandsupercenters,whichgrewby0.6%.Thedepartmentstoresectordeclinedfortheeleventhconsecutiveyearin2016,shrinkingby3.1%.

$0

$100

$200

$300

$400

$500

$600

$700

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

WarehouseClubsandSupercenters

DepartmentStores

GroceryStores

Inthefaceofcompetitionfromdiscountchannels,Internetpureplaysandspecialists,somenonspecializedretailsectorsarefaltering

Page 17

17|V

Thefigurebelowbreaksdownthebigthreewarehouseclubs’combinedrevenueintermsofdomesticandinternationalsales.Salesinbothmarketsegmentsgrewfrom2012through2016.

Figure18.BigThreeWarehouseClubs:CombinedAnnualSales(USDBil.)

Source:Companyreports/FungGlobalRetail&Technology

Revenuegrowthforthebigthreewarehouseclubswasmuchlowerin2015thanintheimmediatelyprecedingyears,andinternationalgrowthuncharacteristicallylaggedthatoftheUSin2015,largelyowingtodeclinesinBrazilandMexico.

Figure19.BigThreeWarehouseClubs:TotalSalesGrowth

Source:Companyreports/FungGlobalRetail&Technology

$142.0 $146.4 $153.8 $156.3 $159.6

$28.1$30.2 $32.6 $31.5 $32.4$170.1 $176.6

$186.3 $187.8$191.9

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

12 13 14 15 16

US Internasonal

7.5%

3.1%

5.0%

1.6% 2.1%

13.5%

7.2%7.9%

(3.1)%

2.6%

(4)%

(2)%

0%

2%

4%

6%

8%

10%

12%

14%

16%

12 13 14 15 16

US Internasonal

Revenuegrowthforthebigthreewarehouseclubswasmuchlowerin2015thanintheimmediatelyprecedingyears,andinternationalgrowthuncharacteristicallylaggedthatoftheUSin2015,largelyowingtodeclinesinBrazilandMexico.

Page 18

18

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

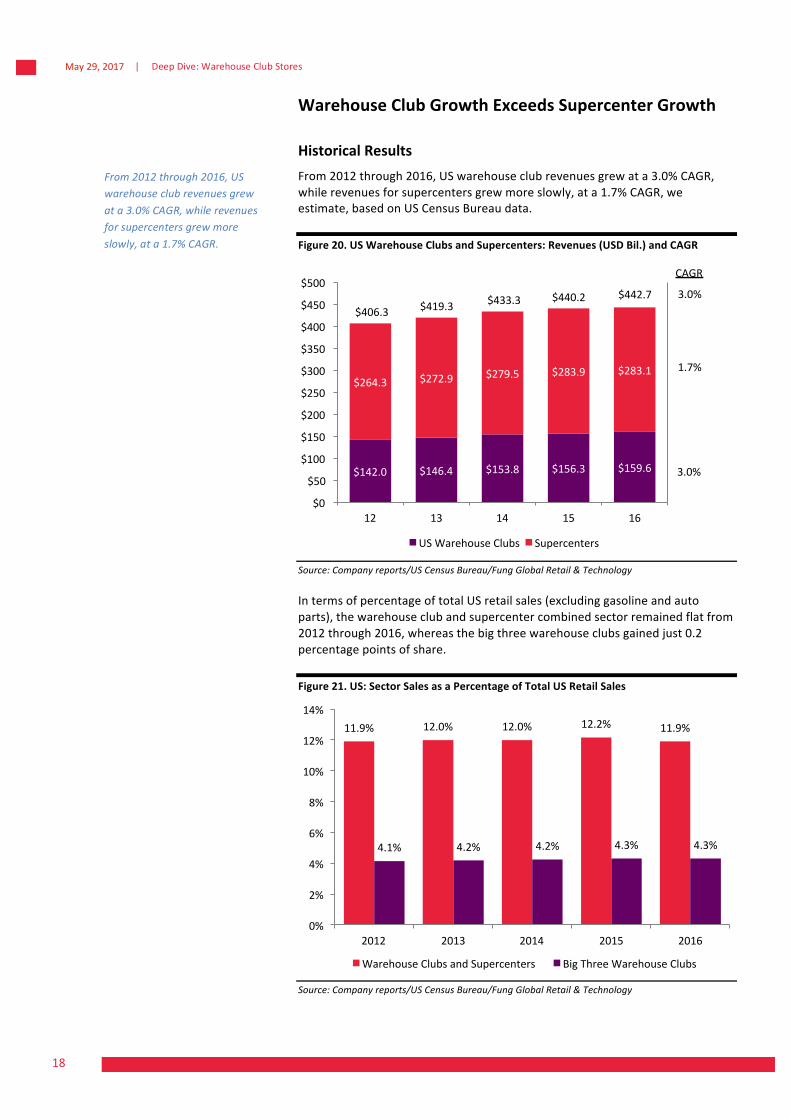

WarehouseClubGrowthExceedsSupercenterGrowth

HistoricalResultsFrom2012through2016,USwarehouseclubrevenuesgrewata3.0%CAGR,whilerevenuesforsupercentersgrewmoreslowly,ata1.7%CAGR,weestimate,basedonUSCensusBureaudata.

