Page 1

Emerging Trends

In

India’s Steel Tubes and Pipes Industry

Project conducted in ET Intelligence Group in June / July 2013

Submitted By:

Karan Ashar

Project done under the guidance of:

Ramkrishna Kashelkar,

ET Intelligence Group

Project Report submitted to:

1. Rahul Joshi, Executive Editor, The Economic Times

2. Shaji Vikraman, Head of ET Intelligence Group

Page 2

2

TABLE OF CONTENTS

EXECUTIVE SUMMARY 3

INDUSTRY OVERVIEW 4

STRUCTURE OF THE INDUSTRY 6

PRODUCT SUMMARY 7

KEY GROWTH DRIVER 8

INTERNATIONAL DEMAND DRIVERS 9

DOMESTIC DEMAND DRIVERS 12

KEY CHALLENGES 15

INDUSTRY FINANCIALS 16

COMPANY FINANCIALS AT A GLANCE 21

A PLAYER TO WATCH FOR 23

BIBLIOGRAPHY 26

Page 3

3

EXECUTIVE SUMMARY

The last decade experienced an evolution in the Indian steel industry, with steel and iron

ore producers expanding their operations on a global scale. On the contrary, the Indian

steel pipe industry witnessed slow growth; however, with promising prospects. At

present, the Indian steel pipe industry enjoys growth through demand on a domestic and

global level, particularly from the oil & gas sector.

For investors the industry has not proven to be a value creator for last five years, rather,

in case of several leading companies the market capitalization has drastically fallen due

to various reasons. While company specific issues, such as high indebtedness, unhedged

forex exposure or promoters pledging their shares, were responsible, the industry also

suffered from growing competition amid raw material price volatility keeping the

margins under check.

Nevertheless, it’s not all gloom and doom. A large growth potential is waiting to be

exploited, with steel tubes and pipes finding robust demand from various sectors in the

domestic market like infrastructure, engineering, real estate, telecommunication, powers,

metros, ports and airports. Globally the petroleum Exploration & Production (E&P)

industry – particularly after the advent of shale gas boom in the US – is providing a

growing demand for the industry.

This is creating a scenario where leaders of the past are falling behind weighed down by

their own set of problems, and mid-sized players are fast emerging as the new leaders of

the industry. For example, the leading players Welspun Corp and Jindal Saw are seen

under pressure due to high debt and pledged shares etc. It then follows that the investors

should focus on these players who are showing promise for the future growth rather than

getting discouraged by the dispirited performance of the leaders.

Page 4

4

INDUSTRY OVERVIEW

India has become a leading country in the world for manufacturing steel pipes mainly due

to its lower cost, high quality and geographical advantages. Still, if compared to the huge

steel industry, the size of domestic steel tubes and pipes industry is a relatively small.

Almost all the major steel manufactures such as SAIL, Tata Steel, Jindal Stainless, Essar

Steel etc. have presence in the pipe manufacturing as a way of forward integration.

However, for their main line of business this forms a minor part. There exists a parallel

industry of focused players who act as converters. The key challenge they face is the high

dependency on purchased raw material, which is as high as 70%-80% of revenues for

some.

The steel tubes and pipes industry caters primarily to the needs to flowing materials to

desired distance under pressure and force. What material needs to be flowed and under

what pressure, temperature etc determines the complexity of the pipes. Every industrial

complex or manufacturing unit usually needs a large amount of piping and plumbing to

work with various types of fluids including water. Of course, here the steel pipes compete

with pipes made from various other materials ranging from cement to plastics depending

on the required usage.

Infrastructure sector also generates a chunk of demand for the industry owing to the fact

that a hollow tube is generally more efficient than a rod in constructions. Thus

construction of dams, power projects, railways and bridges etc. typically consume a huge

quantity of pipes. Polished steel pipes are also being increasingly used to add glitz to the

interiors of malls as well as hotels.

High level of tensile strength and corrosion resistance has made the steel pipes a

preferred option in the oil & gas industry – particularly in the exploration and production

phase. Sensing the opportunity in this sector, Indian companies have been proactive in

obtaining global accreditations and certifications, enabling them to supply to most of the

world’s largest petroleum companies.

