29

INDIAN INSURANCE INDUSTRY INDIAN INSURANCE INDUSTRY 2001-02 2001-02 D. SENGUPTA D. SENGUPTA CHAIRMAN GENERAL INSURANCE CORPORATION OF INDIA

| Date post: | 10-Dec-2015 |

| Category: |

Documents |

| Upload: | rahul-pujari |

| View: | 235 times |

| Download: | 0 times |

INDIAN INSURANCE INDUSTRYINDIAN INSURANCE INDUSTRY2001-022001-02

D. SENGUPTAD. SENGUPTACHAIRMAN

GENERAL INSURANCE CORPORATION OF INDIA

The Indian general insurance business has been in the Government sector since 1973 and transacted by GIC and its four wholly owned subsidiary companies.

In consonance with Government’s commitment to WTO, in 1999 the insurance industry is opened up to private sector insurance companies with foreign partners

Opening up of Indian Insurance Industry

Opening up of Indian Insurance Industry

India is the world’s largest democracy with population of over 1 billion in 2000. It is a member of the Commonwealth. It is a Union of States comprising 28 States and 4 Union Territories.

About 28% population is urbanDespite changes in ruling parties, the country remained democratic with an elected government since independence in 1947The Per Capita Gross Domestic Product is approx. US$ 350 The per capita general insurance premium is Rs. 98 (US$ 2.09)Economic Growth Rate is approximately 6.1%Inflation rate is 5.4% (Aug-2001)

Exchange rate : US$ is Rupees 47.10 (Aug-2001)

India - factsIndia - facts

• Prior to 1999 Government owned GIC was acting as holding company and reinsurer

• Four GIC-owned companies carrying out all the non-life insurance business in the country.

• The four companies have a net work of 4127 Offices spread all over the country. They also have branch offices and/or joint venture operations in 30 foreign countries.

• Gross Direct Premium as at 31-Mar-2001 is Rs. 97998 Million which is approximately US $ 2085 Million

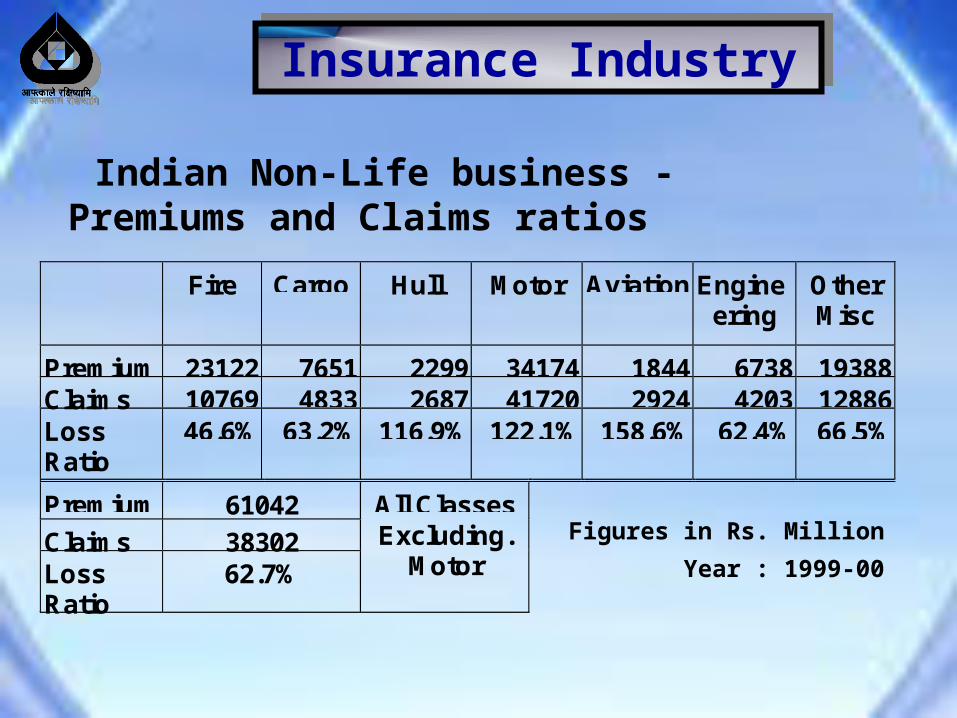

Insurance IndustryInsurance Industry

Fire Cargo Hull Motor Aviation Engineering

OtherMisc

Premium 23122 7651 2299 34174 1844 6738 19388Claims 10769 4833 2687 41720 2924 4203 12886LossRatio

46.6% 63.2% 116.9% 122.1% 158.6% 62.4% 66.5%

Premium 61042

Claims 38302LossRatio

62.7%

All ClassesExcluding.

Motor

Indian Non-Life business - Premiums and Claims ratios

Figures in Rs. Million

Year : 1999-00

Insurance IndustryInsurance Industry

• A large portion of general insurance business is Tariff controlled.

• Fire, Motor and Engineering classes are fully tariff controlled. Marine Hull major fleets are Tariff rated. Some part of Marine Cargo business is also tariffed.

• 20% of the premium written by the direct companies is ceded to the GIC as Obligatory Cessions.

• Around 89% of the premium was retained within the country and 11% is ceded outside the country.

Insurance IndustryInsurance Industry

• Reinsurance premium ceded out is mainly in respect of Excess of Loss protections and proportional premium in respect of Fire/IAR Peak Risks, large engineering construction projects, Marine Hull- super tankers, Oil cargo shipments and Aviation-airline fleet risks.

• Largest valued fire risk is an oil refinery with a PML of Rs. 23000 Million (Approx. US$ 490 Million).

Insurance IndustryInsurance Industry

• Life insurance business was transacted by the state owned Life Insurance Corporation of India with branch and agency net-work all over the country.

• Total life premium in the country for the financial year 2000-01 is Rs. 348.77 Billion which is approximately US $ 7.42 million. It is estimated that for 2001-02 it would be Rs. 480 Billion ($ 10.20 Billion)..

Insurance IndustryInsurance Industry

• In 1999 the Insurance ReguIatory and Development Authority (IRDA) Act was enacted and an authority (the Regulator) to control, regulate and enable development of insurance industry namely the IRDA was set up.

