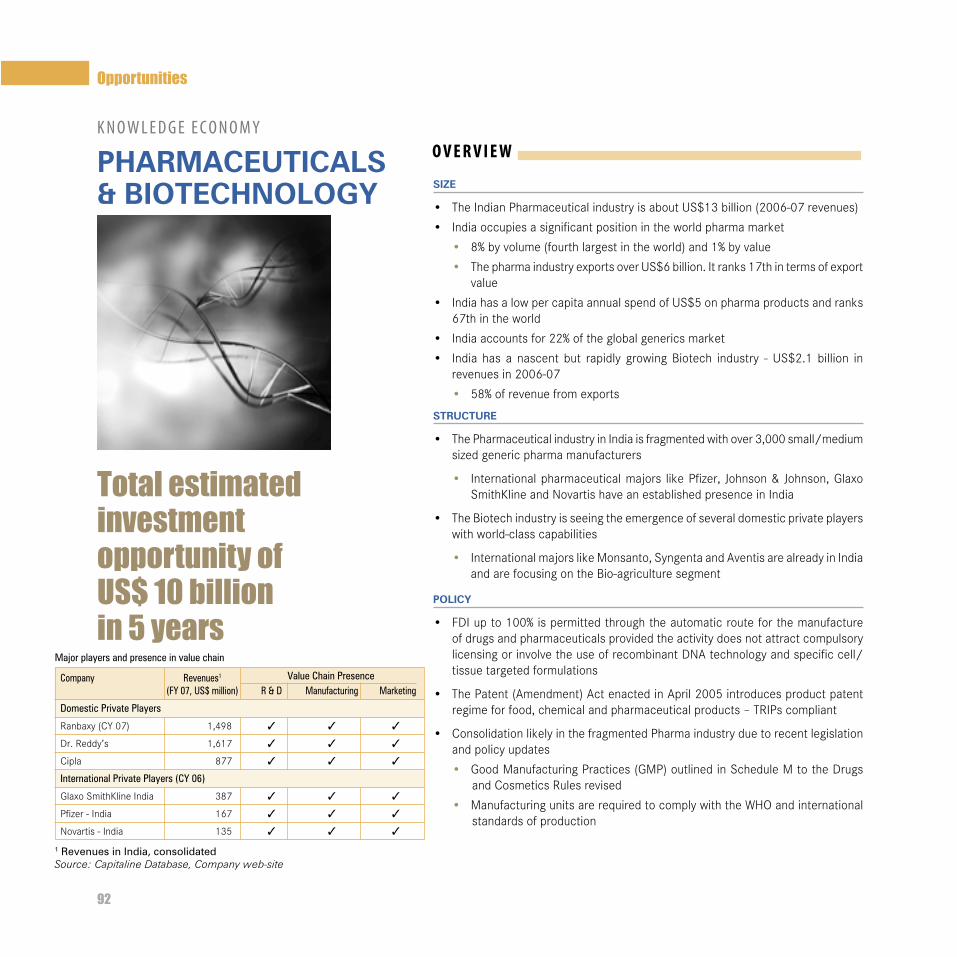

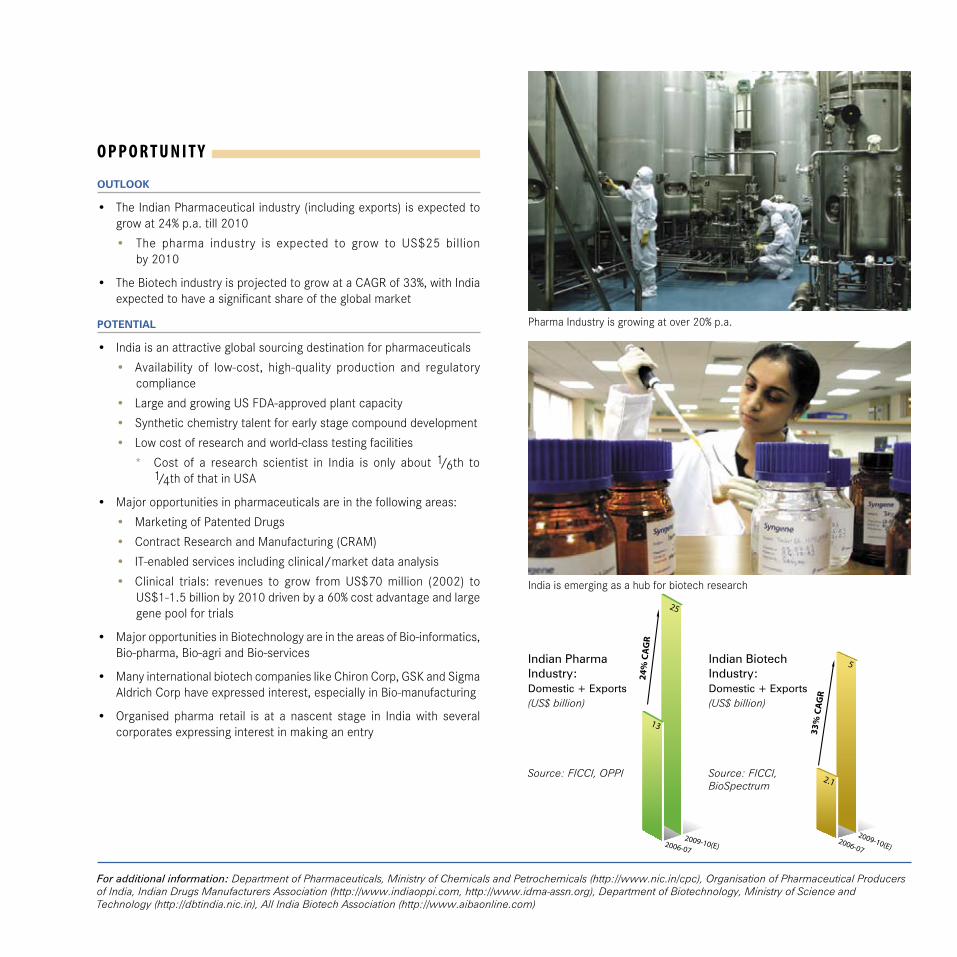

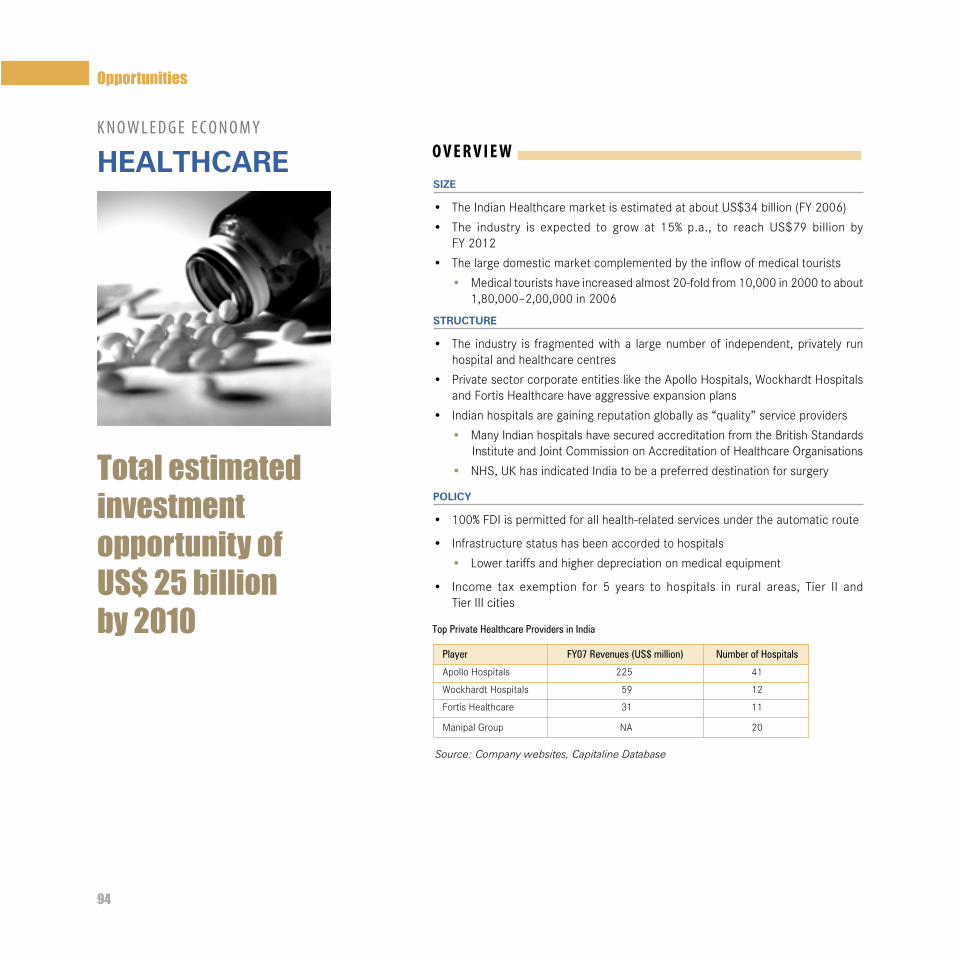

132

India Opportunities in the world’s largest democracy

INVESTMENT COMMISSION

Government of India

www.investmentcommission.in

India

Opportunities in theworld’s largest democracy

C M Y K TATA Invest Commi Cover 1-4.pmd C M Y K TATA Invest Commi Cover 1-4.pmdTATA Invest Commi Cover 1-4.pmd 18/01/2006, 8:11 PM1

India has long been known for the diversity of its culture, for the inclusiveness

of its people and for the convenience of geography. Today, the world’s largest

democracy has come to the forefront as a global resource for industry

in manufacturing and services. Its pool of technical skills, its base of an

English-speaking populace with an increasing disposable income and its

burgeoning market have all combined to enable India emerge as a viable

partner to global industry.

Investment opportunities in India are today perhaps at a peak. Supported by

natural strengths, India offers investment opportunities in excess of US$850

billion in diverse sectors over the next five years.

The Government of India is committed to enabling foreign investors discover

India as a partner - with whom they can work in synergy to achieve their

objectives of growth and profitability.

Welcome to India!

Namaste!

TATA-2734_FDI Brochure_08_Pg no.1 1 8/4/08 5:36:34 PM

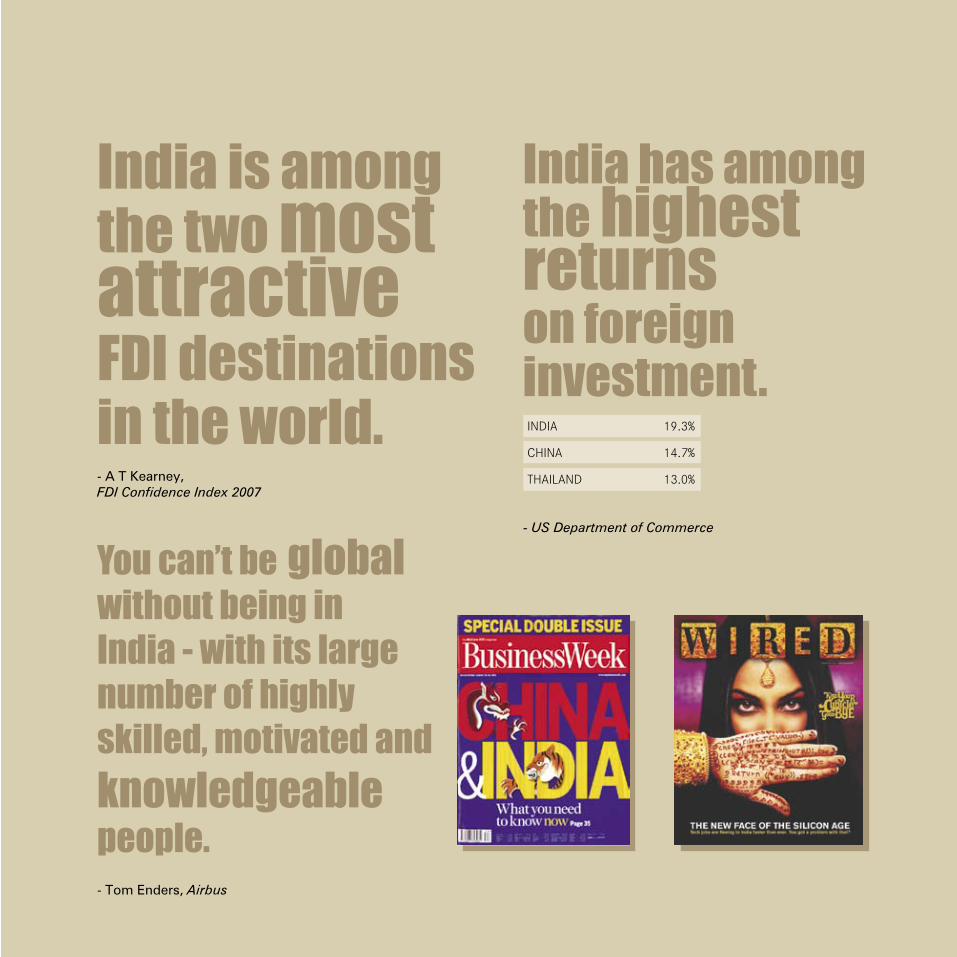

India is amongthe two most attractiveFDI destinationsin the world.

India has among the highest returns on foreign investment.INdIa 19.3%

ChINa 14.7%

ThaIlaNd 13.0%

- US Department of Commerce

- A T Kearney, FDI Confidence Index 2007

You can’t be global without being in India - with its large number of highly skilled, motivated and knowledgeable people.- Tom Enders, Airbus

TATA-2734_FDI Brochure_08_Pg no.2 2 8/4/08 5:36:35 PM

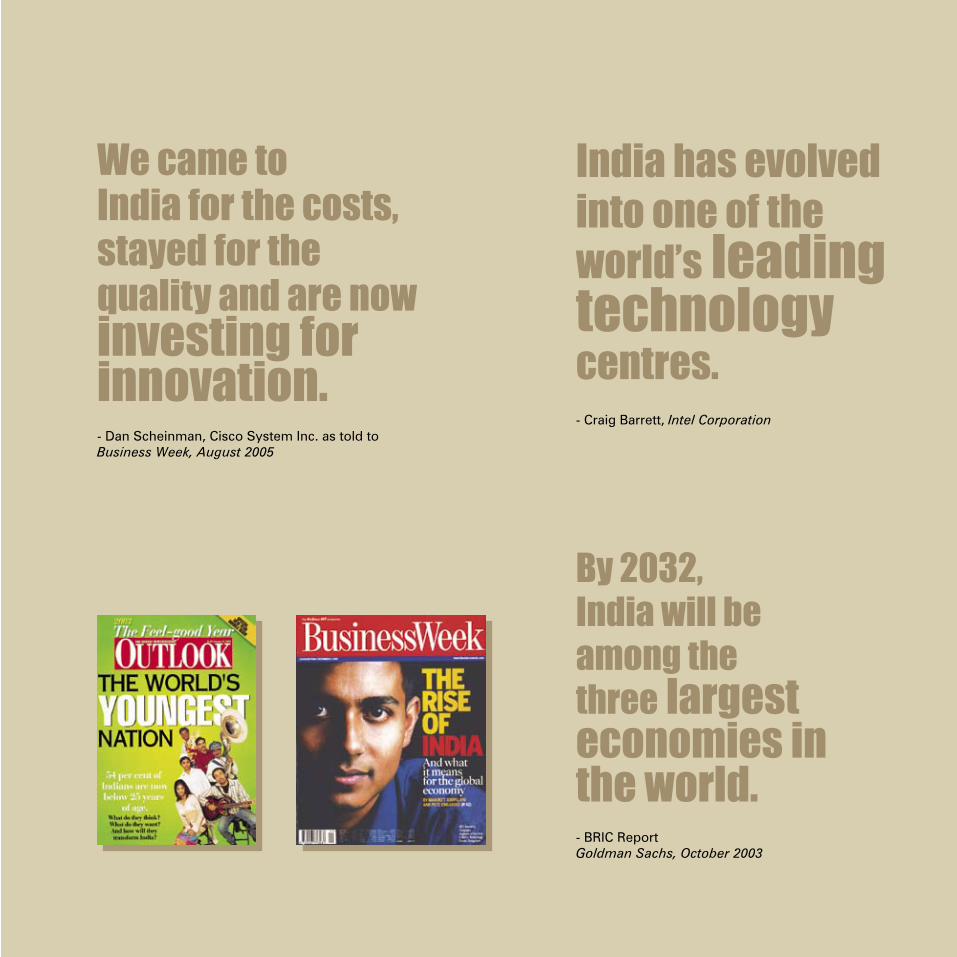

By 2032, India will be among the three largest economies in the world.- BRIC Report Goldman Sachs, October 2003

India has evolved into one of the world’s leading technology centres.- Craig Barrett, Intel Corporation

We came to India for the costs, stayed for the quality and are now investing for innovation.- Dan Scheinman, Cisco System Inc. as told to Business Week, August 2005

TATA-2734_FDI Brochure_08_Pg no.3 3 8/4/08 5:36:36 PM

Floorless trading system at the National Stock Exchange (NSE), India.

TATA-2734_FDI Brochure_08_Pg no.4 4 8/4/08 5:36:38 PM

c o n t e n t s

Destination IndiaINFRaSTRUCTURE Power 30 Telecommunications 32Roads 34Ports 36Civil aviation & airports 38Petroleum & Natural Gas 40Urban Infrastructure 42Infrastructure at a glance (map) 44

SERVICESBanking & Financial Services 48Insurance 50Real Estate & Construction 52Retail 54Tourism 56Tourism at a glance (map) 59

MaNUFaCTURINGMetals: Steel and aluminium 62Textiles & Garments 64Electronics hardware 66Chemicals 68automobiles 70auto Components 72Gems and Jewellery 74Food & agro Products 76Manufacturing at a glance (map) 78

NaTURal RESOURCES Coal 82Metal Ores 84Oil & Gas Exploration 86Resources at a glance (map) 88

KNOWlEdGE ECONOMYPharmaceuticals & Biotechnology 92healthcare 94IT & IT-Enabled Services 96Knowledge Economy at a glance (map) 98

