www.rti.org RTI International is a registered trademark and a trade name of Research Triangle Institute. Innovation Corridor Innovation and Economic Data Analysis Michael Hogan, Sara VanLear, Elizabeth Brown, Alison Bean, Joshua Fletcher and Sara Lawrence April 2020

Transcript

www.rti.orgRTI International is a registered trademark and a trade name of Research Triangle Institute.

Innovation Corridor Innovation and Economic Data Analysis

Michael Hogan, Sara VanLear, Elizabeth Brown, Alison Bean, Joshua Fletcher and Sara LawrenceApril 2020

The Innovation Corridor study includes four phases of research to develop ideas for transformative growth in NC over the next few decades. This Data Appendix represents PhaseI of RTI’s research: a summary of NC’s and the Innovation Corridor’s economic and innovation performance over the last decade.

Innovation Corridor Data Appendix Overview

Summary of Research Approach

Innovation and Economic Analysis

Qualitative Review of

KC’s Regional Needs

Targeted Industry and

Market Analysis

Blueprint for Innovation Corridor

Phase I

Summarized state and regional innovation

economy.

Developed economic and innovation profiles for the Corridor and the

four economic hubs.

Created this Data Appendix.

Phase II

Conducted exploratory interviews with stakeholders.

Ground-truthed Phase I findings, identified

emerging and cross-cutting innovation trends, and refined research outcomes.

Phase III

Determined industry sectors with high

potential for tech-driven growth and economic

opportunity.

Determined market size, potential, and capabilities

required for growth.

Phase IV

Conducted targeted interviews with stakeholders

in each economic hub. Assessed key investments

required to enhance “quality of place” to attract business

and talent.

Created blueprint for Innovation Corridor.

The Innovation Corridor Geography

RTI proposed an integrated Innovation Corridor from Winston-Salem to Greenville to expand the potential, opportunity, and impacts of an innovation economy across North Carolina. This corridor represents:

§ A diverse economic region with nearly 4.4 million residents and over $218 billion in economic output.

§ Economic activities that are integrated by commuting patterns and supply chain linkages.

§ Cities with geographic and economic diversity that provide a “test bed” for analyzing the types of investments that can transform growth in a range of regional contexts.

The Proposed Innovation CorridorThe study area is a continuous corridor including the combined statistical areas (CSAs) of

Greensboro-Winston-Salem-High Point, Raleigh-Durham-Chapel Hill, Rocky Mount-Wilson-Roanoke Rapids, and Greenville-Washington.

Source: U.S. Census Bureau, Combined Statistical Areas.

2. Economic Overview of North Carolina (Slides 16-29)a) Macroeconomic Indicators (17-18)b) Industry Composition and Trends (19-21)c) High-Tech Industry Trends (22-23)d) Innovation Performance (24-26)e) Jobs and Occupations Trends (27-29)

3. Understanding the Innovation Corridor (Slides 30-68)a) Population Summary (31-34)

i. Socioeconomic Trendsii. Economic Mobility

b) Commuting Patterns (35-36)c) Industry Makeup and Trends across Innovation

Corridor (37-42)i. Industry Trends: Greenville-Washington CSAii. Industry Trends: Rocky Mount-Wilson-Roanoke Rapids CSAiii. Industry Trends: Greensboro-Winston-Salem-High Point CSAiv. Industry Trends: Raleigh-Durham-Chapel Hill CSA

d) Jobs in High-Technology Industries (43-48)i. Jobs in High Tech in Industry Subsectors in KC CSAsii. Jobs in High Tech: Greenville-Washington CSAiii. Jobs in High Tech: Rocky Mount-Wilson-Roanoke Rapids

CSAiv. Jobs in High Tech: Greensboro-Winston-Salem-High Point

CSAv. Jobs in High Tech: Raleigh-Durham-Chapel Hill CSA

e) STEM Jobs (49-54)i. STEM Jobs: Occupations in KC CSAsii. STEM Jobs: Greenville-Washington CSAiii. STEM Jobs: Rocky Mount-Wilson-Roanoke Rapids CSAiv. STEM Jobs: Greensboro-Winston-Salem-High Point CSAv. STEM Jobs: Raleigh-Durham-Chapel Hill CSA

f) Talent Pipeline (55-56)i. Degrees Conferredii. Science and Engineering Degrees

g) Innovation Assets (57-68)i. Innovation Ecosystem Assets across KC CSAsii. Patents Granted in North Carolinaiii. Startup Capitaliv. R&D Expenditures and Licensing

4. Data Definitions and Limitations (Slides 69-73)

Appendix Table of Contents

Innovation and Economic Analysis: Overall Findings

North Carolina’s Economy and Industries

§ North Carolina’s population has grown by 11% over a 10-year period, yet economic growth as measured by gross domestic product (GDP) has not kept pace.– NC has recovered from the 2008–2009 recession, but the economy as a whole is

growing more slowly (36.9%) than the national average (39.3%).§ NC has seen an industry shift from manufacturing to a range of services

during the same time period.– Professional services, wholesale trade, and real estate rental and leasing grew the

most. – Manufacturing, the largest single contributor to GDP, grew by 24%, which is slower

than overall state growth (36.9%) and national manufacturing growth (30%). § The state’s high-technology industry is growing at twice the rate of the

national average.

North Carolina’s Jobs and Wages

§ There is growth in high-skilled, high-wage occupations, such as computer, financial, and health care jobs, and in highly skilled industries such as professional and technical services and finance. This growth is concentrated in the Research Triangle region.

§ Manufacturing job losses have affected Greensboro, Rocky Mount, and Greenville. These losses have had an indirect effect on job losses in transportation, warehousing, wholesale trade, and construction.

§ Some of the largest areas of employment, including accommodation and food services, retail, and some areas of health care, are seeing growth in low-wage jobs.

North Carolina’s Technology and Innovation Performance

§ Eight percent of jobs in North Carolina are in high-tech industries. High-tech jobs are growing at close to two times the national average, but they tend to pay less than the national average for high-tech jobs.

§ Compared with national and regional peers, the state has risen quickly in the ranks of research and development (R&D) expenditures, patenting, SBIR funding, and STEM and high-tech jobs.

§ Venture capital per $1 million of GDP in the state had risen in total value to $875 in 2018 (from $567 in 2010), but relative performance is flat with a steady ranking of 12th over the 10-year period.

Innovation Corridor’s Economy and Industries

The region has recovered from its pre-recession peak of over 1.4 million jobs, with a net job growth of 8% between 2008 and 2018. The fastest growing job segments were leisure and hospitality (27% growth) and professional and business services (20% growth).

Over the same period, manufacturing jobs in the region declined by 12% compared with an 8% decline for the state.

Economic output for the Innovation Corridor is $218 billion. The region has over 1.6 million private-sector jobs with most employment in:

§ Trade, transportation, and utilities (21%) § Education and health services (18%)§ Professional and business services (18%)

The Innovation Corridor is a region of extremes. For example population ranges from 2.2 million in the Raleigh-Durham-Chapel Hill CSA to 226,000 in the Greenville-Washington CSA, and the poverty rate is 12% and 25% respectively in these two CSAs.

Growth Is Concentrated in Raleigh-Durham

Since 2008, the growth in the Innovation Corridor has been highly concentrated in the Research Triangle region (Raleigh and Durham-Chapel Hill metropolitan statistical areas [MSAs]). It has a fast-growing and highly diversified high-tech sector.

From 2008 through 2018, the region grew by 132,000 private-sector jobs (19%), while the remaining regions saw flat or negative job growth.

In 2018, within the Innovation Corridor, the Raleigh-Durham-Chapel Hill CSA had: § 52% of all jobs§ 70% of science and engineering degrees conferred§ 74% of all jobs in high-tech industries§ 78% of STEM jobs

Raleigh and Durham-Chapel Hill MSAs

Innovation Corridor’s Jobs and Wages

§ STEM jobs in the Innovation Corridor are highly concentrated and growing in the Triangle region. The Raleigh-Durham-Chapel Hill CSA has 38% of the STEM occupations in the state and 78% of STEM jobs in the Innovation Corridor. The majority of STEM jobs in the region are in computer science.

§ The Piedmont Triad (Greensboro-Winston-Salem-High Point CSA) benefits from a core of headquarters and management, but high-tech growth is occurring in smaller emerging sectors, including professional services and aerospace manufacturing. – Major corporate headquarters contribute many jobs, but the management sector is declining

slowly in the region. § Pharmaceutical manufacturing is the primary source of high-tech jobs and

growth in the eastern part of the Innovation Corridor largely because of the manufacturing facilities of Pfizer, Merck, Thermo Fischer, and others.

§ STEM jobs pay a median wage of $81,000 per year compared with $34,000 per year for non-STEM jobs.

Trends in Innovation and Research

§ Private-sector companies headquartered in NC make up 33% of patents granted to North Carolina inventors. – Common technologies include computing, calculating, counting; medical or

veterinary science, hygiene; electronic communication; and basic electric elements.

§ Emerging technology areas with growth in patents granted include wireless communication, power electronics, gene therapy, microorganisms, and health care informatics.

§ The Corridor boasts significant innovation assets, including 267 organizations that support R&D, technology commercialization, and entrepreneurship.

Innovation Corridor’s Innovation Performance and Assets

The Research Triangle has a large, fast-growing, and highly diversified high-tech sector driven by computer systems, R&D, and professional services firms.

– Computer systems design, software publishing, and R&D services have seen double-digit percentage growth in the region over the last 5 years.

Triangle-based companies receive 99% of the venture capital deals in the Corridor.

– Large late-stage deals, including the 2018 Epic Games deal, make information technology (IT) the largest recipient of venture funding in the region.

– The largest percentage of early-stage funding in the Corridor is going to startups in health care, which include life science and bioscience startups.

