Information Content and Forecasting Ability of Sentiment Indicators: Case of Real Estate Market Gianluca Marcato and Anupam Nanda Abstract We evaluate a number of real estate sentiment indices to ascertain current and forward-looking information content that may be useful for forecasting demand and supply activities. Analyzing the dynamic relationships within a Vector Auto-Regression (VAR) framework and using the quarterly US data over 1988-2010, we test the efficacy of several sentiment measures by comparing them with other coincident economic indicators. Overall, our analysis suggests that the sentiment in real estate convey valuable information that can help predict changes in real estate returns. These findings have important implications for investment decisions, from consumers’ as well as institutional investors’ perspectives. Keywords: Sentiment Index, Predictability, VAR, Impulse Response, Out-of-sample Forecast JEL Classifications: C53, C82, E37, R31.

Transcript

Information Content and Forecasting Ability of Sentiment Indicators:

Case of Real Estate Market

Gianluca Marcato and Anupam Nanda

Abstract

We evaluate a number of real estate sentiment indices to ascertain current and forward-looking information content that may be useful for forecasting demand and supply activities. Analyzing the dynamic relationships within a Vector Auto-Regression (VAR) framework and using the quarterly US data over 1988-2010, we test the efficacy of several sentiment measures by comparing them with other coincident economic indicators. Overall, our analysis suggests that the sentiment in real estate convey valuable information that can help predict changes in real estate returns. These findings have important implications for investment decisions, from consumers’ as well as institutional investors’ perspectives.

The appraisal at time t (Vt) is obtained as a weighted average of the true unobserved value/price of

the property at time t (Vt’) with probability p and the observed value at time t-1 (Vt-1) with

probability (1-p). This is due to the fact that the properties are not transacted regularly and the prices

are only observed infrequently. In an informationally efficient market, we assume that Vt , Vt’ and

Vt-1 are represented as a function of contemporaneous information contained in macroeconomic

variables (Econt for the first two and Econt-1 for the latter) and sentiment indices (respectively Sentt

and Sentt-1)13. As a consequence, the pricing (i.e. value) at time t may be significantly predicted by the

sentiment indices at time t-1 because the information content of such indices is already factored in

the value at t-1 – which represents one of the two components contributing to the price formation at

time t as explained in equation (6). In fact, if the weight on new unobservable information (p) was

100% (i.e. if we remove smoothing and assume markets being strongly efficient), we would not

expect any significant prediction (as reported in Tables 6 and 7).

[INSERT TABLE 8 HERE]

5.4 Liquidity

As a further robustness check, we also test for the impact of liquidity on our model estimation and

we find that our results do hold true. The liquidity, treated as an endogenous variable in the VAR

24

system, is significant in almost all models and boosts the goodness of fit, but the real estate

sentiment still remains significant for the residential market and insignificant for the non-residential

market. As a proxy for liquidity in the non-residential sector, we use a metric computed as the

difference between the demand and supply indices in percentage of the Transaction-Based Price

Index as the average of the two indices (Fisher et al., 2007). For the residential market, we use a

proxy for the funding liquidity measured by tightness levels in the banking system as provided by the

Federal Reserve Board through the Senior Loan Officer Opinion Survey on Bank Lending

Practices.14

5.5 Impulse Responses

Figures 1 and 2 present the impulse responses for the residential and non-residential sectors

respectively. In general, the directions of changes conform to our theoretical expectations.

Specifically for the residential model in Figure 1, a one standard deviation shock to our variable of

interest (‘pure’ component of the HMI) has a moderate positive short-run impact and overall

positive net impact. For the non-residential model (Figure 2), one standard deviation shock to the

‘pure’ component of ABI does not have any noticeable impact on changes in the TBI price index.

[INSERT FIGURES 1 AND 2 HERE]

5.6 Principal Component Analysis

It is quite likely that various sentiment measures will have some degree of commonality. The

presence of such common factors may prevent us from isolating the true effects. To explore this

issue further, we conduct a Principal Component Analysis (PCA) to extract common components

embedded in the sentiment measures (after performing the orthogonalization step). We have

25

conducted the PCA analysis for both the residential and non-residential sectors. By taking into

account five factors (as many as the sentiment indices used in our analysis for both the residential

and non-residential sector), we find that the previous results reported in Tables 4-7 hold true. Two

main factors for the residential sector are found to convey information and to contain predictive

power. We may interpret these two factors as measures reflecting general and real-estate specific

market sentiment. Finally, consistent with our results in Tables 5 and 6, no principal component is

significant in the non-residential market.

5.7 Out-of-sample Evaluation

To establish the importance of sentiment indicators in predicting real estate price changes, we have

also performed an out-of-sample test. To check the robustness of our out-of-sample evaluation, we

consider 1, 2 and 3-year evaluation windows and present selected forecast evaluation parameters in

Table 8. For the residential market (Panel A), there are improvements which are most prominent for

the 2- and 3-year windows. Both bias and variance proportion measures are generally small and the

covariance proportion measures reveal that the random component comprises more than the half of

the error (normally around 90-95%). Moreover, although in the out-of-sample evaluation exercise

we have perhaps chosen the worst time-period (in terms of economic uncertainties) the

improvement is still quite significant. Therefore, the out-of-sample predictions clearly show evidence

of a significant ‘gain’ in our forecasting ability when we incorporate indices based on the attitude

data and forward-looking surveys in the residential market (see also graph plotting actual values in

blue line against the forecast obtained with the hard economic data only in red line and the hard

economic data combined with the sentiment indices in green line).