India - the fastest growing free- 07 market democracy

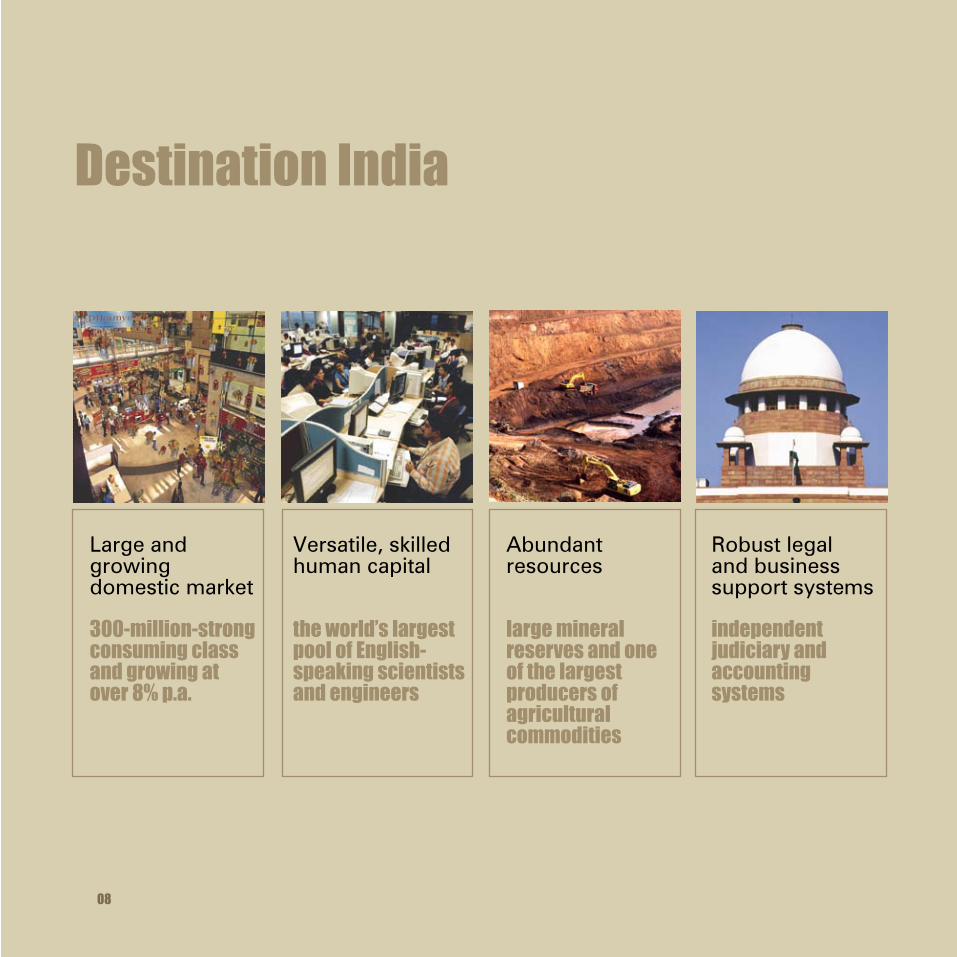

large and growing domestic market 11

Versatile, skilled human capital 12

abundant resources 14

Robust legal & business support systems 16

Sound economic fundamentals 17

Stable economic reform regime 18

healthy, vibrant financial sector 20

Enriched quality of life 21

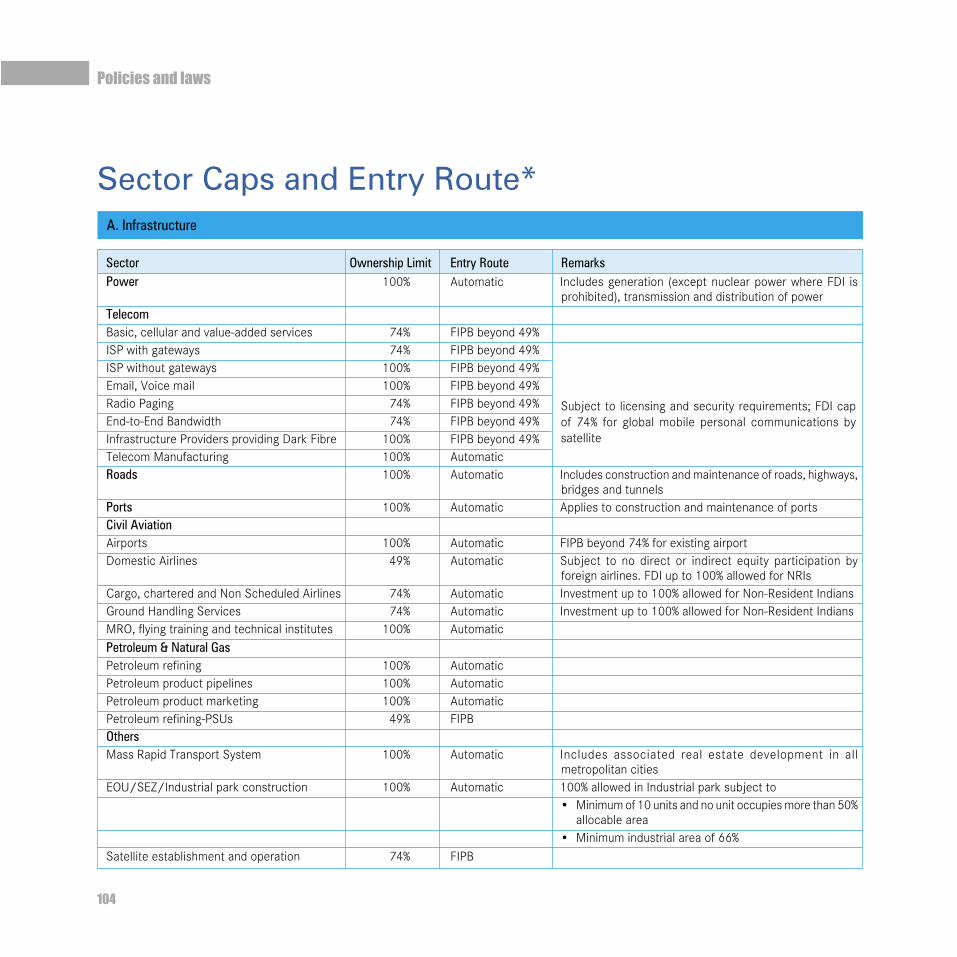

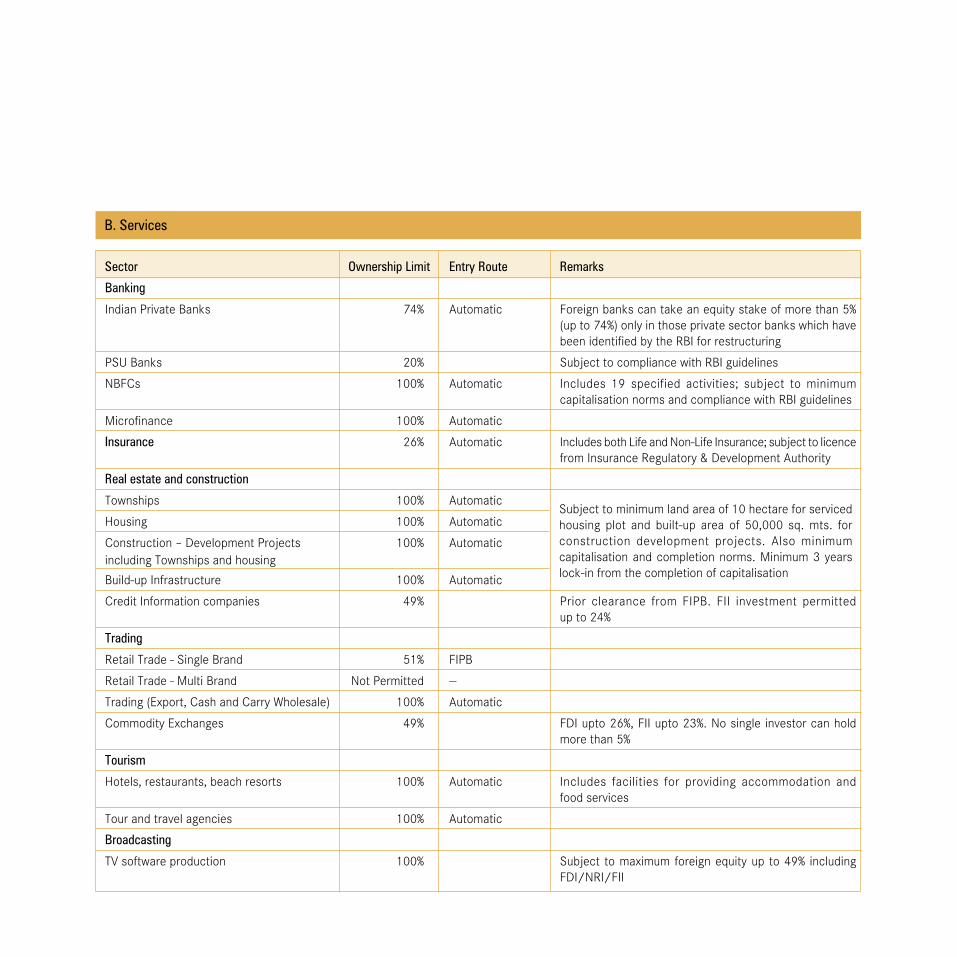

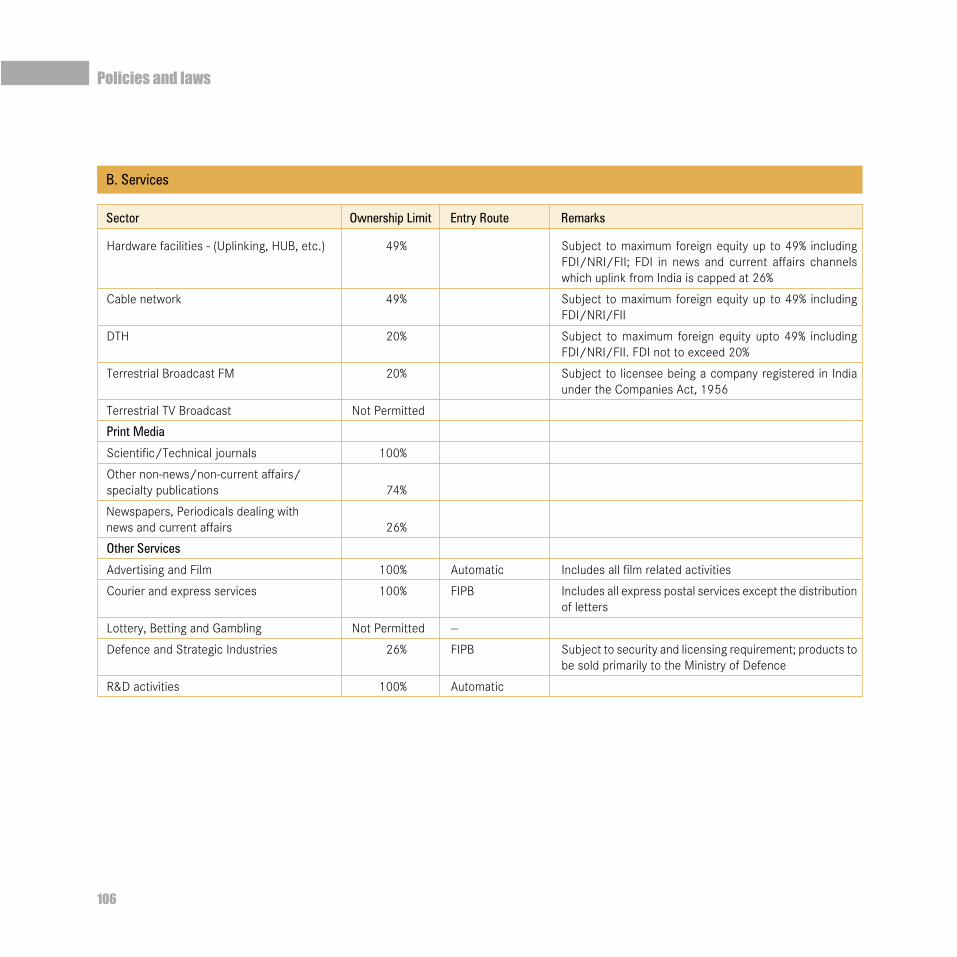

FdI policy overview 102

Sector caps and entry route 104

Entry options for foreign investors 109

Industrial policy 111

Key acts governing foreign investment 112

Important laws governing business 112

Investment facilitation agencies 114

Opportunities Policies and laws01 02

Map of India 118

The Government of India 120

Economic and social indicators 121

Key metros 124

Glossary of Terms and abbreviations 126

03

04General information

TATA-2734_FDI Brochure_08_Pg no.5 5 8/4/08 5:36:39 PM

�

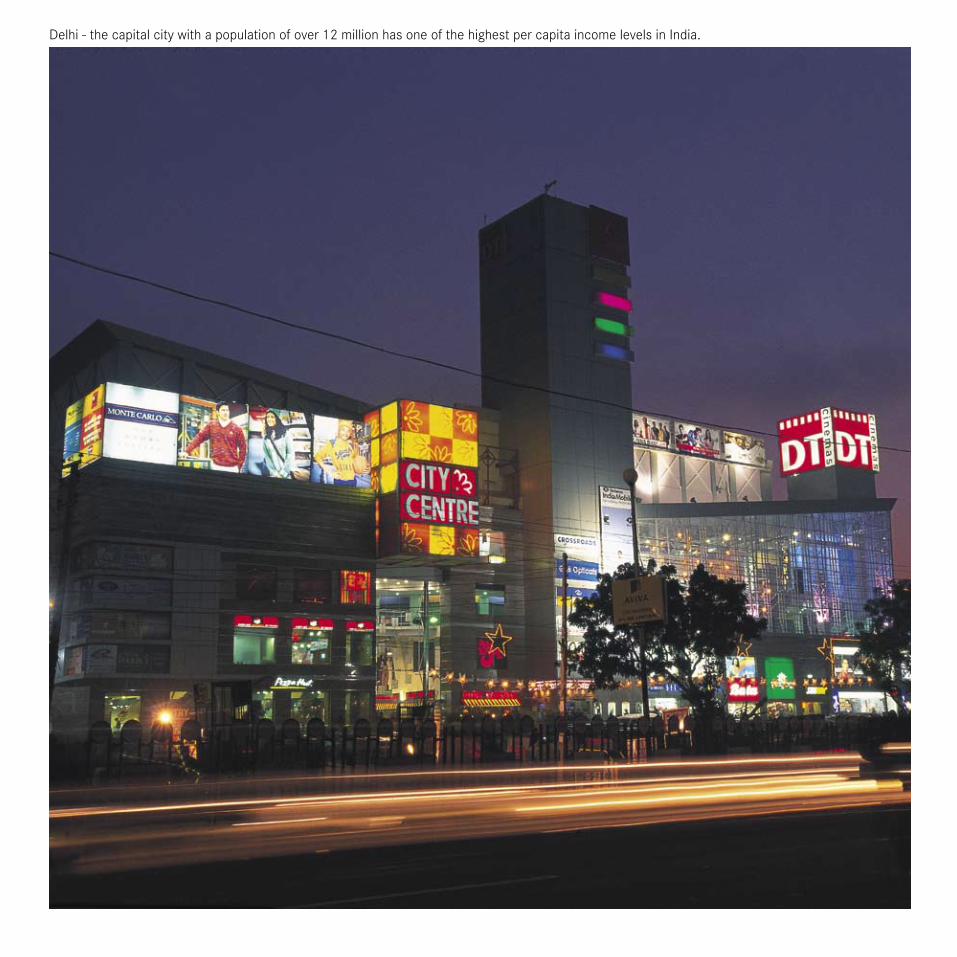

delhi - the capital city with a population of over 12 million has one of the highest per capita income levels in India.

TATA-2734_FDI Brochure_08_Pg no.6 6 8/4/08 5:36:47 PM

GermanyJapanIndiaChinaUS

13.02

10.04

4.244.20

2.57

2003-04

2004-05

2005-06

2006-07

2007-08

8.5

7.5

9.0

9.49.0

India - the fastest growingfree-market democracy

GDP growth of over 8% p.a.expected

Source: Central Statistical Organisation

India’s competitiveness from a natural and human resources standpoint is making it

the destination of choice for investors.

India is a fast-growing economy with a dynamic and robust financial system. Being

a democracy ensures a stable policy environment and its independent institutions

guarantee the rule of law.

This highly diversified economy has shown rapid growth and remarkable resilience

since 1991, when economic reforms were initiated with the progressive opening of

the economy to international trade and investment. Events such as the asian currency

crisis, the dotcom bust and rising oil prices have had no significant impact on India’s

growth, with the economy recording an average annual GdP growth of over 6.5%

in the past decade. Going forward, the country is targeting an average GdP growth

rate of over 8% per annum.

India is in the global arena for increased foreign investment - both through the Equity

markets - termed Foreign Institutional Investment (FII) and Foreign direct Investment

(FdI). While its size and growth potential make India attractive as a market, the most

compelling reason for investors to be in India is that it provides a high return on

investment. India is a free-market democracy with a legal and regulatory framework

that rewards free enterprise, entrepreneurship and risk taking.

GDP (PPP)*(US$ trillion)

Source: World Bank* Purchasing Power Parity

Destination India

One of thefive largesteconomiesin the world

TATA-2734_FDI Brochure_08_Pg no.7 7 8/4/08 5:36:50 PM

Versatile, skilled human capital

the world’s largest pool of English-speaking scientists and engineers

Large and growing domestic market

300-million-strong consuming class and growing at over 8% p.a.

Robust legal and business support systems

independent judiciary and accounting systems

Destination India

08

Abundant resources

large mineral reserves and one of the largest producers ofagricultural commodities

TATA-2734_FDI Brochure_08_Pg no.8 8 8/4/08 5:36:54 PM

Sound economic fundamentals

moderate inflation rate and increasing savings rate

Enriched quality of life

cosmopolitan, multicultural lifestyle

Steady economic reform regime

over a decade and a half of economic reform

Healthy, vibrant financial sector

transparent, modern and well-governed financial sector

TATA-2734_FDI Brochure_08_Pg no.9 9 8/4/08 5:36:57 PM

10

India is experiencing a boom in consumer spending

TATA-2734_FDI Brochure_08_Pg no.10 10 8/4/08 5:37:01 PM

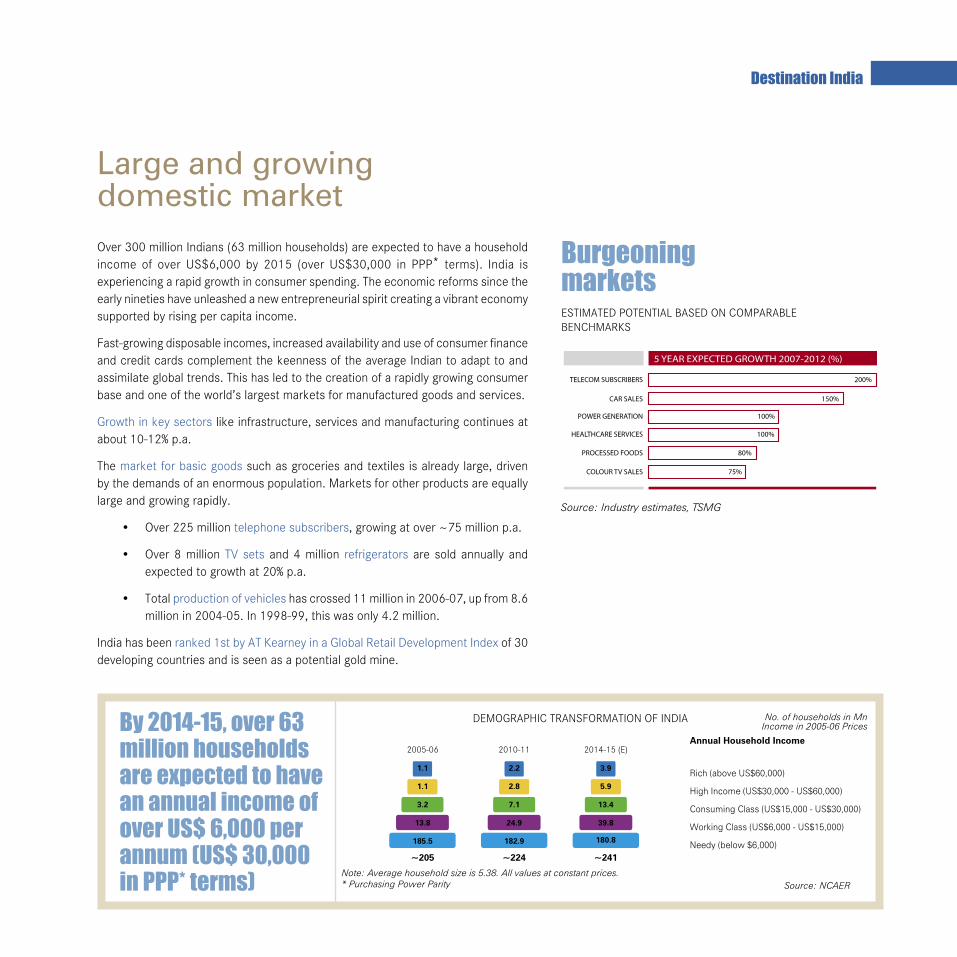

Over 300 million Indians (63 million households) are expected to have a household income of over US$6,000 by 2015 (over US$30,000 in PPP* terms). India is experiencing a rapid growth in consumer spending. The economic reforms since the early nineties have unleashed a new entrepreneurial spirit creating a vibrant economy supported by rising per capita income.

Fast-growing disposable incomes, increased availability and use of consumer finance and credit cards complement the keenness of the average Indian to adapt to and assimilate global trends. This has led to the creation of a rapidly growing consumer base and one of the world’s largest markets for manufactured goods and services.

Growth in key sectors like infrastructure, services and manufacturing continues at about 10-12% p.a.

The market for basic goods such as groceries and textiles is already large, driven by the demands of an enormous population. Markets for other products are equally large and growing rapidly.

• Over 225 million telephone subscribers, growing at over ~75 million p.a.

• Over 8 million TV sets and 4 million refrigerators are sold annually and expected to growth at 20% p.a.

• Total production of vehicles has crossed 11 million in 2006-07, up from 8.6 million in 2004-05. In 1998-99, this was only 4.2 million.

India has been ranked 1st by aT Kearney in a Global Retail development Index of 30 developing countries and is seen as a potential gold mine.

Large and growing domestic market

Destination India

ESTIMaTEd POTENTIal BaSEd ON COMPaRaBlE BENChMaRKS

Source: Industry estimates, TSMG

Burgeoning markets

5 YEAR EXPECTED GROWTH 2007-2012 (%)

TELECOM SUBSCRIBERS

CAR SALES

POWER GENERATION

HEALTHCARE SERVICES

PROCESSED FOODS

COLOUR TV SALES

200%

150%

100%

100%

80%

75%

dEMOGRaPhIC TRaNSFORMaTION OF INdIaBy 2014-15, over �3 million households are expected to have an annual income of over US$ �,000 per annum (US$ 30,000 in PPP* terms) Source: NCAER

Annual Household Income

Rich (above US$60,000)

High Income (US$30,000 - US$60,000)

Consuming Class (US$15,000 - US$30,000)

Working Class (US$6,000 - US$15,000)

Needy (below $6,000)

Note: Average household size is 5.38. All values at constant prices.* Purchasing Power Parity

No. of households in Mn Income in 2005-06 Prices

~205 ~224 ~241

1.1

1.1

3.2

13.8

185.5

2005-06

2.2

2.8

7.1

24.9

182.9

2010-11

3.9

5.9

13.4

39.8

180.8

2014-15 (E)

TATA-2734_FDI Brochure_08_Pg no.11 11 8/4/08 5:37:03 PM

12

IndiaChinaUSA

Japan

43

36

33

25

an unparalleled resource of an educated, hard-working, skilled and ambitious workforce is the

hallmark of India’s human capital.

That this workforce is also one of the world’s youngest adds to India’s attractiveness as an

investment destination. Of the BRIC* countries, India is projected to stay the youngest with its

working-age population estimated to rise to 70% of the total demographic by 2030 - the largest

in the world. India will see 70 million new entrants to its workforce over the next 5 years.

English is the language of business in India and the large English-speaking workforce is a

benefit to investors and employers. In fact, the number of Indians who know English is more

than the population of the USa. India’s diverse cultural heritage puts its citizens at ease with

people from other cultures and vice versa.

