April - June 2013 A quarterly newsletter on transfer pricing developments India, at Arm’s Length We are pleased to present the fourteenth edition of India, at Arm’s Length, our quarterly publication that focuses on transfer pricing (TP) developments in India and provides a round-up of key developments pertaining to TP worldwide. There have been significant developments in the area of transfer pricing in India in the last quarter. The much awaited Rangachary Committee Report was released by the Central Board of Direct Taxes (CBDT). A new format for the TP Accountant’s Report (Form 3CEB) under section 92E of the Income-tax Act, 1961 (Act) was notified in line with the recent amendments extending the scope of TP regulations. Furthermore, there have been certain clarifications from the CBDT on TP issues relating to development centers. Indian Revenue authorities have also concluded the eighth round of TP audits, continuing with their rigorous enforcement on sensitive issues such as location savings. Some of these recent enforcement efforts and administrative developments are likely to require taxpayers to review the impact of these on their existing TP policies and documentation. The “Viewpoint” section of this edition provides an overview of the “location savings” issue in the context of global scenario and an India perspective. In our “Insights” section, we provide information on current trends and experiences in the field of TP controversy and dispute resolution. “By Order!” covers TP decisions in India, while “Around the world” provides a round-up of key TP developments around the world. We hope you find this publication both timely and useful, and we look forward to your feedback and suggestions to improve it further. Best regards, Ernst & Young Transfer Pricing team In this edition: Viewpoint 02 Insights 06 By order! 09 Around the world 16

Transcript

April - June 2013A quarterly newsletter on

transfer pricing developments

India, at Arm’s LengthWe are pleased to present the fourteenth edition of India, at Arm’s Length, our quarterly publication that focuses on transfer pricing (TP) developments in India and provides a round-up of key developments pertaining to TP worldwide.

There have been significant developments in the area of transfer pricing in India in the last quarter. The much awaited Rangachary Committee Report was released by the Central Board of Direct Taxes (CBDT). A new format for the TP Accountant’s Report (Form 3CEB) under section 92E of the Income-tax Act, 1961 (Act) was notified in line with the recent amendments extending the scope of TP regulations. Furthermore, there have been certain clarifications from the CBDT on TP issues relating to development centers.

Indian Revenue authorities have also concluded the eighth round of TP audits, continuing with their rigorous enforcement on sensitive issues such as location savings.

Some of these recent enforcement efforts and administrative developments are likely to require taxpayers to review the impact of these on their existing TP policies and documentation.

The “Viewpoint” section of this edition provides an overview of the “location savings” issue in the context of global scenario and an India perspective.

In our “Insights” section, we provide information on current trends and experiences in the field of TP controversy and dispute resolution.

“By Order!” covers TP decisions in India, while “Around the world” provides a round-up of key TP developments around the world.

We hope you find this publication both timely and useful, and we look forward to your feedback and suggestions to improve it further.

Best regards,

Ernst & Young Transfer Pricing team

In this edition:

Viewpoint 02

Insights 06

By order! 09

Around the world 16

2 India, at Arm’s Length

Viewpoint

IntroductionIn the past decade, since the introduction of TP regulations in India, there has been a significant rise in TP litigation as well as the nature of issues, which are being contested by Revenue authorities. TP aspects of “location savings” seem to be yet another emerging challenge in the transfer pricing universe in India.

With the advent of globalization, many multinational enterprises (MNEs) offshore some of their global operations to economies, such as India and China, to take advantage of the relatively low labor costs. While its initial value proposition hinged on basic outsourcing advantages of cost and talent, the industry focus has shifted to enhanced value-added services, innovation and transformation. Outsourcing has developed as a result of economic pressure in some markets to become one of the top strategic matters of many MNEs. Global sourcing is now evolving from being tactical to being of strategic benefit. India has retained its position as the leading global off-shoring destination.

Where significant location savings are derived, the question arises whether and, if so, how the location savings (assuming they are retained by the MNE — and not passed on to customers — locating to the place where costs are low) should be shared among related parties.

This article provides an overview of the TP aspects of “location savings” issue in the context of global scenario and an India perspective.

Concept of “location savings”Location savings are generally defined as the (net) cost savings realized by an MNE as a result of transfer of some of its functions from a high-cost to a low-cost jurisdiction resulting in maximization of profits. Cost savings typically result from the lower cost production/service such as labor cost, raw material costs, rent, training costs, subsidies, incentives including tax exemptions and infrastructure costs. Such savings are netted against potential dis-savings (additional costs) such as relocation costs, transportation costs, warranty costs, legal/regulatory constraints, funding challenges etc.

UN Practical Manual on Transfer Pricing for Developing Countries (UN Manual) defines location savings as follows:

“Location savings are the net cost savings that an MNE realizes as a result of relocation of operations from a high cost jurisdiction to a low cost jurisdiction.”

Location savings also finds a brief mention in the chapter on business restructuring in para 9.148 of the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2010 (OECD Guidelines) as follows:

“Location savings can be derived by an MNE group that relocates some of its activities to a place where costs (such as labor costs, real estate costs, etc.) are lower than in the location where the activities were initially performed, account being taken of the possible costs involved in the relocation (such as termination costs for the existing operation, possibly higher infrastructure costs in the new location, possibly higher transportation costs if the new operation is more distant from the market, training costs of local employees, etc.).”

Location savings focuses only on reduction in costs under relocation circumstances; however, other geographical benefits such as highly specialized skilled manpower and knowledge, proximity to growing local/regional market, large customer base with increased spending capacity, advanced infrastructure (e.g. information/communication networks, distribution system) or market premium are not discussed in the location saving concept. This is where location‐ specific advantages come in the picture, which also takes into account other geographical benefits apart from location savings.

Accordingly, taken together, location savings and each of the other geographical benefits are called location specific advantages [LSAs].

Location rent is the incremental profits derived from LSAs. UN Manual in Para 5.3.2.42 defines location rent as “The incremental profit, if any, derived from the exploitation of LSAs is known as “location rent”.

The prime focus of this section is on the concept of location savings and its importance from transfer pricing perspective.

Quantification of location savings and its allocation from transfer pricing perspectiveAs mentioned in the UN Manual, it is possible that in a particular case, even though LSAs exist there may not be any attribution for location savings. For example, in situations in which the market for the end product is highly competitive and potential competitors also have access to LSAs, much or all of the benefits of LSAs will be passed on to customers through reduced prices of products, resulting in little or no location rents.

Location Savings: another emerging challenge in transfer pricing

3India, at Arm’s Length

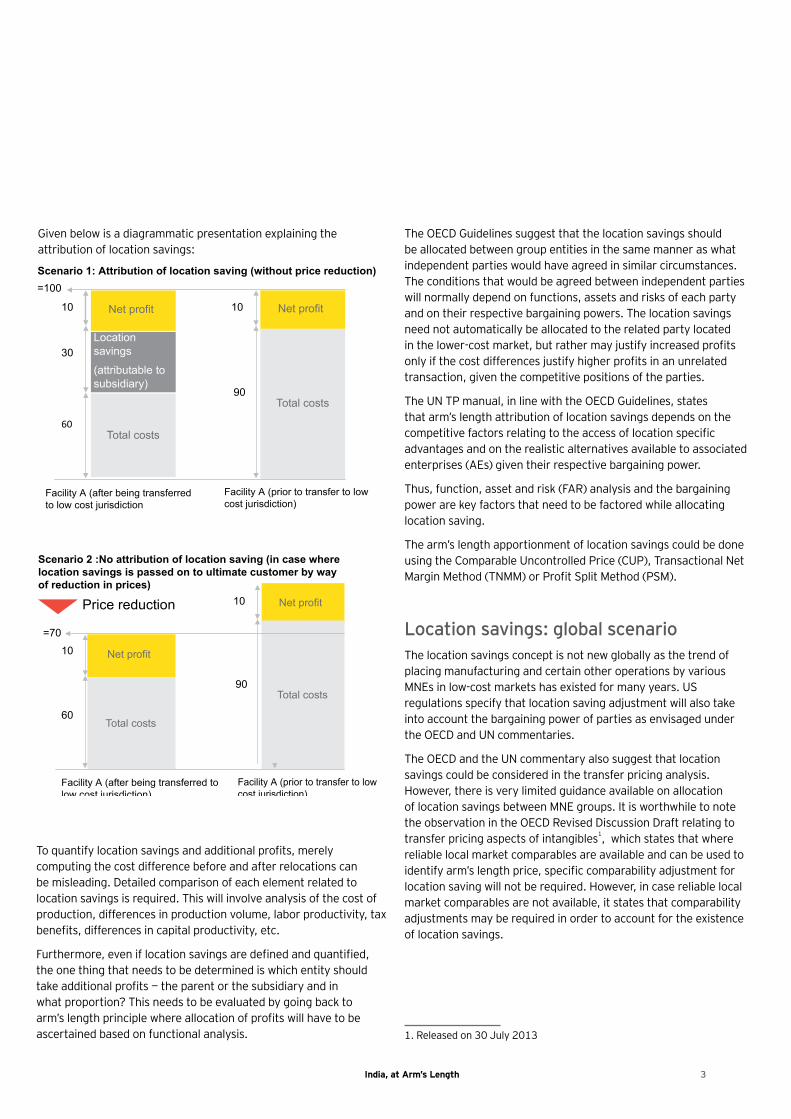

To quantify location savings and additional profits, merely computing the cost difference before and after relocations can be misleading. Detailed comparison of each element related to location savings is required. This will involve analysis of the cost of production, differences in production volume, labor productivity, tax benefits, differences in capital productivity, etc.