• Insurance companies in the private sector are allowed both in Life and Non-Life categories but composite companies are not permitted.

Insurance IndustryInsurance Industry

The requirements for private sector Insurance Companies are

• Minimum share capital of Rs. 1000 Million (US$ 21.25 Million approx)

• Foreign joint-venture partners if any, are allowed to hold a maximum of 26% of the share capital.

• GIC appointed as the “Indian Reinsurer” with exclusively reinsurance function and corollary functions.

Insurance IndustryInsurance Industry

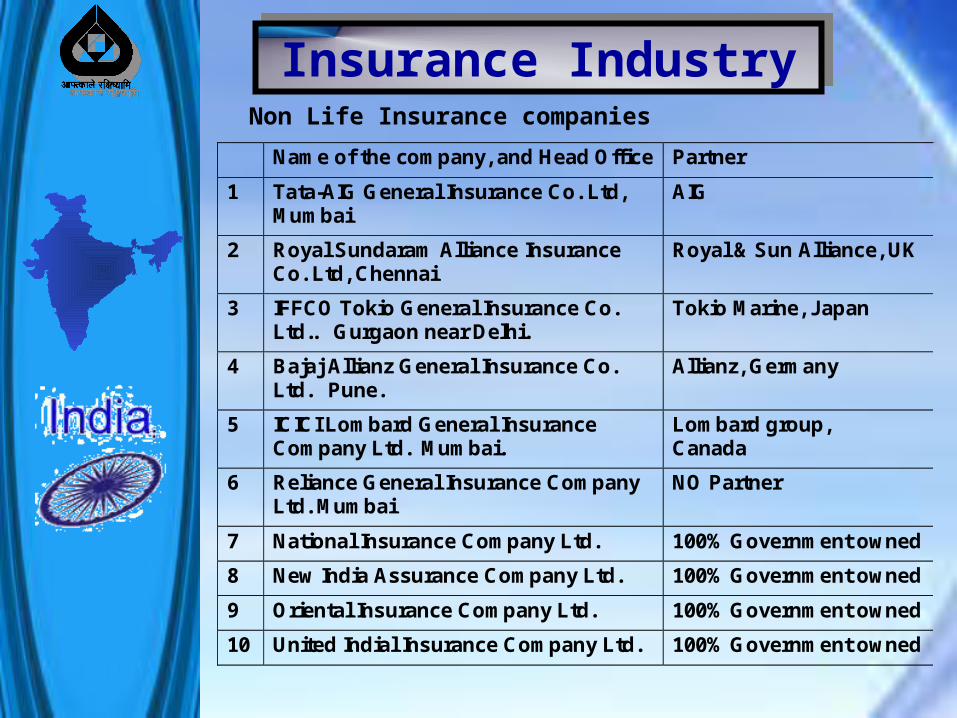

• The Industry today

Today in addition to the four existing public-sector general insurance companies, six private insurance companies have been licensed to function.

Most of them have started functioning from the beginning of this financial year. Following Tables show details

