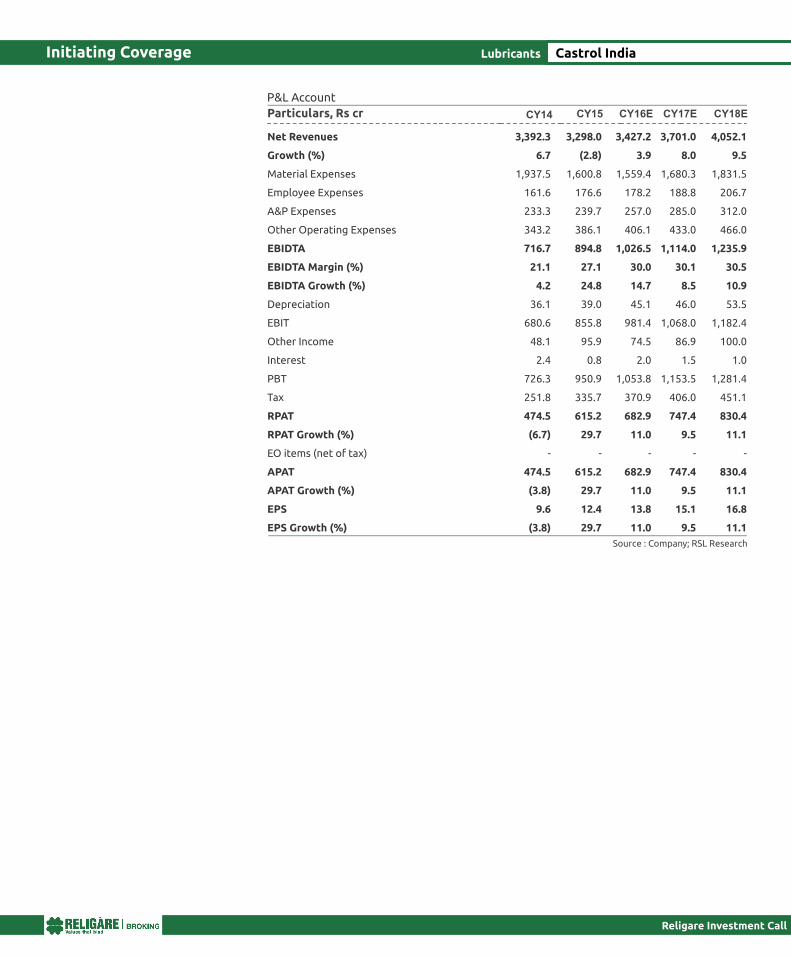

Castrol India Religare Investment Call November 18, 2016 Incorporated in 1979, Castrol India Ltd (CIL) is one of the leading automotive and industrial lubricant manufacturing and marketing companies in India. CIL is a public limited company with 51% stake held by Castrol Ltd, UK, a 100% subsidiary of global petroleum major British Petroleum group. With 3 manufacturing plants, 420+ distributors and over 1.05 lacs retail outlets, CIL derives ~88% of its sales volumes from the Automotive segment and commands leadership in the urban retail automotive lubricant segment with market share of 22.4%. After a subdued performance over the last few years, the Indian lubricant industry is set to witness a turnaround on the back of an anticipated revival in the Autos and GDP/IIP cycle. Auto sector is likely to witness a healthy growth, led by falling interest rates, cooling inflation and revival in the Capex cycle. Some signs of recovery are already visible over the last few quarters, especially in the personal mobility space, which has improved the lubricant consumption. With leadership, strong brand recall, vast reach, innovating offerings and parental support, CIL is well placed to capitalize on the available opportunities. After five straight years of de-growth, CIL has delivered a healthy volume growth of 5% in 9MCY16. Demand uptick for lubricants, new launches, increasing presence in fast growing personal mobility space and sustained investments in A&P should help CIL report a decent 6.6% volume growth over CY15-18E. With rising share of power brands and premium synthetic products, net realisations should improve gradually. CIL has a strong tie up with established OEMs like Maruti Suzuki, Volkswagen group, Tata Motors, Ford, JCB, Bosch, John Deere, GM, Federal Mogul, Komatsu, JSW Steel, Skoda, Audi etc. Going forward, we expect CIL to continue strengthening its partnership with existing OEMs and enter into new partnerships as well, which should strengthen its brand positioning. While we expect the raw material benefits to wane out from Q4CY16 / Q1CY17 on the back of likely stability in the base oil prices and unfavourable base (base oil prices have fallen by ~37%% over the last two years), we expect structural levers like improved mix and operating leverage to drive the margins over the longer term. CIL's revenues are likely to grow by 7.1% CAGR over CY15-18E (largely volume led), led by demand revival in the Auto industry and improved GDP / IIP growth. Improved mix and operating leverage should result in EBIDTA margin gains of 337bps (at 30.5%) over CY15- 18E. At CMP of Rs 401, CIL is trading at 23.9x CY18E EPS. Bright prospects, cash rich and debt-free status, superior return ratios and high and consistent dividend payouts (average payouts over CY11-15 stood at 76%) justify the premium valuations, which should sustain. Valuing at 30x CY18E EPS, we recommend a BUY on the stock with a target price of Rs 504. Financial Summary Lubricants CMP (Rs) Target Price (Rs) Potential Upside Sensex Nifty Key Stock data BSE Code NSE Code Bloomberg Shares o/s, Cr (FV 5) Market Cap (Rs Cr) 3M Avg Volume 52 week H/L Shareholding Pattern (%) Promoter FII DII Others 1 Year price performance 401 504 26% 26,228 8,080 500870 CASTROLIND CSTRL IN 49.5 19,834 17,35,772 495 / 361 Mar-16 71.0 5.9 7.9 15.2 Jun-16 59.5 9.7 13.4 17.4 Sep-16 51.0 12.3 17.5 19.2 Analyst Mehernosh K. Panthaki [email protected]+91 - 22 - 67288053 Investment rationale: Initiating Coverage Outlook and valuation: Particulars, Rs cr CY14 CY15 CY16E CY17E CY18E Source : Company; RSL Research Net Revenues EBIDTA EBIDTA margin (%) APAT APATM (%) EPS (Rs) RoCE (%) RoE (%) 3,392.3 716.7 21.1 474.5 14.0 9.6 109.1 76.0 3,298.0 894.8 27.1 615.2 18.7 12.4 159.6 114.7 3,427.2 1,026.5 30.0 682.9 19.9 13.8 162.1 112.8 3,701.0 1,114.0 30.1 747.4 20.2 15.1 160.0 111.9 4,052.1 1,235.9 30.5 830.4 20.5 16.8 162.1 113.8 60 70 80 90 100 110 120 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Castrol Niy

