44

INDONESIA PROPERTY MARKET OUTLOOK Pattaya, Thailand October 26, 2012

INDONESIA PROPERTY MARKET

OUTLOOK

Pattaya, Thailand October 26, 2012

PRESENTATION AGENDA

MACRO ECONOMIC INDICATORS

PROPERTY MARKET SNAPSHOT

MAJOR INSTRUCTIONS

• CBD Office • Retail Market • Condominium • Industrial Estate

• First Media • Bank Mandiri • Indosat

MACROECONOMIC INDICATORS

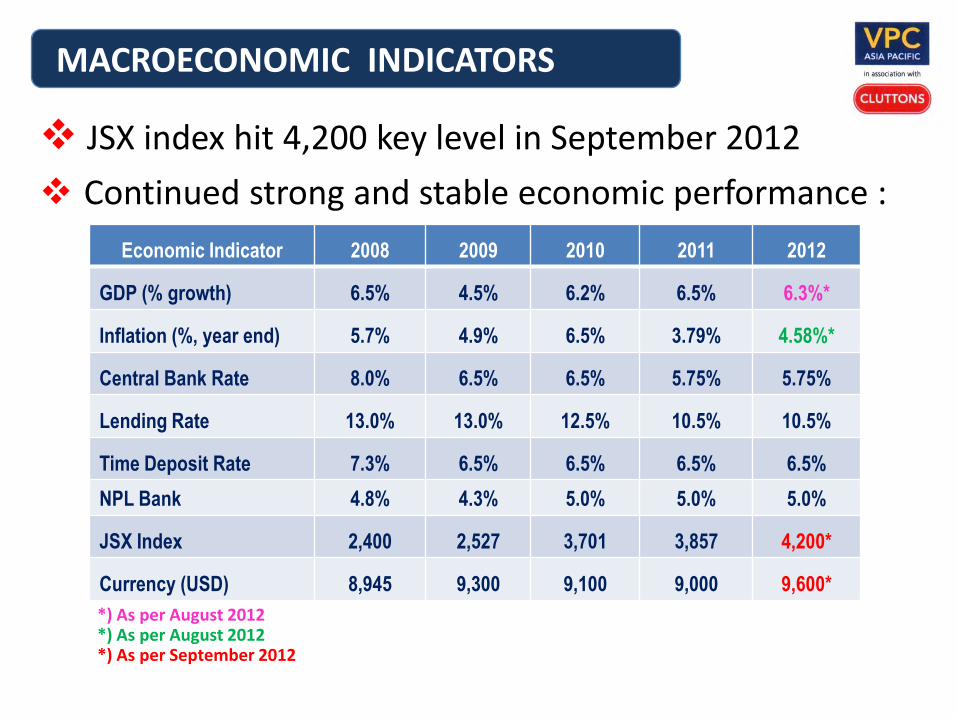

Economic Indicator 2008 2009 2010 2011 2012

GDP (% growth) 6.5% 4.5% 6.2% 6.5% 6.3%*

Inflation (%, year end) 5.7% 4.9% 6.5% 3.79% 4.58%*

Central Bank Rate 8.0% 6.5% 6.5% 5.75% 5.75%

Lending Rate 13.0% 13.0% 12.5% 10.5% 10.5%

Time Deposit Rate 7.3% 6.5% 6.5% 6.5% 6.5%

NPL Bank 4.8% 4.3% 5.0% 5.0% 5.0%

JSX Index 2,400 2,527 3,701 3,857 4,200*

Currency (USD) 8,945 9,300 9,100 9,000 9,600*

*) As per August 2012 *) As per August 2012 *) As per September 2012

JSX index hit 4,200 key level in September 2012

Continued strong and stable economic performance :

MACROECONOMIC INDICATORS

PROPERTY MARKET SNAPSHOT

PROPERTY MARKET SNAPSHOT CBD OFFICE

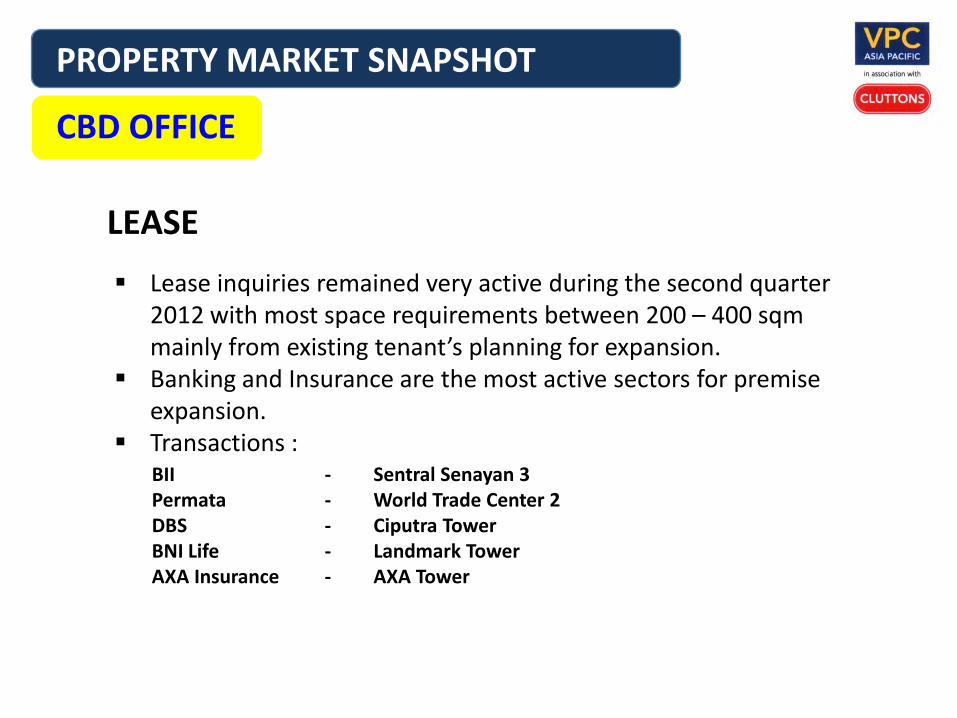

Lease inquiries remained very active during the second quarter 2012 with most space requirements between 200 – 400 sqm mainly from existing tenant’s planning for expansion.

Banking and Insurance are the most active sectors for premise expansion.

Transactions :

LEASE

BII - Sentral Senayan 3 Permata - World Trade Center 2 DBS - Ciputra Tower BNI Life - Landmark Tower AXA Insurance - AXA Tower

PROPERTY MARKET SNAPSHOT CBD OFFICE

PROPERTY MARKET SNAPSHOT CBD OFFICE

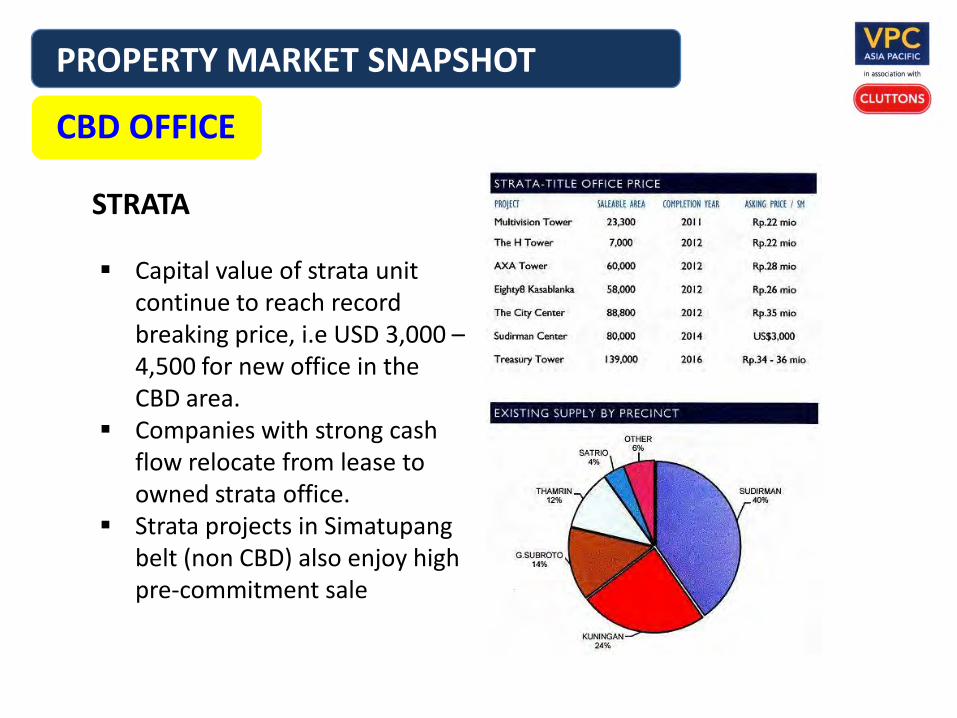

Capital value of strata unit continue to reach record breaking price, i.e USD 3,000 – 4,500 for new office in the CBD area.