26

For the non-residential market (Panel B), the results are less prominent, with a slightly higher bias

and variance proportion measures than those for the residential market. The gains obtained with the

inclusion of the sentiment indices are mainly achieved in the short-term (1-year forecast), even if the

Theil inequality coefficient reveals improvements in the 2- and 3-year forecasts too. Clearly, the out

of sample predictions do confirm that the non-residential sector is more informationally efficient

than the housing sector.

[INSERT TABLE 9 HERE]

6. Conclusion

In this study, we analyze the information content of several sentiment indices and their relative

importance in modeling real estate price changes. Due to several idiosyncrasies in the real estate

market such as infrequent transactions, lumpy investment and information asymmetry, this exercise

provides a good testing ground for analyzing the role of sentiment. Moreover, the real estate markets

(and particularly the residential sector) generally lead economic cycles. We employ a Vector Auto-

Regression (VAR) framework and use quarterly US data over 1988-2010 to test the predictability of

several sentiment measures. After testing for the stationarity, contemporaneous and inter-temporal

relationships, we estimate a VAR system. To extract the ‘pure’ sentiment effect, we orthogonalize

the sentiment measures against a set of macroeconomic variables. Overall, our analysis suggests that

the ‘pure’ sentiment in the residential sector may convey valuable information which should be

embedded in the modeling exercise to predict changes in the real estate returns. Our results suggest

that the sentiment indicators are important in explaining residential real estate price changes as there

are statistically significant information gains from using such survey-based indices. However, we do

27

not find any significant effects for the non-residential sector. Finally, our results are robust across

several model specifications, including the returns of a valuation-based index and common factors

of several sentiment measures estimated using a Principal Component Analysis.

Overall, our findings indicate that price changes in the residential sector respond significantly to

changes in sentiment, while the non-residential sector does not show any significant effects. This

may reflect a greater responsiveness of the residential market to shocks in ‘pure’ sentiment, possibly

being transmitted through the changes in the underlying demand shifters. Due to a typically inelastic

short-run supply curve in the residential market, any shift in the demand schedule is almost fully

reflected in the price change, with the short-run positive impact lasting for about two and a half

quarters. The consequent dampening of the effect may be attributed to a supply-side adjustment

mitigating the price effect. It can be argued that the role of uncertainty in transactions due to the

presence of significant information asymmetry (and therefore formation of future price expectation

by households) may be more prominent in the residential market than in the non-residential sector.

In fact, the extent of information asymmetry may be less prominent in generally more ‘informed’

non-residential markets, where economic agents – e.g. institutional investors – may have access to a

more comprehensive information set and their information processing may also be more formalized

than the agents in the residential sector. Another plausible explanation may be due to the nature of

contracting in the non-residential sector. Long-term contracts and complex price-setting exercises

may also prevent sentiment from influencing the pricing in the non-residential sector in the short

run. Future research may focus on the interaction of demand- and supply-side factors, investor type

and asymmetry in their behavior across various stages of the economic cycle. The evidences

provided in this paper suggest that there may be significant heterogeneity in information efficiency

28

across different sectors of the real estate market, which may stem from the variations in investment

patterns and channels in these sectors.

29

References

Akerlof, G. A. and R. J. Shiller, Animal Spirits. Princeton: Princeton University Press, 2009. Acemoglu, D. and A. Scott, Consumer confidence and rational expectations: are agents’ beliefs consistent with the theory? Economic Journal, 1994, 104, 1–19. Baker, M. and J. Wurgler, Investor sentiment and the cross-section of stock returns, Journal of Finance, 2006, 61, 1645–1680. Baker, M. and J. Wurgler, Investor sentiment in the stock market, Journal of Economic Perspectives, 2007, 21, 129-151. Baker, K. and D. Saltes, Architecture Billings as a Leading Indicator of Construction, Business Economics, 2005, October. Bram, J. and S. Ludvigson, Does Consumer Confidence Forecast Household Expenditure? A Sentiment Index Horse Race, FRBNY Economic Policy Review, 1998. Carroll, C. D., J. C. Fuhrer and D. W. Wilcox, Does consumer sentiment forecast household spending? If so, why? American Economic Review, 1994, 84, 1397–1408. Case, K. E. and R. J. Shiller, The Efficiency of the Market for Single-Family Homes, American Economic Review, 1989, 79, 125-137. Case, K. E. and R. J. Shiller, Is There a Bubble in the Housing Market? Brookings Papers on Economic Activity, 2003, 2, 300-361. Case, K. E., R. J. Shiller and A. Thompson, What Have They Been Thinking? Home Buyer Behavior in Hot and Cold Markets, NBER Working Paper Series No. 18400, 2012. Chang, C., P. H. Franses and M. McAleer, How accurate are government forecasts of economic fundamentals? The case of Taiwan, International Journal of Forecasting, 2011, 27(4), 1066-1075. Changha J., G. Soydemir and A. Tidwell, The U.S. Housing Market and the Pricing of Risk: Fundamental Analysis and Market Sentiment, Journal of Real Estate Research, 2014, 36(2). Chua, C. L. and S. Tsiaplias, Can Consumer Sentiment and its Components Forecast Australian GDP and Consumption? Journal of Forecasting, 2009, 28, 698–711. Clayton, J., D. Ling and A. Naranjo, Non-residential Real Estate Valuation: Fundamentals Versus Investor Sentiment, Journal of Real Estate Finance and Economics, 2009, 38(1), 5-37. Croce, R. M. and D. R. Haurin, Predicting turning points in the housing market, Journal of Housing Economics, 2009, 18, 281–293. Dua, P., Analysis of Consumers’ Perceptions of Buying Conditions for Houses, Journal of Real Estate Finance and Economics, 2008, 37, 335–350.

