22

Industry information K Coetzee August 2013

| Date post: | 13-Dec-2015 |

| Category: |

Documents |

| Upload: | cornelia-parks |

| View: | 219 times |

| Download: | 4 times |

Industry information

K Coetzee

August 2013

Contents

• International economy• International dairy situation• SA economic situation• SA dairy situation

Global growth

• Slight improvement in 2013/ 2014

• Developing countries grow at higher rate

Source: WEO update , July 2013

2010 2011 2012 2013 20140

1

2

3

4

5

6

7

8

World Advanced economies

Developing economies South Africa

% G

DP

gro

wth

/ BB

P g

roei

FAO food price indices, Jan-10 – Jul-13

• Increase in grain prices in 2012

• Followed by dairy prices from mid-2012 and in the first quarter of 2013

Source: FAO, 2013

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13100

150

200

250

300

Food Meat Dairy Cereals

Ind

ex (

2002

- 2

004

= 1

00)

Global milk production

0%

1%

2%

3%

4%

5%

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012%

Mil.

To

nn

es

Cows' milk Annual growth

Source: IDF, November 2012

Production growth 2013 vs 2012

• Europe– 3 months -1,4%

• USA– 4 months =0,2%

• Australia– 5 months – 7,0%

• New Zealand– 3 months -4,2%

• Argentina– 3 months -9,6%

Source: CNIEL July 2013

Global demand

• Stable in spite of:– Economic conditions

• Global exports up 6% on 2011• China demand growth high

Source: CNIEL, July2013

GlobalDairytrade® Sale price index Dec 2012 – Aug 2013

• Prices firmed from mid-2012

• Sharp increase since February 2013

• Reasons• Drought in NZ• Slow start to EU

season• Low stock levels• Period of

adjustment after sharp increase.

Source: gDt Index, August 2013

4-Dec

-12

15-D

ec-1

2

26-D

ec-1

2

6-Ja

n-13

17-J

an-1

3

28-J

an-1

3

8-Feb

-13

19-F

eb-1

3

2-M

ar-1

3

13-M

ar-1

3

24-M

ar-1

3

4-Apr-1

3

15-A

pr-13

26-A

pr-13

7-M

ay-1

3

18-M

ay-1

3

29-M

ay-1

3

9-Ju

n-13

20-J

un-13

1-Ju

l-13

12-J

ul-13

23-J

ul-13

3-Aug-1

31000

1100

1200

1300

1400

1500

1600

1700

1800

Inde

ks (M

aart

201

0 =

1000

)

International prices, Jan-07 – Jul 13

• Dairy prices at all-time record level

• Fonterra sales prices showed slight decrease

Source: USDA, July 2013; Reserve Bank, 2013

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-1310,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

Butter/ Botter SMP/ AMP Cheddar FMP/ VMP

Rand

per

ton

International producer prices, June 2013

• Higher producer prices in most countries

• Subsidies still play major role

• Price based on 4,2% butterfat, 3,4% protein.

Source: LTO, August 2013; IFCN, 2012; MPO, 2013

New Zealand

South Africa

USA

Netherlands

England

Germany

Denmark

France

Ireland

Belgium

Italy

Finland

0 1 2 3 4 5 6 7

Producer price Direct subsidiesRand per litre

SA economic activity

• Co-incident indicator show continuing growth

• Leading indicator recovered from July 2012 low

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12125

130

135

140

145

150

155

160

165

170

Leading indicator Co-incident indicator

Ind

ex (

2000

= 1

00)

Source: SA Reserve Bank, August 2013

Economic growth

• 2012 growth varied between 1,2% and 3,1%

• Weak growth in first quarter of 2013.

Source: Stats SA, June 2013

10-1 10-2 10-3 10-4 11-1 11-2 11-3 11-4 12-1 12-2 12-3 12-4 13-10

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

An

nu

alis

ed

gro

wth

ra

te (

%)

