Page 1

MFI Grading

BWR MF 1 MFI Grading Scale at Brickwork Ratings

The MFI Grading Scale at Brickwork Ratings is on an 8

point scale from BWR MF 1 to BWR MF8 with BWR MF

1 corresponding to the highest grade while BWR MF 8

is the lowest grade.

The MFI grades assigned refer to the ability of the MFI

to manage its operations in a sustainable manner; they

do not refer to the credit quality of the MFI and should

not be used as a proxy for the creditworthiness of the

company.

BWR MF 2

BWR MF 3

BWR MF 4

BWR MF 5

BWR MF 6

BWR MF 7

BWR MF 8

Analysts Media

[email protected]

[email protected]

Phone Relationship Contact

Phone: 1-860-425-2742

[email protected]

Mic

ro

fin

an

ce

In

sti

tuti

on

Gr

ad

ing

Margdarshak Financial Services

Ltd. (MFSL)

Page 2

Brickwork MFI Grading | Margdarshak Financial Services Limited 2 | P a g e

Table of Contents

Grading Rationale .................................................................................................................................. 3

Profile ...................................................................................................................................................... 4

Mission & Vision of the company .......................................................................................................... 5

Management Details .............................................................................................................................. 5

Lending Model & Products Strengths .................................................................................................... 6

Operational Model .................................................................................................................................. 7

Collections Process ................................................................................................................................. 8

MIS & Reporting .................................................................................................................................... 8

Share Holding Pattern ........................................................................................................................... 8

Transparency .......................................................................................................................................... 9

Financial Statements ............................................................................................................................ 13

Operational Indicators ......................................................................................................................... 16

Projected Business Growth ……………………………………………………………………………………………..17

Portfolio Details …………………………………………………………………………………………………………….17

Conclusion ……………………………………………………………………………………………………………………19

Page 3

Brickwork MFI Grading | Margdarshak Financial Services Limited 3 | P a g e

Grading Rationale

Brickwork Ratings has assigned ‘MF 2’ grading to Margdarshak Financial Services Ltd (‘MFSL’

or the ‘MFI’).

The grading has factored the long track record of operations, extensive experience of the promoters

and management in the micro finance industry, significant improvement in the operational &

financial performance, adequate capital adequacy and healthy asset quality with 96.20% recovery

rate during FY17. The grading also draws strength from the well-defined operational procedures &

policies, adequate internal controls, risk & cash management policies and robust MIS & IT systems

adopted by the MFI. The grading is, however, constrained due to geographical concentration of the

portfolio in the Northern states, mainly Uttar Pradesh, and other inherent risks associated with the

micro finance industry in terms of regulatory framework and other socio-political issues viz.

unsecured nature of lending, vulnerable customer profile, exposure to vagaries of political situation

in states, and cash handling associated with the NBFC-MFI sector.

Headquartered in Lucknow, Uttar Pradesh, Margdarshak Financial Services Limited (MFSL) a non-

deposit taking NBFC-MFI is a part of the Margdarshak Group promoted by development

professionals in 2004 to carry out financial inclusion activities in the state of Uttar Pradesh. In 2007

Margdarshak group commenced its microfinance operations under the name of ‘Margdarshak

Development Services’ (a not for profit group company). Later in 2010, the promoters of

Margdarshak group acquired a NBFC to carry out the business of financial services in a sustainable

manner with appropriate legal status. MFSL had received the NBFC-MFI license from Reserve Bank

of India in December 2013. MFSL is engaged in a wide range of community development and

livelihood strengthening initiatives across India and is working towards the objective of economic

empowerment for women and poverty alleviation.

The Company is engaged in providing microfinance loans based on Joint Liability Group (“JLG”)

(comprising of 5-15 members) model to poor women residents of urban (~60% of total portfolio)

and rural areas (~40% of total portfolio) to carry out income generation ventures such as trading,

retailing, embroidery shops, eateries, agriculture and allied related activities among others. The

organisation currently operates in 5 states through a network of 120 branches spread across 33

districts of Uttar Pradesh, 9 districts of Bihar, 4 districts of Haryana, 1 district of Uttrakhand and 3

districts of Himachal Pradesh. The operations are well spread across rural, peri-urban and urban

areas of the state, with loan products designed for various segments of the society. The districts have

been chosen taking into consideration the objective of enterprise and livelihood financing in the long

term. All districts have a large number of micro entrepreneurs and workers involved in

internationally acclaimed crafts. The mix of districts allows the company to provide financial services

in both rural and urban areas.

Page 4

Brickwork MFI Grading | Margdarshak Financial Services Limited 4 | P a g e

Profile Summary

Margdarshak Financial Services Limited (MFSL) - MFI Grading Report

Year of incorporation Incorporated in 1996

Year of commencement of

microfinance operations 2007

Legal status Non-Deposit taking Non-Banking Finance Company

Microfinance Institution (NBFC-MFI) registered with RBI.

Lending model Joint Liability Group (JLG)

Managing Director Mr. Rahul J Mittra

Geographical areas of

operation Presence in 50 districts across 5 states of UP, Bihar,

Haryana, Uttarakhand, and Himachal Pradesh.

Branches 120

Business Correspondence

(“BC”) arrangement

IDBI Bank, Yes Bank and Reliance Capital (Direct

assignment)

Margdarshak Financial Services Limited (“MFSL”) is a category B, non-deposit taking NBFC-MFI

headquartered in Lucknow, Uttar Pradesh. The Company is engaged in the business of financial

inclusion and microfinance in North India. Its areas of activities include wide range of community

development and livelihood strengthening initiatives across India. The Company is mainly working

towards the objective of economic empowerment for women and poverty alleviation.

As of March 31st, 2017, MFSL had achieved a Gross Loan portfolio (owned + managed) of

Rs 292.18 Crs, out of which Rs 197.08 crore is own books, Rs 80.95 Crs under Business Correspondence

(“BC”) arrangement with IDBI Bank, Yes Bank and Reliance Capital and Rs 14.14 Crs under direct

assignment.

MFSL has a professional board consisting of promoters, institutional nominees and independent

Directors. Mr Rahul J. Mittra, the founder of MFSL is also the Secretary of Uttar Pradesh Microfinance

Association. The company has raised capital from 2 institutional investors viz. SIDBI & Dia Vikas

Capital Pvt. Ltd apart from the debt support from 14 public sector banks, 2 private sector banks, 12

NBFCs and 4 DFIs.

Page 5

Brickwork MFI Grading | Margdarshak Financial Services Limited 5 | P a g e

● Mission & Vision of the Company

The Mission of the MFI is to provide a holistic bouquet of financial products and services to the

economically weaker enterprising sections of the community for enabling mainstreaming and socio-

economic betterment.

The Vision of the MFI is to adapt industry best practices in all aspects of organization for emerging as

financial service provider of choice for 5,00,000 families in Uttar Pradesh, Bihar and Neighboring

States.

Management Details

Name Designation Experience

Mr. D.P.S. Rathore

Non-Executive

Chairman &

Independent

Director

Over 36 years of banking experience with the Reserve Bank

of India, he retired as Regional Director-RBI in 2011. He

heads the Asset Liability Management Committee and HR &

Compensation Management Committee and guides the

management in the areas of Organizational strengthening,

product development and environment management.

