Page 1

JM Financial Institutional Securities Limited

1QFY17 preview: Stable June, uncertain March

We expect a modest 2–4% organic USD revenue growth in 1QFY17 across the

top-6 players (except a flat quarter for TECHM), helped by seasonal recovery

in volume and a stable cross-currency. While the margin will expectedly

decline QoQ for most players due to seasonal factors (annual wage hike

and/or visa costs), mild INR appreciation (c1% QoQ) and adjustments due to

shift to IndAS, we believe the impact could be lower than traditional levels

given the adjustments we see across players in their appraisals/payout

methodologies to manage the margin impact vs. traditional levels. A steady

1QFY17 notwithstanding, an increased uncertainty on the medium-term

growth outlook following ‘Brexit’ could weigh on sector valuations, in our

view. TECHM (stability in telecom vertical + improving deal wins +

inexpensive valuations) and OFSS (seasonal strength in licence sales + U/P

vs. global peers) are our preferred picks.

1QFY17F – revenue growth to recover… We estimate the USD revenue to

increase 0–4% QoQ for our IT services coverage, driven by seasonal recovery in

volume growth and modest cross-currency tailwinds (0–60bps). In constant

currency organic revenue growth, we estimate INFO at the upper end (ramp-up

in large deals) and TECHM at the lower end (seasonal decline in Comviva).

Among mid-caps, we expect a strong 12% USD revenue growth for OFSS, led by

seasonally strong license sales.

… with seasonal softness in margin. EBIT margin could decline 50–180bps

QoQ across the top-6 players; the decline should be sharper for INFO and TCS

due to the annual wage hike, though we expect the impact could be lower than

the traditional levels (c220bps), given the shift in appraisal methods (individual

evaluation vs. bell-curve based earlier) and coverage (INFO has moved wage hike

for middle and senior management to July). We expect FX gains to be positive,

despite the translation impact due to the swing in quarter-close rates. We expect

a -5–2% QoQ PAT growth for the top-6 players (player-wise details in Exhibit 5).

‘Brexit’ is the incremental headwind… While the immediate impact of ‘Brexit’

will be from the adverse cross-currency movement – likely to be more visible in

2QFY17 than 1Q – a slower decision making on large deals/discretionary spend

could affect medium-term volume growth, in our view. The UK accounted for

13%, in TCV terms, of large deals awarded globally in FY16, according to ISG, an

outsourcing advisor. Also, the sharp GBP depreciation, if not re-negotiated,

could affect profitability of ongoing deals and consequently players’ medium-

term margins, in our view. Indian companies may also need to make changes in

the European delivery/sales infrastructure that could affect longer-term margin.

… though players may remain circumspect. We expect companies to retain

their current FY17 volume growth outlook with a cautious (but indefinite) stance

on the ‘Brexit’ impact. INFO could adjust the FY17 USD revenue growth guidance

for the currency; we estimate the constant currency growth guidance could get

revised to 11.1–13.1% (11.5–13.5% at present).

Margin management to be the differentiator. Our channel checks indicate IT

spend by clients remains calibrated with a heightened due diligence of vendor

responses to RFPs. An incremental slow-down in volume growth (from ‘Brexit’) is

thus an incremental margin risk; note, EBIT margins have declined up to 400bps

for the top-4 players over the past eight quarters, adjusted for currency impact

(INR+cross-currency). We see minimal EPS upgrades post results for most

players. We retain our preference for players with subdued/modest margin

expectations and relatively inexpensive valuations.

Pankaj Kapoor

[email protected]

Tel: (+91 22) 66303089

Abhishek Kumar

[email protected]

