68

Moving the debate forward The Policy Paper Series • Number 9 • January 2009 India: The Impact of Mobile Phones

Moving the debate forward The Policy Paper Series • Number 9 • January 2009

India: The Impact

of Mobile Phones

b

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

This study on India is part of the Vodafone Public Policy series launched in 2004. Our aim is to provide a platform for leading experts to write on issues that are important to us at Vodafone and which may help policy makers as they strive to provide a regulatory environment which stimulates growth and economic development.

We hope you find this report informative.

Vittorio Colao, Chief Executive, Vodafone Group

ForewordIn this report, we have returned to the important subject of the economic impact of telecommunications on emerging markets by undertaking research looking in detail at India. As in the other reports in the Vodafone Public Policy Series, we have asked leading researchers to conduct the analysis. We are delighted that a team led by Dr. Rajat Kathuria of the Indian Council for Research on International Economic Relations (ICRIER), one of India’s foremost independent research institutes, was able to direct and conduct this work.

The opinions expressed in this document are not ours but those of independent experts whose views we respect even if we do not always agree with them. We believe that they have important things to say that should be of interest to anyone concerned with good public policy, and the policies towards economic and social development of India and other emerging markets.

Neil Gough, Director, Public Policy-Emerging Markets, Vodafone Group Diane Coyle, OBE, Enlightenment Economics and chair of Vodafone SIM Panel

Welcome

This paper can be seen online at www.vodafone.com/publicpolicyseries

Published by Vodafone Group Plc Copyright © 2009 Vodafone Group Plc ISBN 978-0-9552578-5-8

Contents Page

Welcome 00 – Vittorio Colao, Chief Executive, Vodafone Group

Foreword 00 – Neil Gough and Diane Coyle

A policy overview 01 – Dr. Rajiv Kumar

An econometric analysis of the impact of mobile 05 – Professor Rajat Kathuria, Dr. Mahesh Uppal and Mamta

The impact of mobiles on agricultural productivity 21 – Sanjay Gandhi, Dr. Surabhi Mittal and Gaurav Tripathi

A survey of usage of mobile in poor urban areas 34 – Professor Ankur Sarin and Professor Rekha Jain

The impact of mobiles in the SME sector 51 – Dr. Mahesh Uppal and Professor Rajat Kathuria

1

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

A policy overviewAmidst the spreading gloom of the economic downturn following the global financial meltdown, the Indian telecom sector provides the proverbial silver lining. The growth in mobile connections has continued at around 10 million a month and investment prospects remain bullish. It is important at this stage to ensure that investor confidence is maintained by further improving the regulatory environment and ensuring that the policy regime promotes growth. In this context, I am delighted that a team of eminent researchers led by Professor Rajat Kathuria of ICRIER undertook to examine the social and economic impacts of mobile telephony in India, with a view to improving the knowledge content for policy-making in this important sector. The project team has analysed what we consider to be an extremely important and relevant topic today. This project is a good example of ICRIER’s strategy of carrying out research which generates analytical and empirical results relevant for generating analytical and empirical inputs pushing forward the reform agenda and for contributing to policy formulation in the country.

We believe the analysis and results reported here to be very important for the Indian economy. There is a growing body of careful empirical economic research which provides a compelling picture of the positive impact of mobile telecommunications on economic growth in developing economies. During the past few years this research has built a detailed understanding of the importance of telecommunications infrastructure to economic development. The unique contribution of this report, which makes it of special interest to policy makers, is that it looks at impacts within a single country, potentially delivering much more robust conclusions.

India has more diversity within its borders than any other country – it comprises 1.1 billion people, living and working in very different circumstances and geographies. Yet it has a national government and policy environment that sets critical economic policies (including telecommunications)

across the whole country. We have taken advantage of that diversity and the availability of state level data to investigate economic impacts within India across states, economic sectors and population segments. Furthermore, because even state level data can mask great differences, we have looked at specific economic sectors (agriculture and small and medium enterprises) and segments of the population (urban slum dwellers) to extend our understanding.

Encouragingly, the econometric analysis reported here extends the conclusion that there is a causal relationship within the same country between higher mobile penetration (mobile subscriptions/population) in a region and higher economic growth. Indian states with high mobile penetration can be expected to grow faster than those states with lower mobile penetration rates, by 1.2% points a year more on average for every 10% increase in the penetration rate. This is an important result. The paper in this report by Kathuria and Uppal suggests, furthermore, that there are important network effects which magnify the economic impact of mobiles on development when the level of mobile penetration exceeds a critical mass of around 25%. This finding underlines the urgency of increasing teledensity across all states and especially in those numerous areas of India that are yet to reach this threshold level.

The extraordinary recent macro-economic performance of the Indian economy has also raised the question of how the benefits of the 8–10% annual GDP growth rate can ‘trickle down’ to poorer socio-economic groups in the country. In that context, the ICRIER researchers have also looked at three segments of the population – the agriculture sector, the Small and Medium Enterprise (SME) sector and urban slum dwellers. In each case, the research demonstrates that access to telecommunications is an important catalyst to realizing productivity and efficiency improvements and thereby making it possible for the benefits of economic growth to be shared. Mobiles currently provide more than 300 million

Rajiv Kumar is the Director and Chief Executive of the Indian Council for Research on International Economic Relations (ICRIER), and a member of the Telecom Regulatory Authority of India since January 2007.

Director and Chief Executive ICRIERDr. Rajiv Kumar

2

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

points of connectivity in India, through which information and opportunity flows. Citizens with access to telecommunications can tap into the benefits of broad economic and social growth much more easily than those who are unconnected.

This result is all the more important for two reasons, one internal and one external. The first is that India is at a stage in its development when there is a large-scale movement of the population from the countryside to the towns, posing new challenges for both rural and urban economies. The second is that the global economic environment has become harsher, and it will be essential to take advantages of all possible opportunities to sustain growth.

Of course, access to mobile telecommunications is certainly not the only thing that matters to economic growth. In this regard, the research also highlights the vital importance of complementary skills and other infrastructure. Unless these are in place, the full potential of better access to telecommunications will not be realised. There is no benefit in farmers knowing the prices that their produce could be sold for in different markets if the roads are too poor for them to be able to transport the goods to those other markets. The research in this report on the uses and impacts of mobiles in agriculture by Gandhi, Mittal and Tripathi show that improving productivity and rural incomes requires an array of enablers in the production cycle, which runs from planting to the final sale of produce; access to information is an important enabler.

Equally, the value in mobiles offering SMEs the potential to introduce different business models which would deliver greater efficiency is only fully realised when the entrepreneurs and their workforce have the basic literacy skills to use the technology appropriately. The case studies of entrepreneurs using mobiles presented in the paper here by Uppal and Kathuria demonstrate not only the potential for improved productivity, incomes and employment (especially for sole traders and very small businesses seeking to improve their livelihoods), but also the barriers to the realisation of that potential – importantly, education and also (in rural areas) teledensity. Telecommunications cannot be seen in isolation from other parts of the development process.

In the urban slums mobile use is associated with relatively high earning households and educational levels. The survey work of Sarin and Jain reported here also reveals that higher household incomes are associated with those families who have enjoyed the benefits of access to mobile communications for the longest period. Importantly, the research shows that those urban slum dwellers who have access to mobiles inhabit an economic and social environment where connectivity is the norm. The research reveals the importance of these network effects, that is the increased value of mobiles if many others in the social and economic milieu are also users of mobiles.

While some parts of India are clearly enjoying the benefits of new-found access to telecommunications, other parts are still lagging behind. The recent extraordinary growth in telecommunication connections in India, which has topped 10 million per month in 2008, has understandably grabbed the headlines. However, other realities are being obscured such as:

• Teledensity in India lags well behind most other countries at similar stages of development (for example, China, Pakistan and Sri Lanka have achieved significantly superior penetration rates of 77%, 60% and 61% respectively).

• There is enormous variation within India, and many of the less developed states have average penetration rates of well below 20%, including Bihar, UP, Orissa, Madhya Pradesh and Assam.

• The level of access to the internet remains persistently low across the whole country (at about 5%) and in less-developed states is virtually non-existent – only 0.1% in Bihar and 0.2% in Assam, for example.

In a world where other countries are increasingly taking advantage of the opportunities being created by telecommunications and other technologies, this is not a comfortable position for India. India needs to catch up with its major trading competitors such as China, Korea and Indonesia if it is truly to join the ranks of emerging economies that have made or are making the transactions to middle income level economies. Other countries enjoying higher penetration telephony and internet access are driving innovation and more sustainable economic growth. India cannot challenge or match the innovation capability of its competitors or meet its indigenous demand for skills and knowledge content if only 5% of the population regularly uses the internet.

What then are the implications for Indian policy makers and telecommunications operators? What are the key elements of a forward looking telecommunications policy agenda that will keep India moving forward at the rate required?

The report clearly shows how putting a mobile in the hands of an individual is unlikely by itself to improve that person’s livelihood. But when it is associated with education on agricultural techniques and tools, as well as with better roads and storage, easier access to information through telephony can become very valuable.

Perhaps it is obvious that there also needs to be investment in other, complementary, infrastructure, but the impact of this interaction between telecommunications and other infrastructure in a developing country may have previously been underestimated. Poverty ultimately needs to be alleviated by improved labour productivity. Mobile telephony has an important role to play because it provides a means for the exchange of information and learning, but it is only one element in the process of productivity growth. For example, 60% of the working population in India is engaged in agriculture and the barriers to raising agricultural productivity gains go far beyond communications access.

Therefore, access to telecommunications needs to be seen as a foundation on which other initiatives can be built. The debate on telecommunications needs to be expanded from a debate only about access, to a broader vision of how individuals can leverage the capabilities of telecommunications to grasp fully the opportunities of economic development.

