Page 1

a

L

ET3OO6 INNOVATION AND ENTERPRISECOMPUTER AIDED DESIGN OF SCUBA

DIVING AIR PRESSURE WARNING DEVICE

Finance SectionBy

YASHAR KHATIB SHAHIDI

BSc. (Honours) Computer Aided Product DesignSchool of Engineering and Built Environment

University of Wolverhampton

Year:Module Leader:Innovation and Enterprise undertaken during:Credit Rating:Mode of Aftendance:

2007 n008Mr. G. HudsonSemester 2 2008, IE

Full Time

Page 2

Contents

Chapter

1. Preface1.1 Why does Oxycheck need finance

2. Background2,1 Type of company2.2 Ovarall background

3. Properties3.1 Year 13.2 Year 2, 3, and 43.3 Year 5

4. Ingurance4,1 Liability lrcuranca4,2 Propedy lnsuranca4,3 Busineeg a3sete and equipment Insunance4.4 TEdesmen lnsurance4.5 Buslnoss Interruption Insurance

5. Legal fees

6. Product Costing6.1 Part costing8.2 Cost of parF each yeat

7. Employeo (Staff, L.bour)7.'l Staff requirements7.2 Director3 3alary7,3 Employoe requirement for yoar 17.4 Employee r€quirement for year 27.5 Employee roquirement for yeat 37.6 Employee rcquirement for year 47.7 Employee rcquirement fo. year 5

8. Utility bills

9. Equipment and tool9.1 Computer (Hardware and Software)9.2 Office equipments9.3 Tools

10. Advertising costs10.1 Initial advertising cost10.2 Advertising cost for year 1

Page

11-4

44-5

6-77-88-99-10

10-1111-1212121212-13

13

1314 -'t515

16-1717-18t8t919202021

21

2222-2424-2929-30

313t3t

Page 3

tt

tl

LtIL

'10.3 Advertising cost for ygar 210.4 Advertising cost for year 3'10.5 Advertising cost for year 410.6 Advertising cost for year 510,7 Summary ot sdvertising cost

11. Distribution cost11.1 Paypal service chargetl.2 Distribution cost in year.lll.3 Distribution cost in year 2'11,4 Distrlbution cost in year 311.5 Distribution co6t in year4l'1.6 Distribution cost in ysar 5

12. Rotail of product12.'l Toleranco in sales

13, Taxes and buslnsss rateg13.1 VAT13.2 Buslne$ rates

14. Availabl€ types of financo sources14.1 Dircctofs finance cont butlon14,2 Bank Loane'14.3 Ovordraft14.4 Grants14,5 Venture capital14.6 Business angel flnanca

15. Cash Fldly forecast and Break-Even polnt Analysis

Appendix

Bibliography

3232323233

33333435353535

4243434lt444

36-3737 -40

4040-4142

45-51

52

53-54

Page 4

f-

1. Preface

Finance is one of the most viial part of any company and almost head of any

company. In order for any company to succe€d and remain competent in

market it nesds to consider financial issues, produc.ts and services. lt takes

money to make money, and every small business needs money to get started,

to op€rate, and to sxpand and grow.

For a new company which is called Oxycheck producing a brand new product

into market (SCUBA air pressurs warning system), it is vital that all of the

L financialaspects and issues arc considered and anticipated.

{.1 tlvhy doe€ Oxycheck need flnance?

It is important to cloarly identiry the purpos€ of lhe funds. Businese finance is

generally used to acquire assets which ar€ employed to help the business

achi€ve its pofit-making objectives, such as:

. To purchase capital items (fixed assets) e.9., plant, equipment, land or

buildings, motor vehicles;

. To increase holdings of trading stock and supplies;

. To fund research and dev€lopment;

. To expand distribution or develop nsfl markets.

Expenditures or costs are categorised inlo two groups' :

. Fixed costs: ll includes rent, insurance, ofti@ expense, equipmenr,

etc., which does not vary as a result of output volume or sales revenue.

1 - o{ine ro$c€ - htts:/ pvw.busin€ssdictiomry.com/defrinon/vadabte-costhtml

Page 5

. Variable costs: Periodic cost that varies, more or less, in step with the

output or the sales revenue of a firm. These include raw material,

energy usage, labour (wages), utility bills, distribution costs, etc.

Differerit aspects of expenditures need to be considered and assessed as

following:

. Property and pt€mises: This s€ction besides property cosls incluoes

additional costs such as Eleclricity, gas, water supply, ventilation etc.

This algo includes any further property development which needs ro be

o@lned for some r€asons such as, product development, acc€ssibility

and sabty.

. Legal feee: lt includes solicitor fees.

. Insurance: lt is very important and essential for any company lo insure

for any areas such as damage, thefr, injury or loss. The policy provides

the firm with fnancial security and ease of mind. These areas include

buildings, employees, machines and etc.

. Tho employees: People, lvho are involved to produce, ass€mble and

pack and also staff involvad in office department such as designing,

finance, accountant and etc. This area include number of staff,

wage/salary, and hours required.

. Utility bills: lt includes cost of electricity per year.

. Accounting fees: Cosl of accounting br Oxycheck (Employing an

accountant).

. Job expenses: Expenditures should be tracked for those direct labour

and material costs to each job. In addition, overhead costs and

allocating them to various jobs should be considered as applicable.

Page 6

This provides accurate profit per product and includes total cost of

manufacturing the product, the total time to manufacture per product,

combined with total employee wage. This is used to make decision on

the Gtail cost of the producl, with a sufficient profit. Consequenfly the

retail of produc{ can be obtained fto previous sections. Total income

and profit can be obtained for period of 5 yeaB.

. itachines and tools: This is additionat cost that is required to

manufacture the product wiich includes hardware and software such

as PC computers and sofh are licences. Oxycheck will not

manuiacture any parts and those paris which need to be manufactured

will be manufaclured by outer manufac.turing companies.

. RepalE and Maintenance: Since Oxycheck will move to new

induslrial units in year 2, therebre the unit will require repairs and

maintenance.

. Security: From year 2 onward the company will employ someone for

s€curity.

. Promotion (Advertleing) costs: This is very important section which

assigns expendituro to introduce tho produc,t in thB market. The

website will promote the produci and company, and also be usad for

communication purposes between sellers and @nsumers.

. Business rent and rate: Business rate coveJs all exoenditures owed

to govemment such as tax, VAT, etc and business renl is called

leasing.

Page 7

Financial management must be accurate and it is vital for any company to be

able to manage their fnancial aspec-ts in oder to be successful. A business

fails b€cause of main reasons as described as followino:

. Running out of fnance

. Failure to providing costs for production, sales and failure lo

anticipating nat profit (Not understanding the cost of sales)

. Failure to paying back creditors (Over bonowing).

Many new business€ witl exhaust the intemal financial resources which are

used during the start-up phase, and will eventually seek additional capital to

contjnue growing.

In managing finance any company musl prcparo itself for the worst situalon

which occuB in company's fJture financ€ issues and be ablo to understand

the '\/vl|at lb'and addr€ss them.

2. Backgrcund

2,1 Type of company

The brand ns,v company Orycheck initially start as a partnership firm. A

partnership company both formally and informally means a situation where

two or more people are working together for a common purpose, with

responsibility, commitmsnt and tho intention of making money.

All partners are liable br partnership debts and protits and are divided equa y

between each member.

4

Page 8

Before making any decisions all the members have to come to an agreement on

all decisions and olans.

Some advaniages are;

. A company based on partnership is able to generate more budget

. Whole the work in company is shared and spreaded almost equally with

each members of the company

. Lossas and profits of the company are shared with each members of the

company

Some disadvantages are:

. The company is limited to the decision of a the members of the company.

ll means allth6 mombers must agree on the decision which can cause

conflict

. Each member of the company are liable and responsible for th€

@nsequences oftheir decision in future which can cause problam and

confl ict amongst members

After discussion between directors of the Oxycheck it was agread that the

company Oxycheck during the beginning stages is based on partnership

business due to sharing responsibilities with 3 members of the company

(Marketing, Design, Production, and finance directors).

After lhe company was established successfutly it will move on to the stage in

which lhe business could develop into a sole trader or a limited company.

Page 9

2.2 Overall background

The finance department produces an accurate cash flow and a business plan.

From the plan, the llnancial aspects can be set.

All type of costs and expenditures which will have effect on company will be

researched and produced it will also include individual costs and overheads.

Orycheck is a brand new firm with a brand new product and so does not have a

financial background to help to predict accurately therefore financial aspects will

be estimated such as expenditures, sales and etc.

The costs might change when the product is actually launched due to a number

of factors such as unforeseen delays and events. These costs are variable and

change which are included in cash flow. Other expenditures such as material

waste, employment leave, overlime, debts and VAT. The cash flow will include

fixed costs such as heating, rent, machinery and etc.

3. Properties

Properties have an important €ff6ct on the cost of any products distribution.

There are some factors that need to be considered. At the beginning the

properties will have a minimum space, cost and facilities, but in second year

Oxycheck will expand and try to add extra properties which specifically fulfil

the needs of a growing business. Eventually once the Oxycheck reached a

number of sales it will consider establish more oermanent oremises. The

premises information including unit area needed for production is obtained from

production department. Some factors need to be considered regarding premises

as follow:

. Location: lfthe property is close to city or town centre then the business

will become more popular and famjliar. The properties need

Page 10

to be located within these areas ior some reasons such as east to tind,

ease of transportation both for producl and employees, ease of

accessibility for distribution. For Ox)rcheck the property is preferably

better to be based in a popular area such as Wolverhampton.

Birmingham, Solihull, and Telficrd. These areas are suitable and

popular for business.

. equipments: The initial equipments will include work area, space for

PC computer€. As th6 business grows and improves more area will be

added such as bigger area to accommodate the growing woakforce,

stafi r@m, stock or storage area, CAD d$ign room, offico for sale,

purchase, gnquires @mmunication and separate rooms for each

direc{or.

. Expendltures: This factor is very crucial. The members of the

company rsquire negotiating and making a final dacision to fnd the

most cosfeftctive properties. The prop€rtios will alter for coming

financial years of 2, 3, 4, and 5. As Oxycheck develops it is crucial for

the company to minimise the unnecessary costs.

3.1 Year I

Year 1 tyill be very sucial for company in terms of cost. Because ihe business

is in its initial stage and low sales and pmft therefore it needs to save money

as much as Oossible,

7

Page 11

After discussion betlv€en directors of the company they came up with a

solution, a cost-effective way. The solution was to run the business in the

existing premises and facilities owned by the direc-tors.

3.2 Year 2,3, and 4

In year 2 the company will intend to develop in terms of premises and sales.

One ot the ways of achieving this is to locate sxternal premises with

equipments and facilities to meet and accommodate the growing in s3les and

demand. Ther€ is cunently an ideal industrial unit in Birmingham'? :

Actdrw:75-79 Wright Street, Small Heath, Birmingham, 810 gSP.

SIze.' 68 so m

Ierrurcj To lgt - lt allo/vs a tenant to give 3 months notice to vacate after 12

months occupation,

Descrtplionj The units will be of ste€l portal frame consiruction with brick and

block inill to half height and metal cladding above with profile matal clad roof

- incorporating roof lights. The units will benefit from concrete floor, fluorescsnl

strip lighting, power operated roller shutter, 3-phase power and toilet facilities.

The offic€ space will benefit from a 3KW heater and double glazed windows

' fitted with intemal s€curity grills. The premises will also feature secure

perimeiar.