Furthermore, even if location savings are defined and quantified, the one thing that needs to be determined is which entity should take additional profits — the parent or the subsidiary and in what proportion? This needs to be evaluated by going back to arm’s length principle where allocation of profits will have to be ascertained based on functional analysis.

The OECD Guidelines suggest that the location savings should be allocated between group entities in the same manner as what independent parties would have agreed in similar circumstances. The conditions that would be agreed between independent parties will normally depend on functions, assets and risks of each party and on their respective bargaining powers. The location savings need not automatically be allocated to the related party located in the lower-cost market, but rather may justify increased profits only if the cost differences justify higher profits in an unrelated transaction, given the competitive positions of the parties.

The UN TP manual, in line with the OECD Guidelines, states that arm’s length attribution of location savings depends on the competitive factors relating to the access of location specific advantages and on the realistic alternatives available to associated enterprises (AEs) given their respective bargaining power.

Thus, function, asset and risk (FAR) analysis and the bargaining power are key factors that need to be factored while allocating location saving.

The arm’s length apportionment of location savings could be done using the Comparable Uncontrolled Price (CUP), Transactional Net Margin Method (TNMM) or Profit Split Method (PSM).

Location savings: global scenarioThe location savings concept is not new globally as the trend of placing manufacturing and certain other operations by various MNEs in low-cost markets has existed for many years. US regulations specify that location saving adjustment will also take into account the bargaining power of parties as envisaged under the OECD and UN commentaries.

The OECD and the UN commentary also suggest that location savings could be considered in the transfer pricing analysis. However, there is very limited guidance available on allocation of location savings between MNE groups. It is worthwhile to note the observation in the OECD Revised Discussion Draft relating to transfer pricing aspects of intangibles1, which states that where reliable local market comparables are available and can be used to identify arm’s length price, specific comparability adjustment for location saving will not be required. However, in case reliable local market comparables are not available, it states that comparability adjustments may be required in order to account for the existence of location savings.

1. Released on 30 July 2013

Scenario 1: Attribution of location saving (without price reduction)

Net profit

Location savings

(attributable to subsidiary)

Total costs

Net profit

Total costs

10

90

30

10

60

=100

Facility A (after being transferredto low cost jurisdiction

Facility A (prior to transfer to lowcost jurisdiction)

Given below is a diagrammatic presentation explaining the attribution of location savings:

Scenario 2 :No attribution of location saving (in case wherelocation savings is passed on to ultimate customer by way of reduction in prices)

Net profit

Total costs

Net profit

Total costs

10

90

10

60

Price reduction

Facility A (after being transferred tolow cost jurisdiction)

Facility A (prior to transfer to lowcost jurisdiction)

=70

4 India, at Arm’s Length

Furthermore, the US Tax Court, in certain cases,2 has dealt with the issue of location saving. Generally the decisions are very fact specific and the key principles, which emerge are consistent with the OECD commentary (as discussed above) on recognition of location saving, basis of allocation, etc.

Location saving concept was also considered recently in Finland by the Supreme Administrative Court of Finland. The decision recognizes location savings and the allocation of these benefits to a low-cost subsidiary provided similar functions were conducted in Finland before the reorganization and benefits availed can be clearly crystallized.

Location savings: India viewpointThe term “location savings” has not been defined/discussed in the Indian transfer pricing regulations. While the tax authorities appear to be generally aware of issues relating to location savings as a transfer pricing concept, there is no formal articulation of the approach for identifying, quantifying, and allocating location savings under the arm’s-length standard in the course of TP audits.

2. Sundstrand Corporation and subsidiaries Vs. Commissioner, (96 T.C.M (CCH) 226 (1991) Compaq Computer Corporation Vs. Commissioner (78 T.C.M. (CCH) 20 (1999) Bausch & Lomb Vs. Comr. 92 T.C 525, 581 (1989)

However, there have been instances where the tax authority has sought to allocate high mark-ups to Indian affiliates by classifying the Indian affiliate as a ‘‘high value’’ or ‘‘high end’’ service provider with passing reference to location savings being generated.

The Indian tax authorities believe that while India, through its cost competitiveness, provides locations savings to MNEs and significantly increases MNEs’ overall profits, the concept is not attributed to the Indian operations in the transfer price. There have also been limited instances where the tax authorities have sought to allocate location savings to India by applying the PSM or its variant.

In the UN TP Manual, Indian administration has advocated location savings as one of the key aspects in comparability analysis. Furthermore, it has commented that PSM should be preferred to allocate location-saving profits considering the functional analysis and bargaining power of enterprises. Indian administration has also commented that cost plus remuneration methodology does not adequately allocate location savings due to difficulty in comparability. Accordingly, PSM can also be considered to determine the arm’s length location savings.

Rangachary Committee in its Report on issues relating to taxation of development centers, states that it may be appropriate for India to seek for a higher mark up under TNMM, possibly, also factoring in location savings and location advantage.

5India, at Arm’s Length

There have been couple of rulings by the Delhi Tribunal wherein location savings concept was discussed. While in case of Li Fung (India) Private Limited, Delhi Tribunal recognized the location benefits associated in low-cost jurisdiction and advocated an increased remuneration to the entity in a low-cost country, in case of Gap International Sourcing (India) Private Limited, the Tribunal observed that:

• ‐ The element of location savings in a developing economy is a characteristic of the entire industry, and not just one taxpayer.

• ‐ Location-specific savings, if any, would be captured in the profitability of the comparables used for benchmarking international transaction.

• ‐ Therefore, no separate allocation/addition is required to be made on account of location savings. In this case, concept of bargaining power of parties was also touched.

The concept of location savings is still evolving in the India transfer pricing context. Even in case of Li Fung, while the ruling raises the question on relevance of location savings/location-specific advantages in transfer pricing, it does not lay down an analytical framework to evaluate the existence of location savings and other location-specific advantages, quantify them and to whom they should be attributed under arm’s length conditions.

Outlook: the road aheadIndia has emerged as a hub for outsourced services such as software development, research and development, engineering design, and business processes as well as low-cost manufacturing. These typically are undertaken on a contract provider model, which insulates the Indian captive unit against most business risks. However, increasingly, some Indian entities have started taking on high-end functions.

In the context of above activities undertaken by Indian entities, a number of taxpayers in India find themselves in the challenging position of documenting and defending their transfer pricing issues as transfer pricing controversy is on the rise due to maturing tax administration audit procedures. Given the widespread extent of outsourced services in India and the increasing focus of the India tax administration on “location savings” aspect, it becomes imperative to carefully review transfer pricing arrangements and contracts for the Indian outsourced activity. Furthermore, it is important to undertake and document robust TP analysis to counter any such argument put forward by the authorities during TP audits.

6 India, at Arm’s Length

InsightsUpdate on the issue of applicability of the turnover filterApplication of turnover filter for selecting comparable companies while conducting benchmarking analysis has been a subject matter of controversy and litigation, particularly in case of service-oriented companies, especially in the ITES/software segment.

There have been conflicting decisions by the Income-tax Appellate Tribunals (ITAT or Tribunal) on appropriateness of use of turnover filter in the context of service-oriented companies. In some cases, it has been held that there is a direct nexus between the level of operations and the profitably because of economies of scale 3. However, recently Mumbai ITAT, in case of Capgemini India P Ltd., observed that the concept of “economy of scale” is relevant for manufacturing and not for service-oriented companies and that there is no linear relationship between margin and turnover of comparables. Similar observations have been made by Mumbai ITAT in case of Wills Processing Services (I) Pvt. Limited.