Mr. Rahul. J. Mittra

Promoter

Director, MD &

CEO

PG in Psychology, has over 20 years of working experience in

rural development at grass root level in North India.

Specializes in rural finance, organizational development, and

strategy development and operations management. Prior to

establishing MFSL in 2006, he has worked with

Entrepreneurship Development Institute of India and Asian

Centre for Organization Research & Development

(“ACORD”).

Mr. Arupjyoti Rai

Baruah

Whole Time

Director

Alumnus of Institute of Rural Management, Anand (IRMA),

& B. Tech from Assam Engineering College, he possesses over

25 years of experience in development and corporate sector.

He specializes in enterprise development, business

facilitation and loan portfolio audit and contributes to

visioning of the organization and in livelihood interventions.

He was earlier associated with Entrepreneurship

Development Institute of India, Nagarjuna Fertilizers and

SAIL.

Page 6

Brickwork MFI Grading | Margdarshak Financial Services Limited 6 | P a g e

Mr. K. Prasad Independent

Director

Mr. Prasad has over 35 years of banking experience with

Reserve Bank of India, from where he retired as Chief General

Manager. He has extensive experience in the areas of

Supervision and Examination of Non- Banking Financial

Institutions & Banks including the Developmental Financial

Institutions. He heads the Audit Committee of the Board and

Risk Management Committee of MFSL and is engaged in

training and guiding the internal audit team of the

organization.

Mr. Saneesh Singh

Institutional

Nominee

He has over 25 years of experience in the field of

development, banking and finance, microfinance, financial

inclusion, MSME lending, capital structuring and social and

impact investments. He is the MD of Dia Vikas Capital Pvt.

Ltd. (a subsidiary of Opportunity International Australia). He

is an associate of the Indian Institute of Bankers and an

alumnus of Indian School of Business.

Ms. Saroj Topno Whole Time

Director

M. Com. from Calcutta University, she has over 20 years of

experience in the field of accounting and finance, direct

finance, refinance, development finance and audit. Prior to

joining MFSL in 2008, she has worked for over 11 years

(1996-2008) in various managerial capacities in different

departments of SIDBI. She is an associate of the Indian

Institute of Bankers.

Mr. Bhanu Prakash

Verma

Nominee Director

He has 23 years of experience in the field of Development

Banking, Promotion & Financing of MSMEs and Micro

finance. Presently, he is posted as Deputy General Manager

in SIDBI Foundation for Micro Credit (SFMC) at SIDBI Head

Quarter, Lucknow.

Ms. Maitrayee

Banerjee

Independent

Director

He has over 30 years of banking experience with public sector

bank in India and abroad where she retired as General

Manager. She has extensive experience in Credit, MSE, Self-

Help Groups, Government Sponsored Schemes, Mid-

Corporate and Corporate Credit - processing, sanction and

monitoring thereof. She also holds experience in Foreign

exchange and Treasury Experience.

Page 7

Brickwork MFI Grading | Margdarshak Financial Services Limited 7 | P a g e

Senior Management

Name Qualification Designation Experience

Ms. Saroj Mittra M.Com, C.A.I.I.B ED & CFO

He has 20 years of

experience in the field of

accounting and finance,

direct finance, refinance,

development finance and

audit.

Mr. Gurmeet Singh

Anand

M.Com, MBA-

Finance

AVP-Resource

Generation &

Business Planning

He has over 15 years of

experience in

Development and

Financial sector.

Mr. Gagan Deep Sehgal MBA-Marketing

& Finance

Chief Operating

Officer

He has over 14 years of

handling banking

operations. Worked with

institutions like ICICI

Bank Ltd, Kotak Mahindra

Bank and IndusInd Bank.

Mr. Rohit Sinha MBA- Marketing Dp. V.P- Risk, Audit

and Monitoring

He has over 12 years of

banking and Financial

Inclusion experience with

institutions such as HDFC

Bank etc.

Mr. Yogendra Bharti B.Tech & MBA DVP- Technology

He has over 10 years of

Technology and FI

experience with

institutions such as FINO,

UIDAI etc.

Ms. Anchit Pandey CS Company Secretary

She has over 5 years of

experience in a Secretarial,

Legal and Managerial work

profile, with proficiency in

handling Corporate Law

matters, statutory

compliances, drafting and

documentation.

Page 8

Brickwork MFI Grading | Margdarshak Financial Services Limited 8 | P a g e

Lending Model & Products Strength

The key lending model and the products offered by MFSL is described below:

• Lends to Joint Liability Groups (JLGs).

• Lends only to Women.

• Progressive Borrowers include economically active women primarily for income generation

purpose such as service enterprises, retail/trading, production & manufacturing unit, livestock,

agri & allied activities etc.

• The first category of loans, which constitutes bulk of the loans, is provided to women who are

involved in a host of agri-allied activities, handicraft, livestock rearing and petty trading related

activities. The loan amount ranges from INR 15,000 to INR 35,000. The Company also offers

Home Improvement Loan product to extend loans to the range of INR 50,000 to INR 75,000

for home improvement, extension and addition (except for new house construction) under

funding support from Habitat Microbuild India Housing Finance Co. Pvt. Ltd.

• Lending process of the company is segregated into various well–defined sub-steps beginning

with area identification where-in areas for expansion are identified. Both primary and

secondary data of the block/tehsil/district is collected on an Excel calibrated sheet. The sheet

gives score to the area on certain predetermined indicators. Areas achieving a score of 60 and

above are picked up for establishing branches. The company’s branch staff does group formation

by conducting promotional meeting and training of potential borrowers on company policy etc.

The borrowers clearing credit bureau check and satisfying other criteria for borrowing are

provided with loan ranging from 15K to 35K. The borrower details are captured on a web based

software of the company. Repayment from borrowers is collected during group meetings

conducted by company staff on a fixed day and time. The collections are recorded on a mobile

handset which enables the company in monitoring collections against schedule on a real time

basis.

• Salient details of the loan products provided by MFSL are given below:

Name of Loan Product

Income Generation Loan Home Improvement Loan

Loan Amount INR 15000-35000 (Multiples of Rs 5000)

INR 50000-75000

Purpose Livestock, vegetable vending, Family enterprises, artisans etc. for

borrowers with monthly Income – Between 7000-10000

Minor Repair and Renovation in the house

ROI 24.92%

23.00%

Duration 12/18/24 month 36 month (Moratorium period of 1

month)

Page 9

Brickwork MFI Grading | Margdarshak Financial Services Limited 9 | P a g e

Loan Processing Charges

1% of Loan amount with applicable taxes

2% of Loan amount with applicable taxes

Repayment Frequency

Monthly/Fortnightly/Weekly as mutually agreed with the

borrower.

Monthly EMI

Other Charges Insurance Premium as per actual Insurance Premium as per actual

Portfolio O/S as of 30-Sep-2017

Rs 186.11 Crs Rs 4.33 Crs

% of Total Portfolio 97.72% 2.28%

Operational Model

Process of loan origination, sanction and disbursement

• Area identification and selection: While identifying the areas for expansion, preference is

given to areas having no or negligible microfinance intervention. Area Identification is primarily

done by the senior management. The list of pre-identified areas has been developed as per the

geographical expansion plan of the organization with specific timelines (year-wise.). The

districts / areas, identified have been selected on the basis of having high population, high no.

of household, high population density and high population growth rate. This has been clubbed

with low microfinance activity and low natural, social and political risks.

