22

Indian Healthcare: Opportunity and Solutions 07 May 2011

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 213 times |

| Download: | 0 times |

Indian Healthcare: Opportunity and Solutions

07 May 2011

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 2

Overview of the presentation

► The Indian healthcare -- landscape and change drivers

► Key imperatives and potential solutions

Indian Healthcare – Landscape and change drivers

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 4

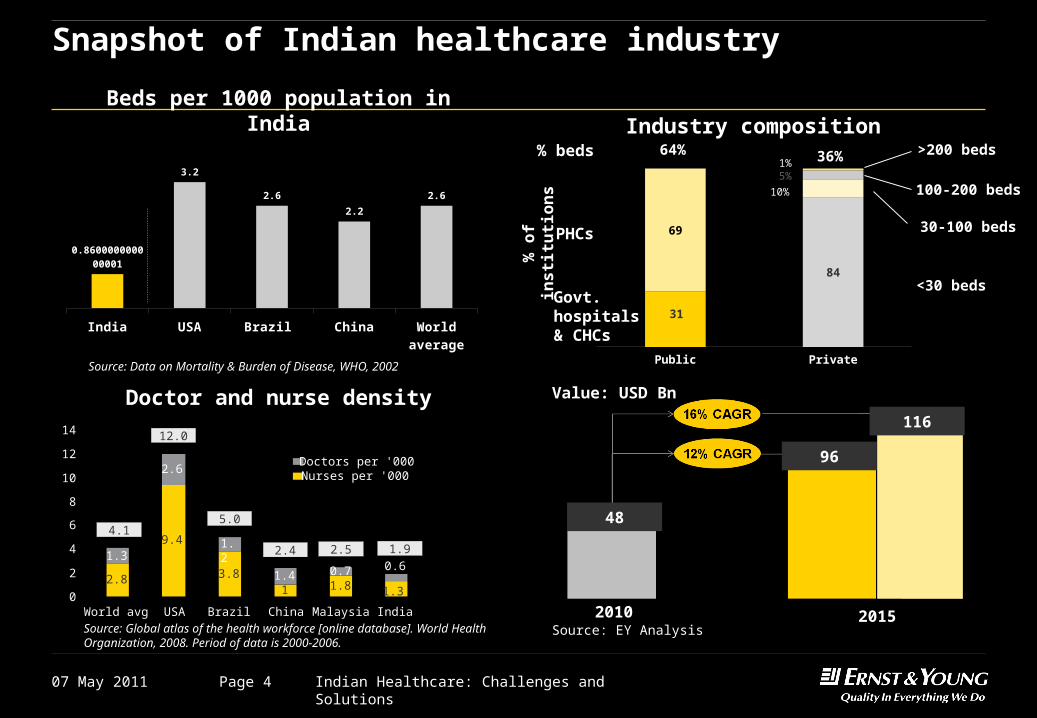

Snapshot of Indian healthcare industry

0.71.3

2.6

1.2

1.42.8

9.4

3.81 1.8 1.3

0.6

0

2

4

6

8

10

12

14

World avg USA Brazil China Malaysia India

Doctors per '000Nurses per '000

4.1

12.0

5.0

2.4 2.5 1.9

Source: Global atlas of the health workforce [online database]. World Health Organization, 2008. Period of data is 2000-2006.

Doctor and nurse density

India USA Brazil China World av-erage

0.860000000000001

3.2

2.6

2.2

2.6

Beds per 1000 population in India

Source: Data on Mortality & Burden of Disease, WHO, 2002Public Private

31

84

69PHCs

Govt. hospitals & CHCs

<30 beds

30-100 beds

100-200 beds

>200 beds% beds 64% 36%5%

10%

1%

Industry composition

% o

f in

sti

tuti

on

s

Value: USD Bn

Source: EY Analysis

48

96

116

2010 2015

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 5

Indian healthcare in its current state is plagued by problems with the key roadblock being the lack of propensity to pay for healthcare

Prevalence

► 17% of world’s population has 20% of world’s disease burden

► Disease burden per 100,000 is 85% more than that of China and 38% more than that of Brazil

► Disease burden for communicable diseases 3 times that of Brazil & 5 times of China

► Pre-dominantly acute (~50%), disease burden with a rapidly growing prevalence of chronic diseases

Provider Propensity

► Highly inadequate infrastructure - Bed density is less than 1/3rd of the world average & less than ½ that of China

► Inequitable distribution of infrastructure - 6 states with 37% of the Indian population have hospital beds per ‘000 less than 2/3rd of national average

► Only 35% of the population has access to modern medicine

► Low expenditure on healthCountry % of GDPUSA 16%France 11%World average 9%

India 4%

► Per capita spend on healthcare ($116) is ½ of China and 1/7 of Brazil

► 64% of health expenditure is out-of-pocket – 4 times the world average

► Insurance covers only 12% population► In addition, monthly per capita

expenditure of the Indian population is low making affordability an issue – 12% ailments remain untreated

MPCE for urban

% urban popn.