North Carolina’s Economy:Current Structure and Performance

Population GDP GDP per Capita

Household Income Poverty Rate

2018 value 10,273,419Rank: 9th

$565.8B Rank: 11th

$45,834Rank: 39th

$52,413Rank: 44th

14.0%Rank: 35th

2008 value 9,222,414Rank: 10th

$413.4BRank: 9th

$37,636Rank: 32nd

$46,549Rank: 40th

14.6%Rank: 36th

10-year% change +11.4% +36.9% +21.8% +17.3% +0.7%

Rank trend

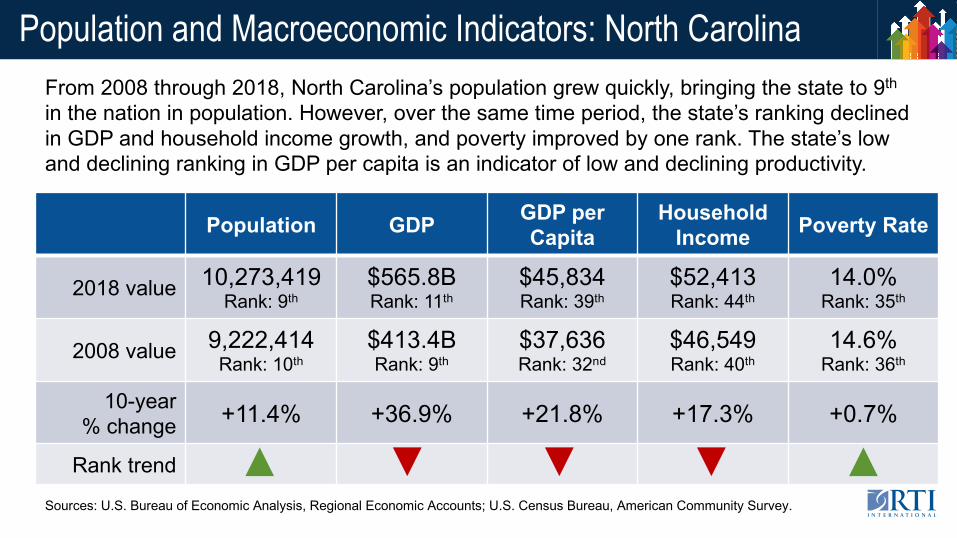

Population and Macroeconomic Indicators: North CarolinaFrom 2008 through 2018, North Carolina’s population grew quickly, bringing the state to 9th

in the nation in population. However, over the same time period, the state’s ranking declined in GDP and household income growth, and poverty improved by one rank. The state’s low and declining ranking in GDP per capita is an indicator of low and declining productivity.

Sources: U.S. Bureau of Economic Analysis, Regional Economic Accounts; U.S. Census Bureau, American Community Survey.

North Carolina has recovered slowly from the 2008–2009 recession.

Since 2008, North Carolina’s economy (36.9% growth) has grown more slowly than the U.S. economy (39.3%) despite being one of the fastest growing states in the nation in population.

Source: U.S. Bureau of Economic Analysis, Regional Economic Accounts.

GDP Growth: 2008–2018North Carolina, Southeast, and National: 2008=100

GDP Industry Growth Composition

Manufacturing (24%)

Real estate and rental and leasing

Finance and insurance

Health care and social assistance

Professional, scientific, and technical services (70%)

Composition of North Carolina GDP Growth: 2008–2018From 2008 through 2018, North Carolina’s GDP grew by 36.9%, more slowly than the nation as a whole at 39.3%.

Professional services (70%), wholesale trade (48%), and real estate rental and leasing (46%) grew the most. Manufacturing, the largest single contributor to GDP, grew by 24%, below the state growth (36.9%) and national manufacturing growth (30%).

Industry (growth percent)

Source: U.S. Department of Commerce, Bureau of Economic Analysis, Regional Economic Accounts.Figures limited to sectors contributing up to 50% of state output. Figures in current dollar value.

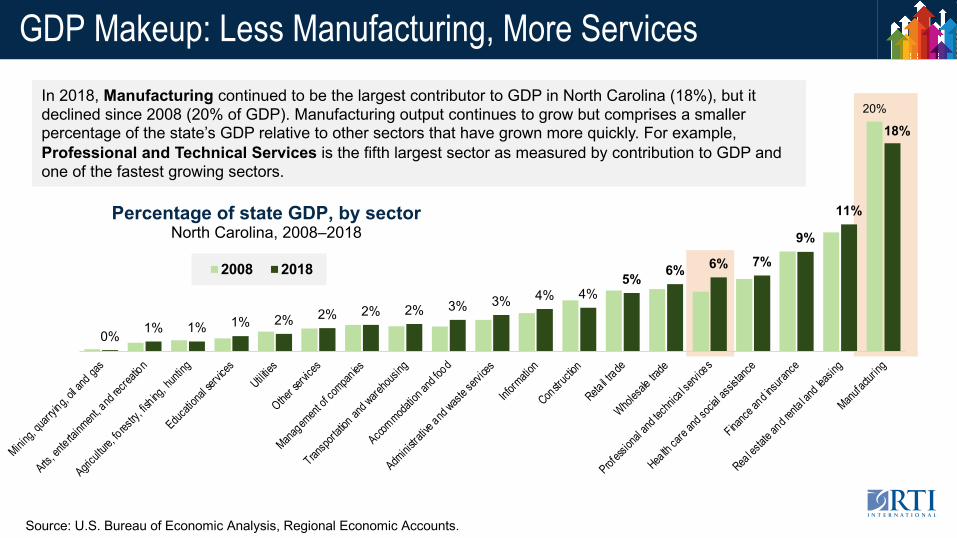

GDP Makeup: Less Manufacturing, More Services

20%

0% 1% 1% 1% 2% 2% 2% 2% 3% 3% 4% 4%5% 6% 6% 7%

9%

11%

18%

Mining, q

uarryin

g, oil a

nd gas

Arts, en

te rtainm

ent, a

nd rec

reation

Agricultu

re, fo res

try, fis

h ing, h

unting

Educatio

nal se

rvices

Utilities

Other se

rvices

Managem

ent of

compan

ies

Transpo

rtation

and w

arehou

sing

Accommoda

tion an

d food

Adminis

trative

and wast

e serv

ices

Inform

ation

Constru

ction

Retail tr

ade

Wholesa

le trad

e

Profess

ional a

nd tec

hnica l se

rvices

Health

care a

nd soc

ial ass

istance

Finance

and in

suranc

e

Real es

tate an

d renta

l and lea

sing

Manufac

turing

2008 2018

Percentage of state GDP, by sectorNorth Carolina, 2008–2018

In 2018, Manufacturing continued to be the largest contributor to GDP in North Carolina (18%), but it declined since 2008 (20% of GDP). Manufacturing output continues to grow but comprises a smaller percentage of the state’s GDP relative to other sectors that have grown more quickly. For example, Professional and Technical Services is the fifth largest sector as measured by contribution to GDP and one of the fastest growing sectors.

Source: U.S. Bureau of Economic Analysis, Regional Economic Accounts.

GDP of Manufacturing: Increasing Output, Declining Jobs

Sources: U.S. Bureau of Economic Analysis, Regional Economic Accounts; U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages. Output expressed in 2018 dollars.

2008–201824% increase in output

Manufacturing Contribution to GDP and Jobs in North Carolina: 1998–2018Over the last two decades, jobs in manufacturing in North Carolina have declined, while GDP output has risen, passing $100 billion in 2018. Manufacturing jobs are 8% below 2008 levels but have increased since 2010.

High-Technology Industries: Why They Matter

Opportunities exist across the Innovation Corridor region to strengthen and grow high-tech industries, which have an outsized impact on R&D intensity and STEM jobs. § High-tech industries make up 3.6% of jobs

nationally, but they account for a greater share of R&D activity, exports, wages, and output.

3.6%

3.8%

6.2%

8.1%

27.2%

58.7%

70.1%

Share of Jobs

Share of Firms

Share of Gross Output

Share of Wages

Share of Exports

Share of R&D Jobs

Share of Business R&DInvestment

Share of Economic Activity by High-Tech IndustriesUnited States, 2017

Source: Information Technology & Innovation Foundation (2017). How Technology-Based Startups Support U.S. Economic Growth, pp.15-16. Bureau of Labor Statistics (BLS).

BLS identifies 28 high-tech industries, including professional services, manufacturing, IT, utilities, and others. They include a mix of STEM and non-STEM occupations.

Source: EMSI.

The high-tech sector in North Carolina outpaces the nation in job growth and is projected to grow at a steady pace.

On average, high-tech jobs in NC tend to pay 12% below the national average high-tech wage.

High-Technology Industries: Growth in North Carolina

401,742Jobs (2018)

4% above national average per capita

+23.4%Growth (2001–2018)

1.9x national average Nation: +12.2%

$118,627Average earnings per job (2018)

12% below national averageNation: $135,849

High-Tech Industries in North Carolina: Job Growth and Earnings

Innovation: NC Performance from 2008 to Present

Indicator - most recent year

10-Year Past

Value

10-Year Past Rank

Current Value

Current Rank

Trend Rank

Gross Expenditures on R&D as a Percentage of GDP (%) - 2015

2.05% 23 2.35% 19 p

Industry Expenditures on R&D as a Percentage of Private Industry Output (%) -2016

1.63% 19 2.24% 15 p

Academic Expenditures on R&D per $1,000 of GDP ($) - 2017

$4.83 8 $5.72 3 p

Patents Awarded per 1,000 Individuals in S&E Occupations (Number) - 2017

12.08 24 17.87 20 p

SBIR and STTR Funding per $1 Million Dollars GDP ($) - 2014-16

$106.67 31 $107.79 19 p

Tech-based Startups as a Share of Total Firms (%) - 2016

NA NA 2.97% 17 NA

Venture Capital per $1 Million GDP ($) -2017

$566.8 12 $875.1 12 —

STEM Workforce: Individuals in S&E Occupations as a Percentage of All Occupations (%) - 2017

3.56% 31 4.82% 18 p

High Tech Jobs as a Percentage of Total Employment (%) - 2017

3.6% 25 5.6% 10 p

GDP ($B) - 2018 $413.3 9 $565.8 11 q

GDP per Capita ($) - 2018 $37,636 32 $45,834 39 q

Population (Number) - 2018 9,309,449 10 10,383,620 9 —

Over the last decade, North Carolina has outperformed the nation in growth of science, technology, and innovation (STI) outputs.

Compared with national and regional peers, the state has risen quickly in the ranks of R&D expenditures, patenting, SBIR funding, and STEM and high-tech jobs.

However, the pay for high-tech jobs is below the national average, and growth in STI indicators has occurred alongside declining GDP per capita rankings (NC ranks 39th).

Innovation: Research and Development Spending

Indicator 2008 Value

2008 Rank

2015-17

Value

2015-17

Rank

Rank Trend

Gross Expenditures on R&D as a Percentage of GDP (%) - 2015

2.0% 23rd 2.4% 19th p

Industry Expenditures on R&D as a Percentage of Private Industry Output (%) - 2016

1.6% 19th 2.2% 15th p

Academic Expenditures on R&D per $1,000 of GDP ($) - 2017

$4.83 8th $5.72 3rd p

Over the past 10 years, North Carolina has moved up nationally in R&D expenditures by both industry and academic institutions. NC is a national leader in academic R&D expenditures, ranking 3rd in expenditures per $1,000 of GDP.

