37

India & ICICI Group Trends & Outlook November 2015

India & ICICI Group

Trends & Outlook

November 2015

Certain statements in these slides are forward-looking statements.

These statements are based on management's current expectations and

are subject to uncertainty and changes in circumstances. Actual results

may differ materially from those included in these statements due to a

variety of factors. More information about these factors is contained in

ICICI Bank's filings with the US Securities and Exchange Commission.

All financial and other information in these slides, other than financial

and other information for specific subsidiaries where specifically

mentioned, is on an unconsolidated basis for ICICI Bank Limited only

unless specifically stated to be on a consolidated basis for ICICI Bank

Limited and its subsidiaries. Please also refer to the statement of

unconsolidated, consolidated and segmental results required by Indian

regulations that has, along with these slides, been filed with the stock

exchanges in India where ICICI Bank’s equity shares are listed and with

the New York Stock Exchange and the US Securities and Exchange

Commission, and is available on our website www.icicibank.com

2

Macro-economic environment 1

3

ICICI Group: performance & strategy 2

Several

policy

measures

Low inflation

& declining

interest rates

Signs of

improvement in

economic

activity

Trends in the Indian economy

Strong

external

position

4

While global developments have implications for emerging

market economies, India is relatively better placed

Trends in the Indian economy

5

India’s external position has improved

• CAD decreased to ~1.2% of GDP in Q1-2016 from a peak of

4.8% of GDP in FY2013

• FDI inflows of ~USD 11.8 billion in April-July 2015; inflow

of USD 34.4 billion in FY2015

• RBI’s forex reserves at ~US$ 353 billion

• Import cover of about 10 months

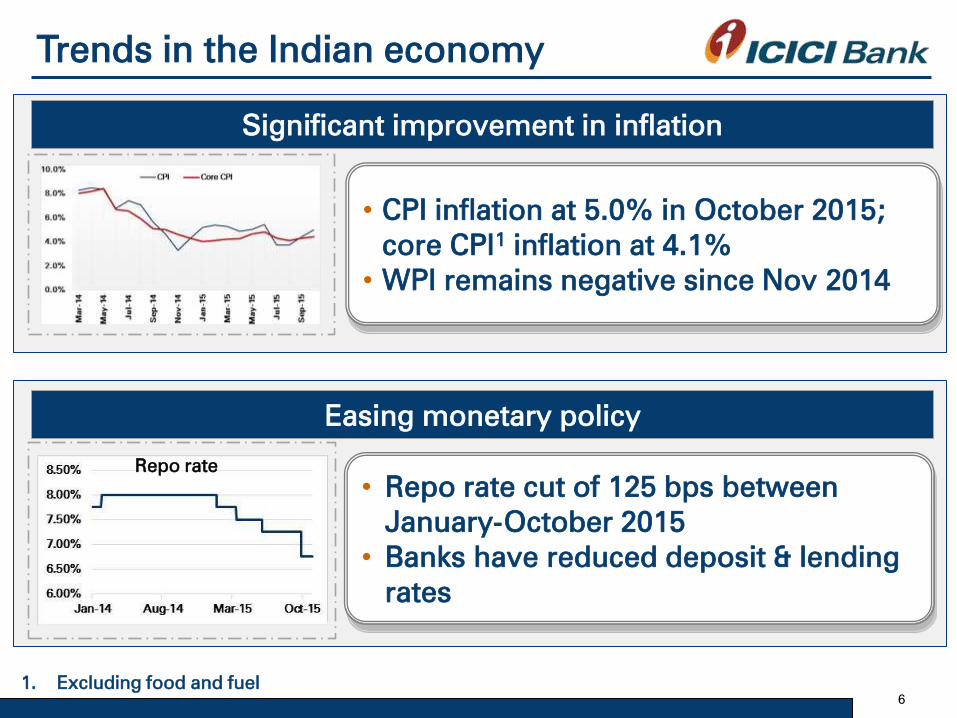

Significant improvement in inflation

• CPI inflation at 5.0% in October 2015;