30

Easaw, J. Z. and S. M. Heravi, Evaluating consumer sentiments as predictors of UK household consumption behaviour: Are they accurate and useful? International Journal of Forecasting, 2004, 20(4), 671-681. Emrath, P., Housing Market Index, Housing Economics, National Association of Home Builders, Washington, DC. 1995, June. Fan, C. S. and P. Wong, Does consumer sentiment forecast household spending? the Hong Kong case, Economics Letters, 1998, 58(1), 77–84. Fuhrer, J. C. What Role Does Consumer Sentiment Play in the U.S. Economy? Federal Reserve Bank of Boston New England Economic Review, 1993, 32-44. Fisher, J., D. Geltner and H. Pollakowski, A Quarterly Transactions-based Index of Institutional Real Estate Investment Performance and Movements in Supply and Demand, Journal of Real Estate Finance and Economics, 2007, 34(1), 5-33. Goodman, J. L., Using attitude data to forecast housing activity, Journal of Real Estate Research, 1994, 9(4), 445–453. Hall, R. E. Stochastic implications of the life cycle-permanent income hypothesis: theory and evidence, Journal of Political Economy, 1978, 86 971-87. Hohenstatt, R. and M. Kaesbauer, ‘GECO’s Weather Forecast’ for the U.K. Housing Market: To What Extent Can We Rely on Google ECOnometrics? Journal of Real Estate Research, 2014, 36(2). Howrey, E. P. The Predictive Power of the Index of Consumer Sentiment, Brookings Papers on Economic Activity, 2001, 175-207. Joseph, K., J. Wintoki and Z. Zhang, Forecasting Abnormal Stock Returns and Trading Volume Using Investor Sentiment: Evidence from Online Search, International Journal of Forecasting, 2011, 27(4), 1116-1127. Jurgilas, M. and K. J. Lansing, Housing Bubbles and Expected Returns to Homeownership: Lessons and Policy Implications. Working paper, http//ssrn.com/abstract=2209719, 2013. Katona G., Psychological Economics, New York: Elsevier, 1975. Kumar, V. R. P. Leone and J. N. Gaskins, Aggregate and disaggregate sector forecasting using consumer confidence measures, International Journal of Forecasting, 1995, 11(3), 361-377. Lee, M., B. Elango and S. P. Schnaars, The accuracy of the Conference Board's buying plans index: A comparison of judgmental vs. extrapolation forecasting methods, International Journal of Forecasting, 1997, 13(1), 127-135. Linden, F., The Consumer as Forecaster, The Public Opinion Quarterly, 1982, 46(3), 353-360.

31

Ling, D., G. Marcato and P. McAllister, Dynamics of Asset Prices and Transaction Activity in Illiquid Markets: the Case of Private Non-residential Real Estate, Journal of Real Estate Finance and Economics, 2009, 39(3), 359-383. Ling, D., J. T. L. Ooi and T. T. Le, Explaining House Price Dynamics: Isolating the Role of Non-Fundamentals, Unpublished Working Paper, 2013. Ling, D., A. Naranjo and B. Scheick, Investor Sentiment, Limits to Arbitrage, and Private Market Returns, Real Estate Economics, 2013, 41(2), 1-47. Lizieri, C., G. Marcato, P. Ogden and A. Baum, Pricing Inefficiencies in Private Real Estate Markets Using Total Return Swaps, Journal of Real Estate Finance and Economics, 2012, 45(3), 774-803 Malgarini, M. and P. Margani, Psychology, consumer sentiment and household expenditures, Applied Economics, 2009, 39(13), 1719-1729. Matsusaka, J. G. and A. M. Sbordone, Consumer Confidence and Economic Fluctuations, Economic Inquiry, 1995, 33(2), 296-318. Milani, F., Expectation Shocks and Learning as Drivers of the Business Cycle, The Economic Journal, 2011, 121, 379–401. Mishkin, F. S. Consumer Sentiment and Spending on Durable Goods, Brookings Papers On Economic Activity, 1978, 1, 217-32. Nanda, A., Examining the NAHB/Wells Fargo Housing Market Index (HMI), Housing Economics, National Association of Home Builders, Washington, DC. March, 2007. Parigi, G. and G. Schlitzer, Predicting consumption of Italian households by means of survey indicators, International Journal of Forecasting, 1997, 13(2), 197-209. Piger, J. M. Consumer Confidence Surveys: Do They Boost Forecasters' Confidence? Regional Economist, Federal Reserve Bank of St. Louis, 2003, April. Quan, D. C. and J. M. Quigley, Inferring an investment return series for real estate from observations on sales, Journal of the American Real Estate and Urban Economics Association, 1989, 17, 218-30. Schmeling, M., Institutional and individual sentiment: Smart money and noise trader risk? International Journal of Forecasting, 2007, 23(1), 127-145. Shiller, R. J., Irrational Exuberance, Princeton, NJ: Princeton University Press, 2000. Souleles N., Expectations, heterogenous forecast errors and consumption: micro evidence from the Michigan consumer sentiment surveys, Journal of Money, Credit and Banking, 2004, 36, 39–72.

