75

Interest Rate Risk Modeling Interest Rate Risk Modeling The Fixed Income Valuation Course Sanjay K. Nawalkha Gloria M. Soto Natalia A. Beliaeva

Interest Rate Risk ModelingInterest Rate Risk ModelingThe Fixed Income Valuation Course

Sanjay K. Nawalkhaj yGloria M. SotoNatalia A. Beliaeva

• Interest Rate Risk Modeling : The Fixed Income V l ti C S j K N lkh Gl i M S tValuation Course. Sanjay K. Nawalkha, Gloria M. Soto, Natalia K. Beliaeva, 2005, Wiley Finance.

Chapter 6 : Hedging with Interest Rate Futures– Chapter 6 : Hedging with Interest-Rate Futures

G l• Goals:– Introduce the contractual details and pricing of the

interest rate futures contractsinterest rate futures contracts.– Show how to hedge and speculate against interest

rate movements using futures contractsrate movements using futures contracts.

2

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

3

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

4

Introduction

• Futures contracts traded primarily on physical p y p ycommodities such as precious metals, agriculture, wood products, and oil.

• It’s an agreement between two parties to trade an asset at some future date for a fixed price agreed upon today.

• Due to features such as standardization, marking to market, futures contracts are more liquid than forward contractscontracts.

5

Introduction

Table 6.1 Interest Rate Futures

Contract Denomination ($) Exchange Open Interest Dec. 10, 2003

U.S. T-Bills 1,000,000 CME 0

Eurodollars 1,000,000 CME 5,203,120

U.S. T-Bonds 100,000 CBOT 490,968

U S T-Notes 100 000 CBOT 986 595

• As we can see the in the Table 6.1, the explosive growth

U.S. T Notes 100,000 CBOT 986,595

, p gof the Eurodollar futures contract has come at the expense of the T-bill futures contract.

6

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

7

Eurodollar Futures

• A Eurodollar deposit is a deposit denominated in U.S. dollars in an American or foreign bank located outsidedollars in an American or foreign bank located outside the United States.

• The interest rate on the Eurodollar deposit is given as the London Interbank Offer Rate (LIBOR) which is thethe London Interbank Offer Rate (LIBOR), which is the ask rate at which large international banks lend U.S. dollars to each other.

• The three-month (90-day) Eurodollar futures contract is based on a hypothetical three-month Eurodollar CD with a face value of $1 million. They expire in the months of M h J S t b d D bMarch, June, September, and December.

8

Eurodollar Futures

• The Eurodollar futures contract is settled in cash.

• The three-month Eurodollar futures is the most liquid and actively traded futures contracts in the world, its success largely resulting from complimentary growth of the over-the counter LIBOR based derivatives products such asthe-counter LIBOR-based derivatives products, such as interest rate swaps, interest rate options, and forward rate agreements (FRAs).g ( )

• Traders often use Eurodollar futures to hedge against ade s o e use u odo a u u es o edge aga sthe exposure in interest rate swaps and other LIBOR-based products.

9

Eurodollar Futures

• Eurodollar Futures

– Futures Prices and Futures Interest Rates

– Hedging with Eurodollar Futures

10

Eurodollar Futures:Futures Prices and Futures Interest Rates

• Let Q be the quoted or the settlement price for a Eurodollar futures contract with an expiration date s.Th l ti hi b t th ttl t i d thThe relationship between the settlement price and the futures interest rate is given as follows:

where q is the 90 day LIBOR futures rate expressed in

q=100-Q (6.1)

where q is the 90-day LIBOR futures rate expressed in percentage with quarterly compounding and an actual/360 day-count convention.actual/360 day count convention.

11

Eurodollar Futures:Futures Prices and Futures Interest Rates

Th di t t b t f d i t• The discrete rate q can be transformed into a continuously compounded annualized rate that uses actual/365 day count convention as follows:actual/365 day count convention as follows:

+ ×+ =* ( , 90/365) (90/365)/ 41 e (6.2)

100f s sq

where f*(s,s+90/365) is the continuously compounded futures rate expressed in decimal form

100

futures rate expressed in decimal form.

• By taking logarithms of both sides we get:By taking logarithms of both sides, we get:

⎛ ⎞+ +⎜ ⎟⎝ ⎠

* 365( , 90 / 365) = ln 1 (6.3)90 400

qf s s

12

⎜ ⎟⎝ ⎠

( ) ( )90 400

Eurodollar Futures:Futures Prices and Futures Interest Rates

Th l ti hi b t th f t t d th• The relationship between the futures rates and the forward rates is dependent on the assumptions of a specific term structure model the followingspecific term structure model, the following approximation is based on Ho and Lee (1986):

1

where f(s s+t) is the annualized forward rate with

σ+ = + +* 21( , ) ( , ) - ( ) (6.4)2

f s s t f s s t s s t

where f(s,s+t) is the annualized forward rate with continuously compounding, t is the maturity of the underlying asset at the delivery date s, and σ is the annual standard deviation of the change in the short-term interest rate.

13

Eurodollar Futures:Futures Prices and Futures Interest Rates

Th f t i t t t i diff t f f d i t t• The futures interest rate is different from forward interest rate. The difference arises because futures contracts are marked-to-market every day which makes these contractsmarked-to-market every day, which makes these contracts more volatile than the corresponding forward contracts.

• The deviations of the Eurodollar futures rates from the forward rates in the U.S. Treasury markets should be due yto two reasons:– The convexity adjustment– The default risk

14

Eurodollar Futures:Futures Prices and Futures Interest Rates• Convexity Adjustment• Convexity Adjustment

The term is known as the convexity 21 ( )2

s s tσ +

adjustment.For short maturities convexity adjustment is close to

2

– For short maturities, convexity adjustment is close to zero, and the Eurodollar futures interest rate can be assumed to be the same as the corresponding p gforward interest rate.

– For long maturity Eurodollar futures, a convexity adjustment must be used for obtaining the implied forward rates.

