Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 1 of 45 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK IN RE SANOFI SECURITIES LITIGATION Case No. 13-CIV-8806 (PAE) AMENDED COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS AMENDED CLASS ACTION COMPLAINT Lead Plaintiff Glenn Tongue, individually and in his capacity as General Partner of Deerhaven Capital Management ("Lead Plaintiff'), individually and on behalf of all other persons similarly situated, by its undersigned attorneys, for its complaint against defendants, alleges the following based upon personal knowledge as to itself and its own acts, and information and belief as to all other matters, based upon, inter al/a, the investigation conducted by and through its attorneys, which included, among other things, a review of the defendants' public documents, conference calls and announcements made by defendants, United States Securities and Exchange Commission ("SEC") filings, wire and press releases published by and regarding Sanofi ("Sanofi" or the "Company"), analysts' reports and advisories about the Company, and information readily obtainable on the Internet. Lead Plaintiff believes that substantial evidentiary support will exist for the allegations set forth herein after a reasonable opportunity for discovery. NATURE OF THE ACTION AND RELEVANT BACKGROUND 1. This is a federal securities class action on behalf of a class consisting of all persons other than Defendants (defined herein) who purchased Sanofi contingent value rights ("CVR5" or "shares") between March 6, 2012 and November 7, 2013, inclusive (the "Class Period"), seeking to recover damages caused by Defendants' violations of the federal securities laws and to pursue remedies under the Securities Exchange Act of 1934 (the "Exchange Act").

Transcript

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 1 of 45

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK

IN RE SANOFI SECURITIES LITIGATION

Case No. 13-CIV-8806 (PAE)

AMENDED COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS

AMENDED CLASS ACTION COMPLAINT

Lead Plaintiff Glenn Tongue, individually and in his capacity as General Partner of

Deerhaven Capital Management ("Lead Plaintiff'), individually and on behalf of all other persons

similarly situated, by its undersigned attorneys, for its complaint against defendants, alleges the

following based upon personal knowledge as to itself and its own acts, and information and belief

as to all other matters, based upon, inter al/a, the investigation conducted by and through its

attorneys, which included, among other things, a review of the defendants' public documents,

conference calls and announcements made by defendants, United States Securities and Exchange

Commission ("SEC") filings, wire and press releases published by and regarding Sanofi ("Sanofi"

or the "Company"), analysts' reports and advisories about the Company, and information readily

obtainable on the Internet. Lead Plaintiff believes that substantial evidentiary support will exist for

the allegations set forth herein after a reasonable opportunity for discovery.

NATURE OF THE ACTION AND RELEVANT BACKGROUND

1. This is a federal securities class action on behalf of a class consisting of all persons

other than Defendants (defined herein) who purchased Sanofi contingent value rights ("CVR5" or

"shares") between March 6, 2012 and November 7, 2013, inclusive (the "Class Period"), seeking to

recover damages caused by Defendants' violations of the federal securities laws and to pursue

remedies under the Securities Exchange Act of 1934 (the "Exchange Act").

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 2 of 45

2. According to its public filings, Sanofi is a global pharmaceutical group engaged in the

research, development, manufacturing and marketing of healthcare products. Sanofi is the fifth

largest pharmaceutical group in the world and the third largest pharmaceutical group in Europe.

The Company operates three main product segments: Pharmaceuticals, Human Vaccines, and

Animal Health.

3. The Company is in a heavily regulated industry, and several of the Company's

products are regulated by the United States Food and Drug Administration ("FDA"), which

oversees the Company's compliance with applicable rules and regulates the Company's covered

products such as vaccines and pharmaceuticals.

4. In 2010, despite booming performance, Sanofi saw that the future presented

substantial obstacles for its continued profitability. The patent on the Company's blockbuster drug

Plavix, which provides protection against heart attack or stroke in patients with a history of heart

disease, would expire in the first quarter of 2012. Plavix's success while under patent was

phenomenal, as the drug became among the most prescribed in history and the best selling drug in

America during the first quarter of 2012.

5. Because of the Company's success with Plavix, and its healthy balance sheet, Sanofi

was in a position whereby it could "buy" its future growth. Thus, to combat the impending "patent

cliff," Sanofi sought acquisition candidates by which it could acquire new pipeline drugs that would

come to market in or around the time that the patent for Plavix would expire thereby smoothing out

the Company's impending loss of revenue. The "patent cliff' is an industry-wide term used to

reference the confluence of events that would lead 18 of the 20 historically best-selling drugs to

lose their patents between 2009 and 2015 at an expected cost of $170 billion in sales for the

companies who own the patents. For Sanofi, 2012 would be its most difficult year, losing

2

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 3 of 45

exclusivity in the U.S. for Plavix, Avapro (hypertension), and Eloxatin (colon and colorectal

cancer). The expiration of Plavix's patent meant that generic drug manufactures would soon be

able to manufacture and sell generic versions of the Company's blockbuster drug, ending the

Company's exclusive hold on profits.

6. To achieve this goal, Sanofi set its sights on (and later acquired) Genzyme Corporation

("Genzme"), which owned Lemtrada, an unapproved-yet-purportedly-promising treatment for

multiple sclerosis - a market estimated to be worth $14 billion worldwide. During the Class Period,

Sanofi (and (I}enzyme as its subsidiary) strongly touted the efficacy and safety of Lemtrada.

7. Part of the reason why Lemtrada presented such an opportunity to become a profitable

drug is that its unique dosing regimen makes it very desirable to patients and doctors. Unlike many

MS drugs which must be taken on a daily basis, Lemtrada's appeal lies in the fact that its

administration schedule consists of just two annual treatment courses. The first treatment course of

Lemtrada is administered via intravenous infusion on five consecutive days, and the second course

is administered on three consecutive days, 12 months later.

8. Sanofi first bid for Genzyme on August 30, 2010, offering $18.5 billion for the

Cambridge, Massachusetts based company. This offer was rejected by the Genzyme Board of

Directors until Sanofi upped its offer in February 2011. On February 16, 2011, Sanofi signed an

agreement (the "Merger Agreement") to acquire Genzyme and substantially all of Genzyme's assets

for just over $20 billion.

