35

1 Inflation Targeting in an Uncertain External Backdrop Mário Mesquita October 2008 Inflation Targeting in an Uncertain External Backdrop Mário Mesquita October 2008

1

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

2

I. An Uncertain External Backdrop

3

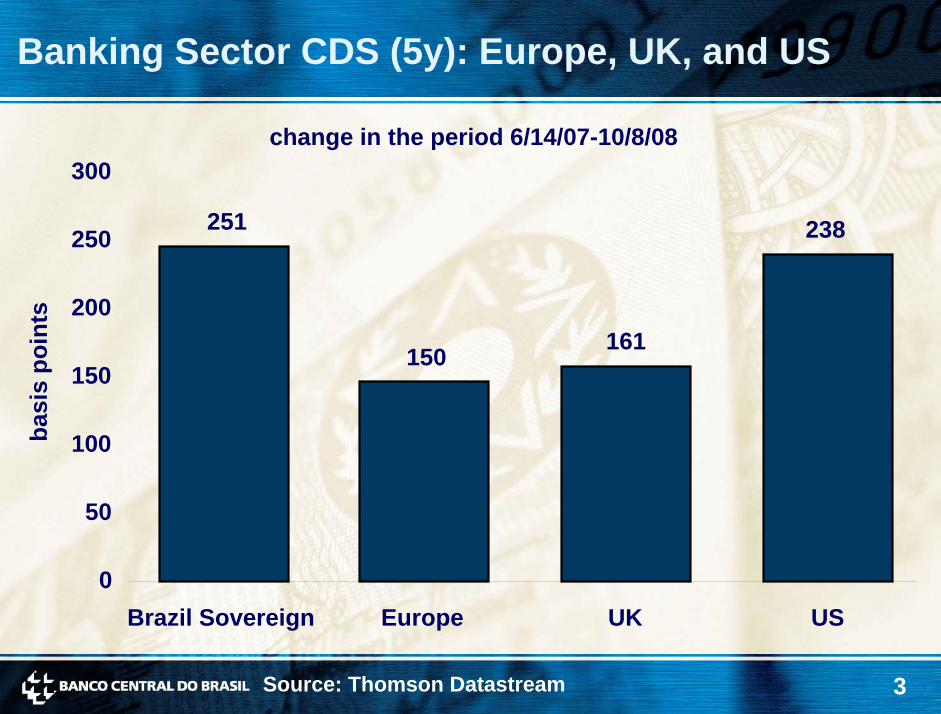

Banking Sector CDS (5y): Europe, UK, and US

change in the period 6/14/07-10/8/08300

Source: Thomson Datastream

basi

s po

ints

251 238250

200161150

150

100

50

0Brazil Sovereign UK USEurope

4

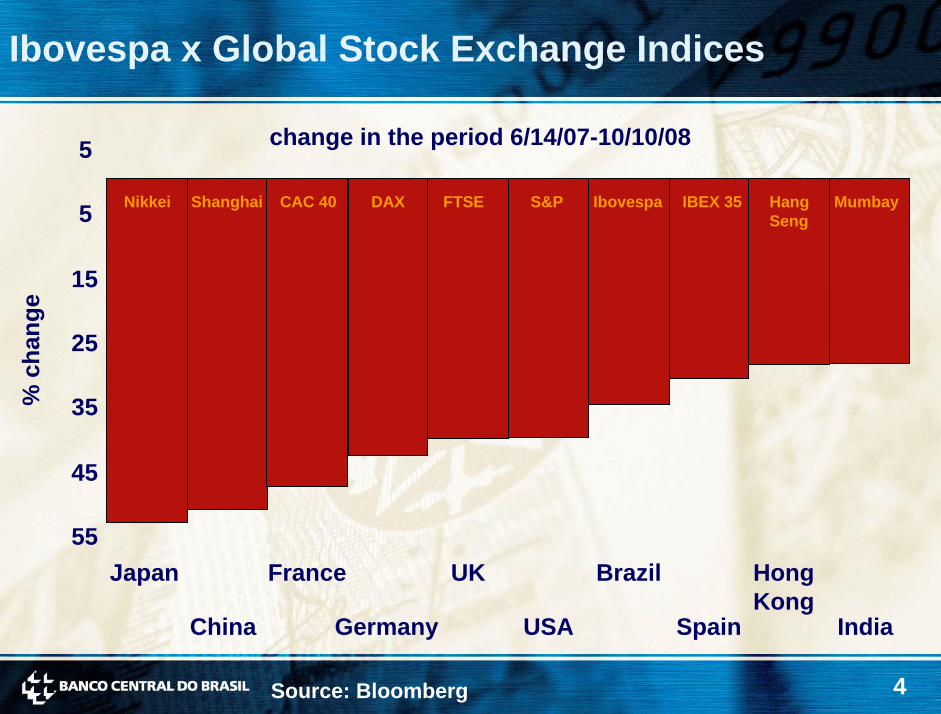

Ibovespa x Global Stock Exchange Indices

change in the period 6/14/07-10/10/085

MumbayShanghai CAC 40Nikkei FTSEDAX S&P HangSeng

Ibovespa IBEX 355

% c

hang

e

15

25

35

45

55Japan France UK Brazil Hong

KongChina Germany USA Spain India

Source: Bloomberg

5

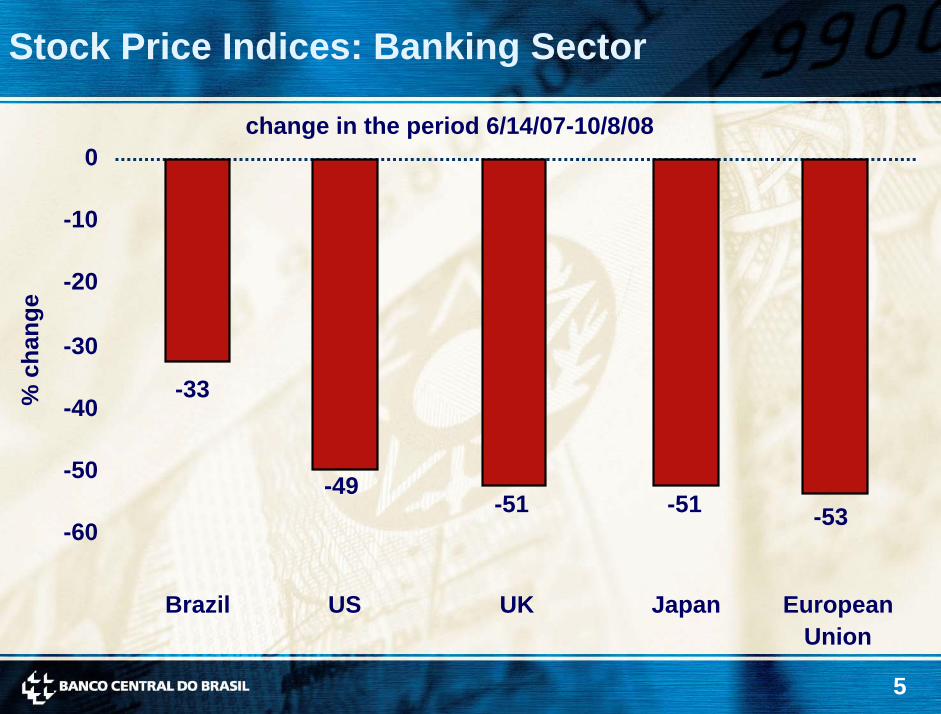

Stock Price Indices: Banking Sector

change in the period 6/14/07-10/8/080

-49-51 -51

-10

% c

hang

e

-20

-30

-33-40

-50

-53-60

Brazil US UK Japan EuropeanUnion

6

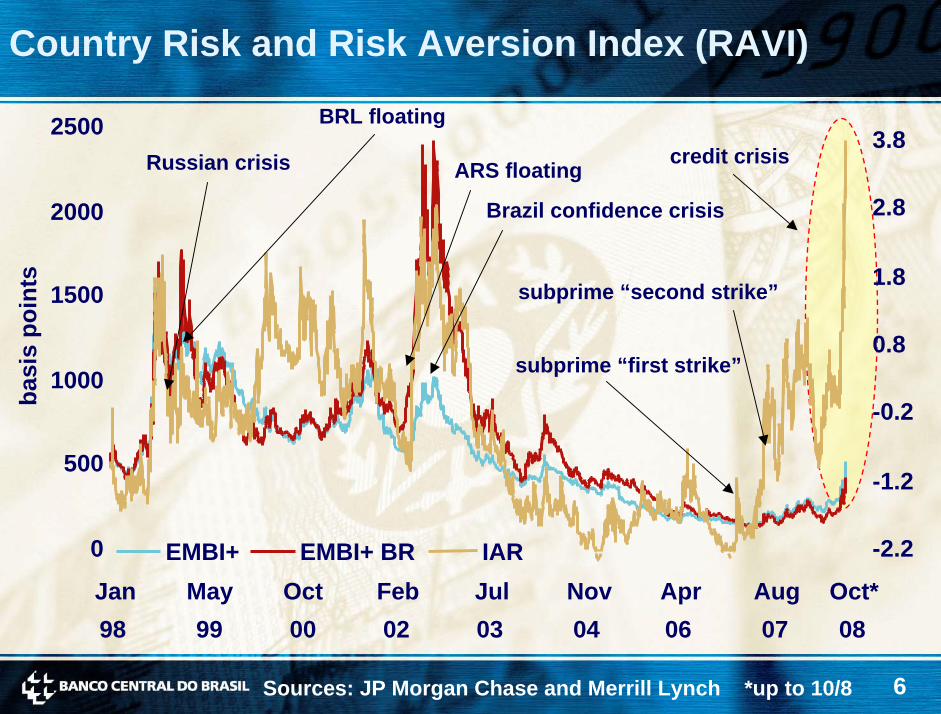

Country Risk and Risk Aversion Index (RAVI)