● Identification of Borrowers: Once an area is approved for intervention, the Field Officer

(FO) along with Branch Head of the organization conducts promotional meetings for

identification of the potential borrowers. The Company runs awareness campaigns about JLG

lending before the launch of its operations in an area. To achieve this, key people in the area are

made aware about the program. In order to educate the people about the concept of micro

finance, meetings are called at a pre-decided venue and time. During the promotional meeting,

field officers are asked to gather potential people who may get converted into member in near

future. The branch team addresses the gathering by giving their introduction & company’s

introduction, and thereafter distributes pamphlets to potential customers. Apart from

promotional meeting, household listing format is also filled by FO for the particular Mohalla /

Village. This information is filled during the door to door visit of FO for the area where the no.

of households is more than 150 or above in the following format.

● Selection of Borrowers: As per company’s policy one family is provided with only one loan

to permanent resident of the locality. The company follows RBI guidelines for borrower

selection and therefore, annual household income should not exceed INR 100,000 for rural

families and INR 1,60,000 for urban families. In addition to the annual household income,

company also ensures that the loan size does not exceed INR 60,000 in 1st cycle and INR

100,000 in subsequent cycles.

● Group Formation and Approval: After the promotional meeting, interested borrowers are

given 3 day orientation on company policies and processes. On the first day, FO forwards the

Page 10

Brickwork MFI Grading | Margdarshak Financial Services Limited 10 | P a g e

KYC through mobile application for processing of Credit Bureau (CB) check at data center. The

report received from CB enables the organization to take the decision on lending to the client.

After analyzing the CB overlap report, additional data of client eligible for loan is incorporated

and clients are allocated in a group. Simultaneously, the group is formed and presented before

Branch Manager (BM) on 3rd day for Group Recognition Test (GRT). The role of BM in GRT is

to do residence verification, business verification and also assess the borrowing and repayment

capacities of the borrower.

● Back Office Appraisal & Sanctioning: Before approval, back office team (IVRS) thoroughly

validates the membership form along with the KYC enclosed and cross verifies the client

requirement/verification through tele-audit. The report received from CB enables the

organization to take the decision on lending to the client. After analyzing the CB overlap report,

complete loan application of client eligible for loan is incorporated in the software. Henceforth,

MIS supervisor sanctions the loan and expected disbursement sheet is generated on the

disbursement mobile application module.

● Disbursement: All approved loan applications are disbursed jointly by the BM and the cashier

from a central location which is branch office. MFSL follows cashless disbursement process for

all loans above Rs 20,000. There is a gap of two days between the date of sanction (sanction in

software after Credit Bureau clearance) and disbursement to ensure proper communication to

the clients of a group. The responsibility of BM is to ensure that loans disbursed are utilized for

income generation purpose and all other members stand guarantee to repay the loan in case of

delinquency by the client. The disbursement to the groups are done on the group meeting day,

where prior to disbursement joint liability agreement is signed in the group meeting itself and

clients are informed about the disbursement timings. The disbursements are made to the clients

in the order as appearing in the disbursement sheet and no cash is collected from the client at

the time of disbursement.

● Group Meeting & Collection: Responsibility for conducting the group meeting is given to

FO on fortnightly basis. As per the company’s loan policy, it is mandatory for all the members

of the group to participate in the group meeting for repaying their instalments. The FO will

enter the amount of cash collected from individual members on Collection Demand Sheet

generated through the mobile application, which indicates about the total outstanding

(principal and interest), total due (principal and interest) and total collection to be received

along with the signature of client. The group in return is provided proper numbered receipt

against the payment of the group instalments. Thereafter, the instalment received is also

updated on the Loan card provided to all the borrowers.

• Post Disbursement Monitoring viz. end use Verifications: Loans provided by the

organization are only to be utilized for income generation activities. The responsibility of FO is

to closely monitor the utilization of each loan disbursed. Within one month of disbursement, all

BMs are required to do Loan Utilization Check (LUC) by visiting the groups to check whether

Page 11

Brickwork MFI Grading | Margdarshak Financial Services Limited 11 | P a g e

the loan has been utilized as per loan purpose mentioned in application form. After one month,

the internal audit team during the field audit also re-verifies 100% of the loan utilization done

by FO’s done in the last month.

• Loan Monitoring Mechanism: MFSL checks the progress of borrower’s business and how

much the income level has increased after the loan disbursement. Monitoring the performance

of the borrower is based on the progress reports prepared through visits and supervision.

Delinquency Management

The organization has a standardized and well established delinquency management process described

below:

● During the group meeting, if any client of the group is not able to pay the current dues, the field

officer’s responsibility is to cross-verify with the client and discuss within the group meeting the

reason for not repaying the instalment. If the reason is genuine, the group members are asked

to jointly contribute towards the current instalment and thereafter Field Officer (FO) updates

the details in the loan card and CDS and issue a proper numbered receipt towards the group

installment.

● In case of wilful default, FO discusses within the group for repaying of default payment for a

particular client and simultaneously informs the branch manager regarding the default. The

Branch Manager (BM) thereafter visits the group and continues with the group meeting where

the BM motivates the defaulting client to repay and asks group to exert peer pressure.

● If joint liability is not exercised, then BM and FO leave the group meeting and return to the same

group after end of all group meeting for the day for concerned FO. The BM/FO tries to motivate

all the clients of the group and inform them there will be no extra interest charged in case of any

delinquent payment but the track record of the group will not be satisfactory.

● If the client/group members are not ready to repay, then BM updates the Area Manager (AM)

on the same day regarding delinquency in the group. During the visit of AM, group meeting is

organized and reason of delinquency is discussed in detail.

● If the group and Client are not ready to pay for delinquent client, then the Field Officer is being

instructed to keeps on following up every week till the recovery of default installment.