In view of the contrary decisions on the issue, a Special Bench comprising three members (Shri PM Jagtap, Shri AD Jain and Shri B. Ramkotaiah) had been constituted in Delhi by the Hon’ble President in the case of M/s. Giesecke & Devrient India (P) Ltd, Gurgaon on appropriateness of turnover filter for selection of comparables to conduct benchmarking analysis. On a practical front, cases before Tribunals, wherein turnover filter has been taken as one of the grounds of appeal, were adjourned in view of the Special Bench constituted on the issue.

However, the Assessee in the aforesaid case [M/s. Giesecke & Devrient India (P) Ltd] moved an application for withdrawing the questions referred before the Special Bench on turnover filter and the same has been allowed by the Special Bench. Accordingly, the appeals of interveners and other adjourned cases would now continue as per the normal appellate procedure.

Rangachary Committee issues its first report on issues relating to taxation of development centersThe Prime Minister constituted a committee under the chairmanship of Mr. N Rangachary, a former Chairman of CBDT, to review taxation of development centers and IT Sector. The Committee submitted its first report dated 14 September 2012, which has been recently released by CBDT in the public domain.

3. Genisys Integrated Systems India P. Ltd v. DCIT (ITA No. 1231(Bang.) / 2010)

DCIT Vs M/s Quark Systems Private Limited (2010-TIOL-31-ITAT-CHD-SB) Egain Communication Private Limited vs ITO (2008-TIOL- 282-ITAT-Pune) Agnity India Technologies Pvt Ltd vs ITO (ITA No. 3856(Del)/2010)

The Committee received representations from various stakeholders. The first report of the Committee covers key concerns, as highlighted by various stakeholders, relating to taxation of development centers as well as taxation issues of the IT sector.

The Report appreciates that transfer pricing disputes are a major cause of concern for captive development centers in India. It provides recommendations on the following specific issues relating to transfer pricing:

• Work carried on by the development centers

• Application of the most appropriate method

• General transfer pricing issues not specific to IT sector

The Report recognizes practical difficulties in the application of PSM in case of development centers engaged in contract R&D services and recommends application of TNMM in such cases. The Report further provides for parameters, which would need to be cumulatively satisfied by a development center to be regarded as contract R&D service provider with insignificant risk.

The Report also mentions that finalization of safe harbour rules for certain sectors including development centers, requires detailed data analysis and the Committee will respond to this matter in its subsequent reports.

CBDT issues revised circulars on transfer pricing issues relating to development centers CBDT issued Circular 2 and 3 dated 26 March 2013 on conditions for identifying development centers engaged as contract R&D service with insignificant risk (Circular 3) and on application of PSM for development centers (Circular 2).

Circular 3 prescribed the conditions that need to be cumulatively satisfied for an arrangement to be regarded as contract R&D. The Circular further stated that the satisfaction of these conditions will be determined primarily by analyzing whether the conduct of parties is consistent with the purported contractual allocation of functions and risks. Furthermore, Circular 2 provided for application of the PSM as the most appropriate method (MAM) in case of controlled transactions involving R&D activity. In case of non-availability of data for applying PSM, the Circular permitted the use of other methods (e.g. TNMM) for such R&D centers, by selecting suitable comparable data and by making adjustments for value of intangible property (IP) that is transferred, location savings etc, as appropriate.

These circulars have been subject matter of debates and discussions and various representations were made to the CBDT by

7India, at Arm’s Length

various stake-holders in the industry. In light of the representations received from the IT Industry and based on recommendations of the Rangachary Committee, the Board has reviewed the earlier circulars and has now issued revised circulars.

• Circular No 5/ 2013 dated 29 June 2013 (Circular 5) rescinding Circular 2 on application of PSM

The Income-tax Act provides that the arm’s length price in relation to an international transaction/specified domestic transaction shall be determined with regard to the “most appropriate method.” The Rules also provide for factors that need to be considered to determine the most appropriate method.

CBDT is of the view that Circular 2 created an impression that PSM was the preferred method for the transactions involving transfer of unique intangibles or in multiple interrelated international transactions. Accordingly, in order to remove the ambiguity created by the aforesaid Circular, CBDT has now withdrawn the same with immediate effect.

• Circular No 6/2013 dated 29 June 2013 (Circular 6) on amendment to conditions relevant for identifying development centers engaged in contract R&D services with insignificant risks

According to Circular 6, R&D centers set up by foreign companies can be classified into the following three broad categories based on functions, assets and risk assumed by the center established in India:

• Centers that are “entrepreneurial” in nature, where the development center performs significantly important functions and assumes substantial risks

• Centers that undertake “contract research and development” where functions, assets and risks are minimal

• Centers that are based on “cost-sharing arrangements” and fall between the first and the second case above

The Circular lays down the guidelines for identifying a development center as a contract R&D service provider with insignificant risk. The Circular states that the tax authorities will determine the appropriate characterization of the development center and the choice of the ”most appropriate method” shall be done with regard to the guidelines provided under the transfer pricing provisions and the Rules made there under. It also states that the tax authorities will be guided by the conduct of the parties and not merely by the terms of the contract.

The amendments by Circular 6, while retaining the substance of Circular 3 conditions, appear to provide a relatively enhanced degree of operational latitude and flexibility to qualify inter-company arrangements as providing contract R&D services.

Board Press Release dated 29 June 2013 also states that ”Safe Harbour rules” are under consideration and will be issued shortly. These rules are expected to provide relative certainty for transfer pricing issues relating to development centers that are engaged in providing contract R&D services.

Changes in the reporting requirements

Accountant’s report (Form 3CEB) to be filed electronically from AY 2013-14

CBDT has issued a notification4 amending Rule 12 of the Income-tax Rules, 1962 and mandating e-filing of Form 3CEB under Section 92E from AY13–14 onwards.

However, still there is no clarity in respect of detailed procedure/guidelines to be followed for electronic filing of Form 3CEB.

Changes in the format of Form 3CEB – additional reporting requirements

CBDT has also notified5 the new format of the Accountant’s Report in Form 3CEB, to be filed under Section 92E.

The scope of the term “international transaction” was expanded by the Finance Act, 2012 to include business restructuring, intra-group financing arrangements, etc. Additionally, specified domestic transactions have also been brought under the ambit of the transfer pricing regulations. The new format, inter alia, provides for the reporting requirements taking into account the extended scope of international transaction and the specified domestic transactions.

This new format also requires reporting of the following transactions:

• Transactions relating to share capital — transactions such as purchase or sale of marketable securities and issue and buyback of equity shares;

• Transactions in the nature of guarantee;

• International transactions arising out of/ being part of business restructuring or reorganization

5. Notification No. 41/2013/ F.No.142/42/2012-TPL dated 10 June 2013

8 India, at Arm’s Length

Issue of Guidance Note on Report under Section 92E

The Institute of Chartered Accountants of India (ICAI) has recently released a Guidance Note on Report under Section 92E of the Act. The Guidance Note is comprehensive and clarifies the nature and scope of information relevant for reporting under Section 92E. However, the Guidance Note was issued prior to the issue of new format of Form 3CEB and hence, does not cover the updated reporting requirements envisaged in the new format.

APA: first round of discussions post filing of main applicationThe APAs scheme has been widely welcomed by taxpayers. By 31 March 2013, close to 150 applications were filed by taxpayers who found themselves in the challenging position of defending their intra-group pricing due to transfer pricing controversies witnessing a sharp increase in the country.

The APA authorities have commenced the work on the applications and have already had initial meetings in the months of April and May 2013. In some cases, the APA authorities have also initiated site visits. Based on the discussions during initial meetings, it is understood that the APA authorities have plans to initiate the work on economic analysis for the applications received over next one or two months.

While globally, conclusion of unilateral APA takes around 1 to 2 years, the Indian APA authorities have assured closure of negotiations at the earliest. The efforts taken by the APA authorities in this regard also reflect in the swift progress made in various cases and the time bound approach followed for different stages involved during the process.

While the deadline for filing an application for APA for FY14–15 is 31 March 2014 (for continuing transactions), taxpayers evaluating the APA route should consider expediting the same in order to fast track the dispute resolution.