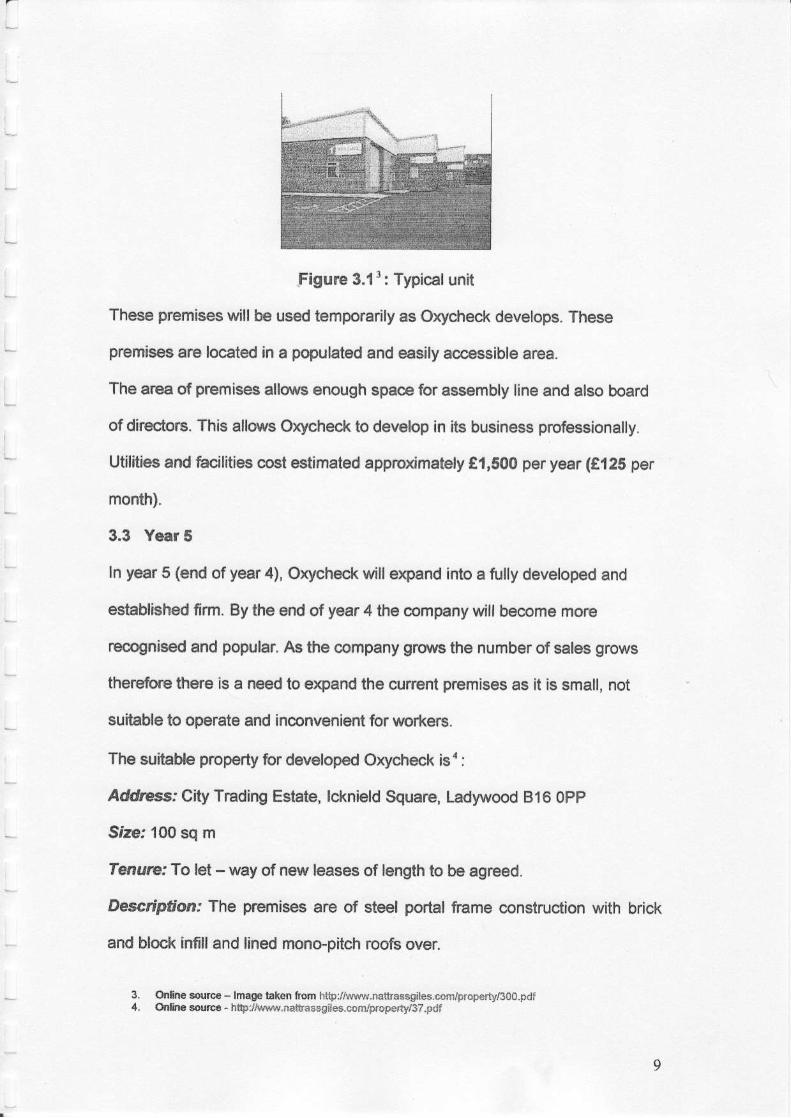

Cosf.' This premises costs €1680 per annum to rent (C140 per month).

- Figure 3.1 shor/s the image of the unit in Birmingham.

2- OfilineEource-htts/'dw.nattrassgiles.cortprcpedyB00,pdf

Page 12

Figure 3.13: Typical unit

These premises will be used temporarily as Oxycheck develops. These

premis€s are located in a populated and easily accassible area.

The area of premises allorvs enough space for assembly line and also board

of direc{ors. This alloivs Oxycheck to develop in its business professionally.

Utilities and facilities cost estimated appmximately €,11500 psr year (e,t25 per

month).

3.3 Year 5

In year 5 (end of year 4), Orycheck will erpand into a fully developed and

established irm. By the end of ysar 4 the company will bacoms more

rocognised and popular. As the company gro\ rs the number of sales grows

therefore thsrs is a need to expand the cunent premises as it is small, not

suilable to oporate and inconvenient for workers.

The suitable property tor developed Oxycheck is4 :

Addess,'City Trading Estate, lcknield Square, Ladywood 816 oPP

Sizei 100 sq m

Tenurei To let - way of new leases of length to be agreed.

Description: The premises are of steel portal frame construction with brick

and block infill and lined mono-pitch roofs over.

Ofline &@- lmigc takDn trorn htF/M.natbassgiles.coolproperty/3oo.pdfOnltie sur6 - htFr i/ww.nadRsssiles.com/,tror€rty/37.pdt

3.

Page 13

In the main the units beneft fiom fluorescent strip lighting, 3 phas€ electricity

and roller shufter, concertina loading door to the front. WC. facilities are also

provided with each unil.

Cosi,' This premises costs E5{ t 1 per annum to rent (€426 per month).

Figure 3.2 shows image of ihe unit in Birmingham.

Flgur€ 3.25 : Industrial Unit

The ptop€rly will help to fuml th6 r€quirements of Oxycheck and also provide

space fur directors and secretaries. Utilitie.e would approximately cost f2500

per year (f,208 per month).

For the first 5 years there ie no need for pr€mis€e development end new

comlruclion.

4, Insunnce

Many businessas such as wholesalers, manu{acturers, suppliers, wholesal6rs,

importors and exporters will r6quir6 insurance. The policy is to protect both

customers and businesses against unwanted events.

6. q he sorrc€ - lmase tak€n lrdn ht$:/ sw.naftassgiteacodpropenyBT.pd

10

Page 14

O)'Vcheck will also need different types of insurance which are now requir€o

by law. lt could be cover that a sensible and prudent business will take out to

proteci the business in the evenl of loss, damage or a claim against them for

damage or negligence.

The types of insurance lhat Oxycheck will need to use are as follow6:

4.1 Liability Insurance:

. Employer Liability: Most businesses will require some level of

liability insurance. The main liability insurance that is required by law is

employers' liability insurance. EmployeIs' liability insurance covers

employees against injury, illness or disease caused during th€ couBe

of their employment. For Oxycheck this kind of cover wil not be needed

until year 2. From year 2 onwards ag number of employees increases

each year a more payment will bs required.

. Public Llability: Public liability insuranca is insurance against damage

caused to third party property or penions.

. Products Liability: lt relates to any damage c€usad by prcducts

supplied by a eompany, whether manufaG-tured by them or not. This is

crucial form of insurance for Oxycheck, espacially as lhe product is

used by divers underwater. The supplier of the initial component which

caused the problem would also be investigated and Oxycheck would

not be completely responsible for the damage.

l l

6. fiine3ow@- ht&rM!1'br6inessinsure.e.uklbusinessimuranequotes_0o2.htm

Page 15

4.2

4.3

. Profcssional Indemnity Insurance: professional Indemnity Insurance

(Pl) covers Oxycheck in the event that a third party should ctaim for

mistakes that Oxycheci( make or ifthe company is found lo be

negligent. Professional indemnity cover Oxycheck from any customers

,l\/ho feel that the Scuba warning air devic€ is unsafe and dangerous

which is minimal for Oxycheck.

Property Insurance: This kind of insurance @vers firs, axplosion, etc.

this also covers any maintenance failure, lighting, etectricity.

Bu$inesa as8ets and Equipment Insurance: This covers a range of

factors, including stock which is damaged or stolen, machinery, electrical

equipm6nl, money loss (such as cash, cheques), laptops, mobiles and

BtC.

4,4 TEdesmen Insurrnce (K6y man Cover)?: Tradesmen lnsurance is

d$igned to protect a business should the key persons such as directors,

di€ or be seriously injured and unabl€ to work.

4.5 Bueinsas Interruptlon Insuranca3: This insurance provides cover for

any expenses incurad for temporary hire of replacemant equipment

folloiving damage to any of items insured under the Of{ice Contents of

Portable Equipment cover.

The cost ot insuranc6 is different each year for Orycheck. For the Jirst year

the cost of insurance is minimal (with no premises and no employees). Tne

cost of insurance will gradually increase from year 2 onwards.

Onkte soscs - Elo1ww'Gdsreapusiness.do.utdrevmdn.nrmlqrc soure nmr'/ww.@[email protected] .

t2

Page 16

The estimated insurance cost for each year (from year '1 to year 5) is shown in

table 4.1.

5. Legalfees

It includes solicitor fees. In year one solicitor will assist Oxycheck in registering

the company and dealing with legal and official tasks, In year 2 onwards the

solicitor will remain and deal with Oxycheck. Table 5.1 shows the estimated cost

of legal fees for each year.

Year lnsurance cost (oer vear) Insurance cost (Per month)12345

E10202144081776e264023120

e8581208148

e260Table 4.1: Estimatednsurance Cost

Year Total cost1

45

t450t36011108110t110

Table 5.'l: Estimated legal fees

6. ProductCosting

The cost of standard parts in bulk plus cost of manufactured parts gives almost

total product cost. In order to reduce the cost of product manufacturing afier

discussion between directors of the company it was decided that company will

purchase the standard parts in bulk and rest of the parts will be manufactured by

outer companies (Manufacturers). Allthe information for product costing such as

cost per unit, Cost of bulk, and cost per unit in bulk are obtained from production

deDartment.

13

Page 17

a

6.1 Part costing

The cost of parts is made up of two groups. Two groups of parts are standard

parts and manufactured parts. The information is gained from production section.

The components and their costs are shown in table 6.1.

Table 6,t: Cost of standard Darts Total = ffi9,A0

Total Mould (two plastic casings) Costs = €25,250

Total oroduct cost = f,69.60

Besides cost of one unit product (€69.60) other costs will contribute to tha

estimation of final unit price of product. Total cost of yaar t has been considered

and divided into number of sales in year 1 which is 1450 (Table 6.2),

Table 6.2: Expenditures per unitTotal expenditures per unit = e14.2

Part Cost per unit Cost of Bulkfl500)

Cost per unit in bulk

TPSA orecisionPressure transmitter

e65.98 862,985 €41.99

Vibrator26DL24O765212

€1.90 t2100 tl.40

Plastic casino € 1.50 t1425 €0.95Main s€al € 1.30 €975 e0.65O rinE s€al LOZO e0,35Screw o rinos e0.10 €1200 e0,80Elsc-tronic modul6 e10.95 €7485 e4.99Neck brace e15.00 84485Adapior e3.50 €3000 €2.00Battary L C.ZV €6435LED e0.39 €435High-Temp AirHose Conneclor

€10.50 €13200 t8.80

Screw r0.18 €150 e0.10

Deecription Expenditures in vear 'l Expendlturas per unitInsuranceLegal feesUtility bills

Hardware andSofiware

Advertising costDistribution cost

Mould cost

LOJO

€4508220

€ 1 173.56

e1804.48t6584.9t9700

90.44c0.31e0.15e0.81

E1.2504.54€6.70

t4

Page 18

Other minor costs are considered in the estimation of final unit price of Droduct.

6,2 Cost of parts each year

The cost of components will be based on predicted sales produced in marketing

department. All the components will be purchased in bulk of 1500 for the amount

of sales which are forecasted. This will reduce the amount of purchasing and

keep the amount of stock to a minimum level.

On the other hand, it is impossible to predict the exact amount of sale and

demand for coming yeaE and also some parts might need replacement due to

faulty during manufac{uring and assembly, Therefore Oxycheck will consider

extra st6k to compens€te that unpredicted shortage.

Table 6.3 shows forecagt number of sales per week, month, and year for 5 yeaB.

Yoat Por week Per Month Per Year1 12'l 1450

b5 3150a 152 608 73004 266 1066 12800

316 1268 15200Total 829 3322 39,900

Table 6,3: Predicted amounl of sales

Th6 total mould and tooling cost will be paid off ov6r tho l2monthsof first y6ar.

Table 6.4 shows total cost of producl each year.

Year Amount Per Yesr Per Month1 '1450 €100.920 €8.4102 3150 t215.240 814.270

7300 t508,080 t42,3404 12800 f890.880 274.2405 15200 e1.057.920 e88.160

Table 6.4: Produc{ cost

15

Page 19

7. Employee (Staff, Labour)

Any company need to have a plan for its staff requirements. Therefore in order

for Oxycheck to run efiiciently in first 5 years it is essential for Oxycheck to have

an efficient plan for its staff. Oxycheck will try to keep its staff in minimum level in

order lo reduce the cost and save money. The company almost will not need

expertise or experienced staff to carry out the job because the product is simply

designed for assembling, testing and packaging. The components which require

to be manufactured will b€ manufactured by different companies. Oxycheck will

employ an accountant and gecurity from year 2. A secretary will be required and

assigned to the Oxycheck in long-term period with a fixed salary.