Insurance IndustryInsurance Industry

Non Life Insurance companies

Insurance IndustryInsurance Industry

Name of the company, and Head Office Partner

1 Tata-AIG General Insurance Co. Ltd,Mumbai

AIG

2 Royal Sundaram Alliance InsuranceCo. Ltd, Chennai

Royal & Sun Alliance, UK

3 IFFCO Tokio General Insurance Co.Ltd.. Gurgaon near Delhi.

Tokio Marine, Japan

4 Bajaj Allianz General Insurance Co.Ltd. Pune.

Allianz, Germany

5 ICICI Lombard General InsuranceCompany Ltd. Mumbai.

Lombard group,Canada

6 Reliance General Insurance CompanyLtd. Mumbai

NO Partner

7 National Insurance Company Ltd. 100% Government owned

8 New India Assurance Company Ltd. 100% Government owned

9 Oriental Insurance Company Ltd. 100% Government owned

10 United Indial Insurance Company Ltd. 100% Government owned

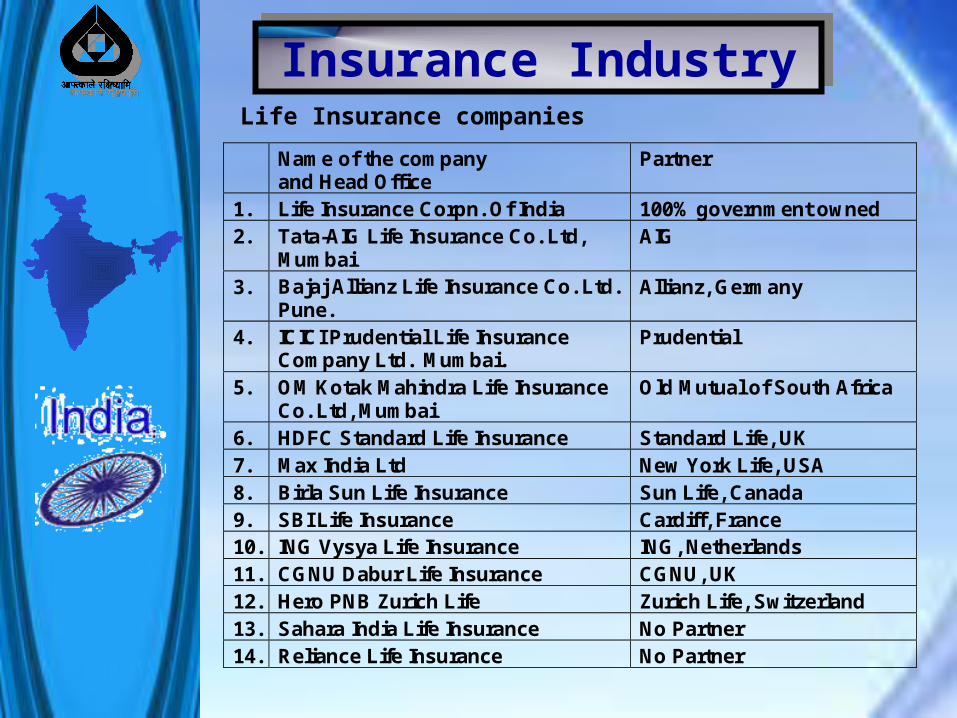

Insurance IndustryInsurance IndustryLife Insurance companies

Name of the companyand Head Office

Partner

1. Life Insurance Corpn. Of India 100% government owned2. Tata-AIG Life Insurance Co. Ltd,

MumbaiAIG

3. Bajaj Allianz Life Insurance Co. Ltd.Pune.

Allianz, Germany

4. ICICI Prudential Life InsuranceCompany Ltd. Mumbai.

Prudential

5. OM Kotak Mahindra Life InsuranceCo. Ltd, Mumbai

Old Mutual of South Africa

6. HDFC Standard Life Insurance Standard Life, UK7. Max India Ltd New York Life, USA8. Birla Sun Life Insurance Sun Life, Canada9. SBI Life Insurance Cardiff, France10. ING Vysya Life Insurance ING, Netherlands11. CGNU Dabur Life Insurance CGNU, UK12. Hero PNB Zurich Life Zurich Life, Switzerland13. Sahara India Life Insurance No Partner14. Reliance Life Insurance No Partner

Insurance IndustryInsurance Industry

Credit Insurance companies

Name of the company, and HeadOffice

Partner

Export Credit GuaranteeCorporation, Mumbai

100% Government owned

New India Assurance Company Gerling global, Germany

Insurance IndustryInsurance Industry

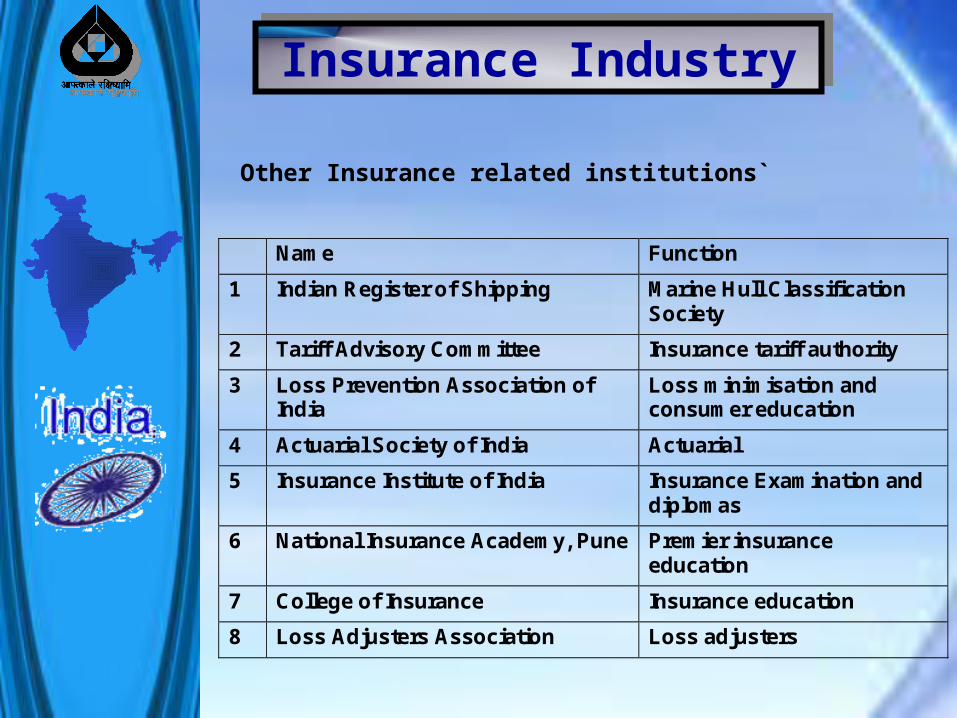

Other Insurance related institutions`

Name Function

1 Indian Register of Shipping Marine Hull ClassificationSociety

2 Tariff Advisory Committee Insurance tariff authority

3 Loss Prevention Association ofIndia

Loss minimisation andconsumer education

4 Actuarial Society of India Actuarial

5 Insurance Institute of India Insurance Examination anddiplomas

6 National Insurance Academy, Pune Premier insuranceeducation

7 College of Insurance Insurance education

8 Loss Adjusters Association Loss adjusters

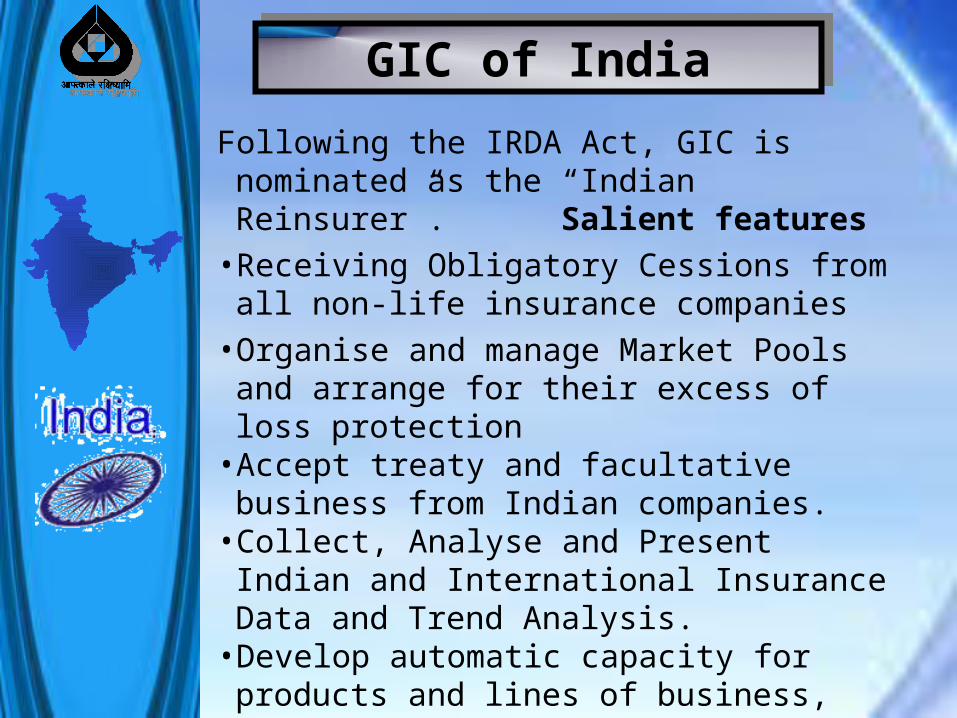

Following the IRDA Act, GIC is nominated as the “Indian Reinsurer”. Salient features

• Receiving Obligatory Cessions from all non-life insurance companies

• Organise and manage Market Pools and arrange for their excess of loss protection

• Accept treaty and facultative business from Indian companies.

