25

Asian Development Outlook 2011 South-South Economic Links Joseph E. Zveglich, Jr. Assistant Chief Economist Economics and Research Department OECD Development Centre Paris 8 April 2011

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 1/25

Asian Development

Outlook 2011South-South Economic Links

Joseph E. Zveglich, Jr.

Assistant Chief Economist

Economics and Research Department

OECD Development Centre

Paris

8 April 2011

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 2/25

Outline

Economic outlook Global outlook

Developing Asia’s outlook

Key challenges Managing inflation

Finding new growth source:South-South economic links?

2

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 3/25

3

Key Messages

Asia’s recovery is firm, with growthnearing 8% in the next 2 years

Asia is leading the global recovery

Rising inflation is a concern

Expanding South-South links present asupplementary growth source

But structural weaknesses need to beaddressed to maximize their potential

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 4/25

Economic outlook

4

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 5/25

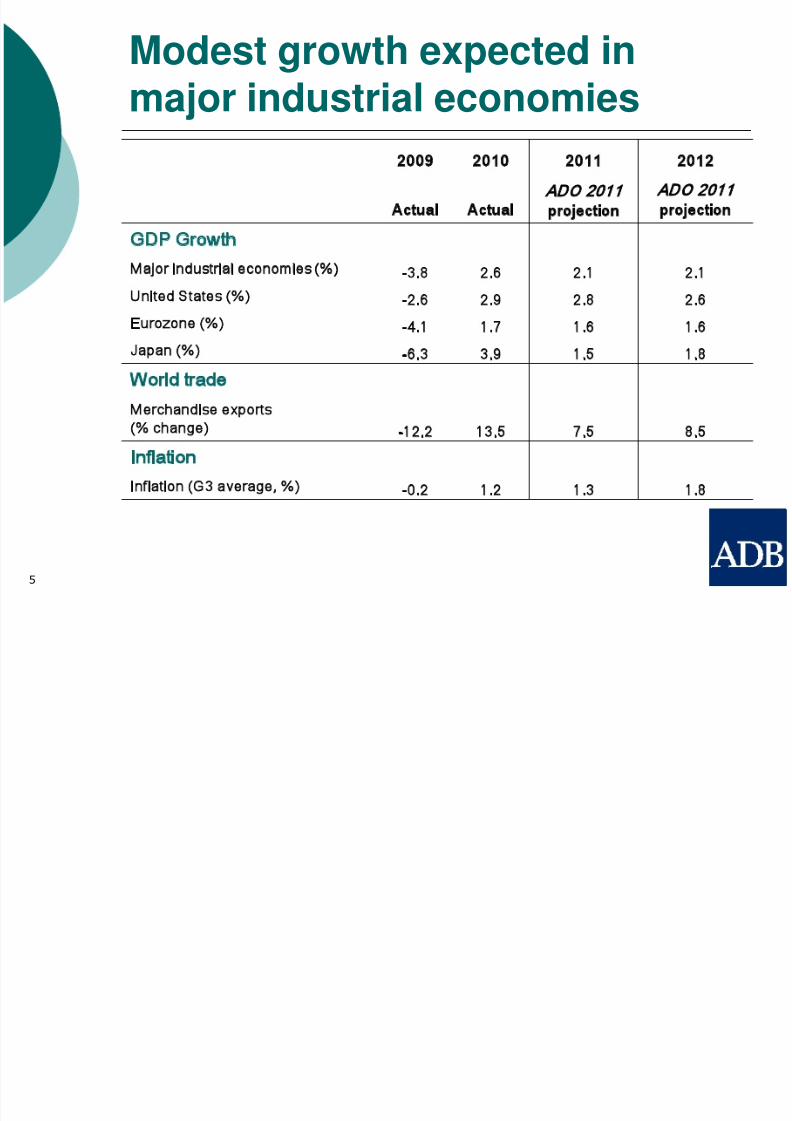

Modest growth expected inmajor industrial economies

2009 2010 2011 2012 Actual Actual ADO 2011

projection ADO 2011

projection GDP Growth

Major industrial economies

(%) -3.8 2.6 2.1 2.1United States (%) -2.6 2.9 2.8 2.6

Eurozone (%) -4.1 1.7 1.6 1.6

Japan (%) -6.3 3.9 1.5 1.8

World trade Merchandise exports(% change) -12.2 13.5 7.5 8.5

Inflation

Inflation (G3 average, %) -0.2 1.2 1.3 1.8

5

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 6/25

6

But risks remain