Transcript

Castrol India

Religare Investment Call

November 18, 2016

Incorporated in 1979, Castrol India Ltd (CIL) is one of the leading automotive and industrial lubricant manufacturing and marketing companies in India. CIL is a public limited company with 51% stake held by Castrol Ltd, UK, a 100% subsidiary of global petroleum major British Petroleum group. With 3 manufacturing plants, 420+ distributors and over 1.05 lacs retail outlets, CIL derives ~88% of its sales volumes from the Automotive segment and commands leadership in the urban retail automotive lubricant segment with market share of 22.4%.

After a subdued performance over the last few years, the Indian lubricant industry is set to witness a turnaround on the back of an anticipated revival in the Autos and GDP/IIP cycle. Auto sector is likely to witness a healthy growth, led by falling interest rates, cooling inflation and revival in the Capex cycle. Some signs of recovery are already visible over the last few quarters, especially in the personal mobility space, which has improved the lubricant consumption. With leadership, strong brand recall, vast reach, innovating offerings and parental support, CIL is well placed to capitalize on the available opportunities.

After five straight years of de-growth, CIL has delivered a healthy volume growth of 5% in 9MCY16. Demand uptick for lubricants, new launches, increasing presence in fast growing personal mobility space and sustained investments in A&P should help CIL report a decent 6.6% volume growth over CY15-18E. With rising share of power brands and premium synthetic products, net realisations should improve gradually.

CIL has a strong tie up with established OEMs like Maruti Suzuki, Volkswagen group, Tata Motors, Ford, JCB, Bosch, John Deere, GM, Federal Mogul, Komatsu, JSW Steel, Skoda, Audi etc. Going forward, we expect CIL to continue strengthening its partnership with existing OEMs and enter into new partnerships as well, which should strengthen its brand positioning.

While we expect the raw material benefits to wane out from Q4CY16 / Q1CY17 on the back of likely stability in the base oil prices and unfavourable base (base oil prices have fallen by ~37%% over the last two years), we expect structural levers like improved mix and operating leverage to drive the margins over the longer term.

CIL's revenues are likely to grow by 7.1% CAGR over CY15-18E (largely volume led), led by demand revival in the Auto industry and improved GDP / IIP growth. Improved mix and operating leverage should result in EBIDTA margin gains of 337bps (at 30.5%) over CY15-18E. At CMP of Rs 401, CIL is trading at 23.9x CY18E EPS. Bright prospects, cash rich and debt-free status, superior return ratios and high and consistent dividend payouts (average payouts over CY11-15 stood at 76%) justify the premium valuations, which should sustain. Valuing at 30x CY18E EPS, we recommend a BUY on the stock with a target price of Rs 504.

Uptick in Autos and GDP / IIP cycle to boost the Indian Lubricant Industry volumes

Industry structure

India is the third largest Lubricant market in the world (in volume terms) after US and China with an annual consumption of ~230cr litres (~5.5% of the global consumption). Excluding process oil, the market is currently estimated at ~160cr litres per annum (LPA). Automobile lubricants account for ~60% (CVs: ~60%; Personal Mobility: ~40%) with engine oil being the largest category (nearly 2/3 of the volumes with balance accounted by grease oil, greases and transmission fluid). The industrial segment (B2B), which includes core industrial sectors such as infra, mining, marine, energy, etc. contributes the balance 40%.

Within the automotive segment, the replacement market is about 90%, while OEM factory-fill channel accounts for 10% (a low margin channel, but gaining traction as it helps the lube players to strengthen their marketing presence in the Retail segment). The replacement market is dominated by bazaar / retail trade (~82%; a profitable channel), which includes distribution channels such as spare-part shops (accounting for higher proportion of lubricant consumption ~50%), mechanic workshops, dedicated lubricant dealers and OEM authorised service centres (gaining traction over the last few years). The balance is contributed by fuel stations (run by PSU refiners; no private sector brands are in this segment) and franchise workshops. The overall Lubricant Industry is 82% organised with presence of over 30 established players.

Industry Structure Chart

Religare Investment Call

Initiating Coverage

Investment rationale

Castrol India Lubricants

India is the third largest Lubricant market in the world after US and China with annual consumption of ~230cr litres

Within the automotive segment, the replacement market is about 90%, which is dominated by Bazaar / Retail segment

India Lubricants Market Structure

Indian Lubricants Market (~230 Cr Ltr)

Automotive + Industrial

(~160 Cr Ltr)

Process Oils

(~70 Cr Ltr)

Automotive Lubes

(~95 Cr Ltr)Industrial Lubes (B2B)

(~65 Cr Ltr)

OEM Factory-fill(~10 Cr Ltr)

Replacement Demand(~85 Cr Ltr)

Bazaar(~70 Cr Ltr)

Fuel Stn(~5 Cr Ltr)

Franchise Workshops(~10 Cr Ltr)