All the information rsgarding staff requirements for production are astimated and

obtained from Droduction deoartment.

The requirements of lhe secretary and accountant are:

Recording company's database and information

Administrating company's loss and profit

Dealing with cuslomers

Dealing with property and insurance

Therefore both secretary and accountant must be experienced and have

knowledge of computer and good communication and be able to work in a team.

16

Page 20

No technician or specialists will be needed for repairement in case of faulty in

product returned by customer or during assembling as replacement or refund will

be issued instead of repair. Directors' salary will vary each year. This is to ensure

that the board of directors are committed and devoted to the company.

Although Oxycheck is a small company at the beginning but it will need long{erm

assemblers and provide them with some benefits such as travel expenditures for

people who don't have private transportation and also sick pay will be

considered.

The budget of transport or travel for each employee will be E8 per week

7.1 Statf requiremonts

It is vital to predict the required number of employee needed to meet the

production rate. lf the right number of employees would be assigned to Orycheck

the company will benefit from cost efficiancy which consequently has effect on

productivity of the company,

According to table 6.4 amount of 1450 in year one will be produced. Therefore 4

directors will be able to produce 120 per month. lt is assumed that one labour will

be able to assemble at least 120 units per month in first year. Therefore each

assembler will be expected to produce approximately 30 per week (From 9am to

spm - fulltime) according to the predicted sales (120 per month). The base of

calculation will be 30 units per assembler per week. And the number of

assemblers for following years will be calculated according to first year.

Required number ofsfaff= Number of produdion per month divided into 120

(Number of finished product per employee per month).

Number of production per month has been extracted from table 7.1.

t7

Page 21

Year Requirednumber of

production (permonth)

Number ofproduction per

employee

Number ofemployees

'l 120 't20 None2 262 't20

609 120 54 '1067 120

't267 120 1 1 + secretarvTable 7.1: Number of required employees

As it was said in year 1 no staff will be employed and the directors of the

company will carry out the assembling tasks.

7.2 Dircctors salary

Directois salary will vary each year. In year one, 35o/o of the sales will be

designated for all the directors (Marketing, Design, Production and Finance). In

year two less than 2070 of the sales in y6ar thrse 20%, in year four 25%, and in

year five 25% of the sales will be designated as director's salary. The dir€ctors

will work for the first two years as part time until year 3. The final price of each

unit forsale is e 122.

The salary of each dirsctor can bs oblained from th6 following relations.

Tohl dlrectors salaty = Percentage (Variable percents each year) x sales per

year

Table 7.2 displays estimated directofs salary:

YeaI Sales per yeat Salary of directorsoer vear

Salary of directors permonth

1 €176.900 cal o lq 15.159.58e384,300 e63.409.s 85,284.13€890,600 217A120 e14.843.33

4 e1,561,600 €390.400 e32.533.33e1,854,400 €463.600

Table 7.2: Directors salarv

18

Page 22

7.3 Employee requiroments for year 1

In year 1 to minimise the costs no labour will be employed. Atl the tasks will be

canied out by directors. The tasks will be assigned to the directors equally.

Design and produclion directors' responsibilities are as follow:

. Assembling

. Packaging

Marketing diractor's responsibilities are as follow:

. Advertising

. Distribution

Finance director's responsibilitias are as iollow:

. Accounting

. Dealing with customers

7.4 Employee requiruments for year 2

In ygar 2 as tha sales rate increases ther6 will be a need to employ extra statf for

assembling and manual lasks. According to table 7.1 in year 2, two persons will

be required as full time. Their task will be assembling. All figures include National

lnsuranc€ numbar and tax. Table 7.3 displays €mployee's wage in year 2.

Table 7.3: Total employee's wage in year 2

Total staff salary for year 2 = 953,820

9, Onlhesource- htts;/helvs.bbc.co,old1/hi/b$in*s/6425965.strn

Job Number ofemDlovees

Rate of paye Houra perweSk

Total pervear

Assemblers (FT)Security

AccountantSecretarv

1'l1

€5.52€5.52e5.52E5.52

38JO

3838

821,528E10,764810,764e10.764

19

Page 23

7.5 Employee requirement for year 3

As the amount of production and sales increas$ for the third year 3 more

employees will be requi.ed. Three additional employees will b€ added. Two

employees will be assigned for assembling and two employees for packing. And

one employee will be needed to assist and where nocessary. ln year 3 the salary

for secretary will be increased. Table 7.4 displays employeo's wage in year 3.

Table 7,4; Total employe€'s wage in year 3

Total staff salary for year 3 = 859,600

7.6 Employo€ requiramont for year 4

In year 4 additional labourg will be employed, and all of them will work on full time

basis. Table 7.5 displays employee's wage in y6ar 4.

Tabl6 7,5: Total employee's wage in year 4

Total 3taff safary for yeat 4 = L98,2O2

Job Number of6mDlOVee€

Rate of pay Hourg pgrweeK

Total pervear

A$emblers (FT)PackeB (FT)Part time staff

Secretarv11

e5.52e5.52€5.52€6.20

3819

821,528t21,52884,454

€12,090

Job Number ofemplovees

Rato of pay Hours perwook

Total perv0ar

Assemblers (FT)Packers (FT)

Secr€lerv

441

15.52e5.52e6.20

38

38

e€,056t43,0s6e12.090

20

Page 24

r

7.7 Employee requirement for year 5

Owing to growing in sales, Oxycheck will look lo develop into a professional

company in year 5. Therefore in year 5, 6 assemblers and 6 packers will be

needed. In year 5 there will be a need for an extra secretary and will be

employed. Table 7.6 displays employee's wage in year 5.

Table 7.6: Total employee's wage in year 5

Total staft balary for year 5 = €153,348

8. WiliU Bills

Electricity is one of the factors which contribute to the cost in annual cash flow.

The eleclricity is suppliod by Poworgen (A company of e.on) company. The

Oxycheck will not consume great deal of elec-tricity as the manufac'turing tasks

coneume big proportion of electricity and the manufacturad parts will be

produced by outer companies. In year 1 the tasks (assembling and office) will be

carried out at directors home and their garages. Estimated costs from year '1 to

year 5 are displayed in table 8.1.

Year Cost Der aeason Total cost Der vear'l

3

5

e5se55LOU

e60€60

t24012402240

Table 8.1: Estimated eleckicity charges

Job Number ofemDlovees

Rate of pay Hours perweek

Total porvear

Assemblers (FT)Packers (FT)

Secrebrvo

85.5285.52LO,ZV

38t64,584€64,584e24.180

2l

Page 25

9. EquipmentandTool

Each company or business will require a range of equipment and facilities to

operate. These facilities will include computers (Hardware and Software),

carpentry, furniture, and etc. all the information regarding equipment and tool for

production such as tool and equipment cost for production is gained from

production department.

9.1 Computer (Hardware and software)

Computer is one of the essential equipment for any business.

For almost all sections of the Oxycheck computer hardware and software is

ess€ntial.

. Marketing needs computers to create websites, leanets, online adverls

(Online purchasing and selling), producing sales graphs and creating

statistics.

. Design will need computer software (CAD software) for CAD designing to

dasign and develop SCUBA air pr6ssura warning system.

. Production will need computer for planning the assembly layout of the

company and also plans of assembly,

o Finance will need computer to produce accurate cash flows, and k6ep

Oxycheck records. The details of a proper computer for reasonable

Derformance are exolained as follow'o:

. 3.2 GHz Intel DUAL CORE 3.2GHz

e 2GB DDR2 RAM

. Hard Drive: 320 cigabyte

. HDD CD Rom: 'l6x DVD Rewritable

10. Online sou.ce - htlpJ vw.sunitek.co uld

Page 26

Local Area Network: 10/100 LAN

USB: 6 USB 2.0 ports 2 Front 4 Back

12 Month Warranty (3 years on CPU)

This package will cost €380 in first year. The price ofthe computer with the sam6

specilications will be reduded. The package also includes online service for any

technical issues. Figure 9.1 shows an image of 9.2 GHz Intel DUAL CORE.

Figure 9.1": 3.2 GHz IntelDUAL CORE

For first yoar Oxych€ck will need only two pos. Th€sB two computers will be

ueed by diroctors and they wlll ehar€ the PCs. In year 2, Oxycheck will purchase

two compulers with sam6 specifications. In y6ar 3 and S the company will

purchase 1 computer. During 5 years almosl all the membeB of the company will

own their c|lfln computeB. In t€rms of sofir,vare company will raquire a rang6 of

software.

11, Ordlne source - IrEg€ tak€n nom htlp:/tuwwsmitek.co.uv

Page 27

Soft^rares which the company will need a€ as follow:

. Miqosofi office XP protessionalt? - €65

. sotidworks 2006,r - €141.78

Table 9.2 displays eslimated costs of computer hardware and software.

Ycar Hardware Software Total (per vear)'1

45

1550e370e0

e413.568413.568206.78

cnE206.78

t1173.56€963.56t576.78

2476.78

TablE 9,2: Eslimated cost of hardware and sofrware

9,2 Offlce equlpmentg

Oxycheck will need a range of equipments. Thes€ 6quipments include fumiture,

computer desk, tables, carpentry, tiling cabinets and etc.

A list of equipments is explained as follow:

Offce D6sk' The desk will be suitable for four direclors and secretary (Figure

9,3).

Figure 9.3'a: Office desk

The pric€ for each desk is t129.99.

ln year 2, 5 desks will be purchased. And in year S, 1 desk wilt be purchased.

onling surce - htE ritrlvw.am4zon @m/l!l'cr o3oti office-Protessionat-ord-v.Fion/op/B0o0o5AF tounnne surce - M.rournevedeurope cooonlhesurce- lmg!taken t|m @

12.13.

24

Page 28

l

Table 9.4 displays cost of office desk.

Year Number of purchaseddeak

Cost perunit

Total cosi

1

4

0

1

€129,99

"o"

8649.95

!95Tablo 9.4: cost o{ offce desk

Sfadonrry.' lt includes A4 pap€rs, pen, p€ncil, notebook, file, ink and etc.

The cost of stationary for each year is estimated as below (Table 9.5).

Yaar Total coat Der vear1

4

€'150€E5LOO

€60€E0

Table 9.5: Cost of

Secu/ny Safe,' h year 2 Orychgck will ne6d a safe (Figur6 9.6) to ke6p its

documents and cash. The company will purchase a safa in year 2. The safe will

coet €105.00.

Figure 9.6't: Security safe

stationary

1A OnHne .ourso - tmag€ bt6n fom htby rww.bkmsecudrv.cn/*curitv.html

25

Page 29

TaUe for assemuing.. For assembling the product from year 2 till year S the

company will purchase 2 tables each year (Figure 9.2). The cost of each table is

€20 per table. The cost of table frcr €ach year is estimated as follow ffable 9.8).

Flgurr 9,716: Aseembling table

Year Number of unlt3 Total cost per year'l2

4

0

2

E40€40€40e40

Table 9,8: Estimated cost ot asbembling table

Oflct chrin in yaar 2, four offce chairs will be n€eded frcr direc{ors and one

chairwill be needed br secrEtary. In year five ong chairwill be purchased. Each

chair will cost !55.

Cost3 of chaiB are estimated in table 9.10.

Figure 9.9'7: Ofice chair

Oflih. lourc6 - lm.g. tat6n trdr Bvw'cbsv.co.ukO h. !our@ - lm.g. laLn ftDm \rvrw.ebav..o_uk

18.