The current Indian regulatory environment has stimulated investment in the mobile sector to an unprecedented level. However, India is now sprinting at a time when other countries

3

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

are already well ahead. Those other countries, such as China and South Korea are shifting their attention from simple tele-density targets to the priorities of ensuring access to high-speed data networks and broadband. It is likely that India’s greatest policy challenges still lay ahead – increasing access to telecommunications for underserved citizens and then also extending that access to the internet.

In this context, what are the implications for Indian policy makers and telecommunications operators? The research points to three areas which seem to be of particular importance. The first is spectrum policy, the second area concerns fees and universal service and the third is about the general investment environment.

Spectrum policy

Spectrum policy is the most obvious. India is burdened with severe spectrum constraints. Minutes per subscriber are higher in India than in almost any other country and cities in India have some of the most densely populated areas. Both these factors increase the need for spectrum, yet Indian operators are struggling with average spectrum allocations only a third of those available to most operators in other countries.

Spectrum is a fundamental driver of cost in mobile networks – the less spectrum, the more sites are needed, and the cost of deployment rises accordingly. This scarcity situation in 2G (GSM) is likely to be replicated in 3G. It causes Indian operators to have to invest more capital building capacity in urban areas in order to overcome spectrum constraints and preserve service quality, but thereby limiting capital available for the expansion of coverage into rural areas or to lower income urban agglomerations.

The civilian spectrum shortage is created by two factors: the occupation of critical frequencies by the military and other government departments; and a policy bias towards a large number of operators. Many commentators argue that fewer operators would achieve greater economies of scale, while still preserving the benefits of vigorous competition.

All over the world and across industries, it is amply demonstrated that a market structure with relatively few players but robust regulatory oversight can be more competitive than one populated by a large number of small players. In fact market fragmentation has the disadvantage of none of the players having enough capacity and resources for innovation and delivering greater value to the customer. There is also the danger of a single large firm emerging as a virtual monopoly in such markets, and drawing monopoly rents. The government would have to weigh these factors against its apparent objectives of maximising resources.

A government initiative whereby additional spectrum is made available to the industry has yet to deliver results. As a consequence, the Indian telecommunications industry is being starved of spectrum and the private sector is being drained of capital.

The losers from this spectrum constraint are the people who are consequently being denied access to

telecommunications services. They are losing out because licensees are diverting investments to maintain quality of service in urban areas. A comprehensive review of the overall national benefit of current policy on spectrum allocation is urgently required. Are there more efficient alternatives for the military and public sector which would free spectrum for private use while not adversely affecting the military’s ability to protect India’s national interests? This should include an estimate of the cost to the nation of the spectrum that is currently being used by the military. Greater transparency in this regard would be most desirable.

The most serious problem facing India surrounds data services. India’s current position, by international standards, is lagging, and we cannot afford any complacency. The rest of the world is increasingly concerned about increasing access to high speed data rather than voice connectivity. High-speed data services and the internet are seen as a critical capability that will drive future global competitiveness in technology and services.

For India, and the rest of the developing world, data services will be delivered by wireless broadband access rather than fixed line copper or fibre networks. But the vision in India is likely to be limited by the reality of insufficient spectrum availability. The first 3G spectrum auction scheduled for January 2009 is to be welcomed but the incremental capacity for each operator is most likely to be consumed by voice capacity as a result of the deficiencies of 2G spectrum allocation. The delivery of world-class data services requires very large blocks of spectrum. A major strategic plan for data services is urgently required to plan the availability of sufficient spectrum.

Licence, spectrum fees and USO

Policy-makers must address the access deficit of the disadvantaged segments of the population. This does not simply equate to the rural population. The paper in this study by Sarin and Jain reminds us how marginalized the urban poor are but also demonstrates how access to telecommunications can offer a route to increased incomes. Tackling the access gap must include the urban poor as well as those living in rural communities. There has been a natural focus in the past on the rural poor given the proportion of India’s population which lives in rural areas, but India is becoming increasingly and dramatically urbanized. At present over 320 million people live in urban areas, and the number is expected to increase to a staggering 575 million by 2020.

The private sector has done much to invest in telecommunications provision for both the urban and rural poor, and private operators continue to invest at ever-increasing levels. However, in the context of the economic dividend from the sector, some aspects of policy must be re-evaluated.

The industry labours under ongoing heavy spectrum charges and licence fees that are likely to be counter-productive to the broader national interests. Yet the prevailing policy mood seems to be to increase them, not reduce them. Even the most minor operator in a less economically developed state will pay a

4

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

minimum of 8% of revenue (before any cost deductions) in respect of combined licence and spectrum fees. How can any licence fee or spectrum fee be justified in areas like these? India needs to find ways to accelerate investment in areas which have low teledensity; licence and spectrum fees levied from users drain resources from operators in those areas and inhibit investment. The recent policy towards reductions in licence fees when a licensee attains coverage targets is a welcome move in the right direction. However, the overall policy towards fees should be re-evaluated in the context of these economic results.

There are significant questions too about the nature of the universal service policy. The coffers of India’s USO fund continue to grow. The funds are being collected, but they are not being spent for their intended purpose of increasing teledensity. This problem is not unique to India but at the moment the USO is effectively an additional tax on the sector, driving up prices of services and effectively dis-enfranchising those the policy is targeted towards. The hard question has to be asked about the most effective means of increasing access – is it though the intensification of competition and the reduction of prices through the removal of government imposed levies and taxes, or through the (unspent) universal service fund?

In the absence of plans for productive use of the accumulated fund, the USO charges should be reviewed. A reduction would improve investment incentives and increase the resources the sector has available for investment, at a time when funding for investment is difficult.

Overall investment environment

At the highest strategic level, Indian policy makers also need to assess whether their approach is consistent with the potential economic value of the sector.

India has chosen a policy of creating a highly competitive, fragmented industry, which has delivered extraordinarily low prices and high minutes of use per subscriber. However, these low prices are only currently enjoyed by about 25–30% of the Indian population – the rest do not have a mobile phone. The real question is to whether the same model will eventually deliver universal access to telecommunications and most importantly access to high-quality data services.

India needs to set out a stable policy framework to attract long-term investment in telecommunications. That requires a stable licensing structure, consistent policy decisions and a predictable framework for regulatory intervention. The history of Indian telecommunications has been one of frequent shifts in policies, regulations and taxation that create uncertainty for investors.

A stable and attractive policy approach is especially important in the context of the current global credit crunch and with capital so scarce. Policies are needed which will attract long-term investors who will make the commitments and investments required to create world-class telecommunications networks and services that will deliver global competitiveness for all the citizens of India.

Therefore this is the time for the government to be assessing fundamental policy issues that impact sector investment, such as foreign direct investment caps, licence extension terms, spectrum availability and allocations, and criteria for mergers and acquisitions. All these issues affect the economics of additional capital investment. There is a need to determine what sort of industry India needs and set the policy framework accordingly.

Conclusion

We believe that these findings from a detailed study of one country carry lessons not only for India but also for other countries facing similar challenges in terms of agricultural productivity, small business growth, and rural and urban poverty. Weaknesses in education and other physical infrastructure need to be tackled to maximise the potential productivity and growth benefits of access to mobile communications in many other countries apart from India. A systematic, integrated set of development policies is required to address this.

We hope that this report will provide some impetus to a policy debate about the priorities and the needs of the telecommunications sector. Its recent track record in India is sufficiently promising that there might not seem to be a pressing need to refresh the policy environment for telecommunications, or to develop a wider vision for the sector. But we believe that such a policy shift will be required to sustain the progress towards the truly world-class telecommunications services that India and its citizens deserve. This will underpin India’s competitiveness in the volatile global marketplace, and ensure that the benefits of growth are more widely shared as the economy develops. The debate needs to start today.

We hope that the following papers will not only stimulate that debate but that they will also be of interest to you.

5

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

Director, Com First (India) Private Ltd

Dr. Mahesh Uppal

Professor of Economics, ICRIER Professor, IMI

Prof. Rajat Kathuria

Rajat Kathuria is Professor of Economics at ICRIER, and is also a professor at the International Management Institute (IMI), New Delhi.

Researcher, ICRIER

Mamta

An econometric analysis of the impact of mobile

Dr. Mahesh Uppal is the Director of Com First (India) Private Ltd, a consultancy specializing in policy, regulation, and strategy.

Mamta is a researcher at the Indian Council for Research on International Economic Relations (ICRIER).

1. Summary

During the past two decades, India has moved away from its former ‘command and control’ policies to become a market-based economy. This process started in the mid-1980s and gathered substantial momentum at the beginning of the 1990s. The process of reform has continued in this decade with a further opening of the economy and the creation of regulatory institutions to oversee the march towards fully competitive markets. As a result of the liberalisation, GDP per capita has been rising by 7% annually, a rate that leads to its doubling in a decade. This contrasts with annual growth of GDP per capita of just 1% in the three decades from 1950 to 1980. Rapid growth turned India into the third largest

economy in the world in 2006 (after the United States and China and just ahead of Japan when measured at purchasing power parities), accounting for nearly 7% of world GDP.1

Although India’s growth rate has been among the highest in the world, it remains a low income country. With a per capita income of US$950 in 2007, India ranks 122nd.2 As well as a low average income, there are substantial disparities in economic performance between states. The average per capita Gross State Domestic Product (GSDP) of Delhi, the richest state, is five times that of Bihar, the poorest. There is a broad consensus amongst policy makers that growth needs to become more inclusive by increasing the prosperity of poorer states, whose economies have expanded at a slower pace than those of the richer states in the past decade.

6

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

Previous research suggests that the differences in economic performance across states are associated with the extent to which they have introduced market-oriented reforms, alongside measures to improve infrastructure, education and basic services.3

The physical infrastructure (or lack thereof) is widely acknowledged to be one of the crucial impediments to achieving higher and more inclusive economic growth in India. The lack of adequate infrastructure is particularly acute in rural areas, home to 70% of India’s population and the 52% of the work force that is primarily engaged in agriculture and related activities.4 Agriculture in India accounts for 18% of national income, implying extremely low agricultural productivity. The resulting migration of excess farm labour to urban areas in search of jobs is straining urban infrastructure and increasing the population living in city slums. India’s urban population is expected to double over the next two decades, to 575 million.

