40

Innovation Economy Outlook UK 2014 Report

| Date post: | 14-Jul-2015 |

| Category: |

Business |

| Upload: | silicon-valley-bank |

| View: | 271 times |

| Download: | 0 times |

Innovation EconomyOutlook UK

2014 Report

Welcome to Innovation Economy Outlook 2014, Silicon Valley Bank’s annual study of executives’ perceptions

in the innovation sector. Each year, we take the pulse of these businesses to find out how they’re doing, from past performance to future prospects, and the challenges and opportunities they foresee.

This year we expanded our survey to include businesses in innovation centres around the world and, in addition to start-ups, larger businesses with revenues upward of $1 billion USD. I’m pleased to offer the most comprehensive look yet at the state of the global innovation economy, with insights reflecting the more than 1,200 survey responses.

Our prognosis is, in a word, momentum. We see abundant potential in the pace of new business formation, global expansion and availability of capital, and the emergence of new products and solutions that will change the world.

Many of the executives surveyed are SVB clients, which should come as no surprise to those of you who know us. SVB is the bank for half of all venture capital-backed technology and life science businesses in the United States, two-thirds of those businesses that went public in 2013 and a majority of the investors who fund them. The make-up of our client base is growing increasingly global and has expanded over the years to serve businesses of all sizes.

As the bank of the global innovation economy, we are committed to bringing clients the connections and tailored financial solutions they need to succeed. We also consider ourselves champions for innovation. With studies like this one, we can build a better understanding of what it takes to disrupt an industry or launch a high-growth business. And with that knowledge, we can help create a better environment in which all innovators can thrive.

Thanks for taking a look at this year’s report. Reading between the statistics, insights and observations, you’ll find stories of the phenomenal intelligence, courage and determination it takes to build a successful business.

Greg Becker President and Chief Executive Officer Silicon Valley Bank and SVB Financial Group

Letter from the CEO

INNOVATION ECONOMY OUTLOOK UK REPORT 2014INNOVATION ECONOMY OUTLOOK UK REPORT 2014

3 Executive summary

4 Report at a glance

3Introduction

6 The UK innovation economy hits its stride

9 2013 in review

11 2014: A look ahead

13 Building from the core

15 Managing capital with realistic expectations

20 Growth means jobs

6Hitting its stride

22 The challenge: Scaling up

27 Connecting to the global innovation economy

32 Seizing the opportunity at hand

22Scaling up

27Connecting

34 About Silicon Valley Bank’s Innovation Economy Outlook 2014

36 A snapshot of survey respondents

34About this report

CON

TEN

TS

INNOVATION ECONOMY OUTLOOK UK REPORT 2014INNOVATION ECONOMY OUTLOOK UK REPORT 2014

If the UK can meet the needs of rapidly growing innovation economy businesses at home and help them tap into global markets, it will reap the benefits of jobs and economic growth.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014INNOVATION ECONOMY OUTLOOK UK REPORT 2014

Executive summaryHeading into 2014, the UK innovation ecosystem,

though young, is vigorous and filled with promise. Three-quarters of the executives surveyed say their business met or beat their 2013 revenue targets. Eight in 10 think business conditions will continue to improve in 2014.

In 2014, UK executives see opportunities in offering new products, entering new markets and increasing their size and scale. This momentum translates into jobs. Eighty-four percent of this year’s respondents plan to grow their workforce in the coming year, outpacing even their peers in the United States.

On a variety of fronts – 2013 performance, 2014 outlook and 2014 views on the fundraising situation – UK executives show they have learnt to manage their businesses and their expectations to reflect the capital available in the UK market.

The foundation has been laid for a vibrant UK innovation economy. What then does the future hold?

In the following pages, we explore the views of respondents to our annual Innovation Economy Outlook survey, including executives from rapidly growing businesses in the software, hardware, healthcare and cleantech sectors. We also examine the opportunities and obstacles facing businesses in the UK, and compare them to what US businesses are seeing.

UK innovation economy executives say their two biggest challenges in 2014 are scaling their operations and recruiting and managing talent. While the vast majority of businesses want to hire, virtually all executives have a difficult time finding people with the skills and experience they need.

For the UK economy, the opportunity is clear. If the UK can meet the needs of rapidly growing innovation economy businesses at home and help them tap into global markets, it will reap the benefits of jobs and economic growth.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 3INNOVATION ECONOMY OUTLOOK UK REPORT 2014 3

HIG

HLI

GH

TSOptimism follows strong 2013. Three-quarters of surveyed UK executives say their business met or beat 2013 revenue targets, and 8 in 10 think business conditions will be even better in 2014.

Growth will come from the core. Growth is expected to stem from new products, new markets and scaling operations.

Capital and talent are essential to take the UK innovation economy to the next level. UK businesses must find the capital and the means to meet their top challenges – scaling operations and recruiting and managing talent – if the innovation economy is to reach its full potential.

The UK innovation economy hits its stride

The challenge: Scaling up Connecting to the global innovation economy

UK businesses have a global perspective on growth. Although UK businesses look first to the UK for 2014 growth, the United States is not far behind. Hiring patterns track these growth aspirations. Overall, UK businesses are more internationally focused than their US peers.

Report at a glanceH

IGH

LIG

HTS 1 2 3

Growth means jobs. More than 8 in 10 surveyed UK executives – even more than in the United States – expect their business will grow in 2014. Young businesses are growing the fastest. At the median, young businesses expect to double in size.

Business conditions outlook

40%39%

19%

2%

Business conditions outlook2014 VS. 2013 (UK)

Much better

Somewhat better

About the same

Somewhat worse

Greatest opportunities in 2014

New products or

markets

Scaling operations

Business conditions in existing

markets

Access to equity

M&A

35%

30%

25%

20%

15%

10%

5%

0%

37%

Top hiring locations◻ UK◻ US◻ Western Europe◻ Eastern Europe

1%

9%

1%

89%36%

UK US

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 4INNOVATION ECONOMY OUTLOOK UK REPORT 2014 4

Overall, UK innovation economy businesses are more internationally focused than

their US peers.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 5INNOVATION ECONOMY OUTLOOK UK REPORT 2014 5

A vibrant innovation economy starts with entrepreneurs – people with ideas and the passion to turn those ideas into breakout businesses. In turn, those entrepreneurs benefit from the resources available in a vibrant innovation economy – talent, capital and a supportive business environment. This ecosystem provides what entrepreneurs need for success.

Five years ago, in the midst of a financial downturn, the outlook for the UK innovation

economy was uncertain.