With over 380 universities, 11,200 colleges and 1,500 research institutions, India has the second

largest pool of scientists and engineers in the world. Over 2.5 million graduates are added to

the workforce every year, including 300,000 engineers and 150,000 IT professionals.

Versatile, skilled human capital

Median Age (years)

Destination India

Among the world’s youngest nations

Source: The World Fact Book (www.cia.gov)

* Brazil, Russia, India and ChinaChina

Taiwan

USThailandIndia

188

1301

2766

210

89

Labour cost (US$ per month)

Low labour costs

Unit: Monthly salary for manufacturing workers.

Source: CEIC, Morgan Stanley Research

TATA-2734_FDI Brochure_08_Pg no.12 12 8/4/08 5:37:05 PM

In India, over 2.5 million graduates are added to the workforce every year.

TATA-2734_FDI Brochure_08_Pg no.13 13 8/4/08 5:37:06 PM

14

4th largestreserves

(253 Bn T)

Coal

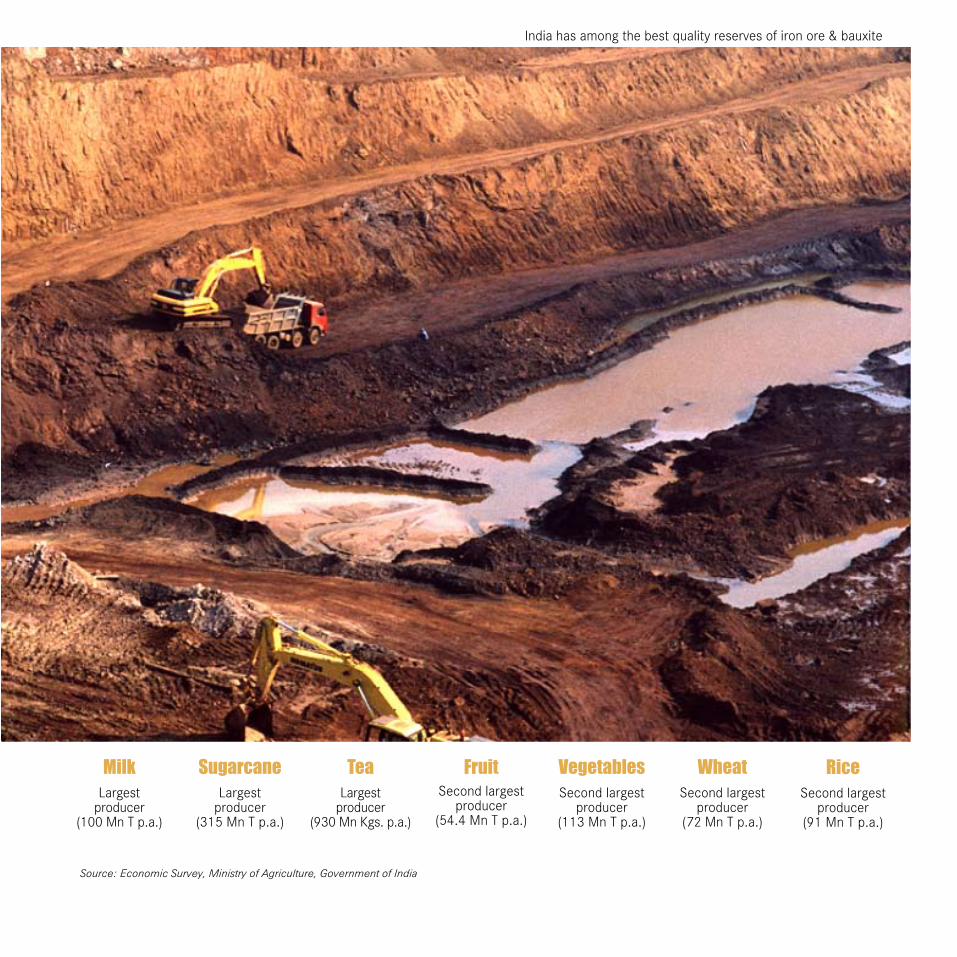

a vast geography endowed with diverse topography has made India the

repository of abundant resources which provides a base for world scale

manufacturing investment.

With an area of 3.3 million square kilometres, India is the seventh largest country in

the world, and the second largest in asia.

India’s reserves of coal, iron ore, manganese, bauxite and chromium are among the

largest in the world. large quantities of mica, titanium ore, chromite, natural gas and

limestone are also to be found in India.

India has the second largest area of arable land in the world, making it one of the

world’s largest food producers - over 200 million tonnes of foodgrains are produced

annually. India is the world’s largest producer of milk, sugarcane and tea and the

second largest producer of rice, fruit and vegetables.

Though an importer of petroleum and natural gas, India has abundant coal reserves

and a large untapped hydroelectric power potential estimated at 150,000 MW.

Abundant resources

Destination India

3rd largest reserves (57 Mn T)

Chromium4th largest reserves

(2.4 Bn T)

Bauxite2nd largest

reserves (240 Mn T)

Manganese

Source: US Geological Survey, Department of Mines, Ministry of Coal, World Fact Book

5th largest reserves (24 Bn T)

Iron Ore

TATA-2734_FDI Brochure_08_Pg no.14 14 8/4/08 5:37:07 PM

Sugarcanelargest

producer(315 Mn T p.a.)

Tealargest

producer(930 Mn Kgs. p.a.)

Second largest producer

(113 Mn T p.a.)

VegetablesSecond largest

producer(72 Mn T p.a.)

WheatFruitSecond largest

producer(54.4 Mn T p.a.)

Source: Economic Survey, Ministry of Agriculture, Government of India

Second largest producer

(91 Mn T p.a.)

Rice

India has among the best quality reserves of iron ore & bauxite

largestproducer

(100 Mn T p.a.)

Milk

TATA-2734_FDI Brochure_08_Pg no.15 15 8/4/08 5:37:07 PM

1�

Robust legal and business support systemsIndia is a free-market democracy with a robust, well-developed legal and administrative

system. The Indian legal system has been derived originally from that of the United

Kingdom and is at par with that of any developed economy.

accounting standards in India are similar to those followed internationally. Many

Indian companies are listed on the NYSE and NaSdaQ and report their results under

US GaaP*.

India has a long history of entrepreneurship, private enterprise and market economics

that dates back to the 19th century. In fact, the Bombay Stock Exchange (BSE) was

set up in 1875.

The original Indian Companies act governing the incorporation and operation of

limited liability companies dates back to 1882, though it has been extensively

updated thereafter.

as a result of the pro-business environment, Indian companies have investments in

most sectors of the economy spanning infrastructure, manufacturing and services.

Several Indian companies conduct their business on a global scale and have worldwide

operations. These, along with numerous companies from the small and medium

enterprise (SME) sector offer considerable scope for joint ventures, collaborations

and partnerships.

India has well-developed support services for business and industry with professional

audit and accounting firms (some are affiliated with international accounting firms)

and qualified corporate law practitioners. Major international advertising companies,

investment banks and consulting firms are also well-represented in India.

Destination India

* Generally accepted accounting Principles

TATA-2734_FDI Brochure_08_Pg no.16 16 8/4/08 5:37:08 PM

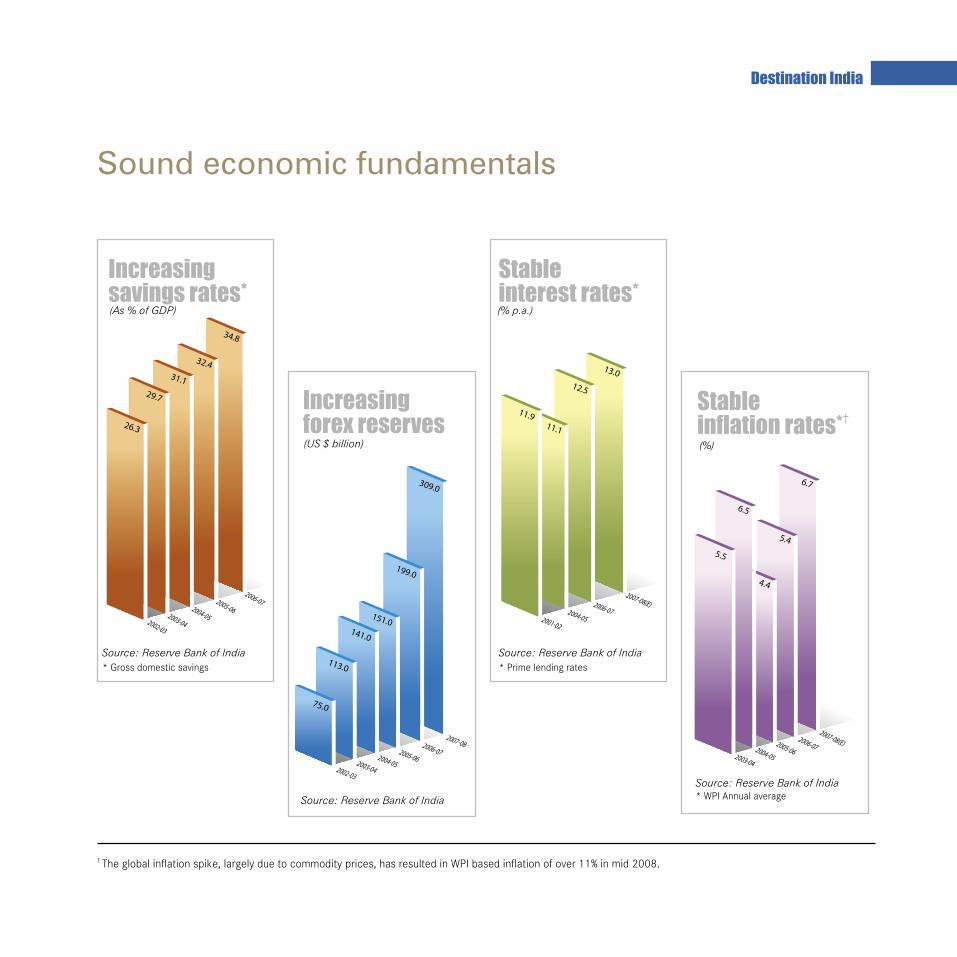

Sound economic fundamentals

Destination India

11.911.1

12.5

13.0

2001-02

2004-05

2006-07

2007-08(E)

Source: Reserve Bank of India* Prime lending rates

Stable interest rates*(% p.a.)

Increasing savings rates*(As % of GDP)

* Gross domestic savings

2002-03

2003-04

2004-05

2005-06

2006-07

32.4

34.8

31.1

29.7

26.3

Source: Reserve Bank of India

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

151.0

199.0

141.0

75.0

113.0

309.0

Increasing forex reserves

Source: Reserve Bank of India

(%)

6.5

5.4

2003-04

2004-05

2005-06

2006-07

2007-08(E)

5.5

6.7

4.4

Stableinflation rates*†

Source: Reserve Bank of India* WPI annual average

(US $ billion)

† The global inflation spike, largely due to commodity prices, has resulted in WPI based inflation of over 11% in mid 2008.

TATA-2734_FDI Brochure_08_Pg no.17 17 8/4/08 5:37:10 PM

Stable economic reform regime

Destination India

Investment friendly policies:• relaxed FDI norms• low tax rates• reduced import duties

after several years of being a largely closed economy, India initiated the process of

opening up its economy in 1991 when it introduced far-reaching economic reforms of

deregulation and liberalisation. These reforms have unlocked India’s enormous growth

potential and unleashed powerful entrepreneurial forces. Since 1991, successive

governments across political parties have successfully carried forward the country’s

economic reform agenda.

during this reform period, India has witnessed increased participation in world trade,

consistent, high economic growth and an increasingly favourable environment for domestic

and foreign investors.

India is a founder member of the GaTT (General agreement on Tariffs and Trade) and is

a signatory to the WTO (World Trade Organisation). India continues to play a significant

role in the current WTO negotiations.

Going forward, infrastructure development is a major focus area and the government is

actively encouraging private investment to bridge the gap. Projects underway include

a ~US$12 billion National highway development Project, the “Sagar Mala” project for

the expansion and modernisation of ports, inland navigation and maritime transport,

the privatisation of Mumbai and delhi airports and development of greenfield airports at

hyderabad and Bengaluru by the private sector.

The Government passed the Special Economic Zones (SEZs) Bill in 2005. SEZs are

treated as deemed foreign territory with no import or export tariffs and extended periods

for waiver of income taxes. Over 130 SEZs have already been formally approved by

the government.

legislation on Intellectual Property Rights (IPRs) has been adopted by the country’s

Parliament. all IPR laws are TRIPS (Trade Related aspects of Intellectual Property Rights)

compliant with a fully functional Intellectual Property appellate Tribunal.

18

TATA-2734_FDI Brochure_08_Pg no.18 18 8/4/08 5:37:11 PM

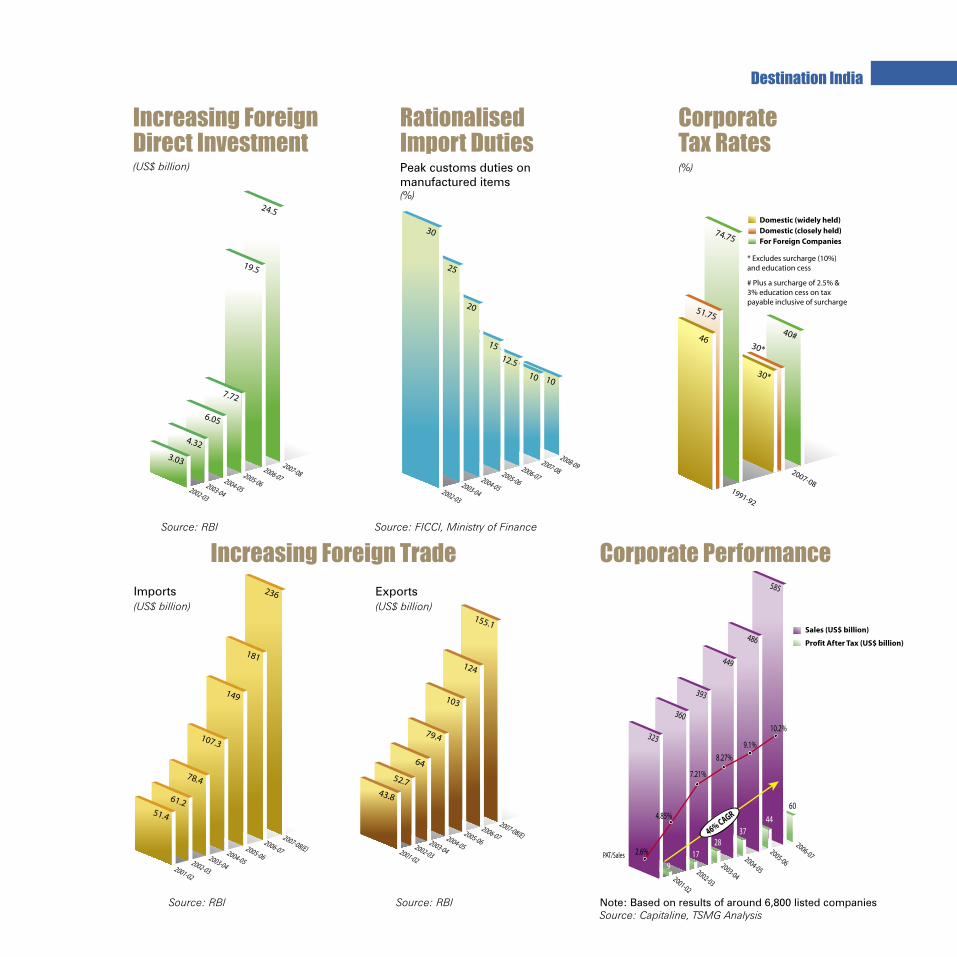

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08(E)

43.8

52.7

64

79.4

103

124

155.1

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08(E)

236

181

149

107.3

78.4

61.251.4

Increasing Foreign Direct Investment(US$ billion) Peak customs duties on

manufactured items (%)

RationalisedImport Duties

Imports(US$ billion)

Exports(US$ billion)

CorporateTax Rates (%)

Source: RBI Source: RBI

Corporate Performance

Note: Based on results of around 6,800 listed companiesSource: Capitaline, TSMG Analysis

Source: RBI

Increasing Foreign Trade

Destination India

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

30

25

20

1512.5

10 10

Source: FICCI, Ministry of Finance

74.75

51.75

4640#

30*

30*

2007-081991-92

* Excludes surcharge (10%) and education cess

# Plus a surcharge of 2.5% & 3% education cess on tax payable inclusive of surcharge

Domestic (widely held)Domestic (closely held)For Foreign Companies

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

24.5

19.5

7.72

6.05

4.32

3.03

917

2837

44

60

7.21%

8.27%

9.1%

Sales (US$ billion)

Profit After Tax (US$ billion)

46% CAGR

323

360

393

449

486

585

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07PAT/Sales 2.6%

10.2%

4.85%

TATA-2734_FDI Brochure_08_Pg no.19 19 8/4/08 5:37:15 PM

20

Destination India

The financial sector in India is characterised by liberal and progressive policies, vibrant

equity and debt markets and prudent banking norms.

India has a transparent, highly technology-enabled and well-regulated stock market

defined by the most modern, nationwide, on-line screen-based trading system

(SBTS), a T+2 rolling settlement system and a market cap of US$1.6 trillion as on

30th december 2007. With the largest number of listed companies - 10,000 - across

23 stock exchanges, India has the third largest investor base in the world.

The country also has a vibrant and modern commodities exchange market ranking

among the top 3 global markets in terms of traded volumes and trades totalling over

US$650 billion in 2006-07. NCdEX, MCX and NMCEI are the major national exchanges

with a diversified portfolio of commodities that include agri-products, bullion, metals

and energy. The exchanges offer future contracts and India was the first to provide

trading in steel futures.

India’s healthy banking system with a network of 70,000 branches is among the

largest in the world. aggregate deposits of commercial banks were about US$445

billion in June 2007 (50% of GdP) and the total bank credit stood at US$320 billion

in June 2007 (36% of GdP). NPa levels of banks in India are under 3%, one of the

lowest among emerging nations. The banking system is Basel I-compliant and moving

towards Basel II norms.

The Reserve Bank of India (RBI), the country’s central bank, has effectively managed

the country’s monetary policy over the last five decades. The country’s current Prime

Minister, dr. Manmohan Singh is a former Governor of the Reserve Bank of India and

a former Finance Minister.

India’s financial sector has been one of the fastest growing sectors in the

economy. It has also witnessed increased private sector activity including an

explosion of foreign banks, insurance companies, mutual funds, venture capital

and investment institutions.

Healthy, vibrant financial sector

India has the largest number of listed companies across 23 Stock Exchanges and the third largest investor base in the world.

TATA-2734_FDI Brochure_08_Pg no.20 20 8/4/08 5:37:16 PM

Enriched quality of life

India offers a multi-cultural, tolerant, inclusive, environment and well-developed social urban

infrastructure with enabling environments for foreigners to settle and do business in the country.

India has five major metros and many large cities that are fast finding a place on the world map.

The capital of India is delhi - a unique amalgam of the modern tree lined avenues of “New”

delhi juxtaposed with the old-world charm of the old city. delhi is the centre of national politics,

international embassies and has one of the highest per capita income levels in India.

Mumbai (formerly Bombay) is the commercial capital of India and one of the largest cities in the

world, supporting a population of over 16 million. It is also the fashion and entertainment capital

of the country.

Bengaluru (formerly Bangalore), known as the Silicon Valley of India is the nerve-centre of the

country’s software industry. It has also gained the reputation of one of the world’s prime Business

Process Outsourcing centres.

Kolkata (formerly Calcutta) is one of the largest metropolitan cities of India with strong cultural and

literary traditions and is home to many old businesses and trading houses.

Chennai (formerly Madras) is a traditional city in South India and with a large industrial base. It is

home to many of India’s engineering and technical enterprises.

India is a country on the move! hotels, clubs, shopping malls, golf courses, theatres, fast-food

chains, fast cars ... all these define the pace, character and modernity of lifestyle in Indian cities.

Indian cuisine is fast gaining popularity all over the world. International cuisines are also widely

available and are received enthusiastically by the local population. Most large Indian cities have

internationally recognised schools and colleges and world-class health care facilities.

In addition to extensive domestic connectivity, India is internationally well-connected by air

and sea. all the major cities are on the international air routes, and international air traffic is

growing rapidly.

