IN THE HIGH COURT OF KARNATAKA AT BANGALORE DATED THIS THE 9 TH DAY OF JUNE, 2014 PRESENT THE HON' BLE MR. JUSTICE N.KUMAR AND THE HON' BLE MR. JUSTICE B.MANOHAR ITA.No.209/2008 c/w ITA Nos.208/2008, 210/2008, 212/2008, 213/2008, 214/2008, 215/2008, 270/2009, 273/2009, 274/2009, 211/2008, 824/2009 ITA NO 209/2008 BETWEEN: 1. The Commissioner of Income Tax C.R.Building, Queens Road, Bangalore, 2.The Income Tax Officer Ward-19(2) International Taxation Bangalore. ...Appellants (By Sri.K.V.Aravind, Advocate)

Transcript

IN THE HIGH COURT OF KARNATAKA AT BANGALORE

DATED THIS THE 9TH DAY OF JUNE, 2014

PRESENT

THE HON' BLE MR. JUSTICE N.KUMAR

AND

THE HON' BLE MR. JUSTICE B.MANOHAR

ITA.No.209/2008

c/w

ITA Nos.208/2008, 210/2008, 212/2008, 213/2008,

214/2008, 215/2008, 270/2009, 273/2009, 274/2009,

211/2008, 824/2009

ITA NO 209/2008

BETWEEN: 1. The Commissioner of Income Tax C.R.Building, Queens Road, Bangalore, 2.The Income Tax Officer Ward-19(2) International Taxation Bangalore. ...Appellants

(By Sri.K.V.Aravind, Advocate)

2

AND: CGI Information Systems and Management Consultants Pvt Ltd 38/1, Naganathapura Singasandra Post Bangalore – 560 068. ...Respondent

(By Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of Order dated 05-10-2007 passed in ITA No. 949/BNG/2005, for the Assessment Year 2003-2004, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 949/BNG/2005,dated 05-10-2007 confirm the orders of the Appellate Commissioner and Income Tax Officer, Ward 19(2), Bangalore.

ITA NO 208/2008

BETWEEN: 1. The Commissioner Of Income Tax C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(2), International Taxation, C.R.Building, Queens Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate)

3

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

Order dated 05-10-2007 passed in ITA No. 948/BNG/2005, for the Assessment Year 2003-2004, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 948/BNG/2005, dated 05-10-2007 confirm the orders of the Appellate Commissioner and Assistant Commissioner of Income Tax Officer, Ward - 19(2), Bangalore. ITA.NO.210/2008

BETWEEN: 1. The Commissioner of Income Tax C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(2), International Taxation, C.R.Building, Queens Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate)

4

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ... Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T. Act, 1961 arising out of

Order dated 05-10-2007 passed in ITA No. 950/BNG/2005, for the Assessment Year 2004-2005, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 950/BNG/2005,dated 05-10-2007 confirm the orders of the Appellate Commissioner and Income Tax Officer, Ward 19(2), Bangalore. ITA NO 212/2008

BETWEEN: 1. The Commissioner of Income Tax Central Circle, C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(1), C.R.Building, Queens Road, Bangalore. ...Appellants

(By Sri. K V Aravind, Advocate)

5

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

Order dated 12-10-2007 passed in ITA No. 412/BNG/2006, for the Assessment Year 2006-2007, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 412/BNG/2006,dated 12-10-2007 confirm the orders of the Appellate Commissioner. ITA NO 213/2008

BETWEEN 1. The Commissioner Of Income Tax Central Circle, C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(1), C.R.Building, Queens Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate)

6

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

Order dated 12-10-2007 passed in ITA No. 413/BNG/2006, for the Assessment Year 2006-2007, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 413/BNG/2006, dated 12-10-2007 confirm the orders of the Appellate Commissioner. ITA.NO.214/2008

BETWEEN: 1. The Commissioner of Income Tax Central Circle, C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(1), C.R.Building, Queens Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate)

7

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of Order dated 12-10-2007 passed in ITA No. 414/BNG/2006, for the Assessment Year 2006-2007, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 414/BNG/2006, dated 12-10-2007 confirm the orders of the Appellate Commissioner. ITA NO 215/2008

