Inferring Trader Behavior from Transaction Data: A Simple Model by David Jackson* First draft: May 08, 2003 This draft: May 08, 2003 * Sprott School of Business Telephone: (613) 520-2600 Ext. 2383 Carleton University email: [email protected]710 Dunton Tower 1125 Colonel By Drive Ottawa, Ontario K1S 5B6

Transcript

Inferring Trader Behavior from Transaction Data:A Simple Model

by

David Jackson*

First draft: May 08, 2003This draft: May 08, 2003

* Sprott School of Business Telephone: (613) 520-2600 Ext. 2383Carleton University email: [email protected] Dunton Tower1125 Colonel By DriveOttawa, Ontario K1S 5B6

Inferring Trader Behavior from Transaction Data:A Simple Model

Abstract

A model is presented that uses trade counts to characterize thearrival of news and the propensity of informed and uninformedtraders to transact. Our model has extremely low data requirements,is very fast to estimate and is adaptable for different researchapplications. The model is used to investigate changes in the bid /ask spread in conjunction with trades. We develop and estimate aninnovative extension of the model that relaxes the assumption thatnews is independent from day to day.

IntroductionIn 1987, Easley and O’Hara (EO) introduced a discrete-time, sequential trade

microstructure model1 that shines a light on the flow of information about an asset and

reveals some characteristics of subsequent informed and uninformed trading. A strength

of the EO model is its limited data requirements. Transaction counts of buying and

selling, along with counts of non-trading periods are enough to estimate the probability

that informed traders are active in a given asset market.

Because most data sets do not provide the buy / sell direction of trades, EO use the Lee

and Ready algorithm2 to classify trade direction. The idea underlying the Lee and Ready

method is to use both transaction and quote data to infer trade direction. A transaction

price above the mid-quote is classified as buy-initiated; a transaction price below the

mid-quote is classified as sell-initiated. As implemented in EO’s published papers, no

allowance is made for the uncertainty introduced by estimating trade direction. In effect,

a researcher using the Lee and Ready algorithm in this way assumes more precise

information than is available. Trade classification schemes have been shown to classify

trades imperfectly,3 however, raising questions about test outcomes that are dependent

upon estimates from the EO model.

In this paper, we derive a sequential trade model that uses trade counts only. There is no

use of the unobserved trade direction, removing any concerns about misclassification of

trades and understated standard errors. Our model, thus, has very low data preparation

1 Easley and O’Hara, Journal of Financial Economics, 1987.2 Lee and Ready, Journal of Finance, 1991.3 Theissen, Journal of International Financial Markets, Institutions & Money, 2000.

03/05/092

requirements, is extremely fast to estimate and is adaptable to different research

applications.

Ours is an example of models in which a subset of traders have private information about

the value of the asset. These traders act to profit from their information at the expense of

uninformed liquidity traders and the market maker. The directed trading behavior of the

informed enables the market maker and other uninformed market observers to make

inferences about the true value of the asset. Glosten and Milgrom provide an early

sequential trade, asymmetric information model.4 Sequential trade models allow only one

trader at a time, and place some limit on the size of an individual trade. Because informed

traders must wait their turn and because trade size is limited, informed trading is not

instantly revealing. Thus, sequential trade models have the potential to show time series

patterns in learning about the asset’s value. Indeed, the process of learning by the market

maker is a primary focus of the Easley and O’Hara BSN model upon which our TNT

model is based. The richness of information provided by buy and sell counts enables the

BSN model to infer a bid / ask spread time series that reflects the parameters of the news

process and the balance of informed and uninformed trading activity. By using trade

counts only, the TNT model gives up the ability to infer the spread. Our contribution is to

provide a model is very easy to work with and that does not suffer from possible

misclassification of trade direction.

We will demonstrate our trade / no-trade (TNT) model and briefly compare our

parameter estimates with those provided by the EO buy / sell / no-trade (BSN) model.

Both the TNT and BSN models assume day-to-day independence of information. We will

03/05/093

test this assumption and extend our model to allow for information that is not revealed to

the public for two days. Finally, we present a generalisation of the TNT model that we

use to investigate whether or not market makers change their quoted spreads in response

to trading activity.

This paper is organised as follows. Section 1 presents the EO buy / sell / no-trade (BSN)

model and our trade / no-trade (TNT) model. The TNT model makes no assumptions

about trade direction. In Section 2 the data is described. In Section 3 the model is

estimated, and some robustness and goodness of fit tests are performed. Section 4

generalizes the model to estimate the propensity of market makers to change spreads

around informed and uninformed trades. In Section 5 we summarise what we have

demonstrated.

1. Two Discrete-Time Sequential Trade ModelsIn a world with a single, risky asset, we model sequential trade between investors and a

market maker. A key feature of the models considered here is that news about the value

of the asset is generated intermittently. On any given day, there is uncertainty about

whether or not the value of the asset has changed since the previous day. Before the start

of trading, news about the end-of-day value of the asset is generated with a probability,

� . Any such news is bad with probability � and good with probability 1 �� . At the end

of each trading day, the news becomes publicly available.

The market maker is risk neutral and faces competition, so quotes are set at the expected

value of the asset, conditional on the trade direction of the next transaction. There are

4 Glosten and Milgrom, Journal of Financial Economics, 1985.

03/05/094

assumed to be a fixed number of trading periods during the day, with one trade possible

during any one period. All trades are for one unit of the asset, with all buys occurring at

the ask and all sells at the bid.

In each trading period, one potential trader arrives at the market. This trader observes any

news with probability � . If news is observed, this (informed) trader always trades,

buying on good news and selling on bad. If news is not observed, this (uninformed)

trader makes a liquidity trade with probability � or chooses not to trade with probability

1 �� . Similarly, on days, with no news, each trader must be uninformed and trades with

probability � or chooses not to trade with probability 1 �� . Uninformed trades are

equally likely to be buys or sells.

The market maker can learn from periods of non-trading because they are more likely on

days with no information than on days with good or bad news.

1.1 The EO BSN ModelThe EO trading structure is depicted in Figure 1. Note that a draw from the news

generating process (no news, good news, bad news) occurs once during the day, whereas

only the first of many trading periods is represented in Figure 1. For a given day, the

probability of observing B buys, S sells, and NT no-trade periods, given the model

The restricted BSN model does not reduce to a multiple of the TNT model.

Since the two equations differ in their first term, the two equations will give different

estimates for the parameters � �, ,� � � . None the less, does the BSN model give