Figure20.USWarehouseClubsandSupercenters:Revenues(USDBil.)andCAGR

Source:Companyreports/USCensusBureau/FungGlobalRetail&Technology

IntermsofpercentageoftotalUSretailsales(excludinggasolineandautoparts),thewarehouseclubandsupercentercombinedsectorremainedflatfrom2012through2016,whereasthebigthreewarehouseclubsgainedjust0.2percentagepointsofshare.

Figure21.US:SectorSalesasaPercentageofTotalUSRetailSales

Source:Companyreports/USCensusBureau/FungGlobalRetail&Technology

$142.0 $146.4 $153.8 $156.3 $159.6

$264.3 $272.9 $279.5 $283.9 $283.1

$406.3 $419.3 $433.3 $440.2 $442.7

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

12 13 14 15 16

USWarehouseClubs Supercenters

CAGR

3.0%

1.7%

3.0%

11.9% 12.0% 12.0% 12.2% 11.9%

4.1% 4.2% 4.2% 4.3% 4.3%

0%

2%

4%

6%

8%

10%

12%

14%

2012 2013 2014 2015 2016

WarehouseClubsandSupercenters BigThreeWarehouseClubs

From2012through2016,USwarehouseclubrevenuesgrewata3.0%CAGR,whilerevenuesforsupercentersgrewmoreslowly,ata1.7%CAGR.

Page 19

19|V

RecentResultsDuringthe2016calendaryear,Costcopostedrevenuesof$119.6billion,up2.5%yearoveryear.Comparablestoresalesfortheyearexcludinggasolineincreasedby2.8%.Consensusestimatescallforrevenuesof$126.7billioninfiscalyear2017,up6.7%,andforEPSof$5.91,up10.9%.

Initsfiscalsecondquarterof2017,Costcoreportedatotalcompincreaseof3%,comprisinga3%increaseintheUS,an8%increaseinCanadaanda2%decreaseinotherinternationalregions.

Infiscal2017,Costcoplanstoopeneightnewwarehouses,fiveintheUSandthreeinCanada.

InMarch2015,CostcoannouncedthatVisawouldreplaceAmericanExpressasthecompanyofferingitsrewardscreditcardbeginningApril1,2016,puttinganendtoa16-yearbusinessrelationship.ThistransitionnegativelyimpactedCostco’sfiscalfirst-quarter2016earningsby$15million,or$0.02ashare.Bytheendoffiscal2016,nearly85%of11.4millionAmericanExpresscardshadbeentransferredandactivated,and730,000newmembershadactivatedtheircards;thesefigureswereaheadofthecompany’sinternalexpectations.

Infiscal2017,Sam’sClubreportedrevenuesof$57.4billion,up0.9%yearoveryear.Intheyear,comparablestoresalesincreasedby0.2%includingfuelandincreasedby1.1%excludingfuel.Forthefourthquarteroffiscal2017,Sam’sClubreportedcompsalesgrowth(excludingfuel)of2.4%.Includingfuel,compsincreasedby3.1%.

InOctober2016,anSECfilingdisclosedthatWalmarthadincreaseditsstakeinChinesee-commercecompanyJD.comaftersellingitsstakeintheYihaodianonlinemarketplacetoJD.cominJune.Initsfiscalthird-quarter2017earningscall,WalmartannouncedthatitsSam’sClubflagshipstorehadlaunchedonJD.com’swebsite,offeringhundredsofmillionsofcustomersaccesstoSam’sClub’sproductswithsame-dayandnext-daydeliveryservice.

InMarch2015,CostcoannouncedthatVisawouldreplaceAmericanExpressasthecompanyofferingitsrewardscreditcardbeginningApril1,2016,puttinganendtoa16-yearbusinessrelationship.ThistransitionnegativelyimpactedCostco’sfiscalfirst-quarter2016earningsby$15million,or$0.02ashare