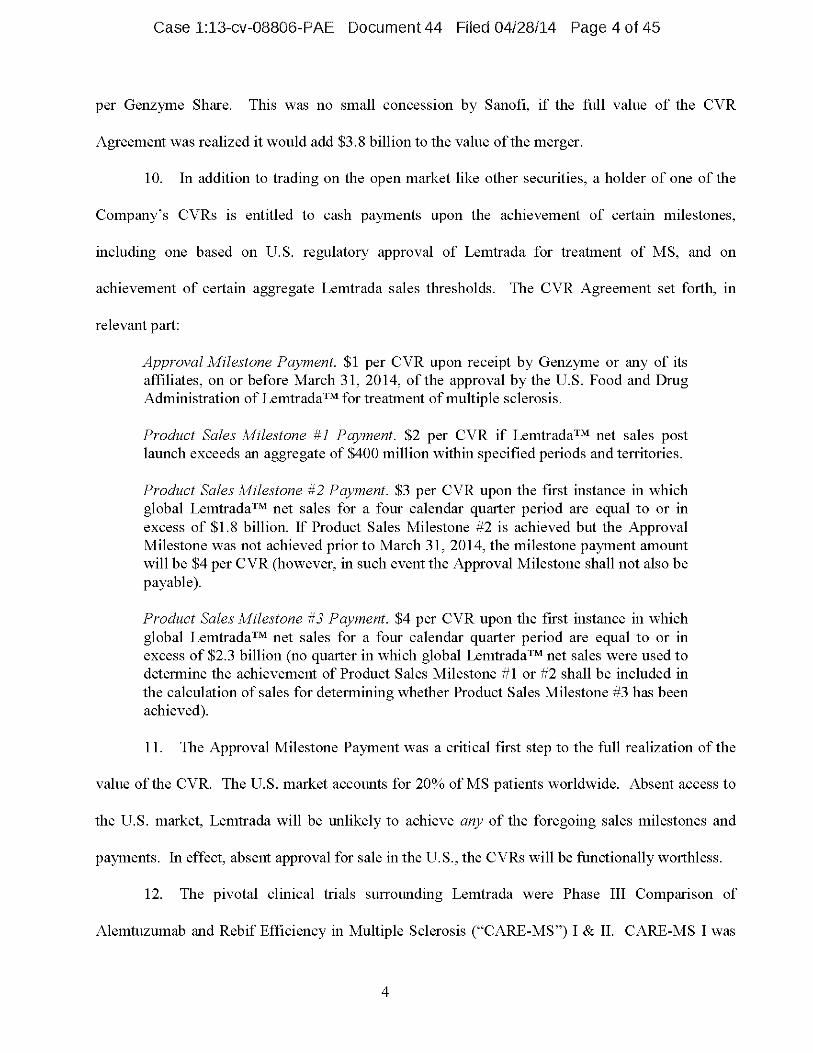

9. In connection with the Genzyme acquisition, Sanofi agreed to amend the outstanding

tender offer to acquire all of the outstanding shares of common stock of Genzyme (the "Genzyme

Shares") in order to increase the price per share from $69.00 to $74.00 in cash plus one CVR to be

issued by Sanofi, subject to, and in accordance with, a CVR agreement (the "CVR Agreement"),

3

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 4 of 45

per Genzyme Share. This was no small concession by Sanofi, if the full value of the CVR

Agreement was realized it would add $3.8 billion to the value of the merger.

10. In addition to trading on the open market like other securities, a holder of one of the

Company's CVRs is entitled to cash payments upon the achievement of certain milestones,

including one based on U.S. regulatory approval of Lemtrada for treatment of MS, and on

achievement of certain aggregate Lemtrada sales thresholds. The CVR Agreement set forth, in

relevant part:

Approval Milestone Payment. $1 per CVR upon receipt by Genzyme or any of its affiliates, on or before March 31, 2014, of the approval by the U.S. Food and Drug Administration of LemtradaTM for treatment of multiple sclerosis.

Product Sales Milestone #1 Payment. $2 per CVR if LemtradaTM net sales post launch exceeds an aggregate of $400 million within specified periods and territories.

Product Sales Milestone #2 Payment. $3 per CVR upon the first instance in which global LemtradaTM net sales for a four calendar quarter period are equal to or in excess of $1.8 billion, if Product Sales Milestone #2 is achieved but the Approval Milestone was not achieved prior to March 31, 2014, the milestone payment amount will be $4 per CVR (however, in such event the Approval Milestone shall not also be payable).

Product Sales Milestone #3 Payment. $4 per CVR upon the first instance in which global LemtradaTM net sales for a four calendar quarter period are equal to or in excess of $2.3 billion (no quarter in which global LemtradaTM net sales were used to determine the achievement of Product Sales Milestone #1 or #2 shall be included in the calculation of sales for determining whether Product Sales Milestone #3 has been achieved).

11. The Approval Milestone Payment was a critical first step to the full realization of the

value of the CVR. The U.S. market accounts for 20% of MS patients worldwide. Absent access to

the U.S. market, Lemtrada will be unlikely to achieve any of the foregoing sales milestones and

payments. In effect, absent approval for sale in the U. S., the CVRs will be functionally worthless.

12. The pivotal clinical trials surrounding Lemtrada were Phase III Comparison of

Alemtuzumab and Rebif Efficiency in Multiple Sclerosis ("CARE-MS") I & II. CARE-MS I was

4

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 5 of 45

focused on patients who were new to MS treatment and CARE-MS II was for patients who had

relapsed while on prior therapy. Both of the CARE-MS trials were randomized two-year pivotal

studies that were purportedly designed to evaluate whether Lemtrada could achieve meaningful

efficacy and safety improvements over Rebif, a leading multiple sclerosis treatment.

13. Throughout the Class Period, Defendants misrepresented to investors the efficacy and

safety of Lemtrada, as well as the likelihood that it would be approved for sale in the U.S.

Defendants also misled investors regarding the design of CARE-MS I & II trials, referenced above,

by specifically failing to disclose that the trials were critically flawed, contained high levels of

placebo effect and observer bias which tainted the results, and failed to disclose that the Company

had been repeatedly warned by the FDA for years that the Company would need to fix these flaws

(which it never did) before Lemtrada could be approved. Nevertheless, throughout the Class

Period, Defendants repeatedly through press releases, conference calls, and SEC filings, hyped

Lemtrada's prospects and import to the Company.

14. For example, on April 24, 2012, data from Lemtrada's CARE-MS II trial were

presented to the American Academy of Neurology. According to the Company's April 26, 2012

Form 6-K filed with the SEC in connection therewith, "[un the trial, patients with pre-existing

disability treated with [Lemtrada] were more than twice as likely to experience a sustained

reduction in disability than patients given Rebif®. Genzyme announced in November [of 2011]

that results for the co-primary endpoints of CARE-MS II trial were highly statistically significant."

The CVRs closed at $1.31 per share on April 24, 2012, up 5.6% over the previous day's closing

price.

15. Then, in a June 12, 2012 press release, Sanofi (through its subsidiary Genzyme)

announced that the Company had submitted a supplemental Biologics License Application

5

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 6 of 45

("5BLA") to the FDA. The press release further touted Lemtrada's efficacy and downplayed

associated adverse events:

The regulatory submissions for LEMTRADA include two-year controlled efficacy and safety data from both treatment-naïve patients and those who relapsed while on therapy, with greater than five years of safety follow-up. Common adverse events associated with alemtuzumab were consistent across the Phase III program and included infusion-associated reactions and infections, which were generally mild to moderate in severity. Autoimmune adverse events were observed in some patients with cases being detected early through a monitoring program and managed using conventional therapies.

16. On August 27, 2012 the Company announced in a press release that Genzyme received

a "Refuse to File" letter from the FDA in response to the sBLA for the approval of Lemtrada. The

Company downplayed the implications of the Refuse to File letter, stating that the FDA had merely

requested that Sanofi modify its presentation of the data sets "to enable the agency to better

navigate the application." The CVRs recorded only a minor downtick as a result of Defendants'

spin on the Refuse to File Letter, closing at $1.39 per share on August 27, 2012 from $1.46 per

share the previous trading day.

17. Several months later, on November 1, 2012, the results of the CARE-MS land CARE-

MS II studies were published in the online issue of The Lancet, a prominent medical journal. An

October 31, 2012 press release from the Company summarized the results, and hyped Lemtrada's

prospects:

In CARE-MS I and CARE-MS II, LEMTRADA was significantly more effective at reducing annualized relapse rates than the active comparator Rebif (high dose subcutaneous interferon beta-la), and more patients on LEMTRADA were relapse-free at two years. In addition, in CARE-MS II, accumulation of disability was significantly slowed in patients given LEMTRADA vs. Rebif. Further, patients treated with LEMTRADA were significantly more likely to experience improvement in disability scores than those treated with Rebif, suggesting a reversal of disability in some patients.

6

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 7 of 45

18. Then, on January 28, 2013, the Company announced that the FDA accepted the sBLA

for Lemtrada and that Sanofi was expecting a final decision from the FDA on Lemtrada during the

second half of 2013. The CVRs closed on January 28, 2013 at $1.86 per share.

19. On November 8, 2013, the market learned that Lemtrada was critically flawed and that

Sanofi's application would not be approved. On that day, the FDA Advisory Committee on

Peripheral and Central Nervous System Drugs issued a briefing report (the "Briefing Report") in

advance of a scheduled formal hearing on November 13, 2013. The Briefing Report sharply

criticized the Company's submission to the FDA, and reported that the Committee had found that

"significant concerns exist regarding the safety profile of alemtuzumab [Lemtrada] and the

adequacy of the efficacy data."' (Emphasis is supplied throughout unless otherwise noted.)