26

Page 30

Table g,l0: Cost of oftice chair

OfficB cabtnet: Orydr€ck wilt need tiling cabinots to store documents and official

l6tters. lt will cost e33 and lhe company will purchase a set of drawings in year 2

and a set in year 5 (Figure 9.,t 1).

Flgutc 9.1113: Ofica cabinet

Tabls S. 1 2 displays co6t of oftice cabin6t.

Table 9.12: Cost of office cabinEt

Cabtnat lor employe€E (AsEqrrbte6): From year 2 Oxycheck will start

employing labour. Therefore they will bo assigned 6ach on6 locker to keeo their

stuff. lt will cost €35 fur each tockar (6 drawers on each lockor _ Figura 9. 1a).

The cost of loc*ers is estimaled as bello\ (Figure 9_.14).

onln $urc. - ldag. taken tilm ww.6b€v.co.ut

Year Number of units Total cost

2

4

04n01

0

0

Yeal Numbsr of unlts Total colt'l

o4

01001

0e33

n0

27

Page 31

L

l

Flgun 9.13": Assembler cabinet

Tlblo 9,{.[: Cost of ass€mbler cabinet

Chrlr fo/,ts'f,mbLrt: each assembler wlll l€quire a chair from year 2.

It will cod el0 per e€dr chair. The cost of cfieir3 is es$mated as bolo\, (Tabte

9.15).

chair ass€mblerB

Yial Numbe. of unltl Totrl coct12345

I

111

€35e35ctt

€354aa

Yeat l{umb€r of unltt Totrl coot12345

0

4612

0820€40€808120

Tlble 0.15: CoBt of

11 q*i. tlrt - [n g. t t n tan ww..b!y.co.uk

2A

Page 32

Coffee machlne: in year 2 a cofbe machine will be purchased. lt will cost €77.

Figure 9.16'o: Cofiae machine

9.3 Tools:

Basic tools will b6 r€quirod to assemblo the components. lt is not a highly

probseional job aE assomblels can be trained to carry out th6 job.

The tools will include screwdrivor, pli€rs, and cutter. A s6t of screwdriver and

pliers will cost €35 and cufter will cost 84 €ach. ThE cost oftools is sstimatod as

balow:

Flgure 9.17": Toole

Table 9. 1 8 displays cost of tools.

on&!3 .ourc. - lm.gr t6k€n no|n ww-ebav.co.|rlonlh. sourc. - lir€gc talcn fiom wt1w.ebav.co.uk

20,21,

Year Number of unltg Total cost12

4

12 t74

274Table 9.'18: Cost of tools

29

Page 33

Soldering iron: Soldering tron crmplete Kit wilh Sland will be purchased for

each assembler each ysar. lt costs e8.OO. Figure 9.19 shows an image of

soldering iron.

Flgure 9,19: Soldaring ircn (www.ebay.co.uk)

Table 9.20 show8 total cost of soldering iron each year.

Yoar Number of a$embletE Cost1

34

42

4o

!16e16L,tz€48

30

Page 34

10. Advertising costs

There are different methods to elevate and promote Oxycheck and SCUBA air

pressure warning system. Affer discussion with marketing director methods of

advertising were appointed. And also all the information regarding advertising is

gained from marketing department.

The following methods will be used through 5 years.

. Exhibitions

. Publications and magazines

. Leaflet

o Email

. Retaiting

. Website (lnternet)

Below is an estimated cost per year provided by marketing director.

10,'l lnitial advertising cost (Table 10.1)

Table 10.1: Initial adverlising cost

lnitial Advertising total cost = f524.48

10.2 Advertising cost for year I (Table 10,2)

Exhibitionsn NEC (Diving show) €180Exhibitionsn London (Oivino show) €250Advertisinon Divers maqazine €190Viroins Business broadband oDtion 1 e480Email throuoh BSAC (3000) Et80Oxvcheck website Free

Table 10.2: Advertising cost for year 1

Desktoo comDuter s380.00Web desion software (Microsoft FrontPaqe 2002)Software for qraphical desiqn (3D studio max) €54.99lllustratino with macromedia flash MX 2004 Nirtual Realitv) e 14.49

Total cost = €'1280

31

Page 35

Table 10.3: Advertising cost for year 2

Total cost = €'l370

10,4 Advoftbing cost for year 3 (Table 10,4)

10.3 Advertising cost for year 2 (Table 10.3)

Exhibitions in NEC (Divino show) ?210Exhibitions in London (Divinq show)Advertisino in Divers maoazine 8210Viroins Business broadband ogtion 1 e480Email throuqh BSAC (3000) e180Oxvcheck website Free

Exhibitions in NEC (Divinq show)Exhibitions in London (Divinq show) t320Adveriisinq in Divers maoazine t230Virqins Business broadband oDtion 1 e480Email throuoh BSAC (3000) e180Oxvcheck website F ree

Exhibitions in NEC (Divino show) t250Exhibitions in London (Divino show)Advertising in Divers maqazine 1230Viroins Business broadband oDtion 1 t480Email throuqh BSAC (6000) t380Oxvcheck wEbsite F reg

Exhibitions in NEC (Divinq show) e280Exhibiiions in London (Divinq show) €400Advedisino in Divers maqazine e250Virqins Business broadband option 1 e480Email throuqh BSAC (6000) €380Oxvcheck website Free

Table 10.6: Advertising cost for year 5

Table 10.4: Advsrtising cost frcr year 3

Total cost = €1440

10.5 Advertlsing cost for year 4 (Table '10,5)

Table {0.5: Advertising cost ior year 4

Total cost = e1700

10.6 Advertblng cost for year 5 (Table 10.6)

Total cost = !1790

32

Page 36

10.7 Summary of advertising cost (Table 10.7):

lnitial Costinq 8524.48Year 1 E1280Yeat 2 81370Year 3 L1440Year 4 e1700Year 5 e1790Total e8104.48

Table 10.7: Totai advertising cost

11 . Distribution cost

It includes packaging, postage internet purchasing service. The distribution is

concerned with the supply chains front-end or channels of distribution that are

dasigned to move the product.

After discussion with marketing director, it was decided that the product would be

sold and digtributed through retailers and internet (direct selling). Oxychock

predicts that a 40% of the sales will be through the retailers.

One of the most popular melhods of selling and purchasing on Internet is PayPal.

PayPal is an e-commerce busingss allowing payments and mongy transfers to

bo made through the Internat. Therefore the Paypal service charge for the 60%

of direct salss will be as following:

11.1 Paypal service charge: 1.4 percent of retail pricepluse0.20 per

transaction.

Members of the Oxycheck (director) agreed on the retail price which is e122.

Paypal service fee = 1.4Vo xt122 + 10.2

Therefore:

The total cost for Paypal service = e 1.708 r e0.2 = e1 .908 per unit

33

Page 37

The cost of Paypal service throughout five years is as foltowing (Tabte 11..1).

Year Unit sales perYear (60%)

Direct unit salesDer vear

Paypal servicefee

12

5

1450315073001280015200

8701890438076809120

t1,659.96t3,606.12€8,357.04t14,653.44e17,400.96

Table 11.1: Paypal service cost

Note: In order to help the company to cover the distribution cost, e6.SO postage

charge will be added to the retail price oithe product.

Packaging cost:

. Vvlite postal boxes (200mm x 140mm x 75mm)

. 50 boxes for !14.30

. Bubble wrapping - large roll (50 meters roll) covering 60 packages for

e19.04

Therobre packaging cost will be figursd out as followingl

Boxes = €414.7

Bubble wrapping = €460.1

Total packaging cost for year I = e874.8

Postage cost:

Standard parcel service cost up lo 1Kg is e3.85 and up to 1oKg is el i.45.

Therefore an average postage cost of 92.60 wilt be applied per unit.

11.2 Distribution co6t in year 1 (Table 11.2)

Paypal service charqe I t ,659.96Packaqino €874.8Postage 83,770Total €6,304.76

Table 11.2: Distribution cost in vear 1

Page 38

'11.3 Distribution cost in year2 (Table tl.3)

Table ,t1.3: Distribution cosl in vear 2

I1,4 Distribution eost ii year 3 (Table lt.4)

Table 1'1,4: Oistribution cost in year 3

11.5 Dlstributlon co.t In year4 (Tabte 11.5)

Table tt.5: Distribution cost in year 4

11.5 Distrlbution cost in year 5:

Table 11.6: Distribution cost in yeai 5

Paypal s€rvice charqe €3,606.12Packaging t1,900.5Postage e8,190Total €13,696.62

Paypal service charoe e8,357.04Packaoino E1,494.3Postage €18,980Total Q31,741.34

Paypal service cha&e € 14,653.44PackaqinoPoEtag6 €33,280Total f55,650.14

Paypal servi@ chame €17,400.96Packaqinq 89,170.7Postage €39,520Total €66.091.66

35

Page 39

12. Retail of product

The future of any company including Oxycheck is deeply depends on its total

proUt per year. Oxycheck will have a large and proUtable market as the SCUBA

air pressure warning system will be cheaper and more competent comparing to

its similar products.

After meeting between directors and consulting with all the members of the

Oxycheck and considering cost of prcduction, distribution, salaries it was decided

that the most reasonable price with sufficient profit is !t22.

At the following table cost of sales is calculated against expenditures.

As directors are the main investors in the company and their salaries increase

when sales increase their salary will not be deduced from the profit.

Total profits can be gained from following formulas (Table 12.'1):

lt is estimated that 1.7o/o of the retail price will form the fixed overhead costs.

Sales = Predicted unit sales per year x €122

Net profits = sales - costs (1 .7o/o of ."-tail price for fixed overheads each year,

production, wages, distribution, and etc)

Year Sales Product andDistribution

cost

Wages, salaries(without Directors

salaries)

1.7o/o olretail price

Profit peryear

12

45

f 176,900e384,300t890,600

e 1,56'1,600e1.854.400

L107,224.76t232,936.621539,821.00e946,536.14

El.124.O11.66

r0!53,820€59,600E98,202

t153.348

€3,007.30e6,533.10El5,140.20t26,547.20t31.524.80

166,667.94e91,010.281276,038.80€490,314.66€545,515.54

Table 12.'l: Total protit per year

36

Page 40

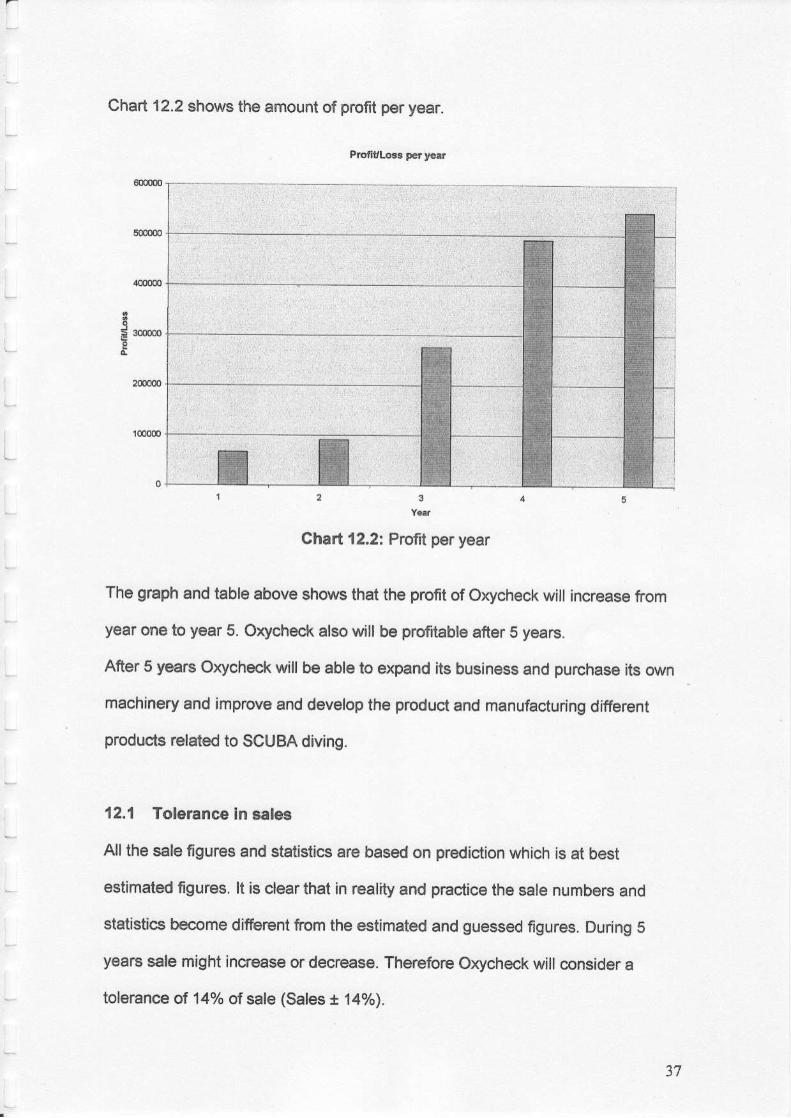

Chart 12.2 shows the amount of profit per year.