Page 20

20

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

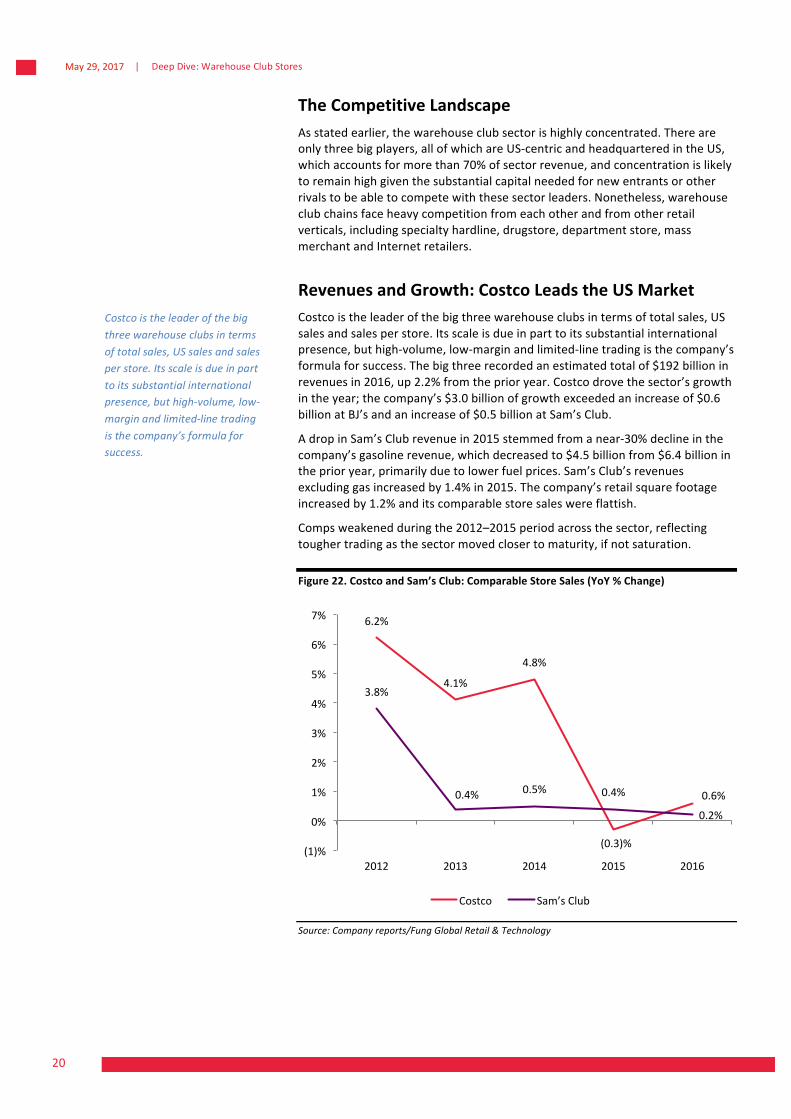

TheCompetitiveLandscapeAsstatedearlier,thewarehouseclubsectorishighlyconcentrated.Thereareonlythreebigplayers,allofwhichareUS-centricandheadquarteredintheUS,whichaccountsformorethan70%ofsectorrevenue,andconcentrationislikelytoremainhighgiventhesubstantialcapitalneededfornewentrantsorotherrivalstobeabletocompetewiththesesectorleaders.Nonetheless,warehouseclubchainsfaceheavycompetitionfromeachotherandfromotherretailverticals,includingspecialtyhardline,drugstore,departmentstore,massmerchantandInternetretailers.

RevenuesandGrowth:CostcoLeadstheUSMarketCostcoistheleaderofthebigthreewarehouseclubsintermsoftotalsales,USsalesandsalesperstore.Itsscaleisdueinparttoitssubstantialinternationalpresence,buthigh-volume,low-marginandlimited-linetradingisthecompany’sformulaforsuccess.Thebigthreerecordedanestimatedtotalof$192billioninrevenuesin2016,up2.2%fromtheprioryear.Costcodrovethesector’sgrowthintheyear;thecompany’s$3.0billionofgrowthexceededanincreaseof$0.6billionatBJ’sandanincreaseof$0.5billionatSam’sClub.

AdropinSam’sClubrevenuein2015stemmedfromanear-30%declineinthecompany’sgasolinerevenue,whichdecreasedto$4.5billionfrom$6.4billionintheprioryear,primarilyduetolowerfuelprices.Sam’sClub’srevenuesexcludinggasincreasedby1.4%in2015.Thecompany’sretailsquarefootageincreasedby1.2%anditscomparablestoresaleswereflattish.

Compsweakenedduringthe2012–2015periodacrossthesector,reflectingtoughertradingasthesectormovedclosertomaturity,ifnotsaturation.

Figure22.CostcoandSam’sClub:ComparableStoreSales(YoY%Change)

Source:Companyreports/FungGlobalRetail&Technology

6.2%

4.1%

4.8%

(0.3)%

0.6%

3.8%

0.4% 0.5% 0.4%

0.2%

(1)%

0%

1%

2%

3%

4%

5%

6%

7%

2012 2013 2014 2015 2016

Costco SamʼsClub

Costcoistheleaderofthebigthreewarehouseclubsintermsoftotalsales,USsalesandsalesperstore.Itsscaleisdueinparttoitssubstantialinternationalpresence,buthigh-volume,low-marginandlimited-linetradingisthecompany’sformulaforsuccess.

