Page 1

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 1/53

1

Indian Industrial Policy and Global Competition

N. S. Siddharthan 1 Institute of Economic Growth

Delhi University North Campus, Delhi – 110007, India

Email: [email protected]

AbstractThis paper evaluates the impact of Indian economic policy, examines the Indianinvestment climate and business environment in relation to our main competitors likeChina and the East Asian countries, and discusses policy options for the future. In

particular, it analyses trends in Foreign Direct Investment (FDI) inflows, regionaldistribution of FDI in India, and issues related to attracting efficiency seekinginvestments. In addition, this paper also analyses the impact of liberalisation measures on

Indian exports, technology acquisition and productivity growth. In this context the crucialrole of the IT sector and small and medium enterprises is reviewed. In analysing theglobal economic environment it considers the main provisions of the WTO regime andthe ongoing technological revolution .

I THE BACKGROUND

In analysing issues relating to Indian industrial policy and global competition it is

important to consider the current international institutional and technological scene,

namely, the World Trade Organisation (WTO), conditions imposed by the International

Monetary Fund (IMF) for lending to countries and the roles of Information Technology

(IT) and internet in global business. The attempts by several developing economies (DEs)

to liberalise and integrate themselves with the global economy has to be viewed in the

context of the changing global institutional and technological environment.

WTO Regime and its I mpact

The emergence of the WTO regime in 1995 has fundamentally changed the international

trade scene. The WTO is the result of t he Uruguay round of negotiations that began in

1 I am grateful to the participants of the seminar on “Indian Industrial Policy and Global Competition” heldat IIMB on August 20-21, 2005 for their several helpful comments and suggestions.

Page 2

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 2/53

2

1986 in Punta del Este, Uruguay and concluded in Marrakech on December 15, 1993.

Two basic principles govern all WTO sections: national treatment and the most favoured

nation status. National treatment to all firms prohibits the local host government from

granting to the local firms favours, privileges and advantages that are not available to the

foreign firms. Thus in matters relating to government purchases, licensing etc., local

firms and foreign firms have to be treated on par. Likewise, the most favoured nation

status prevents the host government from favouring firms from one WTO member

country over firms from other WTO member countries. WTO has generally improved

transparency (it is one of the core WTO principles that extends across all agreements just

as national treatment and non-discrimination do), and it extends the rule of law. These

improvements reduce transaction costs through the external market. The new and heavily

used dispute settlement procedure improves compliance and enables firms to seek to

enforce fair trade by actions taken on their behalf by their governments. These

institutional changes have reduced transaction costs and have made exporting, licensing

of a firm’s proprietary knowledge and knowledge sharing in networking alliances

attractive options. Further, reductions in tariffs are also a part of WTO, and this

stimulates exports and efficiency-seeking FDI.

However, the WTO regime also restricts the scope for the governments of DEs to

regulate and control. For example, the Indian pharmaceutical industry developed rapidly

mainly due to the restrictive patenting regime in India, where product patents were not

allowed and process patents were for a shorter duration. Under the WTO regime, India

has to grant products patents for 20 years from the date of filing. Furthermore, copyrights

are now protected for 50 years, and they cover several items like software, databases,

Page 3

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 3/53

3

recordings, performances and broadcasts (20 years). Trademarks and service marks are

protected for 7 years and are renewable indefinitely. Moreover, compulsory licensing and

linking of foreign and domestic trademarks are prohibited. These are enforceable through

courts. The enforcement mechanism should be efficient and transparent.

Till recently, India and several other Asian countries have been insisting on local

content requirements from foreign firms. In this regard, in several cases, physical targets

were fixed to promote domestic procurement and to increase the local content. To prevent

the outflow of foreign exchange, trade balancing requirements were also imposed. These

limit the imports of foreign firms to their earnings of foreign exchange through exports.

In some cases, less stringent requirements like foreign exchange neutrality, namely, some

balance between foreign exchange inflows (through exports and investments and other

transfers) and outflows were enforced. WTO provisions prohibit all these measures.

Consequently developing countries had to give up measures like local content, trade

balancing and foreign exchange neutrality since January 2000.

Studies (Kumar 2002; Siddharthan and Rajan 2002) have shown that these

measures could reduce the quality of FDI inflows and inhibit the development of

domestic component industries.

I M F Conditionality

It is important to distinguish the operations of IMF and the conditionality imposed by it

from the operations of the WTO regime. While the WTO regulations apply to all member

countries, the IMF conditionality affects only those member countries that borrow from

IMF. By and large, IMF provides funds on the condition that the borrowing countries cut

deficits, raise taxes and interest rates, liberalise trade and currency exchange rates and

Page 4

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 4/53

4

move towards making their currency convertible in both current and capital accounts. In

some cases, the IMF fixes targets for each of these variables and monitors their

performance. In addition to liberalisation measures, it could also insist on privatisation of

government owned enterprises (Stiglitz 2002).

The Impact of I nf ormation Technology

The emergence of the current generation of information technology tools, in

particular the internet, has radically altered the nature of international transactions.

Earlier market-seeking multinational enterprises (MNEs) invested in foreign locations

mainly to exploit their firms’ ownership advantages (Dunning 1993, Caves 1996).

Currently, partly due to the WTO regulations and partly due to the vast changes in

information and communication technology (ICT), MNEs are opting for efficiency

seeking investments and especially non-equity alliances that often include acquisition of

knowledge assets. This change in the MNEs’ strategy has led to some notable

consequences. Traditionally, design, engineering, and technological innovation were

mainly conducted in the home country. Very little R&D was performed in the host

countries and where it was performed, it was of an adaptive nature intended to modify the

product or process to suit the resource conditions or tastes and preferences of the host

country. By and large, the MNEs invested abroad to exploit the advantages that they

possessed at home. However, unlike the earlier investments, some of the current

investments are technology-augmenting investments aimed at exploiting host country

resources (asset- seeking FDI). In the MNE’s decision process the new factor considered

is the skilled labour possessed in the form of a thin strata of educated labour in some

developing countries. This applies already in industries such as software and

Page 5

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 5/53

5

pharmaceuticals (and it is arising in some manufacturing industries also), and in countries

such as India and China (Kumar and Siddharthan 1997, Siddharthan and Rajan 2002,

Belderbos 2001, Florida 1997, Kuemmerle 1999).

Most importantly, the new knowledge sharing methods adopted by MNEs need

not be fulfilled by FDI. The internet revolution enables a range of non-equity alliances to

substitute for FDI. The immobility of labour across nations that compelled international

growth to take place either by trade or investment no longer applies to a range of

professional and technical activities. The internet revolution has created virtual labour

mobility. Professionals in home and host countries can transmit their labour services

electronically and instantly across borders; they do not need to move geographically.

Investments in operations abroad are not necessary; outsourcing and networking serve as

effectively. This has encouraged the creation of global R&D units that have removed the

differences in the R&D performed by the home and host country R&D units.

Consequently several MNEs have set-up strategic alliances with R&D units in a less

developed country like India where they are performing innovative R&D aimed at

pushing technological frontiers (Reddy 1997, Siddharthan and Rajan 2002). In the

pursuit of efficiency, MNEs are also likely to source high-tech components from their

strategic partners with whom they also share knowledge

In recent years, internet and e-commerce and in particular business to business

(B2B) commerce, have assumed importance. The study by Freund and Weinhold (2004)

finds that internet stimulates trade. They show that internet reduces the fixed cost of entry

into a foreign market and that helps firms from less developed countries and in particular

small and medium enterprises (SMEs). Using data on bilateral trade from 1995 to 1999

Page 6

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 6/53

6

and controlling for the standard determinants of trade growth, they find that the growth in

the number of websites in a country helps to explain export growth in the following year.

