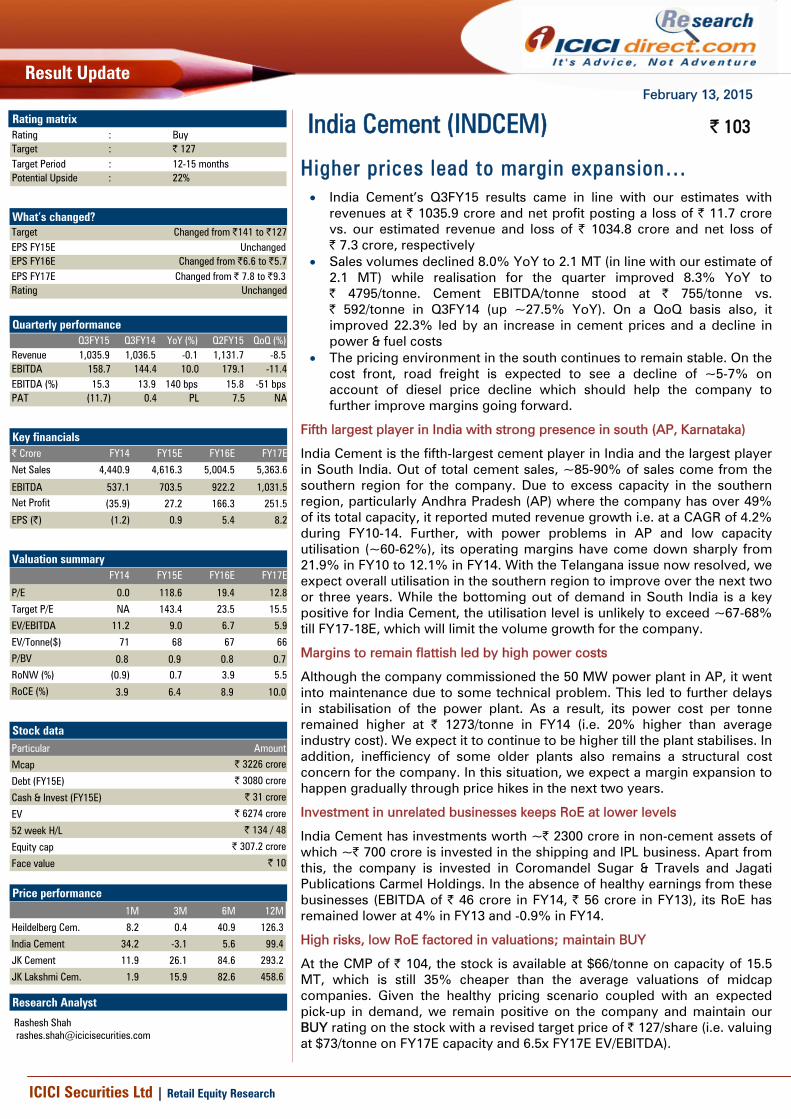

February 13, 2015 ICICI Securities Ltd | Retail Equity Research Result Update Higher prices lead to margin expansion… • India Cement’s Q3FY15 results came in line with our estimates with revenues at | 1035.9 crore and net profit posting a loss of | 11.7 crore vs. our estimated revenue and loss of | 1034.8 crore and net loss of | 7.3 crore, respectively • Sales volumes declined 8.0% YoY to 2.1 MT (in line with our estimate of 2.1 MT) while realisation for the quarter improved 8.3% YoY to | 4795/tonne. Cement EBITDA/tonne stood at | 755/tonne vs. | 592/tonne in Q3FY14 (up ~27.5% YoY). On a QoQ basis also, it improved 22.3% led by an increase in cement prices and a decline in power & fuel costs • The pricing environment in the south continues to remain stable. On the cost front, road freight is expected to see a decline of ~5-7% on account of diesel price decline which should help the company to further improve margins going forward. Fifth largest player in India with strong presence in south (AP, Karnataka) India Cement is the fifth-largest cement player in India and the largest player in South India. Out of total cement sales, ~85-90% of sales come from the southern region for the company. Due to excess capacity in the southern region, particularly Andhra Pradesh (AP) where the company has over 49% of its total capacity, it reported muted revenue growth i.e. at a CAGR of 4.2% during FY10-14. Further, with power problems in AP and low capacity utilisation (~60-62%), its operating margins have come down sharply from 21.9% in FY10 to 12.1% in FY14. With the Telangana issue now resolved, we expect overall utilisation in the southern region to improve over the next two or three years. While the bottoming out of demand in South India is a key positive for India Cement, the utilisation level is unlikely to exceed ~67-68% till FY17-18E, which will limit the volume growth for the company. Margins to remain flattish led by high power costs Although the company commissioned the 50 MW power plant in AP, it went into maintenance due to some technical problem. This led to further delays in stabilisation of the power plant. As a result, its power cost per tonne remained higher at | 1273/tonne in FY14 (i.e. 20% higher than average industry cost). We expect it to continue to be higher till the plant stabilises. In addition, inefficiency of some older plants also remains a structural cost concern for the company. In this situation, we expect a margin expansion to happen gradually through price hikes in the next two years. Investment in unrelated businesses keeps RoE at lower levels India Cement has investments worth ~| 2300 crore in non-cement assets of which ~| 700 crore is invested in the shipping and IPL business. Apart from this, the company is invested in Coromandel Sugar & Travels and Jagati Publications Carmel Holdings. In