20. The Briefing Report further stated that:

Dr. Mentari's review discusses numerous safety concerns associated with the use of alemtuzumab for MS. These include the incidence of an array of autoimmune diseases including immune thrombocytopenia (ITP), autoimmune hemolytic anemia, immune pancytopenia, anti-glomerular basement membrane (Anti-C}BM) disease, membranous glomerulonephritis, thyroid disorders, endocrine ophthalmopathy, acquired hemophilia A, type 1 diabetes mellitus, acute epitheliopathy of the retina, autoimmune skin disease, and undifferentiated connective tissue disorders, along with the incidence of malignancies, notably including thyroid cancer and melanoma. As these concerns are serious and potentially fatal, Dr. Mentari does not recommend approval of alemtuzumab unless substantial clinical benefit exists.

Dr. Marler's review discusses various concerns associated with the data presented by the applicant in support of a demonstration of clinical benefit. These stem from issues involved with the adequacy of the design of the primary trials on which the application relies for support. In particular, Dr. Marler has grave concerns that the failure to blind patients and treating physicians in the open-label design of the trials introduced bias that confounds interpretation of their ostensible results. Because of these issues, Dr. Marler finds that the applicant has not submitted evidence from

1 Drs. Evelyn Mentari and John Marler prepared reports regarding the clinical safety and efficacy, respectively, of Lemtrada for the FDA. Also on behalf of the FDA, Dr. Sharon Yan prepared a report regarding the statistical impact and analysis of the data presented by Sanofi in connection with its Lemtrada submission.

7

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 8 of 45

adequate and well-controlled studies to support the effectiveness of alemtuzumab for treating multiple sclerosis.

Dr. Yan's review discusses the statistical aspects of the data presented by the applicant in support of a demonstration of clinical benefit, and largely reinforces the concerns of Dr. Marler. Dr. Yan also feels that troublesome design issues and the presence of bias in the trials prevents reliance on their results, and that a valid, accurate, and interpretable effect on the two main clinical outcomes of interest, relapse rate and sustained accumulation of disability, has not been established. Dr. Yan finds, like Dr. Marler, that the applicant has not provided evidence from adequate and well-controlled studies in this application and that such studies still need to be conducted to establish the effectiveness of alemtuzumab for the treatment ofpatients with multiple sclerosis.

21. In short, the FDA concluded that not only had Sanofi failed to demonstrate

Lemtrada's efficacy, but that its use presented "serious and potentially fatal" dangers to anyone who

took the drug. The FDA's conclusions are of critical import: in evaluating Sanofi's submission, the

FDA relied upon information presented by Sanofi itself. That is, all of the information that revealed

- uniformly - that the trials were deeply flawed and the drug was both dangerous and ineffective

were known to Defendants. Thus, there is no reason to suspect that Defendants had any reason

(save profit) to conclude and represent otherwise to the public. As further detailed below, the

Company's Chief Executive Officer ("CEO") Christopher A. Viehbacher ("Viehbacher") admitted

that the FDA's findings "[weren't] a total surprise." And yet, prior to Defendant Viehbacher's

belated disclosure, and despite repeated FDA warnings (discussed below) of the serious flaws in

CARE-MS I & II, Defendants had gone to great lengths to convince investors of the exact opposite.

22. In response to the public disclosure of the FDA's rejection of Sanofi's submission, the

market price of Sanofi's CVRs declined $1.23 per share, or nearly 62%, to close at $0.77 per share

on November 8, 2013 on extremely high volume of over 30 million shares. But the bad news did

not end on November 8, 2013.

Case 1:13cv-08806-PAE Document 44 Filed 04/28/14 Page 9 of 45

23. Five days later, on November 13, 2013, the FDA's Peripheral and Central Nervous

System Drugs Advisory Committee Meeting released the "Background Package" for Lemtrada,

revealing to the public that since as long ago as 2006, that Genzyme had been repeatedly warned

that the structure of the CARE-MS trials was deeply flawed. Specifically, the FDA noted:

(a) On November 21, 2006, FDA met with Genzyme to discuss current and future development plans for alemtuzumab [Lemtrada]. Clinical comments in the minutes regarding trial design included the following:

"FDA responded that a rater blinded (but patient not blinded) study may be adequate if the effect is large. However, a totally blinded study is more likely to be found persuasive if the treatment effect is relatively small."

"The FDA noted that using a low dose active comparator would assist with the blinding. However, the sponsor was hesitant to have a treatment arm with ineffective therapy, such as placebo or very low dose alemtuzumab. The FDA again noted that they prefer double-blinded, controlled studies, especially for the pivotal trials."

(b) In a June 29, 2007 letter, the FDA response to Genzyme's submission of two protocols for additional trials. The letter stated:

FDA strongly recommends that you use a double-dummy placebo control in your pivotal trials. The acceptability of your rater-blinded study will be a matter of review. If your study results reveal an extremely large effect, then FDA may potentially accept this rater-blinded design for the pivotal trials. Also, you should carefully assess the effectiveness of your blinding during the trial and at its conclusion to determine if the rater blind was maintained.

(c) On March 17, 2010 the FDA would meet with Genzyme and note:

FDA was "concerned by the potential bias introduced by the absence of blinding of patients, the possibility of unblinding of EDSS raters, the initiation of alternative MS therapies after the first relapse, and the elimination of censoring. The interpretation of the results from the statistical analysis will be challenging, and extremely robust findings will be necessary to overcome these issues."

"Blinding procedures were discussed in detail. For EDSS and relapse reporting, the bias introduced by unblinding of physicians and patients remains a significant problem which will cause serious difficulties in interpreting the results of the trial. Trial procedures leave doubt about the extent of any unblinding of EDSS raters.

(d) On January 24, 2011 the FDA met with Genzyme at a pre-BLA meeting and noted the following:

9

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 10 of 45

"Beginning with our initial review of the CAMMS323 and CAMMS324 protocols, the lack of double-blinding has consistently concerned us. The lack of blinding remains a major concern. We [FDA] note that, despite these previous concerns that have been communicated to you, there was little discussion of the unblinded design of the trials in the meeting material. We emphasize the importance of presenting a full discussion and analysis of the impact of having the patients and treating physicians unblinded. You need to present data and analyses that evaluate the objectivity of the EDSS and MRI outcomes as well as the relapses. To do so requires full descriptions of the procedures for ensuring the blind and data to support compliance with the different blinding procedures in the protocols.

24. These same concerns formed the precise basis for the FDA's decision to reject

Lemtrada. For example, on November 13, 2013, the FDA stated:

(a) Dr. Marler's review discusses various concerns associated with the data presented by the applicant in support of a demonstration of clinical benefit. These stem from issues involved with the adequacy of the design of the primary trials on which the application relies for support. In particular, Dr. Marler has grave concerns that the failure to blind pati ents and treating physicians in the open-label design of the trials introduced bias that confounds interpretation of their ostensible results. Because of these issues, Dr. Marler finds that the applicant has not submitted evidence from adequate and well-controlled studies to support the effectiveness of alemtuzumab for treating multiple sclerosis.

(b) Dr. Yan's review discusses the statistical aspects of the data presented by the applicant in support of a demonstration of clinical benefit, and largely reinforces the concerns of Dr. Marler. Dr. Yan also feels that troublesome design issues and the presence of bias in the trials prevents reliance on their results, and that a valid, accurate, and interpretable effect on the two main clinical outcomes of interest, relapse rate and sustained accumulation of disability, has not been established. Dr. Yan finds, like Dr. Marler, that the applicant has not provided evidence from adequate and well-controlled studies in this application and that such studies still need to be conducted to establish the effectiveness of alemtuzumab for the treatment of patients with multiple sclerosis.