Page 12

Brickwork MFI Grading | Margdarshak Financial Services Limited 12 | P a g e

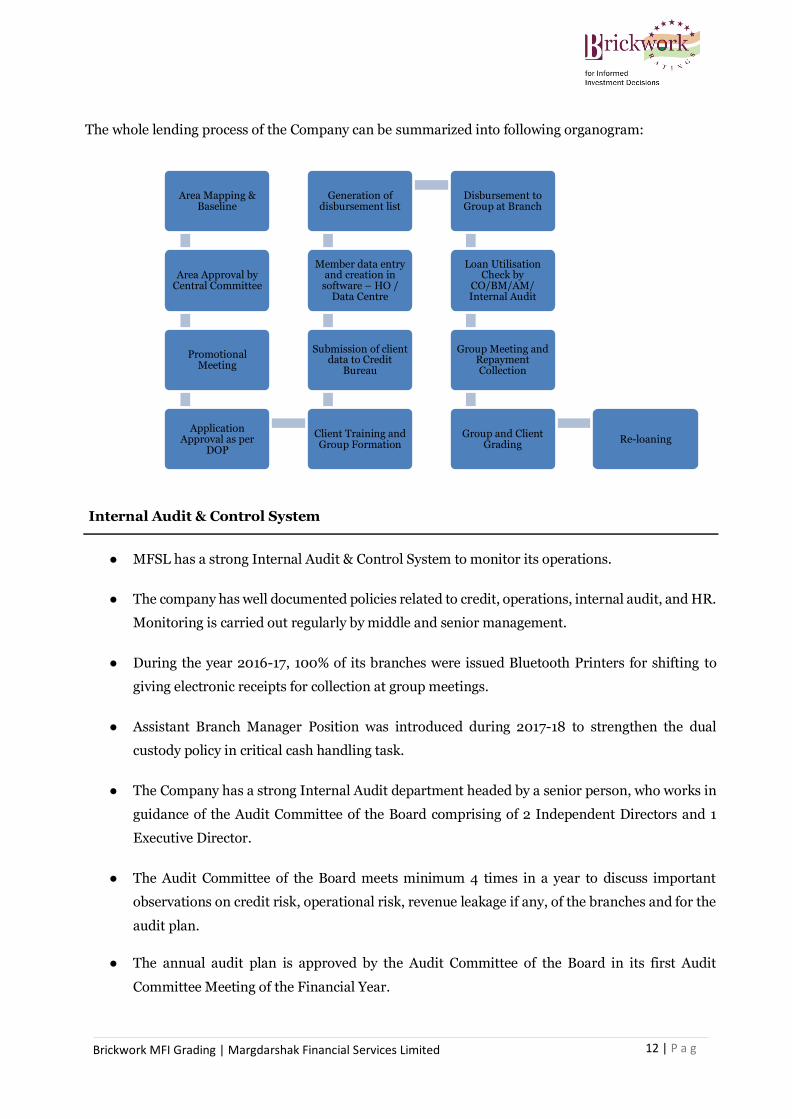

The whole lending process of the Company can be summarized into following organogram:

Internal Audit & Control System

● MFSL has a strong Internal Audit & Control System to monitor its operations.

● The company has well documented policies related to credit, operations, internal audit, and HR.

Monitoring is carried out regularly by middle and senior management.

● During the year 2016-17, 100% of its branches were issued Bluetooth Printers for shifting to

giving electronic receipts for collection at group meetings.

● Assistant Branch Manager Position was introduced during 2017-18 to strengthen the dual

custody policy in critical cash handling task.

● The Company has a strong Internal Audit department headed by a senior person, who works in

guidance of the Audit Committee of the Board comprising of 2 Independent Directors and 1

Executive Director.

● The Audit Committee of the Board meets minimum 4 times in a year to discuss important

observations on credit risk, operational risk, revenue leakage if any, of the branches and for the

audit plan.

● The annual audit plan is approved by the Audit Committee of the Board in its first Audit

Committee Meeting of the Financial Year.

Area Mapping &

Baseline

Area Approval by

Central Committee

Promotional

Meeting

Application

Approval as per DOP

Client Training and Group Formation

Submission of client

data to Credit Bureau

Member data entry and creation in

software – HO / Data Centre

Generation of

disbursement list

Disbursement to Group at Branch

Loan Utilisation Check by

CO/BM/AM/ Internal Audit

Group Meeting and

Repayment Collection

Group and Client

Grading Re-loaning

Page 13

Brickwork MFI Grading | Margdarshak Financial Services Limited 13 | P a g e

● The audit procedure covers following broad aspects:

● Field Audit: In field audit, auditors check the adherence of process & policies,

verification of loan utilization, group meetings, CGT & GRT and overall group discipline.

The audit team also verifies and checks the client attendance, agent involvement if any

and overall group discipline & whether the field staff is following the code of conduct as

per the Company’s norms or not.

● Branch Audit: In branch audit, the auditor verifies the various aspects including the

branch opening time, cash handling, attendance register and leave register, cash book,

key register, movement register, stock register, stationary register, stationary storage,

physical cash verification, denomination matching, petty cash book maintenance,

voucher verification and cheque register. The audit team also checks the disbursement

process.

● Document Audit: In this, the auditor checks the group files which include loan

document, joint liability agreement, CGT form, membership details data, loan

application, GRT, KYC document, demand promissory note and joint liability form.

● Tele Audit: Tele audit consists of 2 parts viz., disbursement check by calling the client

and to verify whether the clients has prepaid the loan or wants normal closure of loan.

● Surprise Audit: Surprise audit include verification of physical cash with cash book

and cash balance book, attendance of field staff, conduct of group meeting and collection

process.

The auditor discusses with the BM/AM and staff regarding the observations. The auditor also discusses

the minor observation with the branch staff during the course of audit and helps in rectifying the

observations. The auditor also checks whether the observation of last audit has been complied with.

MIS & Reporting

● MFSL uses web-based integrated software for information management developed by Force Ten

Technologies, a Kolkata based Software Company. The web based software is an advanced

version of the LAN based software used earlier.

● The software integrates operations management, accounting, HR management and financial

management. The migration to web-based software has enabled the organization in de-

centralizing its operations management & monitoring thus reducing load at HO level & enabling

localization of operations management.

● The de-centralization has further reduced the TAT in following up on discrepancies at the field

level and addressing the same in a reasonable time.

● MFSL has introduced mobiles for managing front end operations.

● As initial steps, the most time consuming aspects of recording client repayments &

Page 14

Brickwork MFI Grading | Margdarshak Financial Services Limited 14 | P a g e

disbursements have been migrated to mobile modules – wherein the facilities have been

provided to client interface management team (operations) to upload & download client data

for operations management.

● The successful integration of mobile modules in the software, have enabled availability of real-

time information related to collections, disbursements and outstanding / overdue with the

central monitoring office.

● This has also reduced the HR requirements and increased information management efficiencies

in the organization.

● The software produces summaries for all available accounts for any given period (by choosing a

beginning and end date for the account summary).

● Integrated reports show information sorted by independent variable (Field Officer, District,

Area etc.) related to groups and members.

● MIS reports regarding loans, security, portfolio, financial ratios and repayment schedules are

also available.

Membership with Credit Bureaus

MFSL is member of 4 RBI accredited credit bureaus- Highmark Credit Information Services, Equifax

Credit Information Services Pvt. Ltd., and Experian along with CIBIL. While client data is submitted to

each credit bureau, credit history checks are made for low end clients (JLG loans) with Highmark and

for individual loans credit history is checked with CIBIL. Currently 100% of client data is shared and

submitted to the CB’s on a weekly basis. The organization is also an active member of Sa-dhan –

Association of Microfinance Institutions, and is one of the founder members of the state chapter of

Sa-dhan. Mr. Rahul Mittra, Managing Director of the company, is Vice President of the state chapter of

Sa-dhan.