32

Stambaugh, R. F., J. Yu and Y. Yuan, The short of it: Investor sentiment and anomalies, Journal of Financial Economics, 2012, 104, 288–302. Tsolacos, S., C. Brooks and O. Nneji, On the Predictive Content of Leading Indicators: The Case of U.S. Real Estate Markets, Journal of Real Estate Research, Forthcoming. Utaka, A., Confidence and the real economy: the Japanese case, Applied Economics, 2003, 35, 337–342. Vuchelen, J., Consumer sentiment and macroeconomic forecasts, Journal of Economic Psychology, 2004, 25, 493–506. Wang, Y., A. Keswani and S. J. Taylor, The relationships between sentiment, returns and volatility, International Journal of Forecasting, 2006, 22(1), 109-123. Weber, W. and M. Devaney, Can consumer sentiment surveys forecast housing starts? Appraisal Journal, 1996, 4, 343–350.

33

Acknowledgement

The authors would like to acknowledge the financial support from the Royal Institution of

Chartered Surveyors (RICS) Education Trust, Real Estate Research Corporation (RERC) and

Henley Business School, University of Reading, School of Real Estate and Planning, UK. The

authors would also like to thank the two anonymous referees, Paul Emrath as well as participants at

the 2011 AREUEA Mid-Year Meeting for comments. Tumellano Sebehela provided excellent

research assistance. All remaining errors are ours.

Gianluca Marcato, Henley Business School, University of Reading, Reading, RG6 6UD, UK or [email protected]. Anupam Nanda, Henley Business School, University of Reading, Reading, RG6 6UD, UK or : [email protected].