Accordingly the success of SMEs would crucially depend on their ability to network,

which in turn would depend on the infrastructure facilities for B2B commerce. Thus IT

has enabled SMEs to globalise. Given the context of the WTO regime and internet

revolution, all the markets have become global and consequently all firms – small,

medium and large - must have a global vision to succeed. Economic policies of DEs have

been responding to the altering international environment.

II INDIAN POLICY REFORMS SINCE THE 1990s

Some studies attribute the Indian reforms introduced in the early 1990s to the balance of

payments crisis in 1991 when India was left with just two weeks’ import cover (Bhaumik

et. al. 2002). The 1991 crisis could have acted as a catalyst for the reforms. But the entire

reform process cannot be attributed to the crisis. India has been deregulating its economy

since the year 1985 in response to the changes in the international environment discussed

in the previous section. Factors like the success of the Chinese and East Asian

liberalisation measures, Uruguay round of negotiations that started in 1986 and that was

nearing completion in the early 1990s, the collapse of the Berlin wall in 1989, the turmoil

in the erstwhile Soviet Union and the ongoing IT revolution contributed significantly to

the introduction of liberalisation measures in India and other DEs. In fact most countries

went in for liberalisation in the 1990s and India was no exception.

Nevertheless, the measures introduced in the year 1991 were not on par with the

earlier reform measures. The year 1991 was a landmark or a watershed. A statement on

Page 7

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 7/53

7

Industrial Policy was introduced in July 1991 that aimed at letting entrepreneurs make

investment decisions on the basis of their own commercial judgement. Under the

industrial license and permit regime this freedom was not given to entrepreneurs. The

statement also declared that the role of the government would be changed from one of

only exercising control to that of providing help and guidance by making essential

procedures fully transparent and by eliminating delays. This statement is a major

departure – a paradigm shift – from the earlier role of the government. Towards this

objective the government introduced a series of “measures to unshackle the Indian

industrial economy from the cobwebs of unnecessary bureaucratic control” (Industrial

Policy Statement 1991, Page 9). They covered several areas – industrial licensing policy,

foreign investment, foreign technology agreements, public sector and the MRTP Act.

These decisions include the abolishing of industrial licensing for all projects

except for a short list of industries attached in Annexure II; liberalisation of the granting

of import licences for capital goods; removal of the requirement of industrial approvals

for locating industries in cities with less than one million population; approval of FDI up

to 51 percent in priority industries (Annex III) and for trading companies; automatic

approval for foreign technology agreements in high priority industries (Annex III) subject

to lump-sum payments being less than one crore rupees and royalty being less than 5%

for domestic sales and 8% for exports; freedom to hire foreign experts; and the

amendment of the MRTP act to remove the threshold limit of assets of MRTP companies

and dominant undertakings. In addition, import duties have drastically come down over

the years. The peak tariff in 1991-92 (excluding high tariff items like alcohol, agricultural

Page 8

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 8/53

Page 9

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 9/53

Page 10

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 10/53

10

The policy also encourages the development of India’s indigenous resources by

enhancing research on traditional medicine and by applying globally acceptable norms of

validation and standardization. A purposeful programme to enhance the Indian share of

the herbal medicine market has been initiated. In this context an IPR (intellectual

property rights) system to protect innovations arising out of traditional knowledge has

been evolved and incorporated in the law.

I ntern ational Collaborations

The document encourages international collaborative programmes between academic

institutions and national laboratories in India and their counterparts in all parts of the

world. It lays special emphasis on collaborations with developing countries of the South

with whom India shares many common problems.

The document lists several policy objectives. They include greatest autonomy for

R&D institutions and science laboratories, interaction between industry and public

institutions in science and technology and international collaborations.

INFORMATION TECHNOLOGY ACT 2000 AND THE INDIAN SOFTWARE

INDUSTRY

The enactment of the IT Act of 2000 is an important landmark in India’s entry to e-

commerce and internet based transactions. The Act provides legal recognition for

transactions carried out by means of electronic data interchange and other means of

electronic communications, like, e-commerce, which involve the use of alternatives to

paper-based methods of communication and storage of information. The Act facilitates

electronic filing of documents with government agencies. In particular the Act provides

Page 11

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 11/53

11

for authentication of electronic records by affixing digital signatures. It allows the use of

asymmetric crypto systems and makes provisions for verifying electronic records.

The IT Act 2000 also ushers in Electronic Governance by according legal

recognition to electronic records and digital signatures. The law provides for the filing o

any form, application or document, the issue of licence or permit and the receipt or

payment of money using electronic records and digital signatures. Furthermore, it also

makes provision for the recognition of foreign certifying authorities. Thus the digital

signatures certified by these authorities will be valid as per the Act. In other words the

Act puts the necessary legal framework in place for Indians to participate and benefit

from the IT and internet revolution.

This section has mainly presented the important reforms introduced since 1990.

The impact of these reforms and the need for further reforms will be discussed later at the

appropriate places.

III FDI INFLOWS: INDIA, CHINA AND EAST ASIAN COMPARISON

The nature and character of FDI flows in the WTO regime is likely to be very different

from the flow during the pre-WTO regime. In the earlier regime one of the important

reasons for FDI inflows was to jump tariffs and exploit the host country markets (Caves

1996 and Dunning 1993). In some of the earlier studies, effective rates of protection

emerged as the most significant variable explaining FDI inflows (Lall and Siddharthan

1982). FDI inflows are mainly analysed using the Ownership – Location – Internalisation

(OLI) paradigm, which states that MNEs enjoy ownership advantages in terms of

technology, brand names and other intangible assets and they prefer to exploit them in a

Page 12

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 12/53

12

foreign location if internalisation advantages are large. That is, ownership advantages

could be exploited in three ways: (1) by producing goods in the home country and

exporting them to third countries, (2) licensing their technology and brand names to third

parties and (3) investing in foreign locations (FDI) and producing the goods in the host

country. The decision to produce goods in a third country instead of exporting to that

country or licensing their intangible assets to their partners will depend on internalisation

advantages and the international trading environment. Here, one of the important motives

for FDI happens to be host market exploitation. The WTO regime has drastically altered

the international trading environment. With the reduction of tariffs and abolition of

quantitative restrictions, exports have emerged as a viable option to market seeking FDI.

Furthermore, the intellectual property regime has made licensing of technology less risky.

Under these changed circumstances, the importance of host market seeking FDI

will decline. At present, partly due to the WTO regulations and partly due to the vast

changes in the communications and information technology, MNEs are deciding on

efficiency seeking investments and are using the host country as a platform to export to

third countries. This change in the MNEs’ strategy has led to some notable consequences.

In the case of host country market exploiting FDI, the MNEs carried out most of their

designing and innovative R&D in the home country. Very little R&D was performed in

the host countries and where it was performed, it was of an adaptive type intended to

modify the product or process to suit the resource conditions or tastes and preferences of

the host country. By and large, the MNEs invested abroad to exploit the advantages that

they possessed in their home. Unlike the earlier investments, some of the current

investments are by way of technology augmenting investments aimed at exploiting the

Page 13

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 13/53

13

host country resource (including knowledge base and human skills) advantages (Kumar

1998, 2000, 2002, Kumar and Siddharthan 1997, Belderbos 2001, Florida 1997,

Kuemmerle 1999, Siddharthan and Rajan 2002). Consequently, MNEs will locate plants

in third countries because it is more efficient to produce in that location. The

determinants of efficiency seeking FDI are very different from those of market seeking

FDI.

The WTO regime will also affect the investment behaviour of domestic firms

(both large and medium sized). In the global regime, Indian firms may not invest in India

if it is not efficient to produce that product in India. They may prefer to produce it in

China, Malaysia or Thailand and import it into India. Already there is some evidence of

this happening from newspaper and media reports. Therefore, it is not enough to study

the changes in the Indian business environment over the years and analyse their changing

trends. It is important to study the Indian business and investment environment in relation

to India’s main competitors in our neighbourhood like China, Malaysia, Thailand and

other ASEAN countries.