A January 2009 survey of 80 UK-based venture capitalists found two-thirds believed the fundraising environment was more difficult than it had been for a decade or longer. Three-quarters of respondents thought venture investments would decrease, and half thought the drop would be significant. Eighty-eight percent said it was difficult or impossible to raise B and C rounds for their businesses – a particularly dire view, since they also believed that over half of their portfolio businesses could not survive the coming year without raising new equity capital.1

In the words of Jeremy Hand, chairman of the British Private Equity & Venture Capital Association, “Survival prospects for many early-stage businesses and investments [were] extremely uncertain,” as “the venture capital market in the UK, in contrast to the US, [had] not achieved the critical mass necessary to fund an appropriate proportion of the most promising and innovative businesses through all stages of their development.”2

Today, the picture is remarkably different. During 2013, the UK reaffirmed its standing as the European destination of choice in the global market for venture capital, with £1.2 billion flowing into UK businesses, up 13 percent from 2012. More important is that the overall ecosystem has moved from fragile to firm.

9 2 0 1 3 I N R E V I E W

1 1 2 0 1 4 : A L O O K A H E A D

1 3 B U I L D I N G F R O M T H E C O R E

1 5 M A N A G I N G C A P I T A L W I T H R E A L I S T I C E X P E C T A T I O N S

2 0 G R O W T H M E A N S J O B S

The UK innovation economy hits its stride

CHA

PTER

1 Silicon Valley Bank’sInnovation Economy Outlook 2014 UK Report

1 British Private Equity & Venture Capital Association, “BVCA/Populus: Venture Capital Outlook Survey 2009,” www.bvca.co.uk/ResearchPublications/ResearchReports/BVCAPopulusVentureCapitalOutlookSurvey.aspx.

2 British Private Equity & Venture Capital Association, “Benchmarking UK Venture Capital to the US and Israel: What lessons can be learned?” www.bvca.co.uk/Portals/0/library/Files/News/2008/2008_0008_benchmarking_uk_vc_to_israel_and_us.pdf.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 6

CONTINUED ON 7

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 6

CONTINUED ON 7

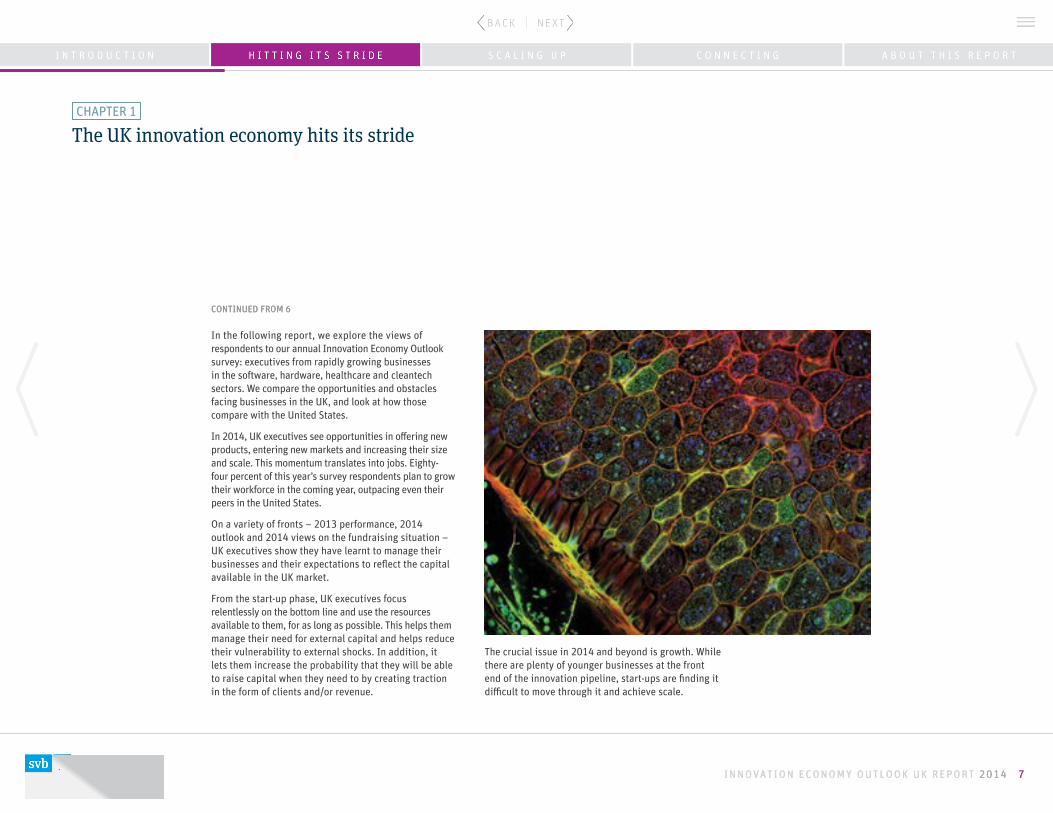

In the following report, we explore the views of respondents to our annual Innovation Economy Outlook survey: executives from rapidly growing businesses in the software, hardware, healthcare and cleantech sectors. We compare the opportunities and obstacles facing businesses in the UK, and look at how those compare with the United States.

In 2014, UK executives see opportunities in offering new products, entering new markets and increasing their size and scale. This momentum translates into jobs. Eighty-four percent of this year’s survey respondents plan to grow their workforce in the coming year, outpacing even their peers in the United States.

On a variety of fronts – 2013 performance, 2014 outlook and 2014 views on the fundraising situation – UK executives show they have learnt to manage their businesses and their expectations to reflect the capital available in the UK market.

From the start-up phase, UK executives focus relentlessly on the bottom line and use the resources available to them, for as long as possible. This helps them manage their need for external capital and helps reduce their vulnerability to external shocks. In addition, it lets them increase the probability that they will be able to raise capital when they need to by creating traction in the form of clients and/or revenue.

The crucial issue in 2014 and beyond is growth. While there are plenty of younger businesses at the front end of the innovation pipeline, start-ups are finding it difficult to move through it and achieve scale.