BRL floating

basi

s po

ints

Russian crisis ARS floating

Brazil confidence crisis

subprime “first strike”

subprime “second strike”

credit crisis

0

500

1000

1500

2000

2500

-2.2

-1.2

-0.2

0.8

1.8

2.8

3.8

EMBI+ EMBI+ BR IARJan May Oct Feb Jul Nov Apr Aug Oct*98 99 00 02 03 04 06 07 08

Sources: JP Morgan Chase and Merrill Lynch *up to 10/8

7

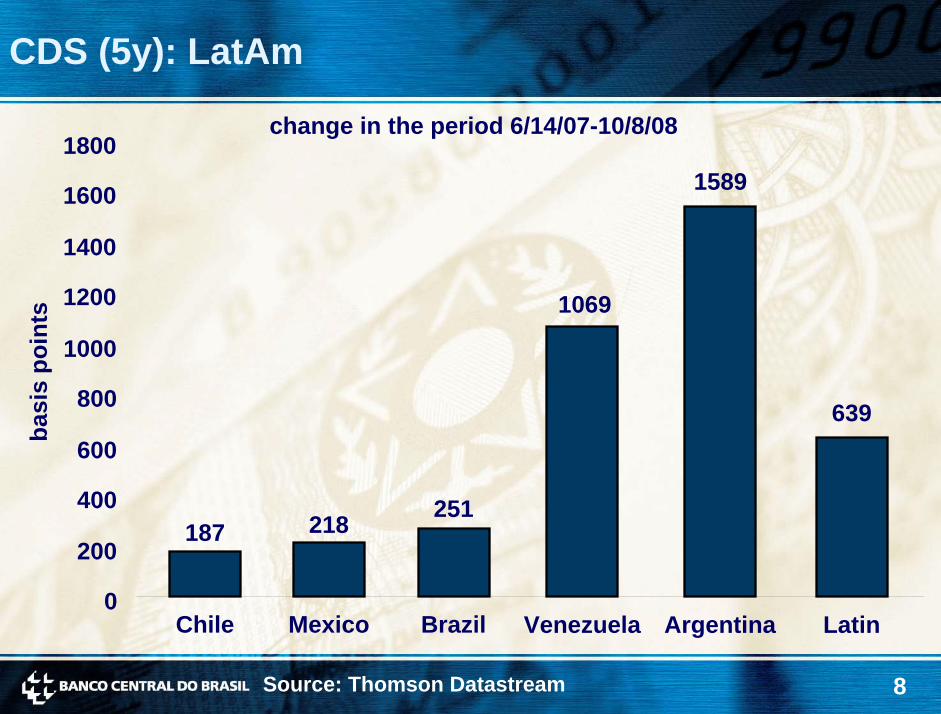

CDS (5y): LatAm

Brazil

Argentina

Venezuela

Mexico

Latin

Chile0

200

400

600

800

1000

1200

1400

1600

6/14 7/21 8/27 10/3 11/912/16 1/22 2/28 4/5 5/12 6/18 7/25 8/31 10/8

18006/14/07-10/8/08

basi

s po

ints

Source: Thomson Datastream

8

CDS (5y): LatAm

change in the period 6/14/07-10/8/081800

15891600

basi

s po

ints

1400

1200 1069

1000

800 639600

400 251218187200

0Chile BrazilMexico LatinArgentinaVenezuela

Source: Thomson Datastream

9

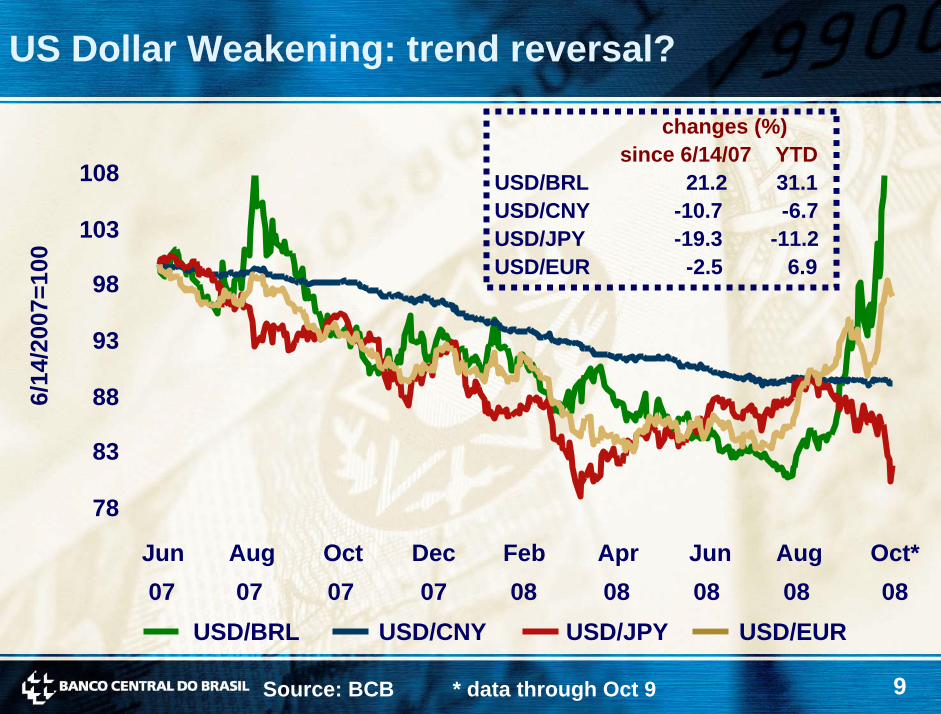

US Dollar Weakening: trend reversal?

