35

INDONESIA’S NON INDONESIA’S NON-BANK BANK ERIC SUGANDI ECONOMIST GLOBAL RESEARCH AUGUST 2011 K FINANCE INSTITUTIONS K FINANCE INSTITUTIONS

INDONESIA’S NONINDONESIA’S NON--BANK FINANCE INSTITUTIONSBANK FINANCE INSTITUTIONS

ERIC SUGANDIECONOMIST

GLOBAL RESEARCH

AUGUST 2011

BANK FINANCE INSTITUTIONSBANK FINANCE INSTITUTIONS

KEY DRIVERS OF GROWTHKEY DRIVERS OF GROWTHKEY DRIVERS OF GROWTHKEY DRIVERS OF GROWTH

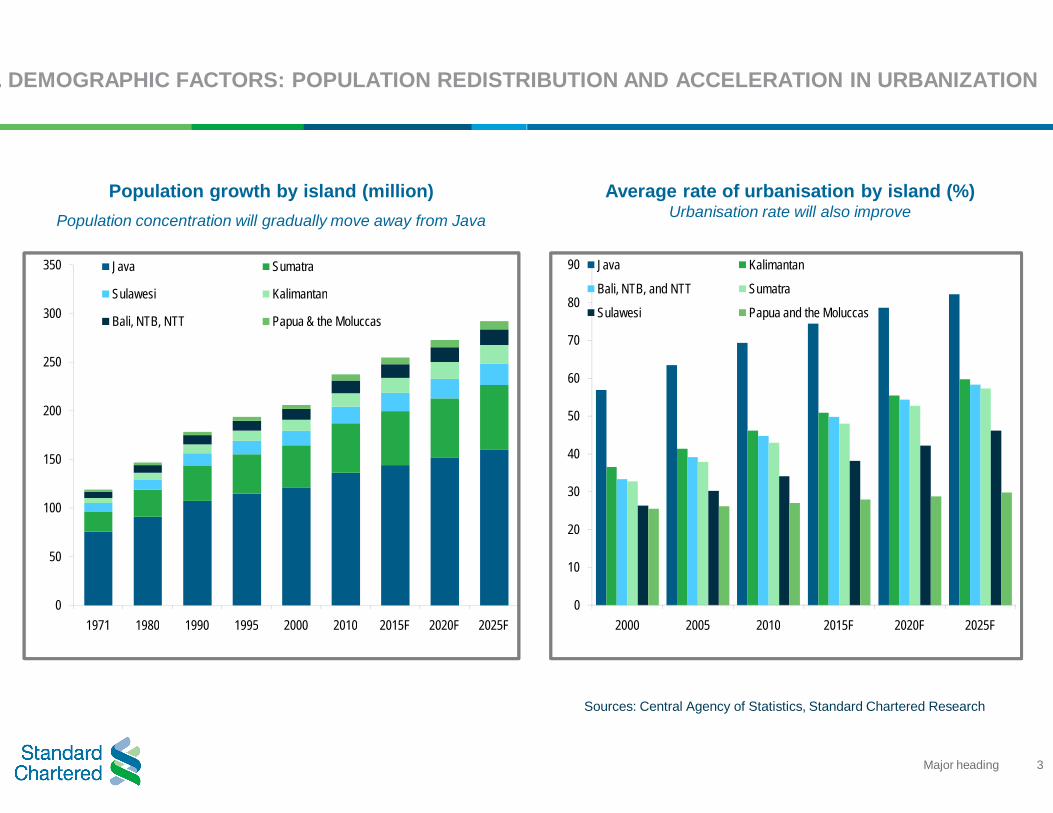

1. DEMOGRAPHIC FACTORS: POPULATION REDISTRIBUTION AND ACCELERATION IN URBANIZATION

0

50

100

150

200

250

300

350

1971 1980 1990 1995 2000 2010 2015F 2020F 2025F

Java Sumatra

Sulawesi Kalimantan

Bali, NTB, NTT Papua & the Moluccas

Population growth by island (million)Population concentration will gradually move away from Java

3Major heading

1. DEMOGRAPHIC FACTORS: POPULATION REDISTRIBUTION AND ACCELERATION IN URBANIZATION

Sources: Central Agency of Statistics, Standard Chartered Research

0

10

20

30

40

50

60

70

80

90

2000 2005 2010 2015F 2020F 2025F

Java Kalimantan

Bali, NTB, and NTT Sumatra

Sulawesi Papua and the Moluccas

Average rate of urbanisation by island (%) Urbanisation rate will also improve

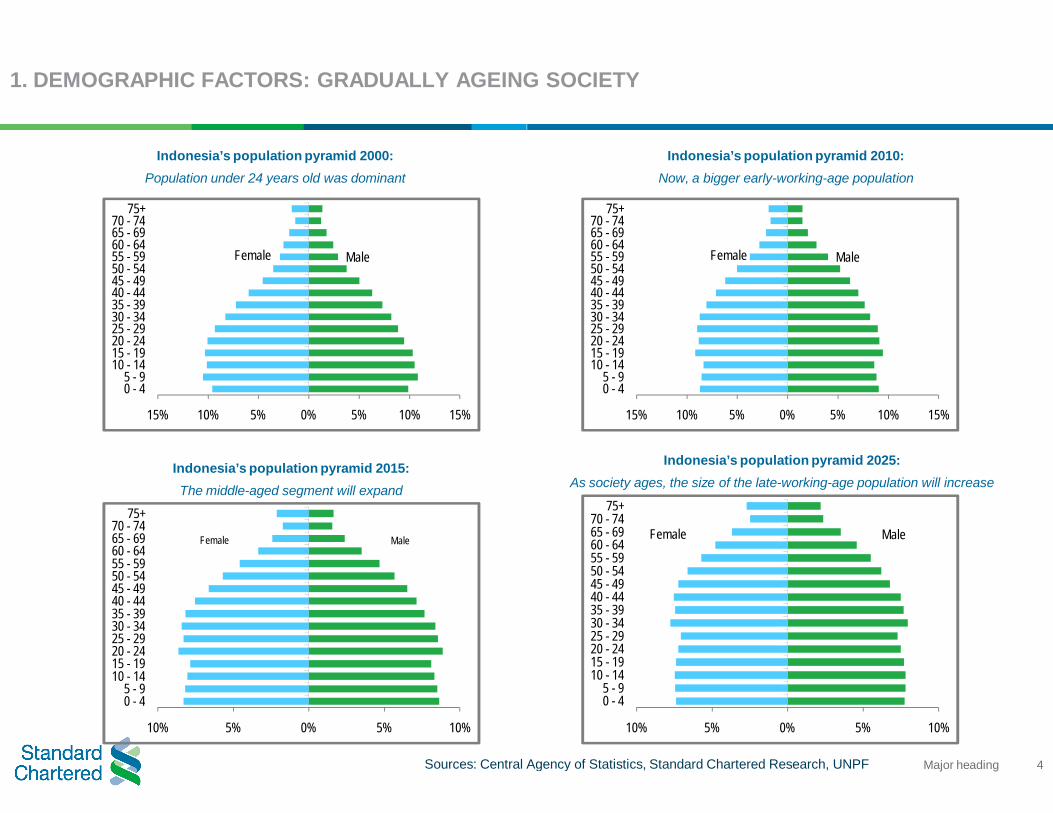

1. DEMOGRAPHIC FACTORS: GRADUALLY AGEING SOCIETY

Sources: Central Agency of Statistics,

Female Male

15% 10% 5% 0% 5% 10% 15%

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 74

75+

Female Male

10% 5% 0% 5% 10%

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 74

75+

Indonesia’s population pyramid 2000:Population under 24 years old was dominant

Indonesia’s population pyramid 2015:The middle-aged segment will expand

4Major heading

1. DEMOGRAPHIC FACTORS: GRADUALLY AGEING SOCIETY

Central Agency of Statistics, Standard Chartered Research, UNPF

Female Male

15% 10% 5% 0% 5% 10% 15%

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 74

75+

Female Male

10% 5% 0% 5% 10%

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 74

75+

Indonesia’s population pyramid 2010:Now, a bigger early-working-age population

Indonesia’s population pyramid 2025:As society ages, the size of the late-working-age population will increase

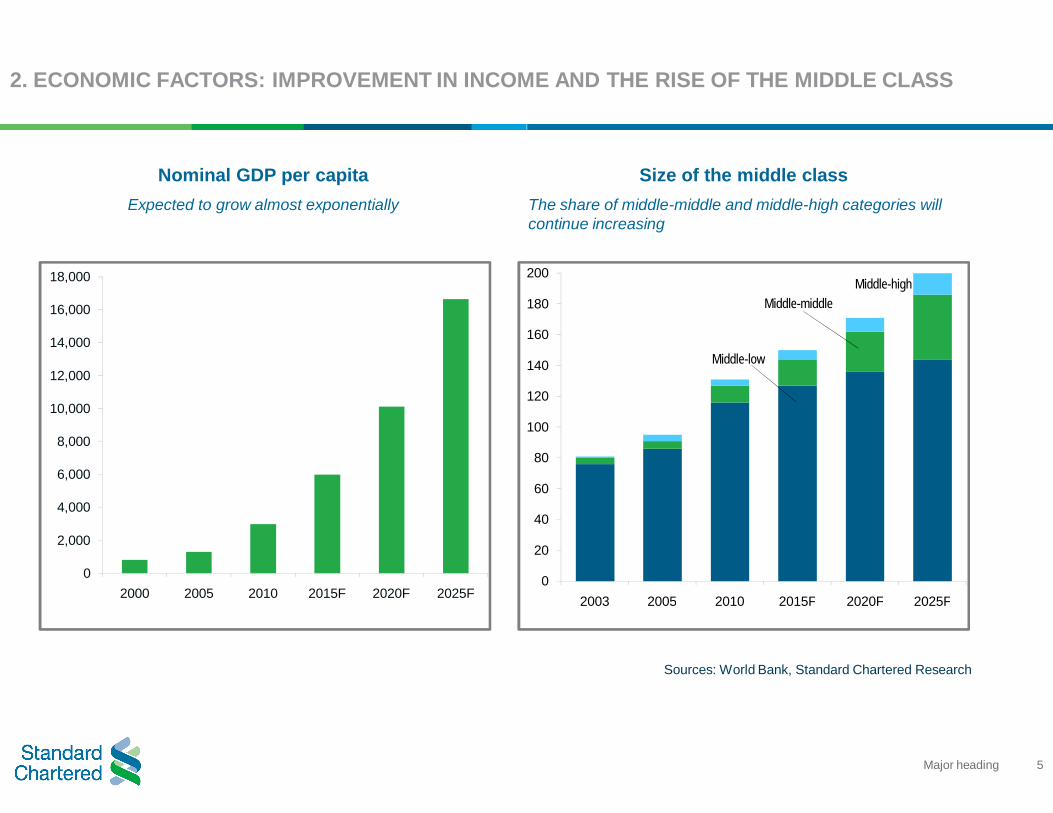

2. ECONOMIC FACTORS: IMPROVEMENT IN INCOME AND THE RISE OF THE MIDDLE CLASS

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2000 2005 2010 2015F 2020F 2025F

Nominal GDP per capitaExpected to grow almost exponentially

5Major heading

2. ECONOMIC FACTORS: IMPROVEMENT IN INCOME AND THE RISE OF THE MIDDLE CLASS

Sources: World Bank, Standard Chartered Research

Middle-low

Middle-middleMiddle-high

0

20

40

60

80

100

120

140

160

180

200

2003 2005 2010 2015F 2020F 2025F

Size of the middle classThe share of middle-middle and middle-high categories will continue increasing