Tel: (+91 22) 66303057

IT coverage universe: Ratings and TPs

RECO TP Upside

INFO BUY 1,340 14.5%

TCS BUY 2,750 7.7%

TECHM BUY 680 34.5%

PSYS HOLD 800 14.7%

MTCL HOLD 780 17.3%

NITEC BUY 640 24.8%

ECLX HOLD 1,400 -3.2%

OFSS BUY 4,050 16.9%

BSE IT vs. Sensex

70

75

80

85

90

95

100

105

110

115

Jun-15 Aug-15 Oct-15 Dec-15 Feb-16 Apr-16 Jun-16

Sensex BSE-IT

IT coverage universe: Valuation

EPS PER

FY1E FY2E FY1E FY2E

INFO 64.9 74.3 18.1x 15.8x

TCS 136.4 154.1 18.7x 16.6x

TECHM 40.3 49.8 12.5x 10.2x

PSYS 42.2 52.5 16.5x 13.3x

MTCL 40.8 48.5 16.3x 13.7x

NITEC 50.2 58.3 10.2x 8.8x

ECLX 94.1 101.6 15.4x 14.2x

OFSS 155.9 181.1 22.2x 19.1x

Source: JM Financial

India IT Services and Software

4 July 2016

India | IT | Sector Update

JM Financial Research is also available

on: Bloomberg - JMFR <GO>,

Thomson Publisher & Reuters,

S&P Capital IQ and FactSet.

Please see Appendix I at the end of this

report for Important Disclosures and

Disclaimers and Research Analyst

Certification.

Page 2

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 2

1QFY17 earnings preview

Exhibit 1. JMF IT coverage universe: 1QFY17’s key estimates

Revenue

EBITDA

EBIT PAT

(USD mn)

Growth

(QoQ)

Cross-

currency

CC* grow.

(QoQ) Margin (%) Change Margin (%) Change (` mn) Change

INFO 2,535 3.6% 33bps 3.3% 26.3% -178bps 23.7% -178bp 34,325 -4.6%

TCS 4,355 3.5% 58bps 2.9% 26.1% -174bps 24.3% -174bp 60,207 -5.1%

TECHM 1,026 0.3% 14bps 0.2% 16.0% -87bps 12.6% -106bp 7,336 -18.1%

PSYS 103 2.3% 0bps 2.3% 14.3% -155bps 10.5% -157bp 671 -16.9%

MTCL 201 2.9% 16bp 2.7% 16.6% -42bp 13.2% -121bp 1,484 -4.9%

NITEC 103 1.3% 10bps 1.2% 16.6% -186bps 12.4% -205bp 646 -17.6%

ECLX 52 1.5% 18bps 1.3% 37.9% -307bps 33.8% -319bp 956 -11.7%

OFSS 168 11.9% 0bps 11.9% 44.6% 875bps 43.5% 890bp 3,614 61.2%

*CC: Constant currency; Source: JM Financial

Exhibit 2. Select players’ estimated cross-currency impact during 1QFY17

Revenue share Change (QoQ) Cross-currency impact

USD GBP EUR AUD USD GBP EUR AUD GBP EUR AUD Total

INFO 69% 7% 10% 7% -0.9% 0.1% 1.9% 1.9% 1bps 19bps 13bps 33bps

TCS 57% 14% 8% 6% -1.0% -0.7% 1.3% 1.2% -10bps 10bps 7bps 58bps

TECHM 51% 11% 11% 5% 1.8% -0.6% 1.3% 1.2% -7bps 15bps 6bps 14bps

MTCL 73% 5% 12% NA 2.7% 0.0% 1.7% NA 0bps 0bps NA 16bps

NITEC 51% 20% 10% 5% 1.5% 0.0% 1.7% 1.1% 0bps 0bps 0bps 10bps

Source: Companies, JM Financial

Exhibit 3. Potential impact on FY17 EBIT margin/EPS due to cross-currency

INFO TCS TECHM MTCL NITEC

If GBP depreciates by 10% -

GBP denominated revenue share 6.70% 13.16% 10.80% 5.00% 20.00%

Reported USD revenue impact -67bps -132bps -108bps -50bps -200bps

EBIT margin impact -23bps -46bps -38bps -18bps -70bps

Reported INR EPS impact -0.70% -1.38% -1.70% -0.79% -3.15%

Additionally if Euro depreciates by 5% -

Euro denominated revenue share 9.60% 7.87% 11.30% 12.00% 10.00%

Reported USD revenue impact -48bps -39bps -57bps -60bps -50bps

EBIT margin impact -17bps -14bps -20bps -21bps -18bps

Reported INR EPS impact -0.50% -0.41% -0.89% -0.95% -0.79%

Combined

Reported USD revenue impact -115bps -171bps -165bps -110bps -250bps

EBIT margin impact -40bps -60bps -58bps -39bps -88bps

Reported INR EPS impact -1.21% -1.79% -2.59% -1.73% -3.94%

Source: Companies, JM Financial

Exhibit 4. At current exchange rate, Infosys’ FY17 cc/USD revenue guidance could be lower by 40/80bps