Source : Industry; RSL Research

Industry volumes to improve with revival in the Auto / GDP growth

Growth in lubricant volumes is directly co-related to growth in auto volumes and IIP. The Indian lubricant market underperformed over FY12-15, impacted by showdown in the GDP, automotive, infrastructure and industrial segments. In automobiles, the Commercial Vehicle (CV) segment was the worst performer, wherein the MHCV sales declined by 12.6% and LCV by 6% over FY12-15. Lower goods movement because of subdued economy, closure in mining and slowdown in infrastructure resulted in a large number of vehicles remaining idle. Higher ownership cost impacted the Passenger Vehicles (PV) sales, which fell by 0.2% over FY12-15. While Two Wheeler (TW) sales grew by 6%, it was much slower than 21% over FY09-12. This was led by high inflation and interest cost and slowdown in rural growth. While the growth in FY16 was relatively better with PV and CV sales growth improving to 7.2% & 11.5% respectively, the TW sales growth remained subdued at 3%. Besides the slowdown in the auto industry, the shift in trend within the lubricant industry towards higher value, technologically advanced energy and fuel-efficient low-viscosity oils (long drain interval products) have further slowed down the consumption.

However, we feel that the worst is behind us and the lubricant industry is set to witness a turnaround over the next two to three years on the back of an anticipated revival in the autos and GDP/IIP cycle. We expect the Auto sector to witness a healthy growth, led by an expected decline in interest rates, cooling inflation, revival in the Capex cycle, and resuming of mining activities. Some signs of revival are already visible over the last few quarters. In H1FY17, the TW sales have grown by 17.5%, while PV sales volumes have also witnessed a healthy revival, up 12.3%. While the growth in the CV space was slower at 6%, we expect the same to revive in the coming quarters with the revival in the CAPEX cycle, road development and mining activities. With increasing rural incomes and better sources of finance, we expect a healthy offtake in the TW sales in the rural markets. The scooter oils sub-category has been doing well recently, and we expect this healthy growth momentum to continue due to surge in demand for gearless scooters. Over FY16-26, the domestic PV sales is expected to grow by 12.9% CAGR, while CV and TW segments are estimated to grow by 11.1% & 11.9% respectively. (Source: SIAM, NEMMP, TechSci Research).

In line with the recovery in the Auto sales, the lubes sales have witnessed an improvement over the last two to three quarters, as evident from healthy volume growth reported by companies like CIL (5% in 9MCY16) and Gulf Oil Lubricants. While the demand for automotive lubricants may not keep pace with vehicle sales growth (due to increasing demand for high end / long drain interval lubricant products), we still expect it to be better than the previous years (in mid-single digits compared to negative growth over FY12-15 and marginally positive growth in FY16). The demand for non-automotive lubricants could revive with Government's push and GST implementation. Low per capita consumption of lubricants in India (which is ~1.2kg, compared to ~5.3kg globally) offers strong growth potential.

CIL is well placed to leverage its strength and exploit the available opportunities

Leadership in the Lubricants space

At the forefront of pioneering technology, CIL is one of the leading automotive and industrial lubricant manufacturing and marketing companies in India, providing high performance range of products and services across automotive, industrial and marine & energy segments. It derives ~88% of its sales volumes from the Automotive segment with personal mobility space accounting for ~40% (Two Wheelers: 75% and Passenger Vehicles: 25%) and CV segment contributing ~48%. Industrial segment (including marine and energy) contributes the balance 12%. With a market share of 22.4%, CIL is a market leader in the urban retail (bazaar) automotive lubricant segment (market share in PVs is ~30% and in CVs is ~20%), providing iconic, high performance power brands like Castrol Edge (synthetic), Castrol Magnatec (semi synthetic) and Castrol GTX for passenger cars; Castrol Power1, Castrol Activ and Castrol Go for motorcycles / scooters and Castrol CRB, Castrol RX and Castrol Vecton for CVs, amongst various others including specialty products.

Religare Investment Call

Initiating Coverage

Growth in Lubricant volume is directly co-related to growth in the Auto volumes and GDP / IIP growth

Lubricant consumption is likely to improve over the next two to three years

Low per capita consumption of lubricants in India offers strong growth potential

CIL is a market leader in urban retail a u to m o t i ve l u b r i c a n t s e g m e n t , commanding a market share of 22.4%