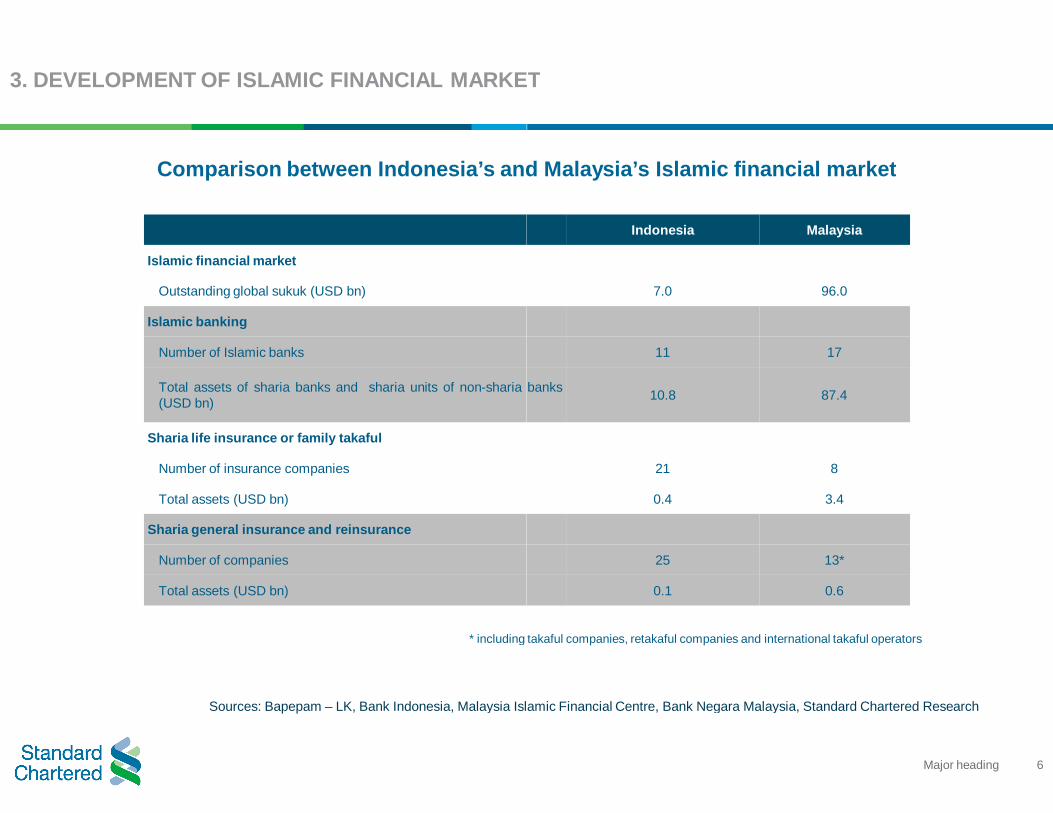

3. DEVELOPMENT OF ISLAMIC FINANCIAL MARKET

Islamic financial market

Outstanding global sukuk (USD bn)

Islamic banking

Number of Islamic banks

Total assets of sharia banks and sharia units of non-sharia(USD bn)

Sharia life insurance or family takaful

Number of insurance companies

Total assets (USD bn)

Sharia general insurance and reinsurance

Number of companies

Total assets (USD bn)

* including

Comparison between Indonesia’s and Malaysia’s Islamic financial market

Sources: Bapepam – LK, Bank Indonesia, Malaysia Islamic Financial Centre, Bank Negara Malaysia, Standard Chartered Research

6Major heading

3. DEVELOPMENT OF ISLAMIC FINANCIAL MARKET

Indonesia Malaysia

7.0 96.0

11 17

banks 10.8 87.4

21 8

0.4 3.4

25 13*

0.1 0.6

* including takaful companies, retakaful companies and international takaful operators

Comparison between Indonesia’s and Malaysia’s Islamic financial market

LK, Bank Indonesia, Malaysia Islamic Financial Centre, Bank Negara Malaysia, Standard Chartered Research

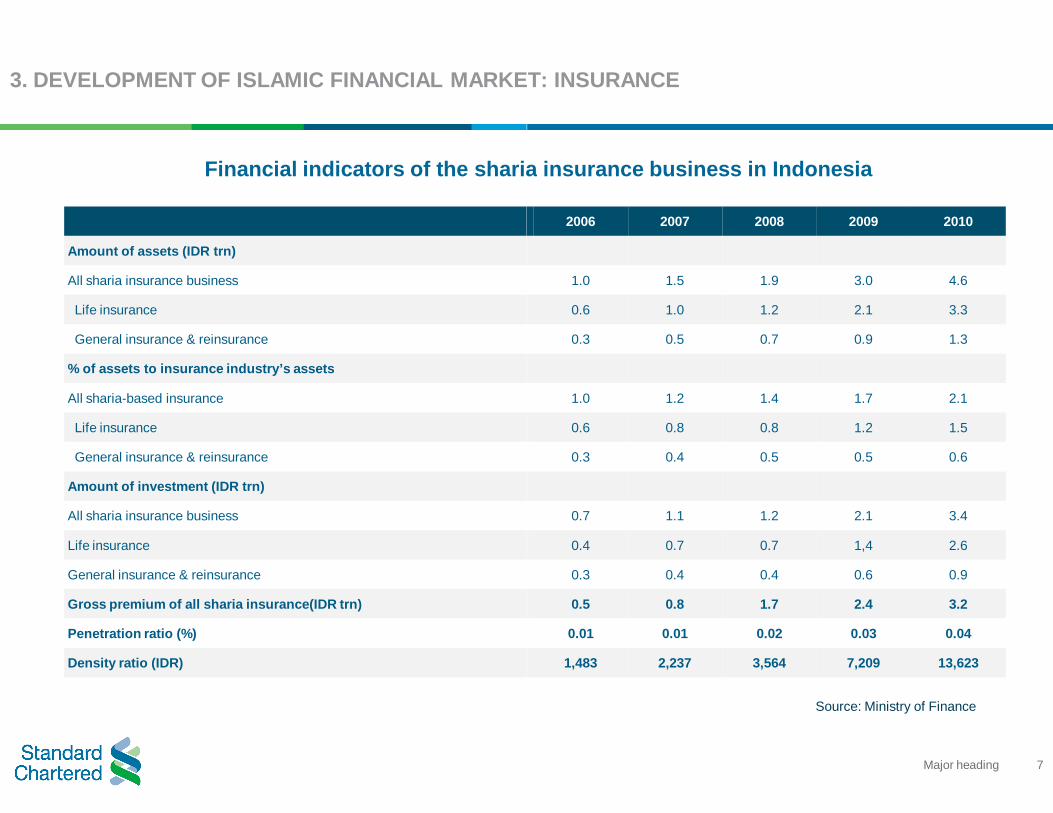

3. DEVELOPMENT OF ISLAMIC FINANCIAL MARKET: INSURANCE

Amount of assets (IDR trn)

All sharia insurance business

Life insurance

General insurance & reinsurance

% of assets to insurance industry’s assets

All sharia-based insurance

Life insurance

General insurance & reinsurance

Amount of investment (IDR trn)

All sharia insurance business

Life insurance

General insurance & reinsurance

Gross premium of all sharia insurance(IDR trn)

Penetration ratio (%)

Density ratio (IDR)

Financial indicators of the sharia

7Major heading

3. DEVELOPMENT OF ISLAMIC FINANCIAL MARKET: INSURANCE

2006 2007 2008 2009 2010

1.0 1.5 1.9 3.0 4.6

0.6 1.0 1.2 2.1 3.3

0.3 0.5 0.7 0.9 1.3

1.0 1.2 1.4 1.7 2.1

0.6 0.8 0.8 1.2 1.5

0.3 0.4 0.5 0.5 0.6

0.7 1.1 1.2 2.1 3.4

0.4 0.7 0.7 1,4 2.6

0.3 0.4 0.4 0.6 0.9

0.5 0.8 1.7 2.4 3.2

0.01 0.01 0.02 0.03 0.04

1,483 2,237 3,564 7,209 13,623

Source: Ministry of Finance

sharia insurance business in Indonesia

3. DEVELOPMENT OF ISLAMIC FINANCE: FINANCE COMPANIES

Sharia financing assets

Non-sharia financing assets

0

500

1,000

1,500

2,000

2,500

2008 2009 2010

Assets of Indonesia’s sharia-based finance companies Mostly in the form of sharia-financing receivables

8Major heading

3. DEVELOPMENT OF ISLAMIC FINANCE: FINANCE COMPANIES

Murabahah

Ijarah muntahiyyah

bittamlik

Wakalah bil ujrah & Ijarah

0

500

1,000

1,500

2,000

2,500

2008 2009 2010

based finance companies Receivables of Indonesia’s sharia-based finance companies Murabahah financing generates revenues the most