25. The Company would formally receive the FDA's response on December 27, 2013 in

the form of a Complete Response Letter which informed Sanofi that its application for Lemtrada

had been rejected.

10

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 11 of 45

26. After the cursory comments from (I}enyzme President and CEO Defendant David

Meeker, stating his "disappointment" with the FDA's decision, a potential appeal with the FDA

(which have a notoriously low success rate), the Company's December 30, 2013 press release on

the Complete Response Letter stated the obvious: "Sanofi does not anticipate that the CVR

milestone of U.S. approval of Lemtrada by March 31, 2014 will be met." The closing price of the

CVRs on December 30, 2013 was $0.32 per share.

27. Then, on January 23, 2014, Defendant Viehbacher admitted to the public that the FDA

rejection "wasn't a total surprise," as the FDA had regularly raised concerns between 2006 and

20]] about the structure of the Lemtrada trials. But during the Class Period, Defendants concealed

this obviously-material information from the public.

28. Indeed, as demonstrated by the below chart, Defendant Viehbacher's "lack of

surprise" was in shocking contrast to what investors had expected based on Defendants' public

statements regarding Lemtrada:

3.nc4i

1.4

H 1 2

I .

Juil H J.inLL

29. That Defendants had no reason to be surprised by the FDA's rejection of Lemtrada is

further confirmed by the statements of one of its former employees who was in charge of the

11

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 12 of 45

design, implementation, and results reporting of Lemtrada's CAMMS323 and CAMMS324 trials -

the very trials on which the FDA predicated its rejection of Lemtrada. Specifically, Confidential

Witness 1 ("CW 1") was employed by Genzyme from 2002 through 2012, and was the Company's

Associate Director of Clinical Research and oversaw project management and operations for the

Company's Lemtrada trials. As discussed in more detail, below, CW 1 had regular contact with

Genzyme's then-Chief Medical Officer, Richard Moscicki ("Moscicki") as well as other senior

employees of Sanofi who were not only aware of Lemtrada's (and the trials) shortcomings but were

hypersensitive to reported adverse events and severity of the drug's side effects meant for

Lemtrada's ultimate commercial viability. 3

30. CW 1 worked with several colleagues to design the Trial Protocol for CARE-MS I and

CARE-MS II and was the Project Manager for Lemtrada's Phase II clinical trial that began in 2002.

Part of CW l's role in developing the Phase III clinical trials was participation in weekly Project

Team meetings, which included representatives from the Company's Regulatory, Biostatistics, Data

Management, Medical, Clinical Development and Safety Departments. CW 1 reports that all

reported adverse events were discussed at these meetings and that Lemtrada's safety profile was

discussed at almost every meeting.

31. CW 1 explained that a Risk Management Plan was developed in response to a death of

a trial subject from immune thrombocytopenia (ITP) reported during Lemtrada's Phase II clinical

trial. The Risk Management Plan implemented additional clinical and laboratory safety

assessments to detect signs of ITP and the FDA placed the Phase II trial on hold for approximately

2 The CAMMS323 and CAMMS324 trials were synonymous with the CARE-MS I & II trials.

Dr. Moscicki now serves as the FDA's Deputy Director for Science Operations, Center for Drug Evaluation and Research; the very department charged with, among other things, regulation and oversight ofprescripti on drugs such as Lemtrada.

12

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 13 of 45

ten months before allowing the trials to proceed. CW 1 noted that the Steering Committee

remained concerned with Lemtrada's safety profile during the Phase III trials, notably occurrences

of progressive multifocal leukoencephalopathy ("PML") and Graves' Disease among patients

enrolled in the Phase III trials. ITT, PML, and Grave's Disease were all very serious side effects

which were historically uncommon in MS patients.

32. According to CW 1, each fiscal quarter the Project Team would report to a Steering

Committee which was chaired by Professor Alastair Compston and included the Company's Chief

Medical Officer Richard Moscicki. So aligned were the Project Team and the Steering Committee,

that CW 1 reports that "pretty often" a member of the Steering Committee would even attend the

weekly meetings of the Project Team. CW 1 noted that the Steering Committee was

"hypersensitiv[e]" to and very concerned about Lemtrada's "emerging safety profile" and recalled

that Moscicki was especially concerned by serious adverse events reported over the course of the

Phase II and Phase III clinical trials. The importance of the fact that Moscicki - a chief officer of

Genzyme - was aware of the serious and dangerous flaws in Lemtrada cannot be understated. As a

senior member of the Company's executive team, his knowledge is necessarily that of the

Company.

33. Given the Company's disclosures, the market response, and the information and

allegations set forth herein, it follows almost as a certainty that as a result of Defendants' wrongful

acts and omissions, and the precipitous decline in the market value of the Company's CVRs,

Plaintiff and other members of the Class (defined further herein) have suffered significant damages.

JURISDICTION AND VENUE

34. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a) of the

Exchange Act, 15 U.S.C. §§ 78j(b) and 78t(a), and Rule lob-S promulgated thereunder by the SEC,

17 C.F.R § 240.10b-5.

13

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 14 of 45

35. This Court has jurisdiction over the subject matter of this action pursuant to 28 U.S.C.

§§ 1331 and 1337, and Section 27 of the Exchange Act, 15 U.S.C. § 78aa.

36. Venue is proper in this District pursuant to Section 27 of the Exchange Act, and 28

U.S.C. § 1391(b). Sanofi's CVRs are traded in this District and many of the acts and practices

complained of occurred in substantial part herein.

37. In connection with the acts alleged in this complaint, Defendants, directly or

indirectly, used the means and instrumentalities of interstate commerce, including, but not limited

to, the mails, interstate telephone communications, and the facilities of the national securities

markets.

PARTIES

38. Lead Plaintiff was appointed pursuant to an Order dated March 3, 2014 (Docket No.

27). Lead Plaintiff purchased CVRs at artificially inflated prices during the Class Period and has

been damaged hereby.

39. Defendant Sanofi is a French corporation maintaining its principal place of business at

54 Rue La Boetie, 75008 Paris, France. Sanofi's CVRs trade on the NASDAQ Global Market

("NASDAQ") under the ticker symbol "GCVRZ."

40. Defendant Viehbacher was, at all relevant times, the Company's CEO.

41. Defendant Meeker was, at all relevant times, the President and CEO of Genzyme.

42. Defendant Jerome Contamine ("Contamine") was, at all relevant times, the

Company's Executive Vice President and Chief Financial Officer ("CFO").

43. Defendants Viehbacher, Meeker and Contamine are referred to herein as the

"Individual Defendants."

44. The parties named above in paragraphs 39 through 42 are collectively referred to

herein as the "Defendants."

14

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 15 of 45

MATERIALLY FALSE AND MISLEADING STATEMENTS MADE DURING THE CLASS PERIOD

45. The Class Period begins on March 6, 2012. On this day, Sanofi filed with the SEC an

annual report on Form 20-F. The Form 20-F was signed by Defendant Viehbacher, and set forth

the following, in relevant part:

Main compounds currently in Phase II or III clinical development: In the Multiple Sclerosis field:

* * *

Alemtuzumab (LemtradaTM) Humanized monoclonal antibody targeting CD52 antigen abundant on the surface of B and T lymphocytes leading to changes in the circulating lymphocyte pool.

Alemtuzumab targets patients with relapsing forms of Multiple Sclerosis (MS). The two Phase III studies demonstrating the safety and efficacy of alemtuzumab were completed in 2011. The first study, CARE-MS I, demonstrated strong and robust treatment effect on the relapse rate co-primary endpoint vs Rebif. The co-primary endpoint of disability progression (time to sustained accumulation of disability SAD) did not meet statistical significance. The second study, CARE-MS II, demonstrated that relapse rate and SAD were significantly reduced in MS patients receiving alemtuzumab as compared with Rebif. In both cases, safety results were consistent with previous alemtuzumab use in MS and adverse events continued to be manageable. The dossier is scheduled to be submitted to FDA review in the second quarter of 2012.

