35

India’s IT/ITeS Industry: The Next Phase Non-linear Growth & Broad-Based Innovation Dr. Anupam Khanna. Chief Economist Knowledge-Based Capital Conference OECD, Paris February 14, 2013

India’s IT/ITeS Industry: The Next Phase

Non-linear Growth & Broad-Based Innovation

Dr. Anupam Khanna. Chief Economist

Knowledge-Based Capital Conference

OECD, Paris February 14, 2013

Implications for the IT-BPO Industry

2 22-Feb-13

Hardware Products Services

IT Services BPO

• Project

Oriented

• Outsourci

ng

• Support &

Training

Embedded

Systems

• Software

Products

• System

Software

• Enterprise

applications

• Vertical

applications

• Personal

Computers

• Network

Equipment

• Storage and

Security

• Servers

• Printers

IT-BPO

ER&D OSPD

• Horizontal

Specific

• Vertical

Specific

3 22-Feb-13

The IT-BPO industry segmentation

INDIAN IT-BPO INDUSTRY

Source: NASSCOM

Brief history of Indian IT-BPO revenue

4 22-Feb-13

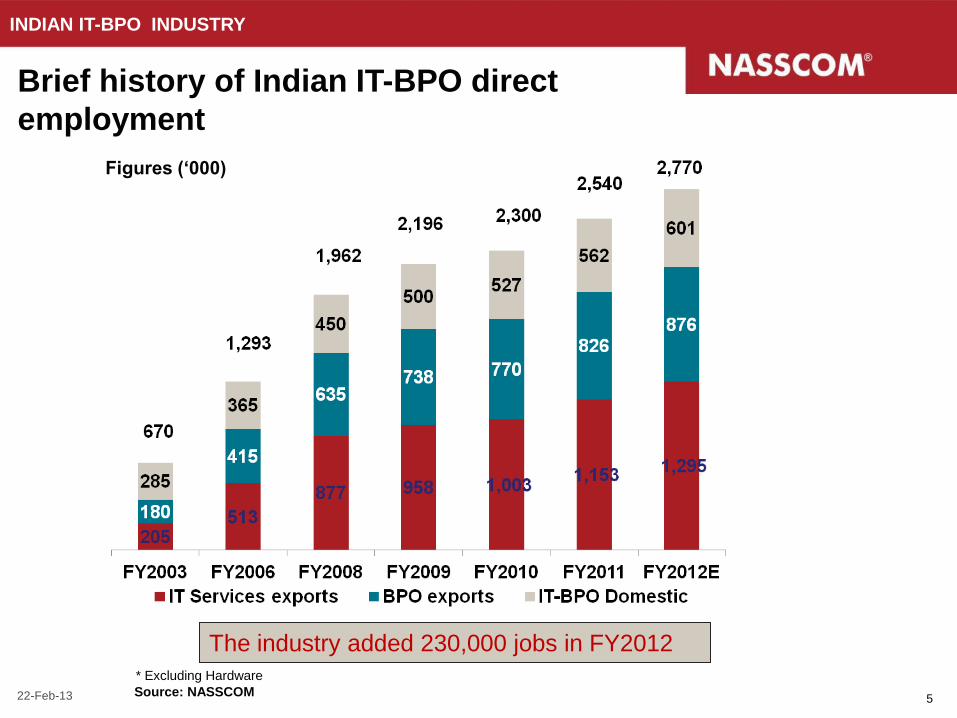

The industry added 230,000 jobs in FY2012

Brief history of Indian IT-BPO direct

employment

INDIAN IT-BPO INDUSTRY

Source: NASSCOM

* Excluding Hardware

Figures (‘000)

5 22-Feb-13

6

Trends in World Exports and Indian Exports of Goods and Services in current USD (Index=100 in 1990)