Source: Ministry of Finance

4. INFRASTRUCTURE DEVELOPMENT AND SOCIAL SECURITY NET

INFRASTRUCTURE DEVELOPMENT

1. Rapid infrastructure development could lead

2. Infrastructure development will acceleratehouseholds’ purchasing power

3. Transport infrastructure development enhancesmarket segments to decentralise

SOCIAL SECURITY NET

1. Health protection

2. Protection against work accidents

3. Annuity provisions

4. Pension funds

5. Life insurance

9Major heading

4. INFRASTRUCTURE DEVELOPMENT AND SOCIAL SECURITY NET

Source: Ministry of Finance

lead to more NBFI financing

accelerate economic development and improve

enhances labour mobility, thus allowing NBFI

NBFI BUSINESSESNBFI BUSINESSESNBFI BUSINESSESNBFI BUSINESSES

INSURANCEINSURANCEINSURANCEINSURANCE

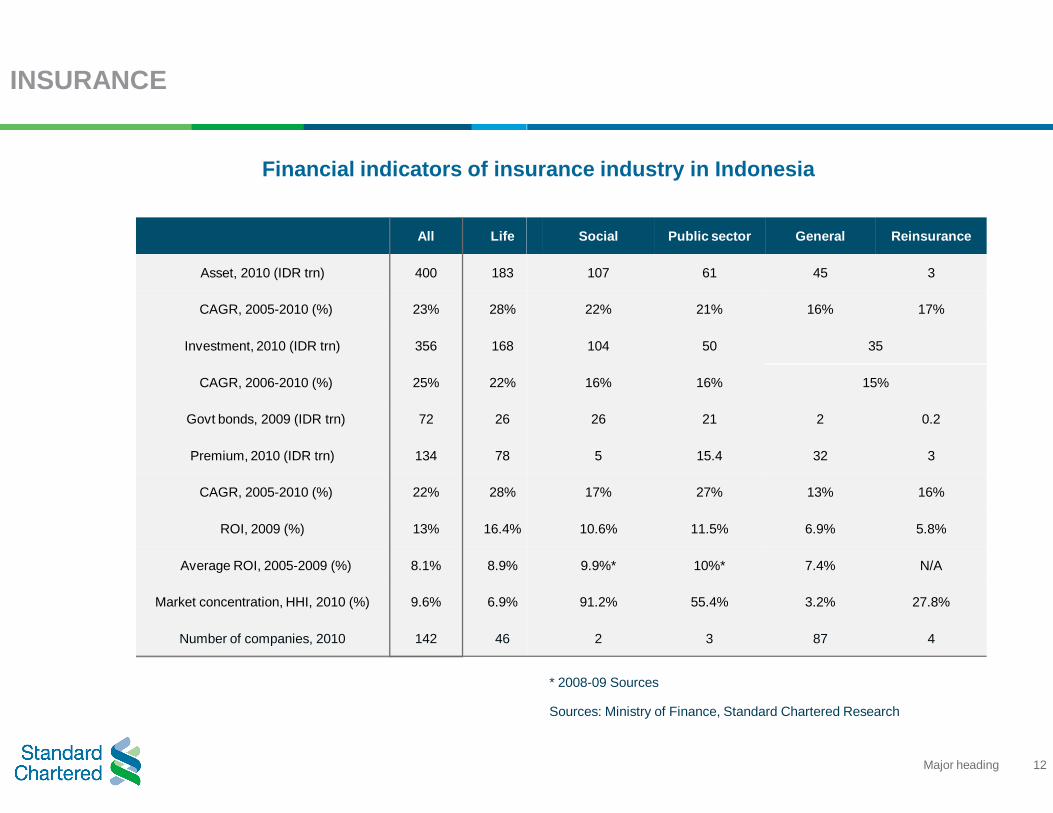

INSURANCE

All Life

Asset, 2010 (IDR trn) 400 183

CAGR, 2005-2010 (%) 23% 28%

Investment, 2010 (IDR trn) 356 168

CAGR, 2006-2010 (%) 25% 22%

Govt bonds, 2009 (IDR trn) 72 26

Premium, 2010 (IDR trn) 134 78

CAGR, 2005-2010 (%) 22% 28%

ROI, 2009 (%) 13% 16.4%

Average ROI, 2005-2009 (%) 8.1% 8.9%

Market concentration, HHI, 2010 (%) 9.6% 6.9%

Number of companies, 2010 142 46

Financial indicators of insurance industry in Indonesia

12Major heading

* 2008-09 Sources

Social Public sector General Reinsurance

107 61 45 3

22% 21% 16% 17%

104 50 35

16% 16% 15%

26 21 2 0.2

5 15.4 32 3

17% 27% 13% 16%

10.6% 11.5% 6.9% 5.8%

9.9%* 10%* 7.4% N/A

91.2% 55.4% 3.2% 27.8%

2 3 87 4

Financial indicators of insurance industry in Indonesia

Sources: Ministry of Finance, Standard Chartered Research

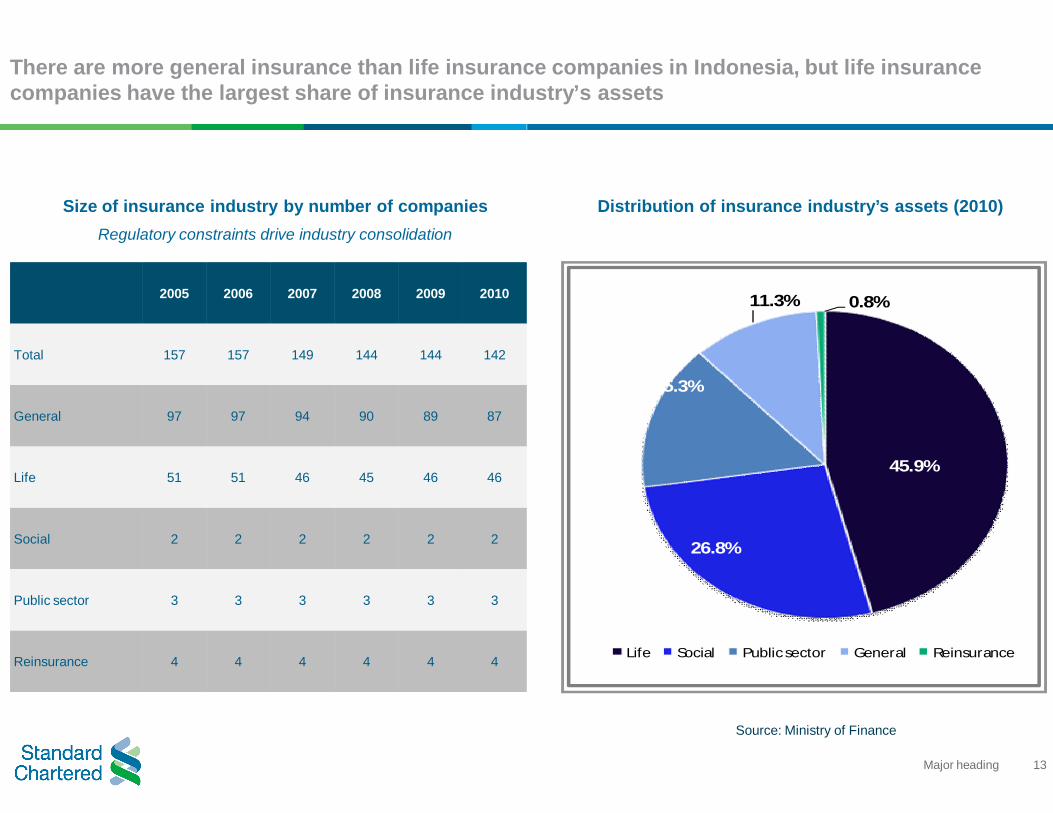

There are more general insurance than life insurance companies in Indonesia, but life insurance companies have the largest share of insurance industry’s assets

2005 2006 2007 2008 2009 2010

Total 157 157 149 144 144 142

General 97 97 94 90 89 87

Life 51 51 46 45 46 46

Social 2 2 2 2 2 2

Public sector 3 3 3 3 3 3

Reinsurance 4 4 4 4 4 4

Size of insurance industry by number of companiesRegulatory constraints drive industry consolidation

13Major heading

There are more general insurance than life insurance companies in Indonesia, but life insurance companies have the largest share of insurance industry’s assets

Source: Ministry of Finance

45.9%

26.8%

15.3%

11.3% 0.8%

Life Social Public sector General Reinsurance

Distribution of insurance industry’s assets (2010)

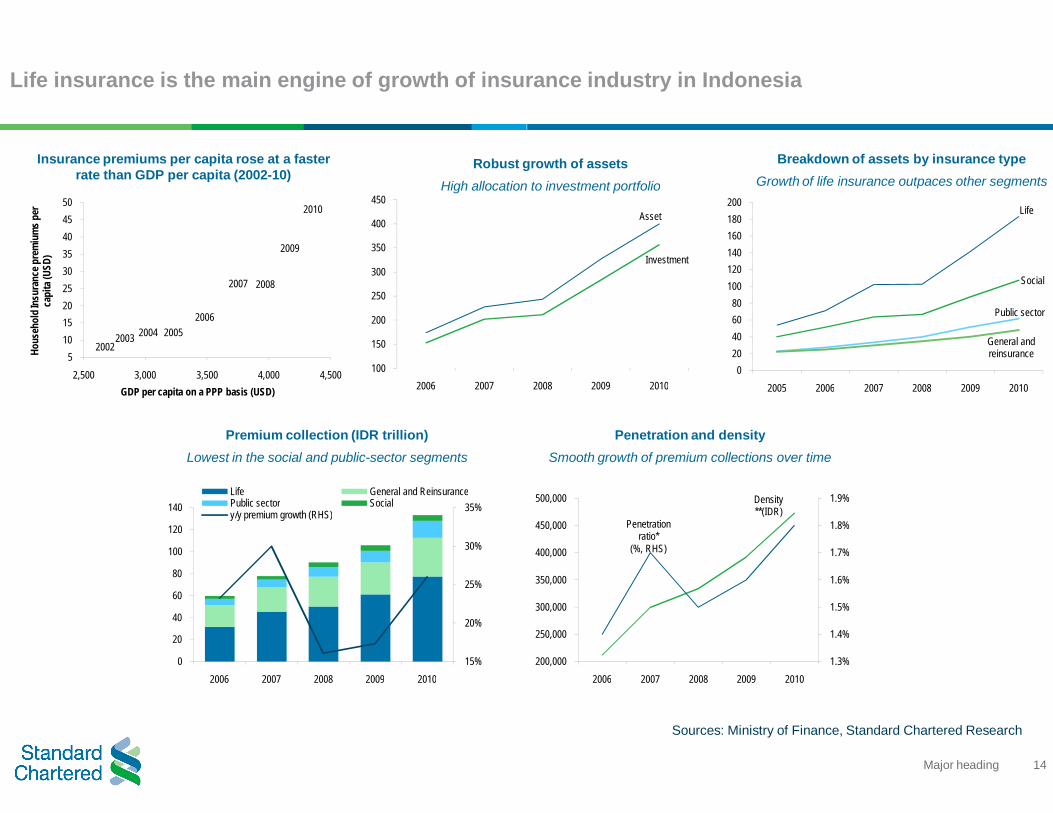

Life insurance is the main engine of growth of insurance industry in Indonesia

20022003 2004 2005

2006

2007 2008

2009

2010

5101520253035404550

2,500 3,000 3,500 4,000 4,500

Hous

ehol

d Ins

uran

ce p

rem

ium

s per

ca

pita

(USD

)

GDP per capita on a PPP basis (USD)

100

150

200

250

300

350

400

450

2006 2007

15%

20%

25%

30%

35%

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010

Life General and ReinsurancePublic sector Socialy/y premium growth (RHS)

Insurance premiums per capita rose at a faster rate than GDP per capita (2002-10)

Robust growth of assetsHigh allocation to investment portfolio

Premium collection (IDR trillion)Lowest in the social and public-sector segments

14Major heading

Life insurance is the main engine of growth of insurance industry in Indonesia

Sources: Ministry of Finance, Standard Chartered Research

Asset

Investment

2008 2009 2010

Life

Social

Public sector

General and reinsurance

020406080

100120140160180200

2005 2006 2007 2008 2009 2010

Robust growth of assetsHigh allocation to investment portfolio

Breakdown of assets by insurance typeGrowth of life insurance outpaces other segments

Density **(IDR)

Penetration ratio*

(%, RHS)

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

1.9%

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2006 2007 2008 2009 2010

Penetration and densitySmooth growth of premium collections over time

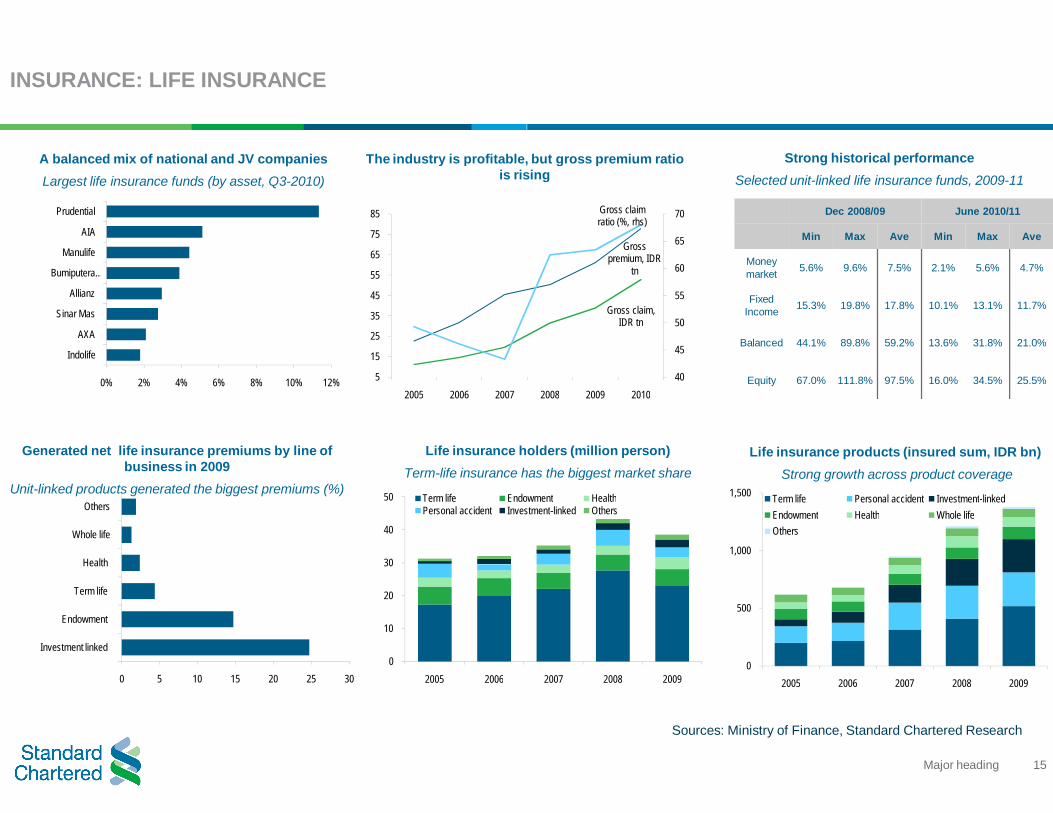

INSURANCE: LIFE INSURANCE

0% 2% 4% 6% 8% 10% 12%

Indolife

AXA

Sinar Mas

Allianz

Bumiputera …

Manulife

AIA

Prudential

5

15

25

35

45

55

65

75

85

2005 2006 2007

0 5 10 15 20 25 30

Investment linked

Endowment

Term life

Health

Whole life

Others

0

10

20

30

40

50

2005 2006

Term life EndowmentPersonal accident Investment

A balanced mix of national and JV companiesLargest life insurance funds (by asset, Q3-2010)