The UK innovation economy hits its strideCHAPTER 1

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 7

CONTINUED FROM 6

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 7

CONTINUED FROM 6

The UK innovation economy hits its strideCHAPTER 1

AMOUNT INVESTED

MILLIONS OF POUNDS

2007 2008 2009 2010 2011 2012 2013

£2,000

£1,500

£1,000

£500

£0

600

500

400

300

200

100

0

Source: British Private Equity & Venture Capital Association

NUMBER OF DEALS

UK venture capital investments: 2007-2013

532

414

350375

367 367347

£1,347

£1,152

£900

£1,604

£1,328 £1,222£1,377

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 8INNOVATION ECONOMY OUTLOOK UK REPORT 2014 8

The innovation economy businesses in this year’s survey performed well in 2013. Seventy-seven percent of executives say they met or beat their revenue targets. This is an even stronger showing than in the US survey, where 65 percent report meeting or exceeding targets.

Most of the businesses that beat targets did so by between 1 and 20 percent, with 40 percent of

businesses even exceeding that performance. That compares with 33 percent of US executives who beat targets by more than 20 percent. At the median, UK executives beat targets by 20 percent, compared with 15 percent among US executives.

Strong performance by UK innovation economy businesses in 2013 partly reflects the fact that UK businesses generally had a good year. We also think it reflects the fact that UK entrepreneurs are realistic or even conservative in forecasting future performance. In fact, we think that the common UK executive approach to goal setting may account for the differences between the UK and US results.

2013 in reviewMeeting and beating revenue targets 2013

UK US

0 %

10 %

20 %

30 %

40 %

50 %

60 %

Revenues were above target

Revenues were roughly on target

Revenues were below target

60%

50%

40%

30%

20%

10%

0%

54%

44%

23%21% 23%

35%

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 9

CONTINUED ON 10

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 9

CONTINUED ON 10

Conservatism appears to be a healthy strategy. UK executives and investors understand the need to manage growth with limited private capital. They also remember the sobering lessons of the 2009 financial downturn. As a result, they tend to raise seed capital and then focus on generating revenue and reaching profitability.

This approach may also have a cultural component. The UK ecosystem tends to echo the swings in the US innovation economy. Optimism (and, when it comes, pessimism) tends to take hold first in the United States and then radiate outward, with the highs in the UK never quite as high and the lows never quite as low as those in the United States.

2013 in reviewCHAPTER 1

Annual venture capital investment by geographic focus

2007 2008 2009 2010 2011 2012 2013

2007-2013 (ALL SECTORS)

◻ US◻ Europe ◻ Asia◻ Others

$60

$50

$40

$30

$20

$10

$0

Source: Dow Jones VentureSource

AMOUNT INVESTED (BILLIONS OF DOLLARS)

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 10

CONTINUED FROM 9

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 10

CONTINUED FROM 9

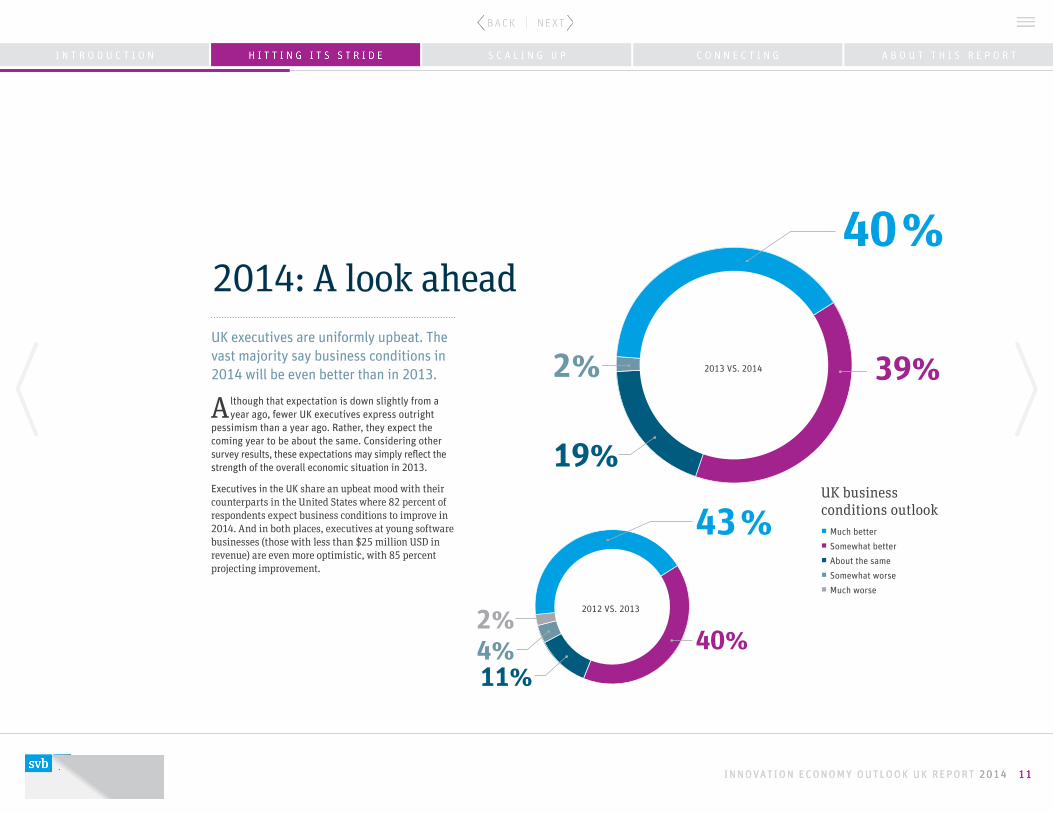

UK executives are uniformly upbeat. The vast majority say business conditions in 2014 will be even better than in 2013.

A lthough that expectation is down slightly from a year ago, fewer UK executives express outright

pessimism than a year ago. Rather, they expect the coming year to be about the same. Considering other survey results, these expectations may simply reflect the strength of the overall economic situation in 2013.

Executives in the UK share an upbeat mood with their counterparts in the United States where 82 percent of respondents expect business conditions to improve in 2014. And in both places, executives at young software businesses (those with less than $25 million USD in revenue) are even more optimistic, with 85 percent projecting improvement.