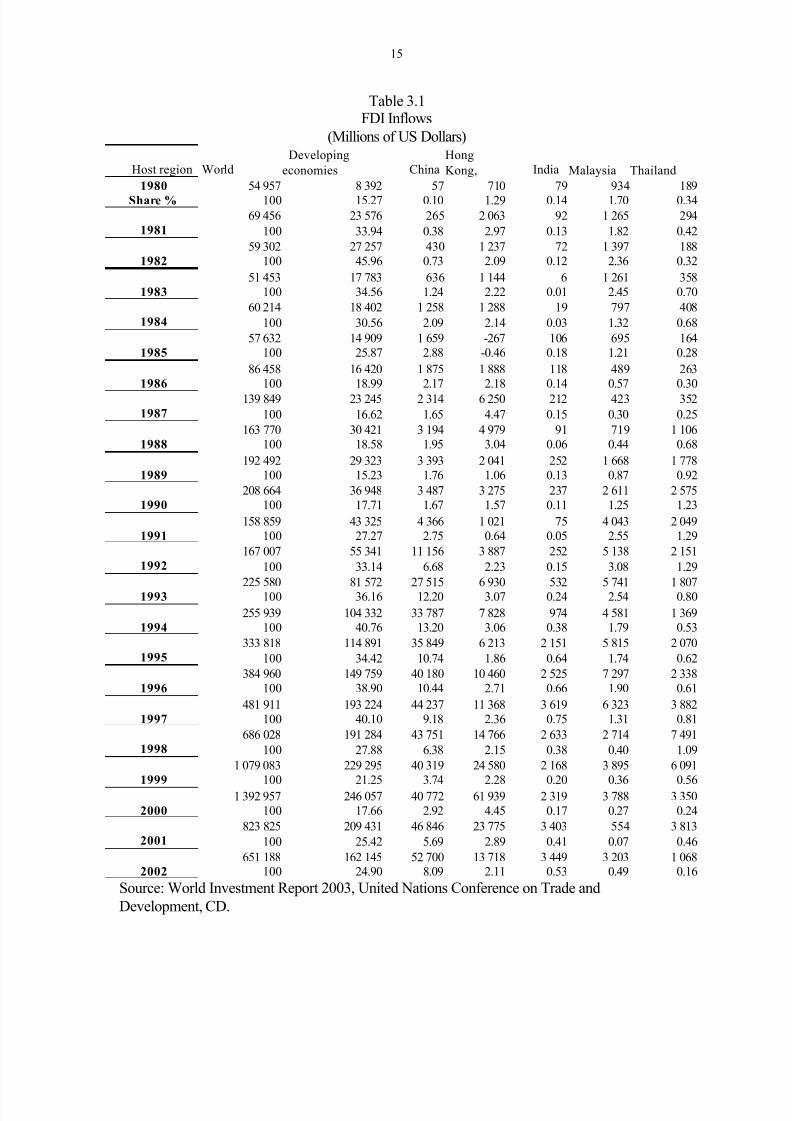

Table 1 presents the trends in FDI inflows – world, developing countries, China,

Hong Kong, India, Malaysia and Thailand. Trends from Table 1 are presented in Charts 1

and 2. Certain trends show up in the table and the charts. The share of the DEs in the FDI

inflows was more than 30 per cent during the first half of the 1980s. They sharply

declined in the second half of the 1980s and the DEs’ share came down to about 15 per

cent during 1989. It started increasing after that and reached over 30 per cent only during

1992. During 1997 it reached its peak of about 40 per cent and started declining again.

Currently the DEs’ share in FDI inflows is about 25 per cent. It turns out that the MNEs

Page 14

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 14/53

14

are mutual invaders and they prefer to invest in high income developed countries that are

also home countries of MNEs rather than investing in DEs. The share of DEs is modest

and FDI to DEs also flows to relatively high growth countries like China and East Asian

countries. Likewise technology has also been flowing into technology rich countries

(Siddharthan and Rajan 2002). Developed countries make more than 85 per cent of the

royalty payments and DEs make very little technology payments.

Page 15

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 15/53

15

Table 3.1FDI Inflows

(Millions of US Dollars)

Host region WorldDeveloping

economies ChinaHongKong, India Malaysia Thailand

1980Share %

54 957100

8 39215.27

570.10

7101.29

790.14

9341.70

1890.34

198169 456

100 23 576

33.94 2650.38

2 0632.97

920.13

1 2651.82

2940.42

198259 302

100 27 257

45.96 4300.73

1 2372.09

720.12

1 3972.36

1880.32

198351 453

100 17 783

34.56 6361.24

1 1442.22

60.01

1 2612.45

3580.70

198460 214

100 18 402

30.56 1 258

2.09 1 288

2.14 19

0.03 7971.32

4080.68

198557 632

100 14 909

25.87 1 659

2.88-267

-0.46 1060.18

6951.21

1640.28

198686 458

100 16 420

18.99 1 875

2.17 1 888

2.18 1180.14

4890.57

2630.30

1987139 849

100 23 245

16.62 2 314

1.65 6 250

4.47 2120.15

4230.30

3520.25

1988163 770

100 30 421

18.58 3 194

1.95 4 979

3.04 91

0.06 7190.44

1 1060.68

1989192 492

100 29 323

15.23 3 393

1.76 2 041

1.06 2520.13

1 6680.87

1 7780.92

1990208 664

100 36 948

17.71 3 487

1.67 3 275

1.57 2370.11

2 6111.25

2 5751.23

1991158 859

100 43 325

27.27 4 366

2.75 1 021

0.64 75

0.05 4 043

2.55 2 049

1.29

1992167 007

100 55 341

33.14 11 156

6.68 3 887

2.23 2520.15

5 1383.08

2 1511.29

1993225 580

100 81 572

36.16 27 515

12.20 6 930

3.07 5320.24

5 7412.54

1 8070.80

1994255 939

100 104 332

40.76 33 787

13.20 7 828

3.06 9740.38

4 5811.79

1 3690.53

1995333 818

100 114 891

34.42 35 849

10.74 6 213

1.86 2 151

0.64 5 815

1.74 2 070

0.62

1996384 960

100 149 759

38.90 40 180

10.44 10 460

2.71 2 525

0.66 7 297

1.90 2 338

0.61

1997481 911

100 193 224

40.10 44 237

9.18 11 368

2.36 3 619

0.75 6 323

1.31 3 882

0.81

1998686 028

100 191 284

27.88 43 751

6.38 14 766

2.15 2 633

0.38 2 714

0.40 7 491

1.09

1999

1 079 083

100

229 295

21.25

40 319

3.74

24 580

2.28

2 168

0.20

3 895

0.36

6 091

0.56

20001 392 957

100 246 057

17.66 40 772

2.92 61 939

4.45 2 319

0.17 3 788

0.27 3 350

0.24

2001823 825

100 209 431

25.42 46 846

5.69 23 775

2.89 3 403

0.41 5540.07

3 8130.46

2002651 188

100 162 145

24.90 52 700

8.09 13 718

2.11 3 449

0.53 3 203

0.49 1 068

0.16Source: World Investment Report 2003, United Nations Conference on Trade andDevelopment, CD.

Page 16

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 16/53

16

Chart 1

Year Wise Graph

- 10 000

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

1 9 8 0

1 9 8 1

1 9 8 2

1 9 8 3

1 9 8 4

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

Years

$ M i l l i o n

China Hong Kong, China India Malaysia Thailand

Page 17

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 17/53

17

Graph

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

1 9 8 0

1 9 8 1

1 9 8 2

1 9 8 3

1 9 8 4

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

Years

$ M i l l i o n

India Malaysia Thailand

Page 18

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 18/53

18

Ever since China started allowing FDI inflows it has been attracting inflows that

are several times that of India. However, FDI inflow figures for China and India are not

strictly comparable. Till recently India did not follow the IMF definition of FDI inflows,

namely, India did not consider retained earnings, reinvestments and raising of Indian

resources by MNEs as FDI. However, China included all these items in FDI.