Castrol India Lubricants

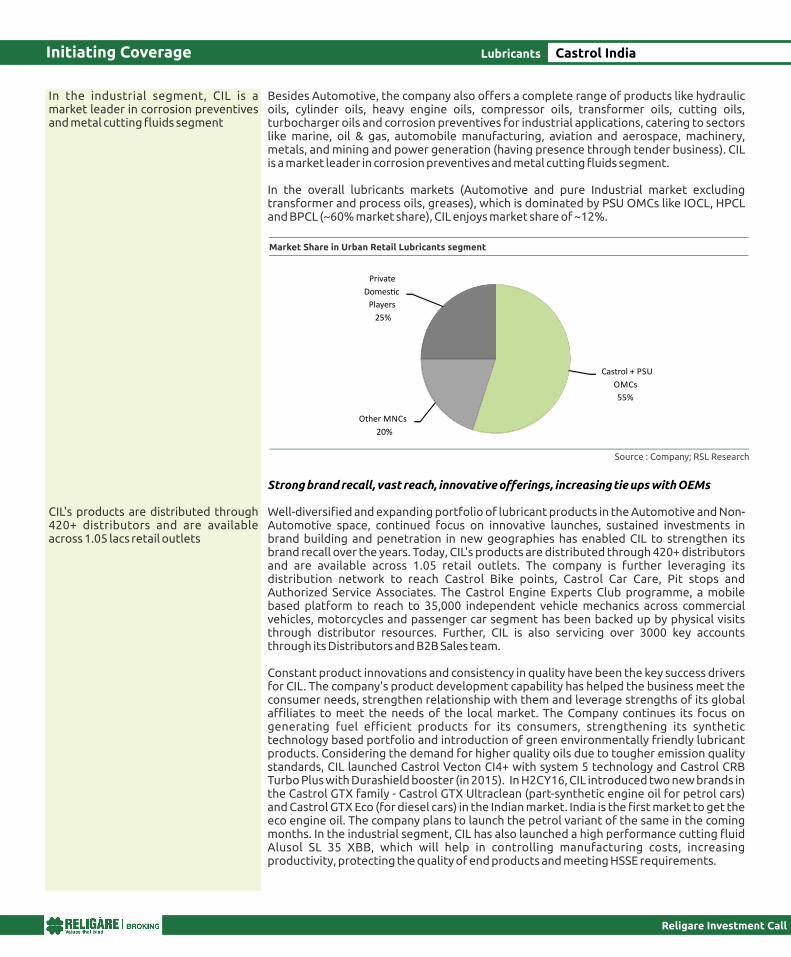

Besides Automotive, the company also offers a complete range of products like hydraulic oils, cylinder oils, heavy engine oils, compressor oils, transformer oils, cutting oils, turbocharger oils and corrosion preventives for industrial applications, catering to sectors like marine, oil & gas, automobile manufacturing, aviation and aerospace, machinery, metals, and mining and power generation (having presence through tender business). CIL is a market leader in corrosion preventives and metal cutting fluids segment.

In the overall lubricants markets (Automotive and pure Industrial market excluding transformer and process oils, greases), which is dominated by PSU OMCs like IOCL, HPCL and BPCL (~60% market share), CIL enjoys market share of ~12%.

Strong brand recall, vast reach, innovative offerings, increasing tie ups with OEMs

Well-diversified and expanding portfolio of lubricant products in the Automotive and Non-Automotive space, continued focus on innovative launches, sustained investments in brand building and penetration in new geographies has enabled CIL to strengthen its brand recall over the years. Today, CIL's products are distributed through 420+ distributors and are available across 1.05 retail outlets. The company is further leveraging its distribution network to reach Castrol Bike points, Castrol Car Care, Pit stops and Authorized Service Associates. The Castrol Engine Experts Club programme, a mobile based platform to reach to 35,000 independent vehicle mechanics across commercial vehicles, motorcycles and passenger car segment has been backed up by physical visits through distributor resources. Further, CIL is also servicing over 3000 key accounts through its Distributors and B2B Sales team.

Constant product innovations and consistency in quality have been the key success drivers for CIL. The company's product development capability has helped the business meet the consumer needs, strengthen relationship with them and leverage strengths of its global affiliates to meet the needs of the local market. The Company continues its focus on generating fuel efficient products for its consumers, strengthening its synthetic technology based portfolio and introduction of green environmentally friendly lubricant products. Considering the demand for higher quality oils due to tougher emission quality standards, CIL launched Castrol Vecton CI4+ with system 5 technology and Castrol CRB Turbo Plus with Durashield booster (in 2015). In H2CY16, CIL introduced two new brands in the Castrol GTX family - Castrol GTX Ultraclean (part-synthetic engine oil for petrol cars) and Castrol GTX Eco (for diesel cars) in the Indian market. India is the first market to get the eco engine oil. The company plans to launch the petrol variant of the same in the coming months. In the industrial segment, CIL has also launched a high performance cutting fluid Alusol SL 35 XBB, which will help in controlling manufacturing costs, increasing productivity, protecting the quality of end products and meeting HSSE requirements.

Religare Investment Call

Initiating Coverage

In the industrial segment, CIL is a market leader in corrosion preventives and metal cutting fluids segment

CIL's products are distributed through 420+ distributors and are available across 1.05 lacs retail outlets

Castrol India Lubricants

Source : Company; RSL Research

Market Share in Urban Retail Lubricants segment

Castrol + PSU

OMCs

55%

Other MNCs

20%

Private

Domes�c

Players

25%

With leadership, experience and strong innovation skills, we expect CIL to benefit the most out of the technological advancements.

Strong brand image and expanding reach has enabled CIL to command better pricing power compared to its peers, despite increasing competition and declining base oil prices (key input for lubricants). Today, consumers have become more brand conscious and are ready to pay a premium price for better quality lubricant oil (which ensures smooth functioning of the engine and longer vehicle life). This, along with an improving demand scenario, stable RM prices and company efforts towards brand building (through creative marketing strategies) and innovative offerings should help CIL maintain its premium pricing (especially in the personal mobility space, which is growing fast and where affordability is higher) with improved volume offtake.

Along with a strong presence in the retail segment, CIL also has a strong tie up with established OEMs like Maruti Suzuki, Volkswagen group, Tata Motors, Ford, JCB, Bosch, John Deere, GM, Federal Mogul, Komatsu, JSW Steel, Skoda, Audi etc to whom it supplies a broad range of lubricants designed for particular operating conditions and environments. Many of its products are recommended by and co-engineered with major OEMs. In 2015, the company successfully launched two transmissions long drain oils for Tata Motors: Axle Extended drain GL-5 80W-140 and Manual Extended drain GL-4 80W-90 oils. Further, recently, CIL launched Castrol EDGE Professional LL IV FE 0W-20, Volkswagen Group's first 0W-20 engine oil, exclusively developed with Volkswagen for the benefit of customers of Volkswagen Group franchised workshops and dealerships. Going forward, we expect CIL to continue strengthening its partnership with existing OEMs and enter into new partnerships as well, which should further strengthen its brand positioning.

Strong Parentage

CIL is 51% owned by UK based Castrol Ltd, a wholly owned subsidiary of global petroleum major BP (British Petroleum) group. Castrol Ltd is the world’s leading manufacturer, distributor and marketer of premium lubricating oils, greases and related services to automotive, industrial, marine, aviation, oil exploration and production customers across the world. The company's delivery network extends throughout 140 countries, covering 800 ports and partnering with over 2000 distributors and agents. While BP has reduced its stake from 71% since May 2016, it intends to continue as a majority shareholder in CIL and remains committed to long term investments in India. This brightens CIL's long term growth prospects.