The industry is profitable, but gross premium ratio is rising

Generated net life insurance premiums by line of business in 2009

Unit-linked products generated the biggest premiums (%)

Life insurance holders (million person)Term-life insurance has the biggest market share

15Major heading

Sources: Ministry of Finance, Standard Chartered Research

Gross premium, IDR

tn

Gross claim, IDR tn

Gross claim ratio (%, rhs)

40

45

50

55

60

65

70

2008 2009 2010

2007 2008 2009

Endowment HealthInvestment-linked Others

Dec 2008/09 June 2010/11

Min Max Ave Min Max Ave

Money market 5.6% 9.6% 7.5% 2.1% 5.6% 4.7%

Fixed Income 15.3% 19.8% 17.8% 10.1% 13.1% 11.7%

Balanced 44.1% 89.8% 59.2% 13.6% 31.8% 21.0%

Equity 67.0% 111.8% 97.5% 16.0% 34.5% 25.5%

0

500

1,000

1,500

2005 2006 2007 2008 2009

Term life Personal accident Investment-linkedEndowment Health Whole lifeOthers

The industry is profitable, but gross premium ratio is rising

Strong historical performanceSelected unit-linked life insurance funds, 2009-11

Life insurance holders (million person)life insurance has the biggest market share

Life insurance products (insured sum, IDR bn)Strong growth across product coverage

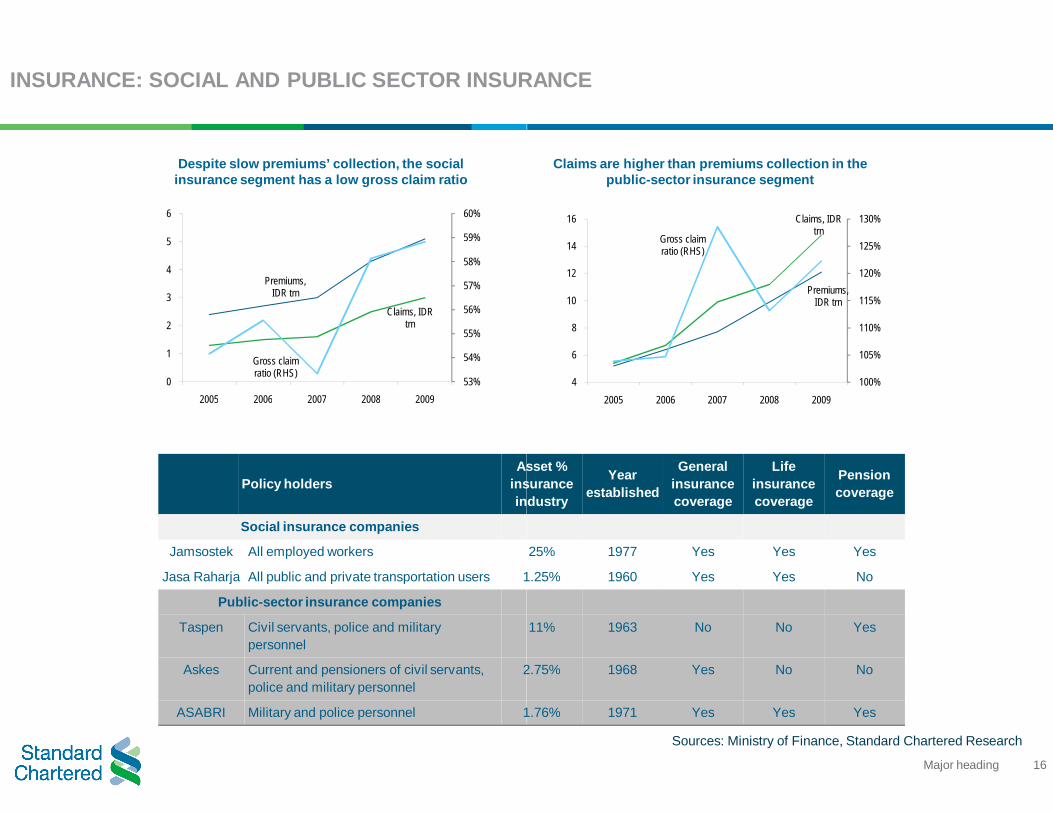

INSURANCE: SOCIAL AND PUBLIC SECTOR INSURANCE

Premiums, IDR trn

Claims, IDR trn

Gross claim ratio (RHS)

53%

54%

55%

56%

57%

58%

59%

60%

0

1

2

3

4

5

6

2005 2006 2007 2008 2009

Policy holdersAsset %

insurance industry

Social insurance companies

Jamsostek All employed workers

Jasa Raharja All public and private transportation users 1.25%

Public-sector insurance companies

Taspen Civil servants, police and military personnel

Askes Current and pensioners of civil servants, police and military personnel

2.75%

ASABRI Military and police personnel 1.76%

Despite slow premiums’ collection, the social insurance segment has a low gross claim ratio

16Major heading

INSURANCE: SOCIAL AND PUBLIC SECTOR INSURANCE

Sources: Ministry of Finance, Standard Chartered Research

Premiums, IDR trn

Claims, IDR trn

Gross claim ratio (RHS)

100%

105%

110%

115%

120%

125%

130%

4

6

8

10

12

14

16

2005 2006 2007 2008 2009

Asset % insurance industry

Yearestablished

General insurance coverage

Life insurance coverage

Pension coverage

25% 1977 Yes Yes Yes

1.25% 1960 Yes Yes No

11% 1963 No No Yes

2.75% 1968 Yes No No

1.76% 1971 Yes Yes Yes

Claims are higher than premiums collection in the public-sector insurance segment

INSURANCE: GENERAL INSURANCE AND REINSURANCE

Sources: Ministry of Finance, Standard Chartered Research

Gross premiums,

IDR trn

Gross claims, IDR trn

Gross claim ratio (%, rhs)

3536373839404142434445

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009 2010

0

5

10

15

2005 2006

AutomotivePersonal accident & healthCredit and surety bond

Govt and CB

Securities

Deposit

Corporate bonds

Stocks

Mutual Fund

Direct Placement

0

20

40

60

80

100

120

140

Life insurance Social Insurance

Public sector General insurance

Reinsurance

Profitability of general insurance and reinsurance companies (premiums versus claims growth)

General insurance coverage (IDR trillion)Dominance of the auto industry

Investment composition by insurance fund, 2009 Social and public-sector funds are more risk-averse

(IDR trillion)

17Major heading

INSURANCE: GENERAL INSURANCE AND REINSURANCE

Sources: Ministry of Finance, Standard Chartered Research

2007 2008 2009

PropertyPersonal accident & health Cargo

Energy

Corp bonds and MTN

Deposit

Equity

Government bonds and SBI

Mutual Fund0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2003 2004 2005 2006 2007 2008 2009 Q4 2010*

general insurance

mutual funds

DB pension fundsDC pension funds

life insurance

pension funds of insurance companies

banks (including BI)

offshore <2Y

offshore 2-5Y offshore >5Y

1Y

250150

50

0

2

4

6

8

10

Y 5Y 10Y 15Y 20Y 25Y 30Y

Yield

(%)

General insurance coverage (IDR trillion)Dominance of the auto industry

The evolution of the investment portfolioAllocation across asset classes is converging

The size and positioning of insurance funds along the government bond yield curve (2011)

PENSION FUNDSPENSION FUNDSPENSION FUNDSPENSION FUNDS

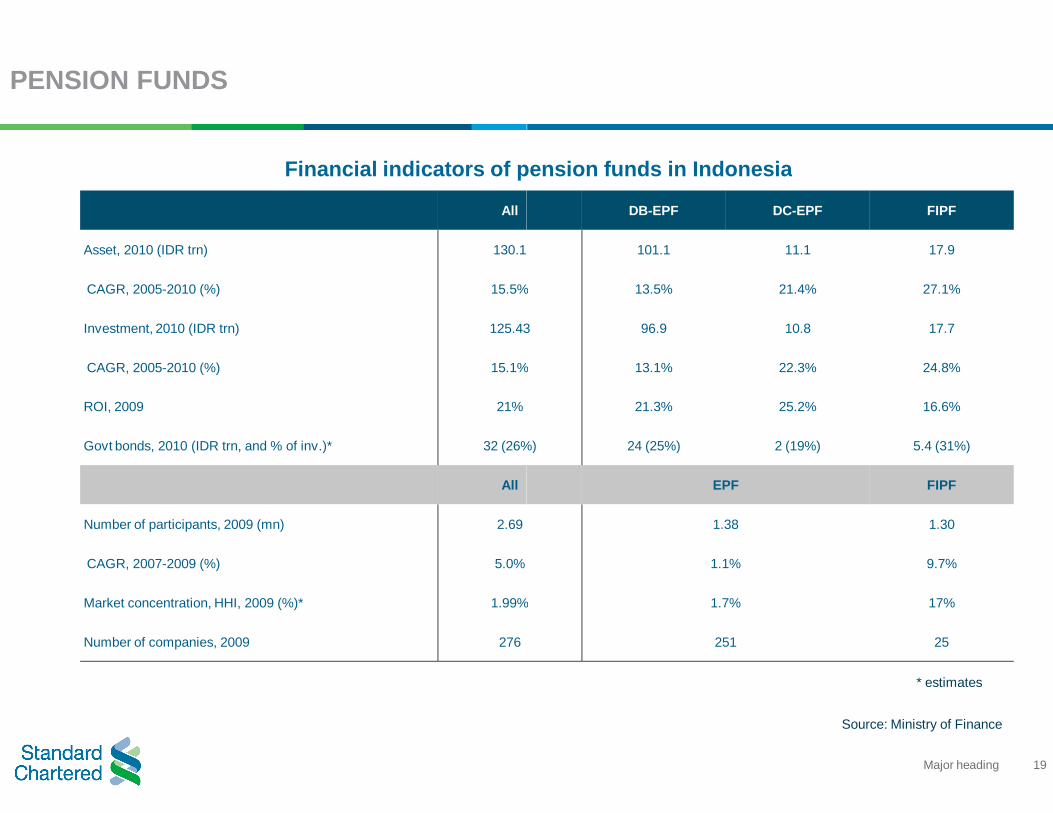

PENSION FUNDS

All

Asset, 2010 (IDR trn) 130.1

CAGR, 2005-2010 (%) 15.5%

Investment, 2010 (IDR trn) 125.43

CAGR, 2005-2010 (%) 15.1%

ROI, 2009 21%

Govt bonds, 2010 (IDR trn, and % of inv.)* 32 (26%)

All

Number of participants, 2009 (mn) 2.69

CAGR, 2007-2009 (%) 5.0%

Market concentration, HHI, 2009 (%)* 1.99%

Number of companies, 2009 276

Financial indicators of pension funds in Indonesia

19Major heading

DB-EPF DC-EPF FIPF

101.1 11.1 17.9

15.5% 13.5% 21.4% 27.1%

125.43 96.9 10.8 17.7

15.1% 13.1% 22.3% 24.8%

21.3% 25.2% 16.6%

32 (26%) 24 (25%) 2 (19%) 5.4 (31%)