Destination India

TATA-2734_FDI Brochure_08_Pg no.21 21 8/4/08 5:37:16 PM

Enriched quality of life in India

TATA-2734_FDI Brochure_08_Pg no.22 22 8/4/08 5:37:22 PM

TATA-2734_FDI Brochure_08_Pg no.23 23 8/4/08 5:37:28 PM

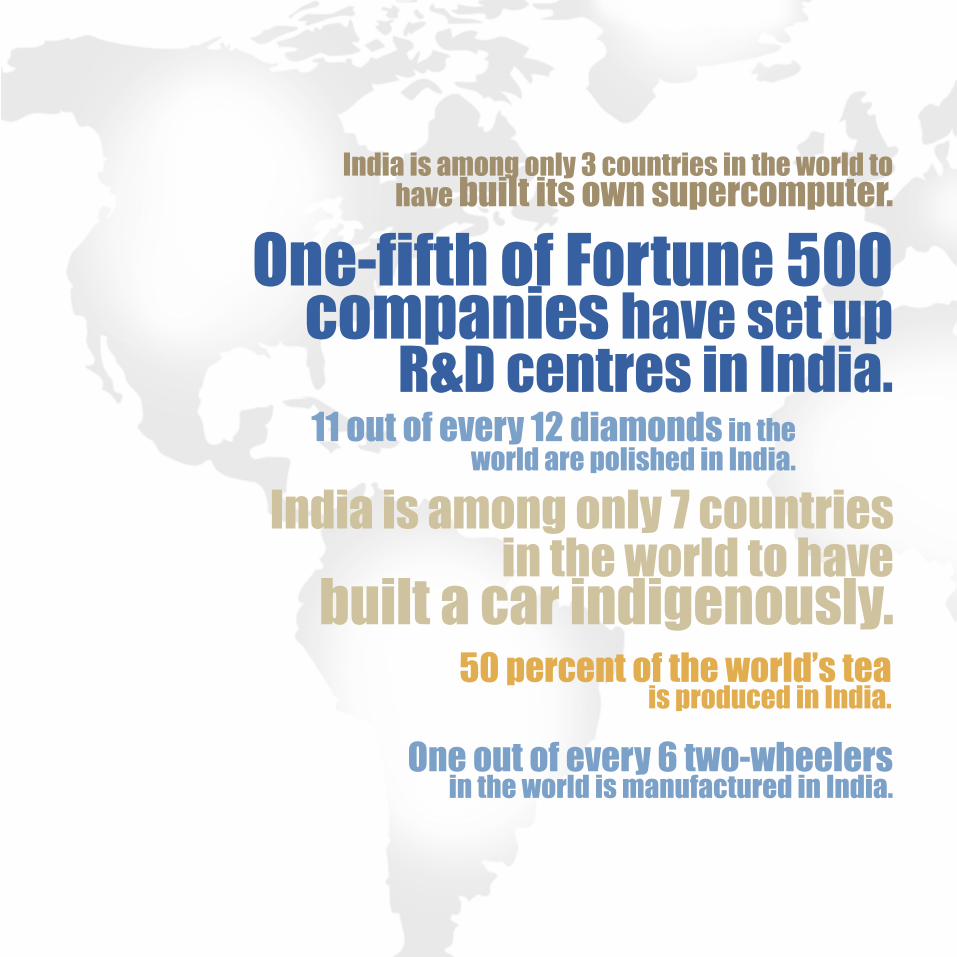

24

One-fifth of Fortune 500 companies have set up

R&D centres in India.

India is among only 3 countries in the world to have built its own supercomputer.

India is among only 7 countriesin the world to have

built a car indigenously.

11 out of every 12 diamonds in the world are polished in India.

50 percent of the world’s teais produced in India.

One out of every � two-wheelers in the world is manufactured in India.

TATA-2734_FDI Brochure_08_Pg no.24 24 8/4/08 5:37:31 PM

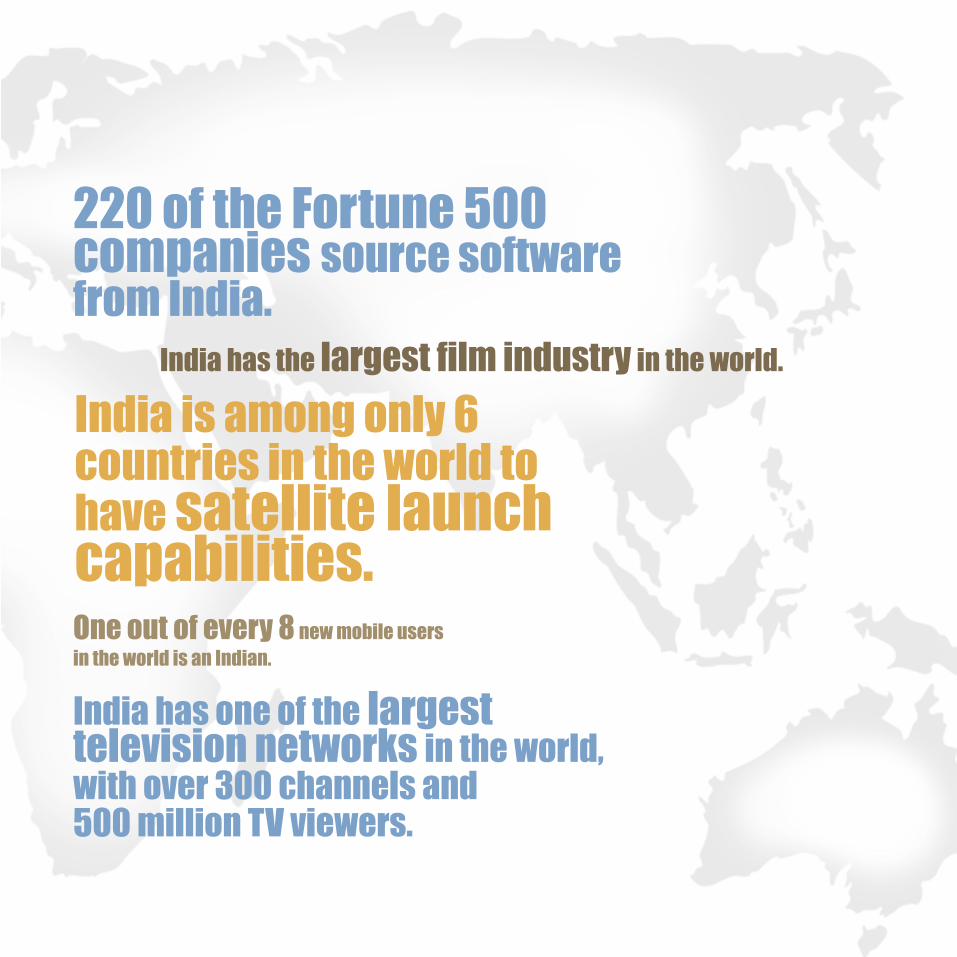

220 of the Fortune 500 companies source software from India.

India is among only � countries in the world to have satellite launch capabilities.One out of every 8 new mobile usersin the world is an Indian.

India has the largest film industry in the world.

India has one of the largesttelevision networks in the world, with over 300 channels and500 million TV viewers.

TATA-2734_FDI Brochure_08_Pg no.25 25 8/4/08 5:37:34 PM

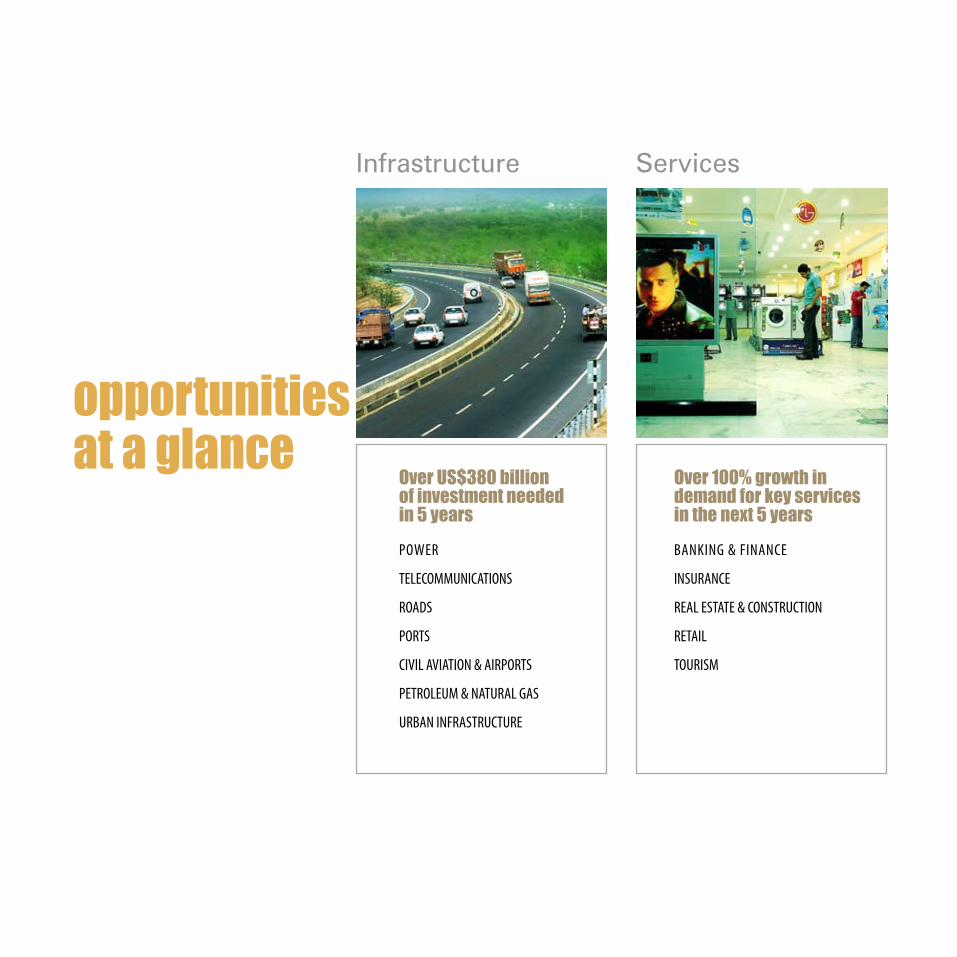

Infrastructure

opportunitiesat a glance

Services

Over US$380 billion of investment needed in 5 years

power

telecommUNIcAtIoNS

roAdS

portS

cIvIl AvIAtIoN & AIrportS

petroleUm & NAtUrAl gAS

UrBAN INFrAStrUctUre

Over 100% growth in demand for key services in the next 5 years

BANkINg & FINANce

INSUrANce

reAl eStAte & coNStrUctIoN

retAIl

toUrISm

TATA-2734_FDI Brochure_08_Pg no.26 26 8/4/08 5:41:32 PM

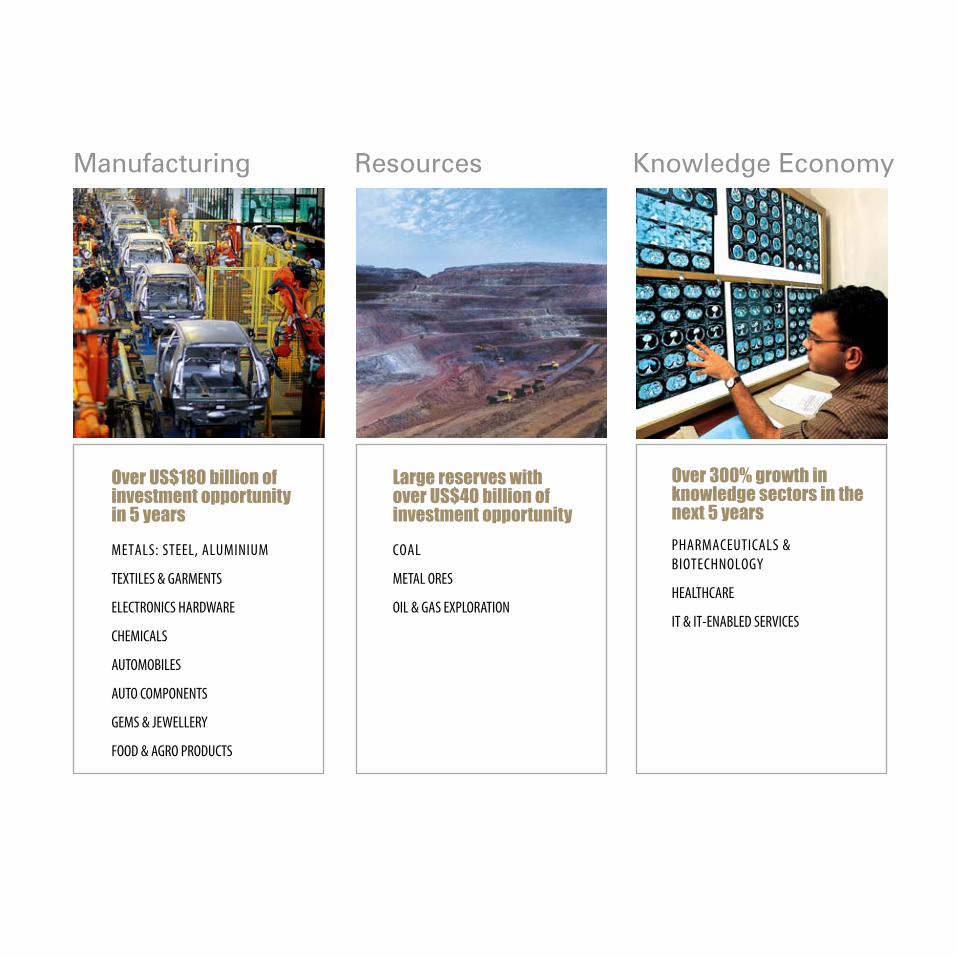

Manufacturing

phArmAceUtIcAlS & BIotechNology

heAlthcAre

It & It-eNABled ServIceS

Knowledge EconomyResources

Over US$180 billion of investment opportunity in 5 years

metAlS: Steel, AlUmINIUm

textIleS & gArmeNtS

electroNIcS hArdwAre

chemIcAlS

AUtomoBIleS

AUto compoNeNtS

gemS & Jewellery

Food & Agro prodUctS

Large reserves with over US$40 billion of investment opportunity

coAl

metAl oreS

oIl & gAS explorAtIoN

Over 300% growth in knowledge sectors in the next 5 years

TATA-2734_FDI Brochure_08_Pg no.27 27 8/4/08 5:41:35 PM

TATA-2734_FDI Brochure_08_Pg no.28 28 8/4/08 5:41:37 PM

• power

• telecommunications

• roads

• ports

• civil Aviation & Airports

• petroleum & Natural gas

• Urban Infrastructure

Infrastructure

TATA-2734_FDI Brochure_08_Pg no.29 29 8/4/08 5:41:37 PM

30

o v e r v i e wSize

• Generation capacity of 141 GW; 663 billion units produced (1 unit=1kwh) -January2008

• CAGRof5%overthelast5years

• Indiahasthefifthlargestelectricitygenerationcapacityintheworld • Lowpercapitaconsumptionat631units;lessthanhalfofChina

• Transmission&Distributionnetworkof6.6millioncircuitkm–thethirdlargestintheworld

• Coalfiredplantsconstitute54%oftheinstalledgenerationcapacity,followedby25%fromhydelpower,10%gasbased,3%fromnuclearenergyand8%fromrenewablesources

Structure

• MajorityofGeneration,TransmissionandDistributioncapacitiesarewitheitherpublicsectorcompaniesorwithStateElectricityBoards(SEBs)

• PrivatesectorparticipationisincreasingespeciallyinGenerationandDistribution • Distributionlicencesforseveralcitiesarealreadywiththeprivatesector • Threelargeultra-megapowerprojectsof4000MWeachhavebeenrecentlyawarded

totheprivatesectoronthebasisofglobaltenders

Policy

• 100%FDIpermittedinGeneration,Transmission&Distribution-theGovernmentiskeentodrawprivateinvestmentintothesector

• Policyframework:ElectricityAct2003andNationalElectricityPolicy2005

• Incentives:Incometaxholidayforablockof10yearsinthefirst15yearsofoperation;waiver of capital goods’ import duties on mega power projects (above 1,000 MWgenerationcapacity)

• IndependentRegulators:CentralElectricityRegulatoryCommissionforcentralPSUsandinter-stateissues.EachstatehasitsownElectricityRegulatoryCommission

Major players and presence in value chainCapacity

(MW) •G •T •D

Public Sector

NationalThermalPowerCorporation 29,144 3

NationalHydroElectricPowerCorporation 2,755 3

NuclearPowerCorporation 4,120 3

Domestic Private Sector

TataPower 2,323 3 3 3

RPGGroup-CESC 975 3 3

RelianceEnergy 941 3 3 3

International Private Sector

ChinaLightandPower(CLP) 655 3

MarubeniCorporation 347 3

I N F r A S t r U c t U r e

Power

Opportunities

Total estimated investment opportunity of US$ 150 billion till 2012

•G-Generation •T-Transmission •D-Distribution

Source: Ministry of Power, Capitaline

TATA-2734_FDI Brochure_08_Pg no.30 30 8/4/08 5:41:38 PM

o p p o r t u n i t y

4.7%

9.7%

105

132

210

2002

2007

2012 (E)

Over150,000MWofHydelPowerisyettobetappedinIndia

outlook

• Over78,000MWofnewgenerationcapacity isplanned in thenextfiveyears

• A corresponding investment is required in Transmission andDistributionnetworks

• Powercostsneedtobereducedfromthecurrenthighof8-10cents/unitbyacombinationof lowerAT&C losses, increasedgenerationefficienciesandaddedlow-costgeneratingcapacity

Potential

• Largedemand-supplygap:AllIndiaaverageenergyshortfallof9%andpeakdemandshortfallof14%

• The implementation of key reforms is likely to foster growth inallsegments

• UnbundlingofverticallyintegratedSEBs

• “OpenAccess”toTransmissionandDistributionnetworks

• Selectdistributioncirclestobefranchised/privatised

• Tariffreformsbyregulatoryauthorities

• OpportunitiesinGenerationfor:

• UltraMegaPowerPlants(UMPP)–9projectsof4000MWeach

• Coal-basedplantsatpitheadorcoastallocations(importedcoal)

• Natural Gas/CNG-based turbines at load centres or neargasterminals

• Hydelpowerpotentialof150,000MWisuntappedasassessedbytheGovernmentofIndia

• Renovation,modernisation,up-ratingandlifeextensionofoldthermalandhydropowerplants

• Opportunities in Transmission network ventures - additional 60,000circuitkmofTransmissionnetworkexpectedby2012

• Private sector participation possible through JV and 100%equitymode

• Total investment opportunity of about US$150 billion over a5-yearhorizon

Indiarequiresanadditional78,000MWofgenerationcapacityby2012

Power Generation Capacity in India(GW)

Source: Ministry of Power

For additional information: Ministry of Power, Central Electricity Regulatory Commission, State Electricity Regulatory Commission (http://powermin.nic.in)

TATA-2734_FDI Brochure_08_Pg no.31 31 8/4/08 5:41:41 PM

o v e r v i e w

32

I N F r A S t r U c t U r e

telecoMMunicationS

Opportunities

Major players and presence in value chain

Total estimated investment opportunity of over US$ 76 billion over the next 5 years

*Launchplanned

Note: 1NationalLongDistance 2InternationalLongDistance

Source: TRAI, DoT, TSMG Analysis

Size

• India is the fifth largest Telecomservicesmarket in theworld;US$23billionrevenuesinFY2007

• Industrygrewbyabout22%inFY2007overFY2006

• 290million subscribers -39million fixed linesand251millionwireless -(February2008)

• Thetelecomsubscriberbasehasgrownatabout40%p.a.overthelast4years

• Wirelesssegmentsubscriberbasegrewat62%p.a.

Structure

• The Indian telecom market has both public and private sector companiesparticipating

• Publicsectorhasover27%subscribermarketshare,downfromover90%in2000

• PrivatecompanieshaveaddedsubscribersataCAGRof80%since2000

• Mobile operators have deployed both CDMA (62 million users) and GSM(189millionusers)wirelessnetworks(February2008)

• Valueaddedservicefeaturesconstituteabout10%ofrevenue(2%in2001)

Policy

• 74%to100%FDIpermittedforvarioustelecomservices

• FIPB approval required for foreign investment exceeding 49% in alltelecomservices

• 100%FDIpermittedintelecomequipmentmanufacturing

• Indiahasatelecompolicythataimstoencourageprivateandforeigninvestment.Highlightsare

• An independent regulator – the Telecom Regulatory Authority ofIndia(TRAI)

• Revenue-sharingmodelforlicencesissuedbytheGovernmentfortelecomservicesinIndia.Unifiedaccesslicencesareavailableforprovidingtelecomservicesonapan-IndiabasisinbothGSM&CDMAtechnologies

• Government has simplified NLD and ILD license norms and loweredentrybarriers

* Newentrantsgiven3yearstosetupinfrastructure

* Entryfeeandnetworthrequirementshavebeenreduced

• PolicyonMobileNumberPortability(MNP)&3Gtobeannouncedshortly

• PolicyonActiveInfrastructureSharingtobeannouncedshortly

• UniversalAccessServiceLicense(UASL)recentlyissuedto5newplayers

Company Services Promoter

Cellular Basic NLD1 ILD2

BhartiAirtel 3 3 3 3 BhartiGroup

RelianceInfocomm 3 3 3 3 RelianceADAGroup

TataTeleservices 3 3 3 3 TataGroup

BSNL 3 3 3 GovernmentofIndia

VodafoneEssar 3 * EssarGroup

IDEACellular 3 * AdityaBirlaGroup

TATA-2734_FDI Brochure_08_Pg no.32 32 8/4/08 5:41:43 PM

o p p o r t u n i t y

outlook

• Indiaisexpectedtobeamongthefastestgrowingtelecommarketsintheworld

• Projectedgrowthof27%p.a.toreach500millionsubscribersbyMarch2010

• Over8millionnewusersareaddedeverymonth–mostlyinwireless

Potential

• Favourable demographics and socio-economic factors leading tohighgrowth

• Growthofdisposableincomecombinedwithchangesinlifestyle

• Increasingaffordability-lowtariffs,easypaymentplansandlow-costhandsets

• Increasedcoverageandavailabilityofmobileservices

• InvestmentopportunityofoverUS$76billionacrossmanyareas

• Networkinfrastructuretoincreaseservicecoverage

• Roll-outofadditionalnetworkfor2G,3G,WIMAXetc.