15

Eurodollar Futures:Futures Prices and Futures Interest Rates

• Default RiskIf th d f lt i k i t d ith E d ll d it iIf the default risk associated with Eurodollar deposits in foreign countries is small then Eurodollar forward rates should be only slightly higher than the U S Treasuryshould be only slightly higher than the U.S. Treasury forward rate.

16

Eurodollar Futures:Futures Prices and Futures Interest Rates

• Example 6.1:futures rate, forward rate, contract priceConsider a five-year maturity Eurodollar futures contract with a quoted price of 96. The quarterly compounded annualized futures rate q, can be calculated as follows:

The continuously compounded annualized futures rate f*(5 5 90/365) i t d f ll

q=100-96=4 (6.1)

f*(5, 5+90/365) is computed as follows:

⎛ ⎞365 4⎛ ⎞+ +⎜ ⎟⎝ ⎠

* 365 4(5,5 90 / 365) = ln 1 (6.3)90 400

f

17

Eurodollar Futures:Futures Prices and Futures Interest Rates

The continuously compounded annualized forward rateThe continuously compounded annualized forward rate, using a standard deviation of 1.2%, is computed as follows (equation 6.4):f(5, 5+90/365)=f*(5, 5+90/365)-1/2*(1.2%)^2*5*(5+90/365)( ) ( ) ( )=0.04035-1/2*(1.2%)^2*5*(5+90/365)=3.846%We can see that the futures rate is higher than the forward rate, due to marking-to-market, futures contracts are riskier than forward contracts.

18

Eurodollar Futures:Futures Prices and Futures Interest Rates• An investor with a long position in the Eurodollar futuresAn investor with a long position in the Eurodollar futures

expects to gain (lose) when interest rates go down (up), while an investor with a short position is expecting vice versa.

• Calculate the gains or losses of futures contractThe contract price (CP) corresponding to the settlement price Q, is given as:

⎛ ⎞= = ⎜ ⎟⎝ ⎠

90Contract Price 10,000 100 - (100 - ) (6.5)360

CP Q

Thus the settlement price of 96 corresponds to as contract price of:

19

= 10,000[100 - 0.25(100 - 96)] =$990,000CP

Eurodollar Futures:Futures Prices and Futures Interest Rates

• Due to the linear relationship in equation 6.1, a change of one basis point in the settlement price Q, corresponds to a change of one basis point the quoted futures rate qto a change of one basis point the quoted futures rate q.

Th t t i h b $25 f b i• The contract price changes by $25 for every one basis point change in either the settlement price or the futures raterate.

20

Eurodollar Futures

• Eurodollar Futures

– Futures Prices and Futures Interest Rates

– Hedging with Eurodollar Futures

21

Eurodollar Futures:Hedging with Eurodollar Futures• Since the contract prices of Eurodollar futures are linear• Since the contract prices of Eurodollar futures are linear

in the quoted futures rates, Eurodollar futures are effective in hedging against the changes in interest rates,effective in hedging against the changes in interest rates, without introducing the nonlinear effects of convexity.

• Two assumptions:1. We use a linear approximation for the derivation of pp

the duration vector of Eurodollar futures.2. We assume that the difference between forward

rates and futures rates is time homogenous and stationary over time.

22

Eurodollar Futures:Hedging with Eurodollar Futures• The percentage change in the contract price of aThe percentage change in the contract price of a

Eurodollar futures can be linearly approximated using the duration vector model as follows:Δ

= × Δ × Δ × Δ + +0 1 2 - (1) - (2) - (3) ... (6.10)f f fCP D A D A D ACP

where, = ×(1) ( ) (90 / 365),fD K Q

= × +

= × +

2 2

3 3

(2) ( ) [( 90 / 365) - ], (3) ( ) [( 90 / 365) - ], (6.11)

f

f

D K Q s sD K Q s s

and K(Q) is defined as follows:⎛ ⎞ ⎛ ⎞− − −⎛ ⎞ ⎛ ⎞100 100 500( ) 1 / 1 (6 12)Q Q QK Q

23

⎛ ⎞ ⎛ ⎞⎛ ⎞ ⎛ ⎞= + − =⎜ ⎟ ⎜ ⎟⎜ ⎟ ⎜ ⎟ +⎝ ⎠ ⎝ ⎠⎝ ⎠ ⎝ ⎠

100 100 500( ) 1 / 1 (6.12)400 400 300

Q Q QK QQ

Eurodollar Futures:Hedging with Eurodollar Futures

• The expression K(Q) remains close to 1 for low levels of interest rates, but as interest rates become high, K(Q) , g , (Q)becomes significantly large than 1, leading to higher duration vector values.

• This implies that the percentage change in the contract price of a Eurodollar futures contract is higher for the same magnitude of rate change, when the initial rates are higherare higher.

24

Eurodollar Futures:Hedging with Eurodollar Futures• Example 6 2:duration vector• Example 6.2:duration vector

Assume that the settlement price quote of a Eurodollar futures contract with 100 days until maturity is 95. Thenfutures contract with 100 days until maturity is 95. Then Q=95 and s=100/360 or 0.2778 years.– The contract price:p

K(Q) and the duration vector:

⎛ ⎞= ⎜ ⎟⎝ ⎠

90 10,000 100 - (100 - 95) (6.5)360

CP

– K(Q) and the duration vector:−

=+

500 95( ) =1.025316 (6.12)300 95

K Q

= × =

= × + =2 2

(1) 1.025316 (90 / 365) 0.2528(2) 1.025316 [(0.2778 90 / 365) - 0.2778 ] 0.2028

f

f

DD

25

= × + =3 3

( ) [( ) ](3) 1.025316 [(0.2778 90 / 365) - 0.2778 ] 0.1259fD

Eurodollar Futures:Hedging with Eurodollar Futures

• Cross-hedging strategy: where Eurodollar futures can be added to a U.S. Treasury bond portfolio to eliminate interest rate risk arising from nonparallel changes.