core CPI1 inflation at 4.1%

• WPI remains negative since Nov 2014

Trends in the Indian economy

6

• Repo rate cut of 125 bps between

January-October 2015

• Banks have reduced deposit & lending

rates

Easing monetary policy

Repo rate

1. Excluding food and fuel

Signs of improvement across several key parameters

• Growth in industrial production,

including manufacturing, has remained

positive for eleven consecutive months

Trends in the Indian economy

7

Industrial production

• Sales of passenger vehicles and

commercial vehicles have improved

• Gradual improvement in capital goods

segment

• Pickup in coal production

Vehicle sales growth

Step-up in government spending expected to support growth

Macro-economic environment 1

8

ICICI Group: performance & strategy 2

Significant progress on operating performance

Strong retail & rural franchise

9

Leadership in technology

Substantial value creation within the ICICI Group

Significant progress on operating performance

Strong retail & rural franchise

10

Leadership in technology

Substantial value creation within the ICICI Group

Performance over the years

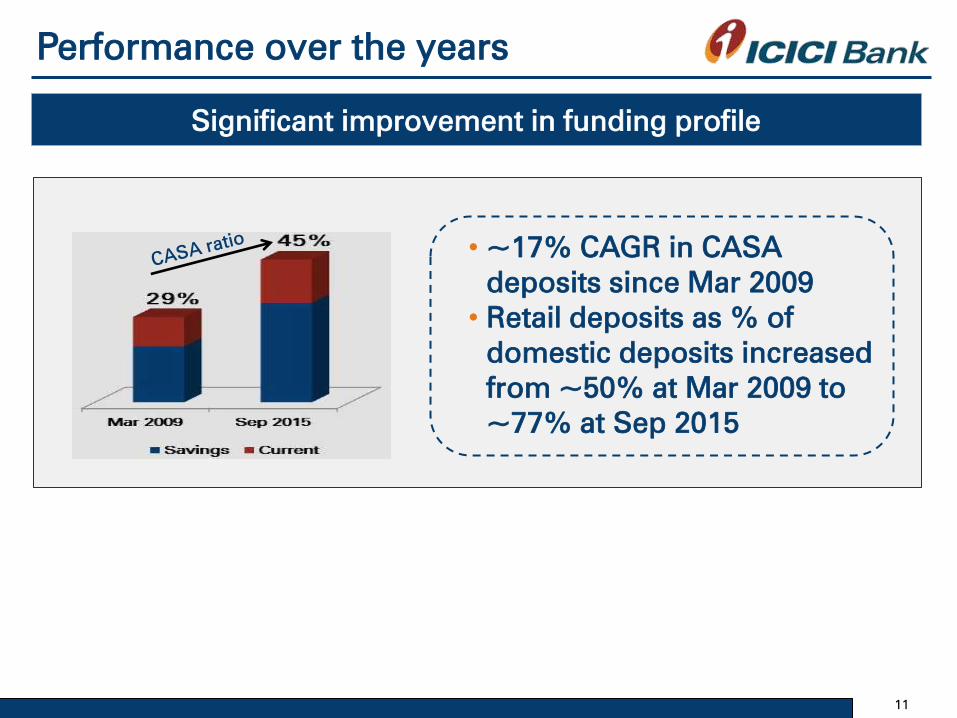

Significant improvement in funding profile

• ~17% CAGR in CASA

deposits since Mar 2009

• Retail deposits as % of

domestic deposits increased

from ~50% at Mar 2009 to

~77% at Sep 2015

11

Performance over the years

Healthy loan mix & growth

• ~ 16% CAGR in

domestic loans since

Mar 2011

• ~21% CAGR in retail

loans since Mar 2012

12

Sustained improvement in net interest margins

Performance over the years

• Margin improvement driven by

focus across businesses

• Domestic margins improved by

~90 bps since FY2010