the absence of healthy earnings from these businesses (EBITDA of | 46 crore in FY14, | 56 crore in FY13), its RoE has remained lower at 4% in FY13 and -0.9% in FY14. High risks, low RoE factored in valuations; maintain BUY At the CMP of | 104, the stock is available at $66/tonne on capacity of 15.5 MT, which is still 35% cheaper than the average valuations of midcap companies. Given the healthy pricing scenario coupled with an expected pick-up in demand, we remain positive on the company and maintain our BUY rating on the stock with a revised target price of | 127/share (i.e. valuing at $73/tonne on FY17E capacity and 6.5x FY17E EV/EBITDA). India Cement (INDCEM) | 103 Rating matrix Rating : Buy Target : | 127 Target Period : 12-15 months Potential Upside : 22% What’s changed? Target Changed from |141 to |127 EPS FY15E Unchanged EPS FY16E Changed from |6.6 to |5.7 EPS FY17E Changed from | 7.8 to |9.3 Rating Unchanged Quarterly performance Q3FY15 Q3FY14 YoY (%) Q2FY15 QoQ (%) Revenue 1,035.9 1,036.5 -0.1 1,131.7 -8.5 EBITDA 158.7 144.4 10.0 179.1 -11.4 EBITDA (%) 15.3 13.9 140 bps 15.8 -51 bps PAT (11.7) 0.4 PL 7.5 NA Key financials | Crore FY14 FY15E FY16E FY17E Net Sales 4,440.9 4,616.3 5,004.5 5,363.6 EBITDA 537.1 703.5 922.2 1,031.5 Net Profit (35.9) 27.2 166.3 251.5 EPS (|) (1.2) 0.9 5.4 8.2 Valuation summary FY14 FY15E FY16E FY17E P/E 0.0 118.6 19.4 12.8 Target P/E NA 143.4 23.5 15.5 EV/EBITDA 11.2 9.0 6.7 5.9 EV/Tonne($) 71 68 67 66 P/BV 0.8 0.9 0.8 0.7 RoNW (%) (0.9) 0.7 3.9 5.5 RoCE (%) 3.9 6.4 8.9 10.0 Stock data Amount Mcap | 3226 crore Debt (FY15E) | 3080 crore Cash & Invest (FY15E) | 31 crore EV | 6274 crore 52 week H/L | 134 / 48 Equity cap | 307.2 crore Face value | 10 Particular Price performance 1M 3M 6M 12M Heildelberg Cem. 8.2 0.4 40.9 126.3 India Cement 34.2 -3.1 5.6 99.4 JK Cement 11.9 26.1 84.6 293.2 JK Lakshmi Cem. 1.9 15.9 82.6 458.6 Research Analyst Rashesh Shah [email protected]

Transcript

February 13, 2015

ICICI Securities Ltd | Retail Equity Research

Result Update

Higher prices lead to margin expansion… • India Cement’s Q3FY15 results came in line with our estimates with

revenues at | 1035.9 crore and net profit posting a loss of | 11.7 crore vs. our estimated revenue and loss of | 1034.8 crore and net loss of | 7.3 crore, respectively

• Sales volumes declined 8.0% YoY to 2.1 MT (in line with our estimate of 2.1 MT) while realisation for the quarter improved 8.3% YoY to | 4795/tonne. Cement EBITDA/tonne stood at | 755/tonne vs. | 592/tonne in Q3FY14 (up ~27.5% YoY). On a QoQ basis also, it improved 22.3% led by an increase in cement prices and a decline in power & fuel costs

• The pricing environment in the south continues to remain stable. On the cost front, road freight is expected to see a decline of ~5-7% on account of diesel price decline which should help the company to further improve margins going forward.

