Incremental analysis is used to find the impact of changes in costs or revenues, given a specific potential scenario. Decisions involving incremental analysis include the following: Make or buy: Should we make a component ourselves or farm out the work to someone else? Qualitative considerations may or may not override quantitative issues. For example, we may be able to subcontract work more economically than we can do it ourselves, but if the contractor is unable to maintain the necessary level of quality or meet delivery schedules, subcontracting may not be worthwhile. The impact of quality and/or delivery problems may not be quantifiable, thus making the whole business a judgment call. Sell or process further: Sell or process further issues often arise in industries which refine raw materials. The key question is whether the incremental revenues from a more highly refined product will at least offset the increased costs associated with additional processing. Special order: Special orders typically involve special requests from customers who want a reduced price or some sort of special work. The extra effort might take the form of extra machining, special finishes, rush delivery [which could entail both an accelerated production schedule as well as air freight or other transportation costs], or an unusually small production run. As with the other decisions discussed here, quantitative and qualitative issues may be in conflict. Suppose an especially valuable customer want some sort of special deal, whether a reduced price or extra work. The lower revenue or added costs may mean taking a loss on the job, but we have to decide whether alienating the customer is more serious than the short term hit on profits. Some costs associated with special orders are not easily accounted for. Special production runs may require extra set ups of machinery which increase total indirect costs; however, such costs are often not easily accounted for, and therefore may not be readily added to the charges to the customer, even if the customer is willing to absorb such charges. Changes in production and/or technology : Modifications in production processes or acquisition of new machinery typically entail adjustments in costs. New machinery or a revised process may enhance efficiency in the use of labor and/or material. It is clearly important to know whether the improvements offset whatever incremental costs may be associated with the changes. It is obviously important to be able to understand how decisions like these affect both fixed and variable costs. If a given costs element does not change with a particular decision, it is irrelevant for purposes of that decision and we can ignore it. This may simplify calculations. For example, if the only change due to a decision is an increase or decrease in variable costs, all we need to do is recalculate the contribution margin. A question of relevance The basic concept underlying almost all incremental analyses is the idea of relevance: What revenues and /or costs are rel evant to the decision in qu estion? In

Transcript

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

many situations requiring incremental analysis, fixed costs remain unchanged,irrespective of the course of action finally taken. Therefore, those fixed costs areirrelevant for the purposes of the decision in question and can be ignored. [This is not tosay that fixed costs are unimportant, or that they don't eventually have to be taken intoaccount. In the long run, fixed costs have to be covered if we are going to make money.]However, incremental analysis is typically used for short run, one-time decisions.

When "one-time decisions" get to be routine, it may be time to reevaluate the situation.For example, suppose a customer wants some sort of special attachment on a product--what on the surface appears to be a "this month only" occurrence. Then perhaps two orthree months later, the same customer calls and says "Remember back in May you dida special job for us? Well, we need another thousand of those. How soon could youhave them?" At some point, management needs to determine whether the "one-timeoccurrence" has suddenly become the "normal circumstances."

Another key element in incremental analysis is the notion of sunk costs. Sunk costs

are costs which were incurred in the past. No future action or inaction can change the

situation. Suppose we spend a million dollars on June 1st for a large machine which will

enhance productivity. On June 2nd, a sales representative offers to sell us a competitive

machine for $500,000; this machine has twice the productivity of the one purchased onJune 1st. In this classic case of "buyer's remorse," it is tempting to we now have a $1.5

million decision. However, the million spent on machine #1 is a sunk cost. We may have

really messed up by not doing our homework and surveying all the options available

before we bought the machine. However, if the second machine really will have the

stated impact on productivity, it would be foolish not to spend the money [if we have, of

course; we may have "shot our wad" on machine #1]. However, no matter what we do,

the million is gone and is irrelevant to the decision about machine #2.

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

Managerial decisions are choices made based on financial and nonfinancial information.

Typically, financial information serves as the first hurdle in identifying a possible course

of action as an alternative. If the financial hurdle is met, then management must

consider the impact of the alternative on the environment, the company's employees,

its image, the community, its partners or alliances, and so on before making a final

decision.

Incremental analysis, sometimes called marginal or differential analysis, is used to

analyze the financial information needed for decision making. It identifies the relevant

revenues and/or costs of each alternative and the expected impact of the alternative on

future income.

