76

1 Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business Indonesian Consumer Update Prepared for Network Club September 12, 2006

1Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

Indonesian Consumer Update

Prepared for Network ClubSeptember 12, 2006

2

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

VNU Companies in Indonesia

●ACNielsen Indonesia–FMCG retail tracking–Consumer panel–Customised

●Nielsen Media Research–Print and radio research–Advertising expenditure monitoring

●AGB Nielsen Media Research–Television Ratings

3

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Topics

● Spending Power● Retail FMCG Sales● Growth of the Modern Trade ● The Media Scene ● Consumer Attitudes● World Cup Survey

16.0

1.06

©AC

Nie

lsen

200

6

Spending Power

We use Expenditure level to measure spending power...

• household spending on day-to-day goods and services eg: routine household expenses on food, washing and cleaning products, children’s school fees, electricity, water, cigarettes, wages of household helpers, petrol, monthly house rental & otherroutine expenses

• excludes major items - cars, houses, etc.

• so does not cover all spending

• validates well with durables ownership and lifestyle

• Long-term trend

SES in major urban centresAll people age 10+, in 9 big cities (base : 40,042,000) in %

13

17

27

21

1174

A1 3001 &OVER

A2 2001 - 3000

B 1501 - 2000

C1 1001 - 1500

C2 701 - 1000

D 501 - 700

E 500 & BELOW2006

Source : Media Index, Nielsen Media Research

SES (Rp. ‘000)

Rural spending is lower…

2213

32

26

21

3218

19

171925

14812

44 614 13 A1 2250 &Over

A2 1750 - 2250

B 1250 - 1750

C1 800 - 1250

C2 600 - 800

D 400 - 600

E 400 & BelowPopulation National Urban RuralIn ‘000 167,781 84,837 82,945

SES (Rp. ‘000)

Source : Media Index, Nielsen Media Research

In %

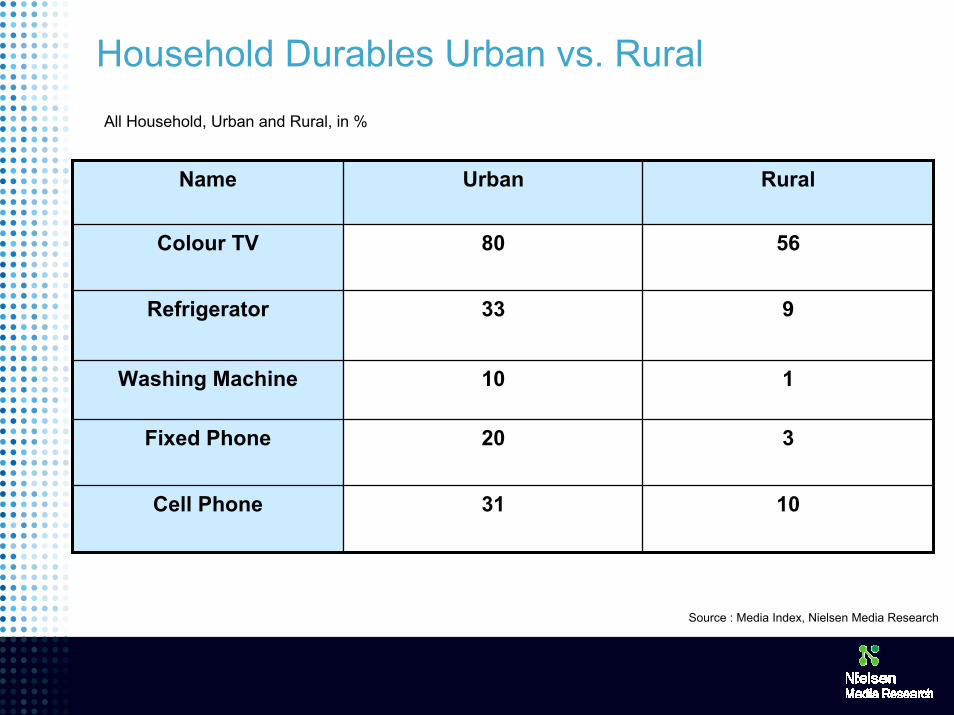

Household Durables Urban vs. RuralAll Household, Urban and Rural, in %

320Fixed Phone

1031Cell Phone

110Washing Machine

933Refrigerator

5680Colour TV

Rural UrbanName

Source : Media Index, Nielsen Media Research

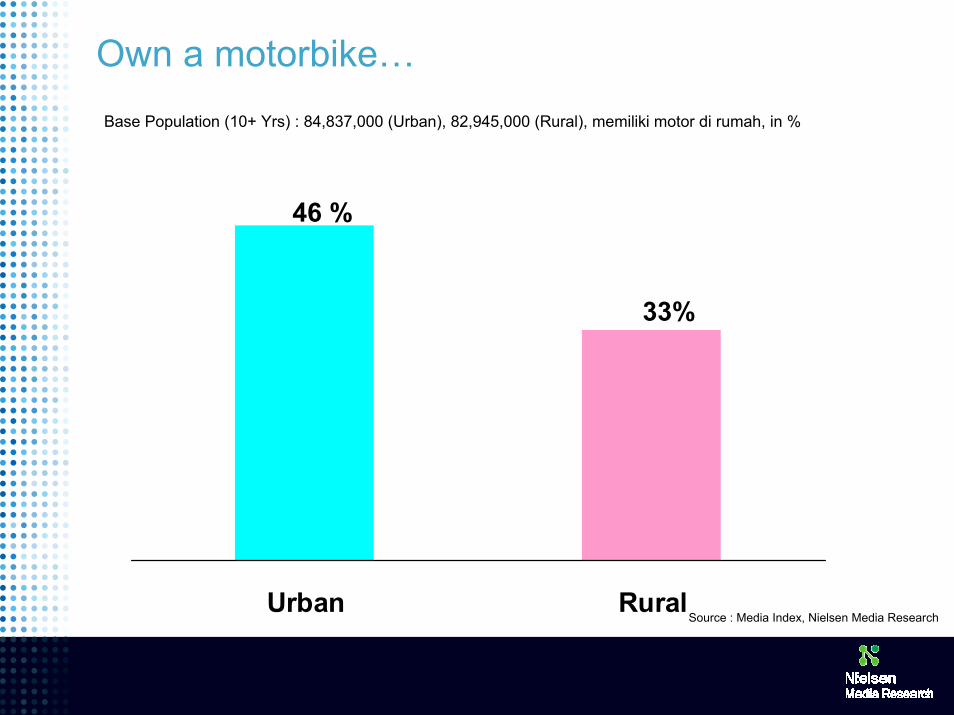

Own a motorbike…Base Population (10+ Yrs) : 84,837,000 (Urban), 82,945,000 (Rural), memiliki motor di rumah, in %

Urban Rural

46 %

33%

Source : Media Index, Nielsen Media Research

In home entertainment…Base Population (10+ Yrs) : 84,837,000 (Urban), 82,945,000 (Rural), Kepemilikan VCD/DVD + CD, in %