Rev. dist. Constant Currency Guidance (FY17) USD Revenue Growth Guidance (FY17)

FY16 Assumed rate Revised rate Impact Assumed rate Revised rate Impact

USD 69.9% 65.59 67.48 2.01% 66.26 67.48 1.29%

GBP 6.6% 1.51 1.36 -0.65% 1.44 1.36 -0.36%

Euro 9.3% 1.1 1.11 0.10% 1.14 1.11 -0.23%

AUD 6.9% 0.73 0.74 0.12% 0.77 0.74 -0.24%

Total 100.00% - - -0.4% - - -0.8%

Source: Companies, JM Financial

Page 3

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 3

Exhibit 5. JMF’s IT services and software coverage universe: Estimates for key financials (Apr–Jun 2016)

Revenue Op. margin PAT

USD mn ` mn (%) ` mn Comments and key assumptions

Infosys 2,535 170,277 26.3% 34,325

Estimate IT services volume/pricing growth of 3.6%/0.3% QoQ

Change – QoQ 3.6% 2.9% -178bp -4.6%

TCS 4,355 291,598 26.1% 60,207 Assume 200bps impact on margins due to wage hike/higher

sub-contracting cost Change – QoQ 3.5% 2.5% -174bp -5.1%

Tech Mahindra 1,026 69,018 16.0% 7,336 Est. USD86mn contribution from LCC+Sofgen (-5% QoQ)

Enterprise growth estimate: 3.3% QoQ; FX gain: `336mn Change – QoQ 0.3% 0.3% -87bp -18.1%

Persistent 103 6,881 14.3% 671 0.5%/7.1% QoQ organic USD revenue growth in Services/IP

Higher G&A due to one-time facility set-up to impact margins;

higher (normalised) tax rate to impact QoQ PAT growth

Change – QoQ 2.3% 1.6% -155bp -16.9%

Mindtree 201 13,405 16.6% 1,484 Estimate volume/pricing growth of 2.2%/0.7% QoQ

Amortization of Intangible (as per IndAS) + incentive pay-out

of USD 2.5mn to impact EBIT margin by 80bps

Change – QoQ 2.9% 1.2% -42bp -4.9%

NIIT Tech 103 6,878 16.6% 646 GIS revenues estimated to decline 33% QoQ due to seasonality

We estimate hedge gain of `20mn reported in revenues Change – QoQ 1.3% 0.5% -186bp -17.6%

eClerx 52 3,452 37.9% 956 Expect utilisation to decline 100bps as short-term project tail

off; wage hike/investments to hit margins Change – QoQ 1.5% 0.6% -307bp -11.7%

OFSS 168 11,255 44.6% 3,614

License revenue estimated to be USD28.8mn (+15% YoY)

Change – QoQ 11.9% 38.2% 875bp 61.2%

Notes: All numbers are consolidated Indian GAAP numbers except Infosys and TCS; Source: Companies, JM Financial

Exhibit 6. JMF’s IT services coverage universe: Apr–Jun 2016 quarter results calendar and key issues

Key issues to focus on

Infosys

(15th

Jul, 2016)

Commentary around impact of Brexit on demand/client spending, especially in BFSI

Potential revision of FY17 constant currency revenue guidance on cross-currency headwinds (11.5–13.5% currently)

Comment on margin band (currently at 24–26%)

TCS

(14th

Jul, 2016)

Outlook for the BFSI vertical especially for UK/EU clients after Brexit

Update on Diligenta/Japan business after headwinds in FY16

Growth in digital business + large deal wins; comments on profile/size of digital deals

Tech Mahindra

(01st

Aug, 2016)

Deal wins/pipeline in telecom + update on post-acquisition integration works in large telecom clients

Margin trajectory in LCC after divesting the low-margin business

Persistent

(24h

Jul, 2016)

Progress on integration of IBM business; potential growth prospects and margin impact on the consol. business

Outlook on the core product development business; progress on enterprise business

NIIT Tech

(15th

Jul, 2016)*

Deal wins and order book position; update on large deal pipeline

Commentary around impact of Brexit on demand/client spending, specifically in EU/UK travel accounts

Mindtree

(18th

Jul, 2016)

FY17 organic revenue growth outlook + TCV of new deal wins; update on digital business