• Applications/softwareforvoice,dataandbroadcastingservices

• Devices like the mobile handset, set top box, modem, gamingconsole,consumerpremiseequipmentsetc.

• Nokia, Siemens, Alcatel, Lucent, Elcoteq, LG, Ericsson are allinvestinginIndia

Indiawillrequirelargeinvestmentsinnetworkinfrastructure

Over150%growthintelecomsubscribersisprojectedin5years

For additional information: Department of Telecommunications, Ministry of Information Technology & Communications (http://www.dotindia.com), Telecom Regulatory Authority of India (http://www.trai.gov.in)

Mar '10 (E)Mar '07Mar '04Mar '01

36

76

206

500

42.5%

18.3%

7.0%

3.5%

Teledensity

Telephone subscribers (fixed + wireless)(million)

Source: TRAI, Crisinfac

TATA-2734_FDI Brochure_08_Pg no.33 33 8/4/08 5:41:45 PM

o v e r v i e w

34

I N F r A S t r U c t U r e

roadS

Opportunities

Total estimated investment opportunity of US$ 90 billion in 5 years

Size

• Indiahasanextensiveroadnetworkof3.3millionkm–thesecondlargestintheworld

• Roadscarryabout65%ofthefreightand80%ofthepassengertraffic

• Highways/Expresswaysconstituteabout66,000km(2%ofallroads)andcarry40%oftheroadtraffic

• The Government of India plans to spend about US$10 billion p.a. on roaddevelopmentoverthenextfiveyears

• Theambitious7-phaseNationalHighwayDevelopmentProject(NHDP)isIndia’slargestroadprojectever.PhaseII,IIIandIVareunderimplementation

• Keysub-projectsundertheNHDPinclude:

* TheGoldenQuadrilateral(PhaseI:GQ-5846kmof4lanehighways)

* North-South & East-West Corridors (Phase II: NSEW-7300 km of4lanehighways)

• Programfor6-laningofabout6500kmofNationalHighwaysisunderway

Structure

• TheNationalHighwaysAuthorityofIndia(NHAI)istheapexgovernmentbodyforimplementingtheNHDP

• All contracts, whether for construction or BOT, are awarded throughcompetitivebidding

• Privatesectorparticipationisincreasingandisthrough:

• Constructioncontracts

• BOTforabout36%oftotalinvestment-basedoncompetitivebiddingorthelowestlumpsumpaymentfromtheGovernment.

* BOTcontractspermittollingonthosestretchesoftheNHDP

Policy

• 100% FDI under the automatic route is permitted for all road developmentprojects

• Incentives:

• 100%incometaxexemptionforaperiodof10years

• NHAI agreeable to provide grants/viability gap funding for marginalprojects

• Modelconcessionagreementsformulated

the Golden Quadrilateral and nSew projects

Nottoscale

TATA-2734_FDI Brochure_08_Pg no.34 34 8/4/08 5:41:47 PM

o p p o r t u n i t y

outlook

• Annualgrowthprojectedat12-15%forpassengertraffic,and15-18%forcargotraffic

• Over US$90 billion investment is required over the next 5 years toimproveroadinfrastructure

• Roadsectorinvestmentsexpectedtogrowat19%p.a.

Potential

• Road development is recognised as essential to sustain India’seconomicgrowth

• The government is planning to increase expenditure on roaddevelopmentsubstantiallywithfundingalreadyinplacebasedonacessonfuel

• Alargecomponentofhighwaysistobedevelopedthroughpublic-privatepartnerships

• SeveralhightrafficstretchesalreadyawardedtoprivatecompaniesonaBOTbasis

• TwosuccessfulBOTmodelsareinplace–theannuitymodelandtheupfront/lumpsumpaymentmodel

• 40%ofIndia’svillagesdonothaveaccesstoAll-Weatherroads

• Thegovernmenthasidentifiedruralroadsasoneofthe6componentsof theUS$40billionBharatNirmanProgramme to improve ruralIndia

• Investmentopportunitiesexistinarangeofprojectsbeingtenderedby NHAI for implementing the remaining phases of the NHDP– contracts are for construction or BOT basis depending on thesectionbeingtendered.

Roaddevelopmentisaprioritysector

Indiahasthesecondlargestroadnetworkintheworld

For additional information: Planning Commission, Government of India (planningcommission.nic.in), Department of Road Transport and Highways, Ministry of Shipping, Road Transport and Highways (http://morth.nic.in), National Highways Authority of India (http://www.nhai.org)

Anannualgrowthof12-15%forpassengertraffichasbeenprojected

TATA-2734_FDI Brochure_08_Pg no.35 35 8/4/08 5:41:49 PM

o v e r v i e w

36

I N F r A S t r U c t U r e

PortS

Opportunities

Total estimated investment opportunity of US$ 21 billion till 2012

Size

• India’smajorportshandledcargoofover463milliontonnesin2006-07-9.5%increaseoverlastyear

• 80%oftheporttrafficbyvolumeisdryandliquidbulk,remaining20%isgeneralcargo,includingcontainers

• Containerisedcargohasgrownatarateof15%p.a.overthelast5years

• India has 12 major ports and 187 minor ports along 7,517 km long Indiancoastline

• Cargohandledbymajorportshasincreasedby10.4%p.a.overlast3years

• Majorportshandle74%ofthetotaltraffic

• Ofthe12majorports,11portsarerunbyPortTrustswhiletheportatEnnoreisacorporationundertheCentralGovernment

• Twomajorgovernmentprojectsunderway

• Project“Sethusamundram”:DredgingofthePalkStraitinSouthernIndiatofacilitatemaritimetradethroughit

• Project“Sagarmala”:US$22billionprojectforthemodernisationofmajorandminorports

Structure

• GovernmentofIndiadominatedmaritimeactivityinthepast.Policydirectionisnoworientedtoencouragingtheprivatesectortotaketheleadinportdevelopmentandoperations

• Majorportstooperatelargelyaslandlordports-internationalportoperatorshavebeeninvitedtosubmitcompetitivebidsforBOTterminalsonarevenue-sharingbasis

• SignificantinvestmentinportterminalsonBOTbasisbyforeignplayersincludeMaersk(Mumbai),DubaiPortsInternational(Mumbai,Chennai,VizagandKochi),andPSA(Tuticorin,Chennai)

• MinorportsarebeingdevelopedbydomesticandinternationalprivateinvestorsPipavavPortbyMaersk,MundraPortbyAdaniGroup

Policy

• 100%FDIundertheautomaticrouteispermittedforportdevelopmentprojects

• 100%incometaxexemptionforaperiodof10years

• TariffAuthorityofMajorPorts(TAMP)regulatestheceilingfortariffschargedbymajorports/portoperators(notapplicabletominorports)

• AcomprehensiveNationalMaritimeDevelopmentPolicyhasbeenformulatedto facilitate private investment, improve service quality and promotecompetitiveness

Source: Indian Ports Association* Twenty foot equivalent unit (TEU)

Cargo handled by Major Ports in India

Major Port Trade Container Traffic (06-07) (06-07, MMT) (million TEU*)ChennaiPort 53 0.79

CochinPort 15 0.23

Ennore 10.7 —

Haldia 42.4 0.11

JNPT 44.8 3.29

KandlaPort 52.9 0.17

KolkataPort 12.5 0.24

Mormagao 34.2 0.01

MumbaiPort 52.4 0.13

NewMangalorePort 32 0.02

ParadipPort 38.5 0.002

TuticorinPort 18 0.37

VizagPort 56.4 0.05

TATA-2734_FDI Brochure_08_Pg no.36 36 8/4/08 5:41:50 PM

o p p o r t u n i t y

outlook

• Cargohandlingat all theports isprojected togrowat7.7%p.a. till2013-14withminorportsgrowingatafasterrateof8.5%comparedto7.4%forthemajorports

• Traffic at major ports estimated to reach 793 million tonnes by2013-14

• Levelofcontainerisationexpectedtoincreasesignificantlyovercurrentlevelsof15%

• Containerisedcargo is expected togrowat17.3%over thenext 9years

• ExportshavegrownataCAGRof25%p.a.overthelast2yearstoreachUS$124billion

• A large portion of the foreign trade to be through the maritimeroute-95%byvolumeand70%byvalue

• MainlineoperatorstoincreasedirectsailingfrequencytoIndianports

Potential

• Growthinmerchandiseexportsprojectedatover13%p.a.underlinestheneedforlargeinvestmentsinportinfrastructure

• IdentifiedinvestmentneedofUS$12.4billioninthemajorportsunderNationalMaritimeDevelopmentProgram(NMDP)toboostinfrastructureattheseportsinthenext9years

• UnderNMDP,276projectshavebeenidentifiedforthedevelopmentofmajorports

• Public–privatepartnershipisseenbythegovernmentasthekeytoimprovemajorandminorports

* 67%oftheproposedinvestmentinmajorportsenvisagedfromprivateplayers

• Theplanproposesanadditionalporthandlingcapacityof545MMTAfrom2006-07inmajorportsthrough:

• Projects related to port development (construction of jetties,berthsetc.)

• Procurement,replacementorupgradationofportequipment

• Deepeningofchannelstoimprovedraft

• Projectsrelatedtoportconnectivity

• ExpectedinvestmentsofUS$7.7billioninminorports

• FourthterminalatJNPTlikelytoinvolveaninvestmentofUS$1billion

For additional information: Department of Shipping, Ministry of Shipping, Road Transport & Highways (http://shipping.nic.in), Planning Commission, Government of India (planningcommission.nic.in)

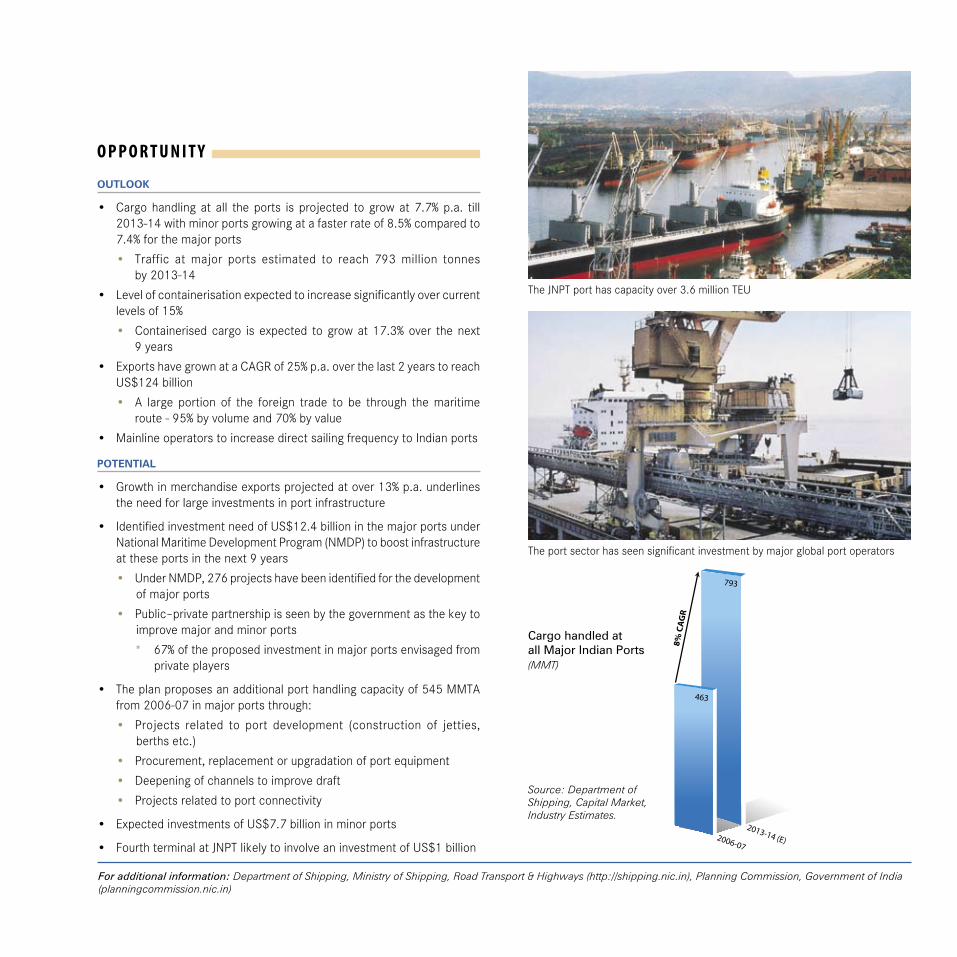

TheJNPTporthascapacityover3.6millionTEU

2013-14 (E)2006-07

463

793

8% C

AG

R

Source: Department of Shipping, Capital Market, Industry Estimates.

Cargo handled at all Major Indian Ports(MMT)

Theportsectorhasseensignificantinvestmentbymajorglobalportoperators

TATA-2734_FDI Brochure_08_Pg no.37 37 8/4/08 5:41:53 PM

o v e r v i e w

38

I N F r A S t r U c t U r e

ciVil aViation & airPortS

Opportunities

Total estimated investment of US$ 8-9 billion by 2012

Size

• Indiahas454airportsandairstrips;ofthese,16aredesignated internationalairports

• In2006-07,Indianairportshandledanestimated95millionpassengersand1.5milliontonnesofcargo

• Passengertrafficgrewinexcessof30%in2006-07over2005-06;cargogrewat11%overthepreviousyear

Structure

• Currently97airportsareownedandoperatedbytheAirportsAuthorityofIndia(AAI)

• Thegovernmentaimstoattractprivateinvestmentinaviationinfrastructure

• MumbaiandDelhiairportshavebeenprivatisedandarebeingupgradedatanestimatedinvestmentofUS$4billionover2006-16

• GreenfieldairportsatBengaluruandHyderabadarebeingbuiltbyprivateconsortiaatatotalinvestmentofoverUS$800million

• SecondgreenfieldairportbeingplannedatNaviMumbai tobedevelopedusingPPPmodeatanestimatedcostofUS$2.5billion

• 35othercityairportsproposedtobeupgraded–citysidedevelopmenttobeundertakenthroughPPPmodewhereaninvestmentofUS$357millionisbeingconsideredoverthenext3years

• Privateairlinesaccountedforover80%ofthedomesticpassengertrafficin2006-07.Somehavestartedinternationalflights

Policy

• 100%FDIispermissibleforairports

• FIPBapprovalrequiredforFDIbeyond74%

• 100%FDIunderautomaticrouteispermissibleforgreenfieldairports

• Private developers allowed to setup captive airstrips and general airports 150kmawayfromanexistingairport.

• 100%taxexemptionforairportprojectsforaperiodof10years

• 49%FDIispermissibleindomesticairlinesundertheautomaticroute,butnotbyforeignairlinecompanies

• 100%equityownershipbyNon-ResidentIndians(NRIs)ispermitted

• 74%FDIpermissibleincargoandnon-scheduledairlines

• TheIndiangovernmentplanstosetupanAirportEconomicRegulatoryAuthoritytoprovidealevelplayingfieldtoallplayers

• The“OpenSky”policyofthegovernmentandrapidairtrafficgrowthhaveresultedintheentryofseveralnewprivatelyownedairlinesandincreasedfrequency/flightsforinternationalairlines

Airport Statistics 2006-07

Source: Director General of Civil Aviation, AAI

Airport Passenger traffic (million, 2006-07)

Bengaluru 8.1

Chennai 8.9

Delhi 20.4

Hyderabad 5.7

Kolkata 5.9

Mumbai 22.2

TATA-2734_FDI Brochure_08_Pg no.38 38 8/4/08 5:41:54 PM

o p p o r t u n i t y

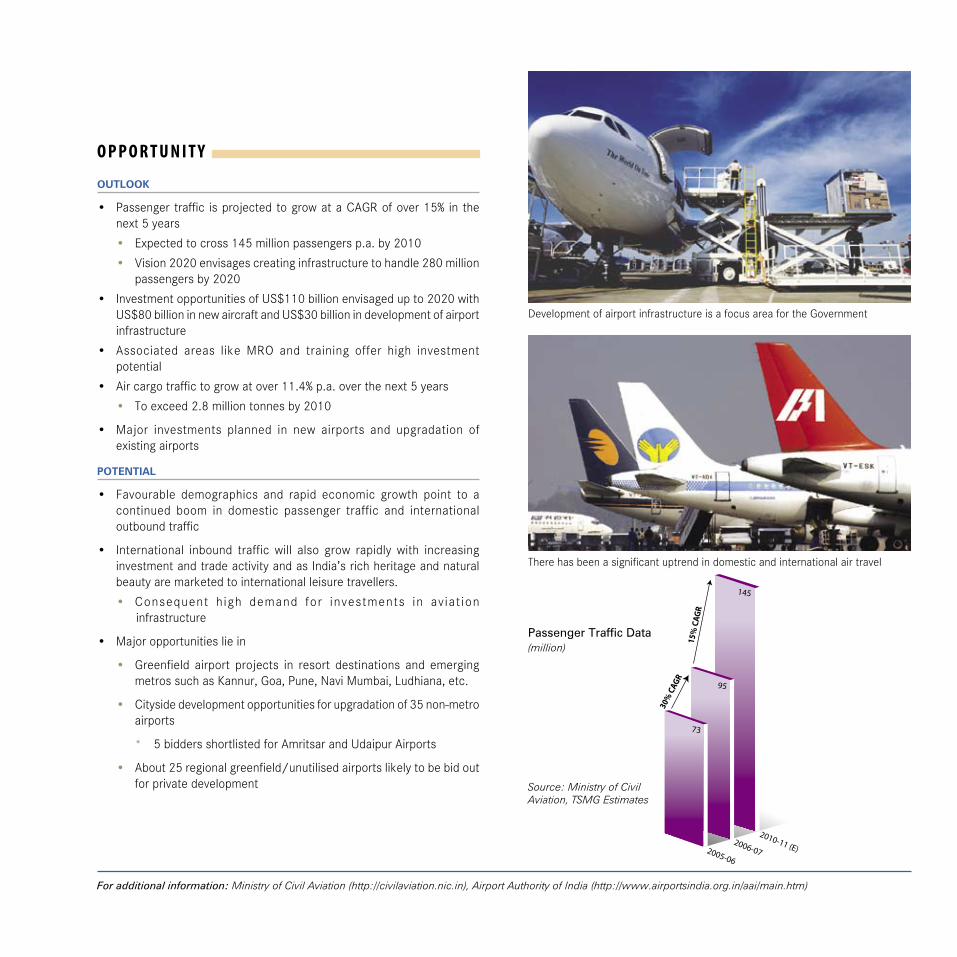

DevelopmentofairportinfrastructureisafocusareafortheGovernment

outlook

• Passengertraffic isprojectedtogrowataCAGRofover15% inthenext5years

• Expectedtocross145millionpassengersp.a.by2010

• Vision2020envisagescreatinginfrastructuretohandle280millionpassengersby2020

• InvestmentopportunitiesofUS$110billionenvisagedupto2020withUS$80billioninnewaircraftandUS$30billionindevelopmentofairportinfrastructure

• Associated areas like MRO and training offer high investmentpotential

• Aircargotraffictogrowatover11.4%p.a.overthenext5years

• Toexceed2.8milliontonnesby2010

• Major investments planned in new airports and upgradation ofexistingairports

Potential

• Favourable demographics and rapid economic growth point to acontinued boom in domestic passenger traffic and internationaloutboundtraffic

• International inbound traffic will also grow rapidly with increasinginvestmentandtradeactivityandasIndia’srichheritageandnaturalbeautyaremarketedtointernationalleisuretravellers.

• Consequent high demand for investments in aviat ioninfrastructure

• Majoropportunitiesliein

• Greenfield airport projects in resort destinations and emergingmetrossuchasKannur,Goa,Pune,NaviMumbai,Ludhiana,etc.