Gross Expenditure on Research & Development Percentage of GDP, North Carolina and Peers, 2001–2015

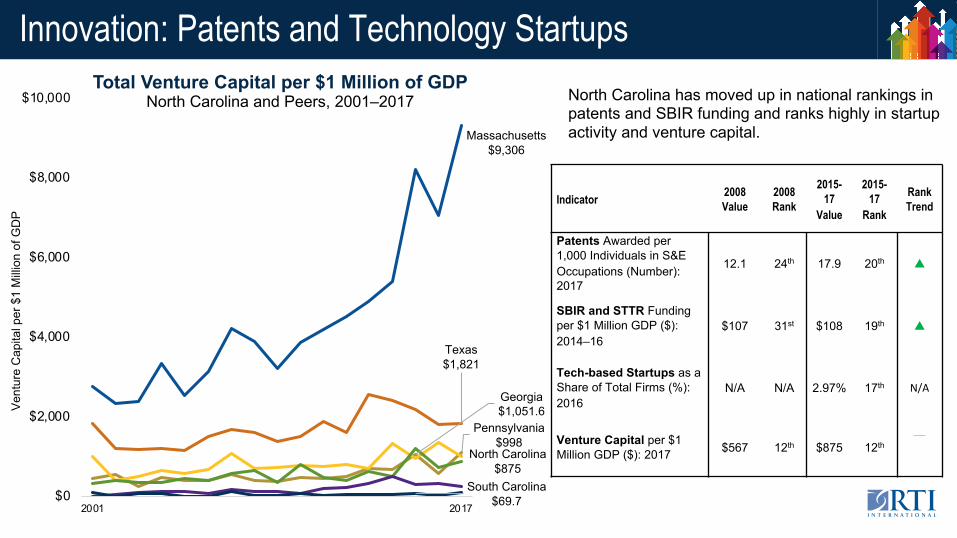

Innovation: Patents and Technology Startups

Indicator 2008 Value

2008 Rank

2015-17

Value

2015-17

Rank

Rank Trend

Patents Awarded per 1,000 Individuals in S&E Occupations (Number): 2017

12.1 24th 17.9 20th p

SBIR and STTR Funding per $1 Million GDP ($): 2014–16

$107 31st $108 19th p

Tech-based Startups as a Share of Total Firms (%): 2016

N/A N/A 2.97% 17th N/A

Venture Capital per $1 Million GDP ($): 2017 $567 12th $875 12th

—

Total Venture Capital per $1 Million of GDPNorth Carolina and Peers, 2001–2017

Massachusetts$9,306

Texas$1,821

Georgia$1,051.6

Pennsylvania$998

North Carolina$875

South Carolina$69.7$0

$2,000

$4,000

$6,000

$8,000

$10,000

2001 2017

Vent

ure

Cap

ital p

er $

1 M

illion

of G

DP

North Carolina has moved up in national rankings in patents and SBIR funding and ranks highly in startup activity and venture capital.

Jobs in North Carolina: Growth Concentrated in Services

3,116

27,087

220,584

474,843

14,498

59,976

72,386

79,912

83,884

86,065

109,889

133,695

173,356

182,400

254,600

296,823

430,408

499,888

505,746

Mining, quarrying, oil and gas

Agriculture, fo restry, fish ing and hunting

Construction

Manufacturing

Utilities

Rea l estate and renta l and leasing

Arts, entertainment, and recreation

Information

Management of compan ies

Educational services

Other services

Transportation and warehousing

Finance and insurance

Wholesale trade

Professional and technica l services

Administrative and waste services

Accommodation and food

Reta il trade

Hea lth care and social assistance

2008

2018

Jobs in year

Sectors gaining jobs

Sectors losing jobs

North Carolina’s post-recession growth has been strongest in services, with high job growth in areas like health care, retail, and food services. Production areas, including manufacturing and construction, have declined.

Growing sectors—health care, retail, and accommodation and food services—are large and growing, supporting 400,000–500,000 jobs each. However, retail and accommodation and food services rank at the bottom for average pay in the state.

Declining sectors: The manufacturing sector is large (475,000 jobs) but has shed employment since 2008. Construction, agriculture, and mining have also lost employment since 2008.

Private-Sector Jobs, by IndustryNorth Carolina, 2008–2018

Source: U.S. Bureau of Labor Statistics, QCEW.

Jobs in North Carolina: Growth in Low-Wage Industries

$17,840$28,632

$31,229$35,105$36,449$37,081

$47,982$49,245$50,823$50,872

$54,610$59,834

$61,805$74,066

$83,926$84,838

$95,254$99,946

$108,530

Accommodation and foodReta il trade

Arts, ente rtainment, and recreationOther services

Agriculture, fo restry, fish ingAdministrative and waste servicesHea lth care and social assistanceTransportation and warehousingRea l estate, rental and leasing

Educational servicesConstruction

ManufacturingMining, quarrying, oil and gas

Wholesale tradeInformation

Professional and technica l servicesUtilities

Finance and insuranceManagement of compan ies

Since 2008, the three largest growing industry sectors in North Carolina (health care, retail, accommodation and food service) have fallen to the bottom 50% of average pay.

Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Professional and technical services has contributed to high wages and job growth since 2008.

Average Annual Pay, by IndustryNorth Carolina, 2018

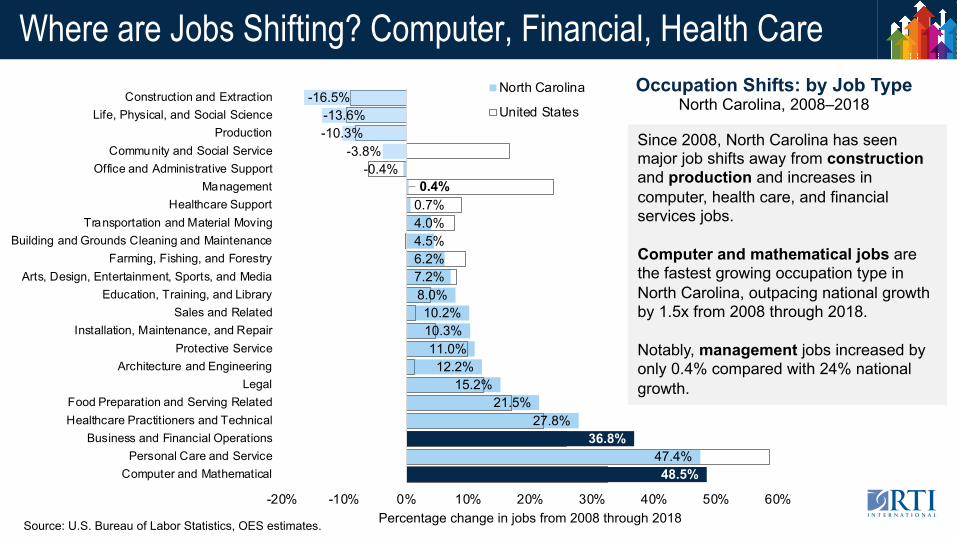

Where are Jobs Shifting? Computer, Financial, Health Care

48.5%47.4%

36.8%27.8%

21.5%15.2%

12.2%11.0%

10.3%10.2%

8.0%7.2%6.2%4.5%4.0%0.7%0.4%

-0.4%-3.8%

-10.3%-13.6%

-16.5%

-20% -10% 0% 10% 20% 30% 40% 50% 60%

Computer and MathematicalPersonal Care and Service

Business and Financial OperationsHealthcare Practitioners and TechnicalFood Preparation and Serving Related

LegalArchitecture and Engineering

Protective ServiceInstallation, Maintenance, and Repair

Sales and RelatedEducation, Training, and Library

Arts, Design, Entertainment, Sports, and MediaFarming, Fishing, and Forestry

Building and Grounds Cleaning and MaintenanceTransportation and Material Moving

Healthcare SupportManagement

Office and Administrative SupportCommunity and Social Service

ProductionLife, Physical, and Social Science

Construction and Extraction

Percentage change in jobs from 2008 through 2018

North Carolina

United States

Source: U.S. Bureau of Labor Statistics, OES estimates.

Since 2008, North Carolina has seen major job shifts away from constructionand production and increases in computer, health care, and financial services jobs.

Computer and mathematical jobs are the fastest growing occupation type in North Carolina, outpacing national growth by 1.5x from 2008 through 2018.

Notably, management jobs increased by only 0.4% compared with 24% national growth.

Occupation Shifts: by Job TypeNorth Carolina, 2008–2018

The Innovation Corridor’s Economic, Talent, and Innovation Assets

Four Innovation Corridor Economies: Overview

2,199,459Population

$126.8BEconomy

$65,093HH Income

12%Poverty

Raleigh-Durham-Chapel Hill CSA

1,663,532Population

$71.3BEconomy

$48,158HH Income

17%Poverty

Greensboro-Winston-Salem-High Point CSA

299,581Population

$11.7BEconomy

$41,220HH Income

16%Poverty

Rocky Mount-Wilson-Roanoke Rapids CSA

226,130Population

$8.4BEconomy

$44,209HH Income

25%Poverty

Greenville-Washington CSA

10,273,419Population

$565.8BEconomy

$52,413Median Household

Income (2018)

14%PovertyNorth Carolina

Source: U.S. Census Bureau, Census Reporter; U.S. Bureau of Economic Analysis, Regional Economic Accounts.

Innovation Corridor’s PopulationThe Innovation Corridor is a region of extremes. For example, population ranges from 2.2 million in the Raleigh-Durham-Chapel Hill CSA (17% growth over the last decade) to just under 300,000 in the Rocky Mount-Wilson-Roanoke Rapids CSA (4% decline over the last decade). Across the Innovation Corridor, the population has grown by 10% since 2010.

A portion of the population change is attributed to in-migration to Innovation Corridor CSAs. The top sources of in-migration include:

Source: U.S. Census, American Community Survey, 2013-2017 Metro Area In-, Out-, Net and Gross Migration.

Innovation Corridor’s Population, Continued The poverty rate is 15% and the unemployment rate is 4%—down from 10% in 2010. The poverty rate is 15% in the Innovation Corridor but varies dramatically across CSAs: the lowest poverty rate is 12% in Raleigh-Durham-Chapel Hill and the highest is in Greenville-Washington at 25%.

The population of the Innovation Corridor is aging. In 2010, 12% of the population was over 65. By 2018, 15% of the population was over 65.

All CSAs in the Innovation Corridor are becoming more racially and ethnically diverse.

All CSAs in the Innovation Corridor have experienced an increase in educational attainment for associate’s, bachelor’s, and doctorate/professional degrees. The share of people getting a college degree grew from 38% to 43%.