changes (%)since 6/14/07 YTD

USD/BRL 21.2 31.1USD/CNY -10.7 -6.7USD/JPY -19.3 -11.2USD/EUR -2.5 6.9

108

6/14

/200

7=10

0

103

98

93

88

83

78

Jun Aug Oct Dec Feb Apr Jun Aug Oct*07 07 07 07 08 08 08 08 08

USD/BRL USD/CNY USD/JPY USD/EUR

Source: BCB * data through Oct 9

10

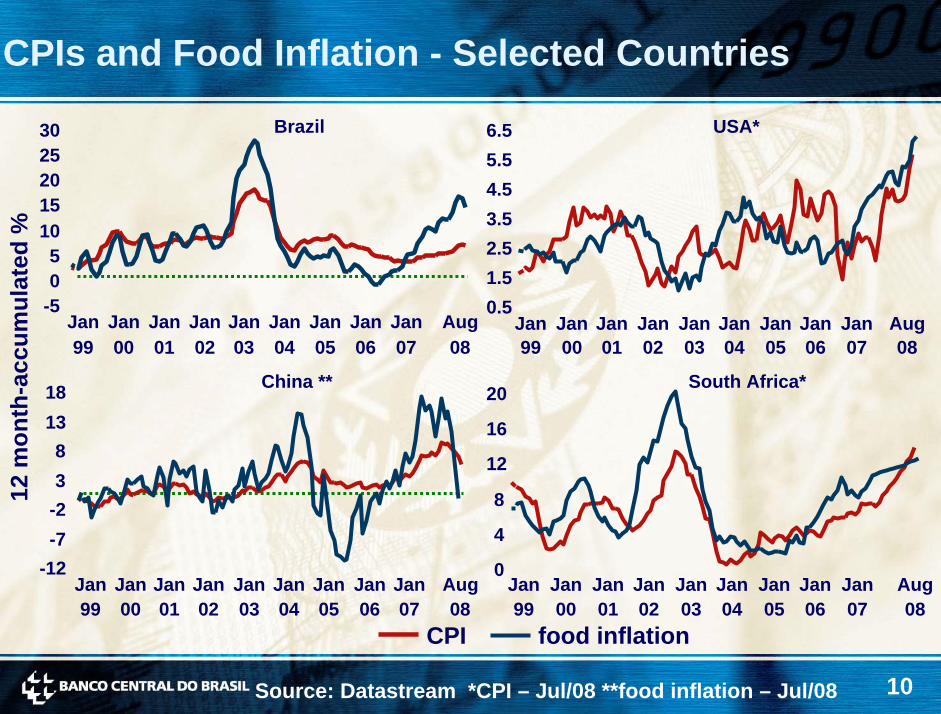

CPIs and Food Inflation - Selected Countries12

mon

th-a

ccum

ulat

ed %

CPI99 00 01 02 03 04 05 06 07

China **

-12-7-238

1318

Jan Jan Jan Jan Jan Jan Jan Jan Jan Aug08

Brazil

-505

1015202530

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

USA*

0.51.52.53.54.55.56.5

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

South Africa*

0

4

8

12

16

20

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

food inflation

Source: Datastream *CPI – Jul/08 **food inflation – Jul/08

11

II. Brazil: Increased Resilience to Shocks

12

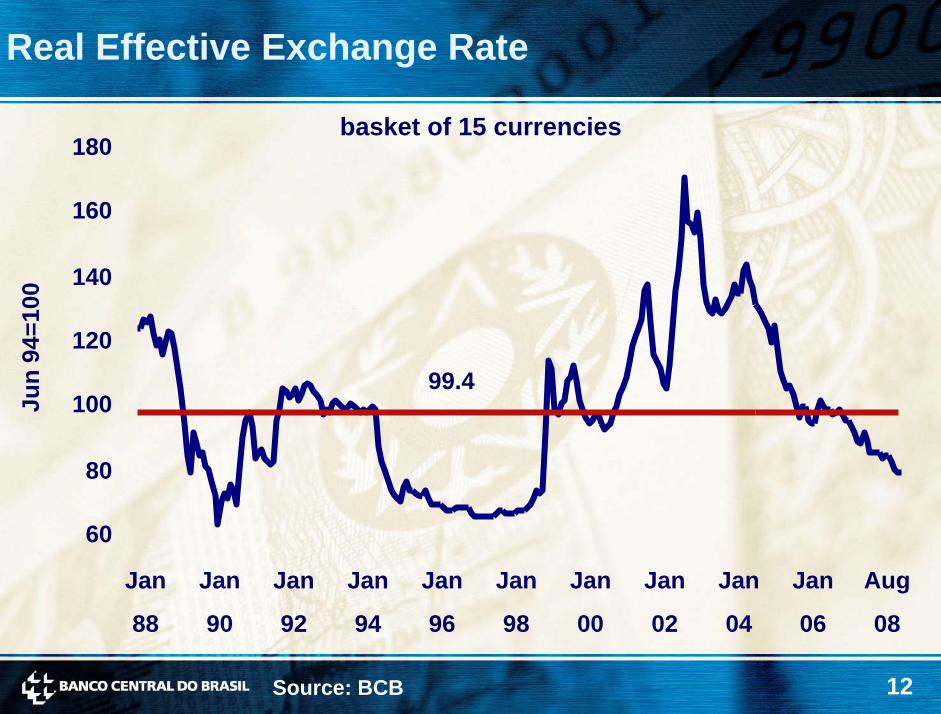

Real Effective Exchange Rate

basket of 15 currencies180

99.4

160

Jun

94=1

00

140

120

100

80

60

Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Aug

88 90 92 94 96 98 00 02 04 06 08

Source: BCB

13

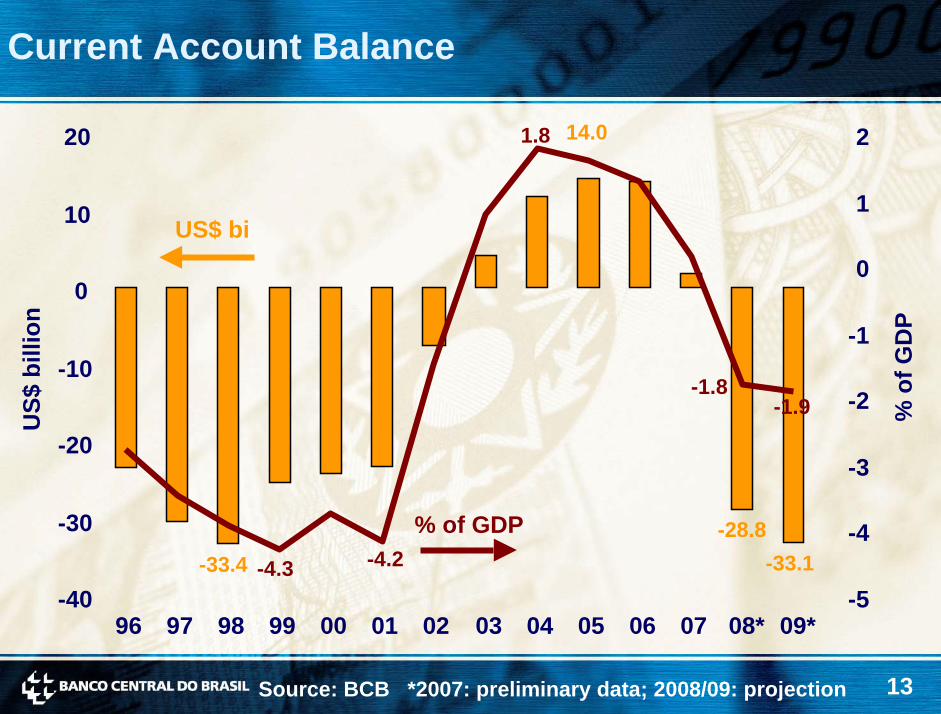

Current Account Balance

-33.4-28.8

-33.1

14.0

-1.9

-4.3 -4.2

-1.8