Page 5

5

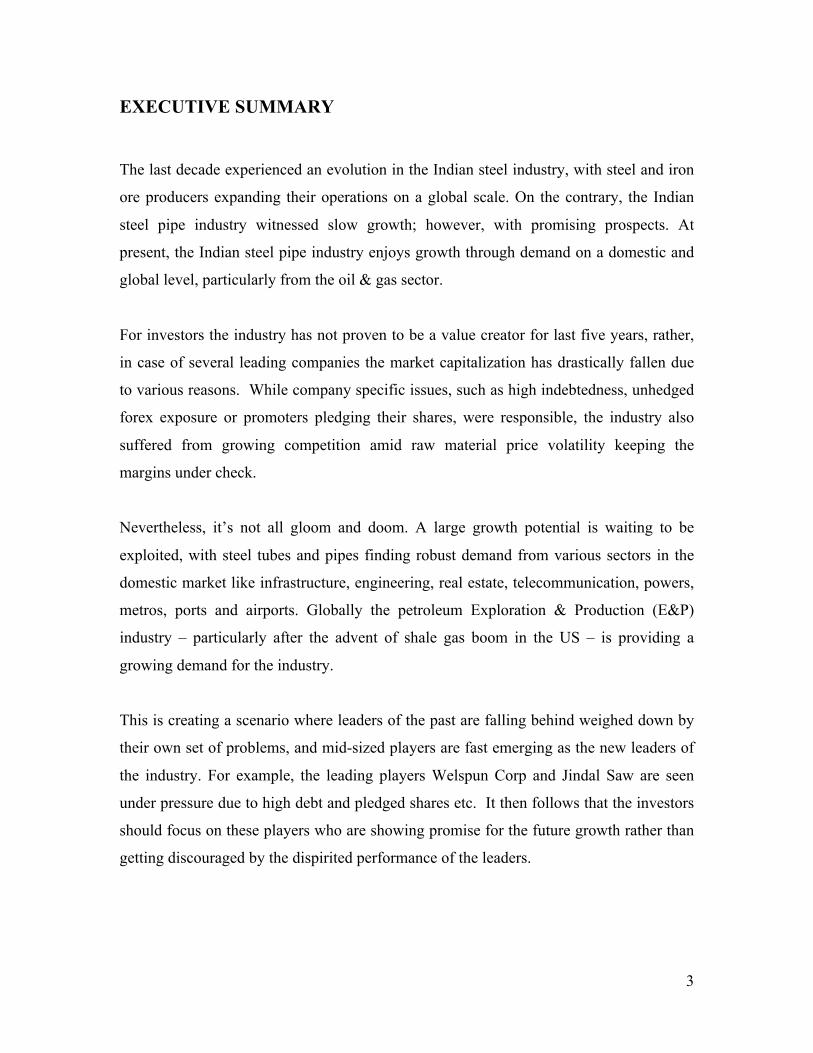

Nevertheless, the steel pipe making has largely remained an unorganized and scattered

industry with just an estimated 35% in the organized sector consisting of 17 listed

companies. These players together had a turnover of Rs 24,100 crore for FY13, which

means the total industry size is around Rs 70,000 crore. These players put together have

witnessed a slow growth of less than 1% annualized in the last 5 years; however, the

players have been expanding.

(Source: Capitaline)

The value of investments has almost doubled to Rs.13,150 crore in a five year period

ended March 2012, as measured by the increase in gross block of these players. Further

investments are taking place as the industry expands. The aggregate market capitalization

of these players stands around Rs 7700 crore.

Experts believe that once the world’s economic problems come to an end and stability

returns, the Indian pipe industry will shoot into a high growth trajectory.

6712.12 8124.89

10129.04 11142.65 13153.77

FY2008 FY2009 FY2010 FY2011 FY2012

Industry Aggregate Gross Block in Rs. Crore (2008-12)

Aggregate Gross Block

Page 6

6

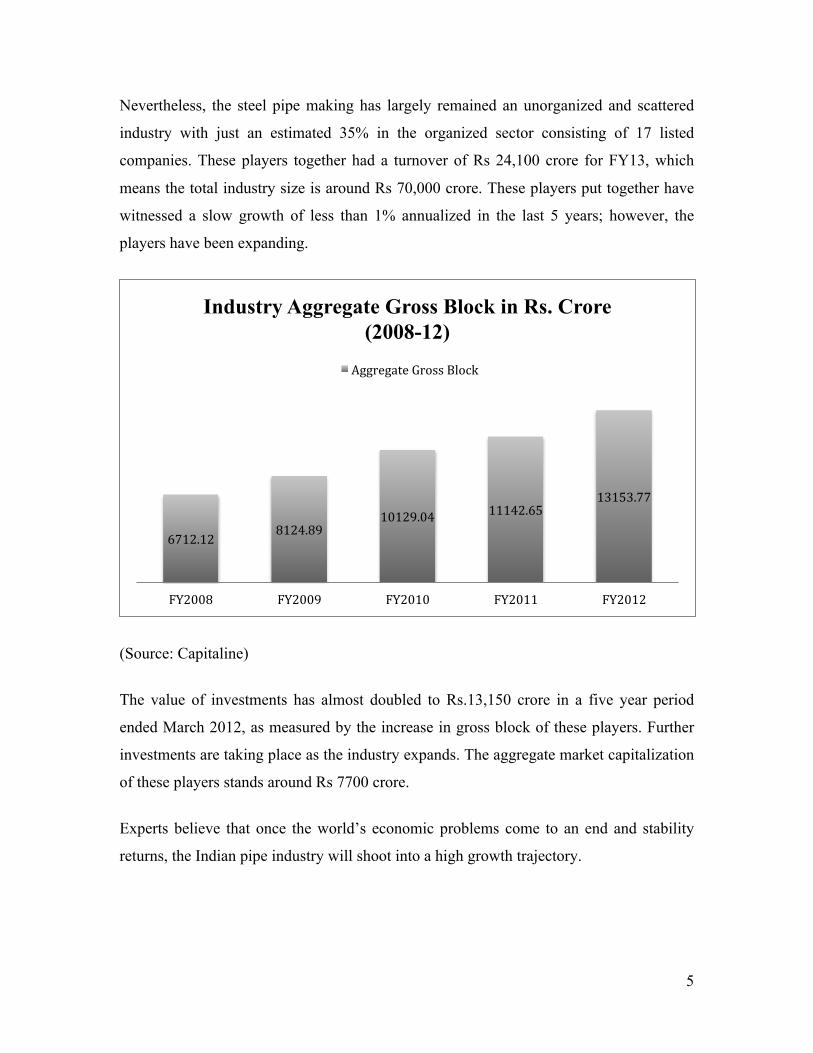

STRUCTURE OF THE INDUSTRY

Steel Tubes & Pipes Industry

Ductile Iron Seamless Welded

Submerged Arc Welded (SAW) Potable Water

Oil & Gas,

Automotive and Power

Longitudinal Submerged Arc

Welded (LSAW)

Helically Submerged Arc

Welded (HSAW)

Electric Resistance

Welded (ERW)

ERW Precision (DOM)

ERW (Structural/

Commercial)

Automotive, White goods

Oil & Gas, Water and sewage,

Modern infrastructure

(airports, metros, malls etc.)