EPF FIPF

1.38 1.30

1.1% 9.7%

1.99% 1.7% 17%

251 25

* estimates

Source: Ministry of Finance

Financial indicators of pension funds in Indonesia

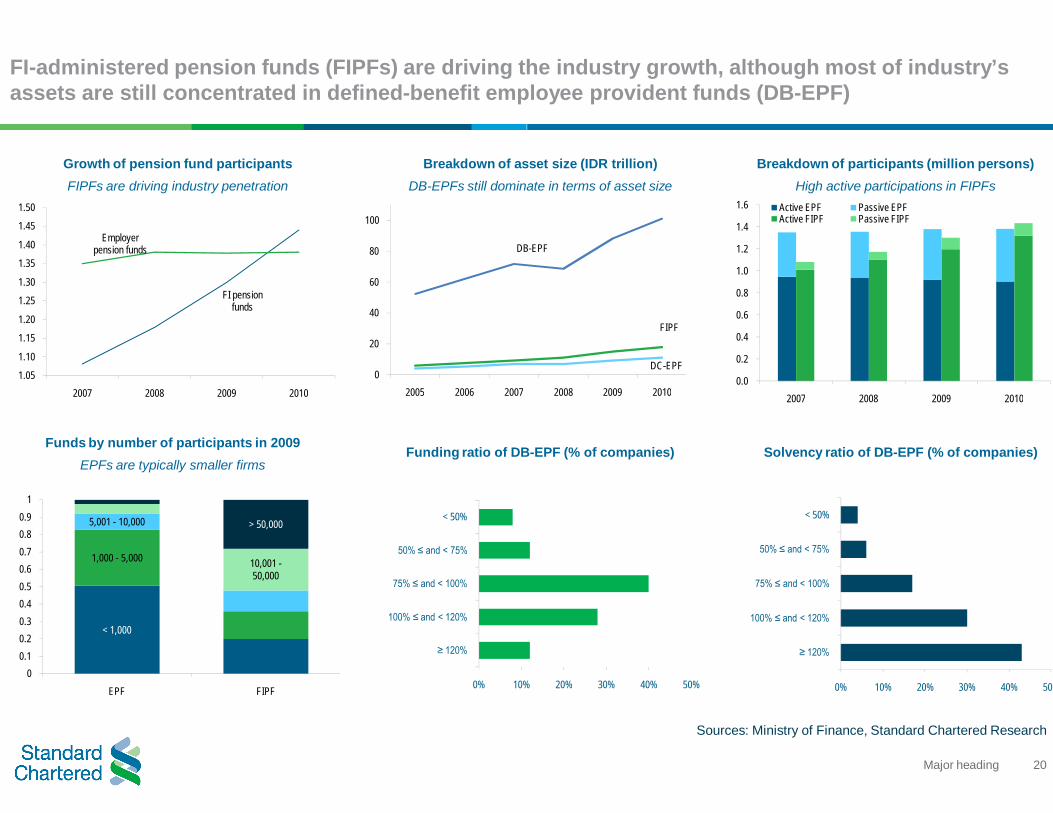

FI-administered pension funds (FIPFs) are driving the industry growth, although most of industry’s assets are still concentrated in defined-benefit employee provident funds (DB

≥ 120%

100% ≤ and < 120%

75% ≤ and < 100%

50% ≤ and < 75%

< 50%

0% 10%

FI pension funds

Employer pension funds

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

2007 2008 2009 2010

DB

0

20

40

60

80

100

2005 2006 2007

< 1,000

1,000 - 5,000

5,001 - 10,000

10,001 -50,000

> 50,000

00.10.20.30.40.50.60.70.80.9

1

EPF FIPF

Growth of pension fund participantsFIPFs are driving industry penetration

Breakdown of asset size (IDR trillion)DB-EPFs still dominate in terms of asset size

Funds by number of participants in 2009EPFs are typically smaller firms

Funding ratio of DB

20Major heading

administered pension funds (FIPFs) are driving the industry growth, although most of industry’s benefit employee provident funds (DB-EPF)

Sources: Ministry of Finance, Standard Chartered Research

10% 20% 30% 40% 50%

≥ 120%

100% ≤ and < 120%

75% ≤ and < 100%

50% ≤ and < 75%

< 50%

0% 10% 20% 30% 40% 50%

DB-EPF

DC-EPF

FIPF

2008 2009 20100.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2007 2008 2009 2010

Active EPF Passive EPFActive FIPF Passive FIPF

Breakdown of asset size (IDR trillion)EPFs still dominate in terms of asset size

Breakdown of participants (million persons)High active participations in FIPFs

Funding ratio of DB-EPF (% of companies) Solvency ratio of DB-EPF (% of companies)

MUTUAL FUNDSMUTUAL FUNDSMUTUAL FUNDSMUTUAL FUNDS

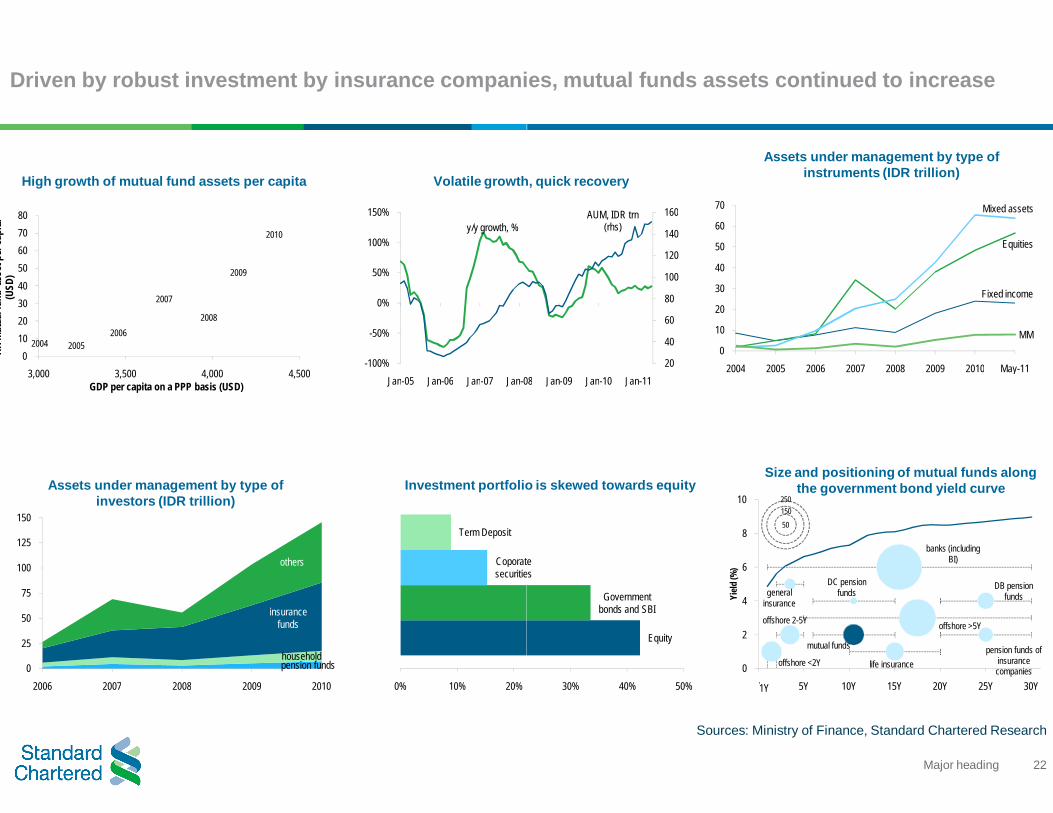

Driven by robust investment by insurance companies, mutual funds assets continued to increase

2004 20052006

2007

2008

2009

2010

01020304050607080

3,000 3,500 4,000 4,500

HH m

utua

l fun

d as

set p

er ca

pita

(U

SD)

GDP per capita on a PPP basis (USD)

y/y growth, %

-100%

-50%

0%

50%

100%

150%

Jan-05 Jan-06 Jan-07 Jan-08

pension fundshousehold

insurance funds

others

0

25

50

75

100

125

150

2006 2007 2008 2009 2010

High growth of mutual fund assets per capita Volatile growth, quick recovery

Assets under management by type of investors (IDR trillion)

Coporate securities

Term Deposit

0% 10% 20%

Investment portfolio is skewed towards equity

22Major heading

Driven by robust investment by insurance companies, mutual funds assets continued to increase

Sources: Ministry of Finance, Standard Chartered Research

AUM, IDR trn (rhs)

20

40

60

80

100

120

140

160

08 Jan-09 Jan-10 Jan-11

Fixed income

Equities

Mixed assets

MM0

10

20

30

40

50

60

70

2004 2005 2006 2007 2008 2009 2010 May-11

Volatile growth, quick recovery

Assets under management by type of instruments (IDR trillion)

Equity

Government bonds and SBI

Coporate securities

30% 40% 50%

Investment portfolio is skewed towards equity

general insurance

mutual funds

DB pension funds

DC pension funds

life insurancepension funds of

insurance companies

banks (including BI)

offshore <2Y

offshore 2-5Y offshore >5Y

1Y

25015050

0

2

4

6

8

10

Y 5Y 10Y 15Y 20Y 25Y 30Y

Yield

(%)

Size and positioning of mutual funds along the government bond yield curve

FINANCE COMPANIESFINANCE COMPANIESFINANCE COMPANIESFINANCE COMPANIES

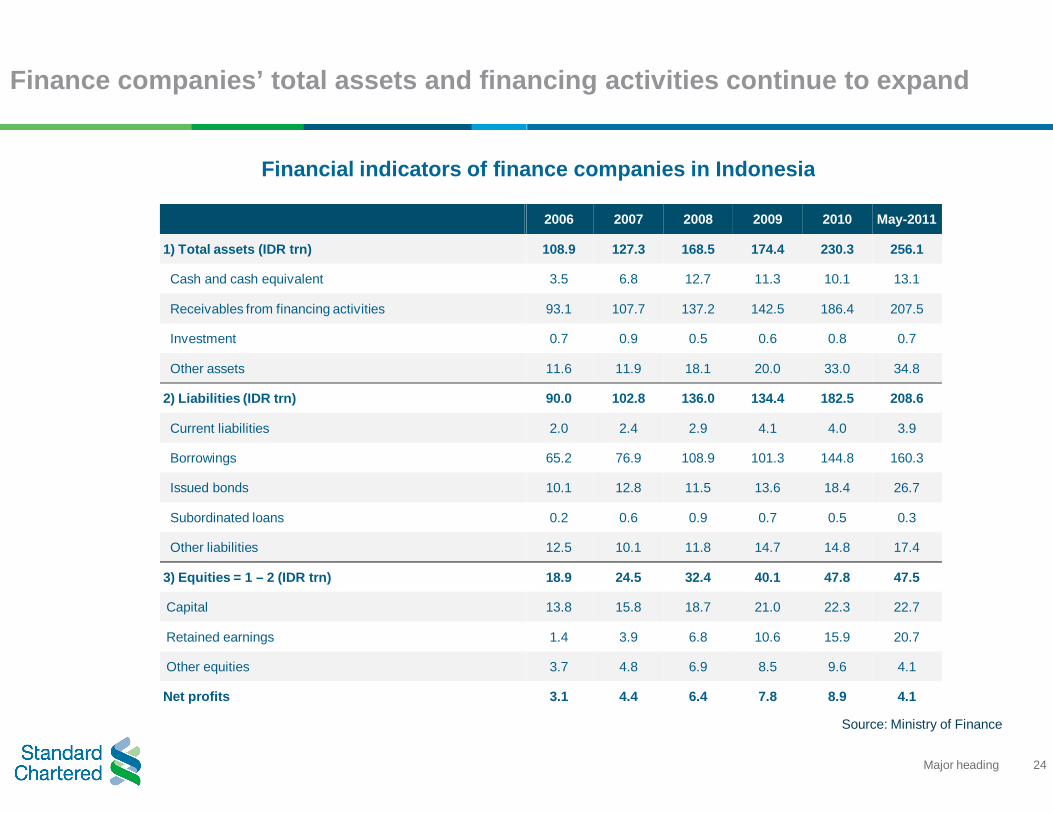

Finance companies’ total assets and financing activities continue to expand

1) Total assets (IDR trn)

Cash and cash equivalent

Receivables from financing activities

Investment

Other assets

2) Liabilities (IDR trn)

Current liabilities

Borrowings

Issued bonds

Subordinated loans

Other liabilities

3) Equities = 1 – 2 (IDR trn)