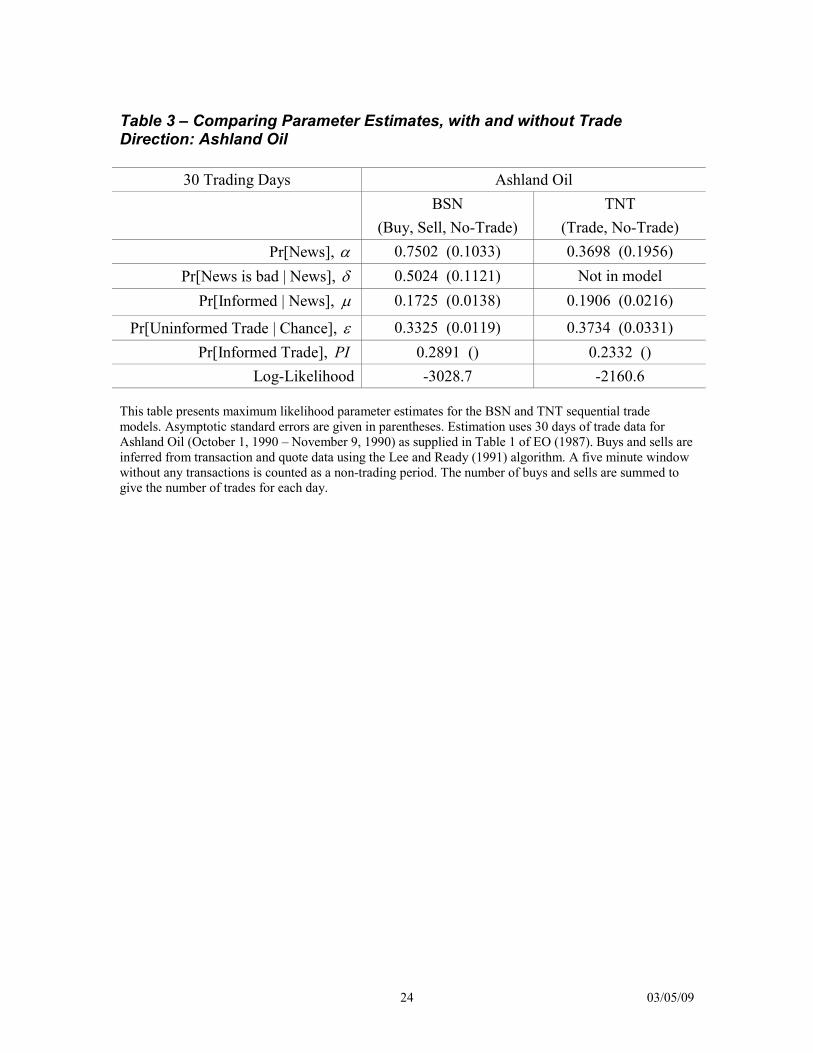

parameter estimates close to those of the TNT model? Table 3 presents estimates for

Ashland Oil,5 the firm used by Easley, Kiefer and O’Hara (1997) to demonstrate the BSN

model. The 95 percent confidence intervals for � �, ,� � � overlap. Since one model is

driven by buy and sell counts and the other model is driven by their sum, we would hope

to find consistent parameter estimates. Notice that � is estimated with much less

precision than � and � . Since there are many trading opportunities during a day, but

5 Thirty trading days of buy / sell / no-trade counts for Ashland Oil come from Table 1 in Easley, Kieferand O’Hara, Review of Financial Studies, 1997.

03/05/099

only one draw from the news process, we effectively have more observations for

estimating � �,� � than � .

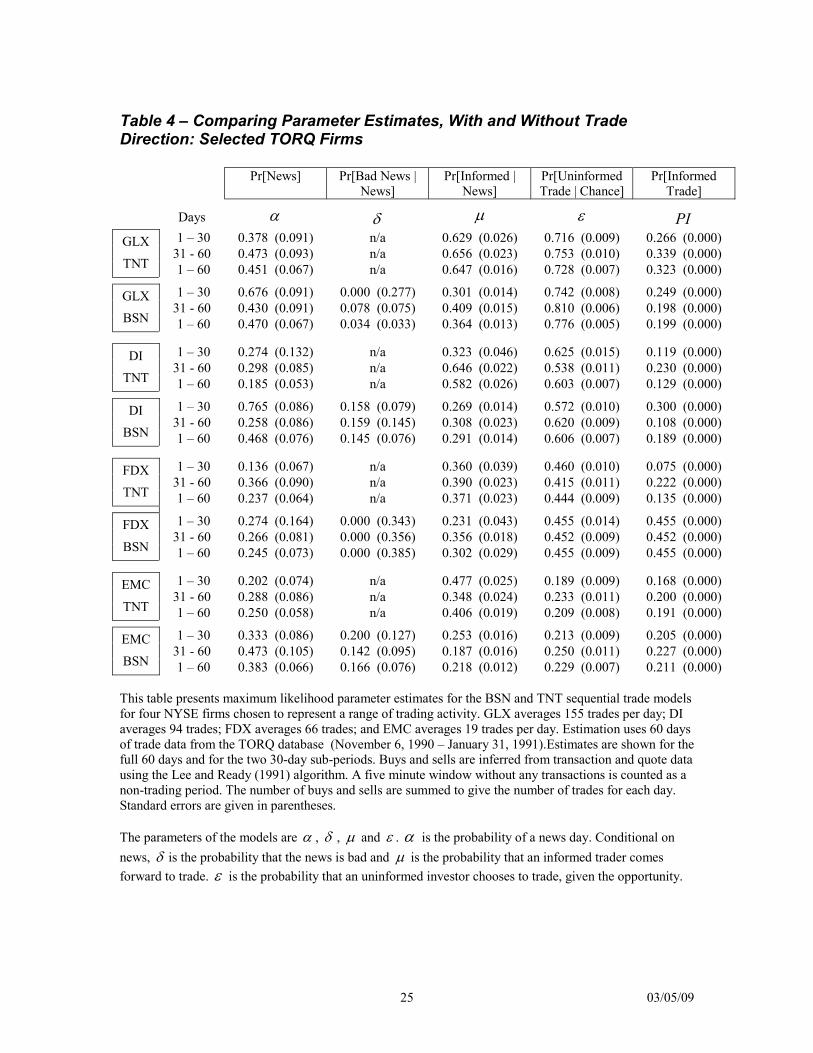

Are parameter estimates always so consistent for the two models? Table 4 presents 30

and 60 day parameter estimates for four NYSE firms that were selected to represent a

range of trading activity. Given the relatively large standard errors, estimates for the

probability of a news day, � , mostly fall within the 95% confidence intervals. Such is

not the case for other parameters, however. The estimates provided by the two models,

for the probability that uninformed traders choose to transact, � , and for the probability

that a trader is informed on a news day, � , differ significantly in many instances.

Estimates of the probability of informed trading, PI, can be quite different too. This

suggests some caution when using either model for research. Tests that rely upon

absolute levels of the parameters may be sensitive to which model is chosen.

Model Specification

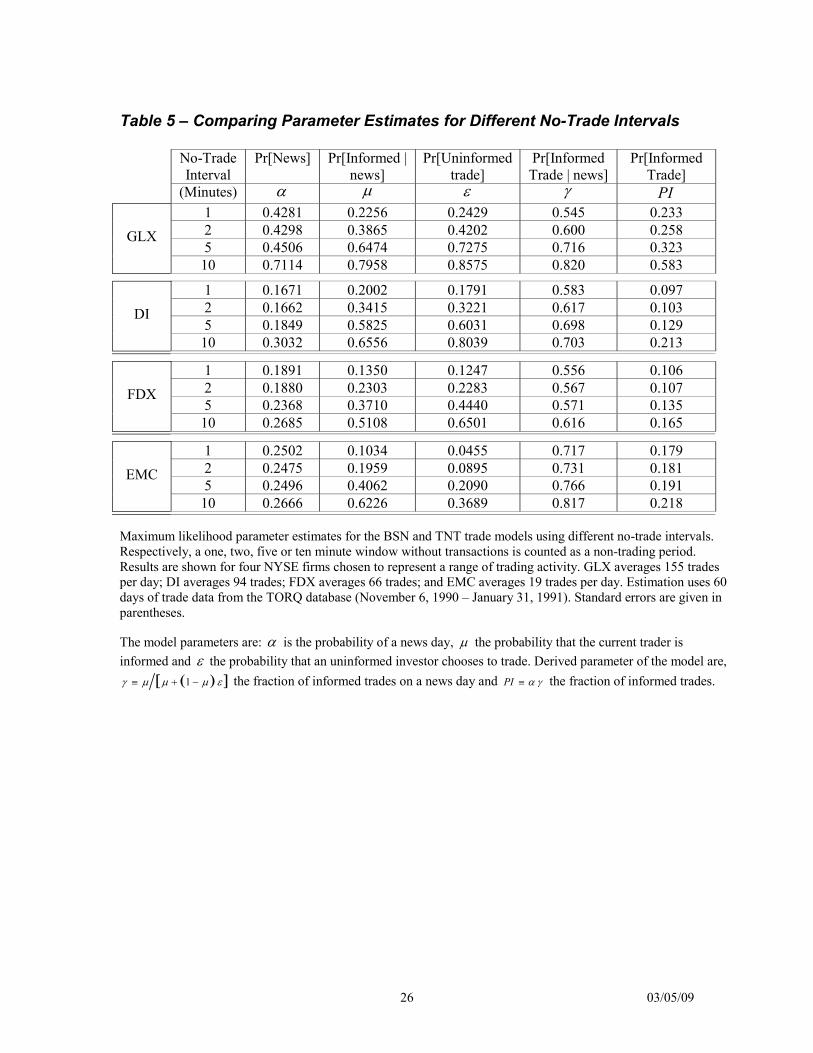

Sensitivity to Choice of No-Trade IntervalA number of specification tests will now be presented. Looking first at parameter

stability, Table 5 shows 60-day parameter estimates as the time specified for a no-trade

period varies from one minute to 10 minutes. All estimates increase with the length of a

no-trade period, especially for the 10 minute interval. Estimates of the probability of

news, � , are fairly consistent for different no-trade periods. This is expected, since �

reflects relative levels of trading from day to day, not relative levels of trading to non-

trading. The probabilities that a trader is informed on a news day, � , and that an

uninformed trader chooses to transact, � , both increase with the length of a no-trade

03/05/0910

period. This is expected, since � and � reflect levels of trading relative to trading

opportunities within each day.