Companies with strong cash flow relocate from lease to owned strata office.

Strata projects in Simatupang belt (non CBD) also enjoy high pre-commitment sale

STRATA

PROPERTY MARKET SNAPSHOT CBD OFFICE

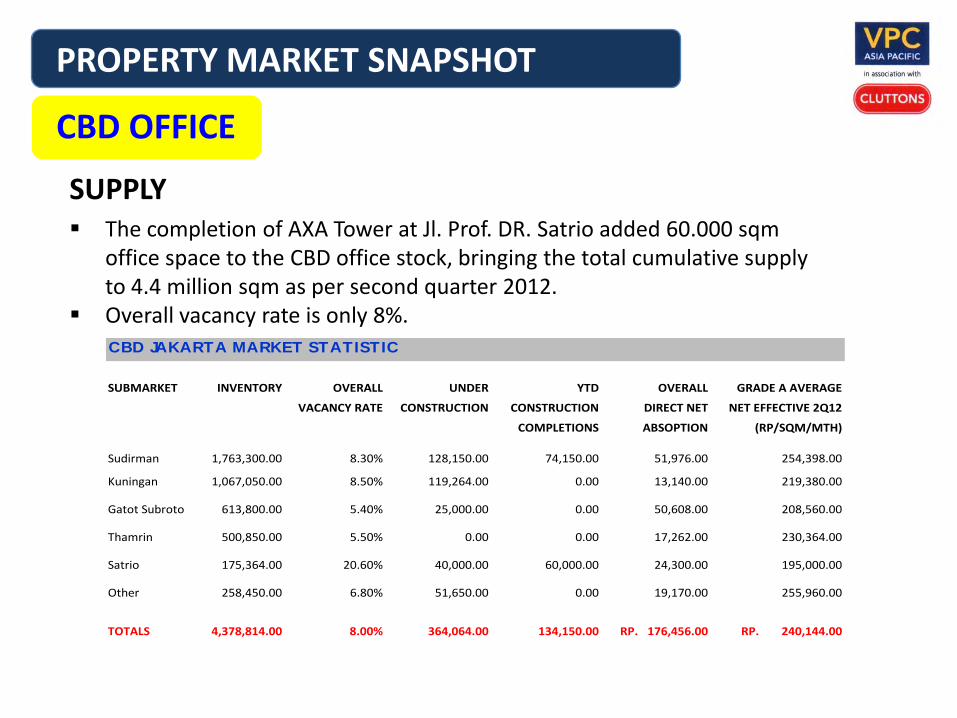

The completion of AXA Tower at Jl. Prof. DR. Satrio added 60.000 sqm office space to the CBD office stock, bringing the total cumulative supply to 4.4 million sqm as per second quarter 2012.

Overall vacancy rate is only 8%.

SUPPLY

CBD JAKARTA MARKET STATISTIC

SUBMARKET INVENTORY OVERALL UNDER YTD

VACANCY RATE CONSTRUCTION CONSTRUCTION

COMPLETIONS

Sudirman 1,763,300.00 8.30% 128,150.00 74,150.00 51,976.00 254,398.00

Kuningan 1,067,050.00 8.50% 119,264.00 0.00 13,140.00 219,380.00

Gatot Subroto 613,800.00 5.40% 25,000.00 0.00 50,608.00 208,560.00

Thamrin 500,850.00 5.50% 0.00 0.00 17,262.00 230,364.00

Satrio 175,364.00 20.60% 40,000.00 60,000.00 24,300.00 195,000.00

Other 258,450.00 6.80% 51,650.00 0.00 19,170.00 255,960.00

TOTALS 4,378,814.00 8.00% 364,064.00 134,150.00 RP. 176,456.00 RP. 240,144.00

ABSOPTION

OVERALL

DIRECT NET

GRADE A AVERAGE

NET EFFECTIVE 2Q12

(RP/SQM/MTH)

PROPERTY MARKET SNAPSHOT CBD OFFICE

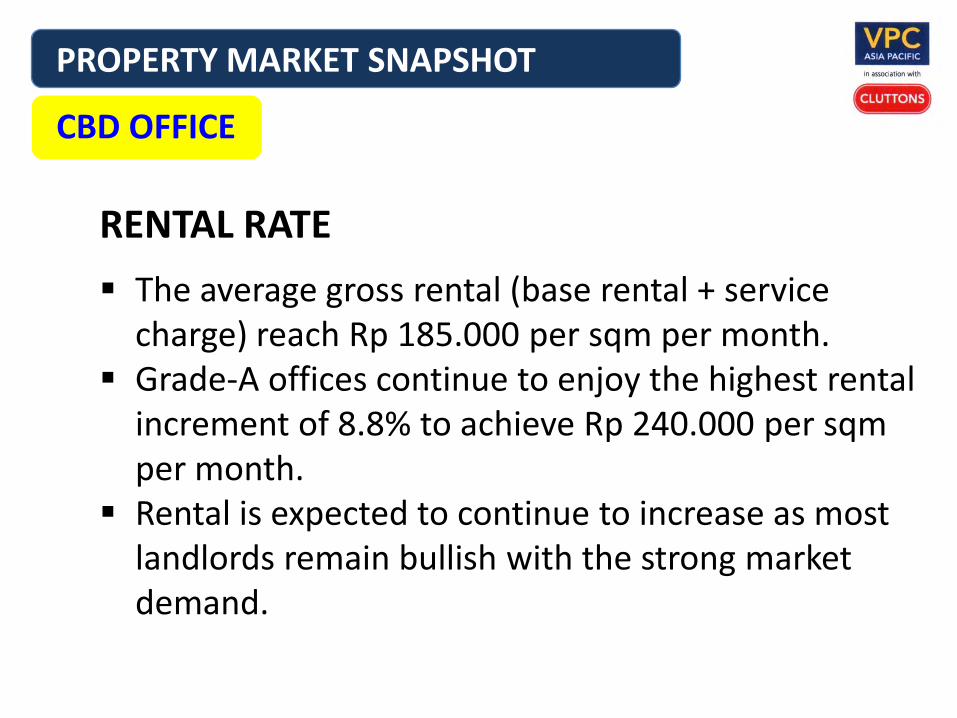

The average gross rental (base rental + service charge) reach Rp 185.000 per sqm per month.

Grade-A offices continue to enjoy the highest rental increment of 8.8% to achieve Rp 240.000 per sqm per month.

Rental is expected to continue to increase as most landlords remain bullish with the strong market demand.

RENTAL RATE

JAKARTA ICONIC BUILDINGS (Planned)