7

Growth Rate of Services Exports, VariousCountries

Share of Services Exports

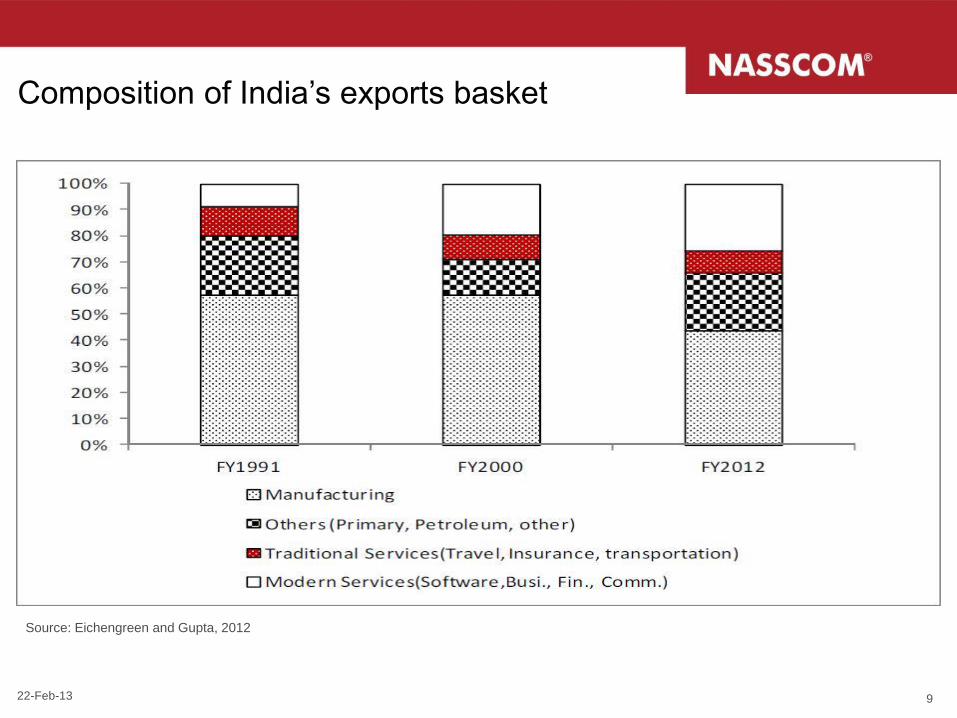

Composition of India’s exports basket

Source: Eichengreen and Gupta, 2012

9 22-Feb-13

10

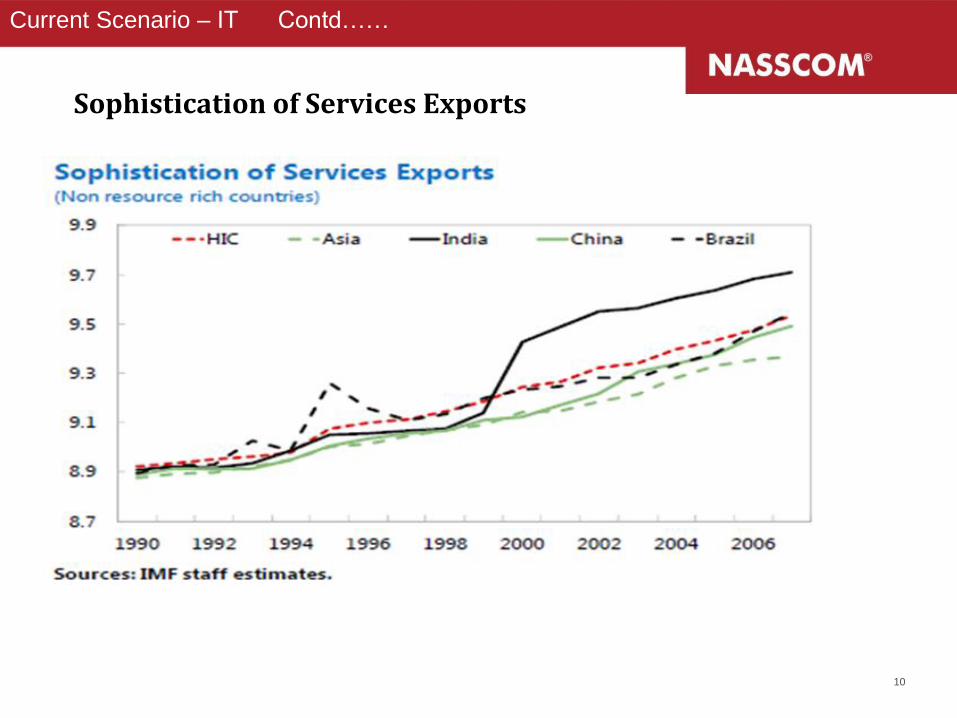

Current Scenario – IT Contd……

Sophistication of Services Exports

11

Trends in Service Exports of India Since 1990

Software+Misc Services (Bus, Fin,

etc.) 44%

Travel 32%

Insurance 2%

Transportation

22%

1990-91 Service Exports = $4,551 million

Misc Services (Bus, Fin, etc.)

22%

Travel 22%

Insurance 2%

Transportation 13%

Software Services

41%

2000-01 Service Exports = $16,268 million

Misc Services (Bus, Fin, etc.)

26%

Travel 12%

Insurance 2%

Transportation 12%

Software Services

48%

2010-11 Service Exports = $1,31972 million

Services Trade – Surprising Resilience

• Experience During Last Crisis (2008)

• Comparison with Manufactures

• Differences Across Service Sectors

• Transport vs Tourism vs Business Services

• Finance vs Insurance

• Supply Side – Low Vulnerability to Credit Squeeze

• Demand Side Features of Business Services

• No inventory or vintage effects

• Less Discretionary Decision-Making

• Long-Term relationships

12 22-Feb-13

Industry moving from “Enterprise service providers”

to “Enterprise solution creators”