Page 15

Brickwork MFI Grading | Margdarshak Financial Services Limited 15 | P a g e

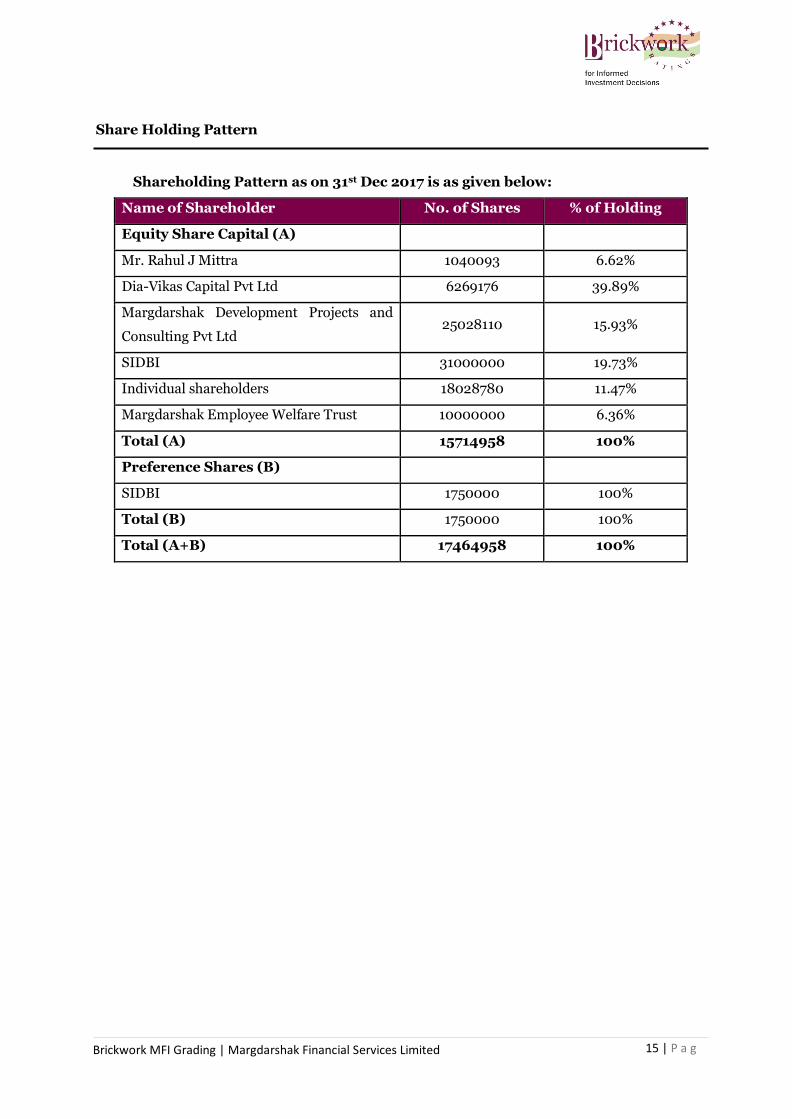

Share Holding Pattern

Shareholding Pattern as on 31st Dec 2017 is as given below:

Name of Shareholder No. of Shares % of Holding

Equity Share Capital (A)

Mr. Rahul J Mittra 1040093 6.62%

Dia-Vikas Capital Pvt Ltd 6269176 39.89%

Margdarshak Development Projects and

Consulting Pvt Ltd 25028110 15.93%

SIDBI 31000000 19.73%

Individual shareholders 18028780 11.47%

Margdarshak Employee Welfare Trust 10000000 6.36%

Total (A) 15714958 100%

Preference Shares (B)

SIDBI 1750000 100%

Total (B) 1750000 100%

Total (A+B) 17464958 100%

Page 16

Brickwork MFI Grading | Margdarshak Financial Services Limited 16 | P a g e

Transparency

1- Management Quality

Extensive microfinance

experience in area of operations

The promoters of the company are well experienced in the

microfinance and asset finance sector. The management team

comprises of professionals from varied fields such as Banking,

Law, Finance and Accounting etc. The Chairman of the Board

was the former Former Regional director of Reserve Bank of

India (RBI). He has almost four decades of experience in

Banking, finance, currency, public debt, administration,

personnel, human resources (specially training field), foreign

exchange (including control as well as management), rural

credit, training, legal work and education, financial literacy etc.

. Also the promoters have hired qualified and experienced

professionals to manage different departments of the company

Business Strategies

The company has well defined operational procedures &

policies. There are adequate policies in place to manage various

types of risks as well as to efficiently manage cash.

Financial and accounting &

Corporate Governance policies

and processes

MFSL has a separate Internal Audit team which verifies the

transactions, financial statements, compliance & operational

aspects periodically. Also, the board includes independent

directors to ensure quality of reporting and corporate

governance.

The management’s stability and

inclusion/exit of key management

personnel

Management team and senior personnel are qualified and

experienced in the microfinance sector. The management keeps

on strengthening its staff in order to accommodate the business

growth and manage its operations efficiently.

Vision and Social Impact expected

to be achieved through

operations.

MFSL, apart from the regular microfinance loans, provides

credit for Home Improvement. It has also tied up with three

insurance Companies viz. Kotak Mahindra Life. DLF Pramerica

& SBI Life Insurance to provide insurance services to its

customers. Further, the company also regularly organizes

activities such as medical check-ups, eye check-up, drug de-

addiction awareness, etc. and arranging presentations on

money management, financial literacy and credit discipline.

Page 17

Brickwork MFI Grading | Margdarshak Financial Services Limited 17 | P a g e

2- Social Impact

The segments of borrowers

financed and the reason for

financing

MFSL primarily finances women borrowers from low/mid

income households, who do not have access to banking

services. The loans given are mainly towards income generating

activities.

The presence of other financial

service companies in the region

MFSL is currently operating in 5 states through a network of

120 branches spread across 33 districts of Uttar Pradesh, 9

districts of Bihar, 4 districts of Haryana, 1 district of

Uttarakhand and 3 districts of Himachal Pradesh.

Tie ups with corporate houses for

Corporate Social Responsibility

Programs etc.

MFSL is constantly working towards economic strengthening

of the clients by understanding their need for financial services,

vocational trainings and business development support.

During the last few years, MFSL had conducted around 175

financial literacy training programs covering around 6,125

participants with the support of SIDBI. During FY17, Digital

Literacy Programme for micro business clusters of Uttar

Pradesh, was conducted during the month of April 2017 in 14

districts of UP covering around 1600 clients which, among

other things, introduced digital platforms of different version

such as Paytm, Oxigen and BHIM to clients and their family

members for transaction.

3- Business Model

Good loan tracking system and

process-control mechanism for

present scale of operations

The entire process is tracked and monitored through the

centralized system. The responsibility of FO is to closely

monitor the utilization of each loan disbursed. Within one

month of disbursement, all BMs are required to do loan

utilization check by visiting the groups to check whether the

loan has been utilized as per loan purpose mentioned in

application form. After one month, the internal audit team

during the field audit also re-verifies 100% of the loan

utilization done by FO’s done in the last month.

Page 18

Brickwork MFI Grading | Margdarshak Financial Services Limited 18 | P a g e

Adequate HR practices

Brickwork Ratings opines that MFSL has satisfactory HR

polices in place for its present scale of operations. The company

has a HR manager who oversees staff recruitment, incentive

planning and annual performance appraisal. Also, MFSL has a

systematic approach to building the pipeline, and it now uses

these trained pool of senior and middle managers to groom the

next level managers for more senior roles.

Adequate Recovery and

collections process

MFSL has well defined and stringent recovery and collection

process. As per the company’s loan policy, it is mandatory for

all the members of the group to participate in the group meeting

for repaying their instalments. The organization has a

standardized and well established delinquency management

process. The recovery is done in the Group meeting and in case

any borrower fails to repay her liability, other members

contribute and make the payment to FO (Field Officer).