46. The foregoing statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established."

15

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 16 of 45

47. On April 24, 2012, the Company issued a press release reporting data from the Phase

III CARE-MS II trial. In that press release, Sanofi reported that Lemtrada significantly slowed

disabilities in patients with multiple sclerosis. The press release set forth, in relevant part:

Accumulation of disability was significantly slowed in patients with multiple sclerosis (MS) who were treated with alemtuzumab versus Rebi9 (high dose subcutaneous interferon beta-la), as measured by the Expanded Disability Status Scale (EDSS), a standard assessment of physical disability progression. In addition, significant improvement in disability scores was observed in some patients treated with alemtuzumab from baseline and compared to patients treated with Rebif, suggesting a reversal of disability in these patients. In the trial, patients with pre-existing disability treated with alemtuzumab were more than twice as likely to experience a sustained reduction in disability than patients given Rebif

CARE-MS II was a randomized Phase III clinical trial comparing the investigational drug alemtuzumab to Rebif in patients with relapsing-remitting multiple sclerosis (RRMS) who had relapsed while on prior therapy. The company announced in November that results for the co-primary endpoints of the trial were highly statistically significant.

Key disability data from the CARE-MS II trial presented today at the 64th Annual Meeting of the American Academy of Neurology include:

• The mean EDSS score for patients treated with alemtuzumab decreased over a two-year period, indicating an improvement in their physical disability, while the mean score for patients given Rebif increased, indicating a worsening of disability (-0.]7vs. 0.24; p < 0.000]). • At two years, 29 percent of patients treated with alemtuzumab had experienced a six-month sustained reduction in disability, meaning their level of disability improved, as compared to only 13 percent with Rebif (p=0.0002). • There was a 42 percent reduction in the risk of six-month sustained accumulation (worsening) of disability (SAD) as measured by EDSS in patients treated with alemtuzumab compared to Rebif over two years of study (p=0.0084), as previously reported. This was a highly statistically significant result for this co-primary endpoint

Key relapse data from the trial presented at AAN include:

• 65 percent of patients treated with alemtuzumab were relapse-free at two years, meaning they did not experience any

16

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 17 of 45

relapses in the trial, compared to 47 percent with Rebif (47 percent risk reduction; p<0.0001). • A 49 percent reduction in relapse rate was observed in patients treated with alemtuzumab 12 mg compared to Rebif over two years of study (p<O.000l), a highly significant result for this co-primary endpoint, as previously reported.

In the CARE-MS II trial, alemtuzumab 12 mg was given as an IV administration a total of eight times over the course of the two-year study. The first treatment course of alemtuzumab was administered on five consecutive days, and the second course was administered on three consecutive days 12 months later. Rebif 44 mcg was administered by subcutaneous injection three times per week, each week, throughout the two years of study.

"Alemtuzumab is the first disease modifying therapy to show a significant effect both on relapse and disability endpoints over and above those of Rebif in a comparative trial," said Professor Alastair Compston, Chair of the Steering Committee overseeing the conduct of the study, principal investigator on the Phase II and III clinical trials of alemtuzumab, and Head of the Department of Clinical Neurosciences at the University of Cambridge, United Kingdom. "The efficacy data from the CARE-MS trial program suggest that, if approved, alemtuzumab will be an important new treatment for relapsing MS patients with active disease." (italics in original)

Additional new data from the CARE-MS II study suggest that alemtuzumab provided significant improvement over Rebif across a number of imaging endpoints, consistent with the effects observed in the clinical endpoints. In MS, imaging can be used to track the development of lesions, or patches of inflammation in the central nervous system (CNS). Statistically significant improvement was observed for alemtuzumab over Rebif in the percentage of patients with new or enlarging T2-hyperintense lesions (46 vs. 68; p<0.0001) and with gadolinium-enhancing lesions (19 vs. 34; p<0.0001). The change in T2-hyperintense lesion volume from baseline to year two, a secondary endpoint, was not significantly different (p=0. 14). In the trial, patients treated with alemtuzumab experienced less change in brain parenchymal fraction (BPF), a measure of brain atrophy or loss of neurons and the connections between them, compared to Rebif (-0.62 vs. -0.81) median percent change from baseline (p -0.0 12), a significant result.

"We believe these ground-breaking results from CARE-MS 11, including reversal of disability accumulation in some patients, achieved over the standard therapy Rebif provide a message of hope for people living with MS," said David Meeker, M.D., President and CEO, Genzyme. "We are on track to submit alemtuzumab for review to U.S. and EU regulatory authorities in the second quarter of this year and are excited about the potential of bringing this important therapy to people living with MS who have unmet treatment needs. " ( italics in original)

17

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 18 of 45

The most common adverse events associated with alemtuzumab in the CARE-MS Ii study were infusion-associated reactions, which were generally mild to moderate. Infections were common in both groups, with a higher incidence in the alemtuzumab group. The most common infections included upper respiratory and urinary tract infections, cutaneous fungal infections and oral herpes. Serious infections occurred in 3.7 percent of the alemtuzumab group as compared to 1.5 percent of the Rebif group. Infections were predominantly mild to moderate in severity and none were fatal.

48. The foregoing statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established."

49. On an April 27, 2012 conference call with analysts to discuss the Company's Qi 2012

financial results, Defendant Viehbacher spoke about the prospects of Lemtrada:

Lemtrada I'm going to come on to in a minute, but we've been able to really for the first time show the data of the CARE-MS II study. Up to now we've been - we've had to be circumspect in what we said, simply because we didn't want to dilute the impact of this presentation at AAM this week.

I've got three slides on Lemtrada and I really only just want to focus on this because I think Lemtrada has had a certain reputation and I have to say I used to share it when we were acquiring Genzyme. I think we rightly had some question about the ultimate value in the absence of data because of the long history of development.

Equally, I think one has to give credit to where data there and where the data are showing a different story and I think actually particularly when you look at the CARE-MS II study, the data are nothing short of stunning. Obviously because of its history Genzyme and before then Bayer set the hurdle high on their Phase III I mean

18

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 19 of 45

they knew that if they are going to come to market they have to had an extremely convincing set of results.

50. Defendant Viehbacher would also downplay the safety issues attributed to Lemtrada in

the Qi 2012 earnings call:

The one that hasn't been filed yet, but clearly is about to be filed is Lemtrada. I know their sales forecast are all over the map. I personally think actually - and I'm recognized, I'm changing my tune on this, but I'm changing my tune on the basis of data. I think this is going to be a major drug. People are concerned about safety, but I don't see the reason for that. We've seen higher incidence on impact for thyroid, but thyroid conditions are not uncommon in this population and indeed others and are pretty easily treated with standard therapy. The ITP has not been as severe as we've seen outside there the population and is all been reversed.

51. Defendant Viehbacher's statements during the conference call were materially false

and misleading and/or omitted to state other facts necessary to make the statements made not

misleading because, according to the Briefing Report: (i) Lemtrada presented "serious and

potentially fatal" side effects such that, in the absence of "substantial clinical benefit" it was not

approvable; (ii) the Company lacked "evidence from adequate and well-controlled studies to

support the effectiveness of [Lemtrada] for treating multiple sclerosis"; and (iii) there were material

"design issues and the presence of bias in the trials [that] preventLedi reliance on their results, and

that a valid accurate, and interpretable effect on the two main clinical outcomes of interest, relapse

rate, and sustained accumulation of disability, has not been established."