Page 21

21|V

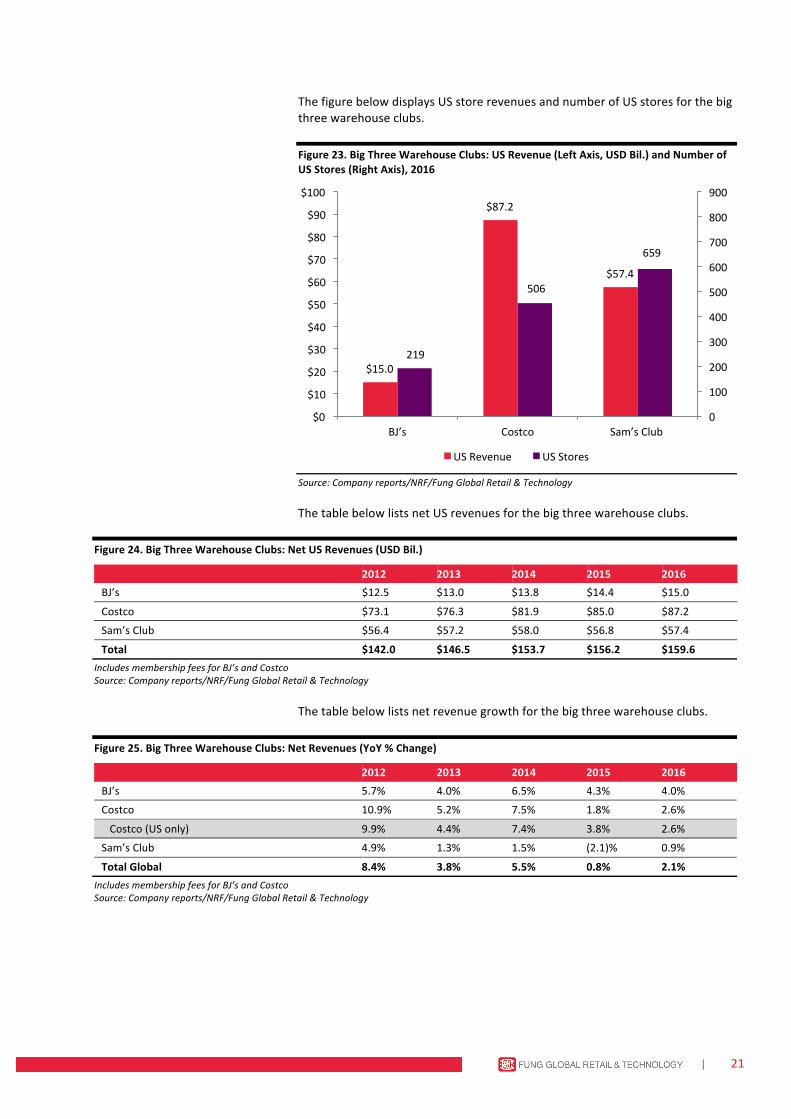

ThefigurebelowdisplaysUSstorerevenuesandnumberofUSstoresforthebigthreewarehouseclubs.

Figure23.BigThreeWarehouseClubs:USRevenue(LeftAxis,USDBil.)andNumberofUSStores(RightAxis),2016

Source:Companyreports/NRF/FungGlobalRetail&Technology

ThetablebelowlistsnetUSrevenuesforthebigthreewarehouseclubs.

Figure24.BigThreeWarehouseClubs:NetUSRevenues(USDBil.)

2012 2013 2014 2015 2016

BJ’s $12.5 $13.0 $13.8 $14.4 $15.0

Costco $73.1 $76.3 $81.9 $85.0 $87.2

Sam’sClub $56.4 $57.2 $58.0 $56.8 $57.4

Total $142.0 $146.5 $153.7 $156.2 $159.6IncludesmembershipfeesforBJ’sandCostcoSource:Companyreports/NRF/FungGlobalRetail&Technology

Thetablebelowlistsnetrevenuegrowthforthebigthreewarehouseclubs.

Figure25.BigThreeWarehouseClubs:NetRevenues(YoY%Change)

2012 2013 2014 2015 2016

BJ’s 5.7% 4.0% 6.5% 4.3% 4.0%

Costco 10.9% 5.2% 7.5% 1.8% 2.6%

Costco(USonly) 9.9% 4.4% 7.4% 3.8% 2.6%

Sam’sClub 4.9% 1.3% 1.5% (2.1)% 0.9%

TotalGlobal 8.4% 3.8% 5.5% 0.8% 2.1%IncludesmembershipfeesforBJ’sandCostcoSource:Companyreports/NRF/FungGlobalRetail&Technology