Recent surge in oil and foodprices

Sovereign debt problems in theeurozone periphery

High unemployment and weak

housing market in the US Impacts of the Japan earthquake

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 7/25

Developing Asia’s recovery is

firming

7

…due to robust domestic demand

9,4

10,1

6,75,9

9,07,8 7,7

0

4

8

12

2006 2007 2008 2009 2010 2011 2012

GDP growth

5-year moving average

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 8/258

-5

0

5

10

15

20

PRC INO KOR MAL PHI SIN THA

Percentage points

Contributions to GDP growthPrivate consumption Government consumption

Investment Net exports

Statistical discrepancy GDP growth

Propelled by robust domesticdemand

PRC=People’s Republic of China; INO=Indonesia; KOR=Republic of Korea;

MAL=Malaysia; PHI=Philippines; SIN=Singapore; THA=Thailand.

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 9/259

Region’s recovery is widespread

GDP growth

0

2

4

6

8

10

Central Asia

East Asia South Asia Southeast Asia

The Pacific Developing Asia

%2010 2011 2012

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 10/2510

Southeast Asia moderating

SEA=Southeast Asia

INO=Indonesia

SIN=Singapore

THA=Thailand

MAL=Malaysia

PHI=Philippines

VIE=Viet Nam

0

5

10

15

SEA INO MAL PHI SIN THA VIE

%GDP growth

2010 2011 2012

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 11/25

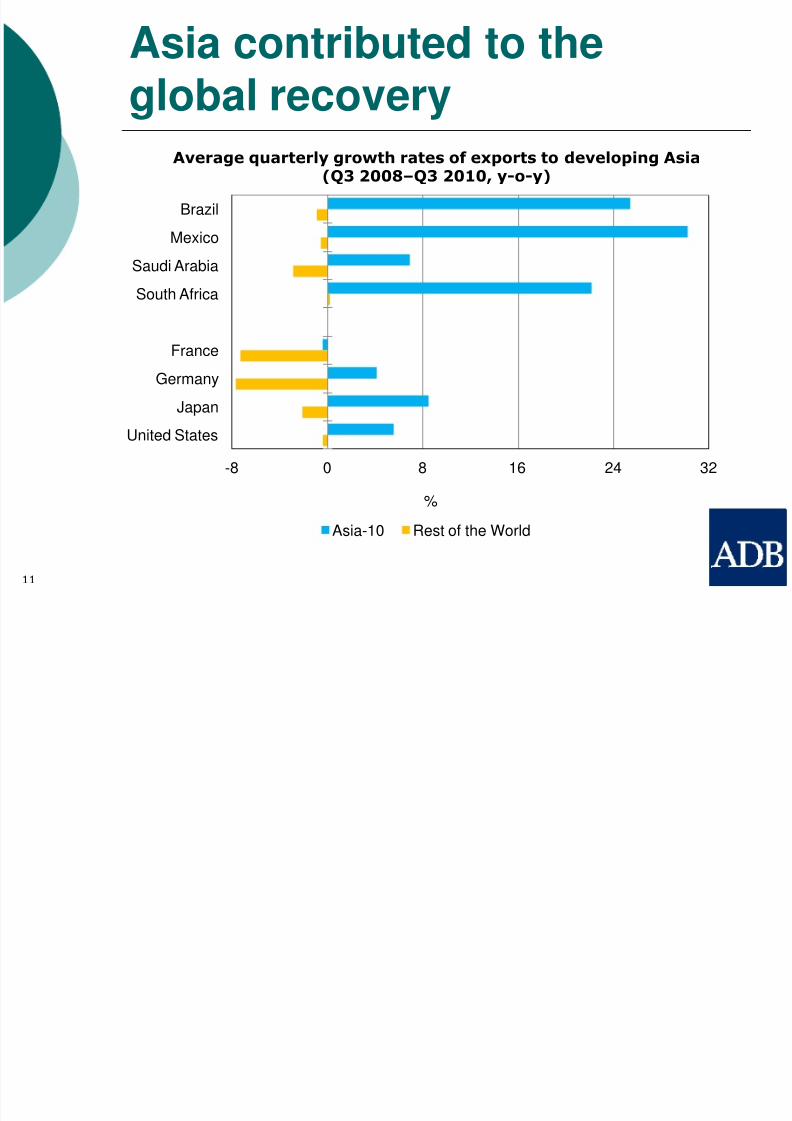

Asia contributed to theglobal recovery

11

-8 0 8 16 24 32

Brazil

Mexico

Saudi Arabia

South Africa

France

Germany

JapanUnited States

%

Asia-10 Rest of the World

Average quarterly growth rates of exports to developing Asia(Q3 2008–Q3 2010, y-o-y)