Furthermore, only less than 30 per cent of Chinese FDI inflows came from OECD

countries (the developed countries). Most of FDI inflows into China came from overseas

Chinese and China’s neighbours (Wei 2004). Nevertheless, even if one takes into account

only OECD investments, the Chinese FDI inflows would turnout to be several times that

of India. During 1993 FDI inflows into both China and India more than doubled. For

China, it increased from 11 thousand million dollars to 28 thousand million dollars (its

world share in FDI inflows increased from 6.68 per cent to 12 per cent) and the inflows to

India increased from 252 million dollars (0.15 per cent of the world share) to 532 million

dollars (0.24 per cent of the world share). Since then the FDI inflows to both China and

India continued to rise till 1997 reaching $44237 million for China (9.18% of world

share) and $3619 million for India (0.75% of world share). From 1997 to 1999 FDI flows

declined for both countries reaching $40319 million for China and $2168 million for

India. Since 2000 FDI inflows have been increasing for both countries and in 2002 they

were $52700 million for China and $3449 million for India. Despite similarities in the

turning points and trends the two countries are not on par as India receives only a small

fraction of FDI compared to China.

The Asian financial crisis took place towards the end of 1997. However, it

affected Malaysia and Thailand differently. In the case of Malaysia FDI inflows

Page 19

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 19/53

Page 20

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 20/53

20

Toyota to virtually stop production in two of its plants in November 1997. But by January

1998, it resumed production by injecting capital and using its influence to increase the

export share. The parent company injected an additional capital of 4000 million baht into

Toyota Motors Thailand, increasing its registered capital. But for this timely investment,

the Thai company would have collapsed.

The second example is that of Honda in Thailand. To save the company

from the economic crisis Honda injected three billion baht into its Thai holding company

and doubled the capital base of its Thai affiliate. In addition, it also injected cash into the

component manufacturers, purchased shares not fully subscribed and increased its equity

share in Showa Corpn, a joint shock-absorber venture in Thailand. Thus the relocation of

components production, injection of capital and the promotion of exports saved the

automobile firms in Thailand from the financial crisis. However, despite these helpful

investments by Japanese MNEs, FDI inflows to Thailand declined sharply during 2002.

Perhaps the investment climate was not favourable.

REGIONAL DI FF ERENCES I N FDI INF LOWS

As shown in Tables 3.2 and 3.3, there are substantial regional differences in FDI inflows

in India and China. In both countries about 8 states/provinces account for more than two

thirds of FDI inflows. Furthermore, these top 8 states/provinces also account for the bulk

of domestic investments and also enjoy higher income and better socio economic

indicators (for India refer to Siddharthan and Rajan 2002; and for China Yao and Zhang

2001).

Table 3.2

Page 21

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 21/53

21

China: FDI by Province and Municipality as of 2000

Region Realized

Value10 Million

Share

Total 34,834,549 100

Beijing 1,439,843 4.13

Tianjin 1,327,461 3.81

Hebei 679,748 1.95

Shanxi 152,585 0.44

InnerMongolia 64,089 0.18

Liaoning 1,484,450 4.26

Jilin 292,167 0.84

Heilongjiang 366,392 1.05

Shanghai 2,833,979 8.14

Jiangsu 4,373,047 12.55

Zhejiang 1,118,759 3.21

Anhui 303,430 0.87

Fujian 3,351,038 9.62

Jiangxi 271,287 0.78

Shangdong 2,110,910 6.06

Henan 431,743 1.24

Hubei 642,956 1.85

Hunan 524,340 1.51

Guangdong 9,819,210 28.19

Guangxi 694,305 1.99

Hainan 622,978 1.79

Sichuan 317,858 0.91Chongqing 224,886 0.65

Guizhou 42,238 0.12

Yunnan 96,978 0.28

Shannxi 304,595 0.87

Page 22

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 22/53

22

Gansu 45,616 0.13

Qinghai 1,968 0.01

Ningxia 12,856 0.04

Xinjiang 36,967 0.11

Others 845,870 2.43Source: www.chinafdi.org.cn

Table 3.3India: FDI Approval by States

(August 1991 – September 2000)

States Investment(Rs.10mill)

Share(Percentage)

Maharashtra 40,726.09 17.12

Delhi 31,817.55 13.37Karnataka 19,796.78 8.32Tamil Nadu 16,895.50 7.10

Gujarat 11,175.31 4.70Madhya Pradesh 9,752.81 4.10

Andhra 9,448.91 3.97West Bengal 8,375.66 3.52

Orissa 9,986.74 3.36Uttar Pradesh 4,067.35 1.71

Haryana 2,983.87 1.25Rajasthan 2,539.62 1.07

Punjab 1,938.90 0.81Kerala 1,277.23 0.54Bihar 851.67 0.36Goa 529.35 0.22

Pondicherry 394.85 0.17Himachal 361.66 0.15

Chandigarh 141.84 0.06Unallocated 66,596.43 27.99

Source: Ministry of Commerce and Industry

In China, by and large, provinces belonging to the Eastern Zone have been attracting FDI

and they also happen to be the provinces enjoying higher per capita income (see Yao and

Zhang 2001). The provinces belonging to the Western Zone have not been attracting FDI

and they also happen to be the poorer provinces. Thus while the average per capita

Page 23

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 23/53

23

income of China in 1995 at 1990 prices was 2970 yuan, it was a mere 1765 yuan for the

Western zone and 4223 yuan for the Eastern Zone. For the Central zone the average was

2299 yuan. In particular, the provinces that got high FDI also enjoyed high per capita

income. Thus the major recipients of FDI like Shanghai (Per capita GDP 10712),

Guangdong (5156) Beijing (6995) and other provinces enjoyed per capita incomes that

were almost double that of the national average.

In the case of India, the states that received FDI also happen to be the states that

received domestic investments (Siddharthan and Rajan 2002). By and large most

investments went to the coastal areas and the national capital region (Delhi and the

surrounding areas). The rest of the states received very little investment both domestic

and foreign. Furthermore, as in the case of China, in India also states that enjoyed higher

per capita income received higher FDI inflows. The per capita income of India in the year

2000 (at current prices) was rupees 15562. The states that received higher inflow of FDI

enjoyed higher levels of per capita income compared to the Indian average. For example,

the per capita income of the major FDI receiving states was: Maharashtra, Rs.23398,

Delhi, Rs.35705, and Tamil Nadu, Rs.19141. States that received less FDI like Bihar and

Uttar Pradesh had lower per capita income levels, namely, Rs.6328 and Rs.9765. In this

respect China and India share some similarities. Nevertheless, there is one major

difference. In the case of China the provinces that received high FDI happen to be the

core provinces. The peripheral provinces did not receive much investment. For India, it

was the other way around. The peripheral non-Hindi speaking coastal areas dominated in

attracting investments. The core Hindi speaking states that are politically important in

terms of the number of seats they represent in the Indian Parliament did not attract much

Page 24

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 24/53

Page 25

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 25/53

25

Tables 4.1 and 4.2 present data on constraints to operations and growth. The

figures represent the percentage of firms ranking the constraint as a “moderate” or

“major” obstacle. The tables in addition to the four countries considered earlier, namely,

India, China, Malaysia and Thailand, also considers Singapore. It was decided to include

data on Singapore also as several studies consider Singapore’s investment climate as a

bench mark to evaluate other countries (Wei 2000). Singapore attracts the most

favourable response from investing firms compared to all the Asian DEs. Table 4.1

presents general constraints and Table 4.2 tax and regulatory constraints.