Margin impact of increased amortization due to IndAS

eClerx

(Jul 4th

week)*

Any revision to FY17 outlook after a guiding for a softer 1HFY17

Commentary around impact of Brexit on BFSI clients/EU digital business

OFSS

(Aug 2nd

week)*

License booking + QoQ change in implementation and AMC revenues (static for past few quarters)

Commentary around impact of Brexit on deal pipeline/conversion

Note: * - Tentative; Source: JM Financial

Exhibit 7. Impact of IndAS on reported financials

Company Potential impact

Tech Mahindra ESOP charges: Impact of USD 7–8mn on FY17 margins

Treasury shares: 96mn treasury shares to be extinguished resulting in 10% higher reported EPS

Non-current investment of `12bn (in TML benefit trust) to be offset against treasury shares in reserve and surplus

This will result in 8% decline in equity base and 1 ppt increase in RoE

Mindtree Lower EBIT due to amortisation of intangible assets

Source: JM Financial

Page 4

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 4

Exhibit 8. Apr–Jun 2016 quarter: Estimated QoQ variance in realised USD-INR rate

Jan–Mar 16 Apr - Jun 16 Variance (%) Comments

Infosys 67.7 67.2 -0.7% We expect a -1.0% to 1.0% QoQ change in the realised USD-

INR rate for our coverage universe. The variation is due to

the different methodologies followed to calculate realised

rates.

TCS 67.6 67.0 -1.0%

Tech Mahindra 67.3 67.3 -0.1%

Persistent 67.4 67.0 -0.7%

Mindtree 67.7 66.6 -1.6%

NIIT Tech 65.6 66.6 1.5%

eClerx 67.6 67.0 -0.9%

OFSS 67.6 67.0 -0.9%

Source: JM Financial

Exhibit 9. Apr–Jun 2016 quarter: Movements in key currencies versus the USD

Apr - Jun 16

Change in Change in

Comments Apr - Jun 16 Jan - Mar 16

Indian rupee/US Dollar – period-end 67.53 1.9% 0.1% Brexit vote towards the end of the quarter

resulted in sharp GBP depreciation against the

USD. However, GBP appreciation against the USD

in the first half of the quarter results in almost

similar average GBP-USD rate QoQ

Currencies of commodity linked economies such

as the Brazilian Real appreciated sharply against

the USD as crude prices bounced back to almost

USD50/barrel.

We estimate a 0bps to 60bps positive cross-

currency impact on reported USD revenue for the

coverage universe; TCS, with higher exposure to

BRL and JPY, will likely see the highest cross-

currency tailwind (60bps) in our coverage

universe, in our view.

Indian rupee/US Dollar – average 66.94 -0.8% 2.4%

British pound/US Dollar – period-end 1.33 -7.3% -2.6%

British pound/US Dollar – average 1.44 0.2% -5.6%

Euro/US Dollar – period-end 1.11 -2.4% 4.8%

Euro/US Dollar – average 1.13 2.3% 0.8%

Australian Dollar/US Dollar – period-end 0.75 -2.7% 5.1%

Australian Dollar/US Dollar – average 0.75 3.1% 0.4%

Brazilian Real/US Dollar – period-end 0.31 11.5% 10.3%

Brazilian Real/US Dollar – average 0.29 11.3% -1.2%

Mexican Peso/US Dollar – period-end 0.05 -5.5% -0.4%

Mexican Peso/US Dollar – average 0.06 -0.4% -7.0%

Uruguay Peso/US Dollar – period-end 0.03 3.9% -5.6%

Uruguay Peso/US Dollar – average 0.03 0.8% -6.3%

Chilean Peso/US Dollar – period-end 0.15 0.9% 6.1%

Chilean Peso/US Dollar – average 0.15 3.4% -0.4%

Source: JM Financial

Exhibit 11. JMF’s IT services and software coverage universe: Recommendations and valuations

EPS (`)

JMF vs. Cons.

P/E

EV/EBITDA

RoE

CPS Div.