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 12/25

Key challenge:Managing inflation

12

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 13/25

Inflation pressures are building…

13

3,3

4,4

6,9

1,2

4,4

5,34,6

0

2

4

6

8

2006 2007 2008 2009 2010 2011 2012

%

Inflation

5-year moving average

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 14/25

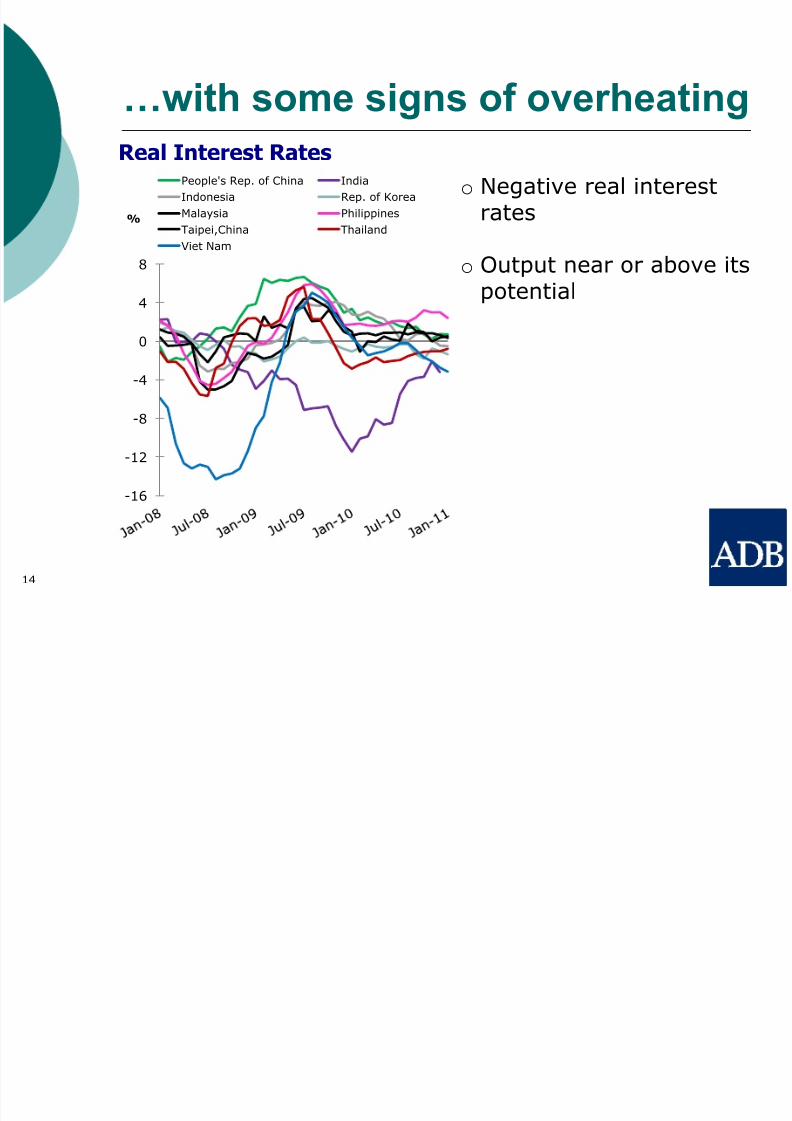

…with some signs of overheating

14

-16

-12

-8

-4

0

4

8

%

Real Interest RatesPeople's Rep. of China India

Indonesia Rep. of Korea

Malaysia Philippines

Taipei,China Thailand

Viet Nam

o Negative real interestrates

o Output near or above itspotential

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 15/25

Inflation matters more for Asia

Bangladesh 58.8

Philippines 46.6

India 46.2

Sri Lanka 45.5Cambodia 44.9

Pakistan 40.3

Viet Nam 39.9

Indonesia 36.2Thailand 33.0

Malaysia 31.4

PRC 30.2

United States 14.8

Eurozone 14.0

Japan 25.9

15

Food share in CPI (%)