SIGNATURE TOWER Sudirman

MENARA JAKARTA Kemayoran

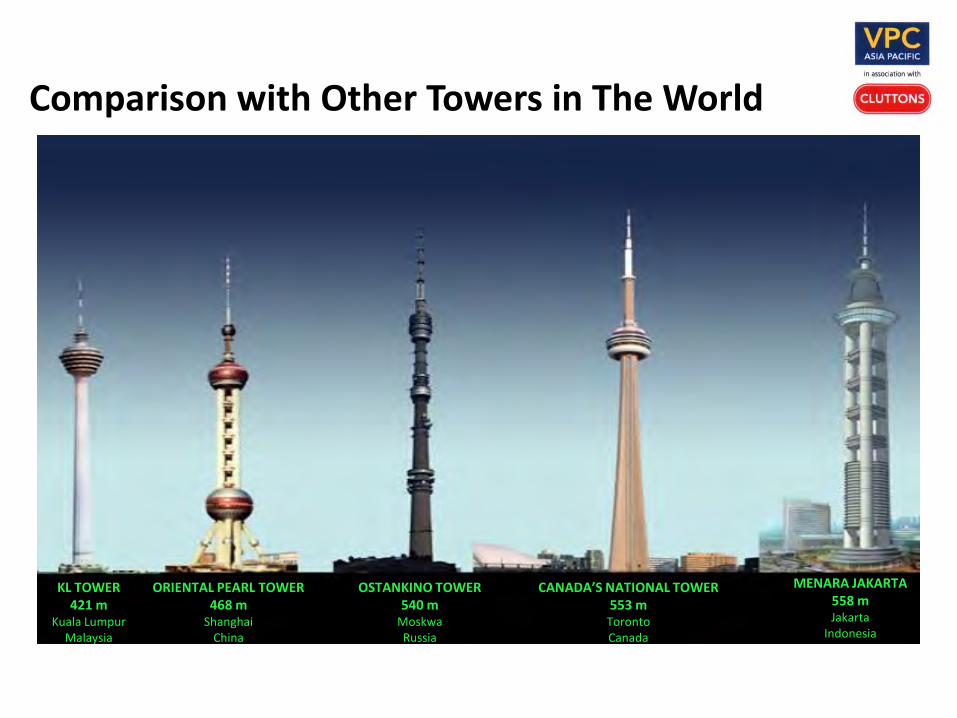

KL TOWER 421 m

Kuala Lumpur Malaysia

ORIENTAL PEARL TOWER 468 m

Shanghai China

OSTANKINO TOWER 540 m

Moskwa Russia

CANADA’S NATIONAL TOWER 553 m

Toronto Canada

MENARA JAKARTA 558 m Jakarta

Indonesia

Comparison with Other Towers in The World

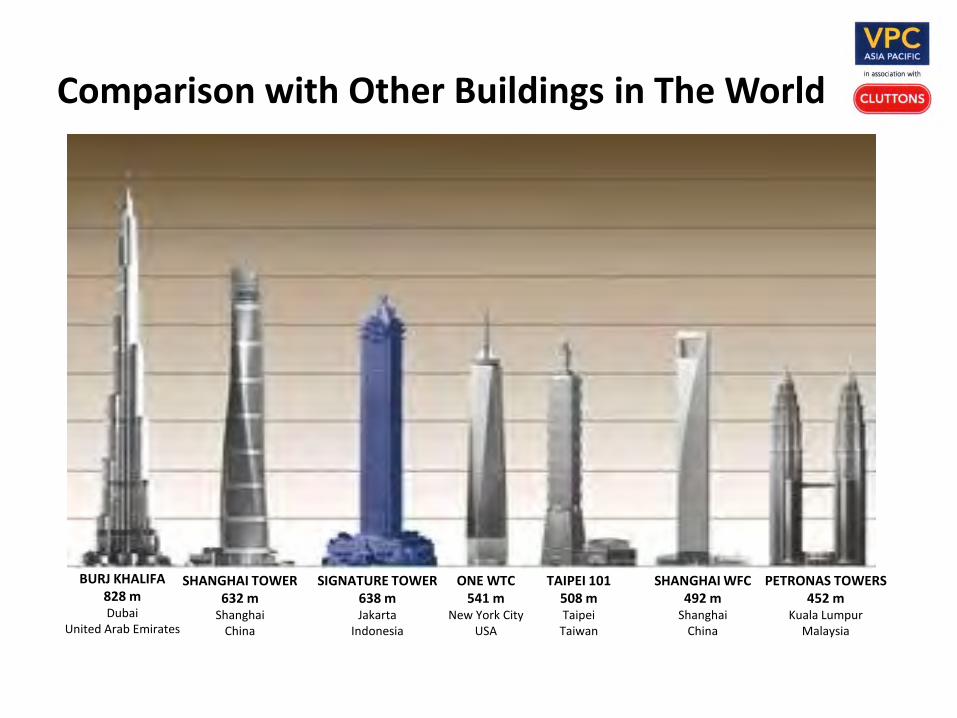

BURJ KHALIFA 828 m Dubai

United Arab Emirates

SHANGHAI TOWER 632 m

Shanghai China

SIGNATURE TOWER 638 m Jakarta

Indonesia

TAIPEI 101 508 m Taipei

Taiwan

ONE WTC 541 m

New York City USA

SHANGHAI WFC 492 m

Shanghai China

PETRONAS TOWERS 452 m

Kuala Lumpur Malaysia

Comparison with Other Buildings in The World

PROPERTY MARKET SNAPSHOT RETAIL MARKET

Jabodetabek’s vibrant and strong market continue to attract major Foreign Retail players to try their luck with the latest arrival of Central Department Store (Thailand), IKEA (Swedish).

NEW BIG PLAYERS

PROPERTY MARKET SNAPSHOT RETAIL MARKET

PROPERTY MARKET SNAPSHOT RETAIL MARKET

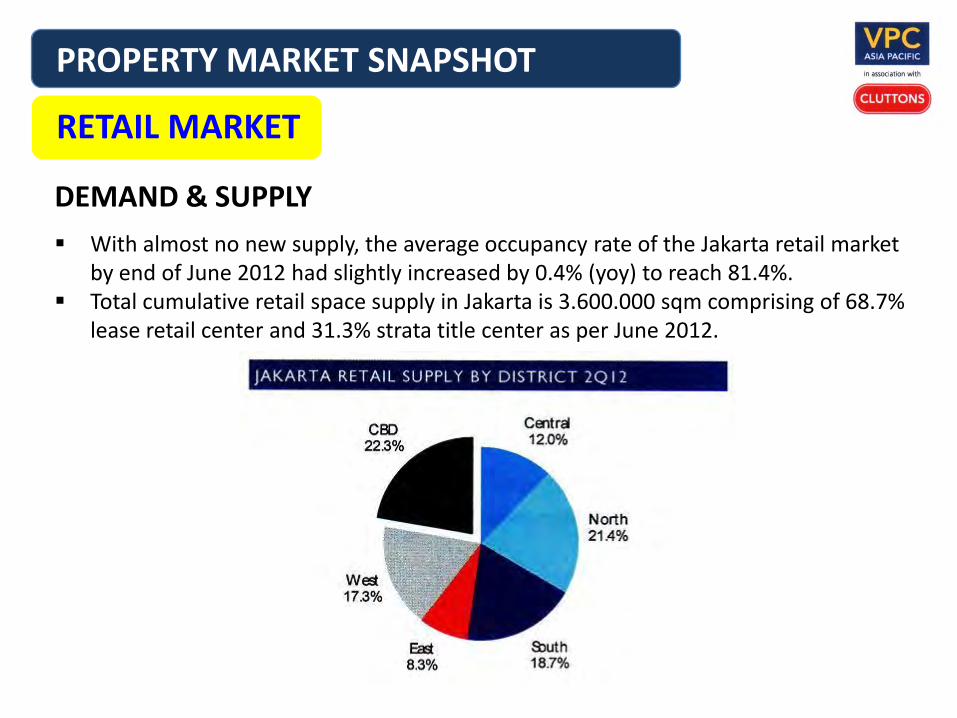

With almost no new supply, the average occupancy rate of the Jakarta retail market by end of June 2012 had slightly increased by 0.4% (yoy) to reach 81.4%.

Total cumulative retail space supply in Jakarta is 3.600.000 sqm comprising of 68.7% lease retail center and 31.3% strata title center as per June 2012.

DEMAND & SUPPLY

PROPERTY MARKET SNAPSHOT RETAIL MARKET

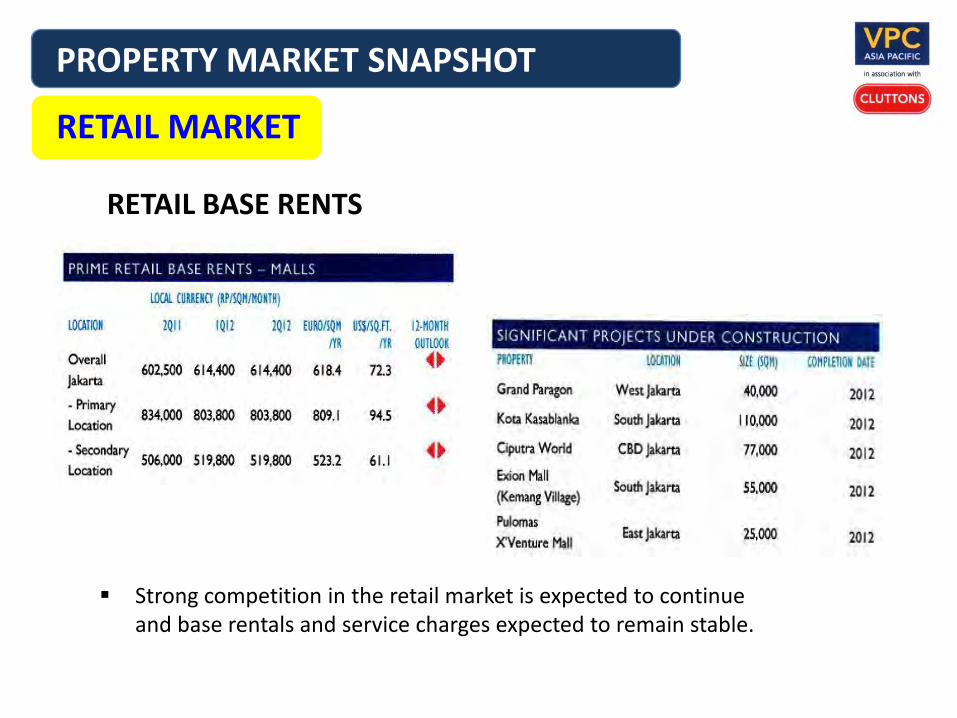

RETAIL BASE RENTS

Strong competition in the retail market is expected to continue and base rentals and service charges expected to remain stable.