• Consider the M duration vector elements of the bond portfolio given as follows:

= ⋅ + ⋅ + + ⋅ =( ) ( ) ( ) ( ) 12 (6 14)D m p D m p D m p D m m M= ⋅ + ⋅ + + ⋅ =K1 1 2 2( ) ( ) ( ) ( ), 1,2,..., . (6.14)PORT J JD m p D m p D m p D m m M

26

Eurodollar Futures:Hedging with Eurodollar Futures

Th ti f th ith E d ll f t t t ith• The proportion of the ith Eurodollar futures contract with respect to the total dollar investment in the bond portfolio as follows: fCPas follows:

=

∑ (6.16)

ff i i

i J

i i

n CPpn P

Where is the number of ith Eurodollar futures contracts, and the ith Eurodollar futures contract price is given as

=∑

1i

and the ith Eurodollar futures contract price is given as .

Transfer the formula a little bit we can get:Transfer the formula a little bit, we can get:

= ∑ (6.19)f J

f ii i i

pn n PCP

27

=∑

1iiCP

Eurodollar Futures:Hedging with Eurodollar Futures

Th M d i i b i• The M duration vector constraints can be given as follows:

+ + + + =

+ + + + =1 1 2 2

21 1 2 2

(1) (1) (1) ... (1)

(2) (2) (2) ... (2)

f f f f f fPORT M M

f f f f f fPORT M M

D p D p D p D H

D p D p D p D H

+ + + + =1 1 2 2

.( ) ( ) ( ) ... ( ) (6.17)f f f f f f M

PORT M MD M p D M p D M p D M H

Larger are the deviation of the duration vector values of the cash portfolio from the horizon vector values largerthe cash portfolio from the horizon vector values, larger will be the positions in the Eurodollar futures to immunize the portfoliothe portfolio

28

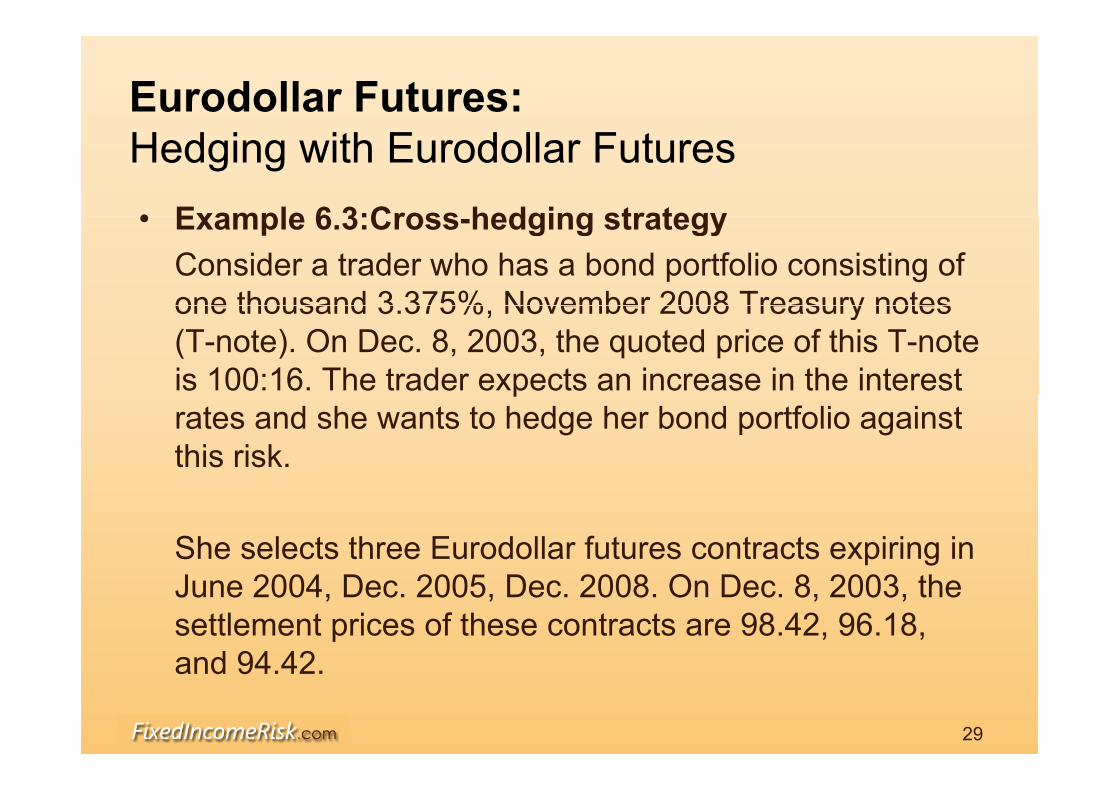

Eurodollar Futures:Hedging with Eurodollar Futures• Example 6 3:Cross hedging strategy• Example 6.3:Cross-hedging strategy

Consider a trader who has a bond portfolio consisting of one thousand 3 375% November 2008 Treasury notesone thousand 3.375%, November 2008 Treasury notes (T-note). On Dec. 8, 2003, the quoted price of this T-note is 100:16. The trader expects an increase in the interest prates and she wants to hedge her bond portfolio against this risk.

She selects three Eurodollar futures contracts expiring in J 2004 D 2005 D 2008 O D 8 2003 thJune 2004, Dec. 2005, Dec. 2008. On Dec. 8, 2003, the settlement prices of these contracts are 98.42, 96.18, and 94 42and 94.42.

