43

Indian Retail Indian Retail Tomorrow¶s ³Promised Land´ Tomorrow¶s ³Promised Land´ Sushant Das Sushant Das

| Date post: | 10-Apr-2018 |

| Category: |

Documents |

| Upload: | sushanta-das |

| View: | 223 times |

| Download: | 0 times |

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 1/43

Indian RetailIndian Retail

Tomorrow¶s ³Promised Land´ Tomorrow¶s ³Promised Land´

Sushant DasSushant Das

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 2/43

IndiaIndia

22ndnd largestlargestgrowinggrowingecomonyecomony

33rdrd largestlargesteconomy ineconomy interms of GDPterms of GDPin the next 5in the next 5

yearsyears44thth largestlargesteconomy in PPPeconomy in PPPtermsterms

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 3/43

India¶s economy growthIndia¶s economy growth ± ± 8%8%

Growth rate to exceed China byGrowth rate to exceed China by20152015

To grow larger than Britain¶sTo grow larger than Britain¶seconomy by 2022economy by 2022

To cross Japan¶s economy by 2032To cross Japan¶s economy by 2032

Be the 3Be the 3rdrd largest economy after USlargest economy after USand Chinaand China

BRIC Report 2004BRIC Report 2004 ±± Goldman SachsGoldman Sachs

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 4/43

Indian Retail ScenarioIndian Retail Scenario

Over 60% of the 700 shopping centersOver 60% of the 700 shopping centerswhich is being developed has beenwhich is being developed has been

sold or leased out already.sold or leased out already.

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 5/43

Indian Retail ScenarioIndian Retail Scenario

In 2005, the top 6 Indian cities accountedIn 2005, the top 6 Indian cities accountedfor 66% of the total organized retailingfor 66% of the total organized retailing

In 2009, the top 6 Indian cities account forIn 2009, the top 6 Indian cities account for

47% of the total organised retailing47% of the total organised retailing

Retail activities are picking up in the Tier 2 Retail activities are picking up in the Tier 2

citiescities ( Surat, Lucknow, Bhopal, Indore, Vadodara,( Surat, Lucknow, Bhopal, Indore, Vadodara,Coimbatore, Nasik, Bhubaneshwar, Varanasi, Chandigarh,Coimbatore, Nasik, Bhubaneshwar, Varanasi, Chandigarh,

Ludhiana, Amritsar,etc )Ludhiana, Amritsar,etc )

The contribution of these Tier 2 cities toThe contribution of these Tier 2 cities to

grow by20

grow by20

±±25 per cent25 per cent

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 6/43

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 7/43

Indian Retail Scenario ( 2011Indian Retail Scenario ( 2011--12)12)

700 shopping centers & multiplexes700 shopping centers & multiplexesconsisting of :consisting of :

200 Hypermarkets200 Hypermarkets

500 Departmental stores500 Departmental stores

2000 Supermarkets2000 SupermarketsOver 15000 Vanilla storesOver 15000 Vanilla stores

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 8/43

Tier 2 cities retail space explosion

Huge technological advancements

More Knowledgeable and empowered customer

New avenues of consumer expenditure evolving1984 : 7% categories consisted of 80% of totalconsumer expenditure2004 : 17% categories consists of 80% of the total

expenditure( Outsourcing domestic help, Gifting, Holidaying, Educationgaining prominence )

Indian Retail Scenario ( 2011Indian Retail Scenario ( 2011--12)12)

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 9/43

Organised Retail : INR 350 Billion

Currently 5.1% of Total Retail Sales & Growth rate @ 15-20%

2012 Projection : Organised Retail will cross INR 1000 Billion

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 10/43

Let¶s analyse a bit«..Let¶s analyse a bit«..

Why such a fuss over India ?Why such a fuss over India ?

What factors has made it possibleWhat factors has made it possible

for the world to take notice of us ?for the world to take notice of us ?How did it all happen ?How did it all happen ?

Also, let¶s debate on«..