Good management information

system (MIS) and process control

mechanism

MFSL uses web-based integrated software for information

management developed by Force Ten Technologies, a Kolkata

based Software Company. The software integrates operations

management, accounting, HR management and financial

management. It produces summaries for all available accounts

for any given period. Integrated reports show information sorted

by independent variables (Field Officer, District, Area etc.)

related to groups and members. MIS reports regarding loans,

security, portfolio, financial ratios and repayment schedules are

also available. MFSL has also introduced mobiles for managing

front end operations.

Cash management system

MFSL has developed Board approved Liquidity and Funding

Risk policy which, among other things, covers cash

management system. So, the Company has a formal cash

management policy. Book keeping and cash management is

handled by the Branch Manager along with the Assistant

Branch Manager. The Cash Management System follows a dual

reporting structure, with operational reporting to the Branch

manager and functional reporting to the data centers. The

Company also avails Cash-in-Transit insurance from Bajaj

Allianz General Insurance Company.

Page 19

Brickwork MFI Grading | Margdarshak Financial Services Limited 19 | P a g e

4- Operational Efficiency

Policy and operational manual in

place

All the operational procedures and policies ranging from client

identification, sanction, disbursement and collection are well

defined.

Management has adequate

experience to upscale and sustain

operations

The management team comprises of professionals from varied

fields such as Banking, Law, Finance and Accounting etc. The

Chairman of the Board was the former Regional director of

Reserve Bank of India (RBI). Also the promoters have hired

qualified and experienced professionals to manage different

departments of the company.

Growth in microfinance

operations and earning profile

MFSL has reported significant growth in its portfolio. The Loan

portfolio (Owned) stood at Rs 197.08 Crs as on

March 31 2017 as against Rs 119.12 Crs as on March 31 2016.

5- Enterprise Risk Management

Independent risk

management division and

independent internal audit

with Monitoring and

supervision

MFSL has a large team of Internal Auditors, responsible for

conducting the audit of all the branches of the Company on a regular

basis covering all the aspects in detail. Internal audit is performed

on a quarterly basis. The audit report is presented to the Head of

Operations. The report and its findings are discussed in the

Operations Meetings as well as in the Audit Meetings. Audit reports

are also shared with the respective Branches, so that they are aware

of their shortcomings and improve them accordingly. The RM

(Regional Manager) with the team takes responsibility to ensure

that relevant actions are taken on the Audit findings. The auditors

in their subsequent visits to the Branch ensure that the findings are

addressed.

Loan sanction and disbursal

policies

MFSL has defined detailed loan sanction and disbursement

procedure that involves various checks at different stages of the

process. End use verification & loan monitoring mechanisms are

also in place to ensure right utilization of the proceeds.

Page 20

Brickwork MFI Grading | Margdarshak Financial Services Limited 20 | P a g e

Management of credit,

market and operational risks

MFSL follows a centralized loan sanctioning process. The company

maintains a stringent KYC policy and is registered with four credit

bureaus to mitigate the credit risk. MFSL has invested in

technology and the company shifted to a cashless disbursement (for

loan amount greater than Rs 20,000) & repayment platform in

order to increase efficiency at operational level and induce greater

transparency. Adequate policies for management of credit and

operational risks are in place.

Fraud detection and

management

The MFI makes efforts to detect fake disbursements & curtail

frauds by creating multiple client verification checkpoints,

triangulation of the data, staff Training, staff awareness on Whistle

Blower Policy, client education & empowerment and cashless

disbursements.

Any misappropriation of collection amount or advances/

commission taken from clients is also monitored closely. The MFI

observes spending patterns of the staff and looks for instances

where lifestyle appears to be beyond his affordability. Client

education, staff training and awareness, staff verification and

guarantee mechanism, proper placement of staff to ensure he does

not work in his own village and rotation and transfer of field staff

after every year are some of the key initiatives of MFSL to monitor

the fraudulent practices.

Management of legal and

compliance risk

MFSL has a Legal department to oversee all the legal affairs of the

company and to ensure provision of appropriate legal advice &

supervision. Further, Vigilance officer ensures ethical conduct and

compliance with rules, regulations and standard processes of the

company.

Reputation and

strategic risks

The promoters are reputed and experienced in the Banking,

Microfinance and Financial Services segment.

Page 21

Brickwork MFI Grading | Margdarshak Financial Services Limited 21 | P a g e

6 - Financial Performance

Adequate Capitalization

As on 30th September 2017, MFSL reported a CRAR of 18.39%.

As per RBI guidelines for NBFCs, they have to maintain a

minimum CRAR of 15%.

Asset Quality

MFSL has always maintained its asset quality and has not

reported any NPAs during the past five years. MFSL writes off

loans where they are overdue for more than 180 days or where

the asset has been declared as loss or non-recoverable, on

receiving the Board approval. MFSL follows the RBI loan

provisioning policies for addressing the risk of delinquency and

default done by borrower.

Funding Profile

MFSL has availed funding from 32 lenders (including 14 PSU

Banks), however their resources profile continues to remain

concentrated towards borrowings from NBFCs which stood at

58% of total borrowings. The borrowings from Reliance Capital

Limited and MAS Financial Services Limited accounts for 23%

of the total borrowings (outstanding debt) as on March 31,

2017. MFSL has also issued NCDs & Subordinated Debt to

retail investors. It has also raised first tranche of Rs. 20.00 Crs

in Aug 2017 out of the rated NCDs of Rs 40 Crs from Japan

ASEAN Women Empowerment Fund @ 13.25%.

Cost of funds

The cost of funds (COF) for MFSL stood relatively lower at

16.08% in Sep-2017 against 16.28% in Mar-2017, despite an

increase in borrowings from NBFCs. While these relationships

with NBFCs have helped MFSL in meeting its funding

requirements to meet the projected growth, however the

company would have to increase its funding mix from banks to

bring down the cost of borrowing.

Earning Profile

The earnings capability of the company increased considerably

during FY17. The Interest Income, Net Interest Income and

PAT increased by 178%, 157% and 142% respectively in FY17.

Page 22

Brickwork MFI Grading | Margdarshak Financial Services Limited 22 | P a g e

Financial Statements

Profit & Loss Summary (Rs. Crores)

Particulars FY14A FY15A FY16A FY17A 6MFY18

(A)

P & L Summary (Rs. in Crores)

Interest Income

7.23

11.40

23.92

42.52

25.17

Interest Expense

2.84

5.25

13.91

26.84

15.35

Net Interest Income

4.39

6.15

10.00

15.68

9.83

Income from Other Financial Services

0.39

2.52

6.38

7.98

4.21

Other Financial Charges

0.37

0.74

1.37 1.34

0.94

Other Income

0.16

0.07

0.15

0.33

0.43

Total Income

4.57

8.00 15.17

22.65

13.53

Employee Benefit Expenses

1.83

2.95

6.16 9.51

6.09

Provision for contingencies

Other Expenses

1.79

2.83

4.38

6.25

3.77

Total Expenses

3.62

5.78

10.54 15.76

9.86

PBDTA

0.95

2.22

4.62

6.89

3.67

Depreciation

0.09

0.57

0.98 1.92

1.17

PBT

0.86

1.65

3.64

4.98

2.51

Taxes

0.28

0.61 1.21 1.53

0.83

PAT

0.58

1.05

2.43

3.44

1.68

Page 23

Brickwork MFI Grading | Margdarshak Financial Services Limited 23 | P a g e

Balance Sheet Details (Rs. Crores)