$15.0

$87.2

$57.4

219

506

659

0

100

200

300

400

500

600

700

800

900

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

BJʼs Costco SamʼsClub

USRevenue USStores

Page 22

22

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

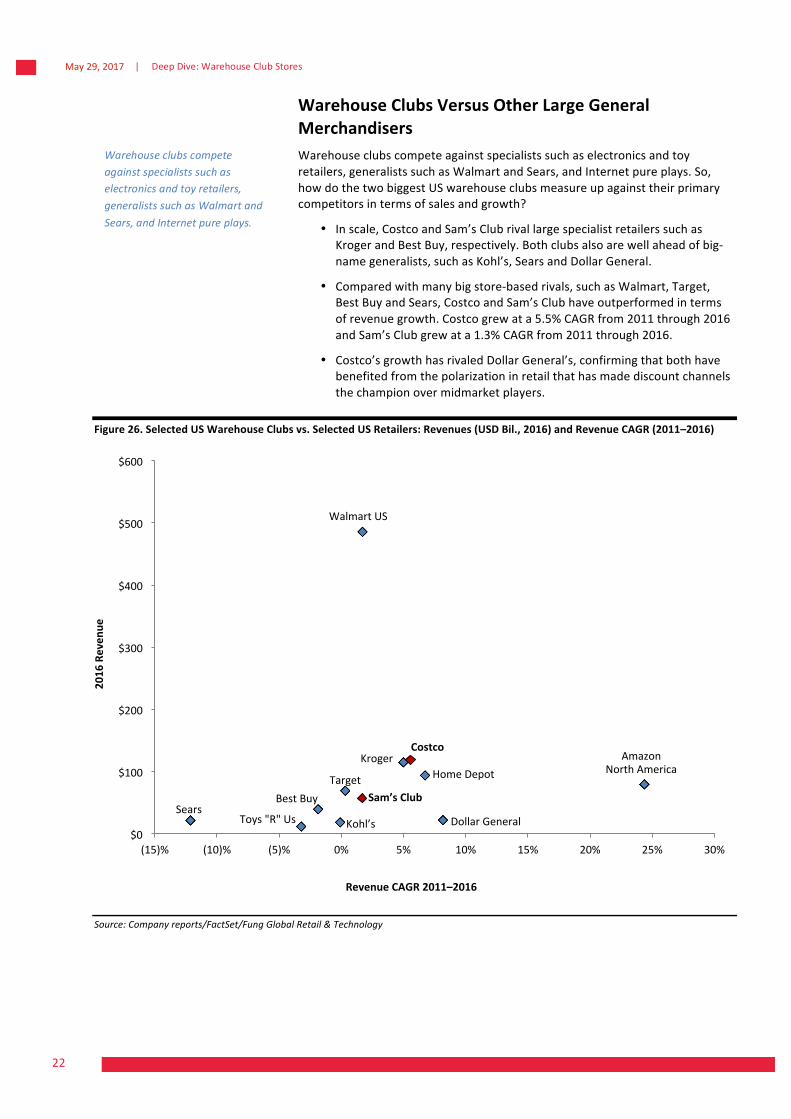

WarehouseClubsVersusOtherLargeGeneralMerchandisersWarehouseclubscompeteagainstspecialistssuchaselectronicsandtoyretailers,generalistssuchasWalmartandSears,andInternetpureplays.So,howdothetwobiggestUSwarehouseclubsmeasureupagainsttheirprimarycompetitorsintermsofsalesandgrowth?

• Inscale,CostcoandSam’sClubrivallargespecialistretailerssuchasKrogerandBestBuy,respectively.Bothclubsalsoarewellaheadofbig-namegeneralists,suchasKohl’s,SearsandDollarGeneral.

• Comparedwithmanybigstore-basedrivals,suchasWalmart,Target,BestBuyandSears,CostcoandSam’sClubhaveoutperformedintermsofrevenuegrowth.Costcogrewata5.5%CAGRfrom2011through2016andSam’sClubgrewata1.3%CAGRfrom2011through2016.

• Costco’sgrowthhasrivaledDollarGeneral’s,confirmingthatbothhavebenefitedfromthepolarizationinretailthathasmadediscountchannelsthechampionovermidmarketplayers.

Figure26.SelectedUSWarehouseClubsvs.SelectedUSRetailers:Revenues(USDBil.,2016)andRevenueCAGR(2011–2016)

Source:Companyreports/FactSet/FungGlobalRetail&Technology

$0

$100

$200

$300

$400

$500

$600

(15)% (10)% (5)% 0% 5% 10% 15% 20% 25% 30%

2016Reven

ue

RevenueCAGR2011–2016

SearsToys"R"Us

BestBuy

Kohlʼs

TargetSamʼsClub

WalmartUS

KrogerHomeDepot

CostcoAmazon

NorthAmerica

DollarGeneral

Warehouseclubscompeteagainstspecialistssuchaselectronicsandtoyretailers,generalistssuchasWalmartandSears,andInternetpureplays.

Page 23

23|V

LargeVolumeCompensatesforUltraslimMarginsWarehouseclubsareinherentlyalow-gross-marginformat:sectorprofitsaredrivenbyvolume,evenmoresothaninotherformsofmass-marketretail.Costcooperatesonespeciallyleangrossmargins,whichfeedthroughtoultraslimoperatingmarginsthatareaninherentpartofitsvalue-for-moneyproposition.Membershipfeescontributethebulkofprofits.Membershiprevenuesalonecontributed2.2%ofCostco’stotalrevenuesinfiscal2016.

Figure27.BigThreeWarehouseClubs:GrossMargin,2016

Source:Companyreports/FungGlobalRetail&Technology

Costco’sreportedandBJ’sestimatedoperatingmarginsgenerallyincreasedduringthe2012–2016period,butSam’sClub’smarginsdeclinedin2015and2016duetohighercostsfrominvestmentinpeople,payroll,technology,promotionsanddemoscombinedwithcostsforexpandedpaymentoptionsandrealestatecharges.

Figure28.BigThreeWarehouseClubs:OperatingMargins,2012–2016

Source:Companyreports/FungGlobalRetail&Technology

11.2%

16.0% 16.5%

Costco SamʼsClub BJʼs

2.8% 2.9% 2.9%3.1%

3.5%3.3% 3.2%

3.4%3.2%

2.9%

1.8% 1.8% 1.9% 1.9% 2.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

12 13 14 15 16

Costco SamʼsClub BJʼs

Warehouseclubsareinherentlyalow-gross-marginformat:sectorprofitsaredrivenbyvolume,evenmoresothaninotherformsofmass-marketretail.Costcooperatesonespeciallyleangrossmargins,whichfeedthroughtoultraslimoperatingmarginsthatareaninherentpartofitsvalue-for-moneyproposition.