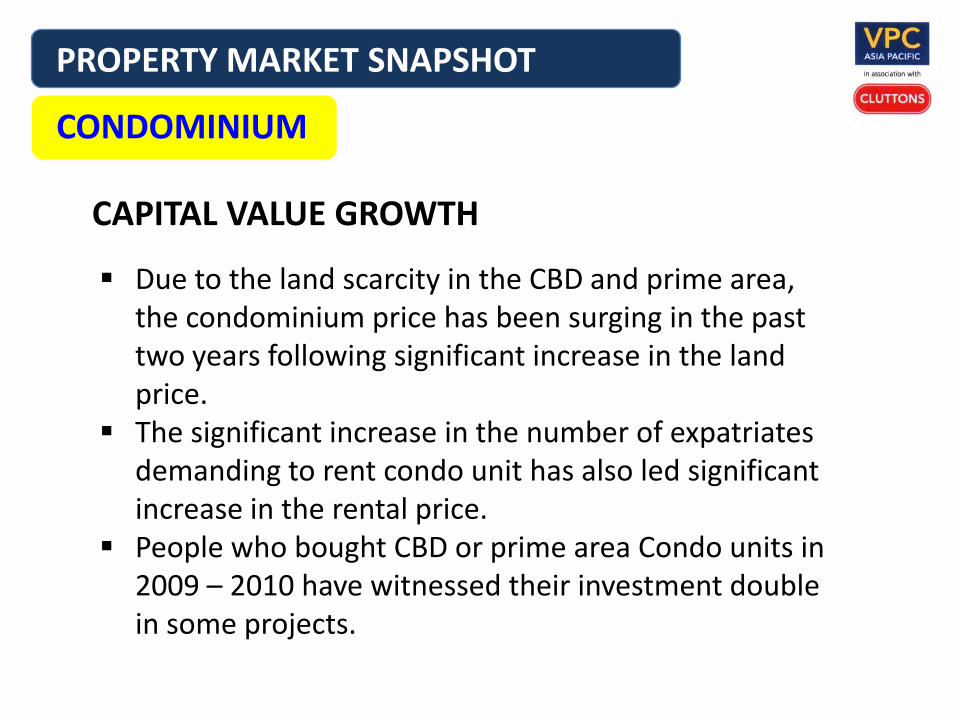

PROPERTY MARKET SNAPSHOT CONDOMINIUM

The rise of young professional middle income family and the change of lifestyle have been attributed to the surge of condominium project sales activities.

The pre-sales rate of the proposed condo projects stood at 61.6% and predicted to increase to 65.52% on the second quarter 2012.

SALES DEMAND

FOUR SEASONS JAKARTA

FOUR SEASONS JAKARTA

PROPERTY MARKET SNAPSHOT CONDOMINIUM

Due to the land scarcity in the CBD and prime area, the condominium price has been surging in the past two years following significant increase in the land price.

The significant increase in the number of expatriates demanding to rent condo unit has also led significant increase in the rental price.

People who bought CBD or prime area Condo units in 2009 – 2010 have witnessed their investment double in some projects.

CAPITAL VALUE GROWTH

PROPERTY MARKET SNAPSHOT INDUSTRIAL ESTATE

The acquisition of 100 Ha land at Suryacipta Industrial Estate by Automotive Giant Toyota has prompted wave of Japanese Manufacturers to relocate to Cikarang – Karawang Industrial Estates

The current spat between China – Japan has further increased the Japanese’s desire to relocate their base to South East Asia (Thailand, Vietnam and Indonesia).

Although deemed lack of infrastructure, Indonesia is seen as having conducive business climate, less expensive labors and strong local market.

REGIONAL MARKET SHIFT

FOUR SEASONS JAKARTA

PROPERTY MARKET SNAPSHOT INDUSTRIAL ESTATE

Demand for industrial land by foreign players will continue to remain strong.

Some Industrial Developers in Bekasi – Cikarang – Karawang area even suspend sales of new land due to sharp increase in price

Relatively higher land price and longer delivery period may force a shift of partial demand toward Serang and Cilegon Industrial Estate.

However due to better infrastructure, Bekasi – Cikarang – Karawang are expected to remain as the preferred location in the near future.