Fifth largest player in India with strong presence in south (AP, Karnataka)

India Cement is the fifth-largest cement player in India and the largest player in South India. Out of total cement sales, ~85-90% of sales come from the southern region for the company. Due to excess capacity in the southern region, particularly Andhra Pradesh (AP) where the company has over 49% of its total capacity, it reported muted revenue growth i.e. at a CAGR of 4.2% during FY10-14. Further, with power problems in AP and low capacity utilisation (~60-62%), its operating margins have come down sharply from 21.9% in FY10 to 12.1% in FY14. With the Telangana issue now resolved, we expect overall utilisation in the southern region to improve over the next two or three years. While the bottoming out of demand in South India is a key positive for India Cement, the utilisation level is unlikely to exceed ~67-68% till FY17-18E, which will limit the volume growth for the company.

Margins to remain flattish led by high power costs

Although the company commissioned the 50 MW power plant in AP, it went into maintenance due to some technical problem. This led to further delays in stabilisation of the power plant. As a result, its power cost per tonne remained higher at | 1273/tonne in FY14 (i.e. 20% higher than average industry cost). We expect it to continue to be higher till the plant stabilises. In addition, inefficiency of some older plants also remains a structural cost concern for the company. In this situation, we expect a margin expansion to happen gradually through price hikes in the next two years.

Investment in unrelated businesses keeps RoE at lower levels

India Cement has investments worth ~| 2300 crore in non-cement assets of which ~| 700 crore is invested in the shipping and IPL business. Apart from this, the company is invested in Coromandel Sugar & Travels and Jagati Publications Carmel Holdings. In the absence of healthy earnings from these businesses (EBITDA of | 46 crore in FY14, | 56 crore in FY13), its RoE has remained lower at 4% in FY13 and -0.9% in FY14.

High risks, low RoE factored in valuations; maintain BUY

At the CMP of | 104, the stock is available at $66/tonne on capacity of 15.5 MT, which is still 35% cheaper than the average valuations of midcap companies. Given the healthy pricing scenario coupled with an expected pick-up in demand, we remain positive on the company and maintain our BUY rating on the stock with a revised target price of | 127/share (i.e. valuing at $73/tonne on FY17E capacity and 6.5x FY17E EV/EBITDA).

What’s changed? Target Changed from |141 to |127EPS FY15E UnchangedEPS FY16E Changed from |6.6 to |5.7EPS FY17E Changed from | 7.8 to |9.3Rating Unchanged

Total Operating Income 1035.9 1103.6 1036.5 -0.1 1,131.7 -8.5Cement volumes declined 3.7% YoY to 2.35 MT while realisation improved sharply by 13.1% YoY to | 4655/tonne

Other Income 4.7 3.5 1.9 143.0 4.2 12.5Raw Material Expenses 145.2 155.0 137.7 5.5 173.6 -16.4Employee Expenses 78.3 75.4 83.1 -5.7 76.8 2.0Stock Adjustment 15.1 0.0 1.3 NA -15.9 -195.1

Power & Fuel 262.0 285.8 296.1 -11.5 296.3 -11.6Low cement volumes coupled with a fall in international coal prices led to a decline in total power cost.On a per tonne basis, it remained flat at | 1261/tonne

EBITDA Margin (%) 15.3 17.7 13.9 140 bps 15.8 -51 bpsLower operating cost led to 408 bps expansion in margins. However, the same remained lower than our estimates due to higher freight costs during the quarter

Key MetricsVolume (MT) 2.35 2.36 2.44 -3.7 2.56 -8.1 Sales volume declined on account of poor demand in APRealisation (|) 4,655 4,394 4,116 13.1 4,244 9.7Cement EBITDA per Tonne (|) 618 538 408 51.3 448 37.9

Better realisation and lower power cost helped to improve EBITDA/tonne for the quarter on a QoQ basis