CBDT issues FAQs on APA

Since the APA is a new program, to increase awareness of the taxpayers about the APA program and its implementation, CBDT has released a booklet called the APA Guidance Booklet with FAQs (APA Guidance). The APA Guidance deals with the procedure to be followed by a taxpayer and the tax authorities before a taxpayer can enter into an APA.

The FAQs section in the APA Guidance provides clarifications on certain general issues raised by the taxpayers with regard to the APA process, disclosure requirements in the application, critical assumptions, detailed functions performed, assets employed and risks assumed (FAR) analysis, conversion of a unilateral APA to a

bilateral/multilateral APA, amendment/renewal/withdrawal of an APA, profit attribution to permanent establishments (PE) and the impact of an APA on the actions of the Assessing Officer/Transfer Pricing Officer. The FAQs section of the Guidance also provides clarifications on the procedural and documentary information required to be provided to APA authorities. The FAQs also seek to clarify certain grey areas such as:

• APA to provide for the “arm’s length price” and benefit of range (i.e., variation of up to 3%) not to be allowed;

• Bilateral APA not feasible with a country where the tax treaty does not contain specific provision for corresponding adjustment of TP disputes [i.e., Article 9(2) of OECD Model Convention];

• Consideration of inter-quartile range.

The APA Guidance provides clarity on many other issues that taxpayers may have had about the APA program. It is expected that the APA Guidance will prove to be an effective and convenient tool to assist taxpayers in complying with the provisions of the program.

Computation of arm’s length price: notified tolerable limit for determination of ALPThe Ministry of Finance released Notification No 30/2013 dated 15 April 2013 providing for the tolerance limit (safe harbour) of 1% of the arm’s length price (ALP) in case of wholesale traders and 3% of the ALP in all other cases. The revised tolerance limit is applicable for transactions undertaken during the financial year ending 31 March 2013, i.e., AY 2013–14. Earlier, the Income Tax Act, 1961 as amended by Finance Act 2012 had reduced the tolerance limit to 3% from the earlier range of 5%.

The notification does not provide any rationale as to why the “wholesale traders” are separately classified and the need for specifying a separate range. Furthermore, neither the Act nor the notification defines the term “wholesale traders.” There is no clarity on whether the lower range of 1% is for the “trading activity” or the “trader.” For example, the complication gets augmented where a taxpayer is engaged in multiple businesses, say, wholesale trading, manufacturing and service activities. This distinction between the two categories of taxpayers could lead to ambiguous results where a particular transaction is concluded to be at arm’s length in case of a manufacturer or retailer but not in case of distributor.

There might arise an issue where reliance on other legislations (such as FDI Policy and Central Excise Act, 1944) will be relevant in order to understand the term “wholesale traders.”

The notification has various open ends and these interpretational issues could again lead to significant litigation unless some follow up clarifications are issued by the Ministry of Finance well in time.

9India, at Arm’s Length

M/s Ford India Private Limited v. DCIT (ITA No. 2089/Mds/2011) - Chennai TribunalChennai Tribunal confirms marketing intangible adjustment, follows LG rulingFord India Private Limited (Ford India or taxpayer) is a wholly owned subsidiary of Ford Motor Company, USA (FMC) and is engaged in the business of manufacturing and distribution of vehicles. Ford India has entered into a technical collaboration agreement with FMC and obtained the license to manufacture motor vehicles using the technical knowhow supplied by FMC. As a consideration, Ford India paid royalty to FMC. Licensed products were motor vehicles, which carried the logo of “Ford” along with the model name.

During FY06–07, Ford India incurred advertising and sales promotion expenses amounting to INR1.26 billion including INR290.7 million in relation to sales consultant remuneration,

training expenses and customer satisfaction surveys. Furthermore, Ford India paid product development expenses amounting to INR148.4 million to FMC.

During the TP audit proceedings for AY07–08, the TPO observed that it was mandatory for Ford India to use “Ford” logo on its motor vehicles through which FMC ensured that its brand name is developed in India over a period of time. Furthermore, the TPO contended that Ford India was only a contract manufacturer of FMC. From a global study of royalty rates on a range of products, TPO came to a conclusion that royalty payment in similar cases varied between 1% and 15%. Accordingly, the TPO considered 1% of sales of Ford India as the ALP for development of brand name and logo of FMC in India and proposed an addition of INR219.1 million.

By order!

10 India, at Arm’s Length

Moreover, the TPO noticed that Ford India incurred AMP expenses to the tune of 5.75% of its sales as compared to 2.58% of sales incurred by comparable companies (Tata Motors Limited, Mahindra and Mahindra Ltd. and Hindustan Motors Ltd.) selected by the TPO. Accordingly, the difference of 3.17%, i.e., excess expenditure on AMP incurred by Ford India was treated as expenditure incurred for promoting “Ford” brand in India and addition of INR694.8 million was proposed.

In relation to product development expenses, the TPO mentioned that since legal ownership of the products developed vests with FMC and assets created through such developmental efforts were real and tangible, Ford India should have recouped the entire sum of INR148.4 million from FMC. Hence, the TPO proposed addition of INR148.4 million.

Aggrieved by the order of the TPO, Ford India filed its objections before DRP. DRP upheld the order of the TPO.

Aggrieved by the directions of DRP, Ford India filed an appeal before ITAT. Chennai ITAT held as follows:

Existence of a transaction and applicability of Special Bench ruling in case of LG Electronics India Private Limited

ITAT stated that there is nothing in the “Technical collaboration agreement,” which precluded Ford India from manufacturing and selling any other motor vehicles other than those manufactured using technology provided by FMC. Ford India admittedly advertised its various brands of cars but each brand started with the logo of “Ford.” Therefore, Ford India made a simultaneous promotion of “Ford” logo. Further, Ford India being a 100% subsidiary of FMC, it is difficult to digest that Ford India could manufacture cars other than those branded as “Ford”. Accordingly, since FMC exercised total control over Ford India, the AMP expenses were incurred according to the plan and strategy of FMC.

In view of the above, ITAT concluded that there was an international transaction to create and improve the marketing intangible, i.e., “Ford” logo and the transaction was in the nature of service as held by Special Bench in case of LG.

Can TPO take suo moto cognizance of a transaction for ALP analysis?

Ford India had not reported the brand promotion exercise as an international transaction as required under Section 92E of the Act. As held by Special Bench in LG ruling, the Chennai Tribunal ruled that even if an international transaction is not reported, it was well within the powers of the TPO to scrutinize the said transaction. Furthermore, by virtue of clause (2B) to Section 92CA inserted by Finance Act 2012 with retrospective effect from 1 June 2002, power of the TPO in this regard has been clarified.

Two separate elements of brand promotion

ITAT held that Department was confused in relation to the demarcating line of the two elements, which made up the “Ford” brand development in India. The argument that Ford India reduced prices and increased AMP expenditure so that FMC derives marketing intangible in the nature of brand is not supported by empirical data. Furthermore, FMC was not charging royalty to Ford India for use of its logo on the cars manufactured by Ford India.

In view of the above, ITAT ruled that the only objective criteria that could be applied was the excess AMP expenditure and the addition of 1% on sales of Ford India as brand development fee was not justified.

Use of bright line test

ITAT placed reliance on Special Bench ruling in case of LG wherein it was held that bright line test is nothing but the cost plus method (CPM). Accordingly, ITAT held that the approach of the department falls within the purview of methods prescribed under Section 92C of the Act. Though the TPO, in effect applied CPM, but the second and third steps, i.e., determination of gross profit mark-up and applying it to the results was not done. However, this lacuna will not lead to a serious flaw, which would invalidate the determination of ALP as a whole by the TPO.

11India, at Arm’s Length

Whether selling expenses to be excluded from AMP?

Special Bench ruled in case of LG that AMP refers only to advertisement, marketing and promotion expenses. There has to be a divider between expenditure for promotion of sales and expenditure in connection with sales and the expenses relating to sales have to be treated differently. Accordingly, the expenditure in relation to sales consultant’s remuneration, training expenses and customer satisfaction surveys need to be excluded from AMP while making an adjustment.

Comparable companies

ITAT rejected the comparable companies identified by the TPO as well as Ford India. The comparable companies selected by TPO were rejected based on the ruling of the Delhi High Court in case of Maruti Suzuki India Ltd. Furthermore, the comparable companies identified by the assessee were rejected since they were using foreign brand. ITAT directed the TPO to identify a different set of comparable companies or consider the same set with appropriate adjustments.