34

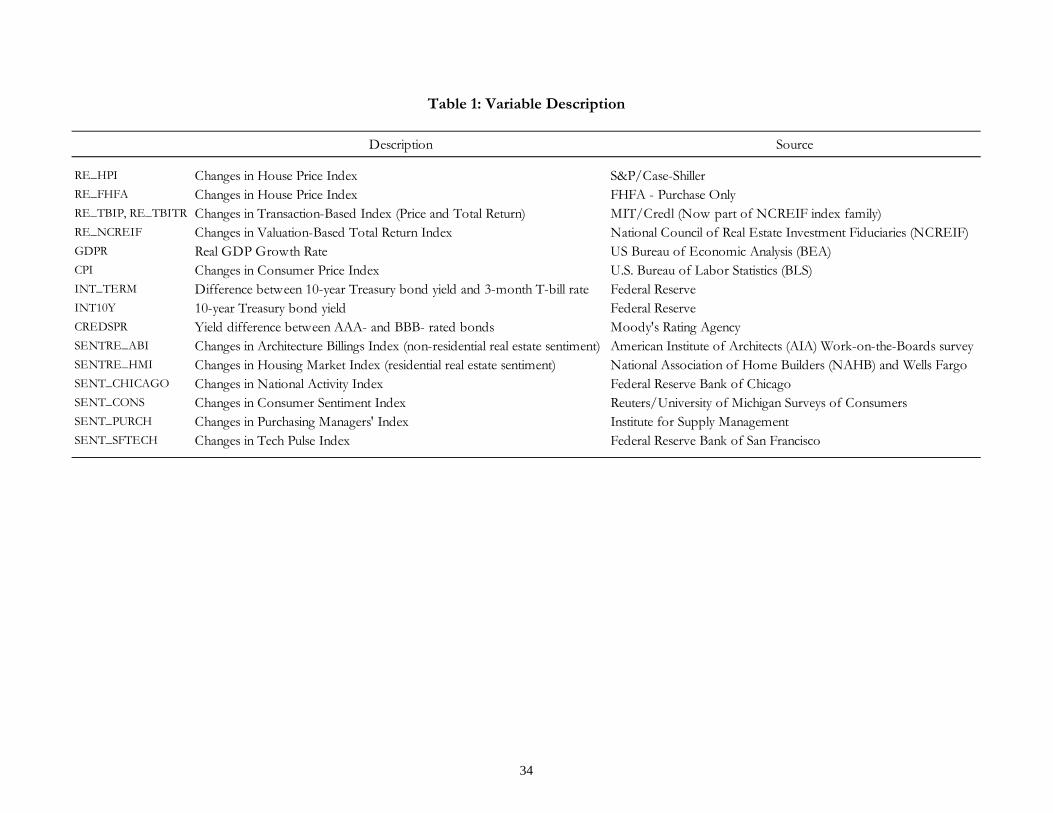

Table 1: Variable Description

Description Source

RE_HPI Changes in House Price Index S&P/Case-ShillerRE_FHFA Changes in House Price Index FHFA - Purchase OnlyRE_TBIP, RE_TBITR Changes in Transaction-Based Index (Price and Total Return) MIT/Credl (Now part of NCREIF index family)RE_NCREIF Changes in Valuation-Based Total Return Index National Council of Real Estate Investment Fiduciaries (NCREIF)GDPR Real GDP Growth Rate US Bureau of Economic Analysis (BEA)CPI Changes in Consumer Price Index U.S. Bureau of Labor Statistics (BLS)INT_TERM Difference between 10-year Treasury bond yield and 3-month T-bill rate Federal ReserveINT10Y 10-year Treasury bond yield Federal ReserveCREDSPR Yield difference between AAA- and BBB- rated bonds Moody's Rating AgencySENTRE_ABI Changes in Architecture Billings Index (non-residential real estate sentiment) American Institute of Architects (AIA) Work-on-the-Boards surveySENTRE_HMI Changes in Housing Market Index (residential real estate sentiment) National Association of Home Builders (NAHB) and Wells FargoSENT_CHICAGO Changes in National Activity Index Federal Reserve Bank of ChicagoSENT_CONS Changes in Consumer Sentiment Index Reuters/University of Michigan Surveys of Consumers SENT_PURCH Changes in Purchasing Managers' Index Institute for Supply ManagementSENT_SFTECH Changes in Tech Pulse Index Federal Reserve Bank of San Francisco

35

Table 2: Descriptive Statistics

Variables: RE_HPI = Changes in S&P/Case-Shiller Home Price Index; RE_FHFA = Changes in FHFA Purchase-only House Price Index; RE_TBIP = Changes in Transaction-Based Price Index; RE_TBITR = Changes in Transaction-Based Total Return Index; GDPR = Real GDP Growth Rate; CPI = Changes in Consumer Price Index; INT_TERM = Difference between 10-year Treasury bond yield and 3-month T-bill rate; INT10Y = 10-year Treasury bond yield; CREDSPR = Yield difference between AAA- and BBB- rated bonds; SENTRE_ABI = Changes in Architecture Billings Index (non-residential real estate sentiment); SENTRE_HMI = Changes in Housing Market Index (residential real estate sentiment); SENT_CHICAGO = Changes in National Activity Index; SENT_CONS = Changes in Consumer Sentiment Index; SENT_PURCH = Changes in Purchasing Managers' Index; SENT_SFTECH = Changes in Tech Pulse Index. The JB-stat indicates the value of the Jarque-Bera test and its p-value is in the next column. The ADF test reports the p-value of the statistic for the first lag with significant value (as suggested in the ‘Lag’ column). The maximum lag with the ADF test still being significant is reported in the ‘Max Lag’ column.

Mean Median Max Min Std. Dev. Skewness Kurtosis JB-stat Prob Sum Sum Sq. Dev. Obs Prob. Lag Max Lag

Variables: RE_TBIP = Changes in Transaction-Based Price Index; RE_HPI = Changes in S&P/Case-Shiller Home Price Index; GDP = Real GDP Growth Rate; CPI = Changes in Consumer Price Index; INT_TERM = Difference between 10-year Treasury bond yield and 3-month T-bill rate; INT10Y = 10-year Treasury bond yield; CREDSPR = Yield difference between AAA- and BBB- rated bonds; SENTRE_ABI = Changes in Architecture Billings Index (non-residential real estate sentiment); SENTRE_HMI = Changes in Housing Market Index (residential real estate sentiment); SENT_CHICAGO = Changes in National Activity Index; SENT_CONS = Changes in Consumer Sentiment Index; SENT_PURCH = Changes in Purchasing Managers' Index; SENT_SFTECH = Changes in Tech Pulse Index. Grange Causality tests are run between each economic data/ sentiment index and real estate price changes for different lags (1 to 12). Start and End report respectively the initial and last lag for which Granger-causality is found (i.e. no causality is found before the starting or after the ending quarter). * The P-values of the coefficients of causation (‘causing’ for economic data / sentiment indices causing real estate price changes, ‘caused’ for economic data caused by real estate price changes) are reported only for the equations when causation starts. For example in Panel A, 0.0127 is the p-value of economic data/sentiment indices Granger causing real estate price changes with one quarter lag (Q1 for ‘Start’), while 0.7918 is the p-value of real estate price changes causing economic data/sentiment indices with 1 quarter lag. Since only the former shows statistical significance with confidence set at 95% level, we conclude that GDP Granger-causes real estate price changes. Initial reversal reports the initial lags when a causation opposite to the one shown by the p-values is found. For Example in Panel A, since SENT_CHICAGO is found to cause real estate price changes from Q3 to Q12 (see p-values of Q3 in the fourth and fifth column), an initial reversal Q1-Q2 indicates that real estate price changes Granger-cause general sentiment (Chicago) in these two quarters. No value in initial reversal indicates that opposite causation is not found at any lag.