F 300000

Chart 12,2: ProJit per year

The graph and table above shows that the profit of Oxycheck will increase from

year one to yoar 5. Oxycheck also will be profitable after 5 years.

After 5 years Oxycheck will be able to expand its business and purchass its own

machinery and improve and develop the product and manufacturing different

producis related to SCUBA diving.

12.'l Toleranco in sales

All the sale figures and statistics are based on prediction which is at best

estimated figures. lt is clear that in reality and practice the sale numbers and

statistics become different from the estimaled and guessed figures. During 5

years sale might increase or decrease. Therefore Oxycheck will consider a

tolerance of 14% of sale (Sales i '14%).

37

Page 41

r

The table below shows figures when sales are 14olo above the predicted sares.

As it was told in section 5.2, extra products will be manufactured within 5 years in

order to compensale lhe lack of product lvfien the sales are above the predicted

figures (Table 12.3).

Year Sales + 14% ofgales

Expenditures Profit per year

1

4c

€201,666E458,'tO2

t1,o15,28481,780,22422.114.016

t110,232.068293,289.72€614,561.20

t 1 ,071 ,285.34t1.308.884.46

891,433.94E144,812.288400,722.80e708,938.66e805.131.54

Table 12.3: Profit p€r year (+14%)

Chart 12.4 shows proft per year.

Chatt 12.4t Profit per year (Sales +147o of sal6s)

lf the sales are less than 14% of predicted tigures then Oxycheck will require an

emergency plan to cope with the reduction in sales.

I

38

Page 42

The table below sho./s that Oxycheck will make profit afrer reduction in sales.

Therefore Oxycheck will plan to reduce purchase of components and employ

fewer labours than predicted figures and also Oxycheck will plan to stop rne

expansion of the company temporarily. Bonowing money from bank is one of the

policies which Orycheck will consider (Tabte 12.5).

Year Sale3 - 14% ofsales

Exp€nditures Proflt per year

'l

45

8152,134t330,498e765,916

81,342,97621.594.784

8110,232.06E293,289.72€614,561.20

E1 ,O71 ,285.34e1.308.884.46

[41,901.94837,208.28

€151,354,80€271,690.66€285.899.54

Table 12.5: Profit per yaar C14olo)

Chart 12.6 shows prof( per y6ar.

I

Chad'12.6: Protit per year (Sales -14% of sales)

39

Page 43

Chart 12.5 compares three different estimated protits in S years.

Pbtn/Los.lmm.ry

@

Chart 12.5: Profit Summary

13. Taxes andbusiness rafes

There are two types of tax that Oxycheck will pay to government. They are called

VAT and business rates.

13.1 VAT

Value Added Tax, or VAT, is a tax that applies to most business transactions that

involve the transfer of goods or sorvices. There are three rates of VAT in the UK:

17.5% (the "standard" rate), 5% ("reduced" rate) and 0% ("zero" rate). The

standard VAT rate is 17.5% which Oxycheck will pay in standard rate (17.S%). Atl

businesses whose taxable tumover is close to lhe current VAT thresholds which

is e61,000 will require registering for VATz.

22. Online source - htF/news.bbc.co !ld1lhilbusjnesE2965814 srrn ({61ooo)

I*

40

Page 44

This means that whenever the company sells or buys anything the business will

have to charge VAT on s€les, and keep proper VAT records on incoming and

outgoing transactions and pay VAT to HM Revenue & Customs (HMRC)

The SCUBA air pressur€ waming system is identi{ied as a taxable business. This

means that when the turnover reaches to the VAT thresholds of €61,OOO then a

17.5% of the products sold will be taken as a charge. A business will pay VAT on

their purchase, which is called input tax, and charge VAT on its sales, which is

called outDut tax.

lf a VAT-registered business charges more oulput tax on ssles than it pays in

input tax on purchases, it must pay the difference to HM Revenue & Cusroms

(HMRC). lf more input tax has baen paid than output tax charged, HMRC will

refund the difference. Oxycheck has predicted that input tax will be lower than

output tax. Therefors 17.5% charge will be issued on the SCUBA air pressure

warning systsm. Orycheck tumover will not reach the required €61,OOO until year

2. At the end of year 2, the input and output will be anticipated and calculated to

specify the amount which will be returnsd to Oxycheck. Oxycheck will predict that

almost 4.5% of the profit will not be retuned and it will be considered as loss. And

the rest of that which is 13% will be retumed to the company because of Inpur

tax. Table '13.1 shows summary of VAT per year.

Year VAT (4.5 % of sal6)12

4b

e17,293.50E40,O77.O0870,272.00€83.448.00

Table 13.1: VAT summary

41

Page 45

13.2 Business rates

Business rates (non-domestic rates) are charged on all businesses according to

the rateable value of the property. Rates are normally paid by the occupier of a

business - usually this is the owner-occupier or leaseholder.

lf the property is empty, the owner or leaseholder will be liable. Every busrness,

unless it is exempt, has a rateable valua ofthe property. The Council calculates

the raie bill by multiplying rateable value of the property by the multiplier set each

year by the government" For 2007-2008, the multiplier is set at 44.4 pence 13 ,

For the tirct property the rate is = t'utolo*oo =aar.ru

For the new propedy in year 5 the ra," t" = r5111}*0444p =€189.,j.1

14. Available types of finance sources

For Ox.ycheck and atl the companies the sources of finance is lmportant.

Especially year 1 is a crltical year for Oxycheck. Oxycheck will need money ro

cover all the expenditures, Allhough Sales play a major role in covering lhe costs

and supporting Oxycheck but Oxycheck will require other different finanqar

sourcas to cover the initial costs such as mould mst, hardware and software and

etc.

23. Odine solrce - htpi//wvwv.tandidge.gov.utdBusiness/busi.essrates/businessrates2O0Z.hlm

42

Page 46

14.'l Directorrs finance contribution

In partnership companies direc{ors are the main shareholders of the company

and committed to the compsny. Therefore in Oxycheck all directors will invest

and contibute e6,000 in the company. Direc{or's investment will be increased

aach year as the sal6s increase each year (Section 7).

14,2 Bank Loans

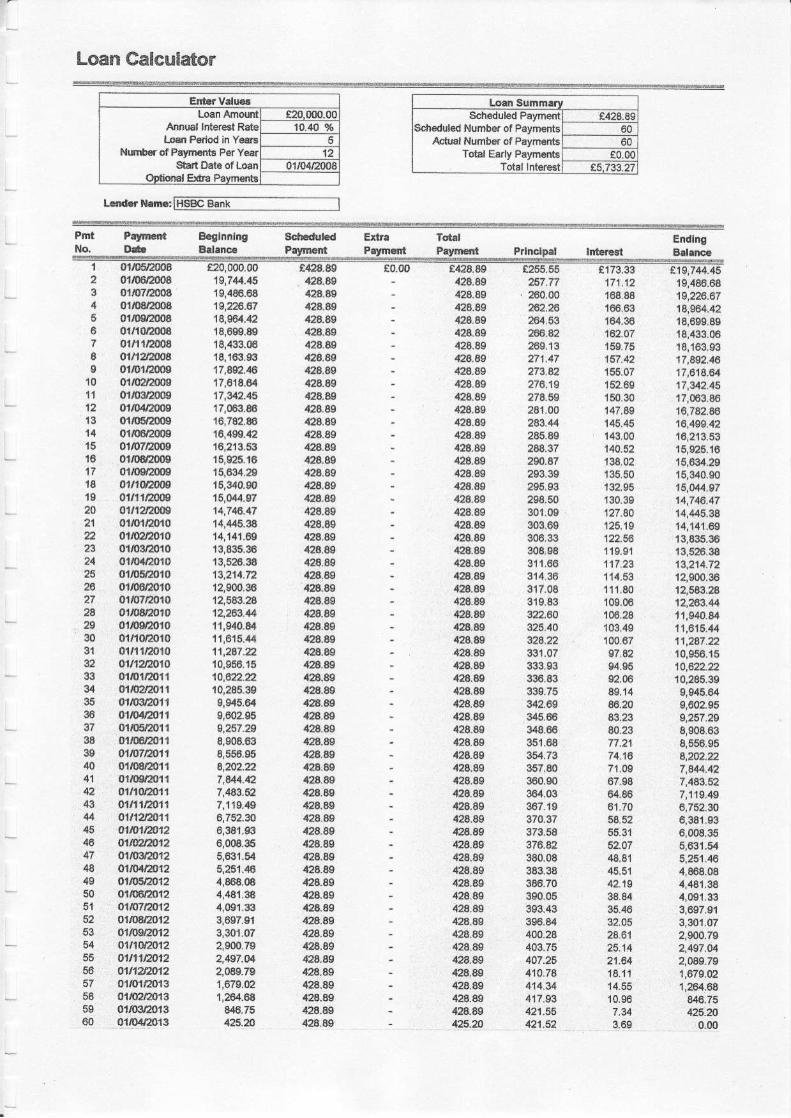

Bank loan is one of lhe financ€ sources which Oxycheck will use. Oxycheck will

take !20,000 from HSBC business loan package with agreed interast rate of

'10,4yo. This package is a small business loan and th6 details ofthe loan are

explained as following u:

Small Buslnos8 Loans AIR%€ l,000 to e4,999€5,000 to e14,999815.000 to €25.000

10.9 - 17.97.9 - 14.96.9 - 13.9

14.3 Overdraft"

Many companios have the need external finance in terms of tinance to secure

the company in short-lerm but not necesssrily on a long-torm basis. A company

might have small cash flo problems from time to time but such probtems don,t

call ior the need for a formal long-term loan. Undsr these circumstances, a

company will ofien go to its bank and anange an overdrafr.

25,

Online 6dlrc6 - httpsJtu/ww.h3bc.co.utd1plbrrsiness/filanc+bofiowino/bi]siness-loan:Jsesslond-0000LHZcstrnTGb0t6E3bbcv041 q.i 2ntf 16atOnlihe sourc€ - hltp//M-bEed.co.uMearn/acc.untinsffnan.ial&urces/overdranJis

43

Page 47

14.4 Gnnts

Grants can be an atractive aspect of a company's financing struc{ure. lf a

company has a sp€cmc issue lhal it wanls or needs to deal with then il could find

that there are grants available from local councits and other bodies that will helD

to pay for il%.

14.5 Venture Capnal

Venture Capital has becomg one of important source of finance market ovsr me

last 10 to 15 years. Venture Capitalcan be d€fined as capital contributed at an

early stage in the developmant of a n6w enterprise, which may have a significant

chanc€ of failure but also a significant chanco of providing above average raturns

and esp€cially where the provider of the capital expects to hav6 some influence

over the diGction of the enterprise. Venture Capital c€n be a high risk strategy rT.