Oil & Gas, Water and sewage Oil & Gas

Page 7

7

PRODUCT SUMMARY

Pipe

Features

Ductile Iron

Seamless

LSAW

HSAW

ERW Precision

(DOM)

ERW (Structural/

Commercial)

Size 3” to 40”

diameter

0.5” to 14”

diameter

16” to 50”

diameter

18” to 120”

diameter

0.5” to 4.5”

diameter

0.5” to 22”

diameter

Key raw

material

Pig iron/ Cast

iron/ Sponge

iron

Steel billets Steel plates HR Coils HR Coils HR Coils

Manufacturing

process

Pig iron in blast

furnace

Piercing

ingots/billets of

steel at high

temperatures

Longitudinally

submerged arc

welding

of steel plates

Spirally

welding

HR coils

Converging HR

coils welded using

high frequency

induction welding

Hot rolled steel

coils using

electrical

resistance welding

process

Application Potable water

transportation

Oil & Gas

Exploration,

Engineering

Oil & Gas

Transportation

Oil & Gas/

Water

Transportat

ion

Automotive, White

goods

Oil & Gas (city gas

distribution), Water

and sewage,

Modern

infrastructure

Key players Electrosteel,

Jindal SAW

Maharashtra

Seamless,

Jindal SAW,

Remi Metals

Jindal Saw,

Welspun Corp,

Man

Industries

PSL, Jindal

Saw,

Welspun

Corp, Man

Industries

Tata Steel,

Innoventive

APL Apollo, Surya

Roshni,

Maharashtra

Seamless

Page 8

8

KEY GROWTH DRIVERS

The steel tubes and pipes find application in a variety of industries including Oil & Gas

exploration, production and transportation as well as Infrastructure projects such as

railways, ports and airports, water projects etc.

The global oil & gas industry has proven to be a major demand driver for Indian steel

tubes and pipes industry — particularly the seamless variety in exploration & production.

With global gas demand expected to rise by 576 million cubic meters from 2012 to 2017,

and emphasis on usage of natural gas, the surge in demand for pipes harbors huge

prospects for the Indian pipe industry to penetrate into the international market and at the

same time maintain interest in a developing domestic market. With energy demand

expected to rise by 60.71% in India by 2025, the domestic market has the potential to

support the growth of the industry.

Oil and gas along with coal continue to be the most widely used fuels, with their global

consumption expected comprise 80% of the energy consumption in 2040. Asia,

responsible for 20% of the global gas consumption and 30% of global pipe demand, is

expected to provide a suitable market for Indian steel pipe makers to target. However, a

global recession has hindered the prospects for growth.

Within India also there exist a number of growth drivers for the steel pipes industry. By

2017, India will have a natural gas pipeline grid stretching 30,000 Km connecting

consumption centers to fuel sources. The 11th Five Year Plan (2007-12) announced by the

government had introduced the decision of investing $83 billion in the water and

irrigation system, thereby deriving demand from water projects.

Being, a developing country, India has laid emphasis on infrastructure, ranging from

malls to airports. Similarly, sectors such as real estate, automobiles and

telecommunications among others hold potential to drive the demand for the pipe

industry.