29

Eurodollar Futures:Hedging with Eurodollar Futures

• The contract prices are given as follows:

1June 2004 contract: = 10,000[100 - 0.25(100-98.42)] = $996,050CP1

2

, [ ( )] ,

December 2005 contract: = 10,000[100 - 0.25(100-96.18)] = $990,450CP2

3December 2008 contract: = 10,000[100 - 0.25(100-94.42)] = $986CP ,050

30

Eurodollar Futures:Hedging with Eurodollar Futures• The delivery dates and times to maturity:y y

Table 6.2 Delivery Dates for Eurodollar Futures Futures Contract Delivery Date Maturity (in years)

/Jun-04 14-Jun-04 0.53 =189/360Dec-05 19-Dec-05 2.03 =2+211/360 Dec-08 15-Dec-08 5.02 =5+7/360

• The duration vector:

Table 6.3 Duration Vector Values of Eurodollar Futures and T-Note Futures Contract D(1) D(2) D(3) Price ($)Jun-04 0 2485 0 3222 0 3171 $996 050Jun-04 0.2485 0.3222 0.3171 $996,050 Dec-05 0.2513 1.0827 3.5016 $990,450 Dec-08 0.2536 2.6079 20.1215 $986,050

$

31

Treasury Note 4.5804 21.9946 107.0826 $1,007.144

Eurodollar Futures:Hedging with Eurodollar Futures

Use the equation 6 18 to solve the proportions in theUse the equation 6.18 to solve the proportions in the three Eurodollar futures contracts for an instantaneous horizon of zero, as follows:horizon of zero, as follows:

−⎡ ⎤ −⎡ ⎤⎡ ⎤1

1 0 4.58040 2485 0 2513 0 2536fp⎡ ⎤ ⎡ ⎤⎡ ⎤⎢ ⎥ ⎢ ⎥⎢ ⎥= × −⎢ ⎥ ⎢ ⎥⎢ ⎥⎢ ⎥ ⎢ ⎥⎢ ⎥ −⎣ ⎦ ⎣ ⎦⎣ ⎦

12

23

0 4.58040.2485 0.2513 0.25360.3247 1.0874 2.6133 0 21.99460.3220 3.5324 20.2041 0 107.0826

f

f

p

p

p ⎢ ⎥⎣ ⎦ ⎣ ⎦⎣ ⎦3 0 107.0826p

⎡ ⎤ ⎡ ⎤1 -3 7133fp⎡ ⎤ ⎡ ⎤⎢ ⎥ ⎢ ⎥=⎢ ⎥ ⎢ ⎥⎢ ⎥ ⎢ ⎥⎣ ⎦⎣ ⎦

1

2

3.7133-11.2497-3.2740

f

f

p

p

p

32

⎢ ⎥⎣ ⎦⎣ ⎦3p

Eurodollar Futures:Hedging with Eurodollar Futures

The number of futures contracts can be computed using equation 6.19 to hedge one thousand Treasury notes as follows:follows:

−× ×

3.7133 1000 1007 144 3 7547fn = × × =1 1000 1007.144 -3.7547996050

fn

-11.2497 1000 1007 144 11 4393f = × × =211.2497 1000 1007.144 -11.4393990450

fn

3 2740= × × =3

-3.2740 1000 1007.144 -3.3441986050

fn

33

Eurodollar Futures:Hedging with Eurodollar Futures

The quoted prices on this day along with the futuresThe quoted prices on this day, along with the futures contract prices, and changes in the contract price are given as follows:given as follows:

Table 6.4 Eurodollar Futures and Treasury note Quoted Prices on Dec. 9, 2003Futures Contract Quoted Price Dec. 9 Price Dec. 9 ($) Price Change ($)

Jun-04 98.38 995,950 -100Dec-05 96.09 990,225 -225Dec-08 94.31 985,775 -275

Treasury Note 100 02 1 002 86 -4 281Treasury Note 100.02 1,002.86 4.281

34

Eurodollar Futures:Hedging with Eurodollar Futures

– The loss on the portfolio of one thousand TreasuryThe loss on the portfolio of one thousand Treasury notes equals:(1,002.863-1,007.144)*1,000= -4.281*1,000= $4,281(1,002.863 1,007.144) 1,000 4.281 1,000 $4,281

– The gain on the futures positions equal to:(-3.7059)*(-100)+(-11.4578)*(-225)+(-3.3738)*(-275)( 3.7059) ( 100) ( 11.4578) ( 225) ( 3.3738) ( 275)= $3,876.41

The loss is offset by the gain, and the residual loss not captured by the immunization strategy is $405.36, which p y gy $ ,is less than 10% of the loss on the cash portfolio of T-notes.

35

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

36

Treasury Bill Futures

• The asset underlying a Treasury bill futures contract is• The asset underlying a Treasury bill futures contract is the 90-day U.S. Treasury bill worth $1 million in face value.value.

• They are traded on the CME, with contract’s expirationThey are traded on the CME, with contract s expiration months March, June, September, and December.

• They are settled via cash, rather than physical delivery.

37

Treasury Bill Futures

• Treasury Bill Futures

– Treasury Bill Pricing

– Futures Prices and Futures Interest Rates

38

Treasury Bill Futures: Treasury Bill Pricing

• The price of a T-bill is quoted with a discount assuming $100 face value and 360 days in a year as follows

= − ×100 (6.20)360

tP d

Where d is the quoted discount rate, and t is the number

360

of days until maturity of the T-bill.

39

Treasury Bill Futures: Treasury Bill Pricing

• Suppose the quoted ask discount rate equals 5.9325 on T bill t i i 91 d Th th ki i f tha T-bill maturing in 91 days. Then the asking price for the

T-bill is given as:

= − × =91100 5.9325 $98.50

360P

• If the face value of the T-bill is $1,000, the buyer of one T bill pays 98 50*10=$985 to the trader to purchase oneT-bill pays 98.50 10=$985 to the trader to purchase one T-bill.

• T-bills can be bought with face values ranging from $1,000 to $1,000,000.$1,000 to $1,000,000.

40

Treasury Bill Futures

• Treasury Bill Futures

– Treasury Bill Pricing

– Futures Prices and Futures Interest Rates

41

Treasury Bill Futures:Futures Prices and Futures Interest Rates• Let q define the quoted futures rate and Q define theLet q define the quoted futures rate and Q define the

quoted settlement price of a T-bill futures contract. Then we can get the equation given as follows:

q=100-Q (6.22)

• Since the 90-day T-bill underlying the T-bill futures contract is a discount instrument, the relationship between the quoted future rate and the continuously compounded futures rate is given:

+ ×

⎛ ⎞− = − =⎜ ⎟⎝ ⎠

* ( , 90/365) (90/365)

90 / 4 11 1 (6.23)360 4 100 ef s s

q q

42

⎝ ⎠ e

Treasury Bill Futures:Futures Prices and Futures Interest Rates

Th t t i f T bill f t i d fi d i th• The contract price of a T-bill future is defined in the same way as that of the Eurodollar futures. A one basis point change in the T-bill futures quoted rate corresponds to achange in the T-bill futures quoted rate corresponds to a $25 change in the futures contract prices.