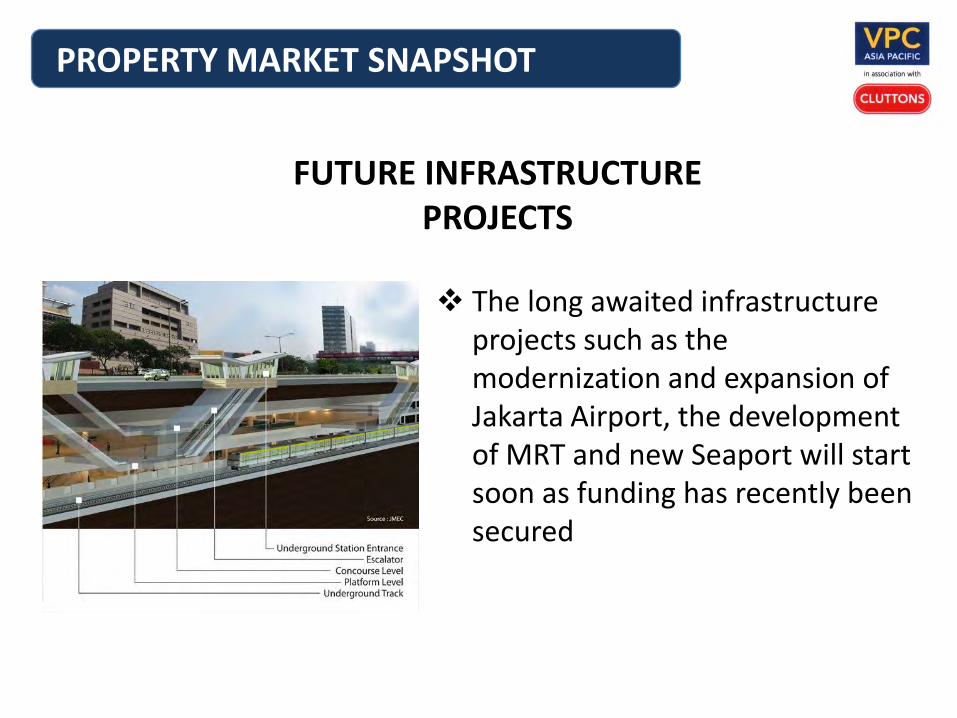

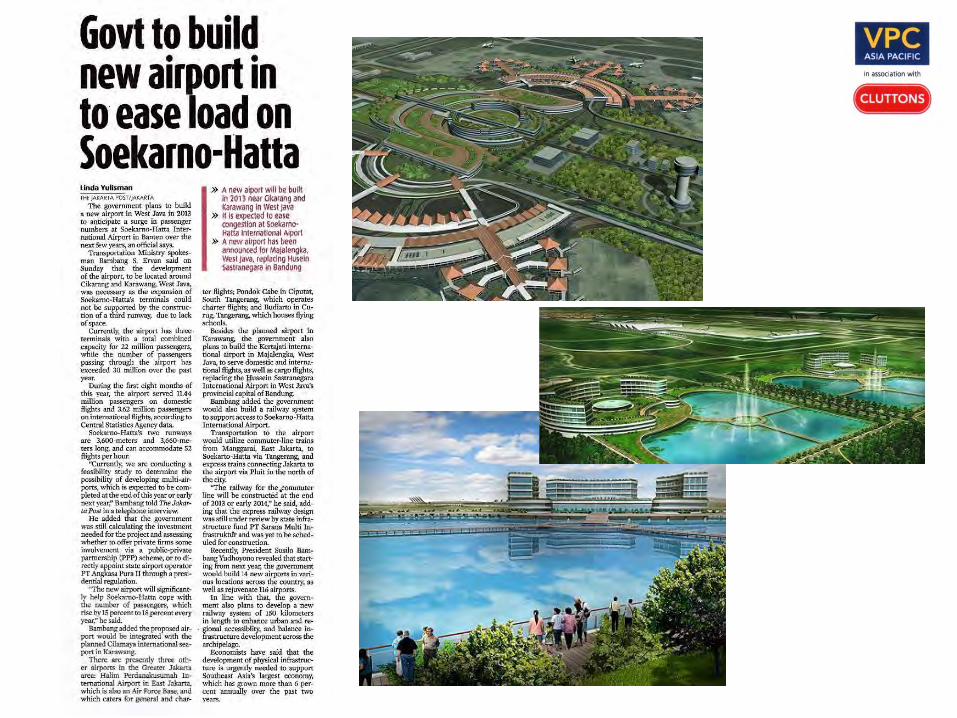

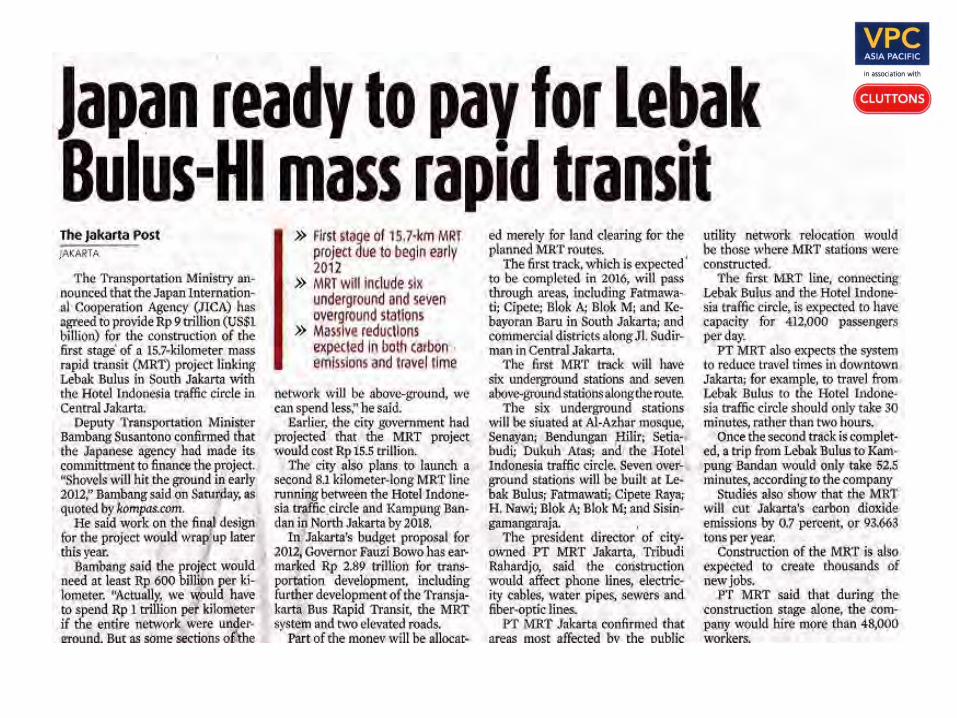

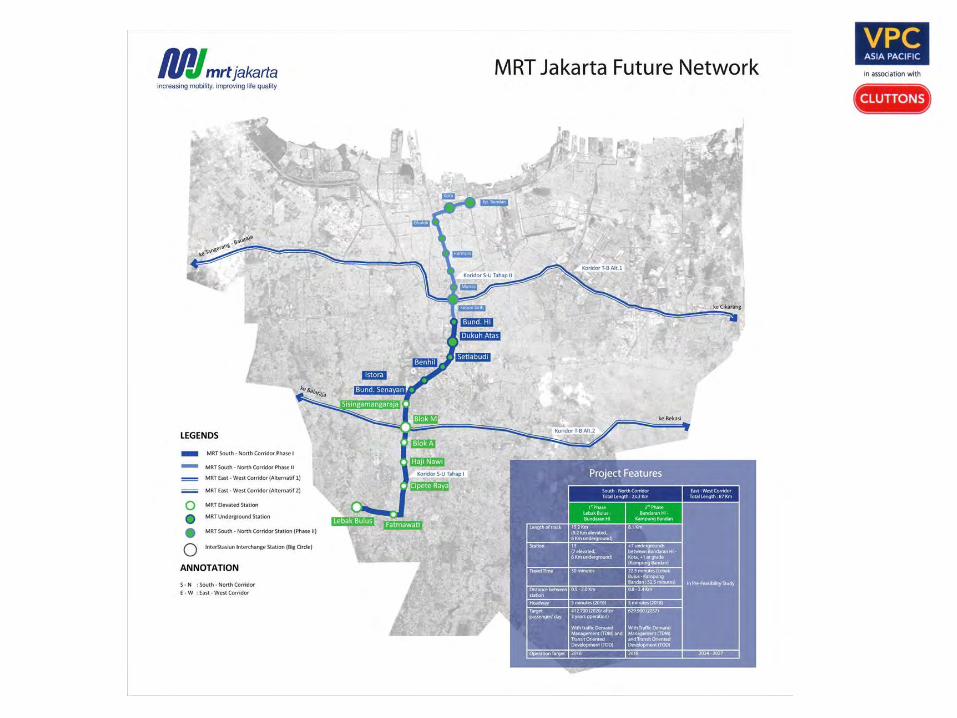

OVERVIEW

The long awaited infrastructure projects such as the modernization and expansion of Jakarta Airport, the development of MRT and new Seaport will start soon as funding has recently been secured

FUTURE INFRASTRUCTURE PROJECTS

PROPERTY MARKET SNAPSHOT

A new Seaport (Cilamaya) will be developed to reduce traffic congestion at existing Tanjung Priok Port

Located near the Karawang / Cikarang Industrial Estates

Funded by Japan International Cooperation Agency (JICA)

PROPERTY MARKET SNAPSHOT

MAJOR INSTRUCTION

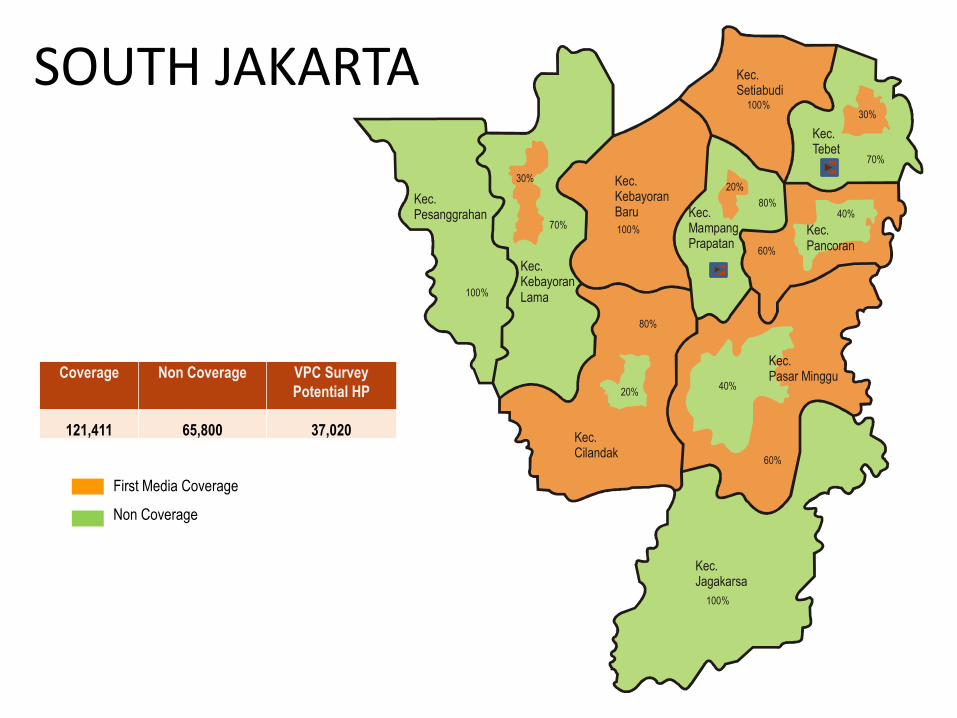

Market Research of Cable TV & Broadband Internet Potential Market in Greater Jakarta with over 1,7 million prospective subscribers findings