Any strategy that seeks to address the problem of inclusive growth will therefore have to contend with these harsh realities of low productivity in the countryside, a massive movement of people to the cities, and extensive poverty in both rural and urban areas. Past policies have not had much success, often being defeated by the magnitude of the problem as well as weaknesses in implementation. But the message is clear. Rural productivity needs to increase both as part of the development process and to raise incomes for millions of Indians who live below the poverty line, in the countryside and the cities.

A sustainably faster rate of growth can only be achieved by improving productivity, but underinvestment in infrastructure is an important barrier. India plans roughly to double investment in infrastructure, to $500 billion over the next five years, or about 8% of GDP each year. The Planning Commission maintains that the growth target of the Eleventh Plan (2007–12) is achievable only if the ‘infrastructure deficit can be overcome and adequate investment takes place to support higher growth’.5 The government expects private investors to contribute two-fifths of the total investment in infrastructure, not only to expand capacity but also to improve the quality of service.

The telecommunications sector has had the most success in attracting private investment and is often held up as an example for other infrastructure sectors.6 Two familiar reasons for this status are worth repeating. First, India’s teledensity has shown extraordinary growth since private participation in the sector was introduced, rising from less than 1% in 1998 to over 30% today. Secondly, several research studies have found that the telecommunications infrastructure is one of the significant factors in economic growth, alongside others such as overall investment, education, energy and transportation networks.7

The change in India’s telecoms landscape has been dramatic. In 1994, the year the National Telecom Policy was drafted, fewer than 1 in 100 Indians owned a phone. Public sector executives working for the incumbent monopoly were highly popular, given their ability to short circuit the endless waiting time for the privilege of owning a telephone. Less than 15

years on, teledensity has increased to more than 32% and subscriber numbers are growing at a rate of about 10 million per month. Ownership of a phone is no longer a function of who you know, but rather conforms to the conventional forces of demand and supply. Waiting lists are down and voice calls in India are amongst the cheapest in the world. The Government’s target of 250 million phones by the end of 2007 was reached, quite unexpectedly, ahead of schedule.8

One of our research aims was to extend earlier studies by analysing the growth impact of telecoms in India. While the telecoms-growth link has been explored across different countries and within a particular country over time, few studies have assessed the relationship at the sub-national level. India’s Federal structure, with some states such as Uttar Pradesh, Maharashtra, and Madhya Pradesh larger in geographical area and population than most European countries, readily lends itself to such analysis.9 Moreover, balanced regional development has always been an objective in India’s plans and therefore studying the impact of telecoms liberalisation across states will provide valuable insights for this policy aim.

The rapid spread of mobile telephony in India is the most obvious manifestation of the benefits of telecom sector liberalisation. Fixed line penetration is in fact showing signs of decline, and future growth will come from mobile. Given that about 10 million wireless subscribers are being added every month, the impact of telecoms on state-level growth rates can be explored through the impact of mobile telephony. This chapter accordingly attempts to answer three questions:

• What is the impact of mobile penetration on state growth rates;

• Do less-developed states show a greater impact of mobile penetration; and

• What are the links through which mobile telephony affects growth and what are the constraints, if any, which limit its impact?

The first two questions are addressed by employing ‘top-down’ econometric analysis using state level economic indicators, while the third question is addressed using ‘bottom-up’ evidence from surveys and other information.

The next section briefly reviews the existing literature on the impact of telecoms on growth. Section 3 assesses India’s regulatory and competitive landscape for telecoms and compares Indian mobile telephony indicators with those of some other countries. The descriptive statistics presented in this section underscore the phenomenal progress made by mobile in India, both when judged against past performance and when compared with other countries, but also show that India still lags other countries in important ways. Disparities in mobile penetration across states and between urban and rural areas are also examined. Section 4 presents and analyses the results of the econometric model and also draws upon survey based evidence to demonstrate the positive impact of mobiles on growth, the first such estimates to confirm the growth dividend of mobile for Indian states. A final section offers some conclusions.

7

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

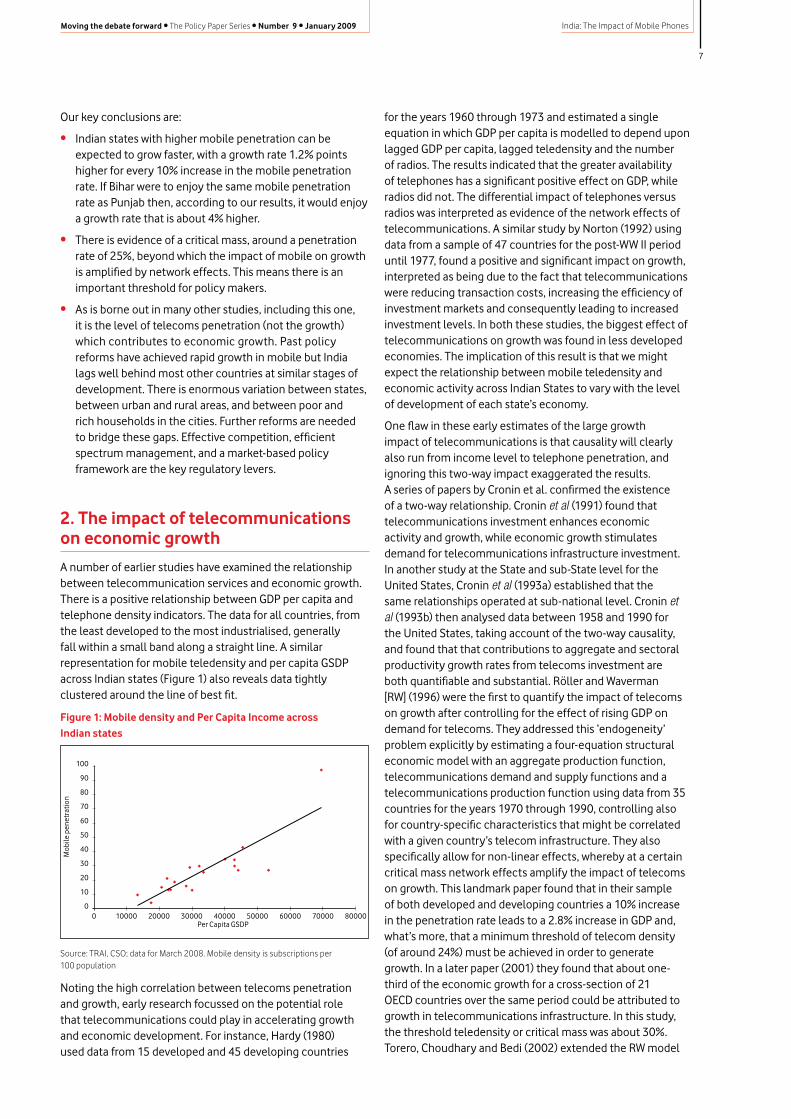

Our key conclusions are:

• Indian states with higher mobile penetration can be expected to grow faster, with a growth rate 1.2% points higher for every 10% increase in the mobile penetration rate. If Bihar were to enjoy the same mobile penetration rate as Punjab then, according to our results, it would enjoy a growth rate that is about 4% higher.

• There is evidence of a critical mass, around a penetration rate of 25%, beyond which the impact of mobile on growth is amplified by network effects. This means there is an important threshold for policy makers.

• As is borne out in many other studies, including this one, it is the level of telecoms penetration (not the growth) which contributes to economic growth. Past policy reforms have achieved rapid growth in mobile but India lags well behind most other countries at similar stages of development. There is enormous variation between states, between urban and rural areas, and between poor and rich households in the cities. Further reforms are needed to bridge these gaps. Effective competition, efficient spectrum management, and a market-based policy framework are the key regulatory levers.

2. The impact of telecommunications on economic growth

A number of earlier studies have examined the relationship between telecommunication services and economic growth. There is a positive relationship between GDP per capita and telephone density indicators. The data for all countries, from the least developed to the most industrialised, generally fall within a small band along a straight line. A similar representation for mobile teledensity and per capita GSDP across Indian states (Figure 1) also reveals data tightly clustered around the line of best fit.

Figure 1: Mobile density and Per Capita Income across Indian states

0

10

20

30

40

50

60

70

80

100

90

0 10000 20000 30000 40000 50000 60000 70000 80000Per Capita GSDP

Mob

ile p

enet

ratio

n

Source: TRAI, CSO; data for March 2008. Mobile density is subscriptions per 100 population

Noting the high correlation between telecoms penetration and growth, early research focussed on the potential role that telecommunications could play in accelerating growth and economic development. For instance, Hardy (1980) used data from 15 developed and 45 developing countries

for the years 1960 through 1973 and estimated a single equation in which GDP per capita is modelled to depend upon lagged GDP per capita, lagged teledensity and the number of radios. The results indicated that the greater availability of telephones has a significant positive effect on GDP, while radios did not. The differential impact of telephones versus radios was interpreted as evidence of the network effects of telecommunications. A similar study by Norton (1992) using data from a sample of 47 countries for the post-WW II period until 1977, found a positive and significant impact on growth, interpreted as being due to the fact that telecommunications were reducing transaction costs, increasing the efficiency of investment markets and consequently leading to increased investment levels. In both these studies, the biggest effect of telecommunications on growth was found in less developed economies. The implication of this result is that we might expect the relationship between mobile teledensity and economic activity across Indian States to vary with the level of development of each state’s economy.