52. On June 12, 2012, the Company issued a press release announcing that Sanofi had

submitted a supplemental Biologics License Application (5BLA) to the FDA seeking approval of

Lemtrada for treatment of relapsing MS. The press release, entitled "Genzyme Submits

Applications to FDA and EMA for Approval of LEMTRADATM (alemtuzumab) for Multiple

Sclerosis," set forth, in relevant part:

Genzyme's clinical development program for LEMTRADA included two Phase III studies in which results for LEMTRADA were superior to Rebif® (high dose

19

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 20 of 45

subcutaneous interferon beta- la) on clinical and imaging endpoints, including a reduction in relapse rate. In addition, as presented last month at the American Academy of Neurology meeting, some patients with preexisting disability treated with LEMTRADA in the CARE-MS II trial were more than twice as likely to experience a sustained reduction in disability over two years than patients treated with Rebif.

"There remains a large unmet treatment need for patients living with active disease and we believe that LEMTRADA, given its efficacy and unique dosing schedule, has the potential to transform the lives of patients with Multiple Sclerosis," said David Meeker, M.D., President and Chief Executive Officer, Genzyme. (italics in original)

The regulatory submissions for LEMTRADA include two-year controlled efficacy and safety data from both treatment-naïve patients and those who relapsed while on therapy, with greater than five years of safety follow-up. Common adverse events associated with alemtuzumab were consistent across the Phase III program and included infusion-associated reactions and infections, which were generally mild to moderate in severity. Autoimmune adverse events were observed in some patients with cases being detected early through a monitoring program and managed using conventional therapies.

53. Defendant Viehbacher's statements during the conference call were materially false

and misleading and/or omitted to state other facts necessary to make the statements made not

misleading because, according to the Briefing Report: (i) Lemtrada presented "serious and

potentially fatal" side effects such that, in the absence of "substantial clinical benefit" it was not

approvable; (ii) the Company lacked "evidence from adequate and well-controlled studies to

support the effectiveness of [Lemtrada] for treating multiple sclerosis"; and (iii) there were material

"design issues and the presence of bias in the trials [that] preventLedi reliance on their results, and

that a valid accurate, and interpretable effect on the two main clinical outcomes of interest, relapse

rate, and sustained accumulation of disability, has not been established."

54. On July 26, 2012 conference call with analysts to discuss the Company's Q2 2012

financial earnings. Defendant Viehbacher would again address Lemtrada's safety profile:

So, the fact that we have this strong safety profile is extremely important, being potentially having the first in class on the PCSK-9, the launches of Lemtrada and Aubagio are clearly very important. I think particularly Lemtrada is a potential game

20

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 21 of 45

changer in multiple sclerosis and Aubagio probably an underestimated opportunity as well.

55. Defendant Viehbacher's statements during the conference call were materially false

and misleading and/or omitted to state other facts necessary to make the statements made not

misleading because according to the Briefing Report: (i) Lemtrada presented "serious and

potentially fatal" side effects such that, in the absence of "substantial clinical benefit" it was not

approvable; (ii) the Company lacked "evidence from adequate and well-controlled studies to

support the effectiveness of [Lemtrada] for treating multiple sclerosis"; and (iii) there were material

"design issues and the presence of bias in the trials [that] preventLedi reliance on their results, and

that a valid accurate, and interpretable effect on the two main clinical outcomes of interest, relapse

rate, and sustained accumulation of disability, has not been established." Lemtrada's safety profile

- despite Defendant Viehbacher's representation to the contrary - was anything but "strong."

56. On October 25, 2012, Contamine spoke to analysts on a conference call discussing the

Company's Q3 2012 financial results. Defendant Contamine suggested the launch of Lemtrada was

imminent:

So this will continue and probably somewhat amplify in the coming quarters as we prepare for the launch of Lyxumia, thereafter for the launch of Lemtrada.

57. On the same call, Defendant Viehbacher touted the Company's future pipeline,

including Lemtrada:

I would say if I'm looking at the PCSK-9 and look at the dengue vaccine I look at even our otamixaban, I look at Lemtrada, I look at Aubagio, I look at our U300, I look at Lyxumia, I would say I'm actually very satisfied with where the progress is going, and where I sit, I think there's a complete - continue with the strategy that we have laid out.

58. The statements during the conference call were materially false and misleading and/or

omitted to state other facts necessary to make the statements made not misleading because

21

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 22 of 45

according to the Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects

such that, in the absence of "substantial clinical benefit" it was not approvable; (ii) the Company

lacked "evidence from adequate and well-controlled studies to support the effectiveness of

[Lemtrada] for treating multiple sclerosis"; and (iii) there were material "design issues and the

presence of bias in the trials [that] preventLedi reliance on their results, and that a valid accurate,

and interpretable effect on the two main clinical outcomes of interest, relapse rate, and sustained

accumulation of disability, has not been established." Indeed, this statement was further false and

misleading in that given the numerous flaws in Lemtrada and the studies, Defendants had an

express duty to tell the whole truth about Lemtrada: that its "launch" was anything but likely to

happen and that the Company should not have been "satisfied" with the progress of an approval

application that would almost certainly be rejected for reasons already known to them.

59. On October 31, 2012, the Company issued a press release entitled "Genzyme

Announces Publication of LEMTRADA (alemtuzumab) Pivotal Studies in The Lancet." This press

release announced clinical results from the Lemtrada CARE-MS I and CARE-MS II pivotal studies

in patients with relapsing-remitting multiple sclerosis. The Company stated that Lemtrada was

significantly more effective at reducing annualized relapse rates than the active comparator Rebif,

and more patients on Lemtrada were relapse-free at two years.

60. Defendants' statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (H) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (Hi) there were material "design issues and the presence of bias in the trials

22

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 23 of 45

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established".

61. On January 28, 2013, the Company issued a press release entitled "Genzyme's

LEMTRADATM (alemtuzumab) Application for MS Accepted for Review by the FDA," which

announced that the FDA had accepted the Company's sBLA file seeking approval of Lemtrada.

62. Defendants' statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established."

63. On February 7, 2013, Defendant Viehbacher spoke to analysts regarding the

Company's Q4 2012 financial results. Defendant Viehbacher would praise the infrastructure Sanofi

created in preparing to launch Lemtrada:

Now the other was a trickier proposition. We put multiple sclerosis into Genzyme, no real experience in multiple sclerosis. We actually had to build a team from scratch, which we have done. That was actually a very significant investment. And it's fair to say that Aubagio did not have a significant awareness level coming into this. However, I think when -- and when we started seeing the first data, we were encouraged by the launch. Personally, I'd like to see a little bit more than a couple of weeks of data to get excited. But here, we have 4 months of data and what you can see is, clearly, that the Aubagio launch is tracking at least as well, if not slightly better, than the Gilenya launch. 80% of MS specialists have now -- have prescribed Aubagio. 1 in 5 patients were treatment-naïve and then, obviously, the rest were

23

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 24 of 45

switches, mostly from Copaxone and Avonex. In doing some of the initial market research, one of the key reasons is actually tolerability of treatment. So I think it augurs well because this also says that we have a team, that should be in good position to launch Lemtrada. It is obviously a huge opportunity that we have to be able to put 2 significant new medicines into an important area like MS. This is a market of some $14 billion worldwide.

64. On the same call with analysts, Defendant Viehbacher would discuss the merits of the

CARE-MS trials:

So with that, let me go to Lemtrada. I think it's probably one of the new medications that is going to truly change, in my opinion, the management of multiple sclerosis patients. As you know, there are effective drugs out there and the demand of the patient population now is towards quality of life and improvement in the tolerability of the treatments that they're receiving. So you'd heard about Aubagio and its launch. In Lemtrada, we filed in Europe and we filed in the U.S., we just heard the file was accepted by the FDA. And if you look at Lemtrada, the reason we think it's an important component of the amatarien [ph] in multiple sclerosis is that it does reduce significantly relapse rates against comparators, not against just placebo, and it also significantly slows the accumulation of disability over 6 months. It's a completely different mode of administration with injections at 1 year apart. So it's almost like a vaccine in many ways. The patients do not have to come back every week or every 2 weeks to get injected. And therefore, it's a really manageable drug from the standpoint of the physicians. It's manageable, also, in terms of its safety profile. Some infusion reactions, a little higher infections, but -- autoimmune events are the ones that have been mentioned but all of them can be detected and managed conventionally. So we have great hopes here. We will also hear about the regulatory decisions in the course of 2013.