Line Item FY14 FY15 FY16 FY17 6MFY18

(A)

Liabilities (Rs. in Crores)

Equity And Reserves 12.79 19.83 24.44 28.65 30.76

Share capital 10.83 16.06 17.61 17.54 17.54

Reserves and Surplus 1.97 3.77 6.83 11.11 13.22

Money Received Against Share Warrants

Non-current liabilities 16.40 27.02 62.24 109.72 96.55

Long-Term Borrowings 16.38 26.94 62.08 109.15 95.75

Deferred Tax Liabilities (Net) 0.01 0.08

Other Long Term Liabilities

Long-Term Provisions

0.16 0.57 0.80

Current liabilities 14.83 44.07 79.75 131.49 130.82

Short-Term Borrowings

2.95

Trade Payables

CPLTD 13.90 39.04 75.84 125.83 123.27

Other Current Liabilities 0.45 1.17 1.99 3.44 4.33

Short-Term Provisions 0.48 0.92 1.91 2.22 3.22

Total 44.02 90.93 166.43 269.87 258.13

Assets (Rs Cr)

Non-current assets 2.71 32.66 55.25 100.10 110.02

Tangible Assets 0.74 1.29 1.86 3.23 3.42

Intangible Assets

Non-Current Investments 1.91 10.93 12.00

-

Deferred Tax Assets (Net)

0.06 0.14 0.16

Long Term Loans and Advances

19.16 37.94 71.60 82.02

Other Non-Current Assets 0.06 1.28 3.41 25.13 24.41

Current assets 41.31 58.27 111.18 169.76 148.11

Current Investments 0.33 1.89 5.85 10.55 13.36

Receivables under Finance Activity

Cash and Cash Equivalents 2.90 13.52 17.70 23.60 17.16

Short-Term Loans and Advances 37.40 40.69 81.99 114.93 108.42

Other Current Assets 0.69 2.17 5.64 20.68 9.17

Total 44.02 90.93 166.43 269.87 258.13

Page 24

Brickwork MFI Grading | Margdarshak Financial Services Limited 24 | P a g e

Key Financial Ratios

Financial Ratios FY15 (A) FY16 (A) FY17 (A) 6MFY18

(A)

Cost Management Ratio

Interest Income/ Interest Expense 48.12% 62.82% 67.53% 65.27%

Operating Expense ratio as a % of gross

loan portfolio (Excluding Provision on

Std. Assets) (in %)

8.12% 7.95% 7.30%

7.75%

Capital Adequacy

CRAR (in %) 27.14% 15.55% 17.21% 18.39%

Asset Quality

Gross NPA (%) Nil Nil Nil 0.82%

Net NPA (%) Nil Nil Nil 0.81%

Viability Indicators

Average cost of borrowings (in %) 14.65% 16.58% 16.28% 16.08%

Net Interest margin (in %) 1.48% 1.78% 1.92% 1.75%

Operational Self Sufficiency (OSS) (in %) 113% 113% 111% 109%

Profitability Indicators

Yield on average portfolio (in %) 25.02% 25.96% 25.67% 25.58%

ROAA (%) 1.55% 1.76% 1.57% 1.27%

ROE (%) 7.72% 14.60% 19.45% 19.11%

Portfolio Quality Indicators

Write-Off Ratio 0.005% 0.04% 0.02% 0.02%

Note: The ratios are as per BWR’s calculation.

• NPA for an NBFC-MFI is recognized for Portfolio at Risk (PAR) greater than 180 days. MFSL

has not reported any NPAs during the past five years.

• CRAR of 17.21% for FY17 is well above the RBI requirement of 15% and hence, the Company

can leverage its balance sheet to meet its future loan portfolio growth

Page 25

Brickwork MFI Grading | Margdarshak Financial Services Limited 25 | P a g e

Operational Indicators

Particulars Performance for last three years 2017-18

FY2015 FY 2016 FY 2017 As of Sep-17

Client details

No. of active members at

the start of year

43527 84011 134566 212805

No. of active borrowers at

the start of year

41258 82670 133847 201185

No. of active members at

the end of year

84011 134566 212805 227597

Own 55409 83340 140524 156545

Managed 28602 50865 72281 71052

No. of active borrowers at

the end of year of which,

82670 133847 201185

215800

Own 54068 82982 128904 144748

Managed 28602 50865 72281 71052

No. of savers at the end of

year, if any

Nil Nil Nil Nil

Organizational details FY2015 FY 2016 FY 2017 As of Sep-17

No. of field offices /

branches

52 89 120 120

Total staff strength 252 487 799 776

Field staff 155 288 449 387

Managerial staff 97 199 350 389

Page 26

Brickwork MFI Grading | Margdarshak Financial Services Limited 26 | P a g e

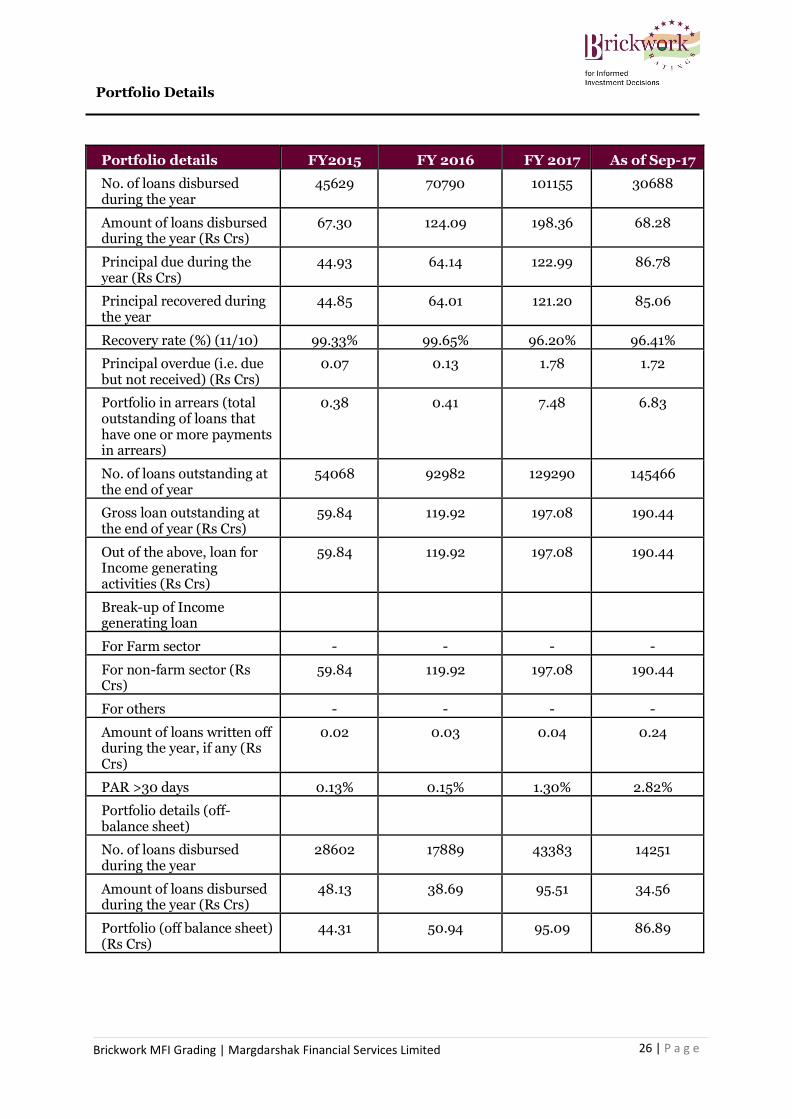

Portfolio Details

Portfolio details FY2015 FY 2016 FY 2017 As of Sep-17

No. of loans disbursed during the year

45629 70790 101155 30688

Amount of loans disbursed during the year (Rs Crs)