New launches, brand building efforts should lead to a meaningful turnaround in revenue growth

Volume recovery on cards with new launches and sustained investments in A&P Increasing competition, slowdown in the lubricant consumption (due to overall slowdown in the Auto segment and GDP/IIP cycle and due to increasing share of long drain interval products) had impacted CIL's volume growth, which declined by 2.7% over CY11-15. However, we feel the worst is over, as the volume trend has reversed. After five straight years of de-growth, CIL has delivered healthy volume growth of ~5% in 9MCY16, driven by improving demand scenario, new launches over the last few quarters, sustained investments in brand building (A&P spends 7.3% of net revenues) and favourable base. With increased vehicle sales and freight movement, the lubricant consumption is improving.

CIL is increasing its focus on the personal mobility space, which is witnessing faster growth over the last few quarters, compared to CV segment. CIL has witnessed double digit volume growth in personal mobility space in H1CY16 and healthy traction in CV and industrial segments (CV segment has reported positive volume growth after 5% de-growth (CAGR) in past four years). In TW, its brand Castrol Activ continued to deliver strong double-digit through sustained investments and effective market interventions. In PV segment, growth has been driven by Magnatec brand led by new customer activations and

Religare Investment Call

Initiating Coverage

Strong brand image and expanding reach has enabled CIL to command better pricing power

CIL has a strong tie up with established O E M s l i k e Ta t a M o t o r s , F o r d , Volkswagen, etc

CIL's parent intends to continue as a majority shareholder in CIL

After 2.7% de-growth over CY11-15, CIL witnessed a revival in volume growth, up 5% in 9MCY16

Castrol India Lubricants

Revenues (Rs cr) - LHS Growth (%) - RHS

2,9

93

.2

3,1

20

.9

3,1

79

.6

3,3

92

.3

3,2

98

.0

3,4

27

.2

3,7

01

.0

4,0

52

.1

-5

-3

-1

1

3

5

7

9

11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

better marketing initiatives. The recent launch of Castrol CRB mini trucks contributed to growth in CV segment.

Demand uptick for lubricants, new launches (with focus on innovative offerings), increasing presence in fast growing personal mobility space (revenue share to improve), sustained investments in A&P (expected to remain between 7-8%) and increasing tie ups with OEMs should enable CIL to report healthy volume growth over the next two to three years. We expect the volumes to grow by 6.6% CAGR over CY15-18E.

Realizations to improve gradually with increasing share of power brands

CIL's new strategy of targeting profitable volume growth (more focus on personal mobility space and other lucrative segments) is clearly yielding benefits. With increasing share of power brands and high end lubricants, we expect the mix to improve, which would result in better realisations going forward (though gradual). Further, improved demand scenario will lower the price discounts / rebates (currently being offered by CIL and smaller players like Gulf Oil, Lubricants and Tide Water Oil) and enable CIL to command premium pricing despite higher competition. We expect CIL's net realisations (currently impacted due to higher rebates offered) to improve from Rs 172.7 per litre in CY15 to Rs 175.2 per litre in CY18E.

Overall revenues to grow by 7.1% over CY15-18E

With turnaround in the volume growth and uptick in realizations, we expect CIL's overall revenues to grow by 7.1% CAGR over CY15-18E, better than 3.8% reported over CY10-15.

Religare Investment Call

Initiating Coverage

Net Realisations to improve gradually with rising share of power brands

Volumes to grow by 6.6% CAGR over CY15-18E, led by demand uptick, new launches & sustained A&P spends

Volume and Realisation uptick should boost the overall revenue growth

Castrol India Lubricants

Source : Company; RSL ResearchSource : Company; RSL Research

Volume growth to witness a turnaround Gradual improvement likely in Net Realizations

Source : Company; RSL Research

Revenues to grow by 7.1% CAGR over CY15-18, led by volumes

Improved mix, operating leverage to aid in margin expansion

CIL's gross margins expanded significantly by 858bps in CY15 to 51.5% and further by 478bps in H1CY16 to 55.7%, aided by sharp decline in the base oil prices (a derivative of crude oil and key input for lubricants, account for ~53% of total cost of materials consumed). EBITDA margins improved 600 bps in CY15 to 27.1% and further by 424 bps in H1CY16 to 31.3%. The crude oil prices have fallen by ~40%, which has led to ~37% fall in the base oil prices over the last two years.

Gross and EBITDA margins are likely to expand by 304bps and 282 bps respectively in CY16, likely to be aided by RM tailwinds. However, assuming that the base oil prices stabilize at current levels, RM tailwinds are likely to wane out from Q4CY16 / Q1CY17 onwards. Despite this, we expect a steady improvement in gross margins (+30 bps) and EBITDA margins (+55bps) over CY16-18E, likely to be driven by structural levers like improved sales mix, operating leverage (likely to kick in with better volume growth). Further decline in the crude oil prices could provide more cushion to margins.

Higher EBITDA margins would translate into higher PAT margins, which are likely to improve by 184bps over CY15-18E. In value terms, we expect the PAT growth to improve to 10.5% over CY15-18E.