Two important composite measures of trade are � , the fraction of informed trades on a

new days and PI, the fraction of informed trades. We would like the model’s estimates of

� and PI to reflect the flow of private information during a given period, without being

sensitive to the choice of a no-trade interval. Table 5 shows that the increase in the

estimates of � and PI are proportional to the length of the no-trade period. The rate of

increase is small, however, averaging 1.5% per minute for � and 1.6% per minute for PI.

Do Intermittent News and Private Information Help Explain Trade?The TNT model explains daily trade counts in terms of intermittent news events, captured

by � , and traders with different trading propensities on days with news than days

without. One test of the model specification is to compare this model to one in which

news is not intermittent, making trading propensity fixed from day to day. Which model

is more likely given the data? The model restriction constrains the probability of news,

� , to be 1. With one parameter constrained, the likelihood ratio statistic is approximately

distributed chi-squared, with one degree of freedom. We reject the restricted model for

large values of the statistic. The five percent rejection value is 3.84. Likelihood ratio

statistics were calculated from 60-day estimates for the 20 NYSE firms. The smallest

statistic from the 20 firms was 269, soundly rejecting the restricted model. The TNT

model, with news on some days and no news on others better explains the data than a

model in which each day is a news day.

03/05/0911

Are News Events Independent from Day to Day?The two sequential trade models considered so far specify that any news about firm value

is revealed at the end of each trading day. This specification results in a model with a

very simple structure, but may be a poor representation of the information process driving

trades. Easley, Kiefer and O’Hara (EKO 1997), test and cannot reject the hypothesis that

day-to-day news is independent for their one firm, Ashland Oil. One wonders whether or

not this daily independence of news holds more generally. Although it is the quality of

the predictions from a model that matters, not the realism of the assumptions, we will test

for independence of day-to-day news events.

Testing for independence is difficult because news events are not observed. Following

EKO, we use the estimated probability of a news day, � , to infer news events. Consider

the firm, FPL, which has an � of 0.368. We assume that approximately 60 22� � � of

the trading days have news events. When FPL’s daily trade counts are sorted, the twenty-

second highest trade count is found to be 166. All days with trade count greater than 166

are categorized as news days; all days with a count less than 166 are categorized as non-

news days. Days with exactly 166 trades are ignored. For FPL there are n = 21 news days

and m = 38 non-news days. Runs of news and non-news days are counted. Under the null

of news independence, the number of runs is approximately normally distributed, with:

� �2 1mean nm n m� � � and

� � � � � �2var 2 2 1 1iance nm nm n m n m n m� �� � � � � � �

� �.

03/05/0912

Table 6 presents the results of the runs tests on the 20 NYSE firms. The null hypothesis

of independence is rejected in 11 of the 20 firms.

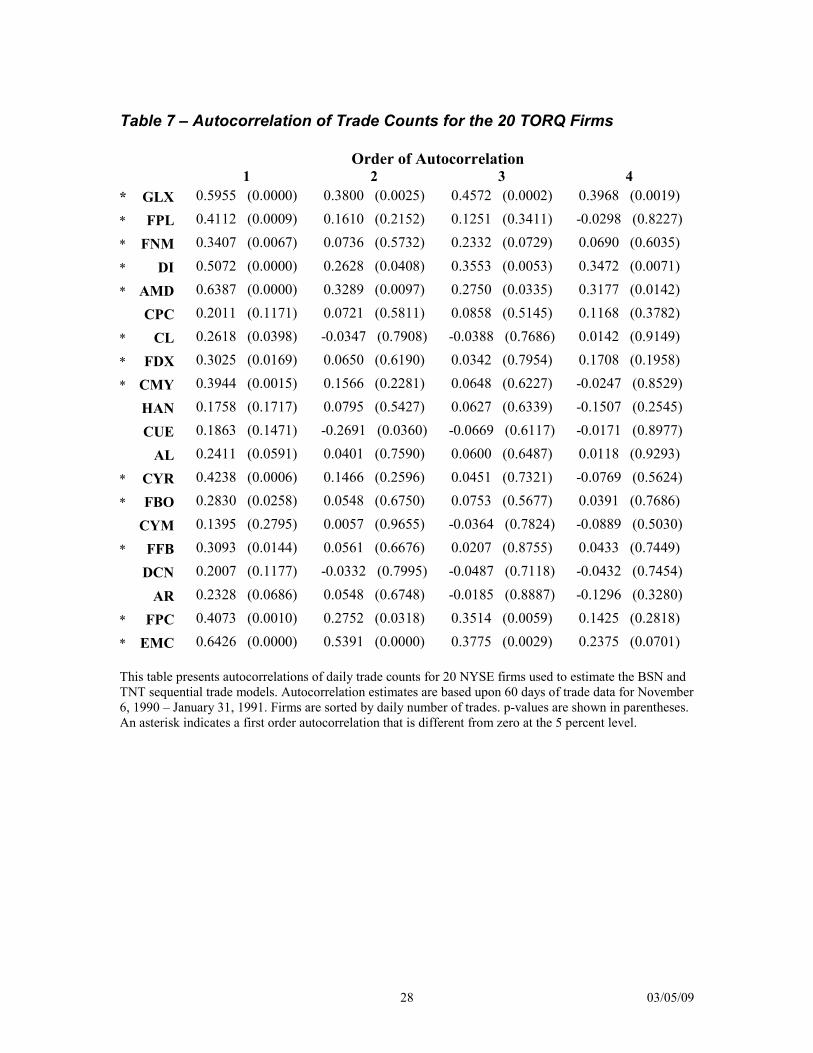

We also look at trade autocorrelations. If news is independent from day to day, there

should be no AR structure to daily trade counts. Table 7 gives the first four

autocorrelations of daily trades for the 20 firms. The first order autocorrelation is

significant for 13 of the firms. Higher order autocorrelations are significant for five of the

13. Together, the runs and autocorrelation tests suggest that news is independent from

day to day for some firms, but not for others.