BETWEEN: 1. The Commissioner Of Income Tax Central Circle, C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer, Ward-19(1), C.R.Building, Queens Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate)

8

AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Singasandra Post, Bangalore-560 068. ... Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

Order dated 12-10-2007 passed in ITA No. 415/BNG/2006, for the Assessment Year 2006-2007, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 415/BNG/2006,dated 12-10-2007 confirm the orders of the Appellate Commissioner ITA NO 270/2009

BETWEEN: 1. The Director of Income Tax International Taxation, Rashtrothana Bhavan, No.14/3, 6th Floor, Nrupathunga Road, Bangalore-560 001. 2. The Income Tax Officer, Ward-19(1), International Taxation, Rashtrothana Bhavan, No.14/3, 6th Floor,

9

Nrupathunga Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate) AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Electronic City Post, Bangalore-560 100. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

Order dated 26-11-2008 passed in ITA.No.825/Bang/2008, for the Assessment year 2007-08, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No.825/Bang/2008, dated 26-11-2008 and confirm the order passed by the Income Tax Officer,Ward-1(1), International Taxation, Bangalore, in the interest of justice and equity. ITA NO 273/2009

BETWEEN: 1. The Commissioner Of Income Tax International Taxation, Rashtrothana Bhavan, No.14/3 6th Floor, Nrupathunga Road, Bangalore.

10

2. The Income Tax Officer, Ward-19(1), International Taxation, Rashtrothana Bhavan, No.14/3 6th Floor, Nrupathunga Road, Bangalore. …Appellants

(By Sri. K V Aravind, Advocate) AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Electronic City Post, Bangalore-560 100. ...Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao and Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T. Act, 1961 arising out of

Order dated 26-11-2008 passed in ITA No.823/BNG/2008, for the Assessment Year 2006-2007, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No.823/BNG/2008, dated 26-11-2008, confirming the order of the Appellate Commissioner and confirm the order passed by the Income Tax Officer, Ward-19(1), Bangalore in the interest of justice and equity. ITA NO 274/2009

BETWEEN 1. The Director (Commissioner) of Income Tax International Taxation,

11

Rashtrothana Bhavan, No.14/3, 6th Floor, Nrupathunga Raod, Bangalore – 560 001. 2. The Income Tax Officer Ward-19(1), International Taxation, No.14/3, 6th Floor, Nrupathunga Road, Bangalore. ...Appellants

(By Sri.K V Aravind, Advocate) AND: CGI Information Systems and Management Consultants (P) Ltd., No 38/1, Naganathapura, Electronic City Post, Bangalore. ...Respondent (By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao, Adv and

Sri.K.S.Ramabhadran, Advocate)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of Order dated 26-11-2008 passed in ITA.No.824/Bang/2008, for the Assessment year 2006-07, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No.824/Bang/2008,dated 26-11-2008 confirming the order of the Appellate Commissioner and confirm the order passed by the Income Tax Officer, Ward-19(1), Bangalore, in the interest of justice and equity.

12

ITA NO 211/2008

BETWEEN 1. The Commissioner of Income Tax C.R.Building, Queens Road, Bangalore. 2. The Income Tax Officer Ward-19(2) C.R.Building, Queens Road, Bangalore. ...Appellants

(By Sri.K.V.Aravind, Advocate) AND: CGI Information Systems and Management Consultants Pvt Ltd 38/1, Naganathapura Singasandra Post Bangalore – 560 068. ... Respondent

(By Sri.G.Sarangan, Sr.Adv for Sri.Balram.R.Rao, Adv)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of Order dated 05-10-2007 passed in ITA No. 530/BNG/2006, for the Assessment Year 2005-2006, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No. 530/BNG/2006, dated 05-10-2007 confirm the orders of the Appellate Commissioner and Income Tax Officer, Ward 19(2), Bangalore.