Source: Company, ICICIdirect.com Research Change in estimates

(| Crore) Old New % Change Old New % Change Old New % Change Comments

Revenue 4,895.3 4,644.6 -5.1 5,331.8 5,040.1 -5.5 NA 5,415.4 NA

We expect FY15 to be a challenging year in terms of volume growth amid excess capacity in the southern region. However, strong pricing environment would be a key driver for revenue growth

EBITDA 746.4 751.2 0.6 916.2 934.8 2.0 NA 1,083.3 NA

EBITDA Margin (%) 15.2 16.2 93 bps 17.2 18.5 136 bps NA 20.0 NA

Margins are expected to recover from FY16E led by improvement pricing environemnt and stabilisation of new power plant

PAT 47.4 74.9 58.0 184.4 174.7 -5.3 NA 286.7 NAEPS (|) 1.5 2.4 58.0 6.0 5.7 -5.3 NA 9.3 NA

FY15E FY16E FY17E

Source: Company, ICICIdirect.com Research Assumptions

Volume (MT) 10.1 10.0 9.5 10.0 10.4 10.4 10.7 NAWe remain conservative on the volume growth front with visible recovery from FY16E onwards

Cement Realisation (|) 4,362 4,183 4,626 4,735 4,958 4,278 4,490.0 NAHowever, we expect pricing environment to remain strong due to improvement in demand

Cement EBITDA per Tonne (|) 783 289 556 670 773 323 518.0 NAExpect lower EBITDA/tonne than industry due to high exposure in AP

EarlierCurrent

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis Largest manufacturer of cement in South India

India Cement is the largest cement manufacturer in the southern region with an installed capacity of 13.1 MTPA in the southern region. While 1.1 MTPA of capacity is in Maharashtra, 1.5 MTPA of capacity is in Banswara, Rajasthan. Out of total revenue, ~85-90% of sales come from the southern region for the company. Due to excess capacity in the southern region, the company is vulnerable to the demand supply mismatch of the southern region. Going ahead, after the resolution of Telangana issue in the region, we expect demand to improve from here on. However, given the additional capacity, the utilisation level is unlikely to exceed ~67-68% till FY17-18E, which will limit the volume growth for the company.

Exhibit 1: Demand supply dynamics of South India Million tonnes FY09 FY10 FY11 FY12 FY13 FY14P FY15E

Operationally inefficient; captive power plants to help, going forward

The company is one of the least efficient players in the industry. The EBITDA margin at the end of FY14 was at 7% only against industry average of 17%. The company currently has 50 MW of power capacity at Sankarnagar to cater to the energy needs of cement plants in Tamil Nadu. Another captive power plant of 50 MW at Vishnupuram in Andhra Pradesh has been installed and is in the process of stabilisation. The plant will cater to the requirement of cement plants in Andhra Pradesh.

Exhibit 2: EBITDA margin compared to industry

33 34

25 23

12

2118

7

31 29 2825

1822

1917

05

10152025303540

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

(%)

India Cement Industry

Source: Company, ICICIdirect.com Research

Exhibit 3: EBITDA/tonne compared to industry

111 156

93

754

412

887

783

289

895

889 942

901

689

956

848

727

0

200

400

600

800

1,000

1,200

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

(|)

India Cement Industry

Source: Company, ICICIdirect.com Research

Huge investments in unrelated non-cement business remain key concern

The company has invested a large sum of money in non-core businesses and other group companies/associates. As of FY14, the company has total loans and advances of | 2552 crore and other investments of | 943 crore, which contributes only ~9% in total EBITDA of the company for FY14. Loans and advances include advances to other body corporate like ICL Financial Services, ICL Securities, Trishul Concrete (RMC business), etc, which have led to low RoEs. The company has several times iterated its intentions of restructuring its non-core businesses. However, till that time, this remains an overhang for the company.

Capacity spread

Tamilnadu38%

Andhra Pradesh

45%

Maharastra7%

Rajasthan10%

ICICI Securities Ltd | Retail Equity Research Page 4

Expect revenue CAGR of 6.5% during FY14-17E

The company’s revenue has grown at a CAGR of 4.2% during FY10-14 while in FY12-14, the growth was lower at 2.8% led by a slowdown in AP coupled with higher cement capacity. Going forward, with the resolution of the Telangana issue and a strong focus towards infrastructure development by the government, we expect revenue CAGR of 6.5% in FY14-17E. We expect volume growth at a CAGR of 1.1% during our forecast period of FY14-17E while realisations are expected to grow at 5.5% on account of an improvement in capacity utilisations.