One flaw in these early estimates of the large growth impact of telecommunications is that causality will clearly also run from income level to telephone penetration, and ignoring this two-way impact exaggerated the results. A series of papers by Cronin et al. confirmed the existence of a two-way relationship. Cronin et al (1991) found that telecommunications investment enhances economic activity and growth, while economic growth stimulates demand for telecommunications infrastructure investment. In another study at the State and sub-State level for the United States, Cronin et al (1993a) established that the same relationships operated at sub-national level. Cronin et al (1993b) then analysed data between 1958 and 1990 for the United States, taking account of the two-way causality, and found that that contributions to aggregate and sectoral productivity growth rates from telecoms investment are both quantifiable and substantial. Röller and Waverman [RW] (1996) were the first to quantify the impact of telecoms on growth after controlling for the effect of rising GDP on demand for telecoms. They addressed this ‘endogeneity’ problem explicitly by estimating a four-equation structural economic model with an aggregate production function, telecommunications demand and supply functions and a telecommunications production function using data from 35 countries for the years 1970 through 1990, controlling also for country-specific characteristics that might be correlated with a given country’s telecom infrastructure. They also specifically allow for non-linear effects, whereby at a certain critical mass network effects amplify the impact of telecoms on growth. This landmark paper found that in their sample of both developed and developing countries a 10% increase in the penetration rate leads to a 2.8% increase in GDP and, what’s more, that a minimum threshold of telecom density (of around 24%) must be achieved in order to generate growth. In a later paper (2001) they found that about one-third of the economic growth for a cross-section of 21 OECD countries over the same period could be attributed to growth in telecommunications infrastructure. In this study, the threshold teledensity or critical mass was about 30%. Torero, Choudhary and Bedi (2002) extended the RW model

8

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

to include mobile phones. They used data from 113 countries over a 20-year period and also found a positive causal link from telecommunications to GDP. The effect in their work appears to be non-linear and is particularly pronounced for countries with a telecom penetration rate in the range 5–15%.

The threshold at which the growth dividend of telecom begins to take effect varies across these studies. It does suggest, however, that increases in teledensity might not immediately generate higher growth effects in states with a particularly poorly developed telecoms infrastructure. The telecoms density in certain states is so low that marginal improvements might not generate the desired growth effects – not until the critical threshold for network effects is reached. Thus, laggard states may require substantial investments in telecommunications infrastructure before they can benefit from the growth-generating effects of these technologies. This is supported by our results, as described below.

It has recently become quite fashionable to adapt the RW framework for developing countries and particularly for estimating the growth dividend of mobile phones. Torero, Choudhary and Bedi (2002), Sridhar and Sridhar (2004) and Waverman, Meschi and Fuss (2005) are some examples. The growth dividend of investment in (fixed) telecommunications infrastructure in developed economies is now fairly well established. Since the growth of mobile phones in developing economies such as India, China, Brazil and others has been sensational; it raises the obvious question whether mobile phones in developing economies are playing the same role that fixed telephony played in the richer economies in the 1970s and 1980s. Mobile phones are often the only means of communication for a large number of people. For example, the most recent numbers available for India reveal that while fixed line penetration is roughly 3.5 per hundred and declining, the corresponding number for mobile stands at 28 per hundred, and growing. Because mobiles substitute for fixed lines in developing economies, their growth impact should be stronger in these than in developed economies, where mobiles complement the extensive fixed service. Waverman, Meschi and Fuss (2005) used data on 92 high and low income countries from 1980 to 2003, and found that mobile telephony has a positive and significant impact on economic growth, and indeed this impact could be twice as large in developing as compared to developed countries.

Mobile phones can perform in underserved areas and regions what fixed lines did in many other regions and countries over two decades ago: widen markets, create better information flows, lower transactions costs and substitute for costly (in time and money) physical transport. The value of a mobile phone can be particularly high because other forms of communication such as postal systems, roads and fixed line networks are often poor in developing countries. At the same time, in many developing countries growth has been low due to a host of other reasons – poor governance, lack of capital, low skill levels and many others. It is unlikely that increased mobile penetration by itself will be able to alleviate these other constraints on growth. This caution is supported by case studies. For instance Jensen (2007) states that ‘improvements in roads have lowered the cost of land transport, leading

to more arbitrage by wholesalers on land... In other cases, poor quality roads may limit the ability of improvements in information (i.e. mobile penetration) to enhance market performance since arbitrage remains prohibitively expensive’. The economic impact of mobile is likely to be strongest when the absence or inadequacy of existing telecommunications facilities acts as a barrier or bottleneck to private economic activities, but also when enough other infrastructure exists to permit the effective use of telecommunications.

There is no study that systematically investigates the growth impact of mobile phones at the sub-national level. India is ideally placed for such an analysis. First, there is wide variation in economic performance across Indian states. Secondly, mobile licences in India have been awarded for geographic areas which are, to a large extent, contiguous with state boundaries.10 The correspondence between a mobile telecom licence and a state boundary allows us to adapt the RW (2001) framework for Indian states. And finally, the explosive growth of mobile in India, especially in the last five years, should allow us to identify any impact on economic performance across states. We attempt to quantify that impact and explain differences, if any, across states.

Three caveats must be mentioned, however. First, mobile in India is relatively young (the first licensee rolled out services in 1995, and it was not until 2003 that the service became available in all Indian states) so there is little real trend as yet. Secondly, since mobiles are so new, there has been extremely rapid growth in mobile penetration starting from zero. There could thus be a tendency to overestimate the impact of mobile on growth, despite controlling for other growth-generating variables such as capital, labour and education. Thirdly, data at the state level for investment comparable to data at the national level obtainable from national accounts are simply not available. Likewise, employment data at the state level are not available. These data have been compiled from different sources described in the Annex. The data problems lead us to be cautious in our interpretation of the estimates reported here. Nevertheless, the results show that the growth dividend of mobile is substantial and policy makers will be well advised to harness its full potential.

3. Indian telecommunications across states

The critical element in the development of the Indian telecommunications infrastructure has been the explosive growth of mobile, which has benefited from a compelling technology and an increasingly liberal policy environment. It is a common sight to observe street vendors, rickshaw pullers and newspaper hawkers routinely talking on their mobile phones in cities. From being viewed as a luxury when it was first introduced, the mobile service is now used everyday by millions of Indians.

9

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

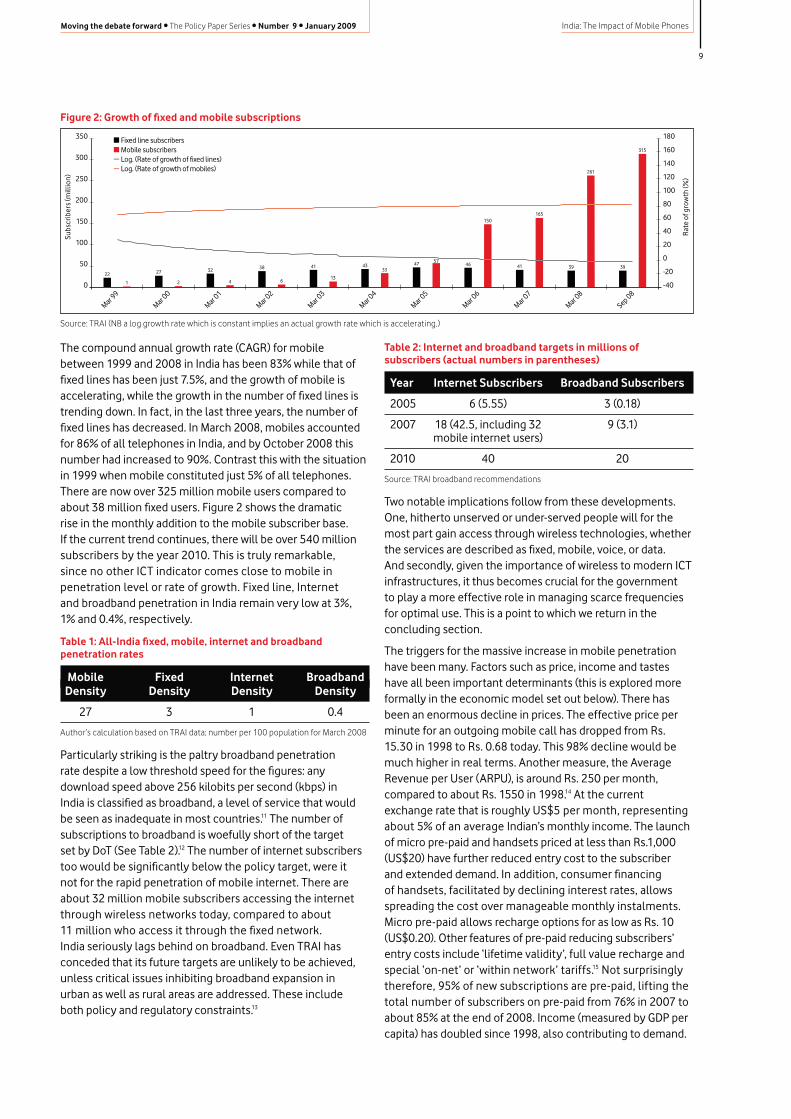

Figure 2: Growth of fixed and mobile subscriptions

Source: TRAI (NB a log growth rate which is constant implies an actual growth rate which is accelerating.)

Table 2: Internet and broadband targets in millions of subscribers (actual numbers in parentheses)

Year Internet Subscribers Broadband Subscribers

2005 6 (5.55) 3 (0.18)

2007 18 (42.5, including 32 9 (3.1) mobile internet users)

2010 40 20

Source: TRAI broadband recommendations

Two notable implications follow from these developments. One, hitherto unserved or under-served people will for the most part gain access through wireless technologies, whether the services are described as fixed, mobile, voice, or data. And secondly, given the importance of wireless to modern ICT infrastructures, it thus becomes crucial for the government to play a more effective role in managing scarce frequencies for optimal use. This is a point to which we return in the concluding section.