Urban Rural

VCD/DVDCD

53%

30%27%

11%

Source : Media Index, Nielsen Media Research

11

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

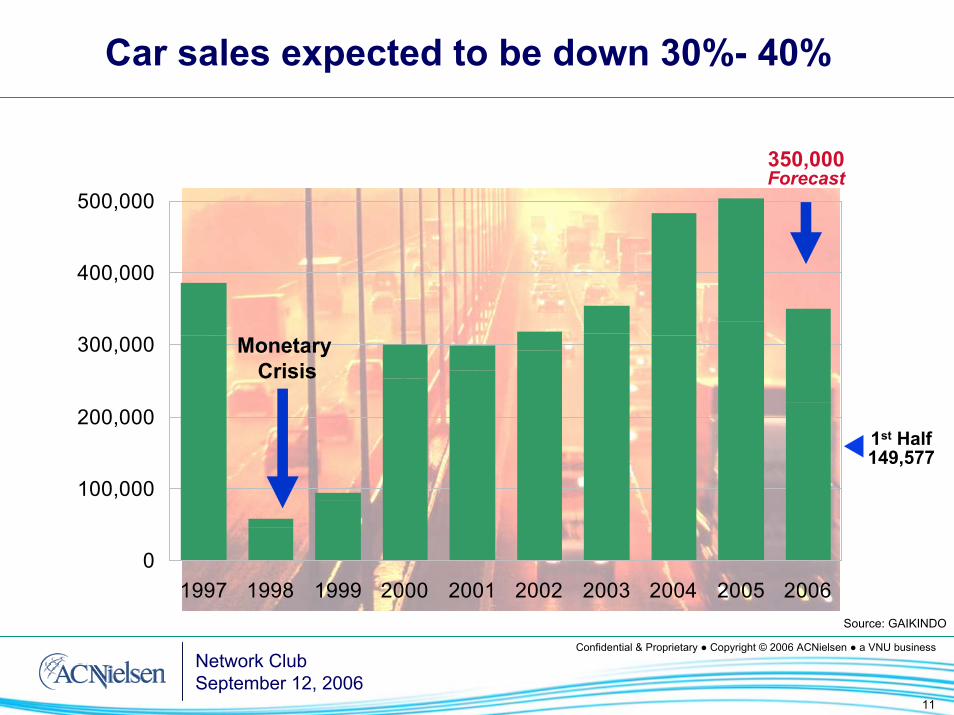

Car sales expected to be down 30%- 40%

0

100,000

200,000

300,000

400,000

500,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Monetary Crisis

350,000 Forecast

1st Half149,577

Source: GAIKINDO

12

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

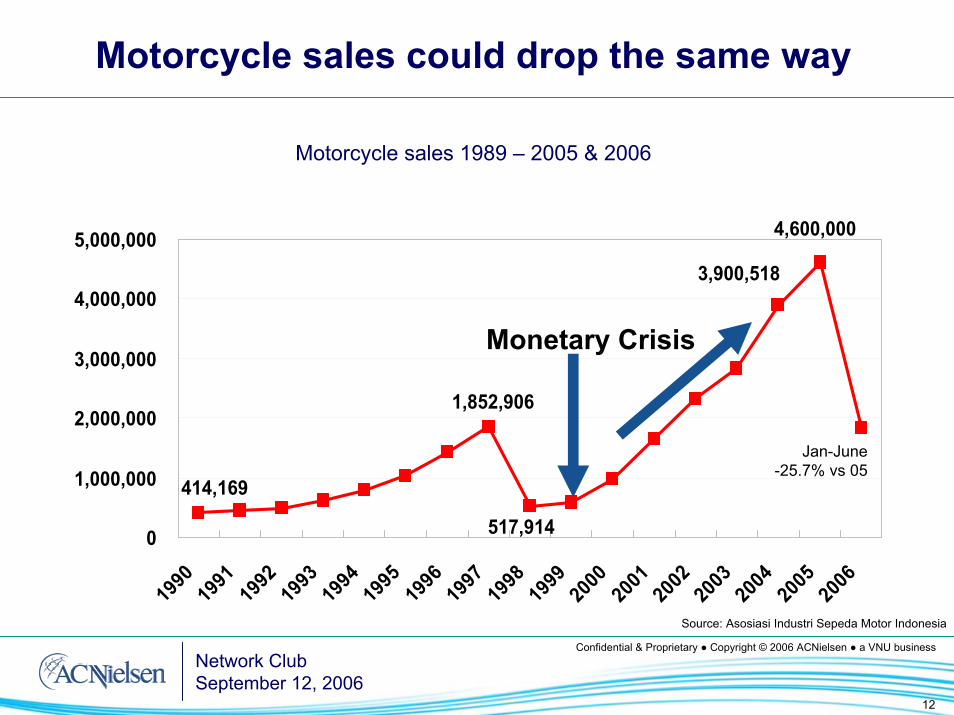

Motorcycle sales could drop the same way

Motorcycle sales 1989 – 2005 & 2006

414,169

1,852,906

517,914

3,900,518

4,600,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Monetary Crisis

Jan-June-25.7% vs 05

Source: Asosiasi Industri Sepeda Motor Indonesia

13

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

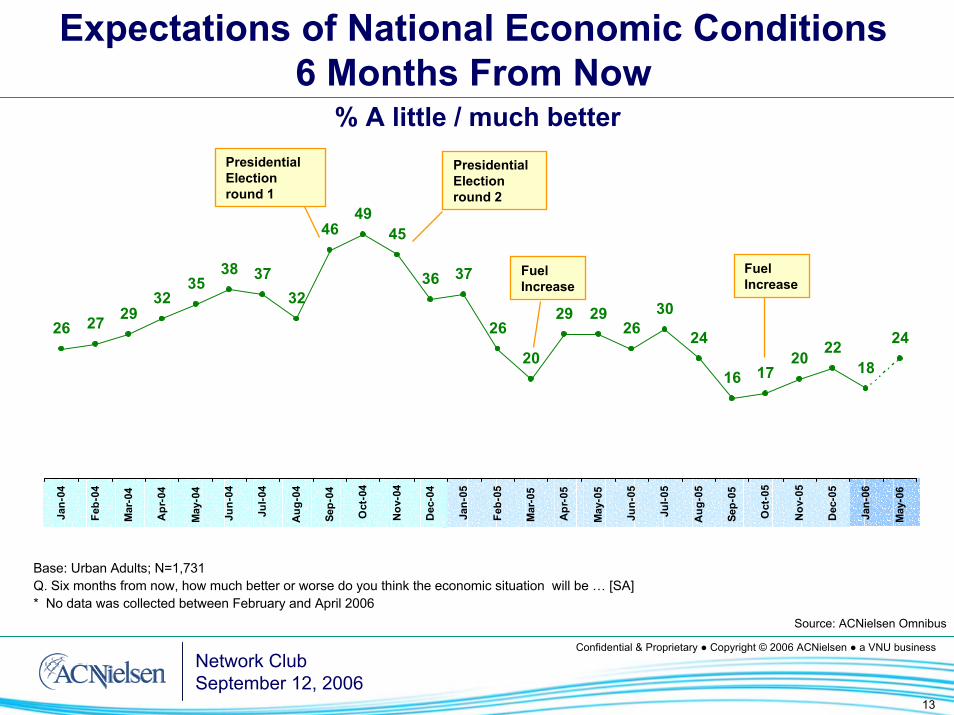

Expectations of National Economic Conditions6 Months From Now

% A little / much better

Base: Urban Adults; N=1,731Q. Six months from now, how much better or worse do you think the economic situation will be … [SA]* No data was collected between February and April 2006

26 27 2932

3538 37

32

4649

45

36 37

26

20

29 2926

30

24

16 1720 22

18

24

Jan-

04

Feb-

04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Aug

-04

Sep-

04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep-

05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

May

-06

Fuel Increase

Fuel Increase

Presidential Election round 2

Presidential Election round 1

Source: ACNielsen Omnibus

14

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Retail FMCG Sales

15

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

In 2005 Indonesia saw the highest growth in SE Asia

Source: ACNielsen ShopperTrends

16

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

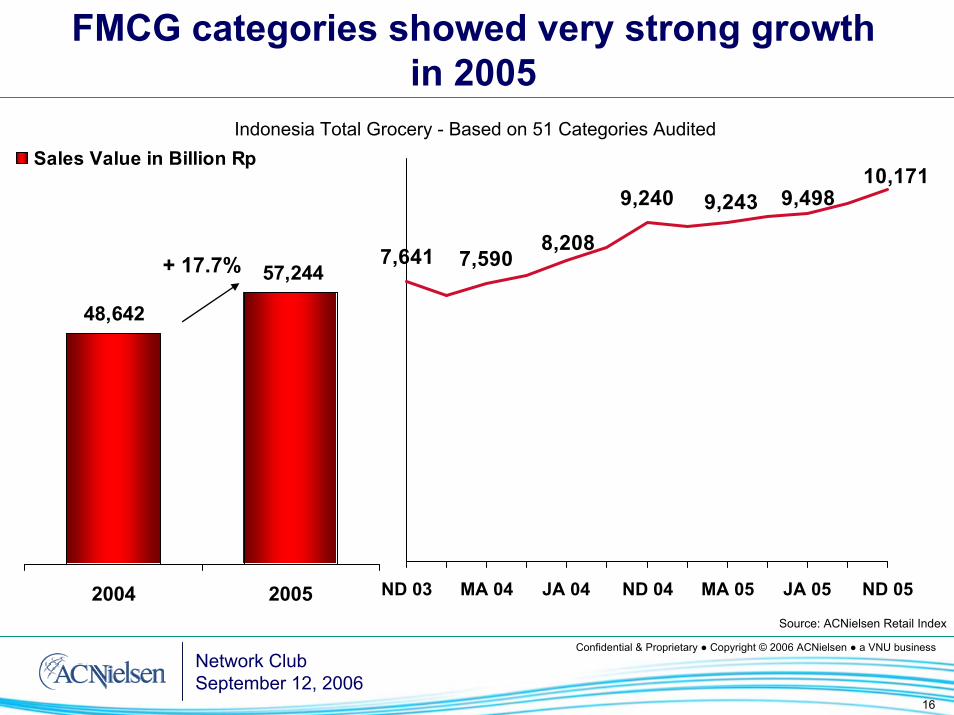

FMCG categories showed very strong growth in 2005

7,5907,641

9,243 9,498

8,208

9,24010,171

ND 03 MA 04 JA 04 ND 04 MA 05 JA 05 ND 05

48,642

57,244

2004 2005

Sales Value in Billion RpIndonesia Total Grocery - Based on 51 Categories Audited

+ 17.7%

Source: ACNielsen Retail Index

17

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

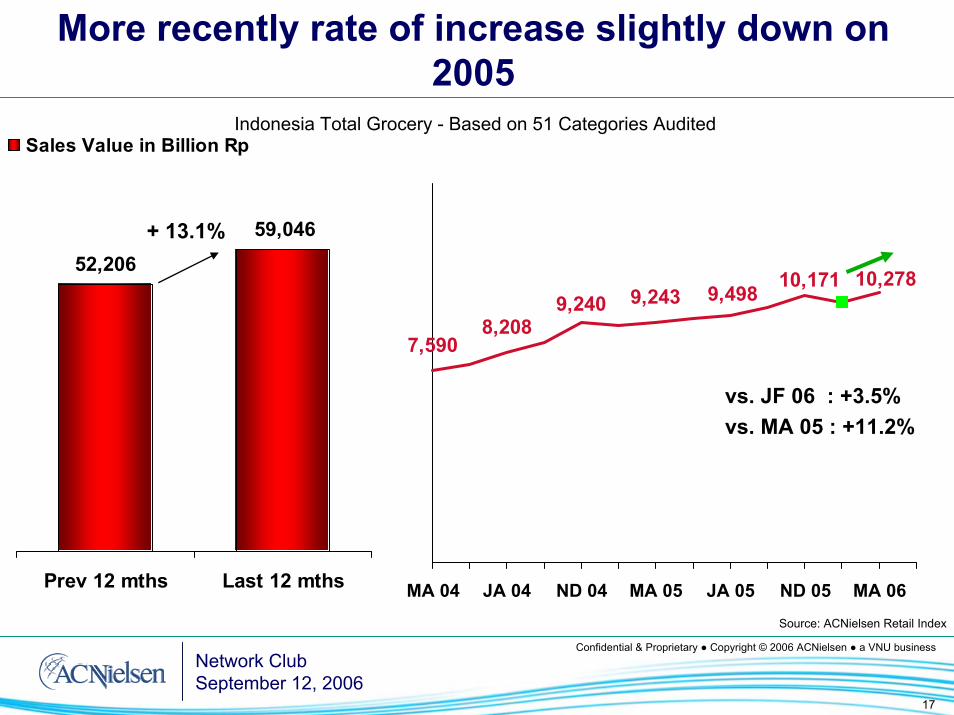

More recently rate of increase slightly down on 2005

8,2087,590

9,49810,171

9,240 9,24310,278

MA 04 JA 04 ND 04 MA 05 JA 05 ND 05 MA 06

52,206

59,046

Prev 12 mths Last 12 mths

Sales Value in Billion RpIndonesia Total Grocery - Based on 51 Categories Audited