Table 4.1

General Constraints to Operation and Growth

Country/Variables India China Malaysia Thailand SingaporeCorruption 60.43 31.25 22.73 87.06 8.00Judiciary 29.12 13.83 21.35 25.00 9.09Financing 52.13 80.20 41.05 75.24 30.30Infrastructure 61.98 30.69 19.79 64.89 11.00

Policy Instability 62.96 41.00 27.37 90.85 11.00Inflation 67.91 42.42 39.26 90.59 12.00Exchange Rates 42.77 21.74 28.26 94.77 26.00Street Crime 22.91 18.18 18.48 92.59 6.00Organised Crime 21.84 19.59 14.61 100.00 10.10Anti CompetitivePolicies

na 38.78 27.27 95.40 20.62

Taxes andRegulations

39.23 28.71 20.43 84.25 11.00

Note: na refers to not asked.

Table 4.1 considers the following constraints: corruption, judiciary, financing,

infrastructure, policy instability, inflation, exchange rates, street crime, organised crime,

anti competitive policies, and taxes and regulation. As seen from Table 4.1 Thailand

comes out poorly with regard to all indicators except judiciary. An overwhelming

Page 26

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 26/53

26

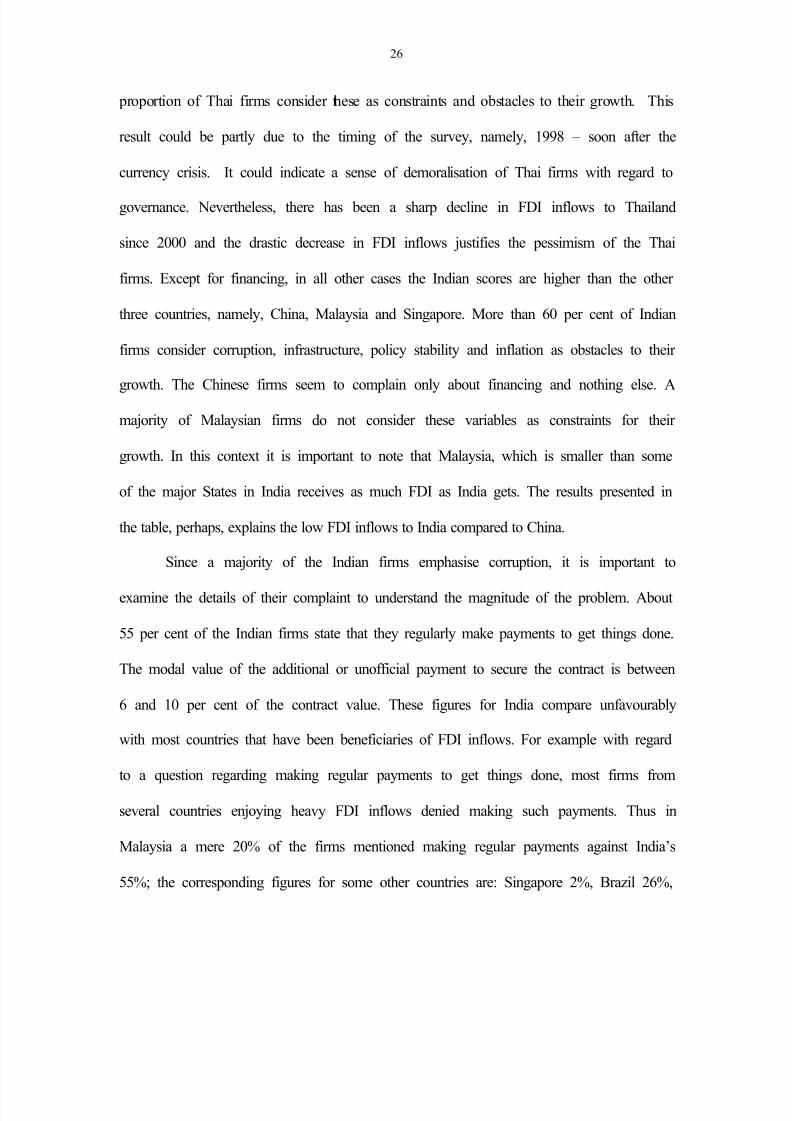

proportion of Thai firms consider these as constraints and obstacles to their growth. This

result could be partly due to the timing of the survey, namely, 1998 – soon after the

currency crisis. It could indicate a sense of demoralisation of Thai firms with regard to

governance. Nevertheless, there has been a sharp decline in FDI inflows to Thailand

since 2000 and the drastic decrease in FDI inflows justifies the pessimism of the Thai

firms. Except for financing, in all other cases the Indian scores are higher than the other

three countries, namely, China, Malaysia and Singapore. More than 60 per cent of Indian

firms consider corruption, infrastructure, policy stability and inflation as obstacles to their

growth. The Chinese firms seem to complain only about financing and nothing else. A

majority of Malaysian firms do not consider these variables as constraints for their

growth. In this context it is important to note that Malaysia, which is smaller than some

of the major States in India receives as much FDI as India gets. The results presented in

the table, perhaps, explains the low FDI inflows to India compared to China.

Since a majority of the Indian firms emphasise corruption, it is important to

examine the details of their complaint to understand the magnitude of the problem. About

55 per cent of the Indian firms state that they regularly make payments to get things done.

The modal value of the additional or unofficial payment to secure the contract is between

6 and 10 per cent of the contract value. These figures for India compare unfavourably

with most countries that have been beneficiaries of FDI inflows. For example with regard

to a question regarding making regular payments to get things done, most firms from

several countries enjoying heavy FDI inflows denied making such payments. Thus in

Malaysia a mere 20% of the firms mentioned making regular payments against India’s

55%; the corresponding figures for some other countries are: Singapore 2%, Brazil 26%,

Page 27

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 27/53

27

and Chile 4%. By and large, the percentage is low for most of the East Asian and Latin

American countries. Likewise most of the East Asian and Latin American firms declare

that they had made no payment to secure government contracts, but only less than 12 per

cent of the Indian firms state that they made no payment.

Table 4.2

Tax and Regulatory ConstraintsCountry/Variable India China Malaysia Thailand Singapore

BusinessRegistration

26.18 27.72 27.55 26.92 9.28

Customs 50.27 21.05 29.89 47.64 10.75Labour 63.68 16.00 42.71 53.98 24.00ForeignCurrency

34.95 14.63 29.67 42.44 9.28

Environmental 40.64 19.79 26.88 42.07 5.10Fire 19.58 14.43 17.53 33.73 5.00High Taxes 67.86 50.00 36.17 80.91 31.96TaxAdministration

41.15 30.00 20.83 69.93 12.00

Table 4.2 presents the views of firms on tax and regulatory constraints relating to

problems and difficulties faced regarding business registration, customs, labour, access to

foreign currency, environmental regulations, fire, high taxes and tax administration. Here

also as in Table 4.1 the values for India are higher than for all the other countries with the

exception of Thailand. A majority of Indian firms had complaints against customs, labour

and high taxes. About 50% of Chinese firms had complains against high taxes. Except for

the high taxes, most of the Chinese firms seem satisfied with tax and regulatory

measures. In the case of Malaysia also only a minority of firms considered these variables

as constraints. Since 1998 India has introduced several tax reforms and currently India

aims at having a tax structure that is on par with ASEAN countries. Therefore, currently

Page 28

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 28/53

28

high taxes may not pose a serious problem for the Indian firms. Nonetheless, problems

relating to customs and other issues remain.