The deterrent factors

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 11/43

Factors driving the Retail ExplosionFactors driving the Retail Explosion

Favourable demographic & psychographic changesFavourable demographic & psychographic changesof consumersof consumers

International ExposureInternational Exposure

Availability of quality retail spaceAvailability of quality retail space

Wider availability of productsWider availability of products

Brand CommunicationBrand Communication

Development of India as a global sourcing hubDevelopment of India as a global sourcing hub

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 12/43

Indian Consumer BaseIndian Consumer Base890 million below 45 years890 million below 45 years ±± Largest young population in the worldLargest young population in the world

More English speaking people than the whole of EuropeMore English speaking people than the whole of Europe

300 million middle class (Real consumers) to grow to 600 million by300 million middle class (Real consumers) to grow to 600 million by

20112011

550 million people would be below the age of 20 by the year 2015550 million people would be below the age of 20 by the year 2015

70 million earning over Rs 8 lakh annually which will grow to 140 70 million earning over Rs 8 lakh annually which will grow to 140 million by 2011million by 2011

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 13/43

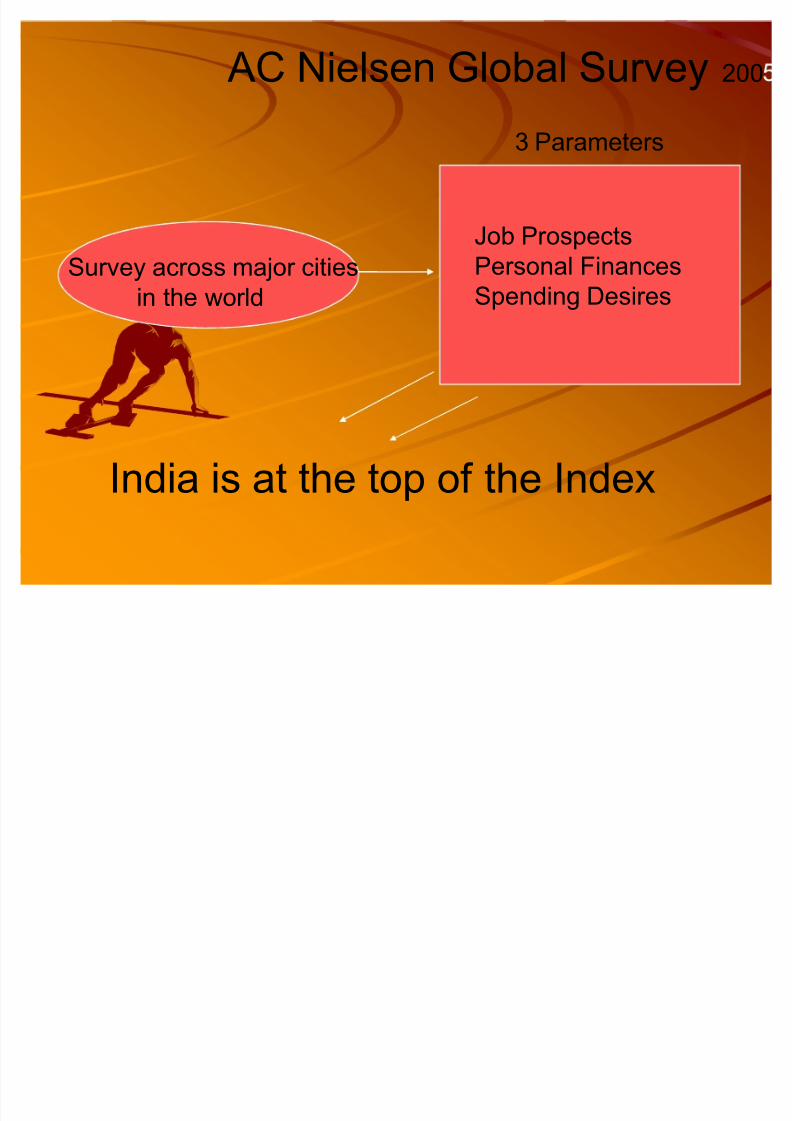

AC Nielsen Global Survey 200

Job Prospects

PersonalF

inancesSpending DesiresSurvey across major citiesin the world

India is at the top of the Index

3 Parameters

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 14/43

Indian Consumer BaseIndian Consumer BaseEmerging Consumer Segments :

Projected Demographic Shifts by 2011

± 510 Million people aged between 20 to 49

± 65% of Total population will be below the age 35

A young consumer base is growing up free from theself-denial of earlier generations.