Source: CLSA, NASSCOM

DIMENSIONS 1990 2000 2010 onwards

SERVICE DELIVERY

DEALS STRUCTURE

PRICING

RESOURCES

TIME TO DEPLOY

SERVICES

STRUCTURE STRUCTURE STRUCTURE

STRUCTURE STRUCTURE STRUCTURE

STRUCTURE STRUCTURE STRUCTURE

STRUCTURE STRUCTURE STRUCTURE

STRUCTURE STRUCTURE STRUCTURE

STRUCTURE STRUCTURE STRUCTURE

Custom,

People-driven

Input-based,

Fixed costs

Staff augmentation

Years Months Weeks or Days

Industrialised, capacity

and method-driven Capacity and IP-driven

Small deal wins, short

duration. End-to-end

Output-based, fixed

costs or gain share Pay per use

Fixed capacity Non-linear

TECHNOLOGY STRUCTURE STRUCTURE STRUCTURE Mainframe to Client

server

Y2K, dotcom

enablement

Cloud, virtualisation,

Mobile computing

Source: CLSA, NASSCOM

CUSTOMER CENTRIC

Enterprise services Enterprise solutions

Multiple vendors, large

size, long duration

Deals related to CAD/M

and maintainence

One client, one solution

Service providers’ value proposition maturing beyond

cost to delivering business outcome

Source: NASSCOM

Service Providers

<2004 2004-2007 2007-2009

•Asset heavy •Dedicated/captive model

•Time & material •Staff augmentation

•Asset-light •Shared services •Resource sharing •Test Labs •Emergence of Managed services

• Shared, Managed services

• SLA driven •Agile •Cloud, Platform •Test Labs, CoEs • Pay-per-use

Shift to Managed

services

2009-2013

Shift to “Pay Per

Use” model

• Shared, Managed services

• Business Tech Mgmt

•Monetisation of assets/platforms

•XaaS, Cloud, Mobility, Social

•Agile methodology

• Verticalised CoEs • Pay-per-use, Risk-reward

COST

• Labour arbitrage

QUALITY

• Process excellence

MATURITY

VA

LU

E

OUTCOME

• Verticalisation

• Innovation

• Transformation

DIFFERENTIATION

• Lower lifecycle

costs

• Faster time to

market

• Differentiation

Efficient Delivery Effective Outcomes

‘Verticalisation’–Business transformer

1. Organisational Design

Verticalised across business functions –

going beyond sales

2. Organic- Internal Capability

Investments in vertical specific tools and

talent

E.g. Hiring doctors/nurses for domain

intensive healthcare - medical coding etc.

3. Inorganic- Value Additions

Fill vertical specific gaps through

acquisitions or enter newer verticals

E.g. Acquisition of platforms such as Life

Admin / Claim adjudication (Insurance)

4. Alignment of KPIs, metrics

Vertical specific P&L accountability, goals

E.g. Horizontal capabilities such as

analytics getting aligned to verticals

15 22-Feb-13

Effort

based

pricing 3. Technology/

IP

Proprietary

software product

3rd party/

custom s/w

2. Process

expertise

Patented

process

flow

Standard-

ized approach/

process flow

1. Go-to-market

model

Direct sales –

Services

Direct + Indirect (Multi-

product, Multi-

business)

People

factory

2. Talent

deployment

model

Dedicated -

visible

3. Technology

deployment

model

Customer

owned

Multi tenant

– On

demand

1. People

expertise

Industry

recognized thought

leaders

Process/

project mgmt

experts

4. Data and

analytics

Advanced Analytics on

proprietary data

Customer data

management

4. Transaction/

Pricing model Outcome/risk

based pricing

Effort based

pricing

Proprietary

platform

Accelerators/

APIs

Dedicated -

invisible

Team

shared at

account

level

Direct sales – Services +

Solutions/ IP

Direct sales – Services +

Products

Single

tenant –

limited

control

Single

tenant –

full

control

Advanced domain

experts

Basic domain

experts Bench-

marks on

process

metrics

Reposi-

tory of

best

practices

Advanced analytics on

customer data

Basic analytics on

customer data Transaction/

Usage based

pricing

IP based

pricing

Define the business outcome

you want to deliver

Building successful “Alternate Business Models” – leading

to significant shifts in business models

Build the foundational capabilities required to deliver ABM

(1. Consultative selling, 2. Product/IP management, 3. Customer Relationship

management, 4. Alliance/ Partnership management, and 5. Risk management)