Educational Attainment as a Share of Total Population2010–2018

2010 2018

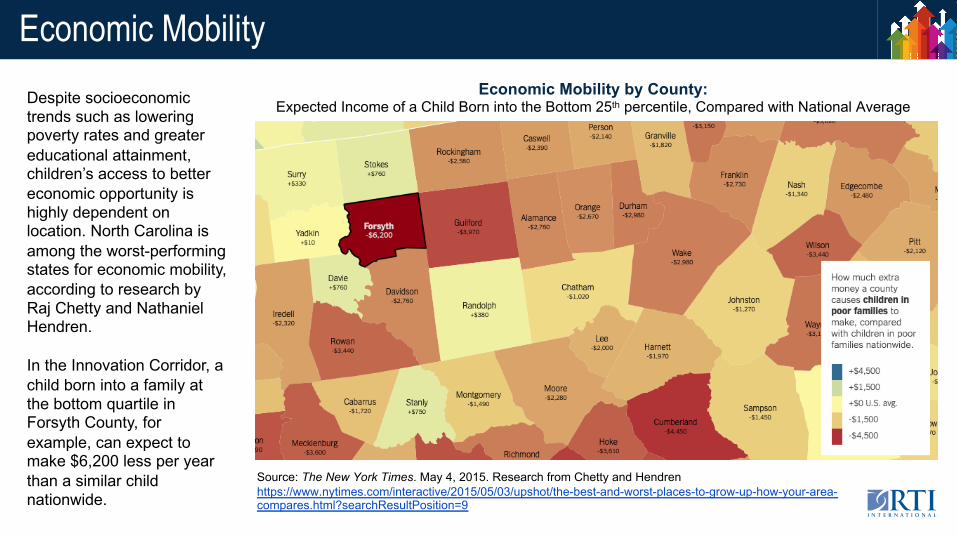

Economic MobilityEconomic Mobility by County:

Expected Income of a Child Born into the Bottom 25th percentile, Compared with National AverageDespite socioeconomic trends such as lowering poverty rates and greater educational attainment, children’s access to better economic opportunity is highly dependent on location. North Carolina is among the worst-performing states for economic mobility, according to research by Raj Chetty and Nathaniel Hendren.

In the Innovation Corridor, a child born into a family at the bottom quartile in Forsyth County, for example, can expect to make $6,200 less per year than a similar child nationwide.

Source: The New York Times. May 4, 2015. Research from Chetty and Hendren https://www.nytimes.com/interactive/2015/05/03/upshot/the-best-and-worst-places-to-grow-up-how-your-area-compares.html?searchResultPosition=9

Commuting Patterns in the Innovation CorridorThe corridor has multiple employment centers and commuters in the corridor are highly mobile: 736,465 people live in a different metro area than their place of work, representing 42% of primary jobs in the corridor.

Commuting Patterns by Metro Area of Primary Job

Proposed Innovation Corridor 2017

Source: U.S. Census Bureau. OnTheMap. Metropolitan Statistical Area (MSA) definitions from Census Bureau.

Metropolitan Statistical Area (MSA)

Net Job: Inflow/ Outflow

Employees Live and Work within MSA

% of Employees Commuting into

Other MSAs

% Employees Commuting from

Corridor Counties

Winston Salem Outflow Majority (63%) 37% 9%

Greensboro-High Point Inflow Majority (60%) 40% 7%

Durham-Chapel Hill Inflow Less than half (47%) 53% 26%

Raleigh Inflow Majority (61%) 39% 5%

Wilson Inflow Less than half (42%) 58% 22%

Rocky Mount Outflow Majority (56%) 44% 16%

Roanoke Rapids Outflow Majority (59%) 41% 11%

Greenville Inflow Majority (55%) 45% 8%

Washington Outflow Less than half (47%) 53% 15%

Commuting patterns are not uniform: 5 of the 9 MSAs have a net inflow of employees. Durham-Chapel Hill and Wilson MSAs have the highest inflow of employees from other Corridor metros or counties.

Source: U.S. Census Bureau. OnTheMap.

Commuting Patterns Across MSAs

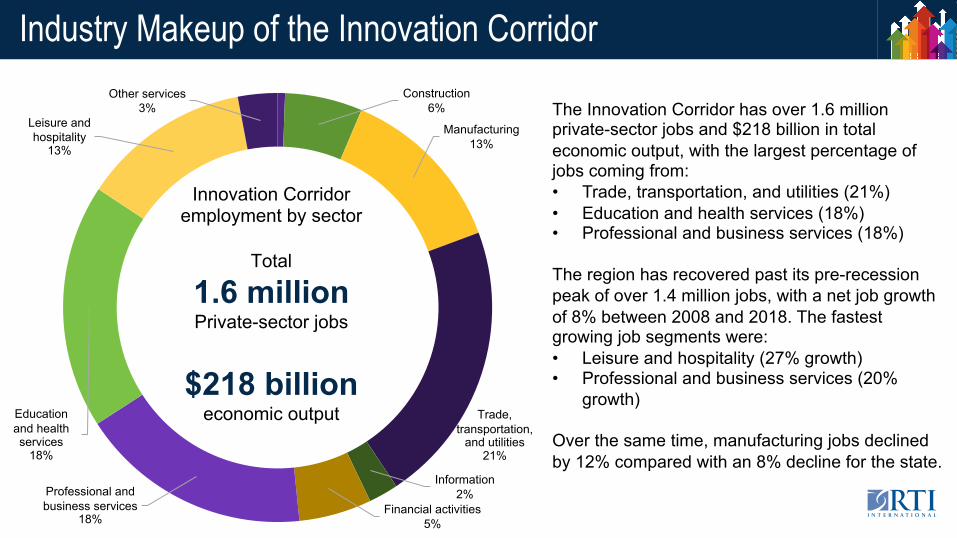

Industry Makeup of the Innovation CorridorConstruction

6%

Manufacturing13%

Trade, transportation,

and utilities21%

Information2%

Financial activities5%

Professional and business services

18%

Education and health services

18%

Leisure and hospitality

13%

Other services3%

Innovation Corridor employment by sector

Total

1.6 million Private-sector jobs

$218 billion economic output

The Innovation Corridor has over 1.6 million private-sector jobs and $218 billion in total economic output, with the largest percentage of jobs coming from: • Trade, transportation, and utilities (21%) • Education and health services (18%)• Professional and business services (18%)

The region has recovered past its pre-recession peak of over 1.4 million jobs, with a net job growth of 8% between 2008 and 2018. The fastest growing job segments were: • Leisure and hospitality (27% growth) • Professional and business services (20%

growth)

Over the same time, manufacturing jobs declined by 12% compared with an 8% decline for the state.

The Geography of Industry Growth in Innovation Corridor

Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Private-Sector Employment by Region Proposed Innovation Corridor: 1998–2018

+19%

Post-recession job growth(2008–2018)

+1%

-2%-10%

Gre

at R

eces

sion

In 2018, there were over 1.6 millionprivate-sector jobs in the Innovation Corridor, an increase from fewer than 1.4 million at the lowest point of the Great Recession in 2010.

The region has seen an uneven recovery since the recession: • The Research Triangle Region

has added over 130,000 jobs compared with pre-recession and makes up 52% of jobs in the Corridor.

• The remaining regions have seen a net loss of 5,600 jobs over the same period, with the largest losses in the Rocky Mount region.

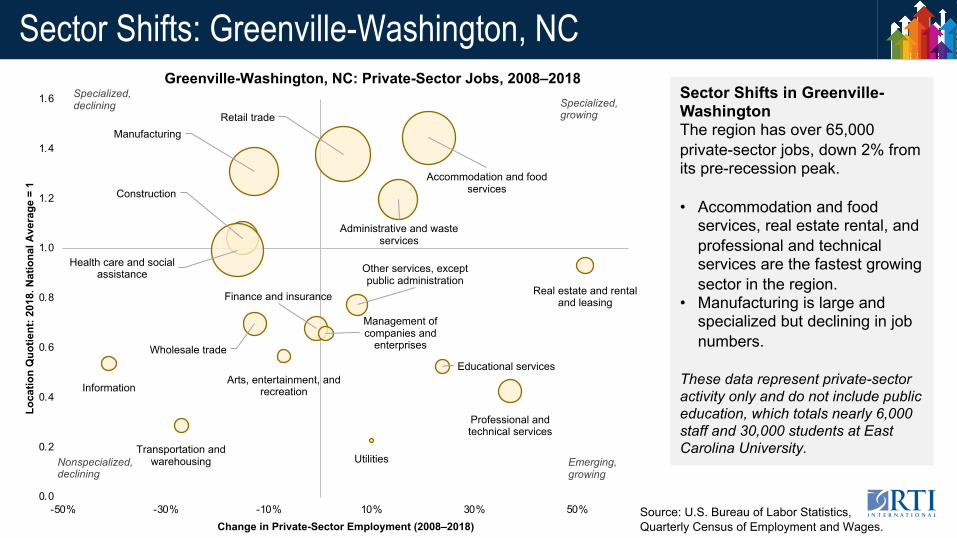

Sector Shifts: Greenville-Washington, NC

Utilities

Construction

Manufacturing

Wholesale trade

Retail trade

Transportation and warehousing

Information

Finance and insurance Real estate and rental and leasing

Sector Shifts in Greenville-WashingtonThe region has over 65,000 private-sector jobs, down 2% from its pre-recession peak.

• Accommodation and food services, real estate rental, and professional and technical services are the fastest growing sector in the region.

• Manufacturing is large and specialized but declining in job numbers.

These data represent private-sector activity only and do not include public education, which totals nearly 6,000 staff and 30,000 students at East Carolina University.

Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Sector Shifts: Rocky Mount-Wilson-Roanoke RapidsSector Shifts in Rocky Mount-Wilson-Roanoke RapidsThe region has over 93,000 private-sector jobs, down 10% from its pre-recession peak.

• Manufacturing is the largest and most specialized sector in the region (2.0X the national average jobs per capita). Large pharmaceutical and tire manufacturers in the region are major employers.

• Private educational services, management, accommodation and food services, and health care are growing in the region.

Agriculture, forestry, fishing and hunting

Utilities

Construction

Manufacturing

Wholesale trade

Retail trade

Transportation and warehousing

Information

Finance and insuranceReal estate and rental

and leasing

Professional and technical services

Management of companies and

enterprisesAdministrative and

waste services

Educational services

Health care and social assistance

Arts, entertainment, and recreation

Accommodation and food services

Other services, except public administration

0.0

0.5

1.0

1.5

2.0

2.5

-40% -30% -20% -10% 0% 10% 20%

Loca

tion

Quo

tient

: 201

8. N

atio

nal A

vera

ge =

1

Change in Total Private-Sector Employment (2008-2018)

Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Sector Shifts: Greensboro-Winston-Salem-High PointSector Shifts in Greensboro-Winston-Salem-High PointThe region has over 620,000 private-sector jobs, an increase of 1% from its pre-recession peak.