Group Age Population

Technology Babies

Impatient Aspirers

Balance SeekersBreaking free

8 ± 19

20 ± 25

26 ± 5051 ± 60

32 M

16 M

41 M9 M

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 15/43

Consumer EvolutionConsumer Evolution -- TrendsTrends

Easier and uninhibited acceptance of luxury

Willingness to experiment

Increased effort to look and feel good

Double Income couples ± Increased propensitytowards disposability

Kids becoming aware of ext. environment & moredemanding

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 16/43

Consumer EvolutionConsumer Evolution -- TrendsTrends

Emphasis on experience and enjoyment

Expectations of return on money spendsignificantly higher

Design & quality acquiring significance

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 17/43

International ExposureInternational Exposure

33% Indians have an intent of using their33% Indians have an intent of using theirdisposal income to embark on a vacationdisposal income to embark on a vacation --

AC Neilsen surveyAC Neilsen survey

Proliferation of Cable channels, Internet hasProliferation of Cable channels, Internet hasled to a high level of awareness andled to a high level of awareness and

expectationexpectation

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 18/43

International ExposureInternational Exposure

The previous generation heard what theworld has to offer

The current generation saw what the worldhas to offer

The next generation wants what the worldhas to offer

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 19/43

Retail SpaceRetail Space95 malls are operational with 22 95 malls are operational with 22

mn sq. ft retail spacemn sq. ft retail space

500 malls would be operational500 malls would be operationalwith approx 125 mn sq. ftwith approx 125 mn sq. ft

retail spaceretail space

2005-06

2011-12

In additionKshitij planning 50 malls with 40 mn sq.ftDefunct mills in Mumbai allowed for Retail DevelopmentReliance mulling over building malls on major highwaysProvogue has floated a company for realty development

Estimation of Retail space is very speculative in nature at

the moment.

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 20/43

Availability of products / services Availability of products / services

GuessGuess Trussardi Giordano ChanelTrussardi Giordano ChanelEspiritEspirit BreguetBreguet SwatchSwatch LottoLottoMothercareMothercare VersaceVersace Hugo BossHugo Boss

Rado Marks & Spencer Tag HeuerRado Marks & Spencer Tag HeuerNext Debenhams NauticaNext Debenhams Nautica

About to enter About to enter

FCUKFCUK ZaraZara CerrutiCerrutiRocheRoche FendiFendi DKNYDKNY IkeaIkea ClarkClark

BuildBuild--aa--bearbear

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 21/43

India as a sourcing hubIndia as a sourcing hub

WalWal-- Mart GAP Tesco JC PennyMart GAP Tesco JC Penny

H&M KarstadtH&M Karstadt--Quelle Sears(K Mart )Quelle Sears(K Mart )

INR 10-20 Billion / year

INR 100-150 Billion / year3± 4 yrs

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 22/43

Bottlenecks

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 23/43

BottlenecksBottlenecksRegulatory BarriersRegulatory Barriers

Lack of skilled manpowerLack of skilled manpower

Differential Taxation systemDifferential Taxation system

Labour legislationLabour legislation

Lack of Industry statusLack of Industry status

Absence of developed supply chain and ITAbsence of developed supply chain and IT

managementmanagementStructural ImpedimentsStructural Impediments

High cost of real estateHigh cost of real estate

Varied customer preferences across regionsVaried customer preferences across regions

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 24/43

Regulatory BarriersRegulatory Barriers

Complex Taxation systemComplex Taxation system ±± Differential sales taxDifferential sales taxrates adds cost and complexity of distributionrates adds cost and complexity of distribution

Cost advantage for smaller stores through taxCost advantage for smaller stores through taxevasionevasion

Mutliple legislations limits flexibility inMutliple legislations limits flexibility in

operationsoperations

Irritant value in establishing chain operations; addsIrritant value in establishing chain operations; addsto overall coststo overall costs

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 25/43

Skilled manpower shortageSkilled manpower shortage

Lack of trained personnelLack of trained personnel

Higher trial and error in managing retail operationsHigher trial and error in managing retail operations

Increase in personnel costsIncrease in personnel costs

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 26/43

Labour LegislationLabour Legislation

Stringent labour laws governing hours of work /Stringent labour laws governing hours of work /minimum wage paymentsminimum wage payments