Page 9

9

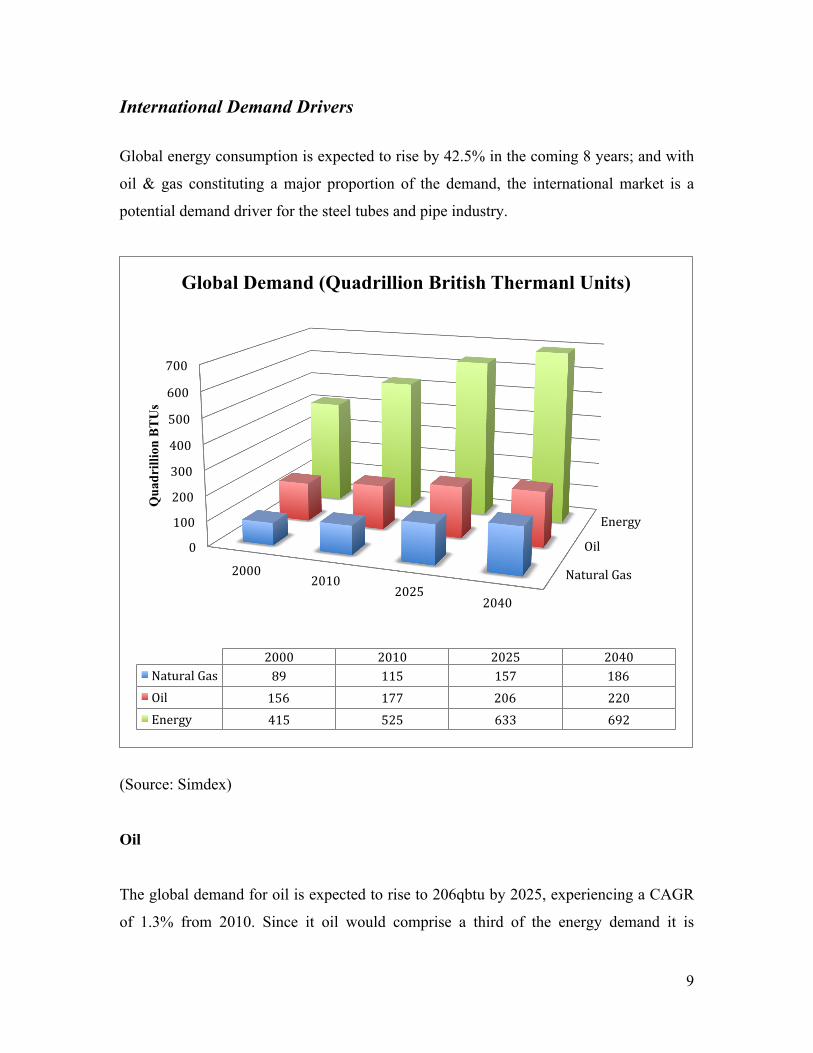

International Demand Drivers

Global energy consumption is expected to rise by 42.5% in the coming 8 years; and with

oil & gas constituting a major proportion of the demand, the international market is a

potential demand driver for the steel tubes and pipe industry.

(Source: Simdex)

Oil

The global demand for oil is expected to rise to 206qbtu by 2025, experiencing a CAGR

of 1.3% from 2010. Since it oil would comprise a third of the energy demand it is

Natural Gas

Oil

Energy

0

100

200

300

400

500

600

700

2000 2010

2025 2040

Qua

drill

ion

BT

Us

2000 2010 2025 2040 Natural Gas 89 115 157 186 Oil 156 177 206 220 Energy 415 525 633 692

Global Demand (Quadrillion British Thermanl Units)

Page 10

10

important for the Indian steel pipe manufacturers to take advantage of the opportunity

presented on the international market. Besides, 2012 recorded a global oil supply capacity

of 91.9 mb/d; this figure is expected to rise by 2016 to 100.6 mb/d, providing an impetus

for the industry to meet the increasing necessity for transportation of oil.

Natural Gas

With oil consumption outstripping oil production there raises a need for an alternative

source of energy, with natural gas being a viable option since it is cheaper than oil.

Besides, it is the cleanest fossil fuel and hence will play an important part in the coming

years. The consumption of fossil fuel in 2008 reached 111 trillion cubic feet, and the

figure is expected to rise to 169 trillion cubic feet, and increase of 52.3%. With the global

demand for natural gas predicted to rise at CAGR of 2.1% from 2010-25, the steel pipe

manufacturers will aim to draw demand from its consumption.

Future pipeline projects: Oil and Gas Transportation and Exploration

(Source: Simdex) [Figures in number of projects (%)]

North America, 192 (27%)

Latin America, 56 (8%)

Europe , 101 (14%)

Africa, 49 (7%)

Middle East , 111 (16%)

Asia, 142 (20%)

Australia, 59 (8%)

Page 11

11

27% of the future pipeline projects are directed towards North America, whereas Asia

holds the second largest share of 142 projects. Since several countries in Asia are in the

developing stage, primarily India and China, it is likely that the along with a demand in

energy, mainly oil and natural gas, there will be an increase in the figure for number of

pipeline projects. Besides demand for pipes for transportation and exploration in the

Middle East, Asia and North America harbor great potential to drive growth of the steel

pipe industry.

Future pipeline projects (Km): Oil and Gas Transportation and Exploration

(Source: Simdex)

Around a third of the total length of pipeline projects is directed towards Asia, primarily

due to developing countries such as India and China. Despite having fewer projects than

North America, the average length of each pipeline project for Asia is 669 Km as

compared to 384 Km for North America. Middle East contributes to 13% of the total

length, where as Europe holds a similar share with 44784 Km of pipeline projects.

0

20000

40000

60000

80000

100000

North America

Latin America

Europe Africa Middle East Asia Australia

Length of Pipeline Projects

Page 12

12

Domestic Demand Drivers

India is poised in the top 3 steel tube/pipe manufacturing hub after Japan and Europe with

production estimated to be 10 million tonnes. Being a developing country, India holds

several sectors that can generate demand for steel tube and pipes.

Power

The 12th 5 year plan (2012-2017) announced by the government added 1,00,000 MW

power capacity with proposed 17426 ckm transmission lines in central, state and private

sector for 2012-13. The power capacity is almost doubled as compared to the estimated

installation of 52,000 MW during the 11th Five Year plan. Hence the power sector will be

a major force in propelling the demand for steel tubes and pipes.

Oil & Gas

India is ranked as the world’s fifth largest energy consumer, with 30% of the total energy

consumption accountable to oil. India has 5.8 billion barrels of proven oil reserves with

an average oil production of 815,000 barrels per day (B/D). With oil consumption

expected to rise to 4 million barrels B/D by 2015, there will be an increased demand on

steel pipes for transportation. Besides, 78% of the country’s sedimentary area is yet to be

explored; hence, stressing on the importance of the industry to provide tubes and pipes

for exploration.

Gas consumption in India is predicted to grow at a CAGR of 7.7% due to slower gas

supplies. However, the total gas demand for the previous year stood at 253 million metric

standard cubic feet per day (mmscmd) and is expected to touch 550 mmscmd by 2019-

20. As a result the increased consumption for gas will help trigger the demand for steel

pipe manufacturers.