Religare Investment Call

Initiating Coverage

EBITDA margins are likely to improve by 337bps over CY15-18E, led by better mix, operating leverage and stable input cost

Improved realisations should keep the gross margins healthy

Higher OPM should translate into higher PAT margins (+184bps over CY15-18E)

Castrol India Lubricants

Source : Company; RSL ResearchSource : Company; RSL Research

Gross margin gains to continue, but gradually Base oil prices have declined sharply over CY14-16

Source : Company; RSL ResearchSource : Company; RSL Research

EBITDA margin to expand further Steady rise in PAT margins to continue

-

20

40

60

80

100

120

140

160

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

Dec

-15

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

Base Oil (USD/BBL) Brent Prices (USD/BBL)Gross margins (%)

40

43

46

49

52

55

58

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

66

9.6

62

2.8

68

7.6

71

6.7

89

4.8

1,0

26

.5

1,1

14

.0

1,2

35

.9

15

18

21

24

27

30

33

0

250

500

750

1,000

1,250

1,500

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

EBITDA (Rs cr) - LHS EBITDA margins (%) - RHS

48

1.0

44

7.4

49

3.4

47

4.5

61

5.2

68

2.9

74

7.4

83

0.4

6

9

12

15

18

21

24

0

150

300

450

600

750

900

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

PAT (Rs cr) - LHS PAT margins (%) - RHS

Premium valuations to sustain, given high dividend payouts, cash rich and debt free status and superior return ratios

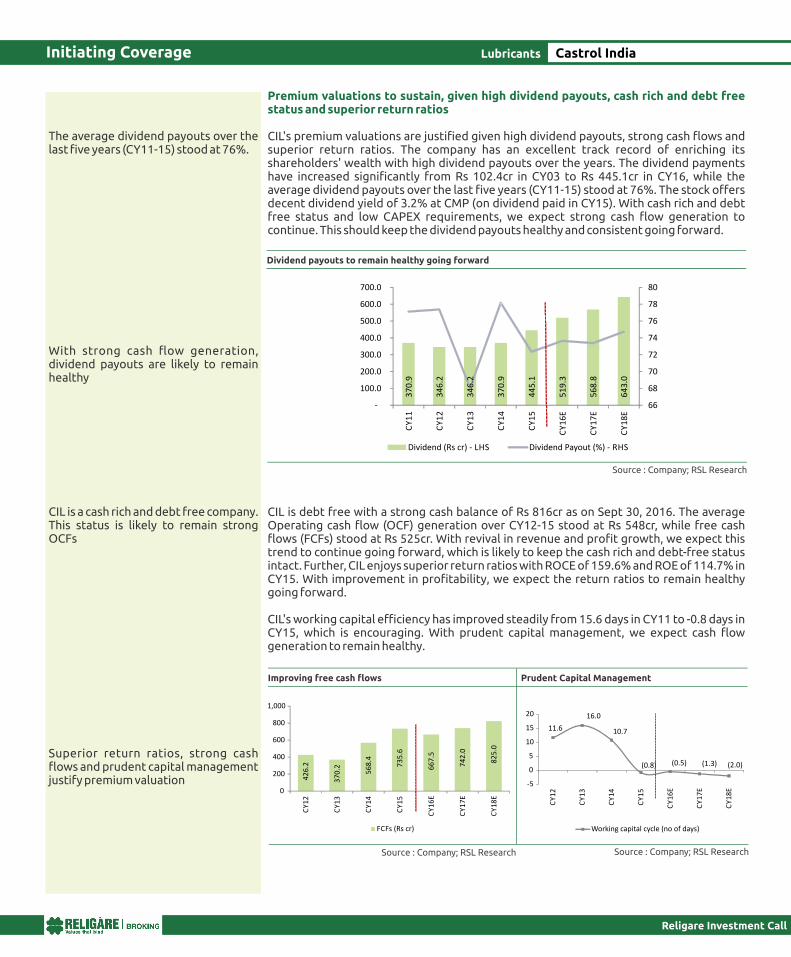

CIL's premium valuations are justified given high dividend payouts, strong cash flows and superior return ratios. The company has an excellent track record of enriching its shareholders' wealth with high dividend payouts over the years. The dividend payments have increased significantly from Rs 102.4cr in CY03 to Rs 445.1cr in CY16, while the average dividend payouts over the last five years (CY11-15) stood at 76%. The stock offers decent dividend yield of 3.2% at CMP (on dividend paid in CY15). With cash rich and debt free status and low CAPEX requirements, we expect strong cash flow generation to continue. This should keep the dividend payouts healthy and consistent going forward.