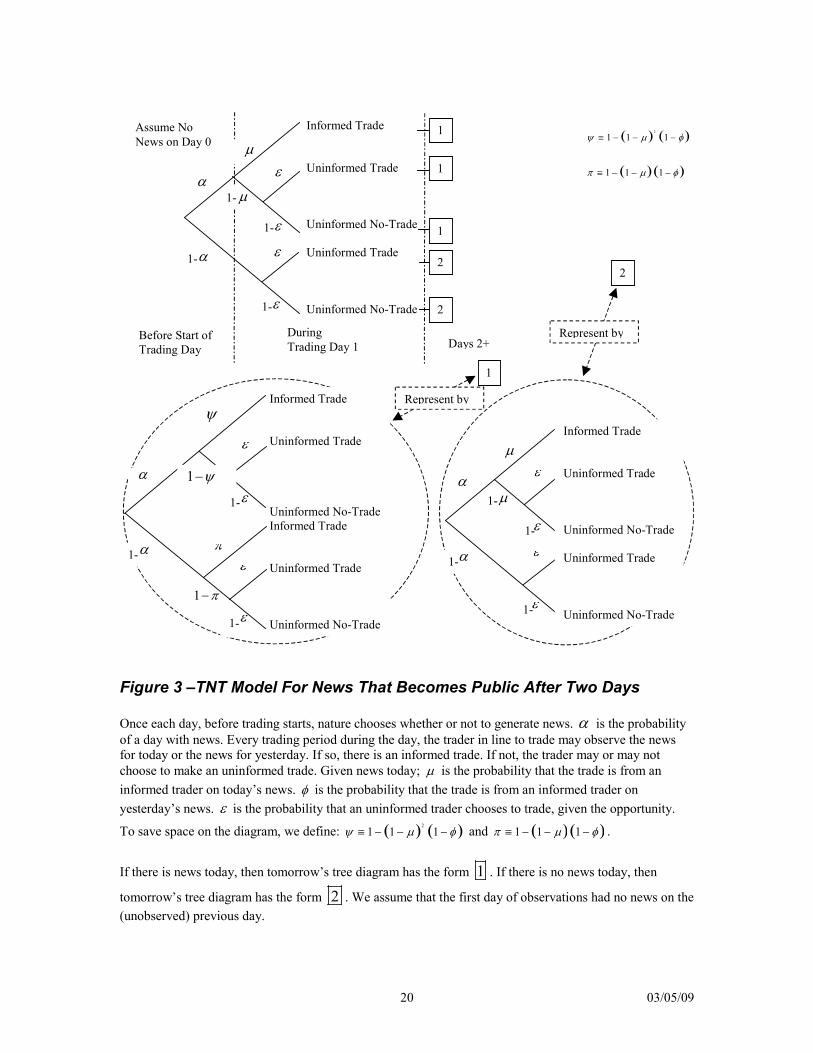

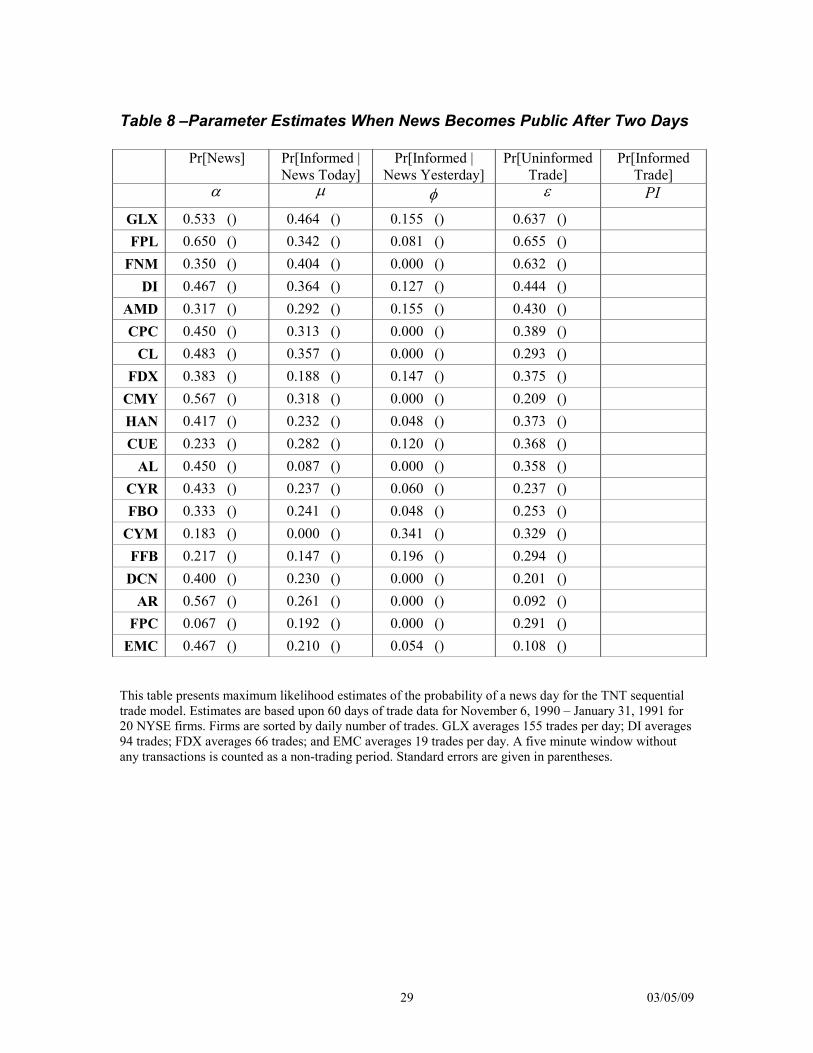

The TNT model can be adapted to model news that lasts more than one day. Figure 3

depicts a generalisation of the TNT model that allows for news that is revealed to the

public at the end of two days. A new parameter in the two-day model is � , the

probability that yesterday’s news is observed today, given that there was news yesterday.

� becomes the probability that today’s news is observed today, given that there is new

today. It seems plausible that the probability of observing news that has been around for a

while may differ from the probability of observing news that has recently been generated.

Yesterday’s informed trading may have lead to a search for yesterday’s news, increasing

the likelihood of it being observed. Alternatively, after yesterday’s informed trading,

much of the value of the news may already be incorporated into prices, reducing the

incentive to search for the old news.

Extending news beyond one day makes the two-day model considerably more complex

than the one-day news model. In particular, the two-day model is dependent upon the

order of days with and without news. Although it would be possible to write out the

03/05/0913

likelihood function for the two-day TNT model, the path dependence means that the

likelihood function is no longer a product of identical daily terms. We have implemented

estimation of the model in a recursive routine. Estimation is fairly fast, but a linearisation

of the log likelihood function is used to prevent overflow and underflow during the

likelihood maximisation. Table 8 presents parameter estimates for the two-day TNT

model. For firms in which news is independent from day to day, we would expect to see a

low value of � , because the probability of seeing yesterday’s news today is zero if the

news was revealed after one day. � should also be smaller than the estimate for the one-

day model, because we are weighting the case in which a trader sees yesterday’s news

yesterday. For firms in which news is not independent from day to day, we expect a non-

zero � , and because yesterday’s news is explaining some of today’s trading, we again

expect � to smaller than the estimate for the one-day model.