1.8

US$ bi

% of GDP

20 2

110

0

US$

bill

ion

0

% o

f GD

P-1-10

-2

-20-3

-30 -4

-5-4096 97 98 99 00 01 02 03 04 05 06 07 08* 09*

Source: BCB *2007: preliminary data; 2008/09: projection

14

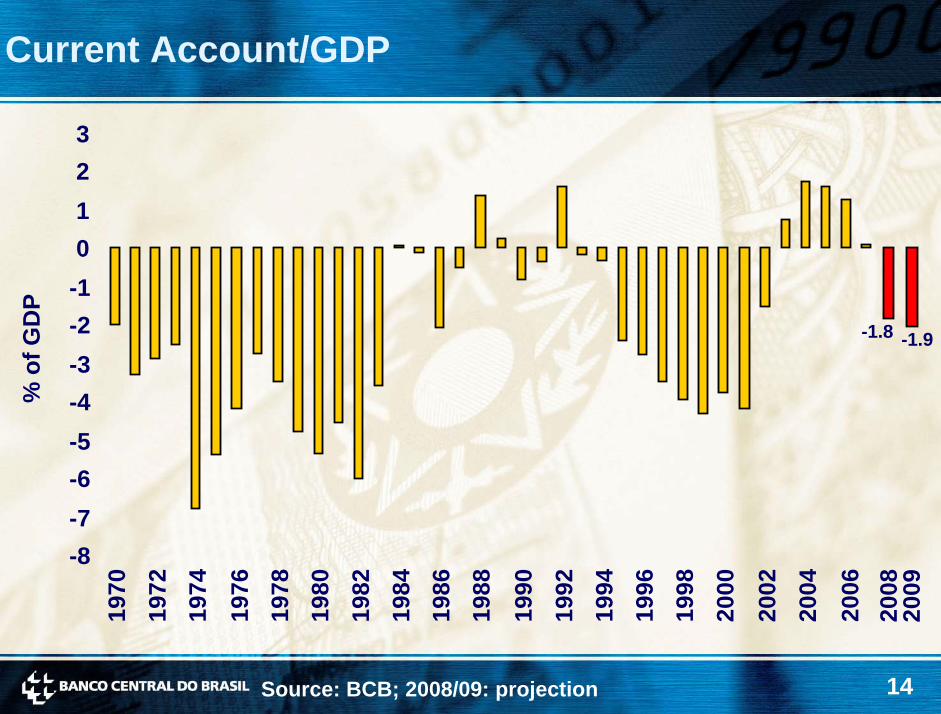

Current Account/GDP

3210

% o

f GD

P

Source: BCB; 2008/09: projection

-8-7-6-5-4-3-2-1

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2009

-1.8 -1.9

15

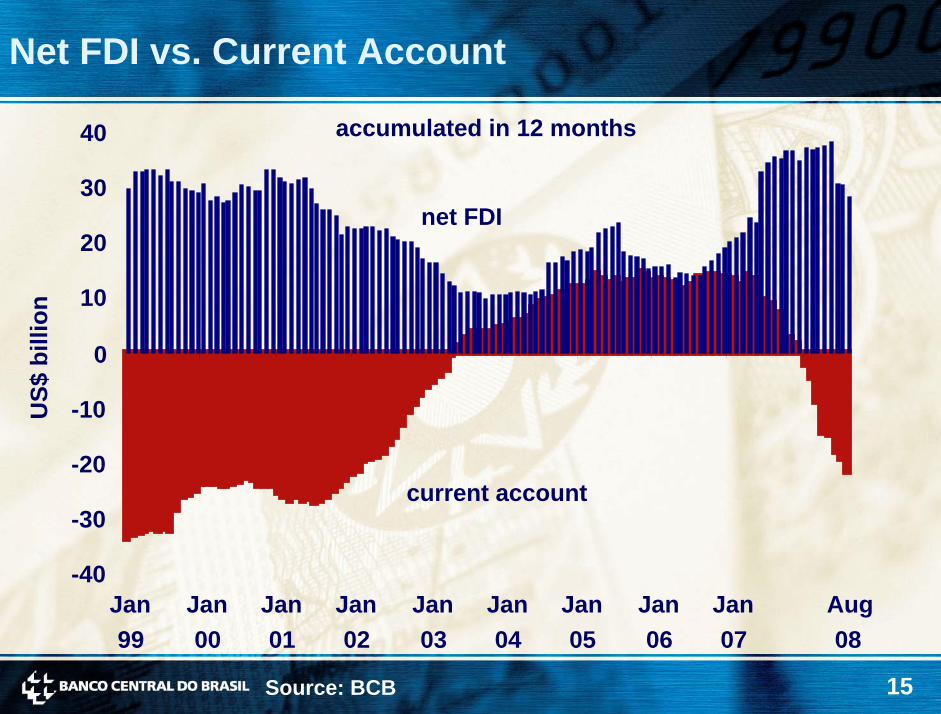

Net FDI vs. Current Account

current account

accumulated in 12 months

net FDI

40

30

20

US$

bill

ion 10

0

-10

-20

-30

-40Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

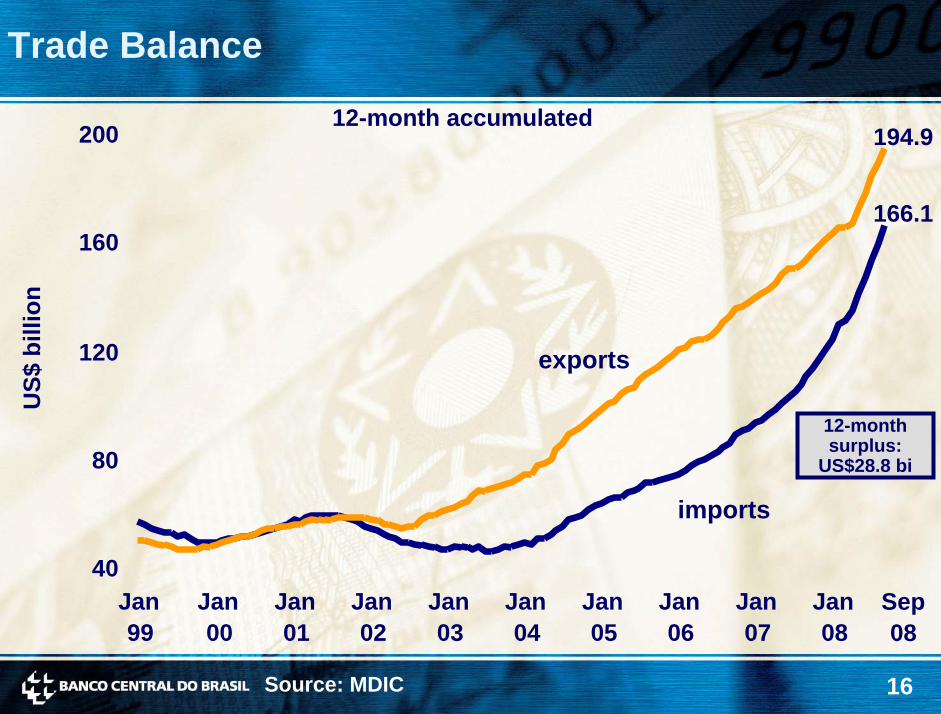

16

Trade Balance

12-month accumulated

exports

imports

US$

bill

ion

12-monthsurplus:

US$28.8 bi

194.9

166.1

40

80

120

160

200

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Sep08

Source: MDIC

17

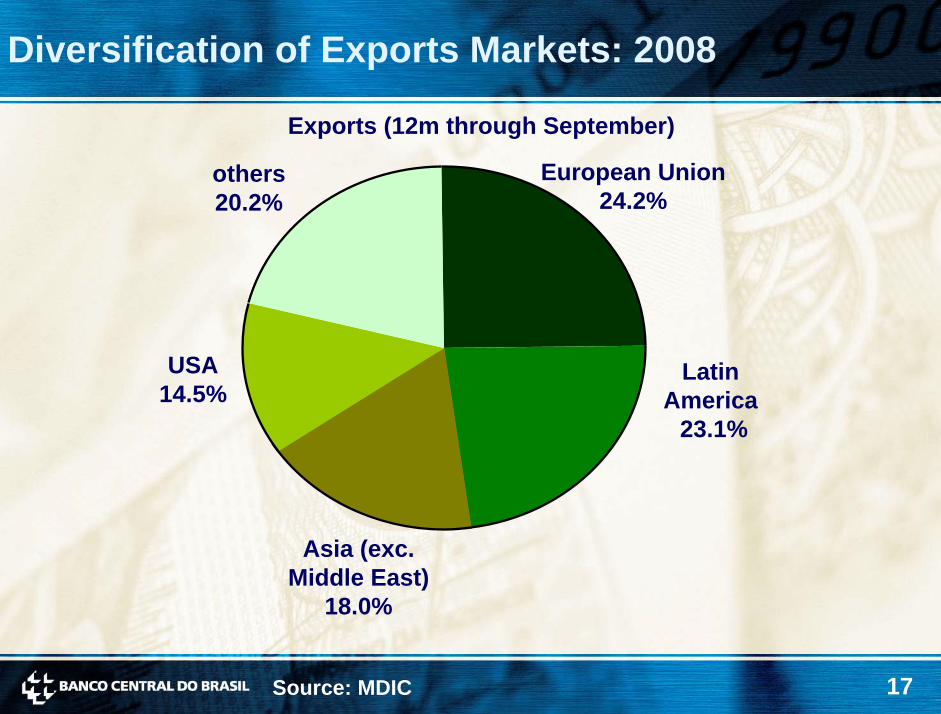

Diversification of Exports Markets: 2008

Exports (12m through September)

USA14.5%

others20.2%

European Union24.2%

LatinAmerica

23.1%

Asia (exc. Middle East)

18.0%

Source: MDIC

18

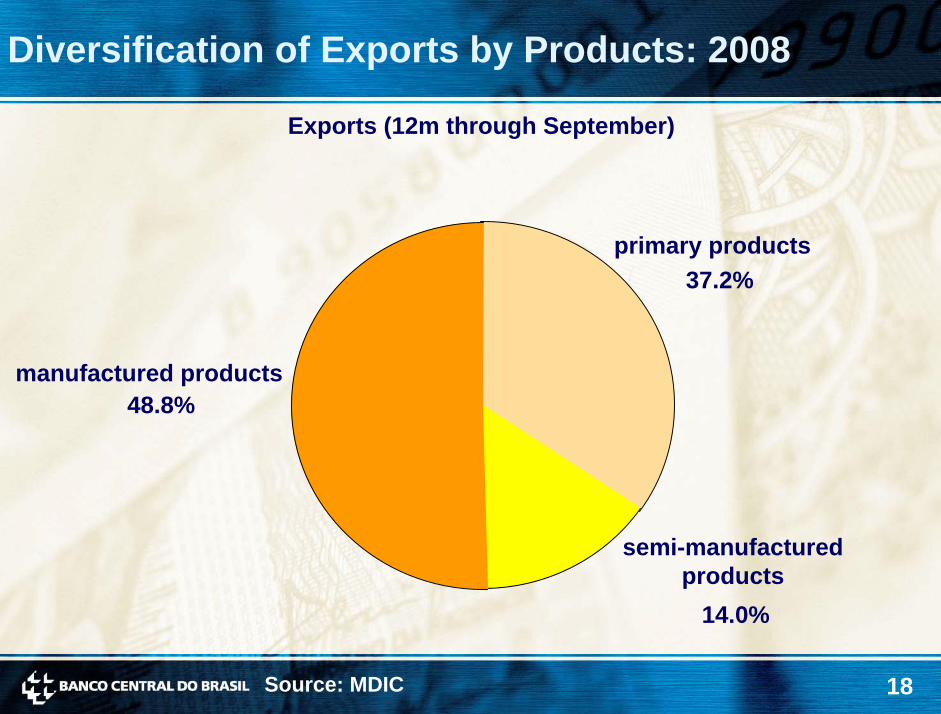

Diversification of Exports by Products: 2008

Exports (12m through September)