+ 13.1%

vs. JF 06 : +3.5%vs. MA 05 : +11.2%

Source: ACNielsen Retail Index

18

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

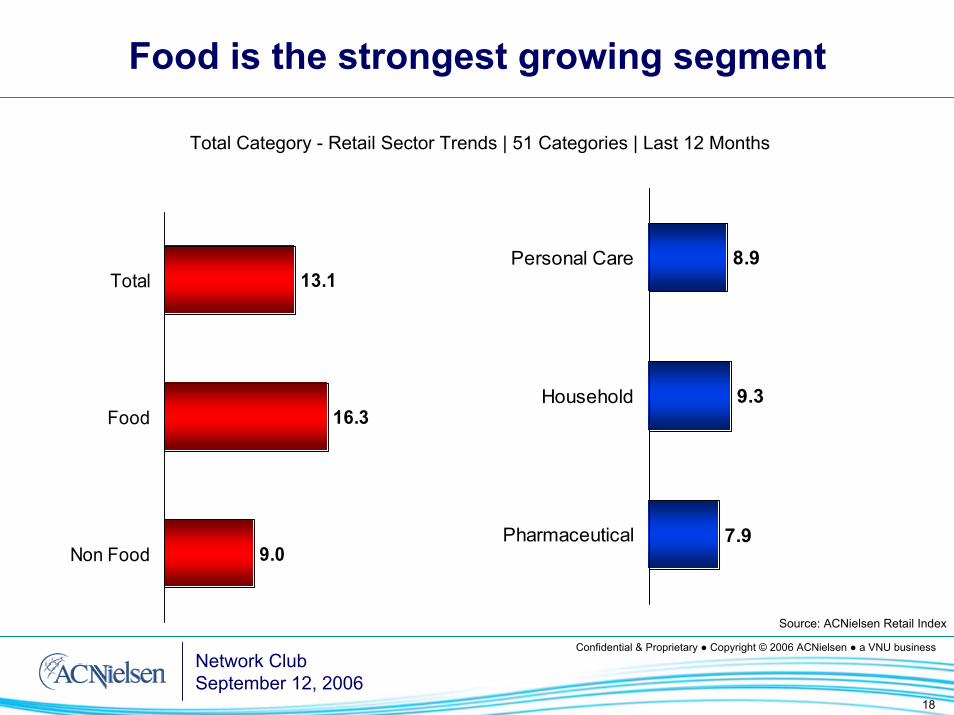

Food is the strongest growing segment

Total Category - Retail Sector Trends | 51 Categories | Last 12 Months

8.9

9.3

7.9

Personal Care

Household

Pharmaceutical

13.1

16.3

9.0

Total

Food

Non Food

Source: ACNielsen Retail Index

19

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

And there are some exceptional volume and percentage growths from Food

Top Growing Categories in FoodFood Categories | Value Growth in Billon Rp and In Percentage Vs. Prev 12 Months

174

173

145

139

262

413

460

606

893

1,101Instant Noodle

Powder Milk

Biscuit

Coffee

SCM

Stock Soup

Cooking Oil

Liquid Milk

Chocolate

Snack

In PercentageValue Gain in Billion Rp

18.5

17.6

17.1

17.1

18.9

23.4

23.5

24.5

24.7

32.3Liquid Milk

Dry noodle

Coffee

Biscuit

Chocolate

Ice cream

SCM

Cooking Oil

Instant Noodle

Powder Milk Source: ACNielsen Retail Index

20

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

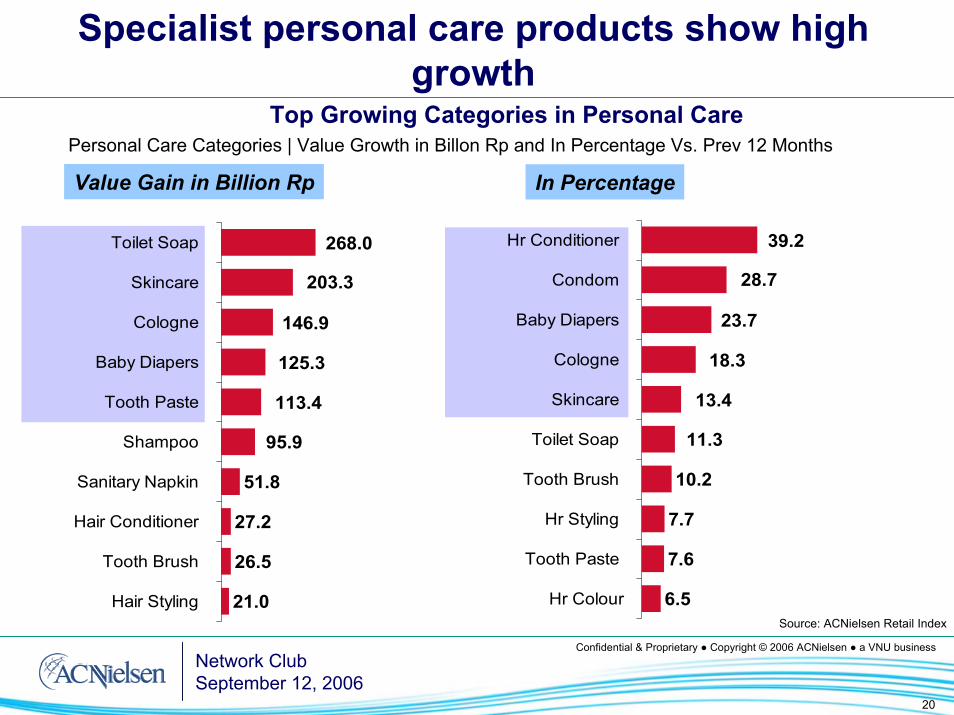

Top Growing Categories in Personal Care

Specialist personal care products show high growth

Personal Care Categories | Value Growth in Billon Rp and In Percentage Vs. Prev 12 Months

Value Gain in Billion Rp In Percentage

51.8

27.2

26.5

21.0

95.9

113.4

125.3

146.9

203.3

268.0Toilet Soap

Skincare

Cologne

Baby Diapers

Tooth Paste

Shampoo

Sanitary Napkin

Hair Conditioner

Tooth Brush

Hair Styling

10.2

7.7

7.6

6.5

11.3

13.4

18.3

23.7

28.7

39.2Hr Conditioner

Condom

Baby Diapers

Cologne

Skincare

Toilet Soap

Tooth Brush

Hr Styling

Tooth Paste

Hr Colour Source: ACNielsen Retail Index

21

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Java and W.Java particularly is still the most attractive market place with the higher growth

Area Contribution in Value - Based on 51 Categories Audited – Last 12 mths

Growth vs. Prev. 12 mths

Jakarta14.8

C.Java 15.1

E.Java 16.2

W.Java 25.4N.Sumatra

6.3

S.Sumatra 9.2

O.Islands 12.9

11.6O.Islands Grocery

7.8S.Sumatra Grocery

6.3N.Sumatra Grocery

12.2E.Java Grocery

13.2C.Java Grocery

20.1W.Java Grocery

10.8Jakarta Grocery

13.1Indonesia Grocery

Source: ACNielsen Retail Index

22

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

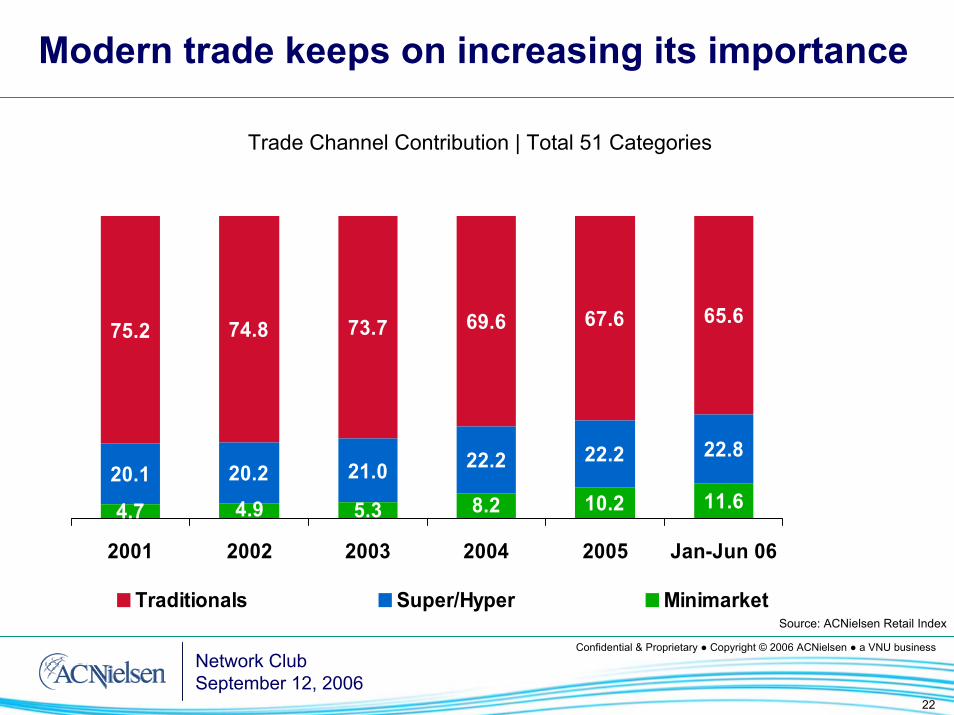

Modern trade keeps on increasing its importance

75.2 74.8 73.7 69.6 67.6 65.6

20.1 20.2 21.0 22.2 22.2 22.8

10.2 11.68.25.34.94.7

2001 2002 2003 2004 2005 Jan-Jun 06

Traditionals Super/Hyper Minimarket

Trade Channel Contribution | Total 51 Categories

Source: ACNielsen Retail Index

23

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Growth of the Modern Trade

24

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Share of Trade in Asia

In 2005, modern trade continued to grow faster in North Asia than in South-East Asia