NEW SLIDE

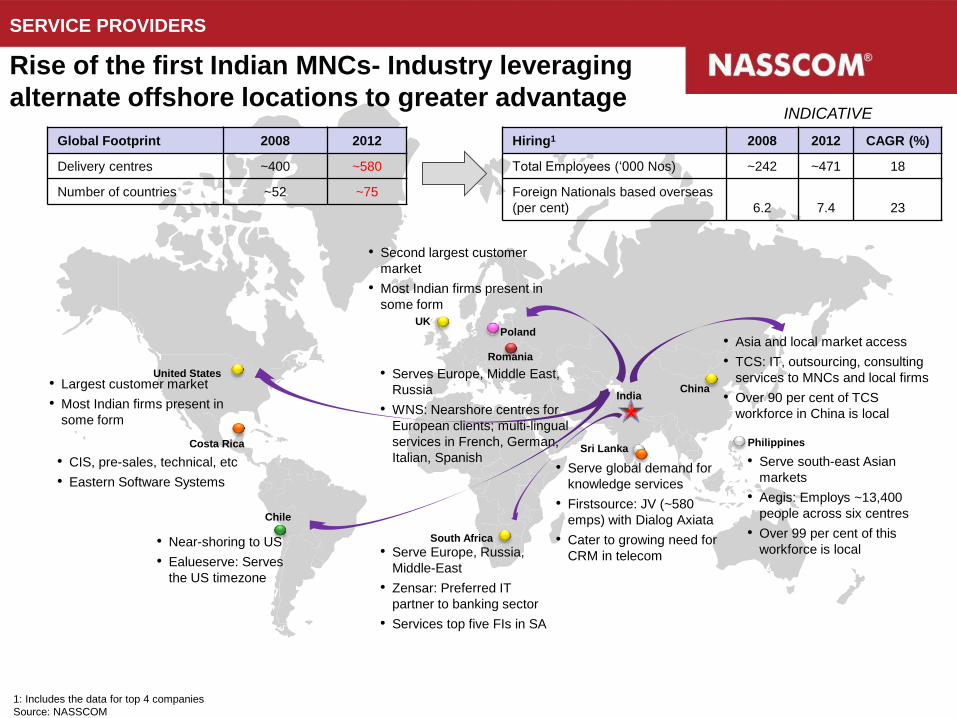

1: Includes the data for top 4 companies

Source: NASSCOM

China India

UK

Romania

Poland

South Africa

United States

Chile

• Serve global demand for

knowledge services

• Firstsource: JV (~580

emps) with Dialog Axiata

• Cater to growing need for

CRM in telecom

• Serves Europe, Middle East,

Russia

• WNS: Nearshore centres for

European clients; multi-lingual

services in French, German,

Italian, Spanish

• Near-shoring to US

• Ealueserve: Serves

the US timezone

Sri Lanka Philippines Costa Rica

• Serve Europe, Russia,

Middle-East

• Zensar: Preferred IT

partner to banking sector

• Services top five FIs in SA

INDICATIVE

SERVICE PROVIDERS

Rise of the first Indian MNCs- Industry leveraging

alternate offshore locations to greater advantage

Global Footprint 2008 2012

Delivery centres ~400 ~580

Number of countries ~52 ~75

Hiring1 2008 2012 CAGR (%)

Total Employees (‘000 Nos) ~242 ~471 18

Foreign Nationals based overseas

(per cent) 6.2 7.4 23

• Serve south-east Asian

markets

• Aegis: Employs ~13,400

people across six centres

• Over 99 per cent of this

workforce is local

• Asia and local market access

• TCS: IT, outsourcing, consulting

services to MNCs and local firms

• Over 90 per cent of TCS

workforce in China is local

• Largest customer market

• Most Indian firms present in

some form

• Second largest customer

market

• Most Indian firms present in

some form

• CIS, pre-sales, technical, etc

• Eastern Software Systems

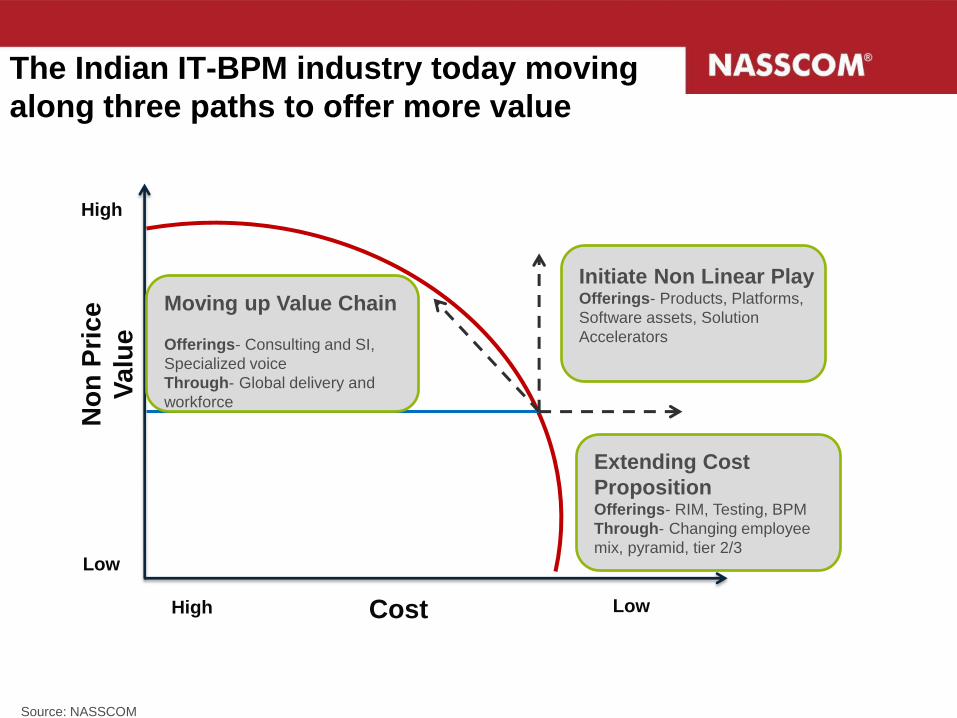

Cost Low

No

n P

ric

e

Va

lue

High

High

Low

Initiate Non Linear Play Offerings- Products, Platforms,

Software assets, Solution

Accelerators

Extending Cost

Proposition Offerings- RIM, Testing, BPM

Through- Changing employee

mix, pyramid, tier 2/3

Moving up Value Chain

Offerings- Consulting and SI,

Specialized voice

Through- Global delivery and

workforce

The Indian IT-BPM industry today moving

along three paths to offer more value

Source: NASSCOM

ER&D Industry - India as Innovation Hub

Evolution of Work Performed in E R&D Industry

• Global Offshorable Revenue of USD

100 Billion by 2020 – Huge untapped

potential

• Developing Products from First

Design Principles (Frugal

Engineering)