13

ITA.NO.824/2009

BETWEEN 1. The Director of Income Tax International Taxation Rashtrothana Bhavan, Nrupathunga Road, Bangalore. 2. The Income Tax Officer, Ward – 19(1), International Taxation, Rashtrothana Bhavan, Nrupathunga Road, Bangalore. ...Appellants

(By Smt.K.V.Aravind, Advocate) AND: CGI Information Systems and Management Consultants P. Ltd. 38/1, Naganathapura Electronic City Post, Bangalore – 560 100. ...Respondent

(By Sri.G.Sarangan, Sr. Adv for Sri.Balram.R.Rao, Adv)

ITA filed u/S.260-A of I.T.Act, 1961 arising out of

order dated 17-07-2009 passed in ITA.No.1376/Bang/2008, for the Assessment year 2007-08, praying that this Hon'ble Court may be pleased to: (i) formulate the substantial questions of law stated therein; (ii) allow the appeal and set aside the order passed by the ITAT Bangalore in ITA No.1376/Bang/2008, dated 17-07-2009 and confirming the order of the Appellate Commissioner and confirm the order

14

passed by the Income Tax Officer, Ward-19(1), International Taxation, Bangalore. These appeals coming on for Hearing this day, N. KUMAR J., delivered the following:

J U D G M E N T

All these appeals are by the revenue challenging the

order passed by the Income Tax Appellate Tribunal,

Bangalore Bench, holding that the assessee was not liable to

deduct tax under Section 195(1) of the Income Tax Act, 1961

(for short hereinafter referred to as ‘the Act’) from the

remittances made to a non-resident.

2. The substantial question of law that arises for

consideration in these appeals is as under:-

Whether the Tribunal was correct in

holding that the payments made by the

assessee for utilizing intranet facilities

provided by the non-resident assessee is not

liable to tax in India and no TDS need be made

as the provisions of Section 195(1) read with

15

9(1)(vi) and (vii) read with Article 12 of the

DTAA between India and Canada are not

applicable?

FACTS IN BRIEF

3. The assessee is engaged in the business of

design, development, implementation and support systems

for the Information Technology (IT) Sector. The assessee

entered into an agreement with CGI Group Inc., a company

incorporated in Canada for sharing costs by which the

Canada Company would procure licenses from Microsoft and

also the communication tool developed by CGI Group Inc.,

and the costs relating to that would be subsequently

invoiced on the assessee. Accordingly, invoice was raised on

the assessee by the Canada Company. While making the

remittance, the assessee deducted TDS at 20% under

Section 195(1) of the Act and also paid the same to

Government account. However, according to the assessee,

since it is a cost sharing agreement and payments were

made by the assesee for reimbursement of cost/expenses, no

16

income is embedded therein. Therefore, the assessee is not

liable to deduct tax under Section 195(1) of the Act. The

appeals were filed by the assessee before the CIT(A) under

Section 248 of the Act. The Appellate Authority sought for a

remand report from the Assessing Officer. The claim of the

assessee was that the payment was in the nature of

reimbursement of expenses. Hence, it was not liable to

deduct tax under Section 195(1) of the Act. Further, the

payments are not in the nature of royalty. The Appellate

Authority held that the payment made by the assessee to the

Canada Company cannot be considered as royalty as the

assessee was not liable to make deduction in respect of this

payment. However, it held the payment made by the

assessee is for rendering “any technical or consultancy

services” and, therefore, the assessee was liable to deduct

tax at source and dismissed the appeal.

4. Aggrieved by the said order, the assessee

preferred an appeal to the Tribunal. The Tribunal by a

17

lengthy order, after considering the rival contentions and

referring to various judgments held that, the payments made

by the assessee are reimbursement of expenses and no

income element is embedded therein; therefore, the

remittances cannot be considered as fees for technical

services. The assessee is liable to deduct tax under Section

195(1) of the Act only on the income embedded in the

remittance. Since there was no income element embedded in

the remittance, the assessee was not liable to deduct tax

from the remittance. It also affirmed the finding of the

Appellate Authority that the remittance made by the

assessee cannot be treated as royalty and Section 44D is

not applicable to the facts of this case. Therefore, the

appeals were allowed. The order passed by the Appellate

Authority as well as the original authority was set aside.

Aggrieved by this order, the revenue is in appeal.