14,8 Bu3ine$ angel flnanca

An angel invsstor or angel (known as a business angel in Europe), is an afflu€nt

individual who provides capital for a businsss slarl-up, usually in exchange for

convertible debt or ownership equity. A small but increasing number of ang6l

investors organize themselves into angel groups or angel networks to share

research and pool their investment capital':3.

frlne Bourc€ - htlpr 4r\,w.bized.co-uMsam/eccountingltinancial/sources/grents.htmOnlhesource - htpl,\dwwbized,co.ul4eafit6c@ungnCffDanciaUsources/index,hhOnfi ne surce - httpr//en.wikip€dia.orgnrvikj/Angeljnvestor

24.27.28.

44

Page 48

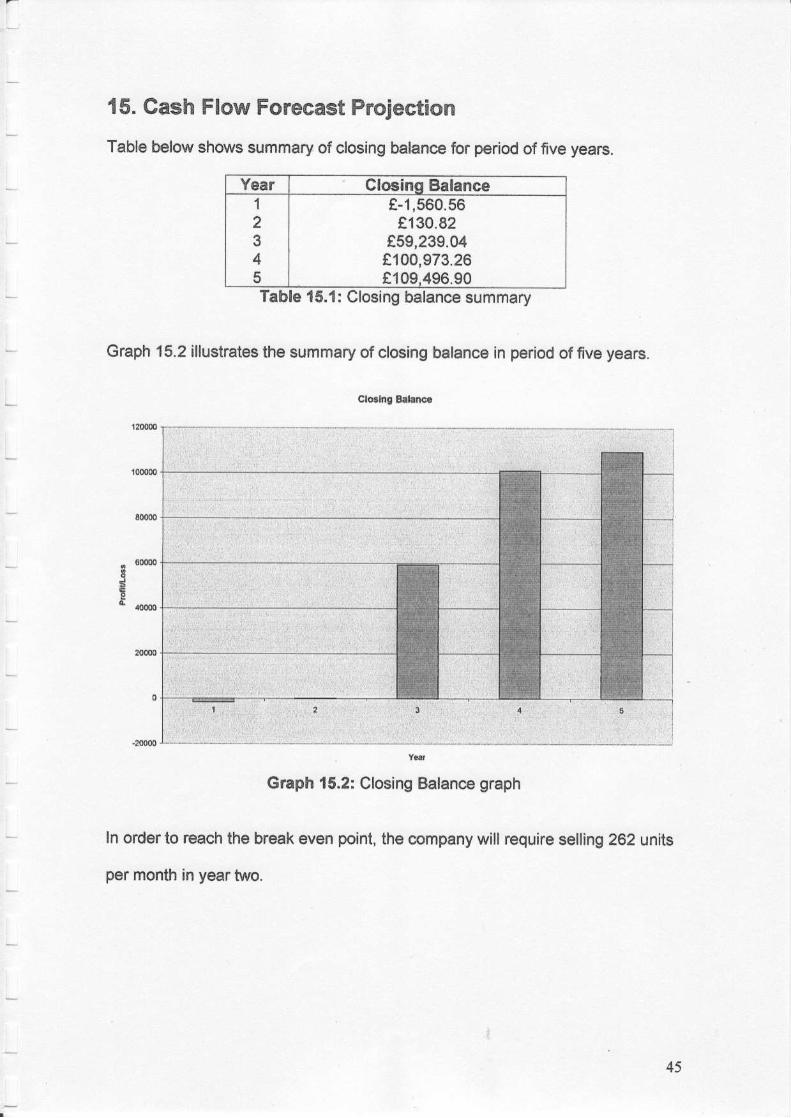

Table below shows summary of closing balance for period of five years.

Year Closinq Balance1

5

€-1,560.56e130.82

e59,239.04e100,973.26e109.496.90

Table 15.1: Closing balance summary

Graph 15.2 illustrates the summary of closing balance in period of five years.

15. Cash Flow Forecast Projection

i

Graph 15.2: Closing Balance graph

In order to reach the break even point, the mmpany will require selling 262 units

per month in year two.

45

Page 49

I

!|dlr.r F. (ufi)r !,lo

roflmcoaia IFC.v|rLlC.aFrurr \€U tla|.o?lbar.llnl aPu.

Arr-Evrt M F.l. al7lll4

hrrralEP (ur) r IFC'(SPUVCU)ECP {el) ' 8€P (u{.) r sPU

l|.

Page 50

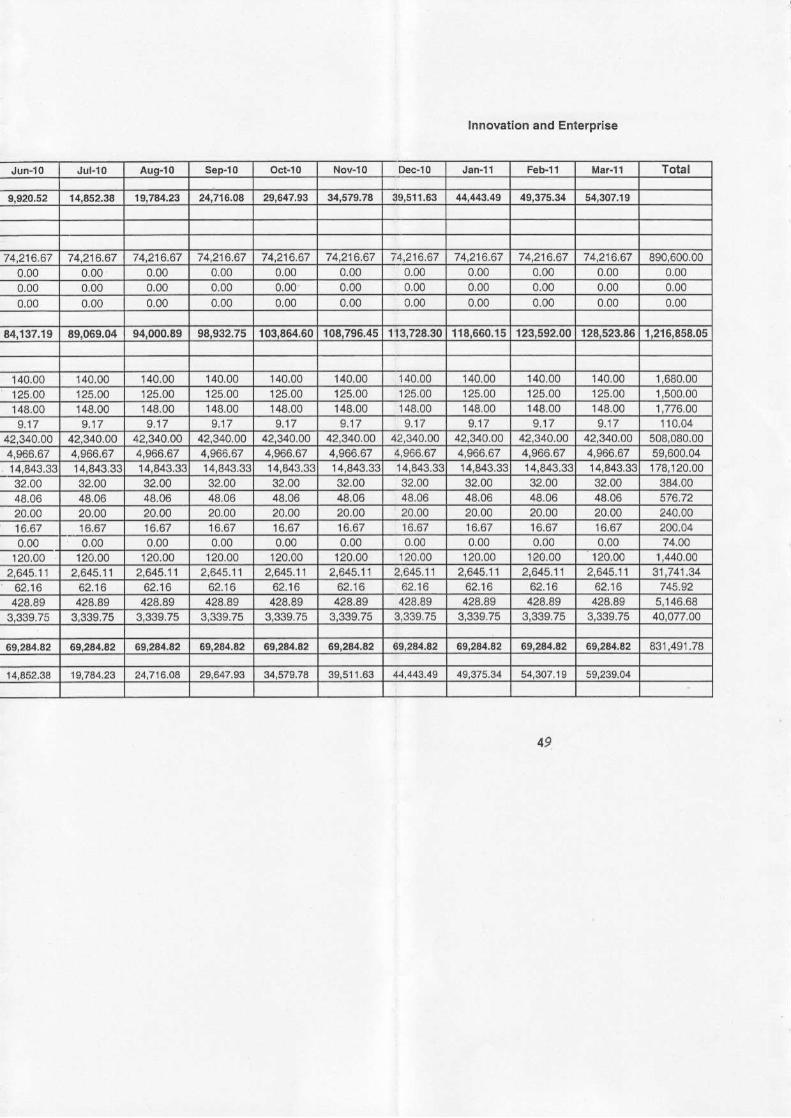

cash Flow Forecasl for Orycheck

UnltoltEu6s $. in UK.lerlr.q {E)

Flnancial year comencing lrom April2008

Inlrlalco3rlnle. Fent (lncl. Feoakrnd Mel

ComDon6nl. and iral.rl.l.S.l.rl.. (lncl, PAYE/N

Ulllhv Blll. (El.clrlc

Total Expendltur€

'14,741.67

0.00

n31,33

0,00

0,00

85.00

4,410.000,00

5,159.s8

37.50

97,80

0.00

15.41

106.67525,400.00

424,49

-274.25

Yashar Kh8tlb Sh6hldl

Page 51

hnovatlon ahd Enterpdse

Total

,560.10 -703.02 445,94 n,13t.79

14,741.67 14.741.67 14,741.67 14,741,67 14,741_67'14.741,67 176.S00,000.00 0.00 0,00 0.00 000 0.00 0.00 0,00 0.00 0.000_00 0,00 0,00 0.00 0.00 0.00 0.00 0.00 0.00 20,000.000,00 0,00 0.00 0.00 0.00 0.00 0.00 0,00 0.00 0,00

1 .42 14,324.49 14.181.57 14.038,65 13,69s.72 13.752,80 13,609.66 13.466.95 13.324.03 195.392,30

0.00 0.00 0.00 0.00 0.00 0.00 0,00 0,00 0.00 0,000.00 0.00 0,00 0,00 0,00 0.00 0,00 0,00 0,00 0.0085.00 85,00 85,00 85.00 85.00 6500 85.00 85.00 85.00 1,020,0037_50 37,50 37.50 37.50 37,50 37.50 37,50 37.50 37.50 450,00410,00 8,410.00 8,410,00 8,410,00 8,410 o0 8,410,00 8,410,00 8,410.00 8,410,00 100,920.000,00 0,00 0.00 0.00 000 0,00 0,00 0.00 0.00 0.00

5,159.56 5,159.58 5,150,58 5.159,54 5.159,58 5,r59.58 5,159.58 5,159,58 5,159,58 61,915.000,00 0,00 0.00 0.00 0,00 0.00 0,00 0,00 0.00 0.00E7.84 s7.80 97,80 97,80 97.60 97,80 97,80 97.60 s7,80 1,173.6018.33 18,33 18.33 r8.33 18.33 18.33 18,33 18,33 18.33 219.9615,42 15.42 '15.42 15,42 15,42 '15,42 15.42 15,42 15,42 185.04

0,00 0,00 0.00 0.00 0.00 0.00 0.00 o,0o 25,321,0010€,67 106.67 106,67 106.67 106,67 106,67 106,67 106,67 106.67 1,804,52525,40 525,40 525.40 525.40 525.40 525.40 525,40 525.40 525,40 5.304,76

0o 0,00 0.00 0,00 0,00 0.00 0.00 0,00 o.0o 0.00424,49 428,89 428.89 428.89 428.89 428,89 428.89 428.89 428.89 5 146,680,00 0.00 0,00 0.00 0,00 0.00 0,00 0,00 0.00 0,00

59 i4,86:t.59 14,864,59 14J44.59 14,3€4,59 t4.t3't,50 14,364.5t1 1'1,864,59 204,.|60,56

-560.10 n,131.79 ,1,560 56

4V

Page 52

Cash Flow Forecast for Oxvcheck

Year 2 Flnancialyear comencing lrom April2009

Unit ol fguc..re in U( cl.rllng (f)

Yashar Khalib Shahldi

0.00

114.16

140.00125.00120.0030.00

18,270.00

5,284.1332.0080.3018.33105.410.00

0.000.00

141.3962.16428.89

340,33

.00

.69

Toralcash av.lhble

lnl t la lcoEtln, F€pak and Me

Slllrl€s ilncl. PAYE/NI

Hardwaro and Sottwa.r

Cloalnq Balrnc6

Page 53

Innovation and Ente$ se

Tolal

1,193,21 -1,0,16.10 398,98 -751.37 .604.75 457,64 -310,52 -163,41 n6,29

32,025.0032,025.0032.025.0032,425.00 32 025.00 32,02s.0032.025.0032,025.0032,025.0032,025.00384,300.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

684.67 30,631.79 30.978.90 31.126.0231,273.1331,420.25 31,567.36 31.714.48 31.861.5932.008.71374,468.87

140.00 140.00 140 00 140.00 140.00 140.00 140.00 140.00 140.00 140.00 1,680.00125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 1,500.00120.00 120.00 120.00 120.00 120.00 120.00 r20.00 120.00 120.00 120.00 1,440.0030.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 360.00