• New Business Models, Flexible

Resource Capacity, Co-Creation, Art-

to-Part

• Participation in Patents Creation –

Grown 30x in last 5 years

• Full Product Development

• High end offerings like prototyping,

tooling, manufacturing support,

program management, supplier

management

• Localized products for Emerging

Markets

ER&D exports to cross USD 10 billion; Key players driving product and process innovation

INDIAN IT-BPO INDUSTRY > EXPORTS

Source: NASSCOM

19

CAGR

12%

ER&D Exports by Industry,

FY2012E 100% = USD 10.2 billion

• ER&D exports at USD 10.2 billion; y-o-y growth

of 14 per cent

• ~15 per cent share in Indian IT-BPO exports

• 400+ players with >200,000 engineers

• ~90 per cent exports from North America and

Europe

• Established hub for Aerospace, Automotive and

Telecom

• Emerging as hub for energy and medical

devices

• 65 per cent exports from Telecom,

Semiconductors, Automotive

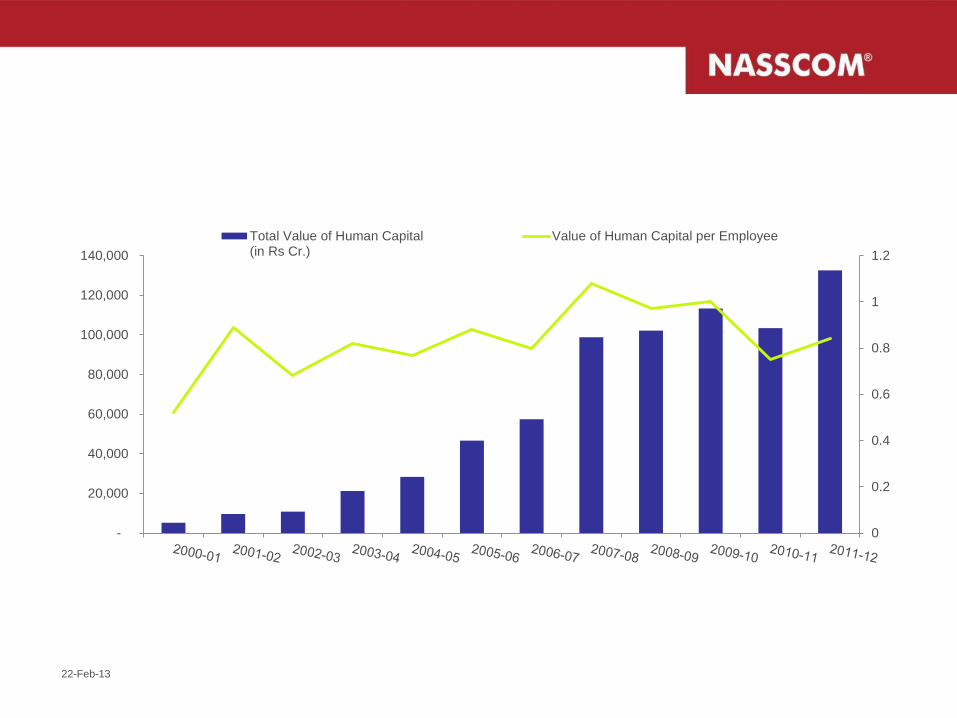

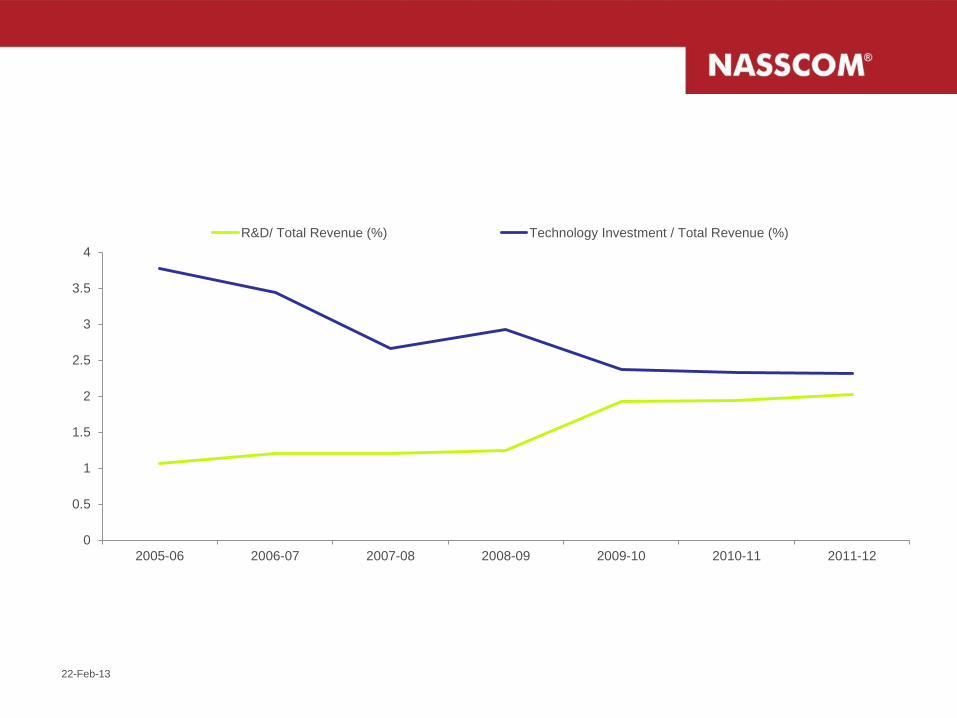

Focusing on R&D and Boosting Innovation

Growing R&D spend Strengthening role in

IP creation

Developing software

products

Attracting global

technology players

Average R&D

spend 0.5–1% of

revenues; 2.5-5% of

profits

Patents in the

Computer/Electronic

s segment increased