• Collect, Analyse and Present Indian and International Insurance Data and Trend Analysis.

• Develop automatic capacity for products and lines of business, including new ones to be introduced

GIC of IndiaGIC of India

GIC as the International Reinsurer• GIC has been accepting foreign inward

reinsurance for 25 years now and has built up strong long-standing relationship with major international reinsurers such as Axa, SCOR, Partner Re, La Reunion, Lloyd’s Syndicates, Munich Re, Swiss Re and Zurich Re.

• Budgeted income from foreign inward business for 2001-02 is US $ 200 Million.

• Capacity offered by GIC USD 50 mln on facultative risks and USD

10 mln for treaties• GIC rated ‘A’ by AM Best

GIC of IndiaGIC of India

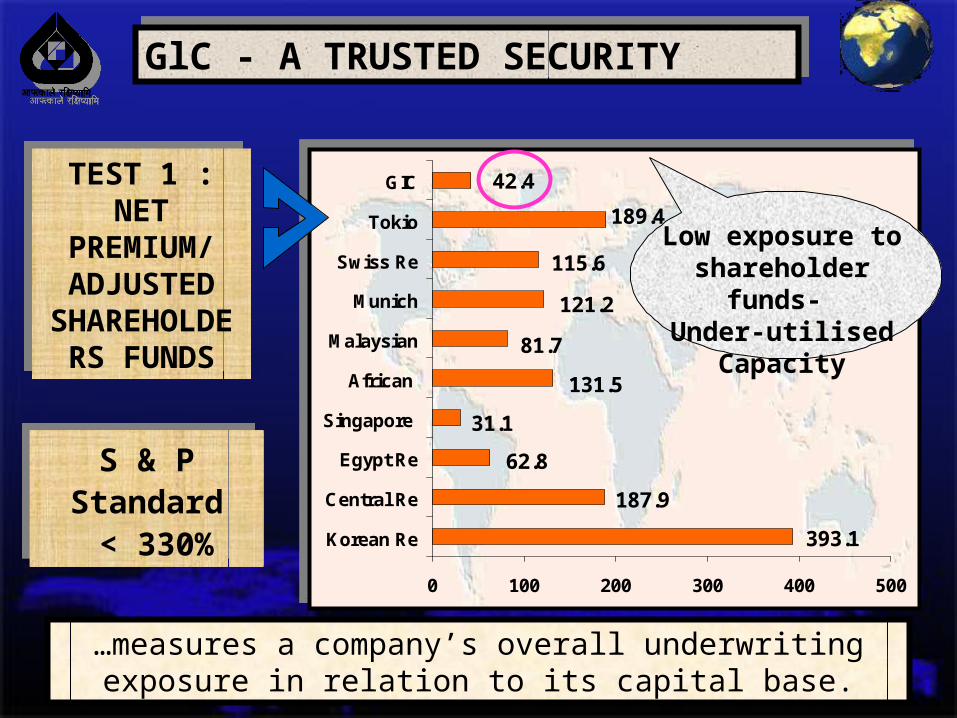

GlC - A TRUSTED SECURITYGlC - A TRUSTED SECURITY

393.1

187.9

62.8

31.1

131.5

81.7

121.2

115.6

42.4

189.4

0 100 200 300 400 500

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

393.1

187.9

62.8

31.1

131.5

81.7

121.2

115.6

42.4

189.4

0 100 200 300 400 500

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

S & P Standard < 330%

S & P Standard < 330%

TEST 1 : NET PREMIUM/ ADJUSTED

SHAREHOLDERS FUNDS

TEST 1 : NET PREMIUM/ ADJUSTED

SHAREHOLDERS FUNDS

…measures a company’s overall underwriting exposure in relation to its capital base.

Low exposure to shareholder funds-

Under-utilised Capacity

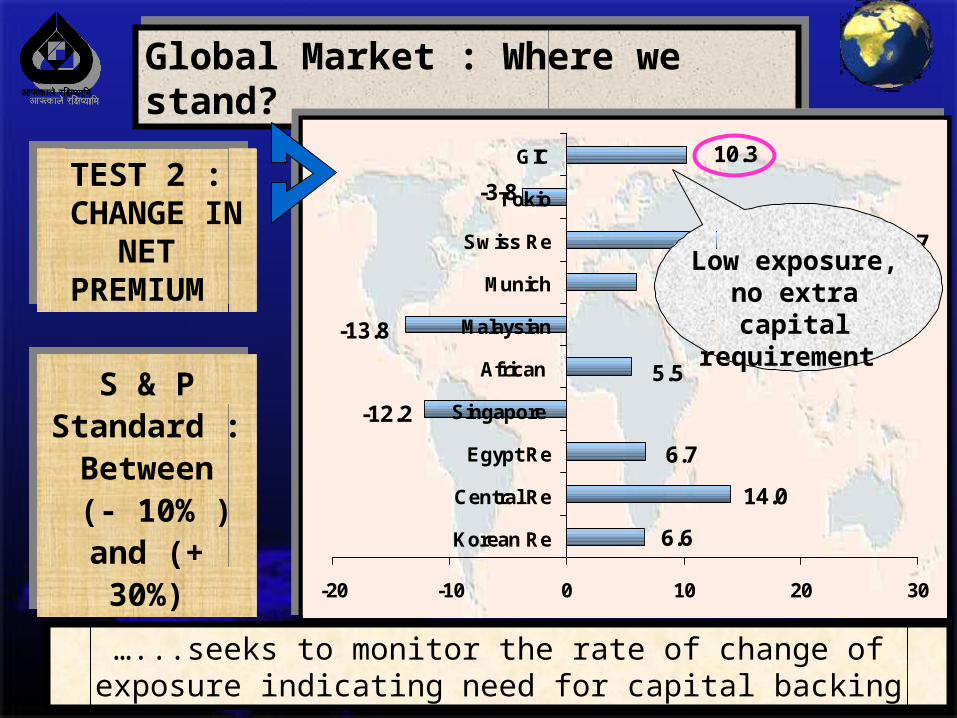

Global Market : Where we stand?Global Market : Where we stand?