67.30 124.09 198.36 68.28

Principal due during the year (Rs Crs)

44.93 64.14 122.99 86.78

Principal recovered during the year

44.85 64.01 121.20 85.06

Recovery rate (%) (11/10) 99.33% 99.65% 96.20% 96.41%

Principal overdue (i.e. due but not received) (Rs Crs)

0.07 0.13 1.78 1.72

Portfolio in arrears (total outstanding of loans that have one or more payments in arrears)

0.38 0.41 7.48 6.83

No. of loans outstanding at the end of year

54068 92982 129290 145466

Gross loan outstanding at the end of year (Rs Crs)

59.84 119.92 197.08 190.44

Out of the above, loan for Income generating activities (Rs Crs)

59.84 119.92 197.08 190.44

Break-up of Income generating loan

For Farm sector - - - -

For non-farm sector (Rs Crs)

59.84 119.92 197.08 190.44

For others - - - -

Amount of loans written off during the year, if any (Rs Crs)

0.02 0.03 0.04 0.24

PAR >30 days 0.13% 0.15% 1.30% 2.82%

Portfolio details (off-balance sheet)

No. of loans disbursed during the year

28602 17889 43383 14251

Amount of loans disbursed during the year (Rs Crs)

48.13 38.69 95.51 34.56

Portfolio (off balance sheet) (Rs Crs)

44.31 50.94 95.09 86.89

Page 27

Brickwork MFI Grading | Margdarshak Financial Services Limited 27 | P a g e

State wise data

State No. of Districts No. of Branches Gross Loan outstanding

(Rs Crs)

UP 33 83 188.60

Bihar 9 21 64.90

Haryana 4 11 20.14

Uttarakhand 1 2 2.27

Himachal Pradesh 3 3 1.42

Total 50 120 277.33

Charts and Graphs

Portfolio Details

The portfolio is majorly concentrated in the state of Uttar Pradesh. Uttarakhand and Himachal

Pradesh have a relatively lower share in the overall portfolio. MFSL needs to increase its presence in

these states as well as add new geographies to reduce the geographical concentration risk and

achieve growth.

0

50

100

150

200

250

300

UP Bihar Haryana Uttarakhand HimachalPradesh

Total

188.6

64.920.14 2.27 1.42

277.33

LOA

N O

/S (

RS

CR

S)

STATES

State wise Loan O/S [Including Managed Loans](Rs Crs)

Page 28

Brickwork MFI Grading | Margdarshak Financial Services Limited 28 | P a g e

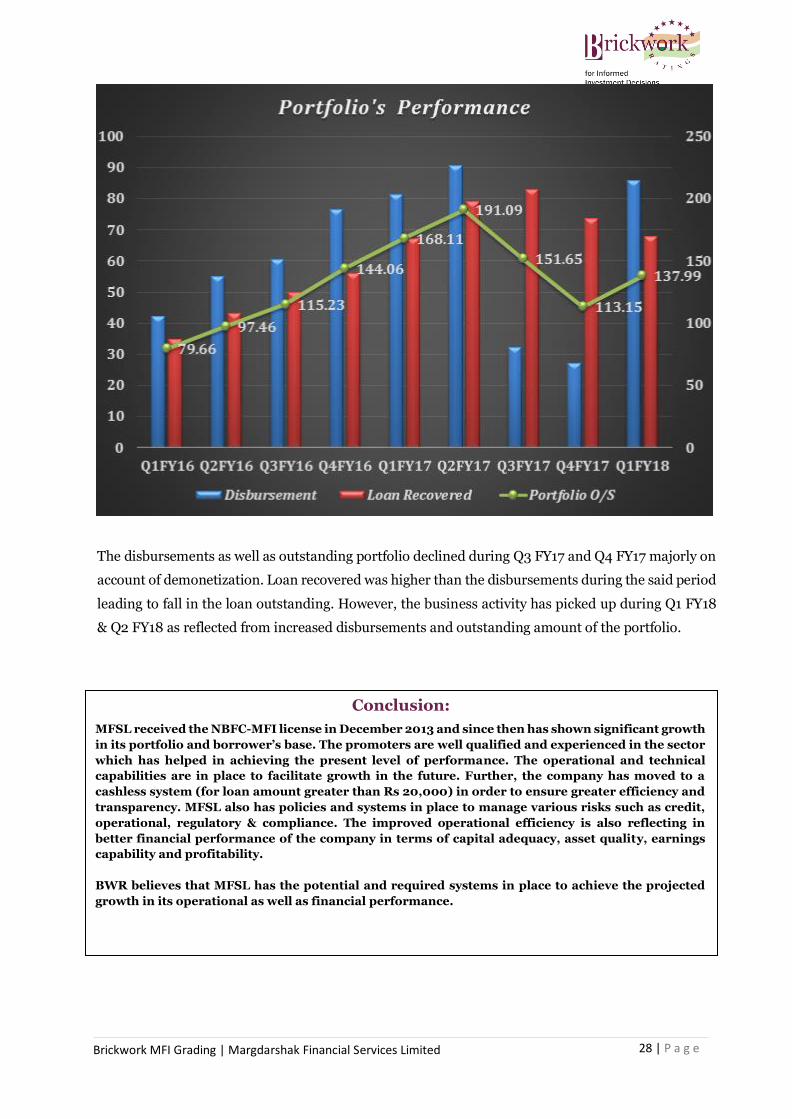

The disbursements as well as outstanding portfolio declined during Q3 FY17 and Q4 FY17 majorly on

account of demonetization. Loan recovered was higher than the disbursements during the said period

leading to fall in the loan outstanding. However, the business activity has picked up during Q1 FY18

& Q2 FY18 as reflected from increased disbursements and outstanding amount of the portfolio.

Conclusion:

MFSL received the NBFC-MFI license in December 2013 and since then has shown significant growth

in its portfolio and borrower’s base. The promoters are well qualified and experienced in the sector

which has helped in achieving the present level of performance. The operational and technical

capabilities are in place to facilitate growth in the future. Further, the company has moved to a

cashless system (for loan amount greater than Rs 20,000) in order to ensure greater efficiency and

transparency. MFSL also has policies and systems in place to manage various risks such as credit,

operational, regulatory & compliance. The improved operational efficiency is also reflecting in

better financial performance of the company in terms of capital adequacy, asset quality, earnings

capability and profitability.

BWR believes that MFSL has the potential and required systems in place to achieve the projected

growth in its operational as well as financial performance.