The triggers for the massive increase in mobile penetration have been many. Factors such as price, income and tastes have all been important determinants (this is explored more formally in the economic model set out below). There has been an enormous decline in prices. The effective price per minute for an outgoing mobile call has dropped from Rs. 15.30 in 1998 to Rs. 0.68 today. This 98% decline would be much higher in real terms. Another measure, the Average Revenue per User (ARPU), is around Rs. 250 per month, compared to about Rs. 1550 in 1998.14 At the current exchange rate that is roughly US$5 per month, representing about 5% of an average Indian’s monthly income. The launch of micro pre-paid and handsets priced at less than Rs.1,000 (US$20) have further reduced entry cost to the subscriber and extended demand. In addition, consumer financing of handsets, facilitated by declining interest rates, allows spreading the cost over manageable monthly instalments. Micro pre-paid allows recharge options for as low as Rs. 10 (US$0.20). Other features of pre-paid reducing subscribers’ entry costs include ‘lifetime validity’, full value recharge and special ‘on-net’ or ‘within network’ tariffs.15 Not surprisingly therefore, 95% of new subscriptions are pre-paid, lifting the total number of subscribers on pre-paid from 76% in 2007 to about 85% at the end of 2008. Income (measured by GDP per capita) has doubled since 1998, also contributing to demand.

The compound annual growth rate (CAGR) for mobile between 1999 and 2008 in India has been 83% while that of fixed lines has been just 7.5%, and the growth of mobile is accelerating, while the growth in the number of fixed lines is trending down. In fact, in the last three years, the number of fixed lines has decreased. In March 2008, mobiles accounted for 86% of all telephones in India, and by October 2008 this number had increased to 90%. Contrast this with the situation in 1999 when mobile constituted just 5% of all telephones. There are now over 325 million mobile users compared to about 38 million fixed users. Figure 2 shows the dramatic rise in the monthly addition to the mobile subscriber base. If the current trend continues, there will be over 540 million subscribers by the year 2010. This is truly remarkable, since no other ICT indicator comes close to mobile in penetration level or rate of growth. Fixed line, Internet and broadband penetration in India remain very low at 3%, 1% and 0.4%, respectively.

Table 1: All-India fixed, mobile, internet and broadband penetration rates

Mobile Fixed Internet Broadband Density Density Density Density

27 3 1 0.4

Author’s calculation based on TRAI data; number per 100 population for March 2008

Particularly striking is the paltry broadband penetration rate despite a low threshold speed for the figures: any download speed above 256 kilobits per second (kbps) in India is classified as broadband, a level of service that would be seen as inadequate in most countries.11 The number of subscriptions to broadband is woefully short of the target set by DoT (See Table 2).12 The number of internet subscribers too would be significantly below the policy target, were it not for the rapid penetration of mobile internet. There are about 32 million mobile subscribers accessing the internet through wireless networks today, compared to about 11 million who access it through the fixed network. India seriously lags behind on broadband. Even TRAI has conceded that its future targets are unlikely to be achieved, unless critical issues inhibiting broadband expansion in urban as well as rural areas are addressed. These include both policy and regulatory constraints.13

Fixed line subscribersMobile subscribersLog. (Rate of growth of fixed lines)Log. (Rate of growth of mobiles)

0

5022

1

27

2

32

4

38

6

41

13

4333

47 5746

150

41

165

39

261

39

315

100

150

200

250

300

350

Mar 99

Mar 00

Mar 01

Mar 02

Mar 03

Mar 04

Mar 05

Mar 06

Mar 07

Mar 08

Sep 08

Subs

crib

ers

(mill

ion)

-40

-20

0

20

60

100

140

180

40

80

120

160

Rat

e of

gro

wth

(%)

10

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

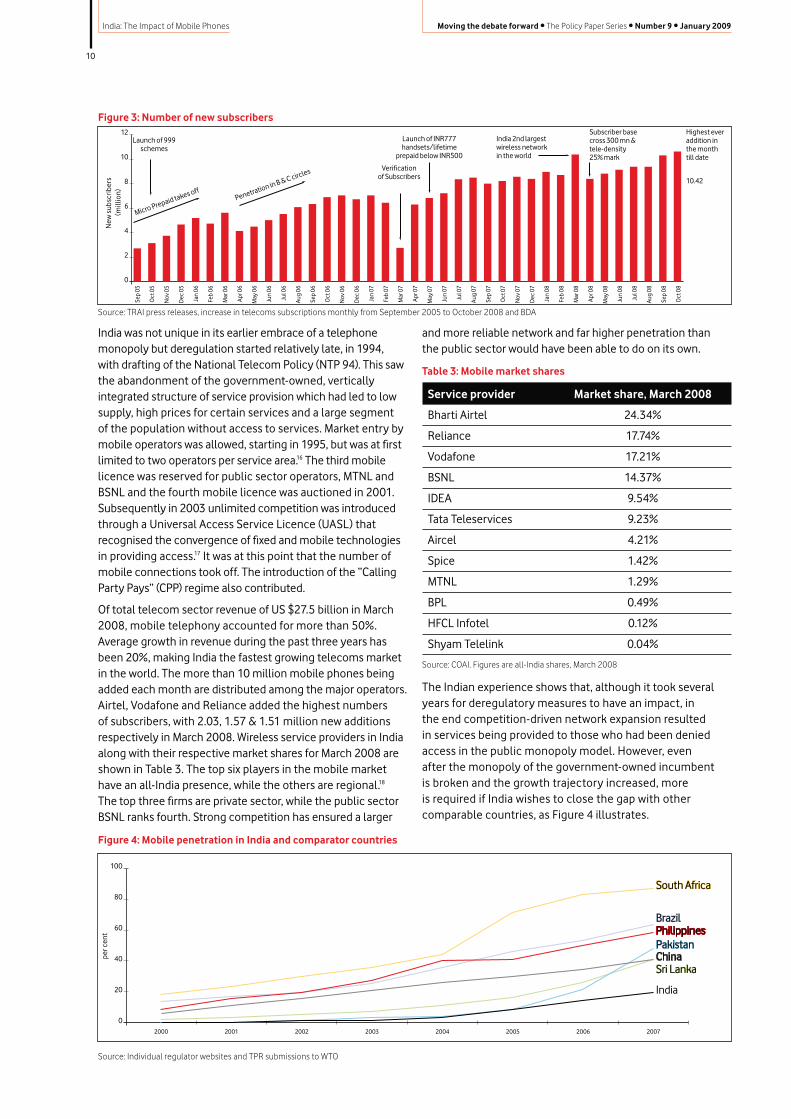

Figure 3: Number of new subscribers

Source: TRAI press releases, increase in telecoms subscriptions monthly from September 2005 to October 2008 and BDA

and more reliable network and far higher penetration than the public sector would have been able to do on its own.

Table 3: Mobile market shares

Service provider Market share, March 2008

Bharti Airtel 24.34%

Reliance 17.74%

Vodafone 17.21%

BSNL 14.37%

IDEA 9.54%

Tata Teleservices 9.23%

Aircel 4.21%

Spice 1.42%

MTNL 1.29%

BPL 0.49%

HFCL Infotel 0.12%

Shyam Telelink 0.04%

Source: COAI. Figures are all-India shares, March 2008

The Indian experience shows that, although it took several years for deregulatory measures to have an impact, in the end competition-driven network expansion resulted in services being provided to those who had been denied access in the public monopoly model. However, even after the monopoly of the government-owned incumbent is broken and the growth trajectory increased, more is required if India wishes to close the gap with other comparable countries, as Figure 4 illustrates.

India was not unique in its earlier embrace of a telephone monopoly but deregulation started relatively late, in 1994, with drafting of the National Telecom Policy (NTP 94). This saw the abandonment of the government-owned, vertically integrated structure of service provision which had led to low supply, high prices for certain services and a large segment of the population without access to services. Market entry by mobile operators was allowed, starting in 1995, but was at first limited to two operators per service area.16 The third mobile licence was reserved for public sector operators, MTNL and BSNL and the fourth mobile licence was auctioned in 2001. Subsequently in 2003 unlimited competition was introduced through a Universal Access Service Licence (UASL) that recognised the convergence of fixed and mobile technologies in providing access.17 It was at this point that the number of mobile connections took off. The introduction of the “Calling Party Pays” (CPP) regime also contributed.

Of total telecom sector revenue of US $27.5 billion in March 2008, mobile telephony accounted for more than 50%. Average growth in revenue during the past three years has been 20%, making India the fastest growing telecoms market in the world. The more than 10 million mobile phones being added each month are distributed among the major operators. Airtel, Vodafone and Reliance added the highest numbers of subscribers, with 2.03, 1.57 & 1.51 million new additions respectively in March 2008. Wireless service providers in India along with their respective market shares for March 2008 are shown in Table 3. The top six players in the mobile market have an all-India presence, while the others are regional.18 The top three firms are private sector, while the public sector BSNL ranks fourth. Strong competition has ensured a larger

Figure 4: Mobile penetration in India and comparator countries

Source: Individual regulator websites and TPR submissions to WTO

0

2

4

6

8

10

12

New

sub

scrib

ers

(mill

ion)