TEST 2 : CHANGE IN

NET PREMIUM

TEST 2 : CHANGE IN

NET PREMIUM

S & P Standard : Between

(- 10% ) and (+ 30%)

S & P Standard : Between

(- 10% ) and (+ 30%)

…...seeks to monitor the rate of change of exposure indicating need for capital backing

6.6

14.0

6.7

-12.2

5.5

-13.8

6.0

25.7

10.3

-3.8

-20 -10 0 10 20 30

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

6.6

14.0

6.7

-12.2

5.5

-13.8

6.0

25.7

10.3

-3.8

-20 -10 0 10 20 30

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Low exposure, no extra capital requirement

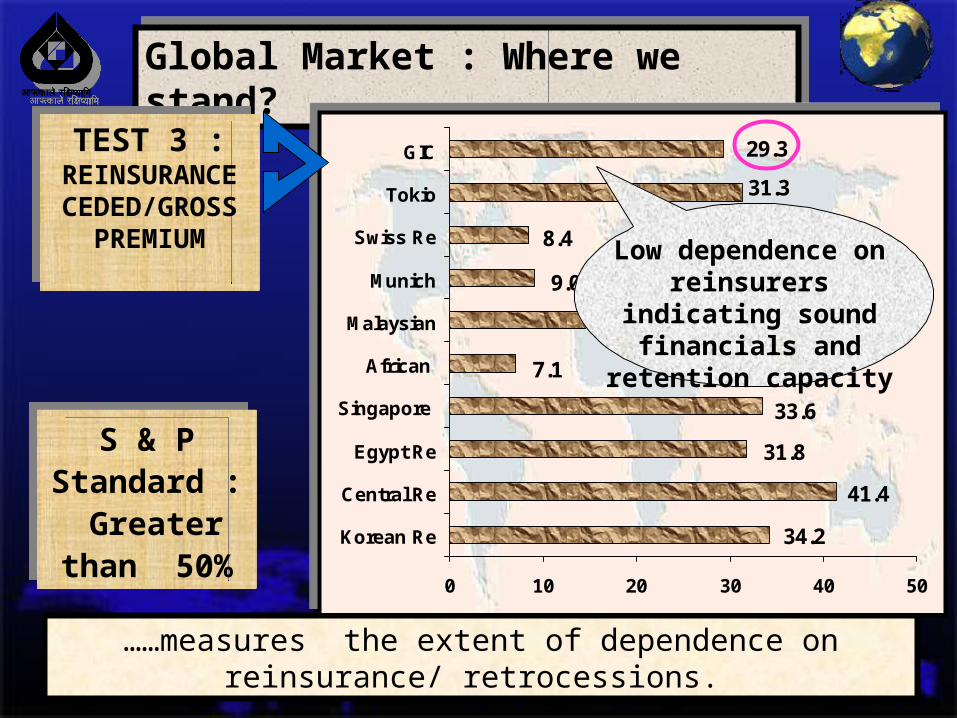

Global Market : Where we stand?Global Market : Where we stand?

TEST 3 : REINSURANCE CEDED/GROSS

PREMIUM

TEST 3 : REINSURANCE CEDED/GROSS

PREMIUM

S & P Standard :

Greater than 50%

S & P Standard :

Greater than 50%

……measures the extent of dependence on reinsurance/ retrocessions.

34.2

41.4

31.8

33.6

7.1

43.7

9.0

8.4

29.3

31.3

0 10 20 30 40 50

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

34.2

41.4

31.8

33.6

7.1

43.7

9.0

8.4

29.3

31.3

0 10 20 30 40 50

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Low dependence on reinsurers indicating sound financials and

retention capacity

Global Market : Where we stand?Global Market : Where we stand?