Exhibit 4: Expect revenue CAGR of 6.5% during FY14-17E

3771 35014203

4597 4441 46165005

5364

0

1000

2000

3000

4000

5000

6000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Net Sales (| crore)

Source: Company, ICICIdirect.com Research

Exhibit 5: Capacity addition plans State Region MT

Sankarnagar, Tirunelveli Tamilnadu South 2.1

Sankari, Salem Tamilnadu South 0.9Dalavoi, Ariyalur Tamilnadu South 1.9

Vallur Village, Tiruvallur Tamilnadu South 1.1Chilamakur, Kadapa Andhra Pradesh South 1.5

Yerraguntla, Kadapa Andhra Pradesh South 0.7

Vishnupuram, Nalgonda Andhra Pradesh South 2.5

Malkapur, Ranga Reddy Andhra Pradesh South 2.4Parli Vaijnath, Beed Maharashtra West 1.1

banswara Rajasthan North 1.5Total 15.7

Source: Company, ICICIdirect.com Research

Exhibit 6: Volume to grow at CAGR of 1.1% during FY14-17E

10.969.97 9.53 10.05 10.02 10.45 11.01 11.51

0.00

3.00

6.00

9.00

12.00

15.00

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Sales Volumes (In mn)

Source: Company, ICICIdirect.com Research

Exhibit 7: Realisation to grow at CAGR of 5.5% during FY14-17E

3266 33754215 4362 4183 4613 4723 4908

0

2000

4000

6000

FY10

FY11

FY12

FY13

FY14

FY15

E

FY16

E

FY17

E

(|/to

nne)

-10

0

10

20

30

(%)

Cement Realisation (|/tonne) -LS Growth (%) -RS

Source: Company, ICICIdirect.com Research

Exhibit 8: Volumes decline 8.0% YoY Q3FY15 due to lower demand…

2.31 2.43

2.19 2.

60

2.38 2.48

2.42 2.

78

2.65

2.44

2.29 2.

64

2.56

2.35

2.11

0.00

0.501.00

1.50

2.002.50

3.00

Q1FY

12

Q2FY

12

Q3FY

12

Q4FY

12

Q1FY

13

Q2FY

13

Q3FY

13

Q4FY

13

Q1FY

14

Q2FY

14

Q3FY

14

Q4FY

14

Q1FY

15

Q2FY

15

Q3FY

15

-15.0

-10.0-5.0

0.0

5.010.0

15.0

Sales volumes (In MT) -LHS Growth (%) -RHS

Source: Company, ICICIdirect.com Research

Exhibit 9: …but realisations up 8.3% YoY to | 4795/tonne

4148

4223

4241

4245 44

6644

1143

7342

2141

8941

16 4429

4027 42

44 4655 4795

2000250030003500400045005000

Q1FY

12Q2

FY12

Q3FY

12Q4

FY12

Q1FY

13Q2

FY13

Q3FY

13Q4

FY13

Q1FY

14Q2

FY14

Q3FY

14Q4

FY14

Q1FY

15Q2

FY15

Q3FY

15

|/to

nne

-1001020304050

(%)

Realisation-LHS Growth (%) -RHS

`

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 5

Margins to improve gradually, going forward

We expect margins to improve gradually during our forecast period of FY14-17E led by healthy realisations and reduction in power & freight cost/tonne.

Exhibit 10: Expect EBITDA/tonne of |723 in FY17E

754

412

887783

289

506658

723

0

200

400

600

800

1000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

|

Cement EBITDA/Tonne

Source: Company, ICICIdirect.com Research

Exhibit 11: Margins to pick-up from FY17E

21.9

12.4

21.518.3

12.115.2

18.4 19.2

05

101520253035

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(%)

EBITDA Margin (%)

Source: Company, ICICIdirect.com Research

Exhibit 12: Q3FY15 cement EBITDA improved due to higher cement prices

988887 862 819

1029

778 792

569 572408

592

388 448

618755

0

200

400

600

800

1000

1200

Q1FY

12

Q2FY

12

Q3FY

12

Q4FY

12

Q1FY

13

Q2FY

13

Q3FY

13

Q4FY

13

Q1FY

14

Q2FY

14

Q3FY

14

Q4FY

14

Q1FY

15

Q2FY

15

Q3FY

15

Source: Company, ICICIdirect.com Research

Exhibit 13: Margin trend (%)