primary products

semi-manufacturedproducts

37.2%

manufactured products48.8%

14.0%

Source: MDIC

19

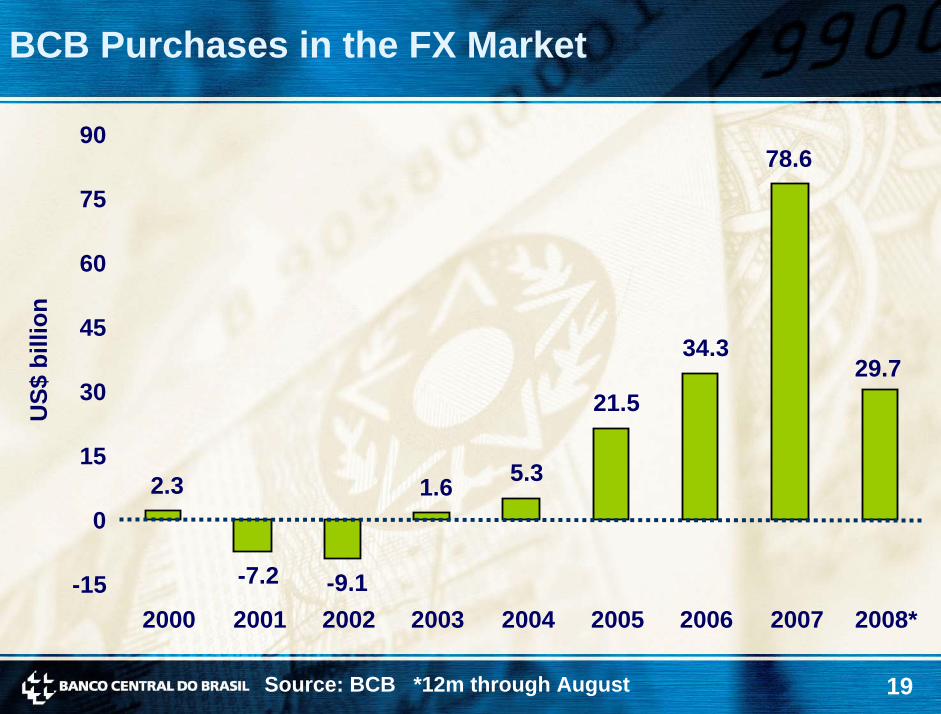

BCB Purchases in the FX Market

9078.6

2.3

-7.2 -9.1

1.6 5.3

21.5

34.329.7

75

60

US$

bill

ion

45

30

15

0

-152000 2001 2002 2003 2004 2005 2006 2007 2008*

Source: BCB *12m through August

20

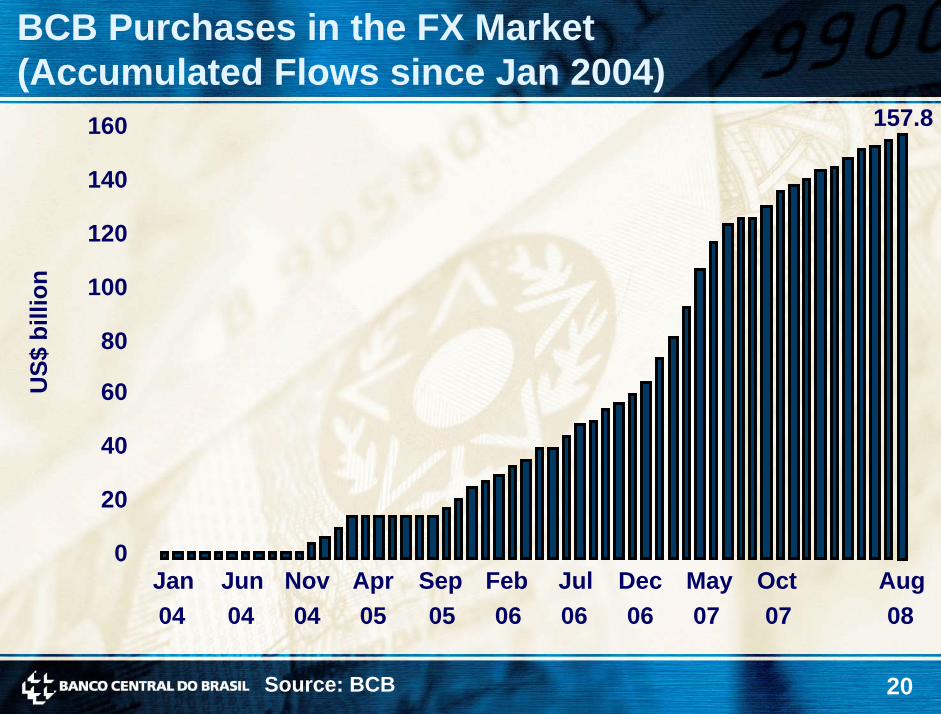

BCB Purchases in the FX Market (Accumulated Flows since Jan 2004)

US$

bill

ion

157.8

0

20

40

60

80

100

120

140

160

Jan04

Jun04

Nov04

Apr05

Sep05

Feb06

Jul06

Dec06

May07

Oct07

Aug08

Source: BCB

21

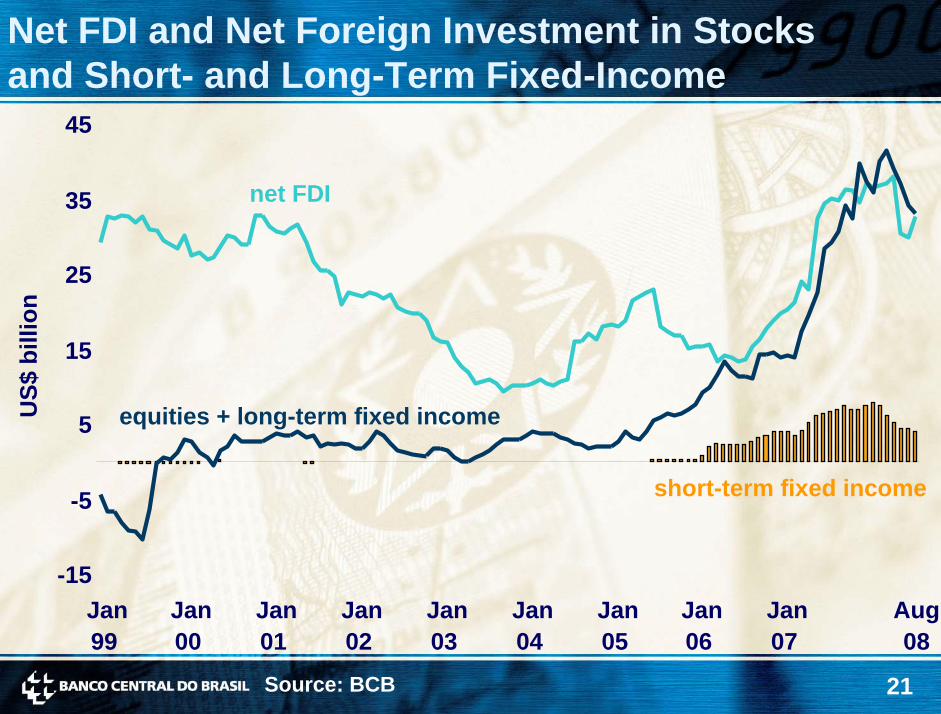

Net FDI and Net Foreign Investment in Stocks and Short- and Long-Term Fixed-Income