* The P-value refers to the starting quarter when the variable granger causes real estate total returns

37

Table 4: VAR Estimation with Real Price Changes: Residential Real Estate-I (S&P/Case-Shiller Home Price Index)

Dependent Variable: HPI = Changes in S&P/Case-Shiller Home Price Index. Independent Variables: Real Estate Sentiment = Changes in the orthogonalized Housing Market Index (residential sentiment index); General Sentiment = Changes in the orthogonalized general sentiment index (Chicago = Changes in National Activity Index; Consumer = Changes in Consumer Sentiment Index; Purchase = Changes in Purchasing Managers' Index; SFTech = Changes in Tech Pulse Index). Macro-economic variables included in the model: GDP = Real GDP Growth Rate; Inflation rate = Changes in Consumer Price Index; Real interest rate = 10-year Treasury bond yield net of inflation; Term Spread = Difference between 10-year Treasury bond yield and 3-month T-bill rate; Credit Spread = Yield difference between AAA- and BBB- rated bonds. Notes: Only the outcome from the price changes equation in the VAR system is reported in the table under each column. Sample period is 1988Q3-2010Q4. The p-values from the joint significance across the lags are reported in the Granger-Causality section of the table. t-stats are reported underneath the coefficient estimates. P-values in bold show significance up to 5% level. P-values in bold and italics show significance up to 10% level.

Return Equation Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Chicago Consumer Purchase SFTech

Table 5: VAR Estimation with Real Price Changes: Residential Real Estate-II (FHFA House Price Index)

Dependent Variable: HPI = Changes in FHFA House Price Index. Independent Variables: Real Estate Sentiment = Changes in the orthogonalized Housing Market Index (residential sentiment index); General Sentiment = Changes in the orthogonalized general sentiment index (Chicago = Changes in National Activity Index; Consumer = Changes in Consumer Sentiment Index; Purchase = Changes in Purchasing Managers' Index; SFTech = Changes in Tech Pulse Index). Macro-economic variables included in the model: GDP = Real GDP Growth Rate; Inflation rate = Changes in Consumer Price Index; Real interest rate = 10-year Treasury bond yield net of inflation; Term Spread = Difference between 10-year Treasury bond yield and 3-month T-bill rate; Credit Spread = Yield difference between AAA- and BBB- rated bonds. Notes: Only the outcome from the price changes equation in the VAR system is reported in the table under each column. Sample period is 1988Q3-2010Q4. The p-values from the joint significance across the lags are reported in the Granger-Causality section of the table. T-stats are reported underneath the coefficient estimates. P-values in bold show significance up to 5% level. P-values in bold and italics show significance up to 10% level.

Return Equation Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Chicago Consumer Purchase SFTech