30X over 2005–09

Software products

revenues more than

tripled over FY06–09

• Number of offshore

development centers

(ODCs) in 2009 is 3x-

4x of ODCs in 2006

Breakdown of R&D costs

Spearheaded India’s thrust on innovation –

30X increase in patents

Innovation driving

additional GDP

contribution of ~2%

by 2020

Key initiatives driving innovation include setting up R&D centers, conducting trainings, events

and workshops around innovation, and collaborating with academic institutions

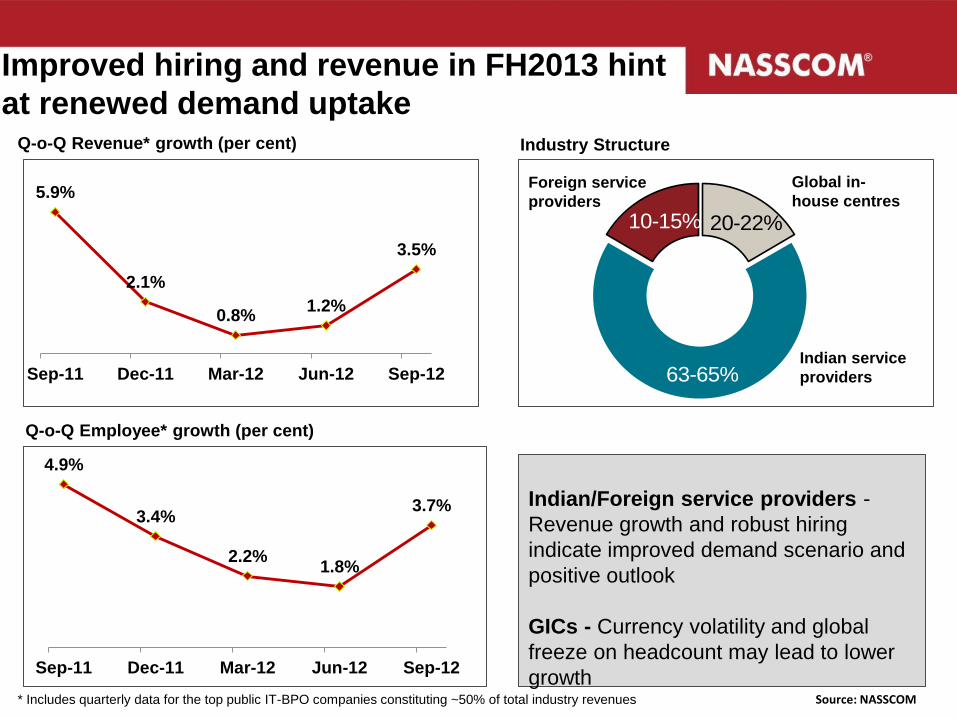

Improved hiring and revenue in FH2013 hint

at renewed demand uptake

5.9%

2.1%

0.8% 1.2%

3.5%

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

Q-o-Q Revenue* growth (per cent)

4.9%

3.4%

2.2% 1.8%

3.7%

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

Q-o-Q Employee* growth (per cent)

63-65%

20-22%10-15%

Global in-

house centres

Indian service

providers

Foreign service

providers

Industry Structure

Indian/Foreign service providers -

Revenue growth and robust hiring

indicate improved demand scenario and

positive outlook

GICs - Currency volatility and global

freeze on headcount may lead to lower

growth

* Includes quarterly data for the top public IT-BPO companies constituting ~50% of total industry revenues Source: NASSCOM