Disallowance of product development expenditure

ITAT held that Ford India as well as FMC benefited from the product development expenditure. Fruits of improvement were enjoyed by Ford India whereas the ownership was with FMC. Accordingly, 50% of the advantage derived on account of product development expenditure benefited Ford India and the balance 50% to FMC. Hence, the adjustment should be restricted to 50%, i.e., INR74.2 million.

M/s Vijai Electricals Limited v. Additional CIT (ITA No. 842/Hyd/2012) – Hyderabad Tribunal

Investment in share capital not an international transaction as there is no income element

Vijai Electricals Limited (Vijai Electricals or taxpayer) is engaged in the business of manufacture and sale of distribution and power transformers and rural electrification projects on turnkey basis.

The assessment of return of income filed by Vijai Electricals under section 143(3) of the Act was completed by the AO. CIT was of the opinion that the order of the AO was prejudicial to the interest of the Revenue and accordingly, CIT proceeded to pass order under section 263 of the Act.

CIT held that the investment made by Vijai Electricals amounting to INR211.88 million in its overseas subsidiaries during AY2007–08

was international transaction as per section 92B of the Act. Furthermore, CIT held that Vijai Electricals failed to file Form 3CEB and AO completed the assessment without making a reference to the TPO to test the arm’s length nature of the above-mentioned international transaction.

In view of the above, CIT set aside the assessment made by the AO and directed the AO to do assessment afresh after referring this transaction to the TPO.

Aggrieved by the action of CIT, Vijai Electricals filed an appeal before ITAT.

Vijai Electricals contended that the transaction of investment in share capital of its overseas subsidiaries is not an international transaction under section 92B of the Act and hence, there was no requirement to file Form 3CEB. Moreover, the transaction is merely an investment in capital and not a sale transaction since it does not give rise to any international transaction in relation to which computation of income as contemplated under Chapter X is required. The assesse relied on Circular 14 dated 22 November 2011, Dana Corporation6 and Amiantit International Holding Limited7 to contend that section 92B(1) is applicable only when there is income chargeable to tax and not for capital investment.

ITAT held that the transaction of investment in share capital is not in the nature of transactions referred in section 92B of the Act and transfer pricing provisions are not applicable as there is no income. Accordingly, ITAT set aside the order passed by CIT under section 263 of the Act and restored the order passed by AO.

DCIT v. CLSA India Limited (ITA No. 2362/Mum/2011) – Mumbai Tribunal

ITAT upholds brand royalty payment, confirms benefit test and rejects CUP

CLSA India Limited (CLSA or taxpayer) is a subsidiary of Credit Lyonnais Securities Asia BV (CLSA BV), which in turn is a group company of CLSA Hong Kong. During AY2002–03, CLSA paid royalty to CLSA BV at 1% of net receipts.

The TPO questioned the royalty payment made by CLSA. In this regard, the company submitted that it was using the brand name of CLSA BV since its incorporation, i.e., 21 November 1994. However, it was not able to make royalty payment due to restrictions in erstwhile Foreign Exchange Regulation Act (FERA). After the replacement of FERA by the Foreign Exchange Management Act (FEMA), CLSA started making royalty payments following RBI

6. 321 ITR 178 (AAR) 7. 322 ITR 678 (AAR)

12 India, at Arm’s Length

approval. Furthermore, CLSA submitted that it is not aware of payment of brand royalty by any other broking companies, since the details are not publicly available.

The TPO observed that CLSA was the only AE in the Group to pay royalty. Moreover, RBI approval did not mean that such payment was at arm’s length. Accordingly, the TPO held that since no other associated enterprise paid royalty for use of brand, there existed internal CUP for no payment and since, CLSA could not submit any details of payment of brand fees by any broking entity engaged in similar business in India, there exists external CUP for non payment. In view of the above, the TPO concluded that payment under both internal and external comparable circumstances were nil. Accordingly, ALP of the transaction was considered as nil and an adjustment was proposed.

CLSA appealed before CIT(A) and demonstrated in detail the benefits of using CLSA brand in the course of its business. Furthermore, CLSA argued that the CUP cannot be applied using transactions with related party and lack of transactions cannot be considered as actual transactions/CUP.

Moreover, CLSA submitted that other CLSA group companies were directly making marketing contributions to CLSA BV and therefore, they were not making any royalty payment. CLSA group companies located in different countries had different business models, for example, Korea had commission-sharing arrangement whereas Taiwan operated as a branch. CLSA demonstrated that the average spend on business development activities by comparable companies is 6.4% of brokerage turnover over a period from March 2000 to March 2009 whereas CLSA incurred an expenditure of 1.28% (inclusive of brand fees) of its turnover.

The CLSA submitted that TNMM should be considered as the most appropriate method to determine the ALP of the brand fees. CLSA provided a set of 29 comparable broking entities with an average margin of -5.55% (16.06% after excluding loss making companies) whereas the margin of CLSA was 57.58%.

CIT(A) accepted the contentions of CLSA and held that TNMM is the most appropriate method in the facts of the case of CLSA and the net margin of CLSA being higher than comparable companies, payment of royalty at 1% needs to be considered at arm’s length. Aggrieved by the order of CIT(A), the Revenue appealed before ITAT.

The Department Representative (DR) reiterated the contentions of TPO. Furthermore, the DR placed reliance on the ruling of Knorr Bremse India Private Limited v. ACIT (ITA No 5017/Del/2011) in support of CUP method applied by TPO and submitted that in case an external CUP was considered appropriate, the matter will be restored to the TPO for fresh examination.

CLSA contended that it was not open to the TPO to question the wisdom of the assesse as to how it should conduct the business and decide the reasonableness of a particular expenditure.

ITAT held that international transactions have to be compared with uncontrolled transactions. There can be internal CUP provided the transaction is with an unrelated party. Furthermore, lack of comparable transaction cannot be considered as a transaction. CUP cannot be applied if relevant information is not available. In addition, ITAT denied restoring the matter to the file of the TPO since no comparable transactions were brought on record by the AO or DRP.

Moreover, ITAT noted that the TPO did not examine in detail why other CLSA entities were not paying royalty, which was because of the fact that CLSA group had different arrangement in different jurisdictions.

ITAT held that CLSA’s business development expenditure was lower at 1.28% including 1% royalty as compared to 6.4% in case of comparable companies. Furthermore, applying TNMM method, average margin of comparable companies is -5.5%, and in case loss-making companies are excluded, 16.06% whereas CLSA’s margin is 57.58%. Therefore, no adjustment is warranted.

Kodak India Private Limited v. Additional CIT (ITA No. 7349/ Mum/ 2012) – Mumbai Tribunal

Deeming fiction under section 92B(2) not attracted in absence of foreign entity’s influence over resident

Kodak India Private Limited (Kodak India or taxpayer) is a subsidiary of Eastman Kodak Co., USA (Kodak US). During AY2008–09, Kodak India sold its medical imaging business to Carestream Health India Private Limited (Carestream India) for US$13.543 million. Kodak India did not report this transaction in its Form 3CEB for AY2008–09.

During the transfer pricing audit proceedings for AY2008–09, the TPO observed that the transaction of sale of health imaging business by Kodak India to Carestream India was pursuant to a similar transaction on global basis between Kodak US and Carestream Inc, USA (holding company of Carestream India). The TPO suo moto assumed jurisdiction over the said transaction, proceeded to lift the corporate veil and concluded that there was an international transaction for which ALP needed to be determined. The TPO determined ALP based on the worldwide revenue breakup among countries and concluded that India accounted for 1.4% thereof, which came to US$32.9 million as against US$13.54

13India, at Arm’s Length

million disclosed by Kodak India. Accordingly, the TPO made an adjustment of INR799.7 million.

DRP confirmed the order of the TPO against which Kodak India filed an appeal before ITAT.

The main issue before ITAT was whether the sale of its imaging business by Kodak India to Carestream India, being a transaction between two domestic companies (neither of whom are non-residents), which were not AEs, can be considered as a deemed international transaction under section 92B(2) of the Act. In this regard, ITAT has held as follows:

Based on a reading of sections 92A(1) and 92B(1), ITAT observed that a transaction could become international transaction, only if either or both the AEs are non-resident. Furthermore, ITAT mentioned that we are dealing with Chapter X, which gets its jurisdiction only if there is an international transaction between AEs.

Moreover, ITAT observed that it is an undisputed fact that Kodak India and Kodak US are AEs and Carestream India and Carestream US are AEs. However, it could neither be established that Kodak India has any AE relation with Carestream US nor Carestream India has any AE relation with Kodak US. In addition, the global agreement did not have any role or effect on the transactions of domestic companies and there was no prior agreement and/or terms and condition for sale, dictated by the non-resident agreement. Section 92B(2) of the Act has to be read in consonance with international transactions, since the deeming provision itself refers to section 92B(1).