23.120.719.3

23.1

18.317.814.115.4

11.713.9

6.9

12.915.3

22.915.8

0

5

10

15

20

25

Q1FY

12

Q2FY

12

Q3FY

12

Q4FY

12

Q1FY

13

Q2FY

13

Q3FY

13

Q4FY

13

Q1FY

14

Q2FY

14

Q3FY

14

Q4FY

14

Q1FY

15

Q2FY

15

Q3FY

15

(%)

EBITDA Margin (%)

Source: Company, ICICIdirect.com Research

Expect net margins to improve during FY14-17E

After reporting a loss in FY14, we expect net margins to improve to 4.7% in FY17E from 3.6% in FY13. Overall, we expect the company to report a net profit of | 251.5 crore during FY17E from a loss of | 35.9 crore in FY14. Exhibit 14: Profitability trend

310.8

65.7

296.0

27.2

166.3

251.5

-35.9

176.39.4

4.7

0.6

3.33.6

7.0

1.9-0.8

-100

0

100

200

300

400

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

| cr

ore

-5

0

5

10

15

20

(%)

Net profit - LS Net profit margin -RS

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

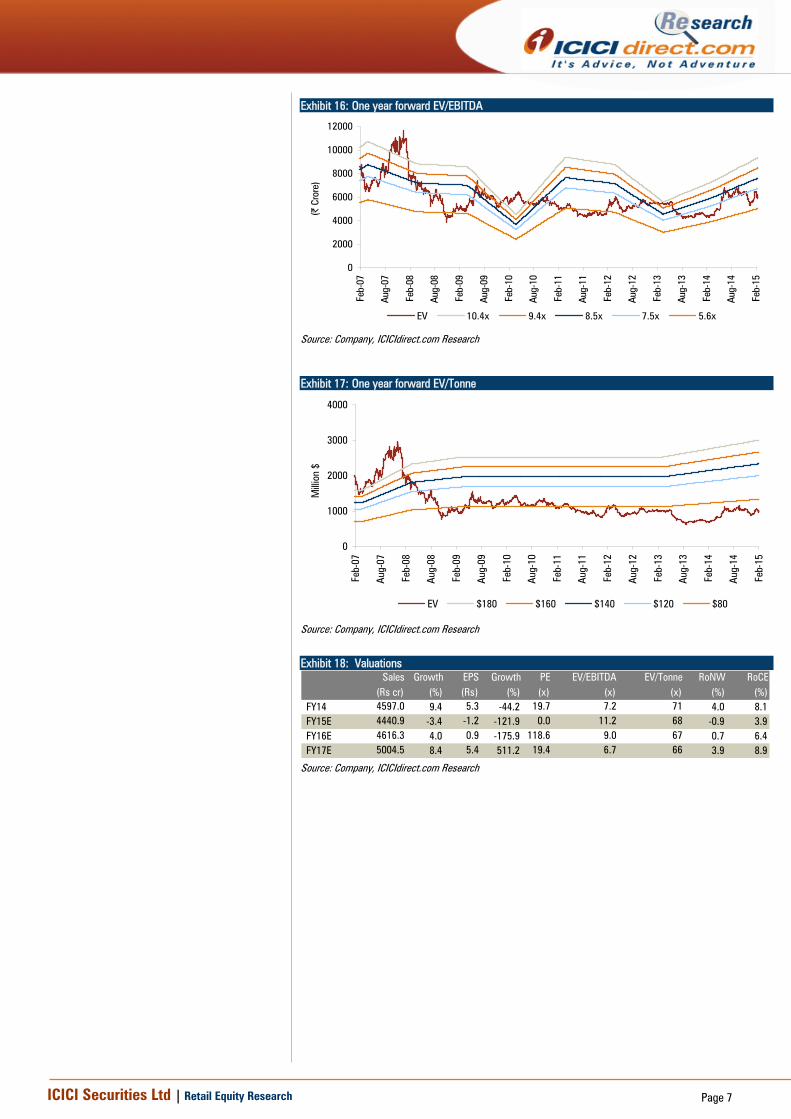

Outlook and valuation With the Telangana issue now resolved, we expect the overall utilisation in the southern region to improve over the next two or three years. While the bottoming out of demand in South India is a key positive for India Cement, the utilisation level is unlikely to exceed the peak of FY13 till FY17-18E, which will limit the volume growth for the company. At the CMP of | 103, the stock is available at $66/tonne on capacity of 15.5 MT, which is still 35% cheaper than the average valuations of midcap companies. Given the healthy pricing scenario coupled with an expected pick-up in demand, we remain positive on the company and maintain our BUY rating on the stock with a revised target price of | 127/share (i.e. valuing at $73/tonne on FY17E capacity and 6.5x FY17E EV/EBITDA).