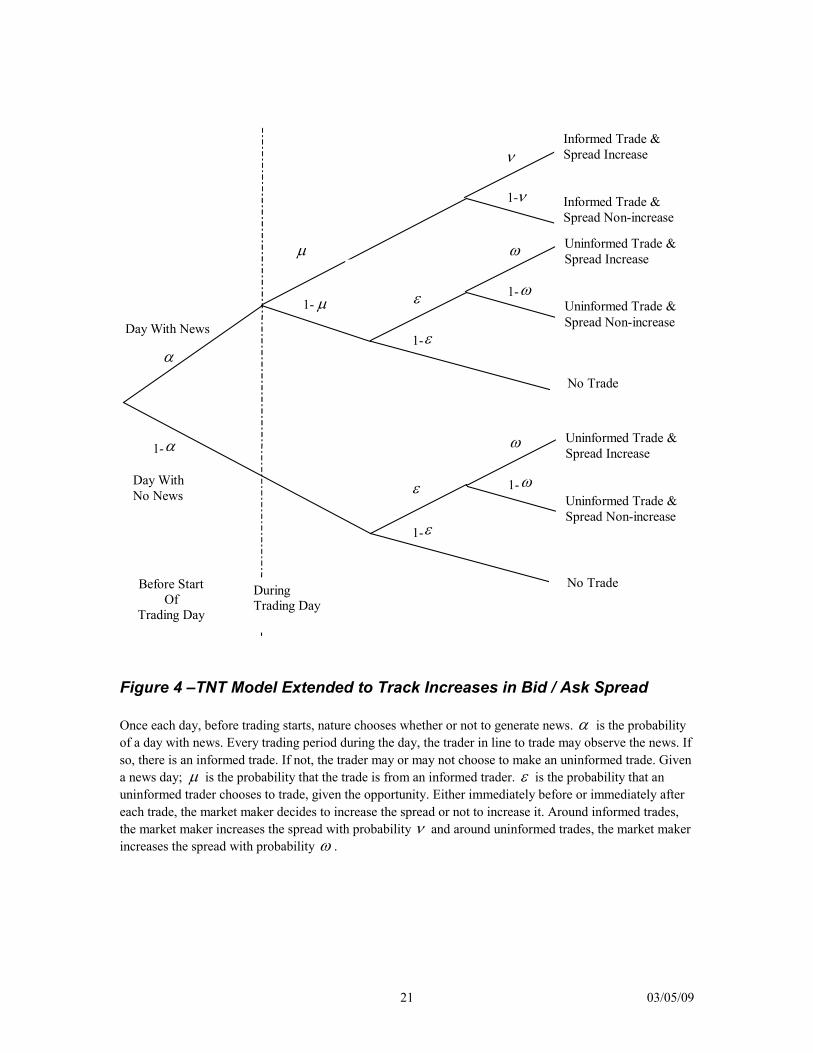

4. Extensions: Do Bid / Ask Spreads Respond to Trading?In their 1997 paper, Easley, Kiefer and O’Hara (EKO) demonstrate an extension of the

BSN model to test whether or not informed trades concentrate in larger trade sizes. EKO

find no evidence that larger trades are more likely to be informed trades. In another

paper, we intend to use the TNT model to give this intriguing result a thorough

examination. In this article, we will demonstrate how the TNT model can be extended to

study how market makers behave in changing the bid / ask spread.

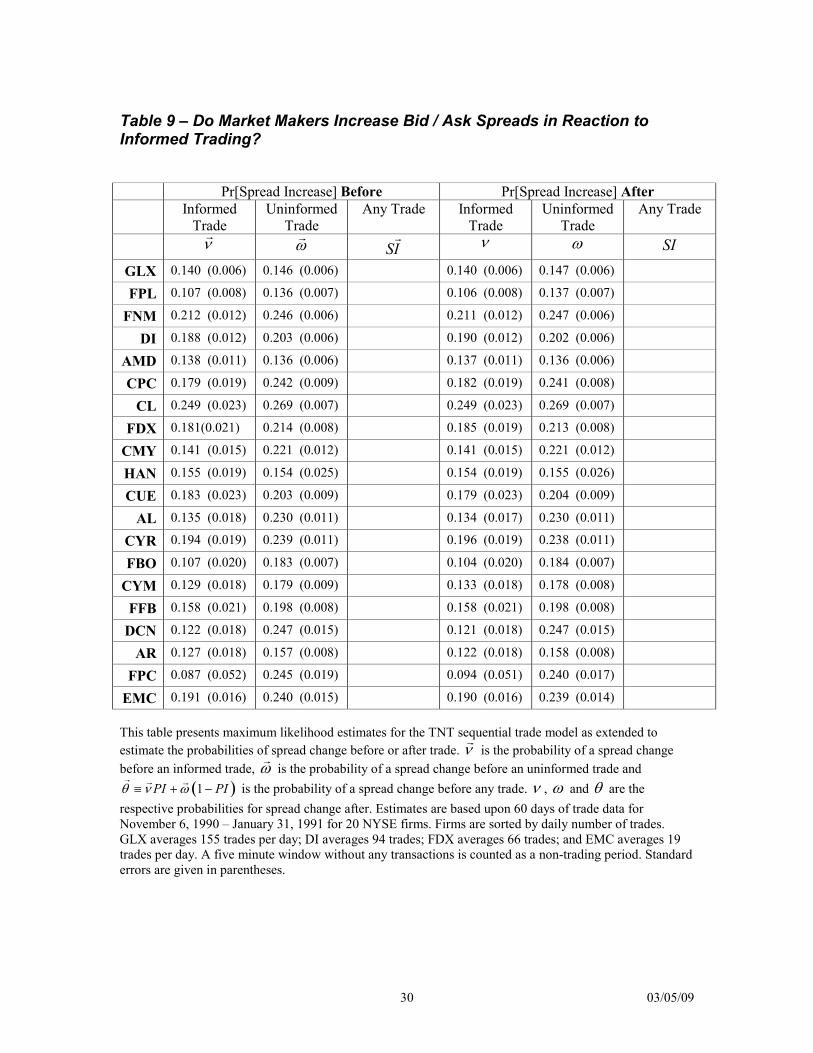

Do market makers increase the spread if they believe that informed traders are active? If

so, are the spreads increased before or after the informed trading? Can market makers

even distinguish informed from uninformed trades on average? To investigate these

03/05/0914

questions, we will use quote data in addition to transaction data to count when there is a

spread increase in conjunction with a trade and when there is no spread increase in

conjunction with a trade. Figure 4 depicts the diagram of the trading process for this

extended model. Two new parameters are added to the model. � is the probability that

the spread increases when there is an informed trade. � is the probability that the spread

increases when there is an uninformed trade.

Table 9 presents 60-day estimates of the model for the 20 NYSE firms. The model

parameters have been estimated twice for each firm – for counts of spread increases

before trade, � �,� �

� � , and for counts of spread increases after trade, � �,� � .6 Table 9 also

shows SI , the probability of a spread increase when there is any trade.

Look first at the question whether the spread tends to increase more often before or after

trade. There is no evidence that �� differs from � or that �� differs from � . Spreads are

not more likely to increase before a trade than after, whether that trade is informed or not.

Look next at the question whether or not the spread tends to increase more in conjunction

with informed than uninformed trading. The estimates of the probability of an increase

with informed trades are generally smaller than the estimates for informed trades, but the

difference is significant at the 5 percent level only for CPC, CMY, AL, FBO and FPC.

These results are similar whether we consider spread changes before or after trades. It

6 The quote time series corresponds to bid and ask quotes in effect at the time of market ordertransactions. The spread is the ask minus the bid. A spread change is calculated as the spread in effect forthe market order transaction at time t minus the spread in effect for the market order transaction at time t-1.Note that the spread may change more than once or not at all between market order transactions, it is thecumulative change that is calculated here.

03/05/0915

would seem that spreads are less likely to increase in conjunction with informed than

uninformed trading.

This result is an interpretation of the data in the context of the model. News days are not

observable. Days with relatively many trades are interpreted as days with news, and some

of the trades on these days are interpreted as informed. Given this, we conclude that

market makers prefer to increase spreads around uninformed trades. One might argue that

this result makes little sense, in that it suggests that market makers have some ability to

distinguish informed from uninformed trades, and that they prefer to increase the spread

around the uninformed trades. A more likely interpretation is that the spread increases for

uninformed trades are related to the lighter trading during days without news. At any

time, proportional spreads tend to be higher for lower volume stocks. For many of the

same reasons, one might expect to see time series variation in spread, reflecting

differences in volume from day to day.

5. ConclusionsWe have demonstrated the viability and usefulness of the trade / no-trade (TNT) model

that depends only upon transaction counts to infer features of market maker and trader

behavior. The model’s assumption of intermittent news performs well compared to one in

which news arrives every day. The model’s assumption of day-to-day independence of

the news is not well supported for many firms. We have shown that the model can be

extended to allow for news that lasts for one day.

Using an extension of the basic one-day news model, we find that market makers are no

more likely to increase the bid / ask spread before a trade than after. We do find that the

03/05/0916

spread is more likely to increase around an uninformed trade than around an informed

trade. This may simply reflect higher per share costs of market making under the lower

trade volume of days with no news.

03/05/0917

ReferencesEasley, D., S. Hvidkjaer, and M. O’Hara, 2002, “Is information risk a determinant of asset returns?,”Working paper.

