16

Innovation Day 2018 Curt Espeland Executive Vice President and Chief Financial Officer

Innovation Day 2018

Curt EspelandExecutive Vice President and Chief Financial Officer

During these presentations, we make certain forward-looking statements concerning plans and expectations for Eastman Chemical Company. We caution you that actual events or

results may differ materially from our plans and expectations. Throughout these presentations, “F” is used to indicate projected, or “forecasted”, amounts. See Eastman’s most recent

Form 10-K and 10-Q filings with the Securities and Exchange Commission and these slides and the remarks in the presentations for risks and uncertainties which could cause actual

results to differ materially from current expectations.

Forward-looking statements

Non-GAAP financial measuresAll earnings measures in these presentations are non-GAAP and exclude certain non-core and unusual items. Full-year 2017 amounts are from our February 1 and 2 public

disclosures of our 2017 financial results but will be final when we file our 2017 Form 10-K with the SEC.

“Adjusted Net Income” is “Net Income” adjusted to exclude the same non-core and any unusual or non-recurring items as are excluded from the Company's other non-GAAP

earnings measures for the same periods.

“Debt to EBITDA” Ratio is defined as Total Debt divided by Adjusted EBITDA.

“Diversified Peers” are BASF, CE, HUN.

“EBITDA” is net earnings or net earnings per share before interest, taxes, depreciation and amortization adjusted to exclude the same non-core and any unusual or non-recurring

items as are excluded from the Company's other non-GAAP earnings measures for the same periods. “EBITDA Margin” is EBITDA divided by the GAAP measure sales revenue

in the Company’s income statement for the period presented. Information concerning use of the non-GAAP measures. Projections of future Adjusted EBITDA and EBITDA

Margin also exclude any non-core or non-recurring items.

“Free cash flow” is cash provided by operating activities less cash used for additions to properties and equipment, both the GAAP measures in the Company’s statements of

cash flows for the period presented. Information concerning use of the non-GAAP measure free cash flow is available in the Company’s Form 10-Q for third quarter 2017.

“Adjusted Free Cash Flow” is cash provided by operating activities excluding non-core or unusual items less cash used for additions to properties and equipment.

“Free cash flow conversion” is Adjusted Free Cash Flow divided by Adjusted Net Income.

“IRR” is the Internal Rate of Return calculated based on 10-year project cash flow assumptions.

“Return on Invested Capital” (or “ROIC”) is adjusted net income plus interest expense after tax divided by average total borrowings plus average stockholders’ equity for the

period presented, each derived from the GAAP measures in the Company’s financial statements for the periods presented.

“Specialty Peers” are ALB, ASH, FMC, IFF, PPG.

“Variable Margin” defined as GAAP measure sales revenue in the Company’s income statement for the period presented minus total raw material costs, total purchased energy

costs, and variable distribution costs divided by the GAAP measure sales revenue in the Company’s income statement for the period presented.

“Operating Margin” defined as operating earnings divided by the GAAP measure sales revenue in the Company’s income statement for the period presented.

Reconciliations to the most directly comparable GAAP financial measures and other associated disclosures, including a description of the excluded and adjusted items, are available

in the Appendix and in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Forms 10-K and 10-Q filed and Forms 8-K

furnished and filed with the SEC for the periods for which non-GAAP financial measures are presented. Projected future earnings exclude any non-core, unusual, or non-recurring

items, and projections of future earnings per share assume that the adjusted tax rate for the most recent completed period will be the actual tax rate for the projected periods. Unless

otherwise indicated, except for earnings per share, all dollar amounts are millions “($M)” or billions “($B)”.

Here’s what you’ve heard today

World-Class

Technology

Platforms

Relentlessly

Engage

the Market

Differentiated

Application

Development

ADDITIVES & FUNCTIONAL PRODUCTS ADVANCED MATERIALS FIBERS

OPERATING

MARGIN

~20%

OPERATING

EARNINGS

CAGR

5%–7%2018–2020

REVENUE

GROWTH

mid-single

digits

OPERATING

MARGIN

~20%

OPERATING

EARNINGS

CAGR

7%–10%2018–2020

REVENUE

GROWTH

mid-single

digits

OPERATING

MARGIN

>25%

OPERATING

EARNINGS

CAGR

1%–3% 2018–2020

REVENUE

GROWTH

low-single

digits

Significant integration and scale enable innovation, reliability and cost advantage