Based on the above, ITAT held that there was no international transaction involved in the sale of imaging business segment by Kodak India to Carestream India and the same is purely a domestic transaction.

The other issue before ITAT is regarding use of the method by the TPO to arrive at ALP.

In this regard, ITAT held that use of word “shall” in section 92C(1) of the Act casts an embargo that no seventh method could be adopted by the TPO for computing ALP. Taking into account the clear and unambiguous wordings of the provisions of the Act and Rules, ITAT held that the method adopted by the TPO is not appropriate.

Furthermore, ITAT refused to restore the matter back to the file of the TPO holding that the methods prescribed by legislature are mandatory, not directory and when a mandatory provision is superseded or ignored, it straightaway affects the jurisdiction. The TPO, suo moto, imported the provisions of Chapter X and even then did not adhere to the prescribed methods consciously and hence, another opportunity to rectify the mistake cannot be allowed.

M/s Onward Technologies Limited v. DCIT (ITA No. 7985/Mum/2010) – Mumbai Tribunal

Rejects AE as tested party, combination of TNMM and cost plus rejected

Onward Technologies Limited (Onward India or taxpayer) is the parent company of Onward Technologies Inc., USA (Onward USA) and Onward Technologies GmbH, Germany (Onward Germany). Onward group is a global provider of engineering software development services and solutions to end users. During AY2006–07, Onward India had various international transactions classified under three segments, i.e., IT-enabled services segment, distribution segment and other transactions including reimbursements.

Onward India identified TNMM as the most appropriate method for benchmarking its international transactions pertaining to IT-enabled services segment. Onward India considered Onward US as tested party and identified six comparable companies operating in the US market and rendering similar services as rendered by Onward US to Onward India.

The TPO accepted the international transactions pertaining to distribution segment and other transactions including reimbursements at arm’s length. However, the TPO did not accept the approach and arm’s length price determined by Onward India in relation to international transactions pertaining to IT-enabled services segment.

The TPO identified 20 Indian companies as comparable to Onward India engaged in rendering IT-enabled services. The average operating profit on total cost of comparable companies was worked at 20.68% by the TPO whereas the operating profit margin of Onward India was 14.05%. Accordingly, TPO proposed an adjustment of INR14.6 million to the international transactions of Onward India.

The transfer pricing addition made by the TPO was confirmed by DRP. Aggrieved by the directions of DRP, Onward India filed an appeal before ITAT. ITAT ruled as follows:

• Ruling of ITAT on the ALP determined by Onward India

Foreign AE as tested party:

ITAT held that comparing profit earned by foreign AE with outside comparable companies entails selecting foreign AE as tested party, which needs to be examined in the context of Indian TP regulations.

14 India, at Arm’s Length

ITAT held that the modus operandi of determining ALP under TNMM is that firstly the profit rate earned by assessee from a transaction with its AE is determined (A), which is then compared with the rate of profit in comparable cases (B) for ascertaining whether A is at arm’s length. Accordingly, B may undergo change with change in comparable cases; however, there is no dispute regarding A since the same has to necessarily result only from the transactions between two or more AEs.

Hence, profit realized by Indian assessee from the transaction with its foreign AE is compared with comparable cases. In any case, the same cannot be substituted with the profit realized by foreign AE from ultimate customers to determine ALP. This makes the substantive section 92 otiose and definition of international transaction under 92B and Rule 10B redundant. Hence, use of foreign AE as tested party is not acceptable under the Indian transfer pricing law.

Furthermore, Onward India contended that the tax authorities cannot go beyond the overall profit of Onward group.

In this regard, ITAT held that based on a reading of section 92 with section 92C, it is crystal clear that ALP is to be determined by any one of the prescribed methods, which is most appropriate in the facts of the case. Accordingly, it is only the choice of method, which is left to the assessee or the tax authorities. It is neither open to the TPO nor the assessee to discard the prescribed methods and invent a new method or apply any other yardstick for determining ALP. Thus, the contention of assessee was rejected.

Case specific submissions:

The subsidiaries of Onward India, i.e., Onward USA and Onward Germany primarily carried out sales and marketing activity along with site support services for clients. The subsidiaries were remunerated at cost plus 5% mark-up. The six comparable companies identified by Onward India were engaged in marketing functions in the US and had arithmetic mean of cost plus at 4.07%.

ITAT noted that Onward India benchmarked its transactions using TNMM as the most appropriate method. However, whether 4.07% was mark-up on costs or profit percentage on some base was not properly emerging. Accordingly, it seemed that Onward India mixed up two methods, i.e., CPM and TNMM. Section 92C provides for use of “any” method but not a combination of methods.

Further, ITAT observed that the international transaction under consideration is receipt of amount from AEs towards software and technical services rendered and not that of paying 5% mark-up on costs incurred by AEs. By comparing the mark-up on costs incurred by AEs, the assessee has changed the complexion of the transaction.

In view of the above, ITAT entirely rejected the methodology adopted by Onward India for computation of ALP in relation to international transactions pertaining to IT-enabled services segment.

• Ruling of ITAT on the ALP determined by Revenue authorities

ITAT noted that while computing operating profit to total cost of Onward India as 14.05%, the TPO considered entity level figures, i.e., including distribution segment and other transactions. However, since the distribution segment and other transactions were concluded to be at arm’s length, the TPO should have considered figures only in relation to IT-enabled services segment.

Comparable companies identified by the TPO:

In relation to the 20 comparable companies selected by the TPO, ITAT held that they are prima facie engaged in different functions as compared to Onward India. In addition, without getting into the details of all 20 companies, ITAT set aside the order of the AO/TPO and restored the matter back to the file of the AO/TPO to determine the ALP of IT-enabled services segment afresh by primarily considering the correct figures of operating profit to total cost in respect of IT-enabled services segment of Onward India and considering only comparable companies out of the twenty companies selected by the TPO. ITAT concluded the same based on an analysis of two comparable companies on sample basis.

Furthermore, ITAT rejected Onward India’s contention that the method adopted by Onward India for determination of ALP should be accepted for the current year since the same was accepted by the TPO in earlier years. In this regard, ITAT noted that a balance needs to be maintained between principle of consistency and the rule of res judicata. ITAT, relying on judicial precedents of higher authorities, held that where the facts of the case clearly show that the authorities took a clearly incorrect view, it cannot be argued in the subsequent year that the same incorrect approach be repeated and that the Revenue authorities cannot be stopped from taking a correct view of statutory provision in later year.

Vodafone India Services Private Limtied v. DCIT (ITA No. 7140/Mum/2012 and 7097/Mum/2012) – Mumbai Tribunal

ITAT rejects high/low-end services distinction for ITeS comparable companies

Vodafone India Services Private Limited (Vodafone India or taxpayer) is a subsidiary of Hutchison Call Centre Holding Limited. During AY2007–08, it was engaged in rendering voice-based call center services. Vodafone India used TNMM for benchmarking its

15India, at Arm’s Length15

international transaction pertaining to rendering of voice based call center services to its holding company and identified 9 comparable companies and considered PBIT/ operating cost as PLI. Average PBIT/ operating cost of comparable companies worked out to 6.10% as against 7% mark-up charged by Vodafone India to its AE. Accordingly, Vodafone India concluded that its international transaction was at arm’s length from an Indian transfer pricing perspective.

The TPO conducted a fresh search and identified 25 comparable companies rendering IT-enabled services including two companies already identified by Vodafone India as comparable. Furthermore, Vodafone India accepted the fact that Spanco Limited is comparable. In respect of balance 22 companies, Vodafone India submitted that these companies were not functionally comparable to Vodafone India. Moreover, Vodafone India requested the TPO to grant working capital adjustment. However, the TPO rejected Vodafone India’s contentions. In addition, the TPO rejected Optimus Global Services Limited identified by Vodafone India, since it had persistent operating losses. Finally, the TPO selected 31 comparable companies, eight from Vodafone India’s search and 23 from his own search, and computed arithmetic mean of the margins of comparable companies at 25.25%. Aggrieved by the order of TPO/AO, Vodafone India filed appeal before CIT(A).