• The duration vector of T-bill futures contracts is:The duration vector of T bill futures contracts is:Δ

= × Δ × Δ × Δ + +0 1 2 - (1) - (2) - (3) ... (6.24)f f fCP D A D A D ACP

where,

(1) 90 / 365fD =

= + 2 2

3 3

(1) 90 / 365,(2) ( 90 / 365) - , (3) ( 90 / 365) (6 25)

f

f

f

DD s sD

43

= + 3 3(3) ( 90 / 365) - (6.25)fD s s

Treasury Bill Futures:Futures Prices and Futures Interest Rates

• Hedging short-term U S Treasury securities with T-billHedging short term U.S. Treasury securities with T billfutures can be accomplished using the duration vector by the technique outlined in equations 6.14 through 6.19.

• However, using T-note futures and T-bond futures may g ybe essential when hedging long-term U.S. Treasury securities.

44

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

45

Treasury Bond Futures

T b d f h l l• Treasury bond futures are the most popular long-term interest rate futures. They are traded on the CBOT, and expire in the months of March June September andexpire in the months of March, June, September, and December.

• The underlying asset in a Treasury bond futures contract is any $100,000 face value government bond with more y $ , gthan 15 years to maturity on the first day of delivery month, and which is noncallable for 15 years from this day.

46

Treasury Bond Futures• The invoice price for the deliverable bond (not including

accrued interest) is the bond’s conversion factor timesaccrued interest) is the bond s conversion factor times the futures price.

Invoice price=FP×CF (6.26)Invoice price FP CF (6.26)where FP=Quoted futures price

CF=Conversion factorCF Conversion factor• T-bond futures price quoted do not include accrued

interest. Therefore, the delivery cash price is always , y p yhigher than the invoice price.

CP=Invoice price + Accrued interest=FP×CF+AI (6.27)

where AI is the accrued interest.

47

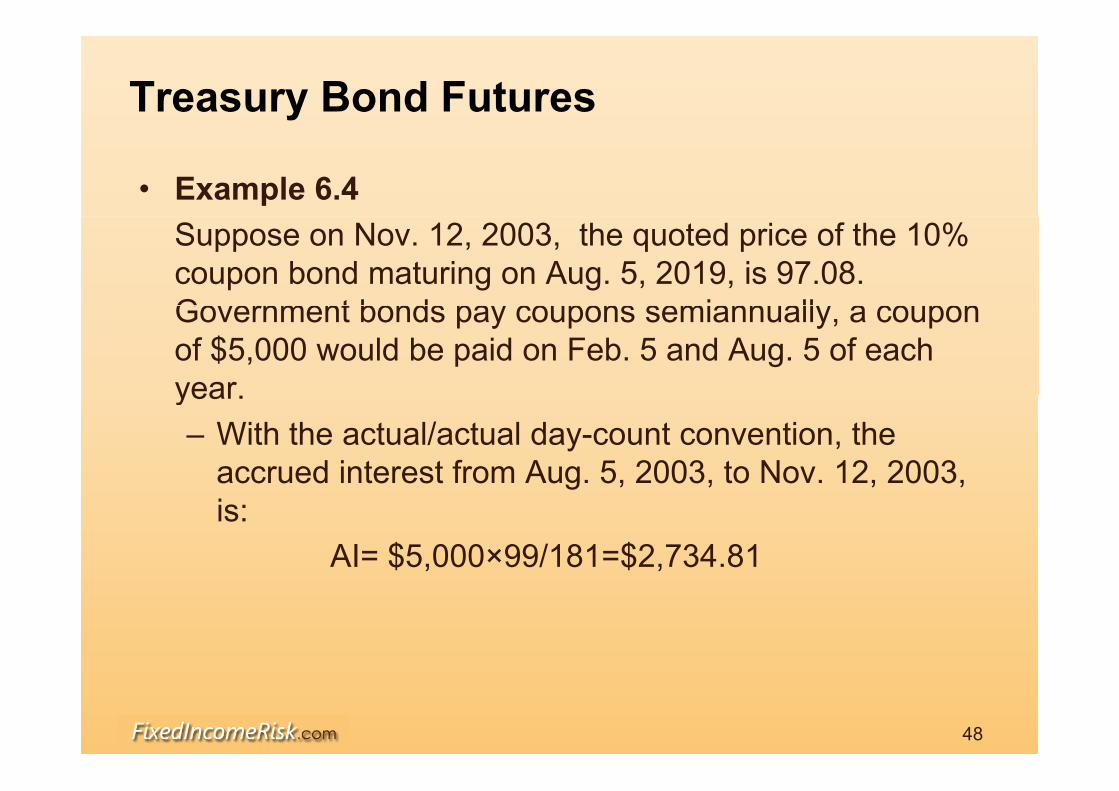

Treasury Bond Futures

• Example 6.4Suppose on Nov. 12, 2003, the quoted price of the 10% coupon bond maturing on Aug. 5, 2019, is 97.08. Government bonds pay coupons semiannually a couponGovernment bonds pay coupons semiannually, a coupon of $5,000 would be paid on Feb. 5 and Aug. 5 of each year.year. – With the actual/actual day-count convention, the

accrued interest from Aug. 5, 2003, to Nov. 12, 2003, g , , , ,is:

AI= $5,000×99/181=$2,734.81

48

Treasury Bond Futures

• Treasury Bond Futures

– Conversion Factor

Ch t t D li B d– Cheapest-to-Deliver Bond

– Options Embedded in T-Bond Futuresp

– Treasury Bond Futures Pricing

– Duration Vector of T-Bond Futures

49

Treasury Bond Futures:Conversion Factor

Th i f t i th f t th t t th• The conversion factor is the factor that converts the quoted futures price to and invoice price applicable for deliverydelivery.