• Manufacturing has seen large job losses but is still the largest and most specialized sector in the region (1.6X the national average jobs per capita). Tobacco, textile, and furniture manufacturers employ fewer people, while aerospace and transportation manufacturing have grown.

• Health care, accommodation and food services, and trade are growing in the region. Agriculture, forestry,

fishing and hunting

Mining, quarrying, and oil and gas extraction

Utilities

Construction

Manufacturing

Wholesale tradeRetail trade

Transportation and warehousing

Information

Finance and insurance

Real estate and rental and leasing

Professional and technical services

Management of companies and

enterprises

Administrative and waste services

Educational services

Health care and social assistance

Arts, entertainment, and recreation

Accommodation and food services

Other services, except public administration

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-50% -30% -10% 10% 30% 50% 70%

Loca

tion

Quo

tient

: 201

8. N

atio

nal A

vera

ge =

1

Change in Total Private Sector Employment (2008-2018)

Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages

Sector Shifts: Raleigh-Durham-Chapel HillSector Shifts in Raleigh-Durham-Chapel Hill The region has over 837,000 private-sector jobs, an increase of 19% from its pre-recession peak.

• Private educational services and professional and technical services are large, highly specialized, and fast-growing sectors.

• Health care and retail trade are the largest employment sectors.

• Manufacturing is less specialized and employs fewer people.

• Finance, health care, accommodation and food services, entertainment, utilities, and transportation and warehousing are emerging and fast-growing sectors. Agriculture, forestry,

fishing and hunting

Utilities

Construction

Manufacturing

Wholesale tradeRetail trade

Transportation and warehousing

Information

Finance and insurance

Real estate and rental and leasing

Professional and technical services

Management of companies and

enterprises

Administrative and waste services

Educational services

Health care and social assistance

Arts, entertainment, and recreation

Accommodation and food services

Other services, except public administration

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-30% -10% 10% 30% 50% 70% 90%

Loca

tion

Quo

tient

: 201

8. N

atio

nal A

vera

ge =

1

Change in Total Private Sector Employment (2008-2018)

Emerging, growing Source: U.S. Bureau of Labor Statistics,

Quarterly Census of Employment and Wages

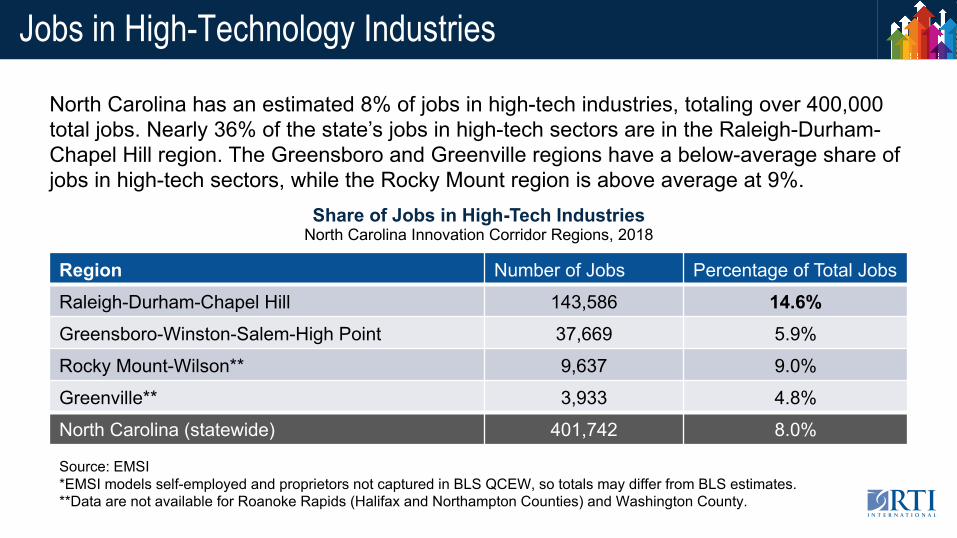

Jobs in High-Technology Industries

Source: EMSI*EMSI models self-employed and proprietors not captured in BLS QCEW, so totals may differ from BLS estimates. **Data are not available for Roanoke Rapids (Halifax and Northampton Counties) and Washington County.

North Carolina has an estimated 8% of jobs in high-tech industries, totaling over 400,000 total jobs. Nearly 36% of the state’s jobs in high-tech sectors are in the Raleigh-Durham-Chapel Hill region. The Greensboro and Greenville regions have a below-average share of jobs in high-tech sectors, while the Rocky Mount region is above average at 9%.

Region Number of Jobs Percentage of Total Jobs

Raleigh-Durham-Chapel Hill 143,586 14.6%Greensboro-Winston-Salem-High Point 37,669 5.9%

Rocky Mount-Wilson** 9,637 9.0%

Greenville** 3,933 4.8%

North Carolina (statewide) 401,742 8.0%

Share of Jobs in High-Tech IndustriesNorth Carolina Innovation Corridor Regions, 2018

Jobs in High-Technology Industries: Subsectors and Regions

967

998

1,044

1,248

1,820

2,025

2,988

3,228

3,834

4,337

6,040

8,883

9,152

9,569

11,351

15,855

17,400

18,387

19,019

26,815

29,102

Industrial Machinery Manufacturing

Commercial and Service Industry Machinery…

Other Information Services

Basic Chemical Manufacturing

Communications Equipment Manufacturing

Other Telecommunications

Electrical Equipment Manufacturing

Aerospace Product and Par ts Manufacturing

Electric Power Generation, Transmission and…

Data Processing, Hosting, and Related Services

Semiconductor and Other Electronic Component…

Navigational, Measur ing, Electromedical, and Control…

Computer and Per ipheral Equipment Manufacturing

Wired and Wireless Telecommunications Carriers

Software Publishers

Pharmaceutical and Medicine Manufacturing

Management, Sc ientific, and Technical Consulting…

Scientific Research and Development Serv ices

Architectural, Engineering, and Related Services

Computer Systems Design and Related Serv ices

Management of Companies and Enterprises

Raleigh-Durham-Chapel Hill

Greensboro-Winston-Salem-High Point

Rocky Mount-Wilson

Greenville

High-tech employment in the Innovation Corridor is concentrated in the Research Triangle and the largest high-tech subsectors include:

§ Management of companies§ Computer science fields including computer

systems design, software publishers, computer equipment manufacturing, electromedical manufacturing, electronic component manufacturing, data processing, telecommunications, and other electronics manufacturing fields

§ Professional services including architecture and engineering, scientific R&D, and management consulting

Number of Jobs in High-Tech IndustriesNC Innovation Corridor, 2018

Source: EMSI, Bureau of Labor Statistics.

Jobs in High-Tech Industries: Greenville

Source: RTI analysis of Emsi - economicmodeling.com.*Note: Data were not available for Washington County.

40

55

64

76

127

148

181

320

361

669

1,823

Software Publishers

Other Telecommunications

Semiconductor and Component Manufacturing

Basic Chemical Manufacturing

Computer Systems Design and Related Services

Electrical Equipment Manufacturing

Wired and Wireless Telecommunications Carriers

Management, Scientific, and Technical ConsultingServices

Architectural, Engineering , and Related Services

Management of Companies and Enterprises

Pharmaceutical and Medicine Manufacturing

20132018

Number of Jobs in High-Tech IndustriesGreenville*: 2013–2018

Pharmaceutical manufacturing is the largest contributor to jobs and growth in the region, with major manufacturers including Thermo Fischer Scientific, Mayne Pharma, and Dyneema.

Architectural and engineering services and management, scientific, and technical consulting are growing slowly in the region.

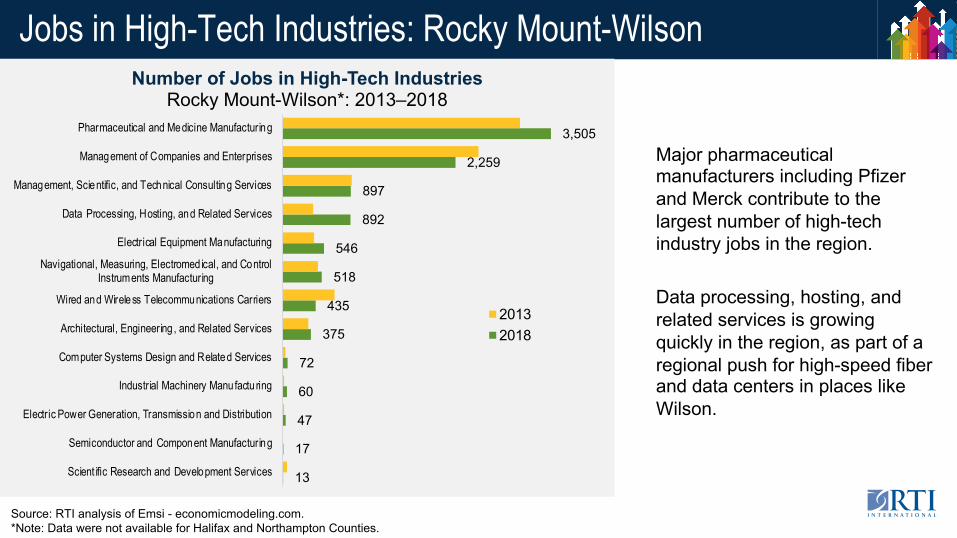

Jobs in High-Tech Industries: Rocky Mount-Wilson

13

17

47

60

72

375

435

518

546

892

897

2,259

3,505

Scient ific Research and Development Services

Semiconductor and Component Manufacturing

Electric Power Generation, Transmission and Distribution

Industrial Machinery Manufactu ring

Computer Systems Design and Related Services

Architectural, Engineering , and Related Services

Wired and Wireless Telecommunications Carriers

Navigational, Measuring, Electromed ical, and ControlInstruments Manufacturing

Electrical Equipment Manufacturing

Data Processing, Hosting, and Related Services

Management, Scientific, and Technical Consulting Services

Management of Companies and Enterprises

Pharmaceutical and Medicine Manufacturing

20132018

Source: RTI analysis of Emsi - economicmodeling.com.*Note: Data were not available for Halifax and Northampton Counties.

Number of Jobs in High-Tech IndustriesRocky Mount-Wilson*: 2013–2018

Major pharmaceutical manufacturers including Pfizer and Merck contribute to the largest number of high-tech industry jobs in the region.

Data processing, hosting, and related services is growing quickly in the region, as part of a regional push for high-speed fiber and data centers in places like Wilson.