• Citysidedevelopmentopportunitiesforupgradationof35non-metroairports

* 5biddersshortlistedforAmritsarandUdaipurAirports

• About25regionalgreenfield/unutilisedairportslikelytobebidoutforprivatedevelopment

2010-11 (E)2006-072005-06

73

95

145

15%

CAG

R

30%

CAG

R

Source: Ministry of Civil Aviation, TSMG Estimates

Passenger Traffic Data(million)

For additional information: Ministry of Civil Aviation (http://civilaviation.nic.in), Airport Authority of India (http://www.airportsindia.org.in/aai/main.htm)

Therehasbeenasignificantuptrendindomesticandinternationalairtravel

TATA-2734_FDI Brochure_08_Pg no.39 39 8/4/08 5:41:56 PM

o v e r v i e w

40

I N F r A S t r U c t U r e

PetroleuM & natural GaS

Opportunities

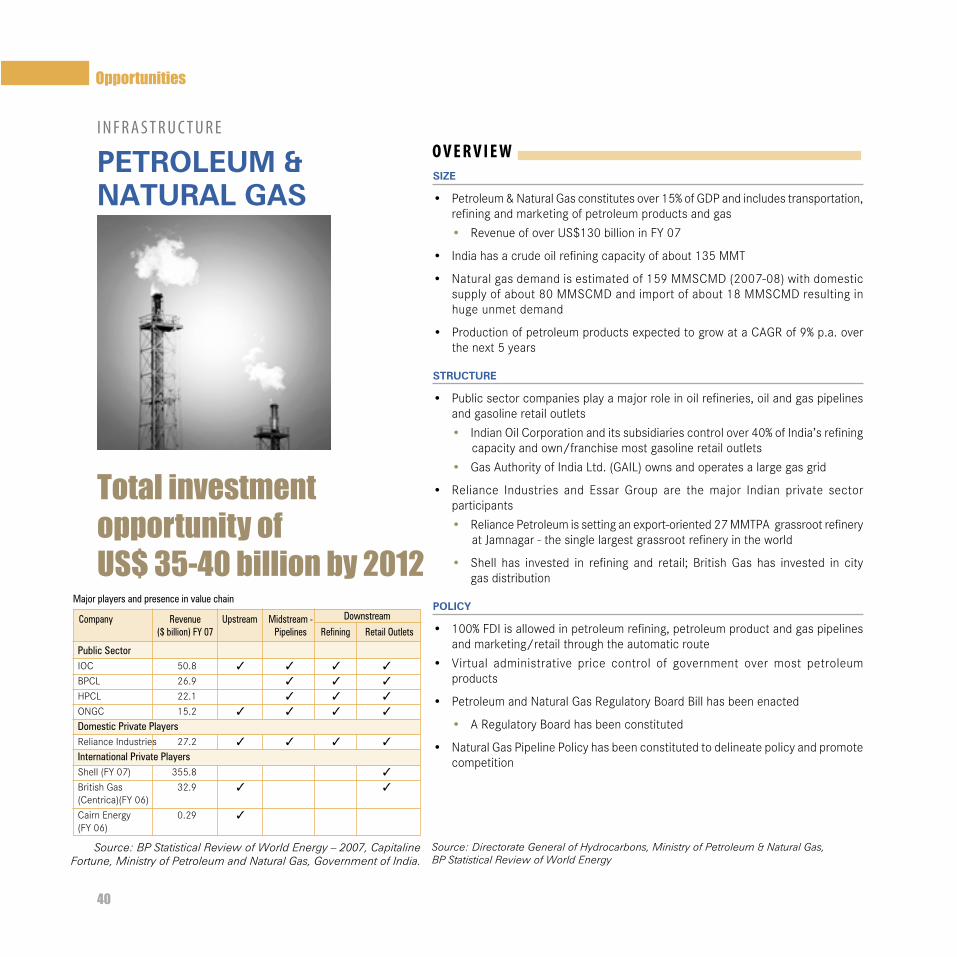

Total investment opportunity of US$ 35-40 billion by 2012

Source: BP Statistical Review of World Energy – 2007, Capitaline Fortune, Ministry of Petroleum and Natural Gas, Government of India.

Major players and presence in value chain

Source: Directorate General of Hydrocarbons, Ministry of Petroleum & Natural Gas, BP Statistical Review of World Energy

Size

• Petroleum&NaturalGasconstitutesover15%ofGDPandincludestransportation,refiningandmarketingofpetroleumproductsandgas

• RevenueofoverUS$130billioninFY07

• Indiahasacrudeoilrefiningcapacityofabout135MMT

• Naturalgasdemandisestimatedof159MMSCMD(2007-08)withdomesticsupplyofabout80MMSCMDandimportofabout18MMSCMDresultinginhugeunmetdemand

• ProductionofpetroleumproductsexpectedtogrowataCAGRof9%p.a.overthenext5years

Structure

• Publicsectorcompaniesplayamajorroleinoilrefineries,oilandgaspipelinesandgasolineretailoutlets

• IndianOilCorporationanditssubsidiariescontrolover40%ofIndia’srefiningcapacityandown/franchisemostgasolineretailoutlets

• GasAuthorityofIndiaLtd.(GAIL)ownsandoperatesalargegasgrid

• Reliance Industries and Essar Group are the major Indian private sectorparticipants

• ReliancePetroleumissettinganexport-oriented27MMTPAgrassrootrefineryatJamnagar-thesinglelargestgrassrootrefineryintheworld

• Shell has invested in refining and retail; British Gas has invested in citygasdistribution

Policy

• 100%FDIisallowedinpetroleumrefining,petroleumproductandgaspipelinesandmarketing/retailthroughtheautomaticroute

• Virtual administrative price control of government over most petroleumproducts

• PetroleumandNaturalGasRegulatoryBoardBillhasbeenenacted

• ARegulatoryBoardhasbeenconstituted

• NaturalGasPipelinePolicyhasbeenconstitutedtodelineatepolicyandpromotecompetition

Public Sector IOC 50.8 3 3 3 3

BPCL 26.9 3 3 3

HPCL 22.1 3 3 3

ONGC 15.2 3 3 3 3

Domestic Private PlayersRelianceIndustries 27.2 3 3 3 3

International Private PlayersShell(FY07) 355.8 3

BritishGas 32.9 3 3(Centrica)(FY06)CairnEnergy 0.29 3

(FY06)

Company Revenue Upstream Midstream - ($ billion) FY 07 Pipelines Refining Retail Outlets

Downstream

TATA-2734_FDI Brochure_08_Pg no.40 40 8/4/08 5:41:58 PM

o p p o r t u n i t y

2011-122007-08

179

279

11.7

% C

AGR

2011-12

159

241

2007-08

10.9

% C

AGR

outlook

• HighGDPgrowthrate,rapidlygrowingvehiclepopulationandbetterroadinfrastructurewilldriveconsumptionofpetroleumproducts

• IndustryisexpectedtohaveCAGRofabout12% • Over92MMTofadditionalrefiningcapacityplannedby2012

• Over100MMSCMDofadditionaldemandforNaturalGasinthenextfouryears

• Recentgasfindsandincreaseduseofgasforpowergeneration,petrochemicals,fertilisersandcitygasdistribution

Potential

• Severalareasofunexploitedpotentialincluding: • Citygasdistribution • LNG(import)infrastructure–terminals,regasification,pipelinesto

industrialconsumers

• Growingdemand-supplymismatchprovidesopportunitiesforinvestmentin the entire value chain for petroleum (refining, product pipelines,storageandretail)andNaturalGas

• Investment need of US$22 billion and US$15 billion estimated inrefiningandthemarketingandgastransportationnetworkrespectivelyby2012

Largegrowthprojectedinfuelretail

For additional information: Ministry of Petroleum & Natural Gas (http://petroleum.nic.in)

Over75MMTofadditionalrefiningcapacityplannedtobeaddedby2012

Crude Oil Refining Capacity(MMTA)

Natural Gas Demand(MMSCMD)

Source: XI Planning Commission Working Group Report

TATA-2734_FDI Brochure_08_Pg no.41 41 8/4/08 5:42:01 PM

o v e r v i e w

42

I N F r A S t r U c t U r e

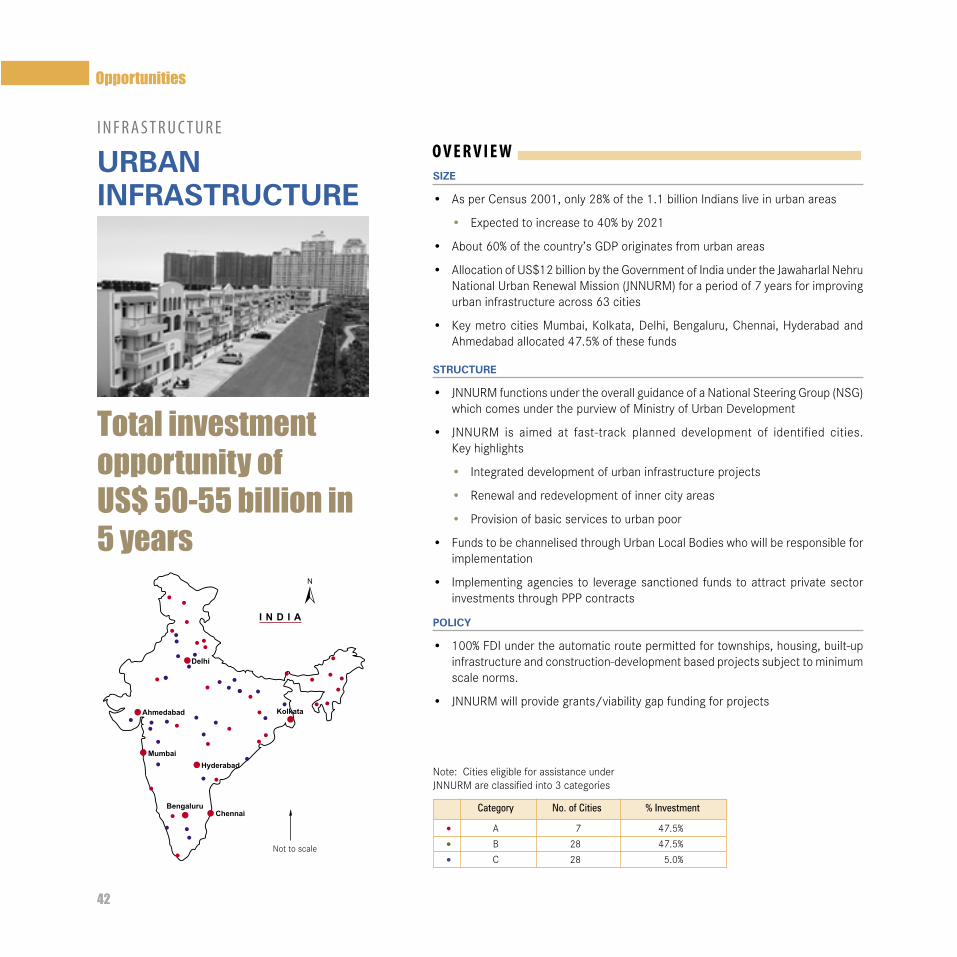

urban infraStructure

Opportunities

Total investment opportunity of US$ 50-55 billion in 5 years

Note: CitieseligibleforassistanceunderJNNURMareclassifiedinto3categories

Size

• AsperCensus2001,only28%ofthe1.1billionIndiansliveinurbanareas

• Expectedtoincreaseto40%by2021

• About60%ofthecountry’sGDPoriginatesfromurbanareas

• AllocationofUS$12billionbytheGovernmentofIndiaundertheJawaharlalNehruNationalUrbanRenewalMission(JNNURM)foraperiodof7yearsforimprovingurbaninfrastructureacross63cities

• KeymetrocitiesMumbai,Kolkata,Delhi,Bengaluru,Chennai,HyderabadandAhmedabadallocated47.5%ofthesefunds

Structure

• JNNURMfunctionsundertheoverallguidanceofaNationalSteeringGroup(NSG)whichcomesunderthepurviewofMinistryofUrbanDevelopment

• JNNURM is aimed at fast-track planned development of identified cities.Keyhighlights

• Integrateddevelopmentofurbaninfrastructureprojects

• Renewalandredevelopmentofinnercityareas

• Provisionofbasicservicestourbanpoor

• FundstobechannelisedthroughUrbanLocalBodieswhowillberesponsibleforimplementation

• Implementingagencies to leveragesanctioned fundstoattractprivatesectorinvestmentsthroughPPPcontracts

Policy

• 100%FDIundertheautomaticroutepermittedfortownships,housing,built-upinfrastructureandconstruction-developmentbasedprojectssubjecttominimumscalenorms.

• JNNURMwillprovidegrants/viabilitygapfundingforprojects

Category No. of Cities % Investment

• A 7 47.5%

• B 28 47.5%

• C 28 5.0%

I N D I A

Delhi

Ahmedabad Kolkata

HyderabadMumbai

BengaluruChennai

N

Nottoscale

TATA-2734_FDI Brochure_08_Pg no.42 42 8/4/08 5:42:03 PM

o p p o r t u n i t youtlook

• InvestmentsofmorethanUS$50billionwouldberequiredinthenext5yearstoimproveandbuildurbaninfrastructure

• JNNURMisthesinglelargestinitiativeofGovernmentofIndiaforplanneddevelopmentofcities

• OpportunityforprivateplayerstopartnerwithUrbanLocalBodies(ULB)indevelopmentofurbaninfrastructuresuchas

• Watersupplyandsanitation

• Slumredevelopment

• Urbantransportationincludingroads,highways,expressways,MassRapidTransportSystem(MRTS)andmetroprojects

• Solidwastemanagement

Potential

• Alargecomponentofdevelopmentworkwillbethroughpublic-privatepartnership

• Watersupplyandsanitationinurbanareastoattract investmentsofoverUS$30billion

• Mumbai is planned to be developed into a international financialcentre

• Thrustondevelopmentoftransportationsystems

• Estimated cost of development is US$40 billion over next10years

• Demandfor1.1millionlow-incomehousesby2015

• Mass Rapid Transport Systems (MRTS) of many major cities suchas Bengaluru, Chennai, Kolkata and Hyderabad are either beingimplementedorexpandedthroughthePPProute

Focusonimprovingurbanroadnetwork

For additional information: Planning Commission, Government of India (planningcommission.nic.in), Ministry of Urban Development (urbanindia.nic.in/), Jawaharlal Nehru National Urban Renewal Mission (http://jnnurm.nic.in)

MajorcitiesareimplementingMetroRailprojects

PotentialforPPPindevelopmentoftransportationinfrastructure

TATA-2734_FDI Brochure_08_Pg no.43 43 8/4/08 5:42:07 PM

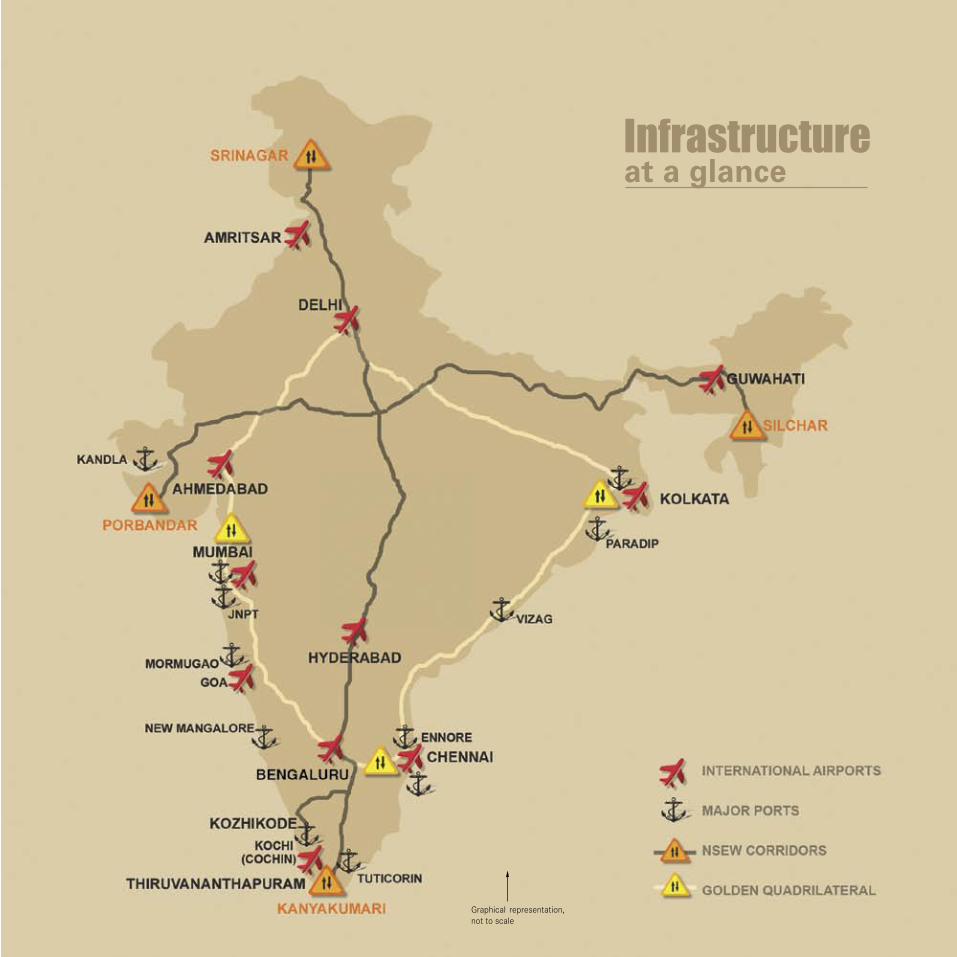

Infrastructure at a glance

Graphical representation,nottoscale

TATA-2734_FDI Brochure_08_Pg no.44 44 8/4/08 5:42:11 PM

New international airports developed in Bengaluru and Hyderabad by private sector led consortia commissioned in 2008

Mumbai & Delhi, the busiest airports in India, have been privatised

JNPT, the biggest container terminal of India, handles 60% of Indian container traffic

Cochin Port is being developed as an international transhipment container terminal

The Golden Quadrilateral and NSEW Corridor with over 13,000 km of four-lane highways is India’s largest roadway project

India will add over 78,000 MW of additional power generation capacity by 2012

TATA-2734_FDI Brochure_08_Pg no.45 45 8/4/08 5:42:12 PM

TATA-2734_FDI Brochure_08_Pg no.46 46 8/4/08 5:42:12 PM

• Banking & Financial Services

• Insurance

• real estate & construction

• retail

• tourism

Services

TATA-2734_FDI Brochure_08_Pg no.47 47 8/4/08 5:42:12 PM

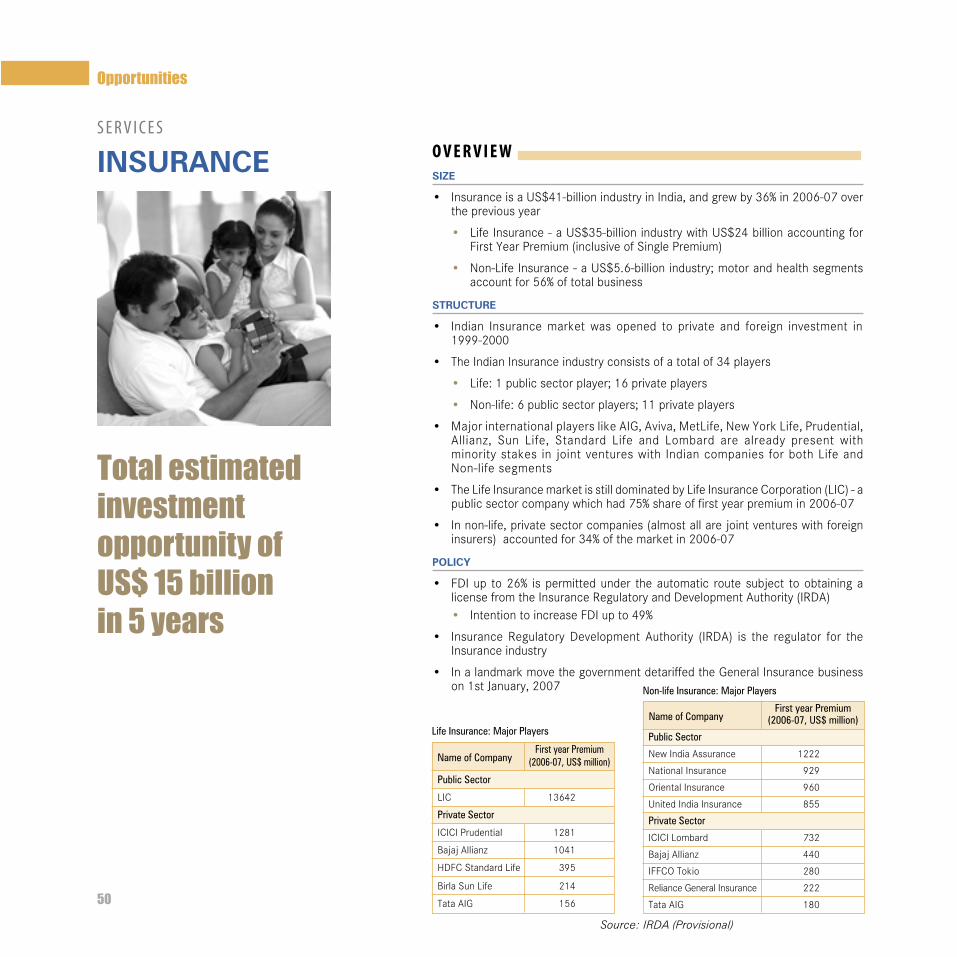

o v e r v i e w

48

S e r v I c e S

bankinG &financial SerViceS

Opportunities

Size

• IndiahasarapidlygrowingBankingandFinancialServicessectorbasedonsoundfundamentals(lowNPAs,BaselIcompliance)

• TotalbankingassetsofaboutUS$816billion in2007:CAGRof24%overlastyear

• Liquidandwellregulatedequitymarkets • Marketcapitalisation(NSE)ofoverUS$1.6billiononDecember2007 • TurnoverhasgrownataCAGRof24%in2007 • MutualfundsassetsundermanagementofUS$130billioninCY2007;growth

of70%overpreviousyear

• 44VentureCapitalandover100PrivateEquityFundsareinIndia

Structure

• Publicsector(government-owned)banksaccountfor75%oftheassets;however,Indianprivatebanksandforeignbanksaregrowingrapidlyandgainingalargershare

• StandardCharteredBank,CitibankandHSBCarethe3largestforeignbanksinIndiawithmorethan65%ofthetotalassetsofforeignbanks

• MostglobalplayersinBanking&FinancialServices–includingGoldmanSachs,MorganStanley,MerrillLynch,JPMorgan,DeutscheBank,UBS,LehmanBrothers,ABNAmro,Barclays,Calyonetc.areactiveinIndia