“SMAC” – Social Media, Mobility, Analytics and Cloud

reshaping the future of the Indian IT Industry

Impact is highly evident

• Create a new digital

operating model and

transformation to a

permeable enterprise

• Engagement with a

growing digital ecosystem

• Empower enterprises to

embrace emerging

technology trends and to

benefit from the value

expectations of customers

• Innovative thinking in

business and enterprise

architectures

SMAC, is becoming a business reality

Social, mobility, analytics and cloud are reshaping

the business, the consumers and all traditional

approaches, Indian Industry has seen till now

Movement towards the next orbit of innovation with

consumerization of IT

Opportunity to move to higher-margin business

by offering creative solutions

Help businesses grow dynamically instead of

increasingly cutting margins for typical IT contracts

Launching luxury product lines that comprise the

SMAC suite of technologies to go the next level

Huge potential for revenue generation

IDC Indian IT vendors expected to generate over

$225 billion in SMAC related revenue by 2020

Drivers/ factors contributing to the changing landscape of Technology

Transformation

Remodelling business processes

through harmonizing technology

advancement

Client- specific outcomes

A meaningful change in the business

requirements i.e., end-to-end solutions

New paradigm for business

Efficiency, Enhanced customer

experience, Reduced time to market,

Connectivity, IT Consumerization

Journey to the Cloud continues; enthusiasm for Big Data, Mobility and Social Analytics also remains strong

Mobile payments Smart cities Connected Health Pivot merchandising

mBanking mHealth Smart Buildings mGovernance Platform-as-a-Service

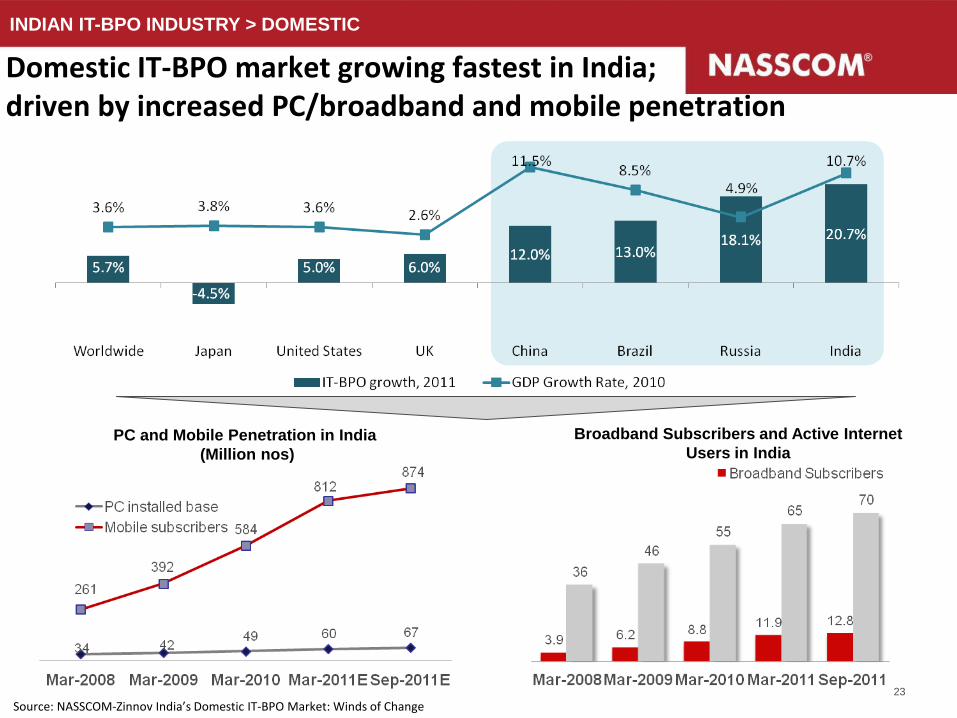

Domestic IT-BPO market growing fastest in India; driven by increased PC/broadband and mobile penetration

INDIAN IT-BPO INDUSTRY > DOMESTIC

23

Source: NASSCOM-Zinnov India’s Domestic IT-BPO Market: Winds of Change

PC and Mobile Penetration in India

(Million nos)

Broadband Subscribers and Active Internet

Users in India

Hypermobility…but only for some ??

25 22-Feb-13

Technology can transform India’s ability to

provide basic services

Basic services Potential technology and services’ solutions

Healthcare 50% of Indians do not have access to primary healthcare –

technology can provide it at half the cost

Financial

services

80% of Indian households are unbanked – technology can

enable access for 200 million families

Education

India faces a 3-fold shortage in teachers – technology can

address this through remote solutions (e.g., virtual

classrooms, recorded lectures by senior faculty, modular

multimedia content)