FIRST MEDIA

SOUTH JAKARTA

Kec.Pesanggrahan

Kec.Jagakarsa

Kec.Cilandak

100%

100%

20%

80%

40%

60%

Kec.Pasar Minggu

40%

60%

Kec.Pancoran

20%

80%Kec.MampangPrapatan

30%

Kec.Tebet

30%

Kec.Kebayoran Lama

70%

70%

Kec.Setiabudi

100%

Kec.KebayoranBaru

100%

First Media Coverage

Non Coverage

Coverage Non Coverage VPC Survey

Potential HP

121,411 65,800 37,020

MAJOR INSTRUCTION

Study on Location Selection and Development Recommendation for Bank Mandiri Regional Main Office located all over Indonesia (12 cities)

BANK MANDIRI

• Study on Asset Optimization and Space Planning for 240 Indosat’s Assets located in 30 provinces all over Indonesia

• Including Gallery, MSC, BTS, SCC, Data Centre, Office Buildings

MAJOR INSTRUCTION I N D O S A T

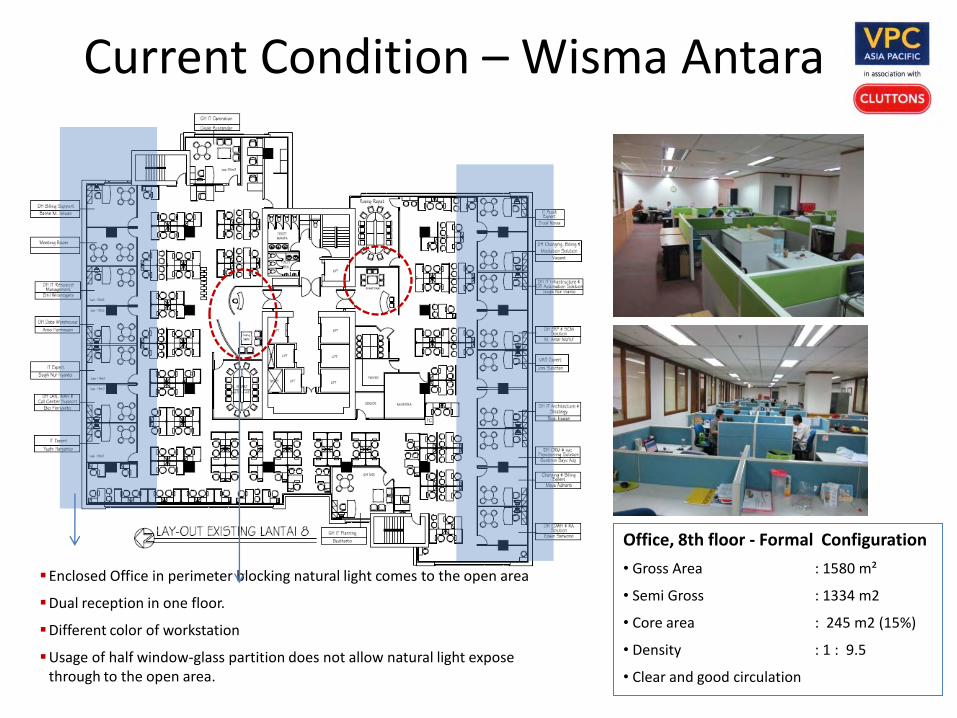

Current Condition – Wisma Antara

Enclosed Office in perimeter blocking natural light comes to the open area

Dual reception in one floor.

Different color of workstation

Usage of half window-glass partition does not allow natural light expose through to the open area.

Office, 8th floor - Formal Configuration

• Gross Area : 1580 m²

• Semi Gross : 1334 m2

• Core area : 245 m2 (15%)

• Density : 1 : 9.5

• Clear and good circulation

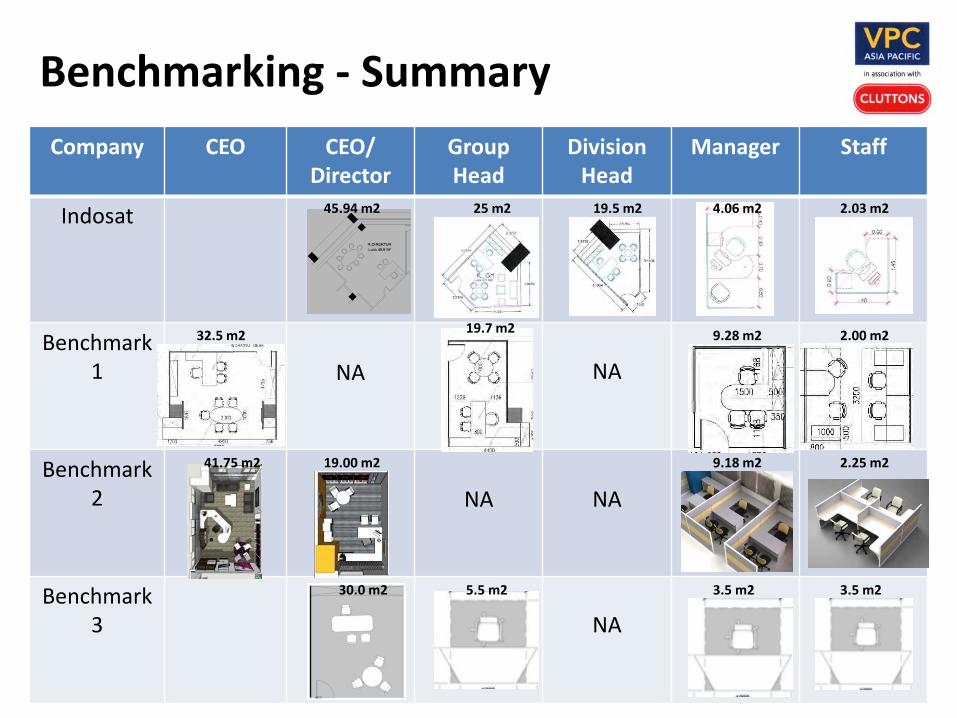

Benchmarking - Summary

Company CEO CEO/ Director

Group Head

Division Head

Manager Staff

Indosat

Benchmark 1 NA

NA

Benchmark 2 NA

NA

Benchmark 3

NA

25 m2 19.5 m2 4.06 m2 2.03 m2 45.94 m2

19.7 m2 2.00 m2 9.28 m2 32.5 m2

2.25 m2 9.18 m2 19.00 m2

5.5 m2 3.5 m2 3.5 m2 30.0 m2

41.75 m2

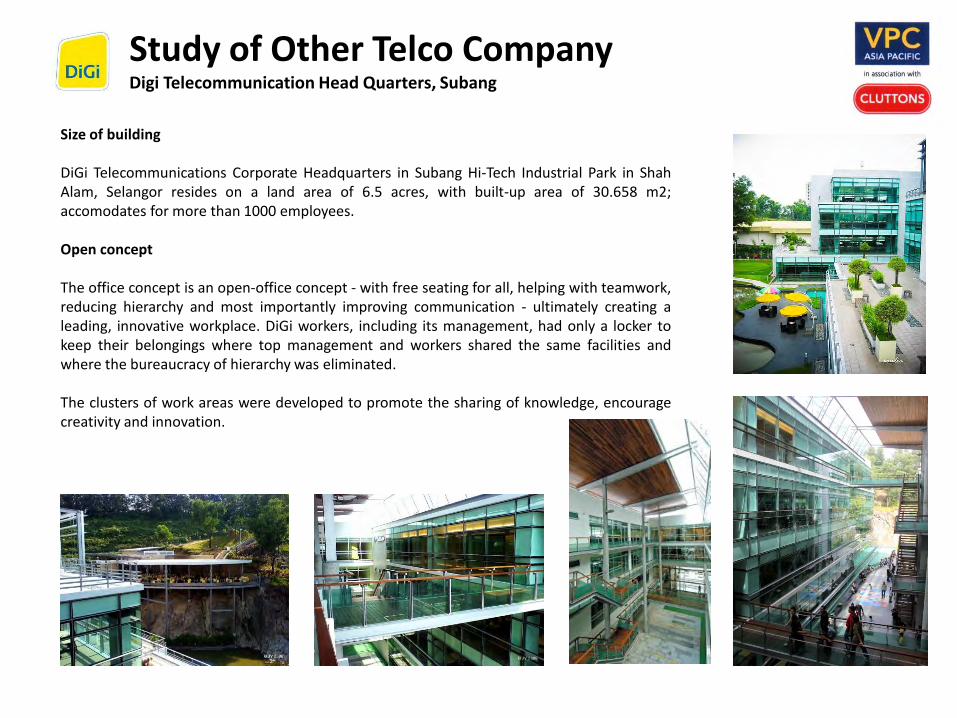

Study of Other Telco Company Digi Telecommunication Head Quarters, Subang

Size of building

DiGi Telecommunications Corporate Headquarters in Subang Hi-Tech Industrial Park in Shah Alam, Selangor resides on a land area of 6.5 acres, with built-up area of 30.658 m2; accomodates for more than 1000 employees.