Table 4.3Obstacles to Firm FinancingCountry/Variable India China Malaysia Thailand Singapore

Collateral 50.53 20.20 41.49 49.35 29.17Bank Paperwork 50.53 29.00 32.99 44.61 21.65High Interests 81.18 35.35 52.58 84.24 32.99SpecialConnections

34.97 25.53 34.74 51.24 18.75

Banks FundShortage

18.48 37.00 20.22 79.39 3.23

Access to

Foreign Banks

22.03 17.14 14.29 71.67 5.43

Access to Non-Banks

23.98 12.79 15.19 61.90 11.24

Access to ExportFinance

25.61 21.33 14.71 64.84 10.11

Access to LeaseFinance

20.59 22.47 7.69 60.61 8.70

Access to Credit 32.12 44.44 21.84 75.34 13.04

Table 4.3 presents obstacles to firm financing. Figures given in the table refer to

percentage of firms ranking each component as “moderate’ or “major” obstacle. The

obstacles listed are collateral, bank paperwork, high interests, special connections, bank

fund shortage, access to foreign banks, access to non banks, access to export finance,

access to lease finance and access to credit. Of these items a majority of Indian firms

complained only against three, collateral, bank paperwork and high interests. Since 1998

(the year of the survey) the Indian interest rates have come down substantially and paper

work has also been simplified. However, many SMEs in India feel that the Indian banks

have a bias in favour of large enterprises and are reluctant to lend to SMEs. Most Thai

firms have complaints with regard to almost all the items listed. However, most Chinese

Page 29

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 29/53

29

and Malaysian firms have not voiced their complaint against most of the items except in

the case of high interest rates where more than 52% Malaysian firms have complained.

By and large, Indian firms do not seem to suffer from financing problems compared to

the Asian neighbours.

Table 4.4Percentage of Firms Rating the Quality of Services as Bad

Country/Variables India China Malaysia Thailand SingaporeCustoms 40.00 14.29 11.59 28.76 1.09Courts 28.34 20.55 29.51 20.26 0Roads 68.53 22.47 21.11 40.00 0

Postal na 11.46 8.60 6.31 0Telephone 26.24 14.14 7.29 15.89 0Power 40.30 14.74 7.29 17.52 2.02Water 29.63 12.64 14.58 20.42 0Health 48.17 30.77 14.46 28.42 2.06Military 8.94 Na 15.63 19.86 1.10Government 40.35 Na 17.78 39.59 1.16Parliament 60.24 Na 25.00 45.17 1.16Central Bank na 15.58 10.45 43.90 1.11

Table 4.4 presents data on the percentage of firms rating the quality of services as

bad. The services included are customs, courts, roads, postal, telephone, power, water,

health, military, government, parliament, and central bank. As seen from the table, except

for military and courts, the Indian scores are higher than other countries. For courts

Malaysia is higher and for military Thailand is higher. However, except in two cases, the

Indian scores, though higher than for other countries is less than 50.

As seen from the four tables, governance factors appear to be more

important than other factors affecting business environment. This finding is in line with

the findings of other studies. In particular, a number of studies have shown that tax

Page 30

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 30/53

30

concessions have not been very effective in attracting investments (Loree and Guisinger

1995). On the other hand, corruption increases the transaction costs, sometimes to

intolerable levels (Wei 2000), and results in costly delays. Porto’s (2005) study shows

that high transport costs, cumbersome customs practices, costly regulations and bribes act

as export taxes that distort the efficient allocation of resources, lower wages, and increase

poverty. Furthermore, high transaction costs and delays will drive away investments by

MNEs and domestic firms.

Wei’s (2000) study analyses the determinants of the bilateral stocks of FDI from

12 source countries to 45 host countries. The source countries include the US, Japan,

Germany, UK, France Canada and Italy. In analysing FDI the following explanatory

variables are used: tax rate, corruption, tax credit, political stability, GDP, population,

distance between the two countries, linguistic ties between countries and wage rates. The

study shows the overwhelming importance of the corruption variable in influencing FDI

in relation to all the other variables. Two measures of corruption are used – the first, the

corruption rating from the International Country Risk Group and the second,

Transparency International Index. The study concludes that an increase in the corruption

level from that of Singapore to that of Mexico would have the same negative effect on

inward FDI as raising the tax rate by 18 to 50 percentage points, depending on the

specifications. This strong result of Wei (2000) has been reinforced by more recent

studies (Habib and Zurawicki 2002; Globerman 2002; Porto 2005 and Globerman and

Shapiro 2003).

Habib and Zurawicki (2002) analyse the impact of corruption on FDI for 89

countries for the period 1996-98. They use the corruption perception index produced by

Page 31

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 31/53

31

Transparency International. In explaining FDI inflows, in addition to corruption they also

introduce the following variables: population, GDP growth, per capita GDP,

unemployment rate, openness of the economy as measured by the ratio of trade to GDP,

science and technology indicators, cultural distance and political stability. Their findings

suggest that corruption is a serious obstacle for investment. Apart from corruption,

geographical distance and economic ties also emerge as important determinants of FDI.

Globerman and Shapiro (2003) examine the statistical importance of government

infrastructure as a determinant of FDI. They conducted the analysis in two stages. In the

first stage the probability that a country was a recipient of US FDI was estimated. In the

second stage their analysis was restricted to those countries that did receive FDI flows

and estimated equations that were focussed on the determinants of the amount of FDI

received. The governance measures were taken from Kaufmann et. al. (1999). These

measures include: rule of law index, which measures contract enforcement, property

rights, theft and crime; political instability and violence index, which measures armed

conflict, social unrest, ethnic tension and terrorists threats; regulatory burden index,

which measures government intervention, trade policy and capital restrictions;

government effectiveness index, measuring red tape and bureaucracy, wastes in

government and public infrastructure; graft and corruption index, measuring corruption

among public and private officials and the extent of bribery; and voice and accountability

index, which measures civil liberties, political rights, free press, and fairness of the legal

system. Their results consistently show that governance infrastructure is an important

direct determinant of whether a country will receive any US FDI, and, if so, how much.

Page 32

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 32/53

32

In sum, the literature surveyed so far clearly demonstrates that governance

infrastructure, and in particular, absence of corruption is a crucial determinant of FDI and

its impact is much stronger than other determinants like tax and fiscal policies, interest

rates and labour laws. Moreover, bribes, cumbersome customs practices and delays lower

wages and increase poverty. It is essential to take cognisance of these findings from the

literature in formulating policies to attract investment and achieve higher rates of growth.

V POLICIES TO IMPROVE INVESTMENT CLIMATE

To improve investment climate and usher in good governance, institutional reforms are a

must and they should aim at reducing if not at eliminating corruption, delays and

bottlenecks. Several less developed countries have not been paying sufficient attention to

these aspects but have been concentrating on other features like tax concessions to attract

investment. The prevalence of corruption can be attributed mainly to three factors:

monopoly power enjoyed by officials and other individuals, lack of accountability and

lack of transparency. Institutional reforms have to target these three factors, reduce

discretionary powers of the bureaucracy wherever possible and increase the role of

accountability and make the decision making process transparent. The 1991 Industrial

Policy Statement mentions these three factors but at the ground level things have not

changed much and India continues to be rated high in the corruption index by agencies

such as Transparency International.