• If the maturity of the bond is rounded down to zero• If the maturity of the bond is rounded down to zero month, yield 6%, then the conversion factor is:

⎡ ⎤1 1 1c

where c is the coupon rate and n is the number of years

⎡ ⎤= − +⎢ ⎥

⎣ ⎦0 2 2

1 1 1 (6.28)2 0.03 0.03(1.03) (1.03)n ncCF

where c is the coupon rate and n is the number of years to maturity.

50

Treasury Bond Futures:Conversion Factor• If the maturity of the bond is rounded down to threeIf the maturity of the bond is rounded down to three

months, then the conversion factor is:+0 2 (6 29)

cCF cCF

• If the maturity of the bond is rounded down to six months,

= −3 12

2 (6.29)4(1.03)

cCF

If the maturity of the bond is rounded down to six months, then the conversion factor is:

⎡ ⎤1 1 1 (6 30)cCF

• If the maturity of the bond is rounded down to nine

+ +

⎡ ⎤= − +⎢ ⎥

⎣ ⎦6 2 1 2 1 (6.30)

2 0.03 0.03(1.03) (1.03)n ncCF

ymonths, then the conversion factor is:

+6 2 (6 31)

cCF cCF

51

= −9 12

2 (6.31)4(1.03)

cCF

Treasury Bond Futures:Conversion Factor• Example 6 5• Example 6.5

Consider a futures contract expiring of Dec. with the underlying deliverable bond given in Example 6 4underlying deliverable bond given in Example 6.4. Assume that the bond is delivered on the first day of the expiration month, Dec. 1, 2003.p– On this day, the bond has 15 years 8 months and 5

days to maturity. (Dec. 1, 2003 ~ Aug. 5, 2019)– Rounding it down, the maturity is 15 years and 6

months. We treat this as 31 six-month periods. Th f th i f t iTherefore the conversion factor is :

⎡ ⎤= − +⎢ ⎥0 31 31

0.10 1 1 1 = 1.4CF

52

+⎢ ⎥⎣ ⎦

0 31 31 1.42 0.03 0.03(1.03) (1.03)

CF

Treasury Bond Futures:Conversion Factor

Suppose the quoted futures price on this bond is 96.04. The time elapsed since the previous coupon payment p p p p ydate, Aug. 5, 2003 ~ Dec. 1, 2003, equals 118 days.

– The accrued interest is:$5,000×118/181=$3,259.67

– The delivery cash price is:CP= $96,125×1.4+$3,259.67=$137,835.49

53

Treasury Bond Futures

• Treasury Bond Futures

– Conversion Factor

Ch t t D li B d– Cheapest-to-Deliver Bond

– Options Embedded in T-Bond Futuresp

– Treasury Bond Futures Pricing

– Duration Vector of T-Bond Futures

54

Treasury Bond Futures:Cheapest-to-Deliver Bond• For the party with the short position in the T-bond futuresFor the party with the short position in the T bond futures

contract can choose to deliver the cheapest-to-deliver bond.

• The cheapest-to-deliver bond is the bond for which the pcost of delivery is the lowest, where the cost of delivery is defined as:

– Cost of delivery= Quoted bond price-Quoted futures price ×

Conversion factor

55

Treasury Bond Futures:Cheapest-to-Deliver Bond• Example 6 6• Example 6.6

Assume that the T-bond quoted futures price on the delivery day is 97 09 and that the party with the shortdelivery day is 97.09, and that the party with the short position in the contract can choose to deliver from the bonds given in Table 6.5.g

Table 6.5 Deliverable Bonds for the T-Bond Futures Contract B d C (%) Q t d B d P i P C ti F tBond Coupon(%) Quoted Bond Price P Convention Factor

1 7.5 98-23 1.01382 6 97-16 1 00002 6 97 16 1.00003 8 99-12 1.02044 6.25 97-30 1.0049

56

Treasury Bond Futures:Cheapest-to-Deliver Bond• The cost of delivering each of these bonds is given in• The cost of delivering each of these bonds is given in

Table 6.6. Using the equation 6.33, the cheapest-to-deliver bond is bond 1.deliver bond is bond 1.

Table 6 6 Cost of DeliveryTable 6.6 Cost of Delivery

Bond Quoted Bond Price

(P)

Quoted Futures Price

(FP)

Convention Factor

(CF)

Cost of Delivery

(P-FP*CF)

1 98.72 97.28 1.0138 0.1

2 97.5 97.28 1.0000 0.22

3 99 38 97 28 1 0204 0 113 99.38 97.28 1.0204 0.11

4 97.94 97.28 1.0049 0.18

57

Treasury Bond Futures

• Treasury Bond Futures

– Conversion Factor

Ch t t D li B d– Cheapest-to-Deliver Bond

– Options Embedded in T-Bond Futuresp

– Treasury Bond Futures Pricing

– Duration Vector of T-Bond Futures

58

Treasury Bond Futures:Options Embedded in T-Bond Futures

• Cheapest-to-deliver option• Wild card play option• Wild card play option

Take advantage of the difference between the T-b d f t t di ti d T b d t dibond futures trading time and T-bond trading time.

59

Treasury Bond Futures

• Treasury Bond Futures

– Conversion Factor

Ch t t D li B d– Cheapest-to-Deliver Bond

– Options Embedded in T-Bond Futuresp

– Treasury Bond Futures Pricing

– Duration Vector of T-Bond Futures

60

Treasury Bond Futures:Treasury Bond Futures Pricing• Assumptions:p

– Both the deliverable bond and delivery date are known

– The wild card play option is not significant• Treasury bond futures price can be approximated by y p pp y

its forward price is given as:×= − ( )( ) (6 34)s y sFP P I e

where P is the current price of the deliverable T-bond,

= −( ) (6.34)FP P I e

I is the present value of the coupons during the life of the futures contract, s is the expiration date of the futures contract and (t) is the ero co pon ield for the term tcontract, and y(t) is the zero-coupon yield for the term t.