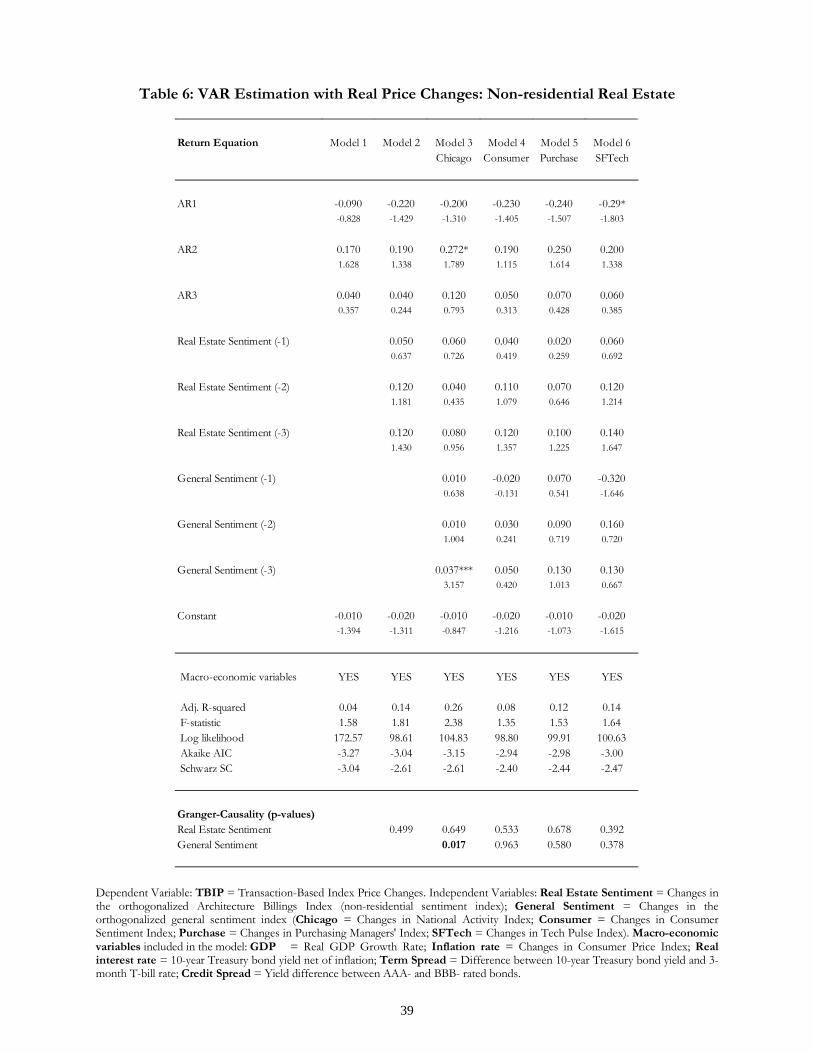

Table 6: VAR Estimation with Real Price Changes: Non-residential Real Estate

Dependent Variable: TBIP = Transaction-Based Index Price Changes. Independent Variables: Real Estate Sentiment = Changes in the orthogonalized Architecture Billings Index (non-residential sentiment index); General Sentiment = Changes in the orthogonalized general sentiment index (Chicago = Changes in National Activity Index; Consumer = Changes in Consumer Sentiment Index; Purchase = Changes in Purchasing Managers' Index; SFTech = Changes in Tech Pulse Index). Macro-economic variables included in the model: GDP = Real GDP Growth Rate; Inflation rate = Changes in Consumer Price Index; Real interest rate = 10-year Treasury bond yield net of inflation; Term Spread = Difference between 10-year Treasury bond yield and 3-month T-bill rate; Credit Spread = Yield difference between AAA- and BBB- rated bonds.

Return Equation Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Chicago Consumer Purchase SFTech

Notes: Only the outcome from the price changes equation in the VAR system is reported in the table under each column. Sample period is 1997Q1-2010Q4. The p-values from the joint significance across the lags are reported in the Granger-Causality section of the table. t-stats are reported underneath the coefficient estimates. P-values in bold show significance up to 5% level. P-values in bold and italics show significance up to 10% level.

41

Table 7: VAR Estimation with Real Total Returns: Non-residential Real Estate

Dependent Variable: TBITR = Transaction-Based Index Total Returns. Independent Variables: Real Estate Sentiment = Changes in the orthogonalized Architecture Billings Index (non-residential sentiment index); General Sentiment = Changes in the orthogonalized general sentiment index (Chicago = Changes in National Activity Index; Consumer = Changes in Consumer Sentiment Index; Purchase = Changes in Purchasing Managers' Index; SFTech = Changes in Tech Pulse Index). Macro-economic variables included in the model: GDP = Real GDP Growth Rate; Inflation rate = Changes in Consumer Price Index; Real interest rate = 10-year Treasury bond yield net of inflation; Term Spread = Difference between 10-year Treasury bond yield and 3-month T-bill rate; Credit Spread = Yield difference between AAA- and BBB- rated bonds. Notes: Only the outcome from price changes equation in the VAR system is reported in the table under each column. Sample period is 1997Q1-2010Q4. The p-values from the joint significance across the lags are reported in the Granger-Causality section of the table. t-stats are reported underneath the coefficient estimates. P-values in bold show significance up to 5% level. P-values in bold and italics show significance up to 10% level.

Return Equation Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Chicago Consumer Purchase SFTech

Table 8: VAR Estimation with Valuation-Based Real Total Returns: Non-residential Real Estate

Dependent Variable: NCREIF = Valuation-based NCREIF Total Return Index. Independent Variables: Real Estate Sentiment = Changes in the orthogonalized Architecture Billings Index (non-residential sentiment index); General Sentiment = Changes in the orthogonalized general sentiment index (Chicago = Changes in National Activity Index; Consumer = Changes in Consumer Sentiment Index; Purchase = Changes in Purchasing Managers' Index; SFTech = Changes in Tech Pulse Index). Macro-economic variables included in the model: GDP = Real GDP Growth Rate; Inflation rate = Changes in Consumer Price Index; Real

Return Equation Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Chicago Consumer Purchase SFTech

interest rate = 10-year Treasury bond yield net of inflation; Term Spread = Difference between 10-year Treasury bond yield and 3-month T-bill rate; Credit Spread = Yield difference between AAA- and BBB- rated bonds. Notes: Only the outcome from the price changes equation in the VAR system is reported in the table under each column. Sample period is 1988Q3-2010Q4. The p-values from the joint significance across the lags are reported in the Granger-Causality section of the table. t-stats are reported underneath the coefficient estimates. P-values in bold show significance up to 5% level. P-values in bold and italics show significance up to 10% level.

Notes: The sample period is 1997Q1 to 2010Q4. Model (1) – hard economic data only – and model (6) – hard economic data & both general and real estate sentiment indicators – in Table 4 are used for these predictions. ‘Forecasts 2008-10’ indicate that models are estimated using the sample 1997Q1 to 2007Q4 and the out-of-sample period refers to 2008Q1 to 2010Q4.

Notes: These forecasts are based on the non-residential models reported in Table 4. The blue line represents actual real estate price changes for the out-of-sample prediction, the red line represents out-of-sample forecasts obtained with a model only including economic variables and the green line represents out-of-sample forecasts obtained with a model including both economic variables and sentiment indicators. Source: Authors’ calculation.