Page 24

24

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

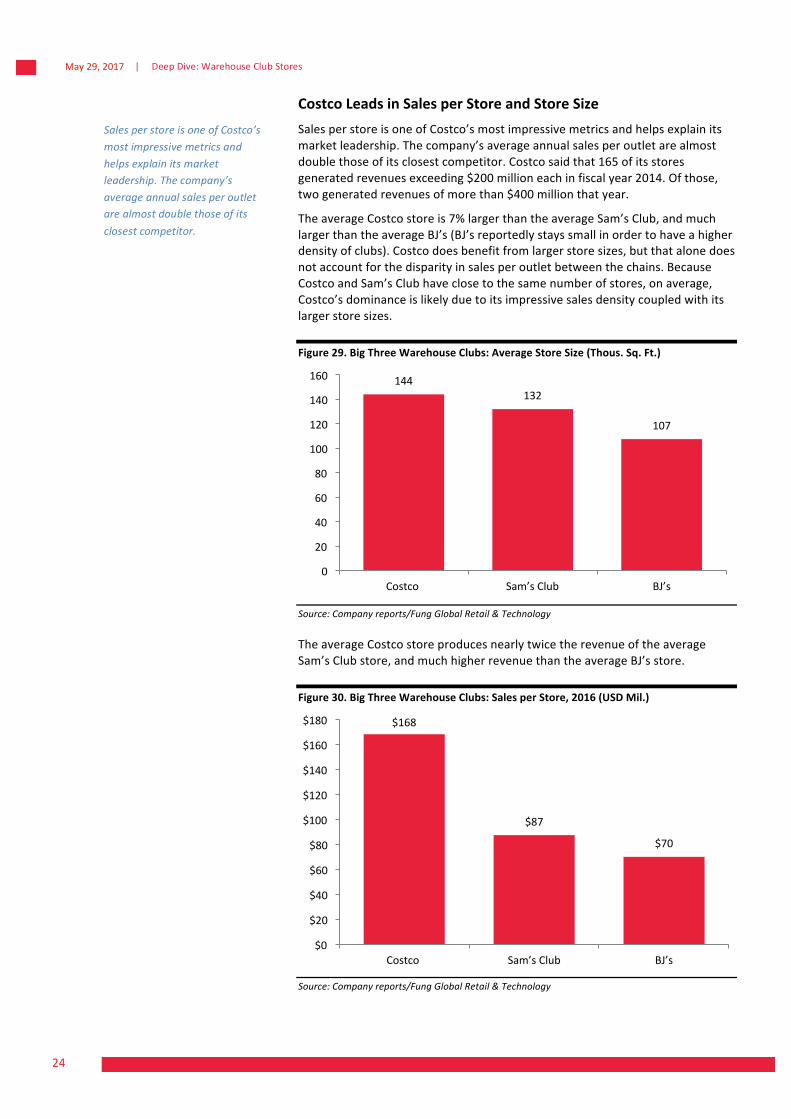

CostcoLeadsinSalesperStoreandStoreSizeSalesperstoreisoneofCostco’smostimpressivemetricsandhelpsexplainitsmarketleadership.Thecompany’saverageannualsalesperoutletarealmostdoublethoseofitsclosestcompetitor.Costcosaidthat165ofitsstoresgeneratedrevenuesexceeding$200millioneachinfiscalyear2014.Ofthose,twogeneratedrevenuesofmorethan$400millionthatyear.

TheaverageCostcostoreis7%largerthantheaverageSam’sClub,andmuchlargerthantheaverageBJ’s(BJ’sreportedlystayssmallinordertohaveahigherdensityofclubs).Costcodoesbenefitfromlargerstoresizes,butthatalonedoesnotaccountforthedisparityinsalesperoutletbetweenthechains.BecauseCostcoandSam’sClubhaveclosetothesamenumberofstores,onaverage,Costco’sdominanceislikelyduetoitsimpressivesalesdensitycoupledwithitslargerstoresizes.

Figure29.BigThreeWarehouseClubs:AverageStoreSize(Thous.Sq.Ft.)

Source:Companyreports/FungGlobalRetail&Technology

TheaverageCostcostoreproducesnearlytwicetherevenueoftheaverageSam’sClubstore,andmuchhigherrevenuethantheaverageBJ’sstore.

Figure30.BigThreeWarehouseClubs:SalesperStore,2016(USDMil.)

Source:Companyreports/FungGlobalRetail&Technology

144132

107

0

20

40

60

80

100

120

140

160

Costco SamʼsClub BJʼs

$168

$87

$70

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

Costco SamʼsClub BJʼs

SalesperstoreisoneofCostco’smostimpressivemetricsandhelpsexplainitsmarketleadership.Thecompany’saverageannualsalesperoutletarealmostdoublethoseofitsclosestcompetitor.