Yld

Rating TP FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY16 FY16

INFO BUY 1,340 64.9 74.3

-2.0 -1.2

18.1 15.8

11.7 10.1

22.6

143.1 1.9

TCS BUY 2,750 136.4 154.1 1.3 2.5 18.7 16.6 13.4 11.7 33.1 150.6 3.1

TECHM BUY 680 40.3 49.8

9.2 18.0

12.5 10.2

13.8 11.9

22.5

51.2 1.2

PSYS HOLD 800 42.2 52.5 -0.7 2.1 16.5 13.3 15.9 11.4 19.0 94.8 2.2

MTCL HOLD 780 40.8 48.5 -1.7 -0.1 16.3 13.7 10.6 8.7 26.4 26.7 2.6

NITEC BUY 640 50.2 58.3

-0.2 4.1

10.2 8.8

4.9 4.1

18.3

54.5 1.9

ECLX HOLD 1,400 94.1 101.6 3.2 0.2 15.4 14.2 8.5 7.5 31.5 131.4 3.2

OFSS BUY 4,050 155.9 181.1 -2.8 -4.8 22.2 19.1 13.8 11.9 35.0 322.2 2.9

Note: Prices as of June 30, 2016; Source: JM Financial

Page 5

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 5

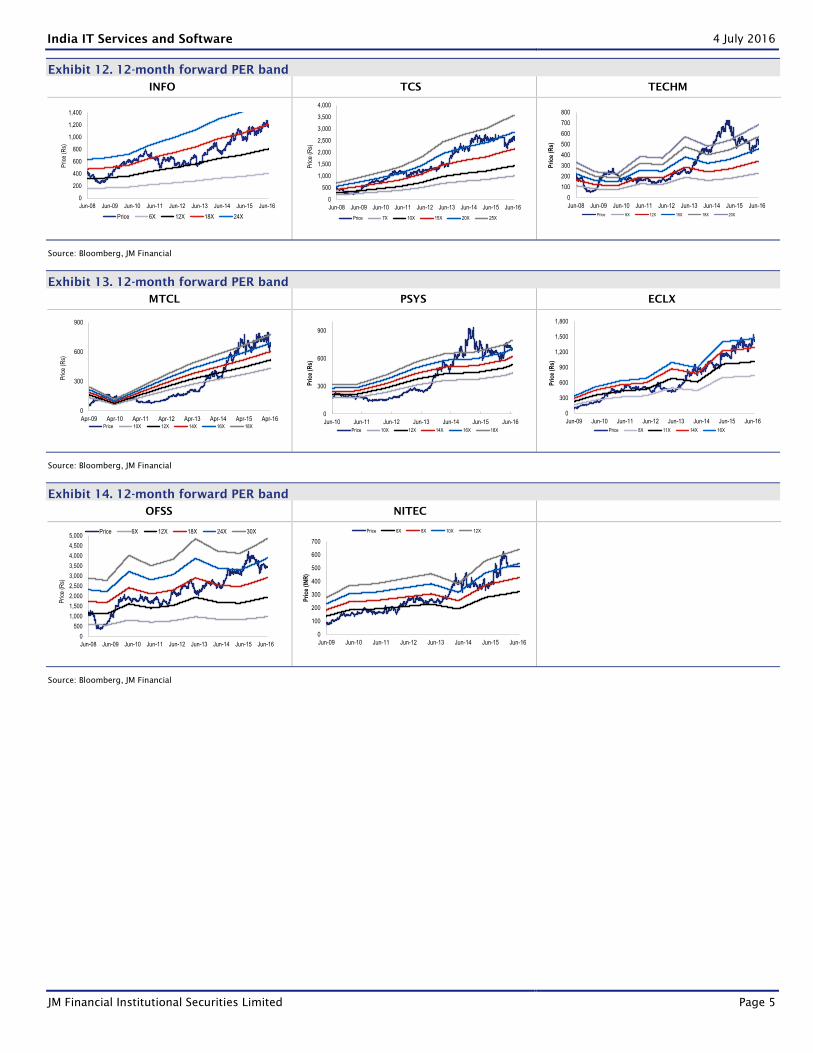

Exhibit 12. 12-month forward PER band

INFO TCS TECHM

0

200

400

600

800

1,000

1,200

1,400

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pric

e (R

s)

Price 6X 12X 18X 24X

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pric

e (R

s)

Price 7X 10X 15X 20X 25X

0

100

200

300

400

500

600

700

800

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pri

ce (

Rs)

Price 6X 12X 15X 18X 20X

Source: Bloomberg, JM Financial

Exhibit 13. 12-month forward PER band

MTCL PSYS ECLX

0

300

600

900

Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15 Apr-16

Pric

e (R

s)