Page 13

13

Ports

Steel tubes and pipes find major application in ports. The Indian coastline extends 7500

Km long and harbors 13 major ports and 200 minor ports. With the need for

development, the Indian government has announced an investment of US$110 billion for

improving its ports and shipbuilding industry by 2020.

Airports

With 136 airports, India presents itself as the 9th largest aviation market. According to the

12th 5-year plan Rs. 547.43 billion was injected into the aviation sector, which is expected

to grow at CAGR of 16% in the years 2010-13. The government has also targeted to

invest US$30 billion in the next decade with the intention to modernize Indian airports.

Besides, 16 Greenfield airports have been approved, of which 12 of them are in their

developing stage.

Water projects

Covering significant sectors such as water transportation, irrigation and drainage, water

projects are beneficial to the steel pipe industry. Transportation of potable water across

several homes in the country will draw demand for tubes and pipes. Besides, a proposal

to allocate Rs 3,000 million to Vidarbha Intensified Irrigation Development Programme

under Rashtriya Krishi Vikas Yojana (RKVY) will provide for increased irrigation and

higher demand for steel pipes/tubes.

Shale Gas

Due to its recent discovery, shale gas has not immediately found its application in India.

However, India boasts 537 trillion cubic feet (tcf) of shale gas in 28 sedimentary basins.

Of this figure around 260 tcf is estimated to be recoverable. Hence, the importance for

exploration, production and transportation of shale gas has fostered the need for steel

Page 14

14

pipes and tubes. The capability of Indian shale gas reserves to extract enough gas to

support the nation for 200 years has generated significance and hence the propelled

demand in the steel pipes industry.

Automobile

An important component in the construction of cars, steel tubes and pipes are likely to

expect demand due to the growth of the automotive industry. The Center for Monitoring

Indian Economy predicted a rise in overall automobile production by a healthy 9.6% in

2012-13 wherein commercial vehicle production is expected to expand by 8.5%. Where

two wheelers production is expected to grow at 9.7%, multi utility vehicle is expected to

experience a rampant 19.7% rise.

City Gas Distribution

The city gas distribution has a network of 26,500 Km spread across India significantly

over western and northern parts of the country. Though CGD comprises of approximately

8-9% of the total gas consumption in India, pipe manufactures can seek respite in the fact

that improvements in the pipeline infrastructure are required on south and east India.

According to the 12th 5-year plan, the CGD sector plans to achieve a CAGR of 28.8%

from 13 mmscmd to 46 mmscmd, thereby triggering demand for the industry.

Besides, several sectors play an important part in propelling the demand for steel tubes

and pipes. Real estate, which grew promisingly in the past few years, generated sales for

the industry. However, with real estate sector in decline mode, it seems less likely to play

major role in the future. Alternatively, transportation of potable water and sewage

treatment require ductile iron pipes, where as bridges and bus body parts will also

contribute to the growth of the industry. Additionally, metros and construction of bridges

will increase the need for steel tubes and pipes.

Page 15

15

KEY CHALLENGES

Although the industry’s growth prospects appear lucrative, most of the domestic players

have been under-performing for last several years. This underlines the fact that the

industry is facing a bunch of uphill tasks.

1. Fluctuations in raw material prices: Since the pipe manufacturers are dependent

on steel as the key input, volatility in steel and iron price hurts them directly.

2. Weak Global Economic Growth: Economic growth and Development tends to

be directly correlated with increased energy consumption. The slowdown and

uncertainties in world’s economic growth has resulted in slowing down

investments in industrial capacities, which is having a negative impact on the

overall demand for pipe industry.

3. Growing Competition: The pipe-making industry is facing growing competition

on domestic as well as international front. Within India most of the players have

aggressively expanded pipe-making capacities in last five years — the gross block

of the listed players has doubled between FY08 and FY12 — with a few players

such as APL Apollo still in expansion mode. Globally, countries like China and

Turkey have seen a growing number of pipe-making companies competing with

Indian players for the international projects.

4. Anti-dumping duty in the US: With a view to protect the domestic steel pipe

makers US has imposed an anti-dumping duty on Indian steel pipes since 2011.

This erodes the competitiveness of Indian products in the US, which is seeing a

burst in demand thanks to the shale gas boom.

5. Weakening Financials: The domestic industry has also become a victim of its

own aggressive growth, as the current status of financial health appears weak. The

industry has seen slowing sales growth and dwindling margins with key return

ratios such as RoCE and RoE falling consistently.

Page 16

16

INDUSTRY FINANCIALS

The industry’s performance of last five years has not been exciting with leading players

facing challenges on revenue growth. As the graph below shows industry leaders such as

Welspun Corp and Jindal Saw had just 10% higher revenues in FY13 as compared to

FY09, while Maharashtra Seamless, Man Industries and PSL are selling less than five

years back.

6109.68 6905.83 6270.4 5769.71 6632.17

5161.06

6974.81

4345.26 5190.72 5612.86

3487.96

2761.52

2578.67 2346.94 2201.32

2183.51

1691.22

1761.27 2291.69 1722.01

4528.3 4081.73

4664.09 5784.74 5649.5

FY2009 FY2010 F2011 FY2012 FY2013

Aggregate Gross Sales in Rs. Crore (2009-13)

Others (Ratnamani, APL Apollo, Man Industry etc.)

Mah. Seamless

PSL

Jindal Saw

Welspun Corp

Page 17

17

On this backdrop, mid-sized firms like APL Apollo and Innoventive Industries have done

exceedingly well with their revenues more than doubling in last five years.