45

net FDI

equities + long-term fixed income

short-term fixed income-5

5

15

25

35

US$

bill

ion

-15Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

22

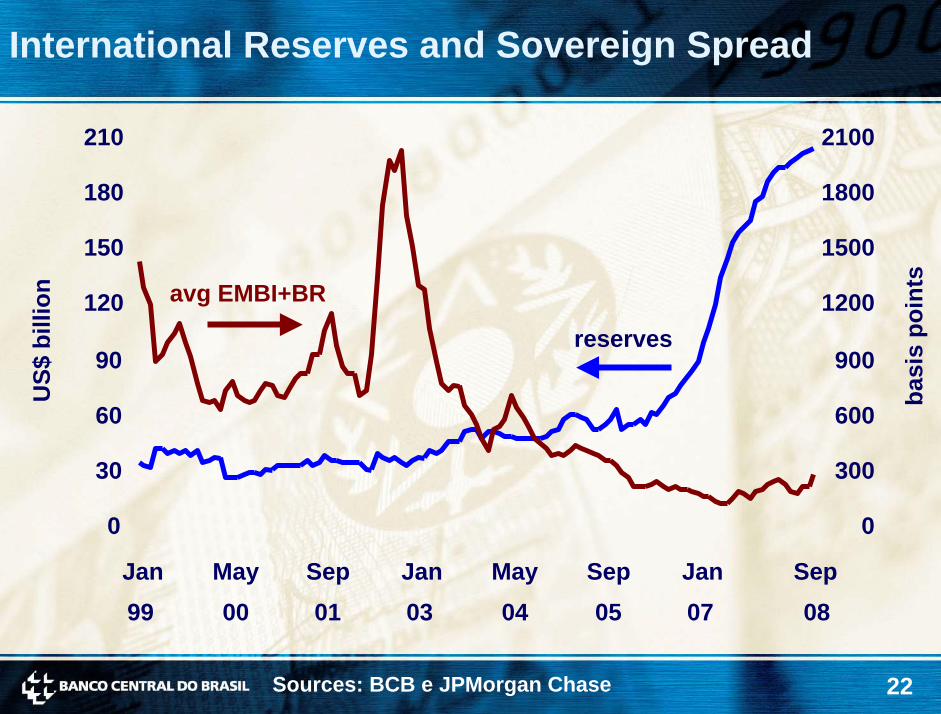

International Reserves and Sovereign SpreadU

S$ b

illio

n

basi

spo

ints

reserves

avg EMBI+BR

Sources: BCB e JPMorgan Chase

0

300

600

900

1200

1500

1800

2100210

180

150

120

90

60

30

0

Jan May Sep Jan May Sep Jan Sep99 00 01 03 04 05 07 08

23

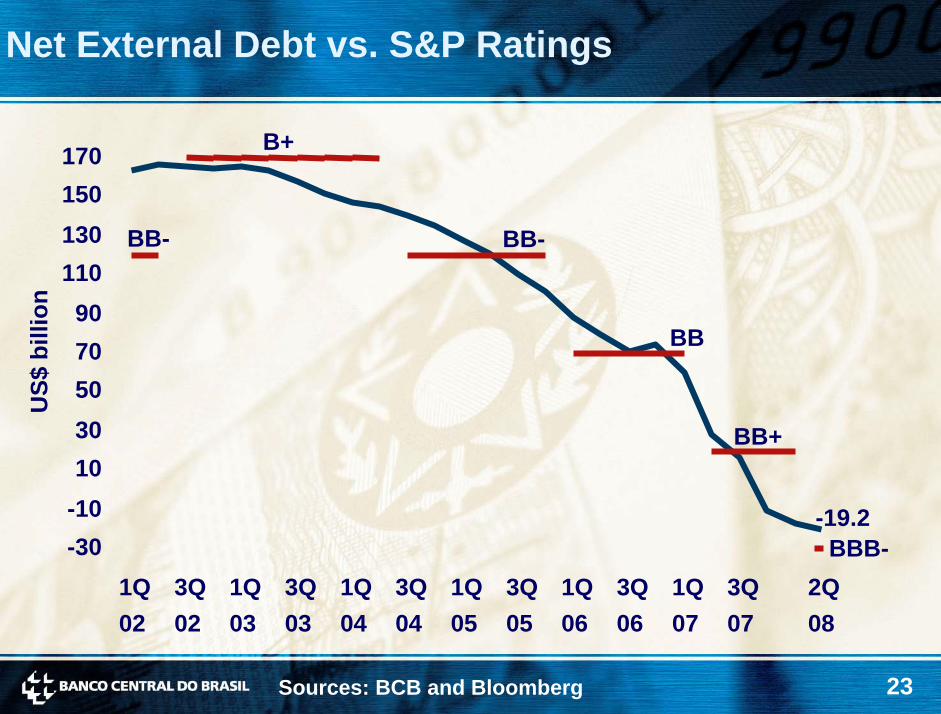

Net External Debt vs. S&P RatingsU

S$ b

illio

n

Sources: BCB and Bloomberg

BBB-

BB+

BB

BB-

B+

BB-

-19.2

170150130110

9070503010

-10-30

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

2Q08

24

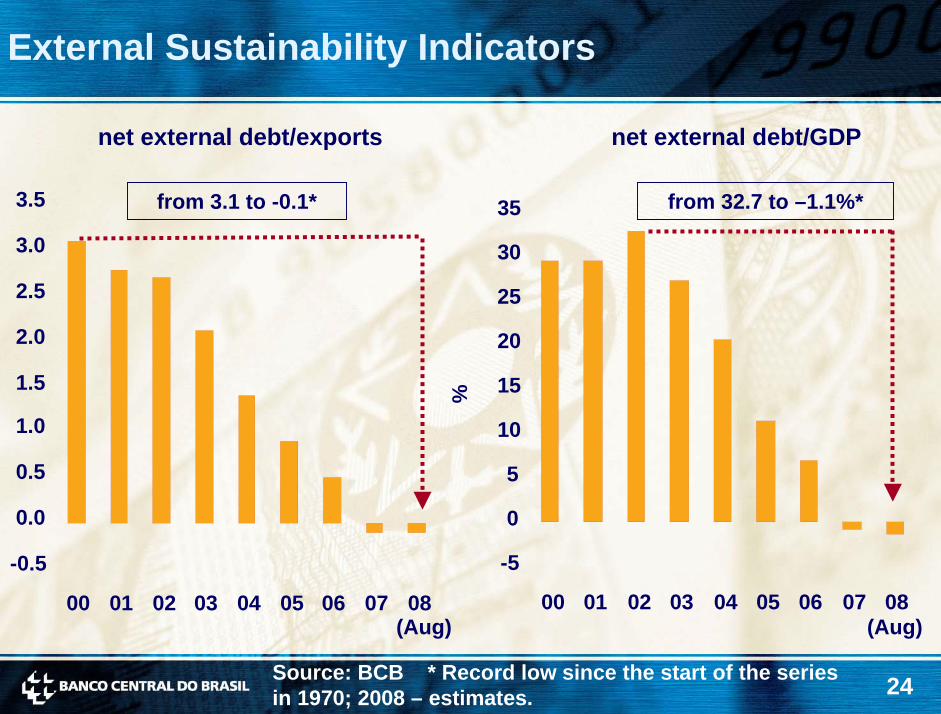

External Sustainability Indicators

net external debt/exports net external debt/GDP

from 3.1 to -0.1* from 32.7 to –1.1%* 3.5 35

Source: BCB * Record low since the start of the series in 1970; 2008 – estimates.

%

(Aug)(Aug)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0 30

25

20

15

10

5

0

-5

00 01 02 03 04 05 06 07 0800 01 02 03 04 05 06 07 08

25

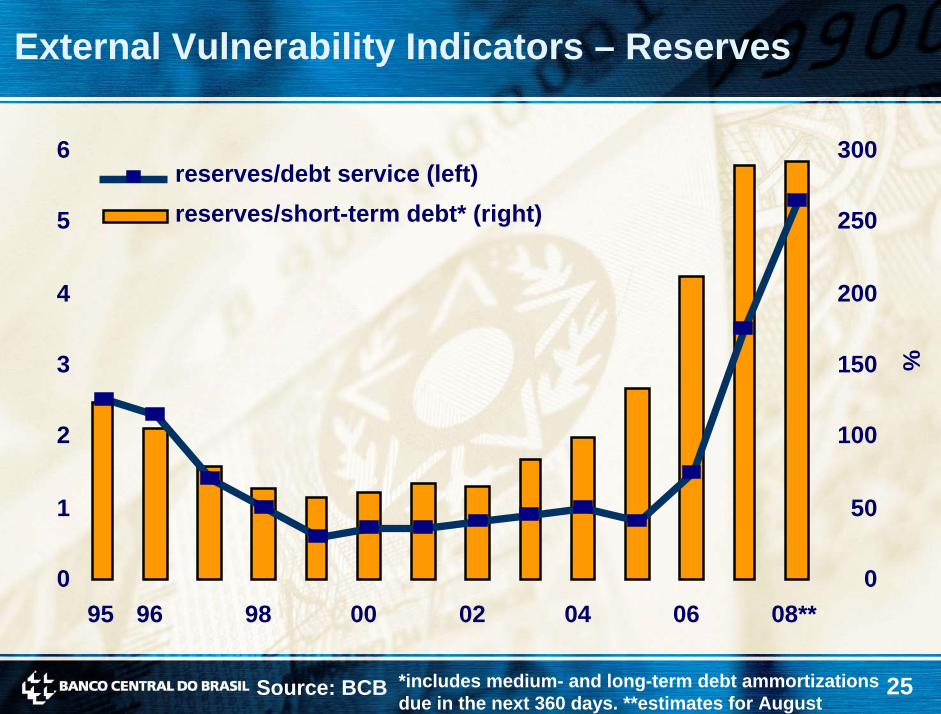

External Vulnerability Indicators – Reserves

3006

reserves/short-term debt* (right)reserves/debt service (left)

96 98 00 02 04 06 08**95

2505

2004

%1503

1002

501

00

Source: BCB *includes medium- and long-term debt ammortizationsdue in the next 360 days. **estimates for August