61

Treasury Bond Futures:Treasury Bond Futures Pricing

0 s+ τ 0 5n s+τ 0 5(n 1) s+τ 0 5(n 2) s+τ 0 5 s s+τ T0 s+ τ -0.5n s+τ-0.5(n-1) s+τ-0.5(n-2) s+τ-0.5 s s+τ T

C C C …… C C C+F

Current time Futures’ expiration

• In the following analysis, we assume that the delivery date is the first day of the expiration month of the futures contract.Th ti li i h i Fi 6 1 Th i f• The timeline is shown in Figure 6.1. The price of a futures contract depends only on cash flows received after the T-bond is delivered

62

after the T bond is delivered.

Treasury Bond Futures:Treasury Bond Futures Pricing• The delivery cash price of the futures contract is given as:The delivery cash price of the futures contract is given as:

( ) ( )

( )2 ( ) ( )

( )0 5 0 5 (6.35)T s s y s s y s

T Tt t

Ce FeCPτ− − × ×

+ + + +

⎡ ⎤= +⎢ ⎥∑

• Using equation 6 27 the quoted price of the futures

( ) ( ) ( )0.5 0.50

( )T y Ts t y s tt ee τ τ ×+ + × × + + ×=

⎢ ⎥⎣ ⎦∑

• Using equation 6.27, the quoted price of the futures contract is given as:

FP=1/CF(CP-AI) (6 36)FP 1/CF(CP AI) (6.36)• Substituting equation 6.35 and the 6.36, we get,

( ) ( )

( )2 ( ) ( )

( )0.5 0.50

1 0.5 (6.37)0.5

T s s y s s y s

T y Ts t y s tt

Ce Fe CFPCF e CFe

τ

τ τ

τ− − × ×

×+ + × × + + ×=

⎡ ⎤ −⎛ ⎞= + − ×⎢ ⎥ ⎜ ⎟⎝ ⎠⎣ ⎦

∑

63

⎣ ⎦

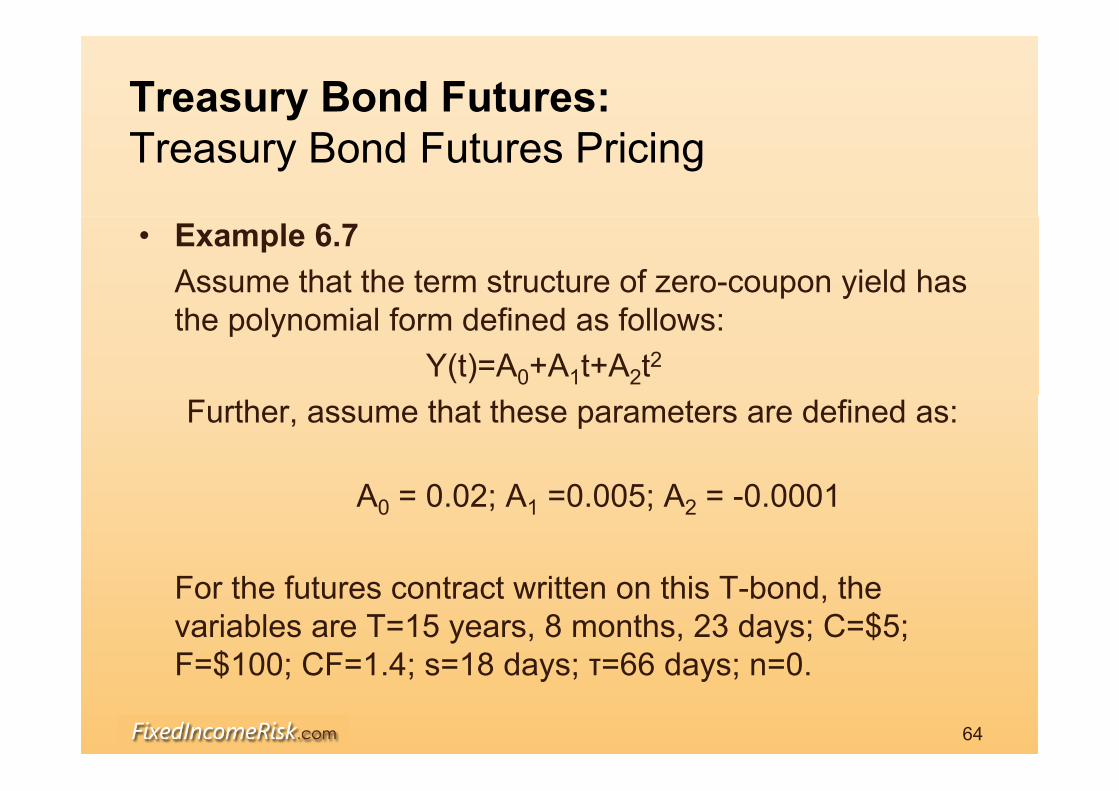

Treasury Bond Futures:Treasury Bond Futures Pricing

• Example 6.7Assume that the term structure of zero-coupon yield has the polynomial form defined as follows:

Y(t)=A0+A1t+A2t2

Further, assume that these parameters are defined as:

A 0 02 A 0 005 A 0 0001A0 = 0.02; A1 =0.005; A2 = -0.0001

For the futures contract written on this T-bond, the variables are T=15 years, 8 months, 23 days; C=$5; F=$100; CF=1 4; s=18 days; τ=66 days; n=0F=$100; CF=1.4; s=18 days; τ=66 days; n=0.