Source: ACNielsen ShopperTrends

25

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Share of Trade for Modern Self-service Outlets SE Asia

Source: ACNielsen ShopperTrends

While the modern trade gained share in Malaysia, Indonesia and Vietnam, traditional trade remains strong in the Philippines

26

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

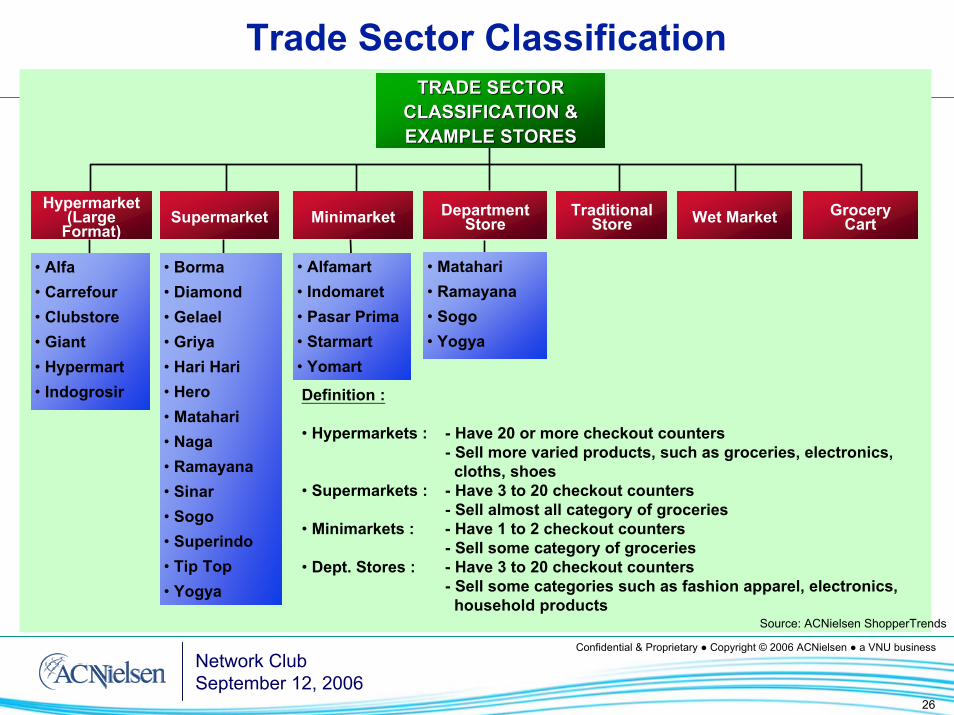

Trade Sector ClassificationTRADE SECTOR TRADE SECTOR

CLASSIFICATION & CLASSIFICATION & EXAMPLE STORESEXAMPLE STORES

Traditional StoreMinimarket Wet Market

Hypermarket(Large

Format)Grocery

CartDepartment

StoreSupermarket

• Alfa• Carrefour• Clubstore• Giant• Hypermart• Indogrosir

• Alfamart• Indomaret• Pasar Prima• Starmart• Yomart

• Borma• Diamond• Gelael• Griya• Hari Hari• Hero• Matahari• Naga• Ramayana• Sinar• Sogo• Superindo• Tip Top• Yogya

• Matahari• Ramayana• Sogo• Yogya

Definition :

• Hypermarkets : - Have 20 or more checkout counters- Sell more varied products, such as groceries, electronics,

cloths, shoes• Supermarkets : - Have 3 to 20 checkout counters

- Sell almost all category of groceries• Minimarkets : - Have 1 to 2 checkout counters

- Sell some category of groceries• Dept. Stores : - Have 3 to 20 checkout counters

- Sell some categories such as fashion apparel, electronics,household products

Source: ACNielsen ShopperTrends

27

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Major Chains

19Griya26Yogya69Ramayana42Matahari83Hero (DFI)46

SupermarketSuperindo Delhaize

AMPM87

Convenience StoreCircle K

52Starmart (DFI)1263Alfamart1270

MinimarketIndomaret

1Goro

6Indogrosir

17WarehouseMakro

5TipTop

4ADA

19Carrefour

16Hypermart(Matahari group)

34Alfa

13HypermarketGiant (DFI)

*) as of December 2005

28

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Indonesia Share of TradeA 15% increase in Minimarket store numbers has lead to them gaining another two

share points from the traditional during 2005

Source: ACNielsen ShopperTrends

29

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

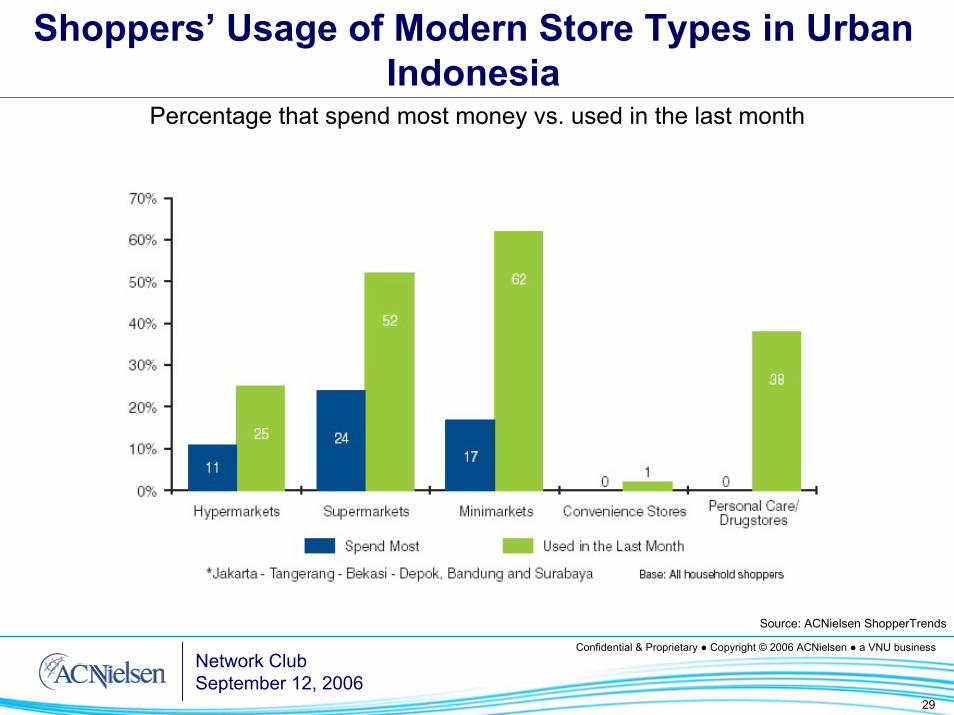

Shoppers’ Usage of Modern Store Types in Urban Indonesia

Percentage that spend most money vs. used in the last month

Source: ACNielsen ShopperTrends

30

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Retail Channels going forward

Hypermarket and minimarket will continue to lead growth

Supermarkets leverage thru assortment and differentiate thru unique items not available at otherstores, developing loyalty

Convenience operators will redefine themselves via foodservice as they lessen their dependence on cigarettes

Drugstores will develop packaged foods range

Retailers will define themselves more by the customers they service than by the products they sell

31

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

PL in Asia Pacific is still to grow

Source: ACNielsen ShopperTrends

32

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Shoppers Who are either Aware of or Bought Private Label in the Last Month

Source: ACNielsen ShopperTrends

33

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

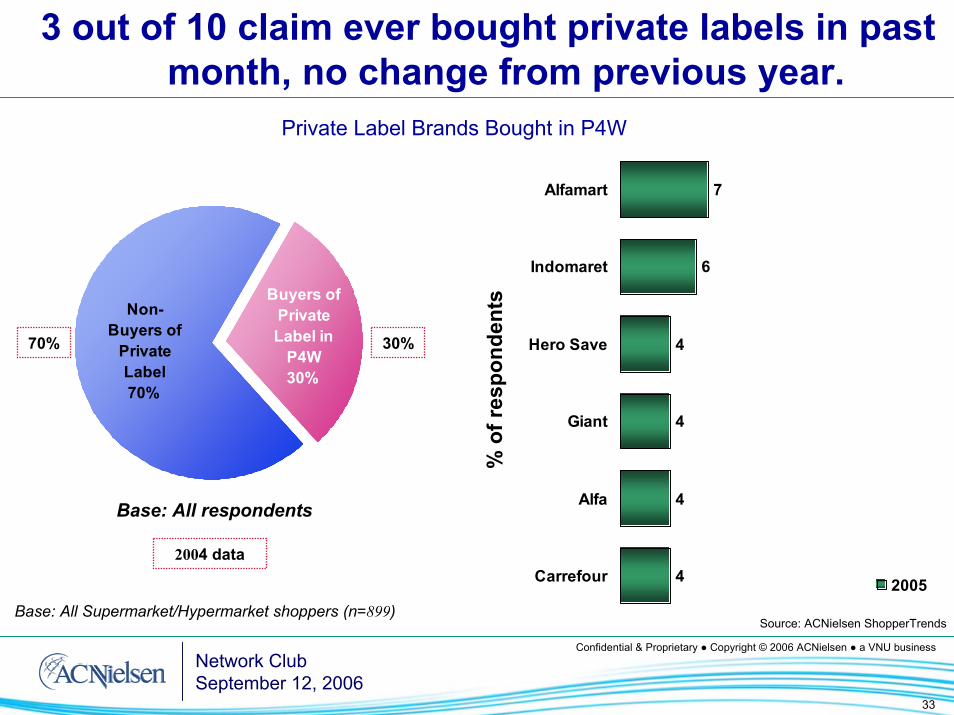

3 out of 10 claim ever bought private labels in past month, no change from previous year.