65. Defendants' statements during the conference call were materially false and

misleading and/or omitted to state other facts necessary to make the statements made not

misleading because, according to the Briefing Report: (i) Lemtrada presented "serious and

potentially fatal" side effects such that, in the absence of "substantial clinical benefit" it was not

approvable; (ii) the Company lacked "evidence from adequate and well-controlled studies to

support the effectiveness of [Lemtrada] for treating multiple sclerosis"; and (iii) there were material

"design issues and the presence of bias in the trials [that] prevent[ed] reliance on their results, and

that a valid accurate, and interpretable effect on the two main clinical outcomes of interest, relapse

24

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 25 of 45

rate, and sustained accumulation of disability, has not been established." The closing price of the

CVRs on February 7, 2013 was $1.87 per share.

66. On or about March 7, 2013, the Company filed with the SEC an Annual Report on

Form 20-F. The Form 20-F was signed by Defendant Viehbacher, and stated the following, in

relevant part:

The main compound currently in Phase III clinical development in the multiple sclerosis field is LemtradaTM (alemtuzumab), a humanized monoclonal antibody targeting CD52 antigen abundant on the surface of B and T lymphocytes leading to changes in the circulating lymphocyte pool. Alemtuzumab has been developed to treat patients with relapsing forms of MS. The two pivotal Phase III studies demonstrating the safety and efficacy of alemtuzumab were completed in 2011 and the results were published in the Lancet in November 2012. The first study, CARE-MS I, demonstrated strong and robust treatment effect on the relapse rate co-primary endpoint vs Rebif in treatment-naive MS patients. The co-primary endpoint of disability progression (time to sustained accumulation of disability: SAD) did not meet statistical significance. The second study, CARE-MS II, demonstrated that relapse rate and SAD were significantly reduced in MS patients receiving alemtuzumab as compared with Rebif in MS patients who had relapsed on prior therapy. Results from CARE-MS II also showed that patients treated with LemtradaTM were significantly more likely to experience improvement in disability scores than those treated with Rebif, suggesting a reversal of disability in some patients. In both pivotal studies, safety results were consistent with previous alemtuzumab use in MS and adverse events continued to be manageable. Marketing applications for LemtradaTM are currently under review by regulatory authorities.

67. Defendants' statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

25

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 26 of 45

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established." The closing price of the CVRs on March 7, 2013 was $1.79 per share.

68. On March 21, 2013, the Company issued a press release entitled "Effect of Genzyme's

LEMTRADA Maintained in Patients Beyond Two-Year Pivotal MS Studies," which announced

interim results from the first year extensions study of Lemtrada. Therein, the Company reported, in

relevant part:

In this analysis of the first year of the extension study, relapse rates and sustained accumulation of disability remained low among patients who had previously received LEMTRADA in either of the Phase III CARE-MS I or CARE-MS II studies. In these pivotal studies, LEMTRADA was given as two annual courses, at the start of the study and 12 months later. More than 80 percent of patients did not receive further treatment with LEMTRADA during the first year of the extension study.

"These findings are important because they suggest that the benefits ofLEMTRADA as observed in the Phase III studies are maintained, even though most patients did not receive further dosing," said Edward Fox, M.D., Director of the Multiple Sclerosis Clinic of Central Texas, who presented the study results today at the annual meeting of the American Academy of Neurology in San Diego, Calif. (italics in original)

The Phase III trials of LEMTRADA were randomized, two-year pivotal studies comparing treatment with LEMTRADA to Rebif (subcutaneous interferon beta-la 44 mcg) in patients with relapsing-remitting MS who were either new to treatment (CARE-MS I) or who had relapsed while on prior therapy (CARE-MSII).

More than 90 percent of the patients who participated in the Phase III pivotal trials enrolled in the extension study. Patients who originally received LEMTRADA were eligible to receive additional treatment in the extension study if they experienced at least one relapse or at least two new or enlarging brain or spinal lesions.

These interim results are from the first year of the extension study for patients who previously received LEMTRADA in the two-year studies. Findings stated below are based on patients who enrolled in the extension study:

• More than half of patients (67 percent in CARE-MS I and 55 percent in CARE-MS II) who received LEMTRADA in the pivotal trials and enrolled in the extension study were still relapse-free through the first year of the extension study.

26

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 27 of 45

• In the first year of the extension phase, the annualized relapse rate for patients who received LEMTRADA in the pivotal trials was 0.24 and 0.25, comparable to the annualized relapse rate for those patients in CARE MS I and CARE-MS II, respectively.

Through year three, 72.4 percent of patients in CARE MS I and 70.0 percent in CARE MS II had improved or stable disability as measured by EDSS.

• At three years, 88 percent and 80 percent of patients who received LEMTRADA in the pivotal trials, respectively, did not experience six-month confirmed sustained accumulation of disability.

"These results underscore the tremendous promise that LEMTRADA holds for MS patients," said David Meeker, M.D., Genzyme's President and Chief Executive Officer. "We're pleased to be able to present these three-year results that provide us with important new information about LEMTRADA and are consistent with the published results from our Phase II extension study." (italics in original)

Safety results from the first year of the extension study were reported for patients who received LEMTRADA in the Phase III pivotal studies. No new risks were identified. The frequency and type of common and serious adverse events in the first year of the extension study were generally similar to those in the Phase III pivotal studies. The most common adverse events during this period of time were infections, including predominantly mild to moderate upper respiratory and urinary tract infections.

There were two deaths. One, as previously reported, was from sepsis. The other was presumed accidental and deemed unrelated to study treatment. The cumulative incidence of autoimmune thyroid disease over three years was 29.9 percent, as expected based on the Phase II study experience.

Additionally, over three years, approximately 1 percent of patients developed immune thrombocytopenia (ITP) and 0.3 percent developed nephropathy, all of whom responded to treatment.

These cases were detected early through routine monitoring. Patient monitoring for autoimmune disorders is incorporated in all Genzyme-sponsored trials of LEMTRADA.

69. Defendants' statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

27

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 28 of 45

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established." The closing price of the CVRs on March 21, 2013 was $1.79 per share.

70. During a May 3, 2013 Defendant Viehbacher conference call with analysts discussing

the Company's Q2 2013 financial results. On the call, Defendant Viehbacher again failed to

disclose to the public any potential obstacles to Lemtrada's FDA approval:

We've got Lemtrada that can start to roll out in the EU, and we expect a decision on Lemtrada by the end of the year. I mean, if you have 2 big products rolling out into a $14 billion market, that is something that we don't have today.

71. Defendant Viehbacher would also field questions from analysts on the same May 3,

2013 call. There, Defendant Viehbacher would again praise the Company's CARE MS noting the

only obstacle would be with the Company's communication team - not FDA approval:

Graham Parry - BofA Merrill Lynch, Research Division

And then thirdly, you're pointing to a slow Lemtrada launch. Is that also because of the high expected price of the very large upfront cost, given that you're given lots of the therapy for a 2-year treatment paradigm upfront or are you looking at ways to spread that cost potentially?