• Overseas margins improved

from 0.41% in FY2010 to 1.65%

in FY2015 and 1.94% in H1-2016

13

Overall NIM

Strong operating efficiency

Performance over the years

14

Cost-income Branch network

Costs contained while continuing scale up in distribution &

investments in technology

Credit costs to average loans (annualised) at 96 bps in H1-2016

compared to 109 bps FY2015

Asset quality trends

15

Performance over the years

FY2014

Gross NPA additions 45.40

` billion FY2015

80.78

Of which: slippages from

restructured loans 7.27 45.29

Restructuring additions 66.33 53.94

H1-2016

38.58

12.15

20.89

Approach to asset quality

16

Concentration risk management framework refined for

incremental lending

Increasing share of retail loans

Focus on lending to higher rated corporates

Close monitoring of existing exposures for resolution &

recoveries

Return ratios

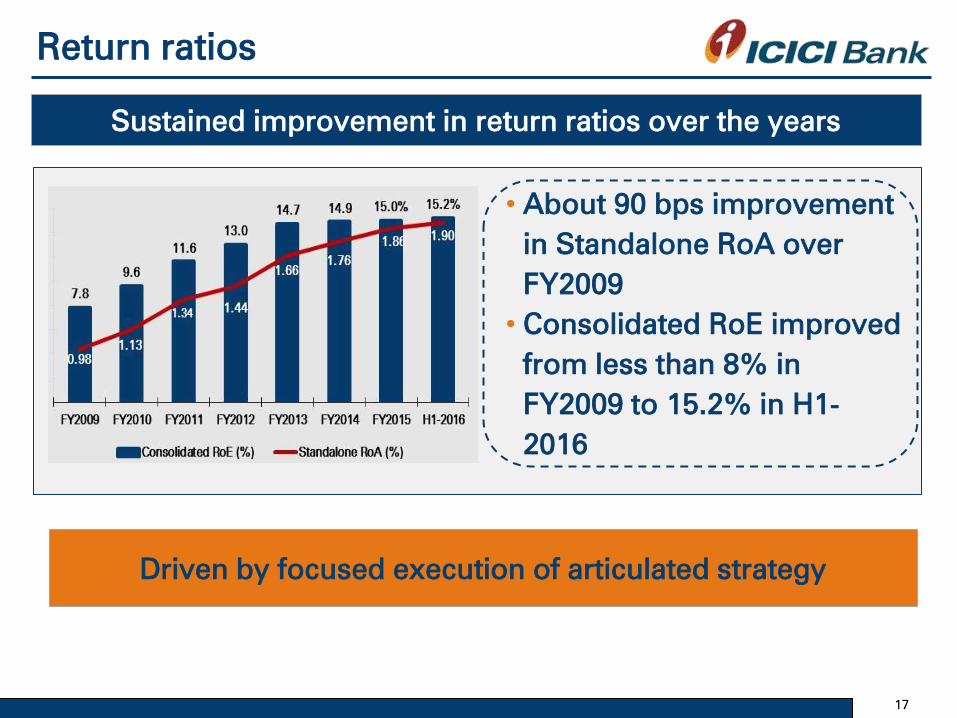

Sustained improvement in return ratios over the years

Driven by focused execution of articulated strategy

• About 90 bps improvement

in Standalone RoA over

FY2009

• Consolidated RoE improved

from less than 8% in

FY2009 to 15.2% in H1-

2016

17

Significant progress on operating performance

Strong retail & rural franchise

18

Leadership in technology

Substantial value creation within the ICICI Group

19

Enhanced retail franchise

Healthy

growth in

fee

income

Sustained

growth in

granular

deposits

Robust

loan

portfolio

growth

Stable

asset

quality

trends

The Bank continues to scale up its retail business and

invest in strengthening the franchise and distribution

infrastructure

Extensive geographical presence

20

Significant investments made in distribution