18,270,0018,270.0018,270.0018,270.0018,270.4O 18,270.001A,27A.OA18.270.0018.270.0014.270.00219.240.004,485.00 4,485.00 4,485.00 4 485.00 .1,485.00 4,485.00 4.485.00 4,485.00 4,485.00 53,820.00

5,244.1 5,2U.1 5.284.13 5.284.13 5,284.13 5,284.13 5,284.13 5.284.1 5,284.1e 5,284.13 63,409.5032.00 32.00 32.00 32.00 32.00 32.00 32.00 32.00 32.00 32.00 384.0080.30 80.30 80.30 80.30 80.30 80.30 80.30 80.30 80.30 80.30 9€3.6018.33 18.33 18.33 18.33 18.33 18.33 18.33 18.33 18.33 18.33 219.96105.41 105.41 105.41 105.41 105.41 105.41 105.41 105.41 10s.41 r05.41 1.264.920.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 74.00

114.16 r 14.16 114.16 114.16 114.16 114.16 114.16 114.16 114.16 114.16 1.369.921.141.39 1,141.39 1.141.39 1,141.39 1,141.39 1.141.39 1.141.39 1,141.39 1,141.39 1 141 39 13,696.6262.16 62.16 62.16 62.16 62.16 62.16 62.15 62.16 62.16 62.16 745.92428.89 428.49 428.89 428.89 428.89 428.89 428.89 428.89 428.89 428 89 5.146.58441 1,441.13 1.441.13 1,441.13 1,441.13 1.441.13 1,441.13 1,441.13 1,441 13 1441.13 17,293.50

3i.a77.ag 31,62t,69 91,877,89 31.877,60 31,4t ,8S 51.877.09 31,8?7.89 31,877,89 31.8?7.89 31.677,89 382,608.62

n,193.21 -1,046.10 .698,98 -741,47 404.75 .457.64 .310.52 -163,41 '16,29 134,e2

4t

Page 54

Cash Flow Forecast for Oxycheck

Year 3 Financial year comencing lrom April 2010

Unir ol flgures ars In UKsterllng(f)

Ya6har Khatlb Shahldl

74,216.670.000.000.00

205.34

140.00125.00148.00

340.004 966.67

32.00

16.670.00

120.00

62.15428.89

20.0048.06

lnhlalCo€l lnFenl l lncl . Bsoalr .nd M.

NCI, PAYFJNI

Ulllltv Blllr

Closlnq Balance

Page 55

lnnovalion and Enterprise

Jul-l0

14.852.38 19,704,23 24,716,04 29,U7,93 34,579,74 i,s11.63 44,443,49 49,375.34 s4.307,19

74,216.67 74.216.67 74,216.67 74,216.67 74,216.67 74,216.67 74,216.67 74,216.67 74.216.67 890,60000000 0.00 0.00 0.00 0.00 000 000 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 000 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 000 000 000 0.00 0.00 0.00 0.00

137.19 89,069.04 9{,000.E998,932.75 103,86460 108.796.451t.728.30118.660.15123,592.00128.523.861.216.856.05

140.00 1.10.00 140.00 140.00 140 00 140 Cro 40 00 140.00 140.00 140.00 1.680.00125.00 125.00 125.00 125.00 125 00 125 o0 25 00 125.00 125.00 125.00 1,500.00148.00 148.00 148.00 148.00 148 00 r 48.Cro 4€.00 148.00 148.00 148.00 1,776.009.17 9.17 9.17 Li7 917 917 9.17 9.17 9.17 110.04

42,340.0042,340.0042.340.0042.340.0042,340 00 42.340 00 4.340.0042.340.0042,340.0042,340.00508,080.00.67 4,9€6.67 4,966.67 4,966.67 4.667 4.9€6 67 €66.67 4,966.67 4,966.67 4,966.67 59.60004

14.843.3! 14,843.33 14,843.33 14,843 33 14.843.33 4 843.33 14.843.33 14.843.3! 14,8€.33 178,120 0032.00 32.00 32.00 32.00 32.00 32 00 32 00 32.00 32.00 32.00 384.0048.06 48.06 48.00 48.06 48.0€ 48 06 48 06 48.06 48.06 48.0620.00 20.00 20.00 20.00 20.00 20@ 20 00 20.00 20.00 20.00 240.0016.67 16.67 15.67 1€.67 16,67 16 67 16.67 16.67 16.67 16.67 200.040.00 0.00 0.00 0.00 0.00 000 000 0.00 0.00 0.00 74.00

120.00 120.00 120.00 120.00 120.00 120 @ r2000 120.00 120.00 120.00 1,440.002 11 2,645.11 2.645.11 2,645.11 2.645 1r 2,6/511 i645.11 2,645.11 2.64ti.11 2.645.11 31.741.34

62.16 62.16 62.16 62.16 62.16 6216 62.16 62.16 745.92428.89 428.89 428.89 428.89 428.89 428 89 r28.69 428.89 424.49 428.89 5.146.68

3 75 3,339.75 3,339.75 3.339.75 3,339 75 3.339 75 :339 75 3,339.75 3,339.75 3,339.75 40.077.00

244.42 69,244.82 69,244,42 49,244,62 69.284.82 59.244.42 0,23:1.82 69,284.62 69,264.82 6t,284,42 831,491.78

14,852.38 10,744,23 24,716,6 2e,647,93 34,579.73 39 5l l 63 40,375,34 54,307.1959,239,0,t

49

Page 56

Innovation and Enlerprise

14.852.38 19.744,23 24,7i6,08 29,647.93 34,579.74 33,511.63 49,375.34 54,307,i9

74,21667 74.216.67 74,216.67 74,216.67 74,216.67 74,216.67 74,214.67 74,216.67 74,216.67 74,216,67 890,600.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0_00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 000 0.00

137.19 E9.069.04 94.000.89 94.932.75 103,664.6010E,796,45113,728.30118,660.t5123,592,00128.523.861.216.65€.05

140.00 140.00 140.00 140.00 140.00 140.00 140.00 140.00 140.00 140.00 1,680.00125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.00 1.500.00148.00 148.00 148.00 148.00 148.00 148.00 148.00 148.00 148.00 1.1800 1,776 009.17 9.17 9.17 9.17 9.17 9.17 9.17 9.17 9.17 9.17 110.04340.00 42,UO.AO 42,340.0042.340.0042.340.4O42.340 00 42 340.00 42.340.40 42.340.0042,340.00 508.080.00

4,966.67 4.966.67 4,966.67 4,966.67 4,966.67 4,966.67 4.966.67 .1.966.67 4,966.67 4,966.67 59,600.0433 14,843.33 14.843.33 14.843.33 14,843.33 14,843.33 r4.843.33 14.843.3314.843.3314.843.33178.120.00

32.00 32.00 32.40 32.00 32.00 32.00 32.00 32.00 32.00 32.00 384.0048.06 48.06 48.06 48.06 48.06 48.06 48.06 48.06 48.06 48.06 576.7220.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 240.00'16.67 16.67 16.67 15 67 16.67 16.67 16.67 16.67 16.67 16.67 200.040.00 0.00 0.00 0.00 0.00 0.00 000 0.00 0.00 0.00 74 00

120.00 120.40 120.00 120.00 120.00 120.00 120.00 120.00 120.00 120.00 1 .440 002.645.11 2.6/15.11 2.645.11 2.645.11 2,645.11 2,645.11 2,645.11 2,645.11 2,645.11 2 645.11 31,741.34

62.16 52.16 62.16 62.16 62.16 62.16 62.16 52.16 62.16 745.92428.89 428.89 42a.A9 428 89 428.89 42S.89 428.89 428.89 428.89 428.89 5,146 68

3,339.75 3.339.75 3.339.75 3.339.75 3,339 75 3,339.75 3,339.75 3,339.75 3.339.75 40,077.00

69,284,82 64,264,42 69,264,82 69.284,82 69,264.62 68,264,62 69,284.82 69,284.82 6s,29r.82 69,284,82 831,491.78

14,852,3819,744_23 24,716.06 29,647,93 34,579,78 30,511.63 49,375.34 s4,307.19 53,239.04

49

Page 57

Cash Flow Forecasl lor Oxycheck

Unil orfgurc. ar€ In UK 6terllng (E)

Financial y€ar comencing frorh Aprll20l1

0.000.00

0.00

742.39

130,133.33

140.00125.00220.009.17

141.67

74,240.008,183.5032,533.3332.000.0020.0019.580.00

62.16428.89

l€l B€nt {lncl.Prop€ l€l B€nt (lncl. A€palr md Mrlnlena

sal.rl.. (ncl. PAYE/N

Ulllltv Blll!

Tolel ExD€ndlturs

Ya3har Khatlb Shahldl

Page 58

Innovation and EnterDdse

Jul-1i Total

133,08 69.617.10 73.101.11 76.545.13 80,069,15 83,553.17 87,037,19 90,521.21 s4,oo5,22 97,489.24

133.33130.133.33130.133 33 130.133.33130,133.33130,133.33130,133.33130,133.33130,133.33130,133.331,561,600.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

96.256.41't99,750.43203.234.45206,718,47210,202.44213.566.50217.170.52220,654,54224.138.56227,622.5A2.501,599,69

140.00 140.00 1.10.00 140.00 140.00 140.00 140.00 140.00 140.00 140.00 1,680.00125.00 125.00 125.00 125.00 125.00 125.00 125.00 125.40 125.00 125.00 1,500.00220.40 220.O0 220_40 220.O0 220.44 220.00 220.4O 220.40 22A.OO 220.4O 2 640.009.17 9.17 9.17 9.17 9.17 9.17 9.17 9.17 9.17 110.04

7 00 74,240.@ 74.240.40 74.240.0074,240 00 74.240.0474.240.0O 74,240.4O 74,240 00 74,240.40 890.880.008,183.50 8,183.50 8,183.50 8,183.50 8,183.50 8,183.50 8,183.50 8.183.50 8,183.50 8,183.50 98,202.00

32.533.3332.533.3332.533.3i 32,533.3332,533.3332.533.3! 32,533.3! 32,533.3332.533.3t390400.0032.00 32.40 32.00 32.00 32.00 32.00 32.00 32.00 32.00 32.00 384.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.0020.00 20.4o 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 240.0419.58 19.58 19.58 19.58 19.58 19.58 19.58 19.58 19.58 19.58 234.960.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 74.00

141.67 141.e7 141.67 141.67 ' t4 l .67 141.67 141.67 141.67 141.67 '141.67 1,700.044,638.01 4,638.01 4,638.01 4,638.01 4.638.01 4,638.01 4,638.01 4.638.01 4,638.01 4,638.01 55 656.14

62.16 62.16 62.16 62.16 62.16 62.16 52.16 62.16 62.16 62.16428 89 426.69 424.49 428.89 424.89 428.89 428.89 428.89 428.89 428.89 5.146.68

5,856.00 5,856.00 5,856.00 s,856.00 5,856.00 5,856.00 5,856.00 5.856.00 5,856.00 74,272.00

126,449,32 126.649,42 126,549,32126,649.32126,649,32126,649.32126,649.32126,640,32i26.649.32 1.519 865 78

69,617.10 73,101.r1 80,069.15 83,553,17 87,037,19 90,521,2194,005.22 s7,4e9 24 100,973 26

Page 59

Cash FIow Forecast lor Oxycheck

Financial year comencing from April 20'12

uK storllng (E)