o The poor are especiallyvulnerable

o Rising in part to Asia’sfaster recovery

o Inflation expectationscan fuel wage-pricespiral

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 16/25

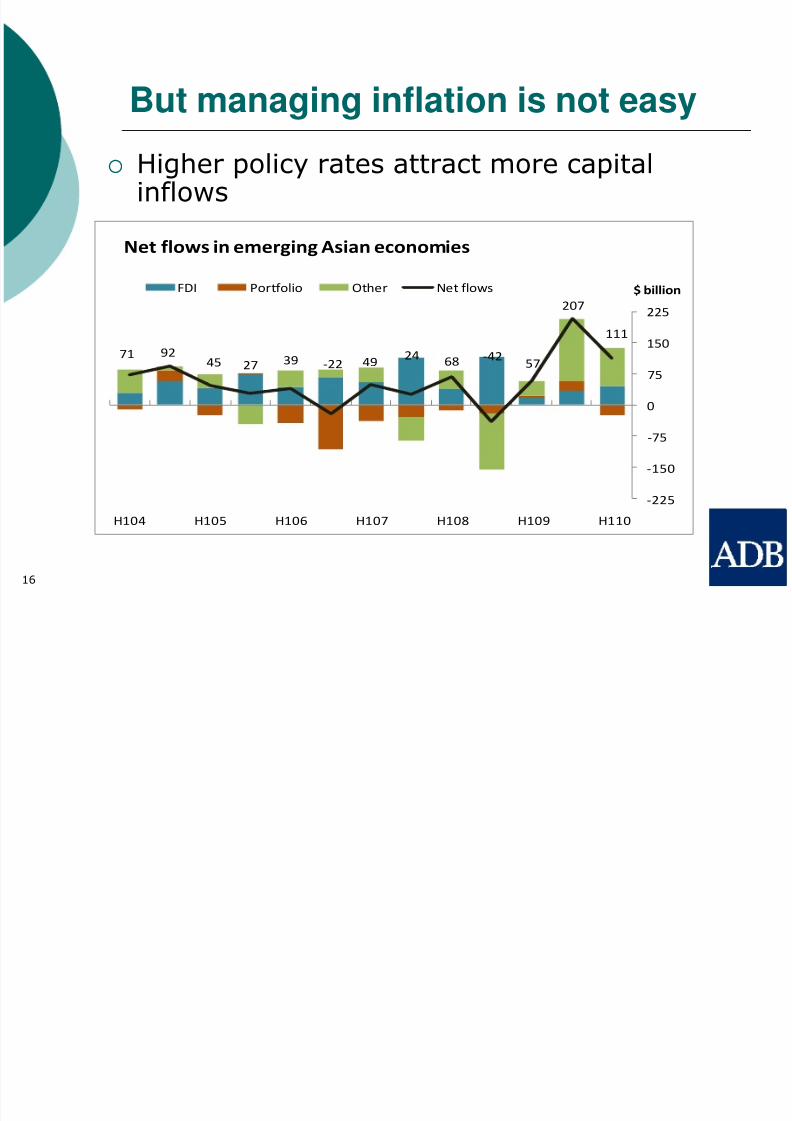

But managing inflation is not easy

Higher policy rates attract more capitalinflows

16

71 9245 27

39 -22 4924

68-42

57

207

111

-225

-150

-75

0

75

150

225

H104 H105 H106 H107 H108 H109 H110

$ billion

Net flows in emerging Asian economies

FDI Portfolio Other Net flows

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 17/25

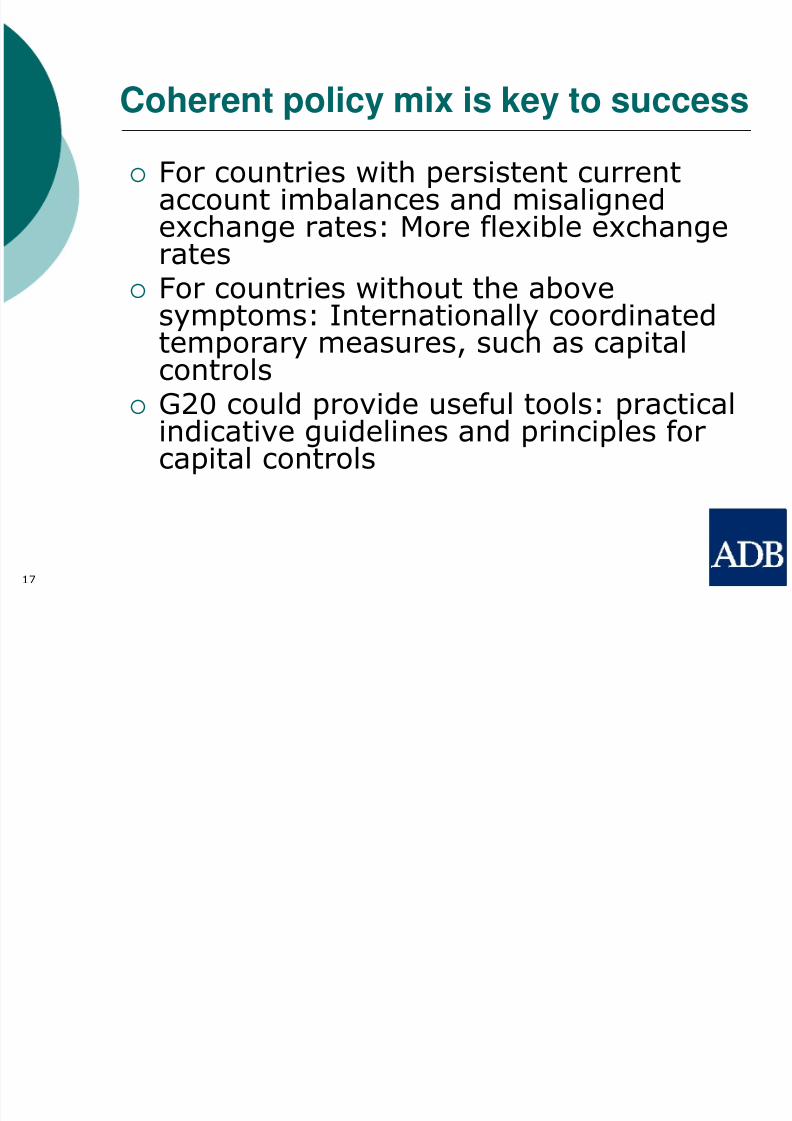

Coherent policy mix is key to success

For countries with persistent currentaccount imbalances and misalignedexchange rates: More flexible exchangerates

For countries without the abovesymptoms: Internationally coordinatedtemporary measures, such as capitalcontrols

G20 could provide useful tools: practicalindicative guidelines and principles forcapital controls

17

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 18/25

Key challenge:South-South economic links

18

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 19/25

Share of the South in global GDP isrising

Share of South in world GDP(%)

27

3233

37

45

0

10

20

30

40

50

1990 1995 2000 2005 2010

Developing Asia’s share in SouthGDP, 2010

PRC30%

OtherAsia

34%

OtherSouth36%

DevelopingAsia

64%

19

PRC = People’s Republic of China

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 20/2520

South-South trade is growing

Developing Asia’s share inSouth-South trade, 2009

OtherSouth26%

OtherAsia

34%

PRC40%

DevelopingAsia74%

Note: Merchandise trade, non-fuel

7

10

1516 17

1990—91* 2000—01* 2006—07* 2008 2009

South-South trade as share of world merchandise trade (%)

PRC = People’s Rep. of China

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 21/25