The industry’s operating profit margins have also been under pressure for last four years

after peaking in FY10. This has also impacted the industry’s ability to generate profits.

The aggregate operating profit of all the listed players in FY13 was barely crossing the

profit levels five years back.

Again in this case, the large sized players Welspun Corp and Jindal Saw have suffered

the biggest margin erosion, while Ratnamani Metals, Man Industries and PSL have

witnessed healthy improvement in margins in this period. For FY13 Ratnamani Metals

enjoyed the best operating profit margins of 21.3% as against APL Apollo that had 8%

PBDIT margin.

2758.24

4016.22 3510.61

2939.45 2788.03

13.3

17.8 16.8

13 11.7

0

2

4

6

8

10

12

14

16

18

20

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY2009 FY2010 FY2011 FY2012 FY2013

Aggregate Operating Profit in Rs. Crore (2009-13)

Operating ProTit Operating ProTit Margin

Page 18

18

The industry has seen overall leverage coming down steadily in last five years. However,

a weakness in overall operating profit margins, coupled with rising interest rates has

resulted in industry’s interest coverage ratio deteriorating to a very low level.

When it comes to the leverage, Maharashtra Seamless is the best placed presently with a

debt-equity ratio of 0.02. Naturally, it is also best placed on the interest coverage ratio

with operating profits sufficient to cover 39.2 times its interest commitment.

On the other side of the spectrum, PSL is carrying the biggest chunk of debt compared to

its equity, with a D/E ratio of 2.9. At 0.9, its interest coverage ratio is one of the lowest

in the industry.

2 1.4 0.6 0.8

0.7

4.2

6.4

5.1

3.5

2.4

FY2009 FY2010 FY2011 FY2012 FY2013

Leverage Ratios (2009-13)

D/E Ratio Interest Covergae Ratio

Page 19

19

On an aggregate level, the return ratios for the industry have been trending downwards

after peaking out in FY10. The industry’s Return on Capital Employed (RoCE) has

dwindled to 12.6% in FY13 from 23.5% of FY10. This is both on account of a slowdown

in revenue growth and margins on one hand and growing investment in the industry on

the other. This has proved to be one key factor in destroying investor value.

In a likewise manner the Return on Equity (RoE) — a matrix that equity investors need to

watch out closely — has dropped to an abysmally low level in FY13.

At the end of FY13, Ratnamani recorded the highest RoCE at 43.7%, whereas Mah.

Seamless slumped to 8.4%. As for RoE, Ratnamani was again the standout performer

with a ratio of 29.6%. With respect to the bottom end, Innoventive experienced a poor

RoE of 2.9%.

20.6%

23.5%

16.3%

11.6% 12.6%

8.7%

14.2%

11.4% 6.9%

2.9%

FY2009 FY2010 FY2011 FY2012 FY2013

Return Ratios (2009-13)

RoCE RoE

Page 20

20

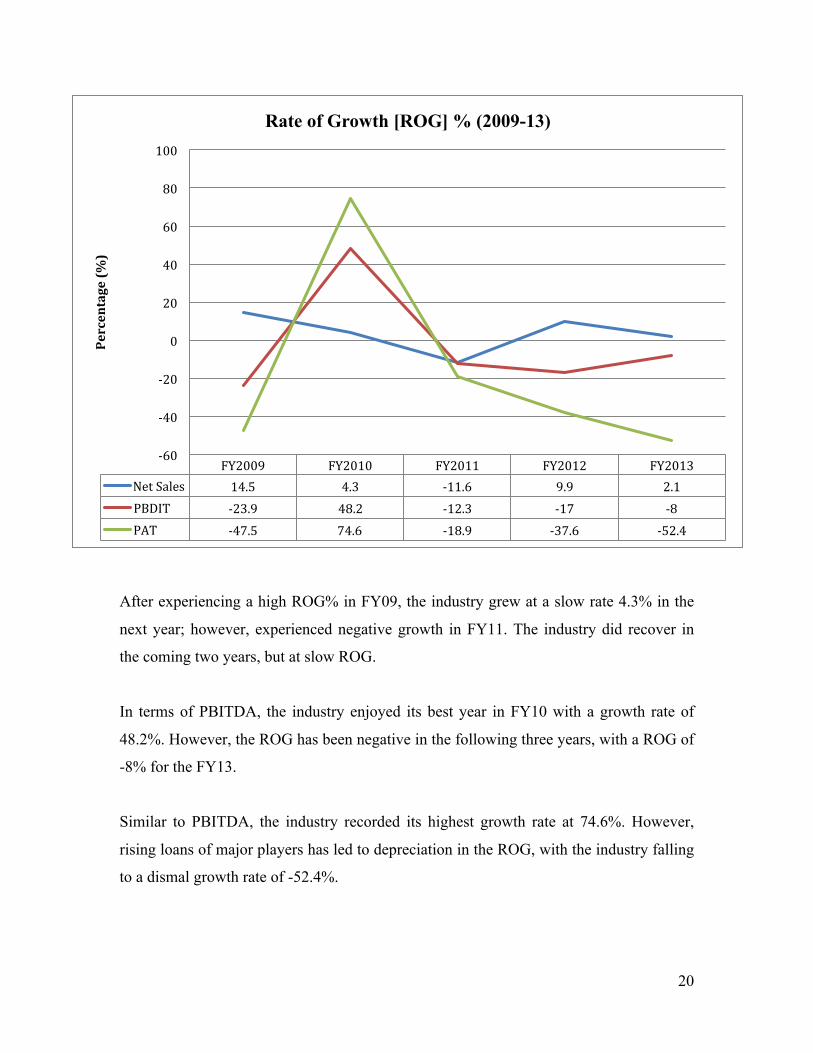

After experiencing a high ROG% in FY09, the industry grew at a slow rate 4.3% in the

next year; however, experienced negative growth in FY11. The industry did recover in

the coming two years, but at slow ROG.