Page 25

25|V

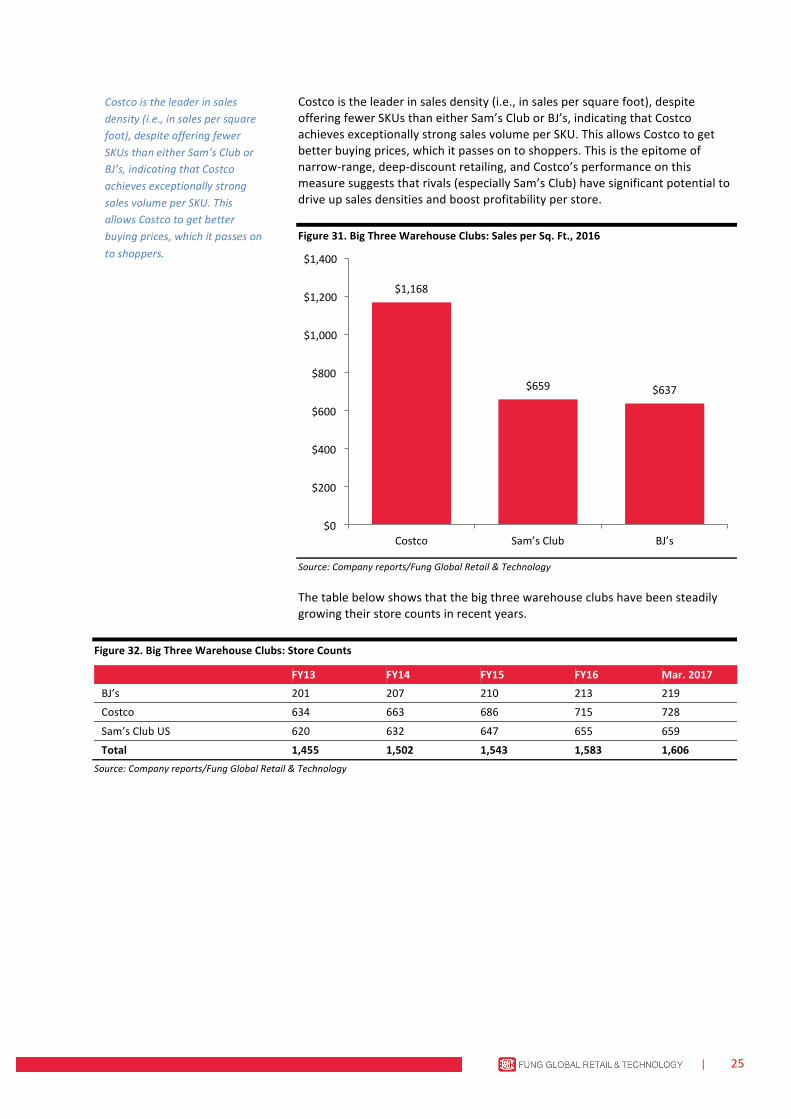

Costcoistheleaderinsalesdensity(i.e.,insalespersquarefoot),despiteofferingfewerSKUsthaneitherSam’sCluborBJ’s,indicatingthatCostcoachievesexceptionallystrongsalesvolumeperSKU.ThisallowsCostcotogetbetterbuyingprices,whichitpassesontoshoppers.Thisistheepitomeofnarrow-range,deep-discountretailing,andCostco’sperformanceonthismeasuresuggeststhatrivals(especiallySam’sClub)havesignificantpotentialtodriveupsalesdensitiesandboostprofitabilityperstore.

Figure31.BigThreeWarehouseClubs:SalesperSq.Ft.,2016

Source:Companyreports/FungGlobalRetail&Technology

Thetablebelowshowsthatthebigthreewarehouseclubshavebeensteadilygrowingtheirstorecountsinrecentyears.

Figure32.BigThreeWarehouseClubs:StoreCounts

FY13 FY14 FY15 FY16 Mar.2017BJ’s 201 207 210 213 219

Costco 634 663 686 715 728

Sam’sClubUS 620 632 647 655 659

Total 1,455 1,502 1,543 1,583 1,606Source:Companyreports/FungGlobalRetail&Technology

$1,168

$659 $637

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Costco SamʼsClub BJʼs

Costcoistheleaderinsalesdensity(i.e.,insalespersquarefoot),despiteofferingfewerSKUsthaneitherSam’sCluborBJ’s,indicatingthatCostcoachievesexceptionallystrongsalesvolumeperSKU.ThisallowsCostcotogetbetterbuyingprices,whichitpassesontoshoppers.