Advantaged growth and execution capability and culture

Aggressive and disciplined portfolio management

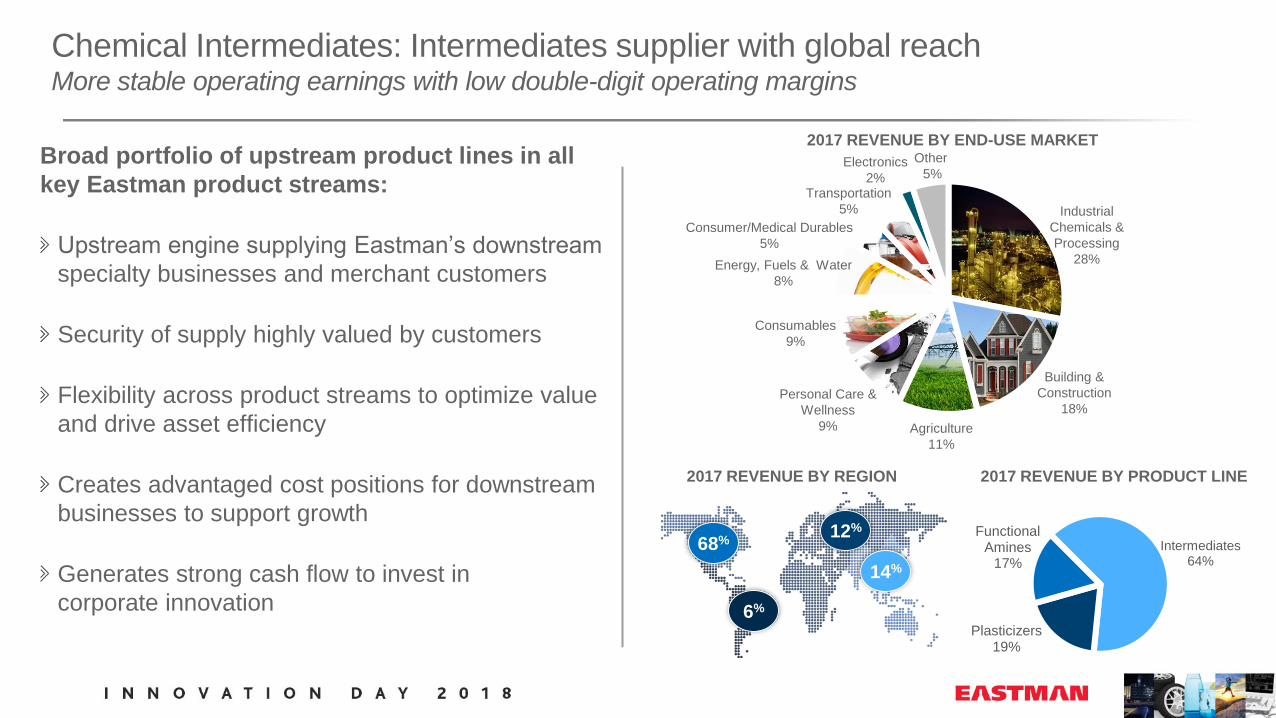

Chemical Intermediates: Intermediates supplier with global reachMore stable operating earnings with low double-digit operating margins

68%

14%

6%

12%

Intermediates64%

Plasticizers19%

Functional Amines

17%

2017 REVENUE BY PRODUCT LINE2017 REVENUE BY REGION

2017 REVENUE BY END-USE MARKETOther

5%

Industrial

Chemicals &

Processing

28%

Building &

Construction

18%Personal Care &

Wellness

9% Agriculture

11%

Consumables

9%

Energy, Fuels & Water

8%

Consumer/Medical Durables

5%

Transportation

5%

Electronics

2%

Broad portfolio of upstream product lines in all

key Eastman product streams:

Upstream engine supplying Eastman’s downstream

specialty businesses and merchant customers

Security of supply highly valued by customers

Flexibility across product streams to optimize value

and drive asset efficiency

Creates advantaged cost positions for downstream

businesses to support growth

Generates strong cash flow to invest in

corporate innovation

Above end-market growth that is sustainable

Key assumptions

Macroeconomic growth similar to 2017:

Industrial production growth to average ~2.5%

Stable oil:

Brent crude oil price forecast $60–$70 per barrel

Stable currencies:

U.S. dollar to Euro exchange rate expected to be ~$1.20

Eastman tax rate expected to be 18%–20%

0%

5%

10%

15%

20%

25%

30%

EMN ALB FMC ASH GRA IFF0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016 2017

Cu

mu

lati

ve

cap

ac

ity i

ncre

as

e (

kM

T)

Crystex Acetyl Stream Olefins

Oxo Aldehydes Polymer Intermediates Copolyesters

PVB Resin

Continued success with productivity and aggressive cost management

LEVERAGING TECHNICAL CAPABILITIES TO INCREASE

CAPACITY THROUGH PRODUCTIVITY/DEBOTTLENECKING

SGA+R&D/REVENUE

RELATIVE TO SPECIALTY PEERS

(2013–2017 average)

Note: 2017 represents mean of available sell-side equity analysts’ estimates for peer companies

as of 12/31/2017.