Price 10X 12X 14X 16X 18X

0

300

600

900

Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pri

ce (

Rs)

Price 10X 12X 14X 16X 18X

0

300

600

900

1,200

1,500

1,800

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pri

ce (

Rs)

Price 8X 11X 14X 16X

Source: Bloomberg, JM Financial

Exhibit 14. 12-month forward PER band

OFSS NITEC

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pric

e (R

s)

Price 6X 12X 18X 24X 30X

0

100

200

300

400

500

600

700

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

Pri

ce (

INR

)

Price 6X 8X 10X 12X

Source: Bloomberg, JM Financial

Page 6

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 6

APPENDIX I

JM Financial Institutional Securities Limited

(Formerly known as JM Financial Institutional Securities Private Limited)

Corporate Identity Number: U65192MH1995PLC092522

Member of BSE Ltd. and National Stock Exchange of India Ltd. and MCX Stock Exchange Ltd.

SEBI Registration Nos.: BSE - INZ010012532, NSE - INZ230012536 and MCX-SX - INZ260012539

Registered Office: 7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai 400 025, India.

Board: +9122 6630 3030 | Fax: +91 22 6630 3488 | Email: [email protected] | www.jmfl.com

Compliance Officer: Mr. Sunny Shah | Tel: +91 22 6630 3383 | Email: [email protected]

Definition of ratings

Rating Meaning

Buy Total expected returns of more than 15%. Total expected return includes dividend yields.

Hold Price expected to move in the range of 10% downside to 15% upside from the current market price.

Sell Price expected to move downwards by more than 10%

Research Analyst(s) Certification

The Research Analyst(s), with respect to each issuer and its securities covered by them in this research report, certify that:

All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their

securities; and

No part of his or her or their compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed

in this research report.

Important Disclosures

This research report has been prepared by JM Financial Institutional Securities Limited (JM Financial Institutional Securities) to provide

information about the company(ies) and sector(s), if any, covered in the report and may be distributed by it and/or its associates solely for the

purpose of information of the select recipient of this report. This report and/or any part thereof, may not be duplicated in any form and/or

reproduced or redistributed without the prior written consent of JM Financial Institutional Securities. This report has been prepared

independent of the companies covered herein.

JM Financial Institutional Securities is registered with the Securities and Exchange Board of India (SEBI) as a Merchant Banker and a Stock

Broker having trading memberships of the BSE Ltd. (BSE), National Stock Exchange of India Ltd. (NSE) and MCX Stock Exchange Ltd. (MCX-SX).

No material disciplinary action has been taken by SEBI against JM Financial Institutional Securities in the past two financial years which may

impact the investment decision making of the investor.

JM Financial Institutional Securities provides a wide range of investment banking services to a diversified client base of corporates in the

domestic and international markets. It also renders stock broking services primarily to institutional investors and provides the research

services to its institutional clients/investors. JM Financial Institutional Securities and its associates are part of a multi-service, integrated

investment banking, investment management, brokerage and financing group. JM Financial Institutional Securities and/or its associates might

have provided or may provide services in respect of managing offerings of securities, corporate finance, investment banking, mergers &

acquisitions, broking, financing or any other advisory services to the company(ies) covered herein. JM Financial Institutional Securities and/or

its associates might have received during the past twelve months or may receive compensation from the company(ies) mentioned in this

report for rendering any of the above services.

JM Financial Institutional Securities and/or its associates, their directors and employees may; (a) from time to time, have a long or short

position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such

securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) covered under

this report or (c) act as an advisor or lender/borrower to, or may have any financial interest in, such company(ies) or (d) considering the

nature of business/activities that JM Financial Institutional Securities is engaged in, it may have potential conflict of interest at the time of

publication of this report on the subject company(ies).

Neither JM Financial Institutional Securities nor its associates or the Research Analyst(s) named in this report or his/her relatives individually

own one per cent or more securities of the company(ies) covered under this report, at the relevant date as specified in the SEBI (Research

Analysts) Regulations, 2014.

Research Analysts or their relatives; (a) do not have any financial interest in the company(ies) covered under this report or (b) did not receive

any compensation from the company(ies) covered under this report, or from any third party, in connection with this report or (c) do not have

any other material conflict of interest at the time of publication of this report. Research Analyst(s) are not serving as an officer, director or

employee of the company(ies) covered under this report.