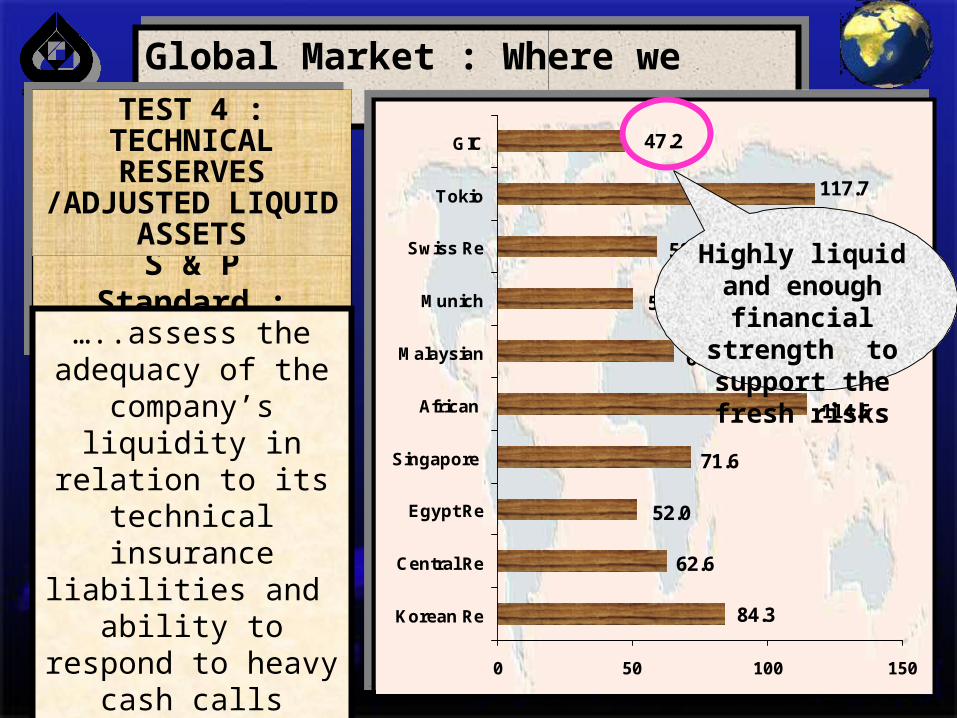

S & P Standard : < 105%

S & P Standard : < 105%

TEST 4 : TECHNICAL RESERVES

/ADJUSTED LIQUID ASSETS

TEST 4 : TECHNICAL RESERVES

/ADJUSTED LIQUID ASSETS

…..assess the adequacy of the

company’s liquidity in relation to its

technical insurance liabilities and

ability to respond to heavy cash calls

117.7

47.2

58.9

50.1

65.5

114.5

71.6

52.0

62.6

84.3

0 50 100 150

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

117.7

47.2

58.9

50.1

65.5

114.5

71.6

52.0

62.6

84.3

0 50 100 150

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Highly liquid and enough financial

strength to support the fresh risks

Global Market : Where we stand?Global Market : Where we stand?

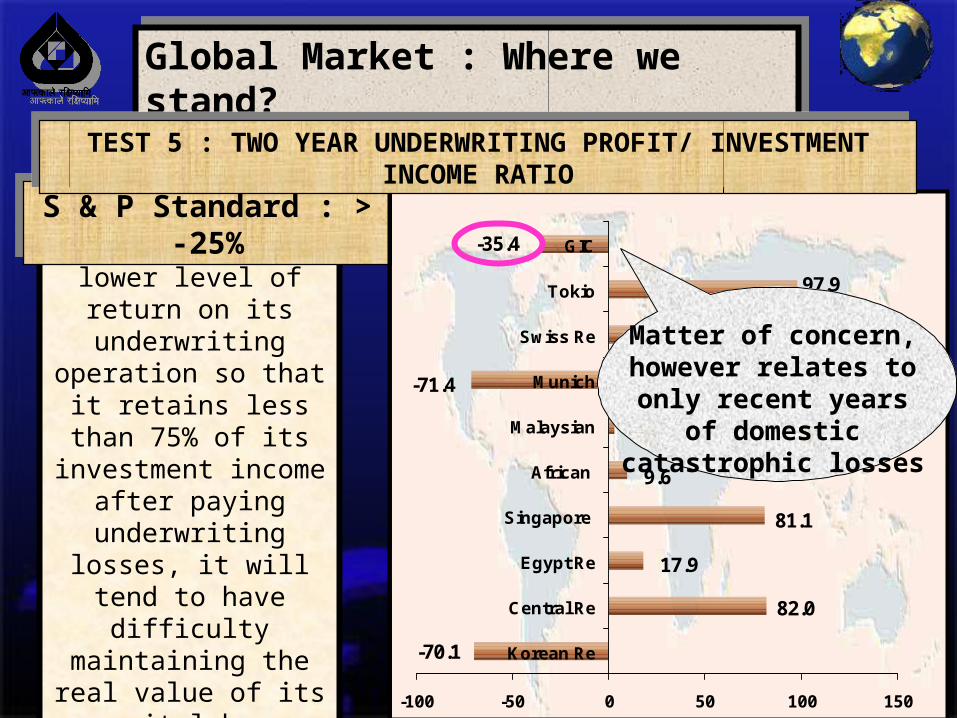

…..where a company has a

lower level of return on its underwriting operation so that it

retains less than 75% of its

investment income after paying

underwriting losses, it will tend to have

difficulty maintaining the real value of its capital

base

S & P Standard : > -25%S & P Standard : > -25%

97.9

-35.4

12.7

-71.4

2.7

9.6

81.1

17.9

82.0

-70.1

-100 -50 0 50 100 150

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

TEST 5 : TWO YEAR UNDERWRITING PROFIT/ INVESTMENT INCOME RATIO

TEST 5 : TWO YEAR UNDERWRITING PROFIT/ INVESTMENT INCOME RATIO

Matter of concern, however relates to only

recent years of domestic catastrophic

losses

Global Market : Where we stand?Global Market : Where we stand?

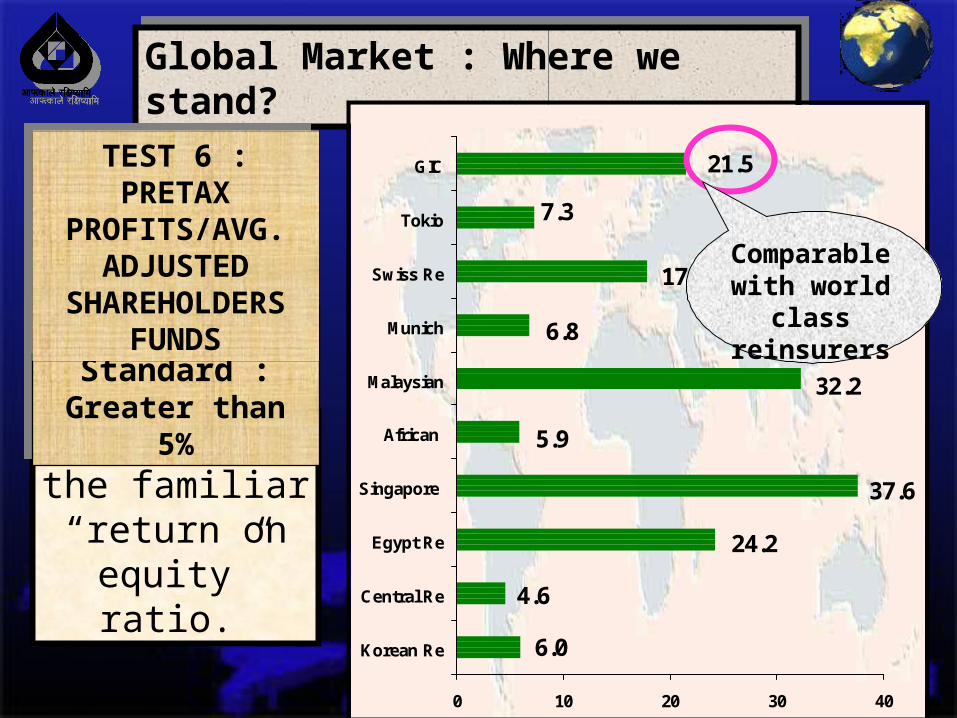

….this is the familiar

“return on equity” ratio.