~52% of branches in semi-

urban and rural areas

Supplemented by

~12,800 ATMs

Branch network

Focus on cross-sell along

with customer service at

branches

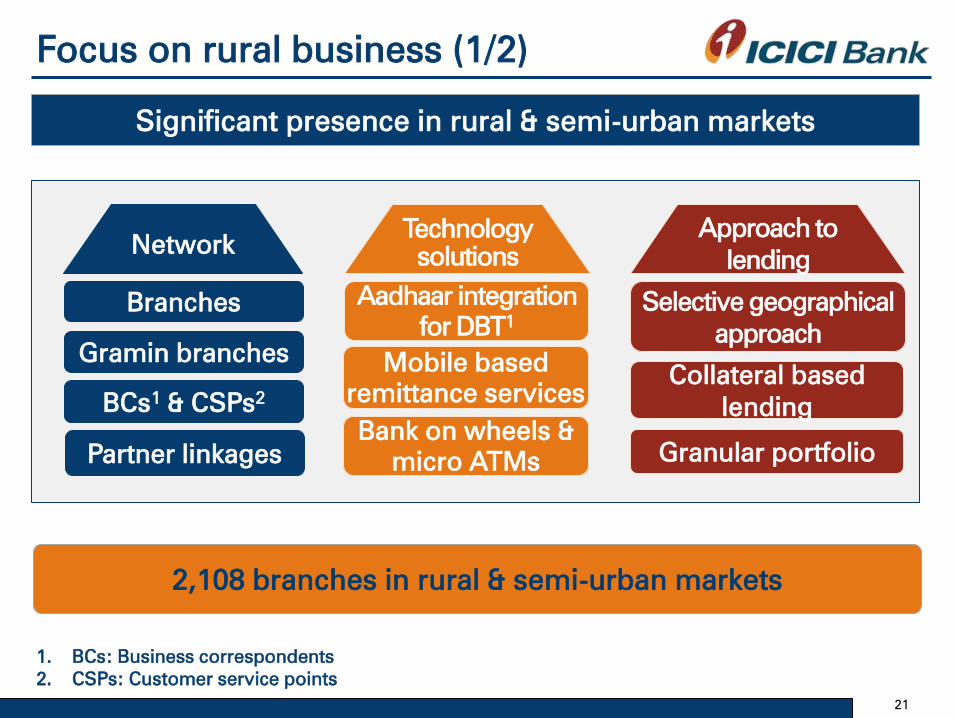

Significant presence in rural & semi-urban markets

Network Technology

solutions

Branches

Gramin branches

BCs1 & CSPs

2

Aadhaar integration

for DBT1

Partner linkages

2,108 branches in rural & semi-urban markets

Focus on rural business (1/2)

Mobile based

remittance services

Bank on wheels &

micro ATMs

21

1. BCs: Business correspondents

2. CSPs: Customer service points

Approach to

lending

Selective geographical

approach

Collateral based

lending

Granular portfolio

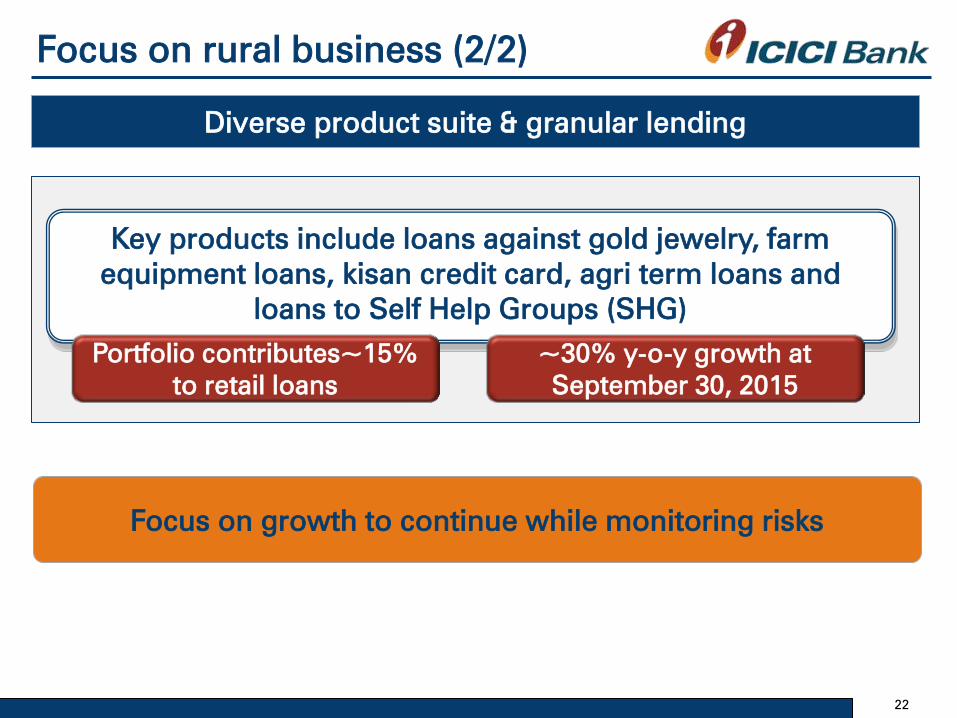

Diverse product suite & granular lending

Focus on growth to continue while monitoring risks

22

Key products include loans against gold jewelry, farm

equipment loans, kisan credit card, agri term loans and

loans to Self Help Groups (SHG)

Portfolio contributes~15%

to retail loans

~30% y-o-y growth at

September 30, 2015

Focus on rural business (2/2)

Significant progress on operating performance

Strong retail & rural franchise

23

Leadership in technology

Substantial value creation within the ICICI Group

Leadership in technology

Digitizing

channels

Digitizing

experience

Digitizing

core

Leveraging digitization & mobility to strengthen franchise &

improve performance

24

• One of the largest bouquets of seamless

services

• Online dashboard - ‘My View’

• Investment management & tax services

tools

• ~15 million unique monthly visitors

• Transactions of over ` 2 trillion processed

annually

25

Digitizing channels (1/2)