Page 26

26

May29,2017

vV

V|DeepDive:WarehouseClubStores

V

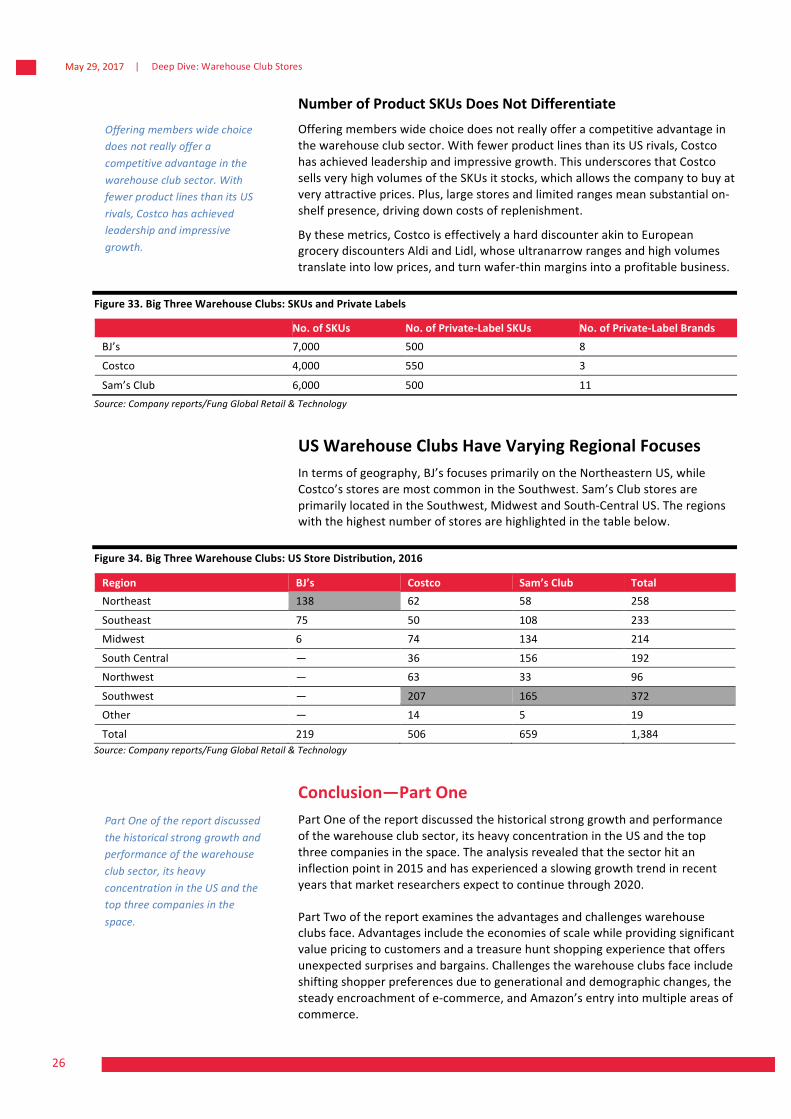

NumberofProductSKUsDoesNotDifferentiateOfferingmemberswidechoicedoesnotreallyofferacompetitiveadvantageinthewarehouseclubsector.WithfewerproductlinesthanitsUSrivals,Costcohasachievedleadershipandimpressivegrowth.ThisunderscoresthatCostcosellsveryhighvolumesoftheSKUsitstocks,whichallowsthecompanytobuyatveryattractiveprices.Plus,largestoresandlimitedrangesmeansubstantialon-shelfpresence,drivingdowncostsofreplenishment.

Bythesemetrics,CostcoiseffectivelyaharddiscounterakintoEuropeangrocerydiscountersAldiandLidl,whoseultranarrowrangesandhighvolumestranslateintolowprices,andturnwafer-thinmarginsintoaprofitablebusiness.

Figure33.BigThreeWarehouseClubs:SKUsandPrivateLabels

No.ofSKUs No.ofPrivate-LabelSKUs No.ofPrivate-LabelBrandsBJ’s 7,000 500 8

Costco 4,000 550 3

Sam’sClub 6,000 500 11Source:Companyreports/FungGlobalRetail&Technology

USWarehouseClubsHaveVaryingRegionalFocusesIntermsofgeography,BJ’sfocusesprimarilyontheNortheasternUS,whileCostco’sstoresaremostcommonintheSouthwest.Sam’sClubstoresareprimarilylocatedintheSouthwest,MidwestandSouth-CentralUS.Theregionswiththehighestnumberofstoresarehighlightedinthetablebelow.

Figure34.BigThreeWarehouseClubs:USStoreDistribution,2016

Region BJ’s Costco Sam’sClub TotalNortheast 138 62 58 258

Southeast 75 50 108 233

Midwest 6 74 134 214

SouthCentral — 36 156 192

Northwest — 63 33 96

Southwest — 207 165 372

Other — 14 5 19

Total 219 506 659 1,384Source:Companyreports/FungGlobalRetail&Technology

Conclusion—PartOnePartOneofthereportdiscussedthehistoricalstronggrowthandperformanceofthewarehouseclubsector,itsheavyconcentrationintheUSandthetopthreecompaniesinthespace.Theanalysisrevealedthatthesectorhitaninflectionpointin2015andhasexperiencedaslowinggrowthtrendinrecentyearsthatmarketresearchersexpecttocontinuethrough2020.

PartTwoofthereportexaminestheadvantagesandchallengeswarehouseclubsface.Advantagesincludetheeconomiesofscalewhileprovidingsignificantvaluepricingtocustomersandatreasurehuntshoppingexperiencethatoffersunexpectedsurprisesandbargains.Challengesthewarehouseclubsfaceincludeshiftingshopperpreferencesduetogenerationalanddemographicchanges,thesteadyencroachmentofe-commerce,andAmazon’sentryintomultipleareasofcommerce.

Offeringmemberswidechoicedoesnotreallyofferacompetitiveadvantageinthewarehouseclubsector.WithfewerproductlinesthanitsUSrivals,Costcohasachievedleadershipandimpressivegrowth.

PartOneofthereportdiscussedthehistoricalstronggrowthandperformanceofthewarehouseclubsector,itsheavyconcentrationintheUSandthetopthreecompaniesinthespace.

Page 27

27|V

DeborahWeinswig,CPAManagingDirectorFungGlobalRetail&TechnologyNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

JohnHarmon,CFASeniorAnalyst

AmyLinResearchAssistant

HongKong:8thFloor,LiFungTower888CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NewYork:1359Broadway,9thFloorNewYork,NY10018Tel:6468397017FungGlobalRetailTech.com