It is not possible to completely eliminate the discretionary powers of the officials

but it is possible to minimise the instances where such powers are used and insist on time

bound decisions. Most bribery cases, in particular, the extortionist ones, occur because of

Page 33

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 33/53

33

the power of the officials to cause costly and intolerable delays. Harassment by causing

delay is a common complaint of persons dealing with port and transport authorities,

customs officials, and income tax officials. Some of the East Asian countries that have

been enjoying a flourishing trade have succeeded in eliminating delays in their ports and

customs. In Singapore, for example, the average ship turnaround for a container ship is

less than 8 hours while for India it could be as long as a week. Container delays at Indian

ports cost about US $70 million per year. Likewise it takes about three weeks to clear

export cargo at Indian air ports, due to the non-availability of Jumbo X-Ray machines

necessitating manual opening and checking of all containers. Indian road transport is also

plagued by delays. Thus commercial vehicles in India run only about 250 km per day

compared to about 600 km in several other countries. Poor mileage in India could be due

to bad roads and delays at road check posts, toll gates etc. (For details on the cost of

delays at Indian ports, airports and roads refer to Banik 2001). Unless India follows their

example and gets rid of delays it will become a victim of the emerging global regime. In

this context, it is also important to point out the inordinate delays in the courts and other

dispute settlement mechanisms. It is essential to note that there are persons who are

beneficiaries of the delays in court cases but they are not often the ones who have been

on the right side of the law. Thus invariably a delay by the judiciary encourages those

who benefit by deliberately breaking the law and the regulations. Countries where

institutions like courts and judiciary dealing with dispute settlements and in particular

commercial disputes, are either not in place or do not function efficiently are not likely to

attract investments. As investors cannot afford costly delays, they will shift their

operations to countries where these institutions are in place. Though these problems are

Page 34

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 34/53

Page 35

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 35/53

35

management patterns has not been sufficiently recognised by enterprises and

governments. Leading technological institutions like the IITs have to introduce

innovative in-service training programmes to improve the knowledge base of

technologists and to familiarise them with the rapid technological changes in their

respective fields. In all these cases the state should network with other institutions - both

the public and privately funded ones. It is not possible to launch a successful and

sustained programme to improve the skill content of the population without achieving

high levels of literacy and ensuring at least ten years of schooling for all children. While

India has been lagging behind in ensuring universal primary and secondary education,

several Asian countries have achieved this objective.

In addition to actively participating in the creation of human infrastructure, the

state has also to take a leading role in the creation of other physical infrastructure like

power, transport and communications Studies have shown that investments in

infrastructure have been more helpful in attracting investments than the offer of

concessions (Wheeler and Modi 1992, Loree and Guisinger 1995). In all these cases, the

state can induce the private sector to invest in infrastructure by removing some of the

century old archaic laws that are still in force. In this context, the Electricity Act of 2003

is in the right direction. However, it could run into several problems due to the practice of

cross subsidies, namely, industrial consumers paying a higher tariff to subsidise others

like agricultural and domestic (households) consumers. One way out of this problem

could be for the state governments to bear the cost of subsidies through a provision in

their budget rather than by asking the power units to bear the cost through cross

subsidisation.

Page 36

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 36/53

36

To drastically increase investment rates, the government should increase the

spending on infrastructure – both physical and social, introduce major administrative

reforms to improve efficiency and reduce delays and bottlenecks. These are not possible

unless the size of the government is reduced and transparency and accountability in

decision-making and administration are introduced. Recent studies have shown that the

per capita income of states that have large governments in terms of the size of the state

cabinet, number of departments and expenditure on bureaucracy has been growing more

slowly than that of those states that have smaller but purposive and more effective

governments. By and large a large, government is an enemy of an effective government.

The outsized governments also tend to spend all their revenue on administration and very

little on infrastructure and target groups like the poor and the underprivileged. The

introduction of a ceiling on the size of state and union cabinets is again a step in the right

direction.

VI FDI AND PRODUCTIVITY SPILLOVERS

It has been argued that FDI, apart from bringing superior technology and managerial and

marketing practices, will also have spillover effects resulting in increased productivity by

local firms. Studies have investigated the existence and importance of spillovers of FDI

for local firms in China, India and several South American countries. These studies show

that not all the local firms are likely to benefit from spillovers. Some firms will benefit

while some others will become victims of FDI inflows. In what follows it is proposed to

survey the main findings from literature and draw policy inferences for India.

Page 37

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 37/53

37

Th e Chin ese Experience

The impact of FDI on the performance of locally owned Chinese firms in manufacturing

has been investigated by Buckley et. al. (2002). In addition to analysing productivity

spillovers their study also analyses exports and the introduction of new products. One

important feature of the study is that it distinguishes different types of productivity

advantages for overseas Chinese investment and investments by developed countries. The

impact of FDI on government owned and privately (including collectively) owned

enterprises is also separately discussed.

The study shows that overseas Chinese capital did not enhance the productivity of

Chinese firms but the non-Chinese investments did. Their results further showed that

while non-Chinese capital generated both technological and market access (exports)

spillovers, the overseas Chinese capital enabled only market access benefits. The non-

Chinese investments also contributed to the creation of new products by the local Chinese

firms. The study also reveals that FDI did not contribute to productivity and export

spillovers for the government owned enterprises. Consequently, the spillovers were

limited to privately owned enterprises. This study thus brings out clearly the differential

capacity of firms to absorb technology based on ownership.

The I ndian Ex peri ence

A study by Siddharthan and Lal (2004) shows the presence of significant spillover effects

from FDI. During the initial years of liberalisation, namely, the early 1990s, the spillover

effects were modest but later they increased sharply and stabilised towards the end of the

decade. However, not all domestic firms gained equally from the spillovers. Domestic

Page 38

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 38/53

Page 39

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 39/53

39

and not due to FDI. Moreover, their results show that the productivity of domestic

enterprises declines when foreign investment increases, suggesting a negative spillover

from foreign to domestic enterprises. They consider this as market stealing effect.

While Aitken and Harrison (1999) obtained a negative spillover effect for

Venezuela, Kokko et.al. (1996) have not found evidence of technology spillovers from

FDI in Uruguayan manufacturing plants. Their regression analysis shows no signs of

spillovers from FDI for a sample of 159 locally owned manufacturing plants. However,

they have found positive spillovers in the case of a sub sample of plants that had small

and moderate technology gaps vis-à-vis foreign firms but not in the case of local plants

facing large gaps. Perhaps when foreign and domestic firms operated on the same

technological paradigm they experienced spillovers, not otherwise. They have also found

many domestic plants experiencing higher productivity levels compared to foreign firms.

In such cases the spillover could be from the domestic to the foreign firm.

Some studies argue that the kind of spillovers will depend on the nature of the

economic regime, namely, import substituting or trade promoting regime. In this context,

Balasubramanayam et. al. (1996) demonstrate that unlike import-substitution regimes,

export-promoting regimes attract FDI which has a significant impact on the growth of

GDP. Kokko et.al. (2001) analyse the characteristics of FDI inflows during two different

trade regimes in Uruguay and examine whether FDI in the two regimes had differential

impacts on Uruguay industry. Their results suggest that foreign firms established in the

import substitution regime, that is, before 1973, generate positive productivity spillovers

to local firms but the impact of foreign firms established after 1973 is the opposite. Thus

the presence of import substituting MNEs had a more beneficial effect on labour

Page 40

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 40/53

40

productivity of local firms than the presence of export oriented MNEs. Some studies

relate the spillovers to the development of local markets. For example, Alfaro et. al.

(2004) argue that the lack of development of local financial markets can limit the

economy’s ability to take advantage of potential spillovers.

Poli cies to I ncrease Spil lovers

From the literature survey three factors emerge important in influencing spillovers –

technological capabilities of the local firms as indicated by the productivity and

technological gap between the local firm and MNE/affiliate; networking of firms,

namely, networking between firms, academic institutions, research laboratories, and

MNEs; and institutional and legal environment. These three factors are not mutually

exclusive. Rather, they mutually interact. Technological capabilities of firms depend on

networking with academic research institutions and national laboratories. The S&T

statement 2001 of the Government of India explicitly recognises the importance of

academic institutions and national laboratories collaborating with industry. However, it

does not present a concrete plan of action. In recent times several developed countries

like Japan and Germany have realised the importance of such collaboration and have

enacted Acts to facilitate such cooperation. India can also benefit from the experience of

these countries and enact similar Acts to promote the technological development of

Indian enterprises.