10.6%

31.6%

55.7%

2.0%< $7

$7 to 20

$20 to 43

>$43

Source: EY-FICCI “Fostering Quality Healthcare for All” 2008

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 6

To summarize, current characteristics of healthcare in India

► Largely a “Sick-care” industry

► Characterized by high disease burden

► Serviced by an inadequate and highly fragmented provider

infrastructure

► Catering to a population that has to spend from out of its pocket for

most of its healthcare needs

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 7

However, the industry is at throes of a transformation driven by three key trends

Growing middle class & higher spend of middle class on healthcare

Low Medium High

He

alt

hc

are

sp

en

d –

S

ha

re o

f w

all

et

Income Level

50 mn

2005 2025

600 mn

Income in Rs.’000

< 200

200 to 1000

>1000

Middle class

Changing mindset from ‘sick care’ to ‘healthcare’

1

2

Emergence of healthcare as a political agenda3

Government outlay for healthcare to increase from 1% to 3% of GDP

BPL population meant to be a significant beneficiary thus driving ‘healthcare inclusiveness’

National immunization programs to expand

Testaments to this changing mindset are – ► The increasing penetration of private insurance – CAGR of more

than 30%► Increase in ‘share of wallet’ for healthcare by 30% in the coming

5 years1995 2005 2015 2025

4% 7% 9% 13%

Healthcare share of wallet

Share of wallet

Source: MGI & EY

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 8

Unleashed demand will require an overhauling rather than incremental changes in healthcare

2008 2025

0.94

2.69

2.9 x

2008 2025

0.53

1.232.3 x

2008 2025

1.3

2.92.2 x

No. of beds (Million) No. of doctors (Million) No. of nurses (Million)

India would need to add 1.75 Million hospital beds, 0.7 Million doctors and 1.6 Million nurses by the year 2025

Source: EY FICCI Healthcare report

(Assuming current doctor to nurse ratio)

Creation of the required infrastructure would require an investment of ~ USD 90bn over next 15 years

Imperatives and solutions

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 10

Key imperatives

Focus on building capacity and capability

Reduce demand on curative care – primarily secondary and tertiary care

Undertake initiatives to enhance access – geographical and financial

1

2

3

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 11

Potential solutions – the “market shapers” and the “game changers”

Market Shapers Game Changers

I. Emphasis on preventive care and

wellness

II. Strengthening of primary care

III. Facilitative changes in norms regulating

medical education and practice in India to

generate additional resources from

existing infrastructure

IV. Focus on tier-II cities for expansion

V. Move to day care surgeries

I. Focus on healthcare inclusiveness

driven through health insurance

II. Creation of healthcare infrastructure

through “Public Private Partnerships”

III. Leveraging IT to enhance access to

care

IV. Training and empowering healthcare

workers to reduce dependence on

MBBS doctors and specialist

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 12

Market shaper – I, II

Strengthening of primary care system, promote health

► Strengthening of rural healthcare infrastructure by government

► Launch of NRHM in 2005 with focus on:

► Creating community health workers (ASHA program): ~ 700,000 enrolled till date

► Primary care infrastructure upgradation/ creation

► Decentralization of healthcare requirement planning

► Initiatives to create awareness, early detection and treatment of non-communicable diseases, e.g. diabetes, dialysis, cancers, strokes, cardiovascular diseases

► Emphasis on promoting health

► Focus on health determinants: Access to safe drinking water, sanitation including waste disposal systems, controlling environmental pollution, minimal level of nutrition safety, and education

► Need for a coordinated approach for securing of these basis entitlements – “Right to Health” by Assam government

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 13

Market shaper - III

Facilitative changes in norms regulating medical education and practice in India

► Facilitative changes in norms regulating medical education and practice in India, e.g.

Allowing capacity addition to existing facilities

► Ceiling for MBBS admissions has been raised from 150 to 250 depending on bed strength, bed to student ratio changes

► Teacher-Student ratio has been relaxed from 1 : 1 to 1: 2 in medical colleges

Facilitate creation of new infrastructure

► Relaxation of land requirement norms (from 25 acres to 20 acres, special concession for NE states and some UT, major cities 10 acres)

► Rationalization of infrastructure requirements setting up new medical colleges

► Relaxation of bed strength and patient occupancy norms

► Companies registered in India permitted to set up medical colleges

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 14

Market shaper - IV

Is access or affordability the key to tap these (Tier 2 & rural) markets?

Rural

Class I/IA

Metro

Class II-IV

No. of towns/villages Population (mn) Households with high-medium purchasing

power

Current market split

(pharma)

35

359

3792

593,807

108 (11%)

88 (9%)

89 (9%)

743 (72%)

39

11

56

27%

34%

20%

19%

Metro: >1 mn population, Class I towns: 0.1-1 mn, Class II-IV: 5000 – 0.1 mn, Rural: less than 5000 ; Tier 1 markets: Metros and Class I towns, Tier 2 markets: Class II-VI towns and Rural areas *High – medium purchasing power – Annual income is Rs. 1 lakh and above

Tier

1

Tier

2

Source: NCAER, MGI, EY analysis

Rur

al

Is access or affordability the key to tap these (Tier 2 & rural) markets?