Over 60% of total transactions for our savings account customers

done through new age digital channels

iMobile

• Integrated view of all ICICI Bank relationships

• Over 100 services available

• First in India: tagging frequent transactions as

favourites; in-app chat functionality; alerts &

notifications through ‘Google Now’; flexible recurring

deposits called ‘iWish’

Refreshed & intuitive

website

26

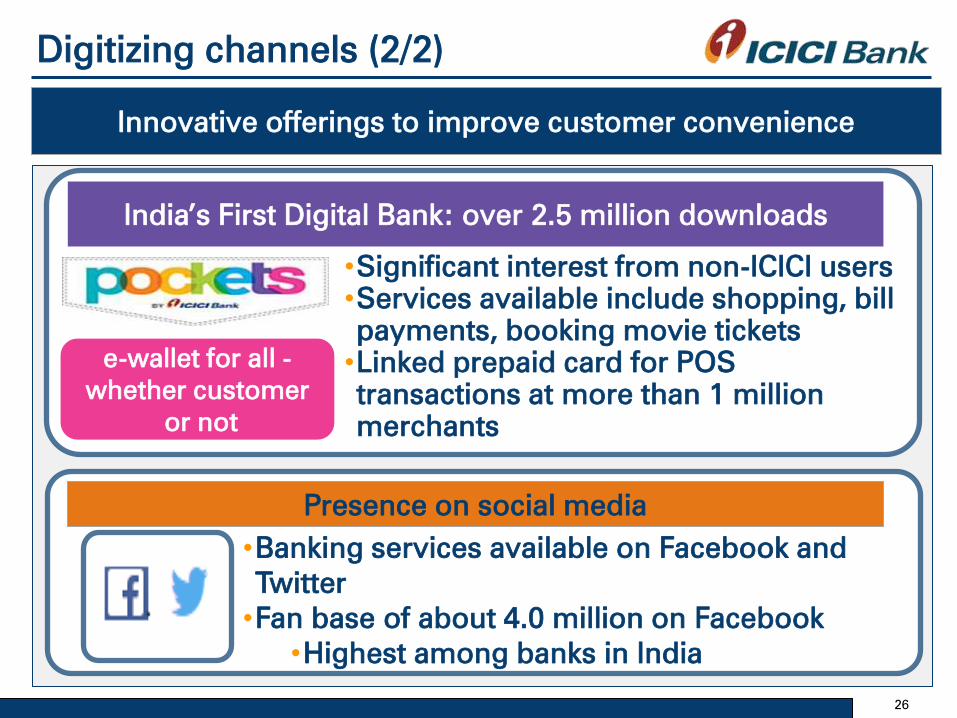

Digitizing channels (2/2)

e-wallet for all -

whether customer

or not

•Significant interest from non-ICICI users

•Services available include shopping, bill

payments, booking movie tickets

•Linked prepaid card for POS

transactions at more than 1 million

merchants

India’s First Digital Bank: over 2.5 million downloads

Presence on social media

Innovative offerings to improve customer convenience

•Banking services available on Facebook and

•Fan base of about 4.0 million on Facebook

•Highest among banks in India

Digitizing experience (1/2)

27

India’s first bank to launch 24x7 fully automated branches

• 108 touch banking branches across

33 cities in India

• Over 1,250 self service kiosks at

other branches

• State of the art robotic

technology

• Hi-tech security system & multi-

level checks

• Example of ‘Make in India’:

~80% Indian components

Smart Vault: first-of-its-kind 24x7 locker facility

Digitizing experience (2/2)

28

Debit & credit cards using near field communication

Contactless payments

Toll and transit solutions

• Transit Metro solutions

• Debit & credit cards with NFC metro smart card chip

• Auto-top up facility on low balance

• Easy recharge using SMS/internet

• Solutions for road transport

• Prepaid card with dual wallet (RFID1 chip & magnetic chip)