Jobs in High-Tech Industries: Greensboro-W-S-High Point

451

471

531

673

687

734

745

750

818

2,036

2,572

2,950

3,012

3,018

3,550

13,776

Basic Chemical Manufacturing

Commercial and Service Indust ry Machinery Manufacturing

Computer and Peripheral Equipment Manufacturing

Navigational, Measuring, Electromed ical, and Control…

Industrial Machinery Manufactu ring

Electric Power Generation, Transmission and Distribution

Pharmaceutical and Medicine Manufacturing

Scient ific Research and Development Services

Data Processing, Hosting, and Related Services

Semiconductor and Other Electronic Component Manufacturing

Aerospace Product and Parts Manufacturing

Wired and Wireless Telecommunications Carriers

Architectural, Engineering , and Related Services

Management, Scientific, and Technical Consulting Services

Computer Systems Design and Related Services

Management of Companies and Enterprises

20132018

Source: RTI analysis of Emsi - economicmodeling.com.

Number of Jobs in High-Tech IndustriesGreensboro-Winston-Salem-High Point: 2013–2018

Major corporate headquarters (management of companies and enterprises) make up a large portion of the industry designated as high-tech, but there has been slow job decline in the sector.

Aerospace product and parts manufacturing is the fastest-growing high-tech sector.

Technical and professional services including computer systems design, architecture and engineering, and data processing are growing slowly in the region.

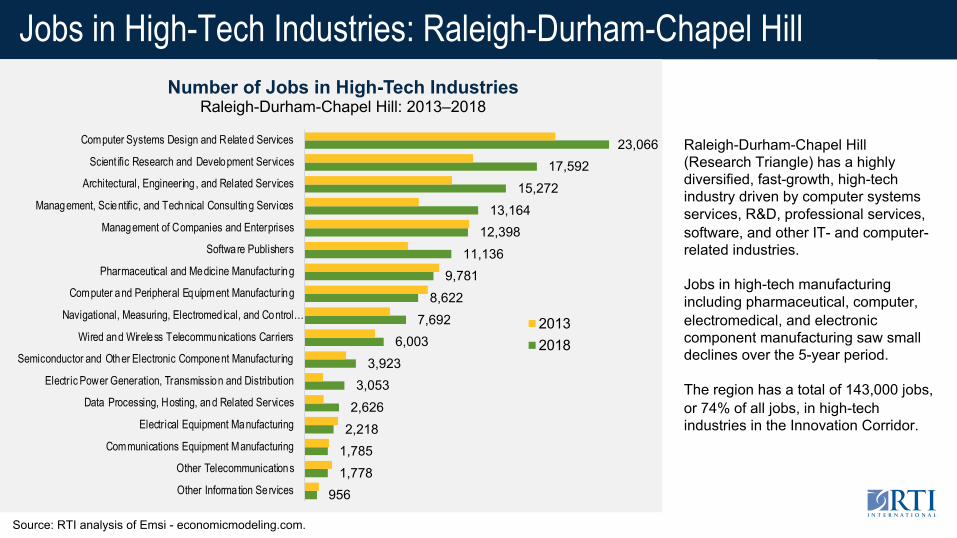

Jobs in High-Tech Industries: Raleigh-Durham-Chapel Hill

956 1,778 1,785 2,218 2,626 3,053

3,923 6,003

7,692 8,622

9,781 11,136

12,398 13,164

15,272 17,592

23,066

Other Information Services

Other Telecommunications

Communications Equipment Manufacturing

Electrical Equipment Manufacturing

Data Processing, Hosting, and Related Services

Electric Power Generation, Transmission and Distribution

Semiconductor and Other Electronic Component Manufacturing

Wired and Wireless Telecommunications Carriers

Navigational, Measuring, Electromed ical, and Control…

Computer and Peripheral Equipment Manufacturing

Pharmaceutical and Medicine Manufacturing

Software Publishers

Management of Companies and Enterprises

Management, Scientific, and Technical Consulting Services

Architectural, Engineering , and Related Services

Scient ific Research and Development Services

Computer Systems Design and Related Services

20132018

Source: RTI analysis of Emsi - economicmodeling.com.

Number of Jobs in High-Tech IndustriesRaleigh-Durham-Chapel Hill: 2013–2018

Raleigh-Durham-Chapel Hill (Research Triangle) has a highly diversified, fast-growth, high-tech industry driven by computer systems services, R&D, professional services, software, and other IT- and computer-related industries.

Jobs in high-tech manufacturing including pharmaceutical, computer, electromedical, and electronic component manufacturing saw small declines over the 5-year period.

The region has a total of 143,000 jobs, or 74% of all jobs, in high-tech industries in the Innovation Corridor.

STEM Jobs: Central to the Innovation Economy

2008* 2018

STEM Jobs*STEM (% of total jobs)* STEM Jobs

STEM (% of total jobs)

Greenville** 610 0.8% 1,770 2.3%

Rocky Mount-Wilson** 590 1.0% 850 1.6%

Greensboro-Winston-Salem-High Point 14,060 2.2% 26,440 3.8%

Raleigh-Durham-Chapel Hill 48,320 6.1% 102,270 10.9%

North Carolina — — 271,090 6.2%

Source: U.S. Bureau of Labor Statistics, OES, 2008 and 2018. *Percentages are estimates based on 2018 definitions. Some data from 2008 are unavailable because of changes in OES methodology over time. **Data are not available for Roanoke Rapids (Halifax and Northampton Counties) and Washington County.

North Carolina’s shifting manufacturing sector and growing service sectors rely on a base of human capital that drives an innovation economy. Science, technology, engineering, and math (STEM) jobs, as defined by Occupational Employment Statistics (OES), are a critical component. They earn a median annual wage of over $81K (compared with $34K for non-STEM).

STEM jobs make up 6.2% of jobs in North Carolina but are unevenly distributed throughout the state and the Innovation Corridor: The Research Triangle Region has 38% of the STEM occupations in the state and 78% of the STEM occupations in the Corridor.

STEM Jobs: Occupations and Geography

16,940

13,110

10,850

7,550

5,9605,320

4,700 4,370 4,320 3,790

SoftwareDevelopers,Applications

ComputerSystems Analysts

Computer UserSupport

Specialists

SalesRepresentat ives,Wholesale andManufacturing,Technical and

In the Innovation Corridor, the majority of STEM jobs in the region are in software and computer occupations: 6 of the top 7 have a computer, software, or IT focus.

Occupations such as industrial engineers are found more frequently in manufacturing sectors concentrated in Greensboro-Winston-Salem-High Point and Rocky Mount-Wilson.

STEM Occupations in the Innovation Corridor (2018)

Source: U.S. Bureau of Labor Statistics, OES, 2018.*Data are not available for Roanoke Rapids (Halifax and Northampton Counties) and Washington County.

STEM Jobs: Greenville-Washington

Top STEM Occupations by Employment

Rank Occupation Employment Median Income

1 Chemists 360 $56,610

2 Computer User Support Specialists 330 $47,540

3 Computer Systems Analysts 120 $79,820

4 Industrial Engineers 120 $80,210

5 Civil Engineers 120 $84,920

6 Network and Computer Systems Administrators 100 $66,860

7 Computer Network Support Specialists 80 $46,020

8 Computer Programmers 80 $69,410

The most common STEM occupation in Greenville is chemist. The occupations mix is reflective of Greenville’s biopharmaceutical manufacturing sector, with a presence of chemists and engineers working in the sector.

Greenville-Washington’s STEM occupations mix also includes IT jobs as computer technicians and support staff, but fewer programmers and developers.

Source: U.S. Bureau of Labor Statistics, OES, 2018.

STEM Jobs: Rocky Mount-Wilson-Roanoke Rapids

Top STEM Occupations by Employment

Rank Occupation Employment Median Income

1 Industrial Engineers 220 $78,630

2 Computer User Support Specialists 120 $43,440

3 Mechanical Engineers 90 $88,030

4 Network and Computer Systems Administrators 80 $69,150

5 Computer Systems Analysts 70 $85,710

6 Electrical Engineers 70 $79,480

7 Electrical and Electronics Engineering Technicians 60 $58,940

8 Industrial Engineering Technicians 40 $46,770

The most common STEM occupation in Rocky Mount-Wilson-Roanoke Rapids is industrial engineer. The region’s STEM jobs mix has many engineering occupations, reflecting its manufacturing sector.

The STEM mix of Rocky Mount-Wilson-Roanoke Rapids also includes computer technicians and support staff.

Source: U.S. Bureau of Labor Statistics, OES, 2018.

STEM Jobs: Greensboro-Winston-Salem-High PointTop STEM Occupations by Employment

Rank Occupation Employment Median Income

1 Computer User Support Specialists 3,060 $49,153

2 Computer Systems Analysts 2,640 $87,817

3 Software Developers, Applications 1,920 $92,300

4 Industrial Engineers 1,850 $76,753

5 Mechanical Engineers 1,520 $83,593

6 Network and Computer Systems Administrators 1,230 $80,995

7 Computer and Information Systems Managers 1,100 $137,255

8Sales Representatives, Wholesale and Manufacturing, Technical and Scientific Products

960 $73,513

Greensboro-Winston-Salem-High Point has a mix of computer, industrial engineering, and mechanical engineering occupations, reflective of its manufacturing sectors.

Greensboro-Winston-Salem-High Point has computer technicians and support staff as well as many software developers and IT managers.

Source: U.S. Bureau of Labor Statistics, OES, 2018.