To illustrate the concept, think about the decision to lease or buy a car. Leasing

involves a regular payment and the return of the vehicle at the end of the lease unless

a one-time payment is made. This arrangement means the car does not legally belong

to the person leasing it. To buy a car requires payment of the purchase price. Thepayment may be made in cash or by signing a note payable for the amount owed. If

you were to prepare financial statements under each alternative, they would look very

different. An operating lease for a car with payments of $300 per month would result in

the annual cost of the lease, $3,600, being reported as an expense on the income

statement. The purchase of a car results in an asset — and a liability, if a note was

signed — being recorded on the company's balance sheet.

Another example is the choice between alternatives A and B, given the following

relevant revenues and expenses:

Al ternative A Al ternative B Net I ncome Increase/(Decrease)

Revenues $100,000 $150,000 $50,000

Expenses78,000 105,000 (27,000)

Net Income$ 22,000 $ 45,000 $23,000

This example shows alternative B generates $23,000 more net income than alternative

A. Management must now consider the nonfinancial information to determine whether

alternative B should be accepted.

Several concepts are incorporated into incremental analysis and need to be defined

before discussing some specific applications of incremental analysis.

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

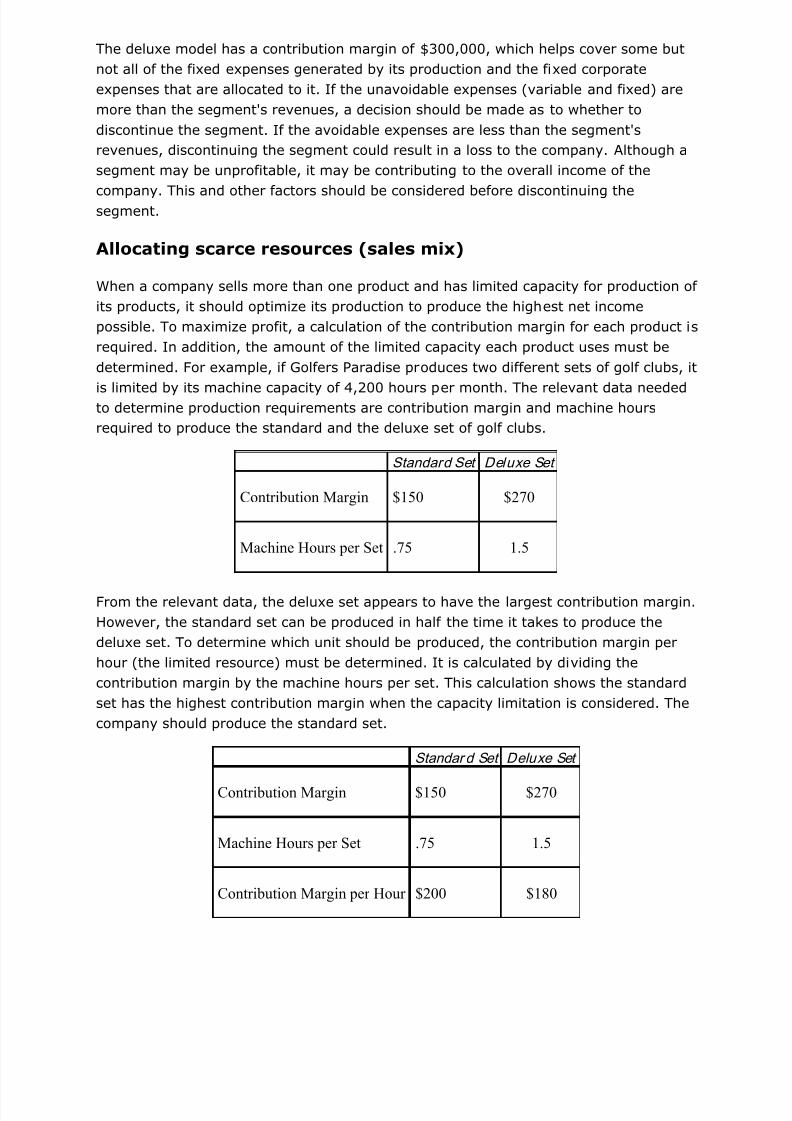

The deluxe model has a contribution margin of $300,000, which helps cover some but

not all of the fixed expenses generated by its production and the fixed corporate

expenses that are allocated to it. If the unavoidable expenses (variable and fixed) are

more than the segment's revenues, a decision should be made as to whether to

discontinue the segment. If the avoidable expenses are less than the segment's

revenues, discontinuing the segment could result in a loss to the company. Although a

segment may be unprofitable, it may be contributing to the overall income of the

company. This and other factors should be considered before discontinuing thesegment.