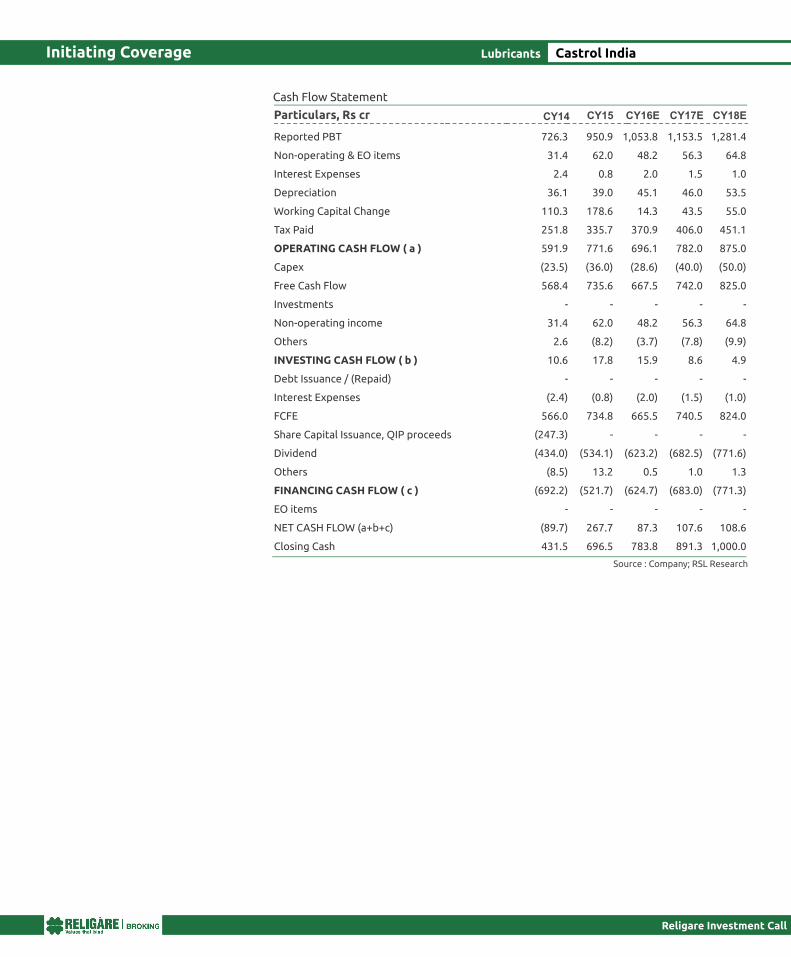

CIL is debt free with a strong cash balance of Rs 816cr as on Sept 30, 2016. The average Operating cash flow (OCF) generation over CY12-15 stood at Rs 548cr, while free cash flows (FCFs) stood at Rs 525cr. With revival in revenue and profit growth, we expect this trend to continue going forward, which is likely to keep the cash rich and debt-free status intact. Further, CIL enjoys superior return ratios with ROCE of 159.6% and ROE of 114.7% in CY15. With improvement in profitability, we expect the return ratios to remain healthy going forward.

CIL's working capital efficiency has improved steadily from 15.6 days in CY11 to -0.8 days in CY15, which is encouraging. With prudent capital management, we expect cash flow generation to remain healthy.

FCFs (Rs cr)

11.6

16.0

10.7

(0.8) (0.5) (1.3) (2.0)

-5

0

5

10

15

20

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

Working capital cycle (no of days)

Religare Investment Call

Initiating Coverage

The average dividend payouts over the last five years (CY11-15) stood at 76%.

With strong cash flow generation, dividend payouts are likely to remain healthy

CIL is a cash rich and debt free company. This status is likely to remain strong OCFs

Superior return ratios, strong cash flows and prudent capital management justify premium valuation

Castrol India Lubricants

Source : Company; RSL Research

Dividend payouts to remain healthy going forward

37

0.9

34

6.2

34

6.2

37

0.9

44

5.1

51

9.3

56

8.8

64

3.0

66

68

70

72

74

76

78

80

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

Dividend (Rs cr) - LHS Dividend Payout (%) - RHS

Source : Company; RSL ResearchSource : Company; RSL Research

Improving free cash flows Prudent Capital Management

42

6.2

37

0.2

56

8.4

73

5.6

66

7.5

74

2.0

82

5.0

0

200

400

600

800

1,000

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

Company Background

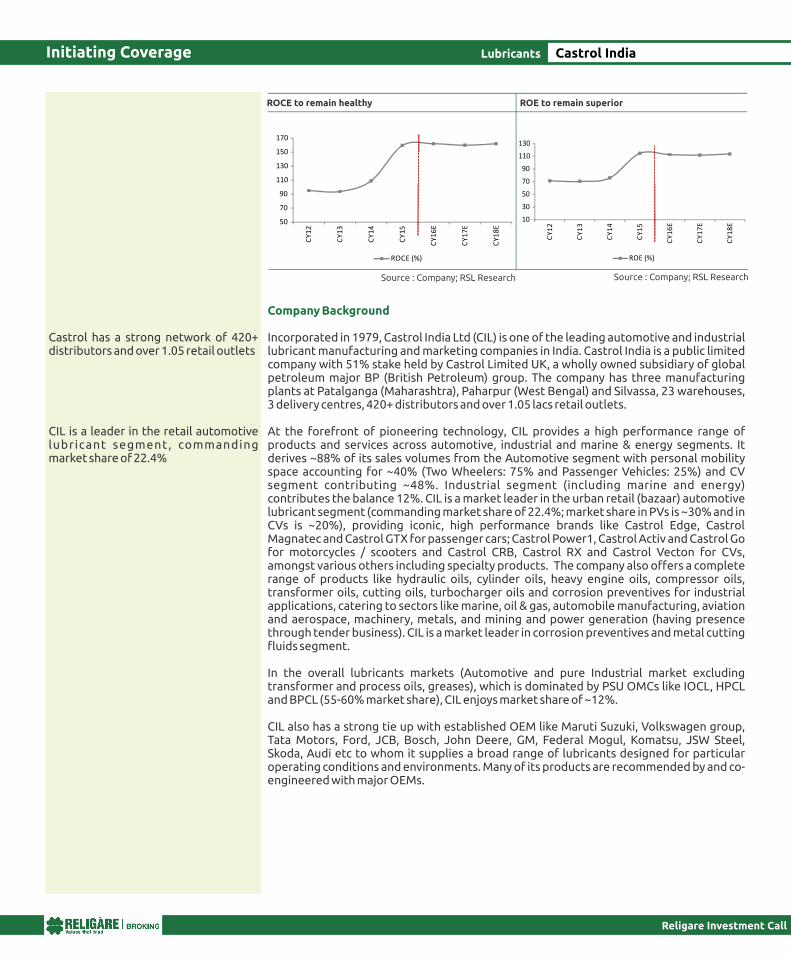

Incorporated in 1979, Castrol India Ltd (CIL) is one of the leading automotive and industrial lubricant manufacturing and marketing companies in India. Castrol India is a public limited company with 51% stake held by Castrol Limited UK, a wholly owned subsidiary of global petroleum major BP (British Petroleum) group. The company has three manufacturing plants at Patalganga (Maharashtra), Paharpur (West Bengal) and Silvassa, 23 warehouses, 3 delivery centres, 420+ distributors and over 1.05 lacs retail outlets.