Open concept

The office concept is an open-office concept - with free seating for all, helping with teamwork, reducing hierarchy and most importantly improving communication - ultimately creating a leading, innovative workplace. DiGi workers, including its management, had only a locker to keep their belongings where top management and workers shared the same facilities and where the bureaucracy of hierarchy was eliminated.

The clusters of work areas were developed to promote the sharing of knowledge, encourage

creativity and innovation.

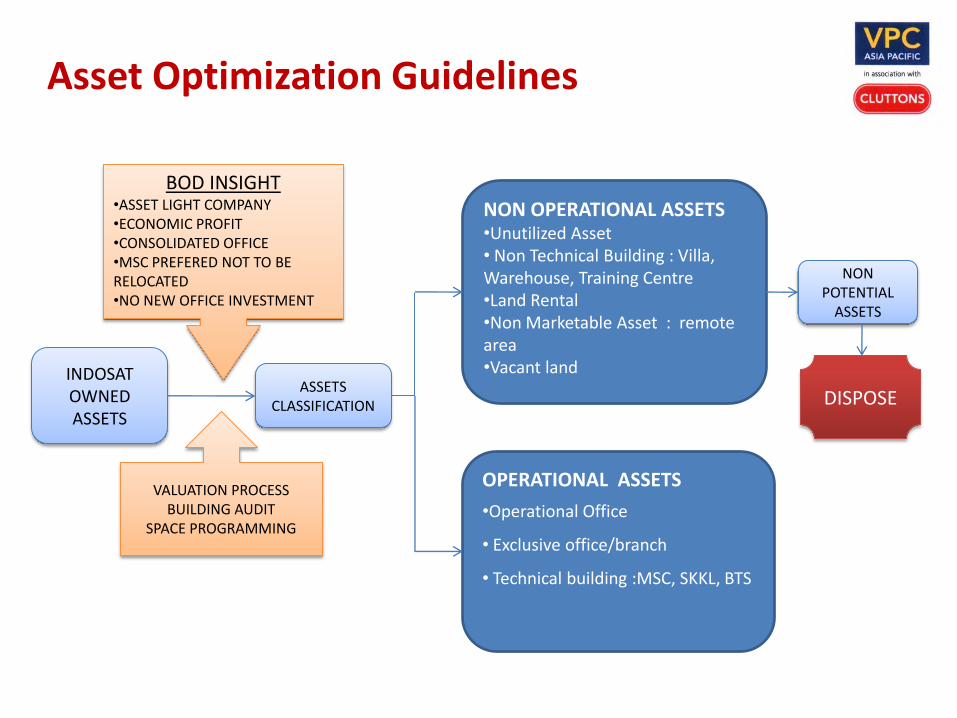

INDOSAT OWNED ASSETS

BOD INSIGHT •ASSET LIGHT COMPANY •ECONOMIC PROFIT •CONSOLIDATED OFFICE •MSC PREFERED NOT TO BE RELOCATED •NO NEW OFFICE INVESTMENT

VALUATION PROCESS BUILDING AUDIT

SPACE PROGRAMMING

ASSETS CLASSIFICATION

NON OPERATIONAL ASSETS •Unutilized Asset • Non Technical Building : Villa, Warehouse, Training Centre •Land Rental •Non Marketable Asset : remote area •Vacant land

OPERATIONAL ASSETS

•Operational Office

• Exclusive office/branch

• Technical building :MSC, SKKL, BTS

NON POTENTIAL

ASSETS

DISPOSE

Asset Optimization Guidelines

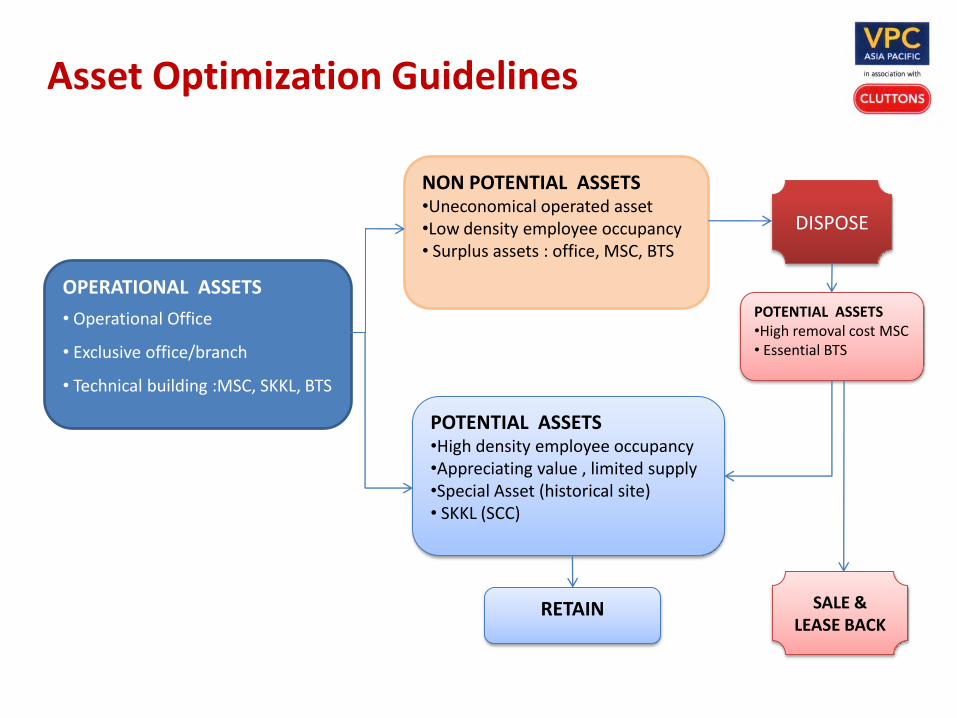

OPERATIONAL ASSETS

• Operational Office

• Exclusive office/branch

• Technical building :MSC, SKKL, BTS

NON POTENTIAL ASSETS •Uneconomical operated asset •Low density employee occupancy • Surplus assets : office, MSC, BTS

POTENTIAL ASSETS •High density employee occupancy •Appreciating value , limited supply •Special Asset (historical site) • SKKL (SCC)