In terms of PBITDA, the industry enjoyed its best year in FY10 with a growth rate of

48.2%. However, the ROG has been negative in the following three years, with a ROG of

-8% for the FY13.

Similar to PBITDA, the industry recorded its highest growth rate at 74.6%. However,

rising loans of major players has led to depreciation in the ROG, with the industry falling

to a dismal growth rate of -52.4%.

FY2009 FY2010 FY2011 FY2012 FY2013 Net Sales 14.5 4.3 -‐11.6 9.9 2.1 PBDIT -‐23.9 48.2 -‐12.3 -‐17 -‐8 PAT -‐47.5 74.6 -‐18.9 -‐37.6 -‐52.4

-‐60

-‐40

-‐20

0

20

40

60

80

100

Percentage (%

)

Rate of Growth [ROG] % (2009-13)

Page 21

21

COMPANY FINANCIALS AT A GLANCE

Company Financials

Welspun Corp

Jindal Saw

PSL

Mah. Seamless

APL Apollo

Man Inds.

Ratnamani Metals

Innoventive Ind.

Remi

Metals Guj.

Zenith Birla

Networth (Rs. Cr.)

3626.1

3728.6

949.5

2848.1

334.8

630.7

597.3

462.2

-182.1

255.7

Networth – 3 Year

CAGR (%)

9.8

1.8

4.2

22.6

19.5

10.7

17.9

87.3

N/A

11.4

Gross Block (Rs. Cr.)

3174.5

2572.8

1376.4

539.9

115.1

590.8

529.3

336.0

428.8

125.4

Gross Block – 3 Year

CAGR (%)

13.8

24.7

25.9

33.3

47.0

1.5

7.8

47.9

8.9

4.7

Net Sales (Rs. Cr.)

6632.2

5612.9

2134.3

1722.0

1609.1

1408.8

1201.1

636.2

353.0

273.2

Net Sales – 3 Year

CAGR (%)

0.0

-6.1

-8.2

2.6

61.9

-2.6

12.1

17.6

-1.7

-17.1

Net Profit (Rs. Cr.)

53.1

193.4

-156.0

153.3

34.7

100.7

136.0

56.5

-93.3

-44.7

Net Profit – 3 Year

CAGR (%)

-53.9

-35.6

N/A

-18.6

26.2

14.5

18.6

27.3

N/A

N/A

OPM (%)

9.3

10.2

14.8

14.0

5.9

16.0

21.3

26.7

-6.4

-6.0

Market Cap (Rs. Cr.)

1132.0

1585.4

125.4

1409.4

352.0

596.7

668.2

430.6

11.9

13.1

P/E Ratio

13.3

5.7

0.0

9.2

10.1

4.3

4.9

7.6

0.0

0.0

P/BV Ratio

0.3

0.4

0.2

0.6

1.0

0.8

1.0

0.9

-0.1

0.1

D/E Ratio

0.7

0.9

2.9

0.0

1.1

0.8

0.3

0.5

N/A

0.8

Current Ratio

1.2

2.6

0.9

6.7

5.1

1.9

2.1

1.5

0.9

2.1

Page 22

22

Company Financials

Welspun Corp

Jindal Saw

PSL

Mah. Seamless

APL Apollo

Man Inds.

Ratnamani Metals

Innoventive Ind.

Remi Metals Guj.

Zenith Birla

RoCE (%)

10.8

9.0

14.9

8.4

20.1

35.6

43.7

21.3

N/A

N/A

RoE (%)

4.7

10.3

5.9

6.8

4.2

7.5

27.6

2.9

N/A

N/A

Promoters Holding

(%)

34.9

46.0

39.4

55.7

47.3

51.6

59.9

45.4

87.3

7.6

Institutional Holding

(%)

20.6

29.9

13.0

25.2

9.7

9.5

13.2

24.3

0.1

3.6

Dividend (%)

10.0

50.0

0.0

120.0

50.0

40.0

200.0

10.0

0.0

0.0

Page 23

23

A PLAYER TO WATCH FOR

APL Apollo

With major companies of the industry recording negative or slow growth over the past 5

years, APL Apollo has displayed positive margins as compared to its peers. With 44%

revenue growth in FY13 and a CAGR of 49% over FY08-13, APL Apollo has posted

robust and consistent growth, highest amongst peers. At a production capacity of 600,000

TPA, APL enjoys 7% of the domestic market share for ERW pipes, gaining share from

the unorganized sector through its product superiority, reach and strategic expansion.