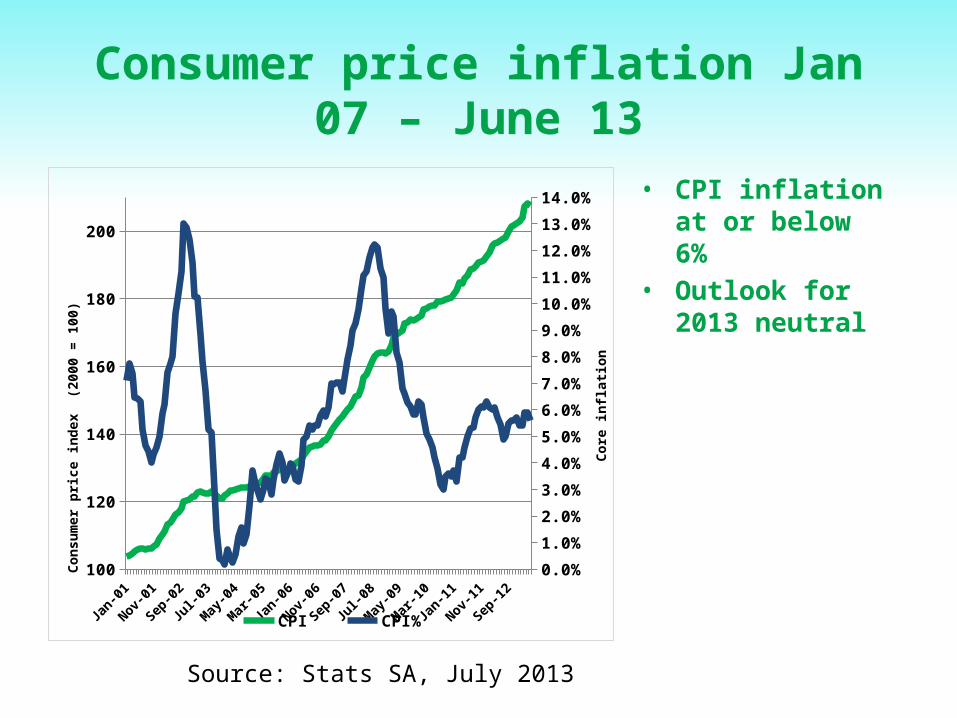

Consumer price inflation Jan 07 – June 13

• CPI inflation at or below 6%

• Outlook for 2013 neutral

Source: Stats SA, July 2013

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2100

120

140

160

180

200

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

CPI CPI%

Co

nsu

mer

pri

ce i

nd

ex

(200

0 =

100

)

Co

re i

nfl

atio

n

Interest rates, Jan 98 – June 13

0

5

10

15

20

25

30

%

Prime rate "Real rate Rate of inflation

• Prime rate low• Real rate at

lowest level since 2009

• Very little upwards pressure

Source: Stats SA, July 2013

Household income and debt

17

19

21

23

25

42

52

62

72

82

PC

Dis

po

sab

le i

nco

me

)

% D

eb

tt

Debt as % of income Real per capita income

• Steady improvement in income

• Lower consumer debt

• More affordable debt

• Unsecured debt !

Source: SA Reserve Bank, June 2013

Retail sales growth, Jan 08 – May 13

• Positive since 2012

• Volatile growth• Between 2% and

6%

Source: Stats SA, May 2013

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Ye

ar

on

ye

ar

gro

wth

(%

)

Monthly raw milk production trend, Jan 2011 – March 2013

• Milk production• 2011 = 2 639 Mil.L.• 2012 = 2 757 Mil. L.

Jan – Jun 13 1274Mil.L. (-0,1%)

• Jan – April 2013 –final

• May – June 2013 - preliminary.