Sep

05

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr 0

6

May

06

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07

Feb

07

Mar

07

Apr 0

7

May

07

Jun

07

Jul 0

7

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

Feb

08

Mar

08

Apr 0

8

May

08

Jun

08

Jul 0

8

Aug

08

Sep

08

Oct

08

Jan

08

Launch of 999schemes

Micro Prepaid takes off

Verificationof Subscribers

Launch of INR777handsets/lifetime

prepaid below INR500

India 2nd largestwireless networkin the world

Highest everaddition inthe monthtill date

10.42

Subscriber base cross 300 mn &tele-density 25% mark

Penetration in B & C circles

0

20

40

60

80

100

per c

ent

2000 2001 2002 2003 2004 2005 2006 2007

PakistanChinaSri Lanka

South Africa

BrazilPhilippines

India

PakistanChinaSri Lanka

South Africa

BrazilPhilippines

11

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

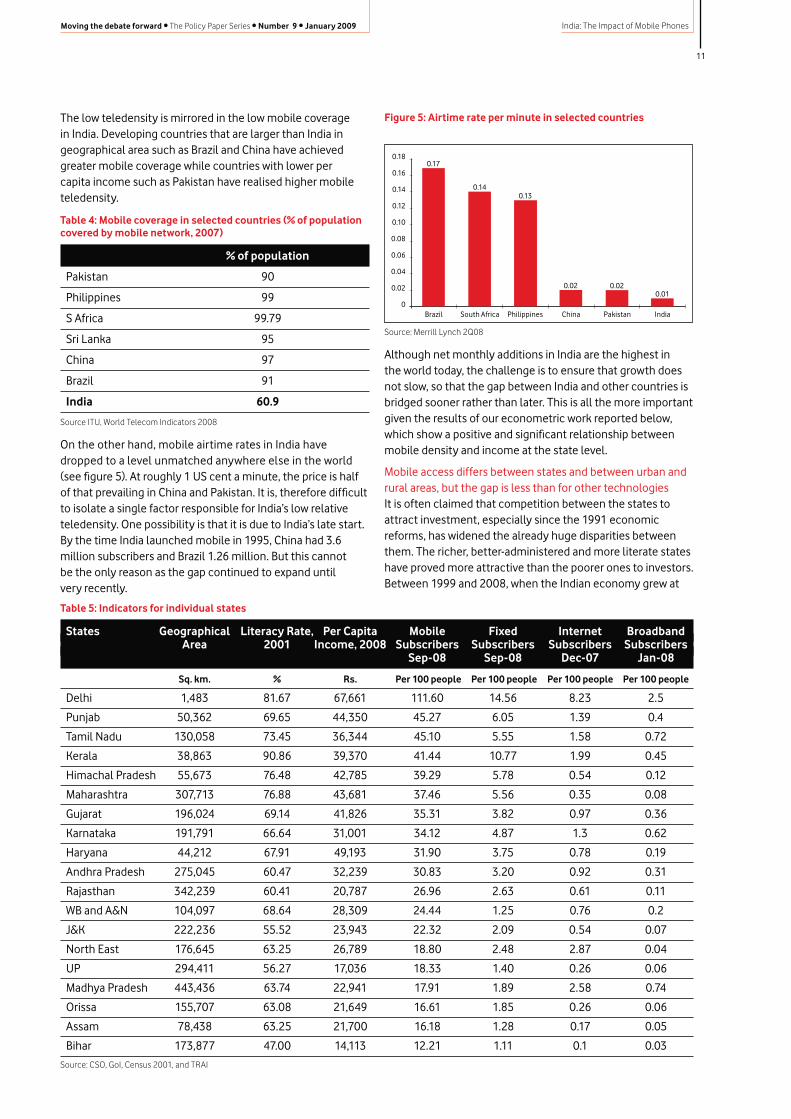

The low teledensity is mirrored in the low mobile coverage in India. Developing countries that are larger than India in geographical area such as Brazil and China have achieved greater mobile coverage while countries with lower per capita income such as Pakistan have realised higher mobile teledensity.

Table 4: Mobile coverage in selected countries (% of population covered by mobile network, 2007)

% of population

Pakistan 90

Philippines 99

S Africa 99.79

Sri Lanka 95

China 97

Brazil 91

India 60.9

Source ITU, World Telecom Indicators 2008

On the other hand, mobile airtime rates in India have dropped to a level unmatched anywhere else in the world (see figure 5). At roughly 1 US cent a minute, the price is half of that prevailing in China and Pakistan. It is, therefore difficult to isolate a single factor responsible for India’s low relative teledensity. One possibility is that it is due to India’s late start. By the time India launched mobile in 1995, China had 3.6 million subscribers and Brazil 1.26 million. But this cannot be the only reason as the gap continued to expand until very recently.

Figure 5: Airtime rate per minute in selected countries

0

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

Brazil

0.17

South Africa Philippines China Pakistan India

0.140.13

0.02 0.020.01

Source: Merrill Lynch 2Q08

Although net monthly additions in India are the highest in the world today, the challenge is to ensure that growth does not slow, so that the gap between India and other countries is bridged sooner rather than later. This is all the more important given the results of our econometric work reported below, which show a positive and significant relationship between mobile density and income at the state level.

Mobile access differs between states and between urban and rural areas, but the gap is less than for other technologiesIt is often claimed that competition between the states to attract investment, especially since the 1991 economic reforms, has widened the already huge disparities between them. The richer, better-administered and more literate states have proved more attractive than the poorer ones to investors. Between 1999 and 2008, when the Indian economy grew at

Table 5: Indicators for individual states

States Geographical Literacy Rate, Per Capita Mobile Fixed Internet Broadband Area 2001 Income, 2008 Subscribers Subscribers Subscribers Subscribers Sep-08 Sep-08 Dec-07 Jan-08

Sq. km. % Rs. Per 100 people Per 100 people Per 100 people Per 100 people

Delhi 1,483 81.67 67,661 111.60 14.56 8.23 2.5

Punjab 50,362 69.65 44,350 45.27 6.05 1.39 0.4

Tamil Nadu 130,058 73.45 36,344 45.10 5.55 1.58 0.72

Kerala 38,863 90.86 39,370 41.44 10.77 1.99 0.45

Himachal Pradesh 55,673 76.48 42,785 39.29 5.78 0.54 0.12

Maharashtra 307,713 76.88 43,681 37.46 5.56 0.35 0.08

Gujarat 196,024 69.14 41,826 35.31 3.82 0.97 0.36

Karnataka 191,791 66.64 31,001 34.12 4.87 1.3 0.62

Haryana 44,212 67.91 49,193 31.90 3.75 0.78 0.19

Andhra Pradesh 275,045 60.47 32,239 30.83 3.20 0.92 0.31

Rajasthan 342,239 60.41 20,787 26.96 2.63 0.61 0.11

WB and A&N 104,097 68.64 28,309 24.44 1.25 0.76 0.2

J&K 222,236 55.52 23,943 22.32 2.09 0.54 0.07

North East 176,645 63.25 26,789 18.80 2.48 2.87 0.04

UP 294,411 56.27 17,036 18.33 1.40 0.26 0.06

Madhya Pradesh 443,436 63.74 22,941 17.91 1.89 2.58 0.74

Orissa 155,707 63.08 21,649 16.61 1.85 0.26 0.06

Assam 78,438 63.25 21,700 16.18 1.28 0.17 0.05

Bihar 173,877 47.00 14,113 12.21 1.11 0.1 0.03

Source: CSO, GoI, Census 2001, and TRAI

12

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

an average annual rate of 7.3%, many richer states grew even faster: Gujarat at 8.8%, Haryana at 8.7% and Delhi at 7.4%. Among the poorest and most populous states, Bihar grew at 5.1%, Uttar Pradesh at 4.4% and Madhya Pradesh at 3.5%.19

Mobile density to a large degree reflects the differences in per capita income across states. The simple correlation coefficient between per capita income and mobile density for 2008 is 0.87 (where 1 would indicate perfect correlation). The corresponding correlation coefficients between per capita income and other ICT indicators across states are also positive but not as large; between fixed and per capita income it is 0.8, for internet and per capita income it is 0.66 while for broadband and per capita income it is 0.62.

Table 6: Coefficient of variation across states

Mobile Fixed Internet Broadband Density Density Density Density

0.66 0.77 1.04 1.16

Source: Author’s estimates

Per capita income is however not the only determinant of penetration rate. A study published by Vodafone in 2005 reported that certain African countries that started early down the path of telecom liberalisation – such as Gabon and Mauritius – had achieved mobile penetration rates that were surprisingly high given their social and economic indicators; and the converse is true for countries where there were no early private licences issued, such as Algeria or Nigeria.20 Such variations also exist across Indian States. For example Haryana is the second richest state in India after Delhi, but ranks ninth in overall mobile density, while Punjab and Tamil Nadu have similar penetration rates, although Punjab is 25% more prosperous. On the other hand, Kerala has a relatively lower per capita income, but a very high mobile penetration rate. One explanation might be a large migrant population from Kerala working in the Middle East wishing to stay in touch with family and friends. Metros, like Delhi and Mumbai, that had a distinct first mover advantage, have achieved much higher mobile penetration rates. While the correlation of mobile density with share of service sector GSDP and literacy rate is positive, (0.72 and 0.46 respectively), and with geographical size it is negative (-0.46), the phenomenon of the diffusion of mobile, however, cuts across many of these obvious characteristics.

There are too many differences across and within Indian states to identify robust explanations for differences in penetration and usage. However competition-driven network expansion has certainly driven airtime charges and ARPUs to extremely low levels. By September 2008, the median number of wireless operators in each state was 6, with only one state having as few as 4 and the rest 5 or more operators. The situation today is extraordinarily different compared to the late nineties, when only a few states had access to mobile services and the service itself was limited to the creamy layer.

As India’s economy grows rapidly, what will happen to the regional disparities? Mobile penetration is growing faster in states with the lowest current levels, showing a trend towards convergence. Internet and broadband penetration are even lower than fixed line penetration. The coefficient of variation across states for the four ICT indicators – mobile, fixed, internet and broadband – is the lowest for mobile, indicating greater uniformity between states than other ICT indicators. This evidence from Indian states is consistent with evidence of convergence in mobile contrasting to divergence in access to other technologies elsewhere in the world.

Interestingly, both internet and broadband availability in India have until now been associated with Public Switched Telephone Network (PSTN) infrastructure consisting of copper loops to subscriber premises. The cost of providing access through this platform is greater than for wireless and is influenced by the distance between the subscriber and the local exchange, the gauge of the phone wire, and the type of technology. Providing high speed broadband access through wireless is cheaper, but depends on the availability and price of spectrum and the extent of backhaul network essential to provide services. Sufficient spectrum has not been made available to provide high-speed internet access. Further, given India’s landmass, the cost of creating backhaul infrastructure in rural areas is substantial and has been a significant barrier. Consequently, the growth of internet access and data services has been severely sluggish. Broadband penetration is negligible and far short of the policy target. At a policy level, therefore, there is need to recognise the significance of wireless in not only delivery of voice, but also data services. Growth in mobile telephony for voice services is important but not sufficient to be competitive on a global stage.