STEM Jobs: Raleigh-Durham-Chapel HillTop STEM Occupations by Employment

Raleigh-Durham-Chapel Hill Greensboro-Winston-Salem-High Point Greenville Rocky Mount-Wilson-RR

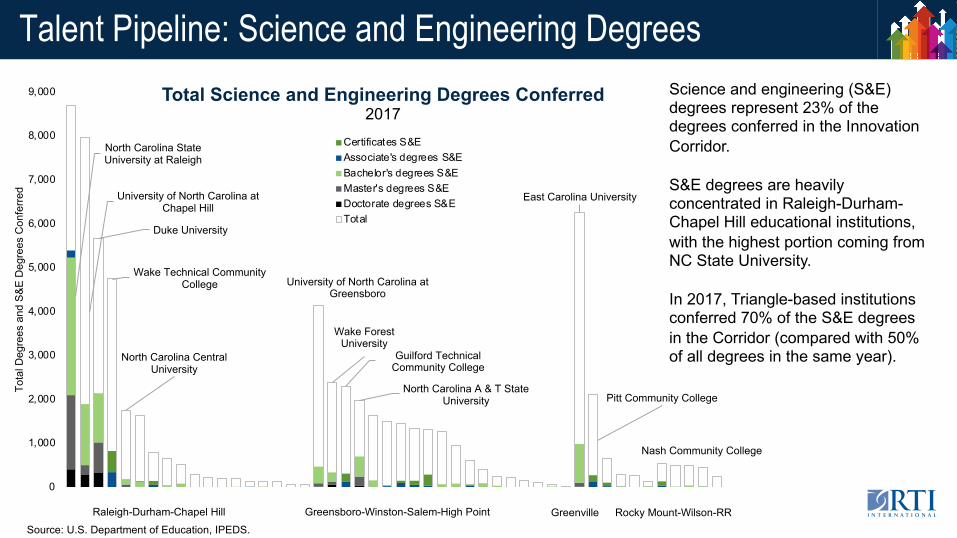

The Innovation Corridor’s human capital is supported by a broad mix of higher education institutions, conferring over 68,000 degrees in 2017. These are relatively evenly distributed throughout the Corridor:

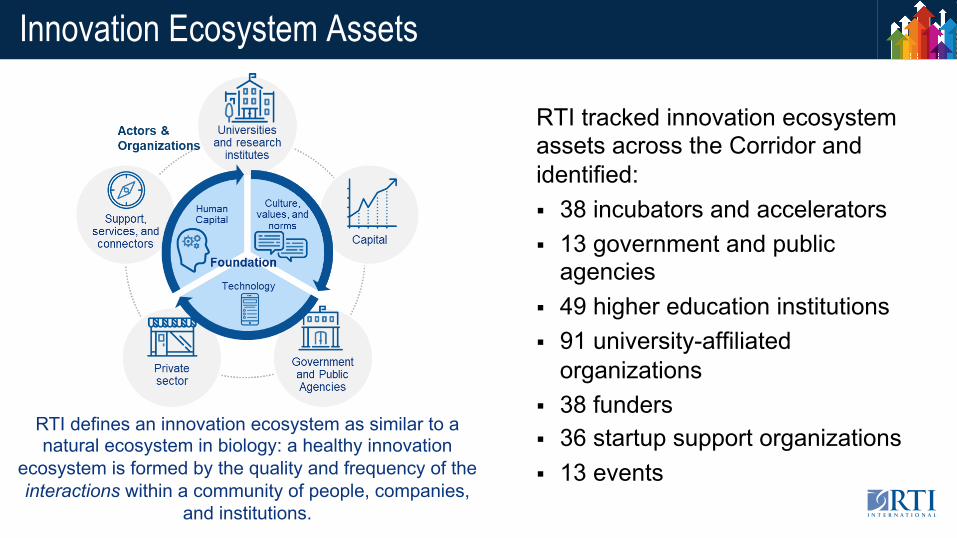

organizations§ 38 funders§ 36 startup support organizations§ 13 events

RTI defines an innovation ecosystem as similar to a natural ecosystem in biology: a healthy innovation

ecosystem is formed by the quality and frequency of the interactions within a community of people, companies,

and institutions.

Innovation Ecosystem Assets: Spread Across the Corridor

Source: RTI. The team tracked innovation ecosystem assets across the Corridor and identified 267 organizations with a physical address, as well as 15 networks and events without a fixed address. Locations are clustered by zip code in the map.

Innovation Ecosystem Assets in the Innovation Corridor

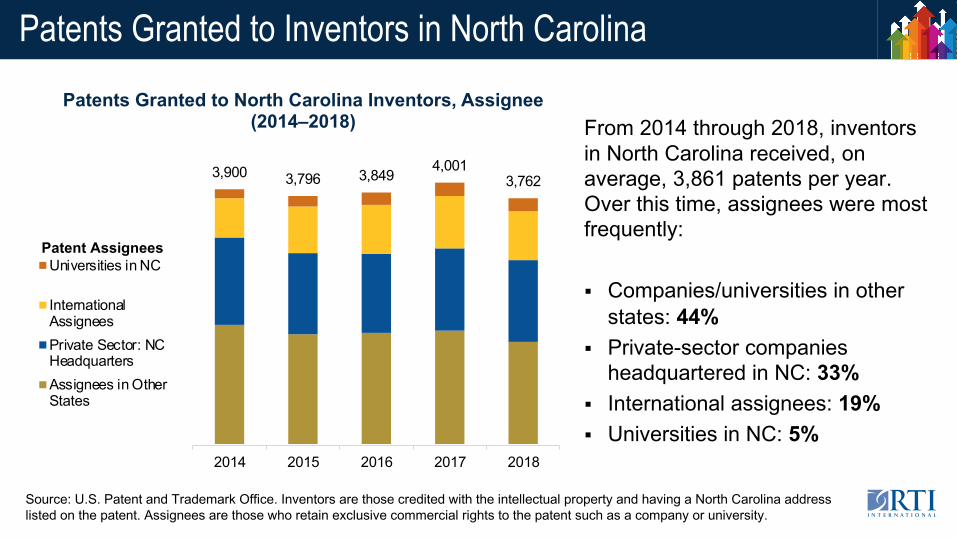

Patents Granted to Inventors in North Carolina

From 2014 through 2018, inventors in North Carolina received, on average, 3,861 patents per year. Over this time, assignees were most frequently:

§ Companies/universities in other states: 44%

§ Private-sector companies headquartered in NC: 33%

§ International assignees: 19%§ Universities in NC: 5%

Patents Granted to North Carolina Inventors, Assignee(2014–2018)

Source: U.S. Patent and Trademark Office. Inventors are those credited with the intellectual property and having a North Carolina address listed on the patent. Assignees are those who retain exclusive commercial rights to the patent such as a company or university.

3,900 3,796 3,849 4,0013,762

2014 2015 2016 2017 2018

Universities in NC

InternationalAssigneesPrivate Sector: NCHeadquartersAssignees in OtherStates

Patent Assignees

Private-sector companies headquartered in NC make up 33% of patents granted, with some of the largest located in the Innovation Corridor. Common technologies include:

§ Data analytics, computing, calculating, and counting

§ Medical or veterinary science, hygiene

§ Electronic communication§ Basic electric elements

Company Patents

Cree (Durham) 673Bank of America, Inc. (Charlotte) 558

Red Hat (Raleigh) 330Corning Optical Communications & Corning Cable Systems (Hickory) 309

Qorvo and RF Micro Devices (Greensboro) 223

SAS Institute (Cary) 216RJ Reynolds Tobacco (Winston-Salem) 142

Patents Granted to Companies Headquartered in NCPatents Granted to North Carolina Inventors

Private-Sector Assignees, 2014–2018Innovation Corridor HQs in bold

Source: U.S. Patent and Trademark Office.

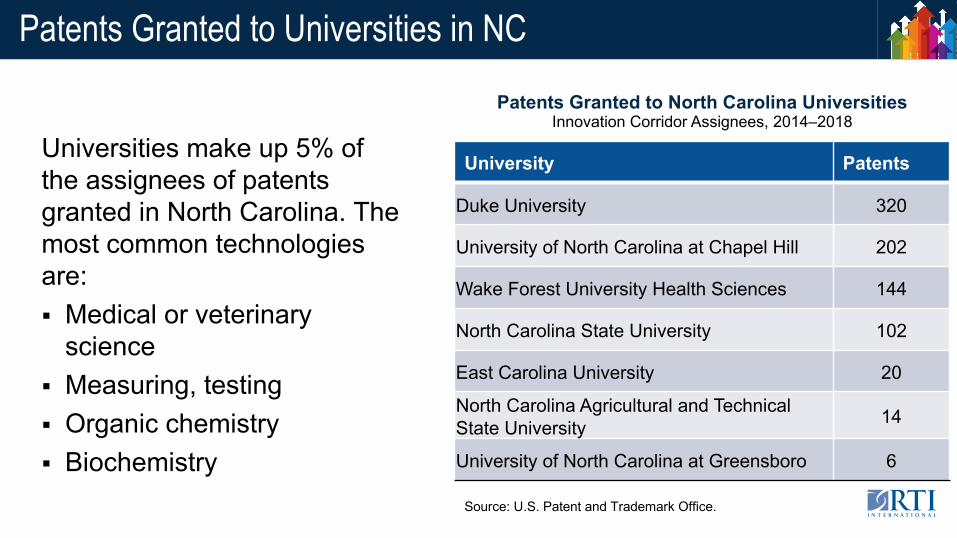

Universities make up 5% of the assignees of patents granted in North Carolina. The most common technologies are: § Medical or veterinary

North Carolina Agricultural and Technical State University 14

University of North Carolina at Greensboro 6

Patents Granted to Universities in NC

Patents Granted to North Carolina UniversitiesInnovation Corridor Assignees, 2014–2018

Source: U.S. Patent and Trademark Office.

Assignees headquartered outside of North Carolina make up the largest percentage of patents (53%).

Large domestic technology (IBM, Cisco, Qualcomm) and international (Lenovo, Ericsson) firms make up the largest portion of patents granted.

Assignee PatentsIBM 3,041

Lenovo 995

Cisco Technology, Inc. 257

QUALCOMM Incorporated 222

Telefonaktiebolaget LM Ericsson 162

NetApp, Inc. 143

EMC Corporation 133

NVIDIA Corporation 108

BorgWarner Inc. 95

Cook Medical Technologies LLC 94

Domestic and International PatentsPatents Granted to North Carolina Inventors

Assignees outside of North Carolina, 2014–2018

Source: U.S. Patent and Trademark Office.

Based on trends in CPC Codes for patents granted from 2014 through 2018, several themes emerged: § Prominent technology areas

include data processing and analytics and medical technology

§ Recent growth in IP production provides a snapshot of future technology areas including power electronics and gene therapy.

§ Some traditional technology areas are declining, including microelectronics and wired telephone technology.

Recent Growth (2014–2018) § Power electronics§ Health care informatics§ Wireless communication, signaling§ Gene therapy, microorganisms

Established But Declining Areas (2014–2018)§ Data analytics*§ Microelectronics, semiconductors§ Electric transmission and wired telephone technology§ Optical systems

*Companies are choosing to maintain trade secrets rather than patent and disclose in data analytics and software, contributing to some of the decline in the number of patents.

Technology Types

Source: U.S. Patent and Trademark Office.

Startup Capital: All Recent DealsTotal Value of Funding Deals, by Sector

Millions of Dollars, 2017–2018In 2017–2018, startups in the Innovation Corridor raised a total of $2.5 billion in funding across all rounds.• Over 99% of funding went to

firms headquartered in the Research Triangle Region; Durham, Raleigh, Morrisville, and Cary accounted for 645 total deals over 2 years.

IT is the largest recipient of venture funding in the region.• Cary-based Epic Games’ $1.2

billion deal in 2018 accounted for 76% of the deal value in IT and 50% of the total deal value.