Public

services

India suffers from a leakage of 40-50% in public food

distribution – technology can ensure transparency

22-Feb-13 25

Inclusive ITeS Innovation Examples

• Mobile Financial Services: EKO

• Mobile Phones for Data and Text

• Rural Development: Ekgaon , Nano Ganesh

• Health Diagnostics (Avoidable Blindness): 3nethra

• Public Health (Maternal & Child Health): e-Mamata

• Travel Services: iXiGO

• Unique Identification System: Aadhar

27

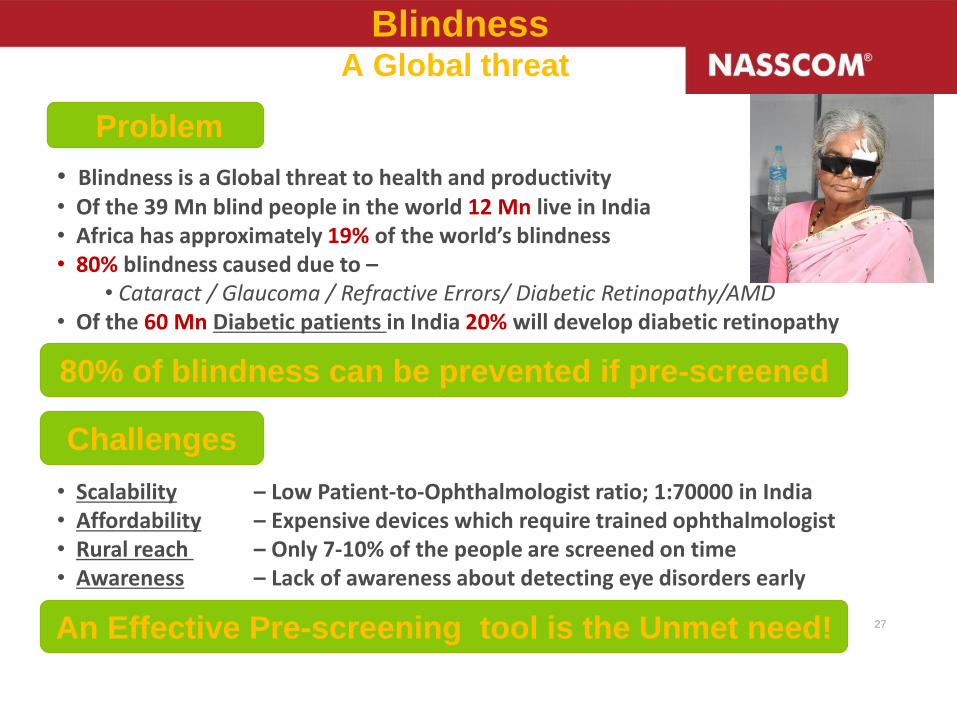

Blindness A Global threat

Problem

Challenges

• Blindness is a Global threat to health and productivity • Of the 39 Mn blind people in the world 12 Mn live in India • Africa has approximately 19% of the world’s blindness • 80% blindness caused due to –

• Cataract / Glaucoma / Refractive Errors/ Diabetic Retinopathy/AMD • Of the 60 Mn Diabetic patients in India 20% will develop diabetic retinopathy

• Scalability – Low Patient-to-Ophthalmologist ratio; 1:70000 in India • Affordability – Expensive devices which require trained ophthalmologist • Rural reach – Only 7-10% of the people are screened on time • Awareness – Lack of awareness about detecting eye disorders early

80% of blindness can be prevented if pre-screened

An Effective Pre-screening tool is the Unmet need!

28

Addressing the Unmet Need!

Scalability

• Take the Ophthalmology pre-screening closer to the patient • Create a new market for remote ophthalmology pre-screening – “Paradigm Change” • Enable diagnostic labs, diabetes centers, clinics etc to perform ophthalmology screening

Affordability • Indigenously developed in India • Robust device with minimum complexity • Low maintenance cost and zero consumables

Rural Reach

• Non-Mydriatic, Non-invasive & portable device • Robust system to be operated in rustic environments • Minimally skilled technician required to operate device

Awareness

• Create awareness about the importance of detecting ophthalmic diseases early

Forus 3nethra

A Pre-screening Ophthalmology Device

Cornea Imaging

Retina Imaging

3nethra is an affordable multi-functional portable ophthalmic imaging system

Refractometer

3nethra ForCare

Cloud based Tele-ophthalmology capability

Take Away’s for Policy & Strategy

• IT not just for “big boys” or rich yuppies...can play

transformational role in society, polity and economy

• Refocusing Strategic Priorities for Indian IT in Next Decade

...Domestic Markets and Developing/Emerging Countries

...Not just about Growth, also about Learning

• Affordability, Scalability, Reach and Education/Awareness

Key to Direction of Entrepreneurship & Innovation

• Innovation is More Than R&D, Even D&E of Products

...Service Dimensions and “Business Models” also Salient

• Government Critical to Shaping “Demand” or Ecosystem

• Advance Market Commitment (e.g. Laptops for Students)

• Platforms (e.g. Aadhar)

• Incentives and Regulation

THANK YOU

22-Feb-13

0

0.2

0.4

0.6

0.8

1

1.2

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Total Value of Human Capital(in Rs Cr.)

Value of Human Capital per Employee

22-Feb-13

0

0.5

1

1.5

2

2.5

3

3.5

4

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

R&D/ Total Revenue (%) Technology Investment / Total Revenue (%)

22-Feb-13

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

-

10,000

20,000

30,000

40,000

50,000

60,000Brand Value (in Rs Cr.) Brand Value as a % of Market Cap

![Working Paper No. 187 - ICRIER | Indian Council for …icrier.org/pdf/Working_Paper_No[1]._187.pdfii Abstract ITES/BPO services is an important and growing component of India’s trade](https://static.documents.pub/doc/80x56/5b0b79727f8b9a61448cc900/working-paper-no-187-icrier-indian-council-for-1187pdfii-abstract-itesbpo.jpg)