26

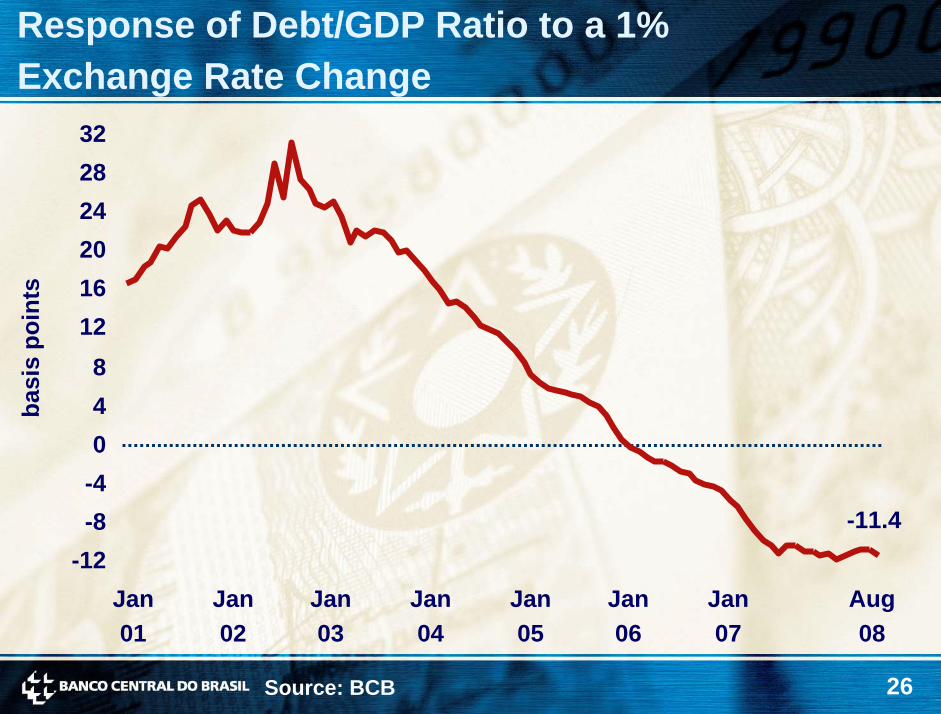

Response of Debt/GDP Ratio to a 1% Exchange Rate Change

basi

spo

ints

-11.4-12

-8-4048

121620242832

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

27

III. Brazil: Inflation Targeting in Practice

28

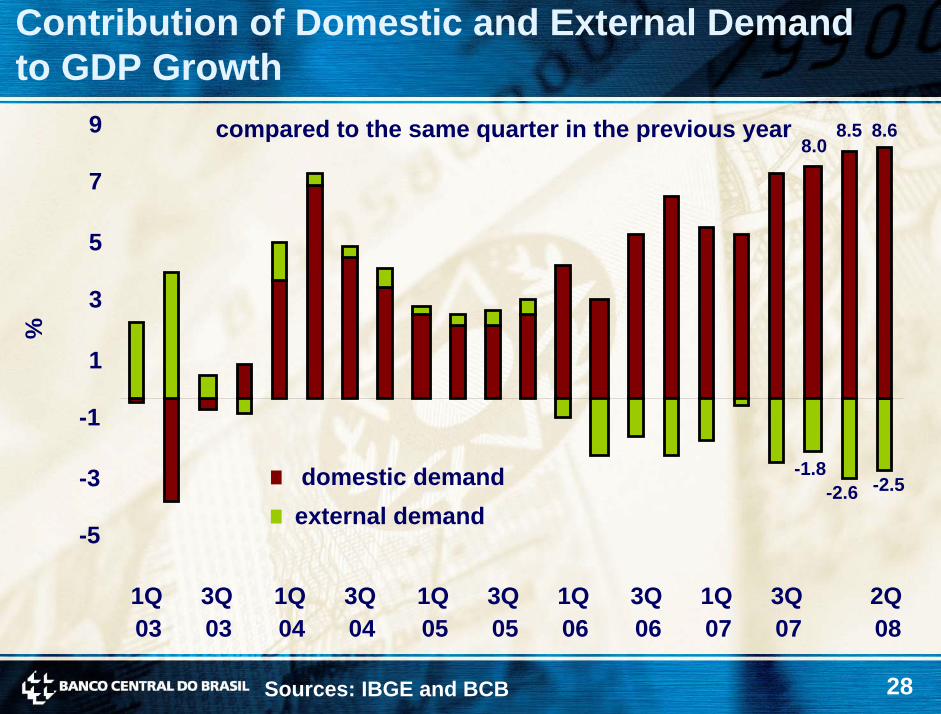

Contribution of Domestic and External Demandto GDP Growth

9 compared to the same quarter in the previous year

domestic demandexternal demand

8.08.5

-2.5-1.8

-2.6

8.6

7

5

3

%

1

-1

-3

-5

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

2Q08

Sources: IBGE and BCB

29

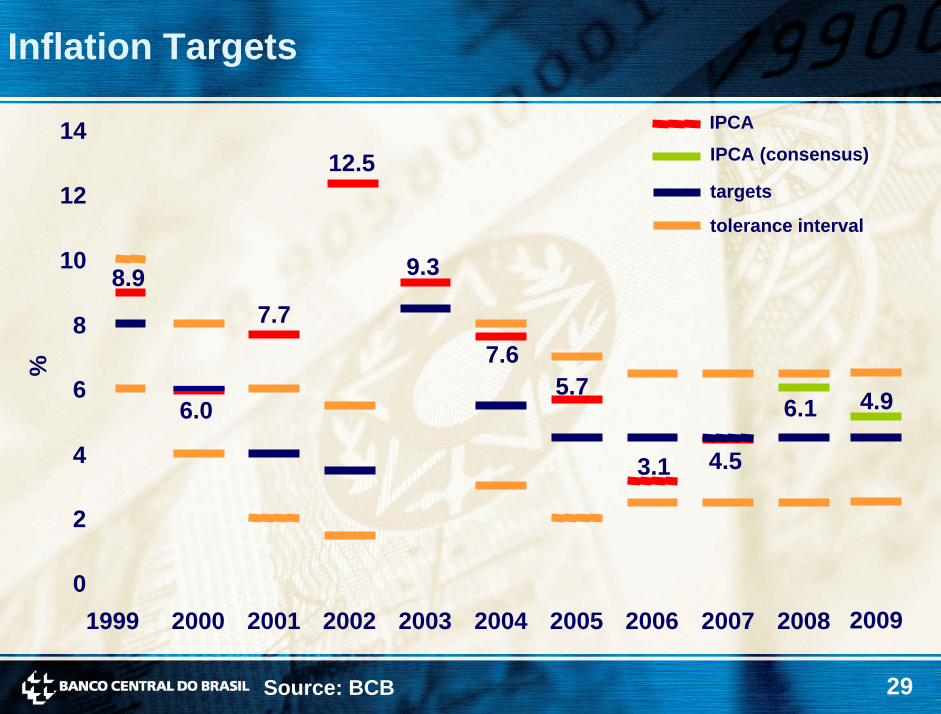

Inflation Targets

IPCA14IPCA (consensus)12.5targets12tolerance interval

%

10 9.38.9

0

2

4

6

8

1999

7.77.6

6.0

3.1

5.7

4.5

2000 2001 2002 2003 2004 2005 2006 2007

6.1 4.9

20092008

Source: BCB

30

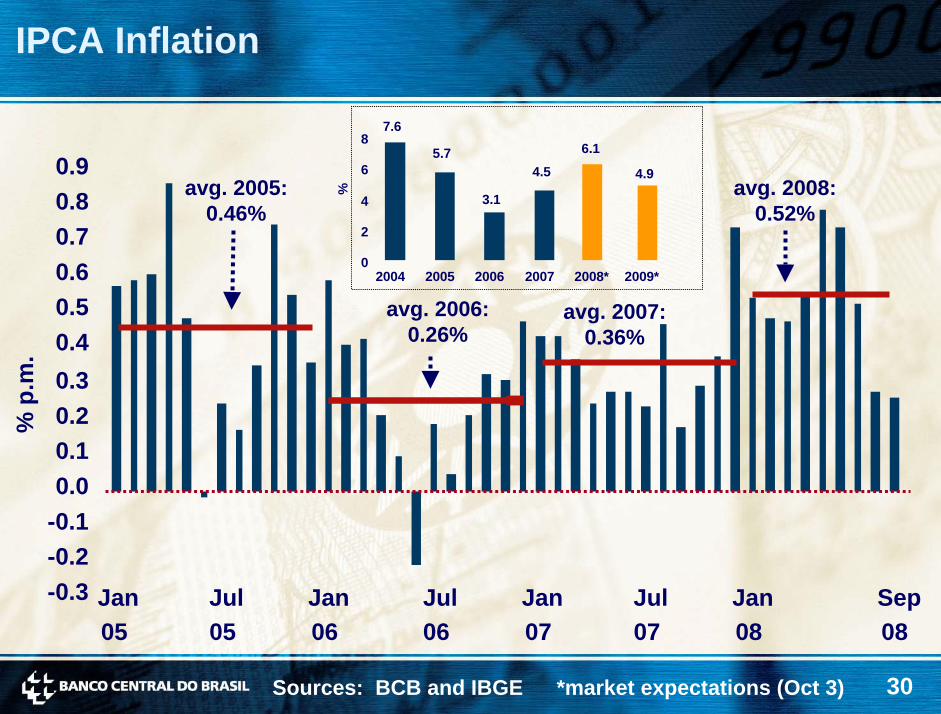

IPCA Inflation

%

7.6

5.7

3.1

4.5

6.1

4.9

0

2

4

6

8

2004 2005 2006 2007 2008* 2009*

Sources: BCB and IBGE *market expectations (Oct 3)

% p

.m.