• TheMutualFundsindustryhasbothdomesticandforeigncompanies-UTIMutualFund,PrudentialICICI,HDFC,FranklinTempleton,BirlaSunLifeMutualFund,TataMutualFund

Policy

• ReserveBankofIndia(RBI),India’scentralbankistheregulatorfortheBankingandFinancialServicesindustry

• HasissuedguidelinesforadoptionofBaselIIbyMarch2008

• RBIapprovalisrequiredforallforeigninvestmentsinthissector • ForeignbankscandobusinessinIndiaeitherbysettingupbranchesorthrough

awhollyownedsubsidiary,afterapprovalbyRBI

• Indianprivatebankscanbe74%foreignowned,witha5%caponownershipbyanyoneentity

Total estimated investment opportunity of US$ 40 billion in 5 years

Source: RBI

Structure of the Indian Banking Industry

Classification of Banks Number of Total Assets (2007) Banks (US$ billion)

PublicSectorBanks 28 575

IndianPrivateBanks 25 175

ForeignBanks 29 48

Total 82 65

TATA-2734_FDI Brochure_08_Pg no.48 48 8/4/08 5:42:13 PM

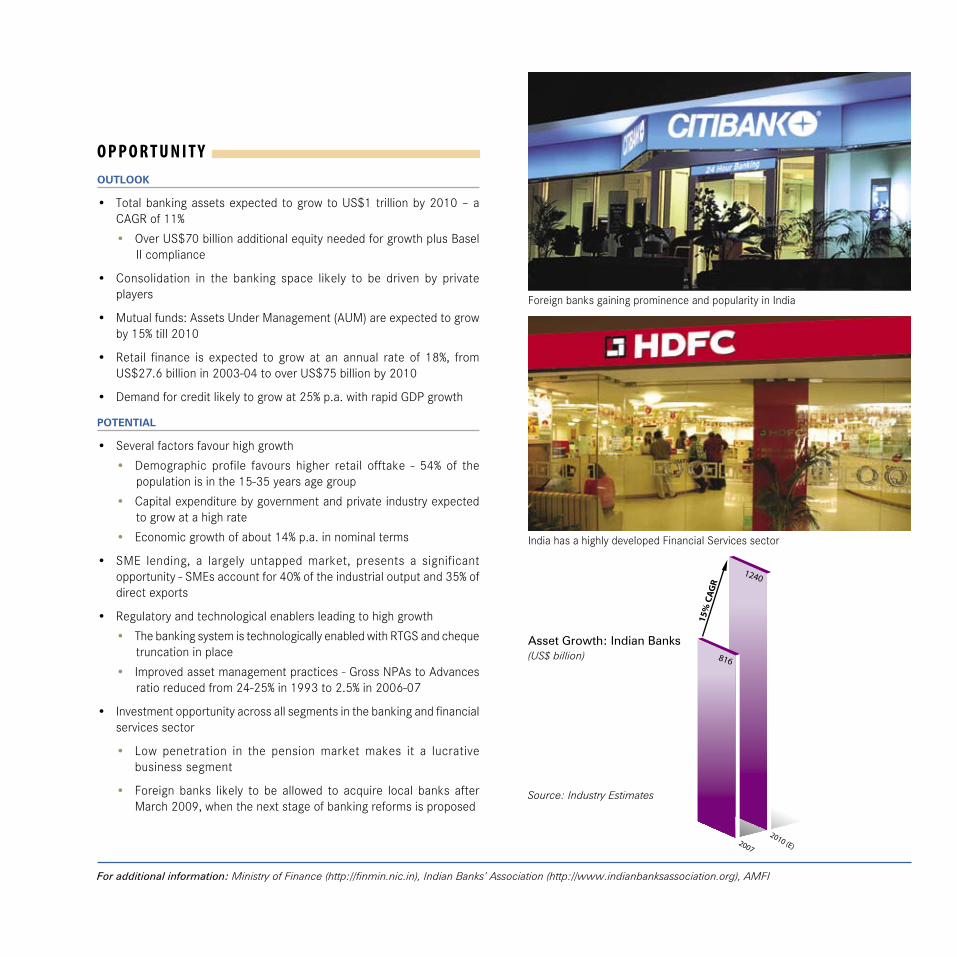

o p p o r t u n i t y

outlook

• Totalbankingassetsexpected togrowtoUS$1trillionby2010–aCAGRof11%

• OverUS$70billionadditionalequityneededforgrowthplusBaselIIcompliance

• Consolidation in the banking space likely to be driven by privateplayers

• Mutualfunds:AssetsUnderManagement(AUM)areexpectedtogrowby15%till2010

• Retail finance is expected to grow at an annual rate of 18%, fromUS$27.6billionin2003-04tooverUS$75billionby2010

• Demandforcreditlikelytogrowat25%p.a.withrapidGDPgrowth

Potential

• Severalfactorsfavourhighgrowth

• Demographic profile favours higher retail offtake - 54% of thepopulationisinthe15-35yearsagegroup

• Capitalexpenditurebygovernmentandprivateindustryexpectedtogrowatahighrate

• Economicgrowthofabout14%p.a.innominalterms

• SME lending, a largely untapped market, presents a significantopportunity-SMEsaccountfor40%oftheindustrialoutputand35%ofdirectexports

• Regulatoryandtechnologicalenablersleadingtohighgrowth

• ThebankingsystemistechnologicallyenabledwithRTGSandchequetruncationinplace

• Improvedassetmanagementpractices-GrossNPAstoAdvancesratioreducedfrom24-25%in1993to2.5%in2006-07

• Investmentopportunityacrossallsegmentsinthebankingandfinancialservicessector

• Low penetration in the pension market makes it a lucrativebusinesssegment

• Foreign banks likely to be allowed to acquire local banks afterMarch2009,whenthenextstageofbankingreformsisproposed

ForeignbanksgainingprominenceandpopularityinIndia

IndiahasahighlydevelopedFinancialServicessector

For additional information: Ministry of Finance (http://finmin.nic.in), Indian Banks’ Association (http://www.indianbanksassociation.org), AMFI

Source: Industry Estimates

Asset Growth: Indian Banks(US$ billion) 816

1240

15%

CA

GR

2007

2010 (E)

TATA-2734_FDI Brochure_08_Pg no.49 49 8/4/08 5:42:15 PM

o v e r v i e w

50

S e r v I c e S

inSurance

Opportunities

Total estimated investment opportunity of US$ 15 billion in 5 years

Source: IRDA (Provisional)

Size

• InsuranceisaUS$41-billionindustryinIndia,andgrewby36%in2006-07overthepreviousyear

• LifeInsurance-aUS$35-billionindustrywithUS$24billionaccountingforFirstYearPremium(inclusiveofSinglePremium)

• Non-LifeInsurance-aUS$5.6-billionindustry;motorandhealthsegmentsaccountfor56%oftotalbusiness

Structure

• Indian Insurance market was opened to private and foreign investment in1999-2000

• TheIndianInsuranceindustryconsistsofatotalof34players

• Life:1publicsectorplayer;16privateplayers

• Non-life:6publicsectorplayers;11privateplayers

• MajorinternationalplayerslikeAIG,Aviva,MetLife,NewYorkLife,Prudential,Allianz, Sun Life, Standard Life and Lombard are already present withminoritystakes in jointventureswith IndiancompaniesforbothLifeandNon-lifesegments

• TheLifeInsurancemarketisstilldominatedbyLifeInsuranceCorporation(LIC)-apublicsectorcompanywhichhad75%shareoffirstyearpremiumin2006-07

• Innon-life,privatesectorcompanies(almostallarejointventureswithforeigninsurers)accountedfor34%ofthemarketin2006-07

Policy

• FDIup to26% ispermittedunder theautomatic routesubject toobtainingalicensefromtheInsuranceRegulatoryandDevelopmentAuthority(IRDA)

• IntentiontoincreaseFDIupto49%

• Insurance Regulatory Development Authority (IRDA) is the regulator for theInsuranceindustry

• InalandmarkmovethegovernmentdetariffedtheGeneralInsurancebusinesson1stJanuary,2007 Non-life Insurance: Major Players

First year Premium (2006-07, US$ million)

Public Sector

NewIndiaAssurance 1222

NationalInsurance 929

OrientalInsurance 960

UnitedIndiaInsurance 855

Private Sector

ICICILombard 732

BajajAllianz 440

IFFCOTokio 280

RelianceGeneralInsurance 222

TataAIG 180

Name of CompanyLife Insurance: Major Players

Name of Company First year Premium (2006-07, US$ million)

Public Sector

LIC 13642

Private Sector

ICICIPrudential 1281

BajajAllianz 1041

HDFCStandardLife 395

BirlaSunLife 214

TataAIG 156

TATA-2734_FDI Brochure_08_Pg no.50 50 8/4/08 5:42:17 PM

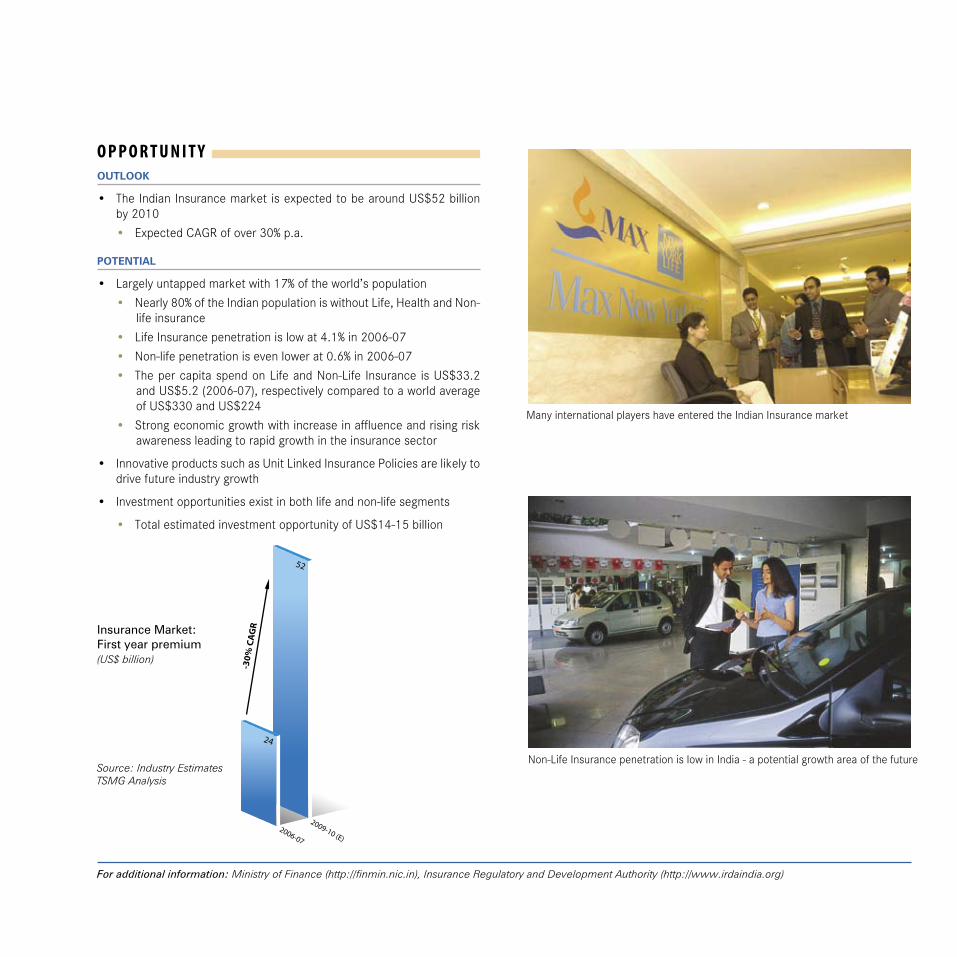

o p p o r t u n i t youtlook

• TheIndianInsurancemarketisexpectedtobearoundUS$52billionby2010

• ExpectedCAGRofover30%p.a.

Potential

• Largelyuntappedmarketwith17%oftheworld’spopulation • Nearly80%oftheIndianpopulationiswithoutLife,HealthandNon-

lifeinsurance • LifeInsurancepenetrationislowat4.1%in2006-07 • Non-lifepenetrationisevenlowerat0.6%in2006-07 • ThepercapitaspendonLifeandNon-Life Insurance isUS$33.2

andUS$5.2(2006-07),respectivelycomparedtoaworldaverageofUS$330andUS$224

• Strongeconomicgrowthwithincreaseinaffluenceandrisingriskawarenessleadingtorapidgrowthintheinsurancesector

• InnovativeproductssuchasUnitLinkedInsurancePoliciesarelikelytodrivefutureindustrygrowth

• Investmentopportunitiesexistinbothlifeandnon-lifesegments

• TotalestimatedinvestmentopportunityofUS$14-15billion

ManyinternationalplayershaveenteredtheIndianInsurancemarket

52

24

-30%

CA

GR

2006-07

2009-10 (E)

Insurance Market:First year premium(US$ billion)

Source: Industry Estimates TSMG Analysis

For additional information: Ministry of Finance (http://finmin.nic.in), Insurance Regulatory and Development Authority (http://www.irdaindia.org)

Non-LifeInsurancepenetrationislowinIndia-apotentialgrowthareaofthefuture

TATA-2734_FDI Brochure_08_Pg no.51 51 8/4/08 5:42:19 PM

o v e r v i e w

52

S e r v I c e S

real eState & conStruction

Opportunities

Size

• RealEstateandConstructionisaUS$16-billion(2006)industryinIndia

• Therehasbeenarapidgrowthintheindustryinthepastfewyears

• Realestateshare in totalFDI increased from10% in2004-05toover25% in2006-07(estimatedatoverUS$5billion)

• High-demandgrowthhasledtopricesdoublingover3yearsinmanycities

Structure

• Fragmentedsectorwithrelativelyfeworganisedplayersofscale

• Largecorporationsbeginningtoshowactiveinterest

• Margins are higher in India (>20%) as compared to the developedmarkets(5-6%)

• Activeparticipationofinstitutionalfinanceinrealestate

• Realestateventurefundspermitted:ProminentIndiancorporateslikeTataGroup,ICICIBank,SBIandHDFChavepromotedrealestateventurefunds

• RealestateInvestmentTrusts(REITs)expectedtobesetupshortly.

• SeveralPrivateEquityfirmshavespecificfundsforrealestateinvestments.RealestatefastdisplacingIT/ITeSasthetopprivateequityinvestmentsectorinIndia

• Various foreign real estate and finance companies such as GE CommercialFinance,TishmanSpeyer,AscendasandFarallonCapital,GoldmanSachs,LehmanBrothersetc.haveenteredtheIndianmarket

Policy

• 100%FDIisallowedinrealestatedevelopmentsubjecttominimumscalenormsofeither:

• 25acresincaseofservicedplotsorintegratedtownships;or

• 50,000sq.mtrs.ofbuilt-upareaforconstructiondevelopmentprojects

• Initialinvestmentislocked-infora3yearperiod

Top Players in the Real Estate & Construction industry

Investment opportunity of over US$ 70-75 billion in the next 5 years

Company Sales Turnover (2007, US$ million)

Unitech 784

DLFLtd. 590

HDIL 286

AnsalProperties 190

Source: Capitaline, Business Press

TATA-2734_FDI Brochure_08_Pg no.52 52 8/4/08 5:42:21 PM

o p p o r t u n i t y

outlook

• TherealestatemarketisprojectedtogrowtoUS$60billionby2010ataCAGRof40%

• Realestatecompanieshavebeensuccessfully tappingthecountry’sboomingcapitalmarketsforfunds

• Companies have also raised equity internationally at the AIMinLondon

• Tier 2 cities (non-metros) likely to experience faster growth in thefuture

Potential

• Several factors are expected to contribute to the rapid growth inrealestate

• Large demand-supply gap in affordable housing, with demandbeing fuelled by tax incentives and a growing middle class withhighersavings

• IncreasingdemandforcommercialandofficespaceespeciallyfromtherapidlygrowingRetail,IT/ITeSandHospitalitysectors

• The recently announced JNNURM expected to provide furtherimpetus

• Investment opportunities exist in almost every segment ofthebusiness

• Housing: about 25 million new units expected to be built in7years

• Office space for IT/ITES: 150 million sq. ft. across urban Indiaby2010

• Commercial space for organised retailing: 220 million sq. ft.by2010

• Hotels and Hospitality: Over 100,000 new rooms in the next5years

• InvestmentopportunityofoverUS$75billioninthenext5years

• MajorforeigninstitutionalinvestorsincludingMorganStanley,GoldmanSachs,MerrillLynch,AIG,BlackstoneandCalpershaveinvestedorareintheprocessofinvestinginIndianrealestate

CommercialandofficecomplexesmushroominginmajorIndianmetros

Over25millionnewhousingunitsrequiredin7years

For additional information: Ministry of Urban Development (http://urbanindia.nic.in), Confederation of Real Estate Developers Associations of India (http://www.credai.com), Indian Brand Equity Foundation (http://ibef.org)

Real Estate Market(US$ billion)

Source: ASSOCHAM Report

39

% C

AG

R

2006

2010 (E)

60

16

TATA-2734_FDI Brochure_08_Pg no.53 53 8/4/08 5:42:23 PM

o v e r v i e w

54

S e r v I c e S

retail

Opportunities

Size

• Indiaisoneofthe10largestretailmarketsintheworld

• RetailsaleswereUS$262billionin2006,constitutingover30%ofIndia’sGDP

• “Organised Retail” constitutes only 4.6% of total retail sales - about US$12billionp.a.

• Hasbeengrowingatover40%p.a.inthelast2years

Structure

• TheIndianretailsectorishighlyfragmented:mostlyowner-run“MomandPop”outlets

• Thereareover15millionsuch“MomandPop”retailoutlets

• RetailchainssuchasPantaloon,TrentandRPGRetailhavebeengrowingrapidly;whileReliance,BhartiandAdityaBirlaGrouphaveannouncedinvestmentsofoverUS$9billioninthesector

• DairyFarm,Metro,Shopritem,Wal-MartandMarks&Spenceraresomeofthemajor international retailchains thatarealreadypresentor in theprocessofenteringthemarket

• Morethan100internationalluxurybrandsareplanningtosetupshopinIndia

Policy

• 100%FDIisallowedinCashandCarryWholesaleformats.Franchiseearrangementsarealsopermittedinretailtrade

• 51%FDIisallowedinsinglebrandretailing

• ThegovernmentisexaminingfurtherliberalisationofFDIinretailtrade

Top Players in the Retail Industry

Total estimated investment opportunity of US$ 5-6 billion in 5 yearsIndian Retail Market:MarketSize:US$262billioninFY06

Players Revenues for Retail Space as Format 2006-07 in US$ on May 2007 millions. (Sq. ft.)