Multiple licenses / clearances requiredMultiple licenses / clearances required

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 27/43

Industry statusIndustry status

Restricted availability of financeRestricted availability of finance

Restricts growth and scaling upRestricts growth and scaling up

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 28/43

Integrated Supply chain / ITIntegrated Supply chain / IT

Limited product range ( segments in food / apparelLimited product range ( segments in food / apparelreserved for SSIs )reserved for SSIs )

Makes scaling up difficultMakes scaling up difficult

High cost and complexity of sourcing & planningHigh cost and complexity of sourcing & planning

Lack of value addition and increase in costs byLack of value addition and increase in costs byalmost 15%almost 15%

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 29/43

Structural ImpedimentsStructural Impediments

Lack of urbanizationLack of urbanization

Poor transportation infrastructurePoor transportation infrastructure ±± Wastage of Wastage of

almost 45% of farm producealmost 45% of farm produce

Consumer habit of buying fresh foodsConsumer habit of buying fresh foods

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 30/43

High Real estate ratesHigh Real estate rates

Difficult to find good real estate in terms of locationDifficult to find good real estate in terms of locationand sizeand size

High land cost owing to constrained supplyHigh land cost owing to constrained supply

Disorganized nature of transactionsDisorganized nature of transactions

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 31/43

Varied Customer PreferencesVaried Customer Preferences

Local consumption habitsLocal consumption habits

Need for variety leads to stocking larger no of SKUsNeed for variety leads to stocking larger no of SKUs

at a store levelat a store level

Increases complexity in sourcing and planningIncreases complexity in sourcing and planning

Increases the cost of store managementIncreases the cost of store management

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 32/43

MAJOR PLAYERS IN THE INDUSTRY

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 33/43

Prominent Retailers in IndiaProminent Retailers in India

RPG RetailRPG RetailPantaloon RetailPantaloon RetailThe Tata GroupThe Tata Group

Raheja GroupRaheja GroupLifestyle IndiaLifestyle IndiaAditya Birla Retail LimitedAditya Birla Retail LimitedReliance Retail IndiaReliance Retail India

Nilgiris¶ Nilgiris¶ SubhikshaSubhikshaTrinethraTrinethraVishal GroupVishal Group

AdaniAdani

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 34/43

Presence of Foreign PlayersPresence of Foreign Players

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 35/43

Presence of Foreign PlayersPresence of Foreign PlayersGerman giant Metro AG & South African Shoprite Holdings hasGerman giant Metro AG & South African Shoprite Holdings has

set up wholesale operationsset up wholesale operations

Carrefour has deputed Gerard Freiszmuth as CEO to exploreCarrefour has deputed Gerard Freiszmuth as CEO to exploreopportunities and oversee workopportunities and oversee work

Wal Mart has tied up with Bharti to co launch retail operationsWal Mart has tied up with Bharti to co launch retail operationsin Indiain India

Australian retailer Woolworths has announced its market entryAustralian retailer Woolworths has announced its market entry

into India. It is entering into a joint venture with the Tatainto India. It is entering into a joint venture with the TataGroup for durable retailingGroup for durable retailing

French retailer Geant is expected to start operationsFrench retailer Geant is expected to start operations

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 36/43

India is ready to leapfrog into the next stage of evolution where a large number of Indian and

international retailers would build scalablemodels with a pan India appeal.

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 37/43

Summarising>>>Summarising>>>INDIAINDIA -- A Vibrant Economy & ResplendentA Vibrant Economy & ResplendentMarketMarket

4 Largest economy in PPP terms after USA, China 4 Largest economy in PPP terms after USA, China& Japan& Japan

To be the 3 largest economy in GDP terms in To be the 3 largest economy in GDP terms innext 5 years.next 5 years.

2 fastest growing economy in the world 2 fastest growing economy in the world

.. A US $580 billion economy grew 8.2 percent in A US $580 billion economy grew 8.2 percent in

the year 03the year 03--0404

Among top 10 FDI destinations Among top 10 FDI destinations

Stable Government with 2 stage reforms in place Stable Government with 2 stage reforms in place Growing Corporate Ethics (Labour laws, Child Growing Corporate Ethics (Labour laws, Child

Labour regulations, environmental protectionLabour regulations, environmental protectionlobby, intellectual/property rights, sociallobby, intellectual/property rights, social

responsibility).responsibility).

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 38/43

Major tax reforms including implementation of Major tax reforms including implementation of VAT.VAT.