But developing Asia’s trade is driven

by factory Asia

0

10

20

30

40

50

60

97 99 01 03 05 07 09

(%)

Developing Asia PRC

Africa Latin America

0

10

20

30

40

50

60

97 99 01 03 05 07 09

(%)

Developing Asia PRC

Africa Latin America

Exports Imports

Share of parts and components (%)

21

• Factory Asia: intermediate goods sourced from South for assemblyand subsequent export to North

• Growing South-South links do not necessarily mean greater

economic independence!

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 22/25

Structural weaknesses need to beaddressed

22

4,25,5 5,1

3,73,2

19,6 20,6

16,0

12,1

9,3

0

5

10

15

20

25

1985-89 1990-94 1995-99 2000-04 2005-08

%

Applied tariffs, simple mean

North South

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 23/25

Other barriers remain too

Trade-relatedinfrastructure andlogistics performance

of the South lagconsiderably behindthe North

South-South FTAsare generally less

consistent with WTOand other global rules

23

2,0

2,5

3,0

3,5

North South

Average Logistic PerformanceIndex scores, North and South

2007 2010

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 24/25

Potential gains from strongerSouth-South links are large

Lowering tariffs could increaseSouth-South trade by 6% points

Industrial migration among theSouth could boost global growth

Recycling South savings for

investment could help globalrebalancing

24

8/3/2019 Inflation in SE Asia

http://slidepdf.com/reader/full/inflation-in-se-asia 25/25

Key Messages

Asia’s recovery is firm, with growthnearing 8% in the next 2 years

Asia is leading the global recovery

Rising inflation is a concern

Expanding South-South links present asupplementary growth source

But structural weaknesses need to beaddressed to maximize their potential