CIT(A) agreed that following six companies identified by TPO were functionally different and should be excluded from the set of comparable companies:

1. Bodhtree Consulting Limited

2. ICRA Techno Analytics Limited

3. Infosys BPO Limited

4. Wipro Limited

5. Triton Corp. Limited

6. Maple (E) Solutions Limited

Furthermore, CIT(A) directed the TPO to look into the margin computation provided by assesse and rectify the same, if required. Apart from the above, CIT(A) rejected all other grounds of appeal of Vodafone India. Aggrieved by the order of CIT(A), Vodafone India and Revenue filed appeal before ITAT.

ITAT held that all companies in IT-enabled services space provide similar services and the difference is only in the way they work internally, which is reflected through difference in qualification and skill of employees. Accordingly, what needs to be examined is whether difference in skill/qualification of employees or their payment structure significantly affects comparability since TNMM is tolerant to minor differences.

Reliance was placed on the ruling of Actis Advisors (P) Ltd8 wherein it was held that any further dissection of IT-enabled services will not be proper as it would be a very subjective exercise. Accordingly, ITAT rejected the contention of Vodafone India since no material was 8. ITA 122/Delhi/2011

brought on record to substantiate that there is high margin in case of high-end services.

Comparables Analysis:

ITAT excluded certain companies based on the following principles:

• ‐ Engaged into activities other than IT-enabled services and segmental results not available (other non-comparable activities are significant)

• ‐ Significant related party transactions

• ‐ Persistent losses for last three years

ITAT accepted certain companies based on the following principles:

• ‐ Functionally comparable and there is no such fact that companies engaged in providing high-end services earn high margins

• ‐ Cannot reject a company, merely because it has super profit margins

• ‐ Results of the BPO segment to be considered for the purpose of comparability

• ‐ Functionally comparable and fact that companies have good brand value, high expenditure on marketing and selling and high turnover as compared to Vodafone India cannot be the basis to reject these companies

• ‐ Functionally comparable and no details regarding merger/amalgamation impacting comparability were placed on record

ITAT remanded back certain companies to TPO/AO directing to verify actual activities of the company from their annual accounts and consider as comparable if engaged in rendering IT-enabled services.

ITAT rejected Vodafone India’s contention that since its income was exempt under section 10A of the Act, there was no intention to avoid tax. ITAT held that once there is an international transaction, ALP has to be computed according to the methods prescribed under the law irrespective of whether the entity is claiming tax holiday.

Furthermore, ITAT rejected the contention of Vodafone India that the margins should be computed as a percentage of assets employed. It was noted that such computation is suitable for manufacturing or other capital/asset-intensive industries and not in case of Vodafone India, which is a service provider.

ITAT accepted Vodafone India’s claim for working capital adjustment and restored the same to the file of TPO/AO for computing and granting working capital adjustment to Vodafone India according to OECD guidelines. Furthermore, ITAT held that since ALP exceeds the transfer price by more than 5%, the benefit of ± 5% cannot be allowed to Vodafone India.

16 India, at Arm’s Length

South Africa

Draft interpretation note on arm’s length basis applied to thin capitalization rules

The South African Revenue Service (SARS) released its draft interpretation note on thin capitalization rules9. The draft interpretation note, which was open for public comments up to 30 June 2013 throws light on:

• The application of the arm’s length basis in the context of determining whether a taxpayer is thinly capitalized and,

• If so, calculating taxable income without claiming a deduction for the expenditure incurred on the excessive portion of finance.

Thin capitalization is an issue in cases where a South African taxpayer is funded either directly or indirectly by non-resident connected persons. The funding of a South African taxpayer with excessive intra-group, back-to-back or intra-group-guaranteed debt will result in excessive interest deductions from taxpayer’s income, thereby depleting the South African tax base.

Determination of taxpayers with high risk

SARS adopts a risk-based audit approach in selecting potential thin capitalization cases for audit. In selecting cases, SARS considers taxpayer to be at increased risk where:

• The Debt: EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) ratio of the South African taxpayer exceeds 3:1.

• The interest rate exceeds the weighted average of the base rate of the country of denomination plus 2%.

However, the ratio is, not a safe harbor and does not preclude SARS from auditing a taxpayer who is within the range of the abovementioned ratio.

Implications

• Taxpayers are required to calculate the allowable portion of deductible interest for the purposes of taxable income based on the arm’s length principle thereby disallowing the excessive portion of interest and other charges.

9. A company is said to be thinly capitalized when its capital is made up of a much greater proportion of debt than equity

• Furthermore, this disallowance gives rise to a secondary adjustment in the form of a deemed outbound loan on which an arm’s length interest amount is imputed.

Documentation requirements

The interpretation note also indicates the level of documentation required to support the level of arm’s length debt, which include a description of the funding structure, a description of the principal business activities, copies of relevant funding agreements, analysis of the financial strategy of the business, group structure covering all relevant companies, summary of financial forecasts. Analysis supporting the borrower’s view of the extent to which the connected party (or supported) debt is considered to be arm’s length etc.

SARS also introduced an enhanced Income Tax Return for Companies (ITR14) wherein taxpayers have to provide certain information that are mentioned as risks harbors in the draft interpretation note on thin capitalization namely, value of certain transactions and financial ratios.

Although tax adjustments on account of thin capitalization have not found their way into India yet, companies may consider making a comparison between the interest payable on the actual debt and that which would be payable on the amount, which would have been borrowed at arm’s length and determine the right capital-structure mix.

OECD

Revision of section on “safe harbours” in TP guidelines

On 16 May 2013, the OECD Council approved the revision of Section E on safe harbours10 in Chapter IV of the Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations.

The previous guidance in Chapter IV had a somewhat negative tone toward transfer pricing safe harbours and their use was not recommended.

10. A safe harbour in a transfer pricing regime is a provision that applies to a defined category of taxpayers or transactions and that relieves eligible taxpayers from certain obligations otherwise imposed by a country’s general transfer pricing rules.

Around the world

17India, at Arm’s Length

Impact of revised guidance

• Although safe harbours primarily benefit taxpayers, by providing for a more optimal use of resources, they can benefit tax administrations as well by shifting audit and examination resources from smaller taxpayers and less complex transactions to more complex, high-risk cases.

• Opportunities for countries to relieve some compliance burdens and to provide increased certainty for cases involving small taxpayers or less complex transactions.

• It encourages, under the right circumstances, the use of bilateral or multilateral safe harbours as they may provide a significant relief from compliance burdens without creating problems of double taxation or double non-taxation.

The revised guidance lists primary benefits of safe harbours, which include:

• Compliance relief

• Certainty

• Administrative simplicity and the specific concerns related to safe harbours

• Divergence from the arm’s length principle

• Risk of double taxation, double non-taxation, and mutual agreement concerns

• Possibility of opening avenues for tax planning

• Equity and uniformity issues

The new Annex 1 to Chapter IV of the Transfer Pricing Guidelines also contains three sample memoranda of understanding, which country competent authorities might use to establish bi- or multilateral safe harbours for common classes of transfer pricing cases.

With the growing need of safe harbours within the gambit in transfer pricing, India may see a future of reduced burden on the taxpayer particularly on the tax litigation front. The Rangachary Committee was also set up to review taxation of development centers and the IT sector in India to curtail increased TP disputes faced by such industries. The report recently released by the committee provides guidance on the use of transfer pricing methods, characterization of an entity and other transfer pricing issues.

Poland

Polish tax authorities’ proposition to implement regulations concerning business restructurings

The Poland’s Ministry of Finance published draft amendments to the TP Decree11 to cover business restructurings. New provisions seek to implement the OECD Guidelines on business restructuring at a local level.

Restructuring will be defined as any transfer (including cross-border) of important functions, assets and risks between related parties. The tax authorities will require to focus on substance, rationality and exit payment during a tax control.

The risk of tax/transfer pricing control cannot be eliminated. The more substantial the business change, the greater is the risk.

In 2012, India has also seen stringent regulations in place with the widening of the definition of “international transaction” to ensure tax control on overseas expansions and outbound acquisitions.

With the implementation of OECD guidelines on business restructuring to various countries locally, the companies should proactively carry out a detailed analysis so as to demonstrate that restructuring activities were carried out in accordance with the arm’s length principle, that is, whether they would have been accepted by independent entities.

United Nations

United Nations launches Practical Manual on Transfer Pricing for Developing Countries

The United Nations Committee of Experts on International Cooperation in Tax Matters (the Committee) successfully adopted a Practical Manual on Transfer Pricing for Developing Countries designed to be in accordance with the “arm’s length principle,” an approximation of the market-based pricing provided for both the UN Model and the OECD Model Conventions.