Capital

Retained earnings

Other equities

Net profits

Financial indicators of finance companies in Indonesia

24Major heading

Finance companies’ total assets and financing activities continue to expand

Source: Ministry of Finance

2006 2007 2008 2009 2010 May-2011

108.9 127.3 168.5 174.4 230.3 256.1

3.5 6.8 12.7 11.3 10.1 13.1

93.1 107.7 137.2 142.5 186.4 207.5

0.7 0.9 0.5 0.6 0.8 0.7

11.6 11.9 18.1 20.0 33.0 34.8

90.0 102.8 136.0 134.4 182.5 208.6

2.0 2.4 2.9 4.1 4.0 3.9

65.2 76.9 108.9 101.3 144.8 160.3

10.1 12.8 11.5 13.6 18.4 26.7

0.2 0.6 0.9 0.7 0.5 0.3

12.5 10.1 11.8 14.7 14.8 17.4

18.9 24.5 32.4 40.1 47.8 47.5

13.8 15.8 18.7 21.0 22.3 22.7

1.4 3.9 6.8 10.6 15.9 20.7

3.7 4.8 6.9 8.5 9.6 4.1

3.1 4.4 6.4 7.8 8.9 4.1

Financial indicators of finance companies in Indonesia

Major finance companies in Indonesia mostly focus on automotive financing

Financial summary of major finance companies in Indonesia

Financing (IDR trn)

Market share(%)

Central Java Power 15.3 8.2

Astra Sedaya Finance 13.1 7.0

Oto Multiartha 12.2 6.5

Federal International Finance 11.4 6.1

Summit Oto Finance 10.8 5.8

Bussan Auto Finance 10.1 5.4

Dipo Star Finance 8.9 4.8

Toyota Astra Financial Services 7.7 4.2

Adira Dinamika Multi Finance 6.5 3.5

Surya Artha Nusantara Finance 3.6 1.9

BFI Finance Indonesia 3.3 1.8

Wahana Ottomitra Multiartha 3.2 1.7

Others 80.3 43.1

Overall industry 186.4 100.0

25Major heading

Major finance companies in Indonesia mostly focus on automotive financing

Sources: Infobank, Ministry of Finance, Standard Chartered Research

Financial summary of major finance companies in Indonesia

Net profit(IDR trn)

Assets(IDR trn)

Equity(IDR trn)

ROA(%)

ROE(%)

-0.1 37.0 3.8 -0.4 -3.4

0.5 13.9 2.1 4.2 26.3

0.6 12.8 2.9 5.4 23.5

1.2 12.1 3.6 11.1 36.2

0.4 11.5 2.8 4.5 17.4

0.3 10.4 1.5 3.6 23.0

0.4 9.6 1.1 4.6 34.2

0.2 8.0 0.8 2.3 22.2

1.5 7.6 3.8 24.6 45.5

0.1 3.6 0.5 3.9 25.6

0.4 3.9 1.9 11.6 20.8

0.1 3.6 0.5 4.5 34.7

3.3 96.3 22.5 -- --

8.9 230.3 47.8 4.3 19.7

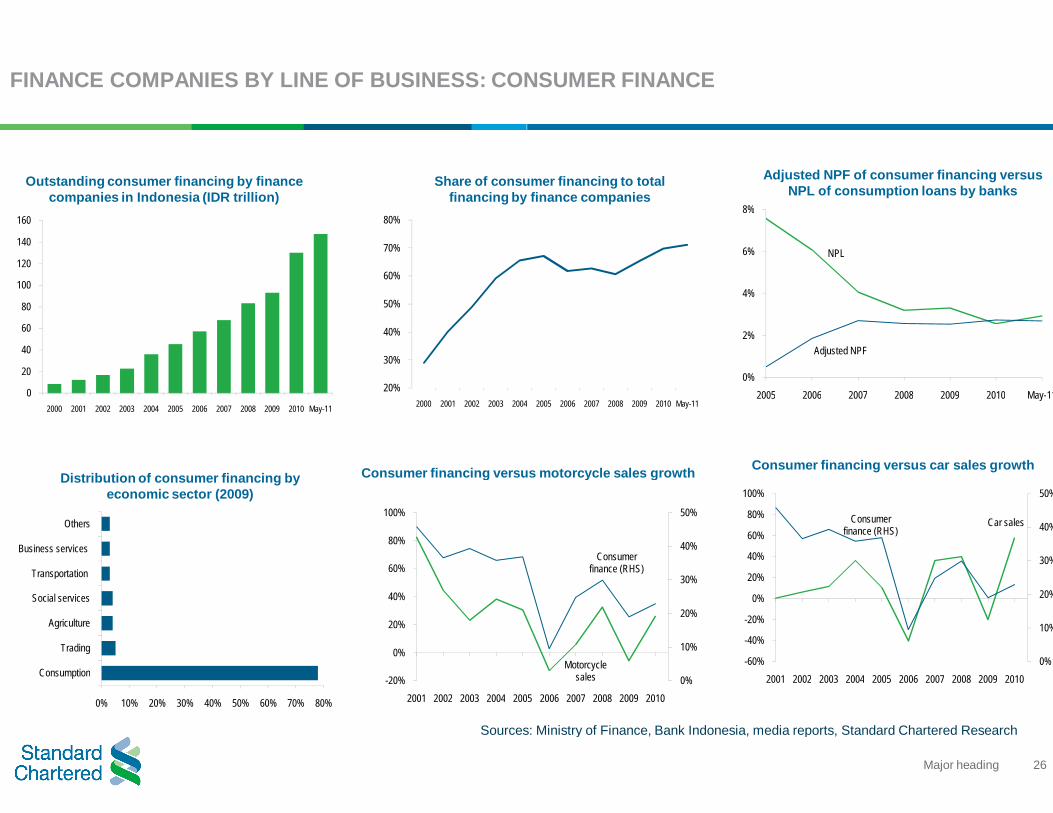

FINANCE COMPANIES BY LINE OF BUSINESS: CONSUMER FINANCE

0

20

40

60

80

100

120

140

160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 May-11

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004

0% 10% 20% 30% 40% 50% 60% 70% 80%

Consumption

Trading

Agriculture

Social services

Transportation

Business services

Others

-20%

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005

Sources: Ministry of Finance, Bank Indonesia, media reports, Standard Chartered Research

Outstanding consumer financing by finance companies in Indonesia (IDR trillion)

Share of consumer financing to total financing by finance companies

Distribution of consumer financing by economic sector (2009)

Consumer financing versus motorcycle sales growth

26Major heading

FINANCE COMPANIES BY LINE OF BUSINESS: CONSUMER FINANCE

2004 2005 2006 2007 2008 2009 2010 May-11

NPL

Adjusted NPF

0%

2%

4%

6%

8%

2005 2006 2007 2008 2009 2010 May-11

Motorcycle sales

Consumer finance (RHS)

0%

10%

20%

30%

40%

50%

2005 2006 2007 2008 2009 2010

Car salesConsumer finance (RHS)

0%

10%

20%

30%

40%

50%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Sources: Ministry of Finance, Bank Indonesia, media reports, Standard Chartered Research

Share of consumer financing to total financing by finance companies

Adjusted NPF of consumer financing versus NPL of consumption loans by banks

Consumer financing versus motorcycle sales growth Consumer financing versus car sales growth

FINANCE COMPANIES BY LINE OF BUSINESS: LEASING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 May-11

0% 10% 20% 30% 40% 50% 60%

Non-finance companies

Government

Individual customers

Outstanding leasing financing by finance companies in Indonesia (IDR trillion)

Distribution of leasing financing by type of customer (2009)

27Major heading

FINANCE COMPANIES BY LINE OF BUSINESS: LEASING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

0%

1%

2%

3%

4%

5%

6%

2005 2006 2007 2008 2009 2010 May-11

0% 5% 10% 15% 20% 25% 30% 35%

Electricity

Construction

Manufacturing

Mining

Transportation

Trading

Services

Agriculture

Others

NPF of leasing financing by finance companies in Indonesia

Distribution of leasing financing by economic sector (2009)

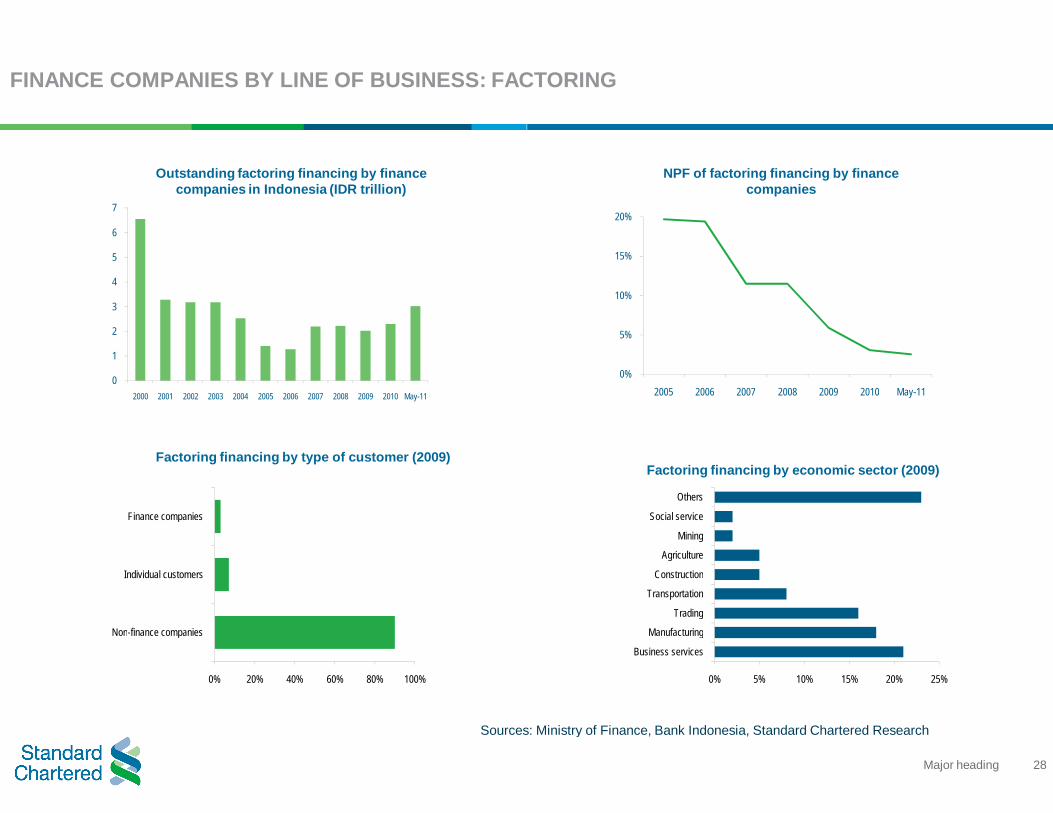

FINANCE COMPANIES BY LINE OF BUSINESS: FACTORING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 May-11

0% 20% 40% 60% 80% 100%

Non-finance companies

Individual customers

Finance companies

Outstanding factoring financing by finance companies in Indonesia (IDR trillion)

Factoring financing by type of customer (2009)

28Major heading

FINANCE COMPANIES BY LINE OF BUSINESS: FACTORING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

0%

5%

10%

15%

20%

2005 2006 2007 2008 2009 2010 May-11

0% 5% 10% 15% 20% 25%

Business services

Manufacturing

Trading

Transportation

Construction

Agriculture

Mining

Social service

Others

NPF of factoring financing by finance companies

Factoring financing by economic sector (2009)