Allocating scarce resources (sales mix)

When a company sells more than one product and has limited capacity for production of

its products, it should optimize its production to produce the highest net income

possible. To maximize profit, a calculation of the contribution margin for each product is

required. In addition, the amount of the limited capacity each product uses must be

determined. For example, if Golfers Paradise produces two different sets of golf clubs, it

is limited by its machine capacity of 4,200 hours per month. The relevant data neededto determine production requirements are contribution margin and machine hours

required to produce the standard and the deluxe set of golf clubs.

Standard Set Deluxe Set

Contribution Margin $150 $270

Machine Hours per Set .75 1.5

From the relevant data, the deluxe set appears to have the largest contribution margin.

However, the standard set can be produced in half the time it takes to produce the

deluxe set. To determine which unit should be produced, the contribution margin per

hour (the limited resource) must be determined. It is calculated by dividing the

contribution margin by the machine hours per set. This calculation shows the standard

set has the highest contribution margin when the capacity limitation is considered. The

company should produce the standard set.

Standar d Set Deluxe Set

Contribution Margin $150 $270

Machine Hours per Set .75 1.5

Contribution Margin per Hour $200 $180

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

If both sets required the same machine hours, the deluxe set would be produced. If the

market for the standard set is less than 67,200 (the number of standard sets that could

be produced in a year), the deluxe sets should be produced for any excess capacity

remaining after the standard sets are produced.

What Does Incremental An alysis Mean?

A decision-making technique used in business to determine the true cost difference between alternatives.

Incremental analysis ignores sunk costs and costs that are the same between the two alternatives to look

only at the remaining costs. For this reason, it is also called the "relevant cost approach," "marginal

analysis" or "differential analysis."

Investopedia explains Incremental Analys is

If a company is considering replacing its old copy machine, using incremental analysis, the companywould not look at the cost of the existing copy machine because it is a sunk cost (the cost of buying itcannot be reversed). They would look at things like the cost of toner cartridges for each machine, the costof the electricity run each machine, and most importantly, the time saved by having employees use amore efficient model and perhaps the cost savings of being able to prepare documents in-house instead

of outsourcing them.

Chapter 11 Incremental Analysis

This chapter addresses incremental analysis which is a simplified approach to

a number of different short-term decisions that managers must often make. A

number of specific management decisions will be introduced in a later

chapter, however this chapter is devoted to the overall concept of incrementalanalysis that will use as a part of capital budgeting.

Decision Components

Decision-making involves choosing between alternatives. The focus of

incremental analysis is to examine what is different between the alternatives

Incremental amounts are often called differential or relevant, however thinking

of incremental amounts as 'what is different' will help you identify them more

quickly. Incremental analysisrelies on cost behavior concepts which separates

costs into variable and fixed components so that managers can anticipate how

each cost will behave in the future.

Why Use Incremental Analysis? Managers typically make decisions by selecting between at least twoalternatives. Because there is often a lot data and information available, amanager's time is used more effectively if he or she examines only theamounts that differ between the decisions. These differences are the onlyRELEVANT amounts that are needed to make a decision because no matterwhat decision a manager makes, non-relevant amounts stay the samebecause they do not differ between the alternatives. One option managerssometimes use in decision-making is to create budgeted, side-by-side income

statements that list the total revenues and total costs to be incurred undereach decision outcome. However, because many costs are the sameregardless of which decision is made, it is preferable, and much more efficientfor managers to concentrate on only the relevant amounts. It is fruitless towaste time on irrelevant amounts when incremental analysis identifies thesame decision choice.

Deciding What is Relevant and What is Not Relevant The easist way to think about costs when deciding are they relevant or not is to set up two

column and label each with the respective decision alternative. For example, a manager is

deciding whether to buy a new delivery truck or keep the old truck. The first column could be

labeled as 'Keep Old Truck', and the second column could be labeled as 'Buy New Truck.'

Under each column label, list the total costs and revenues under each situation. The costs that

are the same under both alternatives are not relevant and can be ignored in the analysis. The

costs that differ are relevant and should be used in the analysis.

Opportunity costs are always relevant because they represent the benefitgiven up as a result of choosing one option over the other. While they are notcash outlays, the represent an increase in profit for one decision over theother.

Sunk costs are never relevant because they have already occurred andcannot be changed no matter which decision option is chosen.

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

How to Perform Incremental Analysis The following steps should be performed to create an incremental analysis: Step 1: Compare revenues under both alternatives. Revenues that changeare relevant. Revenues that do not change are not relevant. Eliminate allirrelevant amounts. If possible, list on the differences.