2014: A look ahead40 %

2%

19%

39%

43 %

2%4% 40%

11%

2012 VS. 2013

2013 VS. 2014

UK business conditions outlook◻ Much better◻ Somewhat better◻ About the same◻ Somewhat worse◻ Much worse

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 11INNOVATION ECONOMY OUTLOOK UK REPORT 2014 11

Executives at young software businesses

(those with less than $25 million USD in

revenue) are even more optimistic, with 85 percent

projecting improvement.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 12INNOVATION ECONOMY OUTLOOK UK REPORT 2014 12

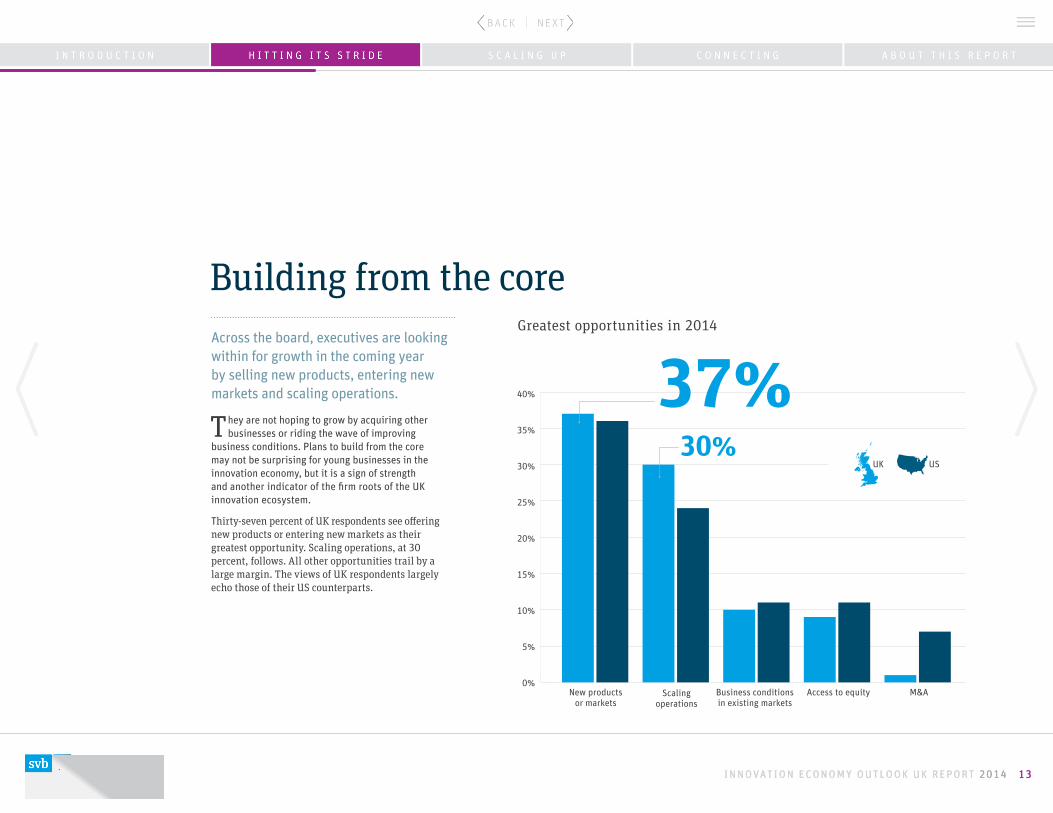

Across the board, executives are looking within for growth in the coming year by selling new products, entering new markets and scaling operations.

They are not hoping to grow by acquiring other businesses or riding the wave of improving

business conditions. Plans to build from the core may not be surprising for young businesses in the innovation economy, but it is a sign of strength and another indicator of the firm roots of the UK innovation ecosystem.

Thirty-seven percent of UK respondents see offering new products or entering new markets as their greatest opportunity. Scaling operations, at 30 percent, follows. All other opportunities trail by a large margin. The views of UK respondents largely echo those of their US counterparts.

Building from the core

40%

35%

30%

25%

20%

15%

10%

5%

0%

Greatest opportunities in 2014

M&AAccess to equityBusiness conditions in existing markets

Scaling operations

New products or markets

37% 30%

UK US

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 13INNOVATION ECONOMY OUTLOOK UK REPORT 2014 13

UK executives are uniformly upbeat. The vast majority say

business conditions in 2014 will be

even better than in 2013.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 14INNOVATION ECONOMY OUTLOOK UK REPORT 2014 14

Although UK venture investing has rebounded to the levels we saw before the financial downturn, global venture capital will continue to flow disproportionately to the United States because the United States is a much larger market, and US-focused funds have performed better overall.

Historically, a smaller pool of venture capital for start-ups has been one of the challenges facing the

UK innovation economy. This is not likely to change.

Even so, capital is a positive sign for the UK innovation economy, because executives have learned how to manage their businesses using the resources that are available to them. Entrepreneurs' responses to this year's survey reveal ways that they deal with the reality they face.

Depending on whom you talk to, access to capital is either an opportunity or a challenge. Nine percent of the executives in the UK survey – and 21 percent of early-stage, pre-revenue businesses – see access to equity as an opportunity.

An equity infusion gives growing businesses the cash they need to develop products, hire employees and extend market reach, making it a powerful growth driver for businesses that can raise money successfully and use it effectively.

Managing capital with realistic expectations

CONTINUED ON 17

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 15INNOVATION ECONOMY OUTLOOK UK REPORT 2014 15

Next source of capital

Looking forward, entrepreneurs plan to reduce reliance on angel funding and government grants while increasing use of other funding types.

Type of capital raised

One source of strength for the UK innovation economy is an increasingly vibrant group of angel investors – private individuals, many of whom have been part of successful innovation economy businesses, who invest in very early-stage start-ups.

CHAPTER 1

Managing capital with realistic expectations

Venture capitalAngel investorBank debtPrivate equityCorporate investorCrowdfundingIPOGovernment grantMergerOther

6%2% 1% 1%

5%

Venture capital

Angelinvestor

Privateequity

Corporateinvestor

Governmentgrant

Crowdfunding Other

61% 41%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Source of funding in 2013

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 16INNOVATION ECONOMY OUTLOOK UK REPORT 2014 16

While 15 percent of UK executives say access to equity is their top challenge, this is less than in the United States, where 21 percent call access to equity their top challenge.

Executives at early-stage, pre-revenue businesses are driving the difference in views. Executives at pre-revenue US companies are twice as likely to say access to equity is their top challenge, suggesting intense competition in the United States for early-stage funding, as well as the appetite for capital among US entrepreneurs looking to reach scale quickly in a large market.

Looking at those businesses that raised capital in 2013, or those that tried and failed, offers a more sanguine view of UK entrepreneurs. In both cases, UK executives report better outcomes than their US counterparts.

Fifty-one percent of UK respondents successfully raised equity capital in 2013, slightly more than in the United States. While this pattern played out among both pre-revenue and revenue-generating businesses, the difference was somewhat larger for pre-revenue businesses.

In a similar vein, only 6 percent of UK respondents say they tried unsuccessfully to raise capital, compared with 13 percent in the US survey.