Figure 6: measures of mobile usage across states

Source: Authors calculation based on TRAI.data. Figures for March 2008.

ARPUMOU

0

100

200

300

400

500

600

700

MO

U, A

RPU

STATES

Assam

Chennai

Gujarat

Haryana

Karnatka

Kolkata

Maharashtra N.E.

Punjab

T.N.

U.P. (W)

A.P.

Bihar

Delhi

H.P.

J & K

Kerala

M.P.

Mumbai

Orissa

Rajasthan

U.P. (E)

W.B. & A &

N

13

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

At a policy level, there is a need to recognise the significance of wireless in not only delivery of voice, but also data services, and to stimulate the installation of backhaul infrastructure in rural areas through the use of appropriate incentives.

Table 7: A growth of mobile telephony in each state

1 J&K 268.35

2 North East 149.97

3 WB and A&N 141.43

4 Himachal Pradesh 121.46

5 Gujarat 113.21

6 Andhra Pradesh 110.92

7 Assam 110.80

8 Tamil Nadu 109.34

9 Bihar 108.60

10 Orissa 107.05

11 Madhya Pradesh 101.04

12 Haryana 100.75

13 Rajasthan 100.39

14 UP(E) 92.57

15 Punjab 92.26

16 Kerala 87.85

17 Maharashtra 85.01

18 Karnataka 81.67

19 UP(W) 79.91

20 Chennai 64.60

21 Kolkata 62.35

22 Mumbai 55.06

23 Delhi 53.20

Source: Author estimates based on TRAI data; growth rate is annual average from inception of mobile services in each state to March 2008.

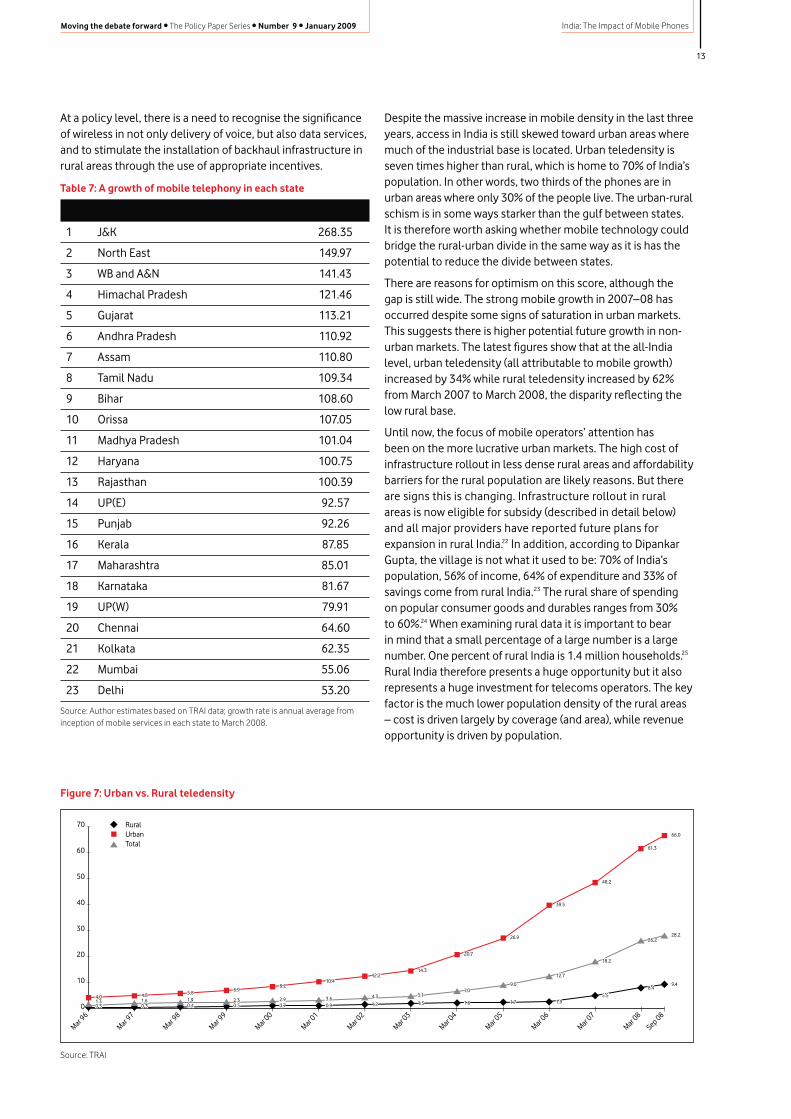

Despite the massive increase in mobile density in the last three years, access in India is still skewed toward urban areas where much of the industrial base is located. Urban teledensity is seven times higher than rural, which is home to 70% of India’s population. In other words, two thirds of the phones are in urban areas where only 30% of the people live. The urban-rural schism is in some ways starker than the gulf between states. It is therefore worth asking whether mobile technology could bridge the rural-urban divide in the same way as it is has the potential to reduce the divide between states.

There are reasons for optimism on this score, although the gap is still wide. The strong mobile growth in 2007–08 has occurred despite some signs of saturation in urban markets. This suggests there is higher potential future growth in non-urban markets. The latest figures show that at the all-India level, urban teledensity (all attributable to mobile growth) increased by 34% while rural teledensity increased by 62% from March 2007 to March 2008, the disparity reflecting the low rural base.

Until now, the focus of mobile operators’ attention has been on the more lucrative urban markets. The high cost of infrastructure rollout in less dense rural areas and affordability barriers for the rural population are likely reasons. But there are signs this is changing. Infrastructure rollout in rural areas is now eligible for subsidy (described in detail below) and all major providers have reported future plans for expansion in rural India.22 In addition, according to Dipankar Gupta, the village is not what it used to be: 70% of India’s population, 56% of income, 64% of expenditure and 33% of savings come from rural India.23 The rural share of spending on popular consumer goods and durables ranges from 30% to 60%.24 When examining rural data it is important to bear in mind that a small percentage of a large number is a large number. One percent of rural India is 1.4 million households.25 Rural India therefore presents a huge opportunity but it also represents a huge investment for telecoms operators. The key factor is the much lower population density of the rural areas – cost is driven largely by coverage (and area), while revenue opportunity is driven by population.

RuralUrbanTotal

0

10

20

30

40

50

60

70

Mar 97

Mar 96

Mar 98

Mar 99

Mar 00

Mar 01

Mar 02

Mar 03

Mar 04

Mar 05

Mar 06

Mar 07

Mar 08

Sep 08

0.31.34.0

0.31.64.8

0.41.95.8

0.52.3

6.9

0.72.9

8.2

0.93.6

10.4

1.2

4.3

12.2

1.5

5.1

14.3

1.6

7.0

20.7

1.7

9.0

26.9

1.9

12.7

39.5

5.5

18.2

48.2

8.4

26.2

61.3

9.4

28.2

66.0

0.31.34.0

0.31.64.8

0.41.95.8

0.52.3

6.9

0.72.9

8.2

0.93.6

10.4

1.2

4.3

12.2

1.5

5.1

14.3

1.6

7.0

20.7

1.7

9.0

26.9

1.9

12.7

39.5

5.5

18.2

48.2

8.4

26.2

61.3

9.4

28.2

66.0

Figure 7: Urban vs. Rural teledensity

Source: TRAI

14

India: The Impact of Mobile Phones Moving the debate forward • The Policy Paper Series • Number 9 • January 2009

There is no doubt about the potential of mobile technology in addressing the digital divide. Already there is more uniformity in mobile penetration between states and between rural and urban areas compared to any other ICT indicator. Helping the process along effectively will require appropriate regulation.