-0.3-0.2-0.10.00.10.20.30.40.50.60.70.80.9

avg. 2006:0.26%

avg. 2007:0.36%

avg. 2008:0.52%

avg. 2005:0.46%

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Sep08

31

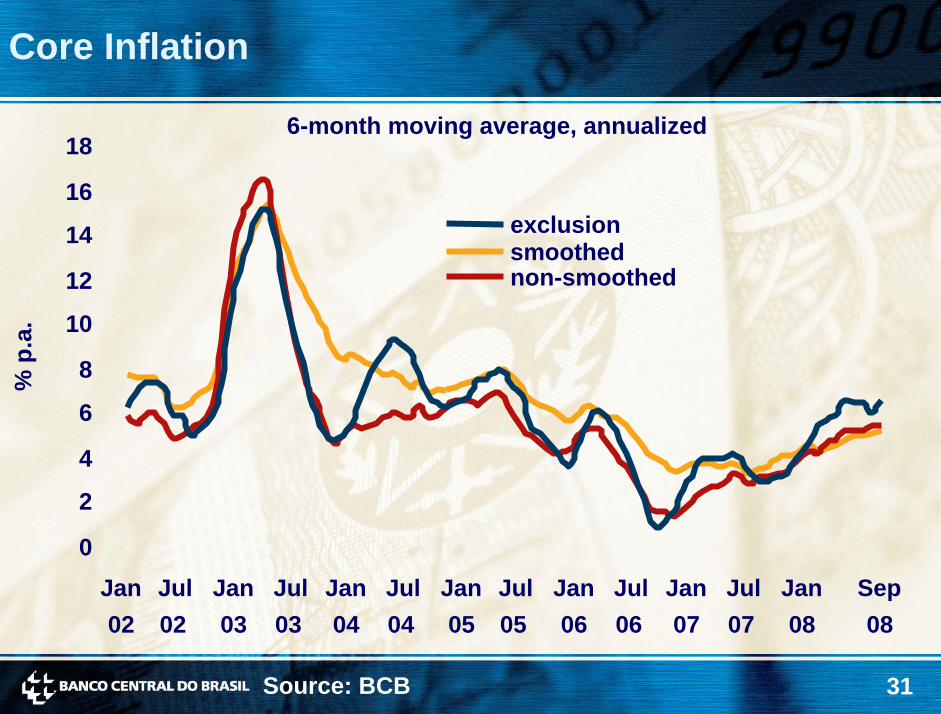

Core Inflation

6-month moving average, annualized18

smoothednon-smoothed

exclusion16

14

12

% p

.a. 10

8

6

4

2

0Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Sep08

Source: BCB

32

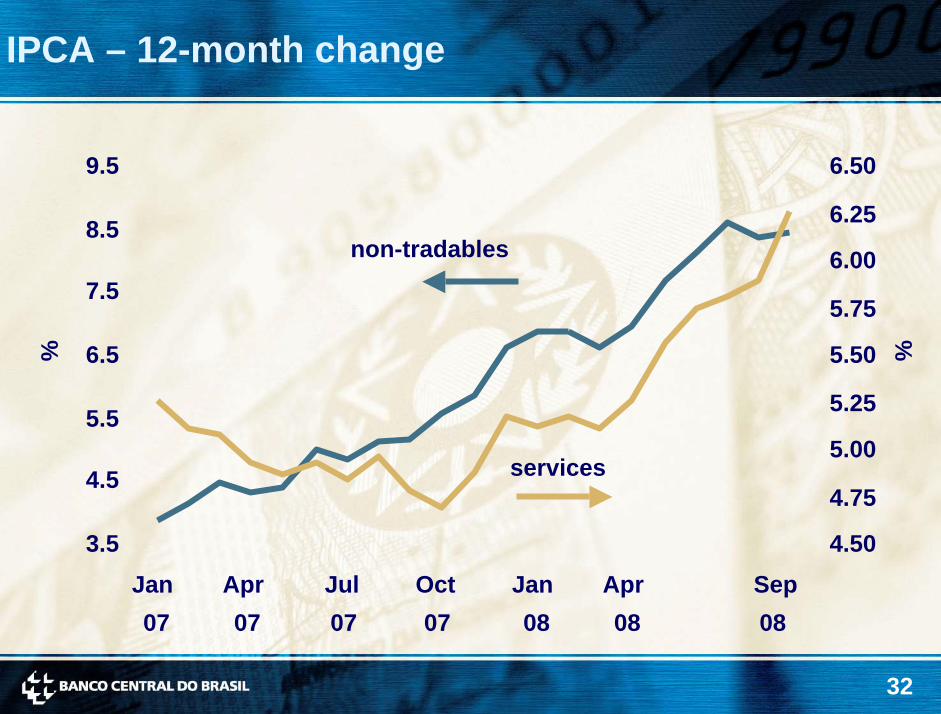

IPCA – 12-month change

6.509.5

non-tradables

services

%

6.258.56.00

7.55.75

% 5.506.5

5.255.55.00

4.54.75

4.503.5Jan Apr Jul Oct Jan Apr Sep07 07 07 07 08 08 08

33

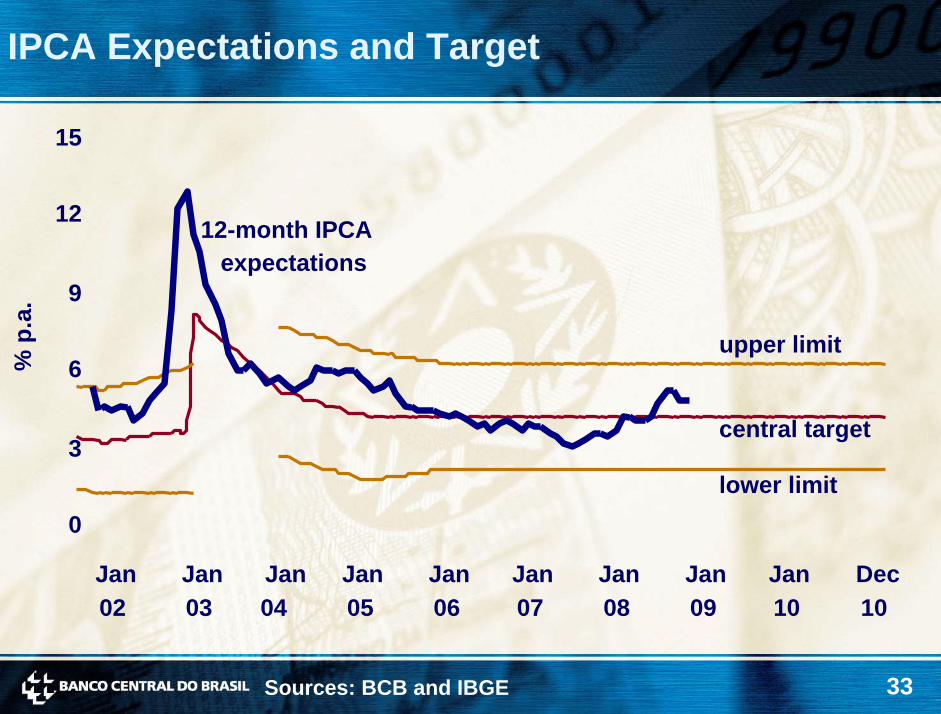

IPCA Expectations and Target

15

central target

12-month IPCA expectations

upper limit

lower limit3

6

9

12

% p

.a.

0

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Dec10

Sources: BCB and IBGE

34

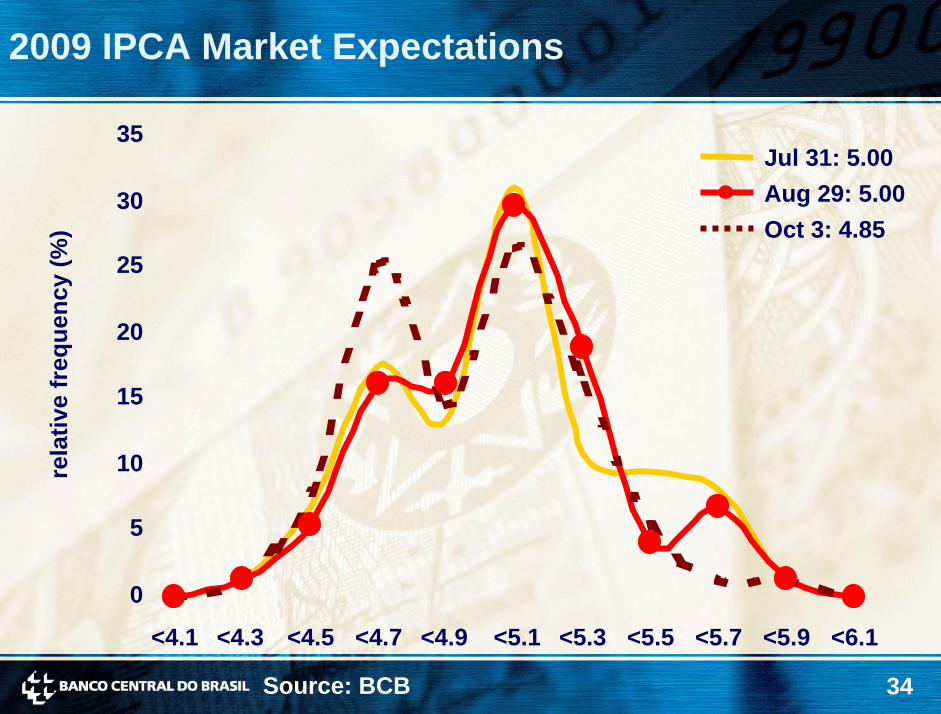

2009 IPCA Market Expectations

35Jul 31: 5.00Aug 29: 5.00Oct 3: 4.85

30

rela

tive

freq

uenc

y(%

)

25

20

15

10

5

0

<4.1 <4.3 <4.5 <4.7 <4.9 <5.1 <5.3 <5.5 <5.7 <5.9 <6.1

Source: BCB

35

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008