Private Label Brands Bought in P4W

7

6

4

4

4

4

Alfamart

Indomaret

Hero Save

Giant

Alfa

Carrefour 2005

Non-Buyers of

Private Label70%

Buyers of Private Label in

P4W30%

Base: All respondents%

of r

espo

nden

ts

Base: All Supermarket/Hypermarket shoppers (n=899)

2004 data

30%70%

Source: ACNielsen ShopperTrends

34

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Still flooding of new items into the market

Newly introduced SKUs based on 47 categories

2151

3328

2211

3387

2180

3453

714

1148

2,637

2,022

Food

Non Food

2002 2003 2004 2005 YTD 06Source: ACNielsen Retail Index

The Media Scene

Media ConsumptionBase Population (10+ Yrs) :

167,781,000 (National), 84,837,000 (Urban), 82,945,000 (Rural)

1

5

3

12

12

14

38

82

CabSat

Cinema

Internet

Tabloid

Magazine

Newspaper

Radio

TVIn %

12

18

16

518

617

622

3640

7590

RuralUrban

Source : Media Index, Nielsen Media Research 2005

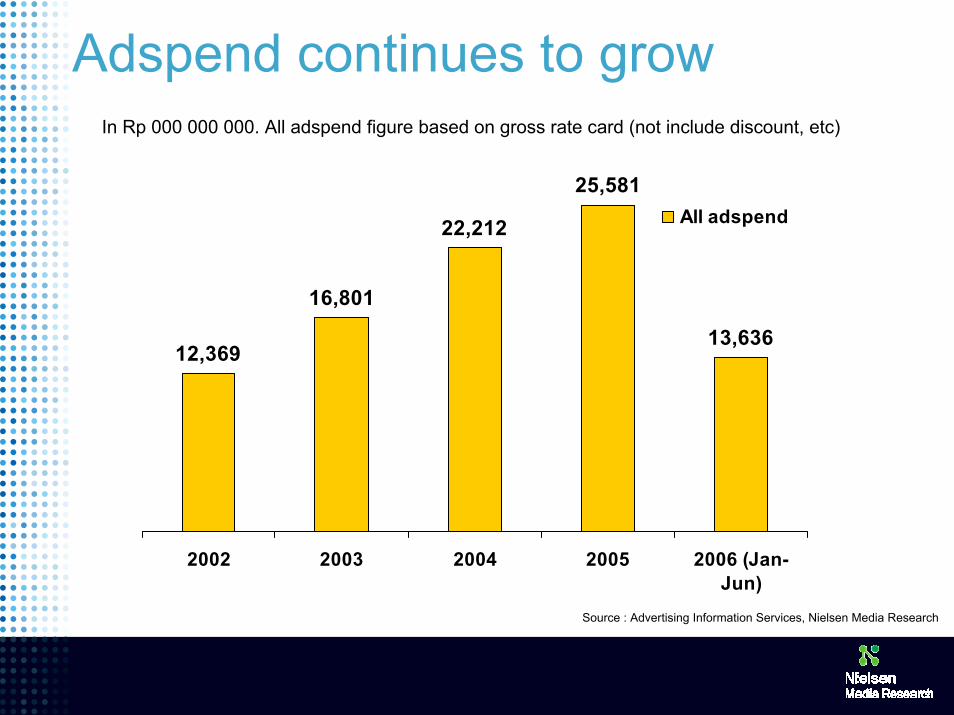

Adspend continues to grow

12,369

16,801

22,212

25,581

13,636

2002 2003 2004 2005 2006 (Jan-Jun)

All adspend

In Rp 000 000 000. All adspend figure based on gross rate card (not include discount, etc)

Source : Advertising Information Services, Nielsen Media Research

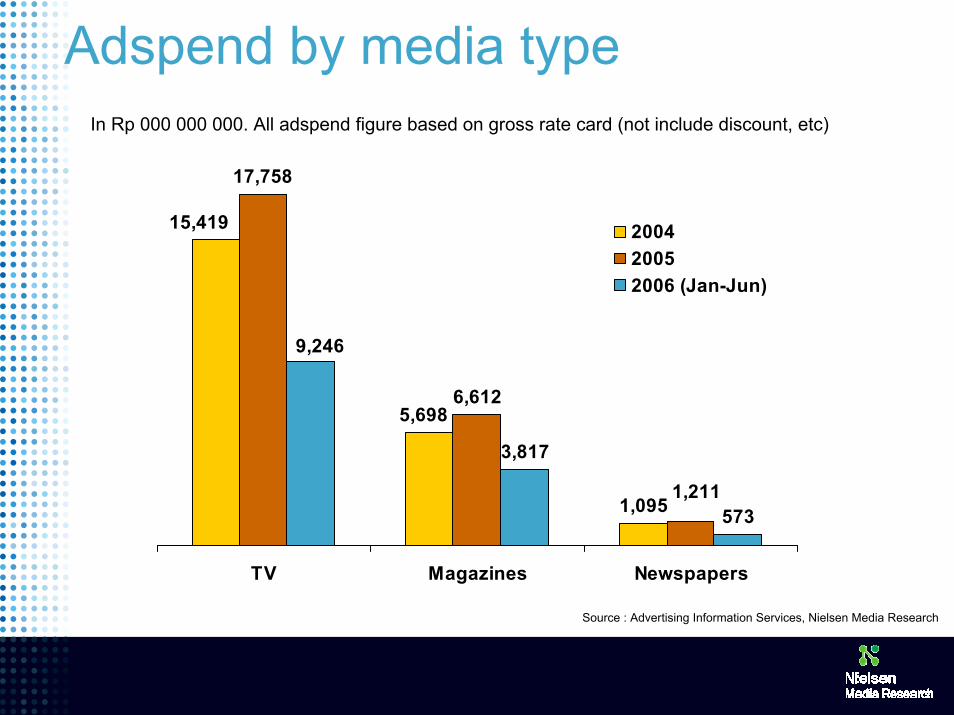

Adspend by media type

1,095

17,758

6,612

3,817

573

5,698

15,419

1,211

9,246

TV Magazines Newspapers

200420052006 (Jan-Jun)

In Rp 000 000 000. All adspend figure based on gross rate card (not include discount, etc)

Source : Advertising Information Services, Nielsen Media Research

Adspend media shareTV reaps the biggest share by far

In Rp 000 000 000. All adspend figure based on gross rate card (not include discount, etc), Jan-Jun 2006

Newspapers4%Magazines

28%

TV68%

Source : Advertising Information Services, Nielsen Media Research

40

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Consumer Attitudes

41

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Survey Method

● Interviewed over 23,300 regular Internet users

● In 42 markets worldwide

● In Indonesia we estimate Internet use at 9%, among urban people.

● These results are not for the whole population, but rather for Internet users

● It is interesting to see how Internet users in Indonesia compare to those around the World

42

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

42 Markets Worldwide

● Asia Pacific (13)– Australia (AUS)– China (CHN)– Hong Kong (HK)– India (IND)– Indonesia (INDO)– Japan (JAP)– South Korea (KOR)– Malaysia (MAL)– New Zealand (NZ)– Philippines (PH)– Singapore (SG)– Taiwan (TW)– Thailand (TH)

● Europe (20)– Austria (AT)– Belgium (BEL)– Czech Republic (CZ)– Denmark (DEN)– Finland (FIN)– France (FRA)– Germany (GER)– Greece (GRE)– Hungary (HU)– Ireland (IRE)– Italy (ITA)– Netherlands (NL)– Norway (NOR)– Poland (POL)– Portugal (POR)– Spain (SPA)– Sweden (SWE)– Switzerland (SWI)– Turkey (TR)– UK (UK)

● Latin America (4)– Argentina (ARG)– Brazil (BRA)– Chile (CHI)– Mexico (MEX)

● North America (2)– USA (US)– Canada (CAN)

● Other (3)– Russia (RUS)– South Africa (SA)– United Arab Emirates

(UAE)

43

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Markets & Sample Sizes

● Survey conducted in:Argentina 500 Hungary 500 Poland 500Australia 500 Hong Kong 500 Portugal 500Austria 500 India 500 Russia 500Belgium 500 Indonesia 500 Singapore 500Brazil 500 Ireland 500 South Africa 500Canada 500 Italy 500 Spain 500Chile 500 Japan 500 Sweden 500Chezh Republic 500 Korea, South 500 Switzerland 500China 1000 Malaysia 500 Taiwan 500Denmark 500 Mexico 500 Thailand 500Finland 500 Netherlands 500 Turkey 500France 1000 New Zealand 500 UAE 300Germany 1000 Norway 500 UK 1000Greece 500 Philippines 500 US 1000

● 13 markets in Asia Pacific: 7,000 consumers with Internet access

44Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

Fuel Prices Survey

45

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Survey Focus

● Do you have a vehicle for which you must buy fuel?

● Are the increases in the prices of fuel affecting you in any way?

● What impact, if any, has higher fuel prices had on your household’s habits?

● Interviewed over 23,500 regular Internet users

● In 42 markets worldwide

46

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Transportation contributes the most to inflation

13.9%

13.7%

13.9%

6.9%

6.1%

8.2%

44.8%

2005 Inflation

Food Stuff

Transportation, Commu-Nication, Financial Services

Prepared Food, Beverages, Cigarette & TobaccoHousing, water,Electricity, Gas, Fuel

Clothing

Medical Care

Education, Recreation, Sports

Source: Bisnis Indonesia

47

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Indonesian claimed the most affected by the fuel hike- Top 10 affected across 42 markets

37%

57% 53% 58%50%

37% 31%15%

45%

59%

39% 40% 35%42%

54% 60%

75%

44%

4% 4% 5% 7% 7% 8% 9% 9% 10% 11%

59%

37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

INDO TH PH SA HUN POR CHI TW MAL GRE

Yes, affecting me a lot Yes, affecting me somewhatNo, not affecting me

Base: All respondents

% of having a vehicle for which they must buy fuel

Source: ACNielsen Global Online Survey - 2005

48

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

63%

37%

31%

25%

16%

7%

7%

5%

1%

1%

9%

6%

Cutting down on non-essential living expenses

Using my vehicle less

Trying harder to combine errands/trips

Using public transport more

Driving in less busy (non-peak) periods

Car pooling (sharing with others)

Buying a new vehicle that is more fuel efficient

Trading in my vehicle for a motorcycle or scooter

Giving up my vehicle altogether

Trading in my vehicle for a bicycle

Using my vehicle more (less traffic)

Something elseBase: those of who own a vehicle for which they must buy fuel

Most consumers change transportation habits and non essential living cost

What impact, if any, have higher fuel prices had on your household’s habits?