Valuation

APL Apollo is currently trading at a price to earnings multiple (P/E) of 5.5 as compared

to an average multiple of 2.7 of its peers. Similarly, its price to book value ratio (P/BV) is

0.55 below in line with an average value of 0.57 of its peers. Considering the growth

prospects, healthy balance sheet and attractive return ratios the company is likely to

emerge a value creator over the next 3 years

Unorganized Sector 60%

APL Apollo 7%

Other Organized Sector 33%

ERW Market Share

Page 24

24

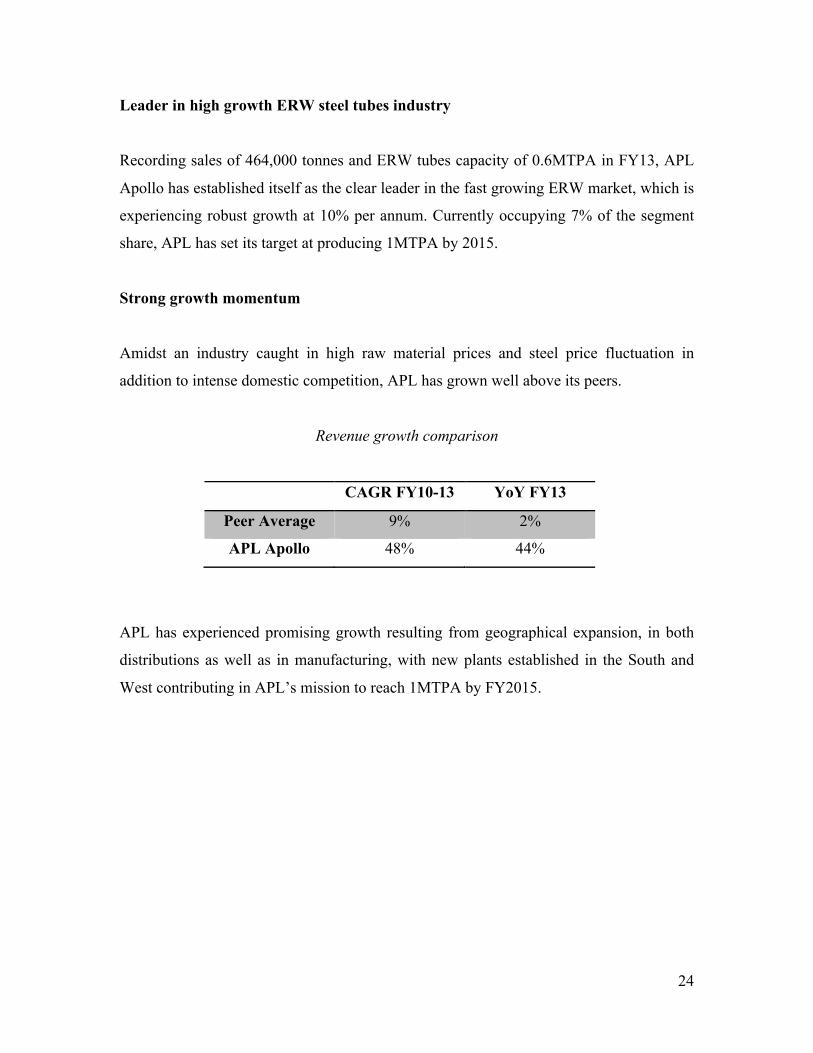

Leader in high growth ERW steel tubes industry

Recording sales of 464,000 tonnes and ERW tubes capacity of 0.6MTPA in FY13, APL

Apollo has established itself as the clear leader in the fast growing ERW market, which is

experiencing robust growth at 10% per annum. Currently occupying 7% of the segment

share, APL has set its target at producing 1MTPA by 2015.

Strong growth momentum

Amidst an industry caught in high raw material prices and steel price fluctuation in

addition to intense domestic competition, APL has grown well above its peers.

Revenue growth comparison

CAGR FY10-13 YoY FY13

Peer Average 9% 2%

APL Apollo 48% 44%

APL has experienced promising growth resulting from geographical expansion, in both

distributions as well as in manufacturing, with new plants established in the South and

West contributing in APL’s mission to reach 1MTPA by FY2015.

Page 25

25

Financial summary (Rs. Crore)

Year

Financials

FY2010 FY2011 FY2012 FY2013

Revenues 618.00 905.20 1392.30 2008.30

EBITDA 57.10 89.70 115.10 159.50

PAT 29.80 43.10 49.10 68.60

EPS 14.7 21.2 23.0 30.7

EBITDA margin 9.2% 9.9% 8.3% 7.9%

Net margin 4.8% 4.8% 3.5% 3.4%

RoE 16.7% 20.2% 18.3% 20.6%

RoCE 15.4% 20.3% 19.7% 21.2%

D/E 0.8 1.0 1.0 1.2

P/E 7.6 6.2 7.7 5.5

EV/EBITDA 6.2 5.4 5.8 4.9

Dividend payout 13.6% 9.4% 8.7% 16.3%

Page 26

26

BIBLIOGRAPHY

Following Sources and References were extensively used in preparation of the report:

1) Capitaline Corporate Database for all the Financial Numbers

2) Annual Reports of all the leading companies in the Steel Pipe making industry

such as Welspun Corp, Jindal SAW, Maharashtra Seamless, PSL Limited, APL

Apollo etc.

3) Annual Reports of leading Steel manufacturing companies such as Tata Steel,

Essar Steel, JSW Steel, Jindal Stainless

4) Presentations and Concall Transcripts of the companies, wherever available

5) Historical references from websites of Economic Times, Mint, Business Standard

6) Research Reports from various brokerage houses on the industry and players

7) SIMDEX, which is a leading provider of worldwide pipeline projects and metal

tube manufacturers

8) www.etintelligence.com

9) Websites of Bombay Stock Exchange (BSE) and National Stock Exchange (NSE)

Contact Details:

Name: Karan Ashar

Email ID: [email protected]

Phone No.: 9920043665