0%

4%

8%

12%

EMN Specialty Diversified

RETURN ON INVESTED CAPITAL(2015-2017 average)

0%

20%

40%

60%

80%

100%

EMN Specialty Diversified

FREE CASH FLOW CONVERSION(2015–2017 average)

0%

4%

8%

12%

EMN Specialty Diversified

EPS CAGR(2010–2017)

0%

5%

10%

15%

20%

25%

EMN Specialty Diversified

EBITDA MARGIN(2015–2017 average)

Established track record of creating value1,2

1) Source: Bloomberg, Nasdaq, and company filings. Refer to non-GAAP financial measures of Forward-Looking Statements slide for peer listing.

2) 2017 represents analyst mean estimate for peer companies as of 12/31/2017

Operating cash flow growing

with our businesses

Will continue working capital

discipline in line with growth

2018 operating cash flow

negatively impacted by coal

gas incident

$0

$300

$600

$900

$1,200

$1,500

$1,800

2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F

Strong and growing cash from operations driven by continued

growth in corporate earnings

OPERATING CASH FLOW 2010–2020F

$M

$0

$100

$200

$300

$400

$500

$600

$700

2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F

Maintenance & incremental growth Growth Incident

% of

sales4% 6% 6% 5% 6% 7% 7% 6% 5% 5% 5%

Targeted capital expenditures funding organic growth

and maintenance

Annual maintenance capital

expected to be $300–$350 million

Will continue to fund targeted

growth initiatives

Anticipate future projects will be

driven by innovation and other

growth programs

Recent examples include TritanTM,

CrystexTM, PVB resin, and ketones

Expected return on growth

investments of 10%–15%+

CAPITAL EXPENDITURES 2010–2020F

$M

10

Acquisitions improve and sustain earnings and free cash flow profile

9–10x EBITDAAcquisition multiple

Corporate tax rate

34%20%>90% key talent retained

11%-13%

post-

completion

IRREMN FCF/Revenue 2%>10%

>$160M cost synergies

Increased breadth

and scale of

innovation

programs

$0

$300

$600

$900

$1,200

$1,500

2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F

Free cash flow over next 3 years expected to be ~$3.5 billion

FREE CASH FLOW 2010–2020F

$M

Expect to fully deploy free cash flow

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2014 2015 2016 2017 2018F 2019F 2020F

Maintain investment-grade credit rating that provides financial flexibility

to invest in growth and reward stockholders

TOTAL DEBT

Expect ~2.5x debt to EBITDA ratio in next 12 to 24 months

$M

Strong balance sheet and sufficient liquidity

$0

$400

$800

$1,200

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2042 2044

Remain committed to investment-grade

credit rating

Expect to delever over next

12–24 months

Manageable debt maturities

in 2019 and 2020

Sources of liquidity:

$1.25 billion revolver

$300 million accounts receivable

securitization program

Meaningful return of cash to stockholders

PUBLIC DEBT MATURITIES

Combination of cash flow generation, strong balance sheet, and liquidity

provides flexibility to pursue growth

$M

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2010 2011 2012 2013 2014 2015 2016 2017 2018F

Long history of returning capital to stockholders

$0

$200

$400

$600

$800

2013 2014 2015 2016 2017 2018F

Dividends Share repurchases

DIVIDENDS PER SHARE CAGR ~13%

(2010–2017)

$2.4B OF CAPITAL RETURNED TO STOCKHOLDERS

(2013–2017)

$M

New $2B share repurchase authorization

Innovation-

Driven

Growth

Earnings

ROICCash flow

A sustained high level of returns as the company grows

0%

5%

10%

15%

20%

2017 2020F

Expect ROIC of 10%–15% as the company grows in a disciplined manner

RETURN ON INVESTED CAPITAL (ROIC)

Position of strength

Expect to generate free cash flow approaching ~$3.5 billion 2018–2020

Maintain capital structure that provides financial flexibility to invest for growth

and reward stockholders

Strong balance sheet and sufficient liquidity foundation for growth

Continue to improve ROIC with an expectation to return 10%–15%

Strong execution track record enables sustainable value creation