Source: Pitchbook.

$1,587

$480

$305

$69 $51$6

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

InformationTechnology

Healthcare BusinessProducts and

Services (B2B)

Materials andResources

ConsumerProducts and

Services (B2C)

FinancialServices

Large late-stage deals, including the 2018 Epic Games deal, make IT the largest recipient of venture funding in the region.

However, the largest percentage of early-stage funding in the Innovation Corridor is going to startups in health care, which include life science and bioscience startups.

Early-stage health care startups raised over $208 million in 61 unique deals in 2017–2018 from private funders, federal grants, local institutions, and academic sources.

Startup Capital: Early-Stage Funding

6.62.3 12.2 9.4 9.4 3.2

1.112.4

29.2

163.8

64.9

31.4

$0

$50

$100

$150

$200

$250

Healthcare InformationTechnology

BusinessProducts and

Services(B2B)

ConsumerProducts and

Services(B2C)

Healthcare InformationTechnology

Materials andResources

Greensboro-Winston-Salem-High Point

Raleigh-Durham-Chapel Hill

Tota

l Val

ue o

f Ear

ly-S

tage

Fun

ding

Dea

ls (m

illion

s $)

Grant

Early Stage VC

Accelerator/Incubator

Seed Round

Angel (individual)

Product Crowdfunding

Value of Early-Stage Funding Deals, by SectorMillions of Dollars, 2017–2018

Source: Pitchbook.

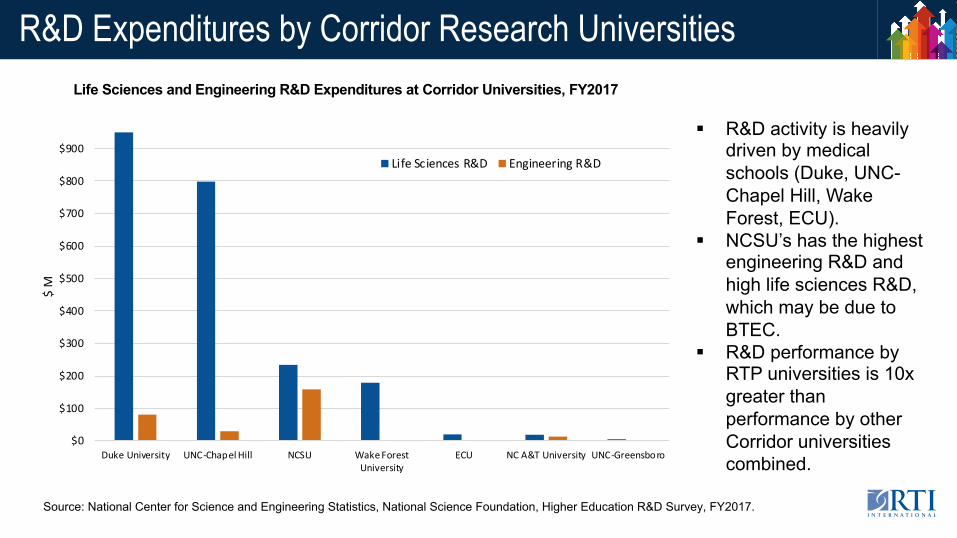

R&D Expenditures by Corridor Research Universities

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Duke University UNC-Chapel Hill NCSU Wake ForestUniversity

ECU NC A&T University UNC-Greensboro

$ M

Life Sciences R&D Engineering R&D

§ R&D activity is heavily driven by medical schools (Duke, UNC-Chapel Hill, Wake Forest, ECU).

§ NCSU’s has the highest engineering R&D and high life sciences R&D, which may be due to BTEC.

§ R&D performance by RTP universities is 10x greater than performance by other Corridor universities combined.

Life Sciences and Engineering R&D Expenditures at Corridor Universities, FY2017

Source: National Center for Science and Engineering Statistics, National Science Foundation, Higher Education R&D Survey, FY2017.

Tech Transfer Metrics for Corridor Research Universities

§ Licensing activity indicates industry demand for technology that has commercial potential.

§ Nationally, universities with medical schools or engineering schools and higher shares of industry-sponsored R&D have more licensing activity and income.

§ Universities with similar total R&D can have very different licensing activity:– Duke issues 2x as many licenses and

generated 10x as much licensing revenue as UNC-Chapel Hill.

– ECU issued the same number of licenses, on average, as UNC-Greensboro but generated 4x the licensing income/$1M R&D expenditures.

FY2015–2017 Average

InstitutionMed

SchoolTotal R&D Exp ($M)

Industry/ Total R&D Exp (%)

Avg Annual

Licenses Issued

Licenses/$10M

R&D Exp

Gross Licensing

Income ($M)

Licensing Income/$1M

R&D Exp

Duke University Yes $1,073.1 22.0% 108 1.0 $38.5 $35,888

UNC-Chapel Hill Yes $1,038.1 3.3% 59 0.6 $3.9 $3,729

NCSU No $486.2 12.4% 91 1.9 $5.3 $10,895

ECU Yes $26.0 9.0% 5 1.8 $0.23 $9,048

UNC-Greensboro no $22.6 1.2% 5 2.2 $0.06 $2,918

Note: AUTM data were not available for Wake Forest and North Carolina A&T University. Source: National Science Foundation, Higher Education R&D Survey, FY2015–FY2017; Association of University Technology Managers, STATT Database, FY2015–FY2017 or latest available year.

R&D Expenditures and Licensing at Corridor Universities, FY2015–2017 Averages

§ NCSU stands out for executing a similar number of licenses as Duke with less than half the R&D expenditures. The income generated from these licenses is one-third of Duke’s but 3x that of UNC-Chapel Hill.

§ Duke’s licenses for blockbuster drugs is a big reason for the skewed licensing income.

R&D and Tech Transfer by Corridor Research Universities

Year InstitutionMed

SchoolNational Rank

in R&DTotal R&D Exp ($M)

Industry R&D Exp ($M)

Industry/ Total R&D

ExpLicenses Executed

Licenses/$10M R&D

Exp

Gross Licensing

Income

Licensing Income/

$1M R&D Exp

$1M+ Licenses

2017 Duke University Yes 8 $1,126.9 $234.8 20.8% 97 0.9 $44,562,379 $39,543 4.0

Note: AUTM data were not available for Wake Forest and North Carolina A&T University. Source: National Center for Sciences and Engineering Statistics, National Science Foundation, Higher Education R&D Survey, FY2015–FY2017; Association of University Technology Managers, STATT Database, FY2015–FY2017 or latest available year.

Data Definitions and Limitations

Data Sources

RTI analyzed each region’s industry base, employment levels, wage profiles, incomes, occupations, and educational pipeline using publicly available data from:

§ U.S. Bureau of Economic Analysis, Regional Economic Accounts§ U.S. Bureau of Labor Statistics, Occupational Employment Statistics§ U.S. Bureau of Labor Statistics, Quarterly Census of Wages§ U.S. Census Bureau, Census Reporter§ U.S. Department of Education, Integrated Postsecondary Education

Data System

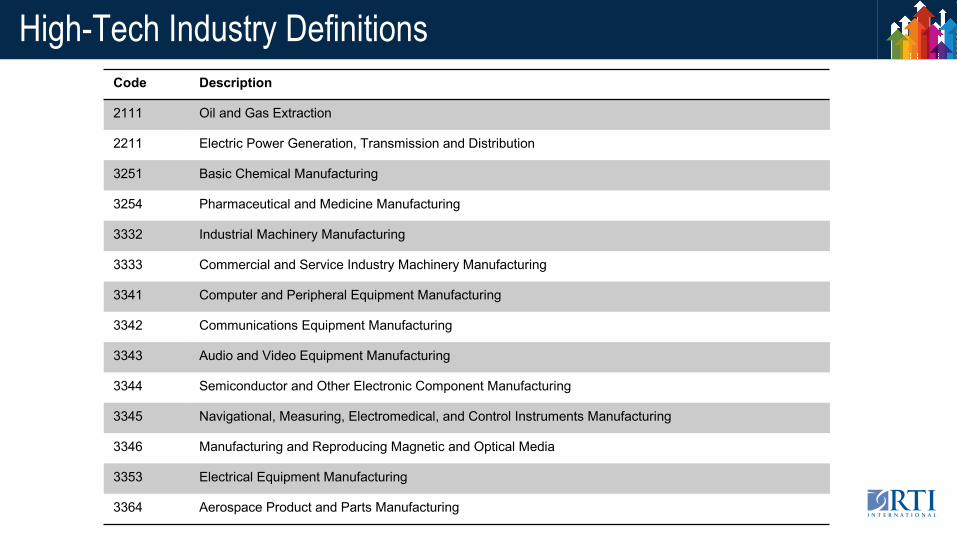

High-Tech Industry DefinitionsCode Description

2111 Oil and Gas Extraction

2211 Electric Power Generation, Transmission and Distribution

3251 Basic Chemical Manufacturing

3254 Pharmaceutical and Medicine Manufacturing

3332 Industrial Machinery Manufacturing

3333 Commercial and Service Industry Machinery Manufacturing

3341 Computer and Peripheral Equipment Manufacturing

3342 Communications Equipment Manufacturing

3343 Audio and Video Equipment Manufacturing

3344 Semiconductor and Other Electronic Component Manufacturing

3345 Navigational, Measuring, Electromedical, and Control Instruments Manufacturing

3346 Manufacturing and Reproducing Magnetic and Optical Media

3353 Electrical Equipment Manufacturing

3364 Aerospace Product and Parts Manufacturing

High-Tech Industry Definitions, Continued Code Description

4861 Pipeline Transportation of Crude Oil

4862 Pipeline Transportation of Natural Gas

4869 Other Pipeline Transportation

5112 Software Publishers

5173 Wired and Wireless Telecommunications Carriers

5174 Satellite Telecommunications

5179 Other Telecommunications

5182 Data Processing, Hosting, and Related Services

5191 Other Information Services

5413 Architectural, Engineering, and Related Services

5415 Computer Systems Design and Related Services

5416 Management, Scientific, and Technical Consulting Services

5417 Scientific Research and Development Services

5511 Management of Companies and Enterprises

Data Limitations

§ Analyzed the CSA for each region, which comprises major MSAs (i.e., Greensboro-High Point, Rocky Mount, Greenville, Raleigh, Durham-Chapel Hill) and adjacent counties with lower population levels.

§ A key limitation is that industry employment and occupation data are often suppressed to protect the identify of individual employers, especially if there are one or two major employers.

§ Data suppression is also an issue at the four-digit NAICS code level. To attempt to circumvent this issue, RTI used Emsi data, which provides data for proprietors and self-employed individuals and employment estimates for major employers.