Of the businesses that successfully raised capital in 2013, UK businesses – at both pre-revenue and revenue-generating stages – were much more likely to look internationally than their US peers.

Twenty-one percent of UK executives say they raised capital internationally, compared with just 8 percent in the United States.

UK entrepreneurs also appear to manage with less debt. Only 14 percent of UK respondents, compared with 24 percent of US respondents, say their business obtained a loan or credit financing in 2013. Among pre-revenue businesses, debt was relatively uncommon in both geographies (9 percent in both the UK and US samples). Among revenue-generating businesses, however, one-third of US executives say they took on debt, compared with only 14 percent of UK executives.

Overall, UK executives are significantly more accepting of the fundraising environment than they were in 2013, even though the number of venture capital deals closed in the UK dropped slightly from 2012 to 2013 (from 367 to 347). The percentage of executives who say the fundraising environment is extremely challenging dropped by more than half, while the number saying it is not very challenging more than doubled.

CONTINUED FROM 15

Managing capital with realistic expectationsCHAPTER 1

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 17

CONTINUED ON 18

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 17

CONTINUED ON 18

In fact, UK executives who successfully raised capital in 2013 are less likely than those in the United States to say the fundraising environment is extremely challenging, and more likely to say it is either somewhat challenging or not very challenging.

This UK-US distinction may reflect the fact that there are so many software businesses in the UK sample. US software executives are more positive about the fundraising environment than the overall US sample. Considering the views of revenue-generating software businesses in both geographies with revenues below $25 million USD, for example, the results are quite comparable.

One source of strength for the UK innovation economy is an increasingly vibrant group of angel investors – private individuals, many of whom have been part of successful innovation economy businesses, who invest in very early-stage start-ups. While angel investing is substantial in both the United States and the UK, it was the main source of early-stage investing for the UK respondents in this year’s survey.

UK executives were also more likely to say they received funding from a government grant and less likely to say they received funding from private equity or corporate investors. Looking forward, entrepreneurs plan to reduce reliance on angel funding and government grants while increasing use of other funding types. Fifteen percent of respondents expect to rely on organic growth rather than raising external capital.

Managing capital with realistic expectationsCHAPTER 1

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 18

CONTINUED FROM 17

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 18

CONTINUED FROM 17

Managing capital with realistic expectationsCHAPTER 1

Looking forward, 15 percent of UK executives say access to equity is their top challenge in 2014.

Fifty-one percent of UK respondents raised equity capital in 2013, slightly more than in the US.

Executives’ view of the fundraising environment◻ Not very challenging◻ Somewhat challenging◻ Extremely challenging

Access to equity: A top challenge◻ UK◻ US

Raising equity capital◻ UK◻ US

TRIED AND FAILED▼

▲ RAISED EQUITY CAPITAL

UK executives who successfully raised capital in 2013 are less likely than those in the United States to say the fundraising environment is extremely challenging.

51% 48%

21%

15%

61% 14%

24%

75%

UK 2014

57%

24%

19%US 2014

81%

Find fundraising somewhat or extremely challenging

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 19INNOVATION ECONOMY OUTLOOK UK REPORT 2014 19

The innovation economy continues as a powerful job creator. Eighty-four percent of UK executives say their business plans to grow in 2014. The remaining 16 percent expect to keep their workforce approximately the same. None expect to shrink.

That is an even stronger showing than among US executives, 76 percent of whom expect to grow.

The percentage increases for software sector and pre-revenue businesses in the United States, which are both heavily weighted in the UK sample. Thus, the UK’s strong hiring outlook may reflect geographic differences as well as the mix of the UK survey sample. Nevertheless, the intention among UK businesses to grow is an important measure of their vigour.

Growth means jobsGrowing in 2014?◻ We will grow our workforce ◻ We will stay flat ◻ We will reduce our workforce

UK 2014

US 2014

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 20

CONTINUED ON 21

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 20

CONTINUED ON 21

In fact, most UK executives expect significant growth. Two-thirds of the respondents who anticipate growing in 2014 predict increases of more than 20 percent. Sixteen percent expect to at least double in size. The median expected growth rate is 50 percent in the UK compared with 30 percent in the United States.

Executives at early-stage UK businesses that are not yet earning revenue are the most upbeat. Nine in 10 say they expect to hire, a larger share of respondents than for the two most growth-minded US categories: pre-revenue and software businesses. Four in 10 of these UK executives expect to at least double the size of their workforce. In total, executives at pre-revenue UK businesses project a median growth rate of 100 percent, identical to that of executives at pre-revenue US businesses and about triple that of US software executives overall.

Growth means jobsCHAPTER 1

ALL RESPONDENTS: EXPECT WORKFORCE TO GROW BY

PRE-REVENUE: EXPECT WORKFORCE TO GROW BY

> 100%51% - 100%21% - 50% 1% - 20%

31% 28% 25%

16%

UK

> 100%51% - 100%21% - 50% 1% - 20%

10%

24%29%

37%

UK

> 100%51% - 100%21% - 50% 1% - 20%

36%32%

18%14%

US

> 100%51% - 100%21% - 50% 1% - 20%

18%27% 24%

30%

US

Expected workforce growth

In total, executives at pre-revenue UK businesses project a median growth rate of 100 percent, identical to that of executives at pre-revenue US businesses and about triple that of US software executives overall.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 21

CONTINUED FROM 20

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 21

CONTINUED FROM 20

Clearly, the foundation for a vibrant UK innovation economy is solid. The UK has a critical mass of well-performing businesses. Executives are optimistic about the future and are demonstrating their capacity to build businesses with the capital that is available to them. Together, this means a strong pipeline for job creation.

The challenge now is to translate this potential into stronger businesses that together create the

critical mass for a successful innovation economy.

UK innovation economy executives say their two biggest challenges in 2014 are scaling their operations and recruiting and managing talent. These are two of the top three challenges most often cited by US executives (access to equity is the third), but UK executives give scaling operations and recruiting/managing talent even greater emphasis. Because scaling operations involves people, the core challenge is very much a matter of finding and retaining talent.

Across the board, innovation economy executives say hiring is a major problem, even more so than last year. Ninety-four percent of UK respondents consider it extremely or somewhat challenging to find the talent they need to grow, the same as US software executives.

Across the survey, in the United States and globally, the proportion is only slightly smaller, with 89 percent calling the search for talent extremely or somewhat challenging.

Two familiar forces are driving this situation: supply and demand.