US $ 130 billion investment plans in infrastructure US $ 130 billion investment plans in infrastructurein next 5 yearsin next 5 years

2 Second most attractive developing market 2 Second most attractive developing market

5th among the 30 emerging markets for retailers 5th among the 30 emerging markets for retailers

A country with the largest young population in theA country with the largest young population in theworldworld -- over 867 million people below 45 years of over 867 million people below 45 years of

age!age!

More English speaking Indians than EuropeansMore English speaking Indians than Europeans300 million odd middle class300 million odd middle class -- the Real consumersthe Real consumers --

is catching the attention of the worldis catching the attention of the world

With over 600 million effective consumers by 2011.With over 600 million effective consumers by 2011.

India to emerge as a major consumer market of theIndia to emerge as a major consumer market of theworld by 2011.world by 2011.

Summarising>>>Summarising>>>

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 39/43

Retailing in IndiaRetailing in IndiaTotal Consumer Spend in the Year 03Total Consumer Spend in the Year 03--04 INR04 INR

930,000 crores (USD 375 billion) growing over 5%930,000 crores (USD 375 billion) growing over 5%annuallyannually

Retail sales 55% at Rs. 28,000 crore (USD 205Retail sales 55% at Rs. 28,000 crore (USD 205

billion)billion)

Organised Retail Only 3% but growing at 30%Organised Retail Only 3% but growing at 30%

Organised retail to cross Rs. 1000 billion mark byOrganised retail to cross Rs. 1000 billion mark by20122012

Rs. 200 billion investment in the pipelineRs. 200 billion investment in the pipeline

Top 6 cities account for 47% of total organizedTop 6 cities account for 47% of total organizedretailing.retailing.

Overwhelming acceptance of modern retail formats.Overwhelming acceptance of modern retail formats.

Fashion drives organized retail.Fashion drives organized retail.

Summarising>>>Summarising>>>

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 40/43

Malls in IndiaMalls in India A decade ago not a single mall A decade ago not a single mall

A year ago less than half a dozen A year ago less than half a dozen

Today 365 malls Today 365 malls

4 years from now 700 malls 4 years from now 700 malls

India Retail By 2011India Retail By 2011--1212

125 million sq ft of quality space under development125 million sq ft of quality space under development

7 major cities to account for 41 million sq ft7 major cities to account for 41 million sq ftdevelopmentdevelopment

700 malls, shopping centres and multiplexes under700 malls, shopping centres and multiplexes underconstructionconstruction

To open 200 hypermarkets, 500 large departmentTo open 200 hypermarkets, 500 large departmentstores, 2000 supermarkets and over 15,000 newstores, 2000 supermarkets and over 15,000 new

outletsoutlets

To add US $ 10 billion of business to organised retail.To add US $ 10 billion of business to organised retail.

Summarising>>>Summarising>>>

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 41/43

Retail ProspectsRetail Prospects

Clothing Clothing Footwear Footwear

Jewellery & watches Jewellery & watches Health & Beauty (including services) Health & Beauty (including services) Food & Grocery Food & Grocery

Catering Services Catering Services Consumer Electronics + mobile sets/ Consumer Electronics + mobile sets/

PeripheralsPeripherals

Books, Music & Gifts Books, Music & Gifts Home Home Entertainment Entertainment Petrol Stations Petrol Stations Rural Retailing Rural Retailing

Summarising>>>Summarising>>>

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 42/43

I ndian Retail Where it standsI ndian Retail Where it standsFive Reasons why I ndian Organized Retail is at Five Reasons why I ndian Organized Retail is at

the brink of Revolution :the brink of Revolution :

Scalable and Profitable Retail Models are well Scalable and Profitable Retail Models are well

established for most of the categoriesestablished for most of the categories

Rapid Evolution of New Rapid Evolution of New--age Young Indianage Young IndianConsumersConsumers

Retail Space is no more a constraint for growth Retail Space is no more a constraint for growth

Partnering among Brands, retailers, franchisees, Partnering among Brands, retailers, franchisees,investors and mallsinvestors and malls

India is on the radar of Global Retailers Suppliers India is on the radar of Global Retailers Suppliers

Summarising>>>Summarising>>>

8/8/2019 Indian Retail Presentation SD

http://slidepdf.com/reader/full/indian-retail-presentation-sd 43/43

Indian Retail

Tomorrow¶s ³Promised Land´