At the forefront of pioneering technology, CIL provides a high performance range of products and services across automotive, industrial and marine & energy segments. It derives ~88% of its sales volumes from the Automotive segment with personal mobility space accounting for ~40% (Two Wheelers: 75% and Passenger Vehicles: 25%) and CV segment contributing ~48%. Industrial segment (including marine and energy) contributes the balance 12%. CIL is a market leader in the urban retail (bazaar) automotive lubricant segment (commanding market share of 22.4%; market share in PVs is ~30% and in CVs is ~20%), providing iconic, high performance brands like Castrol Edge, Castrol Magnatec and Castrol GTX for passenger cars; Castrol Power1, Castrol Activ and Castrol Go for motorcycles / scooters and Castrol CRB, Castrol RX and Castrol Vecton for CVs, amongst various others including specialty products. The company also offers a complete range of products like hydraulic oils, cylinder oils, heavy engine oils, compressor oils, transformer oils, cutting oils, turbocharger oils and corrosion preventives for industrial applications, catering to sectors like marine, oil & gas, automobile manufacturing, aviation and aerospace, machinery, metals, and mining and power generation (having presence through tender business). CIL is a market leader in corrosion preventives and metal cutting fluids segment.

In the overall lubricants markets (Automotive and pure Industrial market excluding transformer and process oils, greases), which is dominated by PSU OMCs like IOCL, HPCL and BPCL (55-60% market share), CIL enjoys market share of ~12%.

CIL also has a strong tie up with established OEM like Maruti Suzuki, Volkswagen group, Tata Motors, Ford, JCB, Bosch, John Deere, GM, Federal Mogul, Komatsu, JSW Steel, Skoda, Audi etc to whom it supplies a broad range of lubricants designed for particular operating conditions and environments. Many of its products are recommended by and co-engineered with major OEMs.

Religare Investment Call

Initiating Coverage

Castrol has a strong network of 420+ distributors and over 1.05 retail outlets

CIL is a leader in the retail automotive lubricant segment, commanding market share of 22.4%

Castrol India Lubricants

Source : Company; RSL ResearchSource : Company; RSL Research

ROCE to remain healthy ROE to remain superior

50

70

90

110

130

150

170

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

ROCE (%)

10

30

50

70

90

110

130

CY

12

CY

13

CY

14

CY

15

CY

16

E

CY

17

E

CY

18

E

ROE (%)

Risks & Concerns

Sharp rise in crude oil prices from current levels could result in higher base oil prices (key input for lubricants, accounting for 53% of cost of materials consumed; additives, chemicals and packaging cost contribute the balance) and impact CIL's margins in the event of company's failure to pass on the cost inflation to the consumers completely.

The growth of the Indian Lubricant industry is driven by uptick in Auto industry and GDP/IIP cycle. Any delay in revival could pose a risk to our growth estimates.

CIL imports ~47% of its raw material (Base Oil) requirement and its exports are just Rs

2.3crs (0.1% of the total revenues). A sharp depreciation in INR could impact its margins significantly.

Castrol continues to face competition from PSU OMCs and other established private players like Gulf Oil Lubricants and Tide Water Oil, who are aggressively marketing their products at competitive prices. This, coupled with entry of new players could continue to put pressure on pricing and keep A&P spends high.

The promoter's (Castrol Ltd, UK) stake has declined from 71% to 51% since May 2016. It

sold 11.5% in May 2016 (for Rs 2,075cr) and further 8.5% in Sept 2016 (for Rs 2,100cr). We feel these divestments were made to meet the demand arising from Gulf of Mexico oil spill. While BP has expressed its intentions to continue as a majority shareholder in CIL through Castrol, any further reduction in the equity stake going forward could be taken negatively by the investors.

The recent move of demonetization of currency by the Indian Government is likely to impact the overall consumption in the economy. This could impact the company’s volume growth for a quarter or two. However, the long term outlook remains intact.

Religare Investment Call

Initiating Coverage

Castrol derives ~88% of its sales volumes from Automotive segment (Personal Mobility: 40%; CVs: 48%)

Key risks include i) input cost inflation, ii) slowdown in the Indian economy, iii) sharp rupee depreciation and iv) rising competition

Castrol India Lubricants

Source : Company; RSL Research

Source : Company; RSL Research

Segmental breakup of Sales volumes

Personal

Mobility

40%

CVs

48%

Industrials

12%

Category Products Two Wheelers

Activ, Power 1, Go

Passenger Vehicles

GTX, Magnatec (semi synthetic) and Edge (fully synthetic)

Before you use this research report , please ensure to go through thedisclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulat ions , 2014 and Research Disc la imer at the fol lowing l ink : http://old.religareonline.com/research/Disclaimer/Disclaimer_RSL.htmlSpecific analyst(s) specific disclosure(s) inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014 is/are as under:Statements on ownership and material conflicts of interest , compensation– Research Analyst (RA) [Please note that only in case of multiple RAs, if in the event answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) below , are given separately]

S. No. Statement Answer

Tick appropriate

I/we or any of my/our relative has any financial interest in the subject company? [If answer is yes, nature of Interestis given below this table]

I/we or any of my/our relatives, have actual/beneficial ownership of one per cent. or more securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance?

I / we or any of my/our relative, has any other material conflict of interest at the time of publication of the research report or at the time of public appearance?

I/we have received any compensation from the subject company in the past twelve months?

I/we have managed or co-managed public offering of securities for the subject company in the past twelve months?

I/we have received any compensation for brokerage services from the subject company in the past twelve months?

I/we have received any compensation for products or services other than brokerage services from the subject company in the past twelve months?

I/we have received any compensation or other benefits from the subject company or third party in connection with the research report?

I/we have served as an officer, director or employee of the subject company?

I/we have been engaged in market making activity for the subject company?

YES NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

NO

Nature of Interest ( if answer to F (a) aboveis Yes : …………………………………………………………………………………………………………………………………………………............................................Name(s)with Signature(s)of RA(s).[Please note that only in case of multiple RAs andif the answers differ inter-se between the RAs, then RA specific answer with respect to questions under F (a) to F(j) above , are given below]

SS.No Name(s) of RA Signatures of RASerial Question of question which the signing RA needs

to make separate declaration / answer YES NO

Copyright in this document vests exclusively with RSL. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose, without prior written permission from RSL. We do not guarantee the integrity of any emails or attached files and are not responsible for any changes made to them by any other person.