• Feb 2012 = 29 days

Source: 2011, 2012, Jan – Apr 13 Milk SA returns; May – Jun 13, Milk SA estimate

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 170 000

190 000

210 000

230 000

250 000

270 000

2 010 2 011 2012 2013*

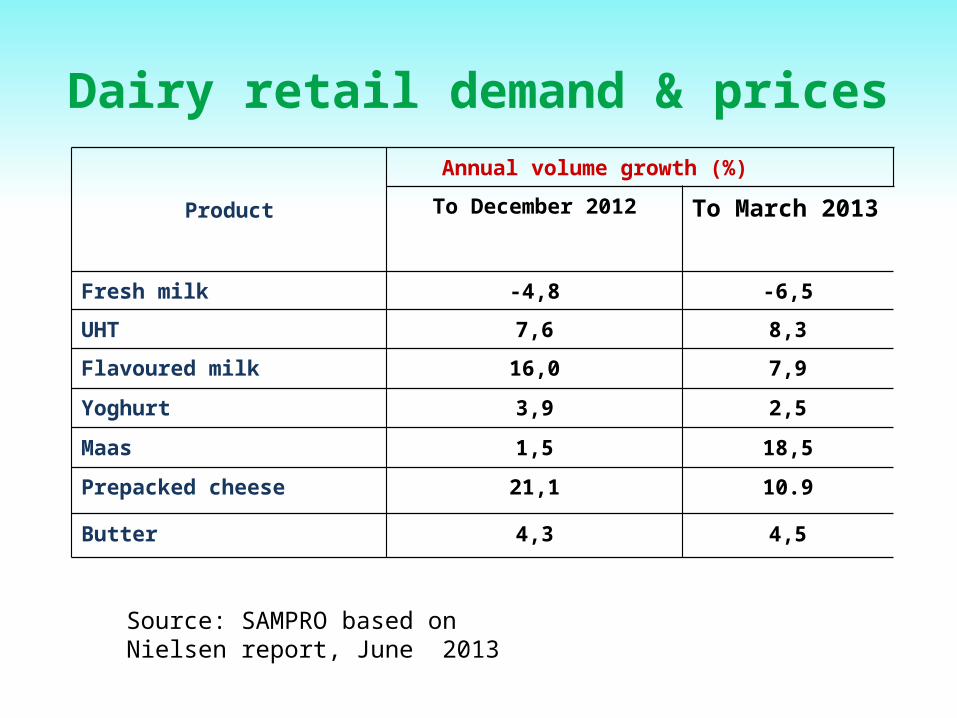

Dairy retail demand & prices

Product

Annual volume growth (%)

To December 2012 To March 2013

Fresh milk -4,8 -6,5

UHT 7,6 8,3

Flavoured milk 16,0 7,9

Yoghurt 3,9 2,5

Maas 1,5 18,5

Prepacked cheese 21,1 10.9

Butter 4,3 4,5

Source: SAMPRO based on Nielsen report, June 2013

Cumulative net imports of dairy products

Source: SARS as supplied by SAMPRO

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec-20

20

60

100

140

180

2010 2011 2012 2013

Mill

ion

litre

milk

equ

ival

ent

Milk: feed price ratio, Jan 03 – July 13

• Historic low Jan 13

• Slight improvement since caused by lower grain prices

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

30.8

1

1.2

1.4

1.6

1.8

2

2.2

Milk

:fe

ed

pri

ce

ra

tio

Source: MPO calculations; Feed = 70% YM1, 30% Soy, Safex nearest month prices, producer price MPO survey

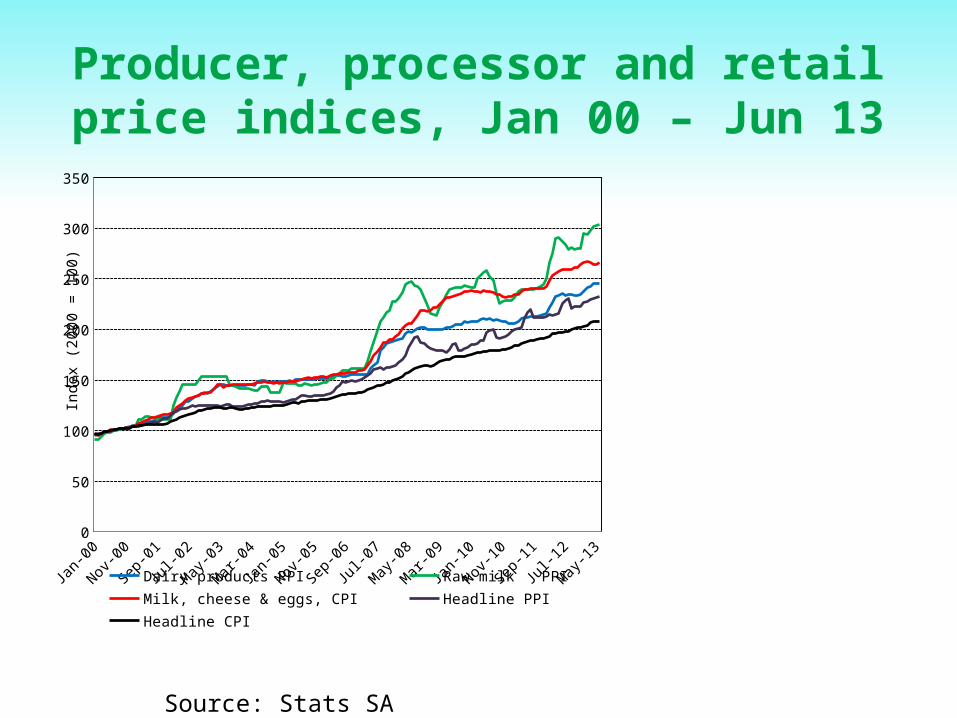

Producer, processor and retail price indices, Jan 00 – Jun 13

Source: Stats SA

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-120

50

100

150

200

250

300

350

Dairy products PPI Raw milk PPI Milk, cheese & eggs, CPI

Headline PPI Headline CPI

Inde

x (2

000

= 1

00)

Retail price 2 litre milk, Jan 00 – Jun 13

Jan-00Jan-01Jan-02Jan-03Jan-04Jan-05Jan-06Jan-07Jan-08Jan-09Jan-10Jan-11Jan-123

4

5

6

7

8

9

10

Retail price/Kleinhandelprys

Ran

d p

er l

itre