64

Treasury Bond Futures:Treasury Bond Futures Pricing

Th t d f t i i i• The quoted futures price is given as:× ⎡ ⎤ −

+ ×⎢ ⎥∑0.05 (0.05) 31 5 100 5 0.5 0.18 (6 38)

yeFP ( ) ( ) ×+ × × + ×=

= + − ×⎢ ⎥⎣ ⎦∑ 15.73 (15.73)0.23 0.5 0.23 0.5

0 (6.38)

1.4 1.4 0.5yt y tt

FPee

y(t) 0.02+0.005t-0.0001t2 (6.39)

Substituting the zero-coupon yield from Table 6.7 into equation 6.38, the quoted price of the futures contract based on a $100 face value is equal to $95.10. The cash price is derived from the quoted futures price using equation 6 36 and is equal to $136 33equation 6.36 and is equal to $136.33.

65

Treasury Bond Futures

• Treasury Bond Futures

– Conversion Factor

Ch t t D li B d– Cheapest-to-Deliver Bond

– Options Embedded in T-Bond Futuresp

– Treasury Bond Futures Pricing

– Duration Vector of T-Bond Futures

66

Treasury Bond Futures:

Th t h i th T b d f t t d

Duration Vector of T-Bond Futures

• The percentage change in the T-bond futures quoted price is given as follows:

h

−

Δ= − Δ − Δ − Δ − − Δ0 1 2 1(1) (2) (3) ... ( ) (6.40)M

CP D A D A D A D M ACP

where,( )( )

( ) ( )

( )τ τ− −× ⎡ ⎤+ + × − −⎢ ⎥= +⎢ ⎥∑

2( ) 0.5 ( )( ) (6 41)m mT ss y s m mC s t se F T sD m

U lik T bill f t T b d f t b d f

( ) ( )τ τ ×+ + × × + + ×=

+⎢ ⎥⎢ ⎥⎣ ⎦∑ ( )0.5 0.5

0( ) (6.41)T y Ts t y s t

tD m

CP ee

Unlike T-bill futures, T-bond futures can be used for hedging long-term bond portfolios, since the deliverable bonds underlying the T-bond futures have longerbonds underlying the T-bond futures have longer maturities.

67

Treasury Bond Futures:Duration Vector of T-Bond Futures• Example 6 8• Example 6.8

0 0.05 0.23 0.23+0.5 0.23+0.5 × 2 15.73

C C …… C C+F

Current time Futures’ expiration

– The term structure parameters change instantaneously is shown in Table 6 8is shown in Table 6.8.

– The original and the new zero-coupon yields based on the parameter in Table 6 8 are given in Table 6 9the parameter in Table 6.8 are given in Table 6.9.

68

Treasury Bond Futures:Duration Vector of T-Bond Futures

Table 6.8 Changes in the Term Structure Parameters Original Parameters Change New Parametersg g

A0 0.02 0.005 0.025A1 0.005 -0.0001 0.0049A2 -0.0001 0 -0.0001

Substituting the new zero-coupon yields into equation 6 35 the new quoted price of the futures contract equals6.35, the new quoted price of the futures contract equals $92.02, which is a decline of 3.24% from the original price of $95.10.p

69

Treasury Bond Futures:Duration Vector of T-Bond Futures• This change is approximated by the first three elements• This change is approximated by the first three elements

of the duration vector model. The duration vector elements are given as:elements are given as:

( )( )( ) ( )

( )τ

τ τ

τ− −×

×+ + × × + + ×

⎡ ⎤+ + × − −⎢ ⎥= +⎢ ⎥∑

2( )

( )0 5 0 5

0.5 ( )( ) (6.41)m mT ss y s m m

T y Ts t y s t

C s t se F T sD mCP e

Using the zero-coupon yields in Table 6 9 we obtain the

( ) ( )τ τ ×+ + × × + + ×=⎢ ⎥

⎢ ⎥⎣ ⎦∑ ( )0.5 0.5

0T y Ts t y s t

tCP ee

Using the zero coupon yields in Table 6.9, we obtain the duration vector as follows:

D(1)=8.73; D(2)=105.97; D(3)=1442.99

70

Treasury Bond Futures:Duration Vector of T-Bond Futures

• Since the actual percentage change is -3 24% duration• Since the actual percentage change is -3.24%, duration overestimates the magnitude of the change.– Using only the durationUsing only the duration

Δ= − Δ = − × = −0

F (1) 8.73 0.005 0.0437F

P D AP

Immunization risk error: -4.37%-(-3.24%)= -1.13%– Using a three-element duration vector model

FP

– Using a three-element duration vector modelΔ

= − Δ − Δ − Δ0 1 2F (1) (2) (3)

FP D A D A D A

P

Immunization risk error: 3 31% ( 3 24%)= 0 07%

= − × − × − = −F

8.73 0.005 105.97 ( 0.0001) 0.0331P

Immunization risk error: -3.31%-(-3.24%)=-0.07%

71

Chapter 6 : Hedging with Interest-Rate Futures

• Introduction

• Eurodollar Futures

• Treasury Bill Futures

• Treasury Bond FuturesTreasury Bond Futures

• Treasury Note Futures

72

Treasury Note Futures

• Three kinds of Treasury note futures are transacted on ythe CBOT given as two-year, five-year, and 10-year T-note futures.

• The two-year T-note futures is not as actively traded as the five-year and the 10-year T-note futures, because both T-bill futures and short-term Eurodollar futures are close competitors of the two year T note futuresclose competitors of the two-year T-note futures.

• The asset underlying the 10 year T note futures contract• The asset underlying the 10-year T-note futures contract is any $100,000 face value T-note. Delivery months are March, June, September, and December.March, June, September, and December.

73

Treasury Note Futures

• The only difference between T-note futures and T-bond futures is the range of maturities of the deliverable bondsfutures is the range of maturities of the deliverable bonds. Hence, all results derived for pricing and hedging using the T-bond futures hold for T-note futures by consideringthe T bond futures hold for T note futures by considering the appropriate range of maturities of deliverable bonds applicable to the specific T-note futures.

74

Interest Rate Risk ModelingInterest Rate Risk ModelingThe Fixed Income Valuation Course

Sanjay K. Nawalkhaj yGloria M. SotoNatalia A. Beliaeva