Y$har Khatlb Shahldl

0.000_000.00

426.00208.00260.009.17

'149.17

88.160.0012,779.00

32.0039.73

19.580.00

20.00

5,507.64189.11428.E9

8,954.00

5.62

lnitial lnve6tmenl

lnltlal c06licrtlla Bent (lncl. Bspalrlnd l{t

Componlnts !nd Mtt.rl.l.s!larlc. (lncl. PAYE/NlOlf.ctor. Sala

comDutor Hardwars and sollwar.u{ tv Blllr (El

Tolal ExDendllur€

Closlno Balanca

Page 60

Innovalion and Enterprise

Junn2 Jul-12 Total

102,316,09103,033,81103,751.52104.459.23 105.136.94 1tts.904.65106,622.36 i07.3,q,.08 108,057.79108,7/5.50

s4.533.33t54 533.33154.533.33154.533.33i54,533.33 154,533.33154,533.33154.533.33154,533 33 154 533.33 1.454.400.000.00 0.00 0_00 0.00 0.00 0.00 0_00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0_00 0.00

25 257,567,14256,284.8525E.002.56259.720.27260.437.99261.1s5.70261.873.41262,591.12263.306.833,112.429.60

426.00 426.00 426.00 426.C4 426.4O 426.OO 42A.OO 426.00 426.00 426.00 5,112.00208.00 208.00 208.00 208.00 208.00 208.00 208.00 208.00 204.00 208.00 2.496.00260.00 260.00 260.00 260.00 260.00 260.00 260.00 260.00 260.00 260.00 3.120.009.17 9.17 9.17 9.17 9.17 9.17 9.17 g. l7 9.17 9.17 110.04160.00 88,160.00 88,160.00 88.160.00 88.160.00 88.160.00 88.160.00 88.160.00 88,160.00 88,160.001,057,92000

12.779.00 12.779.0O 12,779.0O '12.779.@ 12,779.4A 12.779.00 12.779.0O 12,77e.04 12,779.40 12.779.04 153.348.0038.633.3338.633.3i 38.633.33 38,633.33 38.633.3338,633 33 38,633.3338,633.33 38,633.333E.€33.3!463.600.0032.00 32.00 32.00 32.00 32.00 32.0O 32.00 32.00 32.00 32.00 s84.003€.73 3e.73 39.73 39.73 39.73 39.73 39.73 39.73 39.73 39.73 474.7620.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 240.0019.58 19.58 19.58 19.58 19.58 19.58 19.58 19.58 19.56 19.58 253.550.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 74,00

149.17 '149.17 '149.17 149.17 149.17 149.17 149.17 149.17 '119.17 149.17 1,790045.s07.64 5.507.64 5.507.64 5,547.44 5.507.64 5,507.64 5,507.64 5,507.44 5,507.64 5.507.64 66.09r.€6189.11 189.11 189.11 189.11 189.11 189.11 189.11 189.11 189.11 189.11 2.269.32424.89 428.89 424.49 42E.E9 42E E9 42A.89 12A.89 429.49 428.89 425.20 5,142.8S

0,954.00 6.954.00 6.954.00 6.954.00 6,954.00 6.954.00 6.954.00 6,954.00 6,954.00 6 954.00 83,448.00

153,615.62153,815,62153,815.62153.016,62t53,815,62 153.815,62153.415.62153,416,62153,8r5,62t5t.41t,93 1.845.876.36

81 103,751.52104,469.23 i05,188.94 105,904.55 106,622 35 107,3110 03 r08,057.79 10e,775,50109,406,90

5l

Page 62

Loan Calcul{or

Lodn AmdnlAnrud tnsest Ratl@n Pdiod in Y@6

Number of PaFnab P6r Y*rS_bn Oat6 of Loan

Ortio.al E (ha Pavrn€nt!

t20.0@_0c

5

01t04/2006

Scheduled P.ymentScn€dulsl Nuhb€r ol Paym.nls

]|tud Numb.r of PayndtsTotal Eeny Payheots

TotattnteBi

e428.0t6060

€0.00t5,733 27

L.id.r |{.m: IHSBC g.nk I

a.ghnlne Eftding

19,48it.6819,22A.O716,9€4.4218,60S.8S18,433.06'18,163.9'31?,892..1t117,A1A.64'17,u2.4517,063.$16,7A2.&O1A 4e9,4216213.5315,926.1015,$42915,340,0015,W.9714,744.4714,445.3t14,141.9913 035.3€13 526.3813,211.7212,000.3612,563.2412,233.4411,040.8111,415.1411,287.2210,e5€.1510,e22.2'r0,285.398,945.649.€02.954,257.2E8908.638,55€.958,2U1.27,A4!..427,483.527,119.496,752.30€,i41.936,008_355,631.545,251.404,8€8.0€4481.384,0e1.333 697.913,301.072,900.792,497.U2,089.791,679.t21,264.64

844.75425.20

0_00

123

56

I

1011

13

1516'1716192021

24252A2T2A2E303t323334

38373839

4243

4546

4a495l)

5253645556

5A5960

ol/o6t2{0a0,1/G/200801to7l?0@01rca|loo601DS/200e0trio20G8ot/ltazlo€olnuxwo1n1t2loool1q,t2o0o0'rollzuogoltwru0r05t?0@0r/u20@AMDW01/!8/20090lltBa2o@oll9tw01t11t2fi901A2t2@g01/0tt201001Mno1001109/?0100lparz'l00l/06/z1001/o6tu1001/0720100t/08/201001/oor20totxfl0r20t00tfit/20100u12m10o1n,|t 11o1@m11ollo?t?'11olMta110ro5r2o1101t8no1101B7t8l10110620|l0t/@t20r101t10t2o11o.'/11/2011uA2ta1101n1m12oltvt6r20t/!0t201201/0azo'1201to5t&120?06/201201Efta1201^'Bno1201x,ofn1201n0t4t12otA1I2Itl201t12t)o12t'10t,20130tiD/20t401nEAA1301nat413

e20,000.0019,74,1.15r9,406.€A19,223.67'16,9a1.4218,69e_8S18,433_!€18,1€3.s|17,8a2.817,€18_6417,U2!517,063.E016,782.6G16,490.4216,213.5316,r25.1015,634.2Q15,34090'15,044.9714,f!.€.1714,4:16.3814,141.0913,835.3613,52E.3013,214.7212,900.3412,583.2812,261.411,e44.411,415-4411,207_210,956.r510,ezz10,285_a09,945.649,602.a5s,267.25I,S08.638,550.954,202.27,444.127,443.527,119.&

6,381,906,008_355,631.545,251-,164,868.004,4€1.384,OS1.ia3697.913,301.072 900.792,49f-U2,089.791,679.021,264.64

446.75425.8

!424_8942A.AE424.89428.89428.89428_09428.8942E.89Qe.8g42s.89aa.u&a.aEa2a.8s424.€S&.aE120.4E428.S91N.8e426.&42€.6942E.60azB.891126.8942E.6e42A.AE48.aA426.68420.4944.AE424.89428.891?!,49/128.89{28.89428.89:r28.89428.894?'.@4?3,4e428,aSaza.8s2t28.89,i28.89:t28.lE12A.6912A.Ag428.49428.49126.4942d8S42439426.S9424.89,126.S9!?8.8942!.A9424_89424_@424.&942e.89

e428.€[email protected] _89428.8912A.AS/t28-89420_89428_49428,4012e.W120.A512A,aS42A.Ag428.E9428.8e428.89,r28.09428.09428.89424.89428.t0428.8e1A.OE428.89428.€[email protected] ,[email protected] €[email protected] ?6.69428.€012A.AS,126.80424.89426.40424.&428.S9428.89t24.e9428 8g428 S9124_89428.89428.89aa.a942A.89429.89424.894B.AS425_20

t255.55257,7?260.00262.28264,53266.62260.13271.47273.52276,19278.59281.00281.4285.€g288.37290.47293.3E295.93288.50301.09303.€990! 33308.08311 663r4.36317.08310.4332,40325.40326.?2331,07333,93336.83330.75342,69345.60348.66351.€8354.73357.803€0.903€4.033€7.19370.37373 58376.823€0.08383.34380.703S0.05393.43396.84400.28403.75407.254to.76

417.93421_56421.52

€173,33171.12168.88166.63164.36142 07150.75157.42155.07152.60150.30147.89145.45143.00140.4218 02135 !0132.95130.39127.80126.19122.8119.91117,23114.53111,80109.061c628103.49r00.67€7.8294.95s2,0489,14@,2483.2380.23f1.21741671.0e67 S664.8661.705t.5255.3152.0748,8145.5142.1938.8435 46

28.6125.1421.6418.1114.5510.96T.U3.69

t19,744.45.:.*

Page 63

t -

17. Bibliography

Expenditure information (2008), business diclionary.com lonline], cited 17thApril 2008, available from<htto:llwww. businessdictionarv.com/definition/variable-cost. htm l>

Premises information (2008), nattrassgites.com lonline], cited 17h April 2008,available from <http:/ /vww.nattrassqiles.com/property/300.pdf>

Insurance information (2008), business insure.co.uk lonline], cited lTth April2008 available from<httD:/,/!1./ww. businessinsure.co. uk/businegsinsuranceouotes 0O2.htm>

Insurance information (2008), insurance 4business.org.uk lonline], cited 17hApril 2008 available from<http://www. insurance4business. oro. u ldkevman. html>

lnsurance informalion (2008), coulsonpritchard.com lonlinel, cited 17h April2008 available from<htto://www.coulsonpritchard.com/businessinteruption.asp>

Rate of pay (2008), news bbc.co.uk [ontinel, cited 1/h April 2OOB avaitabtefrom <http://n€ws.bbc.co.uk/1/hi/business/642596S.61m>

Computer information (2008), sunitek.co.uk lontinel, cited 17h Aprit 2OOBavailable from <http://www.sunitek.co. uk/>

Software information (2006), amazon.co,uk [online], cited 18h April 2OO8available trom <htto:/ v\,vwamazon.coVersion/do/800005AF l0>

Sofrware information (2008), joumey edeurope.com lonline], cited 1Bm April2008 available from <www.iournevedeurooe.com>

Office equipment (2008), desk warehouse,co.uk lonlinel, cited j 8fr April 2OOEavailable from <htto://www.deskwarehouse.co. uUshoo/viewdetails.aso?oroduc D=624>

Office equipment (2008), brawn security.com lontine], cited 18th April 2OOgavailable from <htto://www. brawnsecurity.com/securitv. htmt>

Office equipment (2008), ebay.co.uk lonlinel, cited 18m Aprit 2OO8 avaitaDtefrom <b1!plut{4ry€bayEg_u!>

VAT informalion (2008), bbc.co.uk lonline], cited 1Bb Aprit 2OO8 avaitabte from<http:/news.bbc.co.uk/1/hi/busjness/2g66814.stm f€61 000)>

s1

Page 64

Business rate (2008), tandridge.gov.uk lonline], cited 18rh April 2008 availablefrom<http:/ /vww.tandridge.gov.uk/Business/businessratevbusinessrates2OOT.htm>

Loan information (2008), hsbc.co.uk lonline], cited tBm April 2008 available ftom<http://www. h sbc. co. u k>

Overdran inbrmation (2008), bizad.co.uk lonlinel, cited i 8th Aprit 2OO8 avaitablefrom <http:/ r\iw.bized.co.uk/learn/accounting/financial/sourcas/overdraft.htm>

Grant€ infcrmation (2008), biz€d.co.uk lonlinel, cited 1Bs Aprit 2OOA availabtefrom <http:/lwww.bized.co.uUlearn/acmunting/financial/sourcevgrants.htm>

Venture capital (2008), bized.co.uk lonlinel, cited l6thAprit 2OOE avaitabte from<http/wwwbized.co.uk/leam/accountingltinancial/sources/index. htm>

Business angel tinance (2008), wikipedia.ory lonlinel, cited i Elr Aprit 2OOBavailable from < http://en.wikipedia.org^^/iki/Angel_investor>

Break - Ev6n Analysis (200E), jwcs.us lontinel, cited 2nd May 2OOg aveilable from<http://jwcs. us/soft ware/BreakEvenTo2ocharVBr6ak-EvenTo2Ochart.xls>

5+