FutureGroup(PantaloonRetail) 821.0 6,630,000 F&G,Specialty

RahejaGroup(Shoppers’Stop) 219.7 1,590,000 F&G,Specialty

TataGroup SpecialityRetail,Electronics,(Trent,InfinitiRetail) 145.2 880,000 HyperMarkets

RPGRetail 146.0 810,000 F&G,Specialty

AVBirlaGroup 61.0 890,000 F&G

Source: TSMG

Food, Grocery & General Merchandise63.7%

Clothing, Textile & Fashion Accessories8.5%

Eating Out4.1%

Home Decor & Furnishings

3.9%

Others15.8%

Durables4.1%

Source: TSMG Analysis

TATA-2734_FDI Brochure_08_Pg no.54 54 8/4/08 5:42:25 PM

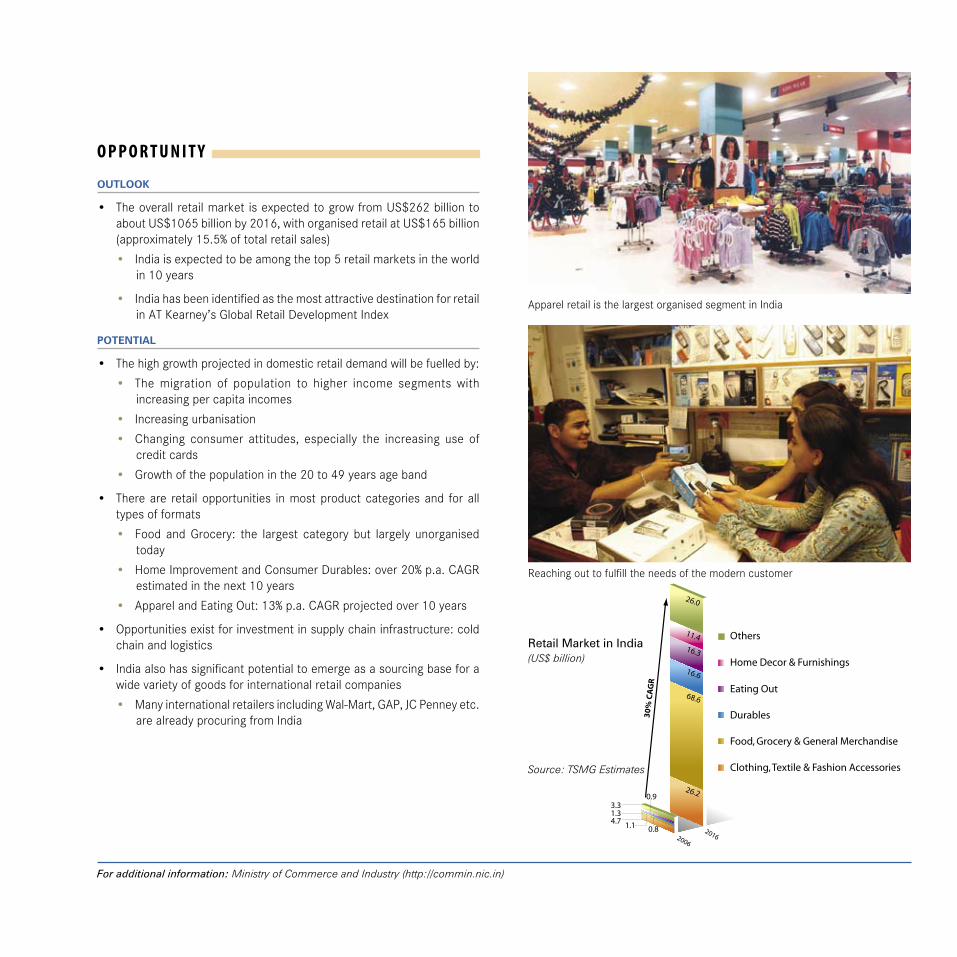

o p p o r t u n i t y

outlook

• TheoverallretailmarketisexpectedtogrowfromUS$262billiontoaboutUS$1065billionby2016,withorganisedretailatUS$165billion(approximately15.5%oftotalretailsales)

• Indiaisexpectedtobeamongthetop5retailmarketsintheworldin10years

• IndiahasbeenidentifiedasthemostattractivedestinationforretailinATKearney’sGlobalRetailDevelopmentIndex

Potential

• Thehighgrowthprojectedindomesticretaildemandwillbefuelledby:

• The migration of population to higher income segments withincreasingpercapitaincomes

• Increasingurbanisation

• Changing consumer attitudes, especially the increasing use ofcreditcards

• Growthofthepopulationinthe20to49yearsageband

• Thereare retailopportunities inmostproductcategoriesand foralltypesofformats

• Food and Grocery: the largest category but largely unorganisedtoday

• HomeImprovementandConsumerDurables:over20%p.a.CAGRestimatedinthenext10years

• ApparelandEatingOut:13%p.a.CAGRprojectedover10years

• Opportunitiesexistforinvestmentinsupplychaininfrastructure:coldchainandlogistics

• Indiaalsohassignificantpotentialtoemergeasasourcingbaseforawidevarietyofgoodsforinternationalretailcompanies

• ManyinternationalretailersincludingWal-Mart,GAP,JCPenneyetc.arealreadyprocuringfromIndia

ApparelretailisthelargestorganisedsegmentinIndia

Others

Home Decor & Furnishings

Eating Out

Durables

Food, Grocery & General Merchandise

Clothing, Textile & Fashion Accessories

20162006

30

% C

AG

R

26.2

68.6

16.6

16.3

11.4

26.0

3.31.34.7

0.8

0.9

1.1

Source: TSMG Estimates

Retail Market in India(US$ billion)

For additional information: Ministry of Commerce and Industry (http://commin.nic.in)

Reachingouttofulfilltheneedsofthemoderncustomer

TATA-2734_FDI Brochure_08_Pg no.55 55 8/4/08 5:42:28 PM

o v e r v i e w

56

S e r v I c e S

touriSM

Opportunities

Size

• TravelandTourismisaUS$41.8-billionindustryinIndia,5.3%ofGDP

• 4.9millioninternationaltouristarrivalsin2007,anincreaseofover9%fromthepreviousyear

• 382milliondomesticvisitsestimatedin2006;thedomestictourismmarketgrewatabout12%CAGRinthelast5years

• Only109,000roomsin1,980hotelsacrossthecountryregisteredin2006*

• Five-starhotelroomsconstitute27%,four-star7.5%andthree-star22%

• AllIndiaindustrywideoccupancyofover66.9%in2006-07

• ScarcityofroomsinseveralcitiessuchasMumbai,DelhiandBengaluruhasresultedinratesofoverUS$300pernight

Structure

• Theindustryisdominatedby4-5largeIndianhotelowner-managers–TheTajGroup,Oberoi,ITC,LeelaandBharatHotels

• MostmajorinternationalchainslikeSheraton/Starwood,InterContinental,Hyatt,Marriott,Hilton,LeMeridien,Carlson,Shangri-La,FourSeasonsarerepresentedby management or franchise contracts. Aman and Accor plan to own hotelsaswell.

• OtherssuchasRitzCarltonandMandarinareintheprocessofestablishingtheirpresenceinIndia,primarilythroughmanagementcontracts

• Thebrandedsegmentrepresentsapproximately30,000roomsor30%ofthetotalhotelstock

• Compounded growth in the last 5 years, in terms of rooms added, was thestrongestinthefive-stardeluxecategoryat6%

Policy

• 100%FDIispermittedinHotelsandTourism,throughtheautomaticroute

• HotelsinDelhisetupbefore2010havebeengrantedinfrastructurestatuswithspecialtaxconcessions

* Registered with the Dept. of Tourism.

Source: WTTC Country Reports, FHRAI, HVS, Dept. of Tourism

Total estimated investment of over US$ 13 billion in 5 years

Key Statistics - India

Travel&TourismRevenue(US$billion,2006) 41.8

InboundTouristArrivalsmillionnos.(2007) 4.9

InboundTourismRevenue(US$billion,2007) 7.7

AverageSpendperTourist(US$,2007) 1566

DomesticTourism(millionvisits.,2005) 382

OutboundTourism(millionnos.,2005) 7.18

HotelIndustry–numberofhotels(2006) 1,980

HotelIndustry–numberofrooms(2006) 1,09,392

TATA-2734_FDI Brochure_08_Pg no.56 56 8/4/08 5:42:29 PM

o p p o r t u n i t y

outlook

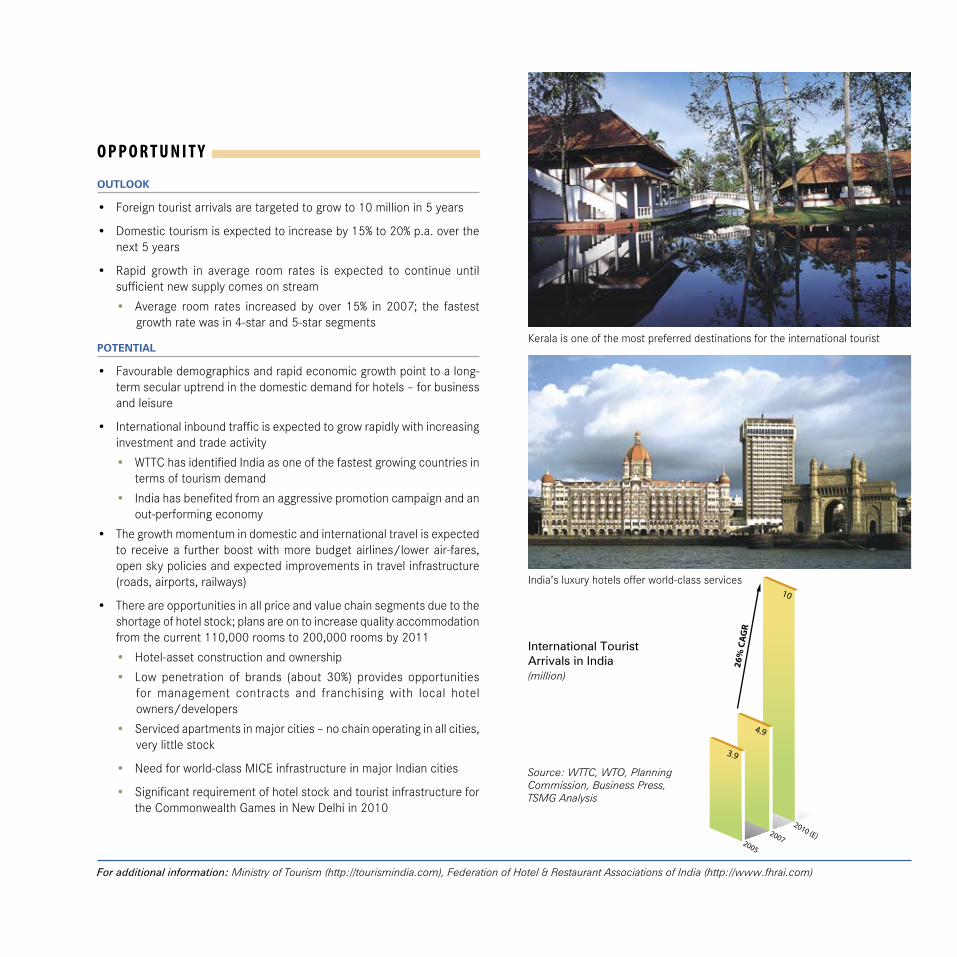

• Foreigntouristarrivalsaretargetedtogrowto10millionin5years

• Domestictourismisexpectedtoincreaseby15%to20%p.a.overthenext5years

• Rapid growth in average room rates is expected to continue untilsufficientnewsupplycomesonstream

• Average room rates increased by over 15% in 2007; the fastestgrowthratewasin4-starand5-starsegments

Potential

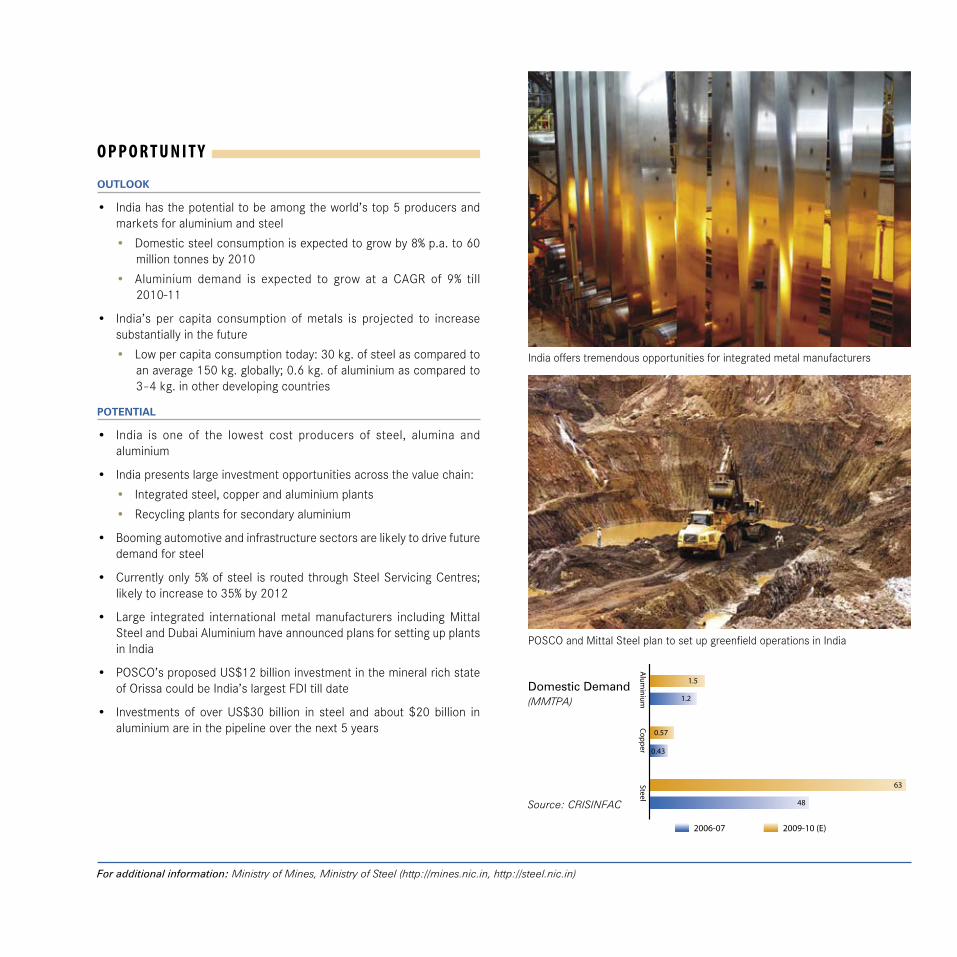

• Favourabledemographicsandrapideconomicgrowthpointtoalong-termsecularuptrendinthedomesticdemandforhotels–forbusinessandleisure

• Internationalinboundtrafficisexpectedtogrowrapidlywithincreasinginvestmentandtradeactivity

• WTTChasidentifiedIndiaasoneofthefastestgrowingcountriesintermsoftourismdemand

• Indiahasbenefitedfromanaggressivepromotioncampaignandanout-performingeconomy

• Thegrowthmomentumindomesticandinternationaltravelisexpectedto receivea furtherboostwithmorebudgetairlines/lowerair-fares,openskypoliciesandexpectedimprovementsintravelinfrastructure(roads,airports,railways)

• Thereareopportunitiesinallpriceandvaluechainsegmentsduetotheshortageofhotelstock;plansareontoincreasequalityaccommodationfromthecurrent110,000roomsto200,000roomsby2011

• Hotel-assetconstructionandownership

• Low penetration of brands (about 30%) provides opportunitiesfor management contracts and franchising with local hotelowners/developers

• Servicedapartmentsinmajorcities–nochainoperatinginallcities,verylittlestock

• Needforworld-classMICEinfrastructureinmajorIndiancities

• SignificantrequirementofhotelstockandtouristinfrastructurefortheCommonwealthGamesinNewDelhiin2010

Keralaisoneofthemostpreferreddestinationsfortheinternationaltourist

For additional information: Ministry of Tourism (http://tourismindia.com), Federation of Hotel & Restaurant Associations of India (http://www.fhrai.com)

26%

CA

GR

2005

2007

2010 (E)

10

4.9

3.9

International Tourist Arrivals in India(million)

Source: WTTC, WTO, Planning Commission, Business Press, TSMG Analysis

India’sluxuryhotelsofferworld-classservices

TATA-2734_FDI Brochure_08_Pg no.57 57 8/4/08 5:42:32 PM

Goa

Bharatpur

Kashmir

Agra Alleppey

TATA-2734_FDI Brochure_08_Pg no.58 58 8/4/08 5:42:56 PM

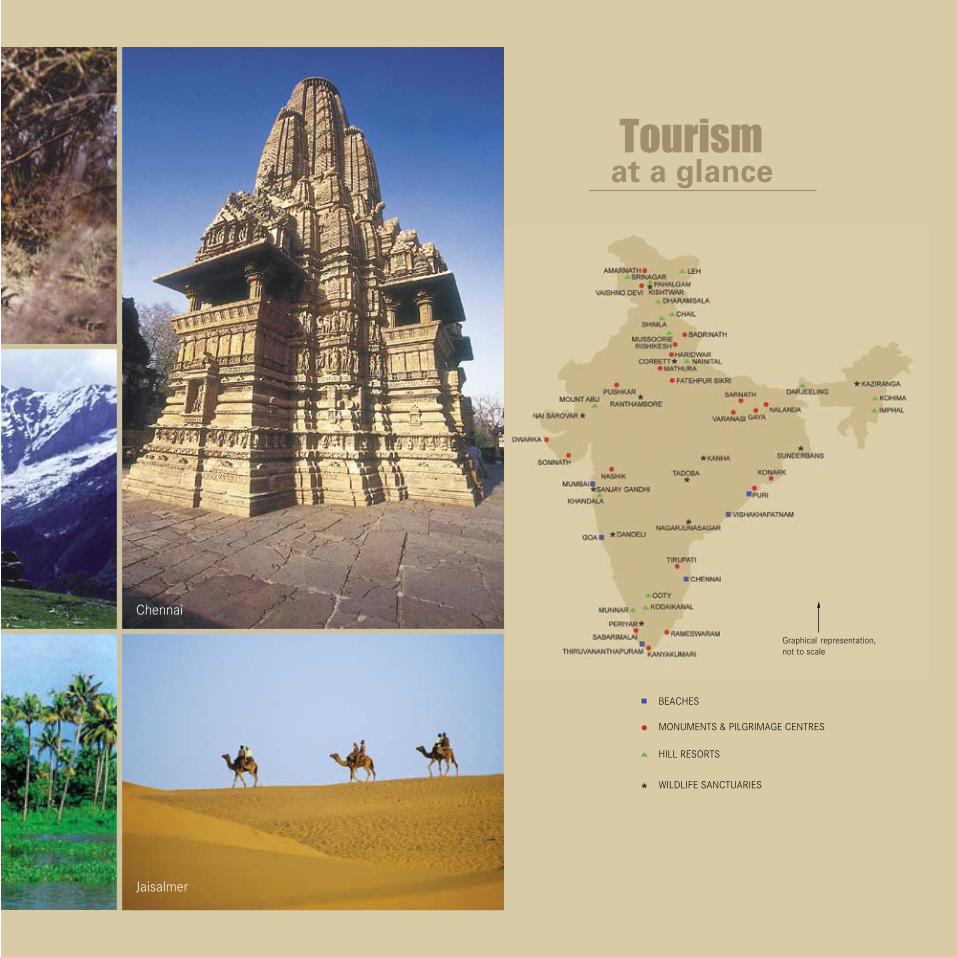

Tourismat a glance

Jaisalmer

Chennai

Graphical representation,nottoscale

BEACHES

MONUMENTS&PILGRIMAGECENTRES

HILLRESORTS

WILDLIFESANCTUARIES

TATA-2734_FDI Brochure_08_Pg no.59 59 8/4/08 5:43:07 PM

TATA-2734_FDI Brochure_08_Pg no.60 60 8/4/08 5:43:09 PM

• metals: Steel & Aluminium

• textiles & garments

• electronics hardware

• chemicals

• Automobiles

• Auto components

• gems & Jewellery

• Food & Agro products

Manufacturing

TATA-2734_FDI Brochure_08_Pg no.61 61 8/4/08 5:43:09 PM

o v e r v i e w

62

m A N U F A c t U r I N g

MetalS: Steel & aluMiniuM

Opportunities

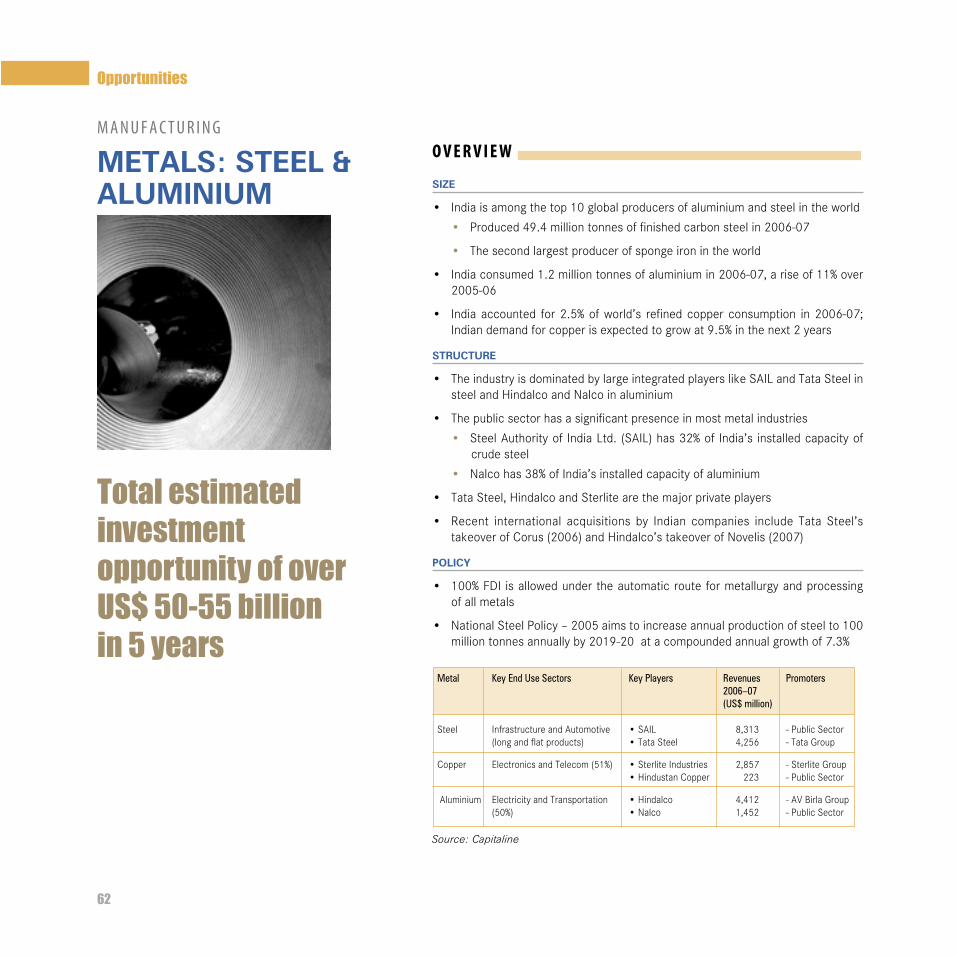

Size

• Indiaisamongthetop10globalproducersofaluminiumandsteelintheworld

• Produced49.4milliontonnesoffinishedcarbonsteelin2006-07

• Thesecondlargestproducerofspongeironintheworld

• Indiaconsumed1.2milliontonnesofaluminiumin2006-07,ariseof11%over2005-06

• Indiaaccounted for2.5%ofworld’s refinedcopperconsumption in2006-07;Indiandemandforcopperisexpectedtogrowat9.5%inthenext2years

Structure