5. The learned counsel for the revenue assailing

the impugned order contended that, the Tribunal has

18

proceeded on the assumption that, as the agreement

between the parties is a cost sharing agreement, the

remittance made by the assessee to the Canada Company is

towards such charges and no profit is embedded in the said

amount paid to the Canadian Company. Therefore, the said

amount was not chargeable to tax under the Act and

consequently, there is no liability on the part of the assessee

to deduct tax at source. He submits that though the

agreement is styled as “cost sharing agreement”, a reading of

the agreement shows that the Canadian Company had

granted a licence to use the facilities which exclusively

belongs to them and the consideration paid under the

agreement is for the right to use that right and, therefore, it

falls within Section 9(1) (vi) of the Act. It constitutes royalty

and the Tribunal has not properly appreciated the facts of

the case and the material placed on record. Therefore, the

order is liable to be set aside.

19

6. Per contra, the learned senior counsel appearing

for the assessee submitted that, no right in the intellectual

property is transferred under the agreement nor any licence

is granted under the agreement. As is clear from the

agreement, the Canadian Company developed a tool

providing Eportal-intranet facility. It was available only to

the members of the Group. The other members of the Group

agreed to share the cost of the said tool. Therefore,

the assessee agreed to share the cost of the tool. No profit is

embedded in the said payment as is clear from the clauses in

the agreement. Clause 4.4. provides that the term ‘cost’

incurred does not include any mark up and is limited to the

actual cost. Therefore, the Tribunal was justified in holding

that it is neither a payment towards royalty nor payment

towards technical services.