On the supply side, innovation economy businesses, particularly younger start-ups, draw heavily on people with sciences, technology, engineering and maths (STEM) skills. This talent pool has not grown rapidly enough to meet increased demand. On the demand side, the strength of the innovation economy – the large number of start-ups being funded and the strong performance among later-stage businesses – means competition for talent is fierce.

Respondents cite skills and education as the most challenging aspect of finding and retaining people to help them grow their businesses. Experience comes second, followed by salary and benefits.

The challenge: Scaling up

CHA

PTER

2 Silicon Valley Bank’sInnovation Economy Outlook 2014 UK Report

CONTINUED ON 24

Top hiring challenges◻ Skills and education◻ Experience◻ Salary and benefits◻ Candidates prefer

businesses of a different size

◻ Location◻ Other

31%

27%

25%

5%3%

9%

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 22INNOVATION ECONOMY OUTLOOK UK REPORT 2014 22

The challenge: Scaling upCHAPTER 2

Greatest challenges in 2014: UK vs. US

UK innovation economy executives say their two biggest challenges in 2014 are scaling their operations and recruiting and managing talent.

Regulatory/political environment

New products or markets

Access to creditBusiness conditions in existing markets

CompetitionAccess to equityRecruiting employees and managing talent

Scaling operations

27%22%24%

15%

30%

25%

20%

15 %

10 %

5 %

0 %

UK US

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 23INNOVATION ECONOMY OUTLOOK UK REPORT 2014 23

The challenge: Scaling upCHAPTER 2

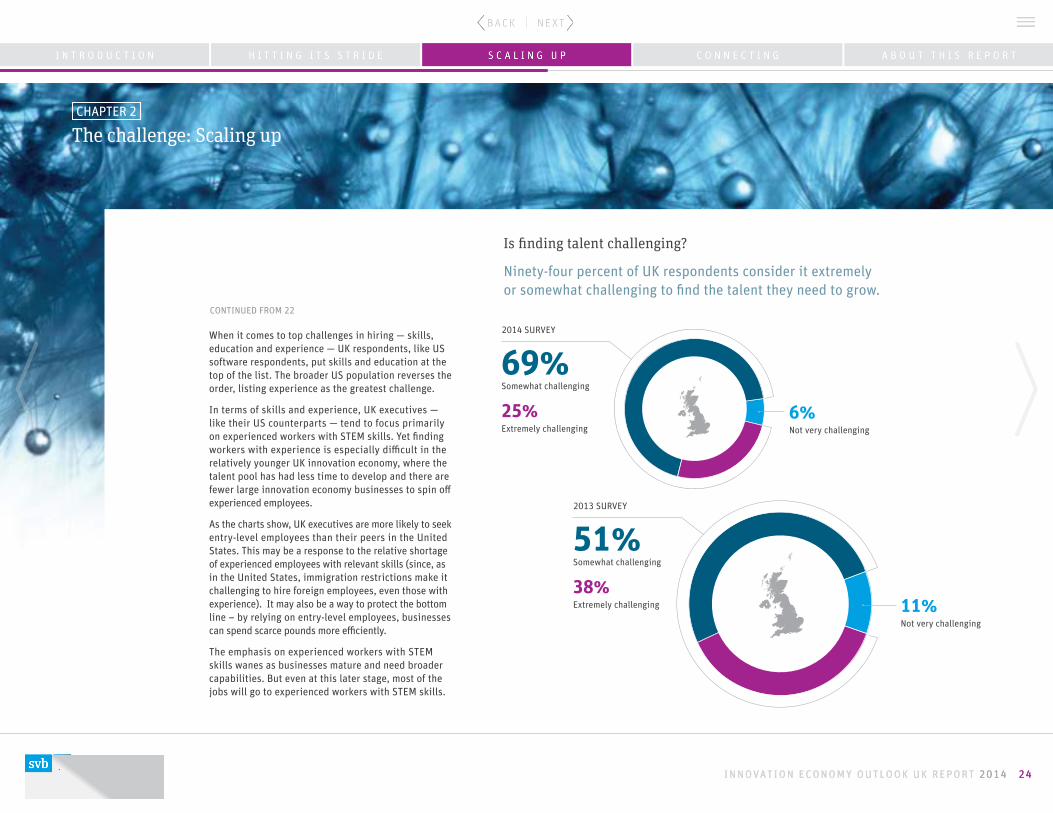

CONTINUED FROM 22

When it comes to top challenges in hiring — skills, education and experience — UK respondents, like US software respondents, put skills and education at the top of the list. The broader US population reverses the order, listing experience as the greatest challenge.

In terms of skills and experience, UK executives — like their US counterparts — tend to focus primarily on experienced workers with STEM skills. Yet finding workers with experience is especially difficult in the relatively younger UK innovation economy, where the talent pool has had less time to develop and there are fewer large innovation economy businesses to spin off experienced employees.

As the charts show, UK executives are more likely to seek entry-level employees than their peers in the United States. This may be a response to the relative shortage of experienced employees with relevant skills (since, as in the United States, immigration restrictions make it challenging to hire foreign employees, even those with experience). It may also be a way to protect the bottom line – by relying on entry-level employees, businesses can spend scarce pounds more efficiently.

The emphasis on experienced workers with STEM skills wanes as businesses mature and need broader capabilities. But even at this later stage, most of the jobs will go to experienced workers with STEM skills.

Is finding talent challenging?

Ninety-four percent of UK respondents consider it extremely or somewhat challenging to find the talent they need to grow.

2013 SURVEY

51%Somewhat challenging

38%Extremely challenging 11%

Not very challenging

2014 SURVEY

69%Somewhat challenging

25%Extremely challenging

6%Not very challenging

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 24INNOVATION ECONOMY OUTLOOK UK REPORT 2014 24

The challenge: Scaling upCHAPTER 2

UK REVENUE-GENERATING

41% Experienced STEM

15%Entry-level STEM

36%Experienced non-STEM

8%Entry-level non-STEM

UK ALL

46%Experienced STEM(53% US)

14%Entry level STEM(9% US)

28%Experienced non-STEM(30% US)

12%Entry-level non-STEM(8% US)

UK PRE-REVENUE

62% Experienced STEM

10%Entry-level STEM

10%Experienced non-STEM

18%Entry-level non-STEM

Jobs and hiringHiring: Looking for experience, looking for STEM skills

UK US

Non-STEM STEM

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

SKILL SETS IN HIGHEST DEMAND IN 2014

Entry-level Experienced

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

ENTRY-LEVEL VS. EXPERIENCE

UK executives are more likely to seek entry-level employees than their peers in the United States.