Easley, D., N. Kiefer, and M. O’Hara, 1996, “Cream-skimming or profit-sharing? The curious role ofpurchased order flow,” Journal of Finance, 51, 811-833.

Easley, D., N. Kiefer, M. O’Hara, and J. Paperman, 1996, “Liquidity, information and infrequently tradedstocks,” Journal of Finance, 51, 1405-1436.

Easley, D., and M. O’Hara, 1987, “Price, trade size, and information in securities markets,” Journal ofFinancial Economics, 19, 69-90.

Easley, D., and M. O’Hara, 1997, “One day in the life of a very common stock,” Review of FinancialStudies, 10, 805-835.

Glosten, L., and P. Milgrom, 1985, “Bid, ask, and transaction prices in a specialist market withheterogeneously informed traders” Journal of Financial Economics, 13, 71-100.

Lee, C., and M. Ready, 1991, “Inferring trade direction from intraday data,” Journal of Finance, 46, 733-746.

Theissen, E., 2000, “A test of the accuracy of the Lee/Ready trade classification algorithm,” Journal ofInternational Financial Markets, Institutions & Money, 11, 147-165.

03/05/0918

Appendix

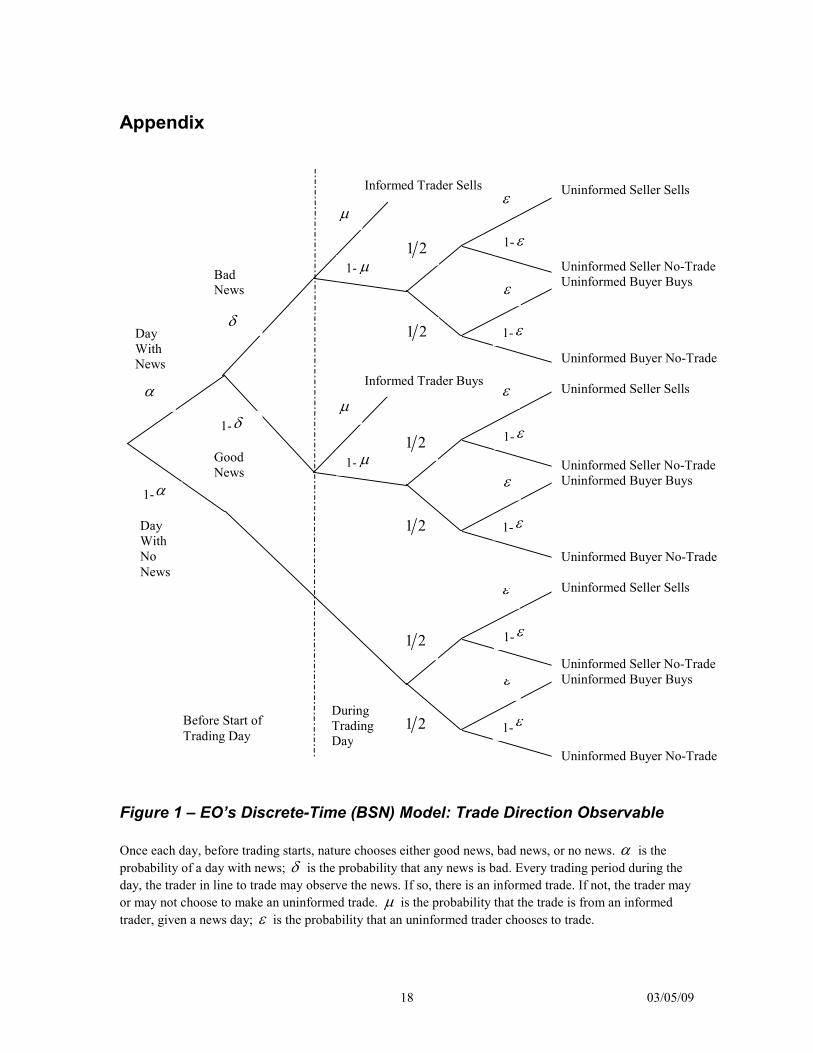

Figure 1 – EO’s Discrete-Time (BSN) Model: Trade Direction Observable

Once each day, before trading starts, nature chooses either good news, bad news, or no news. � is theprobability of a day with news; � is the probability that any news is bad. Every trading period during theday, the trader in line to trade may observe the news. If so, there is an informed trade. If not, the trader mayor may not choose to make an uninformed trade. � is the probability that the trade is from an informedtrader, given a news day; � is the probability that an uninformed trader chooses to trade.

Uninformed Seller Sells

Uninformed Seller No-TradeUninformed Buyer Buys

Uninformed Buyer No-Trade

Uninformed Seller Sells

Uninformed Seller No-TradeUninformed Buyer Buys

Uninformed Buyer No-Trade

Uninformed Seller Sells

Uninformed Seller No-TradeUninformed Buyer Buys

Uninformed Buyer No-Trade

�

�

1-�

1-�

�

�

1-�

1-�

�

�

1-�

1-�

1 2

1 2

1 2

1 2

�

1-�

�

1-�

DayWithNews

�

1-�

DayWithNoNews

BadNews

�

1-�

GoodNews

Informed Trader Sells

Informed Trader Buys

1 2

1 2

Before Start ofTrading Day

DuringTradingDay

03/05/0919

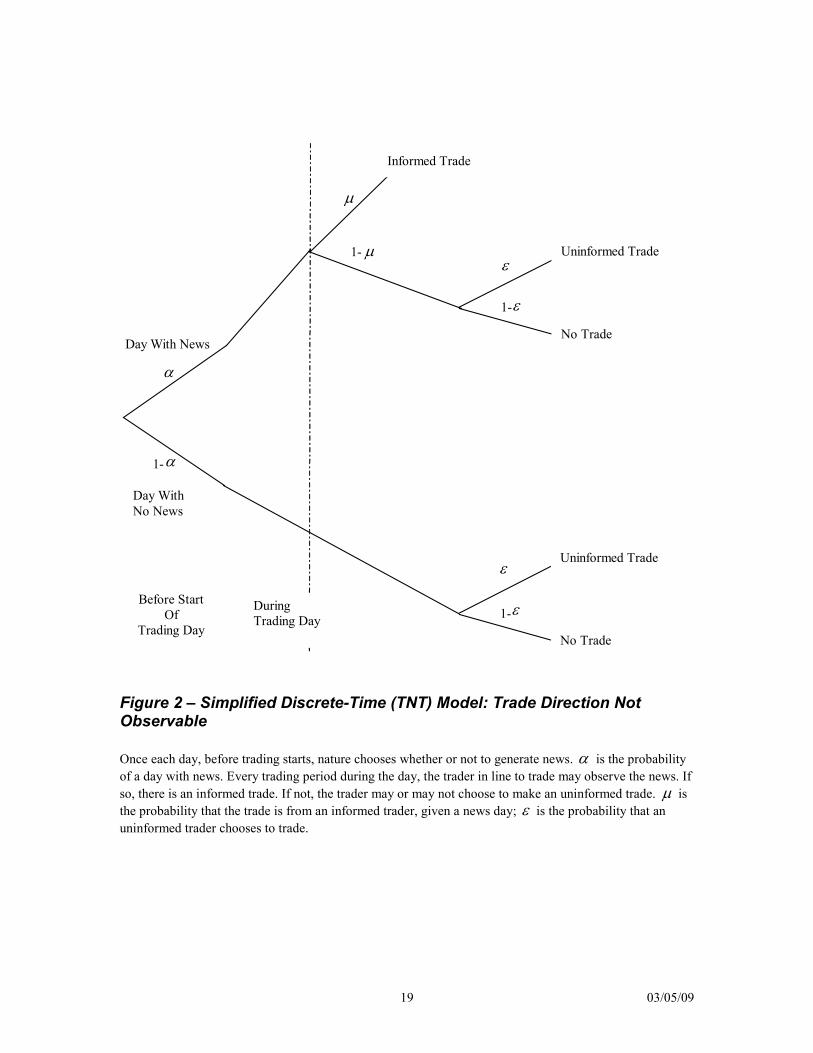

Figure 2 – Simplified Discrete-Time (TNT) Model: Trade Direction NotObservable

Once each day, before trading starts, nature chooses whether or not to generate news. � is the probabilityof a day with news. Every trading period during the day, the trader in line to trade may observe the news. Ifso, there is an informed trade. If not, the trader may or may not choose to make an uninformed trade. � isthe probability that the trade is from an informed trader, given a news day; � is the probability that anuninformed trader chooses to trade.