Viehbacher: On Lemtrada, my cautious approach on this is largely, on the one hand, we clearly have the best efficacy data that anybody has ever demonstrated in a product. I mean, you're talking about over 50% prevention of relapse against an active comparator. So nobody, but nobody has ever shown that level of efficacy against an active comparator. And indeed, we've actually seen for the very first time ever in about 23%, 24% of patients, some improvement in the physical disability. And I think those are both numbers that clearly, or I think, of what was behind making sure that we have a broader indication, at least from the European regulators. Now my only cautious point on this is that this is obviously a drug that has been in development for 20 years. There are an awful lot of misperceptions, I think, that have accumulated over those 20 years. We, obviously, are going to be out there in full force. We have 1-year follow up data from our Phase III study, so we can now demonstrate that this relapse rate largely extends into the third year. And as we go to

28

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 29 of 45

payors, they're already paying somewhere around, if I look at Europe, somewhere between EUR 30,000 and EUR 45,000 a year and on a continuous basis. And here, we have a product where you're going to get 5 infusions 1 year and 3 the next, and nothing else really after that, and with some unparalleled efficacy. So from a market access point of view, I don't really foresee much difficulty just because of the force of the data. I think I'm just cautious because this has typically been a conservative population. I mean, this -- the neurologist is particularly affected by what happened with Tysabri, to a lesser extent, with Gilenya. And there tends to be a cautious approach to use of new medicines. I may be wrong, and I hope I'm wrong on that. But I think, really, in order to be transparent, I think one has to say, we -- this drug has been in development a long, long time, and we have, I think, a big communication lob to do. I'm not -- the price, again, we'll give -- we'll let you know when we get closer to getting some market access going. But I don't think price is going to be an issue. But equally, I think we have all of the data we need to get a fair and equitable price versus our competition, that's for sure.

72. Defendants' statements during the conference call were materially false and

misleading and/or omitted to state other facts necessary to make the statements made not

misleading because, according to the Briefing Report: (i) Lemtrada presented "serious and

potentially fatal" side effects such that, in the absence of "substantial clinical benefit" it was not

approvable; (ii) the Company lacked "evidence from adequate and well-controlled studies to

support the effectiveness of [Lemtrada] for treating multiple sclerosis"; and (iii) there were material

"design issues and the presence of bias in the trials [that] preventLedi reliance on their results, and

that a valid accurate, and interpretable effect on the two main clinical outcomes of interest, relapse

rate, and sustained accumulation of disability, has not been established." The closing price of the

CVRs on May 3, 2013 was $1.70 per share.

73. On October 30, 2013 Defendant Viehbacher would convene a call with analysts to

discuss the Company's Q3 2013 financial results and again tout the Company's pipeline:

But quite honestly, I'm feeling pretty, pretty relaxed because if I look at our Phase III pipeline, there's an awful lot of really good stuff in there, whether it's the U300, whether it's the dengue vaccine, whether it's in the Lyxumia rolling out. We've got Aubagio and Lemtrada rolling out.

29

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 30 of 45

74. Defendants' statements were materially false and misleading and/or omitted to state

other facts necessary to make the statements made not misleading because, according to the

Briefing Report: (i) Lemtrada presented "serious and potentially fatal" side effects such that, in the

absence of "substantial clinical benefit" it was not approvable; (ii) the Company lacked "evidence

from adequate and well-controlled studies to support the effectiveness of [Lemtrada] for treating

multiple sclerosis"; and (iii) there were material "design issues and the presence of bias in the trials

[that] preventLedi reliance on their results, and that a valid accurate, and interpretable effect on the

two main clinical outcomes of interest, relapse rate, and sustained accumulation of disability, has

not been established." The closing price of the CVRs on October 30, 2013 was $1.88 per share.

THE TRUTH IS REVEALED

75. On November 8, 2013, the FDA Advisory Committee on Peripheral and Central

Nervous System Drugs issued the Briefing Report in advance of its November 13, 2013 hearing.

The Briefing Report sharply criticized the Company's submission to the FDA, and found that,

"significant concerns exist regarding the safety profile of alemtuzumab [Lemtrada] and the

adequacy of the efficacy data."

76. The Briefing Report further disclosed the following concerns:

Dr. Mentari 's review discusses numerous safety concerns associated with the use of alemtuzumab for MS. These include the incidence of an array of autoimmune diseases including immune thrombocytopenia (ITP), autoimmune hemolytic anemia, immune pancytopenia, anti-glomerular basement membrane (Anti-GBM) disease, membranous glomerulonephritis, thyroid disorders, endocrine ophthalmopathy, acquired hemophilia A, type I diabetes mellitus, acute epitheliopathy of the retina, autoimmune skin disease, and undifferentiated connective tissue disorders, along with the incidence of malignancies, notably including thyroid cancer and melanoma. As these concerns are serious and potentially fatal, Dr. Mentari does not recommend approval of alemtuzumab unless substantial clinical benefit exists.

Dr. Marler 's review discusses various concerns associated with the data presented by the applicant in support of a demonstration of clinical benefit. These stem from issues involved with the adequacy of the design of the primary trials on which the application relies for support. In particular, Dr. Marler has grave concerns that the

30

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 31 of 45

failure to blind patients and treating physicians in the open-label design of the trials introduced bias that confounds interpretation of their ostensible results. Because of these issues, Dr. Marler finds that the applicant has not submitted evidence from adequate and well-controlled studies to support the effectiveness of alemtuzumab for treating multiple sclerosis.

Dr. Yan's review discusses the statistical aspects of the data presented by the applicant in support of a demonstration of clinical benefit, and largely reinforces the concerns of Dr. Marler. Dr. Yan also feels that troublesome design issues and the presence of bias in the trials prevents reliance on their results, and that a valid, accurate, and interpretable effect on the two main clinical outcomes of interest, relapse rate and sustained accumulation of disability, has not been established. Dr. Yan finds, like Dr. Marler, that the applicant has not provided evidence from adequate and well-controlled studies in this application and that such studies still need to be conducted to establish the effectiveness of alemtuzumab for the treatment of patients with multiple sclerosis.

77. On this news, Sanofi's CVRs declined $1.23 per share, or nearly 62%, to close at

$0.77 per share on November 8, 2013 on extremely high volume of over 30 million shares.

78. On November 14, 2013, The Boston Globe published an article entitled "Genzyme MS

Drug Gets Mixed Review." This article revealed, in relevant part:

A panel of medical specialists convened to advise US regulators concluded Wednesday that safety concerns about Genzyme's much-anticipated multiple sclerosis drug don't mean it can't be approved for sale to patients who have tried other MS treatments.

But the Food and Drug Administration advisory committee also said the clinical trials of Genzyme 's drug, called Lemtrada, were flawed. That raised the question of whether the FDA will sign off on a medicine that while eagerly awaited by many patients underwent clinical studies deemed inadequate.

The advisory panel, in a daylong meeting in Silver Spring, Md., peppered representatives of Cambridge-based Genzyme and the FDA with questions about an FDA staff report that suggested Lemtrada may be too dangerous to approve because data linked it to side effects such as rashes and bleeding and a higher long-term risk of thyroid cancer.

In the end, the panel took a series of seemingly contradictory votes that generated as much confusion as guidance. The advisers, by an 11 -to-6 vote, accepted the view of FDA staffers that there was "bias" in Genzyme's clinical trials because the company didn't keep patients from knowing whether they were taking Lemtrada or another drug.

31

Case 1:13-cvM8806PAE Document 44 Filed 04/28/14 Page 32 of 45

"We indicated our discomfort with the clinical trial as designed," Dr. Billy Dunn, acting deputy director of the FDA's Division of Neurology Products, told the advisers.

But the committee, through a 12-to-6 vote, said Genzyme provided substantial evidence that Lemtrada worked for patients with relapsing MS, a potentially debilitating autoimmune disease that affects the brain and central nervous system of an estimated 400,000 people in the United States and 2.5 million worldwide.

By a 17-to-0 vote, the panel concluded that Lemtrada's safety concerns shouldn't preclude its approval for patients for whom other drugs aren't effective. At the same time, it voted 16-to-O that Genzyme 's drug should not be allowed for sale in the United States as a so-called first-line treatment for newly diagnosed MS patients. (Members of the panel abstained from some votes.)

While the panel pored over evidence from clinical trials, it also heard from MS patients, some of whom had taken Lemtrada in trials and testified it had been safe and effective. Panelists also heard from patient advocates, who noted other approved medicines also carry safety risks.