Assume that AT, Inc. plans to produce and sell 80,000 calculators next year to be soldat $7 each. Management is considering raising the selling price to $8 per unit, but thisis likely to cause the sales volume to drop to 76,000 units. Since both units and sellingprice will change, you must consider both changes as part of the incrementalrevenue. The incremental approach determines the difference between old and newrevenue:

Original revenue: 80,000 x $7 $560,000

Adjusted revenue: 76,000 x $8 608,000

Incremental revenue $48,000 Step 2: Compare costs under both alternatives. Costs that do not change are not relevant.

Eliminate all irrelevant amounts, including sunk costs. List only costs that change because they

are the only costs that are relevant. Assume that the variable cost per unit is $4 for AT, Inc. and fixed costs are $100,000. The

relevant variable cost is the difference between the total variable costs in both alternatives.

There will be a cost savings for variable costs because fewer units will be sold. Because fixed

costs remain the same at all levels of activity, there is no change to fixed costs. Step 3: Separate relevant costs into variable and fixed categories and determine the differences

of each. The relevant variable cost is $4 per unit. The number of units will decrease given that 4,000fewer units (80,000 - 76,000) will be sold. Instead of additional costs, there will be a cost

savings:

Variable cost savings: (80,000 - 76,000) x $4 $16,000

Step 4: List and clearly label each incremental revenue, incremental cost, and incremental cost

savings. Include a + sign if the incremental amount increases profit (i.e., a benefit). Show the

amount in ( ) parentheses if profit will decline. Note that a decrease in costs causes an increase

in profits, so the amount should be added to reflect the increase in profit. Total up the amounts.

If the result is positive (incremental revenues exceed the incremental costs), profit increases, sothe decision should be accepted. If the result is negative (incremental revenues are less than

incremental costs), profit decreases, so do not accept.

Original revenue: 80,000 x $7 $560,000

Adjusted revenue: 76,000 x $8 608,000

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

(80,000 - 76,000) x $4 + 16,000 Incremental increase in profit +$64,000 The net effect of the changes is an increase in profit of $64,000. Note that the incremental

analysis did not determine the total profit under either alternative. Only the relevant amounts

were considered.

Qualitative Issues Qualitative effects (nonfinancial amounts) must be considered regardless, but

should not be the sole basis for decision.

Walk-Thru Problem #1 Walker Company sells hammers. During the past year, 4,000 hammers were produced and sold

at $20 each. Variable cost per unit was $9 and total fixed costs were $32,000. Walker would like

to change the selling price per hammer to $19 each, and feels that this will increase sales to

4,600 hammers per year. Which costs are not relevant and why? How much is the incremental

revenue? How much is the incremental profit? Solution: Fixed costs are not relevant since the amount stays the same regardless of whether theselling price stays at $20, or is reduced to $19.

Incremental revenue is: Incremental revenue: (4,600 x $19) - (4,000 x $20)

$7,400

Incremental profit is the difference between incremental revenue and incremental costs.Only variable costs are relevant because fixed costs stay the same in total no matterwhat decision is made.

Incremental revenue +$7,400

Incremental cost: (4,600 - 4,000) x $9 (5,400) Incremental increase in profit +$2,000

Walk-Thru Problem #2 Don’s Donuts budgets the following costs for the production of 36,000 boxes of donuts next

year: Rent, $20,000; other fixed costs, $6,000; materials, $54,000, and hourly labor,

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

$36,000. The normal selling price is $4.00 per box. A new convenience store has offered to

pay Don’s $3.00 per box to supply them with 10,000 boxes of donuts during the year. Assuming

that Don’s has the capacity to fill this order along with their other production and that accepting

this order will not cause problems with any of their other customers, should Don’s Donuts sell th

10,000 boxes to the cops? Justify your answer with computations. Solution: First determine incremental revenue:

Incremental revenue ($3.00 x 10,000) +

$30,000

If the order is accepted, revenue increases by $30,000 due to the increase of 10,000boxes sold at $3 per box. Incremental cost is based on the only the change in variablecosts since fixed cost remain the same in total no matter how many boxes of donuts aresold. Total variable cost is $54,000 plus $36,000, or $90,000 when 36,000 boxes ofdonuts are produced and sold. The unit variable cost is $90,000 divided by 36,000boxes for a cost of $2.50 per box. The analysis should appear as follows:

Incremental revenue ($3.00 x 10,000) +

$30,000

Incremental cost: $2.50 x 10,000 boxes (25,000)

Incremental increase in profit + $ 5,000

Because costs increase, profit drops. When profit declines, parentheses areplaced around the amount to show the effect on profit.