Source: ACNielsen Global Online Survey - 2005

Global Average30%

44%

40%

24%

12%

10%

8%

3%

3%

3%

3%

14%

Indonesia Average

49Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

When Money Gets Tight

50

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Survey Focus

● At times when the cost of living is rising rapidly, what actions do you take in order to stay within your budget?

51

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

At times when the cost of living is rising rapidly, what actionsdo you take in order to stay within your budget?

55%

54%

47%

44%

41%

37%

31%

22%

21%

25%

Base: All respondents

Cut down on take-away meals

Cut down on out of home entertainment

Delay upgrading technology, such as pc, mobile, etc

Cut down on telephone expenses

Try to save on gas and electricity

Spend less on new clothes

Delay the replacement of major household items

Use vehicle less often

Cut out annual vacation

Switch to cheaper grocery brandsSource: ACNielsen Global Online Survey - 2005

Global Average46%

58%

52%

31%

40%

51%

336%

27%

26%

30%

Indonesia Average

52Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

Consumers and Employment

53

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Survey Focus

● Do you think the hours you work are too long…just right…?

● Compared to the past, do you think companies value staff loyalty less today?

● Do you think your job is secure?

● Have you or anyone in your immediate family been made redundant from a job in the last year?

● Do you think your government is doing enough to encourage job creation?

54

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Do you think the hours you work are:

56% 51% 52% 50% 54%

35% 33%28%

39%32%

34%

6% 7%13%

6%16% 8%

5% 4% 7% 3% 3% 4%

54%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Asia-Pacific Europe North America Latin America Other Global average

Just right Too long Not enough Don’t know/undecided

Base: those who work

55

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

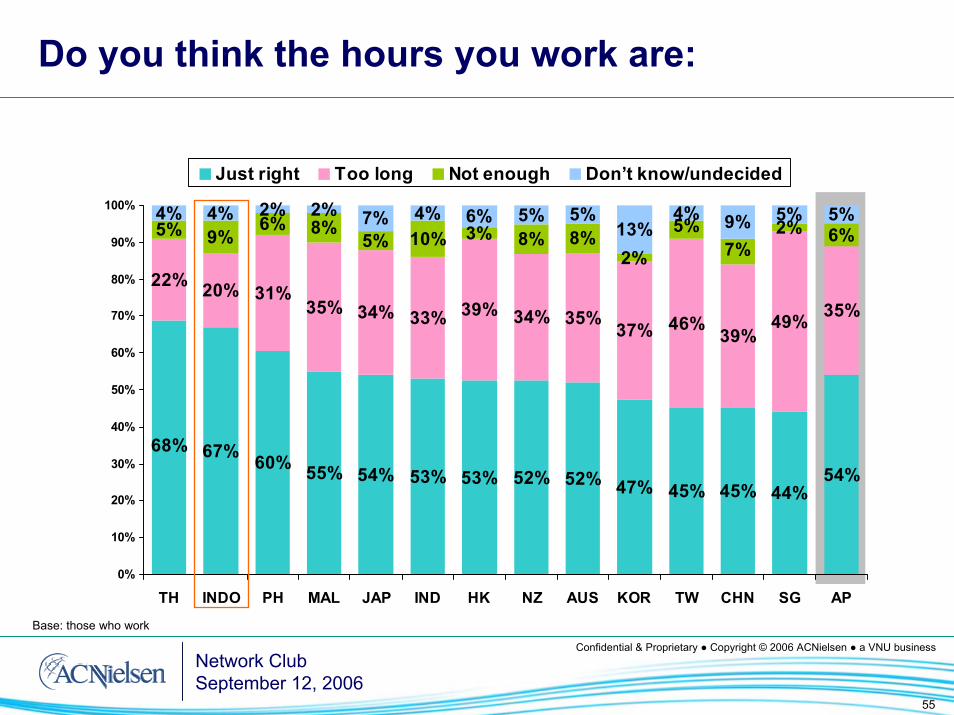

Do you think the hours you work are:

67% 60% 55% 54% 53% 53% 52% 52% 47% 45% 45% 44%54%

22% 20% 31%35% 34% 33% 39% 34% 35% 37% 46% 39%

49% 35%

5% 9%6% 8%

5% 10% 3% 8% 8%2%

2% 6%4% 4% 2% 2% 7% 4% 6% 5% 5%

13%4% 9% 5% 5%

68%

5%7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TH INDO PH MAL JAP IND HK NZ AUS KOR TW CHN SG AP

Just right Too long Not enough Don’t know/undecided

Base: those who work

56

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

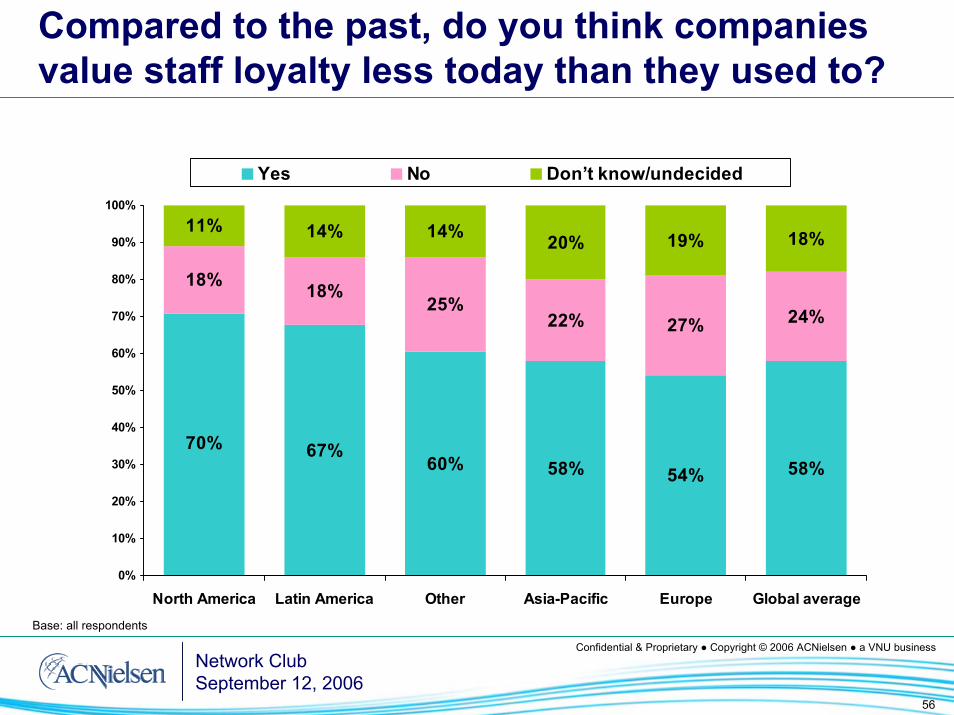

Compared to the past, do you think companies value staff loyalty less today than they used to?

67%60% 58% 54% 58%

18% 18%25%

22% 27% 24%

11% 14% 14% 20% 19% 18%

70%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

North America Latin America Other Asia-Pacific Europe Global average

Yes No Don’t know/undecided

Base: all respondents

57

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Compared to the past, do you think companies value staff loyalty less today than they used to?

71% 69% 66% 62% 59% 59% 56% 49% 49% 47% 46% 44%58%

15% 15% 18% 21% 26%

13%28% 27%

12%26% 26% 22%

40%22%

12% 14% 12% 12% 12%27%

14% 17%

38%26%

17% 20%

73%

27% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AUS SG NZ MAL IND KOR PH TW JAP HK TH CHN INDO AP

Yes No Don’t know/undecided

Base: all respondents

58

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

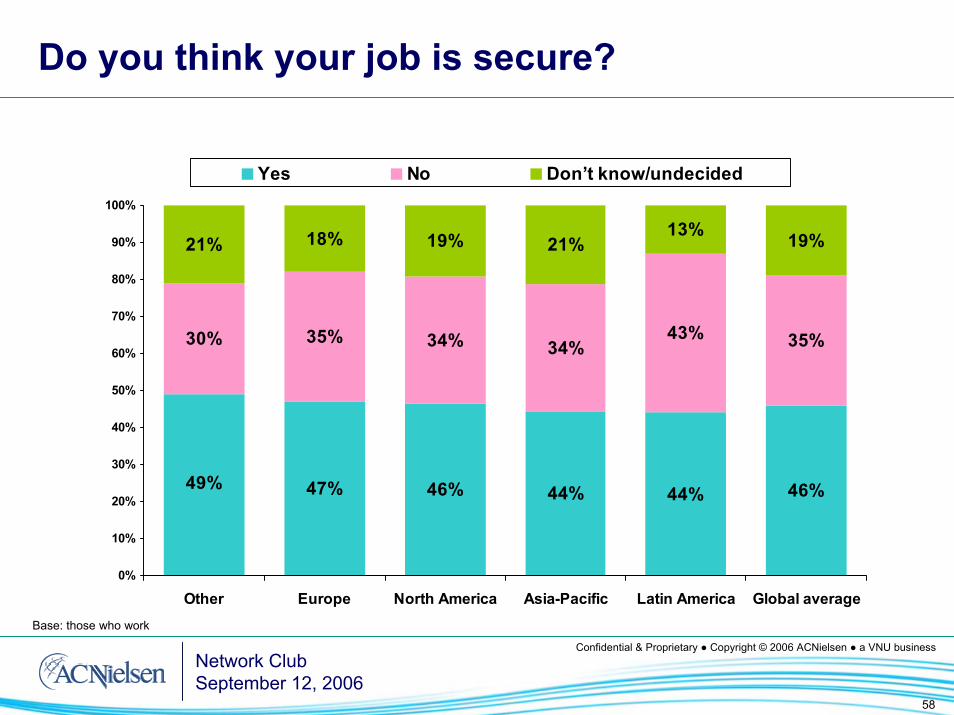

Do you think your job is secure?