�

1-�

�

1-�

�

1- �

Day With News

�

1-� Day With No News

Informed Trade

Before Start Of

Trading Day

During Trading Day

Uninformed Trade

No Trade

Uninformed Trade

No Trade

03/05/0920

Before Start ofTrading Day

DuringTrading Day 1

Informed Trade

Uninformed Trade

Uninformed No-TradeInformed Trade

Uninformed Trade

Uninformed No-Trade

1 ��

�

�

1-�

1-�

�

�

1-��

Informed Trade

Uninformed Trade

Uninformed No-Trade

Uninformed Trade

Uninformed No-Trade

�

�

1-�

1-�

�

1-��

1-�

1

�

�

1-�

1-�

�

1-��

1-�

Informed Trade

Uninformed Trade

Uninformed No-Trade

Uninformed Trade

Uninformed No-Trade

Days 2+

Assume NoNews on Day 0

Represent by

Represent by

1

1

2

2

1 ��

1

2

� � � �2

1 1 1� � �� � � �

� � � �1 1 1� � �� � � �

Figure 3 –TNT Model For News That Becomes Public After Two Days

Once each day, before trading starts, nature chooses whether or not to generate news. � is the probabilityof a day with news. Every trading period during the day, the trader in line to trade may observe the newsfor today or the news for yesterday. If so, there is an informed trade. If not, the trader may or may notchoose to make an uninformed trade. Given news today; � is the probability that the trade is from aninformed trader on today’s news. � is the probability that the trade is from an informed trader onyesterday’s news. � is the probability that an uninformed trader chooses to trade, given the opportunity.

To save space on the diagram, we define: � � � �2

1 1 1� � �� � � � and � � � �1 1 1� � �� � � � .

If there is news today, then tomorrow’s tree diagram has the form 1 . If there is no news today, then

tomorrow’s tree diagram has the form 2 . We assume that the first day of observations had no news on the(unobserved) previous day.

03/05/0921

Figure 4 –TNT Model Extended to Track Increases in Bid / Ask Spread

Once each day, before trading starts, nature chooses whether or not to generate news. � is the probabilityof a day with news. Every trading period during the day, the trader in line to trade may observe the news. Ifso, there is an informed trade. If not, the trader may or may not choose to make an uninformed trade. Givena news day; � is the probability that the trade is from an informed trader. � is the probability that anuninformed trader chooses to trade, given the opportunity. Either immediately before or immediately aftereach trade, the market maker decides to increase the spread or not to increase it. Around informed trades,the market maker increases the spread with probability � and around uninformed trades, the market makerincreases the spread with probability � .

�

1-�

�

1- �

Day With News

�

1-� Day With No News

�

1-�

Before Start Of

Trading Day

During Trading Day

No Trade

�

1-�

�

1-�

�

1-�

Informed Trade & Spread Increase

Informed Trade & Spread Non-increase

Uninformed Trade & Spread Increase

Uninformed Trade & Spread Non-increase

No Trade

Uninformed Trade & Spread Increase

Uninformed Trade & Spread Non-increase

03/05/0922

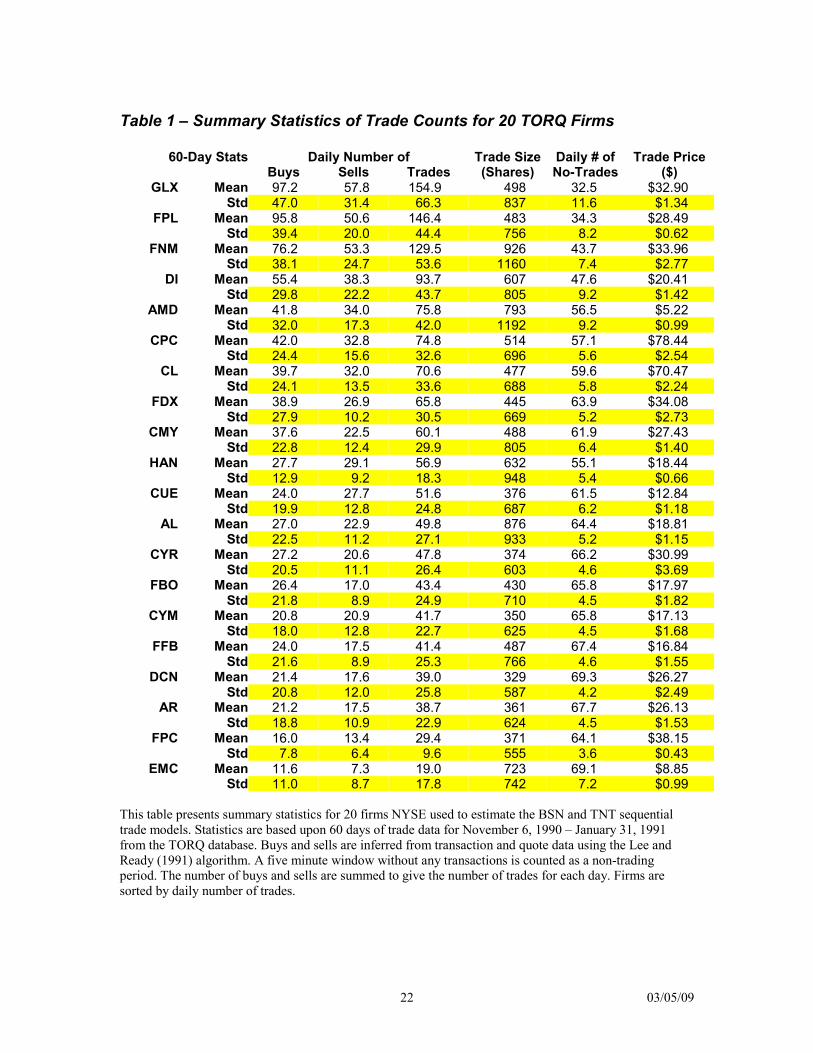

Table 1 – Summary Statistics of Trade Counts for 20 TORQ Firms

60-Day Stats Daily Number of Trade Size Daily # of Trade PriceBuys Sells Trades (Shares) No-Trades ($)

This table presents summary statistics for 20 firms NYSE used to estimate the BSN and TNT sequentialtrade models. Statistics are based upon 60 days of trade data for November 6, 1990 – January 31, 1991from the TORQ database. Buys and sells are inferred from transaction and quote data using the Lee andReady (1991) algorithm. A five minute window without any transactions is counted as a non-tradingperiod. The number of buys and sells are summed to give the number of trades for each day. Firms aresorted by daily number of trades.