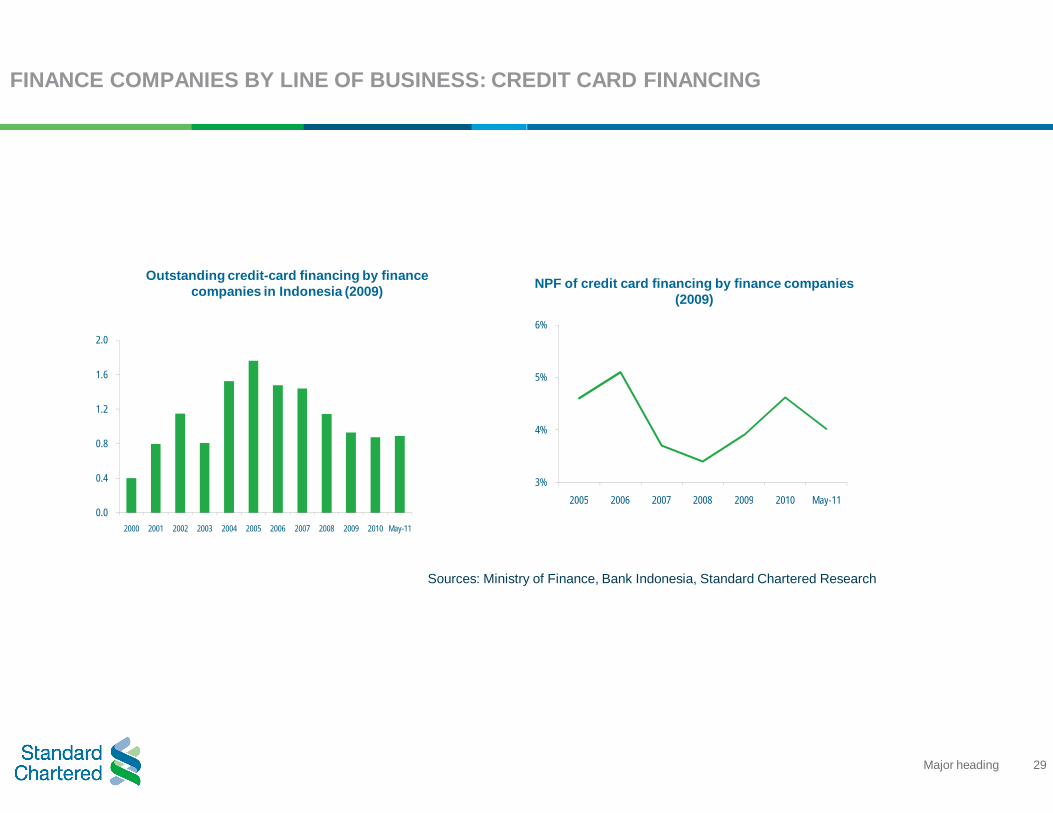

FINANCE COMPANIES BY LINE OF BUSINESS: CREDIT CARD FINANCING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

0.0

0.4

0.8

1.2

1.6

2.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 May-11

Outstanding credit-card financing by finance companies in Indonesia (2009)

29Major heading

FINANCE COMPANIES BY LINE OF BUSINESS: CREDIT CARD FINANCING

Sources: Ministry of Finance, Bank Indonesia, Standard Chartered Research

3%

4%

5%

6%

2005 2006 2007 2008 2009 2010 May-11

NPF of credit card financing by finance companies (2009)

GOVERNMENT REGULATIONSGOVERNMENT REGULATIONSGOVERNMENT REGULATIONSGOVERNMENT REGULATIONS

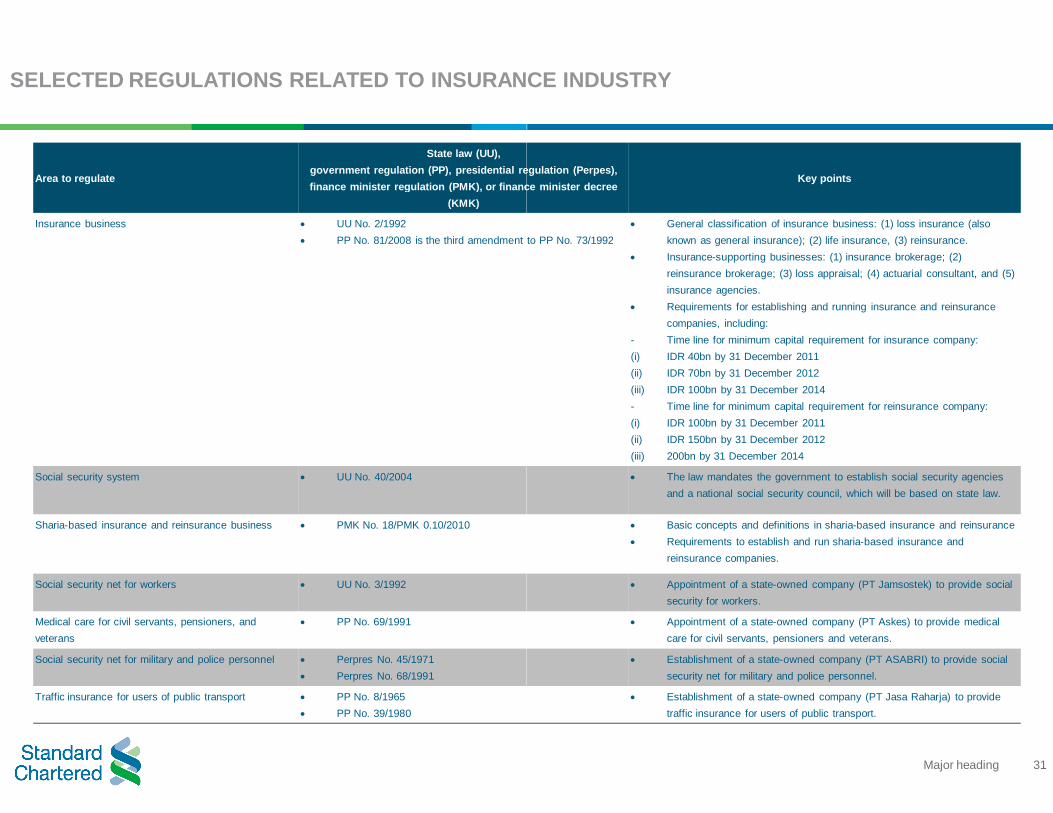

SELECTED REGULATIONS RELATED TO INSURANCE INDUSTRY

Area to regulate

State law (UU), government regulation (PP), presidential regulation (finance minister regulation (PMK), or finance minister decree

(KMK)

Insurance business UU No. 2/1992 PP No. 81/2008 is the third amendment to PP No. 73/1992

Social security system UU No. 40/2004

Sharia-based insurance and reinsurance business PMK No. 18/PMK 0.10/2010

Social security net for workers UU No. 3/1992

Medical care for civil servants, pensioners, and veterans

PP No. 69/1991

Social security net for military and police personnel Perpres No. 45/1971 Perpres No. 68/1991

Traffic insurance for users of public transport PP No. 8/1965 PP No. 39/1980

31Major heading

SELECTED REGULATIONS RELATED TO INSURANCE INDUSTRY

government regulation (PP), presidential regulation (Perpes), finance minister regulation (PMK), or finance minister decree

Key points

PP No. 81/2008 is the third amendment to PP No. 73/1992 General classification of insurance business: (1) loss insurance (also

known as general insurance); (2) life insurance, (3) reinsurance. Insurance-supporting businesses: (1) insurance brokerage; (2)

reinsurance brokerage; (3) loss appraisal; (4) actuarial consultant, and (5) insurance agencies.

Requirements for establishing and running insurance and reinsurance companies, including:

- Time line for minimum capital requirement for insurance company:(i) IDR 40bn by 31 December 2011 (ii) IDR 70bn by 31 December 2012(iii) IDR 100bn by 31 December 2014- Time line for minimum capital requirement for reinsurance company:(i) IDR 100bn by 31 December 2011 (ii) IDR 150bn by 31 December 2012(iii) 200bn by 31 December 2014

The law mandates the government to establish social security agencies and a national social security council, which will be based on state law.

Basic concepts and definitions in sharia-based insurance and reinsurance Requirements to establish and run sharia-based insurance and

reinsurance companies.

Appointment of a state-owned company (PT Jamsostek) to provide social security for workers.

Appointment of a state-owned company (PT Askes) to provide medical care for civil servants, pensioners and veterans.

Establishment of a state-owned company (PT ASABRI) to provide social security net for military and police personnel.

Establishment of a state-owned company (PT Jasa Raharja) to provide traffic insurance for users of public transport.

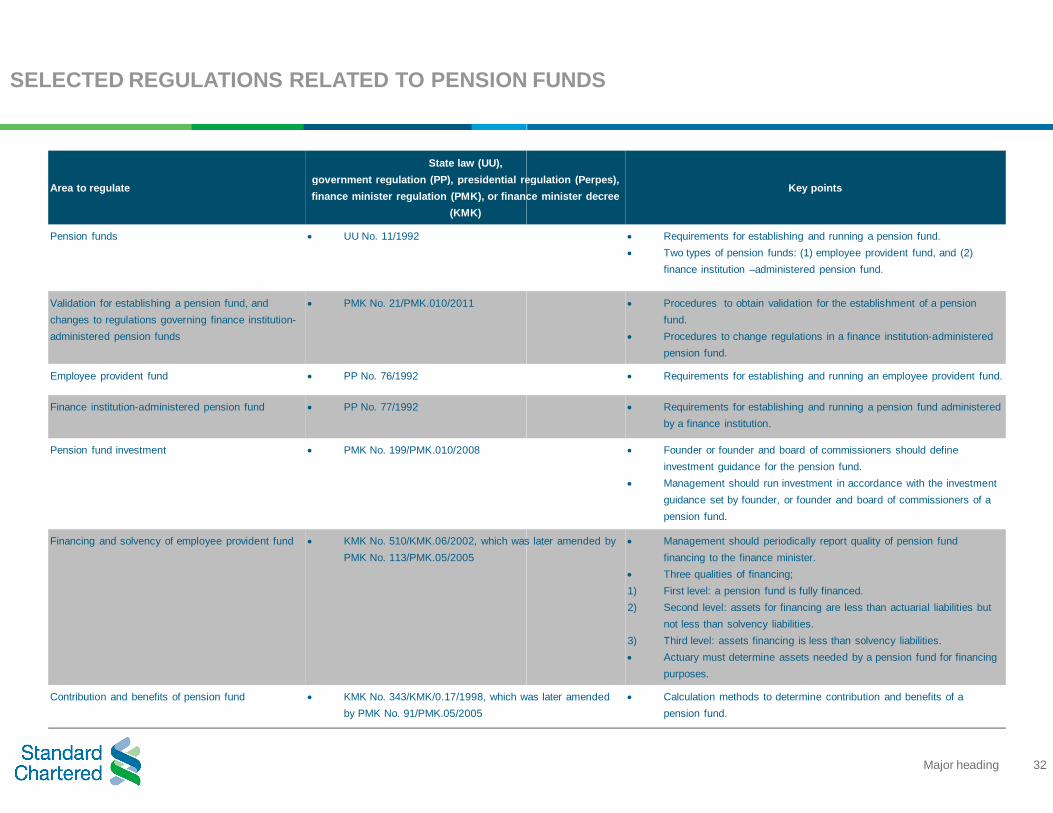

SELECTED REGULATIONS RELATED TO PENSION FUNDS

Area to regulate

State law (UU),government regulation (PP), presidential regulation (finance minister regulation (PMK), or finance minister decree

(KMK)

Pension funds UU No. 11/1992

Validation for establishing a pension fund, and changes to regulations governing finance institution-administered pension funds

PMK No. 21/PMK.010/2011

Employee provident fund PP No. 76/1992

Finance institution-administered pension fund PP No. 77/1992

Pension fund investment PMK No. 199/PMK.010/2008

Financing and solvency of employee provident fund KMK No. 510/KMK.06/2002, which was later amended by PMK No. 113/PMK.05/2005

Contribution and benefits of pension fund KMK No. 343/KMK/0.17/1998, which was later amended by PMK No. 91/PMK.05/2005

32Major heading

SELECTED REGULATIONS RELATED TO PENSION FUNDS

government regulation (PP), presidential regulation (Perpes), finance minister regulation (PMK), or finance minister decree

Key points

Requirements for establishing and running a pension fund. Two types of pension funds: (1) employee provident fund, and (2)

finance institution –administered pension fund.