While reasonable care has been taken in the preparation of this report, it does not purport to be a complete description of the securities,

markets or developments referred to herein, and JM Financial Institutional Securities does not warrant its accuracy or completeness. JM

Page 7

India IT Services and Software 4 July 2016

JM Financial Institutional Securities Limited Page 7

Financial Institutional Securities may not be in any way responsible for any loss or damage that may arise to any person from any inadvertent

error in the information contained in this report. This report is provided for information only and is not an investment advice and must not

alone be taken as the basis for an investment decision. The investment discussed or views expressed or recommendations/opinions given

herein may not be suitable for all investors. The user assumes the entire risk of any use made of this information. The information contained

herein may be changed without notice and JM Financial Institutional Securities reserves the right to make modifications and alterations to this

statement as they may deem fit from time to time.

This report is neither an offer nor solicitation of an offer to buy and/or sell any securities mentioned herein and/or not an official

confirmation of any transaction.

This report is not directed or intended for distribution to, or use by any person or entity who is a citizen or resident of or located in any

locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or

which would subject JM Financial Institutional Securities and/or its affiliated company(ies) to any registration or licensing requirement within

such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors.

Persons in whose possession this report may come, are required to inform themselves of and to observe such restrictions.

Persons who receive this report from JM Financial Singapore Pte Ltd may contact Mr. Ruchir Jhunjhunwala ([email protected] ) on

+65 6422 1888 in respect of any matters arising from, or in connection with, this report.

Additional disclosure only for U.S. persons: JM Financial Institutional Securities has entered into an agreement with Enclave Capital LLC

("Enclave Capital"), a U.S. registered broker-dealer and member of the Financial Industry Regulatory Authority ("FINRA") in order to conduct

certain business in the United States in reliance on the exemption from U.S. broker-dealer registration provided by Rule 15a-6, promulgated

under the U.S. Securities Exchange Act of 1934 (the "Exchange Act"), as amended, and as interpreted by the staff of the U.S. Securities and

Exchange Commission ("SEC") (together "Rule 15a-6").

This research report is distributed in the United States by Enclave Capital in compliance with Rule 15a-6, and as a "third party research report"

for purposes of FINRA Rule 2711. In compliance with Rule 15a-6(a)(3) this research report is distributed only to "major U.S. institutional

investors" as defined in Rule 15a-6 and is not intended for use by any person or entity that is not a major U.S. institutional investor. If you

have received a copy of this research report and are not a major U.S. institutional investor, you are instructed not to read, rely on, or

reproduce the contents hereof, and to destroy this research or return it to JM Financial Institutional Securities or to Enclave Capital.

This research report is a product of JM Financial Institutional Securities, which is the employer of the research analyst(s) solely responsible for

its content. The research analyst(s) preparing this research report is/are resident outside the United States and are not associated persons or

employees of any U.S. registered broker-dealer. Therefore, the analyst(s) are not subject to supervision by a U.S. broker-dealer, or otherwise

required to satisfy the regulatory licensing requirements of FINRA and may not be subject to the Rule 2711 restrictions on communications

with a subject company, public appearances and trading securities held by a research analyst account.

JM Financial Institutional Securities only accepts orders from major U.S. institutional investors. Pursuant to its agreement with JM Financial

Institutional Securities, Enclave Capital effects the transactions for major U.S. institutional investors. Major U.S. institutional investors may

place orders with JM Financial Institutional Securities directly, or through Enclave Capital, in the securities discussed in this research report.

Additional disclosure only for U.K. persons: Neither JM Financial Institutional Securities nor any of its affiliates is authorised in the United

Kingdom (U.K.) by the Financial Conduct Authority. As a result, this report is for distribution only to persons who (i) have professional

experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion)

Order 2005 (as amended, the "Financial Promotion Order"), (ii) are persons falling within Article 49(2)(a) to (d) ("high net worth companies,

unincorporated associations etc.") of the Financial Promotion Order, (iii) are outside the United Kingdom, or (iv) are persons to whom an

invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in

connection with the matters to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such

persons together being referred to as "relevant persons"). This report is directed only at relevant persons and must not be acted on or relied

on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant

persons and will be engaged in only with relevant persons.