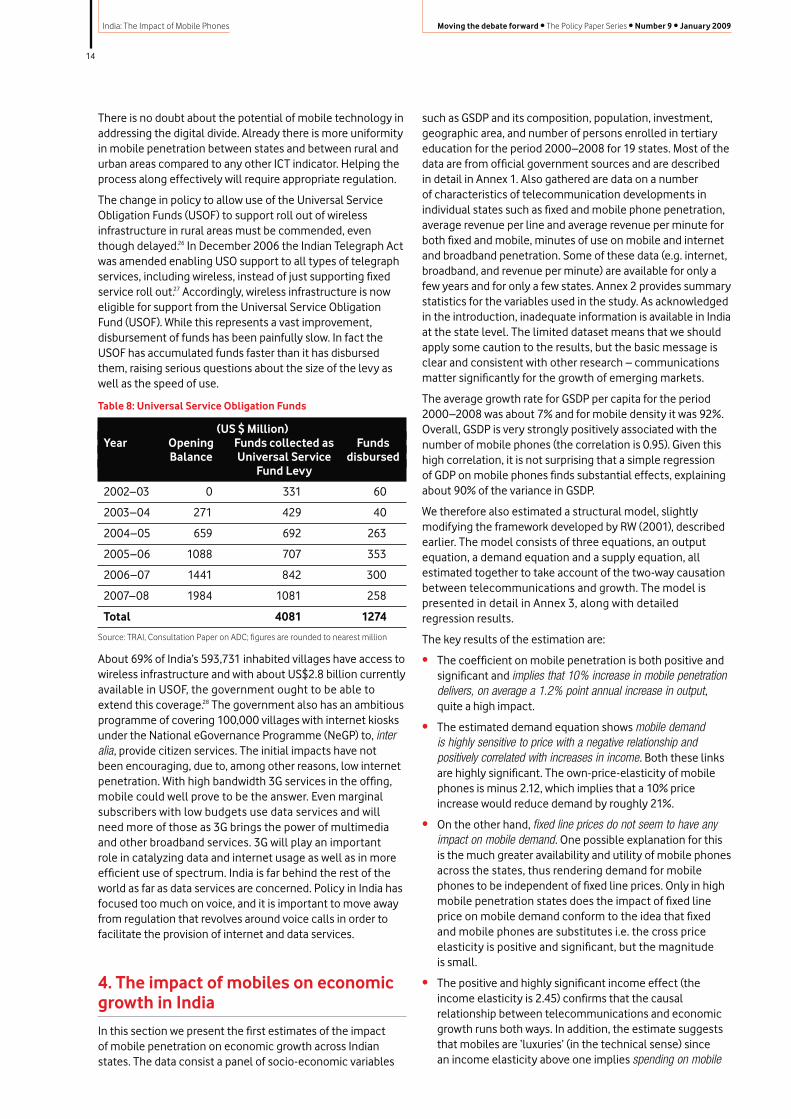

The change in policy to allow use of the Universal Service Obligation Funds (USOF) to support roll out of wireless infrastructure in rural areas must be commended, even though delayed.26 In December 2006 the Indian Telegraph Act was amended enabling USO support to all types of telegraph services, including wireless, instead of just supporting fixed service roll out.27 Accordingly, wireless infrastructure is now eligible for support from the Universal Service Obligation Fund (USOF). While this represents a vast improvement, disbursement of funds has been painfully slow. In fact the USOF has accumulated funds faster than it has disbursed them, raising serious questions about the size of the levy as well as the speed of use.

Table 8: Universal Service Obligation Funds

(US $ Million) Year Opening Funds collected as Funds Balance Universal Service disbursed Fund Levy

2002–03 0 331 60

2003–04 271 429 40

2004–05 659 692 263

2005–06 1088 707 353

2006–07 1441 842 300

2007–08 1984 1081 258

Total 4081 1274

Source: TRAI, Consultation Paper on ADC; figures are rounded to nearest million

About 69% of India’s 593,731 inhabited villages have access to wireless infrastructure and with about US$2.8 billion currently available in USOF, the government ought to be able to extend this coverage.28 The government also has an ambitious programme of covering 100,000 villages with internet kiosks under the National eGovernance Programme (NeGP) to, inter alia, provide citizen services. The initial impacts have not been encouraging, due to, among other reasons, low internet penetration. With high bandwidth 3G services in the offing, mobile could well prove to be the answer. Even marginal subscribers with low budgets use data services and will need more of those as 3G brings the power of multimedia and other broadband services. 3G will play an important role in catalyzing data and internet usage as well as in more efficient use of spectrum. India is far behind the rest of the world as far as data services are concerned. Policy in India has focused too much on voice, and it is important to move away from regulation that revolves around voice calls in order to facilitate the provision of internet and data services.

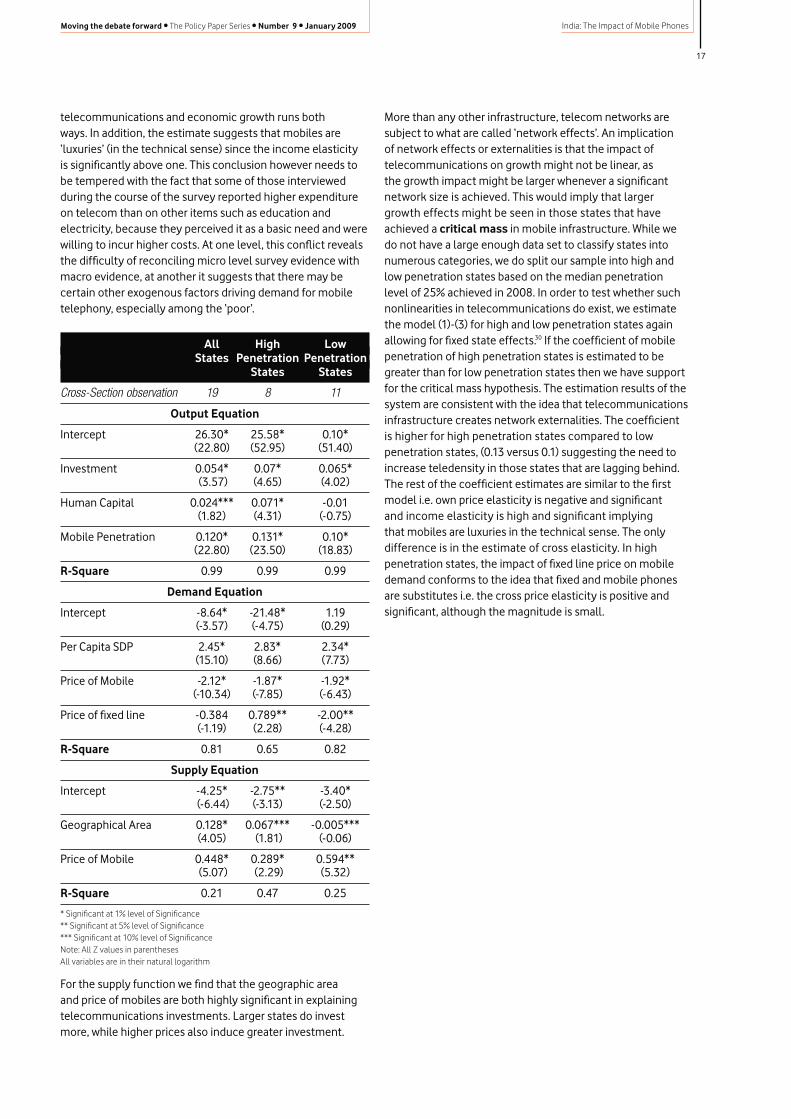

4. The impact of mobiles on economic growth in India

In this section we present the first estimates of the impact of mobile penetration on economic growth across Indian states. The data consist a panel of socio-economic variables

such as GSDP and its composition, population, investment, geographic area, and number of persons enrolled in tertiary education for the period 2000–2008 for 19 states. Most of the data are from official government sources and are described in detail in Annex 1. Also gathered are data on a number of characteristics of telecommunication developments in individual states such as fixed and mobile phone penetration, average revenue per line and average revenue per minute for both fixed and mobile, minutes of use on mobile and internet and broadband penetration. Some of these data (e.g. internet, broadband, and revenue per minute) are available for only a few years and for only a few states. Annex 2 provides summary statistics for the variables used in the study. As acknowledged in the introduction, inadequate information is available in India at the state level. The limited dataset means that we should apply some caution to the results, but the basic message is clear and consistent with other research – communications matter significantly for the growth of emerging markets.

The average growth rate for GSDP per capita for the period 2000–2008 was about 7% and for mobile density it was 92%. Overall, GSDP is very strongly positively associated with the number of mobile phones (the correlation is 0.95). Given this high correlation, it is not surprising that a simple regression of GDP on mobile phones finds substantial effects, explaining about 90% of the variance in GSDP.

We therefore also estimated a structural model, slightly modifying the framework developed by RW (2001), described earlier. The model consists of three equations, an output equation, a demand equation and a supply equation, all estimated together to take account of the two-way causation between telecommunications and growth. The model is presented in detail in Annex 3, along with detailed regression results.

The key results of the estimation are:

• The coefficient on mobile penetration is both positive and significant and implies that 10% increase in mobile penetration delivers, on average a 1.2% point annual increase in output, quite a high impact.

• The estimated demand equation shows mobile demand is highly sensitive to price with a negative relationship and positively correlated with increases in income. Both these links are highly significant. The own-price-elasticity of mobile phones is minus 2.12, which implies that a 10% price increase would reduce demand by roughly 21%.

• On the other hand, fixed line prices do not seem to have any impact on mobile demand. One possible explanation for this is the much greater availability and utility of mobile phones across the states, thus rendering demand for mobile phones to be independent of fixed line prices. Only in high mobile penetration states does the impact of fixed line price on mobile demand conform to the idea that fixed and mobile phones are substitutes i.e. the cross price elasticity is positive and significant, but the magnitude is small.

• The positive and highly significant income effect (the income elasticity is 2.45) confirms that the causal relationship between telecommunications and economic growth runs both ways. In addition, the estimate suggests that mobiles are ‘luxuries’ (in the technical sense) since an income elasticity above one implies spending on mobile

15

India: The Impact of Mobile PhonesMoving the debate forward • The Policy Paper Series • Number 9 • January 2009

rises more than in proportion with income. This conclusion however needs to be tempered with the fact that some people surveyed reported higher expenditure on telecoms than on other items such as education and electricity, because they perceived it as a basic need and were willing to incur higher costs. At one level, this conflict reveals the difficulty of reconciling micro level survey evidence with macro evidence; at another it suggests that there may be certain other exogenous factors driving demand for mobile telephony, especially among people with low incomes.

• More than any other infrastructure, telecom networks are subject to ‘network effects’ meaning the growth impact might be larger whenever a significant threshold network size is achieved. This would imply that larger growth effects might be seen in those states that have achieved a critical mass in mobile infrastructure. We split our sample into high and low penetration states based on the median penetration level of 25% achieved in 2008 to test whether such nonlinearities in telecommunications exist. The coefficient is higher for high penetration states compared to low penetration states, (0.13 versus 0.1), implying that there is a threshold for critical mass, which has significant policy implications.

5. Conclusions

Despite the challenges, it is difficult not to have an acute sense that this is a momentous time for telecommunications in India. This sense is palpable in the sector as 10 years after liberalisation, multinational companies which left India are returning to bid for 3G licences. A unique combination of factors is now in play that could usher in a renewed period of growth for telecommunications and consequently enhanced economic activity in the individual states. Past policies have delivered some important successes. However, India lags far behind comparator countries in telecommunications access, and there is huge untapped potential in certain states and in rural areas, and increasingly in poor urban areas. There is an urgent need to bridge the gaps.