Procedures to obtain validation for the establishment of a pension fund.

Procedures to change regulations in a finance institution-administered pension fund.

Requirements for establishing and running an employee provident fund.

Requirements for establishing and running a pension fund administered by a finance institution.

Founder or founder and board of commissioners should define investment guidance for the pension fund.

Management should run investment in accordance with the investment guidance set by founder, or founder and board of commissioners of a pension fund.

KMK No. 510/KMK.06/2002, which was later amended by Management should periodically report quality of pension fund financing to the finance minister.

Three qualities of financing;1) First level: a pension fund is fully financed.2) Second level: assets for financing are less than actuarial liabilities but

not less than solvency liabilities.3) Third level: assets financing is less than solvency liabilities. Actuary must determine assets needed by a pension fund for financing

purposes.

KMK No. 343/KMK/0.17/1998, which was later amended Calculation methods to determine contribution and benefits of a pension fund.

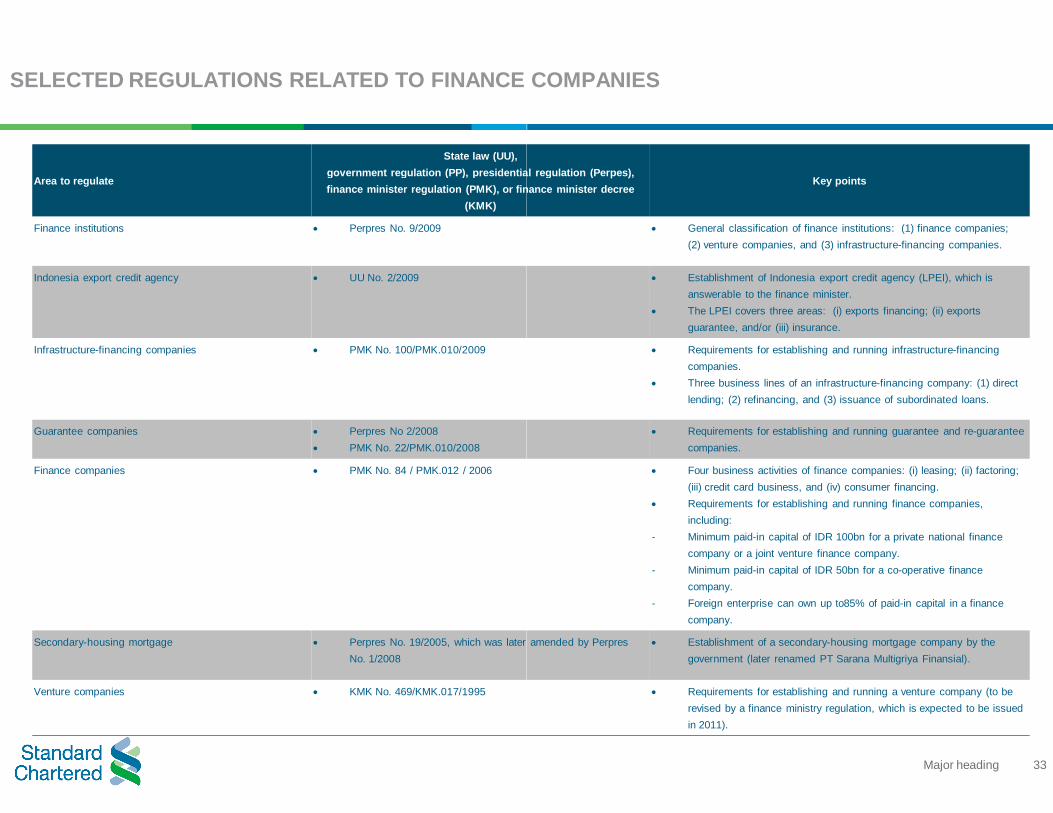

SELECTED REGULATIONS RELATED TO FINANCE COMPANIES

Area to regulate

State law (UU),government regulation (PP), presidential regulation (finance minister regulation (PMK), or finance minister decree

(KMK)

Finance institutions Perpres No. 9/2009

Indonesia export credit agency UU No. 2/2009

Infrastructure-financing companies PMK No. 100/PMK.010/2009

Guarantee companies Perpres No 2/2008 PMK No. 22/PMK.010/2008

Finance companies PMK No. 84 / PMK.012 / 2006

Secondary-housing mortgage Perpres No. 19/2005, which was later amended by No. 1/2008

Venture companies KMK No. 469/KMK.017/1995

33Major heading

SELECTED REGULATIONS RELATED TO FINANCE COMPANIES

government regulation (PP), presidential regulation (Perpes), finance minister regulation (PMK), or finance minister decree

Key points

General classification of finance institutions: (1) finance companies; (2) venture companies, and (3) infrastructure-financing companies.

Establishment of Indonesia export credit agency (LPEI), which is answerable to the finance minister.

The LPEI covers three areas: (i) exports financing; (ii) exports guarantee, and/or (iii) insurance.

Requirements for establishing and running infrastructure-financing companies.

Three business lines of an infrastructure-financing company: (1) direct lending; (2) refinancing, and (3) issuance of subordinated loans.

Requirements for establishing and running guarantee and re-guarantee companies.

Four business activities of finance companies: (i) leasing; (ii) factoring; (iii) credit card business, and (iv) consumer financing.

Requirements for establishing and running finance companies, including:

- Minimum paid-in capital of IDR 100bn for a private national finance company or a joint venture finance company.

- Minimum paid-in capital of IDR 50bn for a co-operative finance company.

- Foreign enterprise can own up to85% of paid-in capital in a finance company.

No. 19/2005, which was later amended by Perpres Establishment of a secondary-housing mortgage company by the government (later renamed PT Sarana Multigriya Finansial).

Requirements for establishing and running a venture company (to be revised by a finance ministry regulation, which is expected to be issued in 2011).

Global Disclaimer (page 1 of 2)Regulatory disclosure

Subject companies: --

Standard Chartered Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year: --.

SCB makes no representation or warranty of any kind, express, implied or statutory regarding this document or any information contained or referred to on the document.

If you are receiving this document in any of the countries listed below, please note the following:

United Kingdom: Standard Chartered Bank ("SCB") is authorised and regulated in the United Kingdom by the Financial Services Authority ("FSA"). This communication is not directed at Retail Clients in the European Economic Area as defined by Directive 2004/39/EC. Nothing in this document constitutes a personal recommendation or investment advice as defined by Directive 2004/39/EC.

Australia: The Australian Financial Services Licence for SCB is Licence No: 246833 with the following Australian Registered Business Number (ARBN : 097571778). Australian investors should note that this document was prepared for wholesale investors only (as defined by Australian Corporations legislation).

China: This document is being distributed in China by, and is attributable to, Standard Chartered Bank (China) Limited which is mainly regulated by China Banking Regulatory Commission (CBRC), State Administration of Foreign Exchange (SAFE), and People’s Bank of China (PBoC).

Hong Kong: This document is being distributed in Hong Kong by, and is attributable to, Standard Chartered Bank (Hong Kong) Limited which is regulated by the Hong Kong Monetary Authority.

Japan: This document is being distributed to the Specified Investors, as defined by the Financial Instruments and Exchange Law of Japan (FIEL), for information only and not for the purpose of soliciting any Financial Instruments Transactions as defined by the FIEL or any Specified Deposits, etc. as defined by the Banking Law of Japan.

Singapore: This document is being distributed in Singapore by SCB Singapore branch only to accredited investors, expert investors or institutional investors, as defined in the Securities and Futures Act, Chapter 289 of Singapore. Recipients in Singapore should contact SCB Singapore branch in relation to any matters arising from, or in connection with, this document.

South Africa: SCB is licensed as a Financial Services Provider in terms of Section 8 of the Financial Advisory and Intermediary Services Act 37 of 2002. SCB is a Registered Credit provider in terms of the National Credit Act 34 of 2005 under registration number NCRCP4.

UAE (DIFC): SCB is regulated in the Dubai International Financial Centre by the Dubai Financial Services Authority. This document is intended for use only by Professional Clients and should not be relied upon by or be distributed to Retail Clients.

United States: Except for any documents relating to foreign exchange, FX or global FX, Rates or Commodities, distribution of this document in the United States or to US persons is intended to be solely to major institutional investors as defined in Rule 15a-6(a)(2) under the US Securities Act of 1934. All US persons that receive this document by their acceptance thereof represent and agree that they are a major institutional investor and understand the risks involved in executing transactions in securities. Any US recipient of this document wanting additional information or to effect any transaction in any security or financial instrument mentioned herein, must do so by contacting a registered representative of Standard Chartered Securities (North America) Inc., 1 Madison Avenue, New York, N.Y. 10010, US, tel + 1 212 667 1000.

WE DO NOT OFFER OR SELL SECURITIES TO U.S. PERSONS UNLESS EITHER (A) THOSE SECURITIES ARE REGISTERED FOR SALE WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION AND WITH ALL APPROPRIATE U.S. STATE AUTHORITIES; OR (B) THE SECURITIES OR THE SPECIFIC TRANSACTION QUALIFY FOR AN EXEMPTION UNDER THE U.S. FEDERAL AND STATE SECURITIES LAWS NOR DO WE OFFER OR SELL SECURITIES TO U.S. PERSONS UNLESS (i) WE, OUR AFFILIATED COMPANY AND THE APPROPRIATE PERSONNEL ARE PROPERLY REGISTERED OR LICENSED TO CONDUCT BUSINESS; OR (ii) WE, OUR AFFILIATED COMPANY AND THE APPROPRIATE PERSONNEL QUALIFY FOR EXEMPTIONS UNDER APPLICABLE U.S. FEDERAL AND STATE LAWS.

Global Disclaimer (page 2 of 2)The information on this document is provided for information purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. Users of this document should seek advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to on this document and should understand that statements regarding future prospects may not be realised. Opinions, projections and estimates are subject to change without notice.

The value and income of any of the securities or financial instruments mentioned in this document can fall as well as rise and an investor may get back less than invested. Foreign-currency denominated securities and financial instruments are subject to fluctuation in exchange rates that could have a positive or adverse effect on the value, price or income of such securities and financial instruments.

Past performance is not indicative of comparable future results and no representation or warranty is made regarding future performance.

SCB is not a legal or tax adviser, and is not purporting to provide you with legal or tax advice. If you have any queries as to the legal or tax implications of any investment you should seek independent legal and/or tax advice.

SCB, and/or a connected company, may have a position in any of the instruments or currencies mentioned in this document. SCB has in place policies and procedures and physical information walls between its Research Department and differing public and private business functions to help ensure confidential information, including ‘inside’ information is not publicly disclosed unless in line with its policies and procedures and the rules of its regulators. You are advised to make your own independent judgment with respect to any matter contained herein.

SCB and/or any member of the SCB group of companies may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to on the website or have a material interest in any such securities or related investment, or may be the only market maker in relation to such investments, or provide, or have provided advice, investment banking or other services, to issuers of such investments.

SCB accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of this document, howsoever arising, and including any loss, damage or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with this document, its contents or associated services, or due to any unavailability of the document or any part thereof or any contents or associated services.

Copyright: Standard Chartered Bank 2010. Copyright in all materials, text, articles and information contained herein is the property of, and may only be reproduced with permission of an authorised signatory of, Standard Chartered Bank. Copyright in materials created by third parties and the rights under copyright of such parties is hereby acknowledged. Copyright in all other materials not belonging to third parties and copyright in these materials as a compilation vests and shall remain at all times copyright of Standard Chartered Bank and should not be reproduced or used except for business purposes on behalf of Standard Chartered Bank or save with the express prior written consent of an authorised signatory of Standard Chartered Bank. All rights reserved. © Standard Chartered Bank 2010.

Regulation AC Disclosure:

The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or Analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and, (2) No part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report. On a general basis, the efficacy of recommendations is a factor in the performance appraisals of analysts.

Data available as of 7 August 2011. This document is released on 9 August 2011