ICICI Securities Ltd | Retail Equity Research Page 8

Company snapshot

0

20

40

60

80

100

120

140

160

180

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5

Jul-1

5

Oct-1

5

Jan-

16

Target price: |127

Source: Bloomberg, Company, ICICIdirect.com Research Key events Date EventMar-08 The company revives their shipping business with the purchase of two ships (dry bulk carriers) with a total capacity of 79,843 DWT. Commences commercial

production of 1 MT grinding plant at Chennai. Also, the company successfully bids for the Chennai franchise of the DLF-IPL 20/20 Cricket Tournament - 'Chennai Super Kings'.

Feb-09 Completes and commences commercial production of 1 MT grinding plant at Parli (Maharashtra). The company's subsidiary, namely, Trishul Concrete Products Ltd gets completed and commences commercial production of 1 lakh cuic metre ready mix concrete plant at Hyderabad (Andhra Pradesh)

Apr-09 The company upgrades capacity of kiln I to 3000 TPD (1700 TPD) at Vishnupuram

Sep-09 Announces plans to set up two 50 MW power plant in Shankar Nagar, Tamil Nadu and Andhra Pradesh with total capex of | 500 crore

Jan-10 ICL Financial Services Ltd (ICLFSL), the company's wholly-owned subsidiary, acquires 60.89% (including shares acquired under open offer) equity share capital in Indo Zinc Ltd (IZL). Consequently, IZL became a subsidiary of ICLFSL and ultimate subsidiary of the company. The company set up PT. Coromandel Minerals Resources as subsidiary in Indonesia for acquiring coal concessions

Apr-10 The company obtains ISO 9001 certification for quality assurance for their Dalavoi Plant.

Jun-10 The company completes upgradation of capacity at Chilamakur to 4500 tonnes per day

Jun-12 CCI fines company with penalty of | 187.5 crore on alleged cartelisation

Aug-12 Reports Q1FY12 results with 39% fall in profit, misses forecast due to overcapacity in South

Sep-12 COMPAT serves notice to CCI in cement cartelisation case

May-13 COMPAT directs cement companies to pay 10% penalty

Oct-13 Supreme Court bars company promoter N Srinivasan from taking charge as BCCI President till investigation gets complete w.r.t. IPL probe

Feb-15 Company transfred IPL division into separate subsidiary company Chennai Super Kings Cricket (CSKC) limited

Source: Company, ICICIdirect.com Research Top 10 Shareholders Shareholding Pattern Rank Name Latest Filing Date % O/S Position (m) Change (m)1 BNY Mellon Asset Management 31-Dec-14 9.80 30.1 0.12 EWS Finance & Investments Ltd. 31-Dec-14 9.00 27.6 0.03 Prince Holdings Madras Pvt. Ltd. 31-Dec-14 8.30 25.5 0.04 Subramanian (Vidya) 31-Dec-14 6.50 20.0 0.05 Life Insurance Corporation of India 31-Dec-14 6.06 18.6 0.06 Trishul Investments Pvt. Ltd. 31-Dec-14 5.71 17.5 0.07 The Boston Company Asset Management, LLC 1-Jul-14 5.24 16.1 -6.28 AfrAsia Capital Management Ltd 31-Dec-14 4.56 14.0 0.09 Anna Investments Pvt. Ltd. 31-Dec-14 4.24 13.0 0.010 HSBC Global Asset Management (Hong Kong) Limited 31-Dec-14 4.10 12.6 -0.4

ICICI Securities Ltd | Retail Equity Research Page 11

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

ICICI Securities Ltd | Retail Equity Research Page 12

ANALYST CERTIFICATION We /I, Rashesh Shah, CA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures: ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com. ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction. ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months. ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. It is confirmed that Rashesh Shah, CA, Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Rashesh Shah, CA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report. ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report. We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.