• Single card for bus ticket payments & retail purchases

• Electronic toll collection: prepaid RFID1 tags for vehicles

1. RFID: Radio-frequency identification

Digitizing core

Front office

• KYC through

scanned documents

• Demo videos for

products & services

• Upsell of mutual

funds & insurance

• Being introduced for

loan products

Over 3 million

savings accounts

sourced through

Tab banking

• Video banking app

• 24X7 face-to-face

banking

• Insta-banking

• Pre-processing of

transactions

• EFT cheques

• App-based cheque

issuance & image

based processing

• Image-based

processing of

documents

• OCR1 to reduce

data entry & error

rates

• Automated

processing

Mid office

Branch services

shifting to

customers’ mobiles

Back office

Digitizing

operations

29

1. OCR: Optical Character Recognition

Significant progress on operating performance

Strong retail & rural franchise

30

Leadership in technology

Substantial value creation within the ICICI Group

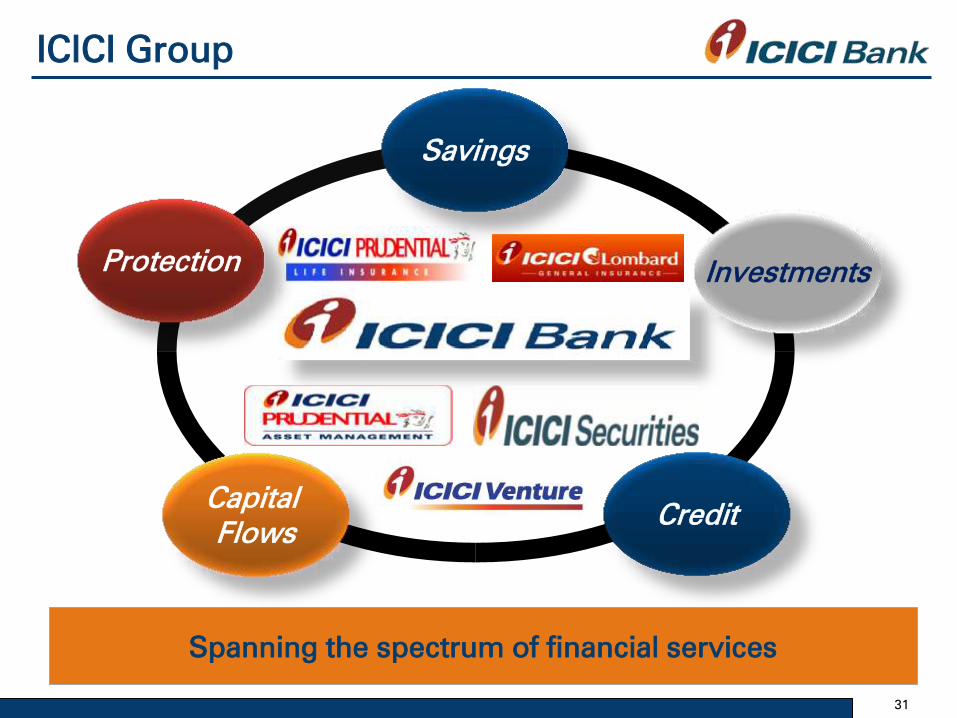

ICICI Group

Savings

Investments

Capital

Flows

Protection

Credit

Spanning the spectrum of financial services

31

32

Life insurance

• Overall market share1 has improved from

7.2% in FY2014 to 11.3% in FY2015 and

12.4% in H1-2016

•21.2% y-o-y growth in new business

premiums1 in H1-2016 compared to 0.4%

y-o-y for industry

Strong growth

& improvement

in market share

1. Based on retail weighted received premium

• PAT of ` 8.12 billion in H1-2016

• Return on equity of over 30%

Sustained &

strong

profitability

• AUM at ~` 991 billion at Sep 30, 2015 Growth in AUM

33

General insurance

• Private sector market leadership

maintained

• Overall market share at 9.0%1 in H1-2016

• Gross written premium grew by 22.0% y-

o-y compared to 11.7% y-o-y growth for

industry

Market

position

• 12.1% y-o-y increase in PAT to ` 2.58

billion in H1-2016; PAT of ` 5.36 billion in

FY2015

• Return on equity at ~17%

Strong

profitability

1. Based on gross written premium

2. Sale is subject to governmental and regulatory approvals

The Board of the Bank approved sale of 9.0% stake in ICICI General

to Fairfax (JV partner) at company valuation of ` 172.25 bn2

34

Other businesses

• 2nd largest AMC in India

• 33.3% y-o-y increase in profits in H1-2016

Asset

management

• Strong platforms for leveraging

favourable markets

• ICICI Securities: over 3.5 million

customers

• ICICI Securities PD: amongst the leaders

in Indian fixed income & money markets

Securities &

primary

dealership

Strong franchise across segments

Investments in a range of areas including digital product

offerings and partnerships

Looking ahead

35

Targeting 17-

18%

consolidated

RoE

Focus on profitability of subsidiaries & return on capital

36

Key priorities going forward

Continue to expand retail & rural

franchise

Maintain technology leadership

Sustain operating efficiency

Selectively grow corporate portfolio

Leverage strong capital position & improve efficiency

Thank you

37