Germany and Japan found that they were lagging behind the US in science-based

sectors like biotechnology. These countries found themselves in what is termed as

“public sector bind” and lacked incentives for scientists to engage in commercial

Page 41

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 41/53

41

activities such as patenting and firm funding (Lehrer and Asakawa 2004, page 922). The

Indian situation is somewhat similar to that of Japan and Germany – the dominance of

national laboratories working in these areas and lack of achievement in terms of

commercialisation and patenting. In order to enhance global competitiveness of Japanese

firms in high tech industries and promote active collaboration between universities and

public sector laboratories Japan enacted the “Strengthening Industrial Technology Bill”

which was passed by the legislature in April 2000. The new law allowed the faculty in

national universities to assume management positions in companies established to

develop their technologies, to work after office hours with pay, and to take up to three

years off to commercialise discoveries and then return to their faculty positions (Lehrer

and Asakawa 2004). Furthermore, the Japanese lawmakers allowed universities to set up

their own technology licensing organisations. In 1999 the “Special Law for Revitalising

Industry” was passed that settled the ownership of government-sponsored research in

favour of the researcher - the US has similar laws in place.

In India, the output of government-sponsored research, in particular, that funded

by the Ministry of Science and Technology, is considered the property of the government

and the researcher has very little say in its commercialisation and application. This

separation of the technology creator from the use of technology has stood in the way of

commercialisation of technology. If India is to benefit from the technology its

laboratories have created, then it should enact laws that are in accordance with

international practice and in particular on the lines of countries that are leaders in

technology creation like the US and Japan. The restrictive Indian rules have resulted in

two negative fallouts. It has stood in the way of attracting world-class talent to national

Page 42

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 42/53

Page 43

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 43/53

43

Cooperation between business firms and research units depends, to a large extent

on the R&D base of business units (Laursen and Salter 2004). Studies show that the

direct contribution of universities to direct industrial practice is concentrated in a small

number of high tech sectors among firms that spend on R&D. In fact one of the

objectives of in-house R&D units is to search and identify relevant technology for

commercialisation (Cohen 1995; Cohen and Levinthal 1989). Knowledge sharing and

cooperation between two units depend largely on forging of long term strategic alliances

(Helm and Kloyer 2004). Arm’s length purchase of technology rarely works as firms

normally do not trust unrelated third parties in matters relating to sharing of intangible

assets like knowledge and technology. The Indian public sector undertakings are at a

disadvantage here as the government audit rules favour arm’s length purchases against

open tenders and disapprove vendor development and long-term strategic alliances that

are crucial for technology development, knowledge sharing and product quality

improvement. Here again it is important to enact appropriate laws and build institutions

to encourage networking, undertaking joint R&D with vendors and backward and

forward integration through strategic alliances.

VII LIBERALISATION, MNEs AND EXPORTS

One of the objectives of liberalisation is to attract export oriented FDI, modernise industries

through technology acquisition and promote exports. International markets for standard and

traditional exports have been stagnating while the market for high tech and differentiated

products have been expanding rapidly (Lall 1999). Under these conditions it is important for

India to promote exports of sophisticated goods and move up the value chain. However,

Page 44

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 44/53

44

studies explaining inter-firm differences in Indian exports have found technology factors

like R&D and skill intensity of workforce important only in the case of low and medium

tech industries. R&D and skill variables were not significant for high tech industries (Kumar

and Siddharthan 1994). With regard to the role of MNEs in promoting exports, most studies

have captured it by using a MNE dummy and by and large, it was not significant, indicating

that the export behaviour of MNE affiliates and Indian firms are not very different.

Furthermore, studies have found that in low and medium tech industries, export

competitiveness is to be obtained on the basis of indigenous technological effort and through

use of labour intensive production process. In the high tech industries, on the other hand,

import of technology and thus networking with MNEs, a higher degree of automation, and

modernisation appear to be important for breaking into international markets.

M NEs and Exports

The statistical support for a positive relationship between MNEs/joint ventures and exports

has been very weak. For example, Aggarwal’s (2002) study does not find MNEs significant

in explaining export intensities of firms in India during the period 1996-2000. In the study

the significant determinants of exports are firm size and import of capital goods, materials

and components. The explanation given by Aggarwal is that India has been attracting host

market seeking MNEs and not efficiency seeking MNEs. For attracting export-oriented

efficiency seeking MNEs India needs to improve its infrastructure and other facilities apart

from introducing liberalisation measures. Likewise, studies for Sri Lanka (Athukorala,

Jayasuriya, and Oczkowski 1995) also show that MNEs’ export intensities are not higher.

Similarly Willmore (1992) found mixed results for Brazil. In this context, some studies

Page 45

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 45/53

45

have raised methodological issues and have questioned the methods used to test for the

role of MNEs in exports.

Siddharthan and Nollen (2004) argue that MNE affiliates behave differently from

other firms and that the magnitude and sign of the coefficients of some determinants of

exports will differ between the MNEs and other firms. Therefore, in order to obtain more

meaningful and interpretable results, they advocate fitting separate equations for different

groups of firms. Mere introduction of a MNE dummy as was done in the earlier studies

may not yield satisfactory results.

Their study demonstrates that for information technology firms in India, the

explanation of export performance depends in part on the firm’s foreign collaboration and

on the amount and type of technology that it acquires from abroad. For affiliates of

MNEs, both explicit technology transfer from purchases of licenses and payments of

royalties, and tacit technology transfer received from foreign ownership contribute to

greater export intensity. They do so independently, without a complementary interaction

to further boost export performance.

In contrast, the explanation for the export performance of strictly domestic firms

that have neither a foreign equity stake nor foreign licenses is different. For these firms,

more imports of raw materials and components as a source of product quality

improvement contribute to more exports of products, as do the larger size of a firm and

greater capital intensity. These export determinants for domestic firms are unimportant

for MNE affiliates, they argue, because the foreign ownership influence in the MNE

affiliates makes them less necessary.

Page 46

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 46/53

46

SM Es and Exports

The relationship between exports, technology and MNEs is a complex one. The Indian

evidence shows that MNEs do not play a significant role in Indian exports. In recent

years the export intensities of MNEs have increased but despite this their share in the

Indian export is small. On the other hand, the exports of small and medium enterprises

(SMEs) constitute the bulk of the Indian exports. If technology is crucial to exports, then

SMEs ought to be at a disadvantage as there are sizable scale economies in in-house

R&D and technology acquisition from other enterprises. This raises the question of the

nature of competitive advantage of the SMEs in exports. In this context there are some

interesting results from studies on the export performance of Italian SMEs and their

competitive advantages. India can draw valuable lessons from these studies.

The study by Nassimbeni (2001) based on a sample of 165 small manufacturing

firms in furniture, manufacturing and electro-electronics sectors in Italy reveals a number

of interesting results relating to technological and innovative capacity related factors that

significantly differentiate exporting and non-exporting small enterprises. It shows the

crucial role of the management of product related activities in promoting exports. Product

management depends on inventiveness and an ability to forge inter-organisational

relationships.

In this context, the role of internet and e-commerce and in particular business to

business (B2B) commerce assumes importance. The study by Freund and Weinhold

(2004) finds that internet stimulates trade. Accordingly the success of SMEs in the export

front would crucially depend on their ability to network, which in turn would depend on

Page 47

8/12/2019 Indian Industrial Policy and Global Competition

http://slidepdf.com/reader/full/indian-industrial-policy-and-global-competition 47/53

47

the infrastructure facilities for doing B2B commerce. These in turn would depend on the

cost, reliability and availability of internet facilities, the band width and connectivity.

L iberali sation and Value of Ex ports

Liberalisation and technology imports can affect exports in two ways: first, by increasing

export intensities of firms and the volume of exports, and second, by increasing the unit