Yes, Don's Donuts should sell the additional boxes because incremental profits willincrease by $5,000.

Cost Classification for Decision Making (Decision Making Costs):

Learning objective of this article:

Define, explain, and give examples of cost classifications used in making decisions:differential costs, opportunity costs, and sunk costs.

Costs can be classified for decision making. Costs are important feature of many businessdecisions. For the purpose of decision making, costs are usually classified as differentialcost, opportunity cost, and sunk cost. It is essential to have a firm grasp of theconcepts differential cost & differential revenue, opportunity cost, and sunk cost.

Definition and Explanation of Differential Cost and Differential Revenue:

Decisions involve choosing between alternatives. In business, each alternative will have

certain costs and benefits that must be compared to the costs and benefits of the other

available alternatives. A difference in cost between any two alternatives is known as

differential cost. A difference in revenue between any two alternatives is known asdifferential revenues. Differential cost includes both cost increase (incremental cost) and

cost decrease (decremental cost). In general the difference (cost and revenue) between

alternatives are relevant in decision making. Those items that are the same under all

alternatives can be ignored.

The accountant's differential cost concept can be compared to the economist's marginal

cost concept. In speaking of changes in cost and revenue, the economists employ the

term marginal cost and marginal revenue. The revenue that can be obtained from

selling one more unit of product is called marginal revenue, and the cost involved inproducing one more unit of a product is called marginal cost. The economists marginal costis basically the same as the accountant's differential concept applied to a single unit of out put.

Example:

Differential cost can be either variable or fixed. To illustrate assume that a company isthinking about changing its marketing method from distribution through retailers to

distribution by door to door direct sale. Present cost and revenues are compared toprojected costs and revenues in the following table.

---------- ---------- ---------- Total 540,000 625,000 85,000

---------- ---------- ---------- Net Operating Income $160,000 $175,000 $15,000

======= ======= ======= *F = Fixed **V = Variable According to the above analysis, the differential revenue is $100,000 and the differential

cost is $85,000,leaving a positive differential net operating income of $15,000 under theproposed marketing plan. The net operating income under the present distribution is$160,000, whereas the net operating income under door to door direct selling is estimated

to be $175,000. Therefore the door to door direct distribution method is preferred, since it

would result in $15,000 higher net operating income. Note that we would have arrive atexactly the same conclusion by simply focusing on the differential revenue, differential cost,

and differential net operating income, which also shows a net operating advantage of$15,000 for the direct selling method. The company can ignore other expenses of $60,000.

Because it has no effect on the decision. If it were removed from the calculation, the door todoor selling method would still be preferred by $15,000. This is anextremely important principle in management accounting.

Opportunity Cost:

Definition:

Opportunity cost is the potential benefit that is given up when one alternative is selected

over another. To illustrate this important concept, consider the following examples:

Example 1:

Vicki has a part-time job that pays her $200 per week while attending college. She would

like to spend a week at the beach during spring break, and her employer has agreed to give

her the time off, but without pay. The $200 in lost wages would be an opportunity cost of

taking week off to be at the beach. Example 2:

Suppose that Neiman Marcus is considering investing a large sum of money in land thatmay be a site for future store. Rather than invest the funds in land, the company could

invest the funds in high-grade securities. If the land is acquired, the opportunity cost will be

the investment income that could have been realized if the securities had been purchasedinstead.

Example 3:

You are employed in a company that pays you $30,000 per year. You are thinking aboutleaving the company and returning to school. Since returning to school would require that

you give up $30,000 salary. The forgone salary would be an opportunity cost of seekingfurther education.

Opportunity cost is not usually entered in the accounting records of an organization, but it is

a cost that must be explicitly considered in every decision a manager makes. Virtually everyalternative has some opportunity cost attached to it.

Sunk Cost:

Definition:

A sunk cost is a cost that has already been incurred and that cannot be changed by anydecision made now or in future.

8/13/2019 Incremental Analysis is Used to Find the Impact of Changes in Costs or Revenues

Sunk costs cannot be changed by any decision. These are not differential costs and should

be ignored in decision making. To illustrate a sunk cost , assume that a company paid

$50,000 several years ago for a special purpose machine. The machine was used to make a

product that is now obsolete and is no longer being sold. Even though in hindsight thepurchase of the machine may have been unwise, no amount of regret can undo that

decision. And it would be folly to continue making the obsolete product to recover the

original cost of the machine. In short, the $50,000 originally paid for the machine has

already been incurred and cannot be differential cost in any future decision. For this reason,such costs are said to be sunk costs and should be ignored in decision making.