Actual Forecast Economy Forecast Economy & Sentiment

45

Panel B: Non-Residential Market

Notes: The sample period is 1997Q1 to 2010Q4. Model (1) – hard economic data only – and model (3) – hard economic data & both general and real estate sentiment indicators – in Table 6 are used for these predictions. ‘Forecasts 2008-10’ indicate that models are estimated using the sample 1997Q1 to 2007Q4 and the out-of-sample period refers to 2008Q1 to 2010Q4.

Notes: These forecasts are based on the non-residential models reported in Table 6. The blue line represents actual real estate price changes for the out-of-sample prediction, the red line represents out-of-sample forecasts obtained with a model only including economic variables and the green line represents out-of-sample forecasts obtained with a model including both economic variables and sentiment indicators. Source: Authors’ calculation.

Actual Forecast Economy Forecast Economy & Sentiment

46

Figure 1: Impulse Responses: Residential Real Estate

Variables: AR Process = Autoregressive Component of the S&P/Case-Shiller Home Price index; Real Estate Sentiment HMI = Changes in the orthogonalized Housing Market Index (residential sentiment index); General Sentiment = Changes in orthogonalized general sentiment index (Chicago = National Activity Index; Consumer = Consumer Sentiment Index; Purchase = Purchasing Managers' Index; SFTech = Tech Pulse Index). Notes: Graphs represent impulse responses of residential real estate price changes to innovations in sentiment indices. All impulse responses are derived from Table 4. Source: Authors’ calculation.

-.004

.000

.004

.008

.012

1 2 3 4 5 6 7 8 9 10

-.004

.000

.004

.008

.012

1 2 3 4 5 6 7 8 9 10

-.004

.000

.004

.008

.012

1 2 3 4 5 6 7 8 9 10

-.004

.000

.004

.008

.012

.016

1 2 3 4 5 6 7 8 9 10

-.004

.000

.004

.008

.012

.016

1 2 3 4 5 6 7 8 9 10

-.004

.000

.004

.008

.012

.016

1 2 3 4 5 6 7 8 9 10

AR process Real Estate Sentiment: HMI

General Sentiment: Chicago

General Sentiment: SFTechGeneral Sentiment: Purchase

General Sentiment: Consumer

Retu

rnRe

turn

Retu

rn

47

Figure 2: Impulse Responses: Non-residential Real Estate

Variables: AR Process = Autoregressive Component of the Real Transaction-Based Price Index; Real Estate Sentiment ABI = Changes in the orthogonalized Architecture Billings Index (non-residential sentiment index); General Sentiment = Changes in orthogonalized general sentiment index (Chicago = National Activity Index; Consumer = Consumer Sentiment Index; Purchase = Purchasing Managers' Index; SFTech = Tech Pulse Index). Notes: Graphs represent impulse responses of non-residential real estate price changes to innovations in sentiment indices. All impulse responses are derived from Table 6. Source: Authors’ calculation.

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

-.04

-.02

.00

.02

.04

.06

1 2 3 4 5 6 7 8 9 10

p _ _

AR process Real Estate Sentiment: ABI

General Sentiment: Chicago

General Sentiment: SFTechGeneral Sentiment: Purchase

General Sentiment: Consumer

Retu

rnRe

turn

Retu

rn

48

1 See Milani (2011) for a recent paper on relaxing rational expectation assumption. Also see paper on investors’ sentiment by Wang, Keswani and Taylor (2006); Schmeling (2007); Joseph, Wintoki and Zhang (2011); Stambaugh, Yu and Yuan (2012).

2 Lee, M., Elango, B. & Schnaars, S. P. (1997) find very little support for using Conference Board’s buying intention data for forecasting sales of durable goods. Also see, Fuhrer (1993), Howrey (2001) and Piger (2003).

3 Ling et al., 2009 find that in UK private real estate, asset turnover provides increased price revelation which may reduce investment risk and thus increases the property values.

4 see http://www.ncreif.org/tbi-returns.aspx

5 For details, see American Institute of Architects (AIA) Work-on-the-Boards survey - http://www.aia.org/practicing/economics/AIAS076265

6 For details, see The NAHB/Wells Fargo Housing Market Index (HMI): http://www.nahb.org/reference_list.aspx?sectionID=134

7 For details, see The Chicago Fed National Activity Index (CFNAI) - http://www.chicagofed.org/webpages/publications/cfnai/index.cfm

8 For details, see The Reuters/University of Michigan Surveys of Consumers: https://customers.reuters.com/community/university/default.aspx

9 For details, see The Purchasing Managers Index (PMI): http://www.ism.ws/ISMReport/content.cfm?ItemNumber=10752&navItemNumber=12961

10 For details, see The Tech Pulse Index: http://www.frbsf.org/csip/pulse.php

11 We also perform Phillips-Perron (PP) test for detecting unit roots and we do not find any significantly different outcome

12 This empirical discussion is drawn from Enders (2010), Chapter 5.

13 This is the reason why we inserted Econ and Sent within brackets next to the variables V in equation (6). For example Vt(Econt,Sentt) means that the variable Vt is a function of Econt and Sentt, i.e. the value of a property at time t is a function of the information set contained in macro-economic variables and sentiment measures released at time t.