47% 46% 44% 44% 46%

30% 35% 34% 34%43% 35%

21% 18% 19% 21%13% 19%

49%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other Europe North America Asia-Pacific Latin America Global average

Yes No Don’t know/undecided

Base: those who work

59

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Do you think your job is secure?

61% 57% 51% 49% 47% 43% 41% 40% 37% 34% 29% 23%

44%

19% 24%23% 28% 33% 33%

33% 36% 39% 45%39% 44%

47%

34%

14% 15% 20% 20% 18% 20% 24% 22% 21% 17%31%

21%

67%

27% 27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NZ HK AUS TH JAP IND CHN MAL INDO PH SG TW KOR AP

Yes No Don’t know/undecided

Base: those who work

60

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

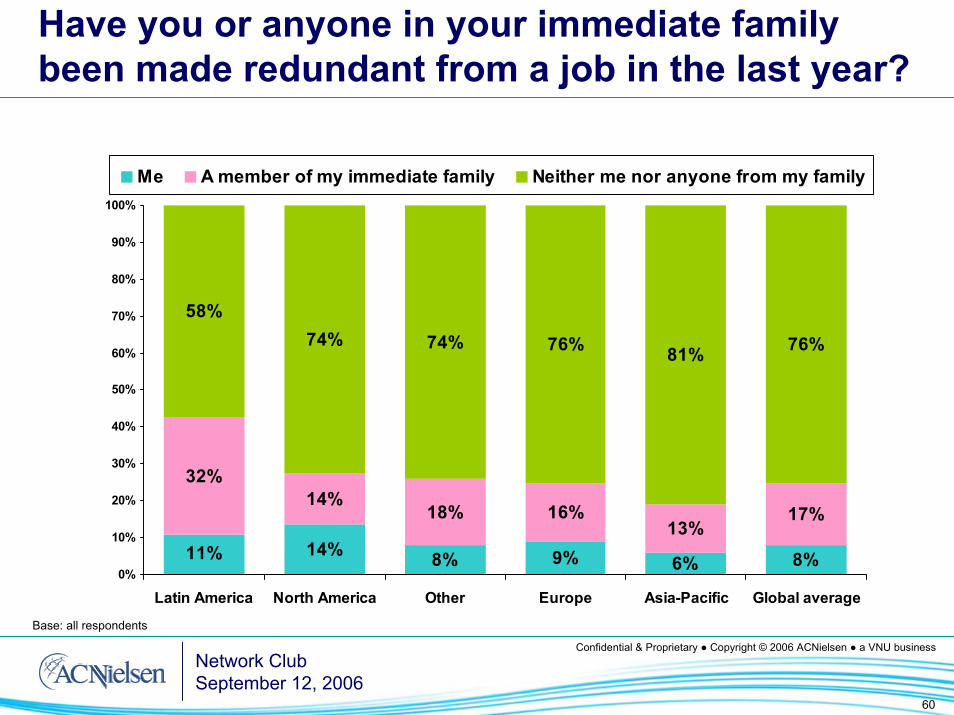

Have you or anyone in your immediate family been made redundant from a job in the last year?

14% 8% 9% 6% 8%

32%14%

18% 16%13%

17%

58%74% 74% 76% 81% 76%

11%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Latin America North America Other Europe Asia-Pacific Global average

Me A member of my immediate family Neither me nor anyone from my family

Base: all respondents

61

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

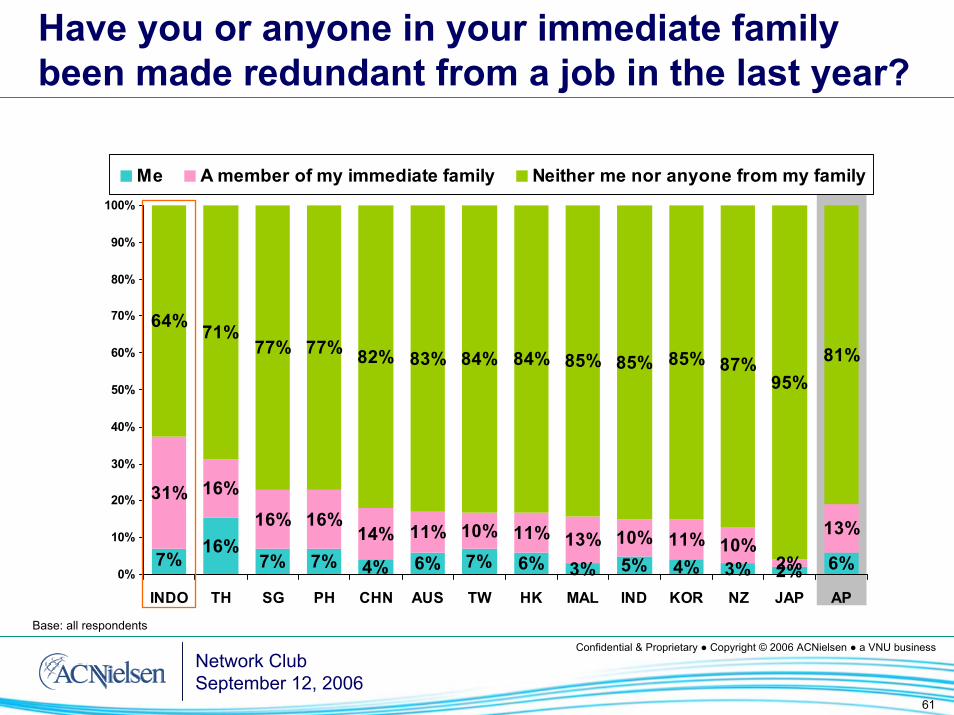

Have you or anyone in your immediate family been made redundant from a job in the last year?

16%7% 7% 4% 6% 7% 6% 3% 5% 4% 3% 2% 6%

31% 16%

16% 16%14% 11% 10% 11% 13% 10% 11% 10%

2%

13%

64% 71%77% 77% 82% 83% 84% 84% 85% 85%

95%81%

7%

85% 87%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

INDO TH SG PH CHN AUS TW HK MAL IND KOR NZ JAP AP

Me A member of my immediate family Neither me nor anyone from my family

Base: all respondents

62Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

Consumers and Designer Brands

63

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

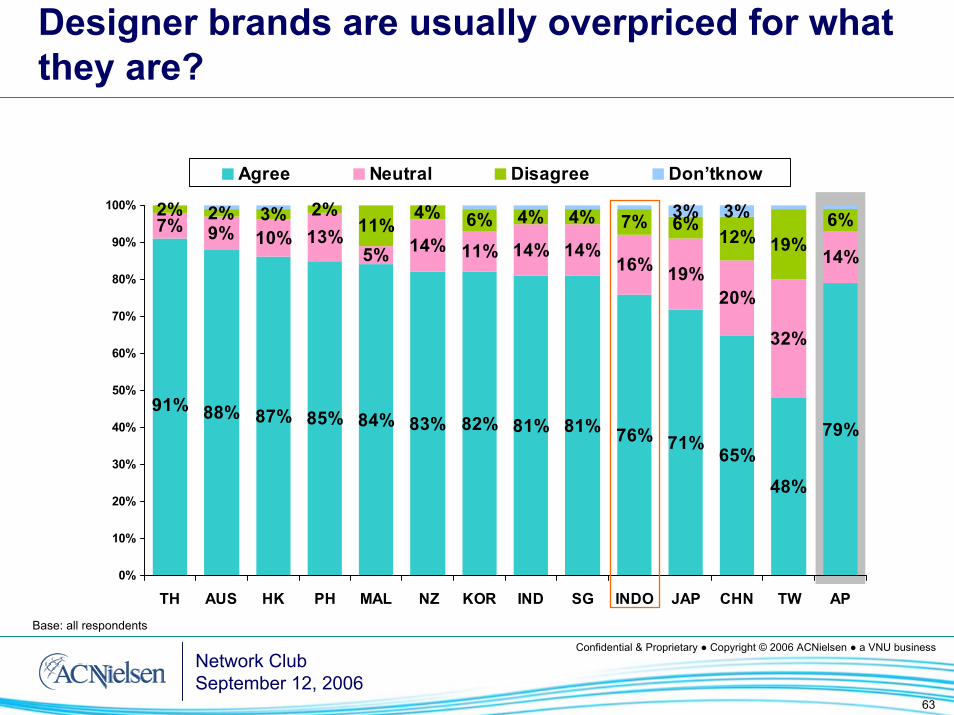

Designer brands are usually overpriced for what they are?