60%74%

40%

26%

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 25INNOVATION ECONOMY OUTLOOK UK REPORT 2014 25

Because scaling operations involves people, the core

challenge is very much a matter of finding and retaining talent.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 26INNOVATION ECONOMY OUTLOOK UK REPORT 2014 26

UK innovation economy businesses want to make their mark at home. At the same time, they see the benefits of extending their reach more broadly by tapping into large sales markets abroad (particularly the United States), accessing new pools of skilled employees and augmenting the capital available domestically in the UK.

To envision the shape of the UK innovation economy in the future, consider the words of Thomas Friedman:

“The world is flat.”

In all aspects of their business, UK innovation businesses are more internationally focused than their US peers.

Although a majority of UK businesses expect most of their 2014 revenue growth to come from within the UK, 41 percent are looking beyond their shores for growth, and virtually all of those (88 percent) are looking to the United States.

When it comes to hiring, UK businesses look primarily at home for talent, but 9 percent say they expect to hire in the United States in 2014.

Looking forward, UK innovation businesses plan to extend their reach in 2014, increasing the gap between UK businesses and their US counterparts. For both sales and service, UK executives are 20 percent more likely to say their business is now active abroad, or will be in the next 12 months, compared with US executives.

What international locations are most appealing to UK entrepreneurs for doing business internationally?

Asia may come to mind first, but the United States remains the primary draw for sales growth and talent. This makes good business sense for UK executives, given the size of the US market, common language and relatively comparable business environments.

Connecting to the global innovation economy

CHA

PTER

3 Silicon Valley Bank’sInnovation Economy Outlook 2014 U.K. Report

3 2 S E I Z I N G T H E O P P O R T U N I T Y A T H A N D

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 27

CONTINUED ON 28

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 27

CONTINUED ON 28

Many UK executives also are considering service centres in the United States to support their sales.

For production, Europe and Asia garner the greatest interest, led by Eastern Europe (20 percent) and China (17 percent). The United States and India tie for third place, at 7 percent each. Perhaps most notably, a full third of UK executives have no preference (compared with only 14 percent of US executives).

For many executives, research and development represents the crown jewel of the innovation economy. For this, however, a preponderance of UK respondents have no geographical preference.

Of those who do, most prefer to stay closer to home. US executives are much more likely to express a preference and twice as likely to look to Asia (especially India) for research and development.

Connecting to the global innovation economyCHAPTER 3

2014 projected revenue growth: UK businesses◻ UK◻ US◻ Asia◻ Europe

Top hiring locations◻ UK◻ US◻ Western Europe◻ Eastern Europe

3%2%

9% 1% 1%

36%

59%

89%

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 28

CONTINUED FROM 27

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 28

CONTINUED FROM 27

Connecting to the global innovation economyCHAPTER 3

International footprint by activityUK◻ Currently◻ Next 12 months

US◻ Currently◻ Next 12 months

Research and development Production, including coding and manufacturing

Service locations Sales

80%

70%

60%

50%

40%

30%

20%

10%

0%

35%39%

11%

8%

14%

4%

6%8%

14%

47%53%

39%36%

44%

52%25%

UK executives are 20 percent more likely than their US counterparts to say their business is now active abroad or will be in the next 12 months.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 29INNOVATION ECONOMY OUTLOOK UK REPORT 2014 29

To envision the shape of theUK innovation economy,

consider the words of Thomas Friedman:“The world is flat.”

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 30INNOVATION ECONOMY OUTLOOK UK REPORT 2014 30

Connecting to the global innovation economyCHAPTER 3

Most appealing international locations by activity◻ US◻ Europe◻ Asia◻ No preference 50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

50%48%

37%39%

SalesResearch and development Production Service

Other Americas and Middle East categories were omitted from the chart as they were less than 5% in any measure.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 31INNOVATION ECONOMY OUTLOOK UK REPORT 2014 31

The UK at last has the makings of a vibrant innovation economy. Entrepreneurs are turning their passion and ingenuity into breakout businesses. The innovation ecosystem is fueling their success by providing early-stage funding and global opportunities. Businesses are making the most of this momentum through careful management of financial resources – and expectations.

The next steps include continuing to make smart choices about where and how to grow. By thinking

about growth using a “both-and” mind-set, UK entrepreneurs can maximize their potential. They can draw upon an increasingly vibrant local scene. And when it makes sense, they can look farther afield to drive top-line revenue growth or find the talent and later-stage capital they need to succeed. Doing so will generate and support the continued economic and jobs growth that makes the global innovation economy such a powerful phenomenon.

Seizing the opportunity at hand

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 32INNOVATION ECONOMY OUTLOOK UK REPORT 2014 32

Entrepreneurs are turning their passion

and ingenuity into breakout businesses.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 33INNOVATION ECONOMY OUTLOOK UK REPORT 2014 33

The Innovation Economy Outlook 2014 is Silicon Valley Bank’s fifth annual report based on its survey of executives in the innovation economy.

When we launched the survey and report in 2010, we focused on United States start-ups –

businesses with up to $50 million USD in revenue and fewer than 500 employees. Not surprisingly, given our focus, we named our findings Startup Outlook.

As SVB has grown by serving entrepreneurs and high-growth businesses of all sizes around the world, so has our survey. Last year, we added start-ups in the UK. This year, we expanded the survey to include executives covering the full depth and breadth of the markets we serve, including executives in larger businesses and from around the world. In light of our expanded focus, we have renamed our report the Innovation Economy Outlook.

This report focuses on the innovation economy in the UK. In light of the deep connections between the United States and UK markets, we also compare the views of UK respondents with those of their counterparts in the United States.

This is a companion to two other reports based on survey findings: one focused on the United States and the other offering a global overview. In each, we examine the views of executives on the business environment, the outlook for 2014 and the opportunities and challenges ahead.

In addition to the three comprehensive reports, we are issuing targeted reports that look at executives’ views by industry sector, business stage and geography. We will also examine key public policy issues, the representation of women in the innovation economy and the ties across geographies that link innovation economy businesses.

We are grateful to the 1,200 executives around the world who took the time to answer this year’s survey.

Through them, we hope we will encourage others to see how much the future has to offer to those willing to do the hard work that drives the innovation economy.