S & P Standard : Greater than 5%S & P Standard : Greater than 5%

TEST 6 : PRETAX PROFITS/AVG.

ADJUSTED SHAREHOLDERS

FUNDS

TEST 6 : PRETAX PROFITS/AVG.

ADJUSTED SHAREHOLDERS

FUNDS

7.3

21.5

17.8

6.8

32.2

5.9

37.6

24.2

4.6

6.0

0 10 20 30 40

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Comparable with world class reinsurers

Global Market : Where we stand?Global Market : Where we stand?

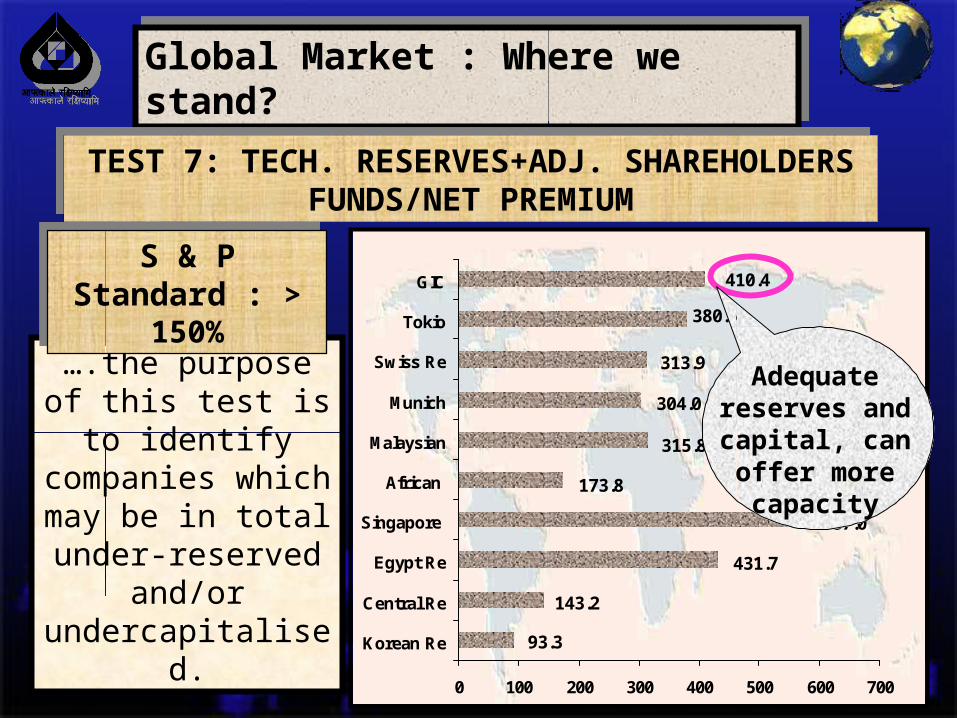

….the purpose of this test is to

identify companies which may be in total under-reserved

and/or undercapitalised.

S & P Standard : > 150%

S & P Standard : > 150%

TEST 7: TECH. RESERVES+ADJ. SHAREHOLDERS FUNDS/NET PREMIUM

TEST 7: TECH. RESERVES+ADJ. SHAREHOLDERS FUNDS/NET PREMIUM

380.6

410.4

313.9

304.0

315.8

173.8

587.0

431.7

143.2

93.3

0 100 200 300 400 500 600 700

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Adequate reserves and capital, can offer more capacity

Global Market : Where we stand?Global Market : Where we stand?

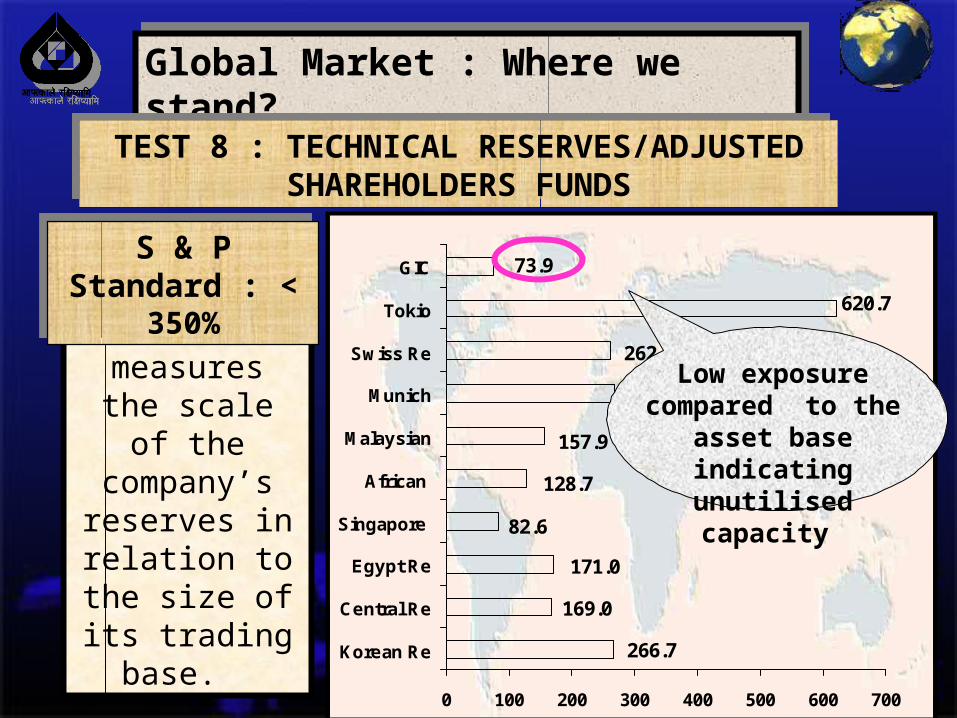

….this test measures the scale of the company’s reserves in

relation to the size of its

trading base.