DISPOSE

POTENTIAL ASSETS •High removal cost MSC • Essential BTS

SALE & LEASE BACK

RETAIN

Asset Optimization Guidelines

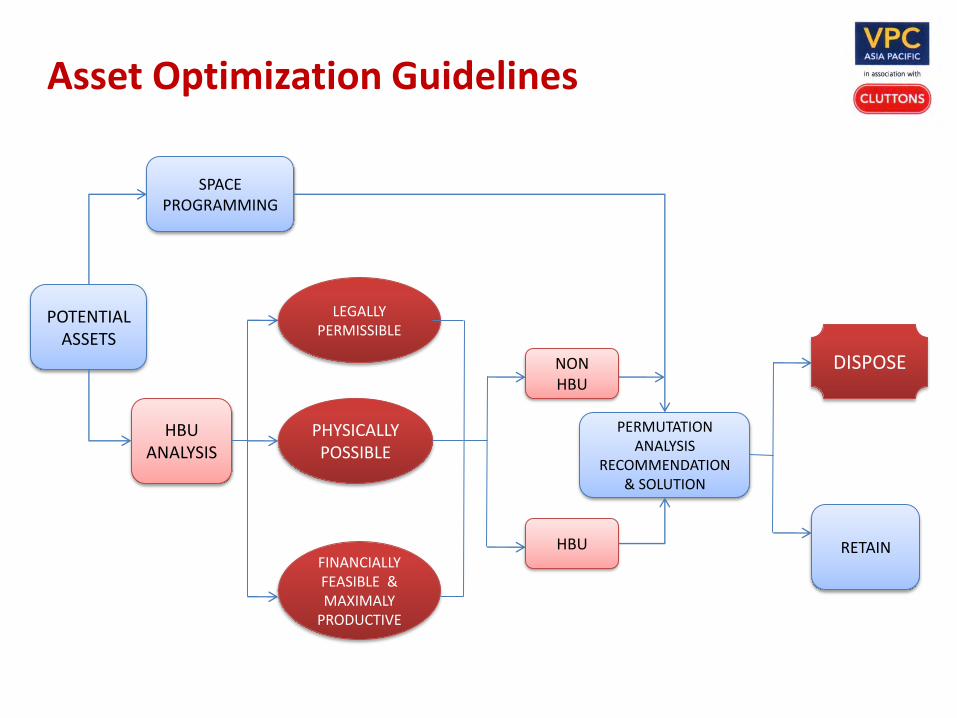

HBU ANALYSIS

FINANCIALLY FEASIBLE & MAXIMALY

PRODUCTIVE

SPACE PROGRAMMING

PERMUTATION ANALYSIS

RECOMMENDATION & SOLUTION

HBU

PHYSICALLY POSSIBLE

LEGALLY PERMISSIBLE

NON HBU

RETAIN

POTENTIAL ASSETS

DISPOSE

Asset Optimization Guidelines

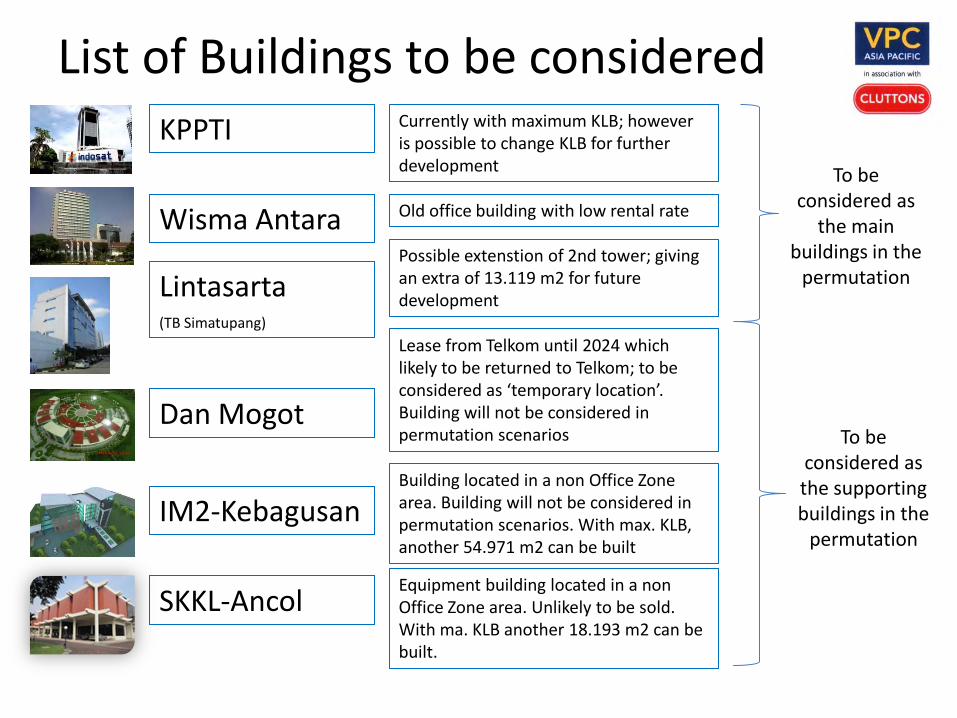

List of Buildings to be considered KPPTI

Lease from Telkom until 2024 which likely to be returned to Telkom; to be considered as ‘temporary location’. Building will not be considered in permutation scenarios

Currently with maximum KLB; however is possible to change KLB for further development

Possible extenstion of 2nd tower; giving an extra of 13.119 m2 for future development

Wisma Antara

Lintasarta (TB Simatupang)

Dan Mogot

IM2-Kebagusan

Old office building with low rental rate

Building located in a non Office Zone area. Building will not be considered in permutation scenarios. With max. KLB, another 54.971 m2 can be built

SKKL-Ancol Equipment building located in a non Office Zone area. Unlikely to be sold. With ma. KLB another 18.193 m2 can be built.

To be considered as

the main buildings in the

permutation

To be considered as the supporting buildings in the

permutation

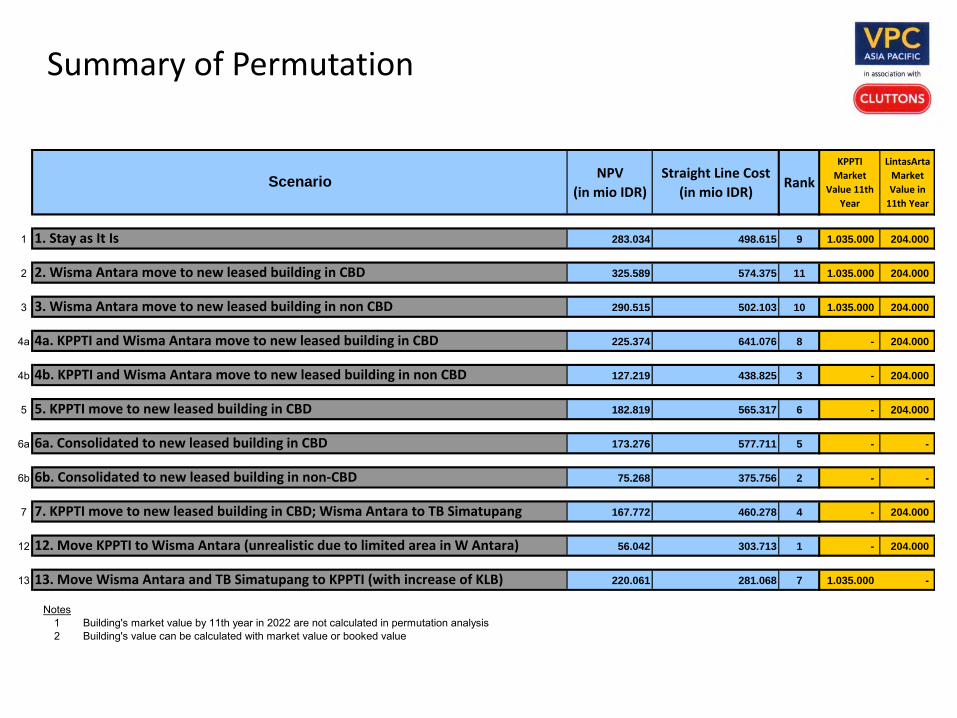

Summary of Permutation

NPV

(in mio IDR)

Straight Line Cost

(in mio IDR)Rank

KPPTI

Market

Value 11th

Year

LintasArta

Market

Value in

11th Year

1 283.034 498.615 9 1.035.000 204.000

2 325.589 574.375 11 1.035.000 204.000

3 290.515 502.103 10 1.035.000 204.000

4a 225.374 641.076 8 - 204.000

4b 127.219 438.825 3 - 204.000

5 182.819 565.317 6 - 204.000

6a 173.276 577.711 5 - -

6b 75.268 375.756 2 - -

7 167.772 460.278 4 - 204.000

12 56.042 303.713 1 - 204.000

13 220.061 281.068 7 1.035.000 -

Notes1 Building's market value by 11th year in 2022 are not calculated in permutation analysis2 Building's value can be calculated with market value or booked value

Scenario

4b. KPPTI and Wisma Antara move to new leased building in non CBD

5. KPPTI move to new leased building in CBD

6a. Consolidated to new leased building in CBD

1. Stay as It Is

2. Wisma Antara move to new leased building in CBD

3. Wisma Antara move to new leased building in non CBD

13. Move Wisma Antara and TB Simatupang to KPPTI (with increase of KLB)

4a. KPPTI and Wisma Antara move to new leased building in CBD

7. KPPTI move to new leased building in CBD; Wisma Antara to TB Simatupang

12. Move KPPTI to Wisma Antara (unrealistic due to limited area in W Antara)

6b. Consolidated to new leased building in non-CBD

THANK YOU