BACK

GRO

UN

DAbout Silicon Valley Bank’s Innovation Economy Outlook 2014

All reports are available at www.svb.com

3 6 A S N A P S H O T O F S U R V E Y R E S P O N D E N T S

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 34INNOVATION ECONOMY OUTLOOK UK REPORT 2014 34

“2014 is the year my company will develop a working prototype. There is immense interest in the company from established players but we are not ready for them.” — CEO, MEDICAL DEVICE BUSINESS

“We hope to renew our financing facilities with SVB this year and expect to increase the level of our FX hedging.” — CFO, ENTERPRISE SOFTWARE BUSINESS

“Overall very positive – we’re predicting around 80 percent growth.” — CFO, ENTERPRISE SOFTWARE BUSINESS

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 35INNOVATION ECONOMY OUTLOOK UK REPORT 2014 35

SNA

PSH

OT UK survey respondents

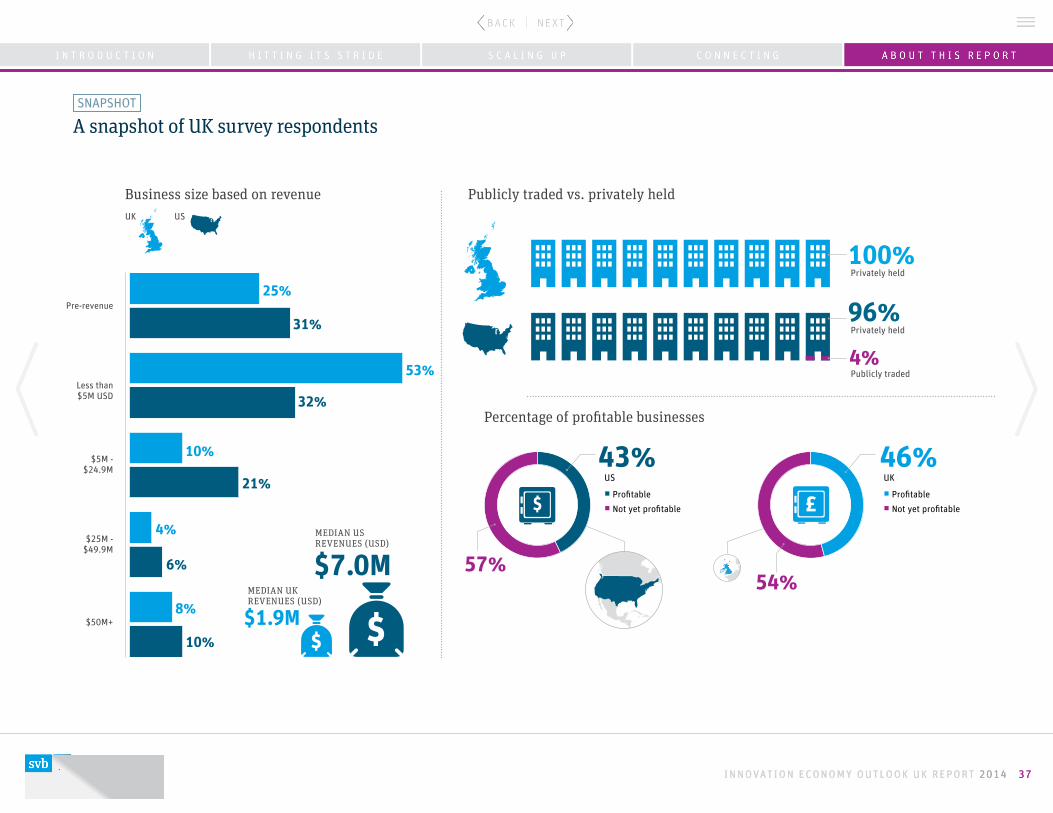

The 2014 survey reflects the views of 100 executives with UK-based high-growth technology and healthcare businesses. More than half of the respondents are CEOs, and 85 percent are C-level executives (CEO, COO, CTO or CFO), comparable numbers to the much larger US survey.

An overwhelming majority of UK respondents come from the software sector. We see more parity in sector distribution than is reflected here

and believe healthcare businesses in particular are underrepresented in this year’s sample. A larger sample size would likely produce a more balanced distribution of industry representation in the UK economy.

In general, the US sample (1,004 executives) draws more broadly from different sectors and includes a somewhat greater proportion of larger businesses. Since software executives tend to be more optimistic, and younger businesses face different opportunities and challenges than mature ones, these differences are important in understanding the survey responses.

UK US

PERCENTAGE OF RESPONDENTS BY SECTOR

◻ Software◻ Hardware◻ Healthcare◻ Other

7%

82%

9%

2%

1000+500-999250-499100-249Fewer than 10 10-24 25-49 50-99

50% 39%

21

10

1%4%

2%9%8%9%

17%15%

13% 11% 13%5%

2% 2%

Company size based on number of employees

MEDIAN NUMBER OF EMPLOYEES: US

MEDIAN NUMBER OF EMPLOYEES: UK

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 36INNOVATION ECONOMY OUTLOOK UK REPORT 2014 36

A snapshot of UK survey respondents SNAPSHOT

Publicly traded vs. privately held

100%

$1.9M

$7.0M

US

◻ Profitable◻ Not yet profitable

Percentage of profitable businesses

UK

◻ Profitable◻ Not yet profitable

UK US

60

Pre-revenue

Less than $5M USD

$5M - $24.9M

$50M+

Business size based on revenue

$25M - $49.9M

25%

31%

32%

53%

MEDIAN UK REVENUES (USD)

MEDIAN US REVENUES (USD)

21%

10%

6%

4%

10%

8%

46%43%

57%54%

Privately held

96%Privately held

4%Publicly traded

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 37INNOVATION ECONOMY OUTLOOK UK REPORT 2014 37

Special thanks to dcIQ for your collaboration on this study. Thank you for your support:

Entrepreneur First

Level 39

Techhub

Seedcamp

Techstars

Startupbootcamp

Acknowledgments

©2014 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of FDIC and Federal Reserve System. SVB>, SVB>Find a way, SVB Financial Group, and Silicon Valley Bank are registered trademarks.A third-party firm, Q&A Research, conducted the survey online on our behalf from January 8 through January 29, 2014.Silicon Valley Bank is registered in England and Wales at 41 Lothbury, London, EC2R 7HF, UK under No. FC029579. Silicon Valley Bank is authorised and regulated by the California Department of Financial Institutions and the United States Federal Reserve Bank; authorised by the Prudential Regulation Authority with number 577295; and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request.

INNOVATION ECONOMY OUTLOOK UK REPORT 2014 38INNOVATION ECONOMY OUTLOOK UK REPORT 2014 38