S & P Standard : < 350%

S & P Standard : < 350%

TEST 8 : TECHNICAL RESERVES/ADJUSTED SHAREHOLDERS FUNDS

TEST 8 : TECHNICAL RESERVES/ADJUSTED SHAREHOLDERS FUNDS

620.7

73.9

262.7

268.5

157.9

128.7

82.6

171.0

169.0

266.7

0 100 200 300 400 500 600 700

Korean Re

Central Re

Egypt Re

Singapore

African

Malaysian

Munich

Swiss Re

Tokio

GIC

Low exposure compared to the asset

base indicating unutilised capacity

• GIC intends to expand the foreign inward operations and emerge as an international professional reinsurer. The targeted thrust areas are the Far-East Asia, South Asia, the Middle East and Africa.

• GIC has opened a representative office in London in 2001 and intends to open further offices in Moscow, Jeddah and Dubai.

• GIC has joint venture partners in Singapore (India International) and Malaysia (United Oriental insurance Co) and Kenya (KenIndia Insurance Co., Nairobi),

GIC of IndiaGIC of India

THANK YOUTHANK YOUTHANK YOUTHANK YOU

GIC of IndiaGIC of India

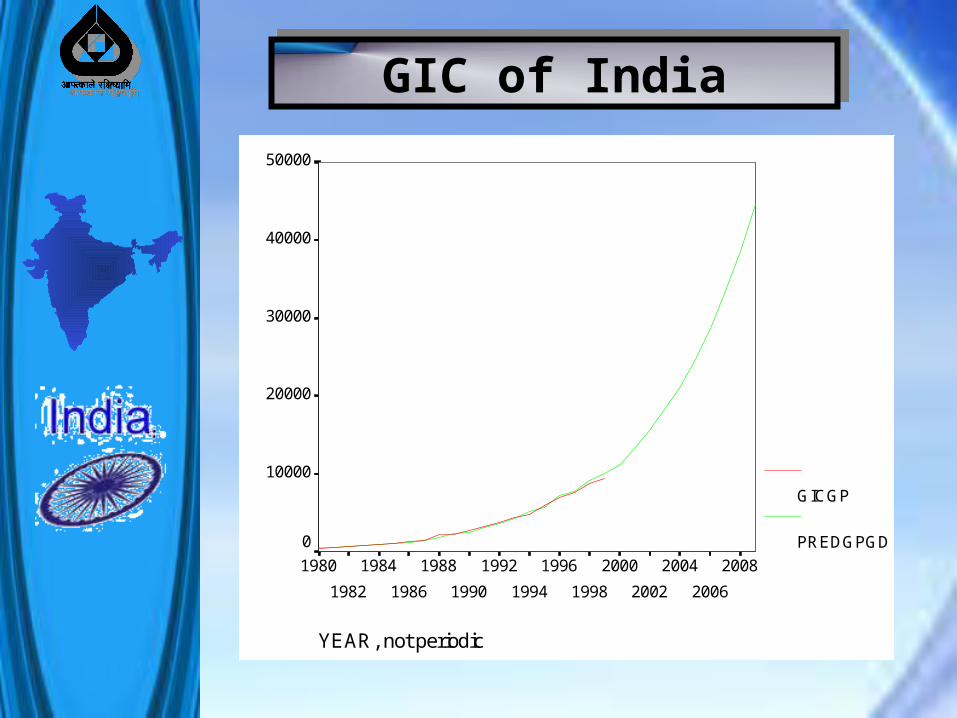

YEAR, not periodic

2008

2006

2004

2002

2000

1998

1996

1994

1992

1990

1988

1986

1984

1982

1980

50000

40000

30000

20000

10000

0

GICGP

PREDGPGD

GIC of IndiaGIC of India

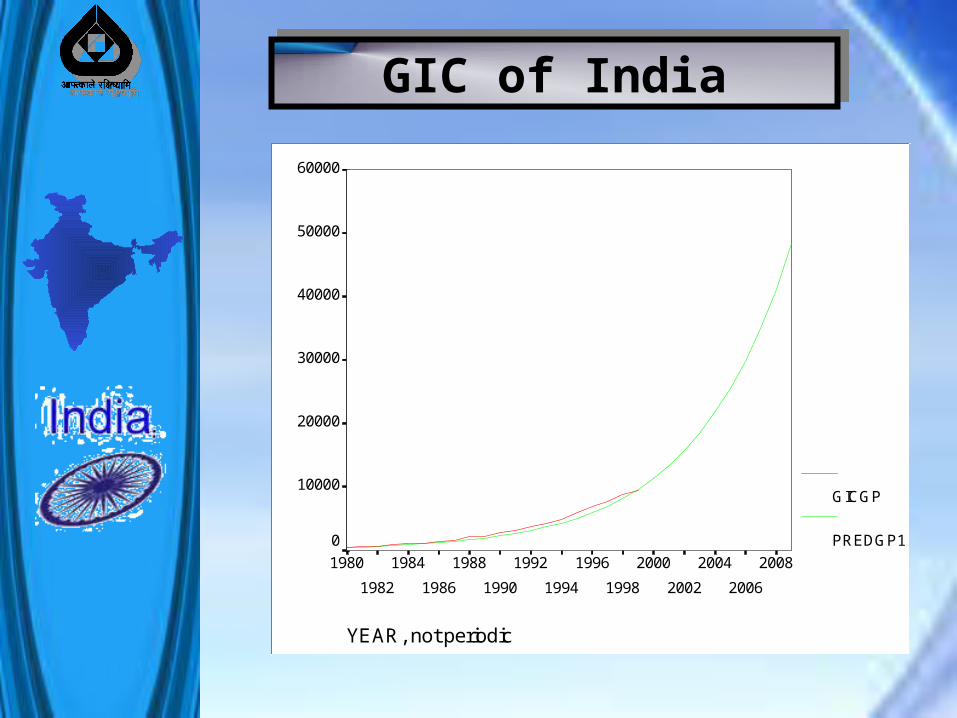

YEAR, not periodic

2008

2006

2004

2002

2000

1998

1996

1994

1992

1990

1988

1986

1984

1982

1980

60000

50000

40000

30000

20000

10000

0

GICGP

PREDGP1