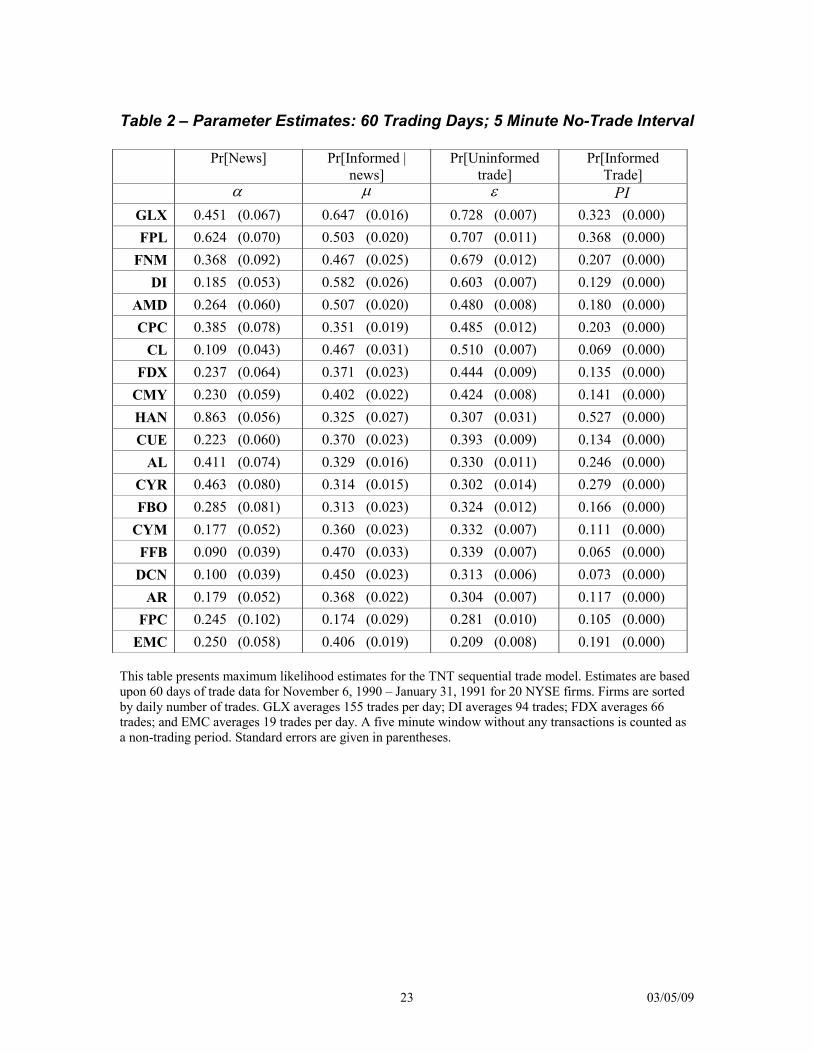

This table presents maximum likelihood estimates for the TNT sequential trade model. Estimates are basedupon 60 days of trade data for November 6, 1990 – January 31, 1991 for 20 NYSE firms. Firms are sortedby daily number of trades. GLX averages 155 trades per day; DI averages 94 trades; FDX averages 66trades; and EMC averages 19 trades per day. A five minute window without any transactions is counted asa non-trading period. Standard errors are given in parentheses.

03/05/0924

Table 3 – Comparing Parameter Estimates, with and without TradeDirection: Ashland Oil

This table presents maximum likelihood parameter estimates for the BSN and TNT sequential trademodels. Asymptotic standard errors are given in parentheses. Estimation uses 30 days of trade data forAshland Oil (October 1, 1990 – November 9, 1990) as supplied in Table 1 of EO (1987). Buys and sells areinferred from transaction and quote data using the Lee and Ready (1991) algorithm. A five minute windowwithout any transactions is counted as a non-trading period. The number of buys and sells are summed togive the number of trades for each day.

03/05/0925

Table 4 – Comparing Parameter Estimates, With and Without TradeDirection: Selected TORQ Firms

This table presents maximum likelihood parameter estimates for the BSN and TNT sequential trade modelsfor four NYSE firms chosen to represent a range of trading activity. GLX averages 155 trades per day; DIaverages 94 trades; FDX averages 66 trades; and EMC averages 19 trades per day. Estimation uses 60 daysof trade data from the TORQ database (November 6, 1990 – January 31, 1991).Estimates are shown for thefull 60 days and for the two 30-day sub-periods. Buys and sells are inferred from transaction and quote datausing the Lee and Ready (1991) algorithm. A five minute window without any transactions is counted as anon-trading period. The number of buys and sells are summed to give the number of trades for each day.Standard errors are given in parentheses.

The parameters of the models are � , � , � and � . � is the probability of a news day. Conditional onnews, � is the probability that the news is bad and � is the probability that an informed trader comesforward to trade. � is the probability that an uninformed investor chooses to trade, given the opportunity.

03/05/0926

Table 5 – Comparing Parameter Estimates for Different No-Trade Intervals

Maximum likelihood parameter estimates for the BSN and TNT trade models using different no-trade intervals.Respectively, a one, two, five or ten minute window without transactions is counted as a non-trading period.Results are shown for four NYSE firms chosen to represent a range of trading activity. GLX averages 155 tradesper day; DI averages 94 trades; FDX averages 66 trades; and EMC averages 19 trades per day. Estimation uses 60days of trade data from the TORQ database (November 6, 1990 – January 31, 1991). Standard errors are given inparentheses.

The model parameters are: � is the probability of a news day, � the probability that the current trader isinformed and � the probability that an uninformed investor chooses to trade. Derived parameter of the model are,

� �� �1� � � � �� � � the fraction of informed trades on a news day and PI � �� the fraction of informed trades.

03/05/0927

Table 6 – Runs Tests for Independence of News from Day to Day

This table present runs tests for the hypothesis that news events are independent from day to day. Becausethe presence of news cannot be observed, estimates of the probability of news, � , from Table 6 are used tocategorize trading days as days with or without news. For each firm, daily trade counts are sorted. The� �60 �� ’th highest trade count is taken as the demarcation point. Days with more than this number oftrades are classified as news days (denoted by 1’s) and days with fewer trades are taken as no-news days(denoted by 0’s). Days with exactly this number of trades are ignored. Runs of 1’s and 0’s are totaled forthe 60 trading days. Under the null hypothesis of day-to-day independence of the news, the number of runshas a normal distribution with:

2 1n mMeann m�

� �

�

and � �

� � � �2

2 21

1n m n m n m

Variancen m n m� � � � �

� �

� � � �

,

where n is the number of news days and m is the number of no-news days.

Estimates are based upon 60 days of trade data for November 6, 1990 – January 31, 1991 for 20 NYSEfirms. Firms are sorted by daily number of trades. GLX averages 155 trades per day; DI averages 94 trades;FDX averages 66 trades; and EMC averages 19 trades per day. Standard errors are given in parentheses. Anasterisk indicates rejection of the null at the 5 percent level.

03/05/0928

Table 7 – Autocorrelation of Trade Counts for the 20 TORQ Firms

This table presents autocorrelations of daily trade counts for 20 NYSE firms used to estimate the BSN andTNT sequential trade models. Autocorrelation estimates are based upon 60 days of trade data for November6, 1990 – January 31, 1991. Firms are sorted by daily number of trades. p-values are shown in parentheses.An asterisk indicates a first order autocorrelation that is different from zero at the 5 percent level.

03/05/0929

Table 8 –Parameter Estimates When News Becomes Public After Two Days

This table presents maximum likelihood estimates of the probability of a news day for the TNT sequentialtrade model. Estimates are based upon 60 days of trade data for November 6, 1990 – January 31, 1991 for20 NYSE firms. Firms are sorted by daily number of trades. GLX averages 155 trades per day; DI averages94 trades; FDX averages 66 trades; and EMC averages 19 trades per day. A five minute window withoutany transactions is counted as a non-trading period. Standard errors are given in parentheses.

03/05/0930

Table 9 – Do Market Makers Increase Bid / Ask Spreads in Reaction toInformed Trading?

Pr[Spread Increase] Before Pr[Spread Increase] AfterInformed

This table presents maximum likelihood estimates for the TNT sequential trade model as extended toestimate the probabilities of spread change before or after trade. �

�

is the probability of a spread changebefore an informed trade, �

�

is the probability of a spread change before an uninformed trade and� �1PI PI� � �� � �

�

� �

is the probability of a spread change before any trade. � , � and � are therespective probabilities for spread change after. Estimates are based upon 60 days of trade data forNovember 6, 1990 – January 31, 1991 for 20 NYSE firms. Firms are sorted by daily number of trades.GLX averages 155 trades per day; DI averages 94 trades; FDX averages 66 trades; and EMC averages 19trades per day. A five minute window without any transactions is counted as a non-trading period. Standarderrors are given in parentheses.