88% 87% 85% 84% 83% 82% 81% 81% 76% 71% 65%

48%

79%

7% 9% 10% 13%5% 14% 11% 14% 14%

16% 19%20%

32%

14%

2% 2% 3% 2%11%

4% 6% 4% 4% 7%19%

6%3% 3%

91%

6%12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TH AUS HK PH MAL NZ KOR IND SG INDO JAP CHN TW AP

Agree Neutral Disagree Don’tknow

Base: all respondents

64

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

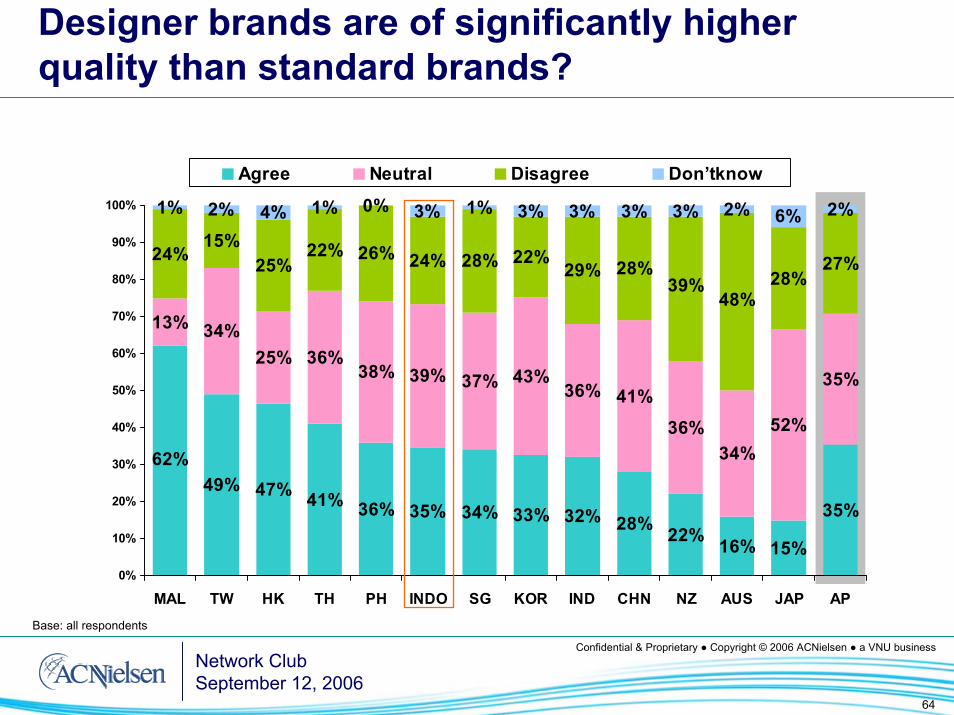

Designer brands are of significantly higher quality than standard brands?

49% 47% 41% 36% 35% 34% 33% 32% 28% 22% 16% 15%

35%

13% 34%25% 36%

38% 39% 37% 43%36% 41%

36%34%

52%

35%

24%15%

25%22% 26% 24% 28% 22%

29% 28% 28%27%

3% 2%

62%

39%48%

6% 2%3%1% 3% 3%4% 3%0%1%2%1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MAL TW HK TH PH INDO SG KOR IND CHN NZ AUS JAP AP

Agree Neutral Disagree Don’tknow

Base: all respondents

65

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Imitation designer brands are just as good as the real ones?

24%17% 17% 15% 15% 12% 12% 10% 9% 8% 6% 3%

14%

36%34%

35% 35%31% 33% 34%

18%

40%

20%

41%

23% 25%

31%

30%36% 44% 45%

46%50% 48%

60%

44%

67%62%

50%

6% 5%

29%

46%

66%

10% 6%4%6% 10% 6%5% 2%8%4%6%4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AUS NZ SG TH IND PH KOR HK INDO MAL CHN TW JAP AP

Agree Neutral Disagree Don’tknow

Base: all respondents

66

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Best male celebrities to endorse sports wear?Indonesia

50%

37%

12%

8%

6%

4%

David Beckham

Tiger Woods

Jackie Chan

Brad Pitt

Ashton Kutcher

Tom Cruise

Base: All respondents Source: ACNielsen Global Online Survey - 2005

67

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Best female celebrities to endorse provocative fashion? Indonesia

35%

27%

15%

12%

10%

8%

Angelina Jolie

Jennifer Lopez

Kylie Minogue

Penelope Cruz

Jessica Simpson

Nicole Kidman

Base: All respondents Source: ACNielsen Global Online Survey - 2005

68

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

And now for something completely different

69Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU business

ACNielsen IndonesiaWorld Cup Survey

Which team do people want to win?Which player is the favorite?Amongst 300 Jakarta respondents

June 2006

Highest viewing is during Grand Final

9 June – 10 July 2006, 9 Cities, All time, WC match only, in ‘000 audience

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

First Round SecondRound

QuarterFinals

Semifinals Final 3/4 Grand Final

Source: AGB NMR Television Audience Measurement

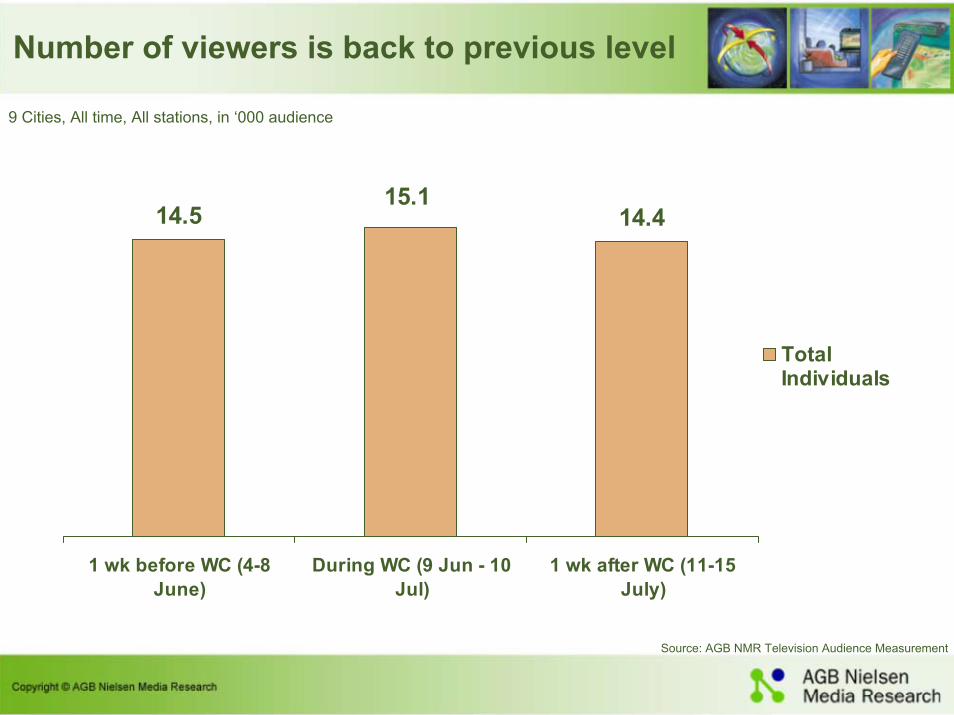

Number of viewers is back to previous level

9 Cities, All time, All stations, in ‘000 audience

14.5 14.415.1

1 wk before WC (4-8June)

During WC (9 Jun - 10Jul)

1 wk after WC (11-15July)

TotalIndividuals

Source: AGB NMR Television Audience Measurement

72

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

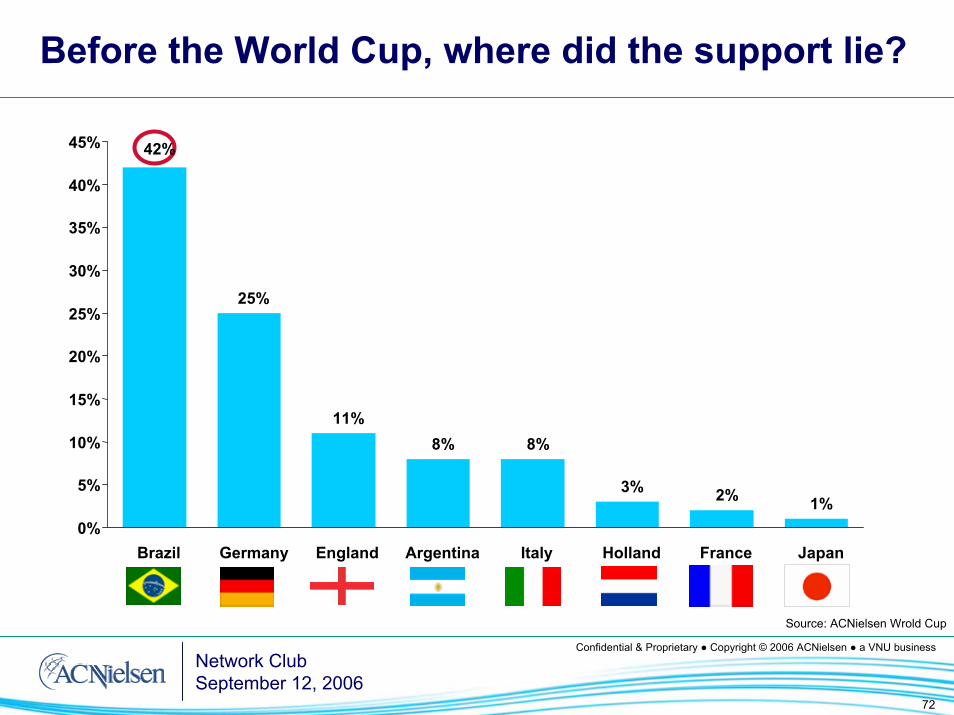

Before the World Cup, where did the support lie?

42%45%

40%

35%

30%25%

25%

20%

15%11%

8% 8%10%

3%5% 2% 1%0%

Brazil Germany England Argentina Italy Holland France Japan

Source: ACNielsen Wrold Cup

73

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

How different the support between males and females?

42%

25%

11%8% 8%

3% 2% 1%

45%

11%

3%1%

39%

30%

16%

5% 4% 5%

1% 0%2%

10%7%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Brazil Germany England Argentina Italy Holland France Japan

Total Males Females

Source: ACNielsen Wrold Cup

74

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

Who’s the pick of the ladies?

23%

8%

1%

33%

11%

4%

3%

24%

MalesFemales

37%

12%

3%

1%Source: ACNielsen Wrold Cup

David Beckham

Ronaldo

Ronaldinho

MichaelBallack

MichaelOwen

ZinedineZidane

75

Confidential & Proprietary ● Copyright © 2006 ACNielsen ● a VNU businessNetwork ClubSeptember 12, 2006

In Summary

● Indonesian consumers have tightened their belts by slowing down on items such as cars, motorcycles whilst FMCG products have surged

●Adspend for all media segments is on the increase●As elsewhere in Asia, the modern trade continues to

flourish and drive volumes. There are now almost eighty hypermarkets across Indonesia

●New products/variants/SKUs continue to flood the market at around 5000 per year and most importantly….

●Will David Beckham continue to be the superstar?