Source: NCAER, MGI, EY analysis

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 15

Market shaper - V

Move towards day care surgeries

Concept:

► Number of day care surgeries: US -- 75% of total surgeries, India ~ 40% which can go

up to 60% given the current infrastructure

Advantages:

►Reduced cost to the patient (can save up to 30% to 40% of typical surgery amount)

►Lesser period of stay for the patient and use of high end technology for faster recovery

►Lower capex requirement, quicker breakevens, Frees up precious hospital

infrastructure (beds)

►Can help enhance access

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 16

Game changer - I

Health Insurance Schemes

► Government sponsored schemes for economically weaker sections of society

► RSBY – 2.98 crore households covered

► Weavers scheme – 18 lacs weaver families

► Aarogyasri scheme (AP) – 2.03 cr BPL families

► Other states: 13 other states have initiated various models of health insurance

schemes in 2008-09 and 2009-10

► Private insurance – growing at a CAGR of 30%

► CGHS and ESIS schemes

These schemes will make healthcare financially accessible to a large section of population which earlier could not afford it

50% of Indian population can be covered by health insurance in 2015 if formal sector and BPL is given mandatory coverage

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 17

Game changer - II

Creation of healthcare infrastructure through “Public Private Partnerships”

► High potential to accelerate access since it can

► Overcome Government’s budgetary constraints

► Promote entrepreneurial action by private players and accelerate facility creation

► Provide quality care at concessional rates to financially disadvantaged and at competitive

market prices to others

► Key success factors:

► Agenda defined by the first “P” – i.e. “Public”

► Strong philosophy of partnership - equity, trust and autonomy

► Risk sharing framework designed with both public and private players assuming risks that

are best suited to them

► Normal rate of return on equity with upsides for efficiency for private players

► National framework and standard templates for concessionaire agreements

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 18

A model for PPP in provider care

Healthcare provider

Centre

Insurance company

BPL Population

APL Population

Viability gap1 funding in form of an annuity for setting up facilities in select non Tier 1 areas

Insurance premium

Land

State

y%

x%

100%Funds operating

and capital expenditure

Provides treatment

Reimburses private provider based on agreed upon tariffs

%

Indi

cate

s sh

are

of f

undi

ng b

etw

een

Cen

tre

and

Sta

te

Cess/ Surcharge/ Health tax

Electronic health cards distributed by government

Out of pocket premium

Out of pocket premium – 0%PUBLIC

SECTORPRIVATE SECTOR

CONSUMER

Stakeholders involved

Monitoring Agency

Ensures governance and quality of care

Financial

monitoring Quality

monitoring

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 19

Game changer - III

Using technology to improve access to healthcare

Public health research

Primary care/ remote consults

Emergency care

Management of long term conditions

Information and self help

Efficiency improvement

Encompasses data-gathering for public health research programs

Tracking of disease outbreaks, epidemics and pandemicsDevelopment of health policyDesign of healthcare interventions

Includes services and applications that support the diagnosis of medical conditions, and the provision of treatment by frontline local medical staff (remotely or at site)

Enhancement of emergency care, in hospitals and elsewhere, through the deployment of mobile technologies

Applications promoting wellness, and incentivizing or encouraging individuals to improve their own health

Using ICT

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 20

Game changer - III

Some business models -- Enabling remote professional

Examples

► 3G Doctor in UK (GBP 35 per consultation)

► Yihe (China) – remote consultation(30 GP process 2000 messages per day, 1.89 mn registered users)

► Sana app for Google Android (connecting rural health workers with specialist doctors), NH for oral/cervical cancer and for cardiovascular diseases

► Teledermascopy, “One stop medical report” China Mobile’s service for remote consultation of diagnostic report (targeted at rural areas)

► Apollo-Aircel: Tele medicine and Tele Triage

Pool of medical experts at central location

Experts can cover more ground – no need to

travel

Skilled health workers equipped with advanced

Smartphone

Skilled health workers can deal with more problems in

consultation with experts

End userPanel

DoctorApp

Developer

Payment company

Mobile operator

Receives transaction fee

Mobile network operator receives fee

for video call

Developer is paid for app and platform

Doctor provides health record platform fro free, but charges for the consultation

End user pays per transaction

07 May 2011 Indian Healthcare: Challenges and SolutionsPage 21

Source: WHO World Health Survey 2003, Morbidity, Healthcare and Condition of the aged NSSO 60th Round, “Financing and Delivery of Health Care Services in India”, Background papers of the National Commission on Macroeconomics and Health”, 2005

Game changer - IV

Skill upgradation, more active role of non-doctor health workers

Overcome Inequitable Distribution

► Need to make our health delivery less doctor dependent and more nurse enabled► Nurse to doctors ratio: India (2.5: 1), UK (5:1), US (3:1)

► Three years rural medical practitioners/ assistant courses (e.g. Assam and Chhattisgarh)

► Inclusion of AYUSH doctors in healthcare delivery specially in underserved areas with necessary skill upgradation

Thank you