7. In the light of what is stated above and the rival

contentions, it is necessary for us to look in to the terms of

the agreement entered into between the parties, understand

20

the intention of the parties and then find out the nature of

transaction. Based on that factual finding, we have to decide

whether it falls within the definition of royalty as provided

under Section 9(1)(vi) or technical services as provided under

Section 9(1)(vii) of the Act. Only if the income is chargeable

to tax under the Act under the aforesaid provisions, the

liability of the assessee to deduct at source would arise. A

copy of the cost sharing agreement is made available to us,

which reads as under:-

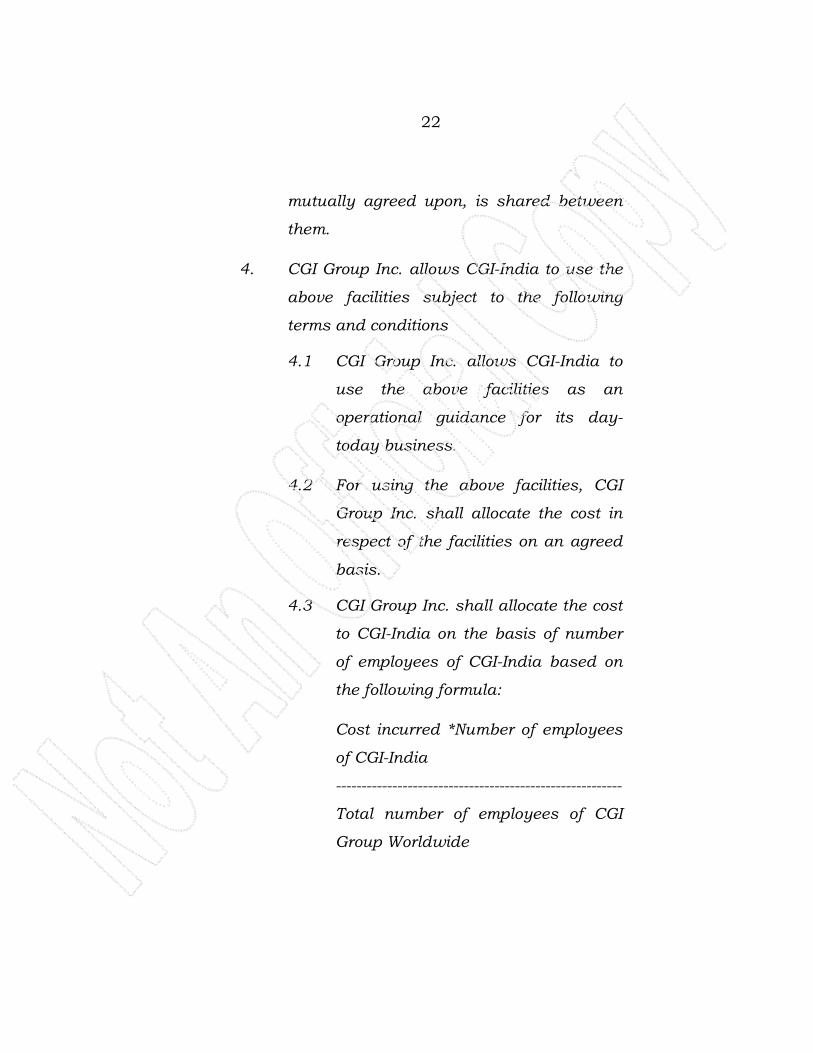

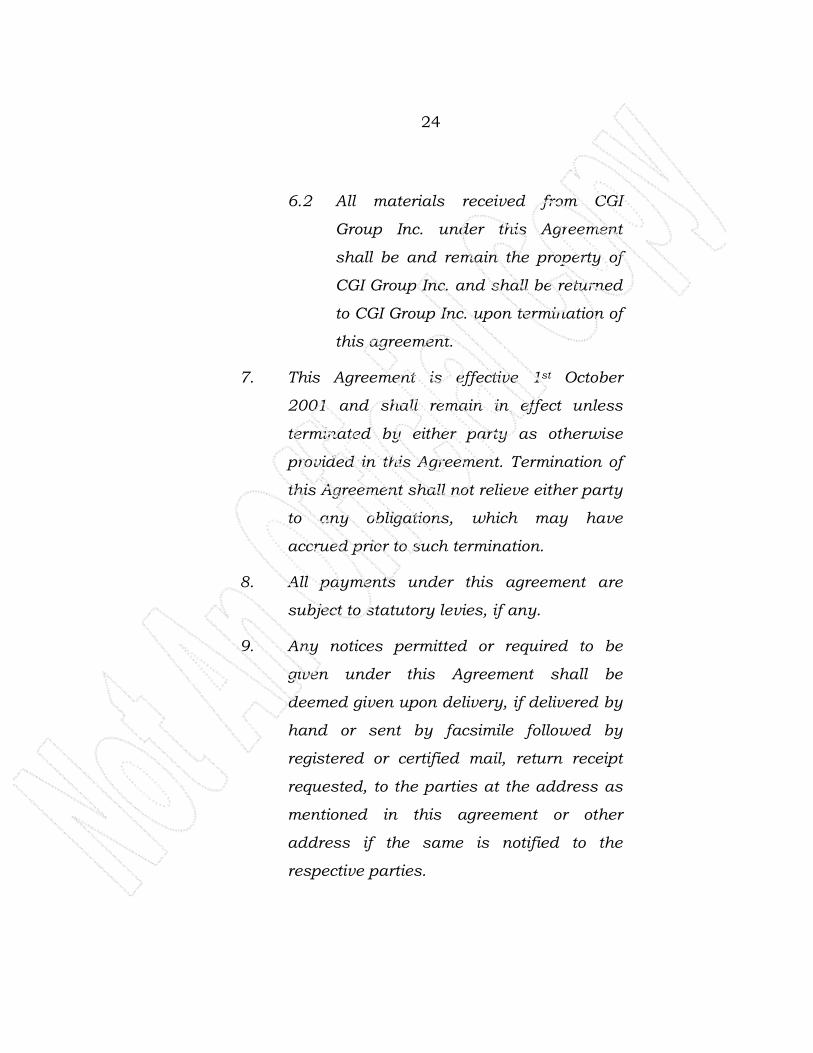

COST SHARING AGREEMENT This agreement is made by and between CGI

Information Systems and Management

Consultants Private Limited (CGI-India), a

Company incorporated under the Indian

Companies Act having its Registered Office at

38/1, Naganathapura, Singasandra Post,

Bangalore – 560 034 and CGI Group Inc. a

company incorporated under the provisions of the

laws of Quebec and having its registered office at