It was launched in an e-version during a special meeting of United Nations Economic and Social Council (ECOSOC) on “International cooperation in tax matters” in New York on 29 May 2013. The Manual will be issued in print shortly.

11. Decree dated 10 September 2009 on the methods and procedures for determining taxable income in case of a transfer pricing adjustment

18 India, at Arm’s Length

The Manual has left it up to each country to choose a tax policy most appropriate for its stage of economic development. The manual contents are briefly described below.

Chapter 1 Introduces the Manual as a whole and represents a broad survey of TP issues for developing countries

Chapter 2 Describes the factors that gave rise to MNEs and shows how an MNE is able to exploit integration opportunities in the cross-border production of goods and provision of services through a “value chain”

Chapter 3 Structural overview of domestic TP legislation and describes key concepts

Chapter 4 Addresses the need for TP capabilities in developing countries

Chapter 5 Deals with comparability analysis under the “arm’s length principle” and addresses the main hurdles faced by developing countries, in finding appropriate comparables

Chapter 6 Review of TP methods used to determine an “arm’s length price” and application of methods in practice

Chapter 7 Importance of documentation

Chapter 8 Surveys audit issues related to TP and need for risk assessment

Chapter 9 Examines processes and procedures of dispute avoidance and resolution and advises on effective ways to prevent disputes

Chapter 10 Compilation of four papers on country practices from China, India, Brazil, and South Africa

The Indian tax administration in the India country-specific chapter has provided its comments on a number of emerging transfer pricing issues from an Indian perspective. With respect to the issues relating to India, the manual seeks to inform the readers on experience in dealing with TP issues relating to filing requirements, contemporaneous comparables, functions, assets and risk analysis and arm’s length range to name a few.

Because of its focus on practicality, the launch of the manual is much welcomed by many developing countries trying to implement or apply transfer pricing rules. The manual is anticipated to be updated on a “rolling” basis.

OECD

OECD provides an update on base erosion and profit shifting project

At the annual OECD tax conference in Washington, DC held in June 2013, developments with respect to OECD’s project on base erosion and profit shifting (BEPS) dominated the discussion. The OECD issued an initial report, Addressing Base Erosion and Profit Shifting, in February this year on issues relating to BEPS and multinational businesses. The OECD has organized the BEPS project around three work clusters — Countering Base Erosion, Jurisdiction to Tax, and Transfer Pricing.

In the discussions on the ongoing OECD work on TP for intangibles, it was noted that plans for TP work in the BEPS project are still under development. It was further noted that there will be a substantial TP component in the action plan to be released in July.

19India, at Arm’s Length

The update provides guidance to companies to evaluate the implications for their business models of the areas that are being targeted for potential change.

Italy

Italy’s Supreme Court issues TP decision on royalties paid to US parent

Facts of the case

The Italian company was a distributor of the software produced by the US entity, resident in Delaware.

Under a software license contract in place between the two entities, the Italian company had paid royalties to its US parent equal to 30% of its proceeds.

The Italian inspectors claimed the amount paid was too high as it was not in line with the arm’s length principle. The authorities recomputed the fair market value of the royalties as 7% of the proceeds basing their position on certain guidelines12.

The Italian company brought proceedings against the tax assessment in front of the Provincial Tax Court of Milan and won.

The Italian tax authorities appealed the first level of judgment before the Regional Tax Court of Lombardy. This court reversed the judgment of the provisional tax court and validated the action of the tax inspectors that disallowed the deduction of a substantial portion of the royalties paid by the Italian subsidiary to the US parent company. The Italian company finally appealed before the Italian Supreme Court.

12. The guideline of the Ministry of Economy and Finance contained in the Circular Letter no. 32 issued on 22 September 1980 - The circular identified some safe-harbors one of which included transactions performed between companies operating in industries characterized by a high level of technology for which the remuneration could increase to 7 % of the annual turnover

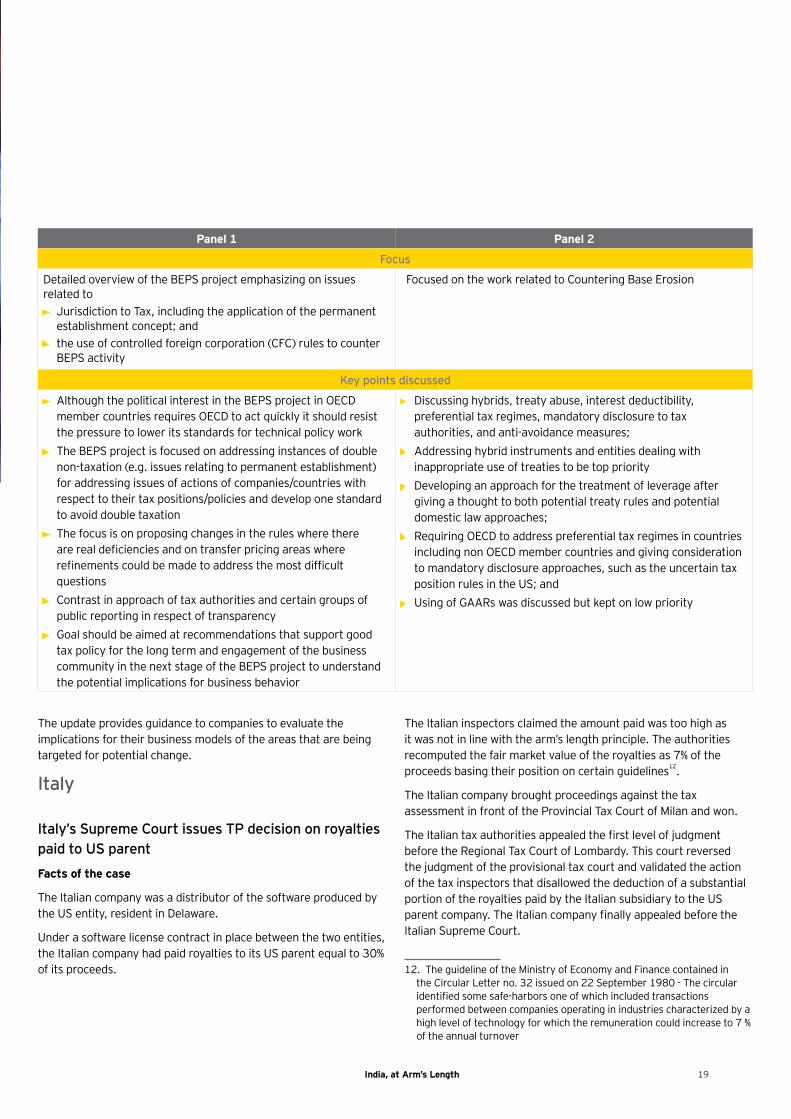

Panel 1 Panel 2

Focus

Detailed overview of the BEPS project emphasizing on issues related to • Jurisdiction to Tax, including the application of the permanent

establishment concept; and• the use of controlled foreign corporation (CFC) rules to counter

BEPS activity

Focused on the work related to Countering Base Erosion

Key points discussed

• Although the political interest in the BEPS project in OECD member countries requires OECD to act quickly it should resist the pressure to lower its standards for technical policy work

• The BEPS project is focused on addressing instances of double non-taxation (e.g. issues relating to permanent establishment) for addressing issues of actions of companies/countries with respect to their tax positions/policies and develop one standard to avoid double taxation

• The focus is on proposing changes in the rules where there are real deficiencies and on transfer pricing areas where refinements could be made to address the most difficult questions

• Contrast in approach of tax authorities and certain groups of public reporting in respect of transparency

• Goal should be aimed at recommendations that support good tax policy for the long term and engagement of the business community in the next stage of the BEPS project to understand the potential implications for business behavior

• Discussing hybrids, treaty abuse, interest deductibility, preferential tax regimes, mandatory disclosure to tax authorities, and anti-avoidance measures;

• Addressing hybrid instruments and entities dealing with inappropriate use of treaties to be top priority

• Developing an approach for the treatment of leverage after giving a thought to both potential treaty rules and potential domestic law approaches;

• Requiring OECD to address preferential tax regimes in countries including non OECD member countries and giving consideration to mandatory disclosure approaches, such as the uncertain tax position rules in the US; and

• Using of GAARs was discussed but kept on low priority

20 India, at Arm’s Length

The Supreme Court decision

The Supreme Court upheld the position of the tax inspectors who denied the application of a 30% royalty paid by an Italian company to its US parent and instead recognized only a 7% royalty.

Finding of the Supreme Court